UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05010

Mutual Fund and Variable Insurance Trust

(Exact name of registrant as specified in charter)

2960 North Meridian Street, Suite 300

Attn: Mutual Fund and Variable Insurance Trust Officer

Indianapolis, IN 46208

(Address of principal executive offices) (Zip code)

Martin R. Dean

The Huntington National Bank

37 West Broad Street, 6th Floor

Columbus, OH 43215

(Name and address of agent for service)

Copies to:

Andrew Davalla

Thompson Hine LLP

41 South High Street

Suite 1700

Columbus, Oh 43215

Registrant’s telephone number, including area code: 1-800-253-0412

Date of fiscal year end: December 31

Date of reporting period: December 31, 2015

| Item 1. | Reports to Stockholders. |

Annual Shareholder Report

DECEMBER 31, 2015

CLASS A SHARES

CLASS C SHARES

INSTITUTIONAL SHARES

Annual Shareholder Report

EQUITY FUNDS

Rational Dividend Capture Fund (formerly Huntington Dividend Capture Fund)

Rational Risk Managed Emerging Markets Fund (formerly Huntington Global Select Markets Fund)

Rational Real Strategies Fund (formerly Huntington Real Strategies Fund)

Rational Defensive Growth Fund (formerly Huntington Situs Fund)

ASSET ALLOCATION FUNDS

Rational Strategic Allocation Fund (formerly Huntington Balanced Allocation Fund)

| | |

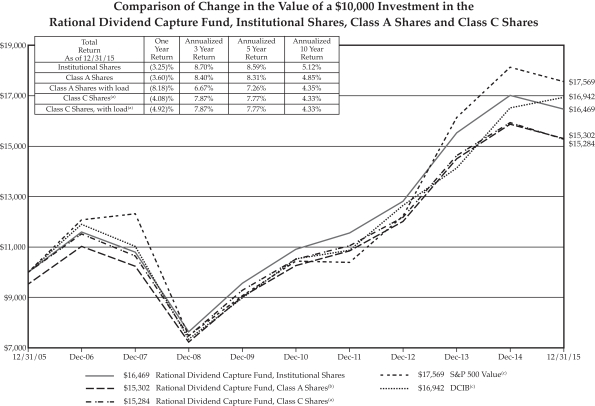

| Rational Dividend Capture Fund | | As of December 31, 2015 |

| | |

| (formerly Huntington Dividend Capture Fund) | | |

Management’s Discussion of Fund Performance

Portfolio Managers:

Kirk Mentzer, MBA

Director of Fund Research

Peter Sorrentino, CFA

Senior Vice President

PERFORMANCE SUMMARY

For the fiscal year ended December 31, 2015, the Rational Dividend Capture Fund’s (the “Fund”) Institutional Shares, Class A Shares and Class C Shares produced total returns (not including the deduction of applicable sales charges) of -3.25%, -3.60% and -4.08%, respectively, based on net asset value. The Fund underperformed relative to the -3.15% total return of the Standard & Poor’s 500 Value Index® (“S&P 500 Value”)(a), its benchmark by -0.45% (A Shares). The Fund underperformed relative to the +2.53% total return of the Dividend Capture Indices Blend (“DCIB”)(b) for the same period.

RECENT FUND ACTION

With valuations at extended levels, profit weakness, sluggish global economic growth trends, and uncertain Federal Reserve (“Fed”) action, we continued to advocate muted cyclical exposure within portfolios. Corporations in aggregate issued a tremendous amount of debt in 2015 and corporate bond risk spreads have widened to reflect the higher risk of default as profit margins, growth, and economic growth have slowed. Continuing a theme that began last year, attempting to de-risk portfolios while maintaining allocations was the balance we struck as a theme for 2015. Sluggish global economic growth did not offer much hope of a robust rebound in activity on the horizon. Below are three recent industry changes:

| | • | | Leisure Products was an area that had severely underperformed over the past year. The industry is domestically focused, which dodges the currency issues negatively impacting so many other groups. Input prices were favorable and translating into improving margins. Valuation was fair, but could allow for upside surprises due to depressed earnings expectations. Balance sheet quality was good as debt levels have been contained. A recession or rising input costs are the two largest potential detractors from the performance of this area. We raised the group to attractive. |

| | • | | Banks vs Real Estate Investment Trusts (“REITs”): While banks have been major beneficiaries of the anticipated Fed tightening, REITs shares have conversely suffered. In the medium term, economic conditions are expected to weaken due to a stronger dollar and slower world growth, and will ultimately weigh on Commercial & Industrial loan quality. Thus, the banks are put on downgrade watch. Following the Fed rate increase in December 2015, REIT shares rebounded thanks to relief that the adjustment was made and additional Fed increases were expected to be mild. This improving monetary environment for REIT shares could result in positive earnings and multiple expansions. |

| | • | | Restaurants had reasonable profit growth expectations and performance has been excellent. However, the outlook was getting less appealing. Market turmoil and weak wage growth may result in weaker sales trends in the future. Trade surveys already signal a trend change. Surprisingly, about half of the industry sales are international. Currency trends continue to work against multinationals, especially for those with emerging markets exposure. We moved the restaurant group from attractive to neutral. |

ATTRIBUTION HIGHLIGHTS

The Fund was managed using our top-down style and portfolio construction techniques, which are aimed at producing a high level of stable income and low volatility by investing in three distinct asset classes: common stocks, REITs, and preferred stocks.

| | • | | Value-style common stocks: Domestic equity market returns were range bound for much of the year as weak earnings growth and uncertainty regarding the direction of Fed monetary policy took their toll on |

Annual Shareholder Report

1

Rational Dividend Capture Fund (Continued)

| | investor confidence. Stocks as measured by the S&P 500 Value ended the year with a -3.15% total return. The Fund was overweight common stocks for the entire period versus the DCIB unmanaged custom index. Within this class, sector allocation subtracted 48 basis points and security selection detracted 200 basis points. As a result, the common stocks in the Fund underperformed the overall market. The Fund’s common stock total return for 2015 was -5.17% compared to the S&P 500 Value of -3.15%. The five largest positive contributors to performance were: General Electric Company (+0.86%), Coca-Cola Enterprises (+0.38%), McDonald’s Corporation (+0.33%), Halliburton Company (+0.28%), and Old Republic International Corporation (+0.25%). The five largest detractors were: Waddell & Reed Financial (-1.00%), Tyco International PLC (-0.57%), Noble Corporation plc (-0.58%), Bank of Nova Scotia (-0.53%) and ConocoPhillips (-0.51%). |

| | • | | REIT’s(c): Flat interest rate trends and mild inflation pressures helped propel REIT markets in 2015. However, the Fund’s REIT holdings produced a total return of -6.67%, which compared unfavorably to the benchmark Standard & Poor’s Supercomposite 1500 Real Estate Investment Trusts Industry Index® (“S&P REIT”)(C) total return of +3.80%. The five largest positive contributors to performance were: Camden Property Trust (+1.09%), Medical Properties Trust (+0.77%), Realty Income Corporation (+0.61%), Kimco Realty (+0.49%), and Piedmont Office Realty Trust (+0.33%). The five largest detractors were: Host Hotels & Resorts (-5.12%), Lexington Realty Trust (-3.28%), Hospitality Properties Trust (-2.13%), HCP, Inc. (-1.14%), and Weyerhaeuser Company (-0.61%). |

| | • | | Preferred Stock(d): A largely range-bound bond market and investors’ search for yield gave preferred stocks a tail wind for the year, making them the best performing asset class of the Fund. The Fund’s preferred share holdings produced a total return of 5.81% which underperformed the benchmark BofA Merrill Lynch U.S. Preferred Stock Fixed Rate Index total return of +7.58%. The five largest positive contributors to performance were: Northern Trust Corp 5.85 % Non-Cumulative Perpetual Preferred (+9.95%), Realty Income Corp 6.63% Preferred Series F (+7.87%), PS Business Parks 6.45 % Preferred Shares Series S (+7.75%), PartnerRe Ltd 7.25% Preferred Shares Series E (+7.19%), and Axis Capital Holdings Ltd 6.88% Preferred Shares Series C (+6.96%). The five largest underperforming issues were: Aegon NV 8% Notes (+2.44%), Senior Housing Properties Trust 5.63% Notes (+1.79%), American Financial Group 7% Notes (+1.36%), Goldman Sachs Group 6.2% Series B (+0.14%), and JPMorgan Chase Capital XXIX 6.7% Capital Series CC (+0.00%). |

| (a) | The S&P 500 Value Index® is an unmanaged market-capitalization-weighted index consisting of those stocks within the S&P 500 Index® that exhibit strong value characteristics. It uses a numerical ranking system based on four value factors and three growth factors to determine the constituents and their weightings. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

| (b) | The DCIB is a custom, blended index comprised of the following three indices with their noted respective weightings: S&P 500 Value Index (40%), Merrill Lynch Fixed Rate Preferred Index (40%) and S&P REIT (20%). This custom, blended index and its respective weightings are reflective of the Fund’s sector diversification. Indices are unmanaged and, unlike the Fund, are not affected by cash flows. It is not possible to invest directly in an Index. |

| (c) | REIT returns represented by the S&P REIT. The S&P REIT is a capitalization-weighted index of the 91 REIT stocks within the S&P 1500 Composite Index®. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

| (d) | Preferred returns represented by BofA Merrill Lynch U.S. Preferred Stock Fixed Rate Index. The BofA Merrill Lynch Fixed Rate Preferred Securities Index is a capitalization-weighted index that tracks the performance of fixed rate U.S. dollar denominated preferred securities issued in the U.S. domestic market. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

This commentary may include statements that constitute “forward looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of the Huntington Asset Advisors, Inc. (the “Advisor”) as of December 31, 2015 and are subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. If these additional fees were reflected, performance would have been lower.

There are no guarantees that dividend paying stocks will continue to pay dividends. In addition, dividend paying stocks may not experience the same capital appreciation potential as non-dividend paying stocks.

Annual Shareholder Report

2

Rational Dividend Capture Fund (Continued)

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end or after-tax returns may be obtained by calling 1-800-253-0412. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured. Total returns, with load, include the 4.75% maximum sales charge for the Class A Shares or the 1.00% maximum deferred sales charge for the Class C Shares.

| | | | | | | | |

| Class | | Gross

Expense Ratios | | | Net Expense Ratios | |

| Institutional Shares | | | 1.46% | | | | 0.96% | |

| Class A Shares | | | 1.71% | | | | 1.21% | |

| Class C Shares | | | 2.21% | | | | 1.71% | |

The above expense ratios are from the Fund’s prospectus dated April 30, 2015. Additional information pertaining to the Fund’s expense ratios as of December 31, 2015 can be found in the financial highlights.

The Fund’s performance assumes the reinvestment of all dividends and distributions on securities. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. The S&P 500 Value and DCIB have been adjusted to reflect reinvestment of dividends on securities in the indices.

Investments in real estate investment trusts (“REITs”) and real-estate related securities involves special risks associated with an investment in real estate, such as limited liquidity and interest rate risks and may be more volatile than other securities. In addition, the value of REITs and other real estate-related investments is sensitive to changes in real estate values, extended vacancies of properties and other environmental and economic factors.

There are no guarantees that dividend paying stocks will continue to pay dividends. In addition, dividend paying stocks may not experience the same capital appreciation potential as non-dividend paying stocks.

Up through December 31, 2015 the Fund was distributed by Unified Financial Securities, LLC (Member FINRA).

| (a) | Class C Shares commenced operations on January 3, 2014. Prior to January 3, 2014, performance is based on the performance of Class A Shares adjusted for the Class C Shares 12b-1 fees and contingent deferred sales charge. |

| (b) | Represents a hypothetical investment of $10,000 in the Fund after deducting the maximum sales load of 4.75% ($10,000 investment minus $475 sales load = $9,525). |

| (c) | The S&P 500 Value and DCIB are not adjusted to reflect sales charges, expenses, or other fees that are reflected in the Fund’s performance. The indices are unmanaged and, unlike the Fund, are not affected by cash flows. It is not possible to invest directly in an index. |

Annual Shareholder Report

3

| | |

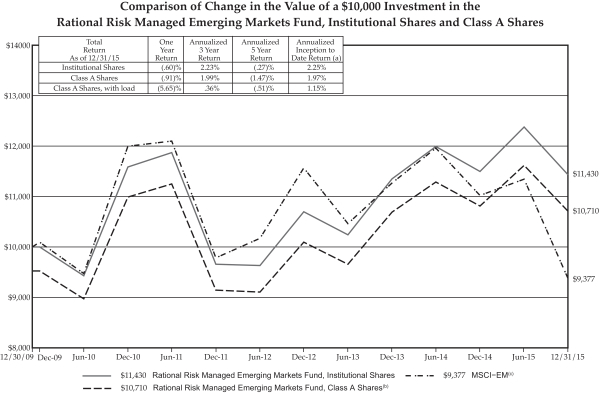

| Rational Risk Managed Emerging Markets Fund | | As of December 31, 2015 |

| | |

| (formerly Huntington Global Select Markets Fund) | | |

Management’s Discussion of Fund Performance

Portfolio Manager:

Paul W. Attwood, CFA

Senior Vice President

PERFORMANCE SUMMARY

For the fiscal year ended December 31, 2015, the Rational Risk Managed Emerging Markets Fund’s (the “Fund”) Institutional Shares and Class A Shares produced total returns (not including the deduction of applicable sales charges) of -0.60% and -0.91%, respectively, based on net asset value. The Fund outperformed relative to the -14.92% total return of the Morgan Stanley Capital International Emerging Markets Index (“MSCI-EM”)(a), its benchmark for the same time period. The Fund’s Class A Shares outperformed its benchmark by +14.01%.

ATTRIBUTION HIGHLIGHTS

The MSCI-EM Index had a weak showing in 2015. Some of the index members, such as Brazil, had enormous declines in both their equity and currency markets. China started the year on a strong note with the Shanghai composite rallying over 40% by June. However, as the concern over an economic downturn increased, equity prices sold off and, while still positive, they have lost a significant amount of value during the third and fourth quarter. The overweight in India and underweight in the above mentioned areas assisted with the funds relative performance.

Due to the decline in commodity prices, specifically Materials and Energy, these stocks were the weakest performing areas. The fund was significantly underweight these areas during 2015. The Fund’s relative overweighted positions were in Technology and Healthcare. Stock selection added to the relative outperformance of the Fund.

The holdings that had the largest positive contribution to the Fund’s performance were KCE Electronics, a manufacturing company in Thailand and the Fund’s holdings in Japan. Specifically, Welcia Holdings, a company involved in the management of drug store chains; and Keyence Corp., a manufacturing company involved in factory automation and programmable logic controllers; performed well.

| (a) | The MSCI-EM is a market-capitalization weighted equity index comprising 21 of the 48 countries in the MSCI universe. Each MSCI country index is created separately, then aggregated, without change, into MSCI indices. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

This commentary may include statements that constitute “forward looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Portfolio, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of the Advisor as of December 31, 2015 and are subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. If these additional fees were reflected, performance would have been lower.

Annual Shareholder Report

4

Rational Risk Managed Emerging Markets Fund (Continued)

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end or after-tax returns may be obtained by calling 1-800-253-0412. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured. Total returns, with load, include the 4.75% maximum sales charge for the Class A Shares.

| | | | | | | | |

| Class | | Gross

Expense Ratios | | | Net Expense Ratios | |

| Institutional Shares | | | 2.26% | | | | 0.91% | |

| Class A Shares | | | 2.51% | | | | 1.16% | |

The above expense ratios are from the Fund’s prospectus dated April 30, 2015. Additional information pertaining to the Fund’s expense ratios as of December 31, 2015 can be found in the financial highlights.

The Fund’s performance assumes the reinvestment of all dividends and distributions on securities. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. The MSCI-EM has been adjusted to reflect reinvestment of dividends on securities in the index.

International investing involves special risks including currency risk, political risk, increased volatility of foreign securities, and differences in auditing and other financial standards. In addition, prices of emerging markets securities can be significantly more volatile than the prices of securities in developed countries.

Up through December 31, 2015 the Fund was distributed by Unified Financial Securities, LLC (Member FINRA).

| (a) | The Fund commenced operations for all share classes on December 30, 2009. |

| (b) | Represents a hypothetical investment of $10,000 in the Fund after deducting the maximum sales load of 4.75% ($10,000 investment minus $475 sales load = $9,525). |

| (c) | The MSCI-EM is not adjusted to reflect sales charges, expenses, or other fees that are reflected in the Fund’s performance. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an index. |

Annual Shareholder Report

5

| | |

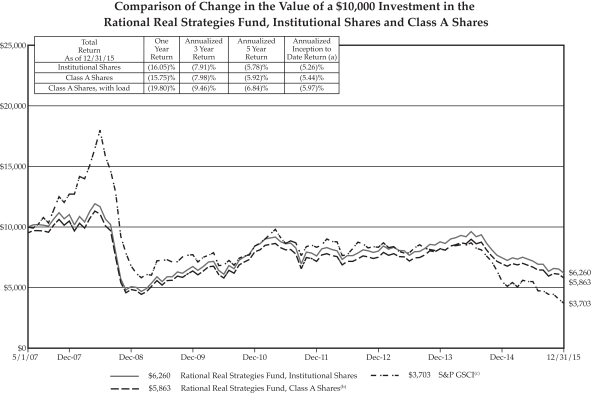

| Rational Real Strategies Fund | | As of December 31, 2015 |

| | |

| (formerly Huntington Real Strategies Fund) | | |

Management’s Discussion of Fund Performance

Portfolio Managers:

Peter Sorrentino, CFA

Senior Vice President

Paul Attwood, CFA

Senior Vice President

PERFORMANCE SUMMARY

For the fiscal year ended December 31, 2015, the Rational Real Strategies Fund’s (the “Fund”) Institutional Shares and Class A Shares produced total returns (not including the deduction of applicable sales charges) of -16.05% and -15.75%, respectively, based on net asset value. This compares to the -32.86% return of the Standard and Poor’s Goldman Sachs Commodity Index® (“S&P GSCI”)(a), the Fund’s benchmark, for the same period. The Fund’s Class A Shares outperformed the benchmark by +17.11%. The Fund outperformed its benchmark primarily due to defensive return generated through the use of covered call options and the positive return from protective put options purchased on the S&P 500 Index® and the MSCI Emerging Market ETF, along with the call options on the CBOE Volatility Index®.

RECENT FUND ACTION

The Fund reduced its exposure to Industrial Service producers during the year. The Fund also continued the shift in emphasis in the Energy sector during the year from North America energy production to pipelines and other energy transportation. Additionally, the Fund increased downside hedging during the period as indications of potential price instability continued to accumulate, and valuations appeared stretched relative to underlying commodity prices.

ATTRIBUTION HIGHLIGHTS

The Fund’s investments in listed options, including defensive hedges, delivered the strongest performance during the period. This performance came throughout the year as market conditions for energy and basic materials deteriorated. The net effective contribution for both the covered call options and defensive hedges was a positive 26.68% for the period. Investments in oil refiner Valero Energy and independent energy producer SM Energy were the largest contributors to the Fund’s performance with a net positive impact of +3.18%. These holdings represented an average weight of 5.96% of the Fund’s net assets during the year. Investments in energy service providers Kinder Morgan and Cheniere Energy were the largest detractors from the Fund’s performance with negative impacts of -3.61% and -2.78% respectively. These holdings represented an average weight of 8.63% of the Fund’s net assets during the year.

| (a) | The S&P GSCI measures general price movements and inflation in the world economy. The Index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

This commentary may include statements that constitute “forward looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Portfolio, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of the Advisor as of December 31, 2015 and are subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. If these additional fees were reflected, performance would have been lower.

Annual Shareholder Report

6

Rational Real Strategies Fund (Continued)

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end or after-tax returns may be obtained by calling 1-800-253-0412. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured. Total returns, at load, include the 4.75% maximum sales charge for the Class A Shares.

| | | | | | | | |

| Class | | Gross

Expense Ratios | | | Net Expense Ratios | |

| Institutional Shares | | | 1.63% | | | | 1.15% | |

| Class A Shares | | | 1.88% | | | | 1.40% | |

The above expense ratios are from the Fund’s prospectus dated April 30, 2015. Additional information pertaining to the Fund’s expense ratios as of December 31, 2015 can be found in the financial highlights.

The Fund’s performance assumes the reinvestment of all dividends and distributions. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. The S&P GSCI has been adjusted to reflect reinvestment of dividends on securities in the indices.

Investments in real estate investment trusts (“REITs”) and real-estate related securities involve special risks associated with an investment in real estate, such as limited liquidity and interest rate risks and may be more volatile than other securities. In addition, the value of REITs and other real estate-related investments is sensitive to changes in real estate values, extended vacancies of properties and other environmental and economic factors.

Commodities-related investments are subject to the same risks as direct investments in commodities and prices may rise and fall in response to many factors such as economic, political and regulatory developments.

Funds whose investments are concentrated in a specific industry or sector may be subject to a higher degree of market risk than funds whose investments are diversified.

Up through December 31, 2015 the Fund was distributed by Unified Financial Securities, LLC (Member FINRA).

| (a) | The Fund commenced operations for all share classes on May 2, 2007. |

| (b) | Represents a hypothetical investment of $10,000 in the Fund after deducting the maximum sales load of 4.75% ($10,000 investment minus $475 sales load = $9,525). |

| (c) | The S&P GSCI is not adjusted to reflect sales charges, expenses, or other fees are reflected in the Fund’s performance. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an index. |

Annual Shareholder Report

7

| | |

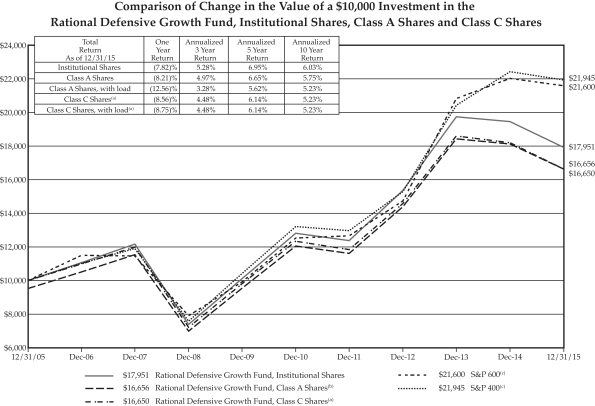

| Rational Defensive Growth Fund | | As of December 31, 2015 |

| | |

| (formerly Huntington Situs Fund) | | |

Management’s Discussion of Fund Performance

Portfolio Managers:

Kirk Mentzer, MBA

Director of Fund Research

Peter Sorrentino, CFA

Senior Vice President

PERFORMANCE SUMMARY

For the fiscal year ended December 31, 2015, the Rational Defensive Growth Fund’s (“Fund”) Institutional Shares, Class A Shares and Class C Shares produced total returns (not including the deduction of applicable sales charges) of -7.82%, -8.21% and -8.56%, respectively, based on net asset value. This compares to the -1.97% return of the Standard and Poor’s SmallCap 600 Index® (“S&P 600”)(a), the Fund’s benchmark, and the -2.18% total return of the Standard and Poor’s MidCap 400 Index® (“S&P 400”)(b), for the same period. The Fund’s Class A Shares underperformed the benchmark by 6.24%.

RECENT FUND ACTION

With valuations at extended levels, profit weakness, sluggish global economic growth trends and uncertain Federal Reserve (“Fed”) action, we continued to advocate muted cyclical exposure within portfolios. Corporations in aggregate have issued a tremendous amount of debt in 2015 and corporate bond risk spreads have widened to reflect the higher risk of default as profit margins, growth and economic growth have slowed. Continuing a theme that began last year, attempting to de-risk portfolios while maintaining allocations was the balance we struck as a theme for 2015. Sluggish global economic growth did not offer much hope of a robust rebound in activity on the horizon. Below are three recent industry changes:

| | • | | Leisure Products was an area that had severely underperformed over the past year. The industry is domestically focused, which dodges the currency issues that negatively impacted so many other groups. Input prices were favorable and translated into improved margins. Valuation was fair, but could allow for upside surprises due to depressed earnings expectations. Quality was good as debt levels have been contained. A recession or rising input costs are the two largest negatives. We raised the group to attractive. |

| | • | | Bank vs Real Estate Investment Trusts (“REITs”): While banks have been major beneficiaries of the anticipated Fed tightening, REIT shares have conversely suffered. In the medium term, economic conditions are expected to weaken due to a stronger dollar, slower world growth and will ultimately weigh on Commercial & Industrial loan quality. Thus, the banks were put on downgrade watch. Following the Fed rate increase in December 2015, REIT shares rebounded thanks to relief that the adjustment was made and additional increases were expected to be mild. This improving monetary environment for REIT shares could result in positive earnings and multiple expansions. |

| | • | | Restaurants had reasonable profit growth expectations and performance had been excellent, however, the outlook was getting less appealing. Market turmoil and weak wage growth may result in weaker sales trends in the future. Trade surveys already signal a trend change. Surprisingly, about half of the industry sales are international. Currency trends continue to work against multinationals, especially for those with emerging markets exposure. We moved the restaurant group from attractive to neutral. |

Annual Shareholder Report

8

Rational Defensive Growth Fund (Continued)

ATTRIBUTION HIGHLIGHTS

Domestic small cap equity markets experienced a sharp decline in late summer, followed by a rebound in the fourth quarter that produced a +0.27% total return for the year as measured by the S&P 600. The Fund underperformed due to sector allocation and security selection. Specifically, sector allocation detracted 0.85% and security selection subtracted -1.56%. The best relative performing sectors were Financials, Health Care and Materials. The worst relative performing sectors were Energy, Industrials and Technology.

The five largest positive contributors to performance were: Myriad Genetics +1.08%, Tyler Technologies +0.90%, Amsurg Corp. +0.71%, Arch Capital Group Ltd. +0.52%, and Tractor Supply Company +0.48%. The five largest detractors were: Geospace Technologies Corporation -2.20%, United States Lime & Minerals -1.16%, Companhia Brasileira de Distribuicao Sponsored ADR -0.84%, Osiris Therapeutics -0.73%, and Flowserve Corporation -0.66%.

Portfolio Risk:

During the year, overall portfolio risk was lowered significantly as measured by the Northfield system. Average market capitalization declined from $5.1 billion to $2.6 billion. Price-to-earnings and price-to-book improved (fell) over 31% and 23%, respectively. Total- and benchmark-risk were both lowered 12.2%. Predicted tracking error fell nearly 25% to 3.77. These adjustments were made to guard against increased market volatility.

| (a) | The S&P 600 is a capitalization-weighted index representing all major industries in the small-cap range of the U.S. stock market. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

| (b) | The S&P 400 is a capitalization-weighted index comprised of common stocks representing all major industries in the mid-range of the U.S. stock market. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

This commentary may include statements that constitute “forward looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of the Advisor as of December 31, 2015 and are subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. If these additional fees were reflected, performance would have been lower.

Annual Shareholder Report

9

Rational Defensive Growth Fund (Continued)

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end or after-tax returns may be obtained by calling 1-800-253-0412. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured. Total returns, with load, include the 4.75% maximum sales charge for the Class A Shares or the 1.00% maximum deferred sales charge for the Class C Shares.

| | | | | | | | |

| Class | | Gross

Expense Ratios | | | Net Expense Ratios | |

| Institutional Shares | | | 1.37% | | | | 1.03% | |

| Class A Shares | | | 1.62% | | | | 1.28% | |

| Class C Shares | | | 2.12% | | | | 1.78% | |

The above expense ratios are from the Fund’s prospectus dated April 30, 2015. Additional information pertaining to the Fund’s expense ratios as of December 31, 2015 can be found in the financial highlights.

The Fund’s performance assumes the reinvestment of all dividends and distributions. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. The S&P 600 and S&P 400 have been adjusted to reflect reinvestment of dividends on securities in the indices.

Small company stocks may be less liquid and subject to greater price volatility than large capitalization stocks.

Funds whose investments are concentrated in a specific industry or sector may be subject to a higher degree of market risk than funds whose investments are diversified. In addition, the Fund may be subject to specific risks of the information technology sector, such as obsolescence.

Up through December 31, 2015 the Fund was distributed by Unified Financial Securities, LLC (Member FINRA).

| (a) | Class C Shares commenced operations on January 3, 2014. Prior to January 3, 2014, performance is based on the performance of Class A Shares adjusted for the Class C Shares’ 12b-1 fees and contingent deferred sales charge. |

| (b) | Represents a hypothetical investment of $10,000 in the Fund after deducting the maximum sales load of 4.75% ($10,000 investment minus $475 sales load = $9,525). |

| (c) | The S&P 600 and S&P 400 are not adjusted to reflect sales charges, expenses, or other fees that are reflected in the Fund’s performance. The indices are unmanaged and, unlike the Fund, are not affected by cash flows. It is not possible to invest directly in an index. |

Annual Shareholder Report

10

| | |

| Rational Strategic Allocation Fund | | As of December 31, 2015 |

| | |

| (formerly Huntington Balanced Allocation Fund) | | |

Management’s Discussion of Fund Performance

Portfolio Managers:

Kirk Mentzer, MBA

Director of Fund Research

Peter Sorrentino, CFA

Senior Vice President

PERFORMANCE SUMMARY

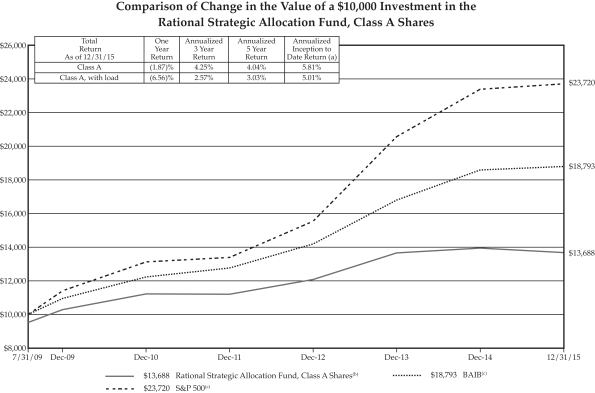

For the fiscal year ended December 31, 2015, the Rational Strategic Allocation Fund’s (the “Fund”) Class A Shares reported a total return (not including the deduction of applicable sales charges) of -1.87% based on net asset value. The Fund underperformed relative to the +1.38% return of the Standard & Poor’s 500® Index (“S&P 500”), its benchmark. The Fund’s Class A Shares underperformed its benchmark by 3.25%. The Fund underperformed relative to the +1.05% total return of the Balanced Allocation Indices Blend (“BAIB”) for the same period. Contributing to the underperformance was the allocation of the Fund’s net assets of 60% in equity funds, 33% in fixed income funds and 7% in money market fund assets.

FUND ALLOCATION

Overall, the Fund was extremely diversified across asset classes and reflected the market expectations of Huntington Asset Advisors, Inc. During the fourth quarter, we attempted to reduce risk exposure away from equity markets towards fixed income in light of our views for the economic environment for the remainder of 2015 and looking ahead to 2016.

Despite the Federal Reserve (the “Fed”) rate hike in December, we believe concerns about global economic growth will likely slow further tightening episodes. Weak growth in Chinese and emerging market economies have resulted in a strong U.S. dollar, commodity price declines, and weakening profit growth trends. Unless there is an upturn in the emerging markets business cycle that serves to reverse these trajectories, we do not expect the Fed to tighten monetary policy significantly 2016.

What are the implications for financial markets? The era of unprecedented monetary accommodation on a global scale has been a major driver of higher stock prices yet economic growth remains sluggish. Removing excess monetary stimulus in the future will be challenging. Furthermore, global sales per share have collapsed for all but the U.S., which has been supported by relatively better GDP growth and share repurchases. However, the U.S. is not an economic island. In a world of too much debt and over capacity, a sudden reversal upward is highly unlikely. Rising corporate bond spreads and volatility measures further confirm the earnings concerns. Downward pressure on earnings remains a major risk for corporate valuations (both bonds and stocks).

Protecting asset values has been a prevalent theme all year. We sought to maintain conservative domestic equity asset allocation in large market capitalized funds that favor defensive sector/industry allocation, lower beta, and high quality bias. Defensive groups are now clearly emphasized in our strategy due to market risks and stretched valuation levels. In terms of fixed income fund emphasis, our allocations shifted towards lower interest rate and credit risk during the fourth quarter which was consistent with our overall market views.

Annual Shareholder Report

11

Rational Strategic Allocation Fund (Continued)

ATTRIBUTION HIGHLIGHTS

| | • | | The Rational Dividend Capture, the Fund’s largest equity holding (13.3% of the Fund’s net assets at the end of the year) reported a total return of -3.25% and underperformed the +1.38% return of the S&P 500. |

| | • | | The second largest equity fund holding, the U.S. Equity Rotation Strategy ETF gained +2.49%. The remaining fund performances included: EcoLogical Strategy ETF gained +0.96%; the Rational Risk Managed Emerging Markets Fund lost -0.60%; and finally, the Rational Defensive Growth Fund lost -7.82%. These holdings represented 12.4%(c), 12.2%(c), 12.1%(c) and 10.2%(c) of the Fund’s net assets at the end of the year, respectively. |

| | • | | The Fund’s fixed income allocation included the Federated Short & Intermediate Bond Fund, the Federated Total Return Bond Fund and the Federated Mortgage Fund (16.0%(c), 9.0%(c) and 8.0%(c) of the Fund’s net assets at the end of the year, respectively). All three gained in performance as interest rates stayed range bound for much of the year. |

| | • | | The largest detractor to the Fund’s performance was its holding in the Rational Defensive Growth Fund, which declined by -7.82% as small cap markets adjusted to lower expected growth and higher anticipated interest rates. However, we believe this Fund provides a significant upside potential in the equity markets in the event that the investment environment changes in the near future. |

| (a) | The S&P 500 is a capitalization-weighted index comprised of 500 stocks and designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

| (b) | The Balanced Allocation Indices Blended Benchmark is a custom blended index comprised of the following two indices with their noted respective weightings: S&P 500 (60%) and the Barclays U.S. Aggregate Bond Index (40%). The Barclays U.S. Aggregate Bond Index is comprised of securities from the Barclays Government/Corporate Bond Index, Mortgage Securities Index and the Asset Based Index. Total return comprises price appreciation/depreciation and income as a percentage of the original investment. Indices are rebalanced monthly by market capitalization. The index is unmanaged and, unlike the Fund, is not affected by cash flows. It is not possible to invest directly in an Index. |

| (c) | Percentage of holdings based on Fund’s net assets as of 12/31/2015. The composition of the Fund’s holdings is subject to change. |

This commentary may include statements that constitute “forward looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Fund, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are those of the Advisor as of December 31, 2015 and are subject to change at any time based upon economic, market, or other conditions and the Advisor undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Fund’s trading intent. Information about the Fund’s holdings, asset allocation or country diversification is historical and is not an indication of future Fund composition, which may vary.

The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. If these additional fees were reflected, performance would have been lower.

Annual Shareholder Report

12

Rational Strategic Allocation Fund (Continued)

The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end or after-tax returns may be obtained by calling 1-800-253-0412. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Mutual funds are not obligations of or guaranteed by any bank and are not federally insured. Total returns, at load, include the 4.75% maximum sales charge for the Class A Shares.

| | | | | | | | |

| Class | | Gross

Expense Ratio | | | Net Expense Ratio | |

| Class A Shares | | | 1.82% | | | | 1.56% | |

The above expense ratio is from the Fund’s prospectus dated April 30, 2015. Additional information pertaining to the Fund’s expense ratio as of December 31, 2015 can be found in the financial highlights.

The Fund’s performance assumes the reinvestment of all dividends and distributions on securities. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. The S&P 500 and BAIB have been adjusted to reflect reinvestment of dividends on securities in the indices.

Up through December 31, 2015 the Fund was distributed by Unified Financial Securities, LLC (Member FINRA).

| (a) | The Fund commenced operations on July 31, 2009. |

| (b) | Represents a hypothetical investment of $10,000 in the Fund after deducting the maximum sales load of 4.75% ($10,000 investment minus $475 sales load = $9,525). |

| (c) | The S&P 500 and BAIB are not adjusted to reflect sales charges, expenses, or other fees that are reflected in the Fund’s performance. The indices are unmanaged and, unlike the Fund, are not affected by cash flows. It is not possible to invest directly in an index. |

Annual Shareholder Report

13

| | |

| Rational Dividend Capture Fund | | December 31, 2015 |

| | |

| Portfolio of Investments Summary Table | | (unaudited) |

| | | | |

| Asset Allocation | | Percentage of

Market Value | |

Financials | | | 32.8% | |

Real Estate Investment Trusts | | | 13.7% | |

Health Care | | | 7.8% | |

Energy | | | 7.5% | |

Short-Term Securities Held as Collateral for Securities Lending | | | 7.2% | |

Consumer Staples | | | 6.8% | |

Industrials | | | 5.7% | |

Information Technology | | | 4.7% | |

Utilities | | | 3.8% | |

Consumer Discretionary | | | 2.9% | |

Telecommunication Services | | | 2.3% | |

Cash | | | 2.3% | |

Materials | | | 1.7% | |

Exchange-Traded Funds | | | 0.8% | |

Total | | | 100.0% | |

Portfolio holdings and allocations are subject to change. As of December 31, 2015, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth below in the Portfolio of Investments which are computed using the Fund’s net assets.

The Portfolio of Investments Summary Table and the Portfolio of Investments are broken down by sectors, and these sectors do not represent industry categories for purposes of identifying “industry concentration” as described in the Investment Company Act of 1940, as amended.

Portfolio of Investments

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — 73.4% | | | | | | |

| Consumer Discretionary — 3.1% | | | | | | |

| | 22,000 | | | General Motors Co. | | $ | 748,220 | | | |

| | 18,000 | | | Johnson Controls, Inc. | | | 710,820 | | | |

| | 14,250 | | | Polaris Industries, Inc. | | | 1,224,787 | | | |

| | 6,250 | | | Starwood Hotels & Resorts Worldwide, Inc. | | | 433,000 | | | |

| | | | | | | | 3,116,827 | | | |

| Consumer Staples — 7.5% | | | | | | |

| | 31,500 | | | Coca-Cola Co./The | | | 1,353,240 | | | |

| | 20,000 | | | Colgate-Palmolive Co. | | | 1,332,400 | | | |

| | 9,000 | | | Kellogg Co. | | | 650,430 | | | |

| | 5,500 | | | Kimberly-Clark Corp. | | | 700,150 | | | |

| | 15,000 | | | PepsiCo, Inc. | | | 1,498,800 | | | |

| | 7,750 | | | Philip Morris International, Inc. | | | 681,303 | | | |

| | 20,000 | | | Wal-Mart Stores, Inc. | | | 1,226,000 | | | |

| | | | | | | | 7,442,323 | | | |

| Energy — 8.2% | | | | | | |

| | 16,750 | | | Chevron Corp. | | | 1,506,830 | | | |

| | 23,250 | | | ConocoPhillips | | | 1,085,543 | | | |

| | 39,750 | | | Exxon Mobil Corp. | | | 3,098,512 | | | |

| | 10,000 | | | Helmerich & Payne, Inc. (a) | | | 535,500 | | | |

| | 15,250 | | | Murphy Oil Corp. | | | 342,363 | | | |

| | 105,000 | | | Noble Corp. PLC (a) | | | 1,107,750 | | | |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Energy — (Continued) | | | | | | |

| | 7,000 | | | Occidental Petroleum Corp. | | $ | 473,270 | | | |

| | | | | | | | 8,149,768 | | | |

| Financials — 16.9% | | | | | | |

| | 274,500 | | | Apollo Investment Corp. (b) | | | 1,432,890 | | | |

| | 32,000 | | | Ares Capital Corp. (b) | | | 456,000 | | | |

| | 29,000 | | | Bank of Nova Scotia/The (a) | | | 1,172,760 | | | |

| | 7,250 | | | Cullen/Frost Bankers, Inc. | | | 435,000 | | | |

| | 37,500 | | | Eaton Vance Corp. (a) | | | 1,216,125 | | | |

| | 36,250 | | | Fifth Third Bancorp | | | 728,625 | | | |

| | 23,750 | | | JPMorgan Chase & Co. | | | 1,568,212 | | | |

| | 132,000 | | | KeyCorp. | | | 1,741,080 | | | |

| | 8,500 | | | PNC Financial Services Group, Inc./The | | | 810,135 | | | |

| | 1,029 | | | RMR Group, Inc./The, Class A * | | | 14,831 | | | |

| | 22,000 | | | Royal Bank of Canada | | | 1,178,760 | | | |

| | 14,500 | | | SunTrust Banks, Inc. | | | 621,180 | | | |

| | 5,250 | | | Travelers Cos., Inc./The | | | 592,515 | | | |

| | 36,100 | | | U.S. Bancorp. | | | 1,540,387 | | | |

| | 24,000 | | | Umpqua Holdings Corp. | | | 381,600 | | | |

| | 38,250 | | | Waddell & Reed Financial, Inc., Class A | | | 1,096,245 | | | |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

14

| | |

| Rational Dividend Capture Fund | | (Continued) |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Financials — (Continued) | | | | | | |

| | 33,850 | | | Wells Fargo & Co. | | $ | 1,840,086 | | | |

| | | | | | | | 16,826,431 | | | |

| Health Care — 8.5% | | | | | | |

| | 9,000 | | | Abbott Laboratories | | | 404,190 | | | |

| | 11,000 | | | AbbVie, Inc. | | | 651,640 | | | |

| | 18,250 | | | GlaxoSmithKline PLC ADR | | | 736,388 | | | |

| | 7,750 | | | Johnson & Johnson | | | 796,080 | | | |

| | 38,250 | | | Merck & Co., Inc. | | | 2,020,365 | | | |

| | 74,000 | | | Pfizer, Inc. | | | 2,388,720 | | | |

| | 14,500 | | | St. Jude Medical, Inc. | | | 895,665 | | | |

| | 6,000 | | | Stryker Corp. | | | 557,640 | | | |

| | | | | | | | 8,450,688 | | | |

| Industrials — 6.2% | | | | | | |

| | 2,500 | | | 3M Co. | | | 376,600 | | | |

| | 19,000 | | | ADT Corp./The (a) | | | 626,620 | | | |

| | 44,250 | | | CSX Corp. | | | 1,148,287 | | | |

| | 18,250 | | | Deluxe Corp. | | | 995,355 | | | |

| | 42,000 | | | General Electric Co. | | | 1,308,300 | | | |

| | 15,000 | | | Hillenbrand, Inc. | | | 444,450 | | | |

| | 40,750 | | | Tyco International PLC | | | 1,299,517 | | | |

| | | | | | | | 6,199,129 | | | |

| Information Technology — 5.1% | | | | | | |

| | 9,000 | | | CA, Inc. | | | 257,040 | | | |

| | 30,000 | | | Cisco Systems, Inc. | | | 814,650 | | | |

| | 23,250 | | | Intel Corp. | | | 800,963 | | | |

| | 7,500 | | | International Business Machines Corp. | | | 1,032,150 | | | |

| | 1,750 | | | Microchip Technology, Inc. (a) | | | 81,445 | | | |

| | 7,500 | | | Paychex, Inc. | | | 396,675 | | | |

| | 37,250 | | | Symantec Corp. | | | 782,250 | | | |

| | 92,000 | | | Xerox Corp. | | | 977,960 | | | |

| | | | | | | | 5,143,133 | | | |

| Materials — 1.9% | | | | | | |

| | 10,500 | | | Packaging Corporation of America | | | 662,025 | | | |

| | 29,250 | | | Sonoco Products Co. | | | 1,195,447 | | | |

| | | | | | | | 1,857,472 | | | |

| Real Estate Investment Trusts — 9.4% | | | | | | |

| | 20,750 | | | Camden Property Trust (a) | | | 1,592,770 | | | |

| | 48,000 | | | HCP, Inc. | | | 1,835,520 | | | |

| | 4,000 | | | Highwoods Properties, Inc. | | | 174,400 | | | |

| | 43,000 | | | Hospitality Properties Trust | | | 1,124,450 | | | |

| | 111,750 | | | Host Hotels & Resorts, Inc. | | | 1,714,245 | | | |

| | 194,000 | | | Lexington Realty Trust | | | 1,552,000 | | | |

| | 7,500 | | | Realty Income Corp. (a) | | | 387,225 | | | |

| | 9,000 | | | Tanger Factory Outlet Centers, Inc. | | | 294,300 | | | |

| | 12,250 | | | Ventas, Inc. | | | 691,268 | | | |

| | | | | | | | 9,366,178 | | | |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Telecommunication Services — 2.5% | | | | | | |

| | 31,000 | | | AT&T, Inc. | | $ | 1,066,710 | | | |

| | 32,000 | | | Verizon Communications, Inc. | | | 1,479,040 | | | |

| | | | | | | | 2,545,750 | | | |

| Utilities — 4.1% | | | | | | |

| | 62,000 | | | CenterPoint Energy, Inc. | | | 1,138,320 | | | |

| | 7,250 | | | Entergy Corp. | | | 495,610 | | | |

| | 45,250 | | | Exelon Corp. | | | 1,256,592 | | | |

| | 11,000 | | | National Fuel Gas Co. | | | 470,250 | | | |

| | 22,000 | | | TransCanada Corp. | | | 716,980 | | | |

| | | | | | | | 4,077,752 | | | |

| Total Common Stocks (Cost $77,313,818) | | | 73,175,451 | | | |

| Preferred Stocks — 24.5% | | | | | | |

| Financials — 19.0% | | | | | | |

| | 61,000 | | | Aegon NV, 8.00% | | | 1,679,940 | | | |

| | 95,000 | | | Allstate Corp./The, 5.10% | | | 2,345,550 | | | |

| | 113,129 | | | Axis Capital Holdings Ltd.,

Series C, 6.88% | | | 3,034,120 | | | |

| | 135,000 | | | KKR Financial Holdings LLC, 8.38% | | | 3,573,450 | | | |

| | 100,000 | | | Raymond James Financial, Inc., 6.90% | | | 2,666,000 | | | |

| | 80,000 | | | U.S. Bancorp,

Series F, 6.50% | | | 2,296,000 | | | |

| | 118,000 | | | Wells Fargo & Co.,

Series J, 8.00% | | | 3,313,440 | | | |

| | | | | | | | 18,908,500 | | | |

| Real Estate Investment Trusts — 5.5% | | | | | | |

| | 10,000 | | | National Retail Properties, Inc., Series D, 6.63% | | | 260,600 | | | |

| | 80,000 | | | PS Business Parks, Inc.,

Series S, 6.45% | | | 2,106,400 | | | |

| | 60,000 | | | Public Storage, Inc.,

Series Q, 6.50% | | | 1,524,600 | | | |

| | 60,000 | | | Realty Income Corp.,

Series F, 6.63% | | | 1,589,400 | | | |

| | | | | | | | 5,481,000 | | | |

| Total Preferred Stocks (Cost $24,229,772) | | | 24,389,500 | | | |

| Exchange-Traded Funds — 0.9% | | | | | | |

| | 12,000 | | | iShares U.S. Real Estate ETF (a) | | | 901,320 | | | |

| Total Exchange-Traded Funds (Cost $912,940) | | | 901,320 | | | |

| Cash Equivalents — 2.5% | | | | | | |

| | 2,475,488 | | | Federated Treasury Obligations Fund, Institutional Class, 0.07% (c) | | | 2,475,488 | | | |

| Total Cash Equivalents (Cost $2,475,488) | | | 2,475,488 | | | |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

15

| | |

| Rational Dividend Capture Fund | | (Continued) |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Short-Term Securities Held as Collateral for

Securities Lending — 7.8% | | | | | | |

| | 7,799,288 | | | Fidelity Institutional Money Market Portfolio, Institutional Class,

0.32% (c) | | $ | 7,799,288 | | | |

| Total Short-Term Securities Held as Collateral

for Securities Lending (Cost $7,799,288) | | | 7,799,288 | | | |

| Total Investments

(Cost $112,731,306) — 109.1% | | | 108,741,047 | | | |

| Liabilities in Excess of Other Assets — (9.1)% | | | (9,044,339) | | | |

| Net Assets — 100.0% | | $ | 99,696,708 | | | |

| (a) | All or a portion of the security was on loan as of December 31, 2015. The total value of securities on loan as of December 31, 2015 was $7,565,415. |

| (b) | Business Development Company. |

| (c) | Rate disclosed is the seven day yield as of December 31, 2015. |

| * | Non-income producing security. |

ADR — American Depositary Receipt

ETF — Exchange Traded Fund

The sectors shown on the portfolio of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Asset Services, LLC.

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

16

| | |

| Rational Risk Managed Emerging Markets Fund | | December 31, 2015 |

| | |

| Portfolio of Investments Summary Table | | (unaudited) |

| | | | |

| Asset Allocation | | Percentage of

Market Value | |

Japan | | | 17.6% | |

China | | | 14.3% | |

Taiwan | | | 11.1% | |

Republic of South Korea | | | 10.2% | |

Cash | | | 7.9% | |

India | | | 7.1% | |

Malaysia | | | 6.4% | |

Indonesia | | | 6.2% | |

Hong Kong | | | 3.7% | |

United Kingdom | | | 3.4% | |

Belgium | | | 3.4% | |

France | | | 3.1% | |

Thailand | | | 2.4% | |

Mexico | | | 2.1% | |

Brazil | | | 1.1% | |

Total | | | 100.0% | |

Portfolio holdings and allocations are subject to change. As of December 31, 2015, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth below in the Portfolio of Investments which are computed using the Fund’s net assets.

The Portfolio of Investments are broken down by sectors, and these sectors do not represent industry categories for purposes of identifying “industry concentration” as described in the Investment Company Act of 1940, as amended.

Portfolio of Investments

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — 83.5% | | | | | | |

| Belgium — 3.1% | | | | | | |

| Consumer Staples — 3.1% | | | | | | |

| | 2,500 | | | Anheuser-Busch InBev SA/NV | | $ | 310,785 | | | |

| Brazil — 1.0% | | | | | | |

| Information Technology — 1.0% | | | | | | |

| | 12,000 | | | Cielo SA | | | 101,736 | | | |

| China — 13.2% | | | | | | |

| Financials — 1.8% | | | | | | |

| | 210,000 | | | Colour Life Services Group Co. Ltd. | | | 179,650 | | | |

| Industrials — 3.2% | | | | | | |

| | 960,000 | | | CT Environmental Group Ltd. | | | 314,629 | | | |

| Information Technology — 8.2% | | | | | | |

| | 3,000 | | | Alibaba Group Holding Ltd. ADR * | | | 243,810 | | | |

| | 4,000 | | | Qihoo 360 Technology Co. Ltd. ADR * | | | 291,240 | | | |

| | 14,500 | | | Tencent Holdings Ltd. | | | 285,320 | | | |

| | | | | | | | 820,370 | | | |

| | | | | | | | 1,314,649 | | | |

| France — 2.9% | | | | | | |

| Industrials — 2.9% | | | | | | |

| | 4,200 | | | Safran SA | | | 289,219 | | | |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Hong Kong — 3.5% | | | | | | |

| Health Care — 3.5% | | | | | | |

| | 378,000 | | | Sino Biopharmaceutical Ltd. | | $ | 344,343 | | | |

| India — 6.2% | | | | | | |

| Financials — 1.2% | | | | | | |

| | 7,200 | | | HDFC Bank Ltd. | | | 117,289 | | | |

| Health Care — 1.8% | | | | | | |

| | 15,000 | | | Sun Pharmaceutical Industries Ltd. | | | 185,191 | | | |

| Information Technology — 3.2% | | | | | | |

| | 3,300 | | | Tata Consultancy Services Ltd. | | | 121,054 | | | |

| | 24,800 | | | Tech Mahindra Ltd. | | | 194,745 | | | |

| | | | | | | | 315,799 | | | |

| | | | | | | | 618,279 | | | |

| Indonesia — 4.5% | | | | | | |

| Consumer Discretionary — 2.7% | | | | | | |

| | 209,000 | | | Matahari Department Store Tbk PT | | | 266,841 | | | |

| Telecommunication Services — 1.8% | | | | | | |

| | 430,000 | | | Tower Bersama Infrastructure Tbk PT | | | 183,261 | | | |

| | | | | | | | 450,102 | | | |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

17

| | |

| Rational Risk Managed Emerging Markets Fund | | (Continued) |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Japan — 16.2% | | | | | | |

| Consumer Staples — 6.9% | | | | | | |

| | 7,100 | | | Seven & i Holdings Co. Ltd. | | $ | 327,829 | | | |

| | 6,400 | | | Welcia Holdings Co. Ltd. | | | 357,804 | | | |

| | | | | | | | 685,633 | | | |

| Health Care — 2.9% | | | | | | |

| | 20,000 | | | Astellas Pharma, Inc. | | | 288,103 | | | |

| Information Technology — 6.4% | | | | | | |

| | 580 | | | KEYENCE Corp. | | | 323,680 | | | |

| | 2,200 | | | Murata Manufacturing Co. Ltd. | | | 321,581 | | | |

| | | | | | | | 645,261 | | | |

| | | | | | | | 1,618,997 | | | |

| Malaysia — 5.9% | | | | | | |

| Consumer Discretionary — 1.0% | | | | | | |

| | 210,000 | | | Berjaya Auto Bhd. | | | 104,572 | | | |

| Health Care — 2.2% | | | | | | |

| | 102,000 | | | Kossan Rubber Industries Bhd. | | | 220,733 | | | |

| Information Technology — 2.7% | | | | | | |

| | 177,000 | | | Globetronics Technology Bhd. | | | 267,714 | | | |

| | | | | | | | 593,019 | | | |

| Mexico — 1.9% | | | | | | |

| Financials — 0.7% | | | | | | |

| | 12,100 | | | Grupo Financiero Interacciones SA de CV | | | 73,376 | | | |

| Utilities — 1.2% | | | | | | |

| | 28,000 | | | Infraestructura Energetica Nova SAB de CV | | | 117,507 | | | |

| | | | | 190,883 | | | |

| Republic of South Korea — 9.4% | | | | | | |

| Consumer Staples — 3.7% | | | | | | |

| | 1,200 | | | Cosmax, Inc. | | | 187,516 | | | |

| | 200 | | | LG Household & Health Care Ltd. | | | 178,344 | | | |

| | | | | 365,860 | | | |

| Health Care — 3.1% | | | | | | |

| | 6,300 | | | InBody Co. Ltd. | | | 310,318 | | | |

| Information Technology — 2.6% | | | |

| | 3,600 | | | Koh Young Technology, Inc. | | | 118,166 | | | |

| | 5,000 | | | KONA I Co. Ltd. | | | 145,648 | | | |

| | | | | | | | 263,814 | | | |

| | | | | | | | 939,992 | | | |

| Taiwan — 10.3% | | | | | | |

| Consumer Discretionary — 4.6% | | | | | | |

| | 70,000 | | | Hota Industrial Manufacturing Co. Ltd. | | | 256,861 | | | |

| | 20,048 | | | PChome Online, Inc. | | | 200,024 | | | |

| | | | | 456,885 | | | |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Taiwan — (Continued) | | | | | | |

| Industrials — 2.3% | | | | | | |

| | 15,750 | | | Voltronic Power Technology Corp. | | $ | 233,802 | | | |

| Information Technology — 3.4% | | | | | | |

| | 59,955 | | | Adlink Technology, Inc. | | | 138,183 | | | |

| | 17,500 | | | Ennoconn Corp. | | | 197,422 | | | |

| | | | | | | | 335,605 | | | |

| | | | | | | | 1,026,292 | | | |

| Thailand — 2.2% | | | | | | |

| Information Technology — 2.2% | | | | | | |

| | 115,000 | | | KCE Electronics PCL | | | 223,425 | | | |

| United Kingdom — 3.2% | | | | | | |

| Consumer Staples — 3.2% | | | | | | |

| | 3,400 | | | Reckitt Benckiser Group PLC | | | 314,814 | | | |

| Total Common Stocks (Cost $7,065,148) | | | 8,336,535 | | | |

| Preferred Stocks — 0.4% | | | | | | |

| India — 0.4% | | | | | | |

| Consumer Discretionary — 0.4% | | | | | | |

| | 2,730,000 | | | Zee Entertainment Enterprises Ltd., 6.00% | | | 36,986 | | | |

| Total Preferred Stocks (Cost $44,695) | | | 36,986 | | | |

| Foreign Government Bonds — 1.2% | | | | | | |

| Indonesia — 1.2% | | | | | | |

| | 1,700,000,000 | | | Indonesia Treasury Bond, Series FR55,

7.38%, 9/15/16 (a) | | | 122,841 | | | |

| Total Foreign Government Bonds

(Cost $200,219) | | | 122,841 | | | |

| Cash Equivalents — 7.3% | | | | | | |

| | 724,746 | | | Federated Treasury Obligations Fund, Institutional Class,

0.07% (b) | | | 724,746 | | | |

| Total Cash Equivalents (Cost $724,746) | | | 724,746 | | | |

| Rights — 0.0% | | | | | | |

| Taiwan — 0.0% | | | | | | |

| Information Technology — 0.0% | | | | | | |

| | 3,343 | | | Adlink Technology, Inc. | | | 1,217 | | | |

| Total Rights (Cost $1,564) | | | 1,217 | | | |

| Total Investments

(Cost $8,036,372) — 92.4% | | | 9,222,325 | | | |

| Other Assets in Excess of Liabilities — 7.6% | | | 761,291 | | | |

| Net Assets — 100.0% | | $ | 9,983,616 | | | |

| (a) | Foreign-denominated security. Principal amount is reported in applicable country’s currency. |

| (b) | Rate disclosed is the seven day yield as of December 31, 2015. |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

18

| | |

| Rational Risk Managed Emerging Markets Fund | | (Continued) |

| * | Non-income producing security. |

ADR — American Depositary Receipt

The sectors shown on the portfolio of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Asset Services, LLC.

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

19

| | |

| Rational Real Strategies Fund | | December 31, 2015 |

| | |

| Portfolio of Investments Summary Table | | (unaudited) |

| | | | |

| Asset Allocation | | Percentage of

Market Value | |

Energy | | | 35.3% | |

Materials | | | 10.9% | |

Industrials | | | 11.3% | |

Cash | | | 16.0% | |

Real Estate Investments | | | 21.3% | |

Exchange-Traded Funds | | | 1.4% | |

Financials | | | 1.4% | |

Short-Term Securities Held as Collateral for Securities Lending | | | 2.4% | |

Total | | | 100.0% | |

Portfolio holdings and allocations are subject to change. As of December 31, 2015, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth below in the Portfolio of Investments which are computed using the Fund’s net assets.

The Portfolio of Investments Summary Table and the Portfolio of Investments are broken down by sectors, and these sectors do not represent industry categories for purposes of identifying “industry concentration” as described in the Investment Company Act of 1940, as amended.

Portfolio of Investments

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — 59.8% | | | | | | |

| Energy — 35.8% | | | | | | |

| | 10,100 | | | Canadian Natural Resources Ltd. | | $ | 220,483 | | | |

| | 3,800 | | | Carrizo Oil & Gas, Inc. | | | 112,404 | | | |

| | 4,800 | | | Cheniere Energy, Inc. | | | 178,800 | | | |

| | 16,510 | | | Chesapeake Energy Corp. (a) | | | 74,295 | | | |

| | 9,400 | | | Enterprise Products Partners LP | | | 240,452 | | | |

| | 6,000 | | | Halliburton Co. | | | 204,240 | | | |

| | 800 | | | Helmerich & Payne, Inc. | | | 42,840 | | | |

| | 6,200 | | | Kinder Morgan, Inc. | | | 92,504 | | | |

| | 6,000 | | | Magellan Midstream Partners LP | | | 407,520 | | | |

| | 5,600 | | | National Oilwell Varco, Inc. | | | 187,544 | | | |

| | 2,400 | | | Schlumberger Ltd. | | | 167,400 | | | |

| | 8,100 | | | Spectra Energy Corp. | | | 193,914 | | | |

| | 11,700 | | | Suncor Energy, Inc. (a) | | | 301,860 | | | |

| | 1,200 | | | Valero Energy Corp. | | | 84,852 | | | |

| | | | | 2,509,108 | | | |

| Financials — 1.4% | | | | | | |

| | 7,600 | | | Cresud SACIF y A ADR * | | | 98,040 | | | |

| Industrials — 11.5% | | | | | | |

| | 4,650 | | | AGCO Corp. | | | 211,063 | | | |

| | 6,000 | | | Chicago Bridge & Iron Co. NV (a) | | | 233,940 | | | |

| | 300 | | | Copa Holdings SA (a) | | | 14,478 | | | |

| | 5,700 | | | GATX Corp. | | | 242,535 | | | |

| | 7,600 | | | Navigator Holdings Ltd. * | | | 103,740 | | | |

| | | | | 805,756 | | | |

| Materials — 11.1% | | | | | | |

| | 1,700 | | | Agrium, Inc. | | | 151,878 | | | |

| | 600 | | | Albemarle Corp. | | | 33,606 | | | |

| | 3,800 | | | BHP Billiton Ltd. ADR (a) | | | 97,888 | | | |

| | 7,300 | | | Potash Corp of Saskatchewan, Inc. | | | 124,976 | | | |

| | 3,900 | | | Rio Tinto PLC ADR | | | 113,568 | | | |

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — (Continued) | | | | | | |

| Materials — (Continued) | | | | | | |

| | 9,800 | | | Southern Copper Corp. (a) | | $ | 255,976 | | | |

| | | | | | | | 777,892 | | | |

| Total Common Stocks (Cost $4,651,872) | | | 4,190,796 | | | |

| Exchange-Traded Funds — 1.4% | | | | | | |

| | 7,500 | | | iShares Silver Trust * | | | 98,925 | | | |

| Total Exchange-Traded Funds (Cost $116,475) | | | 98,925 | | | |

| Real Estate Investments — 21.7% (b) (c) (d) | | | | | | |

| | | | Grocery & Pharmacy DST | | | 823,108 | | | |

| | | | | New York Power DST (e) | | | 695,985 | | | |

| Total Real Estate Investments (Cost $1,791,705) | | | 1,519,093 | | | |

| Cash Equivalents — 16.3% | | | | | | |

| | 1,141,603 | | | Federated Treasury Obligations Fund, Institutional Class, 0.07% (e) | | | 1,141,603 | | | |

| Total Cash Equivalents (Cost $1,141,603) | | | 1,141,603 | | | |

| Short-Term Securities Held as Collateral for

Securities Lending — 2.4% | | | | | | |

| | 171,255 | | | Fidelity Institutional Money Market Portfolio, Institutional Class, 0.32% (f) | | | 171,255 | | | |

| Total Short-Term Securities Held as Collateral for

Securities Lending (Cost $171,255) | | | 171,255 | | | |

| Total Investments

(Cost $7,872,910) — 101.6% | | | 7,121,672 | | | |

| Liabilities in Excess of Other Assets — (1.6)% | | | (110,215) | | | |

| Net Assets — 100.0% | | $ | 7,011,457 | | | |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

20

| | |

| Rational Real Strategies Fund | | (Continued) |

| (a) | All or a portion of the security was on loan as of December 31, 2015. The total value of securities on loan as of December 31, 2015 was $167,548. |

| (c) | Investments do not offer shares. Fair value represents direct ownership of Real Estate. |

| (d) | Security is currently being valued by the Pricing Committee according to the fair value procedures approved by the Board of Trustees. |

| (e) | Investment in affiliate. |

| (f) | Rate disclosed is the seven day yield as of December 31, 2015. |

| * | Non-income producing security. |

ADR — American Depositary Receipt

DST — Delaware Statutory Trust

The sectors shown on the portfolio of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Asset Services, LLC.

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report

21

| | |

| Rational Defensive Growth Fund | | December 31, 2015 |

| | |

| Portfolio of Investments Summary Table | | (unaudited) |

| | | | |

| Asset Allocation | | Percentage of

Market Value | |

Financials | | | 17.3% | |

Information Technology | | | 13.3% | |

Short-Term Securities Held as Collateral for Securities Lending | | | 12.6% | |

Industrials | | | 11.9% | |

Health Care | | | 11.5% | |

Exchange-Traded Funds | | | 7.6% | |

Consumer Discretionary | | | 7.1% | |

Cash | | | 5.8% | |

Utilities | | | 4.0% | |

Materials | | | 2.8% | |

Consumer Staples | | | 2.6% | |

Energy | | | 1.9% | |

Real Estate Investment Trusts | | | 1.3% | |

Telecommunication Services | | | 0.3% | |

Total | | | 100.0% | |

Portfolio holdings and allocations are subject to change. As of December 31, 2015, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth below in the Portfolio of Investments which are computed using the Fund’s net assets.

The Portfolio of Investments Summary Table and the Portfolio of Investments are broken down by sectors, and these sectors do not represent industry categories for purposes of identifying “industry concentration” as described in the Investment Company Act of 1940, as amended.

Portfolio of Investments

| | | | | | | | | | |

| Shares | | | | | Fair Value | | | |

| | | | | | | | | | |

| Common Stocks — 85.7% | | | | | | |

| Consumer Discretionary — 8.2% | | | | | | |

| | 13,000 | | | Dorman Products, Inc. * | | $ | 617,110 | | | |

| | 15,500 | | | Gentherm, Inc. * | | | 734,700 | | | |

| | 23,000 | | | La-Z-Boy, Inc. | | | 561,660 | | | |

| | 5,500 | | | Papa John’s International, Inc. | | | 307,285 | | | |

| | 7,500 | | | Pinnacle Entertainment, Inc. * | | | 233,400 | | | |

| | 12,500 | | | Texas Roadhouse, Inc. | | | 447,125 | | | |

| | | | | 2,901,280 | | | |

| Consumer Staples — 3.0% | | | | | | |

| | 14,000 | | | Cal-Maine Foods, Inc. (a) | | | 648,760 | | | |

| | 5,250 | | | Sanderson Farms, Inc. (a) | | | 406,980 | | | |

| | | | | 1,055,740 | | | |

| Energy — 2.1% | | | | | | |

| | 21,000 | | | Archrock, Inc. | | | 157,920 | | | |

| | 28,500 | | | Atwood Oceanics, Inc. (a) | | | 291,555 | | | |

| | 10,500 | | | Exterran Corp. * | | | 168,525 | | | |

| | 7,000 | | | SM Energy Co. | | | 137,620 | | | |

| | | | | 755,620 | | | |

| Financials — 20.2% | | | | | | |

| | 30,000 | | | American Equity Investment Life Holding Co. | | | 720,900 | | | |

| | 18,750 | | | Community Bank System, Inc. | | | 748,875 | | | |