UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4984

AMERICAN BEACON FUNDS

(Exact name of registrant as specified in charter)

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(Address of principal executive offices)-(Zip code)

GENE L. NEEDLES, JR., PRESIDENT

220 East Las Colinas Boulevard, Suite 1200

Irving, Texas 75039

(Name and address of agent for service)

Registrant’s telephone number, including area code: (817) 391-6100

Date of fiscal year end: October 31, 2015

Date of reporting period: October 31, 2015

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

About American Beacon Advisors

Since 1986, American Beacon Advisors has offered a variety of products and investment advisory services to numerous institutional and retail clients, including a variety of mutual funds, corporate cash management, and separate account management.

Our clients include defined benefit plans, defined contribution plans, foundations, endowments, corporations, financial planners, and other institutional investors. With American Beacon Advisors, you can put the experience of a multi-billion dollar asset management firm to work for your company.

HIGH YIELD BOND FUND RISKS

Investments in high yield securities are subject to greater levels of credit, interest rate, market and liquidity risks than investment-grade securities. Investing in foreign securities may involve heightened risk due to currency fluctuations and economic and political risks. Investing in small- and medium-capitalization stocks may involve greater volatility and lower liquidity than larger company stocks. Please see the prospectus for a complete discussion of the Fund’s risks. There can be no assurances that the investment objectives of this Fund will be met.

INTERMEDIATE BOND FUND RISKS

The use of fixed-income securities entails interest rate and credit risks. Investing in foreign securities may involve heightened risk due to currency fluctuations and economic and political risks. Please see the prospectus for a complete discussion of the Fund’s risks. There can be no assurances that the investment objectives of this Fund will be met.

SHORT-TERM BOND FUND RISKS

The use of fixed-income securities entails interest rate and credit risks. Investing in foreign securities may involve heightened risk due to currency fluctuations and economic and political risks. Please see the prospectus for a complete discussion of the Fund’s risks. There can be no assurances that the investment objectives of this Fund will be met.

Any opinions herein, including forecasts, reflect our judgment as of the end of the reporting period and are subject to change. Each advisor’s strategies and each Fund’s portfolio composition will change depending on economic and market conditions. This report is not a complete analysis of market conditions, and, therefore, should not be relied upon as investment advice. Although economic and market information has been compiled from reliable sources, American Beacon Advisors, Inc. makes no representation as to the completeness or accuracy of the statements contained herein.

| | |

| American Beacon Funds | | October 31, 2015 |

| | |

| | Dear Shareholders, During much of the 12-month period ended October 31, 2015, uneven global economic growth, declining commodity prices and disparate central bank policies set the stage for mixed returns in all markets. The weakening of many currencies against the U.S. dollar also took a toll on total returns for dollar-based investors in many international markets. Uncertainty over the timing of the U.S. Federal Reserve’s first interest rate increase since emergency lending rates were established during the 2008 financial crisis continued to weigh heavily on investors’ minds. At its October 2015 meeting, the Federal Open Market Committee decided against changing interest rates, but kept December on the table as a possibility. |

For the period under review, performances of the funds’ benchmarks were modest. The American Beacon High Yield Bond Fund’s standard, the JPMorgan Global High-Yield Index, returned -2.45%. The American Beacon Intermediate Bond Fund’s touchstone, the Barclays Capital U.S. Aggregate Bond Index, gained 1.96%. And the American Beacon Short-Term Bond Fund’s yardstick, the BofA Merrill Lynch 1-3 Year Gov./Corp. Index, returned 0.88%.

We are proud to offer a broad range of funds to help investors navigate the economic storms and market downturns in the U.S. and abroad. Our years of experience evaluating sub-advisors has led us to identify and partner with several asset managers who have adhered to their disciplined processes for many years and through a variety of economic and market conditions.

For the 12-month period ended October 31, 2015:

| • | | American Beacon High Yield Bond Fund (Investor Class) returned -7.38%. |

| • | | American Beacon Intermediate Bond Fund (Investor Class) returned 1.36%. |

| • | | American Beacon Short-Term Bond Fund (Investor Class) returned 0.03%. |

These funds are closed to new investors.

Thank you for your continued investment in the American Beacon Funds and we are grateful you have placed your confidence in us. For additional information about the Funds or to access your account information, please visit our website at www.americanbeaconfunds.com.

|

Best Regards, |

|

|

|

Gene L. Needles, Jr. |

President |

American Beacon Funds |

1

Bond Market Overview

October 31, 2015 (Unaudited)

The 12-month period ended October 31, 2015 concluded on a soft note for the bond market, yet still managed to report attractive returns overall.

Fixed-income markets, as defined by the Barclays Aggregate Index, returned 2.0% for the year, but finished with a -0.1% return for the final six-month period.

The year began well for bonds as winter economic data indicated the U.S. economy was in a soft patch. Longer-term interest rates declined, pushing bond prices up, but credit spreads soon began to widen.

After the spring thaw, economic readings improved and helped strengthen the desire of the U.S. Federal Reserve (“the Fed”) to raise interest rates. Shorter-term yields edged up, but credit sectors then began to fret about the Fed tightening money supply.

As the Fed’s September 2015 meeting approached, market volatility increased across the globe. The U.S. jobs reports weakened, China devalued its currency, and Europe struggled with persistently slow growth. These events were independent of the Fed, but they created unwanted volatility.

To calm the markets, the Fed remained on hold and pushed their rate-hike plans further out into the future.

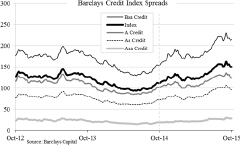

The period ended with interest rates nearly unchanged but with credit spreads wider. High quality outperformed, as did longer-term maturities.

| | | | | | | | |

| | | Total Returns

Periods ended 10/31/15 | |

| | | 6 Month | | | 12 Month | |

Sector | | | | | | | | |

Treasury | | | 0.31 | | | | 2.39 | |

Agency | | | 0.53 | | | | 2.08 | |

Agency Mortgage | | | 0.57 | | | | 2.50 | |

Commercial Mortgage | | | 0.38 | | | | 2.61 | |

Asset Backed | | | 0.61 | | | | 1.64 | |

Credit: | | | -1.33 | | | | 0.90 | |

Industrial | | | -1.91 | | | | 0.26 | |

Utility | | | -1.80 | | | | 1.18 | |

Finance | | | 0.07 | | | | 2.49 | |

Non-Corporate | | | -1.61 | | | | 0.30 | |

| | |

Credit Sector Quality | | | | | | | | |

Aaa | | | 0.22 | | | | 1.71 | |

Aa | | | -0.25 | | | | 2.32 | |

A | | | -0.54 | | | | 2.07 | |

Baa | | | -2.64 | | | | -0.73 | |

| | |

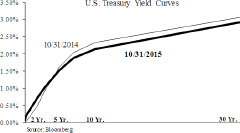

U.S. Treasury | | | | | | | | |

2 Year | | | 0.24 | | | | 0.66 | |

3 Year | | | 0.41 | | | | 1.23 | |

5 Year | | | 0.60 | | | | 2.34 | |

10 Year | | | -0.01 | | | | 3.58 | |

30 Year | | | -2.80 | | | | 4.54 | |

| | |

(Source: Barclays Capital) | | | | | | | | |

2

High Yield Bond Market Overview

October 31, 2015 (Unaudited)

During the 12-month period ended October 31, 2015, the high-yield bond market generated negative returns largely due to weak commodities prices and concern over a slowing global economy. Commodity price weakness was widespread across most types of commodities. That said, weakness in crude oil and natural gas prices had an outsized impact on the high-yield markets, as energy was the largest industry in the benchmark. Accordingly, the high-yield market fell sharply in early December 2014 following OPEC’s decision at its late November 2014 meeting to not cut production as weakness in energy bonds led to fears of contagion across the broader market. A rebound in oil prices helped lead to a rally in the overall high-yield market in the spring of 2015, but the relief proved to be temporary as both oil prices and the overall high-yield market resumed their decline over the summer.

While lower commodity prices arguably are good for a large portion of high-yield issuers, such as those in industrial manufacturing and consumer-related industries, concerns about slowing economic growth in China and the global economy in general were more pervasive and harder to overcome. Continued moderate growth in the U.S. economy was more than offset by signs that Chinese growth was below expectations, and the Chinese government’s often awkward attempts to deal with the problem only fueled the market’s concerns. At the same time, the commodity slump led to concerns over potential weakness in emerging markets economies in general, since many emerging countries are net commodity exporters.

Despite the numerous headwinds, the overall high-yield default rate remained below its historical average. However, valuations cheapened as spreads widened from 5% to 6.7%, which more than offset a slight decline in U.S. Treasury yields over the course of the year. Accordingly, price declines more than offset coupon income and the benchmark returned negative 2.5%.

Note: Spread and return data based on the JPMorgan Global High Yield Index.

3

American Beacon High Yield Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

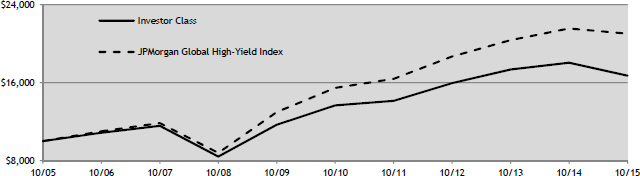

The Investor Class of the High Yield Bond Fund (the “Fund”) returned -7.38% for the twelve months ended October 31, 2015. The Fund trailed the JPMorgan Global High-Yield Index (the “Index”) return of -2.45% for the period.

Comparison of Change in Value of a $10,000 Investment for the period from 10/31/05 through 10/31/15

Total Returns for the Period ended 10/31/15

| | | | | | | | | | | | | | | | | | |

| | | Ticker | | 1 Year | | | 5 Years | | | 10 Years | | | Value of

$10,000

10/31/05-

10/31/15 | |

Institutional Class (1,7) | | AYBFX | | | (7.28 | )% | | | 4.35 | % | | | 5.51 | % | | $ | 17,093 | |

Y Class (1,3,7) | | ACYYX | | | (7.13 | )% | | | 4.16 | % | | | 5.43 | % | | | 16,963 | |

Investor Class (1,7) | | AHYPX | | | (7.38 | )% | | | 4.10 | % | | | 5.27 | % | | | 16,706 | |

A Class with sales charge (1,4,7) | | ABHAX | | | (11.65 | )% | | | 3.11 | % | | | 4.78 | % | | | 15,954 | |

A Class without sales charge (1,4,7) | | ABHAX | | | (7.29 | )% | | | 4.11 | % | | | 5.29 | % | | | 16,750 | |

C Class with sales charge (1,5,7) | | AHBCX | | | (9.09 | )% | | | 3.34 | % | | | 4.85 | % | | | 16,059 | |

C Class without sales charge (1,5,7) | | AHBCX | | | (8.09 | )% | | | 3.34 | % | | | 4.85 | % | | | 16,059 | |

AMR Class (1,2,7) | | ABMRX | | | (6.98 | )% | | | 4.63 | % | | | 5.75 | % | | | 17,492 | |

JPMorgan Global High-Yield Index (6) | | | | | (2.45 | )% | | | 6.33 | % | | | 7.71 | % | | | 21,015 | |

| 1. | Performance shown is historical and is not indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is calculated based on the published end of day net assets as of date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month end, please visit www.americanbeaconfunds.com or call 1-800-967-9009. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. A portion of the fees charged to the Institutional Class of the Fund was waived through 2004 and since 2013. Performance prior to waiving fees was lower than the actual returns shown for these periods. A portion of the fees charged to the Investor Class of the Fund has been waived since 2013. Performance prior to waiving fees was lower than the actual returns shown since 2013. |

| 2. | Fund performance for the ten-year period represents the total return achieved by the Institutional Class from 10/31/05 up to 9/4/07, the inception date of the AMR Class, and the returns of the AMR Class since its inception. Expenses of the AMR Class are lower than those of the Institutional Class. As a result, total returns shown may be lower than they would have been had the AMR Class been in existence since 10/31/05. |

| 3. | Fund performance for the ten-year period represents the returns achieved by the Institutional Class from 10/31/05 up to 3/1/10, the inception date of the Y Class, and the returns of the Y Class since its inception. Expenses of the Y Class are higher than those of the Institutional Class. As a result, total returns shown may be higher than they would have been had the Y Class been in existence since 10/31/05. A portion of the fees charged to the Y Class of the Fund was waived from 2011 to 2013 and recovered in 2014 and 2015. Performance prior to waiving fees was lower than the actual returns shown from 2011 to 2013. |

| 4. | Fund performance for the ten-year period represents the returns achieved by the Investor Class from 10/31/05 up to 5/17/10, the inception date of the A Class, and the returns of the A Class since its inception. Expenses of the A Class are higher than those of the Investor Class. As a result, total returns shown may be higher than they would have been had the A Class been in existence since 10/31/05. A portion of the fees charged to the A Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum sales charge for A Class is 4.75%. |

| 5. | Fund performance for the ten-year period represents the returns achieved by the Investor Class from 10/31/05 up to 9/1/10, the inception date of the C Class, and the returns of the C Class since its inception. Expenses of the C Class are higher than those of the Investor Class. As a result, total returns shown may be higher than they would have been had the C Class been in existence since 10/31/05. A portion of the fees charged to the C Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum contingent deferred sales charge for C Class is 1.00% for shares redeemed within one year of the date of purchase. |

4

American Beacon High Yield Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

| 6. | The JPMorgan Global High-Yield Index (“JPMorgan Index”) is an unmanaged index of fixed income securities with a maximum credit rating of BB+ or Ba1. Issues must be publicly registered or issued under Rule 144A under the Securities Act of 1933, with a minimum issue size of $75 million (par amount). A maximum of two issues per issuer are included in the JPMorgan Index. Convertible bonds, preferred stock, and floating-rate bonds are excluded from the JPMorgan Index. One cannot directly invest in an index. |

| 7. | The total annual Fund operating expense ratio set forth in the most recent Fund prospectus for the Institutional, Y, Investor, A, C, and AMR Class shares was 0.88%, 0.94%, 1.11%, 1.24%, 2.00%, and 0.59%, respectively. The expense ratios above may vary from the expense ratios presented in other sections of this report that are based on expenses incurred during the period covered by this report. |

From a sector standpoint, the Fund’s returns were hampered primarily by the Energy sector, detracting significantly from Fund performance. Additionally, the Manufacturing, Electric, and Finance sectors detracted from Fund returns. Conversely, holdings in the Consumer sector contributed positively to Fund performance, slightly offsetting losses in the aforementioned sectors.

From a credit quality perspective, the Fund’s returns were hindered predominantly by holdings in the B-rated category. In addition, Fund holdings in the CCC-rated and BB-rated categories detracted from Fund performance.

The sub-advisors’ “bottom-up,” research intensive investment process, which focuses on companies with strong cash flow and fundamental credit strength, remains in place.

The Fund ended operations on December 15, 2015 and in advance of this event, the Fund’s investment managers were invested only in cash and cash-equivalent securities.

Top Ten Holdings (% Net Assets)

| | | | |

Rockies Express Pipeline LLC, 6.875%, Due 4/15/2040, 144A | | | 2.8 | |

Park Ohio Industries, Inc., 8.125%, Due 4/1/2021 | | | 2.1 | |

NGPL PipeCo LLC, 9.625%, Due 6/1/2019, 144A | | | 2.1 | |

Landry’s, Inc., 9.375%, Due 5/1/2020, 144A | | | 1.8 | |

Select Medical Corp., 6.375%, Due 6/1/2021 | | | 1.7 | |

Xerium Technologies, Inc., 8.875%, Due 6/15/2018 | | | 1.6 | |

LBI Media, Inc., 4.25%, Due 4/15/2020, 144A | | | 1.5 | |

Cogent Communications Finance, Inc., 5.625%, Due 4/15/2021, 144A | | | 1.4 | |

First Data Corp., 12.625%, Due 1/15/2021 | | | 1.3 | |

Cenveo Corp., 8.50%, Due 9/15/2022, 144A | | | 1.3 | |

Total Fund Holdings | | | 100 | |

Sector Allocation (% Investments)

| | | | |

Short-Term Investments | | | 91.7 | |

Service | | | 2.3 | |

Energy | | | 2.1 | |

Manufacturing | | | 1.9 | |

Telecommunications | | | 0.9 | |

Finance | | | 0.8 | |

Transportation | | | 0.2 | |

Currency | | | 0.1 | |

Consumer | | | 0.0 | |

5

American Beacon Intermediate Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

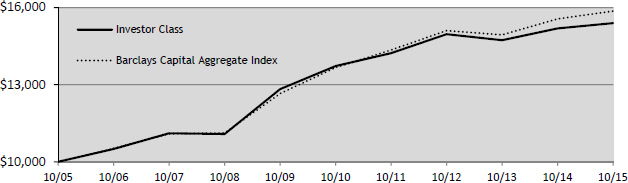

The Investor Class of the Intermediate Bond Fund (the “Fund”) returned 1.36% for the twelve months ended October 31, 2015, trailing the Barclays Capital Aggregate Index (the “Index”) return of 1.96% for the same period.

Comparison of Change in Value of a $10,000 Investment for the period from 10/31/05 through 10/31/15

Total Returns for the Period ended 10/31/15

| | | | | | | | | | | | | | | | | | |

| | | Ticker | | 1 Year | | | 5 Years | | | 10 Years | | | Value of

$10,000

10/31/05-

10/31/15 | |

Institutional Class (1,7) | | AABDX | | | 1.80 | % | | | 2.80 | % | | | 4.74 | % | | $ | 15,891 | |

Y Class (1,3,7) | | ACTYX | | | 1.44 | % | | | 2.53 | % | | | 4.59 | % | | | 15,663 | |

Investor Class (1,2,7) | | ABIPX | | | 1.36 | % | | | 2.32 | % | | | 4.41 | % | | | 15,391 | |

A Class with sales Charge (1,4,7) | | AITAX | | | (3.59 | )% | | | 1.17 | % | | | 3.80 | % | | | 14,524 | |

A Class without sales Charge (1,4,7) | | AITAX | | | 1.25 | % | | | 2.16 | % | | | 4.31 | % | | | 15,250 | |

C Class with sales Charge (1,5,7) | | AIBCX | | | (0.51 | )% | | | 1.40 | % | | | 3.92 | % | | | 14,690 | |

C Class without sales Charge (1,5,7) | | AIBCX | | | 0.49 | % | | | 1.40 | % | | | 3.92 | % | | | 14,690 | |

Barclays Capital Agg. Index (6) | | | | | 1.96 | % | | | 3.03 | % | | | 4.72 | % | | | 15,862 | |

| 1. | Performance shown is historical and is not indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is calculated based on published end of day net asset values as of date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month end, please visit www.americanbeaconfunds.com or call 1-800-967-9009. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. |

| 2. | Fund performance for the ten-year period represents the total returns achieved by the Institutional Class up to 3/2/09, the inception date of the Investor Class, and the returns of the Investor Class since its inception. Expenses of the Investor Class are higher than those of the Institutional Class. As a result, total returns shown may be higher than they would have been had the Investor Class been in existence since 10/31/05. A portion of the fees charged to the Investor Class of the Fund has been waived since 2009. Performance prior to waiving fees was lower than the actual returns shown since 2009. |

| 3. | Fund performance for the ten-year period represents the total returns achieved by the Institutional Class from 10/31/05 up to 3/1/10, the inception date of the Y Class, and the returns of the Y Class since its inception. Expenses of the Y Class are higher than those of the Institutional Class. As a result, total returns shown may be higher than they would have been had the Y Class been in existence since 10/31/05. A portion of the fees charged to the Y Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. |

| 4. | Fund performance for the ten-year period represents the total returns achieved by the Institutional Class from 10/31/05 through 3/2/09, the Investor Class from 3/2/09 up to 5/17/10, the inception date of the A Class, and the returns of the A Class since its inception. Expenses of the A Class are higher than those of the Institutional and Investor Classes. As a result, total returns shown may be higher than they would have been had the A Class been in existence since 10/31/05. A portion of the fees charged to the A Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum sales charge for A Class is 4.75%. |

| 5. | Fund performance for the ten-year period represents the total returns achieved by the Institutional Class from 10/31/05 through 3/2/09, the Investor Class from 3/2/09 up to 9/1/10, the inception date of the C Class, and the returns of the C Class since its inception. Expenses of the C Class are higher than those of the Institutional and Investor Classes. As a result, total returns shown may be higher than they would have been had the C Class been in existence since 10/31/05. A portion of the fees charged to the C Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum contingent deferred sales charge is 1.00% for shares redeemed within one year of the date of purchase. |

6

American Beacon Intermediate Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

| 6. | The Barclays Capital Aggregate Index is a market value weighted index of government, corporate, mortgage-backed and asset-backed fixed-rate debt securities of all maturities. One cannot directly invest in an index. |

| 7. | The total annual Fund operating expense ratios set forth in the most recent Fund prospectus for the Institutional, Y, Investor, A, and C Class shares was 0.33%, 0.71%, 0.91%, 1.00%, and 1.78%, respectively. The expense ratios above may vary from the expense ratios presented in other sections of this report that is based on expenses incurred during the period covered by this report. |

The Fund’s underperformance relative to the Index was largely attributable to its allocation among the various sectors; however, this poor performance was somewhat offset by favorable security selection. Allocation among the various credit quality categories also detracted from performance.

During the period, the Fund’s underweight in U.S. Treasuries detracted value relative to the Index. The Fund’s overweight position in Corporates, specifically within the Telecom and Energy sectors, also hindered performance. The aforementioned poor performance was somewhat offset by good security selection among corporate bonds in the Manufacturing and Energy sectors and within the MBS sector which added relative value.

The Fund’s allocation across the various credit quality categories constrained returns. A significant underweight position among the AA-rated category and the Fund’s overweight among the BBB-rated category detracted from performance, although issuer selection within the AA-rated and BBB-rated categories proved beneficial.

The Fund’s security selection, mostly in the 0 to 1 and 1 to 3 year duration ranges, also detracted value relative to the Index.

The Fund ended operations on November 30, 2015 and in advance of this event, the Fund’s investment managers were invested only in cash and cash-equivalent securities.

Sector Allocation (% Investments)

| | | | |

Short-Term Investments | | | 100.0 | |

7

American Beacon Short-Term Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

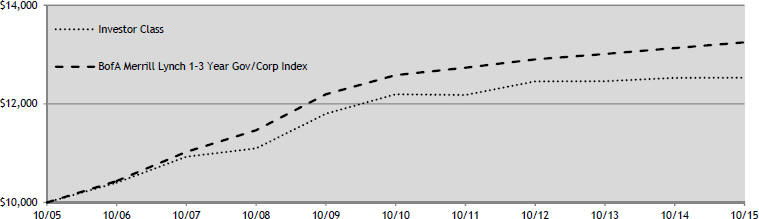

The Investor Class of the Short-Term Bond Fund (the “Fund”), which has a net annual expense ratio of 0.80%, returned 0.03% for the twelve-month period ended October 31, 2015 and underperformed the BofA Merrill Lynch 1-3 Year Gov/Corp Index (the “Index”) return of 0.88%.

Comparison of Change in Value of a $10,000 Investment for the period from 10/31/05 through 10/31/15

Total Returns for the Period ended 10/31/15

| | | | | | | | | | | | | | | | | | |

| | | Ticker | | 1 Year | | | 5 Years | | | 10 Years | | | Value of

$10,000

10/31/05-

10/31/15 | |

Institutional Class (1,6) | | AASBX | | | 0.45 | % | | | 0.92 | % | | | 2.71 | % | | $ | 13,069 | |

Y Class (1,2,6) | | ACOYX | | | 0.18 | % | | | 0.75 | % | | | 2.62 | % | | | 12,952 | |

Investor Class (1,6) | | AALPX | | | 0.03 | % | | | 0.55 | % | | | 2.28 | % | | | 12,531 | |

A Class with sales Charge (1,3,6) | | ANSAX | | | (2.41 | )% | | | (0.02 | )% | | | 2.00 | % | | | 12,192 | |

A Class without sales Charge (1,3,6) | | ANSAX | | | 0.06 | % | | | 0.49 | % | | | 2.26 | % | | | 12,498 | |

C Class with sales Charge (1,4,6) | | ATBCX | | | (1.65 | )% | | | 0.25 | % | | | 1.87 | % | | | 12,038 | |

C Class without sales Charge (1,4,6) | | ATBCX | | | (0.65 | )% | | | 0.25 | % | | | 1.87 | % | | | 12,038 | |

BofA Merrill Lynch 1-3 Yr. Gov./Corp Index (5) | | | | | 0.88 | % | | | 1.04 | % | | | 2.85 | % | | | 13,248 | |

| 1. | Performance shown is historical and is not indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is calculated based on the published end of day net asset values as of date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month end, please visit www.americanbeaconfunds.com or call 1-800-967-9009. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. A portion of the fees charged to the Investor Class of the Fund has been waived since 2005. Performance prior to waiving fees was lower than the actual returns shown since 2005. |

| 2. | Fund performance for the ten-year period represents the total returns achieved by the Institutional Class from 10/31/05 through 3/1/10, the inception date of the Y Class, and the returns of the Y Class since its inception. Expenses of the Y Class are higher than those of the Institutional Class. As a result, total returns shown may be higher than they would have been had the Y Class been in existence since 10/31/05. A portion of the fees charged to the Y Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. |

| 3. | Fund performance for the ten-year period represents the total returns achieved by the Investor Class from 10/31/05 up to 5/17/10, the inception date of the A Class, and the returns of the A Class since its inception. Expenses of the A Class are higher than those of the Investor Class. As a result, total returns shown may be higher than they would have been had the A Class been in existence since 10/31/05. A portion of the fees charged to the A Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum sales charge for A Class is 2.50%. |

| 4. | Fund performance for the ten-year period represents the total returns achieved by the Investor Class from 10/31/05 up to 9/1/10, the inception date of the C Class, and the returns of the C Class since its inception. Expenses of the C Class are higher than those of the Investor Class. As a result, total returns shown may be higher than they would have been had the C Class been in existence since 10/31/05. A portion of the fees charged to the C Class of the Fund has been waived since 2010. Performance prior to waiving fees was lower than the actual returns shown since 2010. The maximum contingent deferred sales charge is 1.00% for shares redeemed within one year of the date of purchase. |

| 5. | The BofA Merrill Lynch 1-3 Yr. Gov./Corp. Index is a market value weighted performance benchmark for government and corporate fixed-rate debt securities with maturities between one and three years. One cannot directly invest in an index. |

8

American Beacon Short-Term Bond FundSM

Performance Overview

October 31, 2015 (Unaudited)

| 6. | The total annual Fund operating expense ratio set forth in the most recent Fund prospectus for the Institutional, Y, Investor, A, and C Class shares was 0.38%, 0.73%, 0.91%, 1.05%, and 1.78%, respectively. The expense ratios above may vary from the expense ratios presented in other sections of this report that are based on expenses incurred during the period covered by this report. |

The Fund held overweight positions in the major credit sectors, including investment-grade Corporate, Asset-Backed and Agency Mortgage-Backed securities, which outperformed given their higher yields. These sectors also performed well in an environment of slightly widening credit spreads due to market volatility in the summer of 2015.

The Fund’s duration position, however, led to its underperformance as the portfolio earned less yield than that of the Index. Interest rates at the very shortest end of the yield curve rose during the period, but rates for longer maturities were essentially flat. As a result, the longer-dated securities outperformed. The Fund’s average duration was approximately 1.3 versus 1.9 for the Index.

Given the unusually low levels of interest rates, we have maintained a short duration to protect the Fund from an ultimate rise in rates. Assuming the economy continues to grow at its recent trajectory, the Fed is expected to begin gradually raising interest rates in 4Q’15.

The Fund ended operations on November 30, 2015 and in advance of this event, the Fund’s investment managers were invested only in cash and cash-equivalent securities.

Sector Allocation (% Investments)

| | | | |

Short-Term Investments | | | 100.0 | |

9

American Beacon FundsSM

Fund Expenses

October 31, 2015 (Unaudited)

Fund Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including redemption fees if applicable, and (2) ongoing costs, including sales charges (loads) on purchase payments including management fees, administrative service fees, distribution (12b-1) fees, and other Fund expenses. The examples below are intended to help you understand the ongoing cost (in dollars) of investing in a particular Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested at the beginning of the period in each Class and held for the entire period from May 1, 2015 through October 31, 2015.

Actual Expenses

The following tables provide information about actual account values and actual expenses. You may use the information on this page, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the “Expenses Paid During Period” for the applicable Fund to estimate the expenses you paid on your account during this period. Shareholders of the Investor and Institutional Classes that invest in a Fund through an IRA or Roth IRA may be subject to a custodial IRA fee of $15 that is typically deducted each December. If your account was subject to a custodial IRA fee during the period, your costs would have been $15 higher.

Hypothetical Example for Comparison Purposes

The following tables provide information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed 5% per year rate of return before expenses (not the Fund’s actual return). You may compare the ongoing costs of investing in a particular Fund with other funds by contrasting this 5% hypothetical example and the 5% hypothetical examples that appear in the shareholder reports of the other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. Shareholders of the Investor and Institutional Classes that invest in a Fund through an IRA or Roth IRA may be subject to a custodial IRA fee of $15 that is typically deducted each December. If your account was subject to a custodial IRA fee during the period, your costs would have been $15 higher.

You should also be aware that the expenses shown in the table highlight only your ongoing costs and do not reflect any transaction costs charged by a Fund, such as redemption fees as applicable. Similarly, the expense examples for other funds do not reflect any transaction costs charged by those funds, such as sales charges (loads), redemption fees or exchange fees. Therefore, the following tables are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. If you were subject to any transaction costs during the period, your costs would have been higher.

10

American Beacon FundsSM

Fund Expenses

October 31, 2015 (Unaudited)

High Yield Bond Fund

| | | | | | | | | | | | |

| | | Beginning

Account

Value

5/1/15 | | | Ending

Account

Value

10/31/15 | | | Expenses Paid

During Period*

5/1/15 - 10/31/15 | |

Institutional Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 931.80 | | | $ | 4.33 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,020.72 | | | $ | 4.53 | |

Y Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 930.66 | | | $ | 4.77 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,020.27 | | | $ | 4.99 | |

Investor Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 931.02 | | | $ | 5.31 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,019.71 | | | $ | 5.55 | |

A Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 931.44 | | | $ | 4.97 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,020.06 | | | $ | 5.19 | |

C Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 926.76 | | | $ | 8.60 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,016.28 | | | $ | 9.00 | |

AMR Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 933.15 | | | $ | 3.02 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,022.08 | | | $ | 3.16 | |

| * | Expenses are equal to the Fund’s annualized expense ratios for the six-month period of 0.89%, 0.98%, 1.09%, 1.02%, 1.77%, and 0.62% for the Institutional, Y, Investor, A, C, and AMR Classes respectively, multiplied by the average account value over the period, multiplied by the number derived by dividing the number of days in the most recent fiscal half-year (184) by days in the year (365) to reflect the half-year period. |

| ** | 5% return before expenses. |

Intermediate Bond Fund

| | | | | | | | | | | | |

| | | Beginning

Account

Value

5/1/15 | | | Ending

Account

Value

10/31/15 | | | Expenses Paid

During Period*

5/1/15 - 10/31/15 | |

Institutional Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 998.16 | | | $ | 1.61 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,023.59 | | | $ | 1.63 | |

Y Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 995.63 | | | $ | 3.27 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,021.93 | | | $ | 3.31 | |

Investor Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 994.92 | | | $ | 3.97 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,021.22 | | | $ | 4.02 | |

A Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 994.39 | | | $ | 4.42 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,020.77 | | | $ | 4.48 | |

C Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 991.69 | | | $ | 8.08 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,017.09 | | | $ | 8.19 | |

| * | Expenses are equal to the Fund’s annualized expense ratios for the six-month period of 0.32%, 0.65%, 0.79%, 0.88%, and 1.61% for the Institutional, Y, Investor, A, and C Classes respectively, multiplied by the average account value over the period, multiplied by the number derived by dividing the number of days in the most recent fiscal half-year (184) by days in the year (365) to reflect the half-year period. |

| ** | 5% return before expenses. |

Short-Term Bond Fund

| | | | | | | | | | | | |

| | | Beginning

Account

Value

5/1/15 | | | Ending

Account

Value

10/31/15 | | | Expenses Paid

During Period*

5/1/15 - 10/31/15 | |

Institutional Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,001.15 | | | $ | 1.77 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,023.44 | | | $ | 1.79 | |

Y Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,000.94 | | | $ | 3.13 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,022.08 | | | $ | 3.16 | |

Investor Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,000.28 | | | $ | 3.83 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,021.37 | | | $ | 3.87 | |

A Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,000.37 | | | $ | 3.68 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,021.53 | | | $ | 3.72 | |

C Class | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 996.76 | | | $ | 6.29 | |

Hypothetical ** | | $ | 1,000.00 | | | $ | 1,018.90 | | | $ | 6.36 | |

| * | Expenses are equal to the Fund’s annualized expense ratios for the six-month period of 0.35%, 0.62%, 0.76%, 0.73%, and 1.25% for the Institutional, Y, Investor, A, and C Classes respectively, multiplied by the average account value over the period, multiplied by the number derived by dividing the number of days in the most recent fiscal half-year (184) by days in the year (365) to reflect the half-year period. |

| ** | 5% return before expenses. |

11

American Beacon FundsSM

Report of Independent Registered Public Accounting Firm

To the Shareholders and the Board of Trustees of

American Beacon High Yield Bond Fund, American Beacon Intermediate Bond Fund, and American Beacon Short-Term Bond Fund:

We have audited the accompanying statements of assets and liabilities, including the schedules of investments, of American Beacon High Yield Bond Fund, American Beacon Intermediate Bond Fund and American Beacon Short-Term Bond Fund (three of the funds constituting the American Beacon Funds) (collectively, the “Funds”), as of October 31, 2015, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Funds’ internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2015, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of American Beacon High Yield Bond Fund, American Beacon Intermediate Bond Fund and American Beacon Short-Term Bond Fund at October 31, 2015, the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended, and the financial highlights for each of five years in the period then ended in conformity with U.S. generally accepted accounting principles.

Dallas, Texas

December 29, 2015

12

American Beacon High Yield Bond FundSM

Schedule of Investments

October 31, 2015

| | | | | | | | |

| | | Shares | | | Fair Value | |

| | | | | | (000’s) | |

COMMON STOCKS - 0.24% (Cost $111) | | | | | | | | |

SERVICE- 0.12% | | | | | | | | |

Communications - 0.12% | | | | | | | | |

Cengage Learning Holdings II Inc.A | | | 1,154 | | | $ | 29 | |

| | | | | | | | |

TELECOMMUNICATION SERVICES- 0.12% | | | | | | | | |

Wireless Telecommunication Services - 0.12% | | | | | | | | |

NII Holdings, Inc.A | | | 4,161 | | | | 29 | |

| | | | | | | | |

Total Common Stocks (Cost $111) | | | | | | | 58 | |

| | | | | | | | |

| | |

| | | Par Amount | | | | |

| | | (000’s) | | | | |

CONVERTIBLE OBLIGATIONS - 0.06% (Cost $21) | | | | | | | | |

Energy - 0.06% | | | | | | | | |

Goodrich Petroleum Corp., 5.00%, Due 10/1/2032 | | $ | 40 | | | | 15 | |

| | | | | | | | |

CORPORATE OBLIGATIONS - 44.93% | | | | | | | | |

Consumer - 0.32% | | | | | | | | |

Motors Liquidation Co., 8.375%, Due 7/15/2049B H I J | | | 1,570 | | | | — | |

Simmons Foods, Inc., 7.875%, Due 10/1/2021C | | | 50 | | | | 47 | |

Spectrum Brands, Inc., 5.75%, Due 7/15/2025C | | | 30 | | | | 32 | |

| | | | | | | | |

| | | | | | | 79 | |

| | | | | | | | |

Energy - 11.52% | | | | | | | | |

Antero Resources Finance Corp., 6.00%, Due 12/1/2020 | | | 40 | | | | 38 | |

California Resources Corp., 6.00%, Due 11/15/2024 | | | 20 | | | | 14 | |

Chesapeake Energy Corp., 6.875%, Due 11/15/2020 | | | 70 | | | | 47 | |

DCP Midstream LLC, | | | | | | | | |

5.35%, Due 3/15/2020C D | | | 55 | | | | 51 | |

6.75%, Due 9/15/2037C D | | | 90 | | | | 74 | |

5.85%, Due 5/21/2043C D | | | 170 | | | | 136 | |

DCP Midstream Operating LP, 3.875%, Due 3/15/2023E | | | 45 | | | | 38 | |

Energy XXI Gulf Coast, Inc., 11.00%, Due 3/15/2020C | | | 35 | | | | 19 | |

Genesis Energy LP / Genesis Energy Finance Corp., 5.75%, Due 2/15/2021E | | | 65 | | | | 61 | |

Goodrich Petroleum Corp., 8.875%, Due 3/15/2018 | | | 200 | | | | 74 | |

Hercules Offshore, Inc., 7.50%, Due 10/1/2021C I | | | 370 | | | | 70 | |

NGPL PipeCo LLC, | | | | | | | | |

7.119%, Due 12/15/2017C D | | | 165 | | | | 153 | |

9.625%, Due 6/1/2019C D | | | 545 | | | | 511 | |

7.768%, Due 12/15/2037C D | | | 135 | | | | 111 | |

Oasis Petroleum, Inc., 6.875%, Due 3/15/2022 | | | 35 | | | | 30 | |

Regency Energy Partners LP / Regency Energy Finance Corp., 5.875%, Due 3/1/2022E | | | 30 | | | | 31 | |

Rockies Express Pipeline LLC, 6.875%, Due 4/15/2040C D | | | 730 | | | | 694 | |

Sabine Pass Liquefaction LLC, 5.75%, Due 5/15/2024D | | | 50 | | | | 48 | |

Sabine Pass LNG LP, 7.50%, Due 11/30/2016E | | | 45 | | | | 46 | |

Sanchez Energy Corp., 6.125%, Due 1/15/2023 | | | 50 | | | | 36 | |

SandRidge Energy, Inc., 8.75%, Due 6/1/2020C | | | 30 | | | | 18 | |

Targa Resources Partners LP / Targa Resources Partners Finance Corp., 5.25%, Due 5/1/2023E | | | 25 | | | | 23 | |

Ultra Petroleum Corp., 6.125%, Due 10/1/2024C | | | 400 | | | | 225 | |

Western Refining Logistics LP / WNRL Finance Corp., 7.50%, Due 2/15/2023E | | | 265 | | | | 270 | |

| | | | | | | | |

| | | | | | | 2,818 | |

| | | | | | | | |

Finance - 4.35% | | | | | | | | |

Cogent Communications Finance, Inc., 5.625%, Due 4/15/2021C | | | 355 | | | | 336 | |

Communications Sales & Leasing Inc / CSL Capital LLC, | | | | | | | | |

6.00%, Due 4/15/2023C D | | | 45 | | | | 44 | |

8.25%, Due 10/15/2023D | | | 20 | | | | 18 | |

ROC Finance LLC / ROC Finance 1 Corp., 12.125%, Due 9/1/2018C D | | | 150 | | | | 159 | |

Stena AB, 7.00%, Due 2/1/2024C | | | 310 | | | | 283 | |

Stena International S.A., 5.75%, Due 3/1/2024C | | | 250 | | | | 223 | |

| | | | | | | | |

| | | | | | | 1,063 | |

| | | | | | | | |

Manufacturing - 10.53% | | | | | | | | |

Advanced Micro Devices, Inc., 7.50%, Due 8/15/2022 | | | 125 | | | | 91 | |

See accompanying notes

13

American Beacon High Yield Bond FundSM

Schedule of Investments

October 31, 2015

| | | | | | | | |

| | | Par Amount | | | Fair Value | |

| | | (000’s) | | | (000’s) | |

AECOM Company, 5.75%, Due 10/15/2022 | | $ | 45 | | | $ | 47 | |

ArcelorMittal, | | | | | | | | |

7.00%, Due 2/25/2022B | | | 40 | | | | 38 | |

6.125%, Due 6/1/2025 | | | 25 | | | | 22 | |

Blue Cube Spinco, Inc., 10.00%, Due 10/15/2025C | | | 15 | | | | 16 | |

Boxer Parent Company, Inc., 9.00%, Due 10/15/2019C F | | | 150 | | | | 107 | |

Chemours Co., 7.00%, Due 5/15/2025C | | | 45 | | | | 34 | |

CPG Merger Sub LLC, 8.00%, Due 10/1/2021C D | | | 40 | | | | 41 | |

Eagle Spinco, Inc., 4.625%, Due 2/15/2021 | | | 60 | | | | 58 | |

First Data Corp., 12.625%, Due 1/15/2021 | | | 275 | | | | 315 | |

Horsehead Holding Corp., 10.50%, Due 6/1/2017C | | | 145 | | | | 125 | |

Liberty Tire Recycling LLC, 11.00%, Due 3/31/2021C D F | | | 176 | | | | 109 | |

Norske Skog Holding AS, 8.00%, Due 2/24/2021C | | | 120 | | | | 55 | |

Nova Chemicals Corp., 5.00%, Due 5/1/2025C | | | 30 | | | | 30 | |

Orbital ATK, Inc., 5.50%, Due 10/1/2023C | | | 20 | | | | 21 | |

Park Ohio Industries, Inc., 8.125%, Due 4/1/2021 | | | 490 | | | | 514 | |

Peabody Energy Corp., 10.00%, Due 3/15/2022C | | | 25 | | | | 7 | |

Pittsburgh Glass Works LLC, 8.00%, Due 11/15/2018C D | | | 10 | | | | 10 | |

Plastipak Holdings, Inc., 6.50%, Due 10/1/2021C | | | 230 | | | | 228 | |

Platform Specialty Products Corp., 6.50%, Due 2/1/2022C | | | 95 | | | | 81 | |

Shea Homes LP / Shea Homes Funding Corp., 5.875%, Due 4/1/2023C E | | | 45 | | | | 47 | |

Taylor Morrison Communities Inc / Monarch Communities, Inc., 5.875%, Due 4/15/2023C | | | 45 | | | | 46 | |

TransDigm, Inc., 6.00%, Due 7/15/2022 | | | 55 | | | | 55 | |

Verso Paper Holdings LLC / Verso Paper, Inc., 11.75%, Due 1/15/2019D | | | 695 | | | | 77 | |

Xerium Technologies, Inc., 8.875%, Due 6/15/2018 | | | 395 | | | | 403 | |

| | | | | | | | |

| | | | | | | 2,577 | |

| | | | | | | | |

Service - 14.45% | | | | | | | | |

Caesars Entertainment Operating Co., Inc., 12.75%, Due 4/15/2018 | | | 400 | | | | 118 | |

Cengage Learning Acquisitions, Inc., Escrow, 11.50%, Due 4/15/2020B C H I J | | | 75 | | | | — | |

Cenveo Corp., | | | | | | | | |

11.50%, Due 5/15/2017 | | | 25 | | | | 24 | |

6.00%, Due 8/1/2019C | | | 35 | | | | 31 | |

8.50%, Due 9/15/2022C | | | 430 | | | | 316 | |

Chinos Intermediate Holdings A, Inc., 7.75%, Due 5/1/2019C F | | | 50 | | | | 18 | |

CHS/Community Health Systems, Inc., 5.125%, Due 8/1/2021 | | | 100 | | | | 103 | |

Clear Channel Worldwide Holdings, Inc., 6.50%, Due 11/15/2022 | | | 525 | | | | 560 | |

Covanta Holding Corp., 5.875%, Due 3/1/2024 | | | 100 | | | | 99 | |

CST Brands, Inc., 5.00%, Due 5/1/2023 | | | 75 | | | | 76 | |

DISH DBS Corp., 5.875%, Due 7/15/2022 | | | 205 | | | | 201 | |

Dollar Tree, Inc., 5.75%, Due 3/1/2023C D | | | 70 | | | | 74 | |

DreamWorks Animation SKG, Inc., 6.875%, Due 8/15/2020C | | | 125 | | | | 124 | |

HealthSouth Corp., 5.75%, Due 9/15/2025C | | | 75 | | | | 75 | |

Jo-Ann Stores Holdings, Inc., 9.75%, Due 10/15/2019C F | | | 295 | | | | 223 | |

Landry’s, Inc., 9.375%, Due 5/1/2020C | | | 400 | | | | 428 | |

LBI Media, Inc., 4.25%, Due 4/15/2020C F | | | 358 | | | | 357 | |

Nexstar Broadcasting, Inc., 6.125%, Due 2/15/2022C | | | 75 | | | | 75 | |

Select Medical Corp., 6.375%, Due 6/1/2021 | | | 460 | | | | 406 | |

Tenet Healthcare Corp., 8.125%, Due 4/1/2022 | | | 175 | | | | 185 | |

United Rentals North America, Inc., 6.125%, Due 6/15/2023 | | | 40 | | | | 42 | |

| | | | | | | | |

| | | | | | | 3,535 | |

| | | | | | | | |

Telecommunications - 4.58% | | | | | | | | |

Avaya, Inc., 10.50%, Due 3/1/2021C | | | 400 | | | | 156 | |

Brightstar Corp., 9.50%, Due 12/1/2016C | | | 35 | | | | 35 | |

Frontier Communications Corp., 11.00%, Due 9/15/2025C | | | 65 | | | | 68 | |

Hughes Satellite Systems Corp., 7.625%, Due 6/15/2021 | | | 75 | | | | 82 | |

Intelsat Luxembourg S.A., 7.75%, Due 6/1/2021 | | | 125 | | | | 74 | |

Nokia OYJ, 6.625%, Due 5/15/2039 | | | 200 | | | | 210 | |

Sprint Capital Corp., 8.75%, Due 3/15/2032 | | | 75 | | | | 68 | |

Sprint Corp., 7.875%, Due 9/15/2023 | | | 35 | | | | 32 | |

Sprint Nextel Corp., | | | | | | | | |

8.375%, Due 8/15/2017 | | | 15 | | | | 15 | |

7.00%, Due 8/15/2020 | | | 40 | | | | 37 | |

Telecom Italia SpA, 5.303%, Due 5/30/2024C | | | 85 | | | | 85 | |

T-Mobile USA, Inc., 6.633%, Due 4/28/2021 | | | 35 | | | | 36 | |

Virgin Media Secured Finance PLC, 5.25%, Due 1/15/2026C | | | 125 | | | | 125 | |

See accompanying notes

14

American Beacon High Yield Bond FundSM

Schedule of Investments

October 31, 2015

| | | | | | | | |

| | | Par Amount | | | Fair Value | |

| | | (000’s) | | | (000’s) | |

Wind Acquisition Finance S.A., 7.375%, Due 4/23/2021C | | $ | 65 | | | $ | 65 | |

Windstream Services LLC, 7.50%, Due 6/1/2022D | | | 40 | | | | 33 | |

| | | | | | | | |

| | | | | | | 1,121 | |

| | | | | | | | |

Transportation - 1.20% | | | | | | | | |

Global Ship Lease, Inc., 10.00%, Due 4/1/2019C | | | 100 | | | | 100 | |

VistaJet Malta Finance PLC / VistaJet Co. Finance LLC, 7.75%, Due 6/1/2020C D G | | | 225 | | | | 195 | |

| | | | | | | | |

| | | | | | | 295 | |

| | | | | | | | |

Utilities - 0.26% | | | | | | | | |

AES Corp., 5.50%, Due 4/15/2025 | | | 25 | | | | 23 | |

Dynegy, Inc., 7.625%, Due 11/1/2024I | | | 40 | | | | 40 | |

| | | | | | | | |

| | | | | | | 63 | |

| | | | | | | | |

Total Corporate Obligations (Cost $13,796) | | | | | | | 11,551 | |

| | | | | | | | |

| | |

| | | Shares | | | | |

SHORT-TERM INVESTMENTS - 499.02% (Cost $122,050) | | | | | | | | |

JPMorgan U.S. Government Money Market Fund, Capital Class | | | 122,050,180 | | | | 122,050 | |

| | | | | | | | |

TOTAL INVESTMENTS - 546.55% (Cost $135,981) | | | | | | | 133,674 | |

LIABILITIES, NET OF OTHER ASSETS - (446.55%) | | | | | | | (109,216 | ) |

| | | | | | | | |

TOTAL NET ASSETS - 100.00% | | | | | | $ | 24,458 | |

| | | | | | | | |

Percentages are stated as a percent of net assets.

| A | Non-income producing security. |

| B | The coupon rate shown on floating or adjustable rate securities represents the rate at period end. The due date on these types of securities reflects the final maturity date. |

| C | Security exempt from registration under the Securities Act of 1933. These securities may be resold to qualified institutional buyers pursuant to Rule 144A. At the period end, the value of these securities amounted to $6,693 or 27.37% of net assets. The Fund has no right to demand registration of these securities. |

| D | LLC - Limited Liability Company. |

| E | LP - Limited Partnership. |

| G | PLC - Public Limited Company. |

| H | Fair valued pursuant to procedures approved by the Board of Trustees. At period end, the value of these securities amounted to $0 or 0.00% of net assets. |

See accompanying notes

15

American Beacon Intermediate Bond FundSM

Schedule of Investments

October 31, 2015

| | | | | | | | |

| | | Shares | | | Fair Value | |

| | | | | | (000’s) | |

SHORT-TERM INVESTMENTS – 6,641.96% (Cost $337,146) | | | | | | | | |

JPMorgan U.S. Government Money Market Fund, Capital Class | | | 337,145,787 | | | $ | 337,146 | |

| | | | | | | | |

TOTAL INVESTMENTS - 6,641.96% (Cost $337,146) | | | | | | | 337,146 | |

LIABILITIES, NET OF OTHER ASSETS - (6,541.96%) | | | | | | | (332,070 | ) |

| | | | | | | | |

TOTAL NET ASSETS - 100.00% | | | | | | $ | 5,076 | |

| | | | | | | | |

Percentages are stated as a percent of net assets.

See accompanying notes

16

American Beacon Short-Term Bond FundSM

Schedule of Investments

October 31, 2015

| | | | | | | | |

| | | Shares | | | Fair Value | |

| | | | | | (000’s) | |

SHORT-TERM INVESTMENTS - 726.13% (Cost $235,991) | | | | | | | | |

JPMorgan U.S. Government Money Market Fund, Capital Class | | | 235,990,551 | | | $ | 235,991 | |

| | | | | | | | |

TOTAL INVESTMENTS - 726.13% (Cost $235,991) | | | | | | | 235,991 | |

LIABILITIES, NET OF OTHER ASSETS - (626.13%) | | | | | | | (203,491 | ) |

| | | | | | | | |

TOTAL NET ASSETS - 100.00% | | | | | | $ | 32,500 | |

| | | | | | | | |

Percentages are stated as a percent of net assets.

See accompanying notes

17

American Beacon FundsSM

Statements of Assets and Liabilities

October 31, 2015 (in thousands except share and per share amounts)

| | | | | | | | | | | | |

| | | High Yield

Bond Fund | | | Intermediate

Bond Fund | | | Short-Term

Bond Fund | |

Assets: | | | | | | | | | | | | |

Investments in unaffiliated securities, at fair value A | | $ | 133,659 | | | $ | 337,146 | | | $ | 235,991 | |

Cash | | | 131 | | | | — | | | | — | |

Dividends and interest receivable | | | 258 | | | | 2 | | | | — | |

Receivable for investments sold | | | 4,353 | | | | — | | | | — | |

Receivable for fund shares sold | | | 4 | | | | — | | | | 4 | |

Receivable for expense reimbursement (Note 2) | | | 1 | | | | 5 | | | | 9 | |

Prepaid expenses | | | 15 | | | | 14 | | | | 19 | |

| | | | | | | | | | | | |

Total assets | | | 138,421 | | | | 337,167 | | | | 236,023 | |

| | | | | | | | | | | | |

Liabilities: | | | | | | | | | | | | |

Payable for investments purchased | | | 918 | | | | — | | | | — | |

Payable for fund shares redeemed | | | 112,911 | | | | 331,943 | | | | 203,403 | |

Dividends payable | | | 4 | | | | — | | | | — | |

Management and investment advisory fees payable | | | 50 | | | | 58 | | | | 39 | |

Administrative service and service fees payable | | | 14 | | | | 15 | | | | 13 | |

Transfer agent fees payable | | | 3 | | | | 4 | | | | 13 | |

Custody and fund accounting fees payable | | | 6 | | | | 7 | | | | 3 | |

Professional fees payable | | | 44 | | | | 44 | | | | 45 | |

Trustee fees payable | | | 2 | | | | 6 | | | | 4 | |

Payable for prospectus and shareholder reports | | | 10 | | | | 13 | | | | 3 | |

Other liabilities | | | 1 | | | | 1 | | | | — | |

| | | | | | | | | | | | |

Total liabilities | | | 113,963 | | | | 332,091 | | | | 203,523 | |

| | | | | | | | | | | | |

Net Assets | | $ | 24,458 | | | $ | 5,076 | | | $ | 32,500 | |

| | | | | | | | | | | | |

Analysis of Net Assets: | | | | | | | | | | | | |

Paid-in-capital | | | 54,417 | | | | 3,514 | | | | 39,945 | |

Undistributed (or overdistribution of) net investment income | | | (332 | ) | | | — | | | | 459 | |

Accumulated net realized gain (loss) | | | (27,305 | ) | | | 1,562 | | | | (7,904 | ) |

Unrealized (depreciation) of investments | | | (2,316 | ) | | | — | | | | — | |

Unrealized (depreciation) of currency transactions | | | (6 | ) | | | — | | | | — | |

| | | | | | | | | | | | |

Net assets | | $ | 24,458 | | | $ | 5,076 | | | $ | 32,500 | |

| | | | | | | | | | | | |

Shares outstanding at no par value (unlimited shares authorized): | | | | | | | | | | | | |

Institutional Class | | | 2,148,044 | | | | 304,050 | | | | 3,132,897 | |

| | | | | | | | | | | | |

Y Class | | | 96,960 | | | | 20,541 | | | | 98,040 | |

| | | | | | | | | | | | |

Investor Class | | | 505,951 | | | | 72,486 | | | | 389,553 | |

| | | | | | | | | | | | |

A Class | | | 104,835 | | | | 42,348 | | | | 51,441 | |

| | | | | | | | | | | | |

C Class | | | 197,999 | | | | 35,795 | | | | 97,685 | |

| | | | | | | | | | | | |

AMR Class | | | 68,622 | | | | N/A | | | | N/A | |

| | | | | | | | | | | | |

Net assets (not in thousands): | | | | | | | | | | | | |

Institutional Class | | $ | 16,818,629 | | | $ | 3,247,260 | | | $ | 27,006,635 | |

| | | | | | | | | | | | |

Y Class | | $ | 762,100 | | | $ | 220,295 | | | $ | 846,833 | |

| | | | | | | | | | | | |

Investor Class | | $ | 3,964,994 | | | $ | 773,613 | | | $ | 3,360,116 | |

| | | | | | | | | | | | |

A Class | | $ | 822,398 | | | $ | 451,981 | | | $ | 443,900 | |

| | | | | | | | | | | | |

C Class | | $ | 1,552,242 | | | $ | 382,582 | | | $ | 842,497 | |

| | | | | | | | | | | | |

AMR Class | | $ | 537,657 | | | $ | N/A | | | $ | N/A | |

| | | | | | | | | | | | |

Net asset value, offering and redemption price per share: | | | | | | | | | | | | |

Institutional Class | | $ | 7.83 | | | $ | 10.68 | | | $ | 8.62 | |

| | | | | | | | | | | | |

Y Class | | $ | 7.86 | | | $ | 10.72 | | | $ | 8.64 | |

| | | | | | | | | | | | |

Investor Class | | $ | 7.84 | | | $ | 10.67 | | | $ | 8.63 | |

| | | | | | | | | | | | |

A Class | | $ | 7.84 | | | $ | 10.67 | | | $ | 8.63 | |

| | | | | | | | | | | | |

A Class (offering price) | | $ | 8.23 | | | $ | 11.20 | | | $ | 8.85 | |

| | | | | | | | | | | | |

C Class | | $ | 7.84 | | | $ | 10.69 | | | $ | 8.62 | |

| | | | | | | | | | | | |

AMR Class | | $ | 7.84 | | | | N/A | | | | N/A | |

| | | | | | | | | | | | |

A Cost of investments in unaffiliated securities | | $ | 135,981 | | | $ | 337,146 | | | $ | 235,991 | |

See accompanying nortes

18

American Beacon FundsSM

Statements of Operations

For the year ended October 31, 2015 (in thousands)

| | | | | | | | | | | | |

| | | High Yield

Bond Fund | | | Intermediate

Bond Fund | | | Short-Term

Bond Fund | |

Investment income: | | | | | | | | | | | | |

Dividend income from unaffiliated securities (net of foreign taxes) A | | $ | 41 | | | $ | 2 | | | $ | 1 | |

Interest income | | | 12,238 | | | | 10,026 | | | | 1,768 | |

Other Income | | | 81 | | | | — | | | | 1 | |

| | | | | | | | | | | | |

Total investment income | | | 12,360 | | | | 10,028 | | | | 1,770 | |

| | | | | | | | | | | | |

Expenses: | | | | | | | | | | | | |

Management and investment advisory fees (Note 2) | | | 767 | | | | 809 | | | | 458 | |

Administrative service fees (Note 2): | | | | | | | | | | | | |

Institutional Class | | | 157 | | | | 201 | | | | 111 | |

Y Class | | | 3 | | | | 1 | | | | 3 | |

Investor Class | | | 16 | | | | 4 | | | | 15 | |

A Class | | | 4 | | | | 1 | | | | 2 | |

C Class | | | 6 | | | | 1 | | | | 3 | |

AMR Class | | | 61 | | | | — | | | | — | |

Transfer agent fees: | | | | | | | | | | | | |

Institutional Class | | | 26 | | | | 13 | | | | 20 | |

Investor Class | | | 2 | | | | 2 | | | | 3 | |

AMR Class | | | 5 | | | | — | | | | — | |

Custody and fund accounting fees | | | 50 | | | | 56 | | | | 30 | |

Professional fees | | | 48 | | | | 54 | | | | 49 | |

Registration fees and expenses | | | 74 | | | | 72 | | | | 76 | |

Service fees (Note 2): | | | | | | | | | | | | |

Y Class | | | 1 | | | | — | | | | 1 | |

Investor Class | | | 13 | | | | 3 | | | | 13 | |

A Class | | | 2 | | | | 1 | | | | 1 | |

C Class | | | 3 | | | | 1 | | | | 2 | |

Distribution fees (Note 2): | | | | | | | | | | | | |

A Class | | | 3 | | | | 1 | | | | 2 | |

C Class | | | 18 | | | | 4 | | | | 11 | |

Prospectus and shareholder report expenses | | | 40 | | | | 33 | | | | 25 | |

Trustee fees | | | 10 | | | | 22 | | | | 12 | |

Other expenses | | | 12 | | | | 24 | | | | 10 | |

| | | | | | | | | | | | |

Total expenses | | | 1,321 | | | | 1,303 | | | | 847 | |

| | | | | | | | | | | | |

Net fees waived and expenses reimbursed (Note 2) | | | (17 | ) | | | (8 | ) | | | (20 | ) |

| | | | | | | | | | | | |

Net expenses | | | 1,304 | | | | 1,295 | | | | 827 | |

| | | | | | | | | | | | |

Net investment income | | | 11,056 | | | | 8,733 | | | | 943 | |

| | | | | | | | | | | | |

Realized and unrealized gain (loss) from investments: | | | | | | | | | | | | |

Net realized gain (loss) from: | | | | | | | | | | | | |

Investments | | | (27,180 | ) | | | 8,315 | | | | 314 | |

Foreign currency transactions | | | (4 | ) | | | — | | | | — | |

Change in net unrealized appreciation or (depreciation) of: | | | | | | | | | | | | |

Investments | | | 3,124 | | | | (10,371 | ) | | | (387 | ) |

Foreign currency transactions | | | (6 | ) | | | — | | | | — | |

| | | | | | | | | | | | |

Net (loss) from investments | | | (24,066 | ) | | | (2,056 | ) | | | (73 | ) |

| | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | $ | (13,010 | ) | | $ | 6,677 | | | $ | 870 | |

| | | | | | | | | | | | |

A Foreign taxes | | | (7 | ) | | | — | | | | — | |

See accompanying notes

19

American Beacon FundsSM

Statements of Changes in Net Assets (in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | High Yield Bond Fund | | | Intermediate Bond Fund | | | Short-Term Bond Fund | |

| | | Year Ended

October 31,

2015 | | | Year Ended

October 31,

2014 | | | Year Ended

October 31,

2015 | | | Year Ended

October 31,

2014 | | | Year Ended

October 31,

2015 | | | Year Ended

October 31,

2014 | |

Increase (Decrease) in Net Assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income | | $ | 11,056 | | | $ | 12,859 | | | $ | 8,733 | | | $ | 8,942 | | | $ | 943 | | | $ | 889 | |

Net realized gain (loss) from investments and foreign currency transactions | | | (27,184 | ) | | | 3,657 | | | | 8,315 | | | | 1,625 | | | | 314 | | | | 562 | |

Change in net unrealized appreciation or (depreciation) of investments and foreign currency transactions | | | 3,118 | | | | (8,008 | ) | | | (10,371 | ) | | | 3,464 | | | | (387 | ) | | | (234 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets resulting from operations | | | (13,010 | ) | | | 8,508 | | | | 6,677 | | | | 14,031 | | | | 870 | | | | 1,217 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Distributions to Shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income: | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | (3,014 | ) | | | (4,444 | ) | | | (9,425 | ) | | | (11,444 | ) | | | (2,245 | ) | | | (1,692 | ) |

Y Class | | | (55 | ) | | | (110 | ) | | | (5 | ) | | | (4 | ) | | | (8 | ) | | | (10 | ) |

Investor Class | | | (287 | ) | | | (447 | ) | | | (23 | ) | | | (42 | ) | | | (32 | ) | | | (52 | ) |

A Class | | | (74 | ) | | | (81 | ) | | | (8 | ) | | | (9 | ) | | | (6 | ) | | | (10 | ) |

C Class | | | (87 | ) | | | (95 | ) | | | (4 | ) | | | (6 | ) | | | — | | | | — | |

AMR Class | | | (7,432 | ) | | | (8,270 | ) | | | — | | | | — | | | | — | | | | — | |

Net realized gain from investments: | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | (1,357 | ) | | | (219 | ) | | | (1,286 | ) | | | (447 | ) | | | — | | | | — | |

Y Class | | | (19 | ) | | | (7 | ) | | | (1 | ) | | | — | | | | — | | | | — | |

Investor Class | | | (100 | ) | | | (26 | ) | | | (4 | ) | | | (2 | ) | | | — | | | | — | |

A Class | | | (24 | ) | | | (4 | ) | | | (1 | ) | | | (1 | ) | | | — | | | | — | |

C Class | | | (28 | ) | | | (7 | ) | | | (1 | ) | | | (1 | ) | | | — | | | | — | |

AMR Class | | | (2,077 | ) | | | (464 | ) | | | — | | | | — | | | | — | | | | — | |

Tax return of capital | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | (183 | ) | | | — | | | | (352 | ) | | | — | | | | — | | | | — | |

Y Class | | | (3 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

Investor Class | | | (13 | ) | | | — | | | | (1 | ) | | | — | | | | — | | | | — | |

A Class | | | (3 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

C Class | | | (4 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

AMR Class | | | (280 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net distributions to shareholders | | | (15,040 | ) | | | (14,174 | ) | | | (11,111 | ) | | | (11,956 | ) | | | (2,291 | ) | | | (1,764 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Capital Share Transactions: | | | | | | | | | | | | | | | | | | | | | | | | |

Proceeds from sales of shares | | | 42,744 | | | | 85,739 | | | | 58,701 | | | | 125,929 | | | | 137,675 | | | | 197,178 | |

Reinvestment of dividends | | | 14,916 | | | | 13,951 | | | | 11,096 | | | | 11,935 | | | | 2,279 | | | | 1,753 | |

Cost of shares redeemed | | | (227,791 | ) | | | (80,199 | ) | | | (476,265 | ) | | | (66,463 | ) | | | (410,329 | ) | | | (56,401 | ) |

Redemption fees | | | (7 | ) | | | 31 | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets from capital share transactions | | | (170,138 | ) | | | 19,522 | | | | (406,468 | ) | | | 71,401 | | | | (270,375 | ) | | | 142,530 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net assets | | | (198,188 | ) | | | 13,856 | | | | (410,902 | ) | | | 73,476 | | | | (271,796 | ) | | | 141,983 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net Assets: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning of period | | | 222,646 | | | | 208,790 | | | | 415,978 | | | | 342,502 | | | | 304,296 | | | | 162,313 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

End of Period * | | $ | 24,458 | | | $ | 222,646 | | | $ | 5,076 | | | $ | 415,978 | | | $ | 32,500 | | | $ | 304,296 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

*Includes undistributed (or overdistribution of) net investment income | | $ | (332 | ) | | $ | (433 | ) | | $ | — | | | $ | (23 | ) | | $ | 459 | | | $ | (556 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes

20

American Beacon FundsSM

Notes to Financial Statements

October 31, 2015

1. Organization

American Beacon Funds (the “Trust”), is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, (the “Act”) as a diversified, open-end management investment company. As of October 31, 2015, the Trust consists of thirty-two active series, three of which are presented in this filing (collectively, the “Funds” and each individually a “Fund”): American Beacon High Yield Bond Fund, American Beacon Intermediate Bond Fund, and American Beacon Short-Term Bond Fund. The remaining twenty-nine active series are reported in separate filings.

Effective April 30, 2015, American Beacon Advisors, Inc. (the “Manager”) became a wholly-owned subsidiary of Astro AB Borrower, Inc., which is indirectly owned by investment funds affiliated with Kelso & Company, L.P. and Estancia Capital Management, LLC, two prominent private equity firms. Prior to April 30, the Manager was a wholly-owned subsidiary of Lighthouse Holdings, Inc., which was indirectly owned by investment funds affiliated with Pharos Capital Group, LLC and TPG Capital, L.P., two leading private equity firms.

The Manager has closed the High Yield Bond, Intermediate Bond and Short-Term Bond Funds to new shareholders as of the close of business on August 20, 2015. Existing shareholders as of that date may continue to purchase, redeem, or exchange shares of the Funds on any business day, which is any day the New York Stock Exchange is open for business.

Class Disclosure

Each Fund has multiple classes of shares designed to meet the needs of different groups of investors; however, not all Funds offer all classes. The following table sets forth the differences amongst the classes:

| | |

Class: | | Offered to: |

| Institutional Class | | Investors making an initial investment of $250,000 |

| Y Class | | Investors making an initial investment of $100,000 |

| Investor Class | | General public and investors investing through an intermediary |

| A Class | | General public and investors investing through an intermediary with applicable sales charges, which may include a front-end sales charge and a contingent deferred sales charge (“CDSC”) |

| C Class | | General public and investors investing through an intermediary with applicable sales charges, which may include a CDSC |

| AMR Class | | Investors in the tax-exempt retirement and benefit plans of the Manager, AMR Corporation, and its affiliates |

Each class offered by the Trust has equal rights as to assets and voting privileges. Income and non-class specific expenses are allocated daily to each class on the basis of the relative net assets. Realized and unrealized capital gains and losses of each class are allocated daily based on the relative net assets of each class of the respective Fund. Class specific expenses, where applicable, currently include administrative service fees, service fees, and distribution fees and vary amongst the classes as described more fully in Note 2.

2. Transactions with Affiliates

Management Agreement

The Trust and the Manager are parties to a Management Agreement that obligates the Manager to provide or oversee the provision of all investment advisory and fund management. Investment assets of the High Yield Bond and Intermediate Bond Funds are managed by one or more investment advisors which have entered into separate investment advisory agreements with the Manager and the Trust. As compensation for performing the duties required under the Management Agreement, the Manager receives from the High Yield Bond Fund an annualized fee equal to 0.05% of the average daily net assets. The Funds pay the investment advisors hired by the Manager to direct investment activities of the Funds. The Manager receives an annualized

21

American Beacon FundsSM

Notes to Financial Statements

October 31, 2015

fee of 0.20% of the average daily net assets of the Intermediate Bond Fund and pays a portion of its fee to an investment advisor hired by the Manager to direct investment activities of a portion of the Fund. The Manager serves as the sole investment advisor to the Short-Term Bond Fund and receives an annualized fee of 0.20% of the average daily net assets of the Fund. Management fees paid during the year ended October 31, 2015 were as follows (dollars in thousands):

| | | | | | | | | | | | | | | | |

| | | Management

Fee Rate | | | Management

Fee | | | Amounts paid

to Investment

Advisors | | | Amounts Paid

to Manager | |

High Yield Bond | | | 0.42 | % | | $ | 767 | | | $ | 675 | | | $ | 92 | |

Intermediate Bond | | | 0.20 | % | | | 809 | | | | 302 | | | | 507 | |

Short-Term Bond | | | 0.20 | % | | | 458 | | | | — | | | | 458 | |

Administration Agreement

The Manager and the Trust entered into an Administration Agreement which obligates the Manager to provide or oversee administrative services to the Funds. As compensation for performing the duties required under the Administration Agreement, the Manager receives an annualized fee of 0.30% of the average daily net assets of the Institutional, Y, Investor, A, and C Classes of each Fund and 0.05% of the average daily net assets of the AMR Class, except for the Institutional Class of the Intermediate and Short-Term Bond Funds from which the Manager receives a fee of 0.05% of average daily net assets.

Distribution Plans

The Funds, except for the A and C Classes of the Funds, have adopted a “defensive” Distribution Plan (the “Plan”) in accordance with Rule 12b-1 under the Act, pursuant to which no separate fees may be charged to the Funds for distribution purposes. However, the Plan authorizes the management and administrative service fees received by the Manager and the investment advisors hired by the Manager to be used for distribution purposes. Under this Plan, the Funds do not intend to compensate the Manager or any other party, either directly or indirectly, for the distribution of Fund shares.

Separate Distribution Plans (the “Distribution Plans”) have been adopted pursuant to Rule 12b-1 under the Act for the A and C Classes of the Funds. Under the Distribution Plans, as compensation for distribution assistance, the Manager receives an annual fee of 0.25% of the average daily net assets of each A Class and 1.00% of the average daily net assets of each C Class. The fee will be payable without regard to whether the amount of the fee is more or less than the actual expenses incurred in a particular month by the Manager for distribution assistance.

Service Plans

The Manager and the Trust entered into Service Plans that obligate the Manager to oversee additional shareholder servicing of the Y, Investor, A, and C Classes. As compensation for performing the duties required under the Service Plans, the Manager receives 0.10% of the average daily net assets of the Y Class, 0.15% of the average daily net assets of the A and C Classes, and up to 0.375% of the average daily net assets of the Investor Class of each Fund.

Interfund Lending Program

Pursuant to an exemptive order by the Securities and Exchange Commission (“SEC”), the Funds, along with other registered investment companies having management contracts with the Manager, may participate in an interfund lending program. This program provides an alternative credit facility allowing the Funds to borrow from or lend to other participating Funds. During the year ended October 31, 2015, the Short-Term Bond Fund loaned on average $1,021,041 for 42 days at an average rate of 0.75% with interest earned of $879. The amount is included as interest income on the Statements of Operations. The High Yield Bond and Intermediate Bond Funds did not participate in the Interfund Lending Program during the year ended October 31, 2015.

22

American Beacon FundsSM

Notes to Financial Statements

October 31, 2015

Expense Reimbursement Plan

The Manager voluntarily and contractually agreed to reimburse the following Funds to the extent that total operating expenses exceeded the Fund’s expense cap. For the year ended October 31, 2015, the Manager reimbursed expenses as follows:

| | | | | | | | | | | | | | | | |

| | | | | Expense Caps | | | | | | |

Fund | | Class | | 11/1/14 to

2/28/15 | | | 3/1/15 to

10/31/15 | | | Reimbursed

(Recovered)

Expenses | | | Expiration of

Reimbursements |