UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive,

Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

Copies to: |

Caroline Kraus | | Geoffrey R.T. Kenyon, Esq. |

Goldman, Sachs & Co. | | Dechert LLP |

200 West Street | | 200 Clarendon Street |

New York, New York 10282 | | 27th Floor |

| | Boston, MA 02116-5021 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: October 31

Date of reporting period: April 30, 2013

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Stockholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | April 30, 2013 |

| | |

| | | | Fundamental International Equity Funds |

| | | | Concentrated International Equity |

| | | | International Small Cap |

| | | | Strategic International Equity |

Goldman Sachs Fundamental International Equity Funds

| n | | CONCENTRATED INTERNATIONAL EQUITY |

| n | | INTERNATIONAL SMALL CAP |

| n | | STRATEGIC INTERNATIONAL EQUITY |

| | | | |

TABLE OF CONTENTS | | | | |

| |

Principal Investment Strategies and Risks | | | 1 | |

| |

Investment Process | | | 2 | |

| |

Market Review | | | 3 | |

| |

Portfolio Management Discussions and Performance Summaries | | | 5 | |

| |

Schedule of Investments | | | 23 | |

| |

Financial Statements | | | 30 | |

| |

Financial Highlights | | | 34 | |

| |

Notes to the Financial Statements | | | 40 | |

| |

Other Information | | | 52 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS FUNDAMENTAL EQUITY INTERNATIONAL FUNDS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectus.

The Goldman Sachs Concentrated International Equity Fund invests primarily in a diversified portfolio of equity investments in companies that are organized outside the United States or whose securities are principally traded outside the United States. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Because the Fund may invest in a relatively small number of issuers, the Fund is subject to greater risk of loss.

The Goldman Sachs International Small Cap Fund invests primarily in a diversified portfolio of equity investments in non-U.S. small-capitalization companies. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. The securities of mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements.

The Goldman Sachs Strategic International Equity Fund invests primarily in a diversified portfolio of equity investments in companies that are organized outside the United States or whose securities are principally traded outside the United States. The Fund’s equity investments are subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile and less liquid than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments.

1

GOLDMAN SACHS FUNDAMENTAL EQUITY INTERNATIONAL FUNDS

What Differentiates Goldman Sachs’ Fundamental International Equity Investment Process?

Goldman Sachs’ Fundamental International Equity investment process is based on the belief that strong, consistent results are best achieved through expert stock selection, performed by research teams working together on a global scale. Our deep, diverse and experienced team of research analysts and portfolio managers combines local insights with global, industry-specific expertise to identify its best investment ideas.

| n | | Fundamental research teams based in the United States, United Kingdom, Japan, China, Korea, Singapore, Brazil, and India and focusing on long-term business and management quality |

| n | | Analysts collaborate regularly to leverage regional and industry-specific research and insights |

| n | | Global perspective is informed by local market expertise |

| n | | A common valuation framework, focusing on long-term earnings power, ensures consistency when valuing and comparing a company to its peers globally |

| n | | Team of experienced Research Analysts is regionally aligned and has sector expertise |

| n | | Team leverages the research of the approximately 40+ regional investment professionals |

| n | | Decision-making process is informed by active participation in the global research process |

| n | | Security selections are aligned with level of investment conviction |

| n | | Risk monitoring considers whether investment and other risks to the Funds are intended and justified |

| n | | Dedicated portfolio construction team assists in ongoing monitoring and adjustment of the Funds |

International equity portfolios that strive to offer:

| | n | | Access to markets across the world | |

| | n | | Disciplined approach to stock selection | |

| | n | | Optimal risk/return profiles | |

2

MARKET REVIEW

Goldman Sachs Fundamental Equity

International Funds

Market Review

International equities rallied during the six-month period ended April 30, 2013 (the “Reporting Period”). The MSCI Europe, Australasia, Far East (EAFE) Index (net, unhedged) (the “MSCI EAFE Index”) posted a return of 16.90%.* The commitment to low interest rates and easy monetary policy from central banks in the U.S., Europe and Japan was one of the biggest drivers of equity markets during the Reporting Period and contributed to particularly strong returns amongst financials stocks.

Japanese equities surged during the Reporting Period and led returns within the MSCI EAFE Index. Japan’s Liberal Democratic Party returned to power late in 2012 after campaigning on a platform of establishing an inflation target and weakening the yen. Once elected, Japan’s new prime minister, Shinzo Abe, followed through on setting an inflation target, while the new head of the Bank of Japan, Haruhiku Kuroda, announced a decision to double Japan’s monetary base. The yen subsequently weakened to its lowest level against the U.S. dollar in four years. The sharp rally in Japanese equity markets reflected optimism that the aggressive policies from its government and central bank would end deflation and stimulate Japan’s economy. In addition, the Japanese equity market responded positively to the weaker yen, which benefits Japan’s export-oriented economy.

European equities advanced solidly, generally reflecting optimism regarding Europe’s ability to work through its debt issues, despite some volatility during the Reporting Period driven by a banking crisis in Cyprus and by Italy’s political stalemate. In April 2013, the International Monetary Fund (“IMF”) lowered slightly its forecast for the Eurozone to a 0.3% contraction in economic growth for calendar year 2013. Other lackluster economic data points for Europe during April 2013 fueled speculation that the European Central Bank (“ECB”) would cut interest rates in early May 2013. Such speculation boosted equity markets broadly and financials stocks in particular. Additionally, a previously well-regarded academic paper linking lower debt-to-GDP ratios and economic growth was repudiated, leading equity markets to reflect the possibility of less austerity in Europe’s future.

For the Reporting Period overall, the consumer discretionary and financials sectors drove international equity market performance, followed closely by health care and information technology. Energy, materials and utilities were the weakest sectors, posting positive but more muted returns. From a country perspective, Japan was the best performer, followed by Greece, Switzerland and New Zealand. Israel, Norway, Italy and the U.K. each posted positive returns during the Reporting Period, but lagged the MSCI EAFE Index most.

Looking Ahead

We believe we will continue to see below-trend global GDP growth for 2013.1 However, we also believe there are companies in all regions of the world that can potentially grow faster than the global GDP average and stocks that will return more than the broader market averages. Looking ahead, we expect our stock selection to reflect two main themes. First, we intend to seek investments in the highest portion of the value chain. We favor business models that can win in a variety of market conditions, have high barriers to entry and/or less risk. An important part of our stock selection process also considers these top companies in light of potential alternatives in other industries, sectors and regions.

| *All | | index returns are expressed in U.S. dollar terms. |

| 1Source: | | The Outlook for 2013 and 2014. Office of the Chairman, GSAM (Nov 2012) |

3

MARKET REVIEW

Secondly, we are looking to gain exposure to secular growth. Many qualities of a good business offer secular growth opportunities — a specialized niche, a strong brand, new technology or potential for market penetration, market share gains or new end markets. These advantages often translate to premium valuations on near-term earnings. However, we are only willing to pay for this growth potential when we judge it to be sustainable and when it is coupled with high returns on capital, particularly in light of modest global GDP growth and corporate earnings outlooks. In this transitioning world, we believe companies with secular growth are likely to be better able to retain margins, which, in our view, are peaking for many other firms. We believe companies that can better protect profits are those that may be rewarded.

Not surprisingly, companies with secular growth are often benefitting from broader secular growth trends that cut across almost all industries and regions of the world. Two of the biggest themes currently expressed in our Funds’ portfolios are the expansion of the growth markets’ middle class and the growing demand for mobile data.

Going forward, we believe equities are likely to look attractive versus other asset classes, as we expect interest rates to remain low in light of modest expectations for global economic growth. In addition, we think companies may take advantage of low financing rates and put high levels of cash to work via mergers and acquisitions, further supporting valuations. Overall, we have positioned our Funds’ portfolios with what we consider to be many higher quality stocks. We believe their better growth profiles and business models can drive returns in a market without a strong macro catalyst.

As always, we maintain our focus on seeking companies that we believe will generate long-term growth in today’s ever-changing market conditions.

4

PORTFOLIO RESULTS

Goldman Sachs Concentrated International

Equity Fund

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Equity Team discusses the Goldman Sachs Concentrated International Equity Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2013 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service and IR Shares generated cumulative total returns, without sales charges, of 15.44%, 14.97%, 15.02%, 15.66%, 15.38% and 15.60%, respectively. These returns compare to the 16.90% cumulative total return of the Fund’s benchmark, the MSCI EAFE Index (net, unhedged) (the “MSCI Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund’s underperformance of the MSCI Index during the Reporting Period can be primarily attributed to individual stock selection. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | The biggest detractors from Fund performance relative to the MSCI Index during the Reporting Period were BG Group, CGG and BNP Paribas. |

| | | BG Group, a U.K. company that specializes in the exploration, production, transmission and distribution of gas, oil and liquefied natural gas, was the biggest detractor from the Fund’s results during the Reporting Period. Its shares fell significantly in October 2012 following a profit warning and an announcement that the company’s production growth rate would be flat in 2013. Our investment thesis for BG Group is that we believe it has the best organic growth potential amongst the global oil majors, mainly driven by developments in Brazil and Australia. The company attributed the slide in its production outlook to a series of delays on projects in the North Sea, Egypt, the U.S. and Brazil. While we were disappointed by the news and by the company’s stock performance, we believe that production expectations for 2013 and beyond remain intact. We think the market overreacted to the company’s news, but we continue to monitor the situation. |

| | | CGG, a French-based seismic company, detracted from the Fund’s relative performance. A new purchase for the Fund during the Reporting Period, our investment thesis for CGG is based on what we see as the cyclical upturn in demand for marine seismic services over the next few years, driven by limited new capacity. However, due to recent delays in licensing in markets such as Brazil, the rate of upturn lagged market expectations. The story has been further complicated by CGG’s acquisition of the seismic business from oilfield services firm Fugro and by the fact that Fugro’s seismic business has disappointed due to the uncertainty with customers regarding this acquisition. We expect to see improvement in CGG’s results during the second half of 2013, with stronger multi-client sales, seismic pricing/utilization, equipment sales with new products and potential integration issues completed. |

| | | French-based financial services firm BNP Paribas, one of the largest banks in Europe, disappointed, with its lagging performance primarily attributable to February and March 2013 when concerns renewed about the European banking sector following the bail-out of Cyprus and its banks. Although regulatory pressures are not going to go away, we believe BNP Paribas, a newly established position for the Fund during the Reporting Period, is a strong bank that can adapt to any environment, including a no or slow growth one, and create value for its shareholders. We see BNP Paribas as a company with a relatively stable return on equity, focused on returning capital to shareholders. |

5

PORTFOLIO RESULTS

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The greatest contributors to Fund performance relative to the MSCI Index during the Reporting Period were Ericsson, Kubota and Mitsubishi Estate. |

| | | Ericsson, the Sweden-based world’s largest maker of wireless network equipment, was the strongest contributor to the Fund’s performance during the Reporting Period. The company saw its sales and profit margin increase sharply during the fourth quarter of 2012, beating consensus estimates. Specifically, Ericsson’s earnings report showed that its sales in North America grew by 51%, as wireless operators and mobile carriers increased their spending to adapt to a growing trend in data consumption and to upgrade their networks to accommodate increased data usage. |

| | | The Fund’s holding in Japanese agricultural and construction machinery company Kubota performed well. Its business was strong during the Reporting Period, as the improving housing environment in the U.S. drove the company’s U.S. business to recover. The depreciating Japanese yen supported the company’s earnings as well. |

| | | Japanese real estate company Mitsubishi Estate was a strong contributor during the Reporting Period. Office fundamentals in Japan have been improving, and there was a market expectation that vacancy rates might have peaked in mid-2012. More specifically, the Tokyo office vacancy rate in October 2012 was 8.74%, further improved from 8.90% in September 2012 and the fourth consecutive month of declines from the 9.43% Tokyo office vacancy rate seen in June 2012. Additionally, aggressive monetary easing driven by the Japanese government and the Bank of Japan and expectations of potential reflation led to a rally in the Japanese real estate sector broadly. |

| | | We sold the Fund’s position in each of these three top contributors during the Reporting Period, as their stocks approached the target price we had set for each. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | The biggest detractors from the Fund’s relative results during the Reporting Period were consumer discretionary, energy and consumer staples, where stock selection in each of these sectors weighed most negatively on performance. |

| | | The sectors that contributed most to the Fund’s performance relative to the MSCI Index were information technology, telecommunication services and industrials, due primarily to effective stock selection in each. Having an overweighted allocation to information technology, which outpaced the MSCI Index during the Reporting Period, also helped. |

| Q | | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the MSCI Index. This effect may be even more pronounced in a concentrated portfolio or in countries that represent only a modest proportion of the MSCI Index. |

| | | That said, the countries that detracted most from the Fund’s performance during the Reporting Period were France, the U.K. and Finland, where stock selection in each hampered results. Having an overweighted allocation to the U.K., which lagged the MSCI Index during the Reporting Period, also hurt. On the positive side, effective stock selection in Sweden, stock selection in and having an underweighted allocation to Germany and having exposure to China, which is not a component of the MSCI Index but which performed quite well, boosted its returns most relative to the MSCI Index. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the Fund remained almost fully exposed to equities following cash inflows or stock sales. |

6

PORTFOLIO RESULTS

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | In addition to those purchases already mentioned, we established new Fund positions during the Reporting Period in Belgium-based diversified chemicals company Solvay and in Japanese credit card company Credit Saison. |

| | | Solvay introduced a new strategy in 2012 aimed at improving returns and boosting free cash flow. We have conviction that its chief executive officer, with his strong track record, should achieve the company’s target of €3 billion earnings before interest, taxes, depreciation and amortization (“EBITDA”) by 2016. |

| | | Credit Saison is the largest independent credit card company in Japan and the exclusive issuer of American Express. Should Japanese consumers start spending more due to rising wages and higher anticipated inflation, we believe Credit Saison should benefit from increased leverage by consumers. |

| | | In addition to those sales already mentioned, we sold out of the Fund’s positions in Imperial Tobacco Group and SKF during the Reporting Period. |

| | | We eliminated the Fund’s position in U.K.-based international tobacco company Imperial Tobacco during the Reporting Period, as volume trends in the U.K. and Europe have been deteriorating, mainly due to concerns about the regulatory environment. We felt this development put our investment rationale on the stock at risk, so we decided to sell. |

| | | We sold the Fund’s position in Sweden’s ball bearings manufacturer SKF, as the stock got close to our target price given higher market expectations for an economic recovery that would potentially increase demand for the company’s products. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or industry bets. That said, during the Reporting Period, there were no notable changes in the Fund’s sector or country weightings during the Reporting Period. |

| Q | | How was the Fund positioned relative to the MSCI Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had more exposure to France, the U.K. and Finland and less exposure to Japan, Switzerland and Spain relative to the MSCI Index. At the end of the Reporting Period, the Fund held neutral positions relative to the MSCI Index in several countries and had no position at all in several other countries, most notably Greece. |

| | | From a sector allocation perspective, the Fund had overweight positions relative to the MSCI Index in financials, industrials and information technology at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the MSCI Index in telecommunication services, consumer discretionary, consumer staples, utilities and health care and was rather neutrally weighted compared to the MSCI Index in energy and materials. |

| | | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

7

FUND BASICS

Concentrated International Equity Fund

as of April 30, 2013

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2012–April 30, 2013 | | Fund Total Return

(based on NAV)1 | | | MSCI EAFE (Net)

Index (unhedged)2 | |

| | Class A | | | 15.44 | % | | | 16.90 | % |

| | Class B | | | 14.97 | | | | 16.90 | |

| | Class C | | | 15.02 | | | | 16.90 | |

| | Institutional | | | 15.66 | | | | 16.90 | |

| | Service | | | 15.38 | | | | 16.90 | |

| | | Class IR | | | 15.60 | | | | 16.90 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The MSCI EAFE Index (net, unhedged, with dividends reinvested) is a market capitalization-weighted composite of securities in 22 developed markets. The Index approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction for withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 3/31/13 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | Inception Date |

| | Class A | | | 7.88 | % | | | -3.01% | | | | 6.56% | | | 4.35% | | 12/01/92 |

| | Class B | | | 8.29 | | | | -3.01 | | | | 6.54 | | | 2.83 | | 5/01/96 |

| | Class C | | | 12.37 | | | | -2.63 | | | | 6.40 | | | 1.41 | | 8/15/97 |

| | Institutional | | | 14.71 | | | | -1.51 | | | | 7.63 | | | 4.06 | | 2/07/96 |

| | Service | | | 14.12 | | | | -2.01 | | | | 7.08 | | | 4.66 | | 3/06/96 |

| | | Class IR | | | 14.56 | | | | N/A | | | | N/A | | | 8.80 | | 8/31/10 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders (although current Class B shareholders may continue to reinvest income and capital gains distributions into Class B Shares, and Class B shareholders may continue to exchange their shares for Class B Shares of certain other Goldman Sachs Funds). |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.goldmansachsfunds.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

8

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.44 | % | | | 1.72 | % |

| | Class B | | | 2.19 | | | | 2.47 | |

| | Class C | | | 2.19 | | | | 2.47 | |

| | Institutional | | | 1.04 | | | | 1.31 | |

| | Service | | | 1.54 | | | | 1.82 | |

| | | Class IR | | | 1.19 | | | | 1.46 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 4/30/135 |

| | | Holding | | % of Net Assets | | | Line of Business | | Country |

| | Isuzu Motors Ltd. | | | 4.0 | % | | Automobiles & Components | | Japan |

| | Scania AB Class B | | | 4.0 | | | Capital Goods | | Sweden |

| | Aurizon Holdings Ltd. | | | 4.0 | | | Transportation | | Australia |

| | BG Group PLC | | | 4.0 | | | Energy | | United Kingdom |

| | Direct Line Insurance Group | | | 3.9 | | | Insurance | | United Kingdom |

| | PLC | | | | | | | | |

| | Shire PLC | | | 3.8 | | | Pharmaceuticals,

Biotechnology & Life

Sciences | | Ireland |

| | Rio Tinto PLC | | | 3.8 | | | Materials | | United Kingdom |

| | Solvay SA | | | 3.3 | | | Materials | | Belgium |

| | Safran SA | | | 3.1 | | | Capital Goods | | France |

| | | Credit Saison Co. Ltd. | | | 3.1 | | | Diversified Financials | | Japan |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

9

FUND BASICS

|

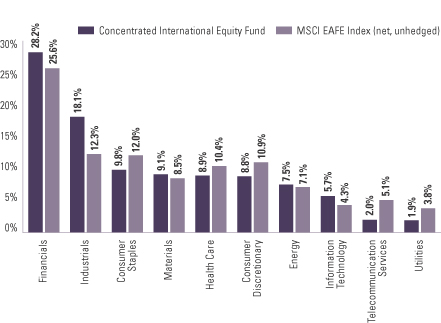

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of April 30, 2013 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

10

PORTFOLIO RESULTS

Goldman Sachs International Small Cap Fund

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Equity Team discusses the Goldman Sachs International Small Cap Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2013 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service and IR Shares generated cumulative total returns, without sales charges, of 15.81%, 15.32%, 15.31%, 16.05%, 15.71% and 15.94%, respectively. These returns compare to the 15.25% cumulative total return of the Fund’s benchmark, the S&P Developed ex-US Small Cap Index (net) (the “S&P Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund’s outperformance of the S&P Index during the Reporting Period can be primarily attributed to individual stock selection. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The greatest contributors to Fund performance relative to the S&P Index during the Reporting Period were Tokai Tokyo Financial Holdings, Eugene Technology and Takara Leben. |

| | Japanese securities firm Tokai Tokyo Financial Holdings was the greatest contributor to the Fund’s relative performance during the Reporting Period. Tokai Tokyo Financial Holdings performed well as a result of strong stock market transactions volume. For example, monthly transaction value of Japanese stocks and unit trust sales increased significantly in December 2012 and did so even more dramatically in January and February 2013. |

| | South Korean semiconductor equipment company Eugene Technology, a new purchase for the Fund during the Reporting Period, was also a strong contributor to the Fund’s relative results. Its shares were strong as a result of an improved memory capital expenditure outlook for the second half of 2013 and for 2014. Additionally, anticipation of overseas client expansion and newly launched equipment for its non-memory business benefited returns, in our view. |

| | Japanese real estate operator and developer Takara Leben’s condo business performed well, supported by the Japanese government’s tax break program for housing. The company provides condos with solar panels, which became popular for electricity savings. Also, aggressive monetary easing, driven by the government and the Bank of Japan, and expectations regarding potential reflation led to a rally in Japan’s real estate sector broadly during the Reporting Period. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | The biggest detractors from Fund performance relative to the S&P Index during the Reporting Period were CGG, Kenmare Resources and Alamos Gold. |

| | CGG, a French-based seismic company, detracted from the Fund’s relative performance most during the Reporting Period. Our investment thesis for CGG is based on what we see as the cyclical upturn in demand for marine seismic services over the next few years, driven by limited new capacity. However, due to recent delays in licensing in markets such as Brazil, the rate of upturn lagged market expectations. The story has been further complicated by CGG’s acquisition of the seismic business from oilfield services firm Fugro and by the fact that Fugro’s seismic business has disappointed due to the uncertainty with customers regarding this acquisition. We believe we should see improvement in CGG’s results during the second half of 2013, with stronger multi-client sales, seismic pricing/ utilization, equipment sales with new products and potential integration issues completed, and thus we added to the Fund’s position in the stock on weakness during the Reporting Period. |

| | A position in U.K.-listed mineral sands mining company Kenmare Resources weighed negatively on the Fund’s relative performance during the Reporting Period. The investment thesis for Kenmare Resources was based on a supply deficit in its key commodities — titanium dioxide and zircon, a 50% production expansion, just completing, and an unwinding of most of its fixed priced legacy contracts in 2012. However, the stock was impacted by sharply weaker global demand for its products, and some minor delays and cost overruns in its expansion. While demand was softer, the sharp downturn in its stock price was caused by destocking, |

11

PORTFOLIO RESULTS

| | or inventory reduction, and by the industry’s reaction of lower output, particularly of zircon. As a result, industry price declines were limited. We believe the company’s stock should benefit if demand recovers with the end of destocking, and if its expansion comes on stream during 2013. At the end of the Reporting Period, we held the position, as we believed the stock has significant upside potential. |

| | Canadian gold miner Alamos Gold is a preferred holding of our team’s within the gold sector, featuring low cost production in Mexico and another low cost project in Turkey entering the development stage. The company is also debt free with a meaningful cash position. However, in January 2013, Alamos Gold announced a takeover bid for fellow Canadian miner Aurizon Mines. Although eventually outbid by another company, the move negatively impacted its stock price performance. Even more significant was a decline in the price of gold bullion in 2013 year-to-date and negative sentiment toward the gold mining sector broadly. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | The sectors that contributed most to the Fund’s performance relative to the S&P Index were information technology, industrials and financials, due primarily to effective stock selection in each. |

| | The biggest detractors from the Fund’s results during the Reporting Period were health care, materials and consumer discretionary, where stock selection overall hurt relative performance. |

| Q | | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the S&P Index. This effect may be even more pronounced in countries that represent only a modest proportion of the S&P Index. |

| | That said, the Fund’s stock selection in Japan, Canada and Australia contributed most positively to the Fund’s performance during the Reporting Period. The countries that detracted most from the Fund’s performance during the Reporting Period were France, the Netherlands and Italy, each due primarily to weak stock selection. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the portfolio remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | In addition to those purchases already mentioned, we established Fund positions in Melrose Industries, IMI and C&C Group during the Reporting Period. |

| | Melrose Industries is U.K.-based international engineering group with worldwide interests in the design, development and manufacture of specialist components for a wide range of markets, including aerospace, information technology, telecommunications, consumer electronics, automotive, medical and consumer durables. We believe Melrose Industries has historically generated significant returns for its shareholders. |

| | U.K.-based IMI applies leading edge valve technology solutions to end markets ranging from truck engines to power stations to beverage dispensers. By moving its portfolio toward engineering-based solutions in niche applications and away from more generic “off the shelf” products, IMI has enjoyed strong returns and performance versus its engineering peer group through the economic cycle. Its management appears to be continuing to drive what we consider to be this positive portfolio mix, supported by a strong balance sheet that provides merger and acquisition optionality should the right opportunity arise. The company’s announcement during the Reporting Period of a stock buy- back program was well received by the market, but we believe the fundamental quality of its current business, coupled with its prospects ahead, were yet to be fully reflected in its share price at the time of our purchase. |

| | C&C Group has a strong franchise in the cider market, predominantly in the U.K. and Ireland. Although the consumer and competitive environment has been challenging for beverage companies in recent years, what we consider to be a strong management team at C&C Group has |

12

PORTFOLIO RESULTS

| | successfully diversified its product portfolio and defended attractive profit margins. We felt the two most positive drivers not being reflected in the company’s share price were a) the strategy of consolidating its Irish drinks market with a broad stable of its own and distributed brands and b) its significant growth opportunity in the U.S. through the acquisition of Vermont Hard Cider Company, giving C&C Group an approximately 50% share in a rapidly growing niche of the U.S. alcoholic beverages market. |

| | We eliminated the Fund’s positions in D’Ieteren, Kabel Deutschland and Andritz during the Reporting Period. |

| | We eliminated the Fund’s position in D’Ieteren, a Belgium-based auto importer/distributor and vehicle glass repair and replacement services company. The hoped-for recovery in the auto glass repair market did not materialize as expected, and difficult market dynamics in the U.K. caused us to question the robustness of the company’s business model more broadly. We sold the Fund’s position after the stock recovered relatively well early in 2013. |

| | We eliminated the Fund’s position in German cable operator Kabel Deutschland following the stock’s sharp upward move in February 2013 on market rumors that Vodafone was considering a bid for the company. |

| | A significant acquisition made by Austrian diversified machinery manufacturer Andritz raised concerns over the strategic direction of the company. Also, the order book in one of its key divisions had reached a peak in our view. We also felt the company’s valuation had reached an expensive level, and thus we sold the Fund’s position in Andritz. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or industry bets. That said, during the Reporting Period, there were no notable changes in the Fund’s sector or country weightings during the Reporting Period. |

| Q | | How was the Fund positioned relative to the S&P Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had more exposure to the U.K., China and Ireland and less exposure to Hong Kong, Sweden and Italy relative to the S&P Index. At the end of the Reporting Period, the Fund held neutral positions relative to the S&P Index in several countries, most notably Canada. |

| | From a sector allocation perspective, the Fund had overweighted positions relative to the S&P Index in information technology and consumer discretionary at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the S&P Index in financials, industrials, telecommunication services, utilities, health care, materials and consumer staples and was rather neutrally weighted relative to the S&P Index in energy. |

| | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

13

FUND BASICS

International Small Cap Fund

as of April 30, 2013

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2012–April 30, 2013 | | Fund Total Return

(based on NAV)1 | | | S&P Developed

ex-US Small Cap

Index (Net)2 | |

| | Class A | | | 15.81 | % | | | 15.25 | % |

| | Class B | | | 15.32 | | | | 15.25 | |

| | Class C | | | 15.31 | | | | 15.25 | |

| | Institutional | | | 16.05 | | | | 15.25 | |

| | Service | | | 15.71 | | | | 15.25 | |

| | | Class IR | | | 15.94 | | | | 15.25 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The S&P Developed ex-US Small Cap Index (net) is the small capitalization stock component of the S&P Developed Broad Market Index (BMI). The BMI is a float-weighted index that spans 22 countries (inclusive of the US) and includes the listed shares of all companies with an available market capitalization (float) of at least $100 million at the annual rebalance. At rebalance, companies are deleted from the index if their float falls below $75 million. The Small Cap ex-US is defined as those stocks falling in the bottom 15% of the cumulative available capital in each country. The Index reflects returns net of withholding taxes applied to foreign investors, calculated daily based on tax rates that would be applied to a Luxembourg-based investor. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 3/31/13 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | Inception Date |

| | Class A | | | 6.42 | % | | | 0.62% | | | | 10.65% | | | 5.19% | | 5/01/98 |

| | Class B | | | 6.75 | | | | 0.63 | | | | 10.64 | | | 5.28 | | 5/01/98 |

| | Class C | | | 10.83 | | | | 1.03 | | | | 10.49 | | | 4.92 | | 5/01/98 |

| | Institutional | | | 13.03 | | | | 2.22 | | | | 11.79 | | | 6.13 | | 5/01/98 |

| | Service | | | 12.54 | | | | 1.69 | | | | 11.21 | | | 5.59 | | 5/01/98 |

| | | Class IR | | | 12.91 | | | | N/A | | | | N/A | | | 13.92 | | 8/31/10 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders (although current Class B shareholders may continue to reinvest income and capital gains distributions into Class B Shares, and Class B shareholders may continue to exchange their shares for Class B Shares of certain other Goldman Sachs Funds). |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.goldmansachsfunds.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

14

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.55 | % | | | 2.18 | % |

| | Class B | | | 2.30 | | | | 2.92 | |

| | Class C | | | 2.30 | | | | 2.92 | |

| | Institutional | | | 1.15 | | | | 1.73 | |

| | Service | | | 1.65 | | | | 2.25 | |

| | | Class IR | | | 1.30 | | | | 1.84 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 4/30/135 |

| | | Holding | | % of Net Assets | | | Line of Business | | Country |

| | Telecity Group PLC | | | 1.2 | % | | Software & Services | | United Kingdom |

| | Persimmon PLC | | | 1.2 | | | Consumer Durables

& Apparel | | United Kingdom |

| | Ingenico | | | 1.1 | | | Technology Hardware

& Equipment | | France |

| | Spirax-Sarco Engineering PLC | | | 1.1 | | | Capital Goods | | United Kingdom |

| | Melrose Industries PLC | | | 1.1 | | | Capital Goods | | United Kingdom |

| | IMI PLC | | | 1.1 | | | Capital Goods | | United Kingdom |

| | C&C Group PLC | | | 1.1 | | | Food, Beverage &

Tobacco | | Ireland |

| | Pfeiffer Vacuum Technology AG | | | 1.1 | | | Capital Goods | | Germany |

| | Lindt & Spruengli AG | | | 1.1 | | | Food, Beverage &

Tobacco | | Switzerland |

| | | GfK SE | | | 1.0 | | | Media | | Germany |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

15

FUND BASICS

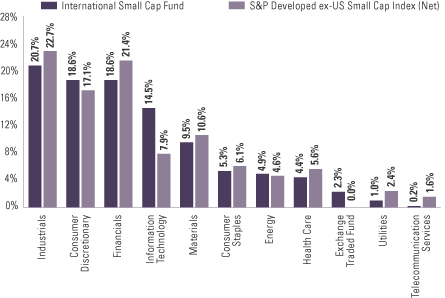

| | |

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 | | |

| As of April 30, 2013 | | |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

16

PORTFOLIO RESULTS

Goldman Sachs Strategic International Equity Fund

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Equity Team discusses the Goldman Sachs Strategic International Equity Fund’s (the “Fund”) performance and positioning for the six-month period ended April 30, 2013 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, B, C, Institutional, IR and R Shares generated cumulative total returns, without sales charges, of 14.88%, 14.45%, 14.42%, 15.08%, 14.95% and 14.67%, respectively. These returns compare to the 16.90% cumulative total return of the Fund’s benchmark, the MSCI EAFE Index (net, unhedged) (the “MSCI Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund’s underperformance of the MSCI Index during the Reporting Period can be primarily attributed to individual stock selection. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Among the biggest detractors from Fund performance relative to the MSCI Index during the Reporting Period were CGG, Rio Tinto and Lixil Group. |

| | CGG, a French-based seismic company, detracted from the Fund’s relative performance most during the Reporting Period. Our investment thesis for CGG is based on what we see as the cyclical upturn in demand for marine seismic services over the next few years, driven by limited new capacity. However, due to recent delays in licensing in markets such as Brazil, the rate of upturn lagged market expectations. The story has been further complicated by CGG’s acquisition of the seismic business from oilfield services firm Fugro and by the fact that Fugro’s seismic business has disappointed due to the uncertainty with customers regarding this acquisition. We expect to see improvement in CGG’s results during the second half of 2013, with stronger multi-client sales, seismic pricing/utilization, equipment sales with new products and potential integration issues completed, and thus we added to the Fund’s position in the stock on weakness during the Reporting Period. |

| | Rio Tinto, a U.K.-based world leader in mining mineral resources, also detracted from the Fund’s results during the Reporting Period. Iron ore prices moved from highs of $160 per tonne at the end of January 2013 to $138 per tonne in March 2013. This price decline, along with a negative sentiment on China’s economy, caused Rio Tinto’s share price to weaken. We added to the Fund’s position in the stock on weakness. |

| | Japanese building materials company Lixil Group’s share price declined, as investors had concern the company might miss its guidance. There had been a delay in launching a new product, and its cost reduction plans did not go as well as anticipated as the company increased bonuses. In turn, Lixil Group’s earnings momentum was not as strong as expected, and the stock underperformed the MSCI Index. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The greatest contributors to Fund performance relative to the MSCI Index during the Reporting Period were Ericsson, Mitsubishi Estate and Sumitomo Mitsui Financial Group. |

| | Ericsson, the Sweden-based world’s largest maker of wireless network equipment, was the strongest contributor to the Fund’s performance during the Reporting Period. The company saw its sales and profit margin increase sharply during the fourth quarter of 2012, beating consensus estimates. Specifically, Ericsson’s earnings report showed that its sales in North America grew by 51%, as wireless operators and mobile carriers increased their spending to adapt to a growing trend in data consumption and to upgrade their networks to accommodate increased data usage. At the end of the Reporting Period, we expected this data consumption trend to continue over the long term and still believed Ericsson was well positioned to benefit. |

17

PORTFOLIO RESULTS

| | Japanese real estate company Mitsubishi Estate was a strong contributor during the Reporting Period. Office fundamentals in Japan have been improving, and there was a market expectation that vacancy rates might have peaked in mid-2012. More specifically, the Tokyo office vacancy rate in October 2012 was 8.74%, further improved from 8.90% in September 2012 and the fourth consecutive month of declines from the 9.43% Tokyo office vacancy rate seen in June 2012. Additionally, aggressive monetary easing driven by the Japanese government and the Bank of Japan and expectations of potential reflation led to a rally in the Japanese real estate sector broadly. We sold the Fund’s position in the company to take profits and used the proceeds for what we considered to be better risk/reward opportunities. |

| | Japan’s Sumitomo Mitsui Financial Group performed well on good fundamentals. Its retail business, including mutual fund sales, was strong, given positive market sentiment, and credit costs were reduced. On the back of these positive fundamentals, the company announced an upward revision of its earnings, which contributed to the stock price increase as well. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | The biggest detractors from the Fund’s results during the Reporting Period were consumer discretionary, energy and consumer staples, where weak stock selection in each hurt most. |

| | | The sectors that contributed most to the Fund’s performance relative to the MSCI Index were health care, industrials and information technology. Stock selection in all three sectors proved effective during the Reporting Period. |

| Q | | Which countries most affected the Fund’s performance during the Reporting Period? |

| A | | Typically, the Fund’s individual stock holdings will significantly influence the Fund’s performance within a particular country or region relative to the MSCI Index. This effect may be even more pronounced in countries that represent only a modest proportion of the MSCI Index. |

| | That said, the countries that detracted most from the Fund’s performance during the Reporting Period were France, the U.K. and Japan. Both stock selection in and having overweighted allocations to France and the U.K., each of which lagged the MSCI Index during the Reporting Period, weighed negatively on relative performance. Having an underweighted exposure to the comparative strong Japanese equity market hampered results. |

| | Conversely, effective individual stock selection in Sweden contributed most positively to the Fund’s results relative to the MSCI Index. Both stock selection in and having an underweighted allocation to Germany, which lagged the MSCI Index during the Reporting Period, boosted the Fund’s performance. Having only a modest exposure to Italy, which significantly lagged the MSCI Index, added value as well. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the portfolio remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | During the Reporting Period, we purchased Fund positions in Sanofi, Anheuser-Busch InBev and AXA. |

| | We initiated a Fund position in Sanofi, a France-based global pharmaceutical company, because of its focus on “long duration assets,” which we characterize as less reliant on cyclical research and development investment and/or less exposed to intellectual property erosion. These long-term assets currently represent 60% of Sanofi’s sales, and we believe this proportion may well grow to 70% by 2016. Compared to its peers, the company has high exposure to emerging markets, providing diversified exposure. |

18

PORTFOLIO RESULTS

| | We established a Fund position in Belgium-based brewer Anheuser-Busch InBev on prospects for higher earnings growth after its proposal to buy control of the Mexican brewer Modelo. |

| | We initiated a Fund position in France-based global insurer AXA because we believe the company was undervalued compared to its peers and that the market was overlooking AXA’s powerful recovery story following the financial crisis. We believe management has been taking the right steps to ensure the business moves forward and generates more cash to support its dividend. |

| | In addition to the sales already mentioned, we sold out of the Fund’s positions in Westpac Banking and UBS during the Reporting Period. |

| | We sold out of the Fund’s position in Westpac, the second largest Australian bank, as it reached our target price given better earnings driven by the solid economic environment in Australia and given the search for stable high yielding stocks. |

| | Similarly, we eliminated the Fund’s position in Swiss diversified banking institution UBS, as it had performed well and approached its target price. We switched into French- based financial services firm BNP Paribas, one of the largest banks in Europe. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In this Fund, both sector weightings and country allocations are largely the result of our bottom-up stock selection process rather than any top-down macroeconomic views or industry bets. That said, during the Reporting Period, there were no notable changes in the Fund’s sector or country weightings during the Reporting Period. |

| Q | | How was the Fund positioned relative to the MSCI Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had more exposure to France, Russia and Belgium and less exposure to Australia, Japan and Germany relative to the MSCI Index. At the end of the Reporting Period, the Fund held neutral positions relative to the MSCI Index in several countries, most notably Switzerland and Sweden. |

| | From a sector allocation perspective, the Fund had overweight positions relative to the MSCI Index in health care and telecommunication services at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the MSCI Index in financials and utilities and rather neutral positions relative to the MSCI Index in consumer staples, consumer discretionary, information technology, materials, industrials and energy. |

| | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

19

FUND BASICS

Strategic International Equity Fund

as of April 30, 2013

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2012–April 30, 2013 | | Fund Total Return

(based on NAV)1 | | | MSCI EAFE (Net)

Index (unhedged)2 | |

| | Class A | | | 14.88 | % | | | 16.90 | % |

| | Class B | | | 14.45 | | | | 16.90 | |

| | Class C | | | 14.42 | | | | 16.90 | |

| | Institutional | | | 15.08 | | | | 16.90 | |

| | Class IR | | | 14.95 | | | | 16.90 | |

| | | Class R | | | 14.67 | | | | 16.90 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The MSCI EAFE Index (net, unhedged, with dividends reinvested) is a market capitalization-weighted composite of securities in 22 developed markets. The Index approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction for withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. The Index is unmanaged and the figures for the Index do not include any deduction for fees or expenses. It is not possible to invest directly in an index. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 3/31/13 | | One Year | | | Five Years | | Since Inception | | Inception Date |

| | Class A | | | 5.15 | % | | -3.09% | | -3.86% | | 6/25/07 |

| | Class B | | | 5.45 | | | -3.13 | | -3.83 | | 6/25/07 |

| | Class C | | | 9.42 | | | -2.72 | | -3.65 | | 6/25/07 |

| | Institutional | | | 11.76 | | | -1.62 | | -2.55 | | 6/25/07 |

| | Class IR | | | 11.57 | | | -1.68 | | -4.17 | | 11/30/07 |

| | | Class R | | | 11.01 | | | -2.26 | | -4.73 | | 11/30/07 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Class R and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders (although current Class B shareholders may continue to reinvest income and capital gains distributions into Class B Shares, and Class B shareholders may continue to exchange their shares for Class B Shares of certain other Goldman Sachs Funds). |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.goldmansachsfunds.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

20

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.47 | % | | | 1.97 | % |

| | Class B | | | 2.22 | | | | 2.72 | |

| | Class C | | | 2.22 | | | | 2.72 | |

| | Institutional | | | 1.07 | | | | 1.53 | |

| | Class IR | | | 1.22 | | | | 1.70 | |

| | | Class R | | | 1.72 | | | | 2.21 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. The Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2014, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 4/30/135 | | |

| | | Holding | | % of Net Assets | | | Line of Business | | Country |

| | HSBC Holdings PLC | | | 3.4 | % | | Banks | | United Kingdom |

| | Novartis AG (Registered) | | | 3.0 | | | Pharmaceuticals, Biotechnology

& Life Sciences | | Switzerland |

| | Vodafone Group PLC | | | 2.9 | | | Telecommunication Services | | United Kingdom |

| | Rio Tinto PLC | | | 2.8 | | | Materials | | United Kingdom |

| | Sanofi | | | 2.4 | | | Pharmaceuticals, Biotechnology

& Life Sciences | | France |

| | Anheuser-Busch InBev NV | | | 2.3 | | | Food, Beverage & Tobacco | | Belgium |

| | Air Liquide SA | | | 2.1 | | | Materials | | France |

| | Sumitomo Mitsui | | | 2.1 | | | Banks | | Japan |

| | Financial Group, Inc. AXA SA | | | 2.0 | | | Insurance | | France |

| | | Unilever NV CVA | | | 2.0 | | | Food, Beverage & Tobacco | | Netherlands |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

21

FUND BASICS

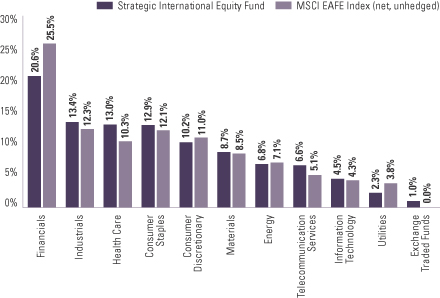

|

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of April 30, 2013 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

22

GOLDMAN SACHS CONCENTRATED INTERNATIONAL EQUITY FUND

Schedule of Investments

April 30, 2013 (Unaudited)

| | | | | | | | |

| Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – 99.6% | | | | |

| | Australia – 6.8% | | | | |

| | 1,341,495 | | | Aurizon Holdings Ltd. (Transportation) | | $ | 5,774,627 | |

| | 388,131 | | | Computershare Ltd. (Software & Services) | | | 3,998,334 | |

| | | | | | | | |

| | | | | | | 9,772,961 | |

| | |

| | Belgium – 3.2% | | | | |

| | 32,109 | | | Solvay SA (Materials) | | | 4,704,358 | |

| | |

| | Finland – 3.7% | | | | |

| | 148,893 | | | Fortum OYJ (Utilities) | | | 2,767,546 | |

| | 59,630 | | | Nokian Renkaat OYJ (Automobiles & Components) | | | 2,590,323 | |

| | | | | | | | |

| | | | | | | 5,357,869 | |

| | |

| | France – 17.6% | | | | |

| | 23,166 | | | Air Liquide SA (Materials) | | | 2,935,044 | |

| | 231,241 | | | AXA SA (Insurance) | | | 4,330,363 | |

| | 77,870 | | | BNP Paribas SA (Banks) | | | 4,341,868 | |

| | 96,738 | | | Compagnie Generale de Geophysique-Veritas (Energy)* | | | 2,092,696 | |

| | 91,931 | | | Safran SA (Capital Goods) | | | 4,518,934 | |

| | 59,104 | | | Total SA (Energy) | | | 2,975,122 | |

| | 86,853 | | | Vinci SA (Capital Goods) | | | 4,186,909 | |

| | | | | | | | |

| | | | | | | 25,380,936 | |

| | |

| | Germany – 8.0% | | | | |

| | 41,700 | | | Bayer AG (Registered) (Pharmaceuticals, Biotechnology & Life Sciences) | | | 4,359,589 | |

| | 46,086 | | | Beiersdorf AG (Household & Personal Products) | | | 4,174,574 | |

| | 24,558 | | | Pfeiffer Vacuum Technology AG (Capital Goods) | | | 2,988,452 | |

| | | | | | | | |

| | | | | | | 11,522,615 | |

| | |

| | Hong Kong – 3.0% | | | | |

| | 967,528 | | | AIA Group Ltd. (Insurance) | | | 4,304,009 | |

| | |

| | Ireland – 5.7% | | | | |

| | 441,059 | | | C&C Group PLC (Food, Beverage & Tobacco) | | | 2,739,856 | |

| | 176,972 | | | Shire PLC (Pharmaceuticals, Biotechnology & Life Sciences) | | | 5,516,567 | |

| | | | | | | | |

| | | | | | | 8,256,423 | |

| | |

| | Japan – 15.2% | | | | |

| | 152,400 | | | Credit Saison Co. Ltd. (Diversified Financials) | | | 4,457,945 | |

| | 873,000 | | | Isuzu Motors Ltd. (Automobiles & Components) | | | 5,817,963 | |

| | 105,100 | | | Nomura Real Estate Holdings, Inc. (Real Estate) | | | 2,825,491 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | | | | |

| | Japan – (continued) | | | | |

| | 94,200 | | | Sumitomo Mitsui Financial Group, Inc. (Banks) | | $ | 4,452,585 | |

| | 67,300 | | | Unicharm Corp. (Household & Personal Products) | | | 4,351,713 | |

| | | | | | | | |

| | | | | | | 21,905,697 | |

| | |

| | Russia – 2.0% | | | | |

| | 223,005 | | | Sberbank of Russia ADR (Banks) | | | 2,878,264 | |

| | |

| | South Korea – 2.9% | | | | |

| | 84,871 | | | Kia Motors Corp. (Automobiles & Components) | | | 4,233,461 | |

| | |

| | Sweden – 4.0% | | | | |

| | 271,190 | | | Scania AB Class B (Capital Goods) | | | 5,799,754 | |

| | |

| | Switzerland – 4.0% | | | | |

| | 73,361 | | | Julius Baer Group Ltd. (Diversified Financials)* | | | 2,924,491 | |

| | 38,170 | | | Novartis AG (Registered) (Pharmaceuticals, Biotechnology & Life Sciences) | | | 2,825,633 | |

| | | | | | | | |

| | | | | | | 5,750,124 | |

| | |

| | United Kingdom – 23.5% | | | | |

| | 340,386 | | | BG Group PLC (Energy) | | | 5,746,172 | |

| | 1,790,312 | | | Direct Line Insurance Group PLC (Insurance) | | | 5,631,487 | |

| | 399,953 | | | HSBC Holdings PLC (Banks) | | | 4,380,281 | |

| | 726,488 | | | Melrose Industries PLC (Capital Goods) | | | 2,753,776 | |

| | 38,891 | | | Reckitt Benckiser Group PLC (Household & Personal Products) | | | 2,839,081 | |

| | 119,866 | | | Rio Tinto PLC (Materials) | | | 5,504,258 | |

| | 296,168 | | | Telecity Group PLC (Software & Services) | | | 4,250,600 | |

| | 927,553 | | | Vodafone Group PLC (Telecommunication Services) | | | 2,830,239 | |

| | | | | | | | |

| | | | | | | 33,935,894 | |

| | |

| | TOTAL INVESTMENTS – 99.6% | | | | |

| | (Cost $135,932,478) | | $ | 143,802,365 | |

| | |

| OTHER ASSETS IN EXCESS OF

LIABILITIES – 0.4% | | | 545,804 | |

| | |

| | NET ASSETS – 100.0% | | $ | 144,348,169 | |

| | |

| | |

| The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. |

* | | Non-income producing security. |

| | | | |

|

Investment Abbreviation: |

ADR | | —American Depositary Receipt |

|

| | |

| The accompanying notes are an integral part of these financial statements. | | 23 |

GOLDMAN SACHS INTERNATIONAL SMALL CAP FUND

Schedule of Investments

April 30, 2013 (Unaudited)

| | | | | | | | |

| Shares | | | Description | | Value | |

| | | | | | | | |

| | Common Stocks – 92.4% | |

| | Australia – 6.5% | | | | |

| | 30,262 | | | Ansell Ltd. (Health Care Equipment & Services) | | $ | 496,189 | |

| | 188,116 | | | Aristocrat Leisure Ltd. (Consumer Services) | | | 768,843 | |

| | 76,536 | | | Bank of Queensland Ltd. (Banks) | | | 796,776 | |

| | 79,014 | | | Boral Ltd. (Materials) | | | 410,128 | |

| | 32,111 | | | Caltex Australia Ltd. (Energy) | | | 717,299 | |

| | 77,618 | | | Computershare Ltd. (Software & Services) | | | 799,582 | |

| | 132,730 | | | David Jones Ltd. (Retailing) | | | 410,273 | |

| | 151,542 | | | Echo Entertainment Group Ltd. (Consumer Services) | | | 568,736 | |

| | 187,182 | | | FKP Property Group (Real Estate) | | | 319,137 | |

| | 42,883 | | | iiNET Ltd. (Telecommunication Services) | | | 274,345 | |

| | 140,782 | | | Metcash Ltd. (Food & Staples Retailing) | | | 597,411 | |

| | 156,904 | | | NIB Holdings Ltd. (Insurance) | | | 382,808 | |

| | 67,632 | | | OZ Minerals Ltd. (Materials) | | | 303,138 | |

| | 223,007 | | | PanAust Ltd. (Materials) | | | 538,686 | |

| | 77,899 | | | Seek Ltd. (Commercial & Professional Services) | | | 903,783 | |

| | | | | | | | |

| | | | | | | 8,287,134 | |

| | |

| | Bermuda – 0.9% | | | | |

| | 114,654 | | | Hiscox Ltd. (Insurance) | | | 999,385 | |

| | 111,740 | | | Hiscox Ltd. Class B (Insurance)* | | | 86,786 | |

| | | | | | | | |

| | | | | | | 1,086,171 | |

| | |

| | Canada – 9.2% | | | | |

| | 42,200 | | | Aimia, Inc. (Media) | | | 666,018 | |

| | 37,800 | | | Alamos Gold, Inc. (Materials) | | | 527,913 | |

| | 9,700 | | | AltaGas Ltd. (Energy) | | | 361,445 | |

| | 87,200 | | | Bellatrix Exploration Ltd. (Energy)* | | | 546,163 | |

| | 8,900 | | | Canadian Real Estate Investment Trust (REIT) | | | 421,126 | |

| | 20,200 | | | Canadian Western Bank (Banks) | | | 570,641 | |

| | 176,200 | | | Capstone Mining Corp. (Materials)* | | | 356,790 | |

| | 74,800 | | | Copper Mountain Mining Corp. (Materials)* | | | 149,979 | |

| | 24,300 | | | Dominion Diamond Corp. (Materials)* | | | 385,201 | |

| | 19,800 | | | Dorel Industries, Inc. Class B (Consumer Durables & Apparel) | | | 854,931 | |

| | 34,800 | | | Enerflex Ltd. (Energy) | | | 480,143 | |

| | 16,100 | | | Ensign Energy Services, Inc. (Energy) | | | 271,037 | |

| | 28,500 | | | Evertz Technologies Ltd. (Technology Hardware & Equipment) | | | 442,727 | |

| | 54,700 | | | Gran Tierra Energy, Inc. (Energy)* | | | 304,055 | |

| | 30,003 | | | Legacy Oil + Gas, Inc. (Energy)* | | | 158,436 | |

| | 29,100 | | | Linamar Corp. (Automobiles & Components) | | | 688,903 | |

| | 8,289 | | | MacDonald Dettwiler & Associates Ltd. (Software & Services) | | | 598,730 | |

| | 164,900 | | | MBAC Fertilizer Corp. (Materials)* | | | 366,644 | |

| | 9,500 | | | Methanex Corp. (Materials) | | | 402,650 | |

| | |

| | | | | | | | |

| | Common Stocks – (continued) | |

| | Canada – (continued) | | | | |

| | 36,800 | | | Progressive Waste Solutions Ltd. (Commercial & Professional Services) | | $ | 820,051 | |

| | 186,500 | | | Rubicon Minerals Corp. (Materials)* | | | 323,961 | |

| | 11,400 | | | ShawCor Ltd. (Energy) | | | 457,946 | |

| | 224,245 | | | Southern Pacific Resource Corp. (Energy)* | | | 146,907 | |

| | 21,900 | | | Toromont Industries Ltd. (Capital Goods) | | | 482,585 | |

| | 36,800 | | | Westjet Airlines Ltd. Class A (Transportation) | | | 903,699 | |

| | | | | | | | |

| | | | | | | 11,688,681 | |

| | |

| | China – 1.9% | | | | |

| | 204,800 | | | China International Marine Containers Group Co. Ltd. Class H (Capital Goods)* | | | 327,906 | |

| | 66,000 | | | ENN Energy Holdings Ltd. (Utilities) | | | 382,111 | |

| | 908,000 | | | Foxconn International Holdings Ltd. (Technology Hardware & Equipment)* | | | 351,094 | |

| | 512,000 | | | Haitian International Holdings Ltd. (Capital Goods) | | | 876,189 | |