UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman, Sachs & Co. | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: August 31

Date of reporting period: February 29, 2016

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | February 29, 2016 |

| | |

| | | | Fundamental Equity Value Funds |

| | | | Focused Value |

| | | | Growth and Income |

| | | | Large Cap Value |

| | | | Mid Cap Value |

| | | | Small Cap Value |

| | | | Small/Mid Cap Value |

Goldman Sachs Fundamental Equity Value Funds

| | | | |

TABLE OF CONTENTS | | | | |

| |

Investment Process | | | 1 | |

| |

Market Review | | | 2 | |

| |

Portfolio Management Discussions and Performance Summaries | | | 6 | |

| |

Schedules of Investments | | | 42 | |

| |

Financial Statements | | | 58 | |

| |

Financial Highlights | | | 66 | |

| |

Notes to Financial Statements | | | 78 | |

| |

Other Information | | | 95 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS FUNDAMENTAL EQUITY VALUE FUNDS

What Differentiates the Goldman Sachs Fundamental Equity Value Investment Process?

Goldman Sachs’ Fundamental Equity Value Team believes that all successful investing should thoughtfully weigh two important attributes of a stock: price and prospects. Through independent fundamental research, the Team seeks to identify and invest in quality businesses that are selling at compelling valuations.

At the heart of our value investment philosophy is a belief in the rigorous analysis of business fundamentals. Our approach may include:

| n | | Meetings with management teams and on-site company visits |

| n | | Industry-specific, proprietary financial and valuation models |

| n | | Assessment of management quality |

| n | | Analysis of each company’s competitive position and industry dynamics |

| n | | Interviews with competitors, suppliers and customers |

We seek to invest in companies when we believe:

| n | | Market uncertainty exists |

| n | | Their economic value is not recognized by the market |

We seek to buy companies with quality characteristics. For us, this means companies that have:

| n | | Sustainable operating earnings, or competitive advantage |

| n | | Excellent stewardship of capital |

| n | | Capability to earn above their cost of capital |

| n | | Strong or improving balance sheets and cash flow |

Value portfolios that strive to offer:

| | n | | Capital appreciation potential as each company’s true value is recognized in the marketplace | |

| | n | | Investment style consistency | |

1

MARKET REVIEW

Goldman Sachs Fundamental Equity Value Funds

Market Review

Overall, U.S. equities struggled during the six months ended February 29, 2016 (the “Reporting Period”) amidst persistent volatility. The Standard & Poor’s 500® Index (the “S&P 500 Index”) ended the Reporting Period with a decline of +0.92%. The Russell 3000® Index generated a return of -2.20%. Central bank policy, a commodity price sell-off, geopolitical tensions, and China and global economic growth concerns were the key themes impacting U.S. equities throughout the Reporting Period.

Following a volatile summer, U.S. equities tumbled further in September 2015, alongside other global equity markets. Equity markets continued to fret about weak macroeconomic data from China and the global implications of that data. Further, the U.S. Federal Reserve (the “Fed”) elected not to raise interest rates in September 2015, thus seemingly reaffirming persistent concerns about the many sources of economic instability and slowing economic growth. Still, domestic economic news was rather positive. U.S. economic growth for the second quarter of 2015 was revised up to an annualized rate of 3.9%, led by stronger consumer and construction spending. Job growth for August 2015 was slightly below consensus expectations, but the unemployment rate continued to decline.

October 2015 saw a strong rebound for U.S. equities. U.S. equity markets maintained their focus on the timing of the Fed’s initial rate hike, and expectations of “lift off,” the term used for that initial rate hike, in December 2015 increased following comments from the Fed regarding solid consumer spending and strength in the housing market. U.S. Gross Domestic Product (“GDP”) growth for the third quarter of 2015 came in at 1.5%, which was generally in line with consensus expectations.

The S&P 500 Index finished November 2015 roughly flat, although this masked a mid-month sell-off, as market expectations of a December 2015 rate hike rose significantly and dampened investor sentiment following a strong October 2015 non-farm payrolls report and hawkish comments from Fed members at the Fed’s October 2015 meeting. However, the message that the U.S. economy was strong enough to withstand higher interest rates, along with an emphasis by the Fed that any tightening would be gradual, sparked a rally in the U.S. equity markets. Economic data was also relatively strong in November 2015, with third quarter 2015 GDP revised up to 2.1%. In December 2015, the Fed finally delivered, as largely expected by markets, and voted unanimously for a 25 basis point hike in the targeted federal funds rate, its first rate hike since 2006. (A basis point is 1/100th of a percentage point.) The fairly dovish language in the Fed’s announcement, which re-emphasized “gradual” adjustments to policy going forward, helped to somewhat assuage the markets. (Dovish language or action tends to be that which is not strong or aggressive (opposite of hawkish).)

Early in 2016, U.S. equities were embroiled in what was a global rout, triggered by investor concerns of an intensifying economic slowdown in China and exacerbated by a plunge in oil prices to less than $30 per barrel, the lowest level since 2003. The Fed’s statement in January 2016 acknowledged the risks from international markets and tightening financial conditions on the U.S. economy. Its statement was also somewhat bearish on economic growth, noting that activity had slowed in 2015. Indeed, U.S. GDP economic growth had slowed in the fourth quarter of 2015 according to preliminary estimates, expanding by just 0.7%, thus bringing the 2015 annual growth rate to 2.4%. While the Fed acknowledged further recovery in the U.S. labor market, its language on its inflation outlook was more dovish.

Market sentiment appeared to improve in February 2016 as central banks outside of the U.S. increasingly acknowledged rising economic risks and sent a more dovish signal, fueling

2

MARKET REVIEW

market expectations of further easing. For example, European Central Bank President Mario Draghi hinted at further stimulus. The People’s Bank of China signaled further monetary easing and a 50 basis point cut in its reserve requirement ratio for banks. Fed Chair Janet Yellen similarly released generally dovish remarks, stressing that the Fed was not on a “pre-set” path for hikes. U.S. equities were also supported during the month by strong U.S. economic data, rallying as fourth quarter 2015 GDP was revised up to 1.0%, coming in above consensus expectations. Also, the U.S. unemployment rate declined to an eight-year low of 4.9%, while retail sales increased 0.2% in January 2016, with the less volatile core retail sales figure increasing 0.6%. Further adding support to the U.S. equity market in the latter half of February 2016 was the oil price recovery, albeit modest, from its trough point on news of talks between oil producers to cap production.

For the Reporting Period overall, all market capitalizations posted negative returns, but large-cap companies performed least poorly, followed by mid-cap companies. Small-cap companies were weakest. Growth stocks outpaced value stocks within the large-cap segment of the U.S. equity market, but value stocks outperformed growth stocks in the mid-cap and small-cap segments of the U.S. equity market. (All as measured by Russell Investments indices.)

Looking Ahead

At the end of the Reporting Period, we expected positive, but below average, returns for global equities in 2016 overall in light of modest economic growth forecasts and rising valuations in some areas of the market. However, in our view, equities still looked more attractive than other asset classes in a persistently low-return environment.

After dipping in 2015, we expect global economic growth to increase modestly in 2016, which we think will be enough to sustain corporate profitability and allow stock prices to move higher. In our view, central banks are likely to remain accommodative given still-fragile global economic growth, which we also see as helpful for equity markets. Even in the U.S., where Fed policy has moved toward normalization, we do not expect to see much negative impact from what are likely to be gradual interest rate increases given continued strength in the housing and labor markets. However, the strong U.S. dollar may well remain a headwind for U.S. multi-nationals.

While the macro outlook remains benign, U.S. credit and equities reflect some typical late-cycle signs, such as more shareholder-friendly actions, an increase in merger and acquisition activity and a pick-up in leverage, all of which tend to coincide with an environment lacking top-line, or revenue, growth. Higher equity valuations are also consistent with late-cycle indicators. In part due to years of ultra-low interest rates, U.S. equity market valuations have risen toward fair value, in our opinion, with some areas looking particularly vulnerable if companies cannot deliver growth.

One common theme across the developed markets is that we believe domestically-focused companies in the major regions could benefit from increasing domestic consumption while being more insulated from currency volatility. In the U.S., we expect that the strong dollar could continue to be a headwind for many globally-exposed companies but believe the consumer remains healthy.

We also believe that some extraordinary dynamics in the U.S. equity market in 2015 may have set up investment opportunities for 2016. The extremely narrow trading breadth of the market hit a 30-year low. For example, just ten stocks accounted for approximately 40% of the total

3

MARKET REVIEW

positive contribution to the S&P 500 Index return in 2015. Also, value stocks notably underperformed growth stocks in 2015. We expect some broadening of the market and reversal of these trends in 2016, as investors focus on the risk of high-priced stocks as well as on the relative attractiveness of the hundreds of stocks trading below the market’s price-earnings multiple. (A stock’s price-earnings multiple is the current market price of a share divided by the company’s earnings per share).

Regardless of market direction, our fundamental, bottom-up stock selection continues to drive our process, rather than headlines or sentiment. We maintain high conviction in the companies the Funds own and believe they have the potential to outperform relative to the broader market regardless of economic growth conditions. We continue to focus on, in our view, undervalued companies that we believe have comparatively greater control of their own destiny, such as innovators with differentiated products, companies with low cost structures or companies that have been investing in their own businesses and may be poised to gain market share. We maintain our discipline in identifying companies with what we believe to be strong or improving balance sheets, led by quality management teams and trading at discounted valuations, and we maintain our long-term investment perspective.

As always, deep research resources, a forward-looking investment process and truly actively managed portfolios are keys, in our view, to both preserving capital and outperforming the market over the long term.

4

MARKET REVIEW

|

| |

| Changes to the Funds’ Portfolio Management Team during the Reporting Period |

| |

Effective January 1, 2016, there was a shift in sector coverage for GSAM’s U.S. Small Cap Value and U.S. Small/Mid Cap Value strategies. Rob Crystal, Managing Director, assumed research responsibility for health care in the GSAM U.S. Small Cap Value and U.S. Small/Mid Cap Value strategies. He has 19 years of industry experience, ten of which were spent covering health care prior to joining the team. Rob continues to serve as co-lead portfolio manager and retains sector responsibilities for technology and industrials. Over the next few months, Rob will transition a portion of his industrials coverage to Sean Butkus, Vice President, a senior sector portfolio manager with 19 years of experience. Additionally, Rob will be supported by a dedicated health care research analyst in our Bengaluru office. David Deuchler, Vice President, now focuses exclusively on the health care and industrials sectors within the GSAM U.S. Mid Cap Value strategy. The U.S. Small Cap Value and U.S. Small/Mid Cap Value team consists of seven senior sector portfolio managers averaging 20 years of experience. The three co-lead portfolio managers (Rob Crystal and Sally Pope Davis, Managing Director, continue to focus exclusively on our Small Cap Value and Small/Mid Cap Value strategies, and Sean Butkus on our Small/Mid Cap Value strategy) have 73 years of combined experience. Our deep, experienced and stable team employs the same disciplined process used in our portfolios since 2000. Sean Gallagher, Chief Investment Officer of GSAM U.S. Value Equity, continues to lead the broader team of 15 portfolio managers, who are supported by more than ten dedicated research analysts. We have a deep bench of talented leaders and investment professionals who are intensely focused on delivering strong, long-term results for our shareholders. |

5

PORTFOLIO RESULTS

Goldman Sachs Focused Value Fund

Portfolio Composition

The Fund’s investment objective is to seek long-term capital appreciation. The Fund invests, under normal circumstances, at least 80% of its net assets plus any borrowings for investment purposes (measured at time of purchase) in a portfolio of equity investments, including common stocks, preferred stocks and other securities and instruments having equity characteristics. The Fund seeks to achieve its investment objective by investing, under normal circumstances, in approximately 20-35 companies that are considered value opportunities, which the Investment Adviser defines as companies with identifiable competitive advantages whose intrinsic value is not reflected in the stock price. The Fund may invest in securities of companies of any capitalization. Although the Fund will invest primarily in publicly traded U.S. securities, it may invest up to 20% of its total assets in foreign securities, including securities of issuers in countries with emerging markets or economies (“emerging countries”) and securities quoted in foreign currencies. The Fund may invest in fixed income securities, such as government, corporate and bank debt obligations.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Value Equity Investment Team discusses the Goldman Sachs Focused Value Fund’s (the “Fund”) performance and positioning for the six-month period ended February 29, 2016 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, IR, R and R6 Shares generated cumulative total returns, without sales charges, of -7.97%, -8.37%, -7.80%, -7.76%, -8.17% and -7.79%, respectively. These returns compare to the -2.87% cumulative total return of the Fund’s benchmark, the Russell 1000® Value Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | Stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole contributed positively, albeit modestly, to the Fund’s results. |

| Q | | Which equity market sectors most significantly affected Fund performance? |

| A | | The sectors that most meaningfully detracted from the Fund’s relative results during the Reporting Period were financials, industrials and energy, where stock selection was challenged. Stock selection was most materially effective in information technology, health care and telecommunication services, which helped the Fund’s performance relative to the Russell Index. Having an overweighted allocation to telecommunication services, which significantly outpaced the Russell Index during the Reporting Period, also contributed positively. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Russell Index were positions in car rental company Hertz Global Holdings and in two oil and gas exploration and production companies — Southwestern Energy and Devon Energy. |

| | Hertz Global Holdings was the top detractor from the Fund’s relative results during the Reporting Period. Its shares initially came under pressure after the company reported third quarter 2015 results that were below market expectations, driven by weaker than expected pricing trends in the U.S. caused by increased airport competition. Its sharp decline in share price in the latter half of the Reporting Period seemed to be driven more by investor fears related to macroeconomic conditions than by industry or stock-specific fundamentals. If the U.S. were to enter a span of slower economic growth, travel trends would likely soften and pressure car rental volumes and prices. A weaker demand environment could also pressure used car prices, which might cause the company to dispose of cars at lower residual values. Despite our positive long-term view of the company’s operational improvement initiatives, available capital deployment options and cost reduction opportunities, |

6

PORTFOLIO RESULTS

| | we sold the Fund’s position in Hertz Global Holdings by the end of the Reporting Period in favor of stocks with what we believed to have less economic sensitivity. |

| | Southwestern Energy was a top detractor from the Fund’s relative performance during the Reporting Period. Exceptionally warm fall and winter weather that added to concerns of an oversupplied natural gas market was the major headwind that led to the stock’s poor performance, as natural gas prices declined substantially. Broad-based declines in global commodities weakened investor appetite for stocks with direct commodity exposure. The company’s third quarter 2015 earnings came in ahead of consensus expectations, driven by higher than expected production metrics coupled with lower operating costs. However, challenging natural gas liquid and natural gas pricing caused shares to underperform following the earnings release. The company similarly reported fourth quarter 2015 earnings that beat consensus expectations due to better than expected gas price realizations and midstream revenues. However, further capital expenditure cuts in 2016 led investors to anticipate a larger decline in production than previously expected, and Southwestern Energy’s shares fell following the release. At the end of the Reporting Period, we continued to believe that Southwestern Energy has an underappreciated resource base, specifically in the Marcellus and Fayetteville shales, and that its newly acquired assets from Chesapeake Energy further strengthen the company’s position and growth opportunities. Additionally, we remained positive on the company’s operational leverage to higher natural gas prices and encouraged by its management team’s commitment to capital efficiency amidst challenging macro fundamentals. |

| | Devon Energy’s shares came under pressure after the company announced plans to acquire approximately $2.5 billion worth of assets in the Anadarko and Powder River Basins. Although the assets strengthen Devon Energy’s positioning in two key shale plays that have exhibited strong well results and although we believed Devon Energy’s large North American asset base was not fully recognized at then-current market levels, we decided to exit the Fund’s position in Devon Energy. We felt risk-adjusted return profiles were more compelling elsewhere in the industry. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The Fund benefited most relative to the Russell Index from positions in discount retailer Wal-Mart Stores, oil and gas exploration and production company Cabot Oil & Gas and generic pharmaceutical company Mylan. |

| | The Fund purchased shares of Wal-Mart Stores, the world’s largest retailer, opportunistically after a period of underperformance resulting from fears of the impact of higher wage costs and secular competitive threats due to e-commerce proliferation. With these concerns priced in, we believed the valuation provided an opportune time to buy the stock. Its shares subsequently appreciated in January 2016 after Wal-Mart Stores emphasized its focus on improving efficiency and profitability by announcing a plan to close many of its smaller format Walmart Express stores and open more supercenter stores. At the end of the Reporting Period, we believed the company’s core operating business was stable, with the potential for incremental traffic benefits following current store improvement initiatives. Further, we remained attracted to the company’s exposure to the possibility that consumers could benefit from depressed energy prices and an improving U.S. economic backdrop. |

| | We initiated a Fund position in Cabot Oil & Gas, an exploration and production company predominantly focused on natural gas opportunistically in January 2016. We believed the natural gas supply and demand dynamic could meaningfully improve, and Cabot Oil & Gas, which is one of the lowest cost producers in the industry, could be a beneficiary. Furthermore, the company has what we consider to be a strong balance sheet and attractive acreage in the Marcellus Shale. The company’s shares appreciated as sentiment on natural gas equities improved, following an increase in natural gas prices through the fiscal year-end. Following its strong performance, we exited the position in favor of opportunities that we believed had more upside potential. |

| | Mylan was a top contributor to the Fund’s relative results during the Reporting Period. Its shares gained after the company reported a full-year 2015 earnings outlook at the high end of its previously stated range and on setbacks for two of its major competitors in its epinephrine injection business. In November 2015, its shares rose sharply after the company reported that its hostile bid for competitor Perrigo, a manufacturer of private label over-the-counter pharmaceuticals, fell short of the needed support from Perrigo shareholders. Investors viewed the outcome favorably as a result of the elevated deal price and lower industry valuations following the announcement of the takeover. Subsequently, Mylan announced authorization of a $1 billion share repurchase program, which we believe indicates shareholder-friendly capital deployment. Following Mylan’s strong |

7

PORTFOLIO RESULTS

| | relative performance, we exited the position in favor of stocks we considered to have more upside potential. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | In addition to those purchases already mentioned, we initiated a Fund position in BP, an integrated oil and gas company. We view the company’s capital efficiency favorably, evidenced by production growth despite capital expenditure reductions. With the July 2015 announcement of a U.S. civil settlement for BP’s 2010 oil spill, we believe a large overhang on the stock was removed. Further, in our view, the legal settlement improved BP’s financial flexibility because a key liability has been defined, and cash payments can be managed with strong free cash flow generation. The capital discipline of BP’s management gives us confidence in the potential sustainability of the company’s dividend, and we believe the company is attractively valued relative to its peers. |

| | We established a Fund position in household products company Procter & Gamble. We believe the company’s successfully completed portfolio restructuring is in the early stages of yielding benefits. Procter & Gamble divested approximately 100 slow-growing brands, which we believe may be an impetus for future revenue growth. The divestitures have also led to a less complex supply chain, which should improve operational efficiency moving forward, in our view. In addition, we believe the company should benefit from weakness in commodity prices, as a large portion of operational costs are derived from the price of oil. Further, Procter & Gamble’s new management team appears to have fostered a culture focused on operational excellence and shareholder returns, which we believe may well be additive to long-term value creation. |

| | Conversely, in addition to those sales mentioned earlier, we exited the Fund’s position in EMC during the Reporting Period. We believed EMC was one of the best positioned information technology hardware vendors in the industry. We also felt the recovery in enterprise spending would benefit EMC, as companies increasingly focus on both storage spending and virtualization. Finally, we believed the company was attractively valued given its strong free cash flow generation and above average growth prospects relative to its peers. Our thesis was validated when it was announced during the Reporting Period that EMC would be acquired by Dell for a healthy premium. Following substantial appreciation in the stock, we sold the position in favor of other opportunities we believed had more upside potential. |

| | We eliminated the Fund’s position in American International Group (“AIG”), a global insurance company. We had initiated the Fund’s position in AIG because we felt its shares were undervalued given the company’s near-term to medium-term opportunities for return on equity improvement. We were also positive on its management’s focus on growing the company’s core insurance business and improving operational performance. Following our initial investment, we were encouraged when its management announced a restructuring program, which included cost reductions and divestitures. However, the plan included major, complex changes within the organization within a relatively short time frame, something we felt was going to be challenging and potentially overly ambitious. Strict to our sell discipline, as key points of our investment thesis became challenged, we sold the stock in favor of other opportunities. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the Russell Index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s allocations in telecommunication services, consumer staples and health care increased compared to the Russell Index as did its position in cash. The Fund’s exposure to the consumer discretionary, financials, industrials, energy and information technology sectors decreased compared to the Russell Index. |

| Q | | How was the Fund positioned relative to its benchmark index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund was overweighted in consumer staples and telecommunication services relative to the Russell Index. On the same date, the Fund had underweighted positions compared to the Russell Index in energy, financials, utilities, industrials and health care and was rather neutrally weighted to the Russell Index in consumer discretionary and information technology. The Fund had no allocation to materials at the end of the Reporting Period. |

8

FUND BASICS

Focused Value Fund

as of February 29, 2016

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | September 1, 2015–February 29, 2016 | | Fund Total Return

(based on NAV)1 | | | Russell 1000®

Value Index2 | |

| | Class A | | | -7.97 | % | | | -2.87 | % |

| | Class C | | | -8.37 | | | | -2.87 | |

| | Institutional | | | -7.80 | | | | -2.87 | |

| | Class IR | | | -7.76 | | | | -2.87 | |

| | Class R | | | -8.17 | | | | -2.87 | |

| | | Class R6 | | | -7.79 | | | | -2.87 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The unmanaged Russell 1000® (with dividends reinvested) is a market capitalization weighted index of the 1,000 largest U.S. companies with lower price-to-book ratios and lower forecasted growth values. The Index figures do not reflect any deduction of fees, expenses or taxes. It is not possible to invest directly in an index. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | | | | | | | | |

| | | For the period ended 12/31/15 | | Since Inception | | | Inception Date | |

| | Class A | | | -12.64 | % | | | 7/31/15 | |

| | Class C | | | -8.79 | | | | 7/31/15 | |

| | Institutional | | | -7.41 | | | | 7/31/15 | |

| | Class IR | | | -7.47 | | | | 7/31/15 | |

| | Class R | | | -7.67 | | | | 7/31/15 | |

| | | Class R6 | | | -7.40 | | | | 7/31/15 | |

| | 3 | | The Standardized Total Returns are average annual or cumulative total returns for periods less than 1 year as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Class IR, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

9

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.13 | % | | | 24.10 | % |

| | Class C | | | 1.89 | | | | 24.86 | |

| | Institutional | | | 0.74 | | | | 23.71 | |

| | Class IR | | | 0.89 | | | | 23.86 | |

| | Class R | | | 1.39 | | | | 24.36 | |

| | | Class R6 | | | 0.72 | | | | 23.69 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | |

| | TOP TEN HOLDINGS AS OF 2/29/165 |

| | | | | | | | |

| | | Holding | | % of Net Assets | | | Line of Business |

| | AT&T, Inc. | | | 7.1 | % | | Diversified Telecommunication Services |

| | Wal-Mart Stores, Inc. | | | 6.2 | | | Food & Staples Retailing |

| | Pfizer, Inc. | | | 5.7 | | | Pharmaceuticals |

| | Cisco Systems, Inc. | | | 5.1 | | | Communications Equipment |

| | Bank of America Corp. | | | 5.0 | | | Commercial Banks |

| | The Procter & Gamble Co. | | | 5.0 | | | Household Products |

| | JPMorgan Chase & Co. | | | 4.8 | | | Commercial Banks |

| | General Electric Co. | | | 4.5 | | | Industrial Conglomerates |

| | BP PLC ADR | | | 4.1 | | | Oil, Gas & Consumable Fuels |

| | | Alphabet, Inc. Class A | | | 4.1 | | | Internet Software & Services |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

10

FUND BASICS

|

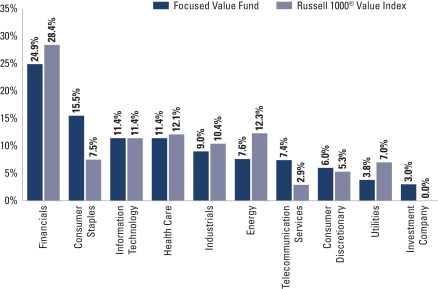

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of February 29, 2016 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”); however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

11

PORTFOLIO RESULTS

Goldman Sachs Growth and Income Fund

Portfolio Composition

Under normal circumstances, the Fund invests at least 65% of its total net assets measured at the time of purchase in equity investments that the Investment Adviser considers to have favorable prospects for capital appreciation and/or dividend-paying ability. Although the Fund will invest primarily in publicly traded U.S. securities, including preferred and convertible securities, master limited partnerships and real estate investment trusts, it may invest up to 25% of its total net assets in foreign securities, including securities of issuers with emerging countries or economies and securities quoted in foreign currencies. The Fund may also invest in fixed income securities, such as government, corporate and bank debt obligations, that offer the potential to further the Fund’s investment objective of long-term capital appreciation and growth of income.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Value Equity Investment Team discusses the Goldman Sachs Growth and Income Fund’s (the “Fund”) performance and positioning for the six-month period ended February 29, 2016 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, Service, IR, R and R6 Shares generated cumulative total returns, without sales charges, of -4.33%, -4.66%, -4.12%, -4.38%, -4.19%, -4.44% and -4.14%, respectively. These returns compare to the -2.87% cumulative total return of the Fund’s benchmark, the Russell 1000® Value Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | Stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole contributed positively to the Fund’s results. |

| Q | | Which equity market sectors most significantly affected Fund performance? |

| A | | The sectors that detracted most from the Fund’s relative results during the Reporting Period were financials, consumer discretionary and utilities, where stock selection proved challenging. Effective stock selection in the industrials, consumer staples and information technology sectors helped the Fund’s relative results most. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Russell Index were positions in two oil and gas exploration and production companies — Devon Energy and Southwestern Energy — and in asset manager AllianceBernstein Holding. |

| | Devon Energy’s shares came under pressure after the company announced plans to acquire approximately $2.5 billion worth of assets in the Anadarko and Powder River Basins. Although the assets strengthen Devon Energy’s positioning in two key shale plays that have exhibited strong well results and although we believed Devon Energy’s large North American asset base was not fully recognized at then-current market levels, we decided to exit the Fund’s position in Devon Energy. We felt risk-adjusted return profiles were more compelling elsewhere in the industry. |

| | Southwestern Energy was a top detractor from the Fund’s relative performance during the Reporting Period. Exceptionally warm fall and winter weather that added to concerns of an oversupplied natural gas market was the major headwind that led to the stock’s poor performance, as natural gas prices declined substantially. Broad-based declines in global commodities weakened investor appetite for stocks with direct commodity exposure. The company’s third quarter 2015 earnings came in ahead of consensus expectations, driven by higher than expected production metrics coupled with lower operating costs. However, |

12

PORTFOLIO RESULTS

| | challenging natural gas liquid and natural gas pricing caused shares to underperform following the earnings release. The company similarly reported fourth quarter 2015 earnings that beat consensus due to better than expected gas price realizations and midstream revenues. However, further capital expenditure cuts in 2016 led investors to anticipate a larger decline in production than previously expected, and Southwestern Energy’s shares fell following the release. At the end of the Reporting Period, we continued to believe that Southwestern Energy has an underappreciated resource base, specifically in the Marcellus and Fayetteville shales, and that its newly acquired assets from Chesapeake Energy further strengthen the company’s position and growth opportunities. Additionally, we remained positive on the company’s operational leverage to higher natural gas prices and encouraged by its management team’s commitment to capital efficiency amidst challenging macro fundamentals. |

| | AllianceBernstein Holding performed poorly amidst a weak environment for asset managers given volatility in capital markets. The company reported a challenging fourth quarter 2015 that drove its stock price lower. Its revenues came in below market expectations, driven by lower performance fees, research services revenues and investment management fees. Also, its negative net flows of approximately $2.5 billion were greater than the market expected. Despite the challenging environment for asset managers, we expect the company’s improved relative performance late in the Reporting Period to translate into better net flows and a higher earnings trajectory going forward. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The Fund benefited most relative to the Russell Index from positions in industrial conglomerate General Electric, discount retailer Wal-Mart Stores and global telecommunications company AT&T. |

| | General Electric was the top positive contributor to the Fund’s relative results during the Reporting Period. The company reported third quarter 2015 earnings results that exceeded consensus expectations, driven by strong organic revenue growth and operating margin improvement. Additionally, its shares rose after General Electric’s long-awaited announcement about spinning off its majority stake in Synchrony Financial to existing shareholders. Further, in December 2015, General Electric held its 2016 outlook meeting, which included a projection of high single-digit earnings growth through 2018, achieved through above-average organic revenue growth, share repurchases, divestitures, and synergies from the company’s acquisition of Alstom Energy. At the end of the Reporting Period, we remained optimistic on the company’s growth prospects, as a strong backlog of orders and accretive synergies from recent transactions could be supportive to earnings in a potentially slow global economic growth environment, in our view. |

| | The Fund purchased additional shares of Wal-Mart Stores, the world’s largest retailer, opportunistically after a period of underperformance resulting from fears of the impacts of higher wage costs and secular competitive threats due to e-commerce proliferation. With these concerns priced in, we believed the valuation provided an opportune time to buy the stock. Its shares subsequently appreciated in January 2016 after Wal-Mart Stores emphasized its focus on improving efficiency and profitability by announcing a plan to close many of its smaller format Walmart Express stores and open more supercenter stores. At the end of the Reporting Period, we believed the company’s core operating business was stable, with the potential for incremental traffic benefits following current store improvement initiatives. Further, we remained attracted to the company’s exposure to the possibility that consumers could benefit from depressed energy prices and an improving U.S. economic backdrop. |

| | Shares of AT&T performed well following constructive commentary from its management team during its fourth quarter 2015 earnings report. The company expects to generate mid-single-digit earnings growth in 2016, driven in part by margin accretion from synergies related to its recent acquisition of DirecTV. Additionally, its management anticipates strong free cash flow generation, which should support dividend coverage and debt repayment, in our view. To drive growth, we believe AT&T is likely to continue to utilize its unique asset base to deliver integrated video and wireless capabilities to consumers. At the end of the Reporting Period, we remained constructive on the risk-adjusted upside potential of AT&T, as what we view as its attractive dividend yield and focus on free cash flow generation remained compelling to us in an environment characterized by uncertainty. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

13

PORTFOLIO RESULTS

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | We initiated a Fund position in M&T Bank. At the time of purchase, we believed M&T Bank was undervalued, and we were positive on the company’s recent acquisition of Hudson City Bancorp, which we believe should be accretive to earnings and allow the company to return more capital to shareholders. Additionally, we are encouraged by what we view as the company’s effective management team and its consistent focus on driving strong risk-adjusted shareholder returns. |

| | We established a Fund position in Whole Foods Market, an organic foods supermarket chain. We are optimistic on the company and its dominant market position. Of note are the significant steps that Whole Foods Market’s management has actively taken to improve the company’s pricing and marketing. We believe these efforts could potentially drive sales growth in the coming quarters. We also like what we consider to be the company’s good earnings visibility from cost-reduction efforts and its potential share buybacks. |

| | Conversely, in addition to those sales already mentioned, we eliminated the Fund’s position in American International Group (“AIG”), a global insurance company. We had initiated the Fund’s position in AIG because we felt its shares were undervalued given the company’s near-term to medium-term opportunities for return on equity improvement. We were also positive on its management’s focus on growing the company’s core insurance business and improving operational performance. Following our initial investment, we were encouraged when its management announced a restructuring program, which included cost reductions and divestitures. However, the plan included major, complex changes within the organization within a relatively short time frame, something we felt was going to be challenging and potentially overly ambitious. Strict to our sell discipline, as key points of our investment thesis became challenged, we sold the stock in favor of other opportunities. |

| | We exited the Fund’s position in Boeing, a designer and manufacturer of commercial jetliners, military defense and spaceflight worldwide. During the Reporting Period, a Securities and Exchange Commission (“SEC”) investigation was announced related to accounting principles on Boeing’s 747 and 787 programs, prompted by an internal whistleblower. We have no insight into whether or not the company is in violation of any generally accepted accounting principles, but our time frame for owning the stock was only a few months to a year, and we believe the investigation could be a headwind for a longer timeframe. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the Russell Index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s allocations in consumer staples, energy, information technology and utilities increased compared to the Russell Index, as did its position in cash. The Fund’s exposure to consumer discretionary, financials, health care and industrials decreased compared to the Russell Index. |

| Q | | How was the Fund positioned relative to its benchmark index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had overweighted positions relative to the Russell Index in the consumer staples and telecommunication services sectors. On the same date, the Fund had underweighted positions compared to the Russell Index in financials, industrials, information technology and consumer discretionary and was rather neutrally weighted to the Russell Index in energy, health care, materials and utilities. |

14

FUND BASICS

Growth and Income Fund

as of February 29, 2016

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | September 1, 2015–February 28, 2016 | | Fund Total Return

(based on NAV)1 | | | Russell 1000®

Value Index2 | |

| | Class A | | | -4.33 | % | | | -2.87 | % |

| | Class C | | | -4.66 | | | | -2.87 | |

| | Institutional | | | -4.12 | | | | -2.87 | |

| | Service | | | -4.38 | | | | -2.87 | |

| | Class IR | | | -4.19 | | | | -2.87 | |

| | Class R | | | -4.44 | | | | -2.87 | |

| | | Class R6 | | | -4.14 | | | | -2.87 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The unmanaged Russell 1000® Value Index (with dividends reinvested) is a market capitalization weighted index of the 1,000 largest U.S. companies with lower price-to-book ratios and lower forecasted growth values. The Index figures do not reflect any deduction of fees, expenses or taxes. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 12/31/15 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | | Inception Date |

| | Class A | | | -8.40 | % | | | 8.31 | % | | | 4.62 | % | | | 6.66 | % | | 2/5/93 |

| | Class C | | | -4.78 | | | | 8.72 | | | | 4.43 | | | | 2.75 | | | 8/15/97 |

| | Institutional | | | -2.70 | | | | 9.99 | | | | 5.63 | | | | 5.81 | | | 6/3/96 |

| | Service | | | -3.17 | | | | 9.44 | | | | 5.11 | | | | 5.37 | | | 3/6/96 |

| | Class IR | | | -2.83 | | | | 9.82 | | | | N/A | | | | 3.90 | | | 11/30/07 |

| | Class R | | | -3.33 | | | | 9.28 | | | | N/A | | | | 3.39 | | | 11/30/07 |

| | | Class R6 | | | N/A | | | | N/A | | | | N/A | | | | -4.19 | | | 7/31/15 |

| | 3 | | The Standardized Total Returns are average annual or cumulative total returns for periods less than 1 year as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service, Class IR, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

15

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.13 | % | | | 1.22 | % |

| | Class C | | | 1.88 | | | | 1.97 | |

| | Institutional | | | 0.73 | | | | 0.82 | |

| | Service | | | 1.23 | | | | 1.32 | |

| | Class IR | | | 0.88 | | | | 0.97 | |

| | Class R | | | 1.38 | | | | 1.47 | |

| | | Class R6 | | | 0.71 | | | | 0.80 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | |

| | TOP TEN HOLDINGS AS OF 2/29/165 |

| | | | | | | | |

| | | Holding | | % of Net Assets | | | Line of Business |

| | Exxon Mobil Corp. | | | 5.0 | % | | Oil, Gas & Consumable Fuels |

| | JPMorgan Chase & Co. | | | 4.6 | | | Commercial Banks |

| | AT&T, Inc. | | | 4.4 | | | Diversified Telecommunication Services |

| | Pfizer, Inc. | | | 4.3 | | | Pharmaceuticals |

| | General Electric Co. | | | 4.0 | | | Industrial Conglomerates |

| | Wells Fargo & Co. | | | 3.9 | | | Commercial Banks |

| | The Procter & Gamble Co. | | | 3.0 | | | Household Products |

| | Wal-Mart Stores, Inc. | | | 2.6 | | | Food & Staples Retailing |

| | BP PLC ADR | | | 2.6 | | | Oil, Gas & Consumable Fuels |

| | | Johnson & Johnson | | | 2.5 | | | Pharmaceuticals |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

16

FUND BASICS

|

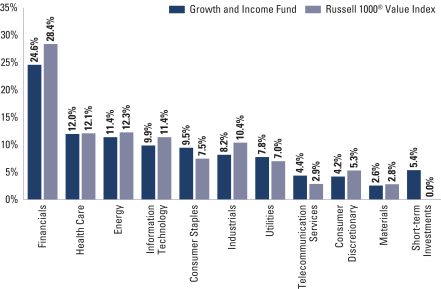

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of February 29, 2016 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”); however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. Short-term investments represent repurchase agreements. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

17

PORTFOLIO RESULTS

Goldman Sachs Large Cap Value Fund

Portfolio Composition

The Fund invests, under normal circumstances, at least 80% of its total net assets plus any borrowings for investment purposes (measured at time of purchase) in a diversified portfolio of equity investments in large-cap U.S. issuers with public stock market capitalizations within the range of the market capitalization of companies constituting the Russell 1000® Value Index at the time of investment. The Fund seeks its investment objective of long-term capital appreciation by investing in value opportunities that the Goldman Sachs Value Equity Investment Team defines as companies with identifiable competitive advantages whose intrinsic value is not reflected in the stock price. Although the Fund will invest primarily in publicly traded U.S. securities, it may invest in foreign securities, including securities of issuers in countries with emerging markets or economies quoted in foreign currencies. The Fund may also invest in companies with public stock market capitalizations outside the range of companies constituting the Russell 1000® Value Index at the time of investment and in fixed income securities, such as government, corporate and bank debt obligations.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Value Equity Investment Team discusses the Goldman Sachs Large Cap Value Fund’s (the “Fund”) performance and positioning for the six-month period ended February 29, 2016 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, Service, IR, R and R6 Shares generated cumulative total returns, without sales charges, of -6.05%, -6.36%, -5.86%, -6.11%, -5.95%, -6.14% and -5.82%, respectively. These returns compare to the -2.87% cumulative total return of the Fund’s benchmark, the Russell 1000® Value Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | Stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole contributed positively, albeit modestly, to the Fund’s results. |

| Q | | Which equity market sectors most significantly affected Fund performance? |

| A | | Detracting most from the Fund’s performance relative to the Russell Index were financials, consumer discretionary and energy, where stock selection was comparatively weak. Effective stock selection in the information technology, consumer staples and materials sectors helped the Fund’s relative results most. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Russell Index were positions in two oil and gas exploration and production companies — Southwestern Energy and Devon Energy — and in car rental company Hertz Global Holdings. |

| | Southwestern Energy was a top detractor from the Fund’s relative performance during the Reporting Period. Exceptionally warm fall and winter weather that added to concerns of an oversupplied natural gas market was the major headwind that led to the stock’s poor performance, as natural gas prices declined substantially. Broad-based declines in global commodities weakened investor appetite for stocks with direct commodity exposure. The company’s third quarter 2015 earnings came in ahead of consensus expectations, driven by higher than expected production metrics coupled with lower operating costs. However, challenging natural gas liquid and natural gas pricing caused shares to underperform following the earnings release. The company similarly reported fourth quarter 2015 earnings that beat consensus due to better than expected gas price realizations and midstream revenues. However, further capital expenditure cuts in 2016 led investors to anticipate a larger decline in production than previously expected, and Southwestern Energy’s shares fell following the release. At |

18

PORTFOLIO RESULTS

| | the end of the Reporting Period, we continued to believe that Southwestern Energy has an underappreciated resource base, specifically in the Marcellus and Fayetteville shales, and that its newly acquired assets from Chesapeake Energy further strengthen the company’s position and growth opportunities. Additionally, we remained positive on the company’s operational leverage to higher natural gas prices and encouraged by its management team’s commitment to capital efficiency amidst challenging macro fundamentals. |

| | Devon Energy’s shares came under pressure after the company announced plans to acquire approximately $2.5 billion worth of assets in the Anadarko and Powder River Basins. Although the assets strengthen Devon Energy’s positioning in two key shale plays that have exhibited strong well results and although we believed Devon Energy’s large North American asset base was not fully recognized at then-current market levels, we decided to exit the Fund’s position in Devon Energy. We felt risk-adjusted return profiles were more compelling elsewhere in the industry. |

| | Hertz Global Holdings was the top detractor from the Fund’s relative results during the Reporting Period. Its shares initially came under pressure after the company reported third quarter 2015 results that were below market expectations, driven by weaker than expected pricing trends in the U.S. caused by increased airport competition. Its sharp decline in share price in the latter half of the Reporting Period seemed to be driven more by investor fears related to macroeconomic conditions than by industry or stock-specific fundamentals. If the U.S. were to enter a span of slower economic growth, travel trends would likely soften and pressure car rental volumes and prices. A weaker demand environment could also pressure used car prices, which might cause the company to dispose of cars at lower residual values. Despite our positive long-term view of the company’s operational improvement initiatives, available capital deployment options and cost reduction opportunities, we sold the Fund’s position in Hertz Global Holdings by the end of the Reporting Period in favor of stocks with what we believed to have less economic sensitivity. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The Fund benefited most relative to the Russell Index from positions in industrial conglomerate General Electric, packaged foods producer Tyson Foods and integrated oil and gas company ConocoPhillips. |

| | General Electric was the top positive contributor to the Fund’s relative results during the Reporting Period. The company reported third quarter 2015 earnings results that exceeded consensus expectations, driven by strong organic revenue growth and operating margin improvement. Additionally, its shares rose after General Electric’s long-awaited announcement about spinning off its majority stake in Synchrony Financial to existing shareholders. Further, in December 2015, General Electric held its 2016 outlook meeting, which included a projection of high single-digit earnings growth through 2018, achieved through above-average organic revenue growth, share repurchases, divestitures, and synergies from the company’s acquisition of Alstom Energy. At the end of the Reporting Period, we remained optimistic on the company’s growth prospects, as a strong backlog of orders and accretive synergies from recent transactions could be supportive to earnings in a potentially slow global economic growth environment, in our view. |

| | Shares of Tyson Foods rose throughout the Reporting Period, as the company consistently delivered strong earnings results and raised forward guidance as a result of strong execution on its strategy to diversify away from traditional fresh meat sales through its acquisition of Hillshire Brands. At the end of the Reporting Period, we continued to believe that Tyson Foods is a high quality business that generates strong cash flow. We had confidence that its management would continue to allocate capital to maximize shareholder value. Additionally, we believe the acquisition of Hillshire Brands should be accretive. However, following such strong relative performance, we exited the position and rotated the proceeds to names with what we believed to be greater upside potential. |

| | We had added to the Fund’s position in ConocoPhillips during the Reporting Period as we felt the stock was oversold and its valuation compelling following a challenging fourth quarter 2015, dragged down by lower production, weaker price realizations and asset write-downs. (A write-down is reducing the book value of an asset because it is overvalued compared to the market value.) ConocoPhillips’ shares subsequently experienced sizable gains as a result of a rally, albeit a modest one, in oil prices. At the end of the Reporting Period, we saw ConocoPhillips as having a diversified portfolio with scale and multiple sources of growth potential. We also felt the company had significant capital flexibility following large reductions in capital and operating expenditures and an ability to grow production in a low commodity price environment despite these capital |

19

PORTFOLIO RESULTS

| | expenditure reductions. Finally, we maintained our view that the company had a return-focused management with a strong record of value creation. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives as part of an active management strategy. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | We established a Fund position in specialty pharmaceuticals company Allergan following unsubstantiated news flow regarding a proposed inversion deal between Allergan and Pfizer. (Corporate inversion refers to re-incorporating a company overseas in order to reduce the tax burden on income earned abroad. Corporate inversion as a strategy is used by companies that receive a significant portion of their income from foreign sources, since that income is taxed both abroad and in the country of incorporation.) In our view, the combined company would have an attractive portfolio of drugs that treat ailments, such as Alzheimer’s and rheumatoid arthritis. The companies expect more than $2 billion a year’s worth of increased efficiencies within three years of the deal close. We have a positive outlook on the deal closing, as we do not see any material changes being made by the U.S. Treasury as it relates to tax inversion deals prior to the deal close. That said, regardless of the deal outcome, we believe Allergan is a compelling asset to own. |

| | We initiated a Fund position in BP, an integrated oil and gas company. We view the company’s capital efficiency favorably, evidenced by production growth despite capital expenditure reductions. With the July 2015 announcement of a U.S. civil settlement for BP’s 2010 oil spill, we believe a large overhang on the stock was removed. Further, in our view, the legal settlement improved BP’s financial flexibility because a key liability has been defined, and cash payments can be managed with strong free cash flow generation. The capital discipline of BP’s management gives us confidence in the potential sustainability of the company’s dividend, and we believe the company is attractively valued relative to its peers. |

| | Conversely, in addition to those sales already mentioned, we exited the Fund’s position in financial institution Citigroup. The decision was made in line within a broader effort to reduce the fund’s exposure to market-sensitive capital markets businesses. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | In constructing the Fund’s portfolio, we focus on picking stocks rather than on making industry or sector bets. We seek to outpace the Russell Index by overweighting stocks that we expect to outperform and underweighting those that we think may lag. Consequently, changes in its sector weights are generally the direct result of individual stock selection or of stock appreciation or depreciation. That said, during the Reporting Period, the Fund’s allocations compared to the Russell Index in health care and utilities increased as did its position in cash. The Fund’s exposure to consumer discretionary, financials and industrials decreased compared to the Russell Index. |

| Q | | How was the Fund positioned relative to its benchmark index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had overweighted positions relative to the Russell Index in the health care and information technology sectors. On the same date, the Fund had underweighted positions compared to the Russell Index in financials, industrials, energy and utilities and was rather neutrally weighted to the Russell Index in consumer discretionary, consumer staples, materials and telecommunication services. |

20

FUND BASICS

Large Cap Value Fund

as of February 29, 2016

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | September 1, 2015–February 29, 2016 | | Fund Total Return

(based on NAV)1 | | | Russell 1000®

Value Index2 | |

| | Class A | | | -6.05 | % | | | -2.87 | % |

| | Class C | | | -6.36 | | | | -2.87 | |

| | Institutional | | | -5.86 | | | | -2.87 | |

| | Service | | | -6.11 | | | | -2.87 | |

| | Class IR | | | -5.95 | | | | -2.87 | |

| | Class R | | | -6.14 | | | | -2.87 | |

| | | Class R6 | | | -5.82 | | | | -2.87 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The unmanaged Russell 1000® Value Index (with dividends reinvested) is a market capitalization weighted index of the 1,000 largest U.S. companies with lower price-to-book ratios and lower forecasted growth values. The Index figures do not reflect any deduction of fees, expenses or taxes. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 12/31/15 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | | Inception Date |

| | Class A | | | -9.93 | % | | | 8.05 | % | | | 4.71 | % | | | 5.26 | % | | 12/15/99 |

| | Class C | | | -7.22 | | | | 8.48 | | | | 4.53 | | | | 4.84 | | | 12/15/99 |

| | Institutional | | | -4.30 | | | | 9.72 | | | | 5.73 | | | | 6.04 | | | 12/15/99 |

| | Service | | | -4.76 | | | | 9.19 | | | | 5.21 | | | | 5.55 | | | 12/15/99 |

| | Class IR | | | -4.44 | | | | 9.57 | | | | N/A | | | | 4.24 | | | 11/30/07 |

| | Class R | | | -4.90 | | | | 9.02 | | | | N/A | | | | 3.74 | | | 11/30/07 |

| | | Class R6 | | | N/A | | | | N/A | | | | N/A | | | | -4.96 | | | 7/31/15 |

| | 3 | | The Standardized Total Returns are average annual or cumulative total returns for periods less than 1 year as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service, Class IR, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

21

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.17 | % | | | 1.20 | % |

| | Class C | | | 1.92 | | | | 1.95 | |

| | Institutional | | | 0.77 | | | | 0.80 | |

| | Service | | | 1.27 | | | | 1.30 | |

| | Class IR | | | 0.92 | | | | 0.95 | |

| | Class R | | | 1.42 | | | | 1.45 | |

| | | Class R6 | | | 0.75 | | | | 0.78 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least December 29, 2016, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | |

| | TOP TEN HOLDINGS AS OF 2/29/165 |

| | | Holding | | % of Net Assets | | | Line of Business |

| | Bank of America Corp. | | | 4.3 | % | | Commercial Banks |

| | General Electric Co. | | | 4.3 | | | Industrial Conglomerates |

| | Exxon Mobil Corp. | | | 4.0 | | | Oil, Gas & Consumable Fuels |

| | JPMorgan Chase & Co. | | | 3.9 | | | Commercial Banks |

| | Wells Fargo & Co. | | | 3.7 | | | Commercial Banks |

| | The Procter & Gamble Co. | | | 3.7 | | | Household Products |

| | AT&T, Inc. | | | 3.1 | | | Diversified Telecommunication Services |

| | Pfizer, Inc. | | | 3.0 | | | Pharmaceuticals |

| | Microsoft Corp. | | | 2.5 | | | Software |

| | | Allergan PLC | | | 2.3 | | | Pharmaceuticals |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

22

FUND BASICS

|

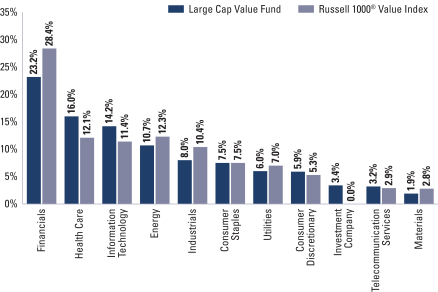

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of February 29, 2016 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”); however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

23

PORTFOLIO RESULTS

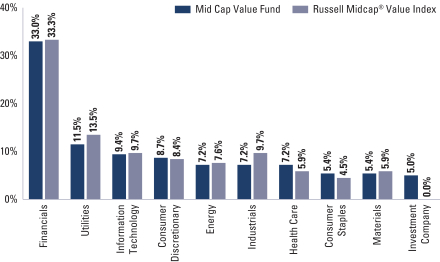

Goldman Sachs Mid Cap Value Fund

Portfolio Composition

The Fund invests, under normal circumstances, at least 80% of its total net assets plus any borrowings for investment purposes (measured at time of purchase) in a diversified portfolio of equity investments in mid-cap issuers with public stock market capitalizations within the range of the market capitalization of companies constituting the Russell Midcap® Value Index at the time of investment. The Fund seeks its investment objective of long-term capital appreciation by investing in mid-cap U.S. equity investments that are believed to be undervalued or undiscovered by the marketplace. Although the Fund will invest primarily in publicly traded U.S. securities, including real estate investment trusts, it may invest in foreign securities, including securities of issuers in emerging countries or economies and securities quoted in foreign currencies. The Fund may also invest in the aggregate up to 20% of its total net assets in companies with public stock market capitalizations outside the range of companies constituting the Russell Midcap® Value Index at the time of investment and in fixed income securities, such as government, corporate and bank debt obligations.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Value Equity Investment Team discusses the Goldman Sachs Mid Cap Value Fund’s (the “Fund”) performance and positioning for the six-month period ended February 29, 2016 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, Service, IR, R and R6 Shares generated cumulative total returns, without sales charges, of -11.95%, -12.29%, -11.77%, -12.00%, -11.84%, -12.06% and -11.78%, respectively. These returns compare to the -5.17% cumulative total return of the Fund’s benchmark, the Russell Midcap® Value Index (with dividends reinvested) (the “Russell Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | Stock selection overall detracted from the Fund’s performance relative to the Russell Index during the Reporting Period. Sector allocation as a whole also detracted, albeit much more modestly, from the Fund’s results. |

| Q | | Which equity market sectors most significantly affected Fund performance? |

| A | | Detracting from the Fund’s performance most relative to the Russell Index was stock selection in the financials, industrials and information technology sectors. The only two sectors to contribute positively to the Fund’s relative results during the Reporting Period were energy and consumer staples, where effective stock selection was the primary driver. Having an underweighted allocation to energy, which was the weakest performing sector in the Russell Index during the Reporting Period, and having an overweighted allocation to consumer staples, which was the second best performing sector in the Russell Index during the Reporting Period, also buoyed the Fund’s relative results. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to its benchmark index were positions in car rental company Hertz Global Holdings, nitrogen-based fertilizer producer and distributor CF Industries and insurance and retirement company Lincoln National. |