UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-5262

MFS SERIES TRUST VIII

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2010

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

MFS® Global Growth Fund

SIPC Contact Information:

You may obtain information about the Securities Investor Protection Corporation (“SIPC”), including the SIPC Brochure, by contacting SIPC either by telephone (202-371-8300) or by accessing SIPC’s website address (www.sipc.org).

The report is prepared for the general information of shareholders. It is authorized for distribution to prospective investors only when preceded or accompanied by a current prospectus.

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE

10/31/10

WGF-ANN

LETTER FROM THE CEO

Dear Shareholders:

After an extended rebound in the financial markets, uncertainty returned in early 2010 as investors began to question the durability of the recovery for global economies and markets. That uncertainty led to increased risk aversion, especially as investors saw the eurozone struggle with the debt woes of many of its members. In September, the U.S. Federal Reserve Board’s promises to further loosen monetary policy helped assuage market fears and drive asset prices off their recent lows. A combination of solid earnings and improving economic data gave an additional boost to investor sentiment. As we near the end of 2010, we are cautiously optimistic that economic growth will continue to improve and that the global economies will recover from the shocks of the past few years. We expect the pace of recovery worldwide will be uneven and volatile.

As always, we continue to be mindful of the many challenges faced at the individual, national, and international levels. It is in times such as these that we want to remind investors of the merits of maintaining a long-term view, adhering to basic investing principles such as asset allocation and diversification, and working closely with their advisors to research and identify investment opportunities.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management®

December 15, 2010

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

PORTFOLIO COMPOSITION

Portfolio structure

| | | | |

| Top ten holdings | | | | |

| BHP Billiton PLC | | | 2.8% | |

| Cisco Systems, Inc. | | | 2.4% | |

| Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 2.2% | |

| Danaher Corp. | | | 2.2% | |

| Oracle Corp. | | | 2.0% | |

| National Oilwell Varco, Inc. | | | 2.0% | |

| Schlumberger Ltd. | | | 1.9% | |

| Groupe Danone | | | 1.8% | |

| Pernod Ricard S.A. | | | 1.7% | |

| Accenture Ltd., “A” | | | 1.7% | |

| | | | |

| Equity sectors | | | | |

| Financial Services | | | 18.0% | |

| Technology | | | 17.3% | |

| Consumer Staples | | | 14.2% | |

| Health Care | | | 13.0% | |

| Basic Materials | | | 9.3% | |

| Retailing | | | 8.0% | |

| Energy | | | 6.7% | |

| Special Products & Services | | | 6.0% | |

| Industrial Goods & Services | | | 5.2% | |

| Leisure | | | 0.8% | |

| Utilities & Communications | | | 0.7% | |

| |

| Issuer country weightings | | | | |

| United States | | | 47.7% | |

| United Kingdom | | | 11.1% | |

| France | | | 8.5% | |

| Switzerland | | | 7.0% | |

| Germany | | | 5.0% | |

| Japan | | | 5.0% | |

| Brazil | | | 3.6% | |

| Taiwan | | | 3.3% | |

| Netherlands | | | 2.0% | |

| Other Countries | | | 6.8% | |

Percentages are based on net assets as of 10/31/10.

The portfolio is actively managed and current holdings may be different.

2

MANAGEMENT REVIEW

Summary of Results

For the twelve months ended October 31, 2010, Class A shares of the MFS Global Growth Fund (the “fund”) provided a total return of 13.92%, at net asset value. This compares with a return of 17.48% for the fund’s benchmark, the Morgan Stanley Capital International (MSCI) All Country World Growth Index. Effective September 30, 2010, the MSCI All Country World Index replaced the MSCI World Growth Index as the fund’s other benchmark. For the twelve months ended October 31, 2010, the MSCI All Country World Index generated a return of 14.65% and the MSCI World Growth Index generated a return of 16.33%.

Market Environment

The first half of the reporting period witnessed a continuation of the financial market and macroeconomic rebounds that had begun in early 2009. These recoveries in global activity and asset valuations were generally synchronized around the world, led importantly by emerging Asian economies, but broadening to include most of the global economy to varying degrees. Primary drivers of the recoveries included an unwinding of the inventory destocking that took place earlier, the production of manufacturing and capital goods, as well as massive fiscal and monetary stimulus.

During the second half of the period, heightened risk surrounding the public-debt profiles of several of the peripheral European countries impaired market sentiment. At the same time, the improving trend in global macroeconomic data began to weaken somewhat. These two dynamics caused many asset prices to retrench significantly, as many questioned the durability of the global recovery.

Towards the end of the period, the U.S. Federal Reserve led markets to believe that further monetary loosening would be forthcoming if macroeconomic activity did not show signs of improvement. Although policy uncertainty remained very elevated, the prospects for more easing by the Fed improved market sentiment and drove asset prices well off their recent lows.

Detractors from Performance

A combination of stock selection and an overweighted position in the financial services sector detracted from the fund’s performance relative to the MSCI All Country World Growth Index. The fund’s holdings of brokerage houses, Nomura Holdings (Japan) (b) and Charles Schwab, stock exchange Deutsche Boerse (Germany), and financial services provider Bank of New York Mellon (b) were among the fund’s top relative detractors.

Bank of New York Mellon underperformed the market during the latter part of the reporting period as the custody bank’s near-term earnings continued to be

3

Management Review – continued

hurt by record low interest rates, which squeezed its net interest revenue and reduced profit from its fixed income portfolios and securities lending business.

Security selection in the energy sector was also a negative factor for relative performance. Our overweighted position in oil and gas exploration company INPEX (Japan), and the timing of our ownership in shares of integrated oil company Total S.A. (France) (h), had a negative impact on relative returns. Shares of INPEX plunged as the company announced that it was going to raise capital using a stock issue to finance the development of the Ichthys natural gas project in Australia.

An underweighted position in the basic materials sector hindered relative results. No individual stocks within this sector were among the fund’s top relative detractors for the reporting period.

Securities in other sectors that held back relative performance included Hong Kong-headquartered retailer Esprit Holdings, telecommunications company China Unicom (Hong Kong) Ltd. (b)(h), and business information provider Dun & Bradstreet Corp.

During the reporting period, the fund’s currency exposure also detracted from relative returns. All of MFS’ investment decisions are driven by the fundamentals of each individual opportunity and as such, it is common for our funds to have different currency exposures than the benchmark.

The fund’s cash position was another negative factor for relative results. The fund holds cash to buy new holdings and to provide liquidity. In a period when equity markets rose, as measured by the fund’s benchmark, holding cash hurt performance versus the benchmark, which has no cash position.

Contributors to Performance

Favorable stock selection in the technology sector boosted relative performance. Not owning poor-performing software giant Microsoft and computer products and services provider Hewlett-Packard benefited relative returns.

Security selection in the retailing sector also contributed to relative results. The fund’s overweighted positions in strong-performing luxury goods companies, Compagnie Financiere Richemont S.A. (Switzerland) and LVMH Moët Hennessy Louis Vuitton (France), had a positive effect on relative performance. Shares of LVMH appreciated after the company reported a significant profit increase during the first half of the reporting period which exceeded analysts’ expectations. In addition, demand for luxury goods has been increasing in China, and U.S. and European retailers have been replenishing inventories following the recession.

4

Management Review – continued

Stock selection in the special products & services sector aided relative returns. Within this sector, the timing of our ownership in product safety testing company Intertek Group (U.K) had a positive impact on results. The company forecasted strong growth in its food and alternative energy divisions due to increases in regulations and product launches. U.S. regulators recently proposed new guidelines to reduce food-borne illnesses and the European Union tightened food-packaging rules. Intertek expects these regulations to result in increased demand for its testing services.

Individual standout contributors in other sectors that bolstered relative performance included oil and gas drilling equipment manufacturer National Oilwell Varco, Brazilian brewer Companhia de Bebidas das Americas, financial services holding company Credicorp (Peru) (h), electrical distribution equipment manufacturer Schneider Electric (France) (b) , and flavors and fragrances supplier Symrise (Germany) (b).

Respectfully,

| | |

| David Antonelli | | Jeffrey Constantino |

| Portfolio Manager | | Portfolio Manager |

| (b) | Security is not a benchmark constituent. |

| (h) | Security was not held in the portfolio at period end. |

Note to Shareholders: Effective January 12, 2010, David Antonelli became a co-manager of the fund. Previously, the fund was co-managed by Barry Dargan.

The views expressed in this report are those of the portfolio managers only through the end of the period of the report as stated on the cover and do not necessarily reflect the views of MFS or any other person in the MFS organization. These views are subject to change at any time based on market or other conditions, and MFS disclaims any responsibility to update such views. These views may not be relied upon as investment advice or an indication of trading intent on behalf of any MFS portfolio. References to specific securities are not recommendations of such securities, and may not be representative of any MFS portfolio’s current or future investments.

5

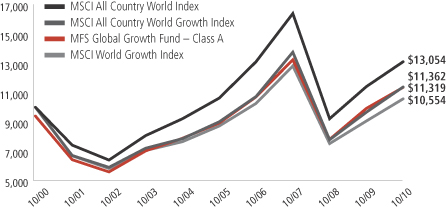

PERFORMANCE SUMMARY THROUGH 10/31/10

The following chart illustrates a representative class of the fund’s historical performance in comparison to its benchmark(s). Performance results include the deduction of the maximum applicable sales charge and reflect the percentage change in net asset value, including reinvestment of dividends and capital gains distributions. The performance of other share classes will be greater than or less than that of the class depicted below. Benchmarks are unmanaged and may not be invested in directly. Benchmark returns do not reflect sales charges, commissions or expenses. (See Notes to Performance Summary.)

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value fluctuate so your shares, when sold, may be worth more or less than the original cost; current performance may be lower or higher than quoted. The performance shown does not reflect the deduction of taxes, if any, that a shareholder would pay on fund distributions or the redemption of fund shares.

Growth of a Hypothetical $10,000 Investment

6

Performance Summary – continued

Total Returns through 10/31/10

Average annual without sales charge

| | | | | | | | | | | | | | |

| | | Share class | | Class inception date | | 1-yr | | 5-yr | | 10-yr | | Life (t) | | |

| | | A | | 11/18/93 | | 13.92% | | 4.77% | | 1.85% | | N/A | | |

| | | B | | 11/18/93 | | 13.06% | | 3.99% | | 1.09% | | N/A | | |

| | | C | | 1/03/94 | | 13.09% | | 4.01% | | 1.08% | | N/A | | |

| | | I | | 1/02/97 | | 14.18% | | 5.04% | | 2.09% | | N/A | | |

| | | R1 | | 4/01/05 | | 13.06% | | 3.94% | | N/A | | 4.36% | | |

| | | R2 | | 10/31/03 | | 13.66% | | 4.38% | | N/A | | 6.37% | | |

| | | R3 | | 4/01/05 | | 13.93% | | 4.71% | | N/A | | 5.15% | | |

| | | R4 | | 4/01/05 | | 14.21% | | 5.00% | | N/A | | 5.43% | | |

| Comparative benchmarks | | | | | | |

| | | MSCI All Country World

Growth Index (f) | | 17.48% | | 4.68% | | 1.28% | | N/A | | |

| | | MSCI All Country World Index (f) | | 14.65% | | 4.23% | | 2.70% | | N/A | | |

| | | MSCI World Growth Index (f) | | 16.33% | | 3.83% | | 0.54% | | N/A | | |

| Average annual with sales charge | | | | | | | | | | |

| | | A

With Initial Sales Charge (5.75%) | | 7.37% | | 3.54% | | 1.25% | | N/A | | |

| | | B

With CDSC (Declining over six years from 4% to 0%) (x) | | 9.06% | | 3.64% | | 1.09% | | N/A | | |

| | | C

With CDSC (1% for 12 months) (x) | | 12.09% | | 4.01% | | 1.08% | | N/A | | |

Class I, R1, R2, R3, and R4 shares do not have a sales charge.

CDSC – Contingent Deferred Sales Charge.

| (f) | Source: FactSet Research Systems Inc. |

| (t) | For the period from the class inception date through the stated period end (for those share classes with less than 10 years of performance history). No comparative benchmark performance information is provided for “life” periods. (See Notes to Performance Summary.) |

| (x) | Assuming redemption at the end of the applicable period. |

Benchmark Definitions

MSCI All Country World Growth Index – a market capitalization-weighted index that is designed to measure equity market performance for growth securities in the global developed and emerging markets.

MSCI All Country World Index – a market capitalization-weighted index that is designed to measure equity market performance in the global developed and emerging markets.

7

Performance Summary – continued

MSCI World Growth Index – a market capitalization-weighted index that is designed to measure equity market performance for growth securities in the global developed markets.

It is not possible to invest directly in an index.

Notes to Shareholders: Effective September 30, 2010, the MSCI All Country World Index became the fund’s other benchmark, replacing the MSCI World Growth Index because MFS believes that the MSCI All Country World Index more closely represents the fund’s investment policies and strategies.

Notes to Performance Summary

Average annual total return represents the average annual change in value for each share class for the periods presented. Life returns are presented where the share class has less than 10 years of performance history and represent the average annual total return from the class inception date to the stated period end date. As the fund’s share classes may have different inception dates, the life returns may represent different time periods and may not be comparable. As a result, no comparative benchmark performance information is provided for life periods.

Performance results reflect any applicable expense subsidies and waivers in effect during the periods shown. Without such subsidies and waivers the fund’s performance results would be less favorable. Please see the prospectus and financial statements for complete details.

From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower.

8

EXPENSE TABLE

Fund expenses borne by the shareholders during the period, May 1, 2010 through October 31, 2010

As a shareholder of the fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on certain purchase or redemption payments, and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period May 1, 2010 through October 31, 2010.

Actual Expenses

The first line for each share class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class in the following table provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

9

Expense Table – continued

| | | | | | | | | | | | | | | | | | |

Share

Class | | | | Annualized

Expense Ratio | | | Beginning

Account Value

5/01/10 | | | Ending Account Value

10/31/10 | | | Expenses Paid During

Period (p)

5/01/10-10/31/10 | |

| A | | Actual | | | 1.54% | | | | $1,000.00 | | | | $1,040.13 | | | | $7.92 | |

| | Hypothetical (h) | | | 1.54% | | | | $1,000.00 | | | | $1,017.44 | | | | $7.83 | |

| B | | Actual | | | 2.29% | | | | $1,000.00 | | | | $1,035.52 | | | | $11.75 | |

| | Hypothetical (h) | | | 2.29% | | | | $1,000.00 | | | | $1,013.66 | | | | $11.62 | |

| C | | Actual | | | 2.29% | | | | $1,000.00 | | | | $1,035.88 | | | | $11.75 | |

| | Hypothetical (h) | | | 2.29% | | | | $1,000.00 | | | | $1,013.66 | | | | $11.62 | |

| I | | Actual | | | 1.29% | | | | $1,000.00 | | | | $1,041.00 | | | | $6.64 | |

| | Hypothetical (h) | | | 1.29% | | | | $1,000.00 | | | | $1,018.70 | | | | $6.56 | |

| R1 | | Actual | | | 2.29% | | | | $1,000.00 | | | | $1,035.94 | | | | $11.75 | |

| | Hypothetical (h) | | | 2.29% | | | | $1,000.00 | | | | $1,013.66 | | | | $11.62 | |

| R2 | | Actual | | | 1.79% | | | | $1,000.00 | | | | $1,038.54 | | | | $9.20 | |

| | Hypothetical (h) | | | 1.79% | | | | $1,000.00 | | | | $1,016.18 | | | | $9.10 | |

| R3 | | Actual | | | 1.54% | | | | $1,000.00 | | | | $1,039.83 | | | | $7.92 | |

| | Hypothetical (h) | | | 1.54% | | | | $1,000.00 | | | | $1,017.44 | | | | $7.83 | |

| R4 | | Actual | | | 1.29% | | | | $1,000.00 | | | | $1,041.32 | | | | $6.64 | |

| | Hypothetical (h) | | | 1.29% | | | | $1,000.00 | | | | $1,018.70 | | | | $6.56 | |

| (h) | 5% class return per year before expenses. |

| (p) | Expenses paid is equal to each class’ annualized expense ratio, as shown above, multiplied by the average account value over the period, multiplied by the number of days in the period, divided by the number of days in the year. Expenses paid do not include any applicable sales charges (loads). If these transaction costs had been included, your costs would have been higher. |

10

PORTFOLIO OF INVESTMENTS

10/31/10

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | | | |

| Common Stocks - 99.1% | | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Aerospace - 0.9% | | | | | | | | |

| United Technologies Corp. | | | 28,740 | | | $ | 2,148,889 | |

| | |

| Alcoholic Beverages - 5.2% | | | | | | | | |

| Companhia de Bebidas das Americas, ADR | | | 22,860 | | | $ | 3,183,026 | |

| Diageo PLC | | | 172,770 | | | | 3,189,174 | |

| Heineken N.V. | | | 30,190 | | | | 1,530,312 | |

| Pernod Ricard S.A. | | | 42,810 | | | | 3,796,030 | |

| | | | | | | | |

| | | | | | | $ | 11,698,542 | |

| Apparel Manufacturers - 3.9% | | | | | | | | |

| Compagnie Financiere Richemont S.A. | | | 37,091 | | | $ | 1,849,933 | |

| Li & Fung Ltd. | | | 300,200 | | | | 1,595,970 | |

| LVMH Moet Hennessy Louis Vuitton S.A. | | | 22,140 | | | | 3,469,707 | |

| NIKE, Inc., “B” | | | 22,460 | | | | 1,829,142 | |

| | | | | | | | |

| | | | | | | $ | 8,744,752 | |

| Broadcasting - 0.8% | | | | | | | | |

| Publicis Groupe | | | 38,130 | | | $ | 1,899,351 | |

| | |

| Brokerage & Asset Managers - 6.5% | | | | | | | | |

| BM&F Bovespa S.A. | | | 214,600 | | | $ | 1,798,536 | |

| Charles Schwab Corp. | | | 128,430 | | | | 1,977,822 | |

| CME Group, Inc. | | | 8,270 | | | | 2,395,406 | |

| Deutsche Boerse AG | | | 31,230 | | | | 2,197,637 | |

| Franklin Resources, Inc. | | | 21,880 | | | | 2,509,636 | |

| ICAP PLC | | | 338,790 | | | | 2,476,528 | |

| Nomura Holdings, Inc. | | | 277,200 | | | | 1,445,441 | |

| | | | | | | | |

| | | | | | | $ | 14,801,006 | |

| Business Services - 6.0% | | | | | | | | |

| Accenture Ltd., “A” | | | 84,590 | | | $ | 3,782,019 | |

| Cognizant Technology Solutions Corp., “A” (a) | | | 22,950 | | | | 1,496,111 | |

| Dun & Bradstreet Corp. | | | 40,750 | | | | 3,032,208 | |

| Hays PLC | | | 639,080 | | | | 1,131,553 | |

| Intertek Group PLC | | | 48,490 | | | | 1,441,297 | |

| MSCI, Inc., “A” (a) | | | 45,570 | | | | 1,633,685 | |

| Verisk Analytics, Inc., “A” (a) | | | 40,710 | | | | 1,213,565 | |

| | | | | | | | |

| | | | | | | $ | 13,730,438 | |

11

Portfolio of Investments – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Common Stocks - continued | | | | | | | | |

| Chemicals - 1.0% | | | | | | | | |

| Monsanto Co. | | | 39,800 | | | $ | 2,364,916 | |

| | |

| Computer Software - 3.1% | | | | | | | | |

| Autodesk, Inc. (a) | | | 69,020 | | | $ | 2,497,144 | |

| Oracle Corp. (s) | | | 155,100 | | | | 4,559,940 | |

| | | | | | | | |

| | | | | | | $ | 7,057,084 | |

| Computer Software - Systems - 5.5% | | | | | | | | |

| Acer, Inc. | | | 846,510 | | | $ | 2,463,840 | |

| Apple, Inc. (a) | | | 11,280 | | | | 3,393,814 | |

| EMC Corp. (a) | | | 56,560 | | | | 1,188,326 | |

| International Business Machines Corp. | | | 25,870 | | | | 3,714,932 | |

| Konica Minolta Holdings, Inc. | | | 170,000 | | | | 1,638,804 | |

| | | | | | | | |

| | | | | | | $ | 12,399,716 | |

| Consumer Products - 4.6% | | | | | | | | |

| Beiersdorf AG | | | 16,680 | | | $ | 1,086,705 | |

| Church & Dwight Co., Inc. | | | 28,380 | | | | 1,868,823 | |

| Colgate-Palmolive Co. | | | 34,270 | | | | 2,642,902 | |

| Procter & Gamble Co. | | | 35,730 | | | | 2,271,356 | |

| Reckitt Benckiser Group PLC | | | 44,690 | | | | 2,499,871 | |

| | | | | | | | |

| | | | | | | $ | 10,369,657 | |

| Electrical Equipment - 3.8% | | | | | | | | |

| Danaher Corp. | | | 113,150 | | | $ | 4,906,184 | |

| Schneider Electric S.A. | | | 25,837 | | | | 3,667,914 | |

| | | | | | | | |

| | | | | | | $ | 8,574,098 | |

| Electronics - 5.5% | | | | | | | | |

| Hoya Corp. | | | 81,800 | | | $ | 1,902,729 | |

| Microchip Technology, Inc. | | | 58,130 | | | | 1,870,623 | |

| Samsung Electronics Co. Ltd. | | | 2,982 | | | | 1,979,951 | |

| Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 455,808 | | | | 4,972,865 | |

| Tokyo Electron Ltd. | | | 31,200 | | | | 1,749,479 | |

| | | | | | | | |

| | | | | | | $ | 12,475,647 | |

| Energy - Independent - 0.9% | | | | | | | | |

| INPEX Corp. | | | 406 | | | $ | 2,118,850 | |

| | |

| Energy - Integrated - 1.9% | | | | | | | | |

| Chevron Corp. | | | 19,000 | | | $ | 1,569,590 | |

| Hess Corp. | | | 24,430 | | | | 1,539,823 | |

| Suncor Energy, Inc. | | | 38,010 | | | | 1,217,930 | |

| | | | | | | | |

| | | | | | | $ | 4,327,343 | |

12

Portfolio of Investments – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Common Stocks - continued | | | | | | | | |

| Food & Beverages - 4.4% | | | | | | | | |

| Groupe Danone | | | 65,440 | | | $ | 4,141,835 | |

| Mead Johnson Nutrition Co., “A” | | | 18,430 | | | | 1,084,053 | |

| Nestle S.A. | | | 39,767 | | | | 2,178,183 | |

| PepsiCo, Inc. | | | 40,330 | | | | 2,633,549 | |

| | | | | | | | |

| | | | | | | $ | 10,037,620 | |

| Food & Drug Stores - 1.2% | | | | | | | | |

| Tesco PLC | | | 397,573 | | | $ | 2,719,253 | |

| | |

| General Merchandise - 0.7% | | | | | | | | |

| Kohl’s Corp. (a) | | | 28,770 | | | $ | 1,473,024 | |

| | |

| Internet - 0.8% | | | | | | | | |

| Google, Inc., “A” (a) | | | 3,010 | | | $ | 1,845,100 | |

| | |

| Machinery & Tools - 0.5% | | | | | | | | |

| Schindler Holding AG | | | 10,242 | | | $ | 1,098,045 | |

| | |

| Major Banks - 6.1% | | | | | | | | |

| Bank of New York Mellon Corp. | | | 94,520 | | | $ | 2,368,671 | |

| Credit Suisse Group AG | | | 57,610 | | | | 2,379,804 | |

| HSBC Holdings PLC | | | 237,926 | | | | 2,474,634 | |

| Julius Baer Group Ltd. | | | 58,399 | | | | 2,465,215 | |

| Standard Chartered PLC | | | 89,989 | | | | 2,603,420 | |

| State Street Corp. | | | 36,630 | | | | 1,529,669 | |

| | | | | | | | |

| | | | | | | $ | 13,821,413 | |

| Medical & Health Technology & Services - 1.3% | | | | | | | | |

| Fresenius Medical Care AG & Co. KGaA | | | 19,360 | | | $ | 1,233,284 | |

| Patterson Cos., Inc. | | | 64,390 | | | | 1,780,384 | |

| | | | | | | | |

| | | | | | | $ | 3,013,668 | |

| Medical Equipment - 6.8% | | | | | | | | |

| Becton, Dickinson & Co. | | | 19,610 | | | $ | 1,480,947 | |

| DENTSPLY International, Inc. | | | 62,680 | | | | 1,967,525 | |

| Essilor International S.A. | | | 17,800 | | | | 1,188,658 | |

| Medtronic, Inc. | | | 45,630 | | | | 1,606,632 | |

| Sonova Holding AG | | | 16,808 | | | | 1,947,169 | |

| St. Jude Medical, Inc. (a) | | | 26,660 | | | | 1,021,078 | |

| Synthes, Inc. | | | 21,176 | | | | 2,526,358 | |

| Thermo Fisher Scientific, Inc. (a) | | | 45,420 | | | | 2,335,496 | |

| Waters Corp. (a) | | | 18,840 | | | | 1,396,609 | |

| | | | | | | | |

| | | | | | | $ | 15,470,472 | |

13

Portfolio of Investments – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Common Stocks - continued | | | | | | | | |

| Metals & Mining - 2.8% | | | | | | | | |

| BHP Billiton PLC | | | 177,000 | | | $ | 6,277,839 | |

| | |

| Network & Telecom - 2.4% | | | | | | | | |

| Cisco Systems, Inc. (a)(s) | | | 242,660 | | | $ | 5,539,928 | |

| | |

| Oil Services - 3.9% | | | | | | | | |

| National Oilwell Varco, Inc. | | | 84,790 | | | $ | 4,558,310 | |

| Schlumberger Ltd. (s) | | | 61,130 | | | | 4,272,376 | |

| | | | | | | | |

| | | | | | | $ | 8,830,686 | |

| Other Banks & Diversified Financials - 5.3% | | | | | | | | |

| Banco Santander Brasil S.A., ADR | | | 225,330 | | | $ | 3,244,752 | |

| China Construction Bank | | | 1,746,000 | | | | 1,667,985 | |

| HDFC Bank Ltd. | | | 23,000 | | | | 1,180,365 | |

| MasterCard, Inc., “A” | | | 12,920 | | | | 3,101,575 | |

| Visa, Inc., “A” | | | 36,160 | | | | 2,826,627 | |

| | | | | | | | |

| | | | | | | $ | 12,021,304 | |

| Pharmaceuticals - 4.9% | | | | | | | | |

| Abbott Laboratories | | | 20,820 | | | $ | 1,068,482 | |

| Allergan, Inc. | | | 18,510 | | | | 1,340,309 | |

| Bayer AG | | | 36,221 | | | | 2,703,112 | |

| Johnson & Johnson | | | 33,000 | | | | 2,101,110 | |

| Roche Holding AG | | | 9,400 | | | | 1,380,316 | |

| Teva Pharmaceutical Industries Ltd., ADR | | | 50,930 | | | | 2,643,267 | |

| | | | | | | | |

| | | | | | | $ | 11,236,596 | |

| Specialty Chemicals - 5.5% | | | | | | | | |

| Akzo Nobel N.V. (l) | | | 48,890 | | | $ | 2,902,804 | |

| L’Air Liquide S.A. | | | 9,259 | | | | 1,197,688 | |

| Linde AG | | | 19,992 | | | | 2,878,482 | |

| Praxair, Inc. | | | 21,680 | | | | 1,980,251 | |

| Shin-Etsu Chemical Co. Ltd. | | | 48,000 | | | | 2,415,564 | |

| Symrise AG | | | 38,820 | | | | 1,179,198 | |

| | | | | | | | |

| | | | | | | $ | 12,553,987 | |

| Specialty Stores - 2.2% | | | | | | | | |

| Esprit Holdings Ltd. | | | 290,930 | | | $ | 1,578,028 | |

| Industria de Diseno Textil S.A. | | | 26,480 | | | | 2,211,660 | |

| Staples, Inc. | | | 54,590 | | | | 1,117,457 | |

| | | | | | | | |

| | | | | | | $ | 4,907,145 | |

14

Portfolio of Investments – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Common Stocks - continued | | | | | | | | |

| Telecommunications - Wireless - 0.7% | | | | | |

| MTN Group Ltd. | | | 88,320 | | | $ | 1,588,625 | |

| Total Common Stocks (Identified Cost, $209,826,910) | | | | | | $ | 225,144,994 | |

| | | | | | | | | | | | | | | | |

| | | | |

| | | Strike Price | | | First Exercise | | | | | | | |

| Rights - 0.1% | | | | | | | | | | | | | | | | |

| Major Banks - 0.1% | | | | | | | | | | | | | | | | |

Standard Chartered PLC (1 share for

1 right) (Identified Cost, $0) (a) | | | GBP 12.80 | | | | 10/22/10 | | | | 11,248 | | | $ | 94,712 | |

| | | |

| Collateral for Securities Loaned - 0.4% | | | | | | | | | | | | | |

| Morgan Stanley Repurchase Agreement, 0.21%, dated 10/29/10, due 11/01/10, total to be received $945,017 (secured by U.S. Treasury and Federal Agency obligations valued at $963,903 in an individually traded account), at Cost | | | $ | 945,000 | | | $ | 945,000 | |

| | | | |

| Money Market Funds (v) - 0.7% | | | | | | | | | | | | | | | | |

MFS Institutional Money Market Portfolio, 0.21%,

at Cost and Net Asset Value | | | | | | | | 1,592,737 | | | $ | 1,592,737 | |

| Total Investments (Identified Cost, $212,364,647) | | | | | | | | | | | $ | 227,777,443 | |

| | | |

| Other Assets, Less Liabilities - (0.3)% | | | | | | | | | | | | (656,694 | ) |

| Net Assets - 100.0% | | | | | | | | | | | | | | $ | 227,120,749 | |

| (a) | Non-income producing security. |

| (l) | All or a portion of this security is on loan. |

| (s) | Security or a portion of the security was pledged to cover collateral requirements for securities sold short. At October 31, 2010, the value of securities pledged amounted to $182,230. At October 31, 2010, the fund had no short sales outstanding. |

| (v) | Underlying fund that is available only to investment companies managed by MFS. The rate quoted is the annualized seven-day yield of the fund at period end. |

The following abbreviations are used in this report and are defined:

| ADR | | American Depository Receipt |

| PLC | | Public Limited Company |

Abbreviations indicate amounts shown in currencies other than the U.S. dollar. All amounts are stated in U.S. dollars unless otherwise indicated. A list of abbreviations is shown below:

See Notes to Financial Statements

15

Financial Statements

STATEMENT OF ASSETS AND LIABILITIES

At 10/31/10

This statement represents your fund’s balance sheet, which details the assets and liabilities comprising the total value of the fund.

| | | | |

| Assets | | | | |

| Investments- | | | | |

| Non-affiliated issuers, at value (identified cost, $210,771,910) | | | $226,184,706 | |

Underlying funds, at cost and value | | | 1,592,737 | |

Total investments, at value, including $889,396 of securities on loan

(identified cost, $212,364,647) | | | $227,777,443 | |

| Foreign currency, at value (identified cost, $774) | | | 775 | |

Receivables for | | | | |

Investments sold | | | 108,288 | |

Fund shares sold | | | 46,576 | |

Interest and dividends | | | 497,296 | |

Total assets | | | $228,430,378 | |

| Liabilities | | | | |

| Payables for | | | | |

Investments purchased | | | $768 | |

Fund shares reacquired | | | 177,058 | |

Collateral for securities loaned, at value | | | 945,000 | |

| Payable to affiliates | | | | |

Investment adviser | | | 22,392 | |

Shareholder servicing costs | | | 77,871 | |

Distribution and service fees | | | 8,542 | |

Administrative services fee | | | 430 | |

| Payable for independent Trustees’ compensation | | | 41,809 | |

Accrued expenses and other liabilities | | | 35,759 | |

Total liabilities | | | $1,309,629 | |

Net assets | | | $227,120,749 | |

| Net assets consist of | | | | |

Paid-in capital | | | $233,483,826 | |

Unrealized appreciation (depreciation) on investments

and translation of assets and liabilities in foreign currencies | | | 15,432,853 | |

Accumulated net realized gain (loss) on investments

and foreign currency transactions | | | (22,210,734 | ) |

Undistributed net investment income | | | 414,804 | |

Net assets | | | $227,120,749 | |

| Shares of beneficial interest outstanding | | | 9,229,697 | |

16

Statement of Assets and Liabilities – continued

| | | | | | | | | | | | |

| | | Net assets | | | Shares

outstanding | | | Net asset value

per share (a) | |

| Class A | | | $183,544,486 | | | | 7,378,317 | | | | $24.88 | |

| Class B | | | 13,562,831 | | | | 588,826 | | | | 23.03 | |

| Class C | | | 14,484,735 | | | | 635,146 | | | | 22.81 | |

| Class I | | | 6,788,046 | | | | 267,322 | | | | 25.39 | |

| Class R1 | | | 790,815 | | | | 34,734 | | | | 22.77 | |

| Class R2 | | | 5,250,492 | | | | 216,530 | | | | 24.25 | |

| Class R3 | | | 2,528,098 | | | | 101,958 | | | | 24.80 | |

| Class R4 | | | 171,246 | | | | 6,864 | | | | 24.95 | |

| (a) | Maximum offering price per share was equal to the net asset value per share for all share classes, except for Class A, for which the maximum offering price per share was $26.40 [100 / 94.25 x $24.88]. On sales of $50,000 or more, the maximum offering price of Class A shares is reduced. A contingent deferred sales charge may be imposed on redemptions of Class A, Class B, and Class C shares. Redemption price per share was equal to the net asset value per share for Classes I, R1, R2, R3, and R4. |

See Notes to Financial Statements

17

Financial Statements

STATEMENT OF OPERATIONS

Year ended 10/31/10

This statement describes how much your fund earned in investment income and accrued in expenses. It also describes any gains and/or losses generated by fund operations.

| | | | |

| Net investment income | | | | |

Income | | | | |

Dividends | | | $4,407,485 | |

Interest | | | 54,540 | |

Dividends from underlying funds | | | 6,157 | |

Foreign taxes withheld | | | (247,496 | ) |

Total investment income | | | $4,220,686 | |

Expenses | | | | |

Management fee | | | $2,013,554 | |

Distribution and service fees | | | 782,042 | |

Shareholder servicing costs | | | 510,896 | |

Administrative services fee | | | 41,693 | |

Independent Trustees’ compensation | | | 14,853 | |

Custodian fee | | | 93,938 | |

Shareholder communications | | | 36,691 | |

Auditing fees | | | 73,241 | |

Legal fees | | | 4,154 | |

Miscellaneous | | | 120,811 | |

Total expenses | | | $3,691,873 | |

Fees paid indirectly | | | (14 | ) |

Reduction of expenses by investment adviser | | | (1,085 | ) |

Net expenses | | | $3,690,774 | |

Net investment income | | | $529,912 | |

Realized and unrealized gain (loss) on investments

and foreign currency transactions | | | | |

Realized gain (loss) (identified cost basis) | | | | |

Investment transactions (net of $772 country tax) | | | $8,359,018 | |

Foreign currency transactions | | | (68,008 | ) |

Net realized gain (loss) on investments

and foreign currency transactions | | | $8,291,010 | |

Change in unrealized appreciation (depreciation) | | | | |

Investments | | | $19,880,556 | |

Translation of assets and liabilities in foreign currencies | | | 10,991 | |

Net unrealized gain (loss) on investments

and foreign currency translation | | | $19,891,547 | |

Net realized and unrealized gain (loss) on investments

and foreign currency | | | $28,182,557 | |

Change in net assets from operations | | | $28,712,469 | |

See notes to financial statements

18

Financial Statements

STATEMENTS OF CHANGES IN NET ASSETS

These statements describe the increases and/or decreases in net assets resulting from operations, any distributions, and any shareholder transactions.

| | | | | | | | |

| | | Years ended 10/31 | |

| | | 2010 | | | 2009 | |

| Change in net assets | | | | | | |

| From operations | | | | | | | | |

Net investment income | | | $529,912 | | | | $911,276 | |

Net realized gain (loss) on investments and

foreign currency transactions | | | 8,291,010 | | | | (24,756,718 | ) |

Net unrealized gain (loss) on investments and

foreign currency translation | | | 19,891,547 | | | | 69,445,156 | |

Change in net assets from operations | | | $28,712,469 | | | | $45,599,714 | |

| Distributions declared to shareholders | | | | | | | | |

From net investment income | | | $(823,079 | ) | | | $(24,131 | ) |

Change in net assets from fund share transactions | | | $(26,067,852 | ) | | | $(14,939,634 | ) |

Total change in net assets | | | $1,821,538 | | | | $30,635,949 | |

| Net assets | | | | | | | | |

At beginning of period | | | 225,299,211 | | | | 194,663,262 | |

At end of period (including undistributed net investment

income of $414,804 and $775,207, respectively) | | | $227,120,749 | | | | $225,299,211 | |

See notes to financial statements

19

Financial Statements

FINANCIAL HIGHLIGHTS

The financial highlights table is intended to help you understand the fund’s financial performance for the past 5 years. Certain information reflects financial results for a single fund share. The total returns in the table represent the rate by which an investor would have earned (or lost) on an investment in the fund share class (assuming reinvestment of all distributions) held for the entire period.

| | | | | | | | | | | | | | | | | | | | |

| Class A | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $21.93 | | | | $17.35 | | | | $29.26 | | | | $23.97 | | | | $20.10 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.08 | | | | $0.11 | | | | $0.08 | | | | $0.25 | | | | $0.11 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 2.96 | | | | 4.47 | | | | (11.82 | ) | | | 5.28 | | | | 3.76 | |

Total from investment operations | | | $3.04 | | | | $4.58 | | | | $(11.74 | ) | | | $5.53 | | | | $3.87 | |

| Less distributions declared to shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.09 | ) | | | $(0.00 | )(w) | | | $(0.17 | ) | | | $(0.24 | ) | | | $— | |

Net asset value, end of period | | | $24.88 | | | | $21.93 | | | | $17.35 | | | | $29.26 | | | | $23.97 | |

Total return (%) (r)(s)(t) | | | 13.92 | | | | 26.40 | | | | (40.34 | ) | | | 23.24 | | | | 19.25 | |

| Ratios (%) (to average net assets) and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 1.55 | | | | 1.70 | | | | 1.62 | | | | 1.58 | | | | 1.61 | |

Expenses after expense reductions (f) | | | 1.55 | | | | 1.67 | | | | 1.52 | | | | 1.48 | | | | 1.51 | |

Net investment income | | | 0.34 | | | | 0.59 | | | | 0.30 | | | | 0.97 | | | | 0.49 | |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $183,544 | | | | $180,278 | | | | $153,184 | | | | $297,956 | | | | $290,952 | |

See Notes to Financial Statements

20

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | | | |

| Class B | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $20.37 | | | | $16.24 | | | | $27.42 | | | | $22.46 | | | | $18.98 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (d) | | | $(0.09 | ) | | | $(0.03 | ) | | | $(0.11 | ) | | | $0.06 | | | | $(0.05 | ) |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.75 | | | | 4.16 | | | | (11.07 | ) | | | 4.95 | | | | 3.53 | |

Total from investment operations | | | $2.66 | | | | $4.13 | | | | $(11.18 | ) | | | $5.01 | | | | $3.48 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $— | | | | $— | | | | $— | | | | $(0.05 | ) | | | $— | |

Net asset value, end of period | | | $23.03 | | | | $20.37 | | | | $16.24 | | | | $27.42 | | | | $22.46 | |

Total return (%) (r)(s)(t) | | | 13.06 | | | | 25.43 | | | | (40.77 | ) | | | 22.35 | | | | 18.34 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 2.30 | | | | 2.43 | | | | 2.27 | | | | 2.23 | | | | 2.26 | |

Expenses after expense reductions (f) | | | 2.30 | | | | 2.43 | | | | 2.27 | | | | 2.23 | | | | 2.26 | |

Net investment income (loss) | | | (0.43 | ) | | | (0.19 | ) | | | (0.47 | ) | | | 0.25 | | | | (0.26 | ) |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $13,563 | | | | $17,219 | | | | $19,582 | | | | $64,416 | | | | $75,573 | |

| |

| Class C | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $20.17 | | | | $16.08 | | | | $27.15 | | | | $22.26 | | | | $18.80 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (d) | | | $(0.09 | ) | | | $(0.03 | ) | | | $(0.11 | ) | | | $0.05 | | | | $(0.06 | ) |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.73 | | | | 4.12 | | | | (10.96 | ) | | | 4.91 | | | | 3.52 | |

Total from investment operations | | | $2.64 | | | | $4.09 | | | | $(11.07 | ) | | | $4.96 | | | | $3.46 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $— | | | | $— | | | | $ (0.00 | )(w) | | | $(0.07 | ) | | | $— | |

Net asset value, end of period | | | $22.81 | | | | $20.17 | | | | $16.08 | | | | $27.15 | | | | $22.26 | |

Total return (%) (r)(s)(t) | | | 13.09 | | | | 25.44 | | | | (40.77 | ) | | | 22.33 | | | | 18.40 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 2.30 | | | | 2.42 | | | | 2.27 | | | | 2.23 | | | | 2.26 | |

Expenses after expense reductions (f) | | | 2.30 | | | | 2.41 | | | | 2.27 | | | | 2.23 | | | | 2.26 | |

Net investment income (loss) | | | (0.41 | ) | | | (0.19 | ) | | | (0.45 | ) | | | 0.21 | | | | (0.27 | ) |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $14,485 | | | | $13,598 | | | | $10,326 | | | | $20,249 | | | | $20,450 | |

See Notes to Financial Statements

21

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | | | |

| Class I | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $22.37 | | | | $17.73 | | | | $29.87 | | | | $24.46 | | | | $20.46 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.14 | | | | $0.16 | | | | $0.14 | | | | $0.32 | | | | $0.17 | |

Net realized and unrealized gain (loss) on investments and foreign currency | | | 3.02 | | | | 4.55 | | | | (12.05 | ) | | | 5.39 | | | | 3.83 | |

Total from investment operations | | | $3.16 | | | | $4.71 | | | | $(11.91 | ) | | | $5.71 | | | | $4.00 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.14 | ) | | | $(0.07 | ) | | | $(0.23 | ) | | | $(0.30 | ) | | | $— | |

Net asset value, end of period | | | $25.39 | | | | $22.37 | | | | $17.73 | | | | $29.87 | | | | $24.46 | |

Total return (%) (r)(s) | | | 14.18 | | | | 26.68 | | | | (40.16 | ) | | | 23.57 | | | | 19.55 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 1.30 | | | | 1.42 | | | | 1.27 | | | | 1.23 | | | | 1.26 | |

Expenses after expense reductions (f) | | | 1.30 | | | | 1.41 | | | | 1.27 | | | | 1.23 | | | | 1.26 | |

Net investment income | | | 0.60 | | | | 0.84 | | | | 0.54 | | | | 1.22 | | | | 0.74 | |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $6,788 | | | | $5,875 | | | | $4,306 | | | | $7,739 | | | | $7,368 | |

| |

| Class R1 | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $20.14 | | | | $16.05 | | | | $27.29 | | | | $22.42 | | | | $18.96 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment loss (d) | | | $(0.08 | ) | | | $(0.02 | ) | | | $(0.12 | ) | | | $(0.10 | ) | | | $(0.07 | ) |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.71 | | | | 4.11 | | | | (10.95 | ) | | | 5.06 | | | | 3.53 | |

Total from investment operations | | | $2.63 | | | | $4.09 | | | | $(11.07 | ) | | | $4.96 | | | | $3.46 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $— | | | | $— | | | | $(0.17 | ) | | | $(0.09 | ) | | | $— | |

Net asset value, end of period | | | $22.77 | | | | $20.14 | | | | $16.05 | | | | $27.29 | | | | $22.42 | |

Total return (%) (r)(s) | | | 13.06 | | | | 25.48 | | | | (40.80 | ) | | | 22.17 | | | | 18.25 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | �� | | | |

Expenses before expense reductions (f) | | | 2.30 | | | | 2.41 | | | | 2.31 | | | | 2.35 | | | | 2.45 | |

Expenses after expense reductions (f) | | | 2.30 | | | | 2.41 | | | | 2.31 | | | | 2.33 | | | | 2.35 | |

Net investment loss | | | (0.38 | ) | | | (0.11 | ) | | | (0.53 | ) | | | (0.43 | ) | | | (0.35 | ) |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $791 | | | | $886 | | | | $632 | | | | $1,009 | | | | $127 | |

See Notes to Financial Statements

22

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | | | |

| Class R2 | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $21.37 | | | | $16.95 | | | | $28.77 | | | | $23.58 | | | | $19.85 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.02 | | | | $0.06 | | | | $0.02 | | | | $0.04 | | | | $0.03 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.90 | | | | 4.36 | | | | (11.66 | ) | | | 5.29 | | | | 3.70 | |

Total from investment operations | | | $2.92 | | | | $4.42 | | | | $(11.64 | ) | | | $5.33 | | | | $3.73 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.04 | ) | | | $— | | | | $(0.18 | ) | | | $(0.14 | ) | | | $— | |

Net asset value, end of period | | | $24.25 | | | | $21.37 | | | | $16.95 | | | | $28.77 | | | | $23.58 | |

Total return (%) (r)(s) | | | 13.66 | | | | 26.08 | | | | (40.70 | ) | | | 22.73 | | | | 18.79 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 1.80 | | | | 1.93 | | | | 1.79 | | | | 1.90 | | | | 2.00 | |

Expenses after expense reductions (f) | | | 1.80 | | | | 1.93 | | | | 1.79 | | | | 1.88 | | | | 1.90 | |

Net investment income | | | 0.10 | | | | 0.36 | | | | 0.06 | | | | 0.16 | | | | 0.15 | |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $5,250 | | | | $5,128 | | | | $4,808 | | | | $4,168 | | | | $619 | |

| |

| Class R3 | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $21.86 | | | | $17.29 | | | | $29.16 | | | | $23.91 | | | | $20.08 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.08 | | | | $0.11 | | | | $0.07 | | | | $0.15 | | | | $0.11 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.96 | | | | 4.46 | | | | (11.78 | ) | | | 5.33 | | | | 3.72 | |

Total from investment operations | | | $3.04 | | | | $4.57 | | | | $(11.71 | ) | | | $5.48 | | | | $3.83 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.10 | ) | | | $— | | | | $(0.16 | ) | | | $(0.23 | ) | | | $— | |

Net asset value, end of period | | | $24.80 | | | | $21.86 | | | | $17.29 | | | | $29.16 | | | | $23.91 | |

Total return (%) (r)(s) | | | 13.93 | | | | 26.43 | | | | (40.37 | ) | | | 23.10 | | | | 19.07 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 1.55 | | | | 1.67 | | | | 1.55 | | | | 1.62 | | | | 1.64 | |

Expenses after expense reductions (f) | | | 1.55 | | | | 1.67 | | | | 1.55 | | | | 1.62 | | | | 1.64 | |

Net investment income | | | 0.34 | | | | 0.60 | | | | 0.28 | | | | 0.58 | | | | 0.48 | |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $2,528 | | | | $2,168 | | | | $1,779 | | | | $3,563 | | | | $1,857 | |

See Notes to Financial Statements

23

Financial Highlights – continued

| | | | | | | | | | | | | | | | | | | | |

| Class R4 | | Years ended 10/31 | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net asset value, beginning of period | | | $21.98 | | | | $17.41 | | | | $29.33 | | | | $24.02 | | | | $20.11 | |

| Income (loss) from investment operations | | | | | | | | | | | | | | | | | | | | |

Net investment income (d) | | | $0.14 | | | | $0.19 | | | | $0.14 | | | | $0.28 | | | | $0.14 | |

Net realized and unrealized gain (loss)

on investments and foreign currency | | | 2.97 | | | | 4.44 | | | | (11.85 | ) | | | 5.31 | | | | 3.77 | |

Total from investment operations | | | $3.11 | | | | $4.63 | | | | $(11.71 | ) | | | $5.59 | | | | $3.91 | |

Less distributions declared to

shareholders | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | $(0.14 | ) | | | $(0.06 | ) | | | $(0.21 | ) | | | $(0.28 | ) | | | $— | |

Net asset value, end of period | | | $24.95 | | | | $21.98 | | | | $17.41 | | | | $29.33 | | | | $24.02 | |

Total return (%) (r)(s) | | | 14.21 | | | | 26.73 | | | | (40.20 | ) | | | 23.47 | | | | 19.44 | |

Ratios (%) (to average net assets)

and Supplemental data: | | | | | | | | | | | | | | | | | | | | |

Expenses before expense reductions (f) | | | 1.30 | | | | 1.38 | | | | 1.29 | | | | 1.33 | | | | 1.35 | |

Expenses after expense reductions (f) | | | 1.30 | | | | 1.38 | | | | 1.29 | | | | 1.33 | | | | 1.35 | |

Net investment income | | | 0.60 | | | | 1.03 | | | | 0.54 | | | | 1.07 | | | | 0.65 | |

Portfolio turnover | | | 63 | | | | 83 | | | | 88 | | | | 68 | | | | 96 | |

Net assets at end of period (000 omitted) | | | $171 | | | | $146 | | | | $46 | | | | $78 | | | | $63 | |

| (d) | Per share data is based on average shares outstanding. |

| (f) | Ratios do not reflect reductions from fees paid indirectly, if applicable. |

| (r) | Certain expenses have been reduced without which performance would have been lower. |

| (s) | From time to time the fund may receive proceeds from litigation settlements, without which performance would be lower. |

| (t) | Total returns do not include any applicable sales charges. |

| (w) | Per share amount was less than $0.01. |

See Notes to Financial Statements

24

NOTES TO FINANCIAL STATEMENTS

| (1) | | Business and Organization |

MFS Global Growth Fund (the fund) is a series of MFS Series Trust VIII (the trust). The trust is organized as a Massachusetts business trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company.

| (2) | | Significant Accounting Policies |

General – The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated subsequent events occurring after the date of the fund’s Statement of Assets and Liabilities through the date that the financial statements were issued. The fund can invest in foreign securities, including securities of emerging market issuers. Investments in foreign securities are vulnerable to the effects of changes in the relative values of the local currency and the U.S. dollar and to the effects of changes in each country’s legal, political, and economic environment. The markets of emerging markets countries are generally more volatile than the markets of developed countries with more mature economies. All of the risks of investing in foreign securities previously described are heightened when investing in emerging markets countries.

Investment Valuations – Equity securities, including restricted equity securities, are generally valued at the last sale or official closing price as provided by a third-party pricing service on the market or exchange on which they are primarily traded. Equity securities, for which there were no sales reported that day, are generally valued at the last quoted daily bid quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Equity securities held short, for which there were no sales reported for that day, are generally valued at the last quoted daily ask quotation as provided by a third-party pricing service on the market or exchange on which such securities are primarily traded. Short-term instruments with a maturity at issuance of 60 days or less generally are valued at amortized cost, which approximates market value. Open-end investment companies are generally valued at net asset value per share. Securities and other assets generally valued on the basis of information from a third-party pricing service may also be valued at a broker/dealer bid quotation. Values obtained from third-party pricing services can utilize both transaction data and

25

Notes to Financial Statements – continued

market information such as yield, quality, coupon rate, maturity, type of issue, trading characteristics, and other market data. The values of foreign securities and other assets and liabilities expressed in foreign currencies are converted to U.S. dollars using the mean of bid and asked prices for rates provided by a third-party pricing service.

The Board of Trustees has delegated primary responsibility for determining or causing to be determined the value of the fund’s investments (including any fair valuation) to the adviser pursuant to valuation policies and procedures approved by the Board. If the adviser determines that reliable market quotations are not readily available, investments are valued at fair value as determined in good faith by the adviser in accordance with such procedures under the oversight of the Board of Trustees. Under the fund’s valuation policies and procedures, market quotations are not considered to be readily available for most types of debt instruments and floating rate loans and many types of derivatives. These investments are generally valued at fair value based on information from third-party pricing services. In addition, investments may be valued at fair value if the adviser determines that an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded (such as foreign exchange or market) and prior to the determination of the fund’s net asset value, or after the halting of trading of a specific security where trading does not resume prior to the close of the exchange or market on which the security is principally traded. Events that occur on a frequent basis after foreign markets close (such as developments in foreign markets and significant movements in the U.S. markets) and prior to the determination of the fund’s net asset value may be deemed to have a material effect on the value of securities traded in foreign markets. Accordingly, the fund’s foreign equity securities may often be valued at fair value. The adviser generally relies on third-party pricing services or other information (such as the correlation with price movements of similar securities in the same or other markets; the type, cost and investment characteristics of the security; the business and financial condition of the issuer; and trading and other market data) to assist in determining whether to fair value and at what value to fair value an investment. The value of an investment for purposes of calculating the fund’s net asset value can differ depending on the source and method used to determine value. When fair valuation is used, the value of an investment used to determine the fund’s net asset value may differ from quoted or published prices for the same investment. There can be no assurance that the fund could obtain the fair value assigned to an investment if it were to sell the investment at the same time at which the fund determines its net asset value per share.

26

Notes to Financial Statements – continued

Various inputs are used in determining the value of the fund’s assets or liabilities. These inputs are categorized into three broad levels. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement. The fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment, and considers factors specific to the investment. Level 1 includes unadjusted quoted prices in active markets for identical assets or liabilities. Level 2 includes other significant observable market-based inputs (including quoted prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3 includes unobservable inputs, which may include the adviser’s own assumptions in determining the fair value of investments. The following is a summary of the levels used as of October 31, 2010 in valuing the fund’s assets or liabilities:

| | | | | | | | | | | | | | | | |

| Investments at Value | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Equity Securities: | | | | | | | | | | | | | | | | |

United States | | | $106,836,019 | | | | $— | | | | $— | | | | $106,836,019 | |

United Kingdom | | | 24,908,280 | | | | — | | | | — | | | | 24,908,280 | |

France | | | 19,361,184 | | | | — | | | | — | | | | 19,361,184 | |

Switzerland | | | 15,825,023 | | | | — | | | | — | | | | 15,825,023 | |

Germany | | | 11,278,417 | | | | — | | | | — | | | | 11,278,417 | |

Japan | | | — | | | | 11,270,867 | | | | — | | | | 11,270,867 | |

Brazil | | | 8,226,314 | | | | — | | | | — | | | | 8,226,314 | |

Taiwan | | | 4,972,866 | | | | 2,463,840 | | | | — | | | | 7,436,706 | |

Netherlands | | | 4,433,116 | | | | — | | | | — | | | | 4,433,116 | |

Other Countries | | | 8,841,847 | | | | 6,821,933 | | | | — | | | | 15,663,780 | |

| Short Term Securities | | | — | | | | 945,000 | | | | — | | | | 945,000 | |

| Mutual Funds | | | 1,592,737 | | | | — | | | | — | | | | 1,592,737 | |

| Total Investments | | | $206,275,803 | | | | $21,501,640 | | | | $— | | | | $227,777,443 | |

For further information regarding security characteristics, see the Portfolio of Investments. Of the Level 1 investments presented above, equity investments amounting to $54,905,745 were considered level 2 investments at the beginning of the period. The primary reason for changes in the classifications between levels 1 and 2 occurs when foreign equity securities are fair valued using other observable market-based inputs in place of the closing exchange price due to events occurring after the close of the exchange or market on which the investment is principally traded. The fund’s foreign equity securities may often be valued at fair value.

Repurchase Agreements – The fund entered into repurchase agreements with approved counterparties. Each repurchase agreement is recorded at cost. The fund requires that the securities collateral in a repurchase transaction be

27

Notes to Financial Statements – continued

transferred to a custodian. The fund monitors, on a daily basis, the value of the collateral to ensure that its value, including accrued interest, is greater than amounts owed to the fund under each such repurchase agreement.

Foreign Currency Translation – Purchases and sales of foreign investments, income, and expenses are converted into U.S. dollars based upon currency exchange rates prevailing on the respective dates of such transactions or on the reporting date for foreign denominated receivables and payables. Gains and losses attributable to foreign currency exchange rates on sales of securities are recorded for financial statement purposes as net realized gains and losses on investments. Gains and losses attributable to foreign exchange rate movements on receivables, payables, income and expenses are recorded for financial statement purposes as foreign currency transaction gains and losses. That portion of both realized and unrealized gains and losses on investments that results from fluctuations in foreign currency exchange rates is not separately disclosed.

Short Sales – The fund may enter into short sales whereby it sells a security it does not own in anticipation of a decline in the value of that security. The fund will realize a gain if the security price decreases and a loss if the security price increases between the date of the short sale and the date on which the fund replaces the borrowed security. Losses from short sales can exceed the proceeds of the security sold; and they can also exceed the potential loss from an ordinary buy and sell transaction. The amount of any premium, dividends, or interest the fund may be required to pay in connection with a short sale will be recognized as a fund expense. The fund segregates cash or marketable securities in an amount that, when combined with the amount of proceeds from the short sale deposited with the broker, at least equals the current market value of the security sold short. At October 31, 2010, the fund has yet to enter into such transactions.

Security Loans – JPMorgan Chase and Co. (“Chase”), as lending agent, loans the securities of the fund to certain qualified institutions (the “Borrowers”) approved by the fund. The loans are collateralized by cash and/or U.S. Treasury and federal agency obligations in an amount typically at least equal to the market value of the securities loaned. The market value of the loaned securities is determined at the close of business of the fund and any additional required collateral is delivered to the fund on the next business day. Chase provides the fund with indemnification against Borrower default. The fund bears the risk of loss with respect to the investment of cash collateral. On loans collateralized by cash, the cash collateral is invested in short-term securities. A portion of the income generated upon investment of the collateral is remitted to the Borrowers, and the remainder is allocated between the fund and the lending agent. On loans collateralized by U.S. Treasury and/or federal agency

28

Notes to Financial Statements – continued

obligations, a fee is received from the Borrower, and is allocated between the fund and the lending agent. Income from securities lending is included in interest income on the Statement of Operations. The dividend and interest income earned on the securities loaned is accounted for in the same manner as other dividend and interest income.

Indemnifications – Under the fund’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into agreements with service providers that may contain indemnification clauses. The fund’s maximum exposure under these agreements is unknown as this would involve future claims that may be made against the fund that have not yet occurred.

Investment Transactions and Income – Investment transactions are recorded on the trade date. Interest income is recorded on the accrual basis. All premium and discount is amortized or accreted for financial statement purposes in accordance with U.S. generally accepted accounting principles. Dividends received in cash are recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded when the fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Dividend and interest payments received in additional securities are recorded on the ex-dividend or ex-interest date in an amount equal to the value of the security on such date.

The fund may receive proceeds from litigation settlements. Any proceeds received from litigation involving portfolio holdings are reflected in the Statement of Operations in realized gain/loss if the security has been disposed of by the fund or in unrealized gain/loss if the security is still held by the fund. Any other proceeds from litigation not related to portfolio holdings are reflected as other income in the Statement of Operations.

Fees Paid Indirectly – The fund’s custody fee may be reduced according to an arrangement that measures the value of cash deposited with the custodian by the fund. This amount, for the year ended October 31, 2010, is shown as a reduction of total expenses on the Statement of Operations.

Tax Matters and Distributions – The fund intends to qualify as a regulated investment company, as defined under Subchapter M of the Internal Revenue Code, and to distribute all of its taxable income, including realized capital gains. As a result, no provision for federal income tax is required. The fund’s federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service. Foreign taxes, if any, have been accrued by the fund in the accompanying financial statements.

29

Notes to Financial Statements – continued

Distributions to shareholders are recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from U.S. generally accepted accounting principles. Certain capital accounts in the financial statements are periodically adjusted for permanent differences in order to reflect their tax character. These adjustments have no impact on net assets or net asset value per share. Temporary differences which arise from recognizing certain items of income, expense, gain or loss in different periods for financial statement and tax purposes will reverse at some time in the future. Distributions in excess of net investment income or net realized gains are temporary overdistributions for financial statement purposes resulting from differences in the recognition or classification of income or distributions for financial statement and tax purposes.

Book/tax differences primarily relate to wash sale loss deferrals and foreign taxes.

The tax character of distributions declared to shareholders for the last two fiscal years is as follows:

| | | | | | | | |

| | | 10/31/10 | | | 10/31/09 | |

Ordinary income (including any

short-term capital gains) | | | $823,079 | | | | $24,131 | |

The federal tax cost and the tax basis components of distributable earnings were as follows:

| | | | |

| As of 10/31/10 | | | |

| Cost of investments | | | $212,614,749 | |

| Gross appreciation | | | 26,972,420 | |

| Gross depreciation | | | (11,809,726 | ) |

| Net unrealized appreciation (depreciation) | | | $15,162,694 | |

| |

| Undistributed ordinary income | | | 468,030 | |

| Capital loss carryforwards | | | (21,960,632 | ) |

| Other temporary differences | | | (33,169 | ) |

As of October 31, 2010 the fund had capital loss carryforwards available to offset future realized gains. Such losses expire as follows:

Multiple Classes of Shares of Beneficial Interest – The fund offers multiple classes of shares, which differ in their respective distribution and service fees. The fund’s income, realized and unrealized gain (loss), and common expenses are allocated to shareholders based on the daily net assets of each class. Dividends are declared separately for each class. Differences in per share dividend rates are generally due to differences in separate class expenses.

30

Notes to Financial Statements – continued

Class B shares will convert to Class A shares approximately eight years after purchase. The fund’s distributions declared to shareholders as reported on the Statements of Changes in Net Assets are presented by class as follows:

| | | | | | | | |

| | | From net investment

income | |

| | | Year ended

10/31/10 | | | Year ended

10/31/09 | |

| Class A | | | $767,065 | | | | $7,021 | |

| Class I | | | 37,502 | | | | 16,937 | |

| Class R2 | | | 7,879 | | | | — | |

| Class R3 | | | 9,694 | | | | — | |

| Class R4 | | | 939 | | | | 173 | |

| Total | | | $823,079 | | | | $24,131 | |

| (3) | | Transactions with Affiliates |

Investment Adviser – The fund has an investment advisory agreement with MFS to provide overall investment management and related administrative services and facilities to the fund. The management fee is computed daily and paid monthly at the following annual rates:

| | | | |

| First $1 billion of average daily net assets | | | 0.90 | % |

| Next $1 billion of average daily net assets | | | 0.75 | % |

| Average daily net assets in excess of $2 billion | | | 0.65 | % |

The management fee incurred for the year ended October 31, 2010 was equivalent to an annual effective rate of 0.90% of the fund’s average daily net assets.

Distributor – MFS Fund Distributors, Inc. (MFD), a wholly-owned subsidiary of MFS, as distributor, received $13,371 for the year ended October 31, 2010, as its portion of the initial sales charge on sales of Class A shares of the fund.

The Board of Trustees has adopted a distribution plan for certain class shares pursuant to Rule 12b-1 of the Investment Company Act of 1940.

The fund’s distribution plan provides that the fund will pay MFD for services provided by MFD and financial intermediaries in connection with the distribution and servicing of certain share classes. One component of the plan is a distribution fee paid to MFD and another component of the plan is a service fee paid to MFD. MFD may subsequently pay all, or a portion, of the distribution and/or service fees to financial intermediaries.

31

Notes to Financial Statements – continued

Distribution Plan Fee Table:

| | | | | | | | | | | | | | | | | | | | |

| | | Distribution

Fee Rate (d) | | | Service

Fee Rate (d) | | | Total

Distribution

Plan (d) | | | Annual

Effective

Rate (e) | | | Distribution

and Service

Fee | |

| Class A | | | — | | | | 0.25% | | | | 0.25% | | | | 0.25% | | | | $449,142 | |

| Class B | | | 0.75% | | | | 0.25% | | | | 1.00% | | | | 1.00% | | | | 152,139 | |

| Class C | | | 0.75% | | | | 0.25% | | | | 1.00% | | | | 1.00% | | | | 141,000 | |

| Class R1 | | | 0.75% | | | | 0.25% | | | | 1.00% | | | | 1.00% | | | | 9,133 | |

| Class R2 | | | 0.25% | | | | 0.25% | | | | 0.50% | | | | 0.50% | | | | 24,830 | |

| Class R3 | | | — | | | | 0.25% | | | | 0.25% | | | | 0.25% | | | | 5,798 | |

| Total Distribution and Service Fees | | | | | | | | $782,042 | |

| (d) | In accordance with the distribution plan for certain classes, the fund pays distribution and/or service fees equal to these annual percentage rates of each class’ average daily net assets. The distribution and service fee rates disclosed by class represent the current rates in effect at the end of the reporting period. Any rate changes, if applicable, are detailed below. |

| (e) | The annual effective rates represent actual fees incurred under the distribution plan for the year ended October 31, 2010 based on each class’ average daily net assets. |

Certain Class A shares are subject to a contingent deferred sales charge (CDSC) in the event of a shareholder redemption within 24 months of purchase. Class C shares are subject to a CDSC in the event of a shareholder redemption within 12 months of purchase. Class B shares are subject to a CDSC in the event of a shareholder redemption within six years of purchase. All contingent deferred sales charges are paid to MFD and during the year ended October 31, 2010, were as follows:

| | | | |

| | | Amount | |

| Class A | | | $78 | |

| Class B | | | 14,267 | |

| Class C | | | 227 | |