UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-5018

Smith Barney Investment Series

(Exact name of registrant as specified in charter)

125 Broad Street, New York, NY 10004

(Address of principal executive offices) (Zip code)

Robert I. Frenkel, Esq.

Legg Mason & Co., LLC

300 First Stamford Place, 4th Floor

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 451-2010

Date of fiscal year end: October 31

Date of reporting period: October 31, 2005

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

EXPERIENCE

ANNUAL REPORT

OCTOBER 31, 2005

SB Growth and Income Fund

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

SB Growth and Income Fund

Annual Report • October 31, 2005

What’s

Inside

Fund Objective

The Fund seeks reasonable growth and income. It invests in a portfolio consisting principally of equity securities, including convertible securities, that provide dividend or interest income. However, it may also invest in non-income producing investments for potential appreciation in value.

Under a licensing agreement between Citigroup and Legg Mason, the names of funds, the names of any classes of shares of funds, and the names of investment advisers of funds, as well as all logos, trademarks and service marks related to Citigroup or any of its affiliates (“Citi Marks”) are licensed for use by Legg Mason. Citi Marks include, but are not limited to, “Smith Barney,” “Salomon Brothers,” “Citi,” “Citigroup Asset Management,” and “Davis Skaggs Investment Management”. Legg Mason and its affiliates, as well as the Fund’s investment manager, are not affiliated with Citigroup.

All Citi Marks are owned by Citigroup, and are licensed for use until no later than one year after the date of the licensing agreement.

Letter from the Chairman

R. JAY GERKEN, CFA

Chairman, President and Chief Executive Officer

Dear Shareholder,

The U.S. economy was surprisingly resilient during the fiscal year. While surging oil prices, rising interest rates, and the impact of Hurricanes Katrina and Rita threatened to derail the economic expansion, growth remained solid throughout the period. After a 3.3% advance in the second quarter of 2005, third quarter gross domestic product (“GDP”)i growth grew to 4.3%, marking the tenth consecutive quarter in which GDP growth grew 3.0% or more.

As expected, the Federal Reserve Board (“Fed”)ii continued to raise interest rates in an attempt to ward off inflation. After raising rates three times from June 2004 through September 2004, the Fed increased its target for the federal funds rateiii in 0.25% increments eight additional times over the reporting period. The Fed again raised rates in early November, after the Fund’s reporting period had ended. All told, the Fed’s twelve rate hikes have brought the target for the federal funds rate from 1.00% to 4.00%. This represents the longest sustained Fed tightening cycle since 1976-1979.

During the 12-month period covered by this report, the U.S. stock market generated solid results, with S&P 500 Indexiv returning 8.72%. Generally positive economic news, relatively benign core inflation, and strong corporate profits supported the market during much of the period.

Looking at the fiscal year as a whole, mid-cap stocks generated superior returns, with the Russell Midcapv, Russell 1000vi, and Russell 2000vii Indices returning 18.09%, 10.47%, and 12.08%, respectively. From a market style perspective, value-oriented stocks significantly outperformed their growth counterparts, with the Russell 3000 Valueviii and Russell 3000 Growthix Indices returning 11.96% and 8.99%, respectively.

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s fiscal year and to learn how those conditions have affected Fund performance.

SB Growth and Income Fund 1

Special Shareholder Notice

On December 1, 2005, Citigroup Inc. (“Citigroup”) completed the sale of substantially all of its asset management business, Citigroup Asset Management (“CAM”), to Legg Mason, Inc. (“Legg Mason”). As a result, the Fund’s investment manager (the “Manager”), previously an indirect wholly-owned subsidiary of Citigroup, has become a wholly-owned subsidiary of Legg Mason. Completion of the sale caused the Fund’s existing investment management contract to terminate. The Fund’s shareholders previously approved a new investment management contract between the Fund and the Manager which became effective on December 1, 2005.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Fund’s Manager and some of its affiliates have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, the Fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund has been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

Important information concerning the Fund and its Manager with regard to recent regulatory developments is contained in the Notes to Financial Statements included in this report.

2 SB Growth and Income Fund

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

December 1, 2005

All index performance reflects no deduction for fees, expenses or taxes. Please note an investor cannot invest directly in an index.

| i | | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| iv | | The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. Please note that an investor cannot invest directly in an index. |

| v | | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index whose average market capitalization was approximately $4.7 billion as of 6/24/05. |

| vi | | The Russell 1000 Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. |

| vii | | The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. |

| viii | | The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. (A price-to-book ratio is the price of a stock compared to the difference between a company’s assets and liabilities.) |

| ix | | The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. |

SB Growth and Income Fund 3

Manager Overview

| | | | |

| |  | | MICHAEL KAGAN PORTFOLIO MANAGER (left) KEVIN CALIENDO PORTFOLIO MANAGER (right) |

Q. What were the overall market conditions during the Fund’s reporting period?

A. The market was led by the energy related (energy and utilities) and the defensive (consumer staples, health care and financials) sectors. Oil and natural gas prices rose through the period, hitting all time highs in late August 2005. Supply/demand fundamentals have been tight for energy for the past twenty-four months, but hit a peak in August from the damage done to Gulf of Mexico production facilities by Hurricanes Katrina and Rita. Energy fundamentals appear balanced to us, with strong demand growth in China and India offset by lower gasoline demand in the US due to higher prices. The Federal Reserve Board (“Fed”)i raised interest rates 0.25% at each of the last twelve meetings. We believe that it is likely that the Fed is likely to continue increasing rates until we hit historical normal levels of real interest rates. That would entail further increases into 2006. Defensive stocks outperformed due to fears that higher oil prices and interest rates would slow economic growth.

The Chinese government partly floated its currency vs. the dollar and the Yen starting in late July. Gold prices began to rise coinciding with the first floating of the Yuan.

General Motors faced two crises in 2005, first the downgrading of its credit rating to below investment grade and second the bankruptcy of Delphi Automotive, its largest parts supplier and onetime spin off. Currently the debt markets are pricing in a 30% probability of GM’s own bankruptcy within eighteen months. General Motors and Ford are struggling with high costs, declining market shares and a shift away from high profit SUV’s. The portfolio has avoided and will continue to avoid any auto related exposure.

Performance Review

For the 12 months ended October 31, 2005, Smith Barney Class A shares of the SB Growth and Income Fund, excluding sales charges, returned 6.16%. These shares underperformed the Lipper Large-Cap Core Funds Category Average1 which increased 8.35%. The Fund’s unmanaged benchmark, the S&P 500 Indexii, returned 8.72% for the same period.

| 1 | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the 12-month period ended October 31, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 877 funds in the Fund’s Lipper category, and excluding sales charges. |

4 SB Growth and Income Fund 2005 Annual Report

| | | | | | |

| Fund Performance as of October 31, 2005 (excluding sales charges) (unaudited) |

| | | |

| | | 6 months | | 12 months | | |

| | | | | | | |

SB Growth and Income Fund—Smith Barney Class A Shares | | 4.70% | | 6.16% | | |

|

S&P 500 Index | | 5.27% | | 8.72% | | |

|

Lipper Large-Cap Core Funds Category Average | | 5.69% | | 8.35% | | |

|

|

| The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, please visit our website at www.citigroupam.com. |

| For Smith Barney Class 1 shares, Smith Barney Class A shares, Smith Barney Class B shares, Salomon Brothers Class A shares, Salomon Brothers Class B shares and Salomon Brothers Class C shares, current reimbursements and/or fee waivers are voluntary, and may be reduced or terminated at any time. Absent these reimbursements or waivers, the performance would have been lower. |

| All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Returns have not been adjusted to include sales charges that may apply when shares are purchased or the deduction of taxes that a shareholder would pay on Fund distributions. Excluding sales charges, Smith Barney Class 1 shares returned 4.79%, Smith Barney Class B shares returned 4.28%, Smith Barney Class C shares returned 4.33%, Smith Barney Class O shares returned 4.56%, Smith Barney Class P shares returned 4.63%, Smith Barney Class Y shares returned 4.91%, Salomon Brothers Class A shares returned 4.62%, Salomon Brothers Class B shares returned 4.11% and Salomon Brothers Class C shares returned 4.27% over the six months ended October 31, 2005. Excluding sales charges, Smith Barney Class 1 shares returned 6.48%, Smith Barney Class B shares returned 5.43%, Smith Barney Class C shares returned 5.51%, Smith Barney Class O shares returned 5.95%, Smith Barney Class P shares returned 5.94%, Smith Barney Class Y shares returned 6.75%, Salomon Brothers Class A shares returned 6.10%, Salomon Brothers Class B shares returned 5.32% and Salomon Brothers Class C shares returned 5.37% over the twelve months ended October 31, 2005. |

| Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the period ended October 31, 2005, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 912 funds for the six-month period and among the 877 funds for the 12-month period in the Fund’s Lipper category and excluding sales charges. |

Q. What were the most significant factors affecting Fund performance?

What were the leading contributors to performance?

A. The Fund had strong performance in the health care sector. Returns were helped by over-weights in HMO’s and generic drug stocks, and an underweight in large capitalization pharmaceuticals. We believe that cost pressures and a large number of drugs coming off patent will help HMO and generic drug company earnings and hurt the earnings of the traditional pharmaceutical companies. The consumer discretionary sector returns were helped by positions in Best Buy Co. Inc. and JC Penney Co., and the absence of any auto related stocks.

SB Growth and Income Fund 2005 Annual Report 5

The biggest contributors to performance were Boeing Co. (BA), Teva Pharmaceutical Industries Ltd. (TEVA) and Coventry Health Care Inc. (CVH). The best performing sectors were health care, consumer discretionary and industrials. Boeing was helped by orders of the new 787 plane, which outdid rival Airbus’ A350. Teva benefited from anticipation of a powerful pipeline of new products to come in 2006. Coventry delivered better than expected cost savings, and saw favorable medical cost trends.

The Fund was hurt by poor stock picking in the technology sector. Technology appears to be seeing a changing of the guard, and the Fund owned too many of the old guard and not enough of the new. Positions in International Business Machines Corp. (IBM), Dell Inc. (DELL) and Nortel Networks Corp. (NT) all detracted from performance.

What were the leading detractors from performance?

A. The stocks that most hurt performance were OSI Pharmaceuticals, Inc. (OSIP), Sara Lee Corp (SLE) and Nortel Networks Corp. (NT). The worst performing sectors were technology, consumer staples and materials. OSI had unfavorable tests of its Tarceva drug, and made what was in the eyes of Wall Street a poor acquisition of Eyetech. Sara Lee’s turnaround under new CEO Brenda Barnes took longer than expected. Sales growth at Nortel was insufficient to create earnings leverage.

Q. Were there any significant changes to the Fund during the reporting period?

A. The portfolio is higher growth and higher quality than it was coming into 2005. US corporate operating margins are now the highest since the late 1960’s. We believe that companies who derive their growth from revenues (typically growth stocks) will show higher earnings per share growth than companies who derive their earnings growth from operating margin expansion (typically value stocks). Many companies with strong franchises, balance sheets and returns, such as Microsoft Corp. and Walmart Stores Inc. and Ecolab Inc., which historically have looked expensive to us, now appear to us to trade at attractive levels.

6 SB Growth and Income Fund 2005 Annual Report

Thank you for your investment in the SB Growth and Income Fund. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | |

| |  |

Michael Kagan Portfolio Manager | | Kevin Caliendo Portfolio Manager |

December 1, 2005

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of October 31, 2005 and are subject to change and may not be representative of the portfolio manager’s current or future investments. The Fund’s top ten holdings (as a percentage of net assets) as of this date were: General Electric Co. (4.1%), Microsoft Corp. (3.7%), Boeing Co. (2.9%), Wells Fargo & Co. (2.5%), Exxon Mobil Corp. (2.5%), Sprint Nextel Corp. (2.4%), Barrick Gold Corp. (2.4%), Total SA (2.2%), JP Morgan Chase & Co. (2.2%) and PepsiCo Inc. (2.2%). Please refer to pages 14 through 18 for a list and percentage breakdown of the Fund’s holdings.

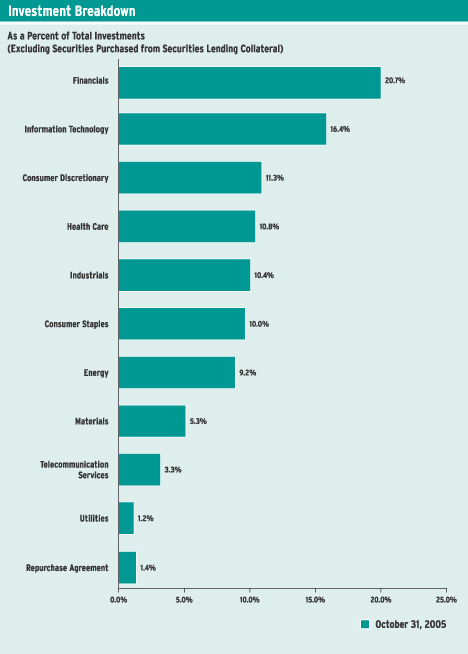

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. Portfolio holdings are subject to change at any time and may not be representative of the portfolio manager’s current or future investments. The Fund’s top five sector holdings (as a percentage of net assets) as of October 31, 2005 were: Financials (20.8%), Information Technology (16.4%), Consumer Discretionary (11.3%) Health Care (10.9%) and Industrials (10.4%). The Fund’s portfolio composition is subject to change at any time.

RISKS: The Fund is subject to certain risks of overseas investing not typically associated with investing in U.S. securities, including currency fluctuations and changes in political and economic conditions. These risks are magnified in emerging markets. Lower- rated, higher yielding bonds known as “junk bonds” are subject to greater credit and liquidity risks, including the risk of default, than higher-rated obligations. As interest rates rise, bond prices fall, reducing the value of the fixed income portion of the Fund. The Fund may engage in short sales. Losses from short sales may be unlimited. The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. The Fund may engage in active and frequent trading, resulting in increased transaction costs, which could detract from the Fund’s performance.

All index performance reflects no deduction for fees, expenses or taxes. Please note an investor cannot invest directly in an index.

| i | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| ii | | The S&P 500 index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S. Please note that an investor cannot invest directly in an index. |

SB Growth and Income Fund 2005 Annual Report 7

Fund at a Glance (unaudited)

8 SB Growth and Income Fund 2005 Annual Report

Fund Expenses (unaudited)

Example

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including front-end and back-end sales charges (loads) on purchase payments, reinvested distributions, including returns of capital, if any; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested on May 1, 2005 and held for the six months ended October 31, 2005.

Actual Expenses

The table below titled “Based on Actual Total Return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

| | | | | | | | | | | | | | | |

| Based on Actual Total Return(1) | | | | | | | | | | | | | |

| | | | | |

| | | Actual Total

Return Without

Sales Charges(2) | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratios | | | Expenses

Paid During

the Period(3) |

Smith Barney Class 1 | | 4.79 | % | | $ | 1,000.00 | | $ | 1,047.90 | | 0.96 | % | | $ | 4.96 |

|

Smith Barney Class A | | 4.70 | | | | 1,000.00 | | | 1,047.00 | | 1.25 | | | | 6.45 |

|

Smith Barney Class B | | 4.28 | | | | 1,000.00 | | | 1,042.80 | | 1.97 | | | | 10.14 |

|

Smith Barney Class C | | 4.33 | | | | 1,000.00 | | | 1,043.30 | | 1.87 | | | | 9.63 |

|

Smith Barney Class O | | 4.56 | | | | 1,000.00 | | | 1,045.60 | | 1.40 | | | | 7.22 |

|

Smith Barney Class P | | 4.63 | | | | 1,000.00 | | | 1,046.30 | | 1.35 | | | | 6.96 |

|

Smith Barney Class Y | | 4.91 | | | | 1,000.00 | | | 1,049.10 | | 0.69 | | | | 3.56 |

|

Salomon Brothers Class A | | 4.62 | | | | 1,000.00 | | | 1,046.20 | | 1.25 | | | | 6.45 |

|

Salomon Brothers Class B | | 4.11 | | | | 1,000.00 | | | 1,041.10 | | 2.00 | | | | 10.29 |

|

Salomon Brothers Class C | | 4.27 | | | | 1,000.00 | | | 1,042.70 | | 1.98 | | | | 10.19 |

|

| (1) | | For the six months ended October 31, 2005. |

| (2) | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect the deduction of the applicable sales charges with respect to Smith Barney Class 1, Smith Barney Class A and Salomon Brothers Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Smith Barney Class B, Smith Barney Class C, Smith Barney Class O, Smith Barney Class P, Salomon Brothers Class B and Salomon Brothers Class C shares. Total return is not annualized, as it may not be representative of the total return for the year. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (3) | | Expenses (net of voluntary fee waiver and/or expense reimbursement) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

SB Growth and Income Fund 2005 Annual Report 9

Fund Expenses (unaudited) (continued)

Hypothetical Example for Comparison Purposes

The table below titled “Based on Hypothetical Total Return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5.00% hypothetical example relating to the Fund with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or back-end sales charges (loads). Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | |

| Based on Hypothetical Total Return(1) |

| | | | | |

| | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | Ending

Account

Value | | Annualized

Expense

Ratios | | | Expenses

Paid During

the Period(2) |

Smith Barney Class 1 | | 5.00 | % | | $ | 1,000.00 | | $ | 1,020.37 | | 0.96 | % | | $ | 4.89 |

|

Smith Barney Class A | | 5.00 | | | | 1,000.00 | | | 1,018.90 | | 1.25 | | | | 6.36 |

|

Smith Barney Class B | | 5.00 | | | | 1,000.00 | | | 1,015.27 | | 1.97 | | | | 10.01 |

|

Smith Barney Class C | | 5.00 | | | | 1,000.00 | | | 1,015.78 | | 1.87 | | | | 9.50 |

|

Smith Barney Class O | | 5.00 | | | | 1,000.00 | | | 1,018.15 | | 1.40 | | | | 7.12 |

|

Smith Barney Class P | | 5.00 | | | | 1,000.00 | | | 1,018.40 | | 1.35 | | | | 6.87 |

|

Smith Barney Class Y | | 5.00 | | | | 1,000.00 | | | 1,021.37 | | 0.69 | | | | 3.46 |

|

Salomon Brothers Class A | | 5.00 | | | | 1,000.00 | | | 1,018.90 | | 1.25 | | | | 6.36 |

|

Salomon Brothers Class B | | 5.00 | | | | 1,000.00 | | | 1,015.12 | | 2.00 | | | | 10.16 |

|

Salomon Brothers Class C | | 5.00 | | | | 1,000.00 | | | 1,015.22 | | 1.98 | | | | 10.06 |

|

| (1) | | For the six months ended October 31, 2005. |

| (2) | | Expenses (net of voluntary fee waiver and/or expense reimbursement) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, then divided by 365. |

10 SB Growth and Income Fund 2005 Annual Report

Fund Performance

| | | | | | | | | | | | | | | |

| Average Annual Total Returns† (unaudited) | |

| |

| | | Without Sales Charges(1)

| |

| | | Smith

Barney

Class 1 | | | Smith

Barney

Class A | | | Smith

Barney

Class B | | | Smith

Barney

Class C | | | Smith

Barney

Class O | |

Twelve Months Ended 10/31/05 | | 6.48 | % | | 6.16 | % | | 5.43 | % | | 5.51 | % | | 5.95 | % |

|

|

Five Years Ended 10/31/05 | | (2.31 | ) | | (2.62 | ) | | (3.55 | ) | | (3.19 | ) | | N/A | |

|

|

Ten Years Ended 10/31/05 | | 6.74 | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Inception* through 10/31/05 | | 8.15 | | | 5.80 | | | 4.89 | | | (2.58 | ) | | (1.82 | ) |

|

|

| | | | | |

| | | Smith

Barney

Class P | | | Smith

Barney

Class Y | | | Salomon

Brothers

Class A | | | Salomon

Brothers

Class B | | | Salomon

Brothers

Class C | |

Twelve Months Ended 10/31/05 | | 5.94 | % | | 6.75 | % | | 6.10 | % | | 5.32 | % | | 5.37 | % |

|

|

Five Years Ended 10/31/05 | | N/A | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Ten Years Ended 10/31/05 | | N/A | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Inception* through 10/31/05 | | (1.79 | ) | | (0.92 | ) | | 7.78 | | | 5.83 | | | 5.83 | |

|

|

| |

| | | With Sales Charges(2)

| |

| | | Smith

Barney

Class 1 | | | Smith

Barney

Class A | | | Smith

Barney

Class B | | | Smith

Barney

Class C | | | Smith

Barney

Class O | |

Twelve Months Ended 10/31/05 | | (2.58 | )% | | 0.85 | % | | 0.43 | % | | 4.51 | % | | 4.95 | % |

|

|

Five Years Ended 10/31/05 | | (4.03 | ) | | (3.61 | ) | | (3.73 | ) | | (3.19 | ) | | N/A | |

|

|

Ten Years Ended 10/31/05 | | 5.80 | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Inception* through 10/31/05 | | 7.64 | | | 5.21 | | | 4.89 | | | (2.58 | ) | | (1.82 | ) |

|

|

| | | | | |

| | | Smith

Barney

Class P | | | Smith

Barney

Class Y | | | Salomon

Brothers

Class A | | | Salomon

Brothers

Class B | | | Salomon

Brothers

Class C | |

Twelve Months Ended 10/31/05 | | 0.94 | % | | 6.75 | % | | 0.00 | % | | 0.32 | % | | 4.37 | % |

|

|

Five Years Ended 10/31/05 | | N/A | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Ten Years Ended 10/31/05 | | N/A | | | N/A | | | N/A | | | N/A | | | N/A | |

|

|

Inception* through 10/31/05 | | (1.99 | ) | | (0.92 | ) | | 4.76 | | | 3.92 | | | 5.83 | |

|

|

SB Growth and Income Fund 2005 Annual Report 11

Fund Performance (continued)

| | | | | | | | | | | |

| Cumulative Total Returns† (unaudited) |

| |

| | | Without Sales Charges(1) |

Smith Barney Class 1 (10/31/95 through 10/31/05) | | | | | | 92.07 | % | | | | |

|

Smith Barney Class A (Inception* through 10/31/05) | | | | | | 67.99 | | | | | |

|

Smith Barney Class B (Inception* through 10/31/05) | | | | | | 55.16 | | | | | |

|

Smith Barney Class C (Inception* through 10/31/05) | | | | | | (12.42 | ) | | | | |

|

Smith Barney Class O (Inception* through 10/31/05) | | | | | | (8.58 | ) | | | | |

|

Smith Barney Class P (Inception* through 10/31/05) | | | | | | (8.46 | ) | | | | |

|

Smith Barney Class Y (Inception* through 10/31/05) | | | | | | (4.43 | ) | | | | |

|

Salomon Brothers Class A (Inception* through 10/31/05) | | | | | | 16.87 | | | | | |

|

Salomon Brothers Class B (Inception* through 10/31/05) | | | | | | 11.94 | | | | | |

|

Salomon Brothers Class C (Inception* through 10/31/05) | | | | | | 11.94 | | | | | |

|

| (1) | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value and does not reflect deduction of the applicable sales charges with respect to Smith Barney Class 1, Smith Barney Class A, and Salomon Brothers Class A shares or the applicable contingent deferred sales charges (“CDSC”) with respect to Smith Barney Class B, Smith Barney Class C, Smith Barney Class O, Smith Barney Class P shares, Salomon Brothers Class B and Salomon Brothers Class C shares. |

| (2) | | Assumes reinvestment of all distributions, including returns of capital, if any, at net asset value. In addition, Smith Barney Class 1, Smith Barney Class A and Salomon Brothers Class A shares reflect the deduction of the maximum initial sales charges of 8.50%, 5.00% and 5.75%, respectively. Smith Barney Class B, Smith Barney Class P shares and Salomon Brothers Class B reflect the deduction of a 5.00% CDSC, which applies if shares are redeemed within one year from purchase payment and declines by 1.00% per year until no CDSC is incurred. Smith Barney Class C, Smith Barney Class O shares and Salomon Brothers Class C also reflect the deduction of a 1.00% CDSC, which applies if shares are redeemed within one year from purchase payment. |

| † | | All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| * | | Inception date for Smith Barney Class 1 shares is April 14, 1987. Inception date for Smith Barney Class A and Smith Barney Class B shares is August 18, 1996. Inception date for Smith Barney Class C shares is October 9, 2000. Inception date for Smith Barney Class O, Smith Barney Class P and Smith Barney Class Y shares is December 8, 2000. Inception date for Salomon Brothers Class A shares is October 3, 2003. Inception date for Salomon Brothers Class B and Salomon Brothers Class C shares is November 5, 2003. |

12 SB Growth and Income Fund 2005 Annual Report

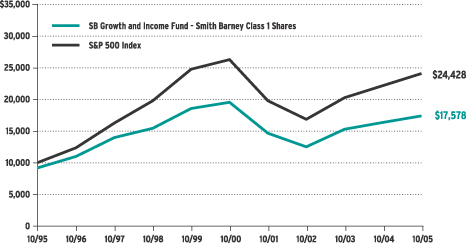

Historical Performance (unaudited)

Value of $10,000 Invested in Smith Barney Class 1 Shares of the SB Growth and Income Fund vs. S&P 500 Index† (October 1995 — October 2005)

| † | | Hypothetical illustration of $10,000 invested in Smith Barney Class 1 shares on October 31, 1995, assuming deduction of the 8.50% maximum sales charge at the time of investment and the reinvestment of distributions, including returns of capital, if any, at net asset value through October 31, 2005. The S&P 500 Index is an index of widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and over-the-counter markets. Figures for the Index include reinvestment of dividends. The Index is unmanaged and is not subject to the same management and trading expenses of a mutual fund. Please note that an investor cannot invest directly in an index. The performance of the Fund’s other classes may be greater or less than the performance of Smith Barney Class 1 shares’ performance indicated on this chart, depending on whether greater or lesser sales charges and fees were incurred by shareholder investing in other classes. |

All figures represent past performance and are not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance figures may reflect voluntary fee waivers and/or expense reimbursements. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower.

SB Growth and Income Fund 2005 Annual Report 13

Schedule of Investments (October 31, 2005)

SB GROWTH AND INCOME FUND

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | | |

| COMMON STOCKS — 98.9% | | | | |

| CONSUMER DISCRETIONARY — 11.3% | | | | |

| Hotels, Restaurants & Leisure — 2.3% | | | | |

| 33,200 | | Ctrip.com International Ltd., ADR (a) | | $ | 1,909,996 | |

| 344,000 | | McDonald’s Corp. | | | 10,870,400 | |

| 151,100 | | Station Casinos Inc. | | | 9,685,510 | |

|

|

| | | Total Hotels, Restaurants & Leisure | | | 22,465,906 | |

|

|

| Household Durables — 1.0% | | | | |

| 415,400 | | Newell Rubbermaid Inc. (a) | | | 9,550,046 | |

|

|

| Media — 4.9% | | | | |

| 175,900 | | Comcast Corp., Class A Shares* | | | 4,895,297 | |

| 320,400 | | EchoStar Communications Corp., Class A Shares* | | | 8,609,148 | |

| 777,902 | | Liberty Media Corp., Class A Shares* | | | 6,199,879 | |

| 906,900 | | News Corp., Class B Shares | | | 13,657,914 | |

| 753,700 | | Time Warner Inc. | | | 13,438,471 | |

|

|

| | | Total Media | | | 46,800,709 | |

|

|

| Specialty Retail — 3.1% | | | | |

| 446,600 | | Best Buy Co. Inc. | | | 19,766,516 | |

| 421,800 | | Staples Inc. | | | 9,587,514 | |

|

|

| | | Total Specialty Retail | | | 29,354,030 | |

|

|

| | | TOTAL CONSUMER DISCRETIONARY | | | 108,170,691 | |

|

|

| CONSUMER STAPLES — 10.0% | | | | |

| Beverages — 2.2% | | | | |

| 352,900 | | PepsiCo Inc. | | | 20,849,332 | |

|

|

| Food & Staples Retailing — 1.8% | | | | |

| 371,600 | | Wal-Mart Stores Inc. | | | 17,580,396 | |

|

|

| Food Products — 3.4% | | | | |

| 340,200 | | Kellogg Co. | | | 15,026,634 | |

| 229,400 | | McCormick & Co. Inc., Non Voting Shares (a) | | | 6,948,526 | |

| 581,200 | | Sara Lee Corp. | | | 10,374,420 | |

|

|

| | | Total Food Products | | | 32,349,580 | |

|

|

| Household Products — 2.6% | | | | |

| 178,300 | | Kimberly-Clark Corp. | | | 10,134,572 | |

| 262,700 | | Procter & Gamble Co. | | | 14,708,573 | |

|

|

| | | Total Household Products | | | 24,843,145 | |

|

|

| | | TOTAL CONSUMER STAPLES | | | 95,622,453 | |

|

|

| ENERGY — 9.2% | | | | |

| Energy Equipment & Services — 1.7% | | | | |

| 166,400 | | ENSCO International Inc. | | | 7,586,176 | |

| 201,700 | | GlobalSantaFe Corp. | | | 8,985,735 | |

|

|

| | | Total Energy Equipment & Services | | | 16,571,911 | |

|

|

See Notes to Financial Statements.

14 SB Growth and Income Fund 2005 Annual Report

Schedule of Investments (October 31, 2005) (continued)

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | | |

| Oil, Gas & Consumable Fuels — 7.5% | | | | |

| 133,400 | | Burlington Resources Inc. | | $ | 9,634,148 | |

| 416,900 | | Exxon Mobil Corp. | | | 23,404,766 | |

| 261,000 | | Nexen Inc. | | | 10,789,740 | |

| 122,800 | | Suncor Energy Inc. | | | 6,585,764 | |

| 168,400 | | Total SA, Sponsored ADR (a) | | | 21,221,768 | |

|

|

| | | Total Oil, Gas & Consumable Fuels | | | 71,636,186 | |

|

|

| | | TOTAL ENERGY | | | 88,208,097 | |

|

|

| FINANCIALS — 20.8% | | | | |

| Capital Markets — 3.6% | | | | |

| 135,000 | | Goldman Sachs Group Inc. | | | 17,059,950 | |

| 260,400 | | Merrill Lynch & Co. Inc. | | | 16,858,296 | |

|

|

| | | Total Capital Markets | | | 33,918,246 | |

|

|

| Commercial Banks — 6.6% | | | | |

| 450,754 | | Bank of America Corp. | | | 19,715,980 | |

| 160,000 | | Comerica Inc. | | | 9,244,800 | |

| 202,500 | | Wachovia Corp. | | | 10,230,300 | |

| 398,700 | | Wells Fargo & Co. | | | 24,001,740 | |

|

|

| | | Total Commercial Banks | | | 63,192,820 | |

|

|

| Consumer Finance — 2.9% | | | | |

| 279,500 | | American Express Co. | | | 13,910,715 | |

| 180,700 | | Capital One Financial Corp. (a) | | | 13,796,445 | |

|

|

| | | Total Consumer Finance | | | 27,707,160 | |

|

|

| Diversified Financial Services — 2.2% | | | | |

| 574,880 | | JPMorgan Chase & Co. | | | 21,052,106 | |

|

|

| Insurance — 4.4% | | | | |

| 158,900 | | AFLAC Inc. | | | 7,592,242 | |

| 227,000 | | American International Group Inc. | | | 14,709,600 | |

| 121 | | Berkshire Hathaway Inc., Class A Shares (a)* | | | 10,393,900 | |

| 105,400 | | Chubb Corp. | | | 9,799,038 | |

|

|

| | | Total Insurance | | | 42,494,780 | |

|

|

| Thrifts & Mortgage Finance — 1.1% | | | | |

| 173,900 | | Golden West Financial Corp. | | | 10,213,147 | |

|

|

| | | TOTAL FINANCIALS | | | 198,578,259 | |

|

|

| HEALTH CARE — 10.9% | | | | |

| Biotechnology — 1.6% | | | | |

| 196,004 | | Amgen Inc.* | | | 14,849,263 | |

|

|

| Health Care Providers & Services — 4.4% | | | | |

| 193,950 | | Coventry Health Care Inc.* | | | 10,471,360 | |

| 295,200 | | UnitedHealth Group Inc. | | | 17,089,128 | |

| 191,600 | | WellPoint Inc.* | | | 14,308,688 | |

|

|

| | | Total Health Care Providers & Services | | | 41,869,176 | |

|

|

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 15

Schedule of Investments (October 31, 2005) (continued)

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | | |

| Pharmaceuticals — 4.9% | | | | |

| 267,700 | | Pfizer Inc. | | $ | 5,819,798 | |

| 385,600 | | Sanofi-Aventis, ADR | | | 15,470,272 | |

| 162,500 | | Sepracor Inc. (a)* | | | 9,140,625 | |

| 443,000 | | Teva Pharmaceutical Industries Ltd., Sponsored ADR (a) | | | 16,887,160 | |

|

|

| | | Total Pharmaceuticals | | | 47,317,855 | |

|

|

| | | TOTAL HEALTH CARE | | | 104,036,294 | |

|

|

| INDUSTRIALS — 10.4% | | | | |

| Aerospace & Defense — 4.3% | | | | |

| 433,200 | | Boeing Co. | | | 28,002,048 | |

| 369,500 | | Raytheon Co. | | | 13,653,025 | |

|

|

| | | Total Aerospace & Defense | | | 41,655,073 | |

|

|

| Building Products — 1.1% | | | | |

| 269,200 | | American Standard Cos. Inc. | | | 10,240,368 | |

|

|

| Industrial Conglomerates — 5.0% | | | | |

| 1,148,400 | | General Electric Co. | | | 38,942,244 | |

| 121,000 | | Textron Inc. | | | 8,716,840 | |

|

|

| | | Total Industrial Conglomerates | | | 47,659,084 | |

|

|

| | | TOTAL INDUSTRIALS | | | 99,554,525 | |

|

|

| INFORMATION TECHNOLOGY — 16.4% | | | | |

| Communications Equipment — 0.9% | | | | |

| 467,434 | | ADC Telecommunications Inc. (a)* | | | 8,156,723 | |

|

|

| Computers & Peripherals — 2.3% | | | | |

| 392,000 | | Dell Inc.* | | | 12,496,960 | |

| 117,200 | | International Business Machines Corp. | | | 9,596,336 | |

|

|

| | | Total Computers & Peripherals | | | 22,093,296 | |

|

|

| Electronic Equipment & Instruments — 0.2% | | | | |

| 143,400 | | Dolby Laboratories Inc., Class A Shares* | | | 2,308,740 | |

|

|

| Internet Software & Services — 1.4% | | | | |

| 26,600 | | Netease.com Inc. ADR (a)* | | | 2,028,782 | |

| 85,600 | | SINA Corp. (a)* | | | 2,169,960 | |

| 253,300 | | Yahoo! Inc.* | | | 9,364,501 | |

|

|

| | | Total Internet Software & Services | | | 13,563,243 | |

|

|

| IT Services — 1.2% | | | | |

| 293,900 | | Paychex Inc. | | | 11,391,564 | |

|

|

| Semiconductors & Semiconductor Equipment — 3.7% | | | | |

| 561,100 | | Applied Materials Inc. | | | 9,190,818 | |

| 415,600 | | ASML Holding NV, NY Registered Shares (a)* | | | 7,056,888 | |

| 367,300 | | Intel Corp. | | | 8,631,550 | |

| 297,800 | | Maxim Integrated Products Inc. | | | 10,327,704 | |

|

|

| | | Total Semiconductors & Semiconductor Equipment | | | 35,206,960 | |

|

|

See Notes to Financial Statements.

16 SB Growth and Income Fund 2005 Annual Report

Schedule of Investments (October 31, 2005) (continued)

| | | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | | | |

| | Software — 6.7% | | | | |

| | 286,600 | | Adobe Systems Inc. | | $ | 9,242,850 | |

| | 254,700 | | Cognos Inc. (a)* | | | 9,558,891 | |

| | 173,800 | | Electronic Arts Inc.* | | | 9,885,744 | |

| | 1,386,100 | | Microsoft Corp. | | | 35,622,770 | |

|

|

|

| | | | Total Software | | | 64,310,255 | |

|

|

|

| | | | TOTAL INFORMATION TECHNOLOGY | | | 157,030,781 | |

|

|

|

| | MATERIALS — 5.4% | | | | |

| | Chemicals — 2.3% | | | | |

| | 285,200 | | E.I. du Pont de Nemours & Co. | | | 11,889,988 | |

| | 290,900 | | Ecolab Inc. | | | 9,622,972 | |

|

|

|

| | | | Total Chemicals | | | 21,512,960 | |

|

|

|

| | Metals & Mining — 3.1% | | | | |

| | 910,200 | | Barrick Gold Corp. | | | 22,982,550 | |

| | 334,700 | | Placer Dome Inc. | | | 6,677,265 | |

|

|

|

| | | | Total Metals & Mining | | | 29,659,815 | |

|

|

|

| | | | TOTAL MATERIALS | | | 51,172,775 | |

|

|

|

| | TELECOMMUNICATION SERVICES — 3.3% | | | | |

| | Wireless Telecommunication Services — 3.3% | | | | |

| | 139,100 | | ALLTEL Corp. | | | 8,604,726 | |

| | 988,915 | | Sprint Nextel Corp. | | | 23,051,609 | |

|

|

|

| | | | TOTAL TELECOMMUNICATION SERVICES | | | 31,656,335 | |

|

|

|

| | UTILITIES — 1.2% | | | | |

| | Multi-Utilities — 1.2% | | | | |

| | 266,300 | | Sempra Energy | | | 11,797,090 | |

|

|

|

| | | | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENTS

(Cost — $785,452,348) | | | 945,827,300 | |

|

|

|

| | |

Face

Amount | | | | | |

| | SHORT-TERM INVESTMENTS — 8.6% | |

| | Repurchase Agreement — 1.5% | |

| $ | 13,854,000 | | State Street Bank & Trust Co., dated 10/31/05, 3.520% due 11/1/05; Proceeds at maturity — $13,855,355; (Fully collateralized by U.S. Treasury Bond, 7.250% due 8/15/22; Market value — $14,137,230) (Cost — $13,854,000) | | | 13,854,000 | |

|

|

|

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 17

Schedule of Investments (October 31, 2005) (continued)

| | | | | | |

| | |

| Shares | | Security | | Value | |

| | | | | | | |

| Securities Purchased from Securities Lending Collateral — 7.1% | |

| 68,197,928 | | State Street Navigator Securities Lending Trust Prime Portfolio (Cost — $68,197,928) | | $ | 68,197,928 | |

|

|

| | | TOTAL SHORT-TERM INVESTMENTS

(Cost — $82,051,928) | | | 82,051,928 | |

|

|

| | | TOTAL INVESTMENTS — 107.5% (Cost — $867,504,276#) | | | 1,027,879,228 | |

| | | Liabilities in Excess of Other Assets — (7.5)% | | | (71,846,650 | ) |

|

|

| | | TOTAL NET ASSETS — 100.0% | | $ | 956,032,578 | |

|

|

| * | | Non-income producing security. |

| (a) | | All or a portion of this security is on loan (See Notes 1 and 3). |

| # | | Aggregate cost for federal income tax purposes is $871,954,107. |

| | |

Abbreviation used in this schedule:

|

| ADR | | — American Depositary Receipt |

See Notes to Financial Statements.

18 SB Growth and Income Fund 2005 Annual Report

Statement of Assets and Liabilities (October 31, 2005)

| | | | |

| ASSETS: | | | | |

Investments, at value (Cost — $867,504,276) | | $ | 1,027,879,228 | |

Cash | | | 88 | |

Receivable for securities sold | | | 8,887,788 | |

Receivable for Fund shares sold | | | 344,979 | |

Dividends and interest receivable | | | 183,501 | |

Prepaid expenses | | | 2,919 | |

|

|

Total Assets | | | 1,037,298,503 | |

|

|

| LIABILITIES: | | | | |

Payable for loaned securities collateral (Notes 1 and 3) | | | 68,197,928 | |

Payable for securities purchased | | | 9,471,636 | |

Payable for Fund shares repurchased | | | 1,537,117 | |

Transfer agent fees payable | | | 1,037,152 | |

Management fee payable | | | 509,154 | |

Trustees’ retirement plan payable | | | 325,135 | |

Trustees’ fees payable | | | 25,999 | |

Service plan fees payable | | | 23,369 | |

Accrued expenses | | | 138,435 | |

|

|

Total Liabilities | | | 81,265,925 | |

|

|

Total Net Assets | | $ | 956,032,578 | |

|

|

| NET ASSETS: | | | | |

Par value (Note 6) | | $ | 633 | |

Paid-in capital in excess of par value | | | 916,053,209 | |

Accumulated net realized loss on investments and foreign currency transactions | | | (120,396,216 | ) |

Net unrealized appreciation on investments | | | 160,374,952 | |

|

|

Total Net Assets | | $ | 956,032,578 | |

|

|

Shares Outstanding: | | | | |

Smith Barney Class 1 | | | 31,473,655 | |

|

|

Smith Barney Class A | | | 17,533,144 | |

|

|

Smith Barney Class B | | | 7,328,720 | |

|

|

Smith Barney Class C | | | 309,666 | |

|

|

Smith Barney Class O | | | 86,397 | |

|

|

Smith Barney Class P | | | 501,011 | |

|

|

Smith Barney Class Y | | | 6,082,692 | |

|

|

Salomon Brothers Class A | | | 7,898 | |

|

|

Salomon Brothers Class B | | | 1,114 | |

|

|

Salomon Brothers Class C | | | 174 | |

|

|

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 19

Statement of Assets and Liabilities (October 31, 2005) (continued)

| | |

Net Asset Value: | | |

Smith Barney Class 1 (and redemption price) | | $15.19 |

|

Smith Barney Class A (and redemption price) | | $15.19 |

|

Smith Barney Class B * | | $14.38 |

|

Smith Barney Class C * | | $14.94 |

|

Smith Barney Class O * | | $15.13 |

|

Smith Barney Class P * | | $15.15 |

|

Smith Barney Class Y (and redemption price) | | $15.22 |

|

Salomon Brothers Class A (and redemption price) | | $15.20 |

|

Salomon Brothers Class B * | | $14.44 |

|

Salomon Brothers Class C * | | $14.91 |

|

Maximum Public Offering Price Per Share: | | |

Smith Barney Class 1 (based on maximum sales charge of 8.50%) | | $16.60 |

|

Smith Barney Class A (based on maximum sales charge of 5.00%) | | $15.99 |

|

Salomon Brothers Class A (based on maximum sales charge of 5.75%) | | $16.13 |

|

| * | | Redemption price is NAV of Smith Barney Class B, Smith Barney Class C, Smith Barney Class O, Smith Barney Class P, Salomon Brothers Class B and Salomon Brothers Class C shares reduced by a 5.00%, 1.00%, 1.00%, 5.00%, 5.00% and 1.00% contingent deferred sales charge (“CDSC”), respectively, if shares are redeemed within one year from purchase payment (See Note 2). |

See Notes to Financial Statements.

20 SB Growth and Income Fund 2005 Annual Report

Statement of Operations (For the year ended October 31, 2005)

| | | | |

| INVESTMENT INCOME: | | | | |

Dividends | | $ | 21,004,920 | |

Interest | | | 345,433 | |

Income from securities lending | | | 97,663 | |

Less: Foreign taxes withheld | | | (213,035 | ) |

|

|

Total Investment Income | | | 21,234,981 | |

|

|

| EXPENSES: | | | | |

Management fee (Note 2) | | | 6,948,212 | |

Transfer agent fees (Notes 2 and 4) | | | 2,883,446 | |

Service plan fees (Notes 2 and 4) | | | 1,970,629 | |

Shareholder reports (Note 4) | | | 145,605 | |

Registration fees | | | 121,867 | |

Trustees’ fees | | | 97,633 | |

Custody fees | | | 85,135 | |

Legal fees | | | 80,320 | |

Audit and tax | | | 28,324 | |

Insurance | | | 12,636 | |

Miscellaneous expenses | | | 13,598 | |

|

|

Total Expenses | | | 12,387,405 | |

Less: Expense reimbursement (Note 2) | | | (451,134 | ) |

|

|

Net Expenses | | | 11,936,271 | |

|

|

Net Investment Income | | | 9,298,710 | |

|

|

REALIZED AND UNREALIZED GAIN (LOSS) ON

INVESTMENTS AND FOREIGN CURRENCY

TRANSACTIONS (NOTES 1 AND 3): | | | | |

Net Realized Gain From: | | | | |

Investments | | | 56,933,025 | |

Foreign currency transactions | | | 274 | |

|

|

Net Realized Gain | | | 56,933,299 | |

|

|

Change in Net Unrealized Appreciation/Depreciation | | | (420,262 | ) |

|

|

Net Gain on Investments and Foreign Currency Transactions | | | 56,513,037 | |

|

|

Increase in Net Assets From Operations | | $ | 65,811,747 | |

|

|

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 21

Statements of Changes in Net Assets (For the years ended October 31,)

| | | | | | | | |

| | |

| | | 2005 | | | 2004 | |

| OPERATIONS: | | | | | | | | |

Net investment income | | $ | 9,298,710 | | | $ | 4,597,795 | |

Net realized gain | | | 56,933,299 | | | | 52,522,589 | |

Change in net unrealized appreciation/depreciation | | | (420,262 | ) | | | 20,430,552 | |

|

|

Increase in Net Assets From Operations | | | 65,811,747 | | | | 77,550,936 | |

|

|

DISTRIBUTIONS TO SHAREHOLDERS

FROM (NOTE 5): | | | | | | | | |

Net investment income | | | (10,230,695 | ) | | | (4,438,675 | ) |

|

|

Decrease in Net Assets From

Distributions to Shareholders | | | (10,230,695 | ) | | | (4,438,675 | ) |

|

|

| FUND SHARE TRANSACTIONS (NOTE 6): | | | | | | | | |

Net proceeds from sale of shares | | | 49,974,009 | | | | 126,454,342 | |

Reinvestment of distributions | | | 7,821,331 | | | | 2,994,814 | |

Cost of shares repurchased | | | (280,789,738 | ) | | | (214,582,297 | ) |

|

|

Decrease in Net Assets From Fund Share Transactions | | | (222,994,398 | ) | | | (85,133,141 | ) |

|

|

Decrease in Net Assets | | | (167,413,346 | ) | | | (12,020,880 | ) |

| NET ASSETS: | | | | | | | | |

Beginning of year | | | 1,123,445,924 | | | | 1,135,466,804 | |

|

|

End of year* | | $ | 956,032,578 | | | $ | 1,123,445,924 | |

|

|

* Includes undistributed net investment income of: | | | — | | | | $536,107 | |

|

|

See Notes to Financial Statements.

22 SB Growth and Income Fund 2005 Annual Report

Financial Highlights

For a share of each class of beneficial interest outstanding throughout each year ended October 31:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class 1 Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001 | |

Net Asset Value, Beginning of Year | | $ | 14.42 | | | $ | 13.53 | | | $ | 11.05 | | | $ | 13.08 | | | $ | 19.03 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.15 | | | | 0.08 | | | | 0.07 | | | | 0.05 | | | | 0.10 | |

Net realized and unrealized gain (loss) | | | 0.78 | | | | 0.88 | | | | 2.46 | | | | (2.02 | ) | | | (4.62 | ) |

|

|

Total Income (Loss) From Operations | | | 0.93 | | | | 0.96 | | | | 2.53 | | | | (1.97 | ) | | | (4.52 | ) |

|

|

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.16 | ) | | | (0.07 | ) | | | (0.05 | ) | | | (0.05 | ) | | | (0.06 | ) |

Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (1.37 | ) |

Return of capital | | | — | | | | — | | | | — | | | | (0.01 | ) | | | — | |

|

|

Total Distributions | | | (0.16 | ) | | | (0.07 | ) | | | (0.05 | ) | | | (0.06 | ) | | | (1.43 | ) |

|

|

Net Asset Value, End of Year | | $ | 15.19 | | | $ | 14.42 | | | $ | 13.53 | | | $ | 11.05 | | | $ | 13.08 | |

|

|

Total Return(3) | | | 6.48 | % | | | 7.08 | % | | | 22.91 | % | | | (15.13 | )% | | | (25.18 | )% |

|

|

Net Assets, End of Year (millions) | | | $478 | | | | $518 | | | | $536 | | | | $494 | | | | $678 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 0.95 | % | | | 0.97 | % | | | 1.00 | % | | | 0.99 | % | | | 0.73 | % |

Net expenses | | | 0.95 | (4)(5) | | | 0.96 | (4) | | | 1.00 | | | | 0.99 | | | | 0.73 | |

Net investment income | | | 1.01 | | | | 0.59 | | | | 0.56 | | | | 0.38 | | | | 0.62 | |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class 1 shares were renamed as Smith Barney Class 1 shares. |

| (3) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (4) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (5) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.00%. |

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 23

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class A Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001 | |

Net Asset Value, Beginning of Year | | $ | 14.42 | | | $ | 13.52 | | | $ | 11.06 | | | $ | 13.07 | | | $ | 19.03 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.11 | | | | 0.04 | | | | 0.02 | | | | 0.02 | | | | 0.03 | |

Net realized and unrealized gain (loss) | | | 0.78 | | | | 0.88 | | | | 2.45 | | | | (2.02 | ) | | | (4.61 | ) |

|

|

Total Income (Loss) From Operations | | | 0.89 | | | | 0.92 | | | | 2.47 | | | | (2.00 | ) | | | (4.58 | ) |

|

|

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.12 | ) | | | (0.02 | ) | | | (0.01 | ) | | | (0.00 | )(3) | | | (0.01 | ) |

Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (1.37 | ) |

Return of capital | | | — | | | | — | | | | — | | | | (0.01 | ) | | | — | |

|

|

Total Distributions | | | (0.12 | ) | | | (0.02 | ) | | | (0.01 | ) | | | (0.01 | ) | | | (1.38 | ) |

|

|

Net Asset Value, End of Year | | $ | 15.19 | | | $ | 14.42 | | | $ | 13.52 | | | $ | 11.06 | | | $ | 13.07 | |

|

|

Total Return(4) | | | 6.16 | % | | | 6.82 | % | | | 22.36 | % | | | (15.29 | )% | | | (25.51 | )% |

|

|

Net Assets, End of Year (millions) | | | $266 | | | | $283 | | | | $278 | | | | $233 | | | | $295 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 1.29 | % | | | 1.28 | % | | | 1.35 | % | | | 1.25 | % | | | 1.17 | % |

Net expenses | | | 1.25 | (5)(6) | | | 1.27 | (5) | | | 1.35 | | | | 1.25 | | | | 1.17 | |

Net investment income | | | 0.70 | | | | 0.28 | | | | 0.21 | | | | 0.12 | | | | 0.19 | |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class A shares were renamed as Smith Barney Class A shares. |

| (3) | | Amount represents less than $0.01 per share. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (5) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (6) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.25%. |

See Notes to Financial Statements.

24 SB Growth and Income Fund 2005 Annual Report

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class B Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001 | |

Net Asset Value, Beginning of Year | | $ | 13.64 | | | $ | 12.91 | | | $ | 10.66 | | | $ | 12.73 | | | $ | 18.70 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | (0.00 | )(3) | | | (0.11 | ) | | | (0.10 | ) | | | (0.11 | ) | | | (0.10 | ) |

Net realized and unrealized gain (loss) | | | 0.74 | | | | 0.84 | | | | 2.35 | | | | (1.96 | ) | | | (4.50 | ) |

|

|

Total Income (Loss) From Operations | | | 0.74 | | | | 0.73 | | | | 2.25 | | | | (2.07 | ) | | | (4.60 | ) |

|

|

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (1.37 | ) |

|

|

Total Distributions | | | — | | | | — | | | | — | | | | — | | | | (1.37 | ) |

|

|

Net Asset Value, End of Year | | $ | 14.38 | | | $ | 13.64 | | | $ | 12.91 | | | $ | 10.66 | | | $ | 12.73 | |

|

|

Total Return(4) | | | 5.43 | % | | | 5.65 | % | | | 21.11 | % | | | (16.26 | )% | | | (26.10 | )% |

|

|

Net Assets, End of Year (millions) | | | $105 | | | | $113 | | | | $117 | | | | $111 | | | | $160 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 2.27 | % | | | 2.37 | % | | | 2.42 | % | | | 2.28 | % | | | 2.00 | % |

Net expenses | | | 1.98 | (5)(6) | | | 2.36 | (5) | | | 2.42 | | | | 2.28 | | | | 2.00 | |

Net investment loss | | | (0.03 | ) | | | (0.81 | ) | | | (0.85 | ) | | | (0.91 | ) | | | (0.65 | ) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class B shares were renamed as Smith Barney Class B shares. |

| (3) | | Amount represents less than $0.01 per share. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (5) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (6) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 2.00%. |

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 25

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class C Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001 | |

Net Asset Value, Beginning of Year | | $ | 14.16 | | | $ | 13.33 | | | $ | 10.94 | | | $ | 13.00 | | | $ | 19.04 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.02 | | | | (0.04 | ) | | | (0.03 | ) | | | (0.07 | ) | | | (0.08 | ) |

Net realized and unrealized gain (loss) | | | 0.76 | | | | 0.87 | | | | 2.42 | | | | (1.99 | ) | | | (4.59 | ) |

|

|

Total Income (Loss) From Operations | | | 0.78 | | | | 0.83 | | | | 2.39 | | | | (2.06 | ) | | | (4.67 | ) |

|

|

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | — | | | | (0.00 | )(3) | | | — | | | | — | | | | — | |

Net realized gains | | | — | | | | — | | | | — | | | | — | | | | (1.37 | ) |

|

|

Total Distributions | | | — | | | | (0.00 | ) | | | — | | | | — | | | | (1.37 | ) |

|

|

Net Asset Value, End of Year | | $ | 14.94 | | | $ | 14.16 | | | $ | 13.33 | | | $ | 10.94 | | | $ | 13.00 | |

|

|

Total Return(4) | | | 5.51 | % | | | 6.23 | % | | | 21.85 | % | | | (15.85 | )% | | | (25.99 | )% |

|

|

Net Assets, End of Year (000s) | | | $4,627 | | | | $5,675 | | | | $5,696 | | | | $4,516 | | | | $5,774 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 1.86 | % | | | 1.82 | % | | | 1.80 | % | | | 1.89 | % | | | 1.85 | % |

Net expenses | | | 1.86 | (5)(6) | | | 1.82 | (5) | | | 1.80 | | | | 1.89 | | | | 1.85 | |

Net investment income (loss) | | | 0.13 | | | | (0.27 | ) | | | (0.25 | ) | | | (0.52 | ) | | | (0.49 | ) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class L shares were renamed as Smith Barney Class L shares. On April 29, 2004, Smith Barney Class L shares were renamed as Smith Barney Class C shares. |

| (3) | | Amount represents less than $0.01 per share. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. |

| (5) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (6) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 2.00%. |

See Notes to Financial Statements.

26 SB Growth and Income Fund 2005 Annual Report

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31, unless otherwise noted:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class O Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001(3) | |

Net Asset Value, Beginning of Year | | $ | 14.28 | | | $ | 13.40 | | | $ | 10.97 | | | $ | 13.04 | | | $ | 16.55 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.07 | | | | 0.01 | | | | 0.01 | | | | (0.06 | ) | | | (0.03 | ) |

Net realized and unrealized gain (loss) | | | 0.78 | | | | 0.87 | | | | 2.42 | | | | (2.01 | ) | | | (3.48 | ) |

|

|

Total Income (Loss) From Operations | | | 0.85 | | | | 0.88 | | | | 2.43 | | | | (2.07 | ) | | | (3.51 | ) |

|

|

Net Asset Value, End of Year | | $ | 15.13 | | | $ | 14.28 | | | $ | 13.40 | | | $ | 10.97 | | | $ | 13.04 | |

|

|

Total Return(4) | | | 5.95 | % | | | 6.57 | % | | | 22.15 | % | | | (15.87 | )% | | | (21.21 | )% |

|

|

Net Assets, End of Year (000s) | | | $1,307 | | | | $1,399 | | | | $1,566 | | | | $1,595 | | | | $2,453 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 1.47 | % | | | 1.51 | % | | | 1.52 | % | | | 1.82 | % | | | 1.53 | %(5) |

Net expenses | | | 1.47 | (6)(7) | | | 1.51 | (6) | | | 1.52 | | | | 1.82 | | | | 1.53 | (5) |

Net investment income (loss) | | | 0.49 | | | | 0.04 | | | | 0.05 | | | | (0.45 | ) | | | (0.18 | )(5) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class O shares were renamed as Smith Barney Class O shares. |

| (3) | | For the period December 8, 2000 (inception date) to October 31, 2001. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. Total returns for periods of less than one year are not annualized. |

| (6) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (7) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.70%. |

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 27

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31, unless otherwise noted:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class P Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001(3) | |

Net Asset Value, Beginning of Year | | $ | 14.30 | | | $ | 13.44 | | | $ | 11.00 | | | $ | 13.04 | | | $ | 16.55 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.09 | | | | (0.00 | )(4) | | | 0.01 | | | | (0.03 | ) | | | (0.03 | ) |

Net realized and unrealized gain (loss) | | | 0.76 | | | | 0.86 | | | | 2.43 | | | | (2.01 | ) | | | (3.48 | ) |

|

|

Total Income (Loss) From Operations | | | 0.85 | | | | 0.86 | | | | 2.44 | | | | (2.04 | ) | | | (3.51 | ) |

|

|

Net Asset Value, End of Year | | $ | 15.15 | | | $ | 14.30 | | | $ | 13.44 | | | $ | 11.00 | | | $ | 13.04 | |

|

|

Total Return(5) | | | 5.94 | % | | | 6.40 | % | | | 22.18 | % | | | (15.64 | )% | | | (21.21 | )% |

|

|

Net Assets, End of Year (000s) | | | $7,591 | | | | $13,521 | | | | $22,993 | | | | $26,301 | | | | $47,719 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 1.51 | % | | | 1.59 | % | | | 1.51 | % | | | 1.61 | % | | | 1.53 | %(6) |

Net expenses | | | 1.51 | (7)(8) | | | 1.58 | (7) | | | 1.51 | | | | 1.61 | | | | 1.53 | (6) |

Net investment income (loss) | | | 0.58 | | | | (0.02 | ) | | | 0.06 | | | | (0.23 | ) | | | (0.20 | )(6) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class P shares were renamed as Smith Barney Class P shares. |

| (3) | | For the period December 8, 2000 (inception date) to October 31, 2001. |

| (4) | | Amount represents less than $0.01 per share. |

| (5) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. Total returns for periods of less than one year are not annualized. |

| (7) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (8) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.75%. |

See Notes to Financial Statements.

28 SB Growth and Income Fund 2005 Annual Report

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31, unless otherwise noted:

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Smith Barney

Class Y Shares(1)(2) | | 2005 | | | 2004 | | | 2003 | | | 2002 | | | 2001(3) | |

Net Asset Value, Beginning of Year | | $ | 14.45 | | | $ | 13.55 | | | $ | 11.08 | | | $ | 13.08 | | | $ | 16.55 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.21 | | | | 0.12 | | | | 0.11 | | | | 0.09 | | | | 0.10 | |

Net realized and unrealized gain (loss) | | | 0.76 | | | | 0.89 | | | | 2.44 | | | | (2.01 | ) | | | (3.51 | ) |

|

|

Total Income (Loss) From Operations | | | 0.97 | | | | 1.01 | | | | 2.55 | | | | (1.92 | ) | | | (3.41 | ) |

|

|

Less Distributions From: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.20 | ) | | | (0.11 | ) | | | (0.08 | ) | | | (0.07 | ) | | | (0.06 | ) |

Return of capital | | | — | | | | — | | | | — | | | | (0.01 | ) | | | — | |

|

|

Total Distributions | | | (0.20 | ) | | | (0.11 | ) | | | (0.08 | ) | | | (0.08 | ) | | | (0.06 | ) |

|

|

Net Asset Value, End of Year | | $ | 15.22 | | | $ | 14.45 | | | $ | 13.55 | | | $ | 11.08 | | | $ | 13.08 | |

|

|

Total Return(4) | | | 6.75 | % | | | 7.48 | % | | | 23.16 | % | | | (14.77 | )% | | | (20.65 | )% |

|

|

Net Assets, End of Year (millions) | | | $93 | | | | $189 | | | | $174 | | | | $136 | | | | $161 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Gross expenses | | | 0.69 | % | | | 0.68 | % | | | 0.67 | % | | | 0.67 | % | | | 0.67 | %(5) |

Net expenses | | | 0.69 | (6)(7) | | | 0.67 | (6) | | | 0.67 | | | | 0.67 | | | | 0.67 | (5) |

Net investment income | | | 1.39 | | | | 0.87 | | | | 0.88 | | | | 0.70 | | | | 0.68 | (5) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % | | | 44 | % | | | 69 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | On May 9, 2003, Class Y shares were renamed as Smith Barney Class Y shares. |

| (3) | | For the period December 8, 2000 (inception date) to October 31, 2001. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. Total returns for periods of less than one year are not annualized. |

| (6) | | The investment manager voluntarily waived a portion of its fees and/or reimbursed certain expenses. Fee waivers and/or expense reimbursements are voluntary and may be reduced or terminated at any time. |

| (7) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.00%. |

See Notes to Financial Statements.

SB Growth and Income Fund 2005 Annual Report 29

Financial Highlights (continued)

For a share of each class of beneficial interest outstanding throughout each year ended October 31, unless otherwise noted:

| | | | | | | | | | | | |

| | | |

Salomon Brothers

Class A Shares(1) | | 2005 | | | 2004 | | | 2003(2) | |

Net Asset Value, Beginning of Year | | $ | 14.42 | | | $ | 13.52 | | | $ | 13.12 | |

|

|

Income (Loss) From Operations: | | | | | | | | | | | | |

Net investment income (loss) | | | 0.07 | | | | 0.04 | | | | (0.00 | )(3) |

Net realized and unrealized gain | | | 0.81 | | | | 0.89 | | | | 0.40 | |

|

|

Total Income From Operations | | | 0.88 | | | | 0.93 | | | | 0.40 | |

|

|

Less Distributions From: | | | | | | | | | | | | |

Net investment income | | | (0.10 | ) | | | (0.03 | ) | | | — | |

|

|

Total Distributions | | | (0.10 | ) | | | (0.03 | ) | | | — | |

|

|

Net Asset Value, End of Year | | $ | 15.20 | | | $ | 14.42 | | | $ | 13.52 | |

|

|

Total Return(4) | | | 6.10 | % | | | 6.89 | % | | | 3.05 | % |

|

|

Net Assets, End of Year (000s) | | | $120 | | | | $50 | | | | $24 | |

|

|

Ratios to Average Net Assets: | | | | | | | | | | | | |

Gross expenses | | | 12.18 | % | | | 11.33 | % | | | 1.25 | %(5) |

Net expenses(6) | | | 1.25 | (7) | | | 1.24 | (7) | | | 1.25 | (5) |

Net investment income (loss) | | | 0.45 | | | | 0.26 | | | | (0.21 | )(5) |

|

|

Portfolio Turnover Rate | | | 57 | % | | | 42 | % | | | 63 | % |

|

|

| (1) | | Per share amounts have been calculated using the average shares method. |

| (2) | | For the period October 3, 2003 (inception date) to October 31, 2003. |

| (3) | | Amount represents less than $0.01 per share. |

| (4) | | Performance figures may reflect voluntary fee waivers and/or expense reimbursements. Past performance is no guarantee of future results. In the absence of voluntary fee waivers and/or expense reimbursements, the total return would have been lower. Total returns for periods of less than one year are not annualized. |

| (6) | | As a result of a voluntary expense limitation, the ratio of expenses to average net assets of the class will not exceed 1.25%. |