UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-05162 |

| |

| Exact name of registrant as specified in charter: | Delaware VIP® Trust |

| |

| Address of principal executive offices: | 2005 Market Street |

| Philadelphia, PA 19103 |

| |

| Name and address of agent for service: | David F. Connor, Esq. |

| 2005 Market Street |

| Philadelphia, PA 19103 |

| |

| Registrant’s telephone number, including area code: | (800) 523-1918 |

| |

| Date of fiscal year end: | December 31 |

| |

| Date of reporting period: | December 31, 2015 |

Item 1. Reports to Stockholders

|

Delaware VIP® Trust |

Delaware VIP Diversified Income Series |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Annual report |

December 31, 2015 |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

| |

| |

| |

Table of contents

Neither Delaware Investments nor its affiliates noted in this document are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise.

Unless otherwise noted, views expressed herein are current as of Dec. 31, 2015, and subject to change for events occurring after such date.

The Series is not FDIC insured and is not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor and member of Macquarie Group. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Series’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

This material may be used in conjunction with the offering of shares in Delaware VIP Diversified Income Series only if preceded or accompanied by the Series’ current prospectus or the summary prospectus.

© 2016 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

| | |

| Delaware VIP® Trust — Delaware VIP Diversified Income Series | | |

| Portfolio management review | | January 12, 2016 |

For the fiscal year ended Dec. 31, 2015, Delaware VIP Diversified Income Series Standard Class shares returned -1.08% and Service Class shares returned -1.34%. Both figures reflect all dividends reinvested. The Series’ benchmark, the Barclays U.S. Aggregate Index, returned +0.55% for the same period.

A key development during the period was the divergence in central bank policies. Even as the European Central Bank was launching its quantitative-easing program in March, the U.S. Federal Reserve was signaling a potential rate hike. Although that hike did not materialize until December, just the prospect of a rate increase had a profound effect on the markets, particularly in currencies, with the U.S. dollar rising sharply. Emerging market economies deteriorated, negatively affecting revenue growth for U.S.-based multinational companies.

The strong dollar cut significantly into the global sales and net earnings of many U.S. corporations. Exports became more expensive, while currency conversions into U.S. dollars became more unfavorable. This affected investment grade corporate credit, leading us to reduce the Series’ credit overweight.

Slowdowns in global growth and global trade, particularly the economic slowdown in China and the collapse in commodity prices, were a concern. That weighed on many emerging market nations and Asian countries that have grown dependent on Chinese demand.

Relative to its benchmark, the Series’ performance was hurt by a significant underweight to U.S. Treasurys, which generally performed better than corporate credit. This was partially offset by the use of futures to manage interest rate risk and yield curve risk.

Our investment grade credit selections contributed positively, even though the asset class underperformed the index. The Series’ holdings within financials contributed significantly to performance. Barclays, Branch Banking & Trust, Bank of America, and General Electric Capital were the strongest performers. We modified the portfolio by investing more in utilities. Our selections, which included bonds issued by NextEra Energy Capital, Puget Energy, and Entergy, outperformed the benchmark in absolute terms and outpaced their index component.

High yield corporate credit and emerging market bond exposure both had a significant negative effect on performance. Although we reduced the Series’ allocation to each, exposure to these sectors was detrimental in an environment where the benchmark had positive returns. Poor security selection compounded this, with Intelsat, a satellite services company, and commodity-focused issuers including Chesapeake Energy and Halcon Resources detracting from performance.

Although security selection was positive in mortgage-backed securities (MBS), the Series’ had a significant underweight to this strong-performing sector. Commercial mortgage-backed securities (CMBS) contributed to performance, outperforming the overall benchmark and the benchmark’s CMBS component.

Another position not included in the benchmark that was helpful was the Series’ small exposure to municipal bonds, including Golden State Tobacco Securitization and City of New York general obligation bonds.

Exposure to below-investment grade assets not included in the benchmark, including emerging market bonds, detracted from performance. The decision to have greater exposure to lower-quality securities detracted significantly, but was partially offset by security selection, especially in corporate credit, which was generally strong.

In our view, the key risk within the Series’ portfolio continues to be credit risk, although we have increased exposure to U.S. Treasurys and MBS. We continue to see significant idiosyncratic (security-specific) risk in the market. Believing that challenges remain for corporate balance sheets, we reduced the Series’ exposure to high yield and investment grade corporate credit.

The Series’ use of derivatives contributed modestly to the Series’ performance. We used derivatives for several hedging purposes. In addition to U.S. Treasury futures, currency forwards, and credit derivatives, we used E-mini S&P 500 futures (these are one-fifth the size of the Standard S&P 500 futures contracts) to hedge some of the portfolio’s exposure to convertible bonds. However, because convertibles only made up about 2% of the portfolio, this had a minimal effect on performance during the fiscal year.

In our view, we don’t see much risk of the United States slipping into recession in the short term. However, we anticipate higher levels of volatility as the Fed appears likely to continue raising interest rates, diverging further from other central banks. Accordingly, we will likely maintain a more conservative position in the Series overall.

| | |

| Unless otherwise noted, views expressed herein are current as of Dec. 31, 2015, and subject to change. |

| | Diversified Income Series-1 |

Delaware VIP® Trust — Delaware VIP Diversified Income Series

Performance summary

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Carefully consider the Series’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Series’ prospectus and its summary prospectus, which may be obtained by calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

| | | | | | | | | | |

Delaware VIP Diversified Income Series Average annual total returns For periods ended Dec. 31, 2015 | | 1 year | | 3 years | | 5 years | | 10 years | | Lifetime |

| | | | | |

Standard Class shares (commenced operations on May 16, 2003) | | -1.08% | | +0.95% | | +3.24% | | +5.96% | | +5.75% |

| | | | | | | | | | |

| | | | | |

Service Class shares (commenced operations on May 16, 2003) | | -1.34% | | +0.70% | | +2.98% | | +5.69% | | +5.48% |

| | | | | | | | | | |

| | | | | |

Barclays U.S. Aggregate Index | | +0.55% | | +1.44% | | +3.25% | | +4.51% | | n/a |

Returns reflect the reinvestment of all distributions. Please see page 3 for a description of the index.

As described in the Series’ most recent prospectus, the net expense ratio for Service Class shares of the Series was 0.92%, while total operating expenses for Standard Class and Service Class shares were 0.67% and 0.97%, respectively. The management fee for Standard Class and Service Class shares was 0.58%.

The Series’ distributor has contracted to limit the 12b-1 fees for Service Class shares to no more than 0.25% of average daily net assets from Jan. 1, 2015 through Dec. 31, 2015.*

Earnings from a variable annuity or variable life investment compound tax-free until withdrawal, and as a result, no adjustments were made for income taxes.

Expense limitations were in effect for both classes during certain periods shown in the Series’ performance chart above and in the Performance of a $10,000 Investment graph on the next page.

Performance data do not reflect insurance fees related to a variable annuity or variable life investment or the deferred sales charge that would apply to certain withdrawals of investments held for fewer than eight years. Performance shown here would have been reduced if such fees were included and the expense limitation removed. For more information about fees, consult your variable annuity or variable life prospectus.

Investments in variable products involve risk.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Series may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Series may be prepaid prior to maturity, potentially forcing the Series to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Series to obtain precise valuations of the high yield securities in its portfolio.

The Series may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The Series may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations. Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

Diversified Income Series-2

Delaware VIP® Diversified Income Series

Performance summary (continued)

If and when the Series invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Series will be subject to special risks, including counterparty risk.

Per Standard & Poor’s credit rating agency, bonds rated AA and A are more susceptible to the adverse effects of changes in circumstances and economic conditions than those in the higher-rated AAA category, but the obligor’s capacity to meet its financial commitment on the obligation is still strong. Bonds rated BBB exhibit adequate protection parameters, although adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. Bonds rated BB, B, and CCC are regarded as having significant speculative characteristics with BB indicating the least degree of speculation of the three.

Bond ratings are determined by a nationally recognized statistical rating organization (NRSRO).

Please read both the contract and underlying prospectus for specific details regarding the product’s risk profile.

*The contractual waiver period is from April 30, 2014 through April 29, 2016.

| | | | |

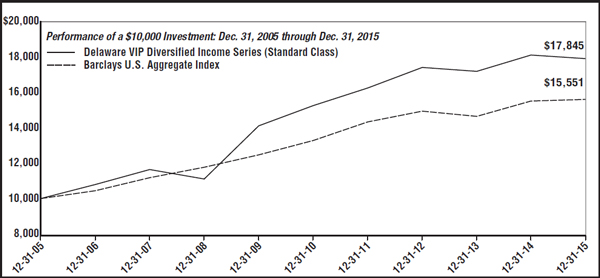

| For period beginning Dec. 31, 2005 through Dec. 31, 2015 | | Starting value | | Ending value |

— Delaware VIP Diversified Income Series (Standard Class) | | $10,000 | | $17,845 |

– – Barclays U.S. Aggregate Index | | $10,000 | | $15,551 |

The graph shows a $10,000 investment in the Delaware VIP Diversified Income Series Standard Class shares for the period from Dec. 31, 2005 through Dec. 31, 2015.

The graph also shows $10,000 invested in the Barclays U.S. Aggregate Index for the period from Dec. 31, 2005 through Dec. 31, 2015. The Barclays U.S. Aggregate Index is a broad composite that tracks the investment grade domestic bond market.

Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

Performance of Service Class shares will vary due to different charges and expenses.

Past performance is not a guarantee of future results.

| | |

| | Diversified Income Series-3 |

Delaware VIP® Trust — Delaware VIP Diversified Income Series

Disclosure of Series expenses

For the six-month period from July 1, 2015 to December 31, 2015 (Unaudited)

As a shareholder of the Series, you incur ongoing costs, which may include management fees; distribution and/or service (12b-1) fees; and other Series expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from July 1, 2015 to Dec. 31, 2015.

Actual expenses

The first section of the table shown, “Actual Series return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Series’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only. As a shareholder of the Series, you do not incur any transaction costs, such as sales charges (loads), redemption fees or exchange fees, but shareholders of other funds may incur such costs. Also, the fees related to the variable annuity investment or the deferred sales charge that could apply have not been included. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. The Series’ actual expenses shown in the table reflect fee waivers in effect for Service Class shares. The expenses shown in the table assume reinvestment of all dividends and distributions.

Expense analysis of an investment of $1,000

| | | | | | | | | | | | | | | | |

| | | Beginning

Account

Value

7/1/15 | | | Ending

Account

Value

12/31/15 | | | Annualized

Expense

Ratio | | | Expenses

Paid During

Period

7/1/15 to

12/31/15* | |

Actual Series return† | |

Standard Class | | | $1,000.00 | | | $ | 986.60 | | | | 0.65% | | | | $3.25 | |

Service Class | | | 1,000.00 | | | | 985.50 | | | | 0.90% | | | | 4.50 | |

Hypothetical 5% return (5% return before expenses) | |

Standard Class | | | $1,000.00 | | | $ | 1,021.93 | | | | 0.65% | | | | $3.31 | |

Service Class | | | 1,000.00 | | | | 1,020.67 | | | | 0.90% | | | | 4.58 | |

| * | “Expenses Paid During Period” are equal to the Series’ annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

| † | Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns. |

| | |

| | Diversified Income Series-4 |

Delaware VIP® Trust — Delaware VIP Diversified Income Series

Security type / sector allocation

As of December 31, 2015 (Unaudited)

Sector designations may be different than the sector designations presented in other Series materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one series being different than another series’ sector designations.

| | | | |

| Security type / sector | | Percentage of

net assets | |

Agency Asset-Backed Securities | | | 0.01% | |

Agency Collateralized Mortgage Obligations | | | 1.80% | |

Agency Mortgage-Backed Securities | | | 20.40% | |

Collateralized Debt Obligations | | | 1.15% | |

Commercial Mortgage-Backed Securities | | | 6.46% | |

Convertible Bonds | | | 1.52% | |

Corporate Bonds | | | 33.26% | |

Automotive | | | 0.27% | |

Banking | | | 6.34% | |

Basic Industry | | | 2.42% | |

Brokerage | | | 0.20% | |

Capital Goods | | | 1.04% | |

Communications | | | 4.29% | |

Consumer Cyclical | | | 1.49% | |

Consumer Non-Cyclical | | | 1.73% | |

Electric | | | 5.25% | |

Energy | | | 2.32% | |

Finance Companies | | | 0.60% | |

Healthcare | | | 0.81% | |

Insurance | | | 1.64% | |

Media | | | 1.04% | |

Real Estate Investment Trusts | | | 1.11% | |

Services | | | 0.46% | |

Technology | | | 0.92% | |

Transportation | | | 0.80% | |

Utilities | | | 0.53% | |

Municipal Bond | | | 0.00% | |

Non-Agency Asset-Backed Securities | | | 3.71% | |

Non-Agency Collateralized Mortgage Obligations | | | 1.39% | |

Regional Bonds | | | 0.23% | |

Senior Secured Loans | | | 9.05% | |

Sovereign Bonds | | | 1.92% | |

Supranational Banks | | | 0.38% | |

U.S. Treasury Obligations | | | 13.46% | |

Common Stock | | | 0.00% | |

Convertible Preferred Stock | | | 0.31% | |

Preferred Stock | | | 0.38% | |

Short-Term Investments | | | 13.07% | |

Total Value of Securities | | | 108.50% | |

Liabilities Net of Receivables and Other Assets | | | (8.50%) | |

Total Net Assets | | | 100.00% | |

Diversified Income Series-5

Delaware VIP® Trust — Delaware VIP Diversified Income Series

Schedule of investments

December 31, 2015

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Asset-Backed Securities – 0.01% | | | | | | | | |

Fannie Mae Grantor Trust | | | | | | | | |

Series 2003-T4 2A5 5.093% 9/26/33 f | | | 256,137 | | | $ | 281,281 | |

Fannie Mae REMIC Trust | | | | | | | | |

Series 2002-W11 AV1 0.762% 11/25/32 • | | | 1,446 | | | | 1,412 | |

| | | | | | | | |

Total Agency Asset-Backed Securities (cost $256,462) | | | | | | | 282,693 | |

| | | | | | | | |

| | |

Agency Collateralized Mortgage Obligations – 1.88% | | | | | | | | |

Fannie Mae Grantor Trust | | | | | | | | |

Series 1999-T2 A1 7.50% 1/19/39 • | | | 512 | | | | 580 | |

Series 2002-T4 A3 7.50% 12/25/41 | | | 10,109 | | | | 11,749 | |

Series 2004-T1 1A2 6.50% 1/25/44 | | | 8,158 | | | | 9,105 | |

Fannie Mae REMIC Trust | | | | | | | | |

Series 2002-W6 2A1 6.321% 6/25/42 • | | | 19,937 | | | | 23,207 | |

Series 2004-W11 1A2 6.50% 5/25/44 | | | 32,931 | | | | 38,325 | |

Fannie Mae REMICs | | | | | | | | |

Series 1996-46 ZA 7.50% 11/25/26 | | | 32,236 | | | | 36,239 | |

Series 2001-50 BA 7.00% 10/25/41 | | | 49,342 | | | | 56,573 | |

Series 2002-90 A1 6.50% 6/25/42 | | | 7,921 | | | | 8,968 | |

Series 2002-90 A2 6.50% 11/25/42 | | | 23,046 | | | | 25,857 | |

Series 2003-26 AT 5.00% 11/25/32 | | | 256,752 | | | | 260,698 | |

Series 2003-38 MP 5.50% 5/25/23 | | | 393,121 | | | | 426,849 | |

Series 2005-70 PA 5.50% 8/25/35 | | | 202,890 | | | | 227,190 | |

Series 2005-110 MB 5.50% 9/25/35 | | | 87,921 | | | | 93,570 | |

Series 2008-15 SB 6.178% 8/25/36 •S | | | 402,712 | | | | 84,213 | |

Series 2009-94 AC 5.00% 11/25/39 | | | 929,824 | | | | 1,018,375 | |

Series 2010-41 PN 4.50% 4/25/40 | | | 1,675,000 | | | | 1,799,091 | |

Series 2010-43 HJ 5.50% 5/25/40 | | | 329,002 | | | | 368,003 | |

Series 2010-96 DC 4.00% 9/25/25 | | | 2,521,374 | | | | 2,664,798 | |

Series 2010-116 Z 4.00% 10/25/40 | | | 69,624 | | | | 72,926 | |

Series 2010-129 SM 5.578% 11/25/40 •S | | | 3,253,511 | | | | 537,975 | |

Series 2011-15 SA 6.638% 3/25/41 •S | | | 3,240,791 | | | | 704,454 | |

Series 2012-122 SD 5.678% 11/25/42 •S | | | 2,108,296 | | | | 471,599 | |

Series 2013-31 MI 3.00% 4/25/33 S | | | 6,369,663 | | | | 921,034 | |

Series 2013-43 IX 4.00% 5/25/43 S | | | 11,799,135 | | | | 2,864,450 | |

Series 2013-44 DI 3.00% 5/25/33 S | | | 8,372,129 | | | | 1,211,341 | |

Series 2014-36 ZE 3.00% 6/25/44 | | | 1,668,297 | | | | 1,456,473 | |

Series 2014-68 BS 5.728% 11/25/44 •S | | | 4,378,702 | | | | 878,021 | |

Series 2014-90 SA 5.728% 1/25/45 •S | | | 12,274,235 | | | | 2,696,932 | |

Series 2015-27 SA 6.028% 5/25/45 •S | | | 1,625,271 | | | | 367,855 | |

Series 2015-44 Z 3.00% 9/25/43 | | | 3,374,173 | | | | 3,141,733 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Collateralized Mortgage Obligations (continued) | | | | | | | | |

Freddie Mac REMICs | | | | | | | | |

Series 1730 Z 7.00% 5/15/24 | | | 25,527 | | | $ | 28,629 | |

Series 2326 ZQ 6.50% 6/15/31 | | | 25,000 | | | | 28,226 | |

Series 2557 WE 5.00% 1/15/18 | | | 226,897 | | | | 233,351 | |

Series 2809 DC 4.50% 6/15/19 | | | 146,342 | | | | 151,042 | |

Series 3123 HT 5.00% 3/15/26 | | | 46,619 | | | | 50,482 | |

Series 3656 PM 5.00% 4/15/40 | | | 1,781,354 | | | | 1,944,920 | |

Series 4065 DE 3.00% 6/15/32 | | | 350,000 | | | | 349,287 | |

Series 4120 IK 3.00% 10/15/32 S | | | 6,549,921 | | | | 885,538 | |

Series 4146 IA 3.50% 12/15/32 S | | | 3,454,759 | | | | 545,527 | |

Series 4159 KS 5.82% 1/15/43 •S | | | 2,970,264 | | | | 732,806 | |

Series 4185 LI 3.00% 3/15/33 S | | | 2,035,150 | | | | 286,085 | |

Series 4191 CI 3.00% 4/15/33 S | | | 858,072 | | | | 113,858 | |

Series 4435 DY 3.00% 2/15/35 | | | 2,810,000 | | | | 2,749,301 | |

Freddie Mac Strips | | | | | | | | |

Series 326 S2 5.62% 3/15/44 •S | | | 2,194,692 | | | | 469,764 | |

Freddie Mac Structured Agency Credit Risk Debt Notes | | | | | | | | |

Series 2015-HQA2 M2 3.222% 5/25/28 • | | | 1,615,000 | | | | 1,613,787 | |

Freddie Mac Structured Pass Through Securities | | | | | | | | |

Series T-54 2A 6.50% 2/25/43 ¿ | | | 13,061 | | | | 15,257 | |

Series T-58 2A 6.50% 9/25/43 ¿ | | | 4,991 | | | | 5,668 | |

GNMA | | | | | | | | |

Series 2010-113 KE 4.50% 9/20/40 | | | 4,115,000 | | | | 4,520,243 | |

Series 2015-133 AL 3.00% 5/20/45 | | | 3,715,000 | | | | 3,543,610 | |

| | | | | | | | |

Total Agency Collateralized Mortgage Obligations (cost $41,177,408) | | | | | | | 40,745,564 | |

| | | | | | | | |

| | |

Agency Mortgage-Backed Securities – 20.40% | | | | | | | | |

Fannie Mae | | | | | | | | |

6.50% 8/1/17 | | | 2,064 | | | | 2,104 | |

Fannie Mae ARM | | | | | | | | |

2.402% 10/1/33 • | | | 2,884 | | | | 3,002 | |

2.408% 6/1/37 • | | | 4,030 | | | | 4,275 | |

2.418% 5/1/43 • | | | 1,096,093 | | | | 1,105,556 | |

2.496% 11/1/35 • | | | 103,205 | | | | 109,435 | |

2.553% 6/1/43 • | | | 369,232 | | | | 374,243 | |

2.576% 8/1/35 • | | | 20,829 | | | | 21,991 | |

2.913% 7/1/45 • | | | 646,791 | | | | 659,317 | |

2.918% 4/1/44 • | | | 630,458 | | | | 645,289 | |

3.177% 4/1/44 • | | | 1,376,860 | | | | 1,418,756 | |

3.259% 3/1/44 • | | | 1,670,780 | | | | 1,724,548 | |

3.277% 9/1/43 • | | | 1,027,542 | | | | 1,060,189 | |

6.10% 8/1/37 • | | | 54,095 | | | | 55,242 | |

Fannie Mae Relocation 15 yr | | | | | | | | |

4.00% 9/1/20 | | | 45,281 | | | | 46,630 | |

Fannie Mae Relocation 30 yr | | | | | | | | |

5.00% 11/1/33 | | | 894 | | | | 972 | |

Diversified Income Series-6

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

Fannie Mae Relocation 30 yr | | | | | | | | |

5.00% 11/1/34 | | | 2,974 | | | $ | 3,229 | |

5.00% 4/1/35 | | | 4,819 | | | | 5,181 | |

5.00% 10/1/35 | | | 16,901 | | | | 18,418 | |

5.00% 1/1/36 | | | 18,610 | | | | 20,226 | |

5.00% 2/1/36 | | | 9,007 | | | | 9,673 | |

Fannie Mae S.F. 15 yr | | | | | | | | |

2.50% 10/1/27 | | | 247,001 | | | | 250,993 | |

2.50% 12/1/27 | | | 647,779 | | | | 658,256 | |

2.50% 4/1/28 | | | 398,887 | | | | 404,174 | |

2.50% 9/1/28 | | | 1,333,915 | | | | 1,354,167 | |

3.00% 9/1/30 | | | 1,931,320 | | | | 1,991,556 | |

3.50% 6/1/26 | | | 1,344,666 | | | | 1,410,805 | |

3.50% 7/1/26 | | | 817,604 | | | | 858,614 | |

3.50% 12/1/28 | | | 325,489 | | | | 342,802 | |

4.00% 4/1/24 | | | 277,865 | | | | 293,963 | |

4.00% 2/1/25 | | | 175,820 | | | | 186,051 | |

4.00% 5/1/25 | | | 530,841 | | | | 562,964 | |

4.00% 11/1/25 | | | 2,190,083 | | | | 2,323,270 | |

4.00% 12/1/26 | | | 837,472 | | | | 888,225 | |

4.00% 1/1/27 | | | 6,266,284 | | | | 6,647,286 | |

4.00% 5/1/27 | | | 1,862,838 | | | | 1,975,988 | |

4.00% 8/1/27 | | | 1,080,000 | | | | 1,144,999 | |

4.50% 2/1/24 | | | 22,380 | | | | 24,153 | |

4.50% 10/1/24 | | | 208,595 | | | | 224,908 | |

4.50% 2/1/25 | | | 79,209 | | | | 84,331 | |

4.50% 7/1/25 | | | 107,026 | | | | 114,688 | |

6.00% 12/1/22 | | | 269,057 | | | | 289,936 | |

Fannie Mae S.F. 15 yr TBA | | | | | | | | |

2.50% 1/1/31 | | | 4,506,000 | | | | 4,541,620 | |

2.50% 2/1/31 | | | 1,171,000 | | | | 1,178,107 | |

Fannie Mae S.F. 20 yr | | | | | | | | |

3.00% 2/1/33 | | | 143,659 | | | | 147,503 | |

3.00% 8/1/33 | | | 507,703 | | | | 521,294 | |

3.50% 4/1/33 | | | 148,231 | | | | 154,968 | |

3.50% 9/1/33 | | | 719,312 | | | | 753,727 | |

4.00% 1/1/31 | | | 248,768 | | | | 265,523 | |

4.00% 2/1/31 | | | 702,586 | | | | 751,538 | |

Fannie Mae S.F. 30 yr | | | | | | | | |

3.00% 7/1/42 | | | 930,732 | | | | 934,243 | |

3.00% 10/1/42 | | | 577,928 | | | | 581,052 | |

3.00% 12/1/42 | | | 2,440,481 | | | | 2,447,705 | |

3.00% 1/1/43 | | | 6,495,702 | | | | 6,510,542 | |

3.00% 2/1/43 | | | 634,874 | | | | 636,325 | |

3.00% 5/1/43 | | | 2,320,605 | | | | 2,325,588 | |

4.00% 5/1/43 | | | 42,684 | | | | 45,482 | |

4.00% 8/1/43 | | | 443,342 | | | | 471,047 | |

4.00% 7/1/44 | | | 2,757,345 | | | | 2,935,510 | |

4.50% 7/1/36 | | | 369,915 | | | | 400,827 | |

4.50% 6/1/38 | | | 1,120,584 | | | | 1,221,005 | |

4.50% 11/1/40 | | | 889,227 | | | | 962,406 | |

4.50% 3/1/41 | | | 1,088,664 | | | | 1,178,247 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

Fannie Mae S.F. 30 yr | | | | | | | | |

4.50% 4/1/41 | | | 2,356,961 | | | $ | 2,550,417 | |

4.50% 7/1/41 | | | 696,286 | | | | 753,509 | |

4.50% 8/1/41 | | | 754,987 | | | | 828,667 | |

4.50% 10/1/41 | | | 152,592 | | | | 165,244 | |

4.50% 1/1/42 | | | 23,522,478 | | | | 25,461,895 | |

4.50% 9/1/42 | | | 14,510,519 | | | | 15,733,991 | |

4.50% 11/1/43 | | | 897,901 | | | | 971,650 | |

4.50% 2/1/44 | | | 324,832 | | | | 352,127 | |

4.50% 6/1/44 | | | 1,587,159 | | | | 1,717,277 | |

4.50% 8/1/44 | | | 543,462 | | | | 587,188 | |

4.50% 10/1/44 | | | 6,742,030 | | | | 7,311,356 | |

4.50% 2/1/45 | | | 15,178,019 | | | | 16,448,365 | |

5.00% 5/1/34 | | | 2,084 | | | | 2,304 | |

5.00% 2/1/35 | | | 193,223 | | | | 213,713 | |

5.00% 4/1/35 | | | 14,958 | | | | 16,511 | |

5.00% 10/1/35 | | | 964,231 | | | | 1,063,835 | |

5.00% 11/1/35 | | | 450,509 | | | | 496,948 | |

5.00% 2/1/37 | | | 35,571 | | | | 39,313 | |

5.00% 4/1/37 | | | 249,669 | | | | 275,286 | |

5.00% 8/1/37 | | | 724,888 | | | | 799,338 | |

5.50% 12/1/32 | | | 50,851 | | | | 57,057 | |

5.50% 2/1/33 | | | 574,157 | | | | 641,897 | |

5.50% 4/1/34 | | | 241,036 | | | | 270,930 | |

5.50% 8/1/34 | | | 37,328 | | | | 41,998 | |

5.50% 11/1/34 | | | 257,644 | | | | 289,792 | |

5.50% 12/1/34 | | | 47,651 | | | | 53,629 | |

5.50% 1/1/35 | | | 940,095 | | | | 1,058,160 | |

5.50% 3/1/35 | | | 133,005 | | | | 149,856 | |

5.50% 6/1/35 | | | 175,382 | | | | 197,006 | |

5.50% 12/1/35 | | | 17,734 | | | | 19,925 | |

5.50% 1/1/36 | | | 1,189,194 | | | | 1,338,016 | |

5.50% 4/1/36 | | | 753,391 | | | | 844,858 | |

5.50% 7/1/36 | | | 96,880 | | | | 108,994 | |

5.50% 9/1/36 | | | 2,977,620 | | | | 3,345,360 | |

5.50% 10/1/36 | | | 522,262 | | | | 596,778 | |

5.50% 11/1/36 | | | 228,010 | | | | 254,594 | |

5.50% 1/1/37 | | | 1,034,578 | | | | 1,157,047 | |

5.50% 2/1/37 | | | 15,444 | | | | 17,247 | |

5.50% 4/1/37 | | | 1,947,459 | | | | 2,178,076 | |

5.50% 8/1/37 | | | 842,102 | | | | 947,623 | |

5.50% 9/1/37 | | | 1,169,882 | | | | 1,308,053 | |

5.50% 1/1/38 | | | 98,610 | | | | 111,733 | |

5.50% 2/1/38 | | | 743,660 | | | | 835,436 | |

5.50% 3/1/38 | | | 483,403 | | | | 539,081 | |

5.50% 6/1/38 | | | 2,086,840 | | | | 2,330,725 | |

5.50% 9/1/38 | | | 914,511 | | | | 1,027,643 | |

5.50% 12/1/38 | | | 909,149 | | | | 1,038,632 | |

5.50% 1/1/39 | | | 3,505,501 | | | | 3,948,490 | |

5.50% 2/1/39 | | | 3,317,946 | | | | 3,728,247 | |

5.50% 10/1/39 | | | 2,291,219 | | | | 2,559,389 | |

| | |

| | Diversified Income Series-7 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

Fannie Mae S.F. 30 yr | | | | | | | | |

5.50% 7/1/40 | | | 1,839,261 | | | $ | 2,060,076 | |

5.50% 9/1/41 | | | 8,616,405 | | | | 9,625,751 | |

6.00% 3/1/29 | | | 608 | | | | 694 | |

6.00% 6/1/30 | | | 2,256 | | | | 2,546 | |

6.00% 4/1/35 | | | 3,740 | | | | 4,251 | |

6.00% 1/1/36 | | | 2,980 | | | | 3,367 | |

6.00% 6/1/36 | | | 88,541 | | | | 100,192 | |

6.00% 9/1/36 | | | 517,079 | | | | 585,657 | |

6.00% 11/1/36 | | | 10,536 | | | | 11,889 | |

6.00% 12/1/36 | | | 281,172 | | | | 318,298 | |

6.00% 2/1/37 | | | 306,492 | | | | 346,792 | |

6.00% 3/1/37 | | | 336,405 | | | | 380,712 | |

6.00% 5/1/37 | | | 763,009 | | | | 863,417 | |

6.00% 6/1/37 | | | 56,084 | | | | 63,828 | |

6.00% 7/1/37 | | | 56,279 | | | | 63,509 | |

6.00% 8/1/37 | | | 612,270 | | | | 693,620 | |

6.00% 9/1/37 | | | 98,533 | | | | 111,468 | |

6.00% 11/1/37 | | | 121,526 | | | | 137,188 | |

6.00% 5/1/38 | | | 1,905,871 | | | | 2,161,060 | |

6.00% 7/1/38 | | | 33,213 | | | | 37,479 | |

6.00% 8/1/38 | | | 159,066 | | | | 179,501 | |

6.00% 9/1/38 | | | 274,492 | | | | 310,636 | |

6.00% 10/1/38 | | | 1,028,621 | | | | 1,161,959 | |

6.00% 11/1/38 | | | 239,863 | | | | 273,153 | |

6.00% 1/1/39 | | | 456,934 | | | | 517,534 | |

6.00% 7/1/39 | | | 14,634 | | | | 16,514 | |

6.00% 9/1/39 | | | 4,845,027 | | | | 5,476,566 | |

6.00% 3/1/40 | | | 399,964 | | | | 452,496 | |

6.00% 7/1/40 | | | 1,651,387 | | | | 1,865,722 | |

6.00% 9/1/40 | | | 355,159 | | | | 401,721 | |

6.00% 11/1/40 | | | 156,943 | | | | 178,925 | |

6.00% 5/1/41 | | | 4,047,672 | | | | 4,579,259 | |

6.50% 2/1/36 | | | 196,419 | | | | 224,477 | |

6.50% 3/1/37 | | | 310,023 | | | | 363,518 | |

7.50% 3/1/32 | | | 247 | | | | 270 | |

7.50% 4/1/32 | | | 834 | | | | 966 | |

Fannie Mae S.F. 30 yr TBA | | | | | | | | |

3.00% 1/1/46 | | | 83,637,000 | | | | 83,637,761 | |

3.00% 2/1/46 | | | 105,414,000 | | | | 105,204,953 | |

4.50% 1/1/46 | | | 15,746,000 | | | | 17,003,712 | |

Freddie Mac ARM | | | | | | | | |

2.347% 8/1/37 • | | | 2,715 | | | | 2,870 | |

2.479% 7/1/36 • | | | 66,124 | | | | 70,132 | |

2.521% 1/1/44 • | | | 3,125,300 | | | | 3,185,140 | |

2.565% 2/1/37 • | | | 165,575 | | | | 174,555 | |

2.567% 10/1/37 • | | | 1,429 | | | | 1,512 | |

2.57% 4/1/34 • | | | 959 | | | | 1,016 | |

2.592% 12/1/33 • | | | 24,993 | | | | 26,261 | |

2.65% 10/1/37 • | | | 12,752 | | | | 13,418 | |

2.727% 6/1/37 • | | | 253,366 | | | | 271,069 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

Freddie Mac ARM | | | | | | | | |

2.832% 9/1/45 • | | | 5,382,294 | | | $ | 5,489,275 | |

2.953% 11/1/44 • | | | 514,117 | | | | 527,509 | |

2.959% 10/1/45 • | | | 1,355,936 | | | | 1,381,600 | |

Freddie Mac Relocation 30 yr | | | | | | | | |

5.00% 9/1/33 | | | 4,606 | | | | 4,993 | |

Freddie Mac S.F. 15 yr | | | | | | | | |

3.50% 11/1/25 | | | 239,496 | | | | 251,065 | |

3.50% 6/1/26 | | | 262,434 | | | | 275,102 | |

3.50% 10/1/26 | | | 276,413 | | | | 290,473 | |

3.50% 1/1/27 | | | 240,083 | | | | 251,633 | |

4.00% 5/1/25 | | | 151,602 | | | | 160,069 | |

4.00% 8/1/25 | | | 314,944 | | | | 332,694 | |

4.00% 11/1/26 | | | 614,863 | | | | 649,294 | |

4.50% 5/1/20 | | | 174,774 | | | | 181,960 | |

4.50% 9/1/26 | | | 614,963 | | | | 658,758 | |

5.00% 6/1/18 | | | 41,406 | | | | 42,823 | |

Freddie Mac S.F. 20 yr | | | | | | | | |

3.50% 1/1/34 | | | 1,275,926 | | | | 1,334,301 | |

3.50% 9/1/35 | | | 1,204,245 | | | | 1,256,040 | |

4.00% 8/1/35 | | | 287,863 | | | | 307,463 | |

4.00% 10/1/35 | | | 1,465,619 | | | | 1,565,419 | |

Freddie Mac S.F. 30 yr | | | | | | | | |

3.00% 10/1/42 | | | 1,081,363 | | | | 1,082,092 | |

3.00% 11/1/42 | | | 1,008,808 | | | | 1,009,736 | |

4.50% 4/1/39 | | | 236,938 | | | | 258,681 | |

4.50% 10/1/39 | | | 672,090 | | | | 724,972 | |

4.50% 4/1/41 | | | 3,221,596 | | | | 3,476,775 | |

5.00% 3/1/34 | | | 12,985 | | | | 14,458 | |

5.50% 3/1/34 | | | 113,369 | | | | 126,003 | |

5.50% 12/1/34 | | | 103,587 | | | | 115,368 | |

5.50% 6/1/36 | | | 63,196 | | | | 70,258 | |

5.50% 11/1/36 | | | 131,321 | | | | 145,985 | |

5.50% 12/1/36 | | | 29,739 | | | | 33,051 | |

5.50% 9/1/37 | | | 141,918 | | | | 157,854 | |

5.50% 4/1/38 | | | 501,573 | | | | 557,918 | |

5.50% 6/1/38 | | | 74,357 | | | | 82,830 | |

5.50% 7/1/38 | | | 514,549 | | | | 572,569 | |

5.50% 6/1/39 | | | 528,791 | | | | 588,441 | |

5.50% 3/1/40 | | | 351,987 | | | | 391,642 | |

5.50% 8/1/40 | | | 261,586 | | | | 291,053 | |

5.50% 1/1/41 | | | 356,303 | | | | 396,424 | |

5.50% 6/1/41 | | | 3,983,783 | | | | 4,431,494 | |

6.00% 2/1/36 | | | 542,647 | | | | 618,966 | |

6.00% 1/1/38 | | | 133,205 | | | | 149,788 | |

6.00% 6/1/38 | | | 375,752 | | | | 423,681 | |

6.00% 8/1/38 | | | 598,606 | | | | 684,239 | |

6.00% 5/1/40 | | | 802,813 | | | | 911,025 | |

6.00% 7/1/40 | | | 847,634 | | | | 956,066 | |

6.50% 8/1/38 | | | 110,977 | | | | 126,387 | |

6.50% 4/1/39 | | | 578,340 | | | | 658,647 | |

| | |

| | Diversified Income Series-8 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

GNMA I S.F. 30 yr | | | | | | | | |

5.00% 6/15/40 | | | 201,517 | | | $ | 222,443 | |

7.00% 12/15/34 | | | 146,366 | | | | 173,023 | |

| | | | | | | | |

Total Agency Mortgage-Backed Securities (cost $441,436,582) | | | | | | | 442,649,620 | |

| | | | | | | | |

| | |

Collateralized Debt Obligations – 1.15% | | | | | | | | |

Avery Point III CLO | | | | | | | | |

Series 2013-3A A 144A 1.715% 1/18/25 #• | | | 2,200,000 | | | | 2,163,260 | |

Benefit Street Partners CLO IV | | | | | | | | |

Series 2014-IVA A1A 144A 1.807% 7/20/26 #• | | | 5,900,000 | | | | 5,848,670 | |

Carlyle Global Market Strategies CLO | | | | | | | | |

Series 2014-2A A 144A 1.832% 5/15/25 #• | | | 2,750,000 | | | | 2,724,700 | |

Cent CLO | | | | | | | | |

Series 2013-20A A 144A 1.80% 1/25/26 #• | | | 667,000 | | | | 656,595 | |

Series 2014-21A A1B 144A 1.713% 7/27/26 #• | | | 2,200,000 | | | | 2,169,860 | |

Magnetite | | | | | | | | |

Series 2014-9A A1 144A 1.74% 7/25/26 #• | | | 6,040,000 | | | | 5,972,352 | |

Neuberger Berman CLO XVII | | | | | | | | |

Series 2014-17A A 144A 1.804% 8/4/25 #• | | | 2,150,000 | | | | 2,130,435 | |

Neuberger Berman CLO XIX | | | | | | | | |

Series 2015-19A A1 144A 1.709% 7/15/27 #• | | | 3,300,000 | | | | 3,263,370 | |

| | | | | | | | |

Total Collateralized Debt Obligations (cost $25,166,129) | | | | | | | 24,929,242 | |

| | | | | | | | |

| | |

Commercial Mortgage-Backed Securities – 6.46% | | | | | | | | |

Banc of America Commercial Mortgage Trust | | | | | | | | |

Series 2006-1 AM 5.421% 9/10/45 • | | | 179,124 | | | | 178,942 | |

Series 2007-4 AM 5.809% 2/10/51 • | | | 1,330,000 | | | | 1,390,155 | |

Bear Stearns Commercial Mortgage Securities Trust | | | | | | | | |

Series 2007-PW18 A4 5.70% 6/11/50 | | | 1,185,000 | | | | 1,235,300 | |

CD Commercial Mortgage Trust | | | | | | | | |

Series 2005-CD1 C 5.284% 7/15/44 • | | | 65,137 | | | | 65,113 | |

CFCRE Commercial Mortgage Trust | | | | | | | | |

Series 2011-C1 A2 144A 3.759% 4/15/44 # | | | 508,811 | | | | 509,831 | |

Citigroup Commercial Mortgage Trust | | | | | | | | |

Series 2007-C6 AM 5.71% 12/10/49 • | | | 1,230,000 | | | | 1,256,854 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Commercial Mortgage-Backed Securities (continued) | | | | | | | | |

Citigroup Commercial Mortgage Trust | | | | | | | | |

Series 2014-GC25 A4 3.635% 10/10/47 | | | 2,275,000 | | | $ | 2,312,741 | |

Series 2015-GC27 A5 3.137% 2/10/48 | | | 5,210,000 | | | | 5,084,606 | |

COMM Mortgage Trust | | | | | | | | |

Series 2013-CR6 A4 3.101% 3/10/46 | | | 1,565,000 | | | | 1,564,435 | |

Series 2014-CR16 A4 4.051% 4/10/47 | | | 2,470,000 | | | | 2,596,455 | |

Series 2014-CR19 A5 3.796% 8/10/47 | | | 2,850,000 | | | | 2,936,978 | |

Series 2014-CR20 A4 3.59% 11/10/47 | | | 980,000 | | | | 992,921 | |

Series 2014-CR20 AM 3.938% 11/10/47 | | | 7,775,000 | | | | 7,967,035 | |

Series 2014-CR21 A3 3.528% 12/10/47 | | | 1,525,000 | | | | 1,537,180 | |

Series 2015-3BP A 144A 3.178% 2/10/35 # | | | 3,960,000 | | | | 3,880,578 | |

Series 2015-CR23 A4 3.497% 5/10/48 | | | 3,450,000 | | | | 3,461,670 | |

Commercial Mortgage Trust | | | | | | | | |

Series 2007-GG9 AM 5.475% 3/10/39 | | | 1,345,000 | | | | 1,375,984 | |

DB-UBS Mortgage Trust | | | | | | | | |

Series 2011-LC1A A3 144A 5.002% 11/10/46 # | | | 1,910,000 | | | | 2,105,359 | |

Series 2011-LC1A C 144A 5.663% 11/10/46 #• | | | 2,000,000 | | | | 2,201,111 | |

Freddie Mac Multifamily Structured Pass Through Certificates | | | | | | | | |

Series K038 A2 3.389% 3/25/24 ¿ | | | 3,110,000 | | | | 3,221,757 | |

FREMF Mortgage Trust | | | | | | | | |

Series 2011-K10 B 144A 4.631% 11/25/49 #• | | | 1,335,000 | | | | 1,399,049 | |

Series 2011-K13 B 144A 4.60% 1/25/48 #• | | | 1,735,000 | | | | 1,837,930 | |

Series 2011-K15 B 144A 4.948% 8/25/44 #• | | | 195,000 | | | | 209,551 | |

Series 2012-K18 B 144A 4.255% 1/25/45 #• | | | 1,020,000 | | | | 1,049,080 | |

Series 2012-K19 B 144A 4.036% 5/25/45 #• | | | 390,000 | | | | 396,654 | |

Series 2012-K22 B 144A 3.687% 8/25/45 #• | | | 1,730,000 | | | | 1,715,527 | |

Series 2012-K22 C 144A 3.687% 8/25/45 #• | | | 1,400,000 | | | | 1,396,939 | |

Series 2012-K707 B 144A 3.883% 1/25/47 #• | | | 700,000 | | | | 713,590 | |

| | |

| | Diversified Income Series-9 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Commercial Mortgage-Backed Securities (continued) | | | | | | | | |

FREMF Mortgage Trust | | | | | | | | |

Series 2012-K708 B 144A 3.754% 2/25/45 #• | | | 2,960,000 | | | $ | 3,013,289 | |

Series 2012-K708 C 144A 3.754% 2/25/45 #• | | | 530,000 | | | | 535,592 | |

Series 2012-K711 B 144A 3.562% 8/25/45 #• | | | 2,030,000 | | | | 2,052,773 | |

Series 2013-K25 C 144A 3.618% 11/25/45 #• | | | 1,480,000 | | | | 1,400,923 | |

Series 2013-K26 C 144A 3.599% 12/25/45 #• | | | 860,000 | | | | 829,723 | |

Series 2013-K30 C 144A 3.556% 6/25/45 #• | | | 1,560,000 | | | | 1,453,071 | |

Series 2013-K31 C 144A 3.627% 7/25/46 #• | | | 3,082,000 | | | | 2,898,556 | |

Series 2013-K33 B 144A 3.503% 8/25/46 #• | | | 1,315,000 | | | | 1,272,138 | |

Series 2013-K33 C 144A 3.503% 8/25/46 #• | | | 450,000 | | | | 428,029 | |

Series 2013-K712 B 144A 3.371% 5/25/45 #• | | | 4,270,000 | | | | 4,283,451 | |

Series 2013-K713 B 144A 3.165% 4/25/46 #• | | | 2,640,000 | | | | 2,624,718 | |

Series 2013-K713 C 144A 3.165% 4/25/46 #• | | | 2,640,000 | | | | 2,541,703 | |

Series 2014-K716 C 144A 3.953% 8/25/47 #• | | | 1,105,000 | | | | 1,098,039 | |

Series 2015-K47 B 144A 3.60% 6/25/48 #• | | | 1,100,000 | | | | 979,607 | |

GRACE Mortgage Trust | | | | | | | | |

Series 2014-GRCE A 144A 3.369% 6/10/28 # | | | 6,755,000 | | | | 6,918,688 | |

GS Mortgage Securities Trust | | | | | | | | |

Series 2010-C1 A2 144A 4.592% 8/10/43 # | | | 3,090,000 | | | | 3,316,917 | |

Series 2010-C1 C 144A 5.635% 8/10/43 #• | | | 1,010,000 | | | | 1,094,253 | |

Series 2014-GC24 A5 3.931% 9/10/47 | | | 2,970,000 | | | | 3,090,141 | |

Series 2015-GC32 A4 3.764% 7/10/48 | | | 925,000 | | | | 945,374 | |

Hilton USA Trust | | | | | | | | |

Series 2013-HLT AFX 144A 2.662% 11/5/30 # | | | 825,000 | | | | 825,618 | |

Series 2013-HLT BFX 144A 3.367% 11/5/30 # | | | 3,810,000 | | | | 3,812,833 | |

Houston Galleria Mall Trust | | | | | | | | |

Series 2015-HGLR A1A2 144A 3.087% 3/5/37 # | | | 3,890,000 | | | | 3,786,860 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Commercial Mortgage-Backed Securities (continued) | | | | | | | | |

JPMBB Commercial Mortgage Securities Trust | | | | | | | | |

Series 2014-C18 A1 1.254% 2/15/47 | | | 1,039,051 | | | $ | 1,028,316 | |

Series 2014-C22 B 4.561% 9/15/47 • | | | 645,000 | | | | 655,473 | |

JPMorgan Chase Commercial Mortgage Securities Trust | | | | | | | | |

Series 2005-CB11 E 5.498% 8/12/37 • | | | 600,000 | | | | 644,617 | |

Series 2005-LDP5 D 5.522% 12/15/44 • | | | 1,110,000 | | | | 1,107,230 | |

Series 2006-LDP8 AM 5.44% 5/15/45 | | | 4,004,000 | | | | 4,073,810 | |

Series 2011-C5 C 144A 5.323% 8/15/46 #• | | | 1,100,000 | | | | 1,170,787 | |

Series 2015-JP1 A5 3.914% 1/15/49 | | | 2,720,000 | | | | 2,801,687 | |

LB-UBS Commercial Mortgage Trust | | | | | | | | |

Series 2004-C1 A4 4.568% 1/15/31 | | | 68,385 | | | | 68,615 | |

Series 2006-C6 AJ 5.452% 9/15/39 • | | | 2,390,000 | | | | 2,404,823 | |

Series 2006-C6 AM 5.413% 9/15/39 | | | 1,590,000 | | | | 1,619,189 | |

Morgan Stanley Bank of America Merrill Lynch Trust | | | | | | | | |

Series 2014-C19 AS 3.832% 12/15/47 | | | 610,000 | | | | 615,852 | |

Series 2015-C22 A3 3.046% 4/15/48 | | | 1,210,000 | | | | 1,169,295 | |

Series 2015-C23 A4 3.719% 7/15/50 | | | 4,090,000 | | | | 4,167,934 | |

Series 2015-C26 A5 3.531% 10/15/48 | | | 2,390,000 | | | | 2,390,588 | |

Morgan Stanley Capital I Trust | | | | | | | | |

Series 2005-HQ7 C 5.191% 11/14/42 • | | | 1,997,300 | | | | 1,994,263 | |

Series 2006-HQ10 B 5.448% 11/12/41 • | | | 1,025,000 | | | | 984,296 | |

Series 2006-TOP21 B 144A 5.312% 10/12/52 #• | | | 800,000 | | | | 798,531 | |

Series 2006-TOP23 A4 5.847% 8/12/41 • | | | 1,215,826 | | | | 1,224,358 | |

TimberStar Trust I | | | | | | | | |

Series 2006-1A A 144A 5.668% 10/15/36 # | | | 1,510,000 | | | | 1,548,690 | |

Wells Fargo Commercial Mortgage Trust | | | | | | | | |

Series 2012-LC5 A3 2.918% 10/15/45 | | | 3,720,000 | | | | 3,697,744 | |

Series 2015-NXS3 A4 3.617% 9/15/57 | | | 1,585,000 | | | | 1,600,435 | |

WF-RBS Commercial Mortgage Trust | | | | | | | | |

Series 2014-C23 A5 3.917% 10/15/57 | | | 610,000 | | | | 633,594 | |

| | | | | | | | |

Total Commercial Mortgage-Backed Securities (cost $143,109,668) | | | | | | | 140,195,748 | |

| | | | | | | | |

| | |

| | Diversified Income Series-10 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Convertible Bonds – 1.52% | | | | | | | | |

Alaska Communications Systems Group 6.25% exercise price $10.28, expiration date 4/27/18 @ | | | 1,504,000 | | | $ | 1,517,160 | |

Ares Capital 5.75% exercise price $18.36, expiration date 2/1/16 | | | 453,000 | | | | 453,849 | |

BGC Partners 4.50% exercise price $9.84, expiration date 7/13/16 | | | 1,195,000 | | | | 1,298,816 | |

BioMarin Pharmaceutical 1.50% exercise price $94.15, expiration date 10/13/20 | | | 370,000 | | | | 496,263 | |

Blackstone Mortgage Trust 5.25% exercise price $28.66, expiration date 12/1/18 | | | 1,497,000 | | | | 1,526,940 | |

Blucora 4.25% exercise price $21.66, expiration date 3/29/19 | | | 652,000 | | | | 543,605 | |

Campus Crest Communities Operating Partnership 144A 4.75% exercise price $12.56, expiration date 10/11/18 #@ | | | 1,232,000 | | | | 1,220,450 | |

Cardtronics 1.00% exercise price $52.35, expiration date 11/27/20 | | | 1,276,000 | | | | 1,190,667 | |

Cemex 3.72% exercise price $11.90, expiration date 3/15/20 | | | 874,000 | | | | 689,914 | |

Chart Industries 2.00% exercise price $69.03, expiration date 7/30/18 @ | | | 1,314,000 | | | | 1,143,180 | |

Ciena 144A 3.75% exercise price $20.17, expiration date 10/15/18 # | | | 632,000 | | | | 786,840 | |

Clearwire Communications 144A 8.25% exercise price $7.08, expiration date 11/30/40 #@ | | | 263,000 | | | | 263,657 | |

GAIN Capital Holdings 4.125% exercise price $12.00, expiration date 11/30/18 @ | | | 699,000 | | | | 702,932 | |

General Cable 4.50% exercise price $33.38, expiration date 11/15/29 @f | | | 1,272,000 | | | | 784,665 | |

Gilead Sciences 1.625% exercise price $22.44, expiration date 4/29/16 | | | 283,000 | | | | 1,265,011 | |

HealthSouth 2.00% exercise price $38.08, expiration date 11/30/43 | | | 947,000 | | | | 1,025,127 | |

Helix Energy Solutions Group 3.25% exercise price $25.02, expiration date 3/12/32 | | | 925,000 | | | | 733,641 | |

Hologic 2.00% exercise price $31.17, expiration date 2/27/42 f | | | 611,000 | | | | 817,976 | |

Huron Consulting Group 1.25% exercise price $79.89, expiration date 9/27/19 | | | 321,000 | | | | 319,194 | |

inContact 144A 2.50% exercise price $14.23, expiration date 4/1/22 # | | | 1,104,000 | | | | 1,043,970 | |

Infinera 1.75% exercise price $12.58, expiration date 5/30/18 | | | 278,000 | | | | 430,205 | |

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |

Convertible Bonds (continued) | | | | | | | | |

Intel 3.25% exercise price $21.47, expiration date 8/1/39 | | | 298,000 | | | $ | 496,171 | |

Jefferies Group 3.875% exercise price $44.53, expiration date 10/31/29 | | | 836,000 | | | | 834,955 | |

Liberty Interactive 144A 1.00% exercise price $64.23, expiration date 9/28/43 # | | | 1,052,000 | | | | 909,323 | |

Meritor 4.00% exercise price $26.73, expiration date 2/12/27 f | | | 1,382,000 | | | | 1,313,764 | |

Microchip Technology 144A 1.625% exercise price $66.61, expiration date 2/13/25 # | | | 531,000 | | | | 530,336 | |

New Mountain Finance 5.00% exercise price $15.93, expiration date 6/14/19 @ | | | 205,000 | | | | 201,413 | |

Novellus Systems 2.625% exercise price $34.37, expiration date 5/14/41 | | | 648,000 | | | | 1,528,065 | |

NuVasive 2.75% exercise price $42.13, expiration date 6/30/17 | | | 1,111,000 | | | | 1,521,376 | |

NXP Semiconductors 1.00% exercise price $102.84, expiration date 11/27/19 | | | 616,000 | | | | 677,985 | |

PROS Holdings 144A 2.00% exercise price $33.79, expiration date 11/27/19 # | | | 1,109,000 | | | | 1,088,206 | |

Spectrum Pharmaceuticals 2.75% exercise price $10.53, expiration date 12/13/18 @ | | | 841,000 | | | | 741,131 | |

Spirit Realty Capital 3.75% exercise price $13.10, expiration date 5/13/21 @ | | | 1,357,000 | | | | 1,286,612 | |

Titan Machinery 3.75% exercise price $43.17, expiration date 4/30/19 @ | | | 218,000 | | | | 143,744 | |

TPG Specialty Lending 4.50% exercise price $25.83, expiration date 12/15/19 @ | | | 792,000 | | | | 783,090 | |

Vector Group 1.75% exercise price $24.64, expiration date 4/15/20 • | | | 1,020,000 | | | | 1,171,087 | |

Vector Group 2.50% exercise price $15.98, expiration date 1/14/19 • | | | 408,000 | | | | 627,217 | |

VEREIT 3.75% exercise price $14.99, expiration date 12/14/20 @ | | | 1,059,000 | | | | 952,443 | |

| | | | | | | | |

Total Convertible Bonds (cost $32,269,410) | | | | | | | 33,060,980 | |

| | | | | | | | |

| | |

Corporate Bonds – 33.26% | | | | | | | | |

Automotive – 0.27% | | | | | | | | |

American Axle & Manufacturing 6.25% 3/15/21 | | | 1,156,000 | | | | 1,200,795 | |

Ford Motor 7.45% 7/16/31 | | | 2,320,000 | | | | 2,869,961 | |

Lear 5.25% 1/15/25 | | | 1,175,000 | | | | 1,201,437 | |

| | |

| | Diversified Income Series-11 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Automotive (continued) | | | | | | | | |

Meritor 6.75% 6/15/21 | | | 516,000 | | | $ | 477,300 | |

| | | | | | | | |

| | | | | | | 5,749,493 | |

| | | | | | | | |

Banking – 6.34% | | | | | | | | |

ANZ New Zealand International 144A 2.60% 9/23/19 # | | | 500,000 | | | | 501,859 | |

Banco Nacional de Comercio Exterior 144A 4.375% 10/14/25 # | | | 2,030,000 | | | | 2,009,700 | |

Bank of America | | | | | | | | |

3.875% 8/1/25 | | | 4,350,000 | | | | 4,424,598 | |

3.95% 4/21/25 | | | 9,070,000 | | | | 8,849,064 | |

Bank of New York Mellon 2.15% 2/24/20 | | | 535,000 | | | | 529,505 | |

BB&T 5.25% 11/1/19 | | | 10,852,000 | | | | 11,891,662 | |

BBVA Bancomer 144A 7.25% 4/22/20 # | | | 765,000 | | | | 816,064 | |

Branch Banking & Trust 3.80% 10/30/26 | | | 3,350,000 | | | | 3,405,540 | |

Citizens Financial Group 4.30% 12/3/25 | | | 2,050,000 | | | | 2,064,881 | |

City National 5.25% 9/15/20 | | | 2,075,000 | | | | 2,308,994 | |

Compass Bank 3.875% 4/10/25 | | | 2,280,000 | | | | 2,093,756 | |

Cooperatieve Centrale Raiffeisen-Boerenleenbank | | | | | | | | |

2.50% 9/4/20 | | NOK | 5,290,000 | | | | 626,838 | |

4.25% 1/13/22 | | AUD | 1,073,000 | | | | 804,291 | |

Credit Suisse Group 144A 6.25% 12/29/49 #• | | | 845,000 | | | | 847,002 | |

Credit Suisse Group Funding Guernsey | | | | | | | | |

144A 3.125% 12/10/20 # | | | 1,985,000 | | | | 1,978,223 | |

144A 3.75% 3/26/25 # | | | 2,755,000 | | | | 2,669,997 | |

Export-Import Bank of Korea | | | | | | | | |

144A 2.711% 12/5/19 # | | CAD | 210,000 | | | | 156,642 | |

144A 3.00% 5/22/18 # | | NOK | 1,100,000 | | | | 128,288 | |

Fifth Third Bancorp 2.875% 7/27/20 | | | 975,000 | | | | 974,952 | |

Finnvera 144A 2.375% 6/4/25 # | | | 3,455,000 | | | | 3,350,027 | |

Goldman Sachs Group | | | | | | | | |

3.55% 8/21/19 • | | AUD | 550,000 | | | | 401,207 | |

3.55% 2/12/21 | | CAD | 400,000 | | | | 305,329 | |

5.20% 12/17/19 | | NZD | 612,000 | | | | 433,300 | |

Industrial & Commercial Bank of China 144A 4.875% 9/21/25 # | | | 2,190,000 | | | | 2,223,818 | |

ING Groep | | | | | | | | |

6.00% 12/29/49 • | | | 400,000 | | | | 402,000 | |

6.50% 12/29/49 • | | | 1,545,000 | | | | 1,516,997 | |

JPMorgan Chase | | | | | | | | |

0.953% 1/28/19 • | | | 1,124,000 | | | | 1,116,522 | |

3.50% 12/18/26 | | GBP | 264,000 | | | | 401,468 | �� |

4.25% 11/2/18 | | NZD | 1,840,000 | | | | 1,273,985 | |

KeyBank | | | | | | | | |

3.30% 6/1/25 | | | 1,665,000 | | | | 1,648,791 | |

6.95% 2/1/28 | | | 4,255,000 | | | | 5,281,242 | |

Lloyds Banking Group 4.50% 11/4/24 | | | 480,000 | | | | 488,144 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Banking (continued) | | | | | | | | |

Lloyds Banking Group | | | | | | | | |

144A 4.582% 12/10/25 # | | | 1,455,000 | | | $ | 1,461,431 | |

7.50% 4/30/49 • | | | 1,695,000 | | | | 1,809,413 | |

Morgan Stanley | | | | | | | | |

1.17% 1/24/19 • | | | 1,126,000 | | | | 1,123,947 | |

3.125% 8/5/21 | | CAD | 972,000 | | | | 725,171 | |

3.95% 4/23/27 | | | 340,000 | | | | 330,740 | |

5.00% 9/30/21 | | AUD | 1,087,000 | | | | 830,398 | |

National City Bank 0.822% 6/7/17 • | | | 1,905,000 | | | | 1,893,705 | |

Nordea Bank 144A 6.125% 12/29/49 #• | | | 1,895,000 | | | | 1,857,479 | |

PNC Bank | | | | | | | | |

1.85% 7/20/18 | | | 700,000 | | | | 698,890 | |

2.60% 7/21/20 | | | 705,000 | | | | 705,280 | |

3.30% 10/30/24 | | | 2,190,000 | | | | 2,194,917 | |

6.875% 4/1/18 | | | 5,710,000 | | | | 6,259,342 | |

Santander Holdings USA 3.45% 8/27/18 | | | 1,650,000 | | | | 1,678,492 | |

Santander Issuances 5.179% 11/19/25 | | | 2,600,000 | | | | 2,565,493 | |

Santander UK 144A 5.00% 11/7/23 # | | | 2,905,000 | | | | 3,028,901 | |

Santander UK Group Holdings | | | | | | | | |

2.875% 10/16/20 | | | 1,000,000 | | | | 995,211 | |

144A 4.75% 9/15/25 # | | | 1,305,000 | | | | 1,294,089 | |

Societe Generale | | | | | | | | |

144A 4.75% 11/24/25 # | | | 2,190,000 | | | | 2,123,242 | |

144A 5.625% 11/24/45 # | | | 435,000 | | | | 418,243 | |

State Street | | | | | | | | |

2.55% 8/18/20 | | | 2,245,000 | | | | 2,274,423 | |

3.10% 5/15/23 | | | 1,360,000 | | | | 1,345,271 | |

3.55% 8/18/25 | | | 2,510,000 | | | | 2,592,037 | |

SunTrust Banks 2.35% 11/1/18 | | | 685,000 | | | | 689,035 | |

SVB Financial Group 3.50% 1/29/25 | | | 1,350,000 | | | | 1,295,887 | |

Toronto-Dominion Bank 2.50% 12/14/20 | | | 2,515,000 | | | | 2,516,884 | |

Turkiye Garanti Bankasi 144A 4.75% 10/17/19 # | | | 2,947,000 | | | | 2,935,875 | |

U.S. Bancorp 3.60% 9/11/24 @ | | | 2,640,000 | | | | 2,685,714 | |

U.S. Bank 2.80% 1/27/25 | | | 2,295,000 | | | | 2,235,518 | |

UBS Group Funding Jersey 144A 4.125% 9/24/25 # | | | 2,645,000 | | | | 2,647,507 | |

USB Capital IX 3.50% 10/29/49 @• | | | 7,185,000 | | | | 5,541,431 | |

Wells Fargo | | | | | | | | |

2.55% 12/7/20 | | | 2,785,000 | | | | 2,773,219 | |

3.50% 9/12/29 | | GBP | 654,000 | | | | 982,764 | |

4.30% 7/22/27 | | | 3,155,000 | | | | 3,227,325 | |

Woori Bank | | | | | | | | |

144A 2.875% 10/2/18 # | | | 1,600,000 | | | | 1,623,696 | |

144A 4.75% 4/30/24 # | | | 2,000,000 | | | | 2,050,476 | |

Zions Bancorporation 4.50% 6/13/23 | | | 2,150,000 | | | | 2,212,296 | |

| | | | | | | | |

| | | | | | | 137,548,428 | |

| | | | | | | | |

| | |

| | Diversified Income Series-12 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Basic Industry – 2.42% | | | | | | | | |

ArcelorMittal | | | | | | | | |

6.125% 6/1/25 | | | 1,135,000 | | | $ | 831,387 | |

10.85% 6/1/19 | | | 2,685,000 | | | | 2,530,613 | |

Ball 5.25% 7/1/25 | | | 1,610,000 | | | | 1,652,263 | |

BHP Billiton Finance 3.25% 9/25/24 | | GBP | 565,000 | | | | 814,129 | |

BHP Billiton Finance USA 144A 6.25% 10/19/75 #• | | | 1,630,000 | | | | 1,599,437 | |

CF Industries 6.875% 5/1/18 | | | 3,830,000 | | | | 4,152,126 | |

Corp Nacional del Cobre de Chile 144A 4.50% 9/16/25 # | | | 2,255,000 | | | | 2,129,232 | |

Dow Chemical 8.55% 5/15/19 | | | 9,161,000 | | | | 10,805,647 | |

Georgia-Pacific 8.00% 1/15/24 | | | 5,210,000 | | | | 6,598,830 | |

Gerdau Holdings 144A 7.00% 1/20/20 # | | | 1,595,000 | | | | 1,435,500 | |

Grace (W.R.) 144A 5.125% 10/1/21 # | | | 345,000 | | | | 349,313 | |

GTL Trade Finance 144A 5.893% 4/29/24 # | | | 565,000 | | | | 403,975 | |

INVISTA Finance 144A 4.25% 10/15/19 # | | | 2,465,000 | | | | 2,403,375 | |

Joseph T Ryerson & Son 11.25% 10/15/18 @ | | | 228,000 | | | | 171,000 | |

Lundin Mining 144A 7.50% 11/1/20 # | | | 1,195,000 | | | | 1,123,300 | |

Methanex 4.25% 12/1/24 | | | 2,890,000 | | | | 2,566,878 | |

MMC Norilsk Nickel | | | | | | | | |

144A 5.55% 10/28/20 # | | | 962,000 | | | | 965,593 | |

144A 6.625% 10/14/22 # | | | 1,095,000 | | | | 1,117,601 | |

NOVA Chemicals 144A 5.00% 5/1/25 # | | | 3,039,000 | | | | 2,940,233 | |

OCP | | | | | | | | |

144A 4.50% 10/22/25 # | | | 2,125,000 | | | | 1,987,011 | |

144A 6.875% 4/25/44 # | | | 1,650,000 | | | | 1,625,795 | |

Phosagro 144A 4.204% 2/13/18 # | | | 1,715,000 | | | | 1,701,066 | |

PolyOne 5.25% 3/15/23 | | | 812,000 | | | | 795,760 | |

PPG Industries 2.30% 11/15/19 | | | 1,770,000 | | | | 1,753,307 | |

| | | | | | | | |

| | | | | | | 52,453,371 | |

| | | | | | | | |

Brokerage – 0.20% | | | | | | | | |

Affiliated Managers Group 3.50% 8/1/25 | | | 2,115,000 | | | | 2,015,703 | |

Jefferies Group | | | | | | | | |

6.45% 6/8/27 | | | 893,000 | | | | 947,614 | |

6.50% 1/20/43 | | | 585,000 | | | | 542,560 | |

Lazard Group 6.85% 6/15/17 | | | 878,000 | | | | 935,141 | |

| | | | | | | | |

| | | | | | | 4,441,018 | |

| | | | | | | | |

| Capital Goods – 1.04% | | | | | | | | |

BWAY Holding 144A 9.125% 8/15/21 # | | | 1,448,000 | | | | 1,361,120 | |

Cemex | | | | | | | | |

144A 6.50% 12/10/19 # | | | 1,270,000 | | | | 1,228,725 | |

144A 7.25% 1/15/21 # | | | 935,000 | | | | 902,275 | |

Cemex Finance 144A 9.375% 10/12/22 # | | | 720,000 | | | | 761,400 | |

Embraer Netherlands Finance 5.05% 6/15/25 | | | 1,435,000 | | | | 1,309,437 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Capital Goods (continued) | | | | | | | | |

Fortune Brands Home & Security 3.00% 6/15/20 | | | 1,310,000 | | | $ | 1,304,197 | |

General Electric 4.00% 12/29/49 • | | | 4,691,100 | | | | 4,696,964 | |

General Electric Capital | | | | | | | | |

2.10% 12/11/19 | | | 795,000 | | | | 795,364 | |

144A 3.80% 6/18/19 # | | | 1,555,000 | | | | 1,635,499 | |

5.55% 5/4/20 | | | 1,295,000 | | | | 1,467,532 | |

6.00% 8/7/19 | | | 2,675,000 | | | | 3,031,832 | |

Lockheed Martin | | | | | | | | |

2.50% 11/23/20 | | | 770,000 | | | | 766,307 | |

3.55% 1/15/26 | | | 1,225,000 | | | | 1,231,835 | |

Owens-Brockway Glass Container 144A 5.875% 8/15/23 # | | | 595,000 | | | | 605,041 | |

TransDigm 6.50% 7/15/24 | | | 35,000 | | | | 34,983 | |

Union Andina de Cementos 144A 5.875% 10/30/21 # | | | 1,465,000 | | | | 1,417,387 | |

| | | | | | | | |

| | | | | | | 22,549,898 | |

| | | | | | | | |

Communications – 4.29% | | | | | | | | |

21st Century Fox America | | | | | | | | |

144A 3.70% 10/15/25 # | | | 760,000 | | | | 759,660 | |

144A 4.95% 10/15/45 # | | | 2,395,000 | | | | 2,367,733 | |

Altice US Finance I 144A 5.375% 7/15/23 # | | | 1,275,000 | | | | 1,281,375 | |

America Movil 5.00% 3/30/20 | | | 1,630,000 | | | | 1,772,156 | |

American Tower | | | | | | | | |

2.80% 6/1/20 | | | 815,000 | | | | 806,448 | |

4.00% 6/1/25 | | | 970,000 | | | | 955,309 | |

American Tower Trust I 144A 3.07% 3/15/23 # | | | 2,430,000 | | | | 2,388,739 | |

AT&T 4.50% 5/15/35 | | | 1,455,000 | | | | 1,349,895 | |

Bell Canada 3.35% 3/22/23 | | CAD | 773,000 | | | | 571,236 | |

Bharti Airtel International Netherlands 144A 5.35% 5/20/24 # | | | 1,735,000 | | | | 1,827,534 | |

CC Holdings GS V 3.849% 4/15/23 | | | 1,710,000 | | | | 1,680,855 | |

CCO Safari II 144A 4.908% 7/23/25 # | | | 5,345,000 | | | | 5,347,870 | |

CenturyLink 5.80% 3/15/22 | | | 3,230,000 | | | | 2,972,407 | |

Colombia Telecomunicaciones 144A 5.375% 9/27/22 # | | | 1,935,000 | | | | 1,751,175 | |

Columbus International 144A 7.375% 3/30/21 # | | | 1,395,000 | | | | 1,386,281 | |

Crown Castle Towers 144A 4.883% 8/15/20 # | | | 9,630,000 | | | | 10,322,317 | |

Deutsche Telekom International Finance 6.50% 4/8/22 | | GBP | 416,000 | | | | 745,564 | |

Digicel Group 144A 8.25% 9/30/20 # | | | 3,320,000 | | | | 2,755,600 | |

Equinix 5.375% 4/1/23 | | | 2,331,000 | | | | 2,389,275 | |

Frontier Communications 144A 8.875% 9/15/20 # | | | 1,865,000 | | | | 1,892,975 | |

Grupo Televisa | | | | | | | | |

5.00% 5/13/45 | | | 720,000 | | | | 622,659 | |

6.125% 1/31/46 | | | 1,200,000 | | | | 1,198,920 | |

| | |

| | Diversified Income Series-13 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Communications (continued) | | | | | | | | |

GTP Acquisition Partners I 144A 2.35% 6/15/20 # | | | 1,095,000 | | | $ | 1,063,234 | |

Level 3 Financing 144A 5.375% 5/1/25 # | | | 2,839,000 | | | | 2,835,451 | |

Millicom International Cellular 144A 6.625% 10/15/21 # | | | 1,760,000 | | | | 1,634,600 | |

MTS International Funding 144A 8.625% 6/22/20 # | | | 1,740,000 | | | | 1,927,649 | |

Myriad International Holdings 144A 5.50% 7/21/25 # | | | 2,590,000 | | | | 2,502,458 | |

Neptune Finco 144A 6.625% 10/15/25 # | | | 450,000 | | | | 469,125 | |

SBA Tower Trust | | | | | | | | |

144A 2.24% 4/16/18 # | | | 1,800,000 | | | | 1,767,161 | |

144A 2.898% 10/15/19 # | | | 1,300,000 | | | | 1,270,371 | |

SES 144A 3.60% 4/4/23 # | | | 3,960,000 | | | | 3,870,385 | |

SES GLOBAL Americas Holdings 144A 5.30% 3/25/44 # | | | 4,565,000 | | | | 4,367,057 | |

Sky 144A 3.75% 9/16/24 # | | | 2,775,000 | | | | 2,715,246 | |

Sprint | | | | | | | | |

7.125% 6/15/24 | | | 3,312,000 | | | | 2,405,340 | |

7.25% 9/15/21 | | | 560,000 | | | | 424,032 | |

Time Warner 4.85% 7/15/45 | | | 2,760,000 | | | | 2,638,262 | |

Time Warner Cable 5.50% 9/1/41 | | | 600,000 | | | | 543,957 | |

T-Mobile USA 6.125% 1/15/22 | | | 1,359,000 | | | | 1,399,770 | |

UPCB Finance IV 144A 5.375% 1/15/25 # | | | 1,198,000 | | | | 1,135,105 | |

Verizon Communications | | | | | | | | |

3.25% 2/17/26 | | EUR | 971,000 | | | | 1,180,652 | |

4.862% 8/21/46 | | | 4,272,000 | | | | 4,060,062 | |

Vimpel Communications 144A 7.748% 2/2/21 # | | | 1,658,000 | | | | 1,700,639 | |

Virgin Media Secured Finance 144A 5.25% 1/15/26 # | | | 2,805,000 | | | | 2,734,875 | |

Wind Acquisition Finance 144A 7.375% 4/23/21 # | | | 1,215,000 | | | | 1,151,213 | |

WPP Finance 2010 5.625% 11/15/43 | | | 545,000 | | | | 554,869 | |

Zayo Group 6.00% 4/1/23 | | | 1,715,000 | | | | 1,629,250 | |

| | | | | | | | |

| | | | | | | 93,126,746 | |

| | | | | | | | |

Consumer Cyclical – 1.49% | | | | | | | | |

AutoNation 3.35% 1/15/21 | | | 490,000 | | | | 488,819 | |

Cencosud 144A 5.15% 2/12/25 # | | | 2,035,000 | | | | 1,895,248 | |

CVS Health 144A 5.00% 12/1/24 # | | | 621,000 | | | | 673,016 | |

Daimler 2.75% 12/10/18 | | NOK | 5,560,000 | | | | 649,509 | |

Delphi Automotive 3.15% 11/19/20 | | | 1,120,000 | | | | 1,119,806 | |

Ford Motor Credit | | | | | | | | |

4.05% 12/10/18 | | AUD | 632,000 | | | | 461,357 | |

5.875% 8/2/21 | | | 1,745,000 | | | | 1,948,247 | |

General Motors Financial | | | | | | | | |

3.45% 4/10/22 | | | 3,055,000 | | | | 2,934,609 | |

4.00% 1/15/25 | | | 2,555,000 | | | | 2,428,589 | |

4.30% 7/13/25 | | | 440,000 | | | | 427,486 | |

4.375% 9/25/21 | | | 1,810,000 | | | | 1,837,742 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Consumer Cyclical (continued) | | | | | | | | |

Hyundai Capital America | | | | | | | | |

144A 2.125% 10/2/17 # | | | 1,570,000 | | | $ | 1,561,092 | |

144A 2.55% 2/6/19 # | | | 685,000 | | | | 680,184 | |

Marriott International 3.375% 10/15/20 | | | 1,670,000 | | | | 1,701,672 | |

Nemak 144A 5.50% 2/28/23 # | | | 1,560,000 | | | | 1,571,700 | |

QVC 5.45% 8/15/34 | | | 2,625,000 | | | | 2,276,964 | |

Sally Holdings 5.75% 6/1/22 | | | 47,000 | | | | 48,880 | |

Signet UK Finance 4.70% 6/15/24 | | | 3,115,000 | | | | 3,072,826 | |

Starwood Hotels & Resorts Worldwide | | | | | | | | |

3.75% 3/15/25 @ | | | 2,230,000 | | | | 2,187,130 | |

4.50% 10/1/34 @ | | | 410,000 | | | | 370,728 | |

Toyota Credit Canada 2.05% 5/20/20 | | CAD | 400,000 | | | | 291,224 | |

Toyota Finance Australia | | | | | | | | |

2.25% 8/31/16 | | NOK | 1,230,000 | | | | 139,620 | |

3.04% 12/20/16 | | NZD | 2,070,000 | | | | 1,409,315 | |

Toyota Motor Credit 2.80% 7/13/22 | | | 755,000 | | | | 752,169 | |

Tupy Overseas 144A 6.625% 7/17/24 #@ | | | 1,550,000 | | | | 1,360,125 | |

| | | | | | | | |

| | | | | | | 32,288,057 | |

| | | | | | | | |

Consumer Non-Cyclical – 1.73% | | | | | | | | |

Amgen 4.00% 9/13/29 | | GBP | 341,000 | | | | 511,717 | |

AstraZeneca | | | | | | | | |

2.375% 11/16/20 | | | 1,885,000 | | | | 1,873,679 | |

3.375% 11/16/25 | | | 3,125,000 | | | | 3,108,828 | |

Becton Dickinson 6.375% 8/1/19 | | | 3,600,000 | | | | 4,067,107 | |

Campbell Soup 3.30% 3/19/25 | | | 2,895,000 | | | | 2,885,134 | |

Celgene 3.25% 8/15/22 | | | 1,575,000 | | | | 1,564,819 | |

ENA Norte Trust 144A 4.95% 4/25/23 # | | | 1,268,693 | | | | 1,299,295 | |

Express Scripts Holding | | | | | | | | |

2.25% 6/15/19 | | | 1,845,000 | | | | 1,835,637 | |

3.50% 6/15/24 | | | 1,045,000 | | | | 1,031,389 | |

JB 144A 3.75% 5/13/25 # | | | 2,650,000 | | | | 2,537,507 | |

JBS Investments 144A 7.75% 10/28/20 # | | | 2,390,000 | | | | 2,306,350 | |

JBS USA 144A 5.75% 6/15/25 # | | | 615,000 | | | | 538,125 | |

Mallinckrodt International Finance | | | | | | | | |

144A 4.875% 4/15/20 # | | | 1,090,000 | | | | 1,054,575 | |

144A 5.50% 4/15/25 # | | | 2,137,000 | | | | 1,976,725 | |

Perrigo 4.00% 11/15/23 | | | 2,870,000 | | | | 2,802,601 | |

Perrigo Finance 3.50% 12/15/21 | | | 815,000 | | | | 793,221 | |

Prestige Brands 144A 5.375% 12/15/21 # | | | 652,000 | | | | 629,180 | |

Zimmer Biomet Holdings | | | | | | | | |

3.375% 11/30/21 | | | 2,750,000 | | | | 2,756,231 | |

4.625% 11/30/19 | | | 3,645,000 | | | | 3,895,561 | |

| | | | | | | | |

| | | | | | | 37,467,681 | |

| | | | | | | | |

Electric – 5.25% | | | | | | | | |

AES Gener | | | | | | | | |

144A 5.00% 7/14/25 # | | | 800,000 | | | | 767,166 | |

144A 5.25% 8/15/21 # | | | 1,250,000 | | | | 1,285,075 | |

144A 8.375% 12/18/73 #@• | | | 1,420,000 | | | | 1,427,100 | |

| | |

| | Diversified Income Series-14 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Electric (continued) | | | | | | | | |

Ameren Illinois | | | | | | | | |

3.25% 3/1/25 | | | 2,090,000 | | | $ | 2,104,509 | |

9.75% 11/15/18 | | | 5,900,000 | | | | 7,111,754 | |

American Transmission Systems 144A 5.25% 1/15/22 # | | | 5,410,000 | | | | 5,909,408 | |

Appalachian Power | | | | | | | | |

3.40% 6/1/25 | | | 550,000 | | | | 537,783 | |

4.45% 6/1/45 | | | 1,360,000 | | | | 1,296,119 | |

Berkshire Hathaway Energy 3.75% 11/15/23 | | | 3,405,000 | | | | 3,499,908 | |

Cleveland Electric Illuminating 5.50% 8/15/24 | | | 365,000 | | | | 411,721 | |

CMS Energy 6.25% 2/1/20 | | | 1,730,000 | | | | 1,963,984 | |

ComEd Financing III 6.35% 3/15/33 @ | | | 2,055,000 | | | | 2,102,662 | |

Commonwealth Edison 4.35% 11/15/45 | | | 2,205,000 | | | | 2,225,010 | |

Consumers Energy 4.10% 11/15/45 | | | 640,000 | | | | 637,260 | |

DTE Energy 144A 3.30% 6/15/22 # | | | 2,180,000 | | | | 2,189,736 | |

Duke Energy | | | | | | | | |

3.75% 4/15/24 | | | 2,745,000 | | | | 2,786,024 | |

4.80% 12/15/45 | | | 2,465,000 | | | | 2,500,210 | |

Dynegy 7.625% 11/1/24 | | | 127,000 | | | | 109,195 | |

Electricite de France 144A 5.25% 1/29/49 #• | | | 3,565,000 | | | | 3,364,469 | |

Enel 144A 8.75% 9/24/73 #• | | | 3,512,000 | | | | 4,008,070 | |

Enel Finance International 144A 6.00% 10/7/39 # | | | 1,275,000 | | | | 1,430,347 | |

Entergy 4.00% 7/15/22 | | | 1,820,000 | | | | 1,859,317 | |

Entergy Arkansas 3.70% 6/1/24 | | | 895,000 | | | | 913,786 | |

Entergy Louisiana 4.05% 9/1/23 | | | 4,045,000 | | | | 4,176,305 | |

Exelon 144A 3.95% 6/15/25 # | | | 2,445,000 | | | | 2,446,526 | |

Great Plains Energy 4.85% 6/1/21 | | | 1,195,000 | | | | 1,284,877 | |

Indiana Michigan Power 3.20% 3/15/23 | | | 1,455,000 | | | | 1,436,750 | |

Integrys Holding 6.11% 12/1/66 @• | | | 3,280,000 | | | | 2,493,276 | |

IPALCO Enterprises 5.00% 5/1/18 | | | 1,365,000 | | | | 1,436,663 | |

ITC Holdings 3.65% 6/15/24 | | | 1,365,000 | | | | 1,346,990 | |

Kansas City Power & Light 3.65% 8/15/25 | | | 3,445,000 | | | | 3,476,064 | |

LG&E & KU Energy 4.375% 10/1/21 | | | 3,765,000 | | | | 3,983,069 | |

Louisville Gas & Electric 4.375% 10/1/45 | | | 1,280,000 | | | | 1,310,993 | |

Metropolitan Edison 144A 4.00% 4/15/25 # | | | 2,270,000 | | | | 2,251,640 | |

MidAmerican Energy 4.25% 5/1/46 | | | 4,250,000 | | | | 4,214,729 | |

National Rural Utilities Cooperative Finance | | | | | | | | |

2.30% 11/1/20 | | | 590,000 | | | | 584,682 | |

3.25% 11/1/25 | | | 495,000 | | | | 493,542 | |

4.75% 4/30/43 • | | | 2,840,000 | | | | 2,808,476 | |

NextEra Energy Capital Holdings | | | | | | | | |

2.40% 9/15/19 | | | 3,380,000 | | | | 3,333,052 | |

3.625% 6/15/23 | | | 1,320,000 | | | | 1,317,216 | |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| | |

Corporate Bonds (continued) | | | | | | | | |

Electric (continued) | | | | | | | | |

NV Energy 6.25% 11/15/20 | | | 2,380,000 | | | $ | 2,706,484 | |

Pennsylvania Electric 5.20% 4/1/20 | | | 3,235,000 | | | | 3,451,968 | |

Perusahaan Listrik Negara 144A 5.50% 11/22/21 # | | | 2,560,000 | | | | 2,614,400 | |

Public Service of Oklahoma 5.15% 12/1/19 | | | 3,700,000 | | | | 4,049,669 | |

Puget Energy 6.00% 9/1/21 | | | 1,080,000 | | | | 1,218,178 | |

SCANA 4.125% 2/1/22 | | | 2,300,000 | | | | 2,256,272 | |

Trans-Allegheny Interstate Line 144A 3.85% 6/1/25 # | | | 2,055,000 | | | | 2,059,178 | |

WEC Energy Group 3.55% 6/15/25 | | | 2,070,000 | | | | 2,085,705 | |

Westar Energy 3.25% 12/1/25 | | | 1,445,000 | | | | 1,450,933 | |

Xcel Energy 3.30% 6/1/25 | | | 3,240,000 | | | | 3,173,680 | |

| | | | | | | | |

| | | | | | | 113,901,930 | |

| | | | | | | | |

Energy – 2.32% | | | | | | | | |

AmeriGas Finance 7.00% 5/20/22 | | | 1,118,000 | | | | 1,087,255 | |

CNOOC Finance 2012 144A 3.875% 5/2/22 # | | | 1,200,000 | | | | 1,215,586 | |

Continental Resources 4.50% 4/15/23 | | | 585,000 | | | | 420,906 | |

Dominion Gas Holdings | | | | | | | | |

3.60% 12/15/24 | | | 2,195,000 | | | | 2,174,657 | |

4.60% 12/15/44 | | | 4,610,000 | | | | 4,300,909 | |

Ecopetrol 5.375% 6/26/26 | | | 2,700,000 | | | | 2,305,125 | |

Enbridge Energy Partners 8.05% 10/1/37 • | | | 3,745,000 | | | | 3,080,263 | |

Energy Transfer Partners 9.70% 3/15/19 | | | 2,189,000 | | | | 2,412,471 | |

EnLink Midstream Partners 4.15% 6/1/25 | | | 2,990,000 | | | | 2,303,876 | |

Enterprise Products Operating 7.034% 1/15/68 • | | | 715,000 | | | | 727,513 | |

Lukoil International Finance 144A 3.416% 4/24/18 # | | | 1,355,000 | | | | 1,322,765 | |

MPLX 144A 4.875% 12/1/24 # | | | 1,103,000 | | | | 995,457 | |

Murphy Oil USA 6.00% 8/15/23 | | | 1,485,000 | | | | 1,566,675 | |

NiSource Finance 6.125% 3/1/22 | | | 2,120,000 | | | | 2,429,772 | |

Noble Energy 5.05% 11/15/44 | | | 1,790,000 | | | | 1,450,163 | |

Petrobras Global Finance 5.875% 3/1/18 | | | 1,145,000 | | | | 1,021,913 | |

Petroleos Mexicanos | | | | | | | | |

144A 3.50% 7/23/20 # | | | 790,000 | | | | 749,710 | |

6.50% 6/2/41 | | | 985,000 | | | | 856,457 | |

Petronas Global Sukuk 144A 2.707% 3/18/20 # | | | 1,885,000 | | | | 1,856,919 | |

Plains All American Pipeline 8.75% 5/1/19 | | | 3,490,000 | | | | 3,831,441 | |

Regency Energy Partners | | | | | | | | |

5.50% 4/15/23 | | | 623,000 | | | | 561,740 | |

5.875% 3/1/22 | | | 3,110,000 | | | | 2,935,066 | |

Williams Partners 7.25% 2/1/17 | | | 2,815,000 | | | | 2,871,289 | |

| | |

| | Diversified Income Series-15 |

Delaware VIP® Diversified Income Series

Schedule of investments (continued)

| | | | | | | | |

| | | Principal

amount° | | | Value (U.S. $) | |

| | |