CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:

(811-00653)

Exact name of registrant as specified in charter:

Putnam Income Fund

Address of principal executive offices:

One Post Office Square, Boston, Massachusetts 02109

Name and address of agent for service:

Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109

Copy to:

Bryan Chegwidden, Esq. Ropes & Gray LLP 1211 Avenue of the Americas New York, New York 10036

Registrant’s telephone number, including area code:

(617) 292-1000

Date of fiscal year end:

October 31, 2014

Date of reporting period :

November 1, 2013 — October 31, 2014

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Putnam Income Fund

Putnam Income Fund

Annual report 10 | 31 | 14

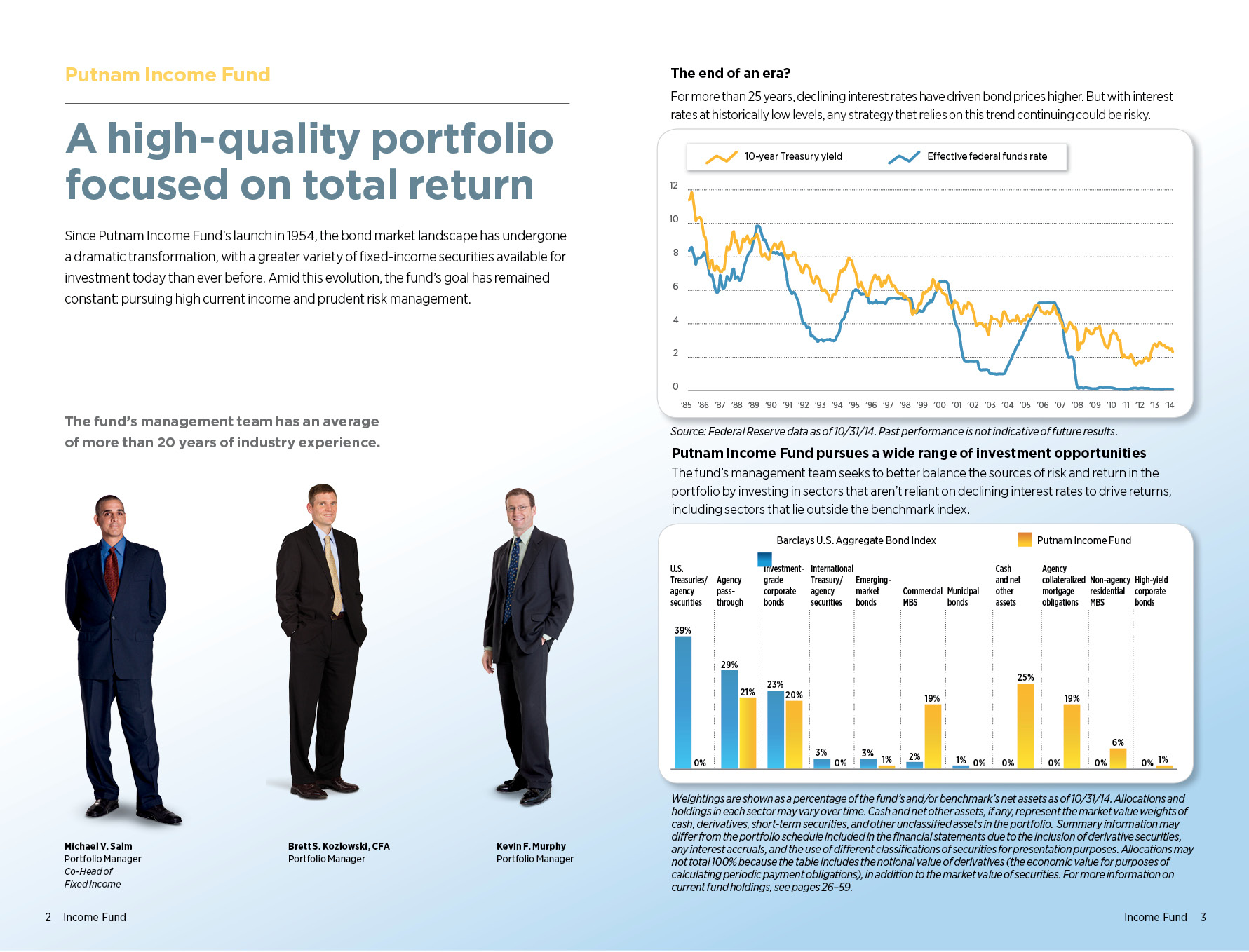

Message from the Trustees

1

About the fund

2

Performance snapshot

4

Interview with your fund’s portfolio manager

5

Your fund’s performance

11

Your fund’s expenses

14

Terms and definitions

16

Other information for shareholders

17

Important notice regarding Putnam’s privacy policy

18

Trustee approval of management contract

19

Financial statements

24

Federal tax information

80

Shareholder meeting results

81

About the Trustees

82

Officers

84

Consider these risks before investing: Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. The value of bonds in the fund’s portfolio may fall or fail to rise over time for several reasons, including general financial market conditions, changing market perceptions of the risk of default, changes in government intervention, and factors related to a specific issuer or industry. These factors may also lead to periods of high volatility and reduced liquidity in the bond markets. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

The U.S. economic recovery has been steadily gaining momentum all year, thanks to positive developments in the key areas of employment, corporate earnings, consumer spending, and energy costs. With the U.S. midterm elections behind us, major stock market indexes achieved record highs in early November.

In October, the nation’s unemployment rate dropped to the lowest level since July 2008. Moreover, third-quarter earnings left investors feeling more confident about equity values and the overall health of corporations. For fixed-income markets, the outlook is more muted. The U.S. Federal Reserve ended its record bond-buying stimulus program in October, and appears to be on track to raise short-term interest rates in mid-2015.

While hardly booming, the U.S. economy has nevertheless emerged as a pillar of strength in the global economy. Meanwhile, the rest of the world may need to do more to nurture growth. Central banks in Europe, Japan, and China have recently augmented their stimulus policies, intending to shore up faltering recoveries. While risks have emerged, it is important to note that markets encountering adversity can still harbor investment potential.

As we head into the new year, it may be an appropriate time for you to meet with your financial advisor to ensure that your portfolio is properly diversified and aligned with your objectives and risk tolerance. Putnam offers a wide range of strategies for all environments, as well as new ways of thinking about building portfolios for today’s markets.

As always, thank you for investing with Putnam.

Respectfully yours,

Robert L. Reynolds President and Chief Executive Officer Putnam Investments

Jameson A. Baxter Chair, Board of Trustees

December 10, 2014

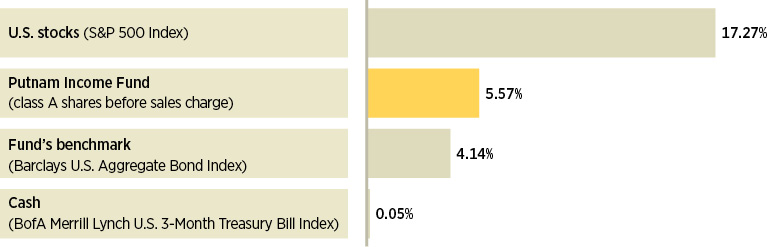

Performance snapshot

Annualized total return (%) comparison as of 10/31/14

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See pages 5 and 11–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

*The fund’s benchmark, the Barclays U.S. Aggregate Bond Index, was introduced on 12/31/75, and the fund’s Lipper category was introduced on 12/31/59. Both post-date the inception date of the fund’s class A shares.

4 Income Fund

Interview with your fund’s portfolio manager

Michael V. Salm

Mike, what was the bond market environment like during the 12 months ended October 31, 2014?

It was a favorable environment for taking mortgage prepayment and credit risk, but there were periods of volatility. The major event marking the early months of the period was the Federal Reserve beginning the process of winding down its bond-buying program, which was announced in December 2013 and launched in January. The Fed concluded its bond purchases in October 2014.

The central bank’s initial $10 billion reduction in bond purchases coincided with lackluster fourth-quarter economic data and an upheaval in emerging markets [EM], which caused investors to assume a more risk-averse posture. As a result, asset flows shifted toward the relative safety of U.S. Treasuries, and pushed the yield on the 10-year note down to 2.61% at the beginning of February. Soon after, however, with EM stress abating, credit markets were buoyed by investors largely dismissing weak economic data, which to a great extent was a function of severe winter weather affecting some of the country’s most densely populated regions.

As we moved into spring, concern about capital flight from Russia due to the Ukraine crisis, along with unrest in the Middle East, prompted investors to once again seek the safety of Treasuries. Demand for Treasuries also received a boost in June when the

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 10/31/14. See pages 4 and 11–13 for additional fund performance information. Index descriptions can be found on page 17.

Income Fund 5

European Central Bank [ECB] implemented a negative deposit rate of –0.10% in the hope of stimulating bank lending to help stave off deflation and bolster eurozone economic growth. Sharply lower yields on sovereign bonds issued by peripheral European countries also indirectly dampened Treasury yields.

Fixed-income markets experienced several bouts of volatility during the latter months of the period. Yields on intermediate- to longer-dated bonds fell globally and most bond market sectors underperformed Treasuries. The high-yield sector saw record outflows in July based on technical factors related to supply and demand. Meanwhile, EM debt faced several unusual events that disrupted that market, including the Russia/Ukraine situation and a technical default by Argentina on its restructured debt.

In mid-October, 10- and 30-year Treasury yields reached 2.15% and 2.92%, respectively — their lows for the period — as geopolitical anxieties and concern about global economic growth once again bolstered demand for Treasuries. Longer-dated bonds also benefited from reduced concern about inflation, as the price index for personal consumption expenditures — the Fed’s preferred inflation gauge — stayed below the central bank’s 2% target rate.

The U.S. dollar rose sharply, and in September, traded at its highest level versus the euro

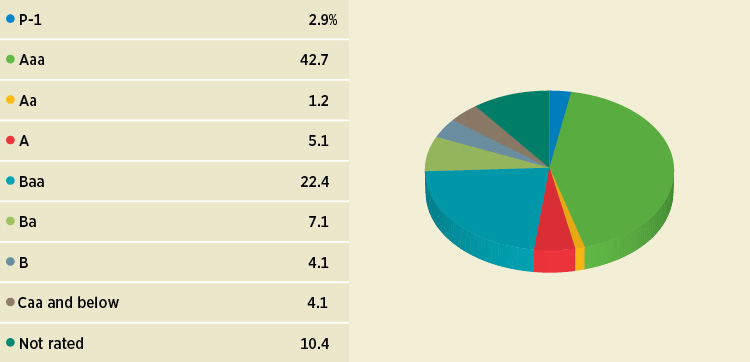

Credit quality overview

Credit qualities are shown as a percentage of the fund’s net assets as of 10/31/14. A bond rated Baa or higher (Prime-3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s (S&P) or, if unrated by S&P, by Fitch ratings, and then included in the closest equivalent Moody’s rating based on analysis of these agencies’ respective ratings criteria. Moody’s ratings are used in recognition of its prominence among rating agencies and breadth of coverage of rated securities. To be announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings and portfolio credit quality may vary over time.

Derivative instruments, including forward currency contracts, are only included to the extent of any unrealized gain or loss on such instruments and are shown in the not-rated category. Cash is also shown in the not-rated category. Derivative offset values are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

6 Income Fund

“We believe U.S. economic growth may accelerate as we move into 2015.”

Mike Salm

since 2008. The greenback advanced as a strengthening U.S. economy prompted investors to conclude that the Fed was likely to begin raising the federal funds rate — its target for short-term interest rates — sometime during 2015. Additionally, divergent policy stances among the Fed, the ECB, and the Bank of Japan [BOJ] — with the U.S. central bank preparing to tighten monetary policy while the ECB and BOJ appear likely to continue easing policy — also fueled dollar strength.

Oil prices fell steadily from midsummer through period-end on concerns that the global market was oversupplied and on signs that the Organization of Petroleum Exporting Countries [OPEC] wasn’t likely to cut output. U.S. dollar strength also put pressure on oil, because oil is priced in dollars and becomes more expensive for buyers using foreign currencies when the dollar strengthens.

The fund outpaced its benchmark and the average return of its Lipper peer group at net asset value during the period. What factors accounted for this solid relative showing?

Our prepayment and mortgage credit strategies were the biggest contributors

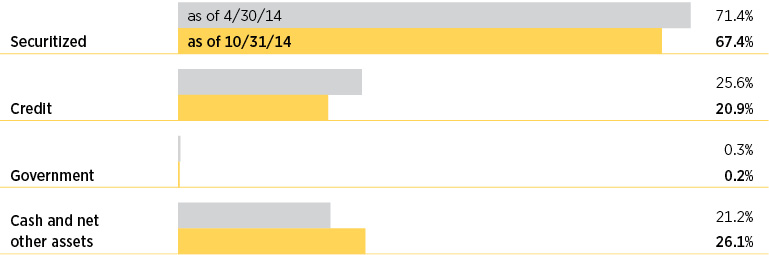

Comparison of top sector weightings

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, and the use of different classifications of securities for presentation purposes. Allocations may not total 100% because the table includes the notional value of derivatives (the economic value for purposes of calculating period payment obligations), in addition to the market value of securities. Holdings and allocations may vary over time.

Income Fund 7

to relative performance. Within prepayment, we implemented our strategies with securities such as interest-only and inverse interest-only collateralized mortgage obligations [CMOs]. Although rates fell during the period, the decline wasn’t severe enough to trigger substantial refinancing of the mortgages underlying our CMO holdings. As a result, prepayment speeds that were slower than expected provided a tailwind to our interest-only CMO positions.

In mortgage credit, our investments in subordinated mezzanine commercial mortgage-backed securities [CMBS] were the most additive. Our CMBS holdings benefited from supportive commercial real estate fundamentals amid an improving U.S. economy, along with persistent investor demand for higher-yielding bonds. Positions in non-agency residential mortgage-backed securities [RMBS] also helped, as their relatively high yields similarly attracted investors. Within this sector, our holdings of pay-option adjustable-rate mortgage-backed securities [pay-option ARMs] were the main contributors to performance.

Elsewhere, security selection in investment-grade corporate bonds provided a further boost to the fund’s relative return. For the period as a whole, investment-grade corporates outperformed Treasuries with comparable maturities, supported by consistent investor demand, solid corporate fundamentals, and an improving domestic economy.

How was the fund positioned with respect to interest-rate sensitivity?

The fund was defensively positioned for a rising-rate environment, resulting in an overall duration — a key measure of interest-rate sensitivity — that was shorter than that of the benchmark. Unfortunately, because rates generally fell during the period, this positioning dampened the fund’s performance versus the benchmark.

How did you use derivatives during the period?

We used bond futures and interest-rate swaps to take tactical positions at various points along the yield curve. We also employed interest-rate swaps and “swaptions” — which give us the option to enter into a swap contract — to hedge the interest-rate risk associated with our CMO holdings. Additionally, we used total return swaps as a hedging tool and to help manage the fund’s sector exposure.

The fund adjusted its dividend rate twice during the period. What led to those decisions?

The fund’s dividend rate per class A share was raised from $0.021 to $0.026 in December, then was decreased to $0.023 in October. The early-period increase was made possible by the higher yields the fund was earning on our securitized holdings, such as CMOs. More recently, however, it became necessary to trim the fund’s dividend rate as credit spreads — the yield advantage various types of bonds offer over Treasuries — trended lower. Similar adjustments were made to other share classes.

What is your outlook for the coming months, and how are you positioning the fund?

We believe U.S. economic growth may accelerate as we move into 2015, given improving trends in employment, and a pickup in consumer and business spending. If this occurs, we think it sets the stage for the Fed to begin raising the federal funds rate sometime next year. That said, with U.S. inflation still running below the central bank’s 2% target, lower oil prices may cause the Fed to take a more dovish stance and defer the first rate increase until later in 2015. We’ll be

8 Income Fund

monitoring these factors closely in the weeks to come.

Given this backdrop, we have slightly increased the fund’s interest-rate sensitivity by bringing its duration closer to the benchmark’s duration. We plan to maintain our diversified mortgage and corporate credit exposure primarily through allocations to mezzanine CMBS and investment-grade corporate bonds. As for prepayment risk, we expect to continue our efforts to capitalize on anticipated slower prepayment speeds through allocations to agency interest-only CMOs. Strategies that attempt to benefit from prepayment risk have historically done well during periods of rising interest rates. Lastly, as of period-end, yields remained reasonably attractive among specific subsectors of the non-agency RMBS market. We remain positive on several of these subsectors, particularly pay-option ARMs.

Thanks for bringing us up to date, Mike.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager Michael V. Salm is Co-Head of Fixed Income at Putnam. He has a B.A. from Cornell University. Michael joined Putnam in 1997 and has been in the investment industry since 1989.

In addition to Michael, your fund’s portfolio managers are Brett S. Kozlowski, CFA, and Kevin F. Murphy.

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

Income Fund 9

IN THE NEWS

In the aftermath of November’s U.S. elections, it’s worth noting that U.S. stocks have gained during every six-month period following midterm votes since 1940. During the past 74 years, 18 midterm elections have been held. In every instance, stocks, as measured by the S&P 500 Index*, have delivered a positive return for the November 1–April 30 period. Gains have often been significant, with stocks delivering an average 17.91% return. The biggest advance of 26.88% took place in 1970–1971. The second biggest return — 26.57% — occurred in 1942–1943. The lowest return was 0.75% in 1946–1947. Why has the market consistently advanced following every midterm election, despite varying economic conditions across these periods? Many market observers believe that it comes down to clarity — in other words, each instance might be considered a “relief rally,” as election-related uncertainty tends to diminish.

*Returns for 1966 and earlier based on Ibbotson U.S. Large Stock Total Return Extended Index.

10 Income Fund

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended October 31, 2014, the end of its most recent fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R5, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 10/31/14

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

(inception dates)

(11/1/54)

(3/1/93)

(7/26/99)

(12/14/94)

(1/21/03)

(7/2/12)

(7/2/12)

(6/16/94)

Before sales charge

After sales charge

Before CDSC

After CDSC

Before CDSC

After CDSC

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Annual average

(life of fund)

7.77%

7.70%

7.62%

7.62%

6.96%

6.96%

7.34%

7.28%

7.50%

7.86%

7.87%

7.86%

10 years

75.78

68.75

65.60

65.60

63.28

63.28

71.46

65.88

71.43

80.28

80.56

80.22

Annual average

5.80

5.37

5.17

5.17

5.03

5.03

5.54

5.19

5.54

6.07

6.09

6.07

5 years

38.45

32.91

33.36

31.36

33.40

33.40

36.88

32.43

36.67

40.31

40.53

40.27

Annual average

6.72

5.86

5.93

5.61

5.93

5.93

6.48

5.78

6.45

7.01

7.04

7.00

3 years

18.37

13.63

15.76

12.76

15.78

15.78

17.53

13.71

17.45

19.46

19.65

19.43

Annual average

5.78

4.35

5.00

4.08

5.00

5.00

5.53

4.38

5.51

6.11

6.16

6.10

1 year

5.57

1.34

4.79

–0.21

4.84

3.84

5.31

1.88

5.27

5.83

5.98

5.90

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B share performance reflects conversion to class A shares after eight years.

Income Fund 11

Comparative index returns For periods ended 10/31/14

Barclays U.S. Aggregate Bond Index

Lipper Core Bond Funds category average*

Annual average (life of fund)

—†

—†

10 years

57.34%

51.75%

Annual average

4.64

4.22 ��

5 years

22.97

25.46

Annual average

4.22

4.62

3 years

8.42

10.11

Annual average

2.73

3.25

1 year

4.14

4.12

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

*Over the 1-year, 3-year, 5-year, and 10-year periods ended 10/31/14, there were 522, 462, 406, and 294 funds, respectively, in this Lipper category.

†The fund’s benchmark, the Barclays U.S. Aggregate Bond Index, was introduced on 12/31/75, and the fund’s Lipper category was introduced on 12/31/59. Both post-date the inception date of the fund’s class A shares.

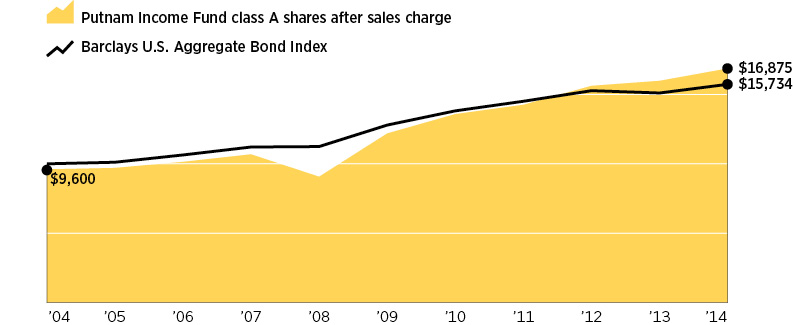

Change in the value of a $10,000 investment ($9,600 after sales charge)

Cumulative total return from 10/31/04 to 10/31/14

Past performance does not indicate future results. At the end of the same time period, a $10,000 investment in the fund’s class B and class C shares would have been valued at $16,560 and $16,328, respectively, and no contingent deferred sales charges would apply. A $10,000 investment in the fund’s class M shares ($9,675 after sales charge) would have been valued at $16,588. A $10,000 investment in the fund’s class R, R5, R6, and Y shares would have been valued at $17,143, $18,028, $18,056, and $18,022, respectively.

12 Income Fund

Fund price and distribution information For the 12-month period ended 10/31/14

Distributions

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Number

12

12

12

12

12

12

12

12

Income

$0.333

$0.276

$0.280

$0.317

$0.320

$0.356

$0.357

$0.351

Capital gains

—

—

—

—

—

—

—

—

Total

$0.333

$0.276

$0.280

$0.317

$0.320

$0.356

$0.357

$0.351

Share value

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

10/31/13

$7.20

$7.50

$7.13

$7.15

$7.05

$7.29

$7.16

$7.29

$7.29

$7.29

10/31/14

7.26

7.56

7.19

7.21

7.10

7.34

7.21

7.35

7.36

7.36

Current rate (end of period)

Before sales charge

After sales charge

Net asset value

Net asset value

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Current dividend rate1

3.80%

3.65%

3.00%

3.16%

3.55%

3.43%

3.66%

3.92%

4.08%

4.08%

Current 30-day SEC yield2

N/A

2.34

1.69

1.68

N/A

2.11

2.18

2.70

2.78

2.67

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

Fund performance as of most recent calendar quarter Total return for periods ended 9/30/14

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

(inception dates)

(11/1/54)

(3/1/93)

(7/26/99)

(12/14/94)

(1/21/03)

(7/2/12)

(7/2/12)

(6/16/94)

Before sales charge

After sales charge

Before CDSC

After CDSC

Before CDSC

After CDSC

Before sales charge

After sales charge

Net asset value

Net asset value

Net asset value

Net asset value

Annual average

(life of fund)

7.78%

7.70%

7.63%

7.63%

6.97%

6.97%

7.34%

7.28%

7.51%

7.87%

7.87%

7.87%

10 years

76.64

69.57

66.38

66.38

63.83

63.83

72.06

66.47

72.01

81.16

81.42

81.07

Annual average

5.85

5.42

5.22

5.22

5.06

5.06

5.58

5.23

5.57

6.12

6.14

6.12

5 years

42.05

36.37

36.87

34.87

36.88

36.88

40.52

35.95

40.46

44.16

44.37

44.09

Annual average

7.27

6.40

6.48

6.17

6.48

6.48

7.04

6.34

7.03

7.59

7.62

7.58

3 years

18.86

14.11

16.26

13.26

16.26

16.26

18.05

14.21

17.94

19.79

19.96

19.73

Annual average

5.93

4.50

5.15

4.24

5.15

5.15

5.69

4.53

5.65

6.20

6.25

6.19

1 year

6.88

2.60

6.12

1.12

6.14

5.14

6.66

3.19

6.58

7.14

7.28

7.18

See the discussion following the fund performance table on page 11 for information about the calculation of fund performance.

Income Fund 13

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Total annual operating expenses for the fiscal year ended 10/31/13

0.87%

1.62%

1.62%

1.12%

1.12%

0.58%

0.51%

0.62%

Annualized expense ratio for the six-month period ended 10/31/14*

0.84%

1.59%

1.59%

1.09%

1.09%

0.57%

0.50%

0.59%

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

*For the fund’s most recent fiscal half year; may differ from expense ratios based on one-year data in the financial highlights.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from May 1, 2014, to October 31, 2014. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

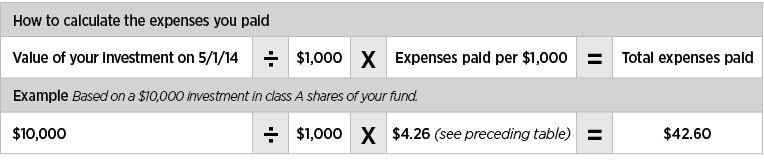

Expenses paid per $1,000*†

$4.26

$8.04

$8.05

$5.52

$5.52

$2.89

$2.54

$3.00

Ending value (after expenses)

$1,011.40

$1,007.30

$1,009.10

$1,010.50

$1,010.60

$1,014.10

$1,014.30

$1,014.10

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 10/31/14. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

14 Income Fund

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended October 31, 2014, use the following calculation method. To find the value of your investment on May 1, 2014, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Class A

Class B

Class C

Class M

Class R

Class R5

Class R6

Class Y

Expenses paid per $1,000*†

$4.28

$8.08

$8.08

$5.55

$5.55

$2.91

$2.55

$3.01

Ending value (after expenses)

$1,020.97

$1,017.19

$1,017.19

$1,019.71

$1,019.71

$1,022.33

$1,022.68

$1,022.23

*Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 10/31/14. The expense ratio may differ for each share class.

†Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

Income Fund 15

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 4.00% maximum sales charge for class A shares and 3.25% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge and may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain employer-sponsored retirement plans.

Class R5 and R6 shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

•Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

•Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

•Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

•Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

•Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

16 Income Fund

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2014, are available in the Individual Investors section of putnam.com, and on the Securities and Exchange Commission (SEC) website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of October 31, 2014, Putnam employees had approximately $494,000,000 and the Trustees had approximately $139,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

Income Fund 17

Important notice regarding Putnam’s privacy policy

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ names, addresses, Social Security numbers, and dates of birth. Using this information, we are able to maintain accurate records of accounts and transactions.

It is our policy to protect the confidentiality of our shareholder information, whether or not a shareholder currently owns shares of our funds. In particular, it is our policy not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use.

Under certain circumstances, we must share account information with outside vendors who provide services to us, such as mailings and proxy solicitations. In these cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. Finally, it is our policy to share account information with your financial representative, if you’ve listed one on your Putnam account.

18 Income Fund

Trustee approval of management contract

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management, LLC (“Putnam Management”) and the sub-management contract with respect to your fund between Putnam Management and its affiliate, Putnam Investments Limited (“PIL”). The Board of Trustees, with the assistance of its Contract Committee, requests and evaluates all information it deems reasonably necessary under the circumstances in connection with its annual contract review. The Contract Committee consists solely of Trustees who are not “interested persons” (as this term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of the Putnam funds (“Independent Trustees”).

At the outset of the review process, members of the Board’s independent staff and independent legal counsel met with representatives of Putnam Management to review the annual contract review materials furnished to the Contract Committee during the course of the previous year’s review and to discuss possible changes in these materials that might be necessary or desirable for the coming year. Following these discussions and in consultation with the Contract Committee, the Independent Trustees’ independent legal counsel requested that Putnam Management furnish specified information, together with any additional information that Putnam Management considered relevant, to the Contract Committee. Over the course of several months ending in June 2014, the Contract Committee met on a number of occasions with representatives of Putnam Management, and separately in executive session, to consider the information that Putnam Management provided, as well as supplemental information provided in response to additional requests made by the Contract Committee. Throughout this process, the Contract Committee was assisted by the members of the Board’s independent staff and by independent legal counsel for the Putnam funds and the Independent Trustees.

In May 2014, the Contract Committee met in executive session to discuss and consider its preliminary recommendations with respect to the continuance of the contracts. At the Trustees’ June 20, 2014 meeting, the Contract Committee met in executive session with the other Independent Trustees to review a summary of the key financial, performance and other data that the Contract Committee considered in the course of its review. The Contract Committee then presented its written report, which summarized the key factors that the Committee had considered and set forth its final recommendations. The Contract Committee then recommended, and the Independent Trustees approved, the continuance of your fund’s management and sub-management contracts, effective July 1, 2014. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees have not attempted to evaluate PIL as a separate entity, and all subsequent references to Putnam Management below should be deemed to include reference to PIL as necessary or appropriate in the context.)

The Independent Trustees’ approval was based on the following conclusions:

•That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds, and the costs incurred by Putnam Management in providing services to the fund; and

Income Fund 19

•That the fee schedule in effect for your fund represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the management arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that some aspects of the arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of fee arrangements in previous years. For example, with some minor exceptions, the current fee arrangements under the management contracts for the Putnam funds were implemented at the beginning of 2010 following extensive review by the Contract Committee and discussions with representatives of Putnam Management, as well as approval by shareholders. Shareholders also voted overwhelmingly to approve these fee arrangements in early 2014, when they were asked to approve new management contracts (with the same fees and substantially identical other provisions) following the possible termination of the previous management contracts as a result of the death of the Honorable Paul G. Desmarais. (Mr. Desmarais, both directly and through holding companies, controlled a majority of the voting shares of Power Corporation of Canada, which (directly and indirectly) is the majority owner of Putnam Management. Mr. Desmarais’ voting control of shares of Power Corporation of Canada was transferred to The Desmarais Family Residuary Trust upon his death and this transfer, as a technical matter, may have constituted an “assignment” within the meaning of the 1940 Act, causing the Putnam funds’ management contracts to terminate automatically.)

Management fee schedules and total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints. The Trustees also reviewed the total expenses of each Putnam fund, recognizing that in most cases management fees represented the major, but not the sole, determinant of total costs to shareholders.

In reviewing fees and expenses, the Trustees generally focus their attention on material changes in circumstances — for example, changes in assets under management, changes in a fund’s investment style, changes in Putnam Management’s operating costs or profitability, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund.

Under its management contract, your fund has the benefit of breakpoints in its management fee schedule that provide shareholders with economies of scale in the form of reduced fee levels as assets under management in the Putnam family of funds increase. The Trustees concluded that the fee schedule in effect for your fund represented an appropriate sharing of economies of scale between fund shareholders and Putnam Management.

As in the past, the Trustees also focused on the competitiveness of each fund’s total expense ratio. In order to ensure that expenses of the Putnam funds continue to meet competitive standards, the Trustees and Putnam

20 Income Fund

Management have implemented certain expense limitations. These expense limitations were: (i) a contractual expense limitation applicable to all retail open-end funds of 32 basis points on investor servicing fees and expenses and (ii) a contractual expense limitation applicable to all open-end funds of 20 basis points on so-called “other expenses” (i.e., all expenses exclusive of management fees, investor servicing fees, distribution fees, investment-related expenses, interest, taxes, brokerage commissions, extraordinary expenses and acquired fund fees and expenses). These expense limitations serve in particular to maintain competitive expense levels for funds with large numbers of small shareholder accounts and funds with relatively small net assets. Most funds, including your fund, had sufficiently low expenses that these expense limitations did not apply. Putnam Management’s support for these expense limitation arrangements was an important factor in the Trustees’ decision to approve the continuance of your fund’s management and sub-management contracts.

The Trustees reviewed comparative fee and expense information for a custom group of competitive funds selected by Lipper Inc. (“Lipper”). This comparative information included your fund’s percentile ranking for effective management fees and total expenses (excluding any applicable 12b-1 fee), which provides a general indication of your fund’s relative standing. In the custom peer group, your fund ranked in the first quintile in effective management fees (determined for your fund and the other funds in the custom peer group based on fund asset size and the applicable contractual management fee schedule) and in the first quintile in total expenses (excluding any applicable 12b-1 fees) as of December 31, 2013 (the first quintile representing the least expensive funds and the fifth quintile the most expensive funds). The fee and expense data reported by Lipper as of December 31, 2013 reflected the most recent fiscal year-end data available in Lipper’s database at that time.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services provided and the profits realized by Putnam Management and its affiliates from their contractual relationships with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management, investor servicing and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability, allocated on a fund-by-fund basis, with respect to the funds’ management, distribution, and investor servicing contracts. For each fund, the analysis presented information about revenues, expenses and profitability for each of the agreements separately and for the agreements taken together on a combined basis. The Trustees concluded that, at current asset levels, the fee schedules in place represented reasonable compensation for the services being provided and represented an appropriate sharing of such economies of scale as may exist in the management of the Putnam funds at that time.

The information examined by the Trustees as part of their annual contract review for the Putnam funds has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, and the like. This information included comparisons of those fees with fees charged to the Putnam funds, as well as an assessment of the differences in the services provided to these different types of clients. The Trustees observed that the differences in fee rates between institutional clients and mutual funds are by no means uniform when examined by individual asset sectors, suggesting that

Income Fund 21

differences in the pricing of investment management services to these types of clients may reflect historical competitive forces operating in separate markets. The Trustees considered the fact that in many cases fee rates across different asset classes are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to its institutional clients. The Trustees did not rely on these comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the investment oversight committees of the Trustees, which meet on a regular basis with the funds’ portfolio teams and with the Chief Investment Officer and other senior members of Putnam Management’s Investment Division throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — based on the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to them, and in general Putnam Management’s ability to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investment results for every fund in every time period.

The Trustees considered that 2013 was a year of strong competitive performance for many of the Putnam funds, with only a relatively small number of exceptions. They noted that this strong performance was exemplified by the fact that the Putnam funds were recognized by Barron’s as the second-best performing mutual fund complex for both 2013 and the five-year period ended December 31, 2013. They also noted, however, the disappointing investment performance of some funds for periods ended December 31, 2013 and considered information provided by Putnam Management regarding the factors contributing to the underperformance and actions being taken to improve the performance of these particular funds. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these efforts and to evaluate whether additional actions to address areas of underperformance are warranted. For purposes of evaluating investment performance, the Trustees generally focus on competitive industry rankings for the one-year, three-year and five-year periods. For a number of Putnam funds with relatively unique investment mandates for which meaningful competitive performance rankings are not considered available, the Trustees evaluated performance based on comparisons of fund returns with the returns of selected investment benchmarks. In the case of your fund, the Trustees considered that its class A share cumulative total return performance at net asset value was in the following quartiles of its Lipper peer group (Lipper Corporate Debt Funds A Rated) for the one-year, three-year and five-year periods ended December 31, 2013 (the first quartile representing the best-performing funds and the fourth quartile the worst-performing funds):

One-year period

1st

Three-year period

1st

Five-year period

1st

For the one-year and five-year periods ended December 31, 2013, your fund’s performance was in the top decile of its Lipper peer group. Over the one-year, three-year and five-year periods ended December 31, 2013, there were 63, 57 and 50 funds, respectively, in your fund’s Lipper peer group. (When considering performance information, shareholders should

22 Income Fund

be mindful that past performance is not a guarantee of future results.)

Brokerage and soft-dollar allocations; investor servicing

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage allocation and the use of soft dollars, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that are expected to be useful to Putnam Management in managing the assets of the fund and of other clients. Subject to policies established by the Trustees, soft dollars generated by these means are used primarily to acquire brokerage and research services that enhance Putnam Management’s investment capabilities and supplement Putnam Management’s internal research efforts. However, the Trustees noted that a portion of available soft dollars continues to be used to pay fund expenses. The Trustees indicated their continued intent to monitor regulatory and industry developments in this area with the assistance of their Brokerage Committee and also indicated their continued intent to monitor the allocation of the Putnam funds’ brokerage in order to ensure that the principle of seeking best price and execution remains paramount in the portfolio trading process.

Putnam Management may also receive benefits from payments that the funds make to Putnam Management’s affiliates for investor or distribution services. In conjunction with the annual review of your fund’s management and sub-management contracts, the Trustees reviewed your fund’s investor servicing agreement with Putnam Investor Services, Inc. (“PSERV”) and its distributor’s contracts and distribution plans with Putnam Retail Management Limited Partnership (“PRM”), both of which are affiliates of Putnam Management. The Trustees concluded that the fees payable by the funds to PSERV and PRM, as applicable, for such services are reasonable in relation to the nature and quality of such services, the fees paid by competitive funds, and the costs incurred by PSERV and PRM, as applicable, in providing such services.

Income Fund 23

Financial statements

These sections of the report, as well as the accompanying Notes, preceded by the Report of Independent Registered Public Accounting Firm, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal year.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

24 Income Fund

Report of Independent Registered Public Accounting Firm

The Board of Trustees and Shareholders Putnam Income Fund:

We have audited the accompanying statement of assets and liabilities of Putnam Income Fund (the fund), including the fund’s portfolio, as of October 31, 2014, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2014, by correspondence with the custodian and brokers or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Putnam Income Fund as of October 31, 2014, the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Teco Finance, Inc. company guaranty sr. unsec. unsub. notes 6.572s, 2017

340,000

388,045

Texas-New Mexico Power Co. 144A 1st mtge. bonds Ser. A, 9 1/2s, 2019

2,840,000

3,639,071

West Penn Power Co. 144A sr. bonds 5.95s, 2017

830,000

936,877

47,961,759

Total corporate bonds and notes (cost $377,203,745)

$403,571,113

44 Income Fund

ASSET-BACKED SECURITIES (3.2%)*

Principal amount

Value

Station Place Securitization Trust 144A FRB Ser. 14-2, Class A, 1.054s, 2016

$59,213,000

$59,213,000

Total asset-backed securities (cost $59,213,000)

$59,213,000

PURCHASED SWAP OPTIONS OUTSTANDING (0.3%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.7175/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.7175

$131,346,000

$2,751,699

Credit Suisse International

(2.52875)/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.52875

372,617,000

1,889,168

2.27125/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.27125

372,617,000

253,380

Total purchased swap options outstanding (cost $4,396,401)

$4,894,247

PURCHASED OPTIONS OUTSTANDING (0.1%)*

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/$103.13

$82,000,000

$792,120

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/102.94

82,000,000

712,580

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/102.63

69,000,000

498,180

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/102.38

69,000,000

426,420

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Dec-14/101.69

26,000,000

26,780

Total purchased options outstanding (cost $2,930,234)

$2,456,080

MUNICIPAL BONDS AND NOTES (0.2%)*

Principal amount

Value

CA State G.O. Bonds (Build America Bonds), 7 1/2s, 4/1/34

$770,000

$1,111,149

IL State G.O. Bonds, 4.421s, 1/1/15

410,000

412,583

North TX, Tollway Auth. Rev. Bonds (Build America Bonds), 6.718s, 1/1/49

675,000

939,553

OH State U. Rev. Bonds (Build America Bonds), 4.91s, 6/1/40

845,000

980,149

Total municipal bonds and notes (cost $2,705,059)

$3,443,434

FOREIGN GOVERNMENT AND AGENCY BONDS AND NOTES (—%)*

Principal amount

Value

Korea Development Bank sr. unsec. unsub. notes 4s, 2016 (South Korea)

$200,000

$210,190

Total foreign government and agency bonds and notes (cost $199,647)

$210,190

SHORT-TERM INVESTMENTS (26.1%)*

Principal amount/shares

Value

Federal National Mortgage Association unsec. discount notes with an effective yield of 0.04%, January 14, 2015

$16,500,000

$16,499,010

Putnam Money Market Liquidity Fund 0.07% L

Shares 144,207,935

144,207,935

Putnam Short Term Investment Fund 0.09% L

Shares 289,802,238

289,802,238

U.S. Treasury Bills with an effective yield of 0.10%, July 23, 2015 #

1,203,000

1,202,300

Income Fund 45

SHORT-TERM INVESTMENTS (26.1%)* cont.

Principal amount/shares

Value

U.S. Treasury Bills with an effective yield of 0.08%, May 28, 2015 Δ

$233,000

$232,933

U.S. Treasury Bills with effective yields ranging from 0.02% to 0.05%, January 15, 2015 # Δ

1,184,000

1,183,964

U.S. Treasury Bills with effective yields ranging from 0.01% to 0.05%, January 8, 2015 # Δ §

6,667,000

6,666,880

U.S. Treasury Bills with an effective yield of 0.03%, January 2, 2015 Δ §

952,000

951,976

U.S. Treasury Bills with effective yields ranging from 0.03% to 0.05%, December 18, 2014 # Δ §

7,373,000

7,372,663

U.S. Treasury Bills with an effective yield of 0.04%, December 11, 2014 Δ

303,000

302,987

U.S. Treasury Bills with effective yields ranging from 0.02% to 0.03%, December 4, 2014 Δ §

3,899,000

3,898,924

U.S. Treasury Bills with effective yields ranging from 0.02% to 0.03%, November 28, 2014 Δ §

6,589,000

6,588,864

U.S. Treasury Bills with an effective yield of 0.05%, November 20, 2014 Δ

1,020,000

1,019,974

U.S. Treasury Bills with an effective yield of 0.05%, November 13, 2014 Δ

614,000

613,990

U.S. Treasury Bills with effective yields ranging from 0.01% to 0.03%, November 6, 2014 Δ

8,608,000

8,607,980

Total short-term investments (cost $489,151,769)

$489,152,618

TOTAL INVESTMENTS

Total investments (cost $2,151,936,271)

$2,222,910,274

Key to holding’s abbreviations

BKNT

Bank Note

FRB

Floating Rate Bonds: the rate shown is the current interest rate at the close of the reporting period

FRN

Floating Rate Notes: the rate shown is the current interest rate at the close of the reporting period

G.O. Bonds

General Obligation Bonds

IFB

Inverse Floating Rate Bonds, which are securities that pay interest rates that vary inversely to changes in the market interest rates. As interest rates rise, inverse floaters produce less current income. The rate shown is the current interest rate at the close of the reporting period.

IO

Interest Only

MTN

Medium Term Notes

PO

Principal Only

TBA

To Be Announced Commitments

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from November 1, 2013 through October 31, 2014 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification 820 Fair Value Measurements and Disclosures and references to “OTC”, if any, represent over-the-counter.

*

Percentages indicated are based on net assets of $1,873,075,186.

†

Non-income-producing security.

#

This security, in part or in entirety, was pledged and segregated with the broker to cover margin requirements for futures contracts at the close of the reporting period.

Δ

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on certain derivative contracts at the close of the reporting period.

46 Income Fund

§

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on the initial margin on certain centrally cleared derivative contracts at the close of the reporting period.

##

Forward commitment, in part or in entirety (Note 1).

F

Security is valued at fair value following procedures approved by the Trustees. Securities may be classified as Level 2 or Level 3 for ASC 820 based on the securities’ valuation inputs (Note 1).

L

Affiliated company (Note 5). The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

R

Real Estate Investment Trust.

At the close of the reporting period, the fund maintained liquid assets totaling $737,556,225 to cover certain derivatives contracts and delayed delivery securities.

Debt obligations are considered secured unless otherwise indicated.

144A after the name of an issuer represents securities exempt from registration under Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

See Note 1 to the financial statements regarding TBA commitments.

The dates shown on debt obligations are the original maturity dates.

FUTURES CONTRACTS OUTSTANDING at 10/31/14

Number of contracts

Value

Expiration date

Unrealized appreciation/ (depreciation)

U.S. Treasury Bond 30 yr (Short)

1,022

$144,197,813

Dec-14

$711,309

U.S. Treasury Bond Ultra 30 yr (Long)

581

91,108,063

Dec-14

85,802

U.S. Treasury Note 5 yr (Short)

63

7,524,070

Dec-14

32,216

U.S. Treasury Note 10 yr (Long)

1,505

190,170,859

Dec-14

61,437

Total

$890,764

WRITTEN SWAP OPTIONS OUTSTANDING at 10/31/14 (premiums $11,613,079)

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

(2.54)/3 month USD-LIBOR-BBA/Aug-25

Aug-15/2.54

$6,948,750

$117,295

(2.54)/3 month USD-LIBOR-BBA/Aug-25

Aug-15/2.54

6,948,750

117,295

(2.557)/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.557

131,346,000

1,071,783

(2.60)/3 month USD-LIBOR-BBA/Jan-25

Jan-15/2.60

83,659,200

1,239,829

Credit Suisse International

(2.40)/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.40

186,308,500

508,622

(2.51)/3 month USD-LIBOR-BBA/Aug-25

Aug-15/2.51

105,976,500

1,673,369

(2.51)/3 month USD-LIBOR-BBA/Aug-25

Aug-15/2.51

105,976,500

1,673,369

2.40/3 month USD-LIBOR-BBA/Nov-24

Nov-14/2.40

186,308,500

2,209,619

JPMorgan Chase Bank N.A.

(2.60)/3 month USD-LIBOR-BBA/Feb-25

Feb-15/2.60

41,829,600

631,209

(6.00 Floor)/3 month USD-LIBOR-BBA/Mar-18

Mar-18/6.00

21,202,000

3,757,596

Total

$12,999,986

Income Fund 47

WRITTEN OPTIONS OUTSTANDING at 10/31/14 (premiums $2,567,031)

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/$102.13

$82,000,000

$431,320

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/101.94

82,000,000

381,300

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/101.75

69,000,000

282,210

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/101.50

69,000,000

236,670

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/101.13

82,000,000

214,020

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/100.94

82,000,000

186,140

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/100.88

69,000,000

149,040

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Jan-15/100.63

69,000,000

122,820

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Dec-14/100.81

26,000,000

7,800

Federal National Mortgage Association 30 yr 3.5s TBA commitments (Put)

Dec-14/99.94

26,000,000

2,080

Total

$2,013,400

FORWARD PREMIUM SWAP OPTION CONTRACTS OUTSTANDING at 10/31/14

Counterparty Fixed right or obligation % to receive or (pay)/Floating rate index/ Maturity date

TBA SALE COMMITMENTS OUTSTANDING at 10/31/14 (proceeds receivable $112,027,070)

Agency

Principal amount

Settlement date

Value

Federal National Mortgage Association, 4 1/2s, November 1, 2044

$49,000,000

11/13/14

$53,122,889

Federal National Mortgage Association, 4s, November 1, 2044

38,000,000

11/13/14

40,348,282

Federal National Mortgage Association, 3 1/2s, November 1, 2044

18,000,000

11/13/14

18,610,312

Total

$112,081,483

CENTRALLY CLEARED INTEREST RATE SWAP CONTRACTS OUTSTANDING at 10/31/14

Notional amount

Upfront premium received (paid)

Termination date

Payments made by fund per annum

Payments received by fund per annum

Unrealized appreciation/ (depreciation)

$9,265,000

$(69,147)

10/29/24

3 month USD-LIBOR-BBA

2.54%

$(6,833)

9,265,000

(61,735)

10/28/24

3 month USD-LIBOR-BBA

2.54%

89

102,977,000 E

64,817

12/17/16

3 month USD-LIBOR-BBA

1.00%

(352,961)

272,805,700 E

4,319,449

12/17/19

3 month USD-LIBOR-BBA

2.25%

(1,353,818)

600,532,300 E

19,224,447

12/17/24

3 month USD-LIBOR-BBA

3.00%

(7,425,376)

16,168,200 E

1,531,115

12/17/44

3 month USD-LIBOR-BBA

3.50%

84,126

204,953,800

(2,705)

10/20/24

3 month USD-LIBOR-BBA

2.335%

(2,340,704)