This report must be preceded or accompanied by a prospectus. To obtain an additional prospectus or summary prospectus, if available, call (800) 728-3337 or your financial representative. We advise you to consider the Fund's objectives, risks, charges and expenses carefully before investing. The summary prospectus and prospectus contain this and other important information about the Fund. Please read the prospectus carefully before you invest.

Although allocation among different asset categories generally limits risk, fund management may favor an asset category that underperforms other assets or markets as a whole. The Fund expects to invest in underlying funds that emphasize alternatives or non-traditional asset categories or investment strategies, and as a result, it is subject to the risk factors of those underlying funds. Some of those risks include stock market risk, credit and interest rate risk, volatility in commodity prices and high-yield debt securities, short sales risk and the political, general economic, liquidity and currency risks of foreign investments, which may be particularly significant for emerging markets. Short sales — which involve selling borrowed securities in anticipation of a price decline, then returning an equal number of the securities at some point in the future — could magnify losses and increase volatility. The Fund may use derivatives, including as part of its Global Tactical Asset Allocation (GTAA) strategy. The Fund also expects to have direct and indirect exposure to derivatives, which may be more volatile and less liquid than traditional securities. The Fund could suffer losses on its derivative positions. See the prospectus for additional risks and specific details regarding the Fund's risk profile.

DWS Investments is part of the Deutsche Asset & Wealth Management division of Deutsche Bank AG.

Fund performance shown is historical, assumes reinvestment of all dividend and capital gain distributions and does not guarantee future results. Investment return and principal value fluctuate with changing market conditions so that, when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please contact your participating insurance company for the Fund's most recent month-end performance. Performance doesn't reflect charges and fees ("contract charges") associated with the separate account that invests in the Fund or any variable life insurance policy or variable annuity contract for which the Fund is an investment option. These charges and fees will reduce returns. While all share classes have the same underlying portfolio, their performance will differ.

The gross expense ratios of the Fund, as stated in the fee table of the prospectus dated May 1, 2012 are 1.91% and 2.16% for Class A and Class B shares, respectively, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. These expense ratios include net expenses of the underlying funds in which the Fund invests.

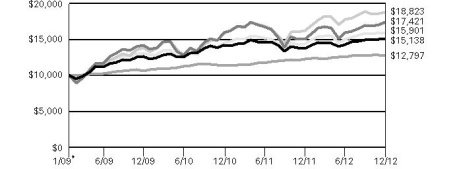

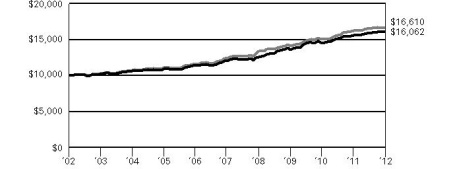

The growth of $10,000 is cumulative.

The growth of $10,000 is cumulative.

The Fund's opportunistic holdings finished the year in positive territory, including DWS Floating Rate Fund, the SPDR Barclays Capital Convertible Securities and the iShares U.S. Preferred Stock Index Fund.

We remain diligent in our search for additional asset classes that we can incorporate into the Fund, and we rebalance the portfolio frequently to maximize diversification and capitalize on moves in the financial markets. During the past year, for instance, we added two new exchange-traded funds — Market Vectors Agribusiness Fund and iShares S&P Global Timber & Forestry Index Fund — in order to augment the Fund's diversification.

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team's views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

Portfolio holdings and characteristics are subject to change.

Following the Fund's fiscal first and third quarter-end, a complete portfolio holdings listing is filed with the SEC on Form N-Q. The form will be available on the SEC's Web site at www.sec.gov, and it also may be reviewed and copied at the SEC's Public Reference Room in Washington, D.C. Information on the operation of the SEC's Public Reference Room may be obtained by calling (800) SEC-0330. The Fund's portfolio holdings are also posted on www.dws-investments.com from time to time. Please see the Fund's current prospectus for more information.

* Non-income producing security.

(a) Affiliated fund managed by Deutsche Investment Management Americas Inc.

(b) The rate shown is the annualized seven-day yield at period end.

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in three broad levels. Level 1 includes quoted prices in active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, and credit risk). Level 3 includes significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments). The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of December 31, 2012 in valuing the Fund's investments. For information on the Fund's policy regarding the valuation of investments, please refer to the Security Valuation section of Note A in the accompanying Notes to Financial Statements.

There have been no transfers between fair value measurement levels during the year ended December 31, 2012.

The accompanying notes are an integral part of the financial statements.

The accompanying notes are an integral part of the financial statements.

The accompanying notes are an integral part of the financial statements.

The accompanying notes are an integral part of the financial statements.

A. Organization and Significant Accounting Policies

DWS Alternative Asset Allocation VIP (formerly DWS Alternative Asset Allocation Plus VIP) (the "Fund") is a diversified series of DWS Variable Series II (the "Trust"), which is registered under the Investment Company Act of 1940, as amended (the "1940 Act"), as an open-end management investment company organized as a Massachusetts business trust. The Fund mainly invests in other affiliated DWS funds (the "Underlying DWS Funds") and exchange-traded funds ("ETFs"). In addition, the Fund may invest in derivatives, including as part of its Global Tactical Asset Allocation (GTAA) strategy. ETFs and Underlying DWS Funds are collectively referred to as "Underlying Funds." Each Underlying DWS Fund's accounting policies and investment holdings are outlined in the Underlying DWS Funds' financial statements and are available upon request.

Investment income, realized and unrealized gains and losses, and certain fund-level expenses and expense reductions, if any, are borne pro rata on the basis of relative net assets by the holders of all classes of shares except that each class bears certain expenses unique to that class (including the applicable Rule 12b-1 fee). Differences in class-level expenses may result in payment of different per share dividends by class. All shares have equal rights with respect to voting subject to class-specific arrangements.

The Fund's financial statements are prepared in accordance with accounting principles generally accepted in the United States of America which require the use of management estimates. Actual results could differ from those estimates. The policies described below are followed consistently by the Fund in the preparation of its financial statements.

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in three broad levels. Level 1 includes quoted prices in active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, and credit risk). Level 3 includes significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments). The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Investments in the Underlying DWS Funds are valued at the net asset value per share of each class of the Underlying DWS Funds and are categorized as Level 1.

ETFs are valued at the most recent sale price or official closing price reported on the exchange (U.S. or foreign) or over-the-counter market on which they trade and are categorized as Level 1 securities. ETFs for which no sales are reported are valued at the calculated mean between the most recent bid and asked quotations on the relevant market or, if a mean cannot be determined, at the most recent bid quotation.

Disclosure about the classification of fair value measurements is included in a table following the Fund's Investment Portfolio.

Under the Regulated Investment Company Modernization Act of 2010, net capital losses incurred post-enactment may be carried forward indefinitely, and their character is retained as short-term and/or long-term. Previously, net capital losses were carried forward for eight years and treated as short-term losses.

At December 31, 2012, the Fund had a net tax basis capital loss carryforward of approximately $446,000 of post-enactment losses, which may be applied against realize net taxable capital gains indefinitely, including short-term losses ($68,000) and long-term losses ($378,000).

The Fund has reviewed the tax positions for the open tax years as of December 31, 2012 and has determined that no provision for income tax is required in the Fund's financial statements. The Fund's federal tax returns for the prior three fiscal years remain open subject to examination by the Internal Revenue Service.

The timing and characterization of certain income and capital gain distributions are determined annually in accordance with federal tax regulations which may differ from accounting principles generally accepted in the United States of America. These differences primarily relate to certain securities sold at a loss. As a result, net investment income (loss) and net realized gain (loss) on investment transactions for a reporting period may differ significantly from distributions during such period. Accordingly, the Fund may periodically make reclassifications among certain of its capital accounts without impacting the net asset value of the Fund.

At December 31, 2012, the Fund's components of distributable earnings on a tax basis were as follows:

In addition, the tax character of distributions paid by the Fund is summarized as follows:

* For tax purposes, short-term capital gain distributions are considered ordinary income distributions.

B. Purchases and Sales of Securities

During the year ended December 31, 2012, purchases and sales of affiliated Underlying Funds (excluding money market funds) aggregated $23,905,926 and $10,418,261, respectively. Purchases and sales of non-affiliated Underlying Funds (excluding money market funds) aggregated $9,534,803 and $2,318,259, respectively.

C. Related Parties

QS Investors, LLC ("QS Investors") acts as an investment subadvisor to the Fund. As an investment subadvisor to the Fund, QS Investors renders strategic asset allocation services and manages the portion of assets allocated from time to time to the Fund's global tactical asset allocation overlay strategy. QS Investors is paid by the Advisor for the services QS Investors provides to the Fund.

RREEF America L.L.C. ("RREEF") acts as an investment subadvisor to the Fund. As an investment subadvisor to the Fund, RREEF provides investment management services to the portions of the Fund's portfolio allocated to direct investments in global real estate and global infrastructure securities. RREEF is paid by the Advisor for the services RREEF provides to the Fund. As of the date of this report, the Fund obtained its exposure to global real estate and global infrastructure securities indirectly through investments in other Underlying DWS Funds.

The Fund does not invest in the Underlying DWS Funds for the purpose of exercising management or control; however, investments within the set limits may represent 5% or more of an Underlying DWS Fund's outstanding shares. At December 31, 2012, the Fund did not invest in more than 5% of any Underlying DWS Fund.

Pursuant to the Investment Management Agreement with the Advisor, the Fund pays a monthly management fee based on the Fund's average daily net assets, computed and accrued daily and payable monthly, at the following annual rates:

In addition, the Advisor will receive management fees from managing the Underlying DWS Funds in which the Fund invests.

For the period from January 1, 2012 through September 30, 2012, the Advisor had contractually agreed to waive its fee and/or reimburse certain operating expenses to the extent necessary to maintain the operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest expense and indirect expenses of Underlying Funds) of each class as follows:

For the period from October 1, 2012 through September 30, 2013, the Advisor has contractually agreed to waive its fee and/or reimburse certain operating expenses to the extent necessary to maintain the operating expenses (excluding certain expenses such as extraordinary expenses, taxes, brokerage, interest expense and indirect expenses of Underlying Funds) of each class as follows:

For the year ended December 31, 2012, the Advisor agreed to waive 0.15% of the monthly management fee based on average daily net assets for the Fund.

Accordingly, for the year ended December 31, 2012, the Advisor waived a portion of its management fee pursuant to the Investment Management Agreement aggregating $194,106, and the amount charged aggregated $9,846, which was equivalent to an annual effective rate of 0.02% of the Fund's average daily net assets.

The Fund indirectly bears its proportionate share of fees and expenses incurred by the Underlying Funds in which it is invested.

In addition, for the year ended December 31, 2012, the Advisor reimbursed $2,876 of non-affiliated recordkeeping fees.

D. Ownership of the Fund

At December 31, 2012, one Participating Insurance Company was the owner of record of 10% or more of the total outstanding Class A shares of the Fund, owning 99%. Two Participating Insurance Companies were the owner of record of 10% or more of the total outstanding Class B shares of the Fund, owning 82% and 13%, respectively.

E. Transactions with Affiliates

The Fund mainly invests in Underlying DWS Funds and ETFs. The Underlying DWS Funds in which the Fund invests are considered to be affiliated investments. A summary of the Fund's transactions with affiliated Underlying DWS Funds during the year ended December 31, 2012 is as follows:

To the Board of Trustees of DWS Variable Series II and Shareholders of DWS Alternative Asset Allocation VIP:

We have audited the accompanying statement of assets and liabilities, including the investment portfolio, of DWS Alternative Asset Allocation VIP (formerly DWS Alternative Asset Allocation Plus VIP) (the "Fund"), one of the funds constituting DWS Variable Series II, as of December 31, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of DWS Alternative Asset Allocation VIP (one of the funds constituting DWS Variable Series II) at December 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein, in conformity with U.S. generally accepted accounting principles.

As an investor of the Fund, you incur two types of costs: ongoing expenses and transaction costs. Ongoing expenses include management fees, distribution and service (12b-1) fees and other Fund expenses. Examples of transaction costs include contract charges and account maintenance fees, which are not shown in this section. The following tables are intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to help you compare these expenses with the ongoing expenses of investing in other mutual funds. In addition to the ongoing expenses which the Fund bears directly, the Fund's shareholders indirectly bear the expense of the Underlying Funds in which the Fund invests. These expenses are not included in the Fund's annualized expense ratios used to calculate the expense estimate in the tables. In the most recent six-month period, the Fund limited the ongoing expenses the Fund bears directly; had it not done so, expenses would have been higher. The examples in the table are based on an investment of $1,000 invested at the beginning of the six-month period and held for the entire period (July 1, 2012 to December 31, 2012).

Please note that the expenses shown in these tables are meant to highlight your ongoing expenses only and do not reflect any transaction costs. The "Expenses Paid per $1,000" line of the tables is useful in comparing ongoing expenses only and will not help you determine the relative total expense of owning different funds. If these transaction costs had been included, your costs would have been higher.

* Expenses are equal to the Fund's annualized expense ratio for each share class, multiplied by the average account value over the period, multiplied by 184 (the number of days in the most recent six-month period), then divided by 366.

** The Fund invests in other funds and indirectly bears its proportionate share of fees and expenses incurred by the Underlying Funds in which the Fund is invested. These ratios do not include these indirect fees and expenses.

For more information, please refer to the Fund's prospectus.

These tables do not reflect charges and fees ("contract charges") associated with the separate account that invests in the Fund or any variable life insurance policy or variable annuity contract for which the Fund is an investment option.

The Fund paid distributions of $0.11 per share from net long-term capital gains during its year ended December 31, 2012, of which 100% represents 15% rate gains.

For corporate shareholders, 3% of income dividends paid during the Fund's fiscal year ended December 31, 2012 qualified for the dividends received deduction.

Please consult a tax advisor if you have questions about federal or state income tax laws, or on how to prepare your tax returns. If you have specific questions about your account, please contact your insurance provider.

The Trust's policies and procedures for voting proxies for portfolio securities and information about how the Trust voted proxies related to its portfolio securities during the 12-month period ended June 30 are available on our Web site — www.dws-investments.com (click on "proxy voting" at the bottom of the page) — or on the SEC's Web site — www.sec.gov. To obtain a written copy of the Trust's policies and procedures without charge, upon request, call us toll free at (800) 728-3337.

The Board of Trustees approved the renewal of DWS Alternative Asset Allocation VIP's investment management agreement (the "Agreement") with Deutsche Investment Management Americas Inc. ("DWS") and sub-advisory agreements (the "Sub-Advisory Agreements" and together with the Agreement, the "Agreements") between DWS and RREEF America L.L.C. ("RREEF"), an affiliate of DWS, and DWS and QS Investors, LLC ("QS Investors") in September 2012.

In terms of the process that the Board followed prior to approving the Agreements, shareholders should know that:

In connection with the contract review process, the Contract Committee and the Board considered the factors discussed below, among others. The Board also considered that DWS and its predecessors have managed the Fund since its inception, and the Board believes that a long-term relationship with a capable, conscientious advisor is in the best interests of the Fund. The Board considered, generally, that shareholders chose to invest or remain invested in the Fund knowing that DWS managed the Fund. DWS and RREEF are part of Deutsche Bank, a major global banking institution that is engaged in a wide range of financial services. The Board believes that there are advantages to being part of a global asset management business that offers a wide range of investing expertise and resources, including hundreds of portfolio managers and analysts with research capabilities in many countries throughout the world.

As part of the contract review process, the Board carefully considered the fees and expenses of each DWS fund overseen by the Board in light of the fund's performance. In many cases, this led to a negotiation with DWS of lower expense caps for the coming year than had previously been in place. As part of these negotiations, the Board indicated that it would consider relaxing these new lower caps in future years following sustained improvements in performance, among other considerations.

In June 2012, Deutsche Bank ("DB"), DWS's parent company, announced that DB's new management team had concluded the strategic review of its global asset management business announced in late 2011 by DB's prior management team, and would combine its Asset Management (of which DWS is a part) and Wealth Management divisions. Prior to approving the investment management agreements, the Independent Trustees were apprised of the expected management and structure of the new combined Asset & Wealth Management division ("AWM") and DWS. DB also advised the Independent Trustees that the U.S. asset management business is a critical and integral part of DB and AWM, and that DB would be reinvesting a significant portion of the substantial savings it expects to realize by combining its Asset Management and Wealth Management divisions into a combined AWM division, including enhancements to its investment capabilities. DB also confirmed its commitment to maintaining strong legal and compliance groups within the combined division.

While shareholders may focus primarily on fund performance and fees, the Fund's Board considers these and many other factors, including the quality and integrity of DWS's, QS Investors' and RREEF's personnel and such other issues as back-office operations, fund valuations, and compliance policies and procedures.

The information considered by the Board as part of its review of management fees included information regarding fees charged by DWS and its affiliates to similar institutional accounts and to similar funds offered primarily to European investors ("DWS Europe funds"), in each case as applicable. The Board observed that advisory fee rates for institutional accounts generally were lower than the management fees charged by similarly managed DWS U.S. mutual funds ("DWS Funds"), but also took note of the differences in services provided to DWS Funds as compared to institutional accounts. In the case of DWS Europe funds, the Board observed that fee rates for DWS Europe funds generally were higher than for similarly managed DWS Funds, but noted that differences in the types of services provided to DWS Funds relative to DWS Europe funds made it difficult to compare such fees.

On the basis of the information provided, the Board concluded that management fees were reasonable and appropriate in light of the nature, quality and extent of services provided by DWS, QS Investors and RREEF.

Based on all of the information considered and the conclusions reached, the Board unanimously determined that the continuation of the Agreements is in the best interests of the Fund. In making this determination, the Board did not give particular weight to any single factor identified above. The Board considered these factors over the course of numerous meetings, certain of which were in executive session with only the Independent Trustees and their counsel present. It is possible that individual Trustees may have weighed these factors differently in reaching their individual decisions to approve the continuation of the Agreements.

Pursuant to an Order entered into by Deutsche Investment Management Americas and affiliates (collectively, "DeAM") with the Attorney General of New York, I, Thomas H. Mack, have been appointed the Independent Fee Consultant for the DWS Funds (formerly the DWS Scudder Funds). My duties include preparing an annual written evaluation of the management fees DeAM charges the Funds, considering among other factors the management fees charged by other mutual fund companies for like services, management fees DeAM charges other clients for like services, DeAM's costs of supplying services under the management agreements and related profit margins, possible economies of scale if a Fund grows larger, and the nature and quality of DeAM's services, including fund performance. This report summarizes my evaluation for 2012, including my qualifications, the evaluation process for each of the DWS Funds, consideration of certain complex-level factors, and my conclusions. I served in substantially the same capacity in 2007, 2008, 2009, 2010 and 2011.

For more than 35 years I have served in various professional capacities within the investment management business. I have held investment analysis and advisory positions, including securities analyst, portfolio strategist and director of investment policy with a large investment firm. I have also performed business management functions, including business development, financial management and marketing research and analysis.

Since 1991, I have been an independent consultant within the asset management industry. I have provided services to over 125 client organizations, including investment managers, mutual fund boards, product distributors and related organizations. Over the past ten years I have completed a number of assignments for mutual fund boards, specifically including assisting boards with management contract renewal.

I hold a Master of Business Administration degree, with highest honors, from Harvard University and Master of Science and Bachelor of Science (highest honors) degrees from the University of California at Berkeley. I am an independent director and audit committee financial expert for two closed-end mutual funds and have served in various leadership and financial oversight capacities with non-profit organizations.

My work focused primarily on evaluating, fund-by-fund, the fees charged to each of the 103 mutual fund portfolios in the DWS Fund family. For each Fund, I considered each of the key factors mentioned above, as well as any other relevant information. In doing so I worked closely with the Funds' Independent Directors in their annual contract renewal process, as well as in their approval of contracts for several new funds (documented separately).

In evaluating each Fund's fees, I reviewed comprehensive materials provided by or on behalf of DeAM, including expense information prepared by Lipper Analytical, comparative performance information, profitability data, manager histories, and other materials. I also accessed certain additional information from the Lipper and Morningstar databases and drew on my industry knowledge and experience.

To facilitate evaluating this considerable body of information, I prepared for each Fund a document summarizing the key data elements in each area as well as additional analytics discussed below. This made it possible to consider each key data element in the context of the others.

In the course of contract renewal, DeAM agreed to implement a number of fee and expense adjustments requested by the Independent Directors which will favorably impact future fees and expenses, and my evaluation includes the effects of these changes.

The competitive fee and expense evaluation for each fund focused on two primary comparisons:

The Fund's contractual management fee (the advisory fee plus the administration fee where applicable) compared with those of a group of typically 12-15 funds in the same Lipper investment category (e.g. Large Capitalization Growth) having similar distribution arrangements and being of similar size.

The Fund's total expenses compared with a broader universe of funds from the same Lipper investment category and having similar distribution arrangements.

These two comparisons provide a view of not only the level of the fee compared with funds of similar scale but also the total expense the Fund bears for all the services it receives, in comparison with the investment choices available in the Fund's investment category and distribution channel. The principal figure-of-merit used in these comparisons was the subject Fund's percentile ranking against peers.

DeAM provided management fee schedules for all of its US domiciled fund and non-fund investment management accounts in any of the investment categories where there is a DWS Fund. These similar products included the other DWS Funds, non-fund pooled accounts, institutional accounts and sub-advisory accounts. Using this information, I calculated for each Fund the fee that would be charged to each similar product, at the subject Fund's asset level.

Evaluating information regarding non-fund products is difficult because there are varying levels of services required for different types of accounts, with mutual funds generally requiring considerably more regulatory and administrative types of service as well as having more frequent cash flows than other types of accounts. Also, while mutual fund fees for similar fund products can be expected to be similar, there will be some differences due to different pricing conditions in different distribution channels (e.g. retail funds versus those used in variable insurance products), differences in underlying investment processes and other factors.

DeAM provided a detailed profitability analysis for each Fund. After making some adjustments so that the presentation would be more comparable to the available industry figures, I reviewed profit margins from investment management alone, from investment management plus other fund services (excluding distribution) provided to the Funds by DeAM (principally shareholder services), and DeAM profits from all sources, including distribution. A later section comments on overall profitability.

Economies of scale — an expected decline in management cost per dollar of fund assets as fund assets grow — are very rarely quantified and documented because of inherent difficulties in collecting and analyzing relevant data. However, in virtually every investment category that I reviewed, larger funds tend to have lower fees and lower total expenses than smaller funds. To see how each DWS Fund compares with this industry observation, I reviewed:

The trend in Fund assets over the last five years and the accompanying trend in total expenses. This shows if the Fund has grown and, if so, whether total expense (management fees as well as other expenses) have declined as a percent of assets.

Whether the Fund has break-points in its management fee schedule, the extent of the fee reduction built into the schedule and the asset levels where the breaks take effect, and in the case of a sub-advised Fund how the Fund's break-points compare with those of the sub-advisory fee schedule.

How the Fund's contractual fee schedule compares with trends in the industry data. To accomplish this, I constructed a chart showing how actual latest-fiscal-year contractual fees of the Fund and of other similar funds relate to average fund assets, with the subject Fund's contractual fee schedule superimposed.

The quality-of-service evaluation focused on investment performance, which is the principal result of the investment management service. Each Fund's performance was reviewed over the past 1, 3, 5 and 10 years, as applicable, and compared with that of other funds in the same investment category and with a suitable market index.

In addition, I calculated and reviewed risk-adjusted returns relative to an index of similar mutual funds' returns and a suitable market index. The risk-adjusted returns analysis provides a way of determining the extent to which the Fund's return comparisons are mainly the product of investment value-added (or lack thereof) or alternatively taking considerably more or less risk than is typical in its investment category.

I also received and considered the history of portfolio manager changes for each Fund, as this provided an important context for evaluating the performance results.

While this evaluation was conducted mainly at the individual fund level, there are some issues relating to the reasonableness of fees that can alternatively be considered across the whole fund complex:

I reviewed DeAM's profitability analysis for all DWS Funds, with a view toward determining if the allocation procedures used were reasonable and how profit levels compared with public data for other investment managers.

I considered whether DeAM and affiliates receive any significant ancillary or "fallout" benefits that should be considered in interpreting the direct profitability results. These would be situations where serving as the investment manager of the Funds is beneficial to another part of the Deutsche Bank organization.

I considered how aggregated DWS Fund expenses had varied over the years, by asset class and in the context of trends in asset levels.

I considered how aggregated DWS Fund performance measures relative to appropriate peers had varied by asset class and over time.

I reviewed the structure of the DeAM organization, trends in staffing levels, and information on compensation of investment management and other professionals compared with industry data.

Based on the process and analysis discussed above, which included reviewing a wide range of information from management and external data sources and considering among other factors the fees DeAM charges other clients, the fees charged by other fund managers, DeAM's costs and profits associated with managing the Funds, economies of scale, possible fall-out benefits, and the nature and quality of services provided, in my opinion the management fees charged the DWS Funds are reasonable.

Thomas H. Mack

President, Thomas H. Mack & Co., Inc.

The following table presents certain information regarding the Board Members and Officers of the fund. Each Board Member's year of birth is set forth in parentheses after his or her name. Unless otherwise noted, (i) each Board Member has engaged in the principal occupation(s) noted in the table for at least the most recent five years, although not necessarily in the same capacity; and (ii) the address of each Independent Board Member is c/o Kenneth C. Froewiss, Chairman, DWS Mutual Funds, P.O. Box 78, Short Hills, NJ 07078. Except as otherwise noted below, the term of office for each Board Member is until the election and qualification of a successor, or until such Board Member sooner dies, resigns, is removed or as otherwise provided in the governing documents of the fund. Because the fund does not hold an annual meeting of shareholders, each Board Member will hold office for an indeterminate period. The Board Members may also serve in similar capacities with other funds in the fund complex.

The fund's Statement of Additional Information ("SAI") includes additional information about the Board Members. The SAI is available, without charge, upon request. If you would like to request a copy of the SAI, you may do so by calling the following toll-free number: (800) 728-3337.

DWS Investments Distributors, Inc.

DECEMBER 31, 2012

ANNUAL REPORT

DWS VARIABLE SERIES II

DWS Diversified International Equity VIP

Contents

16 Statement of Assets and Liabilities 17 Statement of Operations 18 Statement of Changes in Net Assets 21 Notes to Financial Statements 26 Report of Independent Registered Public Accounting Firm 27 Information About Your Fund's Expenses 29 Investment Management Agreement Approval 32 Summary of Management Fee Evaluation by Independent Fee Consultant 34 Board Members and Officers |

This report must be preceded or accompanied by a prospectus. To obtain an additional prospectus or summary prospectus, if available, call (800) 728-3337 or your financial representative. We advise you to consider the Fund's objectives, risks, charges and expenses carefully before investing. The summary prospectus and prospectus contain this and other important information about the Fund. Please read the prospectus carefully before you invest.

Investing in derivatives entails special risks relating to liquidity, leverage and credit that may reduce returns and/or increase volatility. Investing in foreign securities, particularly those of emerging markets, presents certain risks, such as currency fluctuations, political and economic changes, and market risks. The Fund may lend securities to approved institutions. Stocks may decline in value. See the prospectus for details.

DWS Investments is part of the Deutsche Asset & Wealth Management division of Deutsche Bank AG.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE NOT A DEPOSIT

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

Performance Summary December 31, 2012 (Unaudited)

Fund performance shown is historical, assumes reinvestment of all dividend and capital gain distributions and does not guarantee future results. Investment return and principal value fluctuate with changing market conditions so that, when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please contact your participating insurance company for the Fund's most recent month-end performance. Performance doesn't reflect charges and fees ("contract charges") associated with the separate account that invests in the Fund or any variable life insurance policy or variable annuity contract for which the Fund is an investment option. These charges and fees will reduce returns.

The gross expense ratio of the Fund, as stated in the fee table of the prospectus dated May 1, 2012 is 1.07% for Class A shares and may differ from the expense ratio disclosed in the Financial Highlights table in this report.

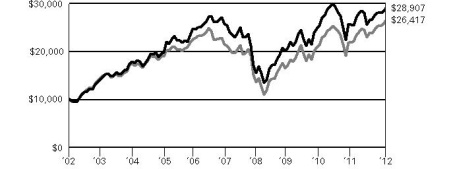

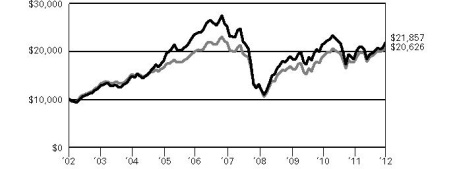

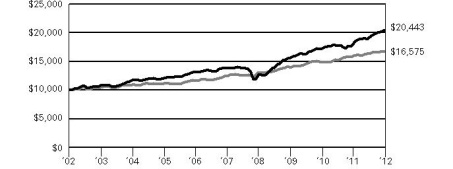

| Growth of an Assumed $10,000 Investment in DWS Diversified International Equity VIP |

| The Morgan Stanley Capital International (MSCI) Europe, Australasia and the Far East EAFE® Index is an unmanaged, free float-adjusted, market capitalization index that tracks international stock performance in the 21 developed markets of Europe, Australasia and the Far East. The index is calculated using closing local market prices and translates into U.S. dollars using the London close foreign exchange rates. Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index. |

| |

| Yearly periods ended December 31 | |

| Comparative Results | |

| DWS Diversified International Equity VIP | | 1-Year | | | 3-Year | | | 5-Year | | | 10-Year | |

| Class A | Growth of $10,000 | | $ | 11,734 | | | $ | 11,445 | | | $ | 7,579 | | | $ | 19,524 | |

| Average annual total return | | | 17.34 | % | | | 4.60 | % | | | -5.39 | % | | | 6.92 | % |

| MSCI EAFE Index | Growth of $10,000 | | $ | 11,732 | | | $ | 11,106 | | | $ | 8,287 | | | $ | 22,021 | |

| Average annual total return | | | 17.32 | % | | | 3.56 | % | | | -3.69 | % | | | 8.21 | % |

The growth of $10,000 is cumulative.

Management Summary December 31, 2012 (Unaudited)

Class A shares of the Fund returned 17.34% (unadjusted for contract charges) for the year ended December 31, 2012, compared with the Fund's benchmark, the MSCI EAFE® Index, which returned 17.32% for the same period.1 While the developed international markets registered a robust return during the past year, the strong performance was largely a second-half story. During the first five months of the year, market performance was pressured by adverse headlines regarding the European debt crisis and the continued slowdown in China's economic growth. However, the summer months brought a gradual restoration of investor confidence that stemmed, in part, from the aggressive response of the world's central banks. In the United States, the U.S. Federal Reserve Board (the Fed) announced expansions of its stimulative "quantitative easing" policy and said that it would maintain near-zero interest rates until unemployment declines significantly. In addition, European Central Bank (ECB) President Mario Draghi announced in July that the ECB would do "whatever it takes" to keep the region's currency union together — an important event that marked a turning point for the markets in 2012.

The largest positive contribution to Fund performance came from our underweight positions in various segments of the Japanese market, including the technology, consumer discretionary and industrials sectors.2 Overall, Japan is the Fund's second-largest country overweight. Our performance was also helped by an overweight position in technology, excluding Japan, and an underweight in energy.

Among the most notable detractors from performance were the Fund's underweights in Germany and France, which outperformed, as well as its allocation to Canada, which lagged. The Fund was also hurt by holding overweight positions in two sectors that lagged the broader market by a wide margin: telecommunications and utilities. Both are "defensive" in nature, meaning that investors tend to gravitate away from these areas when risk appetites are improving — as was the case in the past year. An underweight position in financials, the best-performing sector in the index during 2012, also cost the Fund some performance relative to its benchmark.

The Fund holds a weighting of 10% in two exchanged-traded funds (ETFs) linked to the performance of the emerging markets: Vanguard MSCI Emerging Markets Fund and iShares MSCI Emerging Markets Index Fund.3 We have held a position in the emerging markets since the Fund's inception in order to provide exposure to the strong economic fundamentals and attractive valuations in the asset class. This position contributed to performance during 2012, as the 18.22% return of the MSCI Emerging Markets Index outpaced the 17.32% gain of the MSCI EAFE Index.4

We expect that volatility is likely to be high in 2013 due to the shifting headlines out of the European debt crisis, China's growth, and U.S. tax policy.

Robert Wang

Russell Shtern, CFA

Portfolio Managers, QS Investors, LLC, Subadvisor to the Fund

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team's views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

1 The Morgan Stanley Capital International (MSCI) Europe, Australasia and the Far East (EAFE) Index is an unmanaged, free float-adjusted, market-capitalization index that tracks international stock performance in the 21 developed markets of Europe, Australasia and the Far East. The index is calculated using closing local market prices and translates into U.S. dollars using the London close foreign exchange rates. Index returns do not reflect fees or expenses and it is not possible to invest directly into an index.

2 "Overweight" means the Fund holds a higher weighting in a given sector or security than the benchmark. "Underweight" means the Fund holds a lower weighting.

3 An exchange-traded fund (ETF) is a security that tracks an index or asset like an index fund, but trades like a stock on an exchange. The Vanguard MSCI Emerging Markets Fund invests in stocks of companies located in emerging markets around the world, such as Brazil, Russia, China, Korea and Taiwan. The fund seeks to track the return of the MSCI Emerging Markets Index over the long term. The iShares MSCI Emerging Markets Index Fund seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in emerging markets, as represented by the MSCI Emerging Markets Index.

4 The Morgan Stanley Capital International (MSCI) Emerging Markets Index is an unmanaged, capitalization-weighted index of companies in a universe of 26 emerging markets. The index is calculated using closing local market prices and translates into U.S. dollars using the London close foreign exchange rates. Index returns do not reflect fees or expenses and it is not possible to invest directly into an index.

Portfolio Summary (Unaudited) Asset Allocation (As a % of Investment Portfolio excluding Securities Lending Collateral) | 12/31/12 | 12/31/11 |

| | | |

| Common Stocks | 88% | 89% |

| Exchange-Traded Funds | 10% | 10% |

| Cash Equivalents | 2% | 0% |

| Preferred Stocks | 0% | 1% |

| | 100% | 100% |

Sector Diversification (As a % of Common and Preferred Stocks and Rights) | 12/31/12 | 12/31/11 |

| | | |

| Telecommunication Services | 15% | 14% |

| Financials | 13% | 11% |

| Health Care | 12% | 13% |

| Information Technology | 12% | 7% |

| Consumer Staples | 12% | 13% |

| Materials | 9% | 9% |

| Utilities | 8% | 11% |

| Industrials | 8% | 8% |

| Consumer Discretionary | 7% | 9% |

| Energy | 4% | 5% |

| | 100% | 100% |

Geographical Diversification (As a % of Investment Portfolio excluding Cash Equivalents and Securities Lending Collateral) | 12/31/12 | 12/31/11 |

| | | |

| Continental Europe | 54% | 49% |

| Japan | 12% | 13% |

| Emerging Markets | 10% | 10% |

| Canada | 7% | 11% |

| United Kingdom | 7% | 8% |

| Asia (excluding Japan) | 6% | 5% |

| Australia | 4% | 4% |

| | 100% | 100% |

Portfolio holdings and characteristics are subject to change.

For more complete details about the Fund's investment portfolio, see page 6.

Following the Fund's fiscal first and third quarter-end, a complete portfolio holdings listing is filed with the SEC on Form N-Q. The form will be available on the SEC's Web site at www.sec.gov, and it also may be reviewed and copied at the SEC's Public Reference Room in Washington, D.C. Information on the operation of the SEC's Public Reference Room may be obtained by calling (800) SEC-0330. The Fund's portfolio holdings are also posted on www.dws-investments.com from time to time. Please see the Fund's current prospectus for more information.

Investment Portfolio December 31, 2012 | | | Shares | | | Value ($) | |

| | | | |

| Common Stocks 88.2% | |

| Australia 3.9% | |

| AGL Energy Ltd. | | | 11,731 | | | | 188,385 | |

| APA Group | | | 20,392 | | | | 117,708 | |

| Asciano Ltd. | | | 5,759 | | | | 28,144 | |

| Aurizon Holdings Ltd. | | | 11,307 | | | | 44,407 | |

| Australia & New Zealand Banking Group Ltd. | | | 2,339 | | | | 61,237 | |

| BHP Billiton Ltd. | | | 4,758 | | | | 185,815 | |

| Brambles Ltd. | | | 9,482 | | | | 75,459 | |

| Coca-Cola Amatil Ltd. | | | 2,294 | | | | 32,252 | |

| Cochlear Ltd. | | | 479 | | | | 39,627 | |

| Commonwealth Bank of Australia | | | 354 | | | | 22,995 | |

| Crown Ltd. | | | 7,919 | | | | 88,216 | |

| CSL Ltd. | | | 2,736 | | | | 154,562 | |

| Echo Entertainment Group Ltd. | | | 6,555 | | | | 23,636 | |

| Leighton Holdings Ltd. | | | 986 | | | | 18,551 | |

| National Australia Bank Ltd. | | | 2,126 | | | | 55,601 | |

| Newcrest Mining Ltd. | | | 1,231 | | | | 28,740 | |

| Origin Energy Ltd. | | | 6,869 | | | | 84,061 | |

| Rio Tinto Ltd. | | | 735 | | | | 51,159 | |

| Santos Ltd. | | | 6,168 | | | | 72,237 | |

| Sonic Healthcare Ltd. | | | 3,281 | | | | 45,816 | |

| SP AusNet | | | 47,515 | | | | 54,572 | |

| TABCORP Holdings Ltd. | | | 15,130 | | | | 48,353 | |

| Tatts Group Ltd. | | | 24,689 | | | | 77,736 | |

| Telstra Corp., Ltd. | | | 106,742 | | | | 486,264 | |

| Toll Holdings Ltd. | | | 4,694 | | | | 22,471 | |

| Transurban Group | | | 7,777 | | | | 49,393 | |

| Wesfarmers Ltd. | | | 3,054 | | | | 117,849 | |

| Westfield Group (REIT) (Units) | | | 2,462 | | | | 27,167 | |

| Westpac Banking Corp. | | | 2,057 | | | | 56,235 | |

| Woodside Petroleum Ltd. | | | 3,625 | | | | 129,193 | |

| Woolworths Ltd. | | | 2,335 | | | | 71,367 | |

| WorleyParsons Ltd. | | | 1,091 | | | | 26,914 | |

| (Cost $1,710,216) | | | | 2,586,122 | |

| Austria 0.6% | |

| Erste Group Bank AG* | | | 5,175 | | | | 165,473 | |

| Immofinanz AG* (a) | | | 21,199 | | | | 89,372 | |

| Raiffeisen Bank International AG | | | 1,218 | | | | 50,914 | |

| Vienna Insurance Group AG Wiener Versicherung Gruppe | | | 1,323 | | | | 70,971 | |

| (Cost $235,592) | | | | 376,730 | |

| Belgium 1.7% | |

| Ageas | | | 4,615 | | | | 137,692 | |

| Anheuser-Busch InBev NV | | | 4,693 | | | | 410,115 | |

| Delhaize Group | | | 593 | | | | 23,753 | |

| Groupe Bruxelles Lambert SA | | | 2,184 | | | | 172,174 | |

| KBC Groep NV | | | 3,189 | | | | 111,001 | |

| Solvay SA | | | 1,060 | | | | 152,588 | |

| Umicore SA | | | 2,235 | | | | 123,240 | |

| (Cost $668,389) | | | | 1,130,563 | |

| Bermuda 0.1% | |

| Seadrill Ltd. (a) (Cost $25,496) | | | 2,436 | | | | 89,777 | |

| Canada 7.3% | |

| Agnico-Eagle Mines Ltd. | | | 600 | | | | 31,445 | |

| Alimentation Couche-Tard, Inc. "B" | | | 1,500 | | | | 73,786 | |

| Bank of Montreal (a) | | | 800 | | | | 48,947 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Bank of Nova Scotia (a) | | | 1,100 | | | | 63,543 | |

| Barrick Gold Corp. (a) | | | 2,100 | | | | 73,512 | |

| BCE, Inc. (a) | | | 3,000 | | | | 128,571 | |

| Bell Aliant, Inc. (a) | | | 1,400 | | | | 37,044 | |

| Bombardier, Inc. "B" | | | 6,500 | | | | 24,570 | |

| Brookfield Asset Management, Inc. "A" (a) | | | 1,000 | | | | 36,634 | |

| CAE, Inc. (a) | | | 2,200 | | | | 22,272 | |

| Canadian Imperial Bank of Commerce (a) | | | 500 | | | | 40,198 | |

| Canadian National Railway Co. | | | 1,500 | | | | 136,217 | |

| Canadian Natural Resources Ltd. | | | 1,400 | | | | 40,310 | |

| Canadian Pacific Railway Ltd. (a) | | | 700 | | | | 71,006 | |

| Canadian Tire Corp., Ltd. "A" | | | 500 | | | | 34,875 | |

| Canadian Utilities Ltd. "A" | | | 1,800 | | | | 130,182 | |

| CGI Group, Inc. "A"* (a) | | | 23,300 | | | | 537,350 | |

| Eldorado Gold Corp. | | | 1,800 | | | | 23,163 | |

| Empire Co., Ltd. "A" | | | 500 | | | | 29,632 | |

| EnCana Corp. (a) | | | 1,000 | | | | 19,765 | |

| Finning International, Inc. | | | 900 | | | | 22,231 | |

| First Quantum Minerals Ltd. | | | 800 | | | | 17,621 | |

| Fortis, Inc. (a) | | | 6,400 | | | | 220,175 | |

| George Weston Ltd. | | | 700 | | | | 49,740 | |

| Gildan Activewear, Inc. | | | 800 | | | | 29,219 | |

| Goldcorp, Inc. | | | 1,800 | | | | 66,177 | |

| Kinross Gold Corp. | | | 2,300 | | | | 22,336 | |

| Loblaw Companies Ltd. (a) | | | 1,500 | | | | 63,230 | |

| Magna International, Inc. "A" (a) | | | 1,106 | | | | 55,239 | |

| Manulife Financial Corp. | | | 2,600 | | | | 35,313 | |

| Metro, Inc. "A" (a) | | | 1,300 | | | | 82,768 | |

| National Bank of Canada (a) | | | 400 | | | | 31,061 | |

| Open Text Corp.* | | | 6,600 | | | | 369,114 | |

| Potash Corp. of Saskatchewan, Inc. (a) | | | 1,300 | | | | 52,904 | |

| Research In Motion Ltd.* (a) | | | 50,600 | | | | 600,261 | |

| Rogers Communications, Inc. "B" (a) | | | 4,800 | | | | 217,923 | |

| Royal Bank of Canada (a) | | | 1,300 | | | | 78,259 | |

| Saputo, Inc. (a) | | | 1,800 | | | | 91,040 | |

| Shaw Communications, Inc. "B" (a) | | | 2,400 | | | | 55,108 | |

| Shoppers Drug Mart Corp. (a) | | | 2,700 | | | | 116,176 | |

| Silver Wheaton Corp. | | | 1,100 | | | | 39,656 | |

| SNC-Lavalin Group, Inc. (a) | | | 600 | | | | 24,321 | |

| Sun Life Financial, Inc. (a) | | | 1,000 | | | | 26,511 | |

| Suncor Energy, Inc. | | | 2,020 | | | | 66,426 | |

| Teck Resources Ltd. "B" (a) | | | 1,200 | | | | 43,611 | |

| Telus Corp. (Non-Voting Shares) (a) | | | 1,900 | | | | 123,547 | |

| Thomson Reuters Corp. (b) | | | 1,158 | | | | 33,651 | |

| Thomson Reuters Corp. (a) (b) | | | 800 | | | | 23,147 | |

| Tim Hortons, Inc. (a) | | | 1,000 | | | | 49,090 | |

| Toronto-Dominion Bank (a) | | | 900 | | | | 75,777 | |

| TransAlta Corp. (a) | | | 8,600 | | | | 130,725 | |

| Valeant Pharmaceuticals International, Inc.* | | | 5,700 | | | | 340,040 | |

| Yamana Gold, Inc. (a) | | | 1,100 | | | | 18,921 | |

| (Cost $4,203,376) | | | | 4,874,340 | |

| Denmark 2.1% | |

| A P Moller-Maersk AS "A" | | | 7 | | | | 49,849 | |

| A P Moller-Maersk AS "B" | | | 18 | | | | 137,780 | |

| Carlsberg AS "B" | | | 4,992 | | | | 490,786 | |

| Danske Bank AS* | | | 17,646 | | | | 299,991 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| DSV AS | | | 2,622 | | | | 68,372 | |

| Novo Nordisk AS "B" | | | 1,669 | | | | 272,581 | |

| Tryg AS | | | 621 | | | | 46,952 | |

| William Demant Holding AS* | | | 291 | | | | 24,974 | |

| (Cost $886,289) | | | | 1,391,285 | |

| Finland 4.3% | |

| Fortum Oyj | | | 14,781 | | | | 277,964 | |

| Kone Oyj "B" | | | 1,396 | | | | 103,370 | |

| Metso Corp. | | | 1,104 | | | | 48,093 | |

| Nokia Oyj (a) | | | 399,372 | | | | 1,570,570 | |

| Pohjola Bank PLC | | | 3,258 | | | | 48,652 | |

| Sampo Oyj "A" | | | 10,661 | | | | 344,738 | |

| Stora Enso Oyj "R" | | | 23,027 | | | | 162,866 | |

| UPM-Kymmene Oyj | | | 20,179 | | | | 239,799 | |

| Wartsila Oyj | | | 1,559 | | | | 68,954 | |

| (Cost $1,991,577) | | | | 2,865,006 | |

| France 6.9% | |

| Air Liquide SA | | | 1,652 | | | | 207,023 | |

| Arkema | | | 421 | | | | 44,266 | |

| AtoS | | | 697 | | | | 49,665 | |

| AXA SA | | | 4,348 | | | | 78,646 | |

| BNP Paribas SA | | | 2,000 | | | | 112,734 | |

| Bouygues SA | | | 734 | | | | 21,643 | |

| Cap Gemini | | | 2,014 | | | | 87,770 | |

| Carrefour SA | | | 2,147 | | | | 55,598 | |

| Casino Guichard-Perrachon SA | | | 247 | | | | 23,760 | |

| Cie de St-Gobain | | | 755 | | | | 32,305 | |

| DANONE SA | | | 2,453 | | | | 162,069 | |

| Dassault Systemes SA | | | 830 | | | | 92,915 | |

| Electricite de France | | | 2,181 | | | | 40,877 | |

| Essilor International SA | | | 2,621 | | | | 265,744 | |

| France Telecom SA | | | 28,037 | | | | 313,975 | |

| GDF Suez | | | 12,916 | | | | 266,120 | |

| Iliad SA | | | 426 | | | | 73,329 | |

| L'Oreal SA | | | 815 | | | | 113,847 | |

| Lafarge SA | | | 843 | | | | 54,018 | |

| LVMH Moet Hennessy Louis Vuitton SA | | | 420 | | | | 78,266 | |

| Pernod Ricard SA | | | 790 | | | | 92,894 | |

| Sanofi | | | 13,398 | | | | 1,270,602 | |

| Schneider Electric SA | | | 894 | | | | 66,678 | |

| Societe Generale* | | | 1,549 | | | | 58,264 | |

| Suez Environnement Co. | | | 1,869 | | | | 22,536 | |

| Technip SA | | | 427 | | | | 49,160 | |

| Total SA | | | 6,134 | | | | 317,481 | |

| Unibail-Rodamco SE (REIT) (a) | | | 265 | | | | 64,874 | |

| Veolia Environnement | | | 4,218 | | | | 51,417 | |

| Vinci SA (a) | | | 944 | | | | 44,927 | |

| Vivendi | | | 19,233 | | | | 433,121 | |

| (Cost $3,844,764) | | | | 4,646,524 | |

| Germany 5.2% | |

| Adidas AG | | | 551 | | | | 49,104 | |

| Allianz SE (Registered) | | | 1,916 | | | | 265,436 | |

| BASF SE | | | 1,618 | | | | 152,078 | |

| Bayer AG | | | 3,118 | | | | 296,093 | |

| Bayerische Motoren Werke (BMW) AG | | | 704 | | | | 67,895 | |

| Beiersdorf AG | | | 1,074 | | | | 87,756 | |

| Commerzbank AG* | | | 17,612 | | | | 33,517 | |

| Continental AG | | | 289 | | | | 33,439 | |

| Daimler AG (Registered) | | | 1,589 | | | | 86,830 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Deutsche Boerse AG | | | 688 | | | | 41,993 | |

| Deutsche Post AG (Registered) (a) | | | 3,555 | | | | 77,952 | |

| Deutsche Telekom AG (Registered) | | | 67,999 | | | | 772,552 | |

| E.ON AG | | | 12,733 | | | | 237,121 | |

| Fresenius Medical Care AG & Co. KGaA | | | 940 | | | | 64,947 | |

| Fresenius SE & Co. KGaA | | | 632 | | | | 72,739 | |

| GEA Group AG | | | 1,223 | | | | 39,501 | |

| Henkel AG & Co. KGaA | | | 1,435 | | | | 98,285 | |

| Infineon Technologies AG | | | 4,778 | | | | 38,772 | |

| K+S AG (Registered) | | | 447 | | | | 20,666 | |

| Kabel Deutschland Holding AG | | | 301 | | | | 22,508 | |

| Linde AG | | | 332 | | | | 57,897 | |

| Merck KGaA | | | 233 | | | | 30,742 | |

| Metro AG | | | 2,014 | | | | 55,831 | |

| Muenchener Rueckversicherungs-Gesellschaft AG (Registered) | | | 388 | | | | 69,663 | |

| RWE AG | | | 3,136 | | | | 129,463 | |

| SAP AG | | | 2,863 | | | | 229,345 | |

| Siemens AG (Registered) | | | 2,778 | | | | 301,940 | |

| Suedzucker AG | | | 67 | | | | 2,742 | |

| Volkswagen AG | | | 110 | | | | 23,632 | |

| (Cost $2,593,709) | | | | 3,460,439 | |

| Hong Kong 2.5% | |

| AIA Group Ltd. | | | 23,000 | | | | 91,665 | |

| Cathay Pacific Airways Ltd. (a) | | | 15,000 | | | | 27,887 | |

| Cheung Kong (Holdings) Ltd. | | | 5,000 | | | | 77,394 | |

| Cheung Kong Infrastructure Holdings Ltd. | | | 7,000 | | | | 43,001 | |

| CLP Holdings Ltd. | | | 17,500 | | | | 147,292 | |

| Galaxy Entertainment Group Ltd.* | | | 12,000 | | | | 47,787 | |

| Hang Lung Properties Ltd. | | | 12,000 | | | | 48,114 | |

| Hang Seng Bank Ltd. (a) | | | 2,200 | | | | 33,986 | |

| Hong Kong & China Gas Co., Ltd. | | | 45,813 | | | | 125,646 | |

| Hong Kong Exchanges & Clearing Ltd. (a) | | | 3,500 | | | | 60,296 | |

| Hopewell Holdings Ltd. | | | 6,000 | | | | 25,944 | |

| Hutchison Whampoa Ltd. | | | 31,000 | | | | 328,857 | |

| Li & Fung Ltd. (a) | | | 36,000 | | | | 64,863 | |

| Link (REIT) | | | 2,000 | | | | 10,016 | |

| MTR Corp., Ltd. | | | 17,500 | | | | 69,273 | |

| Noble Group Ltd. | | | 51,363 | | | | 49,529 | |

| NWS Holdings Ltd. | | | 30,000 | | | | 51,205 | |

| Orient Overseas International Ltd. | | | 5,000 | | | | 32,955 | |

| Power Assets Holdings Ltd. | | | 14,000 | | | | 120,163 | |

| Shangri-La Asia Ltd. | | | 12,000 | | | | 24,180 | |

| SJM Holdings Ltd. | | | 12,000 | | | | 28,239 | |

| Sun Hung Kai Properties Ltd. | | | 5,000 | | | | 75,726 | |

| Swire Pacific Ltd. "A" | | | 2,000 | | | | 24,854 | |

| Wharf Holdings Ltd. | | | 6,000 | | | | 47,513 | |

| Yue Yuen Industrial (Holdings) Ltd. (a) | | | 5,000 | | | | 16,880 | |

| (Cost $1,155,346) | | | | 1,673,265 | |

| Ireland 3.1% | |

| CRH PLC (b) | | | 20,956 | | | | 434,855 | |

| CRH PLC (b) | | | 56,843 | | | | 1,188,225 | |

| Elan Corp. PLC* | | | 31,025 | | | | 320,408 | |

| Experian PLC | | | 1,159 | | | | 18,726 | |

| Prothena Corp. PLC* | | | 757 | | | | 5,547 | |

| Shire PLC | | | 3,629 | | | | 111,458 | |

| (Cost $1,879,352) | | | | 2,079,219 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Italy 3.9% | |

| Assicurazioni Generali SpA | | | 6,464 | | | | 117,908 | |

| Atlantia SpA | | | 7,403 | | | | 134,268 | |

| Enel Green Power SpA | | | 16,188 | | | | 30,275 | |

| Enel SpA | | | 71,348 | | | | 296,835 | |

| Eni SpA | | | 9,990 | | | | 246,449 | |

| Fiat Industrial SpA | | | 18,223 | | | | 199,806 | |

| Fiat SpA* (a) | | | 22,794 | | | | 115,136 | |

| Finmeccanica SpA* | | | 7,959 | | | | 46,126 | |

| Intesa Sanpaolo | | | 40,339 | | | | 69,786 | |

| Luxottica Group SpA | | | 3,208 | | | | 133,296 | |

| Pirelli & C. SpA (a) | | | 5,969 | | | | 68,482 | |

| Prysmian SpA | | | 5,291 | | | | 107,048 | |

| Saipem SpA | | | 1,195 | | | | 46,363 | |

| Snam SpA | | | 16,191 | | | | 75,289 | |

| Telecom Italia SpA | | | 530,993 | | | | 479,976 | |

| Telecom Italia SpA (RSP) | | | 357,071 | | | | 282,551 | |

| Terna — Rete Elettrica Nationale SpA | | | 14,939 | | | | 59,828 | |

| UBI Banca — Unione di Banche Italiane ScpA | | | 3,919 | | | | 18,280 | |

| UniCredit SpA* | | | 21,088 | | | | 104,134 | |

| (Cost $2,579,369) | | | | 2,631,836 | |

| Japan 11.3% | |

| AEON Co., Ltd. | | | 5,200 | | | | 59,439 | |

| Ajinomoto Co., Inc. | | | 6,000 | | | | 79,387 | |

| Alfresa Holdings Corp. | | | 500 | | | | 19,539 | |

| Asahi Group Holdings Ltd. | | | 3,400 | | | | 72,070 | |

| Asahi Kasei Corp. | | | 5,000 | | | | 29,527 | |

| Astellas Pharma, Inc. | | | 3,800 | | | | 170,701 | |

| Bridgestone Corp. | | | 1,200 | | | | 31,105 | |

| Canon, Inc. | | | 1,500 | | | | 58,833 | |

| Central Japan Railway Co. | | | 300 | | | | 24,341 | |

| Chubu Electric Power Co., Inc. | | | 13,200 | | | | 176,131 | |

| Chugai Pharmaceutical Co., Ltd. | | | 2,300 | | | | 44,080 | |

| Chugoku Electric Power Co., Inc. | | | 6,300 | | | | 98,796 | |

| Dai-ichi Life Insurance Co., Ltd. | | | 35 | | | | 49,247 | |

| Daiichi Sankyo Co., Ltd. | | | 5,800 | | | | 88,969 | |

| Dainippon Sumitomo Pharma Co., Ltd. | | | 1,800 | | | | 21,625 | |

| Daito Trust Construction Co., Ltd. | | | 400 | | | | 37,641 | |

| Daiwa House Industry Co., Ltd. | | | 2,000 | | | | 34,413 | |

| Daiwa Securities Group, Inc. (a) | | | 10,000 | | | | 55,697 | |

| Denso Corp. | | | 800 | | | | 27,836 | |

| Eisai Co., Ltd. | | | 2,100 | | | | 87,684 | |

| Electric Power Development Co., Ltd. | | | 1,600 | | | | 37,929 | |

| FamilyMart Co., Ltd. | | | 500 | | | | 20,582 | |

| FANUC Corp. | | | 200 | | | | 37,193 | |

| FUJIFILM Holdings Corp. | | | 1,200 | | | | 24,170 | |

| Hisamitsu Pharmaceutical Co., Inc. (a) | | | 700 | | | | 34,708 | |

| Hitachi Ltd. | | | 7,000 | | | | 41,196 | |

| Hokkaido Electric Power Co., Inc. | | | 2,100 | | | | 25,501 | |

| Hokuriku Electric Power Co. | | | 2,800 | | | | 33,104 | |

| Honda Motor Co., Ltd. | | | 1,600 | | | | 58,973 | |

| HOYA Corp. | | | 1,400 | | | | 27,565 | |

| Idemitsu Kosan Co., Ltd. | | | 300 | | | | 26,129 | |

| INPEX Corp. | | | 21 | | | | 112,074 | |

| Japan Petroleum Exploration Co., Ltd. | | | 700 | | | | 24,464 | |

| Japan Real Estate Investment Corp. (REIT) | | | 5 | | | | 49,044 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Japan Tobacco, Inc. | | | 7,400 | | | | 208,618 | |

| JFE Holdings, Inc. | | | 1,400 | | | | 26,394 | |

| JX Holdings, Inc. | | | 22,920 | | | | 129,091 | |

| Kansai Electric Power Co., Inc. | | | 15,900 | | | | 167,057 | |

| Kao Corp. | | | 4,500 | | | | 117,245 | |

| KDDI Corp. | | | 3,400 | | | | 240,159 | |

| Keyence Corp. | | | 110 | | | | 30,359 | |

| Kikkoman Corp. | | | 2,000 | | | | 28,570 | |

| Kirin Holdings Co., Ltd. | | | 8,000 | | | | 94,003 | |

| Komatsu Ltd. | | | 900 | | | | 23,031 | |

| Kyocera Corp. | | | 400 | | | | 36,272 | |

| Kyowa Hakko Kirin Co., Ltd. | | | 3,000 | | | | 29,627 | |

| Kyushu Electric Power Co., Inc. | | | 9,500 | | | | 108,446 | |

| Lawson, Inc. (a) | | | 500 | | | | 33,987 | |

| MEIJI Holdings Co., Ltd. | | | 500 | | | | 21,671 | |

| Miraca Holdings, Inc. | | | 500 | | | | 20,132 | |

| Mitsubishi Chemical Holdings Corp. | | | 6,500 | | | | 32,423 | |

| Mitsubishi Corp. | | | 1,900 | | | | 36,521 | |

| Mitsubishi Estate Co., Ltd. | | | 4,000 | | | | 95,625 | |

| Mitsubishi Tanabe Pharma Corp. | | | 2,200 | | | | 28,685 | |

| Mitsubishi UFJ Financial Group, Inc. | | | 43,700 | | | | 235,156 | |

| Mitsui & Co., Ltd. | | | 2,500 | | | | 37,401 | |

| Mitsui Fudosan Co., Ltd. | | | 3,000 | | | | 73,293 | |

| Mizuho Financial Group, Inc. | | | 77,200 | | | | 141,248 | |

| MS&AD Insurance Group Holdings, Inc. | | | 2,400 | | | | 47,948 | |

| Nintendo Co., Ltd. | | | 200 | | | | 21,340 | |

| Nippon Building Fund, Inc. (REIT) | | | 4 | | | | 41,241 | |

| Nippon Meat Packers, Inc. | | | 2,000 | | | | 27,534 | |

| Nippon Steel & Sumitomo Metal | | | 16,000 | | | | 39,357 | |

| Nippon Telegraph & Telephone Corp. | | | 5,409 | | | | 227,212 | |

| Nishi-Nippon City Bank Ltd. | | | 8,000 | | | | 19,708 | |

| Nissan Motor Co., Ltd. | | | 3,400 | | | | 32,271 | |

| Nisshin Seifun Group, Inc. | | | 3,000 | | | | 37,539 | |

| Nissin Foods Holdings Co., Ltd. | | | 700 | | | | 26,543 | |

| Nitto Denko Corp. | | | 600 | | | | 29,520 | |

| NKSJ Holdings, Inc. | | | 1,750 | | | | 37,269 | |

| Nomura Holdings, Inc. | | | 12,000 | | | | 70,851 | |

| Nomura Real Estate Office Fund, Inc. (REIT) | | | 5 | | | | 28,689 | |

| NTT DoCoMo, Inc. | | | 187 | | | | 268,560 | |

| Olympus Corp.* | | | 1,900 | | | | 36,877 | |

| Ono Pharmaceutical Co., Ltd. | | | 700 | | | | 35,721 | |

| Oriental Land Co., Ltd. | | | 200 | | | | 24,168 | |

| ORIX Corp. | | | 580 | | | | 65,447 | |

| Osaka Gas Co., Ltd. | | | 30,000 | | | | 108,967 | |

| Otsuka Holdings KK | | | 2,600 | | | | 72,995 | |

| Panasonic Corp. (a) | | | 3,100 | | | | 18,836 | |

| Resona Holdings, Inc. | | | 6,900 | | | | 31,283 | |

| Santen Pharmaceutical Co., Ltd. | | | 700 | | | | 26,801 | |

| Seven & I Holdings Co., Ltd. | | | 6,200 | | | | 174,499 | |

| Shikoku Electric Power Co., Inc. | | | 2,600 | | | | 41,465 | |

| Shin-Etsu Chemical Co., Ltd. | | | 700 | | | | 42,756 | |

| Shionogi & Co., Ltd. | | | 3,400 | | | | 56,636 | |

| Shiseido Co., Ltd. (a) | | | 3,500 | | | | 49,219 | |

| Showa Shell Sekiyu KK | | | 4,000 | | | | 22,712 | |

| SOFTBANK Corp. | | | 11,000 | | | | 402,509 | |

| Sony Corp. | | | 1,300 | | | | 14,546 | |

| Sumitomo Chemical Co., Ltd. | | | 6,000 | | | | 18,930 | |

| Sumitomo Metal Mining Co., Ltd. | | | 2,000 | | | | 28,223 | |

| Sumitomo Mitsui Financial Group, Inc. | | | 4,800 | | | | 174,379 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Sumitomo Mitsui Trust Holdings, Inc. | | | 13,410 | | | | 47,115 | |

| Sumitomo Realty & Development Co., Ltd. | | | 2,000 | | | | 66,455 | |

| Suzuken Co., Ltd. | | | 900 | | | | 25,362 | |

| Sysmex Corp. | | | 400 | | | | 18,326 | |

| T&D Holdings, Inc. | | | 3,600 | | | | 43,877 | |

| Taisho Pharmaceutical Holdings Co., Ltd. | | | 300 | | | | 20,490 | |

| Takeda Pharmaceutical Co., Ltd. | | | 6,300 | | | | 281,545 | |

| Terumo Corp. | | | 1,400 | | | | 55,627 | |

| Toho Gas Co., Ltd. | | | 7,000 | | | | 37,576 | |

| Tohoku Electric Power Co., Inc.* | | | 10,000 | | | | 93,060 | |

| Tokio Marine Holdings, Inc. | | | 2,200 | | | | 61,340 | |

| Tokyo Electric Power Co., Inc.* | | | 24,100 | | | | 57,763 | |

| Tokyo Gas Co., Ltd. | | | 44,000 | | | | 201,166 | |

| TonenGeneral Sekiyu KK | | | 4,000 | | | | 34,468 | |

| Toray Industries, Inc. | | | 4,000 | | | | 24,391 | |

| Toshiba Corp. | | | 8,000 | | | | 31,634 | |

| Toyo Suisan Kaisha Ltd. | | | 1,000 | | | | 26,650 | |

| Toyota Motor Corp. | | | 2,200 | | | | 102,688 | |

| Tsumura & Co. | | | 700 | | | | 21,096 | |

| Unicharm Corp. | | | 900 | | | | 46,851 | |

| Yakult Honsha Co., Ltd. (a) | | | 700 | | | | 30,673 | |

| (Cost $6,903,485) | | | | 7,545,411 | |

| Luxembourg 0.3% | |

| ArcelorMittal | | | 4,154 | | | | 71,910 | |

| Millicom International Cellular SA (SDR) | | | 1,194 | | | | 103,778 | |

| Tenaris SA (a) | | | 1,718 | | | | 35,814 | |

| (Cost $164,913) | | | | 211,502 | |

| Macau 0.1% | |

| Sands China Ltd. | | | 16,000 | | | | 71,775 | |

| Wynn Macau Ltd.* (a) | | | 9,200 | | | | 25,355 | |

| (Cost $36,554) | | | | 97,130 | |

| Netherlands 6.6% | |

| AEGON NV | | | 13,027 | | | | 83,019 | |

| Akzo Nobel NV | | | 2,534 | | | | 167,211 | |

| ASML Holding NV | | | 23,043 | | | | 1,491,796 | |

| Corio NV (REIT) | | | 729 | | | | 33,164 | |

| Gemalto NV | | | 952 | | | | 86,190 | |

| Heineken Holding NV | | | 913 | | | | 50,011 | |

| Heineken NV | | | 780 | | | | 52,028 | |

| ING Groep NV (CVA)* | | | 27,123 | | | | 259,369 | |

| Koninklijke (Royal) KPN NV | | | 86,611 | | | | 428,309 | |

| Koninklijke Ahold NV | | | 6,503 | | | | 86,377 | |

| Koninklijke DSM NV | | | 1,774 | | | | 106,856 | |

| Koninklijke Philips Electronics NV | | | 5,110 | | | | 137,093 | |

| Koninklijke Vopak NV | | | 374 | | | | 26,371 | |

| Randstad Holding NV | | | 918 | | | | 33,887 | |

| Reed Elsevier NV | | | 23,165 | | | | 343,212 | |

| Royal Dutch Shell PLC "A" | | | 1,952 | | | | 68,973 | |

| Royal Dutch Shell PLC "B" | | | 2,331 | | | | 82,500 | |

| TNT Express NV | | | 2,201 | | | | 24,898 | |

| Unilever NV (CVA) | | | 7,993 | | | | 301,606 | |

| Wolters Kluwer NV | | | 11,096 | | | | 229,443 | |

| Ziggo NV | | | 9,664 | | | | 312,330 | |

| (Cost $3,617,125) | | | | 4,404,643 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Norway 2.0% | |

| DnB ASA | | | 24,697 | | | | 314,811 | |

| Gjensidige Forsikring ASA | | | 2,423 | | | | 34,870 | |

| Norsk Hydro ASA | | | 22,115 | | | | 112,662 | |

| Statoil ASA | | | 7,119 | | | | 178,645 | |

| Telenor ASA | | | 23,063 | | | | 468,564 | |

| Yara International ASA | | | 4,676 | | | | 232,099 | |

| (Cost $690,347) | | | | 1,341,651 | |

| Singapore 3.2% | |

| CapitaLand Ltd. (a) | | | 20,000 | | | | 61,356 | |

| ComfortDelGro Corp., Ltd. | | | 29,000 | | | | 42,503 | |

| DBS Group Holdings Ltd. | | | 10,000 | | | | 122,413 | |

| Fraser & Neave Ltd. | | | 7,000 | | | | 55,715 | |

| Genting Singapore PLC (a) | | | 175,000 | | | | 200,240 | |

| Global Logistic Properties Ltd. | | | 17,000 | | | | 39,089 | |

| Golden Agri-Resources Ltd. | | | 173,000 | | | | 93,132 | |

| Hutchison Port Holdings Trust (Units) | | | 63,000 | | | | 50,157 | |

| Jardine Cycle & Carriage Ltd. | | | 3,000 | | | | 119,360 | |

| Keppel Corp., Ltd. | | | 15,400 | | | | 139,932 | |

| Olam International Ltd. (a) | | | 43,000 | | | | 55,148 | |

| Oversea-Chinese Banking Corp., Ltd. | | | 14,000 | | | | 112,639 | |

| SembCorp Industries Ltd. | | | 16,000 | | | | 69,716 | |

| SembCorp Marine Ltd. | | | 8,000 | | | | 30,456 | |

| Singapore Airlines Ltd. | | | 6,000 | | | | 53,064 | |

| Singapore Exchange Ltd. | | | 7,000 | | | | 40,582 | |

| Singapore Press Holdings Ltd. | | | 37,000 | | | | 122,415 | |

| Singapore Technologies Engineering Ltd. | | | 15,000 | | | | 47,349 | |

| Singapore Telecommunications Ltd. | | | 157,000 | | | | 426,734 | |

| StarHub Ltd. | | | 14,000 | | | | 43,716 | |

| United Overseas Bank Ltd. | | | 7,000 | | | | 114,649 | |

| Wilmar International Ltd. | | | 50,000 | | | | 138,191 | |

| (Cost $1,503,370) | | | | 2,178,556 | |

| Spain 5.0% | |

| Abertis Infraestructuras SA | | | 10,380 | | | | 172,989 | |

| Acciona SA | | | 263 | | | | 19,944 | |

| ACS, Actividades de Construccion y Servicios SA (a) | | | 2,511 | | | | 64,261 | |

| Amadeus IT Holding SA "A" | | | 16,502 | | | | 414,106 | |

| Banco Bilbao Vizcaya Argentaria SA (a) | | | 12,973 | | | | 119,097 | |

| Banco Santander SA | | | 26,579 | | | | 214,309 | |

| Enagas SA | | | 2,258 | | | | 48,319 | |

| Ferrovial SA (a) | | | 7,677 | | | | 113,191 | |

| Gas Natural SDG SA | | | 4,736 | | | | 86,602 | |

| Iberdrola SA | | | 50,661 | | | | 282,505 | |

| Industria de Diseno Textil SA | | | 3,008 | | | | 421,414 | |

| Red Electrica Corporacion SA (a) | | | 1,484 | | | | 73,321 | |

| Repsol SA | | | 20,305 | | | | 416,997 | |

| Telefonica SA | | | 61,238 | | | | 831,534 | |

| Zardoya Otis SA (a) | | | 3,050 | | | | 43,961 | |

| (Cost $2,910,128) | | | | 3,322,550 | |

| Sweden 3.5% | |

| Assa Abloy AB "B" | | | 1,207 | | | | 45,450 | |

| Atlas Copco AB "A" | | | 2,084 | | | | 57,692 | |

| Boliden AB | | | 10,746 | | | | 204,250 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Electrolux AB "B" | | | 1,087 | | | | 28,549 | |

| Hennes & Mauritz AB "B" | | | 5,804 | | | | 201,685 | |

| Hexagon AB "B" | | | 2,788 | | | | 70,083 | |

| Husqvarna AB "B" | | | 4,852 | | | | 29,412 | |

| Nordea Bank AB | | | 10,270 | | | | 98,358 | |

| Sandvik AB | | | 3,095 | | | | 49,744 | |

| Skandinaviska Enskilda Banken AB "A" | | | 4,035 | | | | 34,409 | |

| Skanska AB "B" | | | 1,724 | | | | 28,365 | |

| SKF AB "B" | | | 1,279 | | | | 32,364 | |

| Svenska Cellulosa AB "B" | | | 13,283 | | | | 290,774 | |

| Svenska Handelsbanken AB "A" | | | 1,999 | | | | 71,624 | |

| Swedbank AB "A" | | | 3,758 | | | | 73,951 | |

| Swedish Match AB | | | 6,442 | | | | 216,972 | |

| Tele2 AB "B" | | | 5,797 | | | | 105,136 | |

| Telefonaktiebolaget LM Ericsson "B" | | | 42,182 | | | | 424,278 | |

| TeliaSonera AB | | | 38,625 | | | | 263,094 | |

| Volvo AB "B" | | | 2,677 | | | | 36,915 | |

| (Cost $1,784,181) | | | | 2,363,105 | |

| Switzerland 7.4% | |

| ABB Ltd. (Registered)* (a) | | | 7,290 | | | | 151,369 | |

| Actelion Ltd. (Registered)* | | | 481 | | | | 23,104 | |

| Adecco SA (Registered)* | | | 824 | | | | 43,677 | |

| Aryzta AG* | | | 598 | | | | 30,682 | |

| Compagnie Financiere Richemont SA "A" | | | 1,918 | | | | 153,370 | |

| Credit Suisse Group AG (Registered)* | | | 2,979 | | | | 74,747 | |

| Geberit AG (Registered)* | | | 246 | | | | 54,459 | |

| Givaudan SA (Registered)* | | | 61 | | | | 64,671 | |

| Glencore International PLC (a) | | | 4,330 | | | | 25,234 | |

| Holcim Ltd. (Registered)* | | | 1,280 | | | | 94,276 | |

| Lonza Group AG (Registered)* | | | 466 | | | | 25,205 | |

| Nestle SA (Registered) | | | 20,152 | | | | 1,313,389 | |

| Novartis AG (Registered) | | | 11,006 | | | | 696,806 | |

| Roche Holding AG (Genusschein) | | | 3,215 | | | | 654,976 | |

| Sika AG | | | 19 | | | | 44,035 | |

| Sonova Holding AG (Registered)* | | | 289 | | | | 32,017 | |

| STMicroelectronics NV | | | 8,506 | | | | 62,017 | |

| Swatch Group AG (Bearer) | | | 87 | | | | 44,773 | |

| Swiss Re AG.* | | | 723 | | | | 52,768 | |

| Swisscom AG (Registered) (a) | | | 2,114 | | | | 911,751 | |

| Syngenta AG (Registered) | | | 246 | | | | 99,232 | |

| UBS AG (Registered)* | | | 5,885 | | | | 92,549 | |

| Wolseley PLC | | | 878 | | | | 41,732 | |

| Xstrata PLC | | | 2,858 | | | | 50,833 | |

| Zurich Insurance Group AG* | | | 398 | | | | 106,422 | |

| (Cost $2,859,380) | | | | 4,944,094 | |

| United Kingdom 7.0% | |

| Anglo American PLC | | | 1,947 | | | | 62,151 | |

| ARM Holdings PLC | | | 28,328 | | | | 362,228 | |

| AstraZeneca PLC | | | 8,219 | | | | 388,556 | |

| BAE Systems PLC | | | 8,559 | | | | 47,023 | |

| Barclays PLC | | | 8,467 | | | | 36,564 | |

| BG Group PLC | | | 3,267 | | | | 54,782 | |

| BHP Billiton PLC | | | 3,282 | | | | 115,328 | |

| BP PLC | | | 14,756 | | | | 102,241 | |

| British American Tobacco PLC | | | 2,622 | | | | 132,857 | |

| British Sky Broadcasting Group PLC | | | 3,065 | | | | 38,288 | |

| BT Group PLC | | | 34,124 | | | | 128,630 | |

| | | Shares | | | Value ($) | |

| | | | | | | | | |

| Burberry Group PLC | | | 877 | | | | 17,956 | |

| Capita PLC | | | 1,652 | | | | 20,456 | |

| Centrica PLC | | | 23,148 | | | | 125,749 | |

| Compass Group PLC | | | 1,662 | | | | 19,656 | |

| Diageo PLC | | | 3,511 | | | | 102,214 | |

| GlaxoSmithKline PLC | | | 34,007 | | | | 738,346 | |

| HSBC Holdings PLC | | | 12,924 | | | | 136,695 | |

| Imperial Tobacco Group PLC | | | 1,507 | | | | 58,193 | |

| Inmarsat PLC | | | 3,673 | | | | 35,456 | |

| International Consolidated Airlines Group SA* | | | 16,625 | | | | 49,133 | |

| Kingfisher PLC | | | 7,038 | | | | 32,508 | |

| Lloyds Banking Group PLC* | | | 35,330 | | | | 28,309 | |

| Marks & Spencer Group PLC | | | 6,157 | | | | 38,387 | |

| National Grid PLC | | | 14,501 | | | | 166,101 | |

| Pearson PLC | | | 2,051 | | | | 40,096 | |

| Reckitt Benckiser Group PLC | | | 814 | | | | 50,992 | |