[ANNOTATED FORM N-CSR FOR ANNUAL REPORTS]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-05624 | |||||||

| ||||||||

Morgan Stanley Institutional Fund, Inc. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

1221 Avenue of the Americas 22nd Floor New York, NY |

| 10020 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Ronald E. Robison | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 1-800-221-6726 |

| ||||||

| ||||||||

Date of fiscal year end: | 12/31 |

| ||||||

| ||||||||

Date of reporting period: | 12/31/05 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The Fund’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

| 2005 Annual Report |

| |

December 31, 2005 |

Morgan Stanley Institutional Fund, Inc.

Global and International Equity Portfolios |

| Fixed Income Portfolio |

|

|

|

Active International Allocation |

| Emerging Markets Debt |

Emerging Markets |

|

|

Global Franchise |

| Money Market Portfolios |

Global Value Equity |

|

|

International Equity |

| Money Market |

International Growth Equity |

| Municipal Money Market |

International Magnum |

|

|

International Real Estate |

|

|

International Small Cap |

|

|

|

|

|

U.S. Equity Portfolios |

|

|

|

|

|

Focus Equity |

|

|

Large Cap Relative Value |

|

|

Small Company Growth |

|

|

U.S. Large Cap Growth |

|

|

U.S. Real Estate |

|

|

2005 Annual Report |

|

December 31, 2005 |

Table of Contents

Shareholder’s Letter |

| 3 |

Performance Summary |

| 4 |

Investment Overview and Portfolios of Investments |

|

|

Global and International Equity Portfolios: |

|

|

Active International Allocation |

| 6 |

Emerging Markets |

| 20 |

Global Franchise |

| 27 |

Global Value Equity |

| 31 |

International Equity |

| 37 |

International Growth Equity |

| 42 |

International Magnum |

| 46 |

International Real Estate |

| 53 |

International Small Cap |

| 58 |

|

|

|

U.S. Equity Portfolios: |

|

|

Focus Equity |

| 63 |

Large Cap Relative Value |

| 67 |

Small Company Growth |

| 72 |

U.S. Large Cap Growth |

| 77 |

U.S. Real Estate |

| 82 |

|

|

|

Fixed Income Portfolio: |

|

|

Emerging Markets Debt |

| 87 |

|

|

|

Money Market Portfolios: |

|

|

Money Market |

| 93 |

Municipal Money Market |

| 96 |

|

|

|

Statements of Assets and Liabilities |

| 101 |

Statements of Operations |

| 105 |

Statements of Changes in Net Assets |

| 109 |

Financial Highlights |

| 117 |

Notes to Financial Statements |

| 133 |

Report of Independent Registered |

|

|

Public Accounting Firm |

| 143 |

Federal Income Tax Information |

| 144 |

Director and Officer Information |

| 146 |

This report is authorized for distribution only when preceded or accompanied by prospectuses of the Morgan Stanley Institutional Fund, Inc. To receive a prospectus and/or SAI, which contains more complete information such as investment objectives, charges, expenses, policies for voting proxies, risk considerations, and describes in detail each of the Portfolio’s investment policies to the prospective investor, please call 1-(800)-548-7786. Please read the prospectuses carefully before you invest or send money. Additionally, you can access portfolio information including performance, characteristics, and investment team commentary through Morgan Stanley Investment Management’s website: www.morganstanley.com/im.

1

| 2005 Annual Report |

| |

December 31, 2005 |

Shareholder’s Letter

Dear Shareholders:

We are pleased to present to you the Fund’s Annual Report for the year ended December 31, 2005. Our Fund currently offers 17 portfolios providing investors with a full array of global and domestic equity and fixed-income products. The Fund’s portfolios, together with the portfolios of the Morgan Stanley Institutional Fund Trust, provide investors with a means to help them meet specific investment needs and to allocate their investments among equities (e.g., value and growth; small, medium, and large capitalization), fixed income (e.g., short, medium, and long duration; investment grade and high yield) and cash (e.g., money market).

Sincerely,

Ronald E. Robison

President and Principal Executive Officer

January 2006

2 |

|

2005 Annual Report |

|

December 31, 2005 |

Performance Summary

|

| Inception Dates |

|

|

| One Year |

| ||||||||

|

| Class A |

| Class B |

| Class A | Class B | Comparable |

| ||||||

Global and International Equity Portfolios: |

|

|

|

|

|

|

|

|

|

| |||||

Active International Allocation |

| 1/17/92 |

| 1/2/96 |

| 14.85 | % | 14.67 | % | 13.54 | % | (1) | |||

Emerging Markets |

| 9/25/92 |

| 1/2/96 |

| 34.54 |

| 34.17 |

| 34.00 | (2) | ||||

Global Franchise |

| 11/28/01 |

| 11/28/01 |

| 11.91 |

| 11.53 |

| 9.49 | (4) | ||||

Global Value Equity |

| 7/15/92 |

| 1/2/96 |

| 5.81 |

| 5.59 |

| 9.49 | (4) | ||||

International Equity |

| 8/4/89 |

| 1/2/96 |

| 6.45 |

| 6.20 |

| 13.54 | (1) | ||||

International Growth Equity† |

| 12/27/05 |

| 12/27/05 |

| — |

| — |

| — | (1) | ||||

International Magnum |

| 3/15/96 |

| 3/15/96 |

| 11.35 |

| 11.04 |

| 13.54 | (1) | ||||

International Real Estate |

| 10/1/97 |

| 10/1/97 |

| 15.52 |

| 15.22 |

| 12.17 | (3) | ||||

International Small Cap |

| 12/15/92 |

| — |

| 13.07 |

| — |

| 26.19 | (5) | ||||

U.S. Equity Portfolios: |

|

|

|

|

|

|

|

|

|

|

| ||||

Focus Equity |

| 3/8/95 |

| 1/2/96 |

| 17.60 |

| 17.30 |

| 5.26 | (6) | ||||

Large Cap Relative Value |

| 1/31/90 |

| 1/2/96 |

| 10.07 |

| 9.81 |

| 7.05 | (9) | ||||

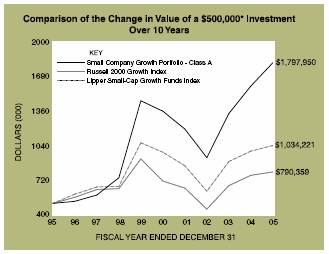

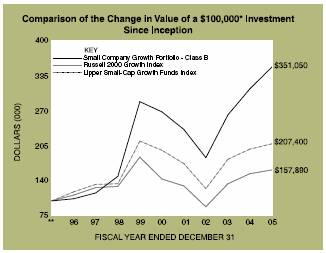

Small Company Growth |

| 11/1/89 |

| 1/2/96 |

| 13.55 |

| 13.35 |

| 4.15 | (7) | ||||

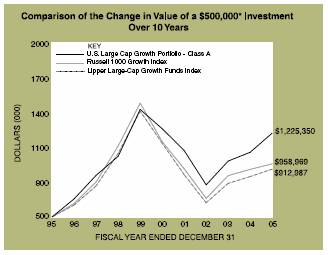

U.S. Large Cap Growth |

| 4/2/91 |

| 1/2/96 |

| 15.72 |

| 15.41 |

| 5.26 | (6) | ||||

U.S. Real Estate |

| 2/24/95 |

| 1/2/96 |

| 17.66 |

| 17.37 |

| 12.16 | (8) | ||||

Fixed Income Portfolio: |

|

|

|

|

|

|

|

|

|

|

| ||||

Emerging Markets Debt |

| 2/1/94 |

| 1/2/96 |

| 12.78 |

| 12.54 |

| 10.73 | (10) | ||||

Money Market Portfolios: |

|

|

|

|

|

|

|

|

|

|

| ||||

Money Market |

| 11/15/88 |

| — |

| — |

| — |

| — |

| ||||

Municipal Money Market |

| 2/10/89 |

| — |

| — |

| — |

| — |

| ||||

Yield Information as of December 31, 2005

|

| 7 Day | 7 Day | 30 Day | 30 Day |

|

|

| ||||

|

| Current | Effective | Current | Comparable |

|

|

| ||||

|

| Yield†† | Yield†† | Yield††† | Yield |

|

|

| ||||

Money Market Portfolios: |

|

|

|

|

|

|

|

|

|

|

| |

Money Market |

| 3.94 | % | 4.01 | % | 3.88 | % | 3.60 | % (11) |

|

| |

Municipal Money Market |

| 3.02 |

| 3.07 |

| 2.72 |

| 2.51 | (12) |

|

| |

† Performance figures are not supplied as the Portfolio commenced operations on December 27, 2005.

†† The 7 day current yield and 7 day effective yield assume an annualization of the current yield with all dividends reinvested. As with all money market portfolios, yields will fluctuate as market conditions change and the 7 day yields are not necessarily indicative of future performance.

††† The 30 day current yield reflects the net investment income generated by the Portfolio over a specified 30 day period expressed as an annual percentage. Expenses accrued for the 30 day period include any fees charged to all shareholders. Yields will fluctuate as market conditions change and are not necessarily indicative of future performance.

3

| 2005 Annual Report |

|

|

| December 31, 2005 |

Performance Summary (cont’d)

Five Year |

| Ten Year |

| Since Inception |

| ||||||||||||||||||||||||||

|

|

|

| Comparable |

|

|

|

|

| Comparable |

|

|

| Comparable |

|

|

| Comparable |

| ||||||||||||

Class A | Class B | Indices |

| Class A | Class B |

| Indices |

| Class A | Class A |

| Class B | Class B |

| |||||||||||||||||

5.08 | % | 4.82 | % | 4.55 | % | (1) | 7.14 | % | — |

| 5.84 | % | (1) | 7.51 | % | 7.02 | % | 6.88 | % | 5.83 | % | (1) | |||||||||

18.33 |

| 18.03 |

| 19.09 | (2) | 9.09 |

| — |

| 6.83 | (2) | 10.08 |

| 9.19 |

| 8.72 |

| 6.76 | (2) | ||||||||||||

— |

| — |

| — | (4) | — |

| — |

| — | (4) | 16.15 |

| 7.85 |

| 15.81 |

| 7.85 | (4) | ||||||||||||

3.40 |

| 3.13 |

| 2.18 | (4) | 9.12 |

| — |

| 7.04 | (4) | 11.39 |

| 8.58 |

| 8.78 |

| 6.99 | (4) | ||||||||||||

8.00 |

| 7.77 |

| 4.55 | (1) | 11.72 |

| — |

| 5.84 | (1) | 11.36 |

| 5.05 |

| 11.39 |

| 5.83 | (1) | ||||||||||||

— |

| — |

| — | (1) | — |

| — |

| — | (1) | — |

| — |

| — |

| — | (1) | ||||||||||||

3.70 |

| 3.42 |

| 4.55 | (1) | — |

| — |

| — | (1) | 5.30 |

| 6.00 |

| 5.02 |

| 6.00 | (1) | ||||||||||||

22.73 |

| 22.40 |

| 20.82 | (3) | — |

| — |

| — | (3) | 14.78 |

| 13.12 |

| 14.49 |

| 13.12 | (3) | ||||||||||||

15.38 |

| — |

| 16.04 | (5) | 12.84 |

| — |

| 5.95 | (5) | 13.64 |

| 7.57 |

| — |

| — | (5) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

(0.09) |

| (0.34 | ) | (3.58) | (6) | 10.80 |

| — |

| 6.73 | (6) | 13.51 |

| 8.77 |

| 10.47 |

| 6.65 | (6) | ||||||||||||

4.28 |

| 4.01 |

| 5.28 | (9) | 10.59 |

| — |

| 10.94 | (9) | 11.06 |

| 12.23 |

| 10.22 |

| 10.88 | (9) | ||||||||||||

5.89 |

| 5.65 |

| 2.28 | (7) | 13.65 |

| — |

| 4.69 | (7) | 13.54 |

| 7.35 |

| 13.38 |

| 4.68 | (7) | ||||||||||||

(0.60) |

| (0.86 | ) | (3.58) | (6) | 9.38 |

| — |

| 6.73 | (6) | 10.95 |

| 8.72 |

| 9.05 |

| 6.65 | (6) | ||||||||||||

19.46 |

| 19.11 |

| 19.08 | (8) | 17.12 |

| — |

| 14.50 | (8) | 17.73 |

| 14.76 |

| 16.71 |

| 14.51 | (8) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

14.43 |

| 14.19 |

| 12.25 | (10) | 12.59 |

| — |

| 12.99 | (10) | 11.37 |

| 11.01 |

| 12.23 |

| 12.86 | (10) | ||||||||||||

— |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| ||||||||||||

— |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| — |

| ||||||||||||

Performance data quoted assumes that all dividends and distributions, if any, were reinvested and represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the figures shown. For the most recent month-end performance figures, please visit www.morganstanley.com/im or call 1-800-548-7786. Investment returns and principal value will fluctuate and fund shares, when redeemed, may be worth more or less than their original cost.

Indices: | ||||

| ||||

(1) | MSCI EAFE (Europe, Australasia, and Far East) | (8) |

| National Association of Real Estate Investment Trusts (NAREIT) Equity |

(2) | MSCI Emerging Markets Free | (9) |

| Russell 1000 Value |

(3) | FTSE EPRA/NAREIT Global Real Estate Index | (10) |

| J.P. Morgan Emerging Markets Global Bond |

(4) | MSCI World | (11) |

| iMoneyNet Money Fund Comparable Yield |

(5) | MSCI EAFE Small Cap Total Return | (12) |

| iMoneyNet Municipal Money Fund Comparable Yield |

(6) | Russell 1000 Growth |

|

|

|

(7) | Russell 2000 Growth |

|

|

|

Investments in the Money Market or Municipal Money Market Portfolios are neither insured nor guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Money Market and Municipal Money Market Portfolios seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in these portfolios. Please read the Portfolios’ prospectuses carefully before you invest or send money.

4

2005 Annual Report | |

|

|

December 31, 2005 | |

Investment Overview

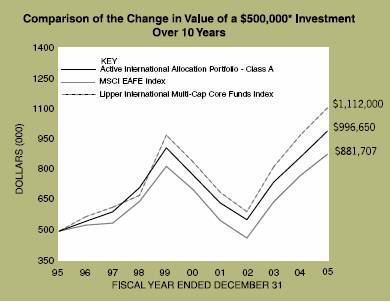

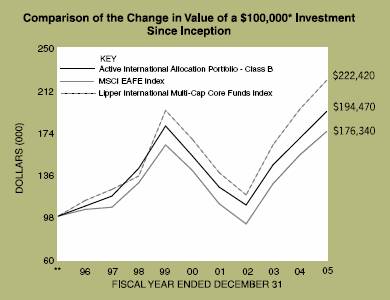

Active International Allocation Portfolio

* Minimum Investment

** Commenced offering on January 2, 1996.

In accordance with SEC regulations, Portfolio performance shown assumes that all recurring fees (including management fees) were deducted and all dividends and distributions were reinvested.

Performance Compared to the Morgan Stanley Capital International (MSCI) EAFE Index(1) and the Lipper International Multi-Cap Core Funds Index(2)

|

| Total Returns(3) |

| ||||||

|

|

|

| Average Annual |

| ||||

|

| One |

| Five | Ten |

| Since |

| |

Portfolio – Class A (4) |

| 14.85 | % | 5.08 | % | 7.14 | % | 7.51 | % |

MSCI EAFE Index |

| 13.54 |

| 4.55 |

| 5.84 |

| 7.02 |

|

Lipper International Multi-Cap |

|

|

|

|

|

|

|

|

|

Core Funds Index |

| 13.76 |

| 5.70 |

| 8.32 |

| — |

|

Portfolio – Class B (5) |

| 14.67 |

| 4.82 |

| — |

| 6.88 |

|

MSCI EAFE Index |

| 13.54 |

| 4.55 |

| — |

| 5.83 |

|

Lipper International Multi-Cap |

|

|

|

|

|

|

|

|

|

Core Funds Index |

| 13.76 |

| 5.70 |

| — |

| 8.26 |

|

(1) The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the U.S. & Canada. The MSCI EAFE Index consists of the follow- ing 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Italy, Japan, the Nether- lands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

(2) The Lipper International Multi-Cap Core Funds Index is an equally weighted performance index of the largest qualifying funds (based on net assets) in the Lipper International Multi-Cap Core Funds classification. The Index, which is adjusted for capital gains distributions and income dividends, is unmanaged and should not be considered an investment. There are currently 10 funds represented in this Index. As of the date of this report, the Portfolio is in the Lipper International Multi-Cap Core Funds classification.

(3) Total returns for the Portfolio reflect fees waived and expenses reimbursed, if applicable, by the Adviser. Without such waivers and reimbursements, total returns would have been lower. Fee waivers and/or expense reimbursements are voluntary and the Adviser reserves the right to commence or terminate any waiver and/or reimbursement at any time.

(4) Commenced operations on January 17, 1992

(5) Commenced offering on January 2, 1996

(6) For comparative purposes, average annual since inception returns listed for the Indexes refer to the inception date or initial offering of the respective share class of the Portfolio, not the inception of the Index.

Performance data quoted represents past performance, which is no guarantee of future results, and current performance may be lower or higher than the figures shown. Performance assumes that all dividends and distributions, if any, were reinvested. For the most recent month-end performance figures, please visit morganstanley.com/im. Investment return and principal value will fluctuate so that Portfolio shares, when redeemed, may be worth more or less than their original cost. Total returns do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

The Active International Allocation Portfolio seeks long-term capital appreciation by investing primarily, in accordance with country and sector weightings determined by the Adviser, in equity securities of non-U.S. issuers which, in the aggregate, replicate broad market indices. Foreign investing involves certain risks, including currency fluctuations and controls, restrictions on foreign investments, less governmental

5

| 2005 Annual Report |

|

|

| December 31, 2005 |

Investment Overview (cont’d)

Active International Allocation Portfolio

supervision and regulation, less liquidity and the potential for market volatility and political instability.

Performance

For the year ended December 31, 2005, the Portfolio had a total return based on net asset value per share of 14.85%, net of fees, for Class A shares and 14.67%, net of fees, for Class B shares compared to 13.54% for the Morgan Stanley Capital International (MSCI) EAFE Index (the “Index”).

Factors Affecting Performance

• Overall, the international equity markets posted a solid gain in 2005. After a relatively weak start, Japan was the strongest performer for the year. The Asia ex-Japan and Europe regions both posted respectable gains. In our view, it was a testament to the mystery of the markets that European equities did so well in 2005 -given poor economic performance, a European Union constitutional crisis, French immigrant riots, and a stalemated German election. The European Central Bank remained largely on hold, however; the weak Euro helped exports and business sentiment, and corporate profits were often very strong. The United Kingdom continued to struggle with slowing consumer spending and a cooling housing market, although the climate improved as the year progressed and the Bank of England implemented a rate cut in the fourth quarter.

• The Portfolio’s performance for the 12-month period benefited primarily from an overweight to Japan relative to the Index, an underweight to the United Kingdom,and exposure (roughly 4% of the total Portfolio) to emerging markets. Above-benchmark allocations to Hong Kong and Switzerland detracted from performance.

• From a sector perspective, the Portfolio’s overweighted positions relative to the Index in materials, industrials and energy contributed to performance. Anunderweight to healthcare and a slight overweight to information technology were a drag to performance.

Management Strategies

• Throughout the period, our view was that the potential for returns in the international equity market outweighed the risks. Accordingly, the Portfolio was fully invested. Consistent with our long-standingdiscipline, we focused on trying to identify the major regions and sectors that offered the most upside, based on at least a six-month horizon.

• We like the economic and sentiment news we have recently seen out of Europe. At the close of the period, the Portfolio was marginally overweighted versus the Index in Germany, based on our view that the country represented an attractively valued, cyclical European market. The Portfolio has been underweight in the United Kingdom for some time.

• Although the Index does not include emerging markets,the Portfolio included a small stake in emerging markets, with a sprinkling in Brazil, Turkey, Russia, Poland, among others. Emerging markets have been driven higher by earnings growth; hence on a relative basis, we believe emerging markets are not wildly overpriced at this time.

• As of the close of the period, global earnings growth, though off-peak, appears to us to be healthy and supported by quiescent labor costs and reform-driven productivity. So far, the baton of economic growth has seemed to be passing with decent precision from Chinese fixed investment and the U.S. consumer to the Chinese consumer, U.S. business, Japan and Europe. In the U.S., economic growth remains on track, unemployment is low, and the Federal Open Market Committee (the “Fed”) has room to take rates higher, should it need to. European and Japanese central banks have appeared to follow the Fed’s cautionary lead of not being overly zealous. That said, we see potential risk to international equities from a range of factors, such as a U.S. housing market decline, an inability to fund the U.S. deficit, and an exogenous or financial shock which throttles global growth.

Expense Examples

As a shareholder of the Portfolio, you may incur two types of costs: (1) transactional costs, including redemption fees; (2) ongoing costs, including management fees, distribution (12b- 1) fees (in the case of Class B); and other Portfolio expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested at the beginning of the six-month period ended December 31, 2005 and held for the entire six-month period.

Actual Expenses

The first line of the tables below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to

6

2005 Annual Report | |

|

|

December 31, 2005 | |

Investment Overview (cont’d)

Active International Allocation Portfolio

estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the tables below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

|

|

|

|

| Expenses Paid |

| ||

|

|

|

| Ending Account |

| During Period* |

| ||

|

| Beginning |

| Value |

| July 1, 2005 — |

| ||

|

| Account Value |

| December 31, |

| December 31, |

| ||

|

| July 1, 2005 |

| 2005 |

| 2005 |

| ||

Class A |

|

|

|

|

|

|

| ||

Actual |

| $1,000.00 |

|

| $1,169.80 |

| $4.38 |

|

|

Hypothetical (5% average annual return before expenses) |

| 1,000.00 |

|

| 1,021.17 |

| 4.08 |

|

|

|

|

|

|

|

|

|

|

|

|

Class B |

|

|

|

|

|

|

|

|

|

Actual |

| 1,000.00 |

|

| 1,169.90 |

| 5.69 |

|

|

Hypothetical (5% averageannual return before expenses) |

| 1,000.00 |

|

| 1,019.96 |

| 5.30 |

|

|

* Expenses are equal to Class A and Class B annualized net expense ratios of 0.80% and 1.04%, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

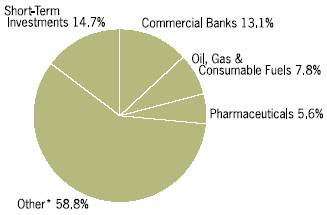

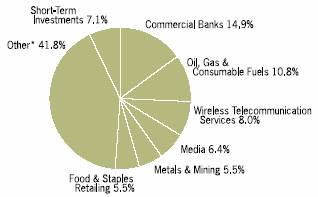

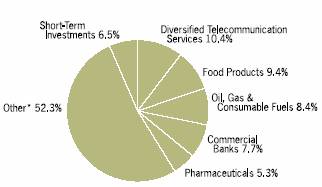

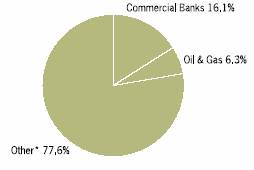

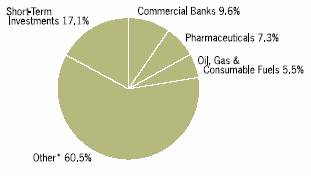

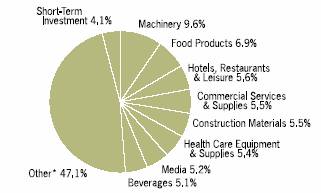

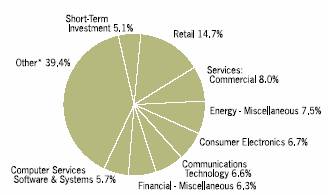

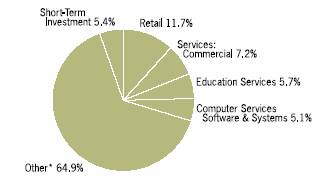

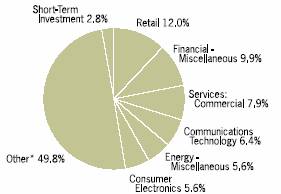

Graphic Presentation of Portfolio Holdings

The following graph depicts the Portfolio’s holdings by industry and/or security type, as a percentage of total investments.

* Industries which do not appear in the above graph, as well as those which represent less than 5% of total investments, if applicable, are included in the category labeled “Other”.

January 2006

7

| 2005 Annual Report |

|

|

| December 31, 2005 |

Portfolio of Investments

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Common Stocks (91.4%) |

|

|

|

|

| |

Australia (3.0%) |

|

|

|

|

| |

Alumina Ltd. |

| 91,525 |

| $ | 498 |

|

Amcor Ltd. |

| (c)71,068 |

| 389 |

| |

AMP Ltd. |

| 42,736 |

| 241 |

| |

Ansell Ltd. |

| 5,679 |

| 46 |

| |

Australia & New Zealand Banking Group Ltd. |

| 46,465 |

| 816 |

| |

Australian Gas Light Co., Ltd. |

| (c)14,942 |

| 188 |

| |

BHP Billiton Ltd. |

| 282,988 |

| 4,721 |

| |

BlueScope Steel Ltd. |

| (c)57,822 |

| 296 |

| |

Boral Ltd. |

| 47,082 |

| 280 |

| |

Brambles Industries Ltd. |

| 31,812 |

| 236 |

| |

Caltex Australia Ltd. |

| 29,853 |

| 424 |

| |

Coca-Cola Amatil Ltd. |

| (c)16,776 |

| 95 |

| |

Coles Myer Ltd. |

| (c)34,518 |

| 258 |

| |

Commonwealth Bank of Australia |

| 38,394 |

| 1,204 |

| |

CSL Ltd. |

| (c)2,842 |

| 89 |

| |

CSR Ltd. |

| 76,379 |

| 195 |

| |

Foster’s Group Ltd. |

| 65,602 |

| 268 |

| |

Insurance Australia Group Ltd. |

| 54,613 |

| 217 |

| |

James Hardie Industries N.V. |

| 37,648 |

| 248 |

| |

John Fairfax Holdings Ltd. |

| (c)32,240 |

| 95 |

| |

Leighton Holdings Ltd. |

| (c)7,115 |

| 93 |

| |

Lend Lease Corp., Ltd. |

| 13,618 |

| 145 |

| |

Macquarie Bank Ltd. |

| 6,715 |

| 336 |

| |

Macquarie Infrastructure Group |

| 72,726 |

| 190 |

| |

Mayne Pharma Ltd. |

| (a)22,671 |

| 42 |

| |

National Australia Bank Ltd. |

| 51,258 |

| 1,218 |

| |

Newcrest Mining Ltd. |

| 26,212 |

| 467 |

| |

OneSteel Ltd. |

| (c)44,821 |

| 110 |

| |

Orica Ltd. |

| (a)22,596 |

| 338 |

| |

Origin Energy Ltd. |

| (c)213,888 |

| 1,178 |

| |

PaperlinX Ltd. |

| (c)36,382 |

| 102 |

| |

Patrick Corp., Ltd. |

| 30,000 |

| 163 |

| |

QBE Insurance Group Ltd. |

| (c)22,311 |

| 321 |

| |

Rinker Group Ltd. |

| 75,117 |

| 906 |

| |

Rio Tinto Ltd. |

| (c)24,545 |

| 1,242 |

| |

Santos Ltd. |

| 157,070 |

| 1,411 |

| |

Sonic Healthcare Ltd. |

| 5,616 |

| 61 |

| |

Stockland |

| 1,020 |

| 5 |

| |

Stockland (New) |

| 22 |

| @— |

| |

Suncorp-Metway Ltd. |

| 17,718 |

| 261 |

| |

Symbion Health Ltd. |

| 28,935 |

| 75 |

| |

TABCORP Holdings Ltd. |

| 13,036 |

| 149 |

| |

Telstra Corp., Ltd. |

| 69,366 |

| 200 |

| |

Transurban Group |

| 18,215 |

| 88 |

| |

Wesfarmers Ltd. |

| (c)12,074 |

| 327 |

| |

Westpac Banking Corp. |

| 54,298 |

| 906 |

| |

Woodside Petroleum Ltd. |

| 85,928 |

| 2,470 |

| |

Woolworths Ltd. |

| 32,252 |

| 399 |

| |

|

|

|

| 24,007 |

| |

Austria (0.9%) |

|

|

|

|

| |

Bank Austria Creditanstalt AG |

| (c)4,989 |

| 555 |

| |

Boehler-Uddeholm AG |

| 607 |

| 103 |

| |

Erste Bank der Oesterreichischen Sparkassen AG |

| 39,914 |

| 2,223 |

| |

Flughafen Wien AG |

| 3,439 |

| 246 |

| |

IMMOFINANZ Immobilien Anlagen AG |

| (a)43,746 |

| $ | 420 |

|

Mayr-Melnhof Karton AG |

| 1,261 |

| 176 |

| |

OMV AG |

| 25,691 |

| 1,506 |

| |

RHI AG |

| (a)(c)4,852 |

| 131 |

| |

Telekom Austria AG |

| 36,248 |

| 815 |

| |

Verbund-Oesterreichische Elektrizitaetswirtschafts |

|

|

|

|

| |

AG, Class A |

| 1,230 |

| 439 |

| |

Voestalpine AG |

| 1,155 |

| 116 |

| |

Wienerberger AG |

| 4,544 |

| 182 |

| |

|

|

|

| 6,912 |

| |

Belgium (0.8%) |

|

|

|

|

| |

AGFA-Gevaert N.V. |

| 4,251 |

| 77 |

| |

Bekaert S.A. |

| 539 |

| 50 |

| |

Belgacom S.A. |

| 6,763 |

| 221 |

| |

Dexia |

| 58,800 |

| 1,356 |

| |

Fortis |

| 90,067 |

| 2,873 |

| |

KBC Groupe N.V. |

| 8,105 |

| 755 |

| |

Solvay S.A., Class A |

| 3,669 |

| 404 |

| |

UCB S.A. |

| 6,911 |

| 325 |

| |

Umicore |

| 1,150 |

| 136 |

| |

|

|

|

| 6,197 |

| |

Brazil (1.1%) |

|

|

|

|

| |

AmBev |

| 241,555 |

| 78 |

| |

AmBev (Preference) |

| 1,200,781 |

| 461 |

| |

Aracruz Celulose S.A., Class B (Preference) |

| 31,988 |

| 127 |

| |

Arcelor Brasil S.A. |

| 5,403 |

| 65 |

| |

Banco Bradesco S.A. (Preference) |

| 29,000 |

| 840 |

| |

Banco Itau Holding Financeira S.A. (Preference) |

| 30,170 |

| 726 |

| |

Brasil Telecom Participacoes S.A. (Preference) |

| 16,991,044 |

| 125 |

| |

Caemi Mineracao e Metalurgica S.A. (Preference) |

| 119,500 |

| 174 |

| |

CEMIG S.A. (Preference) |

| 7,110,000 |

| 289 |

| |

Cia Brasileira de Distribuicao Grupo Pao de |

|

|

|

|

| |

Acucar ADR (Preference) |

| (c)900 |

| 30 |

| |

Cia Siderurgica Nacional S.A. |

| 5,976 |

| 128 |

| |

Contax Participacoes S.A. |

| 9,831 |

| 12 |

| |

CVRD, Class A (Preference) |

| 40,221 |

| 1,440 |

| |

Electrobras S.A., Class B (Preference) |

| 8,073,614 |

| 137 |

| |

Embraer (Preference) |

| 24,416 |

| 240 |

| |

Embratel Participacoes S.A. (Preference) |

| (a)7,843,216 |

| 23 |

| |

Gerdau S.A. (Preference) |

| 15,500 |

| 260 |

| |

Klabin S.A. (Preference) |

| 43,000 |

| 76 |

| |

Petrobras S.A. (Preference) |

| 158,500 |

| 2,522 |

| |

Sadia S.A. (Preference) |

| 34,500 |

| 97 |

| |

Souza Cruz S.A. |

| 5,800 |

| 72 |

| |

Tele Centro Oeste Celular Participacoes S.A. |

| 5,908 |

| 68 |

| |

Tele Norte Leste Participacoes S.A. (Preference) |

| 20,831 |

| 370 |

| |

Telesp Celular Participacoes S.A. (Preference) |

| (a)13,125 |

| 50 |

| |

Unibanco ADR |

| (c)5,650 |

| 359 |

| |

Usiminas S.A., Class A (Preference) |

| 7,400 |

| 176 |

| |

Votorantim Celulose e Papel S.A. (Preference) |

| 5,968 |

| 74 |

| |

|

|

|

| 9,019 |

| |

Denmark (0.6%) |

|

|

|

|

| |

AP Moller - Maersk A/S |

| 74 |

| 766 |

| |

Danske Bank A/S |

| 34,745 |

| 1,224 |

| |

DSV A/S |

| 1,175 |

| 145 |

| |

8 | The accompanying notes are an integral part of the financial statements. |

2005 Annual Report | |

|

|

December 31, 2005 | |

Portfolio of Investments (cont’d)

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Denmark (cont’d) |

|

|

|

|

| |

GN Store Nord A/S |

| 21,800 |

| $ | 285 |

|

Novo-Nordisk A/S, Class B |

| 17,800 |

| 1,001 |

| |

Novozymes A/S, Class B |

| 3,014 |

| 165 |

| |

TDC A/S |

| 11,000 |

| 659 |

| |

Vestas Wind Systems A/S |

| (a)10,650 |

| 175 |

| |

|

|

|

| 4,420 |

| |

Finland (1.2%) |

|

|

|

|

| |

Cargotec Corp., Class B |

| (a)2,604 |

| 90 |

| |

Fortum Oyj |

| 16,886 |

| 317 |

| |

Kesko Oyj, Class B |

| 4,358 |

| 124 |

| |

Kone Oyj, Class B |

| (a)5,208 |

| 207 |

| |

Metso Oyj |

| 7,730 |

| 212 |

| |

Neste Oil Oyj |

| (a)6,952 |

| 196 |

| |

Nokia Oyj |

| 323,165 |

| 5,911 |

| |

Outokumpu Oyj |

| (c)15,450 |

| 229 |

| |

Sampo Oyj, Class A |

| 22,919 |

| 399 |

| |

Stora Enso Oyj, Class R |

| 33,411 |

| 452 |

| |

TietoEnator Oyj |

| 10,536 |

| 385 |

| |

UPM-Kymmene Oyj |

| 29,359 |

| 576 |

| |

Uponor Oyj |

| (c)2,904 |

| 62 |

| |

Wartsila Oyj, Class B |

| 4,034 |

| 119 |

| |

|

|

|

| 9,279 |

| |

France (6.9%) |

|

|

|

|

| |

Accor S.A. |

| (c)18,464 |

| 1,016 |

| |

Alcatel S.A. |

| (a)87,177 |

| 1,081 |

| |

Alstom |

| (a)6,792 |

| 391 |

| |

Atos Origin S.A. |

| (a)1,557 |

| 103 |

| |

Autoroutes du Sud de la France |

| 5,067 |

| 300 |

| |

AXA S.A. |

| 142,852 |

| 4,610 |

| |

BNP Paribas S.A. |

| 75,639 |

| 6,120 |

| |

Bouygues S.A. |

| 16,979 |

| 830 |

| |

Business Objects S.A. |

| (a)4,600 |

| 186 |

| |

Cap Gemini S.A. |

| (a)13,124 |

| 527 |

| |

Carrefour S.A. |

| 31,579 |

| 1,480 |

| |

Casino Guichard Perrachon S.A. |

| (c)3,591 |

| 239 |

| |

Cie de Saint-Gobain |

| 18,247 |

| 1,085 |

| |

Cie Generale d’Optique Essilor International S.A. |

| 3,527 |

| 285 |

| |

CNP Assurances |

| 5,372 |

| 424 |

| |

Credit Agricole S.A. |

| 34,585 |

| 1,089 |

| |

Dassault Systemes S.A. |

| 4,244 |

| 240 |

| |

France Telecom S.A. |

| 75,785 |

| 1,883 |

| |

Gecina S.A. REIT |

| 3,084 |

| 354 |

| |

Groupe Danone |

| (c)13,945 |

| 1,457 |

| |

Hermes International |

| 445 |

| 111 |

| |

Imerys S.A. |

| 1,967 |

| 142 |

| |

Klepierre REIT |

| 2,600 |

| 244 |

| |

L’Air Liquide S.A. |

| 5,939 |

| 1,142 |

| |

L’Oreal S.A. |

| 2,146 |

| 160 |

| |

Lafarge S.A. |

| (c)9,247 |

| 832 |

| |

Lagardere S.C.A. |

| 6,292 |

| 484 |

| |

LVMH Moet Hennessy Louis Vuitton S.A. |

| 10,888 |

| 967 |

| |

Michelin (CGDE), Class B |

| 4,696 |

| 264 |

| |

Neopost S.A. |

| 2,457 |

| 246 |

| |

Pernod-Ricard S.A. |

| (c)1,088 |

| 190 |

| |

Peugeot S.A. |

| (c)5,348 |

| $ | 308 |

|

PPR S.A. |

| 2,823 |

| 318 |

| |

Publicis Groupe |

| 4,217 |

| 147 |

| |

Renault S.A. |

| (c)5,505 |

| 449 |

| |

Safran S.A. |

| 4,910 |

| 117 |

| |

Sanofi-Aventis S.A. |

| (c)65,208 |

| 5,713 |

| |

Schneider Electric S.A. |

| 13,164 |

| 1,174 |

| |

Societe BIC S.A. |

| 1,627 |

| 97 |

| |

Societe Generale |

| 29,834 |

| 3,670 |

| |

Societe Television Francaise 1 |

| (c)5,196 |

| 144 |

| |

Sodexho Alliance S.A. |

| (c)10,220 |

| 421 |

| |

Suez S.A. (VVPR-strip) |

| (a)2,940 |

| @— |

| |

Suez S.A. |

| 34,213 |

| 1,065 |

| |

Technip S.A. |

| 1,528 |

| 92 |

| |

Thales S.A. |

| (c)6,720 |

| 305 |

| |

Thomson |

| (c)10,855 |

| 227 |

| |

Total S.A. |

| 34,878 |

| 8,762 |

| |

Unibail |

| 4,206 |

| 560 |

| |

Valeo S.A. |

| 5,295 |

| 197 |

| |

Veolia Environnement |

| (c)7,021 |

| 318 |

| |

Vinci S.A. |

| (c)8,430 |

| 725 |

| |

Vivendi Universal S.A. |

| 39,320 |

| 1,232 |

| |

Zodiac S.A. |

| 631 |

| 40 |

| |

|

|

|

| 54,563 |

| |

Germany (6.9%) |

|

|

|

|

| |

Adidas-Salomon AG |

| 2,861 |

| 542 |

| |

Allianz AG (Registered) |

| 36,512 |

| 5,530 |

| |

Altana AG |

| 5,626 |

| 306 |

| |

BASF AG |

| 29,360 |

| 2,249 |

| |

Bayer AG |

| 35,613 |

| 1,488 |

| |

Bayerische Hypo-und Vereinsbank AG |

| (a)72,962 |

| 2,212 |

| |

Beiersdorf AG |

| 6,137 |

| 756 |

| |

Celesio AG |

| 2,419 |

| 208 |

| |

Commerzbank AG |

| 91,364 |

| 2,814 |

| |

Continental AG |

| 5,688 |

| 505 |

| |

DaimlerChrysler AG |

| 38,537 |

| 1,968 |

| |

Deutsche Bank AG (Registered) |

| 52,584 |

| 5,098 |

| |

Deutsche Boerse AG |

| 20,350 |

| 2,085 |

| |

Deutsche Lufthansa AG (Registered) |

| 18,151 |

| 269 |

| |

Deutsche Post AG (Registered) |

| (c)64,771 |

| 1,570 |

| |

Deutsche Telekom AG (Registered) |

| (c)165,931 |

| 2,766 |

| |

Douglas HoldingAG |

| 1,380 |

| 53 |

| |

E. ON AG |

| 51,698 |

| 5,349 |

| |

Epcos AG |

| (a)3,649 |

| 48 |

| |

Fresenius Medical Care AG |

| (c)4,509 |

| 475 |

| |

Fresenius Medical Care AG (Preference) |

| 300 |

| 28 |

| |

Henkel KGaA (Non-VotingShares) |

| 4,261 |

| 429 |

| |

Hochtief AG |

| 700 |

| 31 |

| |

Hypo Real Estate HoldingAG |

| 16,900 |

| 880 |

| |

InBev N.V. |

| 3,651 |

| 159 |

| |

Infineon Technologies AG |

| (a)28,610 |

| 262 |

| |

KarstadtQuelle AG |

| (a)(c)714 |

| 11 |

| |

Linde AG |

| 4,994 |

| 389 |

| |

MAN AG |

| 9,024 |

| 482 |

| |

Merck KGaA |

| 4,664 |

| 386 |

| |

Metro AG |

| 13,436 |

| 649 |

| |

The accompanying notes are an integral part of the financial statements. | 9 |

| 2005 Annual Report |

|

|

| December 31, 2005 |

Portfolio of Investments (cont’d)

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Germany (cont’d) |

|

|

|

|

| |

Muenchener Rueckversicherungs AG (Registered) |

| 8,843 |

| $ | 1,197 |

|

Porsche AG (Non-VotingShares) |

| 365 |

| 262 |

| |

ProSiebenSAT.1 Media AG (Non-VotingShares) |

| 3,088 |

| 60 |

| |

Puma AG Rudolf Dassler Sport |

| 957 |

| 279 |

| |

RWE AG |

| 30,540 |

| 2,262 |

| |

RWE AG (Non-VotingShares) |

| 900 |

| 58 |

| |

SAP AG |

| 18,279 |

| 3,314 |

| |

ScheringAG |

| 11,591 |

| 777 |

| |

Siemens AG (Registered) |

| 58,294 |

| 4,997 |

| |

ThyssenKrupp AG |

| 20,103 |

| 419 |

| |

TUI AG |

| (c)15,183 |

| 311 |

| |

Volkswagen AG |

| (c)10,014 |

| 529 |

| |

Volkswagen AG (Non-VotingShares) |

| 5,035 |

| 194 |

| |

Wincor Nixdorf AG |

| 1,324 |

| 140 |

| |

|

|

|

| 54,796 |

| |

Greece (0.2%) |

|

|

|

|

| |

Alpha Bank A.E. |

| 11,274 |

| 330 |

| |

EFG Eurobank Ergasias S.A. |

| 6,542 |

| 207 |

| |

National Bank of Greece S.A. |

| 14,133 |

| 602 |

| |

OPAP S.A. |

| 12,910 |

| 445 |

| |

Titan Cement Co., S.A. |

| 3,150 |

| 128 |

| |

|

|

|

| 1,712 |

| |

HongKong(4.2%) |

|

|

|

|

| |

Bank of East Asia Ltd. |

| 344,594 |

| 1,042 |

| |

BOC HongKong Holdings Ltd. |

| 782,500 |

| 1,504 |

| |

Cathay Pacific Airways Ltd. |

| (c)214,000 |

| 374 |

| |

Cheung Kong Holdings Ltd. |

| (c)335,000 |

| 3,437 |

| |

Cheung Kong Infrastructure Holdings Ltd. |

| 107,000 |

| 337 |

| |

CLP Holdings Ltd. |

| 348,800 |

| 2,024 |

| |

Esprit Holdings Ltd. |

| 206,000 |

| 1,464 |

| |

Hang Lung Properties Ltd. |

| 408,000 |

| 637 |

| |

Hang Seng Bank Ltd. |

| (c)145,900 |

| 1,904 |

| |

Henderson Land Development Co., Ltd. |

| (c)145,000 |

| 683 |

| |

Hong Kong & China Gas Co., Ltd. |

| 839,079 |

| 1,791 |

| |

Hong Kong Exchanges & Clearing Ltd. |

| 221,000 |

| 916 |

| |

Hong Kong Electric Holdings Ltd. |

| 298,000 |

| 1,476 |

| |

Hopewell Holdings Ltd. |

| 131,000 |

| 329 |

| |

Hutchison Telecommunications International, Ltd. |

| (a)281,000 |

| 406 |

| |

Hutchison Whampoa Ltd. |

| 451,200 |

| 4,297 |

| |

Hysan Development Co., Ltd. |

| 135,958 |

| 337 |

| |

Johnson Electric Holdings Ltd. |

| 332,000 |

| 315 |

| |

Kerry Properties Ltd. |

| 89,250 |

| 236 |

| |

Kingboard Chemical Holdings Ltd. |

| 103,500 |

| 280 |

| |

Li & FungLtd. |

| 341,000 |

| 657 |

| |

Link REIT (The) |

| (a)349,000 |

| 662 |

| |

MTR Corp. |

| (c)293,585 |

| 577 |

| |

New World Development Ltd. |

| 479,598 |

| 659 |

| |

PCCW Ltd. |

| (c)775,411 |

| 477 |

| |

SCMP Group Ltd. |

| 18,000 |

| 7 |

| |

Shangri-La Asia Ltd. |

| 212,424 |

| 355 |

| |

Sino Land Co. |

| (c)274,109 |

| 332 |

| |

Sun Hung Kai Properties Ltd. |

| (c)268,000 |

| 2,610 |

| |

Swire Pacific Ltd., Class A |

| 184,000 |

| 1,652 |

| |

Techtronic Industries Co. |

| 186,500 |

| 444 |

| |

Television Broadcasts Ltd. |

| 58,000 |

| $ | 308 |

|

Wharf Holdings Ltd. |

| 266,600 |

| 942 |

| |

Yue Yuen Industrial Holdings Ltd. |

| 101,500 |

| 283 |

| |

|

|

|

| 33,754 |

| |

Ireland (0.4%) |

|

|

|

|

| |

Allied Irish Banks plc |

| 45,808 |

| 979 |

| |

Bank of Ireland |

| 53,484 |

| 842 |

| |

CRH plc |

| 29,769 |

| 876 |

| |

DCC plc |

| 1,882 |

| 40 |

| |

Elan Corp. plc |

| (a)22,642 |

| 298 |

| |

Grafton Group plc |

| (a)13,307 |

| 145 |

| |

Independent News & Media plc |

| 11,532 |

| 34 |

| |

Irish Life & Permanent plc |

| 3,435 |

| 70 |

| |

|

|

|

| 3,284 |

| |

Italy (1.2%) |

|

|

|

|

| |

Alleanza Assicurazioni S.p.A. |

| (c)7,412 |

| 92 |

| |

Assicurazioni Generali S.p.A. |

| 12,537 |

| 438 |

| |

Autogrill S.p.A. |

| (c)5,283 |

| 72 |

| |

Autostrade S.p.A. |

| 10,821 |

| 260 |

| |

Banca Antonveneta S.p.A. |

| 323 |

| 10 |

| |

Banca Fideuram S.p.A. |

| 2,390 |

| 13 |

| |

Banca Intesa S.p.A. |

| 87,231 |

| 462 |

| |

Banca Intesa S.p.A. RNC |

| 6,672 |

| 33 |

| |

Banca Monte dei Paschi di Siena S.p.A. |

| 6,867 |

| 32 |

| |

Banca Nazionale del Lavoro S.p.A. |

| (a)9,649 |

| 32 |

| |

Banca Popolare di Milano Scrl |

| 2,043 |

| 23 |

| |

Banche Popolari Unite Scrl |

| 611 |

| 14 |

| |

Banco Popolare di Verona e Novara Scrl |

| 8,766 |

| 177 |

| |

Benetton Group S.p.A. |

| 1,341 |

| 15 |

| |

Capitalia S.p.A. |

| 2,980 |

| 17 |

| |

Enel S.p.A. |

| 28,852 |

| 227 |

| |

ENI S.p.A. |

| 149,164 |

| 4,138 |

| |

Fiat S.p.A. |

| (a)(c)9,055 |

| 79 |

| |

Finmeccanica S.p.A. |

| 10,081 |

| 195 |

| |

Italcementi S.p.A. |

| (c)1,087 |

| 20 |

| |

Luxottica Group S.p.A. |

| 3,903 |

| 99 |

| |

Mediaset S.p.A. |

| 9,656 |

| 102 |

| |

Mediobanca S.p.A. |

| 4,940 |

| 94 |

| |

Mediolanum S.p.A. |

| (c)1,796 |

| 12 |

| |

Pirelli & C S.p.A. |

| 81,385 |

| 75 |

| |

Riunione Adriatica di Sicurta S.p.A. |

| 4,478 |

| 108 |

| |

Sanpaolo IMI S.p.A. |

| 36,041 |

| 564 |

| |

Seat Pagine Gialle S.p.A. |

| (a)38,991 |

| 18 |

| |

Snam Rete Gas S.p.A. |

| 4,549 |

| 19 |

| |

Telecom Italia S.p.A. |

| (c)314,268 |

| 915 |

| |

Telecom Italia S.p.A. RNC |

| 179,946 |

| 446 |

| |

Tiscali S.p.A. |

| (a)(c)2,748 |

| 9 |

| |

UniCredito Italiano S.p.A. |

| 108,755 |

| 749 |

| |

|

|

|

| 9,559 |

| |

Japan (28.6%) |

|

|

|

|

| |

77 Bank Ltd. (The) |

| 64,000 |

| 486 |

| |

Acom Co., Ltd. |

| (c)8,080 |

| 520 |

| |

Advantest Corp. |

| (c)9,190 |

| 927 |

| |

Aeon Co., Ltd. |

| 39,200 |

| 998 |

| |

Aeon Credit Service Co., Ltd. |

| 2,100 |

| 199 |

| |

10 | The accompanying notes are an integral part of the financial statements. |

2005 Annual Report | |

|

|

December 31, 2005 | |

Portfolio of Investments (cont’d)

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Japan (cont’d) |

|

|

|

|

| |

Aiful Corp. |

| 7,150 |

| $ | 597 |

|

Ajinomoto Co., Inc. |

| 62,400 |

| 639 |

| |

Alps Electric Co., Ltd. |

| (c)15,800 |

| 220 |

| |

Amada Co., Ltd. |

| 26,000 |

| 229 |

| |

Asahi Breweries Ltd. |

| (c)33,600 |

| 410 |

| |

Asahi Glass Co., Ltd. |

| (c)108,800 |

| 1,406 |

| |

Asahi Kasei Corp. |

| 103,000 |

| 697 |

| |

Asatsu-DK, Inc. |

| 3,400 |

| 108 |

| |

Astellas Pharma, Inc. |

| 44,100 |

| 1,721 |

| |

Bank of Fukuoka Ltd. (The) |

| 86,000 |

| 736 |

| |

Bank of Kyoto Ltd (The) |

| 22,000 |

| 266 |

| |

Bank of Yokohama Ltd. (The) |

| 146,000 |

| 1,195 |

| |

Benesse Corp. |

| 5,000 |

| 175 |

| |

Bridgestone Corp. |

| (c)84,000 |

| 1,749 |

| |

Canon, Inc. |

| (c)69,800 |

| 4,085 |

| |

Casio Computer Co., Ltd. |

| (c)33,600 |

| 563 |

| |

Central Japan Railway Co. |

| 124 |

| 1,189 |

| |

Chiba Bank Ltd. (The) |

| 61,000 |

| 512 |

| |

Chiyoda Corp. |

| 18,000 |

| 414 |

| |

Chubu Electric Power Co., Inc. |

| (c)42,200 |

| 1,006 |

| |

Chugai Pharmaceutical Co., Ltd. |

| 20,607 |

| 442 |

| |

Citizen Watch Co., Ltd. |

| (c)34,300 |

| 285 |

| |

Coca-Cola West Japan Co., Ltd. |

| (c)1,300 |

| 30 |

| |

COMSYS Holdings Corp. |

| (c)15,000 |

| 215 |

| |

Credit Saison Co., Ltd. |

| (c)15,300 |

| 764 |

| |

CSK Holdings Corp. |

| (c)8,600 |

| 430 |

| |

Dai Nippon Printing Co., Ltd. |

| 37,600 |

| 670 |

| |

Daicel Chemical Industries Ltd. |

| 12,000 |

| 86 |

| |

Daiichi Sankyo Co., Ltd. |

| (a)61,005 |

| 1,177 |

| |

Daikin Industries Ltd. |

| 15,800 |

| 462 |

| |

Daimaru, Inc. |

| 24,000 |

| 346 |

| |

Dainippon Ink & Chemicals, Inc. |

| (c)53,000 |

| 230 |

| |

Daito Trust Construction Co., Ltd. |

| (c)14,100 |

| 730 |

| |

Daiwa House Industry Co., Ltd. |

| 73,600 |

| 1,151 |

| |

Daiwa Securities Group, Inc. |

| 300,000 |

| 3,402 |

| |

Denki Kagaku Kogyo K.K. |

| 36,000 |

| 159 |

| |

Denso Corp. |

| (c)60,250 |

| 2,080 |

| |

Dowa Mining Co., Ltd. |

| 49,000 |

| 531 |

| |

East Japan Railway Co. |

| 302 |

| 2,077 |

| |

Ebara Corp. |

| 30,800 |

| 166 |

| |

Eisai Co., Ltd. |

| (c)23,602 |

| 991 |

| |

FamilyMart Co., Ltd. |

| 4,900 |

| 166 |

| |

Fanuc Ltd. |

| 16,600 |

| 1,409 |

| |

Fast Retailing Co., Ltd. |

| 7,700 |

| 753 |

| |

Fuji Electric Holdings Co., Ltd. |

| 15,000 |

| 80 |

| |

Fuji Photo Film Co., Ltd. |

| (c)39,100 |

| 1,293 |

| |

Fuji Soft ABC, Inc. |

| 4,000 |

| 134 |

| |

Fuji Television Network, Inc. |

| 31 |

| 78 |

| |

Fujikura Ltd. |

| (c)22,000 |

| 178 |

| |

Fujitsu Ltd. |

| 153,200 |

| 1,167 |

| |

Furukawa Electric Co., Ltd. |

| (a)(c)53,800 |

| 421 |

| |

Hankyu Department Stores, Inc. |

| 9,000 |

| 79 |

| |

Hirose Electric Co., Ltd. |

| (c)4,900 |

| 654 |

| |

Hitachi Construction Machinery Co., Ltd. |

| 2,800 |

| 65 |

| |

Hitachi Ltd. |

| 294,000 |

| 1,983 |

| |

Hokkaido Electric Power Co., Inc. |

| 8,200 |

| $ | 167 |

|

Hokuhoku Financial Group, Inc. |

| (c)165,000 |

| 771 |

| |

Honda Motor Co., Ltd. |

| 84,404 |

| 4,818 |

| |

Hoya Corp. |

| 41,900 |

| 1,507 |

| |

Ibiden Co., Ltd. |

| 9,800 |

| 525 |

| |

Index Corp. |

| 111 |

| 201 |

| |

INPEX Corp. |

| 29 |

| 258 |

| |

Isetan Co., Ltd. |

| (c)16,100 |

| 343 |

| |

Ishihara Sangyo Kaisha Ltd. |

| 15,000 |

| 27 |

| |

Ishikawajima-Harima Heavy Industries Co., Ltd. |

| (a)93,000 |

| 294 |

| |

Ito En Ltd. |

| 1,900 |

| 114 |

| |

Itochu Corp. |

| 123,000 |

| 1,027 |

| |

Itochu Techno-Science Corp. |

| (c)3,400 |

| 163 |

| |

Japan Airlines Corp. |

| 79,000 |

| 215 |

| |

Japan Real Estate Investment Corp. REIT |

| 53 |

| 437 |

| |

Japan Retail Fund Investment Corp. REIT |

| 48 |

| 373 |

| |

Japan Tobacco, Inc. |

| 67 |

| 977 |

| |

JFE Holdings, Inc. |

| 32,000 |

| 1,075 |

| |

JGC Corp. |

| (c)24,000 |

| 457 |

| |

Joyo Bank Ltd. (The) |

| 115,000 |

| 685 |

| |

JS Group Corp. |

| (c)21,900 |

| 438 |

| |

JSR Corp. |

| 12,900 |

| 339 |

| |

Kajima Corp. |

| (c)113,400 |

| 652 |

| |

Kamigumi Co., Ltd. |

| 1,000 |

| 9 |

| |

Kaneka Corp. |

| 21,000 |

| 254 |

| |

Kansai Electric Power Co., Inc. (The) |

| 60,200 |

| 1,294 |

| |

Kao Corp. |

| 50,000 |

| 1,340 |

| |

Kawasaki Heavy Industries Ltd. |

| (c)93,000 |

| 339 |

| |

Kawasaki Kisen Kaisha Ltd. |

| 5,000 |

| 31 |

| |

Keihin Electric Express Railway Co., Ltd. |

| (c)32,000 |

| 252 |

| |

Keio Corp. |

| (c)19,000 |

| 114 |

| |

Keyence Corp. |

| 4,900 |

| 1,394 |

| |

Kikkoman Corp. |

| 10,000 |

| 97 |

| |

Kinden Corp. |

| 1,000 |

| 9 |

| |

Kintetsu Corp. |

| 140,200 |

| 561 |

| |

Kirin Brewery Co., Ltd. |

| (c)83,400 |

| 973 |

| |

Kobe Steel Ltd. |

| 166,000 |

| 538 |

| |

Kokuyo Co., Ltd. |

| 5,700 |

| 85 |

| |

Komatsu Ltd. |

| 96,400 |

| 1,595 |

| |

Konami Corp. |

| 11,900 |

| 262 |

| |

Konica Minolta Holdings, Inc. |

| 49,000 |

| 499 |

| |

Kubota Corp. |

| 132,000 |

| 1,110 |

| |

Kuraray Co., Ltd. |

| (c)29,500 |

| 306 |

| |

Kurita Water Industries Ltd. |

| (c)5,800 |

| 110 |

| |

Kyocera Corp. |

| 14,700 |

| 1,072 |

| |

Kyowa Hakko Kogyo Co., Ltd. |

| 28 |

| @— |

| |

Kyushu Electric Power Co., Inc. |

| 26,400 |

| 573 |

| |

Lawson, Inc. |

| 4,700 |

| 194 |

| |

Leopalace21 Corp. |

| 17,800 |

| 646 |

| |

Mabuchi Motor Co., Ltd. |

| (c)2,700 |

| 150 |

| |

Marubeni Corp. |

| (c)120,000 |

| 644 |

| |

Marui Co., Ltd. |

| 35,800 |

| 703 |

| |

Matsushita Electric Industrial Co., Ltd. |

| 176,000 |

| 3,396 |

| |

Matsushita Electric Works Ltd. |

| 28,000 |

| 262 |

| |

Meiji Dairies Corp. |

| (c)16,000 |

| 81 |

| |

The accompanying notes are an integral part of the financial statements. | 11 |

| 2005 Annual Report |

|

|

| December 31, 2005 |

Portfolio of Investments (cont’d)

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Japan (cont’d) |

|

|

|

|

| |

Meiji Seika Kaisha Ltd. |

| 19,000 |

| $ | 101 |

|

Meitec Corp. |

| (c)2,400 |

| 78 |

| |

Millea Holdings, Inc. |

| 123 |

| 2,118 |

| |

Minebea Co., Ltd. |

| 33,000 |

| 176 |

| |

Mitsubishi Chemical Holdings Corp. |

| (a)73,500 |

| 463 |

| |

Mitsubishi Corp. |

| 109,700 |

| 2,429 |

| |

Mitsubishi Electric Corp. |

| 186,800 |

| 1,323 |

| |

Mitsubishi Estate Co., Ltd. |

| 178,000 |

| 3,699 |

| |

Mitsubishi Heavy Industries Ltd. |

| 316,000 |

| 1,394 |

| |

Mitsubishi Logistics Corp. |

| (c)7,000 |

| 118 |

| |

Mitsubishi Materials Corp. |

| (c)161,000 |

| 823 |

| |

Mitsubishi Rayon Co., Ltd. |

| (c)42,000 |

| 278 |

| |

Mitsubishi UFJ Financial Group, Inc. |

| 662 |

| 8,984 |

| |

Mitsui & Co., Ltd. |

| (c)132,800 |

| 1,707 |

| |

Mitsui Chemicals, Inc. |

| (c)42,000 |

| 283 |

| |

Mitsui Fudosan Co., Ltd. |

| 127,400 |

| 2,588 |

| |

Mitsui Mining & Smelting Co., Ltd. |

| 96,000 |

| 603 |

| |

Mitsui OSK Lines Ltd. |

| 13,000 |

| 113 |

| |

Mitsui Sumitomo Insurance Co., Ltd. |

| 102,000 |

| 1,248 |

| |

Mitsui Trust Holdings, Inc. |

| 48,545 |

| 583 |

| |

Mitsukoshi Ltd. |

| 32,000 |

| 209 |

| |

Mizuho Financial Group, Inc. |

| 844 |

| 6,701 |

| |

Murata Manufacturing Co., Ltd. |

| 19,800 |

| 1,270 |

| |

Namco Bandai Holdings, Inc. |

| (a)2,400 |

| 35 |

| |

NEC Corp. |

| 196,400 |

| 1,223 |

| |

NEC Electronics Corp. |

| (c)4,600 |

| 151 |

| |

Net One Systems Co., Ltd. |

| (c)69 |

| 167 |

| |

NGK Insulators Ltd. |

| (c)34,600 |

| 515 |

| |

NGK Spark Plug Co., Ltd. |

| (c)21,000 |

| 454 |

| |

Nidec Corp. |

| (c)10,000 |

| 851 |

| |

Nikko Cordial Corp. |

| 51,000 |

| 808 |

| |

Nikon Corp. |

| (c)27,000 |

| 426 |

| |

Nintendo Co., Ltd. |

| 13,000 |

| 1,571 |

| |

Nippon Building Fund, Inc. REIT |

| (c)63 |

| 532 |

| |

Nippon Electric Glass Co., Ltd. |

| 17,000 |

| 371 |

| |

Nippon Express Co., Ltd. |

| (c)74,800 |

| 456 |

| |

Nippon Meat Packers, Inc. |

| 18,600 |

| 195 |

| |

Nippon Mining Holdings, Inc. |

| 43,500 |

| 310 |

| |

Nippon Oil Corp. |

| 134,800 |

| 1,046 |

| |

Nippon Paper Group, Inc. |

| (c)70 |

| 280 |

| |

Nippon Sheet Glass Co., Ltd. |

| (c)37,000 |

| 162 |

| |

Nippon Steel Corp. |

| (c)418,000 |

| 1,489 |

| |

Nippon Telegraph & Telephone Corp. |

| 567 |

| 2,578 |

| |

Nippon Yusen Kabushiki Kaisha |

| 99,000 |

| 679 |

| |

Nishi-Nippon Bank Ltd (The) |

| 44,000 |

| 263 |

| |

Nissan Chemical Industries Ltd. |

| 11,000 |

| 157 |

| |

Nissan Motor Co., Ltd. |

| (c)250,900 |

| 2,543 |

| |

Nisshin Seifun Group, Inc. |

| 12,500 |

| 132 |

| |

Nisshinbo Industries, Inc. |

| 6,000 |

| 66 |

| |

Nissin Food Products Co., Ltd. |

| 6,500 |

| 188 |

| |

Nitto Denko Corp. |

| 17,800 |

| 1,388 |

| |

Nomura Holdings, Inc. |

| 181,500 |

| 3,479 |

| |

Nomura Research Institute Ltd. |

| 2,900 |

| 355 |

| |

NSK Ltd. |

| 62,000 |

| 424 |

| |

NTN Corp. |

| (c)44,000 |

| 348 |

| |

NTT Data Corp. |

| (c)166 |

| $ | 827 |

|

NTT DoCoMo, Inc. |

| 749 |

| 1,144 |

| |

Obayashi Corp. |

| 77,000 |

| 568 |

| |

Obic Co., Ltd. |

| 900 |

| 198 |

| |

OJI Paper Co., Ltd. |

| (c)96,400 |

| 570 |

| |

Oki Electric Industry Co., Ltd. |

| (c)52,000 |

| 190 |

| |

Okumura Corp. |

| 21,000 |

| 118 | �� | |

Olympus Corp. |

| (c)11,000 |

| 289 |

| |

Omron Corp. |

| 19,600 |

| 452 |

| |

Onward Kashiyama Co., Ltd. |

| (c)16,000 |

| 315 |

| |

Oracle Corp. Japan |

| (c)4,200 |

| 209 |

| |

Oriental Land Co., Ltd. |

| 5,700 |

| 311 |

| |

ORIX Corp. |

| 12,100 |

| 3,084 |

| |

Osaka Gas Co., Ltd. |

| 155,600 |

| 537 |

| |

Pioneer Corp. |

| (c)14,454 |

| 201 |

| |

Promise Co., Ltd. |

| 9,950 |

| 663 |

| |

Resona Holdings, Inc. |

| (a)411 |

| 1,656 |

| |

Ricoh Co., Ltd. |

| 56,000 |

| 981 |

| |

Rohm Co., Ltd. |

| 13,200 |

| 1,437 |

| |

Sanden Corp. |

| 1,000 |

| 5 |

| |

Sanken Electric Co., Ltd. |

| 13,000 |

| 210 |

| |

Sanyo Electric Co., Ltd. |

| (c)148,000 |

| 402 |

| |

Sapporo Holdings Ltd. |

| (c)17,000 |

| 95 |

| |

Secom Co., Ltd. |

| 14,600 |

| 764 |

| |

Seiko Epson Corp. |

| (c)9,800 |

| 246 |

| |

Sekisui Chemical Co., Ltd. |

| 44,000 |

| 298 |

| |

Sekisui House Ltd. |

| (c)87,600 |

| 1,103 |

| |

Seven & I Holdings Co., Ltd. |

| (a)64,000 |

| 2,741 |

| |

Sharp Corp. |

| 73,200 |

| 1,114 |

| |

Shimachu Co., Ltd. |

| 5,300 |

| 161 |

| |

Shimamura Co., Ltd. |

| (c)2,000 |

| 277 |

| |

Shimano, Inc. |

| (c)8,600 |

| 226 |

| |

Shimizu Corp. |

| 81,600 |

| 600 |

| |

Shin-Etsu Chemical Co., Ltd. |

| 33,896 |

| 1,803 |

| |

Shinsei Bank Ltd. |

| 140,000 |

| 810 |

| |

Shionogi & Co., Ltd. |

| (c)29,000 |

| 409 |

| |

Shiseido Co., Ltd. |

| (c)32,000 |

| 597 |

| |

Shizuoka Bank Ltd. (The) |

| 52,000 |

| 521 |

| |

Showa Denko K.K. |

| (c)55,000 |

| 215 |

| |

Showa Shell Sekiyu K.K. |

| (c)14,300 |

| 171 |

| |

Skylark Co., Ltd. |

| 11,200 |

| 179 |

| |

SMC Corp. |

| 5,800 |

| 829 |

| |

Softbank Corp. |

| 96,900 |

| 4,093 |

| |

Sompo Japan Insurance, Inc. |

| 70,000 |

| 947 |

| |

Sony Corp. |

| 62,097 |

| 2,539 |

| |

Stanley Electric Co., Ltd. |

| (c)6,300 |

| 102 |

| |

Sumitomo Bakelite Co., Ltd. |

| (c)11,000 |

| 91 |

| |

Sumitomo Chemical Co., Ltd. |

| 117,600 |

| 808 |

| |

Sumitomo Corp. |

| 80,400 |

| 1,040 |

| |

Sumitomo Electric Industries Ltd. |

| 59,800 |

| 908 |

| |

Sumitomo Heavy Industries Ltd. |

| 38,000 |

| 319 |

| |

Sumitomo Metal Industries Ltd. |

| 248,000 |

| 955 |

| |

Sumitomo Metal Mining Co., Ltd. |

| 90,800 |

| 1,124 |

| |

Sumitomo Mitsui Financial Group, Inc. |

| 198 |

| 2,099 |

| |

Sumitomo Realty & Development Co., Ltd. |

| 76,000 |

| 1,654 |

| |

Sumitomo Trust & Banking Co., Ltd. (The) |

| 113,000 |

| 1,155 |

| |

12 | The accompanying notes are an integral part of the financial statements. |

2005 Annual Report | |

|

|

December 31, 2005 | |

Portfolio of Investments (cont’d)

Active International Allocation Portfolio

|

|

|

| Value |

| |

|

| Shares |

| (000) |

| |

Japan (cont’d) |

|

|

|

|

| |

T&D Holdings, Inc. |

| 19,350 |

| $ | 1,284 |

|

Taiheiyo Cement Corp. |

| 52,000 |

| 211 |

| |

Taisei Corp. |

| 110,000 |

| 499 |

| |

Taisho Pharmaceutical Co., Ltd. |

| 15,441 |

| 289 |

| |

Taiyo Yuden Co., Ltd. |

| (c)7,000 |

| 96 |

| |

Takara Holdings, Inc. |

| 10,000 |

| 59 |

| |

Takashimaya Co., Ltd. |

| (c)33,000 |

| 527 |

| |

Takeda Pharmaceutical Co., Ltd. |

| 78,600 |

| 4,254 |

| |

Takefuji Corp. |

| 7,080 |

| 481 |

| |

Takuma Co., Ltd. |

| (c)7,000 |

| 47 |

| |

TDK Corp. |

| 10,600 |

| 731 |

| |

Teijin Ltd. |

| 74,400 |

| 473 |

| |

Teikoku Oil Co., Ltd. |

| (c)8,000 |

| 105 |

| |

Terumo Corp. |

| 17,300 |

| 512 |

| |

THK Co., Ltd. |

| 3,400 |

| 89 |

| |

TIS, Inc. |

| (c)4,004 |

| 124 |

| |

Tobu Railway Co., Ltd. |

| 76,400 |

| 401 |

| |

Toho Co., Ltd. |

| 6,000 |

| 134 |

| |

Tohoku Electric Power Co., Inc. |

| 35,500 |

| 723 |

| |

Tokyo Broadcasting System, Inc. |

| 9,500 |

| 258 |

| |

Tokyo Electric Power Co., Inc. (The) |

| 88,000 |

| 2,139 |

| |

Tokyo Electron Ltd. |

| (c)20,000 |

| 1,257 |

| |

Tokyo Gas Co., Ltd. |

| 183,600 |

| 816 |

| |

Tokyo Tatemono Co., Ltd. |

| (c)28,000 |

| 279 |

| |

Tokyu Corp. |

| (c)85,400 |

| 604 |

| |

TonenGeneral Sekiyu K.K. |

| 29,000 |

| 312 |

| |

Toppan Printing Co., Ltd. |

| (c)36,600 |

| 428 |

| |

Toray Industries, Inc. |

| 103,100 |

| 841 |

| |

Toshiba Corp. |

| (c)294,000 |

| 1,756 |

| |

Tosoh Corp. |

| (c)40,000 |

| 176 |

| |

Toto Ltd. |

| (c)43,600 |

| 369 |

| |

Toyo Seikan Kaisha Ltd. |

| (c)16,600 |

| 271 |

| |

Toyobo Co., Ltd. |

| (c)5,000 |

| 17 |

| |

Toyoda Gosei Co., Ltd. |

| 800 |

| 16 |

| |

Toyota Industries Corp. |

| 8,850 |

| 318 |

| |

Toyota Motor Corp. |

| 272,800 |

| 14,161 |

| |

Trend Micro, Inc. |

| (a)(c)12,700 |

| 480 |

| |

Uni-Charm Corp. |

| 3,500 |

| 157 |

| |

Uniden Corp. |

| (c)5,000 |

| 97 |

| |

UNY Co., Ltd. |

| (c)10,000 |

| 158 |

| |

Ushio, Inc. |

| (c)3,500 |

| 82 |

| |

USS Co., Ltd. |

| 2,730 |

| 174 |

| |

Wacoal Holdings Corp. |

| 6,000 |

| 81 |

| |

West Japan Railway Co. |

| 31 |

| 129 |

| |

Yahoo! Japan Corp. |

| 992 |

| 1,506 |

| |

Yakult Honsha Co., Ltd. |

| (c)8,800 |

| 183 |

| |

Yamada Denki Co., Ltd. |

| 9,700 |

| 1,214 |

| |

Yamaha Corp. |

| (c)8,600 |

| 143 |

| |

Yamaha Motor Co., Ltd. |

| 3,500 |

| 91 |

| |

Yamato Holdings Co., Ltd. |

| 24,000 |

| 398 |

| |

Yamazaki Baking Co., Ltd. |

| (c)8,000 |

| 65 |

| |

Yokogawa Electric Corp. |

| (c)19,300 |

| 329 |

| |

|

|

|

| 227,322 |

| |

Luxembourg (0.1%) |

|

|

|

|

| |

Arcelor |

| 27,629 |

| 685 |

| |

Mexico (1.0%) |

|

|

|

|

| |

Alfa S.A. de C.V., Class A |

| 27,500 |

| $ | 153 |

|

America Movil S.A. de C.V. |

| 1,487,000 |

| 2,172 |

| |

Cemex S.A. de C.V. |

| 240,400 |

| 1,426 |

| |

Coca-Cola Femsa S.A. de C.V. |

| 11,500 |

| 32 |

| |

Corp. GEO S.A. de C.V. |

| (a)31,700 |

| 112 |

| |

Fomento Economico Mexicano S.A. de C.V. |

| 52,600 |

| 381 |

| |

Grupo Carso S.A. de C.V., Class A1 |

| 61,700 |

| 150 |

| |

Grupo Financiero Banorte S.A. de C.V., Class O |

| 110,100 |

| 228 |

| |

Grupo Mexico S.A. de C.V., Class B |

| 87,200 |

| 203 |

| |

Grupo Modelo S.A., Class C |

| 43,400 |

| 157 |

| |

Grupo Televisa S.A. |

| 173,900 |

| 695 |

| |

Kimberly-Clark de Mexico S.A. de C.V., Class A |

| 41,500 |

| 148 |

| |

Telefonos de Mexico S.A. de C.V. |

| (c)1,000,500 |

| 1,238 |

| |

Urbi Desarrollos Urbanos S.A. de C.V. |

| (a)10,000 |

| 69 |

| |

Wal-Mart de Mexico S.A. de C.V., Series V |

| 151,400 |

| 840 |

| |

|

|

|

| 8,004 |

| |

Netherlands (4.7%) |

|

|

|

|

| |

ABN AMRO Holding N.V. |

| 116,252 |

| 3,040 |

| |

Aegon N.V. |

| 139,741 |

| 2,275 |

| |

Akzo Nobel N.V. |

| 15,033 |

| 697 |

| |

ASML Holding N.V. |

| (a)32,756 |

| 655 |

| |

Corio N.V. REIT |

| 5,854 |

| 318 |

| |

Euronext N.V. |

| 6,578 |

| 343 |

| |

European Aeronautic Defense & Space Co. N.V. |

| 14,611 |

| 552 |

| |

Hagemeyer N.V. |

| (a)4,613 |

| 15 |

| |

Heineken N.V. |

| 48,272 |

| 1,530 |

| |

ING Groep N.V. CVA |

| 126,199 |

| 4,377 |

| |

Koninklijke DSM NV |

| 8,260 |

| 337 |

| |

Koninklijke Numico N.V. |

| (a)8,920 |

| 369 |

| |

Koninklijke Philips Electronics N.V. |

| 56,394 |

| 1,753 |

| |

OCE N.V. |

| 6,272 |

| 91 |

| |

Reed Elsevier N.V. |

| 29,077 |

| 406 |

| |

Rodamco Europe N.V. REIT |

| 4,805 |

| 400 |

| |

Royal Dutch Shell plc |

| 244,852 |

| 7,461 |

| |

Royal Dutch Shell plc, Class B |

| 183,643 |

| 5,871 |

| |

Royal KPN N.V. |

| 106,404 |

| 1,067 |

| |

TNT N.V. |

| 46,071 |

| 1,440 |

| |

Unilever N.V. CVA |

| 48,175 |

| 3,299 |

| |

VNU N.V. |

| 10,953 |

| 363 |

| |

Wereldhave N.V. REIT |

| 2,385 |

| 225 |

| |

Wolters Kluwer N.V. CVA |

| 15,333 |

| 310 |

| |

|

|

|

| 37,194 |

| |

New Zealand (0.0%) |

|

|

|

|

| |

Carter Holt Harvey Ltd. |

| 50,325 |

| 86 |

| |

Telecom Corp. of New Zealand Ltd. |

| 20,139 |

| 83 |

| |

|

|

|

| 169 |

| |

Norway (0.4%) |

|

|

|

|

| |