UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| Caroline Kraus, Esq. | Copies to: | |

| Goldman Sachs & Co. LLC | Geoffrey R.T. Kenyon, Esq. | |

| 200 West Street | Dechert LLP | |

| New York, New York 10282 | 100 Oliver Street | |

| 40th Floor | ||

| Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code:(312) 655-4400

Date of fiscal year end: December 31

Date of reporting period: December 31, 2018

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| Annual Report | December 31, 2018 | |||

Fund of Funds Portfolios | ||||

Balanced Strategy | ||||

Equity Growth Strategy | ||||

Growth and Income Strategy | ||||

Growth Strategy | ||||

Satellite Strategies | ||||

It is our intention that beginning on January 1, 2021, paper copies of the Portfolios’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from a Portfolio or from your financial intermediary. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. At any time, you may elect to receive reports and certain communications from a Portfolio electronically by calling the applicable toll-free number below or by contacting your financial intermediary.

You may elect to receive all future shareholder reports in paper free of charge. If you hold shares of a Portfolio directly with the Portfolio’s transfer agent, you can inform the transfer agent that you wish to receive paper copies of reports by callingtoll-free 800-621-2550 for Institutional, Service, Class R6 and Class P shareholders or800-526-7384 for all other shareholders. If you hold shares of a Portfolio through a financial intermediary, please contact your financial intermediary to make this election. Your election to receive reports in paper will apply to all Goldman Sachs Funds held in your account if you invest through your financial intermediary or all Goldman Sachs Funds held with a Portfolio’s transfer agent if you invest directly with the transfer agent.

Goldman Sachs Fund of Funds Portfolios

| ∎ | BALANCED STRATEGY |

| ∎ | EQUITY GROWTH STRATEGY |

| ∎ | GROWTH AND INCOME STRATEGY |

| ∎ | GROWTH STRATEGY |

| ∎ | SATELLITE STRATEGIES |

| 1 | ||||

| 4 | ||||

| 5 | ||||

| 38 | ||||

| 39 | ||||

| 53 | ||||

| 60 | ||||

| 68 | ||||

| 76 | ||||

| 84 | ||||

| 92 | ||||

| 100 | ||||

| 132 | ||||

| 133 | ||||

| NOT FDIC-INSURED | May Lose Value | No Bank Guarantee | ||

MARKET REVIEW

Fund of Funds Portfolios

The capital markets were influenced most during the 12 months ended December 31, 2018 (the “Reporting Period”) by economic data, central bank monetary policy, higher commodity prices and geopolitical events.

In the first quarter of 2018, when the Reporting Period began, global equity markets experienced their first pullback after rallying for eight consecutive calendar quarters. Global equity prices peaked during the last week of January 2018 before retreating on news of stronger than consensus expected U.S. wage growth data in early February. In addition to the wage growth data, which led investors to anticipate a faster pace of U.S. Federal Reserve (“Fed”) interest rate hikes, rising concerns about potential trade protectionism and worsening market sentiment about U.S. information technology stocks weighed on global equity prices. In the second half of March 2018, U.S. information technology stocks sold off due to investor concerns about data privacy. During the first calendar quarter overall, macroeconomic data moderated in the developed markets, particularly in Europe and Japan. Emerging markets equities generally outperformed their developed markets peers because of what many considered to be attractive valuations, because of the comparatively stronger economic data within emerging markets countries and because of higher commodity prices. In the fixed income markets, the10-year U.S. Treasury yield rose during the first quarter of 2018, driven by the Fed’s decision to raise interest rates at its March policy meeting as well as by a modest pickup in inflation and a higher than consensus expected U.S. fiscal deficit. The outcome of the Fed’s policy meeting was generally considered dovish by investors but was also in line with market expectations. (Dovish tends to imply lower interest rates; opposite of hawkish.) The U.S. dollar weakened relative to other major developed markets currencies during the first calendar quarter.

During the second quarter of 2018, developed markets equities generated positive returns, while emerging markets equities experienced broad-based weakness. Two large themes were at play: 1) divergence between U.S. economic growth compared to that of the rest of the world and 2) continued escalation of trade tensions. Within developed markets, U.S., U.K., European and Japanese equities rallied. U.K. export-driven stocks, in particular, benefited strongly from the depreciation of the British pound versus other major currencies. Meanwhile, emerging markets equities substantially underperformed developed markets stocks, as emerging markets’ economic growth slowed and disputes between the U.S. and China about trade tariffs soured investors’ appetite for emerging markets assets in general. Broad-based selling also contributed to the weakness of emerging markets stocks. Within fixed income, the10-year U.S. Treasury yield rose, as U.S. macroeconomic data remained relatively strong, inflation increased and crude oil prices rose. The U.S. dollar strengthened against major currencies, driven by comparatively better U.S. economic growth and tighter Fed monetary policy. The Mexican peso and euro were among those currencies experiencing some of the largest drops versus the U.S. dollar. Weakening appetite for emerging markets assets and the looming Mexican presidential election weighed on the Mexican peso, while slower Eurozone economic growth and a dovish European Central Bank pressured the euro. Meanwhile, moderating global economic growth and escalating trade tensions weighed on the prices of metals, such as copper, and the stronger U.S. dollar pushed down gold prices.

In the third quarter of 2018, global economic growth continued to moderate, especially outside of the U.S. At the same time, U.S.-China trade tensions escalated, leading to tariffs of $250 billion on U.S. imports from China. In terms of monetary policy, the Fed raised short-term interest rates at its September policy meeting and signaled one more hike in 2018. Global

1

MARKET REVIEW

equities overall posted gains during the third calendar quarter, driven by a rally in developed markets stocks. Within developed markets stocks, U.S. equities outperformed, recording one of their best performing quarters in five years due to strong corporate earnings and economic data. European equities retreated, as softer economic activity and concerns around Italy weighed on their performance. Japanese equities rallied on the back of a weakening Japanese yen. Meanwhile, emerging markets equities declined, primarily due to the negative performance of Chinese stocks. Regarding fixed income, the10-year U.S. Treasury yield rose in response to strong U.S. economic activity, which caused the market to price in additional Fed rate hikes. In Europe, the spread, or yield differential, between10-year Italian and German government bonds widened, reflecting higher risk premiums on Italian assets because of increased concerns about the Italian government’s budget. Also during the third quarter of 2018, the currencies of emerging markets countries with significant financing needs fell to their 2018 calendar year lows versus the U.S. dollar; the Turkish lira and Argentinian peso, as prime examples, were down 42% and 50%, respectively, between January 1 and August 31. Within commodities, higher U.S. interest rates and slowing Chinese economic growth dampened gold and copper prices.

In the fourth quarter of 2018, softer global economic data, which led to downward consensus expectations for corporate earnings growth, and the Fed’s less accommodative monetary policy weighed on global equity markets, driving a double-digit decline across most major equity indices. Within developed markets stocks, Japanese equities turned in the weakest performance, as cyclical stocks were pressured by decelerating global economic growth, and export-oriented stocks were hurt by a stronger Japanese yen. U.S. and European equities also experienced substantial losses. Despite weaker economic data from China, emerging markets equities outperformed developed markets equities during the fourth calendar quarter, thanks in large part to rallies in Brazilian and Indian stocks. Brazilian risk assets broadly benefited from renewed investor optimism about potentially market-friendly measures from its new government and relatively better economic data. Indian equities were helped by lower crude oil prices and improving macro data. Within fixed income, the10-year U.S. Treasury yield fell in response to a decline in U.S. inflation, driven by the drop in crude oil prices and signs of slowing U.S. economic growth. Yields of government bonds in other developed markets countries also fell but by a lesser magnitude. Investors revised downward their expectations for 2019 Fed monetary policy action from two short-term interest rate increases to no rate hike at all. The Fed, however, still projected two rate hikes during the 2019 calendar year. Within commodities, crude oil prices declined on market concerns about global economic growth and as oversupply led investors to unwind long positions. Regarding metals, copper prices fell, while gold prices rallied. As for currencies, the Japanese yen was the best performing major currency during the fourth quarter of 2018. The U.S. dollar strengthened overall versus most major currencies.

Looking Ahead

At the end of the Reporting Period, we emphasized three macro themes. First, we expected to see an elongated U.S. economic expansion in 2019, with U.S. economic growth slowing but remaining at above trend levels. Second, we expected to see renewed convergence in global economic growth, as the U.S. economy slows, the European economy stabilizes and emerging markets economic growth (outside of China) improves. Third, we saw attractive opportunities in the wake of the 2018 market downturn. In our view, valuations and investor expectations had adjusted significantly since the start of 2018, and we had become more positive about potential returns in the near term.

2

MARKET REVIEW

At the asset class level, we were positive on equities over the medium term. We believed a slowdown in U.S. economic growth, which could eventually reduce labor market pressures, had increased the likelihood at the margin of an elongation in the U.S. economic cycle. This, along with the 2018 equity market downturn, continued corporate earnings growth and global economic expansion, should support equity returns, in our view. As for fixed income, we remained bearish on government bonds. In our opinion, the elongated U.S. economic cycle is likely to lead to higher yields due to Fed interest rate hikes, and we expected a path that is more hawkish than what the market was pricing in at the end of the Reporting Period. Additionally, we considered credit spreads rather wide and expected to see some compression in the near term. Over the course of 2019, credit spreads are likely to tighten further, we believe. Finally, while we still thought emerging markets assets would likely outperform developed markets assets over the long term, deterioration in China’s economic growth has been worse than we expected. As a result, we decided to reduce the Portfolios’ allocation to emerging markets assets in the medium term because we believe there is increased uncertainty around the timing and magnitude of economic growth improvements for China.

3

GOLDMAN SACHS FUND OF FUNDS PORTFOLIOS

What Differentiates Goldman Sachs’

Approach to Asset Allocation?

We believe that strong investment results through asset allocation are best achieved through teams of experts working together on a global scale:

| ∎ | Goldman Sachs’ Global Portfolio Solutions Group determines the strategic and tactical asset allocations. The team is comprised of over 150* professionals with significant academic and practitioner experience. |

| ∎ | Goldman Sachs’ Portfolio Management Teams offer expert management of the mutual funds that are contained within each Portfolio. These same teams manage portfolios for institutional and high net worth investors. |

Goldman Sachs Asset Allocation Investment Process

Global Portfolio Solutions Group

Each Portfolio represents a diversified global portfolio on the efficient frontier.† The Portfolios differ in their long-term objective, and therefore, their asset allocation mix. The long-term strategic asset allocation is the primary source of risk and the corresponding primary determinant of total return. It therefore represents an anchor, or neutral starting point, from which tactical asset allocation decisions are made.

Global Portfolio Solutions Group

For each Portfolio, the long-term strategic asset allocation is adjusted through a tactical investment process that seeks to react to and capitalize on changes in the market, the economic cycle, and macroeconomic environment. Within each strategy, we shift assets away from the strategic allocation by over and underweighting certain asset classes and by taking long or short positions in specific sectors, regions and countries. Using a proprietary fundamental analysis and portfolio construction process, the team develops views based on its current market and economic outlook across asset classes like global developed equity, emerging market equity, investment grade and non-investment grade fixed income, and currency markets.

| *As | of December 2018. |

| †Portfolios | on the efficient frontier are optimal in both the sense that they offer maximal expected return for some given level of risk and minimal risk for some given level of expected return. The efficient frontier is the line created from the risk-reward graph, comprised of optimal portfolios. The optimal portfolios plotted along the curve have the highest expected return possible for the given amount of risk. |

4

PORTFOLIO RESULTS

Fund of Funds Portfolios

Investment Objectives

The Goldman Sachs Balanced Strategy Portfolio seeks current income and long-term capital appreciation. The Goldman Sachs Equity Growth Strategy Portfolio seeks long-term capital appreciation. The Goldman Sachs Growth and Income Strategy Portfolio seeks long-term capital appreciation and current income. The Goldman Sachs Growth Strategy Portfolio seeks long-term capital appreciation and, secondarily, current income.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Global Portfolio Solutions Team discusses the performance and positioning of the Goldman Sachs Fund of Funds Portfolios — Asset Allocation (the “Portfolios”) for the12-month period ended December 31, 2018 (the “Reporting Period”).

| Q | How did the Portfolios perform during the Reporting Period? |

| A | Goldman Sachs Balanced Strategy Portfolio — During the Reporting Period, the Balanced Strategy Portfolio’s Class A, C, Institutional, Service, Investor, R and R6 Shares generated average annual total returns of-6.90%,-7.58%,-6.53%,-6.93%,-6.61%,-7.07% and-6.52%, respectively. This compares to the-2.57% average annual total return of the Portfolio’s blended benchmark, which is composed 60% of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (“Bloomberg Barclays Global Index”) and 40% of the MSCI All Country World Index (Net, USD, Unhedged) (“MSCI ACWI Index”), during the same period. |

| The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated average annual total returns of 1.76% and-9.41%, respectively, during the Reporting Period. |

| For the period since their inception on April 17, 2018 through December 31, 2018, the Portfolio’s Class P Shares generated a cumulative total return of-6.67% compared to the-2.28% cumulative total return of the blended benchmark. The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated cumulative total returns of 1.93% and-10.45%, respectively, during the same period. |

| Goldman Sachs Equity Growth Strategy Portfolio — During the Reporting Period, the Equity Growth Strategy Portfolio’s Class A, C, Institutional, Service, Investor, R and R6 Shares generated average annual total returns of-11.40%,-12.04%,-11.07%,-11.48%,-11.18%,-11.63% and-11.00%, respectively. This compares to the -9.41% average annual total return of the Portfolio’s benchmark, the MSCI ACWI Index, during the same period. |

| For the period since their inception on April 17, 2018 through December 31, 2018, the Portfolio’s Class P Shares generated a cumulative total return of-12.80% compared to the-10.45% cumulative total return of the Portfolio’s benchmark. |

| Goldman Sachs Growth and Income Strategy Portfolio — During the Reporting Period, the Growth and Income Strategy Portfolio’s Class A, C, Institutional, Service, Investor, R and R6 Shares generated average annual total returns of-8.94%,-9.62%,-8.63%,-9.00%,-8.68%,-9.10% and-8.61%, respectively. This compares to the-4.81% average annual total return of the Portfolio’s blended benchmark, which is composed 40% of the Bloomberg Barclays Global Index and 60% of the MSCI ACWI Index, during the same period. |

| The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated average annual total returns of 1.76% and-9.41%, respectively, during the Reporting Period. |

| For the period since their inception on April 17, 2018 through December 31, 2018, the Portfolio’s Class P Shares generated a cumulative total return of-9.29% compared to the-4.61% cumulative total return of the blended benchmark. The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated cumulative total returns of 1.93% and-10.45%, respectively, during the same period. |

Goldman Sachs Growth Strategy Portfolio — During the Reporting Period, the Growth Strategy Portfolio’s Class A, |

5

PORTFOLIO RESULTS

C, Institutional, Service, Investor, R and R6 Shares generated average annual total returns of-10.98%,-11.58%,-10.65%,-11.06%,-10.74%,-11.18% and-10.55%, respectively. This compares to the-7.09% average annual total return of the Portfolio’s blended benchmark, which is composed 80% of the MSCI ACWI Index and 20% of the Bloomberg Barclays Global Index, during the same period. |

| The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated average annual total returns of 1.76% and-9.41%, respectively, during the Reporting Period. |

| For the period since their inception on April 17, 2018 through December 31, 2018, the Portfolio’s Class P Shares generated a cumulative total return of -11.39% compared to the-6.99% cumulative total return of the blended benchmark. The components of the Portfolio’s blended benchmark, the Bloomberg Barclays Global Index and the MSCI ACWI Index, generated cumulative total returns of 1.93% and-10.45%, respectively, during the same period. |

| Q | What key factors were responsible for the Portfolios’ performance during the Reporting Period? |

| A | The Portfolios seek to achieve their respective investment objectives by investing mainly in a combination of underlying funds and exchange-traded funds (“ETFs”) (collectively, the “Underlying Funds”). Some of the Portfolios’ Underlying Funds invest primarily in fixed income or money market instruments (the “Underlying Fixed Income Funds”); some of the Underlying Funds invest primarily in equity securities (the “Underlying Equity Funds”); and other Underlying Funds invest dynamically across equity, fixed income, commodity and other markets using various strategies including a managed-volatility or trend-following approach (the “Underlying Dynamic Funds”). |

| Performance is driven by four sources of return: long-term strategic asset allocation, medium-term cycle-aware allocation, short-term tactical allocation and excess returns from investments in Underlying Funds. Strategic asset allocation is the process by which we seek to budget or allocate portfolio risk, as opposed to capital, across a set of asset allocation risk factors, including but not limited to, equity, interest rate, emerging markets, credit, momentum and active risk. The resulting strategic asset allocations are implemented using a range ofbottom-up security selection strategies across equity, fixed income and dynamic asset classes, which may utilize fundamental or quantitative investment techniques. We then incorporate our medium-term cycle-aware views and short-term tactical views into the Portfolios in order to react to changes in the economic cycle and the markets, respectively. Each Portfolio’s positioning may therefore change over time based on medium- and short-term market views on dislocations and attractive investment opportunities. These views may impact the relative weighting across asset classes, the allocation to geographies, sectors and industries as well as the Portfolios’ duration and sensitivity to inflation. (Duration is a measure of a portfolio’s sensitivity to changes in interest rates.) |

| During the Reporting Period, the Portfolios generated negative returns on an absolute basis, with those having greater equity exposure producing greater negative results. In addition, all four Portfolios underperformed their respective benchmark indices.* Our long-term strategic asset allocation generally detracted most. The Portfolios were also hurt overall by our medium-term cycle-aware views and by security selection within the Underlying Funds. The contribution from our short-term tactical decisions was mixed. |

| Strategic asset allocation was the main detractor from performance for three of the four Portfolios — the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio. The impact of strategic asset allocation on the performance of the Goldman Sachs Equity Growth Strategy Portfolio was rather neutral overall. Negative performance was driven by strategic allocations to emerging markets assets. Strategic allocations to emerging markets equities detracted from the performance of all four Portfolios, while strategic allocations to U.S.-dollar denominated emerging markets debt and local currency emerging markets debt detracted from the performance of all Portfolios, except the Goldman Sachs Equity Growth Strategy Portfolio. Emerging markets assets generally struggled during the Reporting Period due to weaker than market expected global economic growth data, rising trade tensions between the U.S. and China and a stronger U.S. dollar. Additionally, strategic allocations to internationalsmall-cap equities detracted from the performance of the |

| *As | measured by Institutional Shares. |

6

PORTFOLIO RESULTS

Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio, assmall-cap stocks underperformedlarge-cap stocks during the Reporting Period amid global economic growth concerns. Small-cap stocks tend to be more economically sensitive thanlarge-cap stocks. On the positive side, strategic allocations to global infrastructure and global real estate contributed positively to the performance of these three Portfolios, as the equity marketsell-off led investors to seek relative safety in higher-yielding equity asset classes. |

| Our medium-term cycle-aware views detracted from the returns of all four Portfolios during the Reporting Period. Within equities, our view that the Portfolios should hold long positions in emerging markets equities versus developed markets equities hurt performance, as developed markets equities outperformed emerging markets equities on the back of weaker than market expected economic growth in the emerging markets, a stronger U.S. dollar and spillover effects from countries with economic imbalances, such as Argentina and Turkey. Within fixed income, we held the view that the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio should each have a short duration bias, which was expressed through a short position in long-maturity German government bonds and short positions in specific segments of the U.S. Treasury yield curve. (Yield curve is a spectrum of interest rates based on maturities of varying lengths. The Goldman Sachs Equity Growth Strategy Portfolio did not adopt any of our fixed income views as it is anall-equity portfolio.) The short position in long-maturity German government bonds detracted from the Portfolios’ performance as German yields fell during the Reporting Period due to slower European economic growth and Italian political risk. A short position in thetwo-year segment of the U.S. Treasury yield curve added marginally, partially offsetting these negative results, as U.S. longer-term interest rates rose. Elsewhere within fixed income, the Portfolios were hampered by their exposure to local emerging markets debt versus U.S. high yield corporate bonds. We established this positioning in May 2018 based on our view that credit spreads, which typically start to widen before an equity market peak, would be a headwind for U.S. high yield corporate bonds in the near term. (Credit spreads are yield differentials between corporate bonds and U.S. Treasury securities of comparable maturity.) Although this view contributed positively during the fourth quarter of 2018, it detracted from the performance of the Portfolios during the Reporting Period overall as U.S. high yield corporate bonds outperformed local emerging markets debt. |

| Our short-term tactical views, which seek to take advantage of what we consider short-term market mispricing, had mixed results during the Reporting Period. Although they added to the performance of the Goldman Sachs Equity Growth Strategy Portfolio, they detracted from the performance of the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio. For these three Portfolios, we used a single implementation vehicle to express our short-term tactical views — the Goldman Sachs Tactical Exposure Fund (the “Underlying Tactical Fund”) — which underperformed its benchmark index during the Reporting Period and therefore detracted from the Portfolios’ returns. That said, within the Goldman Sachs Equity Growth Strategy Portfolio, the impact of our country-specific views was mixed. Overall, our view to hold long positions in certain developed markets stocks, including Singaporean equities and Europeanlarge-cap stocks, and short positions in certain emerging markets stocks, such as South African and Mexican equities, added to the Portfolio’s performance. This was offset by country-specific long positions in emerging markets equities, which detracted from results, as emerging markets assets were broadly challenged during the Reporting Period. |

| Security selection within the Underlying Funds detracted from the returns of all four of the Portfolios during the Reporting Period, especially the Goldman Sachs Equity Growth Strategy Portfolio because of its relatively higher proportion of equity assets. |

| Q | How did the Portfolios’ Underlying Funds perform relative to their respective benchmark indices during the Reporting Period? |

| A | Among Underlying Fixed Income Funds, the Goldman Sachs Local Emerging Markets Debt Fund underperformed its benchmark index most during the Reporting Period. The Goldman Sachs Emerging Markets Debt Fund, the Goldman Sachs Global Income Fund, the Goldman Sachs High Yield Floating Rate Fund and the Goldman Sachs High Yield Fund also lagged their respective benchmark indices. In addition, the Goldman Sachs Access High Yield Corporate Bond ETF underperformed its benchmark index. On the positive side, the Goldman Sachs Access Investment Grade Corporate Bond ETF outperformed its benchmark index. Among Underlying Equity Funds, the Goldman Sachs Large Cap Growth Insights Fund underperformed its benchmark index |

7

PORTFOLIO RESULTS

most during the Reporting Period. Also, the Goldman Sachs Large Cap Value Insights Fund, the Goldman Sachs ActiveBeta Emerging Markets Equity ETF, the Goldman Sachs International Small Cap Insights Fund and the Goldman Sachs Emerging Markets Equity Insights Fund all underperformed their respective benchmark indices. Conversely, the Goldman Sachs Small Cap Equity Insights Fund outperformed its benchmark index, while the Goldman Sachs ActiveBeta U.S. Large Cap Equity ETF and the Goldman Sachs ActiveBeta International Equity ETF were essentially flat versus their respective benchmark indices. Among Underlying Funds that invest in real assets, the Goldman Sachs Real Estate Securities Fund outperformed its benchmark index and the Goldman Sachs Global Infrastructure Fund underperformed its benchmark index during the Reporting Period. |

| Q | How did the Portfolios use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, all four Portfolios used derivatives for passive replication of asset classes. Specifically, each of the Portfolios held a strategic position in S&P 500®Index futures (negative impact). |

| The primary purpose of derivatives in the Portfolios was to express medium-term cycle-aware views across equities and fixed income. The Goldman Sachs Equity Growth Strategy Portfolio was the only Portfolio to use derivatives to express our short-term tactical views across developed and emerging markets equities. The Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio used a single implementation vehicle to express our short-term tactical views — the Underlying Tactical Fund. |

| Within equities, the Goldman Sachs Equity Growth Strategy Portfolio employed equity index futures to establish tactical short positions in Australian equities and U.K. large cap equities (both had a negative impact) and in Mexican equities and South African equities (both had a positive impact). The Portfolio also used equity index futures to establish tactical long positions in Singaporean equities and European bank stocks (both had a positive impact). The Portfolio utilized equity index futures to take tactical long positions in Chinese onshore- and offshore- listed equities, emerging markets stocks, European high-dividend equities, Japanese equities and South Korean equities (all had a negative impact). Over the course of the Reporting Period, the Portfolio used both long and short positioning in European equity index futures and international developed markets equity index futures to express our tactical views (both had a negative impact). Furthermore, during the Reporting Period, the Goldman Sachs Equity Growth Strategy Portfolio used equity call options to adopt long positions in emerging markets equities and European equities (both had a negative impact) and U.S.large-cap stocks and Japanese equities (both had a positive impact). |

| Within fixed income, the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio used interest rate futures to express our medium-term cycle-aware views on the U.S. Treasury yield curve (positive impact) and on long-term German interest rates (negative impact). (The Goldman Sachs Equity Growth Strategy Portfolio did not adopt any of our fixed income views as it is anall-equity portfolio.) |

| The Portfolios also used forward foreign currency exchange contracts within a foreign currency hedging strategy (positive impact), which seeks to manage the risk associated with investing innon-U.S. currencies. |

| During the Reporting Period overall, some of the Portfolios’ Underlying Funds, including the Underlying Tactical Fund, used derivatives to apply their active investment views with greater versatility and potentially to afford greater risk management precision. As market conditions warranted during the Reporting Period, some of these Underlying Funds engaged in forward foreign currency exchange contracts, financial futures contracts, options, swap contracts and structured securities to attempt to enhance portfolio return and for hedging purposes. |

| Q | What changes did you make during the Reporting Period within the Portfolios? |

| A | In May 2018, we made changes to the strategic allocations of three of the four Portfolios — the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio. Specifically, we added strategic allocations to the Goldman Sachs Access Investment Grade Corporate Bond ETF and the Goldman Sachs Access High Yield Corporate Bond ETF. Additionally, we added strategic allocations to a volatility selling strategy. (Our volatility selling strategy seeks to benefit from the difference between implied volatility (i.e., expectations of future volatility) and realized volatility (i.e., historical volatility) in equity markets.) In addition, we implemented a foreign currency hedging strategy. |

8

PORTFOLIO RESULTS

| In October 2018, we made changes to the medium-term cycle aware views of all four Portfolios, wherein we began reducing risk related to the emerging markets. More specifically, we decreased the Portfolios’ exposure to emerging markets equities versus developed markets equities. In three of the Portfolios — the Goldman Sachs Balanced Strategy Portfolio, the Goldman Sachs Growth and Income Strategy Portfolio and the Goldman Sachs Growth Strategy Portfolio — we reduced exposure to local emerging markets debt relative to U.S. high yield corporate bonds. By the end of the Reporting Period, we had partially reduced the Portfolios’ overweight positions compared to their respective benchmarks in emerging markets assets. |

| Q | Were there any changes to the Portfolios’ portfolio management team during the Reporting Period? |

| A | Effective June 21, 2018, Edward J. Tostanoski III no longer served as a portfolio manager of the Portfolios. By design, all investment decisions for the Portfolios are performed within aco-lead or team structure, with multiple subject matter experts. This strategic decision making has been the cornerstone of our approach and ensures continuity in the Portfolios. At the end of the Reporting Period, the portfolio managers for the Portfolios were Raymond Chan and Christopher Lvoff. (On February 19, 2019, after the end of the Reporting Period, Raymond Chan no longer served as a portfolio manager for the Portfolios. At the same time, Neill Nuttall became a portfolio manager for the Portfolios, joining Christopher Lvoff.) |

9

FUND BASICS

Balanced Strategy

as of December 31, 2018

| PERFORMANCE REVIEW |

| |||||||||||||||||

| January 1, 2018– December 31, 2018 | Portfolio Total Return (based on NAV)1 | Balanced Strategy Composite Index2 | Bloomberg Barclays Global Index | MSCI ACWI Index | ||||||||||||||

Class A | -6.90 | % | -2.57 | % | 1.76 | % | -9.41 | % | ||||||||||

Class C | -7.58 | -2.57 | 1.76 | -9.41 | ||||||||||||||

Institutional | -6.53 | -2.57 | 1.76 | -9.41 | ||||||||||||||

Service | -6.93 | -2.57 | 1.76 | -9.41 | ||||||||||||||

Investor | -6.61 | -2.57 | 1.76 | -9.41 | ||||||||||||||

Class R | -7.07 | -2.57 | 1.76 | -9.41 | ||||||||||||||

Class R6 | -6.52 | -2.57 | 1.76 | -9.41 | ||||||||||||||

April 17, 2018– | ||||||||||||||||||

Class P | -6.67 | % | -2.28 | % | 1.93 | % | -10.45 | % | ||||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Portfolio(ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance assumes the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Balanced Strategy Composite Index (“Balanced Composite”) is a composite representation prepared by the Investment Adviser of the performance of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. The Balanced Composite is comprised of a blend of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (“Bloomberg Barclays Global Index”) (60%) and the MSCI All Country World Index (Net, USD, Unhedged) (“MSCI® ACWI Index”) (40%). The Bloomberg Barclays Global Index is an unmanaged index, provides a broad-based measure of the global investment gradefixed-rate debt markets and covers the most liquid portion of the global investment gradefixed-rate bond market, including government, credit and collateralized securities. The index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The MSCI® ACWI Index is a freefloat-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI® ACWI Index consists of 47 country indices comprising 23 developed and 24 emerging market country indices. The developed market country indices included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indices are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates. The index figures do not include any deduction for fees or expenses. It is not possible to invest directly in an unmanaged index. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

10

FUND BASICS

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||

| For the period ended 12/31/18 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||

Class A | -12.00% | 0.84 | % | 4.71 | % | 3.76 | % | 1/2/98 | ||||||||||

Class C | -8.53 | 1.23 | 4.51 | 3.27 | 1/2/98 | |||||||||||||

Institutional | -6.53 | 2.40 | 5.73 | 4.46 | 1/2/98 | |||||||||||||

Service | -6.93 | 2.06 | 5.28 | 3.98 | 1/2/98 | |||||||||||||

Investor | -6.61 | 2.26 | 5.56 | 2.85 | 11/30/07 | |||||||||||||

Class P | N/A | N/A | N/A | -6.67 | 4/17/18 | |||||||||||||

Class R | -7.07 | 1.78 | 5.07 | 2.37 | 11/30/07 | |||||||||||||

Class R6 | -6.52 | N/A | N/A | 2.21 | 7/31/15 | |||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendarquarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initialsales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service, Investor, Class P, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| EXPENSE RATIOS4 |

| |||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.28 | % | 1.34 | % | ||||||

| Class C | 2.03 | 2.09 | ||||||||

| Institutional | 0.89 | 0.95 | ||||||||

| Service | 1.39 | 1.45 | ||||||||

| Investor | 1.03 | 1.09 | ||||||||

| Class P | 0.88 | 0.94 | ||||||||

| Class R | 1.53 | 1.59 | ||||||||

| Class R6 | 0.88 | 0.94 | ||||||||

| 4 | The expense ratios of the Portfolio, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Portfolio and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to contractual arrangements, the Portfolio’s waivers and/or expense limitations will remain in place through at least April 30, 2019, and prior to such date, the Investment Adviser may not terminate the arrangements without the approval of the Portfolio’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

11

FUND BASICS

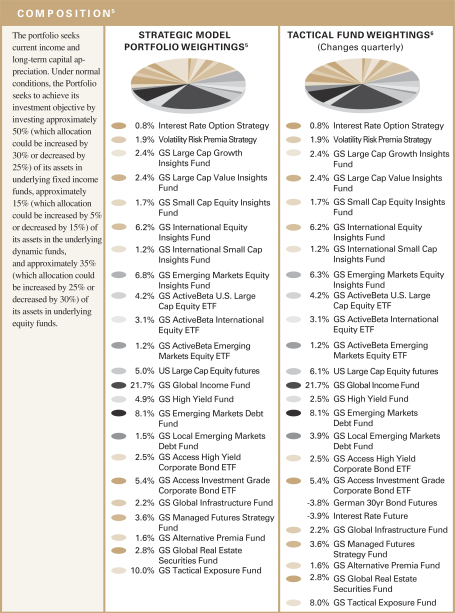

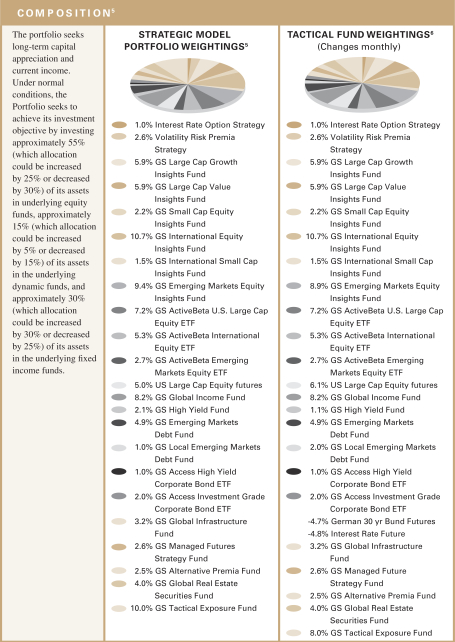

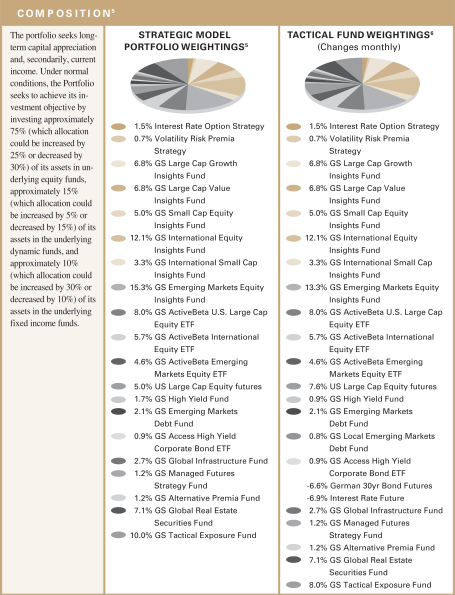

| 5 | Strategic allocation is the process of determining the areas of the global markets in which to invest, and in what long-term proportion, for each underlying fund. Our global approach attempts to generate strong long-term returns across geographies and asset classes, and is determined through a careful review of market opportunities and risk/return tradeoffs. On a monthly basis or as needed, we shift assets around the strategic allocation, over and under-weighting asset classes and countries relative to the neutral starting point, seeking to benefit from changing short-term conditions in global capital markets. This is called tactical asset allocation. |

| 6 | Generally, tactical fund weightings are rebalanced approximately monthly, but they may be rebalanced more or less frequently at the discretion of the Investment Adviser based on the market environment and its macro views. The weightings in the chart above reflect the allocations as of December 31, 2018. Actual Fund weighting in the Portfolio may differ from the figures shown above due to rounding, differences in returns of the Underlying Funds, or both. The above figures are not indicative of future allocations. |

12

FUND BASICS

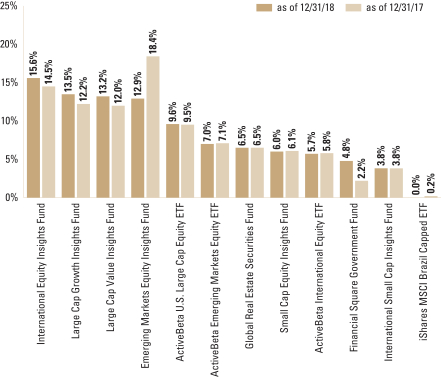

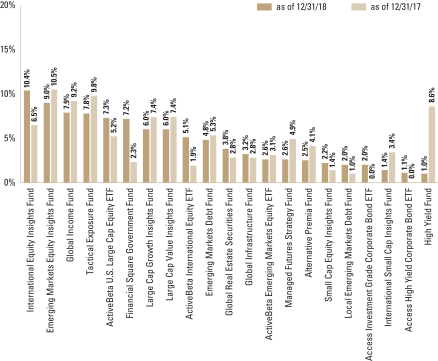

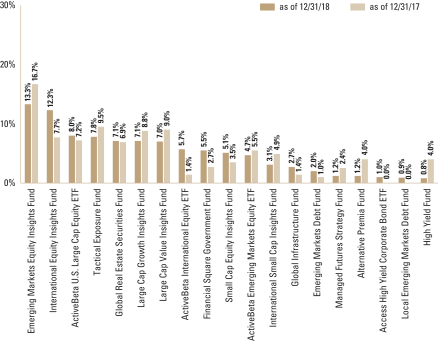

| OVERALL UNDERLYING FUND WEIGHTINGS7 |

| Percentage of Net Assets |

| 7 | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each underlying fund reflects the value of that underlying fund as a percentage of net assets of the Portfolio. Figures in the above graph may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. The graph depicts the Portfolio’s investments but may not represent the Portfolio’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

13

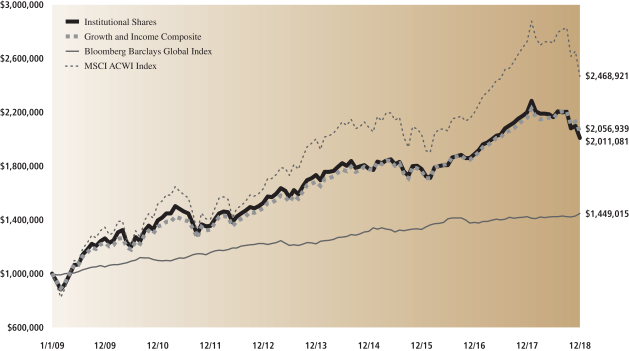

GOLDMAN SACHS BALANCED STRATEGY PORTFOLIO

Performance Summary

December 31, 2018

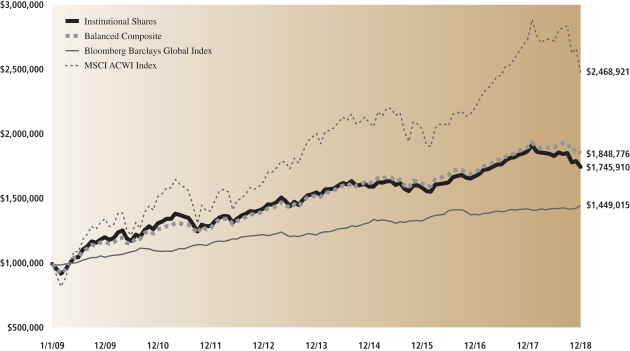

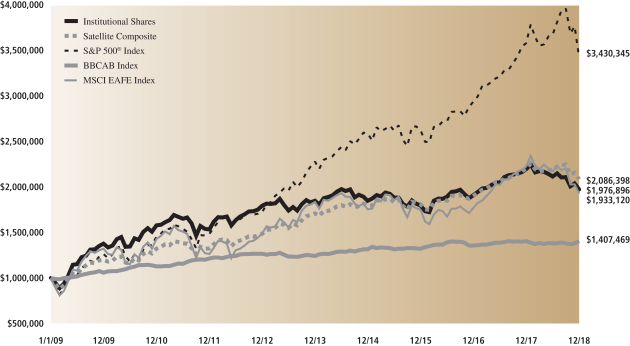

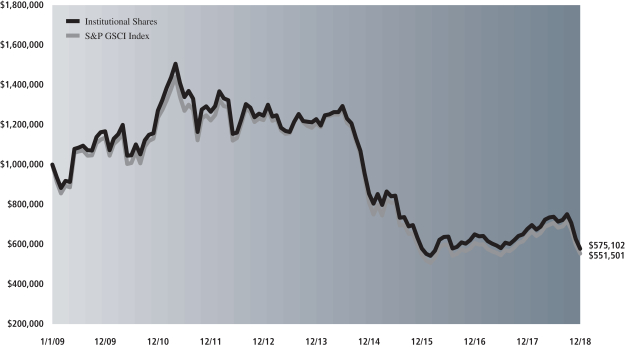

The following graph shows the value, as of December 31, 2018, of a $1,000,000 investment made on January 1, 2009 in Institutional Shares at NAV. For comparative purposes, the performance of the Portfolio’s benchmarks, the Balanced Strategy Composite Index (the “Balanced Composite”), which is comprised of 60% of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (the “Bloomberg Barclays Global Index”) and 40% of the MSCI® All Country World Index (Net, USD, Unhedged) (the “MSCI ACWI Index”), the Bloomberg Barclays Global Index and the MSCI ACWI Index (each with distributions reinvested), are shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations currently in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance of Class A, Class C, Service, Investor, Class P, Class R and Class R6 Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding underlying fund selection and allocations among them, other factors may affect Portfolio performance. These factors include, but are not limited to, Portfolio operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Portfolio.

| Balanced Strategy Portfolio’s 10 Year Performance |

Performance of a $1,000,000 investment, with distributions reinvested, from January 1, 2009 through December 31, 2018.

| Average Annual Total Return through December 31, 2018 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced January 2, 1998) | ||||||||||||||

Excluding sales charges | -6.90% | 1.99% | 5.30% | 4.04% | ||||||||||

Including sales charges | -12.00% | 0.84% | 4.71% | 3.76% | ||||||||||

| ||||||||||||||

Class C (Commenced January 2, 1998) | ||||||||||||||

Excluding contingent deferred sales charges | -7.58% | 1.23% | 4.51% | 3.27% | ||||||||||

Including contingent deferred sales charges | -8.53% | 1.23% | 4.51% | 3.27% | ||||||||||

| ||||||||||||||

Institutional (Commenced January 2, 1998) | -6.53% | 2.40% | 5.73% | 4.46% | ||||||||||

| ||||||||||||||

Service (Commenced January 2, 1998) | -6.93% | 2.06% | 5.28% | 3.98% | ||||||||||

| ||||||||||||||

Investor (Commenced November 30, 2007) | -6.61% | 2.26% | 5.56% | 2.85% | ||||||||||

| ||||||||||||||

Class P (Commenced April 17, 2018) | N/A | N/A | N/A | -6.67%* | ||||||||||

| ||||||||||||||

Class R (Commenced November 30, 2007) | -7.07% | 1.78% | 5.07% | 2.37% | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | -6.52% | N/A | N/A | 2.21% | ||||||||||

| ||||||||||||||

| * | Total return for periods of less than one year represents cumulative total return. |

14

FUND BASICS

Equity Growth Strategy

as of December 31, 2018

| PERFORMANCE REVIEW |

| |||||||||

| January 1, 2018–December 31, 2018 | Portfolio Total Return (based on NAV)1 | MSCI® ACWI Index2 | ||||||||

Class A | -11.40 | % | -9.41 | % | ||||||

Class C | -12.04 | -9.41 | ||||||||

Institutional | -11.07 | -9.41 | ||||||||

Service | -11.48 | -9.41 | ||||||||

Investor | -11.18 | -9.41 | ||||||||

Class R | -11.63 | -9.41 | ||||||||

Class R6 | -11.00 | -9.41 | ||||||||

April 17, 2018–December 31, 2018 | ||||||||||

Class P | -12.80 | % | -10.45 | % | ||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Portfolio(ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance assumes the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Portfolio’s benchmark is the MSCI All Country World Index (Net, USD, Unhedged) (“MSCI® ACWI Index”). The MSCI® ACWI Index is a freefloat-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI® ACWI Index consists of 47 country indices comprising 23 developed and 24 emerging market country indices. The developed market country indices included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indices are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates. The index figures do not include any deduction for fees or expenses. It is not possible to invest directly in an unmanaged index. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

15

FUND BASICS

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 12/31/18 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

Class A | -16.29 | % | 3.19 | % | 8.57 | % | 4.37 | % | 1/2/98 | |||||||||||

Class C | -12.92 | 3.59 | 8.38 | 3.88 | 1/2/98 | |||||||||||||||

Institutional | -11.07 | 4.78 | 9.62 | 5.05 | 1/2/98 | |||||||||||||||

Service | -11.48 | 4.26 | 9.08 | 4.54 | 1/2/98 | |||||||||||||||

Investor | -11.18 | 4.63 | 9.47 | 3.09 | 11/30/07 | |||||||||||||||

Class P | N/A | N/A | N/A | -12.80 | 4/17/18 | |||||||||||||||

Class R | -11.63 | 4.11 | 8.96 | 2.62 | 11/30/07 | |||||||||||||||

Class R6 | -11.00 | N/A | N/A | 4.41 | 7/31/15 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendarquarter-end.They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service,Investor, Class P, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| EXPENSE RATIOS4 |

| |||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

Class A | 0.83 | % | 0.92 | % | ||||||

Class C | 1.58 | 1.67 | ||||||||

Institutional | 0.44 | 0.53 | ||||||||

Service | 0.94 | 1.03 | ||||||||

Investor | 0.58 | 0.67 | ||||||||

Class P | 0.43 | 0.52 | ||||||||

Class R | 1.08 | 1.17 | ||||||||

Class R6 | 0.43 | 0.52 | ||||||||

| 4 | The expense ratios of the Portfolio, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Portfolio and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to contractual arrangements, the Portfolio’s waivers and/or expense limitations will remain in place through at least April 30, 2019, and prior to such date, the Investment Adviser may not terminate the arrangements without the approval of the Portfolio’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

16

FUND BASICS

| 5 | Strategic allocation is the process of determining the areas of the global markets in which to invest, and in what long-term proportion, for each underlying fund. Our global approach attempts to generate strong long-term returns across geographies and asset classes, and is determined through a careful review of market opportunities and risk/return tradeoffs. On a monthly basis or as needed, we shift assets around the strategic allocation, over and under-weighting asset classes and countries relative to the neutral starting point, seeking to benefit from changing short-term conditions in global capital markets. This is called tactical asset allocation. |

| 6 | Generally, tactical fund weightings are rebalanced approximately monthly, but they may be rebalanced more or less frequently at the discretion of the Investment Adviser based on the market environment and its macro views. The weightings in the chart above reflect the allocations as of December 31, 2018. Actual underlying fund weighting in the Portfolio may differ from the figures shown above due to rounding, differences in returns of the underlying funds, or both. The above figures are not indicative of future allocations. |

17

FUND BASICS

| OVERALL UNDERLYING FUND WEIGHTINGS7 |

| Percentage of Net Assets |

| 7 | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each underlying fund reflects the value of that underlying fund as a percentage of net assets of the Portfolio. Figures in the above graph may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. The graph depicts the Portfolio’s investments but may not represent the Portfolio’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

18

GOLDMAN SACHS EQUITY GROWTH STRATEGY PORTFOLIO

Performance Summary

December 31, 2018

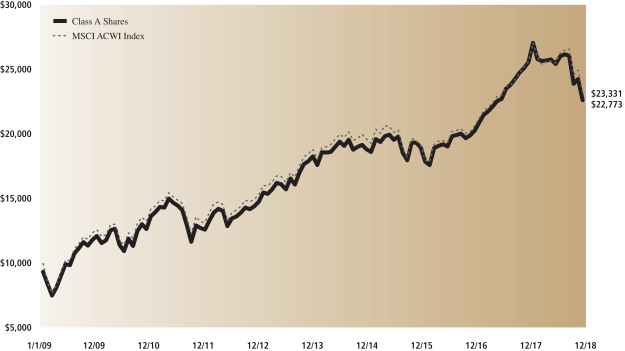

The following graph shows the value, as of December 31, 2018, of a $10,000 investment made on January 1, 2009 in Class A Shares (with the maximum sales charge of 5.5%). For comparative purposes, the performance of the Portfolio’s benchmark, the MSCI® All Country World Index (Net, USD, Unhedged) (“MSCI ACWI Index”) (with distributions reinvested), is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations currently in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance of Class C, Institutional, Service, Investor, Class P, Class R and Class R6 Shares will vary from Class A Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding underlying fund selection and allocations among them, other factors may affect Portfolio performance. These factors include, but are not limited to, Portfolio operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Portfolio.

| Equity Growth Strategy Portfolio’s 10 Year Performance |

Performance of a $10,000 investment, with distributions reinvested, from January 1, 2009 through December 31, 2018.

| Average Annual Total Return through December 31, 2018 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced January 2, 1998) | ||||||||||||||

Excluding sales charges | -11.40% | 4.36% | 9.19% | 4.65% | ||||||||||

Including sales charges | -16.29% | 3.19% | 8.57% | 4.37% | ||||||||||

| ||||||||||||||

Class C (Commenced January 2, 1998) | ||||||||||||||

Excluding contingent deferred sales charges | -12.04% | 3.59% | 8.38% | 3.88% | ||||||||||

Including contingent deferred sales charges | -12.92% | 3.59% | 8.38% | 3.88% | ||||||||||

| ||||||||||||||

Institutional (Commenced January 2, 1998) | -11.07% | 4.78% | 9.62% | 5.05% | ||||||||||

| ||||||||||||||

Service (Commenced January 2, 1998) | -11.48% | 4.26% | 9.08% | 4.54% | ||||||||||

| ||||||||||||||

Investor (Commenced November 30, 2007) | -11.18% | 4.63% | 9.47% | 3.09% | ||||||||||

| ||||||||||||||

Class P (Commenced April 17, 2018) | N/A | N/A | N/A | -12.80%* | ||||||||||

| ||||||||||||||

Class R (Commenced November 30, 2007) | -11.63% | 4.11% | 8.96% | 2.62% | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | -11.00% | N/A | N/A | 4.41% | ||||||||||

| ||||||||||||||

| * | Total return for periods of less than one year represents cumulative total return. |

19

FUND BASICS

Growth and Income Strategy

as of December 31, 2018

| PERFORMANCE REVIEW |

| |||||||||||||||||

| January 1, 2018– December 31, 2018 | Portfolio Total Return (based on NAV)1 | Growth and Income Composite Index2 | Bloomberg Barclays Global Index | MSCI ACWI Index | ||||||||||||||

Class A | -8.94 | % | -4.81 | % | 1.76 | % | -9.41 | % | ||||||||||

Class C | -9.62 | -4.81 | 1.76 | -9.41 | ||||||||||||||

Institutional | -8.63 | -4.81 | 1.76 | -9.41 | ||||||||||||||

Service | -9.00 | -4.81 | 1.76 | -9.41 | ||||||||||||||

Investor | -8.68 | -4.81 | 1.76 | -9.41 | ||||||||||||||

Class R | -9.10 | -4.81 | 1.76 | -9.41 | ||||||||||||||

Class R6 | -8.61 | -4.81 | 1.76 | -9.41 | ||||||||||||||

April 17, 2018– | ||||||||||||||||||

Class P | -9.29 | % | -4.61 | % | 1.93 | % | -10.45 | % | ||||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Portfolio(ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance assumes the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Growth and Income Strategy Composite Index (“Growth and Income Composite”) is a composite representation prepared by the Investment Adviser of the performance of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. The Growth and Income Composite is comprised of a blend of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (“Bloomberg Barclays Global Index”) (40%) and the MSCI All Country World Index (Net, USD, Unhedged) (“MSCI® ACWI Index”) (60%). The Growth and Income Composite figures do not reflect any deduction for fees, expenses or taxes. The Bloomberg Barclays Global Index is an unmanaged index, provides a broad-based measure of the global investment-gradefixed-rate debt markets and covers the most liquid portion of the global investment gradefixed-rate bond market, including government, credit and collateralized securities. The index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The MSCI® ACWI Index is a freefloat-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI® ACWI Index consists of 47 country indices comprising 23 developed and 24 emerging market country indices. The developed market country indices included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indices are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates. The index figures do not include any deduction for fees or expenses. It is not possible to invest directly in an unmanaged index. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

20

FUND BASICS

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 12/31/18 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

Class A | -13.92 | % | 1.45 | % | 6.22 | % | 4.09 | % | 1/2/98 | |||||||||||

Class C | -10.52 | 1.83 | 6.02 | 3.59 | 1/2/98 | |||||||||||||||

Institutional | -8.63 | 3.00 | 7.23 | 4.78 | 1/2/98 | |||||||||||||||

Service | -9.00 | 2.51 | 6.71 | 4.27 | 1/2/98 | |||||||||||||||

Investor | -8.68 | 2.87 | 7.07 | 2.67 | 11/30/07 | |||||||||||||||

Class P | N/A | N/A | N/A | -9.29 | 4/17/18 | |||||||||||||||

Class R | -9.10 | 2.36 | 6.56 | 2.18 | 11/30/07 | |||||||||||||||

Class R6 | -8.61 | N/A | N/A | 2.79 | 7/31/15 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendarquarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service,Investor, Class P, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor���s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| EXPENSE RATIOS4 |

| |||||||||

| Net Expense Ratio (Current) | Gross Expense Ratio (Before Waivers) | |||||||||

| Class A | 1.25 | % | 1.29 | % | ||||||

| Class C | 2.00 | 2.04 | ||||||||

| Institutional | 0.86 | 0.90 | ||||||||

| Service | 1.36 | 1.40 | ||||||||

| Investor | 1.00 | 1.04 | ||||||||

| Class P | 0.85 | 0.89 | ||||||||

| Class R | 1.50 | 1.54 | ||||||||

| Class R6 | 0.85 | 0.89 | ||||||||

| 4 | The expense ratios of the Portfolio, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Portfolio and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to contractual arrangements, the Portfolio’s waivers and/or expense limitations will remain in place through at least April 30, 2019, and prior to such date, the Investment Adviser may not terminate the arrangements without the approval of the Portfolio’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

21

FUND BASICS

| 5 | Strategic allocation is the process of determining the areas of the global markets in which to invest, and in what long-term proportion, for each underlying fund. Our global approach attempts to generate strong long-term returns across geographies and asset classes, and is determined through a careful review of market opportunities and risk/return tradeoffs. On a monthly basis or as needed, we shift assets around the strategic allocation, over and under-weighting asset classes and countries relative to the neutral starting point, seeking to benefit from changing short-term conditions in global capital markets. This is called tactical asset allocation. |

| 6 | Generally, tactical fund weightings are rebalanced approximately monthly, but they may be rebalanced more or less frequently at the discretion of the Investment Adviser based on the market environment and its macro views. The weightings in the chart above reflect the allocations as of December 31, 2018. Actual underlying fund weighting in the Portfolio may differ from the figures shown above due to rounding, differences in returns of the underlying funds, or both. The above figures are not indicative of future allocations. |

22

FUND BASICS

| OVERALL UNDERLYING FUND WEIGHTINGS7 |

| Percentage of Net Assets |

| 7 | The Portfolio is actively managed and, as such, its composition may differ over time. The percentage shown for each underlying fund reflects the value of that underlying fund as a percentage of net assets of the Portfolio. Figures in the above graph may not sum to 100% due to rounding and/or the exclusion of other assets and liabilities. |

23

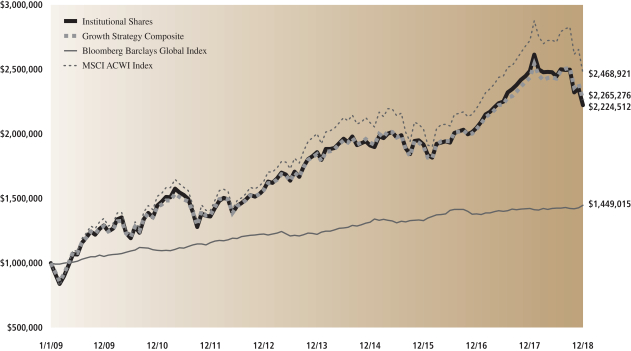

GOLDMAN SACHS GROWTH AND INCOME STRATEGY PORTFOLIO

Performance Summary

December 31, 2018

The following graph shows the value, as of December 31, 2018, of a $1,000,000 investment made on January 1, 2009 in Institutional Shares at NAV. For comparative purposes, the performance of the Portfolio’s benchmarks, the Growth and Income Strategy Composite Index (the “Growth and Income Composite”), which is comprised of 60% of the MSCI® All Country World Index (Net, USD, Unhedged) (the “MSCI ACWI Index”) and 40% of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (the “Bloomberg Barclays Global Index”), the Bloomberg Barclays Global Index and the MSCI ACWI Index (each with distributions reinvested), are shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations may cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations currently in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares. Performance of Class A, Class C, Service, Investor, Class P, Class R and Class R6 Shares will vary from Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding underlying mutual fund selection and allocations among them, other factors may affect Portfolio performance. These factors include, but are not limited to, Portfolio operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Portfolio.

| Growth and Income Strategy Portfolio’s 10 Year Performance |

Performance of a $1,000,000 investment, with distributions reinvested, from January 1, 2009 through December 31, 2018.

| Average Annual Total Return through December 31, 2018 | One Year | Five Years | Ten Years | Since Inception | ||||||||||

Class A (Commenced January 2, 1998) | ||||||||||||||

Excluding sales charges | -8.94% | 2.61% | 6.82% | 4.37% | ||||||||||

Including sales charges | -13.92% | 1.45% | 6.22% | 4.09% | ||||||||||

| ||||||||||||||

Class C (Commenced January 2, 1998) | ||||||||||||||

Excluding contingent deferred sales charges | -9.62% | 1.83% | 6.02% | 3.59% | ||||||||||

Including contingent deferred sales charges | -10.52% | 1.83% | 6.02% | 3.59% | ||||||||||

| ||||||||||||||

Institutional (Commenced January 2, 1998) | -8.63% | 3.00% | 7.23% | 4.78% | ||||||||||

| ||||||||||||||

Service (Commenced January 2, 1998) | -9.00% | 2.51% | 6.71% | 4.27% | ||||||||||

| ||||||||||||||

Investor (Commenced November 30, 2007) | -8.68% | 2.87% | 7.07% | 2.67% | ||||||||||

| ||||||||||||||

Class P (Commenced April 17, 2018) | N/A | N/A | N/A | -9.29%* | ||||||||||

| ||||||||||||||

Class R (Commenced November 30, 2007) | -9.10% | 2.36% | 6.56% | 2.18% | ||||||||||

| ||||||||||||||

Class R6 (Commenced July 31, 2015) | -8.61% | N/A | N/A | 2.79% | ||||||||||

| ||||||||||||||

| * | Total return for periods of less than one year represents cumulative total return. |

24

FUND BASICS

Growth Strategy

as of December 31, 2018

| PERFORMANCE REVIEW |

| |||||||||||||||||

January 1, 2018– December 31, 2018 | Portfolio Total Return (based on NAV)1 | Growth Strategy Composite Index2 | Bloomberg Barclays Global Index | MSCI ACWI Index | ||||||||||||||

Class A | -10.98 | % | -7.09 | % | 1.76 | % | -9.41 | % | ||||||||||

Class C | -11.58 | -7.09 | 1.76 | -9.41 | ||||||||||||||

Institutional | -10.65 | -7.09 | 1.76 | -9.41 | ||||||||||||||

Service | -11.06 | -7.09 | 1.76 | -9.41 | ||||||||||||||

Investor | -10.74 | -7.09 | 1.76 | -9.41 | ||||||||||||||

Class R | -11.18 | -7.09 | 1.76 | -9.41 | ||||||||||||||

Class R6 | -10.55 | -7.09 | 1.76 | -9.41 | ||||||||||||||

April 17, 2018– | ||||||||||||||||||

Class P | -11.39 | % | -6.99 | % | 1.93 | % | -10.45 | % | ||||||||||

| 1 | The net asset value (“NAV”) represents the net assets of the class of the Portfolio(ex-dividend) divided by the total number of shares of the class outstanding. The Portfolio’s performance assumes the reinvestment of dividends and other distributions. The Portfolio’s performance does not reflect the deduction of any applicable sales charges. |

| 2 | The Growth Strategy Composite Index (“Growth Composite”) is a composite representation prepared by the Investment Advisor of the performance of the Portfolio’s asset classes weighted according to their respective weightings in the Portfolio’s target range. The Growth Composite is comprised of a blend of the Bloomberg Barclays Global Aggregate Bond Index (Gross, USD, Hedged) (“Bloomberg Barclays Global Index”) (20%) and the MSCI All Country World Index (Net, USD, Unhedged) (“MSCI® ACWI Index”) (80%). The Growth Strategy Composite figures do not reflect any deduction for fees, expenses or taxes. The Bloomberg Barclays Global Index is an unmanaged index, provides a broad-based measure of the global investment-gradefixed-rate debt markets and covers the most liquid portion of the global investment gradefixed-rate bond market, including government, credit and collateralized securities. The index figures do not include any deduction for fees, expenses or taxes. It is not possible to invest directly in an unmanaged index. The MSCI® ACWI Index is a freefloat-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI® ACWI Index consists of 47 country indices comprising 23 developed and 24 emerging market country indices. The developed market country indices included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. The emerging market country indices are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and the United Arab Emirates. The index figures do not include any deduction for fees or expenses. It is not possible to invest directly in an unmanaged index. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.gsamfunds.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

25

FUND BASICS

| STANDARDIZED TOTAL RETURNS3 | ||||||||||||||||||||

| For the period ended 12/31/18 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||

Class A | -15.87 | % | 2.07 | % | 7.28 | % | 3.97 | % | 1/2/98 | |||||||||||

Class C | -12.46 | 2.46 | 7.09 | 3.48 | 1/2/98 | |||||||||||||||

Institutional | -10.65 | 3.64 | 8.32 | 4.66 | 1/2/98 | |||||||||||||||

Service | -11.06 | 3.14 | 7.79 | 4.14 | 1/2/98 | |||||||||||||||

Investor | -10.74 | 3.50 | 8.17 | 2.51 | 11/30/07 | |||||||||||||||

Class P | N/A | N/A | N/A | -11.39 | 4/17/18 | |||||||||||||||

Class R | -11.18 | 2.97 | 7.62 | 2.00 | 11/30/07 | |||||||||||||||

Class R6 | -10.55 | N/A | N/A | 3.31 | 7/31/15 | |||||||||||||||

| 3 | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendarquarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional, Service,Investor, Class P, Class R and Class R6 Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns represent past performance. Past performance does not guarantee future results. The Portfolio’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recentmonth-end returns.Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.