UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Mutual Funds

Nuveen Income Funds

For investors seeking attractive monthly income and portfolio diversification potential.

Annual Report

June 30, 2012

| | | | | | | | | | |

| | | Share Class / Ticker Symbol |

| | | | | |

| Fund Name | | Class A | | Class B | | Class C | | Class R3 | | Class I |

Nuveen Core Plus Bond Fund

(formerly Nuveen Core Bond Fund) | | FAFIX | | FFIBX | | FFAIX | | FFISX | | FFIIX |

Nuveen High Income Bond Fund | | FJSIX | | FJSBX | | FCSIX | | FANSX | | FJSYX |

Nuveen Inflation Protected Securities Fund | | FAIPX | | — | | FCIPX | | FRIPX | | FYIPX |

Nuveen Intermediate Government Bond Fund | | FIGAX | | — | | FYGCX | | FYGRX | | FYGYX |

Nuveen Intermediate Term Bond Fund | | FAIIX | | — | | NTIBX | | — | | FINIX |

Nuveen Short Term Bond Fund | | FALTX | | — | | FBSCX | | NSSRX | | FLTIX |

Nuveen Strategic Income Fund

(formerly Nuveen Total Return Bond Fund) | | FCDDX | | FCBBX | | FCBCX | | FABSX | | FCBYX |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Table of Contents

Chairman’s

Letter to Shareholders

Dear Shareholders,

Investors have many reasons to remain cautious. The challenges in the Euro area are casting a shadow over global economies and financial markets. The political support for addressing fiscal issues is eroding as the economic and social impacts become more visible. At the same time, member nations appear unwilling to provide adequate financial support or to surrender sufficient sovereignty to strengthen the banks or unify the Euro area financial system. The gains made in reducing deficits, and the hard-won progress on winning popular acceptance of the need for economic austerity, are at risk. To their credit, European political leaders press on to find compromise solutions, but there is increasing concern that time will begin to run out.

In the U.S., strong corporate earnings have enabled the equity markets to withstand much of the downward pressures coming from weakening job creation, slower economic growth and political uncertainty. The Fed remains committed to low interest rates but has refrained from predicting another program of quantitative easing unless economic growth were to weaken significantly or the threat of recession appears on the horizon. Pre-election maneuvering has added to the already highly partisan atmosphere in the Congress. The end of the Bush-era tax cuts and implementation of the spending restrictions of the Budget Control Act of 2011, both scheduled to take place at year-end, loom closer.

During the last year, U.S. based investors have experienced a sharp decline and a strong recovery in the equity markets. The experienced investment teams at Nuveen keep their eye on a longer time horizon and use their practiced investment disciplines to negotiate through market peaks and valleys to achieve long-term goals for investors. Experienced professionals pursue investments that will weather short-term volatility and at the same time, seek opportunities that are created by markets that overreact to negative developments. Monitoring this process is an important consideration for the Fund Board as it oversees your Nuveen Fund on your behalf.

As always, I encourage you to contact your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

August 23, 2012

Portfolio Managers’ Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

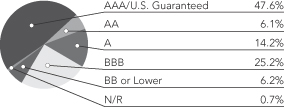

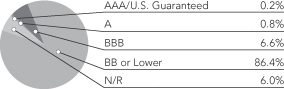

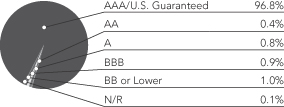

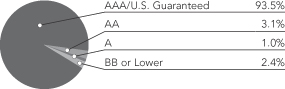

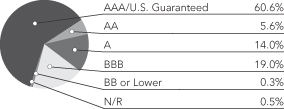

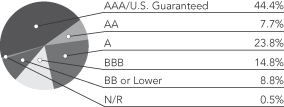

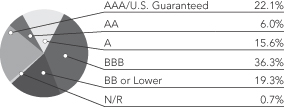

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by a national rating agency.

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen Investments. In this report, the various portfolio management teams for the Funds examine economic and market conditions, key investment strategies and the Funds’ performance during the twelve months ending June 30, 2012. These management teams include:

Nuveen Core Plus Bond Fund (formerly Nuveen Core Bond Fund)

Effective May 14, 2012, the Nuveen Core Bond Fund’s name changed to the Nuveen Core Plus Bond Fund. There were no changes to the Fund’s management team, investment objectives or policies. Chris Neuharth, CFA, who has 31 years of investment experience, has managed the Fund since 2006. Timothy Palmer, CFA, with 26 years of investment experience, Wan-Chong Kung, CFA, with 28 years of financial experience, and Jeffrey Ebert, with 21 years of financial experience, have been part of the management team for the Fund since 2003, 2001, and 2005, respectively.

Nuveen High Income Bond Fund

John Fruit, CFA, who has 24 years of investment experience, has managed the Fund since 2006. Jeffrey Schmitz, CFA, with 25 years of investment experience, has been part of the management team for the Fund since 2008.

Nuveen Inflation Protected Securities Fund

Wan-Chong Kung, CFA, has managed the Fund since its inception in 2004. Chad Kemper, who has 13 years of investment experience, joined the Fund as a co-portfolio manager in October 2010.

Nuveen Intermediate Government Bond Fund

Wan-Chong Kung, CFA, has managed the Fund since 2002. Chris Neuharth, CFA, and Jason O’Brien, CFA, who has 19 years of investment experience, have been on the Fund’s management team since 2009.

Nuveen Intermediate Term Bond Fund

Effective May 14, 2012, the Fund’s benchmark was changed to the Barclays Aggregate Bond Index to more closely reflect its investment universe. At the same time, Chris Neuharth, CFA, joined the Fund as a co-portfolio manager. Wan-Chong Kung, CFA, has managed the Fund since 2002 and Jeffrey Ebert since 2000.

Nuveen Short Term Bond Fund

Chris Neuharth, CFA, has been a co-portfolio manager of the Fund since 2004. Peter Agrimson, CFA, who has seven years of investment experience, joined the Fund as a co-portfolio manager on January 1, 2011.

Nuveen Strategic Income Fund (formerly Nuveen Total Return Bond Fund)

Effective May 14, 2012, the Nuveen Total Return Bond Fund’s name changed to the Nuveen Strategic Income Fund. In addition, the Fund’s investment objective and investment policies also changed; however, its management team remained the same. Please refer to the Fund’s prospectus for additional information regarding these changes. Timothy Palmer, CFA, has been the lead manager of the Fund since 2005. Jeffrey Ebert has been on the management team since 2000. Marie Newcome, CFA, who has 20 years of investment experience, joined the Fund as a co-portfolio manager in 2011.

What factors affected the U.S. economic and fixed-income market environments during the twelve-month reporting period ended June 30, 2012?

During the period, the U.S. economy’s progress toward recovery from recession remained sluggish. The Federal Reserve (Fed) maintained its efforts to improve the overall economic environment by continuing to hold the benchmark Fed Funds rate at the record low level of zero to 0.25% that it had established in December 2008. At its June 2012 meeting, the central bank affirmed its opinion that economic conditions would likely warrant keeping the rate at “exceptionally low levels” through at least late 2014. The Fed also announced that it would extend its so-called Operation Twist program, whereby it is lengthening the average maturity of its holdings of U.S. Treasury securities, through the end of December 2012. The goals of this program are to lower longer-term interest rates, make broader financial conditions more accommodating, support a stronger economic recovery and help ensure that inflation remains at levels consistent with the Fed’s mandates of maximum employment and price stability.

In the second quarter of 2012, the U.S. economy slowed to an annualized growth rate of 1.5%, according to initial estimates for U.S. gross domestic product (GDP). While this marked the twelfth consecutive quarter of positive growth, it was also a significant slowdown from the previous few quarters. The Consumer Price Index (CPI) rose 1.7% year-over-year as of June 2012, the same figure as May 2012, which was the lowest twelve-month rate of change since February 2011. Core CPI (which excludes food and energy) increased 2.2% during the period, remaining above the Fed’s unofficial objective of 2.0% or lower for this inflation measure. However, the number was slightly below the 2.3% figure reported in the previous three months. Labor market conditions continued to be slow to improve, with the national unemployment rate registering 8.2% in June 2012. While this figure was down from 9.1% one year ago, it was still a slight uptick from the 8.1% reading in April 2012. The housing market remained the major weak spot in the economy, beleaguered by a high level of distressed properties and difficult credit conditions. For the twelve months ended May 2012 (the most recent data available at the time this report was prepared), the average home price in the Standard & Poor’s

(S&P)/Case-Shiller Index of 20 major metropolitan areas lost 0.7%. Housing prices remained at the lowest levels since spring 2003, down more than one-third from their summer 2006 peak.

Throughout the fiscal year period, fixed-income markets were buffeted by concerns about the tepid U.S. economic recovery combined with the ballooning U.S. federal deficit, the seemingly unending European debt crisis and a broader slowdown in global growth, especially emerging markets. These macro events caused the financial markets to fluctuate between embracing risk and shunning risk several times during the period. In late summer of 2011, the markets experienced a massive flight to quality, leading U.S. Treasuries to outperform all risk assets, particularly equities, high yield and investment-grade corporate bonds. However, late fall brought about a renewed appetite for risk as the European crisis appeared to be on the mend and U.S. economic indicators strengthened. Risk premiums on non-government bonds contracted and asset classes such as high-yield corporates, emerging market debt and commercial mortgage-backed securities (CMBS) substantially outperformed Treasuries. In the final months of the reporting period, however, the situation reversed once again as a broad slowdown in global growth together with renewed political discord and sovereign funding pressures in Europe cast a malaise over the markets. Not surprisingly, risk premiums on non-government bonds widened once again as U.S. Treasuries renewed their safe haven status, outperforming other riskier asset classes.

When all was said and done, longer maturity Treasuries and Treasury Inflation-Protected Securities (TIPS) ended the one-year period as the top-performing asset classes in the taxable fixed-income market. While short Treasury rates remained at historically low levels throughout the fiscal year, dipping even lower midway through the period, intermediate and longer term Treasuries saw their rates fall fairly steadily throughout the period. For example, yields on five-year Treasuries dropped from 1.80% at the beginning of July 2011 to 0.72% as of June 30, 2012, while 30-year Treasuries started at 4.40% and ended at 2.69%. The prices of these securities move in the opposite direction of interest rates. Meanwhile, investment-grade corporates also turned in relatively strong results over the one-year period, outperforming other non-government bonds such as high-yield corporates, CMBS, mortgage-backed securities (MBS) and asset-backed securities, with a 9.54% return as measured by Barclays Corporate Investment Grade Index.

How did the Funds perform during the twelve-month period ended June 30, 2012?

The tables in the Fund Performance and Expense Ratios section of this report provide total return performance information for the one-year, five-year, ten-year and/or since inception periods ending June 30, 2012. Each Fund’s Class A Share total returns are compared with the performance of the appropriate Barclays Index and Lipper classification average.

What strategies were used to manage the Funds during the twelve-month reporting period? How did these strategies influence performance?

All of the Funds continued to employ the same fundamental investment strategies and tactics used previously, although implementation of those strategies depended on the

individual characteristics of the portfolios, as well as market conditions. The Funds’ management teams used a highly collaborative, research-driven approach that we believe offers the best opportunity to achieve consistent, superior long-term performance on a risk-adjusted basis across the full range of market environments. Going into the reporting period, we were generally comfortable with each Fund’s positioning and saw little need to make large-scale shifts to weightings. However, in the case of the Nuveen Intermediate Term Bond Fund, its benchmark was changed from the Barclays Intermediate Government/Credit Bond Index to the Barclays Aggregate Bond Index effective May 14, 2012. As a result, that Fund’s management team made several more significant changes to its composition which are discussed later in this report. In addition, all of the Funds invested in various derivative instruments during this reporting period, which are discussed in more detail later in this report.

Nuveen Core Plus Bond Fund (formerly Nuveen Core Bond Fund)

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Barclays Aggregate Bond Index and the Lipper Intermediate Investment Grade Debt Funds Classification Average for the twelve-month period. The fixed income investing climate experienced dramatic shifts between “risk-off” and “risk-on” modes during the Fund’s fiscal year as macro events buffeted the markets. The Fund’s fiscal year began with a massive flight to quality late in the summer of 2011, as the markets reacted negatively to the European debt crisis, the seemingly endless U.S. debt ceiling debate and a global growth slowdown. U.S. Treasuries outperformed all other fixed income asset classes, particularly high yield and investment-grade corporate bonds during the first several months of the reporting period. The tide turned in late fall 2011 as markets embraced risk once again, emboldened by perceived stabilization in Europe and improving economic indicators. Fixed income risk premiums contracted as higher beta asset classes, such as high yield corporate bonds, emerging market (EM) debt and commercial mortgage-backed securities (CMBS), outpaced Treasuries by significant margins. The situation, however, was somewhat short lived as risk aversion resurfaced again in the final months of the reporting period due to slowdowns in U.S. and global growth combined with renewed political discord and sovereign funding pressures in Europe. Once again U.S. Treasuries were viewed as a safe haven with long-term rates falling significantly as investor demand for both duration and riskless assets seemed insatiable. Risk premiums on non-government bonds expanded, causing Treasuries to outperform spread sectors such as high yield corporate bonds and CMBS.

The Fund’s underperformance versus the benchmark and peers was mainly the result of our sector positioning. Specifically, we positioned the Fund with a broad-based underweight to Treasuries to reflect our strategic view that the long-term risk/reward profile of this sector was extremely overvalued and that investment-grade spread sectors offered more compelling value. Given the macro stresses, this view was not productive as U.S. Treasuries were the top-performing asset class over the one-year period. At the same time, the Fund had significant allocations to investment-grade credit as well as the non-government securitized sectors, including CMBS, mortgage-backed securities (MBS) and asset-backed securities (ABS). In the case of investment-grade credit, the segment overall turned in comparable results to Treasuries over the one-year period; however, our

portfolio had nearly twice as much exposure to financials versus that of the index. This overweight proved detrimental given the weaker performance of the financial sub-sector of the corporate market overall during the fiscal period. The Fund’s allocations in non-government securitized sectors also hindered performance as CMBS, MBS and ABS all posted lower returns than Treasuries during the fiscal year. Our interest rate strategy was tactical in nature and centered on trading market dislocations around a generally neutral stance. Several moves aimed at adjusting the Fund’s sensitivity to interest rate changes added marginally to investment performance, including our tactical move to lengthen duration after the rates market sold off significantly in March 2012, and our overweight to longer dated securities as rates fell late in the period.

While our investment themes remained largely intact, we did slightly moderate the active risk profile of the Fund toward the end of the reporting period out of respect for deteriorating macro fundamentals and heightened uncertainty. We reduced the Fund’s weightings to CMBS, ABS, investment-grade credit and high yield credit, while adding modestly to its Treasury and agency MBS positions as an offset. However, the Fund’s investment-grade corporate exposure still ended the fiscal year quite a bit higher than it was at the beginning. Earlier in the period, we had taken advantage of market volatility and new issue concessions to add a diversified array of corporate product at what we believed were extremely attractive levels on a long-term basis.

Nuveen High Income Bond Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Barclays High Yield 2% Issuer Capped Index and the Lipper High Current Yield Funds Classification Average for the twelve-month period. Much of the Fund’s underperformance during the fiscal year took place during the extreme “risk-off,” high volatility environment in late summer of 2011. During this dramatic flight to quality, our Fund suffered disproportionately due to its above average weighting in CCC rated securities, emerging market (EM) debt, non-rated securities and its corresponding underweight to securities in the BB sector. We made up much, but not all, of the performance shortfall in the “risk-on” months during the middle of the fiscal year as risk appetites improved and better liquidity returned to the markets. This helped the prices of some of our less liquid securities bounce back, as many of these were the same to sell off during the previous summer. We refer to much of this price fluctuation as “mark-to-market” risk because the underlying fundamentals were substantially unchanged, but the pricing of the securities became much more haphazard during bouts of illiquidity.

Overall credit fundamentals within the high yield asset class remained fairly strong; however, the default rate did inch up during the period as measured by Moody’s trailing 12-month global speculative grade corporate default rate, which rose to 2.7% by June 2012 after falling below the 2% level at the end of 2011. Credit impairment within the Fund was well contained, with two notable exceptions: domestic coal producer Patriot Coal and European oil refiner PetroPlus Holdings. While credit conditions remained generally favorable, both of these securities demonstrated how tightening lending standards can lead to bankruptcy risk. This is especially true in Europe where commercial banks are under even more pressure to protect precious capital and have become more conservative in extending credit.

In terms of sectors, the Fund’s overweight to metals/mining and energy caused some underperformance during the second half of the fiscal year. Both of these sectors are cyclical in nature; therefore, they were hurt by slowing worldwide economic indicators, especially in the United States and China, which contributed to lower commodity prices. However, this shortfall was partially offset by the Fund’s overweight in the housing and automotive industries, which were net positive contributors over the course of the fiscal year. The auto industry benefited from lower overall breakeven production levels and improving credit protection measures. Meanwhile, the housing market began to show signs of stabilization on a number of fronts.

Although the Fund’s exposure to EM bonds was a slight detractor to performance during the fiscal year’s risk-averse periods, these credits fared much better during spring 2012’s weakness than they did during the erratic market in late summer of 2011. While overall credit quality and fundamentals remained strong, the growing anxiety over China’s slowing growth rate caused weakness in certain commodity and base metals credits, most notably coal and steel. Default rates within the EM universe continued to run at a rate of less than 1% during the period, and therefore have perhaps nowhere to go but to possibly tick higher.

The Fund continued to maintain an allocation to out of index holdings, which included preferred/convertible securities focused in the U.S. financial and real estate investment trust (REIT) segments. U.S. financials began to perform much better during the period’s most recent rally, benefiting from their safe haven status compared to Europe. Indeed, the broader high yield financial sector has been the top performing area of the market year-to-date in 2012. The Fund also had small allocations in other specialized, income generating assets such as closed-end funds, exchange traded funds (ETFs) and high yielding equities. In addition to adding diversification to the Fund’s portfolio, we believe these out-of-index holdings will demonstrate less interest rate sensitivity than most high yield bonds and particularly other higher quality fixed income securities in the event that interest rates begin to rise.

In light of heightened volatility and slowing worldwide economic indicators, we made slight adjustments to the Fund’s composition over the course of the performance period. We added modestly to the Fund’s weighting in the BBB rating category in order to increase the portfolio’s liquidity. We believe this shift is prudent given some of the heightened macro risks. We ended the fiscal year positioned for moderate economic growth amid robust corporate profitability and balance sheets by maintaining a modest overweight in the CCC credit segment. We believe the extra yield that CCC-rated bonds provide over B and BB-rated credits is adequate compensation for accepting the segment’s higher risks. We also believe that CCCs will continue to perform well in light of sound credit fundamentals and the reasonable probability that the U.S. economy will avoid a recession in the next six to nine months. Perhaps even more important are the underlying technicals surrounding flows and issuance in high yield, which we believe will remain constructive for the market.

Other portfolio shifts included a reduction in the Fund’s exposure to the oil services sector due to profit taking and the lower commodity price environment. However, oil services

still remains an overweight in the Fund as we continue to find attractively priced issues that also carry security in the form of first liens on drilling rigs. In addition, we believe the sector should still benefit from overall strong energy prices as well as robust drilling activity. We also maintain an emphasis on home builders as we believe an uptick in housing sentiment and the policies surrounding home mortgage refinancing could help out the sector. We have lowered the Fund to a market weight position in the energy exploration and production sector due to continued low natural gas prices and the prospect for significant negative free cash flow and funding requirements for shale companies. At the same time, the Fund maintains an underweight in defensive sectors such as health care and utilities. Health care credits remain exposed to the risk of potential cuts in Medicare and Medicaid reimbursements while the utility sector is exposed to commodity risk in the form of low natural gas prices.

Nuveen Inflation Protected Securities Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed the Lipper Treasury Inflation Protected Securities Funds Classification Average and performed in line with the Barclays U.S. TIPS Index for the twelve-month period. The annual reporting period was marked by dramatic shifts back and forth between “risk-off” and “risk-on” modes as investors reacted to a rapidly changing economic and investment backdrop. In the first several months of the fiscal year, fixed income markets experienced a massive flight to quality in reaction to the European debt crisis, slowing global growth and the U.S. debt ceiling debate. In this environment, nominal U.S. Treasuries outperformed all other fixed income asset classes, particularly high yield and investment-grade corporate bonds. Treasury inflation protected securities (TIPS) outperformed non-government securities, while falling short of nominal Treasuries due to lower inflation expectations and weaker growth. During this period, the Fund’s significant underweight to TIPS versus the index was helpful as breakeven spreads (the difference between the yields of nominal Treasuries and TIPS) tightened and TIPS underperformed nominal Treasuries. Our relative positioning along the TIPS yield curve also aided performance, especially the Fund’s underweight versus the index to securities at the short end of the maturity spectrum. The shortest maturity TIPS were the worst performing segment along the TIPS yield curve during the risk-averse period. However, the Fund’s small allocations to non-Treasury spread sectors, particularly high yield corporate bonds and commercial mortgage-backed securities (CMBS), partially offset these positives as these sectors underperformed both nominal Treasuries and TIPS.

In the middle six months of the reporting period, markets embraced risk once again, caused by perceived stabilization in Europe and improving economic indicators. Fixed income risk premiums contracted as higher beta asset classes, such as high yield corporate bonds, emerging market (EM) debt and CMBS, outpaced Treasuries by significant margins. Despite very low yields on TIPS, this segment experienced renewed investor interest, driven by relatively attractive breakeven spreads and anticipation over an improvement in seasonal Consumer Price Index (CPI) prints. Market speculation also increased regarding the prospects of another round of easing by the Federal Reserve, which could potentially increase inflation expectations. In almost a mirror image of the previous period, the Fund’s performance was enhanced by our allocation to non-U.S.

Treasury spread sectors, which produced significant excess returns. Beneficial positions included high yield corporate securities and CMBS, the two top-performing domestic fixed income sectors. However, the Fund was negatively impacted by its relative allocations along the TIPS yield curve. Specifically, the Fund’s underweight at the front end of the TIPS curve became detrimental as the shortest maturities were the best performers along the curve.

As the final months of the reporting period drew to a close, a broad slowdown in global growth coupled with renewed political discord and sovereign funding pressures in Europe caused risk aversion to resurface. U.S. Treasury securities remained a safe haven and were well bid, with long-term rates falling significantly as investor demand for both duration and riskless assets seemed insatiable. Risk premiums on non-government bonds once again expanded, causing Treasuries to outperform spread sectors such as high yield corporate bonds and CMBS. The flight to quality benefited nominal Treasuries more than TIPS, which were negatively impacted by the downgrades in economic growth and inflation outlooks. Investor interest in TIPS waned as persistently lower energy prices led to a softening of actual and forecasted CPI prints; however, TIPS still outpaced spread sectors during the final months. As was the case in the earlier “risk-off” environment, the Fund benefited from its significant underweight to TIPS, especially the shortest maturities, while our small allocations to spread sectors were detrimental. Performance was also enhanced by our longer duration than the benchmark during this period, which alters the Fund’s sensitivity to changing interest rates, as rates dropped substantially.

While our primary investment themes remained intact during the period, we made smaller scaled shifts on an ongoing basis to help improve the Fund’s profile in response to changing growth and inflation forecasts. Later in the reporting period, we increased the Fund’s underweight to TIPS as we began to see global growth conditions deteriorate. We also reduced the Fund’s exposure to non-Treasury spread sectors, as we tried to be cautious with the Fund’s risk allocation given the negative overall environment. This included lowering the Fund’s high yield exposure. In addition, we added duration, thereby increasing the Fund’s sensitivity to interest rates in order to benefit from the strong safe haven bid to Treasuries.

Nuveen Intermediate Government Bond Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed both the Barclays Intermediate Government Bond Index and the Lipper Intermediate U.S. Government Funds Classification Average for the twelve-month period. As we entered the reporting period, we had positioned the Fund for a gradual economic recovery with a corresponding view that the fundamental and technical environment for non-U.S. Treasury securities would continue to support their valuations. In addition, we believed that European policymakers were making positive steps toward resolving the region’s sovereign debt crisis. However, fixed income markets experienced a massive flight to quality in August and September of 2011 sparked by the convergence of a number of negative factors, including a deterioration of progress in Europe, fears of a global growth slowdown and months of U.S. debt ceiling debate. Rates dropped and U.S. Treasuries rallied, outperforming all other non-government risk assets. The negative environment reversed midway through the period as progress was made on the European front and

various economic indicators experienced modest improvement. Non-government “spread” sectors outperformed Treasuries by substantial margins from December 2011 through the first quarter of 2012. However, risk aversion reappeared in the second quarter due to slowdowns in U.S. and global growth combined with renewed political discord and sovereign funding pressures in Europe. Once again U.S. Treasuries were viewed as a safe haven, which led to another round of underperformance for non-government securities.

With the uncertain nature of the markets as a backdrop, the Fund’s sector weightings were responsible for the majority of its underperformance versus the benchmark and classification average. The Fund’s underweight to U.S. Treasuries was the main negative contributor as all of the spread sectors underperformed for the year ended June 2012 as a whole. Our Fund’s sector overweight within the commercial mortgage-backed securities (CMBS) and mortgage-backed securities (MBS) sectors registered lower returns than intermediate maturity Treasuries during the fiscal year.

While our primary investment themes remained intact during the period, we made smaller scaled shifts on an ongoing basis that were geared toward improving the Fund’s profile in response to changing fundamental conditions and changes in relative valuations. During the first three months of the period, we increased the Fund’s CMBS and asset-backed security (ABS) exposure during the weakness in those sectors. As performance improved in early 2012, we reduced the Fund’s exposure to CMBS and ended the period with a lower weight in that sector. We also increased the Fund’s MBS weighting on weakness in April and May of 2012. These tactical moves helped offset some of the negative performance associated with the Fund’s overweight to spread product.

We also made several tactical yield curve positioning and duration moves during the period which included the use of interest rate futures, for overall risk management and to adjust the Fund’s sensitivity to interest rates. However, for most of the fiscal year, the Fund’s duration remained modestly short of the Barclays Index. While our tactical trades proved to be slight detractors to the Fund’s performance during the Treasury rally in the first half of the fiscal year, our overweight to longer, intermediate maturity securities helped offset some of this shortfall in the second half of the period.

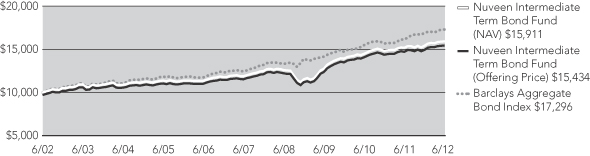

Nuveen Intermediate Term Bond Fund

The Fund’s Class A Shares at net asset value (NAV) underperformed the Barclays Aggregate Bond Index and the Lipper Intermediate Investment Grade Debt Funds Classification Average for the twelve-month period. The fixed income investing climate experienced dramatic shifts between “risk-off” and “risk-on” modes during the Fund’s fiscal year as macro events buffeted the markets. The Fund’s fiscal year began with a massive flight to quality late in the summer of 2011, as the markets reacted negatively to the European debt crisis, the seemingly endless U.S. debt ceiling debate and a global growth slowdown. U.S. Treasuries outperformed all other fixed income asset classes, particularly high yield and investment-grade corporate bonds during the first several months of the reporting period. The tide turned in late fall 2011 as markets embraced risk once again, coupled with the perceived stabilization in Europe and improving economic indicators. Fixed income risk premiums contracted as higher beta asset classes, such as high yield corporate bonds, emerging market (EM) debt and commercial mortgage-backed securities (CMBS) outpaced Treasuries by significant margins. The situation,

however, was somewhat short lived as risk aversion resurfaced again in the final months of the reporting period due to slowdowns in U.S. and global growth combined with renewed political discord and sovereign funding pressures in Europe. Once again U.S. Treasuries were viewed as a safe haven and were well bid, with long-term rates falling significantly as investor demand for both duration and riskless assets seemed insatiable. Risk premiums on non-government bonds expanded, causing Treasuries to outperform spread sectors such as high yield corporate bonds and CMBS.

With the uncertain nature of the markets as a backdrop, the Fund’s underperformance versus the benchmark and peers was mainly the result of our sector positioning. Specifically, we positioned the Fund with a broad-based underweight to Treasuries to reflect our strategic view that the long-term risk/reward profile of this sector was extremely overvalued and that investment-grade spread sectors offered more compelling value. Given the macro stresses, this view was not productive as U.S. Treasuries were the top performing asset class over the one-year period. At the same time, the Fund had significant allocations to investment-grade credit as well as the non-government securitized sectors, including CMBS, mortgage-backed securities (MBS) and asset-backed securities (ABS). In the case of investment-grade credit, the segment overall turned in comparable results to Treasuries over the one-year period; however, our portfolio had nearly twice as much exposure to financials versus that of the index. This overweight proved detrimental given the weaker performance of the financial sub-sector of the corporate market overall during the fiscal period. The Fund’s allocations in non-government securitized sectors also hindered performance as CMBS, MBS and ABS all posted negative excess returns versus Treasuries during the fiscal year. Our duration policy, which indicates the Fund’s sensitivity to interest rate changes, was tactical in nature and centered on trading market dislocations around a generally neutral stance. The Fund’s results did modestly benefit from our tactical move to lengthen duration after the rates market sold off significantly in March 2012.

While our investment themes remained largely intact, we changed the composition of the Fund in mid-May in response to changes to its management philosophy and benchmark. The Fund is now managed to the Barclays Aggregate Bond Index, as opposed to the Barclays Intermediate Government/Credit Bond Index, and portfolio positioning has been modified to reflect this change. The rationale for the change was to recognize that the Fund provides shareholders with investment exposure similar to the broad fixed income market, as represented by the Fund’s new benchmark. The new benchmark, by encompassing the broad fixed income market, is less concentrated than the old benchmark, and provides a more accurate representation of the portfolio by including securitized products, an asset class that represents 35% of the strategy’s investments. The most significant effects of this change were a reduction in the Fund’s exposure to investment-grade credit, an increase in allocation to the U.S. MBS sector and a modest lengthening in the portfolio’s duration. As such, the change to the benchmark represents a moderate increase in the Fund’s risk profile. In addition, recognizing that the sovereign and bank funding crises in Europe may deteriorate further, we increased the Fund’s U.S. Treasury and agency holdings, while remaining underweight versus the benchmark.

Nuveen Short Term Bond Fund

The Fund’s Class A Shares at net asset value (NAV) outperformed the Barclays 1-3 Year Government/Credit Bond Index and fell short of the Lipper Short Investment Grade Debt Funds Classification Average for the twelve-month period. At the beginning of the reporting period, we viewed the long-term risk/reward for both high-grade and high yield corporate bonds as quite compelling. Along with our view that the global economy would expand and U.S. Treasury rates would remain extremely low, we believed domestic bottom-up credit fundamentals were very supportive and valuations on corporate bonds were at attractive levels. Therefore, we began the Fund’s fiscal year positioned with an overweight in both investment-grade and non-investment-grade corporate bonds. We also held a marginal weighting in higher quality securities from three securitized sectors not represented in the benchmark: commercial mortgage-backed securities (CMBS), mortgage backed securities (MBS) and asset-backed securities (ABS). At the same time, the Fund was substantially underweighted in U.S. Treasury and agency securities.

Although fixed income markets moved between “risk-off” and “risk-on” modes several times during the period, the Fund was able to outperform the Barclays benchmark due its well-diversified exposure across the corporate, MBS, ABS, and CMBS segments. In particular, our weights and security selection within the ABS and CMBS sectors were significant positive contributors for the Fund. We also positioned the Fund’s duration and yield curve exposure for a flattening curve, which benefited performance over the fiscal year. However, the Fund generally had a much shorter duration than most of its peers, which hurt it modestly as rates dropped sharply in the intermediate portion of the curve during the reporting period.

While we kept our main strategic emphasis on non-government sectors in place, we did make smaller scaled shifts to the Fund’s weightings that were geared toward improving its profile in response to changing fundamental conditions and significant changes in relative valuations. Over the course of the reporting period, we added slightly to the Fund’s investment-grade corporate exposure as our fundamental view on strong bottom-up credit metrics remained largely intact. We made offsetting reductions to the Fund’s weightings in the securitized sectors, including ABS, MBS and CMBS, which held their value much better than corporate securities during the reporting period. We continued to take a cautious approach toward managing risk in the Fund’s portfolio in response to deteriorating macro fundamentals and heightened uncertainty. For example, we slightly lowered the Fund’s already very small exposure to emerging market debt and non-dollar denominated bonds, while modestly increasing its cash weighting by period end.

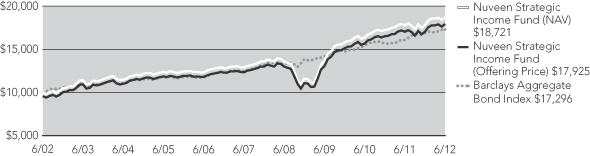

Nuveen Strategic Income Fund (formerly Nuveen Total Return Bond Fund)

The Fund’s Class A Shares at net asset value (NAV) fell short of the Barclays Aggregate Bond Index, but outperformed the Lipper Multi-Sector Income Funds Classification Average, for the twelve-month period. Toward the beginning of the fiscal year (late summer 2011), financial markets experienced a massive flight to quality induced by the European sovereign debt crisis, the seemingly endless U.S. debt ceiling debate and a global growth slowdown. For the first several months of the reporting period, U.S. Treasuries significantly outpaced all other fixed income asset classes, especially high yield and investment-grade bonds. The financial sector performed particularly poorly, weighed

down by the stresses in Europe. However late in the fall of 2011, financial markets embraced risk once again as progress was made on the European front and economic results began to gain positive traction. Fixed income risk premiums contracted and risk assets such as high yield corporate bonds, emerging market (EM) debt and commercial mortgage-backed securities (CMBS) outperformed Treasuries by substantial margins. In the final months of the reporting period, risk aversion took hold of the markets yet again as the European situation reignited while economic indicators pointed to slowing growth both in the United States and overseas. Investors’ unquenchable thirst for income solutions and less risky assets caused them to flock to U.S. Treasuries, driving down long-term rates. In this environment, Treasuries again outperformed spread sectors as risk premiums on non-government bonds expanded.

Throughout the fiscal year, we positioned the Fund with an overweight to investment-grade credit sectors, along with positions in CMBS and EM debt. At the same time, we maintained an underweight to Treasuries and mortgage-backed securities (MBS) in the Fund’s portfolio. Given the macro stresses in the market, particularly early in the fiscal year, and underperformance by non-government sectors over the period as a whole, this positioning was not productive and drove the Fund’s shortfall versus the index. Although high yield bonds were similarly pressured, exposure to this sector had a minimal net impact on Fund performance due to our adjustments in weightings and the additional income these bonds generated during the period. On a credit selection basis, our emphasis on holdings in financials detracted significantly early in the period and economically sensitive industries underperformed later in the period. Meanwhile, the Fund’s foreign currency exposure, which was focused in several of the strongest performing countries such as Australia and Canada, had a roughly neutral impact on performance due to active changes in exposure, despite the U.S. dollar’s rise during the period. While our large underweight in U.S. government securities contributed to underperformance versus the benchmark index, the Fund did fare well compared to its peer group during the reporting period.

Our interest rate strategy was tactical in nature and centered on trading market dislocations around a generally neutral stance. Several moves aimed at adjusting the Fund’s sensitivity to interest rate changes added marginally to investment performance, including our beneficial duration underweight as interest rates rose earlier in 2012, and then our subsequent overweight to longer dated securities as rates fell late in the period. Our yield curve exposure was biased toward a flattening, which was beneficial to Fund performance during the year.

Although we kept our main strategic emphasis on non-government sectors in place, we did make smaller scaled shifts to the Fund’s weightings that were geared toward improving its profile in response to changing fundamental conditions and significant changes in relative valuations. Early in 2012, we increased the Fund’s weighting to investment-grade corporate bonds, particularly given attractive new issues coming to market. After reducing currency exposures in the spring of 2012, we opportunistically added to currency exposure as well as high yield credit toward the end of the reporting period, as valuations discounted significant negative potential outcomes and fundamental credit metrics remained intact. We funded increased weightings in investment-grade and

high yield credit largely by reducing holdings in the MBS sector, as well as smaller decreases in asset-backed securities (ABS) and CMBS. Within credit, we also continued to take advantage of the new issue calendar and secondary market conditions to reposition Fund holdings within the sector.

Investments in Derivatives

During the reporting period, each of the Funds held investments in derivatives. All of the Funds invested in interest rate futures contracts. The Funds used long and short U.S. Treasury note and bond futures to manage portfolio duration and yield curve exposure. For example, to increase the duration of the Fund’s portfolio, a long Treasury bond or Treasury note futures position would be acquired. To manage foreign currency exposure, the Inflation Protected Securities Fund and Strategic Income Fund also invested in foreign currency futures contracts. For example, to reduce unwanted currency exposure from the Fund’s portfolio, a short foreign currency future would be acquired. The funds no longer held these contracts at the end of the fiscal period.

The Core Plus Bond Fund, Inflation Protected Securities Fund, Intermediate Term Bond Fund, Short Term Bond Fund and Strategic Income Fund invested in credit default swap contracts to add diversified exposure to a broad segment of the credit markets, or to express a view on credit as part of an overall portfolio sector management strategy. For example, to increase the Fund’s credit exposure to the Investment Grade or High Yield Bond segment of the market, a long CDX Investment Grade Index swap and CDX High Yield Index swap, respectively, would be acquired. The Strategic Income Fund still held these contracts at the end of the fiscal year. These Funds also continued to be hedged against changes in interest rate spreads by taking a short interest rate swap position.

The Inflation Protected Securities Fund, Short Term Bond Fund and Strategic Income Fund utilized forward foreign currency exchange contracts to manage foreign currency exposure. For example, to reduce unwanted currency exposure from the Fund’s portfolio, a short foreign currency forward would be acquired.

The Strategic Income Fund purchased options on Treasury notes/bond futures as part of an overall portfolio interest rate strategy. For example, call options may be purchased to hedge the portfolio against adverse interest rate movements while limiting downside exposure to a portfolio. The Strategic Income Fund also wrote call and put options to manage its views on portfolio volatility, writing out-of-the-money calls and puts when implied volatility is high. The Fund no longer held these contracts as of the close of the fiscal period.

Risk Considerations

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Funds, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, and income risk. The value of, and income generated by debt securities will decrease or increase based on changes in market interest rates. As interest rates rise, bond prices fall. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Below investment grade or high yield debt securities such as those held by the Core Plus Bond Fund, the High Income Bond Fund, the Inflation Protected Securities Fund, the Short Term Bond Fund and the Strategic Income Fund are subject to liquidity risk and heightened credit risk.

Foreign investments such as those held by the Core Plus Bond Fund, the High Income Bond Fund, the Inflation Protected Securities Fund, the Intermediate Term Bond Fund, the Short Term Bond Fund, and the Strategic Income Fund involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets.

For the Inflation Protected Securities Fund, the guarantee provided by the U.S. government to Treasury inflation protected securities (TIPS) relates only to the prompt payment of principal and interest and does not remove the market risks of investing in the Fund shares. The Fund’s investment in inflation protected securities has tax consequences that may result in income distributions to shareholders.

Fund Performance and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown on the following fourteen pages.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

Fund Performance and Expense Ratios (continued)

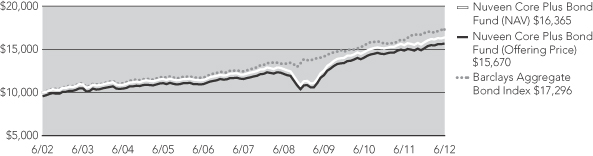

Nuveen Core Plus Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 5.52% | | | | 6.28% | | | | 5.05% | |

Class A Shares at maximum Offering Price | | | 1.01% | | | | 5.36% | | | | 4.60% | |

Barclays Aggregate Bond Index* | | | 7.47% | | | | 6.79% | | | | 5.63% | |

Lipper Intermediate Investment Grade Debt Funds Classification Average* | | | 6.97% | | | | 6.19% | | | | 5.19% | |

| | | |

Class B Shares w/o CDSC | | | 4.74% | | | | 5.52% | | | | 4.27% | |

Class B Shares w/CDSC | | | -0.26% | | | | 5.36% | | | | 4.27% | |

Class C Shares | | | 4.68% | | | | 5.50% | | | | 4.26% | |

Class R3 Shares | | | 5.27% | | | | 6.08% | | | | 4.87% | |

Class I Shares | | | 5.79% | | | | 6.57% | | | | 5.32% | �� |

Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 0.78% | |

Class B Shares | | | 1.53% | |

Class C Shares | | | 1.53% | |

Class R3 Shares | | | 1.03% | |

Class I Shares | | | 0.53% | |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

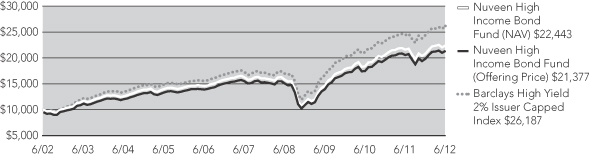

Nuveen High Income Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 3.76% | | | | 6.65% | | | | 8.42% | |

Class A Shares at maximum Offering Price | | | -1.16% | | | | 5.61% | | | | 7.90% | |

Barclays High Yield 2% Issuer Capped Index* | | | 7.21% | | | | 8.62% | | | | 10.10% | |

Lipper High Current Yield Funds Classification Average* | | | 5.15% | | | | 5.88% | | | | 8.14% | |

| | | |

Class B Shares w/o CDSC | | | 3.18% | | | | 5.86% | | | | 7.63% | |

Class B Shares w/CDSC | | | -1.60% | | | | 5.72% | | | | 7.63% | |

Class C Shares | | | 3.18% | | | | 5.90% | | | | 7.65% | |

Class R3 Shares | | | 3.46% | | | | 6.37% | | | | 8.19% | |

Class I Shares | | | 4.15% | | | | 6.92% | | | | 8.70% | |

Class A Shares have a maximum 4.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 1.01% | |

Class B Shares | | | 1.76% | |

Class C Shares | | | 1.76% | |

Class R3 Shares | | | 1.26% | |

Class I Shares | | | 0.76% | |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

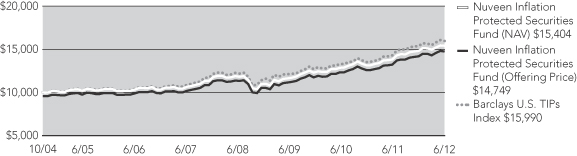

Nuveen Inflation Protected Securities Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | Since

Inception* | |

Class A Shares at NAV | | | 11.44% | | | | 8.09% | | | | 5.90% | |

Class A Shares at maximum Offering Price | | | 6.67% | | | | 7.15% | | | | 5.31% | |

Barclays U.S. TIPs Index** | | | 11.66% | | | | 8.44% | | | | 6.46% | |

Lipper Treasury Inflation Protected Securities Funds Classification Average** | | | 9.21% | | | | 7.15% | | | | 5.82% | |

| | | |

Class C Shares | | | 10.62% | | | | 7.27% | | | | 5.09% | |

Class R3 Shares | | | 11.10% | | | | 7.65% | | | | 5.55% | |

Class I Shares | | | 11.62% | | | | 8.33% | | | | 6.14% | |

Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 0.88% | | | | 0.86% | |

Class C Shares | | | 1.63% | | | | 1.61% | |

Class R3 Shares | | | 1.13% | | | | 1.11% | |

Class I Shares | | | 0.63% | | | | 0.61% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2013, so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired Fund fees and expenses, do not exceed 0.85%, 1.60%, 1.10% and 0.60% for Class A, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Since inception returns are from 10/01/04. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

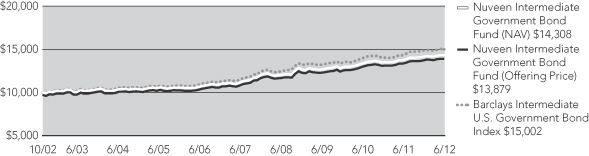

Nuveen Intermediate Government Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | Since

Inception* | |

Class A Shares at NAV | | | 4.24% | | | | 5.39% | | | | 3.87% | |

Class A Shares at maximum Offering Price | | | 1.15% | | | | 4.74% | | | | 3.54% | |

Barclays Intermediate Government Bond Index** | | | 5.01% | | | | 5.77% | | | | 4.38% | |

Lipper Intermediate U.S. Government Funds Classification Average** | | | 6.61% | | | | 5.90% | | | | 4.24% | |

| | | |

Class I Shares | | | 4.50% | | | | 5.57% | | | | 4.03% | |

| | | | | | | | |

| |

| | | Average Annual | |

| | |

| | | 1-Year | | | Since

Inception* | |

Class C Shares | | | 3.35% | | | | 3.25% | |

Class R3 Shares | | | 3.79% | | | | 3.70% | |

Class A Shares have a maximum 3.00% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 0.89% | | | | 0.85% | |

Class C Shares | | | 1.64% | | | | 1.60% | |

Class R3 Shares | | | 1.14% | | | | 1.10% | |

Class I Shares | | | 0.64% | | | | 0.60% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2013, so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired Fund fees and expenses, do not exceed 0.85%, 1.60%, 1.10% and 0.60% for Class A, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Since inception returns for Class A and Class I Shares, and for the comparative index and Lipper average are from 10/25/02. Since inception returns for Class C and Class R3 Shares are from 10/28/09. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen Intermediate Term Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 4.93% | | | | 6.02% | | | | 4.75% | |

Class A Shares at maximum Offering Price | | | 1.82% | | | | 5.38% | | | | 4.44% | |

Barclays Aggregate Bond Index* | | | 7.47% | | | | 6.79% | | | | 5.63% | |

Lipper Intermediate Investment Grade Debt Funds Classification Average* | | | 6.97% | | | | 6.19% | | | | 5.19% | |

| | | |

Class I Shares | | | 5.18% | | | | 6.17% | | | | 4.91% | |

| | | | | | | | |

| |

| | | Average Annual | |

| | |

| | | 1-Year | | | Since

Inception** | |

Class C Shares | | | 3.97% | | | | 3.97% | |

Class A Shares have a maximum 3.00% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 0.78% | |

Class C Shares | | | 1.53% | |

Class I Shares | | | 0.53% | |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| ** | Since inception return for Class C Shares is from 1/18/11. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen Short Term Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 1.42% | | | | 3.52% | | | | 3.09% | |

Class A Shares at maximum Offering Price | | | -0.85% | | | | 3.05% | | | | 2.86% | |

Barclays 1-3 Year Government/Credit Bond Index* | | | 1.12% | | | | 3.67% | | | | 3.43% | |

Lipper Short Investment Grade Debt Funds Classification Average* | | | 1.72% | | | | 3.04% | | | | 3.13% | |

| | | |

Class I Shares | | | 1.51% | | | | 3.67% | | | | 3.25% | |

| | | | | | | | |

| |

| | | Average Annual | |

| | |

| | | 1-Year | | | Since

Inception** | |

Class C Shares | | | 0.50% | | | | 1.73% | |

| | | | |

| |

| | | Cumulative | |

| |

| | | Since

Inception** | |

Class R3 Shares | | | 2.92% | |

Class A Shares have a maximum 2.25% sales charge (Offering Price). Class A Share purchases of $250,000 or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | |

| |

| | | Expense

Ratios | |

Class A Shares | | | 0.73% | |

Class C Shares | | | 1.48% | |

Class R3 Shares | | | 0.98% | |

Class I Shares | | | 0.48% | |

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

| ** | Since inception return for Class C Shares is from 10/28/09. Since inception return for Class R3 Shares is from 9/23/11. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

Nuveen Strategic Income Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of June 30, 2012

| | | | | | | | | | | | |

| |

| | | Average Annual | |

| | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 5.14% | | | | 7.74% | | | | 6.47% | |

Class A Shares at maximum Offering Price | | | 0.64% | | | | 6.80% | | | | 6.01% | |

Barclays Aggregate Bond Index* | | | 7.47% | | | | 6.79% | | | | 5.63% | |

Lipper Multi-Sector Income Classification Average* | | | 4.96% | | | | 6.22% | | | | 7.31% | |

| | | |

Class B Shares w/o CDSC | | | 4.32% | | | | 6.89% | | | | 5.66% | |

Class B Shares w/CDSC | | | -0.68% | | | | 6.73% | | | | 5.66% | |

Class C Shares | | | 4.32% | | | | 6.90% | | | | 5.67% | |

Class R3 Shares | | | 4.83% | | | | 7.40% | | | | 6.24% | |

Class I Shares | | | 5.35% | | | | 7.97% | | | | 6.73% | |

Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 0.89% | | | | 0.86% | |

Class B Shares | | | 1.64% | | | | 1.61% | |

Class C Shares | | | 1.64% | | | | 1.61% | |

Class R3 Shares | | | 1.14% | | | | 1.11% | |

Class I Shares | | | 0.64% | | | | 0.61% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2013, so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired Fund fees and expenses, do not exceed 0.84%, 1.59%, 1.59%, 1.09% and 0.59% for Class A, Class B, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Growth of an Assumed $10,000 Investment as of June 30, 2012 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Yields as of June 30, 2012

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a Fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

Nuveen Core Plus Bond Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 3.45% | | | | 3.57% | |

Class B Shares | | | 2.86% | | | | 2.98% | |

Class C Shares | | | 2.90% | | | | 2.99% | |

Class R3 Shares | | | 3.38% | | | | 3.48% | |

Class I Shares | | | 3.87% | | | | 3.98% | |

Nuveen High Income Bond Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 7.81% | | | | 8.13% | |

Class B Shares | | | 7.47% | | | | 7.80% | |

Class C Shares | | | 7.45% | | | | 7.80% | |

Class R3 Shares | | | 7.97% | | | | 8.30% | |

Class I Shares | | | 8.46% | | | | 8.80% | |

Nuveen Inflation Protected Securities Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 1.95% | | | | 0.42% | |

Class C Shares | | | 1.28% | | | | -0.32% | |

Class R3 Shares | | | 1.79% | | | | 0.17% | |

Class I Shares | | | 2.29% | | | | 0.67% | |

Nuveen Intermediate Government Bond Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 2.06% | | | | 1.30% | |

Class C Shares | | | 1.33% | | | | 0.61% | |

Class R3 Shares | | | 1.86% | | | | 1.09% | |

Class I Shares | | | 2.33% | | | | 1.59% | |

Nuveen Intermediate Term Bond Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 2.62% | | | | 1.87% | |

Class C Shares | | | 1.92% | | | | 1.19% | |

Class I Shares | | | 2.88% | | | | 2.18% | |

| (1) | The SEC Yield for Class A Shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

Nuveen Short Term Bond Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 2.36% | | | | 2.08% | |

Class C Shares | | | 1.62% | | | | 1.39% | |

Class R3 Shares | | | 2.11% | | | | 1.88% | |

Class I Shares | | | 2.65% | | | | 2.38% | |

Nuveen Strategic Income Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares(1) | | | 3.87% | | | | 4.29% | |

Class B Shares | | | 3.28% | | | | 3.79% | |

Class C Shares | | | 3.29% | | | | 3.75% | |

Class R3 Shares | | | 3.75% | | | | 4.32% | |

Class I Shares | | | 4.27% | | | | 4.89% | |

| (1) | The SEC Yield for Class A Shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |