UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05601

SEI Institutional International Trust

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

Timothy D. Barto, Esq.

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 610-676-1000

Date of fiscal year end: September 30, 2020

Date of reporting period: September 30, 2020

| Item 1. | Reports to Stockholders. |

September 30, 2020

ANNUAL REPORT

SEI Institutional International Trust

| International Equity Fund

| |

| Emerging Markets Equity Fund

| |

| International Fixed Income Fund

| |

| Emerging Markets Debt Fund |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can follow the instructions included with this disclosure, if applicable, or you can contact your financial intermediary to inform it that you wish to continue receiving paper copies of your shareholder reports. If you invest directly with the Funds, you can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-DIAL-SEI. Your election to receive reports in paper will apply to all funds held with the SEI Funds or your financial intermediary.

The Trust files its complete schedule of portfolio holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Trust’s Form N-PORT reports are available on the Commission’s website at http://www.sec.gov.

A description of the policies and procedures that the Trust uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how a Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-800-DIAL-SEI; and (ii) on the Commission’s website at http://www.sec.gov.

September 30, 2020 (Unaudited)

To Our Shareholders:

The fiscal year ending September 30, 2020, began with strong returns in the equity markets over the final months of 2019. After hitting all-time highs in February, concerns about the international spread of a novel coronavirus (COVID-19) dominated investor concerns, and by the end of March most equity indexes had fallen into bear-market territory. Plans to reopen economic activity and developments in the race for COVID-19 treatments encouraged investors in April and May; global financial markets rallied sharply amid renewed “risk-on” sentiment, with U.S. equity markets eclipsing their pre-pandemic peaks before the end of the fiscal year. Despite tension around a U.S.-China trade deal and ongoing Brexit concerns in late 2019, the lingering effects of COVID-19 demanded plenty of attention from investors.

The Federal Reserve (Fed) cut interest rates three times prior to March. Two off-cycle moves in February brought the federal-funds rate to near zero and were designed to bolster the economy in response to the economic threat posed by the coronavirus outbreak; the emergency actions were the first since the global financial crisis. Additionally, the Fed committed to purchasing unlimited amounts of Treasurys and established or renewed multiple facilities designed to support the economy.

Christine Lagarde succeeded Mario Draghi as European Central Bank (ECB) President in November. The ECB restarted its asset-purchase program in November with a monthly pace of €20 billion and stated it intends to continue to fully reinvest the principal payments from maturing securities purchased under the program. In response to COVID-19, the ECB announced a new quantitative easing (QE) package in March—the Pandemic Emergency Purchase Programme

— amounting to €750 billion, which should bring total QE-related asset purchases to more than €1.3 trillion in 2020.

The Japanese yen, typically viewed as a safe-haven asset in “risk-off” environments, finished the period 2.5% higher against the U.S. dollar, while the Bank of Japan indicated it would continue a negative rate policy through 2023. The Chinese yuan finished the fiscal year up 5.3%; the currency rebounded from an 11-year low reached before the start of the fiscal year after a U.S.-China phase-one trade agreement was signed.

West Texas Intermediate crude-oil prices stayed mostly range-bound over the first quarter of the reporting period. From January onward, the commodity became a victim of an oil-production impasse between Saudi Arabia and Russia and travel restrictions that sapped usage due to the coronavirus pandemic. Between the high price toward the end of 2019 and the April lows, crude-oil prices fell over 80%. Record supply cuts and a pickup in global fuel demand toward the end of the reporting period helped drive a partial price recovery, and oil finished down over 25% for the 12-month period.

Geopolitical events

Market volatility accelerated in the first quarter of 2020 following concerns about COVID-19 and its eventual economic effect: as the outbreak spread from China to other countries, governments issued stay-at-home orders and initiated widespread lockdowns. Beyond the threat to public health, the outbreak and resulting containment measures evoked concerns about the potential halt to global economic activity. The official daily infection rate continued to trend generally higher, with over 33 million cases worldwide at the end of September, while in the U.S., the total recorded number of COVID-19-related deaths surpassed 200,000 by the end of September—out of about 1,000,000 total worldwide. Nevertheless, markets remained generally optimistic over the last half of the reporting period as forward-looking investors attempted to spot sources of encouragement.

At least 68 countries and territories postponed elections between February 21 and July 26, also citing concerns about COVID-19 containment, according to the Wall Street Journal; at least 49 countries and territories committed to holding their elections as scheduled. The U.S. presidential election cycle formally progressed to its final phase before Election Day, as President Donald Trump accepted the Republican Party’s nomination and former Vice President Joe Biden accepted the Democratic Party’s nomination at their respective quadrennial conventions during August. The U.S. general election will proceed in early November.

The United States-Mexico-Canada trade agreement was ratified by all three countries in December and officially replaced the North American Free Trade Agreement on July 1. The Trump administration announced in September that it would not pursue a 10% tariff on U.S. imports of Canadian aluminum previously announced in August, as trade is now expected to normalize in the coming months following high import levels earlier in 2020. President Trump

SEI Institutional International Trust / Annual Report / September 30, 2020 |

1 |

LETTER TO SHAREHOLDERS (Continued)

September 30, 2020 (Unaudited)

and France’s President Emmanuel Macron successfully walked back threats of tariffs that originated with French plans for a digital tax that would have targeted U.S.-based multi-national technology companies. The prospect of a digital tax re-surfaced in other countries—including the U.K., Italy, Austria and Turkey—which prompted more threats of retailiatory tariffs by Treasury Secretary Steven Mnuchin. Sajid Javid, the UK’s former Chancellor of the Exchequer, disappointed Secretary Mnuchin by explaining during a joint interview in late January at the World Economic Forum that the U.K. would prioritize trade negotiations with the EU over a deal with the U.S.

China and the U.S. formalized a “phase one” trade deal in mid-January that offered tariff relief to China (via the reduction of existing tariffs and the delay of additional scheduled tariffs). In exchange, China committed to purchasing $200 billion in U.S. products over a two-year period; addressing its long-standing practice of forcing the transfer of intellectual property and technology to Chinese counterparts in exchange for access to the Chinese market; and promising to continue opening its financial-services industry to foreign investors. The tense U.S.-China relationship was stressed in May by a U.S. push for more transparency in the ownership of U.S.-listed Chinese companies and the U.S. government’s barring of certain Chinese securities from its retirement plans.

Under Boris Johnson, the UK’s Conservative Party consolidated its power in a mid-December election—winning a majority of seats in the House of Commons and gaining approval for Prime Minister Boris Johnson’s EU departure deal. The country officially left the EU at the end of January 2020, giving way to an 11-month transition period to negotiate terms of the future U.K.-EU relationship. Johnson emerged from his personal battle with COVID-19 in April, having been hospitalized in intensive care and temporarily deputizing Foreign Secretary Dominic Raab to fulfill his role while incapacitated.

Japan’s ruling Liberal Democratic Party selected Yoshihide Suga to succeed Prime Minister Shinzo Abe, who resigned in August due to health issues. Elsewhere in Asia, China-Taiwan tensions flared in September after a high-level U.S. government official’s visit to Taiwan; China was angered by what it saw as one of its territories assuming sovereignty by inappropriately conducting international diplomacy. Chinese planes made a show of force to coincide with the visit, prompting Taiwan to quickly mobilize its military jets. The island’s government had previously condemned nearby Chinese military drills as provocations. In Beijing, a military spokesman accused Taiwan’s ruling Democratic Progressive Party of “collusion” with the U.S., and said the U.S. is trying to “use Taiwan to control China.”

Economic performance

U.S. gross domestic product (GDP) grew 2.1% in the fourth quarter of 2019, driven by an increase in net trade but weakened by a sharp slowdown in consumer spending. The economy saw a decline of 5.0% in the first quarter of 2020, the largest drop since the global financial crisis, but reflected just two weeks of lockdowns that began across the country in March. The economy contracted by a worst-ever 31.4% in the second quarter, falling in all 50 states. The abrupt halt to the 10-year economic expansion came amid mandated lockdowns throughout most of the country.

The U.S. unemployment rate touched a 50-year low of 3.5% during the fiscal year before jumping as high as 14.7% in April and settling at 7.9% in the final reading; the number of Americans filing for initial unemployment benefits hit record numbers as many non-essential businesses were forced to close in the wake of the pandemic. The labor-force participation rate ended at 61.4%, down from 63.2% a year earlier. Average hourly earnings gained 4.7% over the fiscal year, as the increase in unemployment tended to hit lower-wage workers hardest.

Broad economic activity in the eurozone slowed to its weakest pace since records began in 1995 during the first quarter of 2020; the 13.6% annualized decline wiped away three years of growth in the area. The region officially fell into recession after a 40.3% contraction in the second quarter and far exceeded that in the U.S. as measures imposed to limit the spread of COVID-19 reflected the closing of everything from restaurants to factories. The magnitude and speed of the contraction solidified the case for continued accommodative policy by the ECB for some time.

The Bank of England’s Monetary Policy Committee cut its Bank Rate to 0.1% in March, the lowest in the 325-year history of its lending rate, during the fiscal year. It also announced a £200 billion asset-purchase program, mostly of government bonds, to be conducted at a monthly pace that will eclipse previous rounds of QE. Additionally, it launched a so-called funding-for-lending scheme to spur banks to lend to small- and medium-sized enterprises, as well as a commercial paper facility with no cap limit, both to be financed by central-bank reserves. Following its mid-June meeting, the central bank announced that it would expand its stock of asset purchases to £745 billion. The U.K.

2 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

economy shrank a record 19.8% seasonally-adjusted at annual rates through the second quarter of 2020; while the decline was less severe than originally thought, it was also the largest since records have been kept.

Japanese GDP contracted 7.2% in seasonally-adjusted annualized terms in the fourth quarter of 2019 as the country’s sales tax hike weakened consumer and business spending; an additional 2.2% decline in the first quarter of 2020 confirmed that Japan had fallen into recession for the first time in over four years. Japan’s economy contracted 28.1% in the second quarter as capital expenditures were hit hard by the pandemic. The Bank of Japan expanded monetary stimulus as pandemic pain worsened late in the period. Meanwhile, GDP in China shrank by 6.8% year-on-year and seasonally-adjusted in the first quarter of 2020, its worst pace in several decades, as consumer spending, exports and fixed-asset investments all were affected by the lockdowns in January and early February; a 3.2% gain in the second quarter came as restrictions eased and the country rolled out stimulus measures intended to aid the economy.

Market developments

The S&P 500 Index finished the fiscal year up 15.15%, despite falling over 30% from its peak on February 19, 2020, to the trough on March 23. Prior to the coronavirus onset, investors enjoyed the continuation of the modest U.S. economic expansion, reasonably strong corporate profitability and accommodative Fed monetary policy. Over the full reporting period, mega-cap stocks, a narrow group of companies with unusually large weights in the broad equity index, outperformed, and growth companies in the information technology sector generally led, while many value stocks underperformed. Commodity-sensitive stocks, particularly those within the energy sector, lagged the most.

U.S. large-cap stocks (Russell 1000 Index) finished the reporting period up 16.01%; small-cap stocks (Russell 2000 Index) were hit harder in the coronavirus-driven selloff, as investors tended to avoid smaller companies with lesser financial strength, and edged just 0.39% higher over the fiscal year.

Despite continued accommodative monetary policy from the ECB, European equities lagged, as fears over trade wars and COVID-19 grew. The MSCI Europe Index (Net) fell 0.79% in U.S. dollar terms and was 7.33% lower in euros; the euro finished up 6.68% versus the U.S. dollar for the period. The MSCI ACWI Index (Net), a proxy for global equities in both developed and emerging markets, climbed 10.44% in U.S. dollar terms.

Despite a strong rally over the second half of the year, the FTSE UK Series All-Share Index lost 12.30% in U.S. dollar terms over the full reporting period, while it fell 16.59% in sterling.

Emerging-market equities were higher. After gaining 9.56% in the final quarter of the fiscal year, the MSCI Emerging Markets Index (Net) finished the reporting period up 10.54% in U.S. dollar terms. U.S.-China trade news generally drove performance for the first three months; however, a rally after the U.S. and China agreed to a “phase-one” trade deal in January was wiped out until COVID-19 concerns in China began to decelerate.

Global government bonds outperformed global high-yield bonds as the escalation of COVID-19 hit the bond market’s most economically sensitive sectors the hardest. The global high-yield market, as measured by the ICE BofA Global High Yield Constrained Index, was 3.84% higher during the reporting period, while global government bonds, as measured by the Bloomberg Barclays Global Treasury Index, did better and climbed 5.84%.

A continuing theme for U.S. fixed-income markets was the inverted yield curve. The spread between 2-year and 5-year Treasurys yields was inverted early in the reporting period, as was the spread between 3-year and 5-year Treasurys. Notably, the spread between 3-month and 10-year rates was inverted for only the second time in about 12 years during the fiscal year, a signal of impending recession to some market watchers that occurred long before any knowledge of the pandemic. The differential reverted during the period and eventually stayed in positive territory from March onward.

Yields for 10-year U.S. government bonds ended the period down 99 basis points at 0.69%, after hitting an all-time low of 0.54% in March as investors rushed to “safe-haven” securities; 2-year yields declined during the fiscal year to finish down 150 basis points at 0.13%.

Inflation-sensitive assets, such as commodities and Treasury inflation-protected securities (TIPS), were mixed. The Bloomberg Commodity Total Return Index (which represents the broad commodity market) finished down 8.20% over the full one-year period, after an oil-production impasse between Saudi Arabia and Russia created a downdraft in the

SEI Institutional International Trust / Annual Report / September 30, 2020 |

3 |

LETTER TO SHAREHOLDERS (Concluded)

September 30, 2020 (Unaudited)

oil market around the same time that demand contracted due to the coronavirus pandemic; the Bloomberg Barclays 1-10 Year US TIPS Index (USD) moved 7.75% higher during the reporting period.

U.S. investment-grade corporate debt was higher; the Bloomberg Barclays US Corporate Investment Grade Index returned 7.90% as investors remained eager to buy higher-yielding securities. U.S. asset- and mortgage-backed securities also managed to rise during the fiscal year.

Coronavirus concerns and the steep drop in global oil prices led to a declining outlook for economic growth in emerging markets; the JP Morgan Global Bond Index-Emerging Markets (GBI-EM) Global Diversified Index, which tracks local-currency-denominated EM bonds, declined 1.45% in U.S. dollar terms. The JP Morgan Emerging Markets Bond Index (EMBI) Global Diversified Index, which tracks EM debt denominated in external currencies (such as the U.S. dollar), managed a 1.29% gain for the fiscal year.

Our view

It has already been an eventful and exhausting year, but we have a sense that the next few months could prove critical to the future course of the global economy and financial markets. Most countries were in V-shaped recovery mode during the third quarter, moving sharply off their low points in May and June. We assume that future lockdowns to contain COVID-19 outbreaks will be far more limited in scope. For developed countries, treatments have improved, vulnerable populations appear to be better-protected, and younger, generally healthier people are accounting for a much larger share of confirmed new cases.

But we doubt there will be a full return to normal economic behavior until safe and effective vaccines are introduced and distributed globally. The news on this score has been positive, and probably is a key reason for the continued buoyancy of equities and other risk assets. According to the World Health Organization, researchers were testing 38 vaccines in clinical trials at the end of September, while 93 more were in pre-clinical testing. Ten vaccines have been approved for large-scale efficacy and safety trials. We think it is realistic to assume that a few different vaccines will be generally available by this time next year, which means that social-distancing measures must still be followed well into 2021 and, most likely, into 2022.

There’s no disputing that U.S. economic activity remains far below normal. Although incomes are now recovering as more people get back to work, the lack of additional income support may drag down consumer spending as we head into the end of the year. Business sentiment appears to have bottomed, but the outlook remains sufficiently uncertain to keep us in a watch-and-wait mode. We would not be surprised to see the official U.S. unemployment rate move up in the months ahead as hard-hit industries eliminate jobs now that government support has run out.

In August, Fed Chairman Jerome Powell officially unveiled a new framework for conducting the central bank’s monetary policy. The Fed has decided to see how low the U.S. unemployment rate can get before it causes the inflation rate to exceed the 2% mark by a meaningful extent.

The FOMC’s own inflation projection does not envision a return to 2% inflation until the end of its forecast window in 2023, so it may be a long time before the federal-funds rate rises.

In our view, all that’s really left in the Fed’s monetary toolbox is quantitative easing, along with the provision of lifeline support to corporations as well as state and local governments through its various credit facilities. Monetization of debt will likely continue until the pandemic crisis is well past and the U.S. unemployment rate approaches its previous lows.

The U.S. presidential election will have a major impact on the economy and financial markets in the months and years ahead. Still, we firmly believe that it would be a mistake to pursue even a short-term investment strategy that necessitates accurately predicting: (1) the election winner; (2) the policies proposed by the newly inaugurated president; (3) the ways in which Congress will modify those proposals throughout the legislative process; or (4) the impact those new laws would have on the economy and financial markets.

Regardless of the election’s outcome, we assume that both candidates would see their platforms tempered before they’re put into practice. There is a high degree of institutional inertia, which is partly deliberate (constitutional checks and balances) and partly happenstance (increasing polarization of opinion in the country tends to favor a draw). While there could be some market volatility plausibly attributed to the election, it is usually best to pay strict attention to the fundamentals and to ignore the politics.

4 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

The U.K. is undergoing its own unique political melodrama, with Prime Minister Boris Johnson facing a rebellion among his own backbenchers and intense criticism from senior Conservatives over his proposal to renege on the withdrawal treaty that would allow Northern Ireland to trade without border restrictions with Ireland and the rest of the EU. The move to abrogate the treaty, if successful, would almost certainly lead to a hard Brexit—a reversion to the World Trade Organization’s most-favored-nation trading rules with the EU. It also could breathe new life into the separatist movement in Northern Ireland itself, not to mention Scotland.

Prime Minister Johnson’s decision reflects his government’s frustration with EU negotiators. There are two main sticking points, one small (EU fishing industry demanding full access to U.K. waters) and one large (EU demanding the UK’s continued adherence to EU strictures on government financial assistance to private-sector businesses).

Obviously, a hard Brexit will not help matters. But the worst impact potentially will be sustained by financial companies and other service- producing entities, since World Trade Organization rules deal mostly with tradable goods. The increase in tariffs, for the most part, will be bearable once border-related issues are worked out. In the meantime, the U.K. and the rest of Europe are facing a second wave of COVID-19 that could turn what’s been a V-shaped recovery into something looking more like a W.

This year’s pandemic and postponement of the summer Olympics proved to be a bitter ending to Japanese Prime Minister Shinzo Abe’s record-breaking term in office. His push to lift Japan out of its deflationary spiral was somewhat successful. Prices mostly stopped declining in the aggregate, but there were few occasions when overall consumer-price inflation rose above 1%. Pandemic pressures have caused a return to outright deflation in recent months.

In our view, it is unlikely that radical changes will be made to the direction of policy under Japan’s new Prime Minister Yoshihide Suga. In the near-term, the priority will be on the response to the coronavirus; fiscal policy will remain quite expansionary. The Bank of Japan will continue to buy most of the government-issued bonds, along with other types of corporate debt and equity, as it has been doing as part of its Quantitative and Qualitative Easing program over the past four years.

The contrast of the big Asian stock markets versus other large emerging-market equities is dramatic. China’s strong gains can be chalked up to its rebound in economic activity. Although travel and other services are still constrained due to lingering concerns about the virus, infrastructure-related spending and manufacturing have experienced an almost-complete recovery to pre-pandemic levels. Investors seem to be unfazed by the deterioration in the US-China economic relationship or by the increasingly fraught diplomatic relations between China and other countries.

Emerging markets are already showing some good news. The price of raw industrials bottomed in early May, and have since enjoyed a sharp move higher. If industrial commodity prices advance in a sustained, multi-year fashion as they have in previous cycles, it’s a good bet that emerging-market corporate profits will also rise sharply.

Our optimism is somewhat tempered by the rising debt burden facing many emerging countries. Much of the increase in emerging-market debt has been tied to the corporate sector—especially in China, where private domestic, non-financial debt has reached an eye-watering 216% of GDP. Of more concern are the mostly small-to-medium-sized countries that are running current-account deficits and are too dependent on external hard-currency debt, or do not have the reserves to easily cover their debt service.

The actions of the world’s major central banks back in March, especially the Fed’s provision of U.S. dollar liquidity, have helped to ease the strain on the market for emerging-country debt. Governments and other official lenders, meanwhile, have granted loan forbearance to nearly 80 countries; it’s a tougher job to get private creditors to agree to do the same. Nonetheless, emerging-market sovereign yields on dollar-denominated debt have fallen back toward their previous record lows, more than reversing the spike endured in March, prior to the Fed’s rescue operations.

Sincerely,

William T. Lawrence, CFA

Head and Chief Investment Officer of Traditional Asset Management, SEI

SEI Institutional International Trust / Annual Report / September 30, 2020 |

5 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2020 (Unaudited)

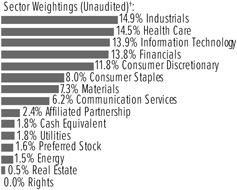

International Equity Fund

I. Objective

The International Equity Fund (the “Fund”) seeks long-term capital appreciation.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2020: Acadian Asset Management LLC (“Acadian”), Causeway Capital Management LLC (“Causeway”), INTECH Investment Management LLC (“INTECH”), JO Hambro Capital Management Limited (“JO Hambro”), Lazard Asset Management LLC (“Lazard”), NWQ Investment Management Company, LLC (“NWQ”) and WCM Investment Management LLC (“WCM”).

During the period, JO Hambro was added to the Fund, while Blackcrane Capital, LLC (“Blackcrane”), and Neuberger Berman Investment Advisers LLC (“Neuberger Berman”), were removed from the Fund.

III. Return vs. Benchmark

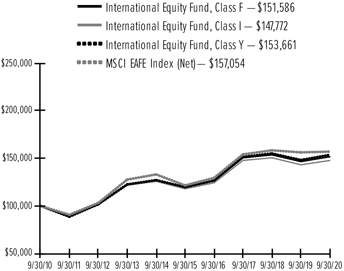

For the year ended September 30, 2020, the Fund’s Class F shares outperformed the MSCI EAFE Index (Net)—which tracks the performance of developed-market equities outside North America—returning 3.44% versus the Index return of 0.49%.

IV. Fund Attribution

As noted in the shareholder letter, developed-market equities rose steadily at the start of the fiscal year as the global economy found footing; the eventual outbreak of COVID-19 in early 2020 forced lockdowns and stay-at-home orders across most countries, sending major equity indexes lower as investors dealt with the economic uncertainty. Over the last half of the reporting period, markets generally rallied as central banks enacted significant monetary and fiscal stimulus measures.

Although Japanese economic growth remained lackluster during the reporting period, Japan was the best-performing country in the MSCI EAFE Index over the full fiscal year. Europe also performed well and was boosted by the strong performance of its healthcare sector. During the worst of the selloff, the European Central Bank announced massive amounts of monetary stimulus, which was eventually accompanied by large amounts of fiscal stimulus from its member nations, to

support the region’s economy. The European Union also made progress in issuing the region’s first common bonds, signaling to investors its determination in helping the region’s economy recuperate. The Pacific ex-Japan region was dragged down by results from Australia’s energy and banking sector. The U.K. was the worst-performing region as the twin headwinds of COVID-19 and a collapse in oil prices put heavy pressure on the region’s equity prices. Lack of progress in Brexit negotiations was also a dampener on equity prices.

The best-performing sectors in the benchmark were information technology and healthcare, with investors flocking to sectors believed to have the most durable and sustainable long-term growth prospects. Healthcare also outperformed given the outbreak-driven demand for healthcare services. Information technology was the Fund’s most significant contributor as stability and momentum managers had favorable results within the sector. The materials sector also did well on strong results from non-commodity-related companies. Real estate contributed as the Fund’s aversion to the sector’s rich valuations and lack of growth opportunities helped avoid losses from the otherwise poorly performing sector. The biggest detractors came from defensive sectors like consumer staples and utilities, which generally matched or outperformed the benchmark and that the Fund was underweight. Energy was the benchmark’s worst-performing sector given the weakness in the oil industry, although the Fund’s underweight was beneficial.

From a regional point of view, Europe was the biggest contributor due to favorable exposure and results in the European industrials and healthcare sectors. Exposure to ex-benchmark emerging-market Asian technology also contributed. An underweight to Pacific ex-Japan, especially the region’s underperforming banks, was beneficial. The U.K. also contributed, primarily due to the Fund’s underweight to the region’s lagging energy sector, which took a hit during the crude oil selloff in the spring. Japan was the biggest regional detractor due to negative results in the Fund’s Japanese healthcare and consumer sectors.

WCM was the Fund’s best-performing manager and outperformed due to tailwinds to stability, especially stocks on the faster growing end of the stability spectrum. During the fiscal year, stocks with durable and stable growth prospects continued to be favored by investors as the COVID-19 break altered expectations for future growth. Acadian also contributed and saw favorable results from its quantitative model-driven selection; headwinds to value were not enough to offset

6 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

the tailwinds from momentum. Blackcrane contributed and enjoyed a tailwind to momentum, as companies with strong fundamental momentum were heavily rewarded. During the period, momentum became more aligned with stability as companies with strong and consistent earnings growth prospects continued to outperform and trend higher. Stability manager Neuberger Berman also benefited from a similar tailwind to stability, and both of the Fund’s momentum managers, INTECH and JO Hambro, enjoyed positive tailwinds to momentum and added to alpha as well.

The Fund’s three value managers—Causeway, NWQ and Lazard—were the only detractors. Performance for our value managers was in line with expectations given the continued headwinds that value faced as investors preferred stability and momentum throughout most of the fiscal year.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| International Equity Fund, Class F | 3.44% | 0.24% | 4.88% | 4.25% | 3.43% | |||||||||||||||

| International Equity Fund, Class I | 3.19% | -0.01% | 4.60% | 3.98% | 3.17% | |||||||||||||||

| International Equity Fund, Class Y | 3.68% | 0.48% | 5.12% | 4.39% | 3.47% | |||||||||||||||

| MSCI EAFE Index (Net) | 0.49% | 0.62% | 5.26% | 4.62% | 4.25% | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the International Equity Fund, Class F, Class I and Class Y, versus the MSCI EAFE Index (Net)

| 1 | For the year ended September 30, 2020. Past performance is no indication of future performance. Class F shares were offered beginning December 20, 1989. Class I shares were offered beginning January 4, 2002. The performance of Class I shares prior to January 4, 2002 is calculated using the performance of Class F shares adjusted for the higher expenses of the Class I shares. Returns for Class I shares are substantially similar to those of Class F shares and differ only to the extent that Class I shares have higher total annual fund operating expenses than Class F shares. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

7 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2020 (Unaudited)

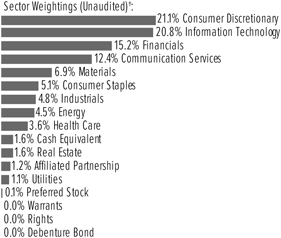

Emerging Market Equity Fund

I. Objective

The Emerging Markets Equity Fund (the “Fund”) seeks capital appreciation.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corp. (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2020: JO Hambro Capital Management Limited (“JO Hambro”), KBI Global Investors (North America) Ltd. (“KBI”), Lazard Asset Management LLC (“Lazard”), Neuberger Berman Investment Advisers LLC (“Neuberger Berman”), Qtron Investments LLC (“Qtron”) and RWC Asset Advisors (US) LLC (“RWC”).

During the period, Delaware Investments Fund Advisers, a series of Macquarie Investment Management Business Trust (“Macquarie”), was removed from the Fund.

III. Return vs. Benchmark

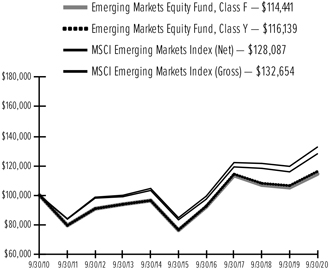

For the year ended September 30, 2020, the Fund’s Class F shares underperformed the MSCI Emerging Markets Index (Net)—which tracks the performance of global emerging market equities—returning 8.75% versus the Index return of 10.54%.

IV. Fund Attribution

Emerging markets finished on a positive note after a rollercoaster performance during the fiscal year. The fourth quarter of 2019 was a positive one, with markets rallying on hopes of a pickup in global economic growth before the outbreak of COVID-19 sent major equity markets into freefall; most global economies enacted business lockdowns and stay-at-home orders. Oil also experienced a major disruption as expected cuts to crude were not realized, sending oil prices crashing and contributing to the equity market freefall, especially in commodity-exporting nations.

Asian countries outperformed the benchmark, led by Chinese equities. China was the first to be impacted by COVID-19 but was also the first to recover, boosted by fiscal and monetary stimulus from the government. Strong demand for online retail and internet platforms (from consumers staying home), as well as technology components, partially fueled the strong performance of Chinese equities. Strong demand for technology components like memory and 5G also helped both Taiwan and Korea outperform. India lagged Asia but kept

pace with the benchmark as COVID-19 exacerbated the country’s economic slowdown.

The Europe, Middle East and Africa region lagged the benchmark as the drop in oil prices, as well as the shock to overall commodity demand, was a drag on South Africa and Russia and the commodity exporters in both countries. A drop in global tourism also impacted Greece and Turkey, which were among the biggest laggards in the region and the benchmark.

Latin America also lagged the benchmark and was the worst-performing region due to weak performance from Brazil, which was affected by both high cases for COVID-19 and the drop in commodity prices. Mexico outperformed the region but lagged the benchmark due to weak performance in banks and consumer stocks.

The best-performing sectors in the benchmark were information technology on strong demand due to significant work-from-home use, as well as healthcare due to pandemic demand. Online retailing and consumer discretionary also outperformed as consumers were forced to stay at home. The worst-performing sectors were energy, which was weakened by price cuts and a slump in demand, and financials, as many emerging-market banks suffered from the drop in local growth.

An overweight to information technology was the largest contributor to Fund performance. Overweights to materials and industrials also contributed due to strong results in select metals, chemicals and capital goods companies. Consumer discretionary was the biggest detractor given the Fund’s low exposure to online retailing stocks amid elevated valuations. Weak selection within the healthcare and consumer staples sectors further challenged Fund performance.

KBI was the biggest detractor as the manager’s dividend-yield process faced headwinds. Investors preferred companies with faster and more durable growth prospects over cheaper companies that tended to have impaired business fundamentals. Neuberger Berman also detracted and lagged expectations given the manager’s stability profile and strong preference for stability. Stability generally outperformed, influenced by investor preferences for fast-growing companies with durable prospects, as well as the large index weights of the big internet and technology companies; Neuberger Berman was tilted towards the smaller, cheaper, and slower-growing end of that stability spectrum. The manager did not have exposure to the expensive and fast-growing online retailing companies that dominated index performance during the reporting period. Lazard was the smallest detractor during the period and

8 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

underperformed largely due to an oversized exposure to high-quality banks in countries like India and Colombia that were hit by slowing economic growth.

JO Hambro was the top-performing manager and benefited from its momentum philosophy. Momentum outperformed as internet, technology and healthcare companies outperformed for most of the fiscal year. Macquarie also contributed and benefited from an underweight to banks and selection within energy and information technology. Qtron’s quantitative model led to above-benchmark returns in all sectors except healthcare and the consumer sectors. RWC contributed slightly during the fiscal year and was helped by an overweight to information technology and strong selection within materials and internet stocks.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| Emerging Markets Equity Fund, Class F | 8.75% | 0.28% | 8.42% | 1.36% | 4.34% | |||||||||||||||

| Emerging Markets Equity Fund, Class Y | 8.99% | 0.52% | 8.69% | 1.51% | 4.40% | |||||||||||||||

| MSCI Emerging Markets Index (Gross) | 10.91% | 2.79% | 9.37% | 2.87% | 6.04% | |||||||||||||||

| MSCI Emerging Markets Index (Net) | 10.54% | 2.42% | 8.97% | 2.50% | N/A | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Equity Fund, Class F and Class Y, versus the MSCI Emerging Markets Index (Net) and the MSCI Emerging Markets Index (Gross)

| 1 | For the year ended September 30, 2020. Past performance is no indication of future performance. Class F shares were offered beginning January 17, 1995. Class Y shares were offered beginning December 31, 2014. Class Y shares performance for the period prior to December 31, 2014 is derived from the performance of Class F shares. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

N/A – Not available

SEI Institutional International Trust / Annual Report / September 30, 2020 |

9 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2020 (Unaudited)

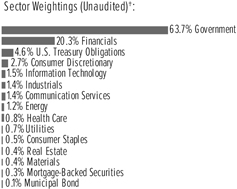

International Fixed Income Fund

I. Objective

The International Fixed Income Fund (the Fund) seeks capital appreciation and current income.

II. Multi-Manager Approach Statement

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corporation (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2020: AllianceBernstein L.P. (“AllianceBernstein”), Colchester Global Investors Limited (“Colchester”) and Wellington Management Company LLP (“Wellington”).

No manager changes were made during the Fund’s fiscal year.

III. Return vs. Benchmark

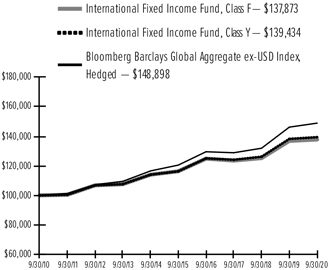

For the year ended September 30, 2020, the Fund’s Class F shares underperformed the Bloomberg Barclays Global Aggregate ex-USD Index, Hedged (the “Index”)—which tracks the performance of the global investment-grade fixed-rate debt markets outside of the U.S.—returning 0.73% versus the Index return of 1.82%.

IV. Fund Attribution

Global fixed income delivered decent performance over the period, although international (ex-U.S. dollar) indexes produced more modest returns given that the U.S. was the best-performing major bond market. Weakness in the U.S. dollar essentially meant that hedged indexes inherently underperformed their unhedged equivalents.

U.S. fixed income started the reporting period with a significant yield advantage over other G7 markets, which gave U.S. bonds a strong starting point from which to outperform through the fiscal year as escalating COVID-19 concerns prompted a sharp rally in sovereign yields. The strong performance of duration-sensitive assets was matched by the weakness in risk assets as credit spreads widened significantly through late February and March. The selloff in credit was dramatic, with spreads widening at a far quicker pace than what was experienced during the global financial crisis. The subsequent retracement in spreads was equally fast, aided by unprecedented levels of monetary support from the U.S. Federal Reserve, European Central Bank and other global central banks, as noted in the shareholder letter. On an excess return basis, sterling and euro corporates outperformed U.S. corporates. Local-currency emerging-market debt (EMD) lagged other risk-sensitive

sectors—including hard-currency debt—during the period as bond gains were pared by general weakness within the EM currency complex.

The Fund underperformed its benchmark during the reporting period. The biggest performance detractor was the overweight to corporate credit, which was a significant drag in March when investor risk aversion peaked. Duration underweights in Japan, core Europe and the U.K. during February/early March also weighed on relative performance as core markets caught a “safe-haven” bid. Active currency positioning was an overall detractor, through long positions in the Mexican peso, Colombian peso, Chilean peso and Russian ruble, as well as shorts in the Swiss franc and New Zealand dollar.

This underperformance was largely offset by out-of-index exposure to the U.S. bond market (both U.S. Treasurys and spread sectors) and an overweight to Mexican local bonds. Currency overweights to British pounds and Swedish krona, as well as shorts in Turkish lira, Hungarian forint and Thai baht also pared losses on other active currency positions.

Wellington lagged during the period. Most of the underperformance was generated at the start of the reporting period due to an ill-timed pivot to overweight duration, and during mid-2020, when the portfolio was short euros. AllianceBernstein was challenged by its overweight exposure to corporate credit (including some off-index high yield) during a period of heightened risk aversion.

Colchester outperformed and benefited from overweights in emerging local-currency debt markets (Mexico and Colombia), off-index exposure to U.S. Treasury inflation-protected securities, as well as currency overweights in Norwegian krone, Swedish krona, British pound, Mexican peso and Colombian peso.

The Fund used financial futures, interest-rate swaps and over-the-counter options during the reporting period to hedge existing exposures and gain exposure to particular areas of the market. The use of derivatives did not have a material impact on performance.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

10 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

AVERAGE ANNUAL TOTAL RETURN1

| 1 Year Return | Annualized 3 Year Return | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| International Fixed Income Fund, Class F | 0.73% | 3.73% | 3.46% | 3.26% | 4.22% | |||||||||||||||

| International Fixed Income Fund, Class Y | 0.88% | 3.96% | 3.69% | 3.38% | 4.26% | |||||||||||||||

| Bloomberg Barclays Global Aggregate ex-USD Index, Hedged | 1.82% | 4.94% | 4.33% | 4.06% | 5.58% | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the International Fixed Income Fund, Class F versus the Bloomberg Barclays Global Aggregate ex-USD Index, Hedged

| ¹ | For the year ended September 30, 2020. Past performance is no indication of future performance. Class F shares were offered beginning September 1, 1993. Class Y shares were offered beginning October 30, 2015. Class Y shares performance for the period prior to October 30, 2015 is derived from the performance of Class F shares. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

11 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FUND PERFORMANCE

September 30, 2020 (Unaudited)

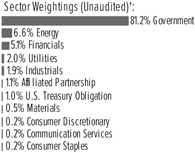

Emerging Markets Debt Fund

I. Objective

The Emerging Markets Debt Fund (the “Fund”) seeks to maximize total return.

II. Multi-Manager Approach

The Fund uses a multi-manager approach, relying on a number of sub-advisors with differing investment approaches to manage portions of the Fund’s portfolio, under the general supervision of SEI Investments Management Corp. (“SIMC”). The Fund utilized the following sub-advisors as of September 30, 2020: Colchester Global Investors Limited (“Colchester”), Marathon Asset Management, L.P. (“Marathon”), Neuberger Berman Investment Advisers LLC (“Neuberger Berman”), Ninety One UK Ltd (fka Investec Asset Management Ltd.) (“Ninety One”) and Stone Harbor Investment Partners LP (“Stone Harbor”).

No manager changes were made during the Fund’s fiscal year.

III. Return vs. Benchmark

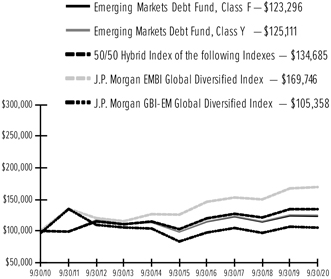

For the year ended September 30, 2020, the Fund’s Class F shares underperformed a hybrid of 50% JP Morgan EMBI Global Diversified Index (which tracks the performance of external debt instruments in the emerging markets) and 50% JP Morgan GBI-EM Global Diversified Index (which tracks the performance of debt instruments issued in domestic currencies by emerging-market governments), returning -0.53% versus the Index return of -0.02%.

IV. Fund Attribution

Emerging markets began the period strongly, with both hard- and local-currency indexes posting positive returns in the fourth quarter of 2019. Emerging-market debt benefited from positive growth with high real yields and (relatively) attractive spreads, providing positive carry through the end of the calendar year.

The severity of the COVID-19 pandemic began to be realized around mid-February. Much of the damage was done by late March, with spread assets repricing two to three times wider. Emerging-market governments responded to the global slowdown and local lockdowns with fiscal packages aimed at providing help to local businesses and consumers alike (though these fiscal packages were modest in size compared to those seen in developed markets), and central banks slashed policy rates to spur consumption; some also implemented asset purchase programs aimed at maintaining liquidity.

Hard-currency markets, as represented by the JP Morgan EMBI Global Diversified Index, saw spreads widen from under 300 basis points over U.S. Treasurys in February to slightly over 700 basis points at peak crisis in March. The ensuing recovery was mostly concentrated in higher-quality assets. The spread of the investment-grade portion of the index ended February at 196 basis points, widened to more than 400 basis points during March, and ended September back at 196 basis points. Sub-investment-grade spreads remained more than 150 basis points wider at the end of the fiscal year than where they stood at the end of February, a sign that investors remained uncomfortable moving into the riskier names of an already risky asset class.

Local rates provided a positive absolute return for the year as inflation continued to be benign and many emerging-market central banks cut policy rates in response to local lockdowns and the slowdown in global trade. Virtually every country in JP Morgan’s local-currency index saw its central bank cut its policy rate at least one time since February, though most cut rates at least twice. In all, central banks of local-index countries produced more than 50 rate cuts since February. Unlike local rates, emerging-market currencies have experienced significant weakening since the coronavirus pandemic. Many currencies weakened more than 10% to the U.S. dollar and, although they have recovered somewhat in the months since the pandemic’s initial outbreak, a majority of currencies in the local index are weaker on a 12-month basis.

The Fund underperformed its blended benchmark during the fiscal year. Overweights to Venezuela (which continued to experience a political crisis along with U.S. sanctions) and the Russian ruble (which weakened over the period with the twin problems of an economic slowdown and lower oil prices) detracted over the period. An underweight to the Polish zloty and positioning in South Africa (which was experiencing fiscal difficulties before the coronavirus slowdown began) further weakened Fund performance. Argentina and Ecuador contributed to performance as each country reached a debt restructuring deal with creditors over the summer of 2020. An underweight to Turkey (where questionable governance at the central bank produced low policy rates despite an economy dogged by high inflation) also contributed to relative return.

Colchester outperformed its local-currency benchmark, benefiting from overweights to Mexico and Colombia, but detracted from overall Fund performance due to its overweight to Brazil and underweight to Poland. Ninety One also outperformed its local-currency benchmark,

12 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

benefiting from an off-benchmark position to Egypt and an underweight to Turkey, but detracted from overall Fund performance due to positioning in South Africa and an underweight to Poland.

Stone Harbor outperformed and benefited from overweights to Ecuador and Mexico; the manager was hurt by exposure to Venezuela and an underweight to China. Marathon outperformed and was helped by an off-benchmark position in Israel and security selection in Ecuador, while exposure to Venezuela and an underweight to Saudi Arabia detracted. Neuberger Berman also outperformed thanks to overweights to Argentina and Egypt, while exposure to South Africa and Turkey detracted.

Currency forwards and swap contracts were used in the Fund for the one-year period ending September 30, 2020, as a way to either hedge particular positions or gain exposure to additional areas of the market. Currency forwards had a material impact on the Fund during the period as 50% of the Index is directly affected by foreign currencies. Positive and negative impacts differed on a country-to-country basis, depending on whether the forward increased or decreased currency exposure and whether the currency strengthened or weakened relative to the U.S. dollar.

Investing is subject to risk, including the possible loss of principal. Past performance is no indication of future results.

AVERAGE ANNUAL TOTAL RETURN1

1 Year | Annualized 3 Year | Annualized 5 Year Return | Annualized 10 Year Return | Annualized Inception to Date | ||||||||||||||||

| Emerging Markets Debt Fund, Class F | -0.53% | 0.19% | 4.60% | 2.12% | 7.16% | |||||||||||||||

| Emerging Markets Debt Fund, Class Y | -0.33% | 0.45% | 4.86% | 2.27% | 7.23% | |||||||||||||||

| JP Morgan EMBI Global Diversified Index | 1.29% | 3.49% | 6.15% | 5.43% | 8.06% | |||||||||||||||

| JP Morgan GBI-EM Global Diversified Index | -1.45% | 0.17% | 4.78% | 0.52% | N/A | |||||||||||||||

| 50/50 Hybrid of the JP Morgan EMBI Global Diversified Index and the JP Morgan GBI-EM Global Diversified Index | -0.02% | 1.89% | 5.53% | 3.02% | N/A | |||||||||||||||

Comparison of Change in the Value of a $100,000 Investment in the Emerging Markets Debt Fund, Class F and Class Y, versus a 50/50 Hybrid of the Following Indexes: the JP Morgan EMBI Global Diversified Index and the JP Morgan GBI-EM Global Diversified Index

| ¹ | For the year ended September 30, 2020. Past performance is no indication of future performance. Class F shares were offered beginning June 26, 1997. The Fund’s Class Y shares commenced operations on December 31, 2014. For periods prior to December 31, 2014, the performance of the Fund’s Class F Shares has been used. Returns for Class Y Shares would have been substantially similar to those of Class F shares and would have differed only to the extent that Class Y shares have lower total annual fund operating expenses than Class F shares. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The returns for the period reflect fee waivers and/or reimbursements in effect for the period; absent fee waivers and reimbursements, performance would have been lower. |

N/A — Not Available.

SEI Institutional International Trust / Annual Report / September 30, 2020 |

13 |

September 30, 2020

International Equity Fund

†Percentages based on total investments. Includes investments held as collateral for securities on loan (see Note 9).

Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK — 94.1% | ||||||||

Argentina — 0.5% | ||||||||

MercadoLibre Inc * | 17,228 | $ | 18,649 | |||||

|

|

| ||||||

Australia — 3.2% | ||||||||

a2 Milk Co Ltd/The *(A) | 1,652,395 | 16,737 | ||||||

Australia & New Zealand Banking Group Ltd | 125,050 | 1,551 | ||||||

Avita Therapeutics Inc * | 199,996 | 990 | ||||||

BlueScope Steel Ltd | 896,249 | 8,179 | ||||||

Brambles Ltd | 224,767 | 1,707 | ||||||

Coles Group Ltd | 37,256 | 456 | ||||||

CSL Ltd | 83,863 | 17,347 | ||||||

CSR Ltd | 792,249 | 2,430 | ||||||

Evolution Mining Ltd | 849,680 | 3,512 | ||||||

Fortescue Metals Group Ltd | 1,647,033 | 19,346 | ||||||

Harvey Norman Holdings Ltd | 896,394 | 2,925 | ||||||

Iluka Resources Ltd | 221,712 | 1,434 | ||||||

Newcrest Mining Ltd | 712,097 | 15,960 | ||||||

Orica Ltd | 318,520 | 3,529 | ||||||

Orora Ltd | 1,270,565 | 2,199 | ||||||

OZ Minerals Ltd | 349,366 | 3,528 | ||||||

Rio Tinto Ltd | 202,214 | 13,723 | ||||||

South32 Ltd | 6,544,807 | 9,649 | ||||||

Technology One Ltd | 57,602 | 329 | ||||||

Wesfarmers Ltd | 26,392 | 844 | ||||||

|

|

| ||||||

| 126,375 | ||||||||

|

|

| ||||||

Austria — 0.2% | ||||||||

BAWAG Group AG | 161,151 | 5,823 | ||||||

Verbund AG, Cl A | 37,632 | 2,058 | ||||||

|

|

| ||||||

| 7,881 | ||||||||

|

|

| ||||||

Belgium — 1.2% | ||||||||

Ageas SA/NV | 495,494 | 20,274 | ||||||

Colruyt SA | 58,532 | 3,798 | ||||||

Groupe Bruxelles Lambert SA | 145,793 | 13,167 | ||||||

UCB SA | 48,928 | 5,555 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Umicore SA | 91,664 | $ | 3,804 | |||||

|

|

| ||||||

| 46,598 | ||||||||

|

|

| ||||||

Canada — 1.2% | ||||||||

Air Canada, Cl A * | 543,100 | 6,379 | ||||||

BRP Inc * | 10,000 | 527 | ||||||

Canadian Pacific Railway Ltd | 53,934 | 16,419 | ||||||

Dollarama Inc | 75,700 | 2,893 | ||||||

Nutrien Ltd (A) | 339,890 | 13,285 | ||||||

Stantec Inc (A) | 68,200 | 2,064 | ||||||

Sun Life Financial Inc | 150,900 | 6,130 | ||||||

|

|

| ||||||

| 47,697 | ||||||||

|

|

| ||||||

China — 1.5% | ||||||||

Baidu Inc ADR * | 232,815 | 29,472 | ||||||

Beijing Capital International Airport Co Ltd, Cl H | 5,718,000 | 3,447 | ||||||

China Communications Services Corp Ltd, Cl H | 4,389,584 | 2,591 | ||||||

China Lesso Group Holdings Ltd | 327,000 | 593 | ||||||

Industrial & Commercial Bank of China Ltd, Cl H | 9,454,000 | 4,932 | ||||||

STMicroelectronics NV | 48,311 | 1,486 | ||||||

Tencent Holdings Ltd | 233,100 | 15,717 | ||||||

|

|

| ||||||

| 58,238 | ||||||||

|

|

| ||||||

Denmark — 3.1% | ||||||||

Ambu A/S, Cl B (A) | 47,633 | 1,347 | ||||||

AP Moller - Maersk A/S, Cl B | 1,656 | 2,625 | ||||||

Carlsberg AS, Cl B | 95,260 | 12,840 | ||||||

DSV PANALPINA A/S | 113,970 | 18,522 | ||||||

Genmab A/S * | 6,406 | 2,320 | ||||||

H Lundbeck A/S | 151,129 | 4,985 | ||||||

Novo Nordisk A/S, Cl B | 429,553 | 29,697 | ||||||

Novozymes A/S, Cl B | 16,007 | 1,004 | ||||||

Orsted A/S | 73,960 | 10,152 | ||||||

Pandora A/S * | 43,948 | 3,147 | ||||||

ROCKWOOL International A/S, Cl B | 18,518 | 7,091 | ||||||

Scandinavian Tobacco Group A/S | 644,917 | 9,567 | ||||||

Vestas Wind Systems A/S | 118,670 | 19,181 | ||||||

|

|

| ||||||

| 122,478 | ||||||||

|

|

| ||||||

Finland — 1.1% | ||||||||

Kone Oyj, Cl B | 167,622 | 14,722 | ||||||

Neste Oyj | 146,007 | 7,669 | ||||||

Nokia Oyj * | 1,229,753 | 4,818 | ||||||

Nokia Oyj ADR * | 1,095,554 | 4,284 | ||||||

Orion Oyj, Cl B | 207,978 | 9,399 | ||||||

Stora Enso Oyj, Cl R | 131,736 | 2,059 | ||||||

|

|

| ||||||

| 42,951 | ||||||||

|

|

| ||||||

France — 8.6% | ||||||||

Air France-KLM *(A) | 201,300 | 696 | ||||||

Airbus SE * | 163,947 | 11,928 | ||||||

Amundi SA * | 54,884 | 3,873 | ||||||

14 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

AXA SA | 615,052 | $ 11,343 | ||||||

BioMerieux | 4,660 | 730 | ||||||

BNP Paribas SA | 556,412 | 20,173 | ||||||

Bollore SA | 2,803,117 | 10,462 | ||||||

Carrefour SA | 1,421,223 | 22,769 | ||||||

Cie de Saint-Gobain * | 88,633 | 3,728 | ||||||

Cie Generale des Etablissements Michelin SCA, Cl B | 7,894 | 842 | ||||||

CNP Assurances * | 112,984 | 1,412 | ||||||

Credit Agricole SA * | 1,023,476 | 8,957 | ||||||

Criteo SA ADR * | 60,571 | 738 | ||||||

Danone SA | 165,707 | 10,703 | ||||||

Edenred | 81,226 | 3,649 | ||||||

Engie SA * | 1,213,062 | 16,222 | ||||||

EssilorLuxottica SA * | 54,965 | 7,477 | ||||||

Iliad SA | 761 | 140 | ||||||

Ipsen SA | 45,627 | 4,784 | ||||||

IPSOS | 18,645 | 467 | ||||||

L’Oreal SA | 30,317 | 9,857 | ||||||

LVMH Moet Hennessy Louis Vuitton SE | 30,077 | 14,067 | ||||||

Nexans SA * | 25,765 | 1,489 | ||||||

Pernod Ricard SA | 48,610 | 7,756 | ||||||

Peugeot SA * | 447,567 | 8,116 | ||||||

Publicis Groupe SA | 381,789 | 12,342 | ||||||

Renault SA * | 107,400 | 2,788 | ||||||

Rexel SA * | 527,080 | 6,628 | ||||||

Sanofi | 505,274 | 50,526 | ||||||

Sartorius Stedim Biotech | 24,563 | 8,478 | ||||||

Schneider Electric SE | 78,011 | 9,670 | ||||||

Thales SA | 215,152 | 16,193 | ||||||

TOTAL SE | 380,375 | 12,980 | ||||||

Ubisoft Entertainment SA * | 78,877 | 7,118 | ||||||

Valeo SA | 153,850 | 4,728 | ||||||

Vinci SA | 113,140 | 9,473 | ||||||

Vivendi SA | 308,400 | 8,578 | ||||||

Wendel SE | 15,501 | 1,408 | ||||||

|

|

| ||||||

| 333,288 | ||||||||

|

|

| ||||||

Germany — 8.5% | ||||||||

adidas AG * | 27,977 | 9,029 | ||||||

Allianz SE | 106,120 | 20,359 | ||||||

BASF SE | 395,561 | 24,049 | ||||||

Bayer AG | 508,676 | 31,330 | ||||||

Bayerische Motoren Werke AG | 62,482 | 4,525 | ||||||

CECONOMY AG * | 237,111 | 1,167 | ||||||

Deutsche Boerse AG | 56,898 | 9,977 | ||||||

Deutsche Post AG | 1,078,925 | 49,071 | ||||||

E.ON SE | 431,930 | 4,763 | ||||||

Evonik Industries AG | 50,057 | 1,296 | ||||||

Fresenius Medical Care AG & Co KGaA | 219,531 | 18,533 | ||||||

Hamburger Hafen und Logistik AG | 24,359 | 427 | ||||||

Hannover Rueck SE | 7,749 | 1,197 | ||||||

HeidelbergCement AG | 22,099 | 1,352 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

HelloFresh SE * | 138,970 | $ 7,755 | ||||||

Infineon Technologies AG | 609,071 | 17,132 | ||||||

KION Group AG | 111,152 | 9,495 | ||||||

Linde PLC | 68,010 | 16,077 | ||||||

Rheinmetall AG | 49,680 | 4,468 | ||||||

RWE AG | 277,463 | 10,378 | ||||||

SAP SE | 204,390 | 31,769 | ||||||

Scout24 AG | 22,886 | 1,998 | ||||||

Siemens AG | 402,821 | 50,900 | ||||||

Siemens Energy AG * | 201,411 | 5,432 | ||||||

thyssenkrupp AG * | 26,790 | 135 | ||||||

|

|

| ||||||

| 332,614 | ||||||||

|

|

| ||||||

Greece — 0.0% | ||||||||

Aegean Airlines SA * | 12,601 | 46 | ||||||

National Bank of Greece SA * | 89,899 | 114 | ||||||

|

|

| ||||||

| 160 | ||||||||

|

|

| ||||||

Hong Kong — 1.9% | ||||||||

AIA Group Ltd | 1,451,200 | 14,386 | ||||||

BOC Hong Kong Holdings Ltd | 385,000 | 1,024 | ||||||

Chaoda Modern Agriculture Holdings Ltd * | 2,440,000 | 16 | ||||||

CITIC Ltd | 839,084 | 620 | ||||||

CK Hutchison Holdings Ltd | 194,500 | 1,178 | ||||||

Country Garden Services Holdings Co Ltd | 402,000 | 2,604 | ||||||

Hong Kong Exchanges & Clearing Ltd | 325,734 | 15,358 | ||||||

Lenovo Group Ltd | 2,622,000 | 1,739 | ||||||

Link REIT ‡ | 293,100 | 2,399 | ||||||

Nine Dragons Paper Holdings Ltd | 1,683,000 | 2,133 | ||||||

Power Assets Holdings Ltd | 10,000 | 53 | ||||||

Sands China Ltd * | 1,242,800 | 4,840 | ||||||

SJM Holdings Ltd | 8,483,340 | 10,119 | ||||||

Techtronic Industries Co Ltd | 444,000 | 5,914 | ||||||

Topsports International Holdings Ltd | 5,332,000 | 7,428 | ||||||

West China Cement Ltd | 3,744,000 | 557 | ||||||

Wharf Real Estate Investment Co Ltd | 166,000 | 680 | ||||||

Zoomlion Heavy Industry Science and Technology Co Ltd | 1,226,800 | 1,189 | ||||||

|

|

| ||||||

| 72,237 | ||||||||

|

|

| ||||||

India — 0.2% | ||||||||

HDFC Bank Ltd ADR * | 180,834 | 9,034 | ||||||

|

|

| ||||||

Ireland — 1.5% | ||||||||

Experian PLC | 409,652 | 15,433 | ||||||

ICON PLC * | 158,190 | 30,229 | ||||||

Ryanair Holdings PLC * | 59,824 | 797 | ||||||

Ryanair Holdings PLC ADR * | 156,760 | 12,817 | ||||||

|

|

| ||||||

| 59,276 | ||||||||

|

|

| ||||||

Israel — 0.8% | ||||||||

Bank Leumi Le-Israel BM | 1,668,755 | 7,381 | ||||||

Check Point Software Technologies Ltd * | 100,467 | 12,090 | ||||||

Isracard Ltd | – | – | ||||||

Mizrahi Tefahot Bank Ltd | 30,121 | 536 | ||||||

SEI Institutional International Trust / Annual Report / September 30, 2020 |

15 |

SCHEDULE OF INVESTMENTS

September 30, 2020

International Equity Fund (Continued)

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Nice Ltd * | 9,345 | $ | 2,123 | |||||

Nice Ltd ADR *(A) | 41,714 | 9,470 | ||||||

|

|

| ||||||

| 31,600 | ||||||||

|

|

| ||||||

Italy — 2.7% | ||||||||

A2A SpA | 293,978 | 428 | ||||||

Assicurazioni Generali SpA | 819,445 | 11,537 | ||||||

Banca Mediolanum SpA | 299,871 | 2,158 | ||||||

De’ Longhi SpA * | 2,846 | 97 | ||||||

Enel SpA | 1,195,704 | 10,378 | ||||||

EXOR NV | 115,844 | 6,309 | ||||||

Ferrari NV | 54,815 | 10,059 | ||||||

Fiat Chrysler Automobiles NV * | 495,169 | 6,073 | ||||||

FinecoBank Banca Fineco SpA * | 669,767 | 9,246 | ||||||

Hera SpA | 636,483 | 2,353 | ||||||

Pirelli & C SpA * | 1,251,944 | 5,370 | ||||||

Recordati Industria Chimica e Farmaceutica SpA | 181,268 | 9,287 | ||||||

Telecom Italia SpA/Milano | 6,763,117 | 2,721 | ||||||

Tenaris SA | 888,739 | 4,430 | ||||||

UniCredit SpA * | 2,842,801 | 23,463 | ||||||

|

|

| ||||||

| 103,909 | ||||||||

|

|

| ||||||

Japan — 18.7% | ||||||||

77 Bank Ltd/The | 33,364 | 515 | ||||||

Advantest Corp | 208,000 | 10,087 | ||||||

AEON Financial Service Co Ltd | 29,500 | 268 | ||||||

Arcland Sakamoto Co Ltd | 33,873 | 694 | ||||||

ASKUL Corp | 14,400 | 588 | ||||||

Bandai Namco Holdings Inc | 76,600 | 5,601 | ||||||

Canon Marketing Japan Inc | 106,500 | 2,125 | ||||||

Capcom Co Ltd | 193,300 | 10,797 | ||||||

Chugai Pharmaceutical Co Ltd | 132,300 | 5,931 | ||||||

CyberAgent Inc | 167,800 | 10,364 | ||||||

Dai Nippon Printing Co Ltd | 491,900 | 9,959 | ||||||

Daifuku Co Ltd | 10,300 | 1,037 | ||||||

Daito Trust Construction Co Ltd | 81,900 | 7,252 | ||||||

Daiwa House Industry Co Ltd | 290,800 | 7,456 | ||||||

Disco Corp | 800 | 194 | ||||||

East Japan Railway Co | 129,200 | 7,940 | ||||||

FANUC Corp | 102,200 | 19,674 | ||||||

Fuji Electric Co Ltd | 36,800 | 1,163 | ||||||

FUJIFILM Holdings Corp | 213,800 | 10,536 | ||||||

Fujitsu Ltd | 258,100 | 35,298 | ||||||

Glory Ltd | 57,200 | 1,273 | ||||||

Hakuhodo DY Holdings Inc | 106,900 | 1,380 | ||||||

Haseko Corp | 231,200 | 3,033 | ||||||

Hikari Tsushin Inc | 3,700 | 879 | ||||||

Hitachi Ltd | 369,667 | 12,509 | ||||||

ITOCHU Corp | 207,800 | 5,310 | ||||||

Itoki Corp | 21,300 | 73 | ||||||

Japan Airlines Co Ltd * | 319,000 | 5,972 | ||||||

Japan Exchange Group Inc | 364,400 | 10,164 | ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Japan Post Holdings Co Ltd * | 313,900 | $ | 2,135 | |||||

Japan Post Insurance Co Ltd | 45,200 | 710 | ||||||

Kao Corp | 124,200 | 9,294 | ||||||

KDDI Corp | 430,900 | 10,858 | ||||||

Keyence Corp | 28,200 | 13,134 | ||||||

Kokuyo Co Ltd | 103,900 | 1,303 | ||||||

Komatsu Ltd | 447,900 | 9,844 | ||||||

Konami Holdings Corp | 132,000 | 5,705 | ||||||

K’s Holdings Corp | 82,700 | 1,115 | ||||||

Kyocera Corp | 60,700 | 3,466 | ||||||

Kyowa Kirin Co Ltd | 223,400 | 6,347 | ||||||

Lion Corp | 41,300 | 849 | ||||||

Mabuchi Motor Co Ltd | 389,800 | 15,123 | ||||||

Mebuki Financial Group Inc | 77,900 | 176 | ||||||

Mitsubishi Electric Corp | 294,600 | 3,988 | ||||||

Mitsubishi Estate Co Ltd | 556,000 | 8,375 | ||||||

Mixi Inc (A) | 121,300 | 3,257 | ||||||

Mizuno Corp * | 41,500 | 750 | ||||||

MS&AD Insurance Group Holdings Inc | 671,000 | 17,987 | ||||||

Murata Manufacturing Co Ltd | 266,100 | 17,168 | ||||||

Nexon Co Ltd | 293,600 | 7,314 | ||||||

Nihon Unisys Ltd | 159,700 | 5,031 | ||||||

Nikon Corp | 90,100 | 606 | ||||||

Nintendo Co Ltd | 39,100 | 22,187 | ||||||

Nippon Telegraph & Telephone Corp | 585,800 | 11,933 | ||||||

Nippon Telegraph & Telephone Corp ADR | 840,932 | 17,374 | ||||||

Nitori Holdings Co Ltd | 38,800 | 8,054 | ||||||

Nitto Denko Corp | 44,100 | 2,874 | ||||||

Nomura Holdings Inc | 537,100 | 2,437 | ||||||

NTT DOCOMO Inc | 475,200 | 17,512 | ||||||

ORIX Corp | 672,800 | 8,349 | ||||||

Otsuka Corp | 199,100 | 10,181 | ||||||

Panasonic Corp | 1,264,500 | 10,705 | ||||||

PeptiDream Inc * | 221,200 | 10,352 | ||||||

Persol Holdings Co Ltd * | 139,100 | 2,263 | ||||||

Rakuten Inc * | 906,100 | 9,770 | ||||||

Recruit Holdings Co Ltd * | 278,700 | 11,111 | ||||||

Renesas Electronics Corp * | 32,900 | 240 | ||||||

Rohm Co Ltd | 200,800 | 15,480 | ||||||

Sankyo Co Ltd | 103,300 | 2,708 | ||||||

Sanwa Holdings Corp | 178,600 | 1,896 | ||||||

SBI Holdings Inc/Japan | 518,000 | 13,398 | ||||||

Secom Co Ltd | 52,400 | 4,791 | ||||||

Seiko Holdings Corp * | 42,200 | 569 | ||||||

Sekisui House Ltd | 745,614 | 13,146 | ||||||

Seria Co Ltd | 7,600 | 323 | ||||||

Seven & i Holdings Co Ltd | 494,900 | 15,293 | ||||||

Shin-Etsu Chemical Co Ltd | 88,086 | 11,490 | ||||||

Shiseido Co Ltd | 135,700 | 7,780 | ||||||

Sompo Holdings Inc | 197,500 | 6,801 | ||||||

Sony Corp ADR | 77,850 | 5,975 | ||||||

Sumitomo Dainippon Pharma Co Ltd | 96,100 | 1,267 | ||||||

16 |

SEI Institutional International Trust / Annual Report / September 30, 2020 |

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

Sumitomo Mitsui Financial Group Inc | 317,400 | $ | 8,811 | |||||

Sumitomo Mitsui Trust Holdings Inc | 365,822 | 9,708 | ||||||

Suruga Bank Ltd | 45,700 | 165 | ||||||

Suzuki Motor Corp * | 151,937 | 6,490 | ||||||

Sysmex Corp | 2,600 | 248 | ||||||

T&D Holdings Inc | 257,000 | 2,523 | ||||||

Takeda Pharmaceutical Co Ltd | 1,077,400 | 38,421 | ||||||

TDK Corp | 24,500 | 2,674 | ||||||

Terumo Corp | 250,900 | 9,985 | ||||||

TIS Inc | 238,900 | 5,062 | ||||||

Tokyo Electric Power Co Holdings Inc * | 1,117,600 | 3,074 | ||||||

Tokyo Electron Ltd (A) | 49,700 | 12,958 | ||||||

Tomy Co Ltd | 135,700 | 1,166 | ||||||

Toppan Printing Co Ltd | 92,600 | 1,303 | ||||||

Toshiba Corp | 142,000 | 3,607 | ||||||

Toyo Suisan Kaisha Ltd | 36,600 | 1,935 | ||||||

Toyota Industries Corp | 110,578 | 6,982 | ||||||

Toyota Motor Corp ADR (A) | 115,231 | 15,261 | ||||||

Universal Entertainment * | 317,053 | 5,808 | ||||||

Yamada Holdings Co Ltd | 296,800 | 1,478 | ||||||

Z Holdings Corp * | 1,632,900 | 10,873 | ||||||

ZOZO Inc | 95,500 | 2,662 | ||||||

|

|

| ||||||

| 730,060 | ||||||||

|

|

| ||||||

Malta — 0.0% | ||||||||

BGP Holdings *(B) | 198,683 | – | ||||||

|

|

| ||||||

Mexico — 0.3% | ||||||||

Arca Continental SAB de CV | 1,940,380 | 8,378 | ||||||

Grupo Financiero Banorte SAB de CV, Cl O * | 1,077,720 | 3,729 | ||||||

|

|

| ||||||

| 12,107 | ||||||||

|

|

| ||||||

Netherlands — 6.3% | ||||||||

Aalberts NV | 44,615 | 1,609 | ||||||

Adyen NV * | 4,775 | 8,799 | ||||||

Akzo Nobel NV | 357,544 | 36,264 | ||||||

ArcelorMittal SA * | 299,342 | 4,003 | ||||||

ASML Holding NV | 26,828 | 9,896 | ||||||

ASR Nederland NV | 180,815 | 6,100 | ||||||

Galapagos NV * | 19,180 | 2,726 | ||||||

ING Groep NV * | 5,070,405 | 36,025 | ||||||

Koninklijke Ahold Delhaize NV | 963,857 | 28,556 | ||||||

Koninklijke DSM NV | 135,711 | 22,373 | ||||||

Koninklijke Philips NV * | 303,632 | 14,292 | ||||||

Koninklijke Vopak NV | 43,888 | 2,476 | ||||||

NN Group NV | 128,474 | 4,823 | ||||||

PostNL NV * | 1,207,552 | 3,688 | ||||||

Prosus NV * | 103,775 | 9,584 | ||||||

Randstad NV * | 153,948 | 8,034 | ||||||

Royal Dutch Shell PLC ADR, Cl B | 429,732 | 10,408 | ||||||

Wolters Kluwer NV | 436,924 | 37,286 | ||||||

|

|

| ||||||

| 246,942 | ||||||||

|

|

| ||||||

| Description | Shares | Market Value ($ Thousands) | ||||||

COMMON STOCK (continued) | ||||||||

New Zealand — 0.3% | ||||||||

a2 Milk Co Ltd/The * | 569,604 | $ | 5,783 | |||||

Fisher & Paykel Healthcare Corp Ltd | 175,906 | 3,861 | ||||||

|

|

| ||||||

| 9,644 | ||||||||

|

|

| ||||||

Norway — 0.8% | ||||||||

Aker BioMarine AS * | 47,749 | 475 | ||||||

Atlantic Sapphire ASA * | 1,293,932 | 15,224 | ||||||

Equinor ASA | 544,173 | 7,708 | ||||||

Kahoot! AS * | 1,409,188 | 6,469 | ||||||

|

|

| ||||||

| 29,876 | ||||||||

|

|

| ||||||

Portugal — 0.0% | ||||||||

EDP - Energias de Portugal SA | 305,767 | 1,503 | ||||||

|

|

| ||||||

Singapore — 0.7% | ||||||||

City Developments Ltd | 1,883,900 | 10,558 | ||||||

DBS Group Holdings Ltd | 467,400 | 6,864 | ||||||

Hong Leong Finance Ltd | 61,282 | 102 | ||||||

Oversea-Chinese Banking Corp Ltd | 1,022,635 | 6,350 | ||||||

Venture Corp Ltd | 83,000 | 1,174 | ||||||

|

|

| ||||||

| 25,048 | ||||||||

|

|

| ||||||

South Africa — 0.0% | ||||||||

DataTec Ltd * | 100,188 | 133 | ||||||

Investec PLC | 416,323 | 775 | ||||||

|

|

| ||||||