UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: | 811-05628 | |

Name of Registrant: | Vanguard Malvern Funds |

Address of Registrant: | P.O. Box 2600 |

| | Valley Forge, PA 19482 |

Name and address of agent for service: | Anne E. Robinson, Esquire |

| | P.O. Box 876 |

| | Valley Forge, PA 19482 |

Registrant’s telephone number, including area code: (610) 669-1000 |

Date of fiscal year end: September 30 | |

Date of reporting period: October 1, 2016 – September 30, 2017 |

Item 1: Reports to Shareholders | |

Annual Report | September 30, 2017

Vanguard U.S. Value Fund

Vanguard’s Principles for Investing Success

We want to give you the best chance of investment success. These principles, grounded in Vanguard’s research and experience, can put you on the right path.

Goals. Create clear, appropriate investment goals.

Balance. Develop a suitable asset allocation using broadly diversified funds. Cost. Minimize cost.

Discipline. Maintain perspective and long-term discipline.

A single theme unites these principles: Focus on the things you can control.

We believe there is no wiser course for any investor.

| |

| Contents | |

| Your Fund’s Performance at a Glance. | 1 |

| Chairman’s Perspective. | 3 |

| Advisor’s Report. | 7 |

| Fund Profile. | 9 |

| Performance Summary. | 10 |

| Financial Statements. | 12 |

| Your Fund’s After-Tax Returns. | 25 |

| About Your Fund’s Expenses. | 26 |

| Glossary. | 28 |

Please note: The opinions expressed in this report are just that—informed opinions. They should not be considered promises

or advice. Also, please keep in mind that the information and opinions cover the period through the date on the front of this

report. Of course, the risks of investing in your fund are spelled out in the prospectus.

See the Glossary for definitions of investment terms used in this report.

About the cover: Nautical images have been part of Vanguard’s rich heritage since its start in 1975. For an

incoming ship, a lighthouse offers a beacon and safe path to shore. You can similarly depend on Vanguard to put

you first––and light the way––as you strive to meet your financial goals. Our client focus and low costs,

stemming from our unique ownership structure, assure that your interests are paramount.

Your Fund’s Performance at a Glance

• For the 12 months ended September 30, 2017, Vanguard U.S. Value Fund

returned nearly 18%, outpacing both its benchmark index and the average return

of its peer group.

• Your fund’s stock selection model generated broad-based performance. The model

focuses on five signals that rank a universe of stocks. Four of those signals—valuation,

growth, sentiment, and management decisions—contributed to performance. In

particular, the valuation and growth signals were significant drivers of the fund’s return.

• Seven of the fund’s 11 industry sectors generated positive results, led by information

technology, materials, and health care.

• Stocks in the energy and consumer discretionary sectors were among those that

detracted most from performance. In addition, growth stocks outperformed their value

counterparts during the period.

| |

| Total Returns: Fiscal Year Ended September 30, 2017 | |

| | Total |

| | Returns |

| Vanguard U.S. Value Fund | 17.87% |

| Russell 3000 Value Index | 15.53 |

| Multi-Cap Value Funds Average | 16.69 |

Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.

| |

| Total Returns: Ten Years Ended September 30, 2017 | |

| | Average |

| | Annual Return |

| U.S. Value Fund | 6.53% |

| Russell 3000 Value Index | 6.01 |

| Multi-Cap Value Funds Average | 5.39 |

Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company.

The figures shown represent past performance, which is not a guarantee of future results. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost.

1

| | |

| Expense Ratios | | |

| Your Fund Compared With Its Peer Group | | |

| | | Peer Group |

| | Fund | Average |

| U.S. Value Fund | 0.23% | 1.10% |

The fund expense ratio shown is from the prospectus dated January 26, 2017, and represents estimated costs for the current fiscal year. For the fiscal year ended September 30, 2017, the fund’s expense ratio was 0.23%. The peer-group expense ratio is derived from data provided by Lipper, a Thomson Reuters Company, and captures information through year-end 2016.

Peer group: Multi-Cap Value Funds.

2

Chairman’s Perspective

Bill McNabb

Chairman and Chief Executive Officer

Dear Shareholder,

Our investors depend on Vanguard to be a responsible steward of their assets. This includes our obvious responsibilities—managing the funds, offering investment perspectives and advice, and assisting with questions and transactions.

But because a long-term perspective informs every aspect of our investment approach, we also work on your behalf in less obvious ways, such as by advocating for responsible governance among the companies in which Vanguard funds invest. Vanguard’s index funds are essentially permanent owners of thousands of publicly traded companies, and we have a special obligation to be engaged stewards actively focused on the long term.

Simply put, we believe that well-governed companies are more likely to perform well over the long run.

Although Vanguard has always been an advocate for strong corporate governance, we have expanded our efforts recently as our investor base continues to grow. Our Investment Stewardship team has doubled in size since 2015, and we continue to add analysts, researchers, and operations team members. The team guides our engagement activities and our funds’ proxy voting by analyzing corporate governance practices in companies around the world.

3

Our four Investment Stewardship pillars

As we evaluate company responsiveness to governance matters, including environmental and social concerns, we focus on four key areas—what we call our Investment Stewardship pillars:

• The board: A high-functioning, well-composed, independent, diverse, and experienced board with effective ongoing evaluation practices.

• Governance structures: Provisions and structures that empower shareholders and protect their rights.

• Appropriate compensation: Pay that incentivizes relative outperformance over the long term.

• Risk oversight: Effective, integrated, and ongoing oversight of relevant industry-and company-specific risks.

Guided by these pillars, our Investment Stewardship team conducted more than 950 engagements, or discussions, with company directors and leaders worldwide during the 12 months ended June 30, 2017.

| | | |

| Market Barometer | | | |

| | | Average Annual Total Returns |

| | Periods Ended September 30, 2017 |

| | One Year | Three Years | Five Years |

| Stocks | | | |

| Russell 1000 Index (Large-caps) | 18.54% | 10.63% | 14.27% |

| Russell 2000 Index (Small-caps) | 20.74 | 12.18 | 13.79 |

| Russell 3000 Index (Broad U.S. market) | 18.71 | 10.74 | 14.23 |

| FTSE All-World ex US Index (International) | 19.49 | 5.11 | 7.35 |

| |

| Bonds | | | |

| Bloomberg Barclays U.S. Aggregate Bond Index | | | |

| (Broad taxable market) | 0.07% | 2.71% | 2.06% |

| Bloomberg Barclays Municipal Bond Index | | | |

| (Broad tax-exempt market) | 0.87 | 3.19 | 3.01 |

| Citigroup Three-Month U.S. Treasury Bill Index | 0.64 | 0.28 | 0.18 |

| |

| CPI | | | |

| Consumer Price Index | 2.23% | 1.22% | 1.30% |

4

We also cast more than 171,000 votes on behalf of Vanguard funds at more than 18,000 shareholder meetings.

Gender diversity on boards and climate risk

As we engage with companies, we are devoting increased attention to two specific topics. The first is gender diversity on boards. It’s no secret that the right combination of talent, skills, and experience leads to better results, so we pay close attention to how company boards are structured and managed, and how they evolve.

In recent years, a growing body of research has demonstrated that greater diversity on boards can lead to improved governance and company performance. We are advocating for boards to incorporate diverse perspectives and experience into their strategic planning and decision-making. One example of our commitment to more diverse boards is our participation in the 30% Club, a global coalition working to increase the representation of women in boardrooms and leadership roles.

The second issue is climate risk. We will continue to engage with companies to understand their responses to this risk. Regardless of one’s perspective on the issue, the potential is real for changing regulations, demographics, and consumption behavior to affect business results for companies in many sectors.

We want to ensure that such business and regulatory risks are sufficiently disclosed so investors can value companies appropriately. In the past year, we have voted for shareholder proposals at several energy companies that called for management to improve its climate risk assessment and planning, and we will consider supporting similar proposals if we believe they are beneficial to long-term shareholder value. When a proposal from a shareholder presents a strong case for change, we’re more than willing to fully consider it. And even if the case falls short, these proposals often catalyze a discussion that generates meaningful change over time.

In addition to considering activists’ proposals, we consult research providers and our own network of experts. When we detect material risks to a company’s long-term value (such as bad leadership, poor disclosure, misaligned compensation structures, or threats to shareholder rights), we act with our voice and our vote.

Our stewardship reflects our mission

But we don’t act as independent agents with our own agenda. Every time we speak with a company chairman, CEO, or director, we’re acutely aware of the role we play in representing the economic interests of more than 20 million Vanguard investors. So you can expect us to speak out when we detect threats to the economic interests of our shareholders.

5

We take positions on these matters not because they are inherently good or noble but because they are tied to the long-term economic value of your funds’ investments.

You trust us to represent your interests across the globe. You can be confident we act on that responsibility with the seriousness and dedication it deserves.

To learn more about our Investment Stewardship program, including how our funds have voted, visit https://about. vanguard.com/investment-stewardship/.

As always, thank you for investing with Vanguard.

F. William McNabb III

Chairman and Chief Executive Officer

October 13, 2017

6

Advisor’s Report

For the 12 months ended September 30, 2017, Vanguard U.S. Value Fund returned nearly 18%. The fund bested its benchmark index, the Russell 3000 Value Index, which returned well over 15%. It also outperformed the average return of its peer group.

Investment environment

As the period began, investors cheered stronger-than-expected third-quarter economic growth that stood in contrast to disappointing results earlier in 2016. That exuberance gained steam after the U.S. presidential election as investors anticipated the benefits of the new administration’s policy initiatives focused on tax reform, infrastructure spending, and greater deregulation. That optimism fueled a move toward riskier assets, propelling many bellwether stock indexes to record highs in 2017.

The Federal Reserve also acknowledged the strength of the U.S. economy. In December, as inflation inched closer to the Fed’s 2% target level, it raised the federal funds rate by a quarter percentage point—only the second increase in a decade. Optimism waned a bit in early 2017 as investors realized policy initiatives would take longer to materialize than had been anticipated. But consumers continued to open their wallets and unemployment continued to decline.

Those developments played a large part in the Fed’s decision to raise rates in March and June, pushing its target range to 1%–1.25%. Those moves, along with the

establishment of a framework for trimming its $4.5 trillion balance sheet, took the Fed closer to normalizing monetary policy after its emergency intervention in response to the Great Recession.

Despite those positive developments, disappointing inflation measures confounded some market outlooks. Annualized core inflation softened a little during the spring. In response, the Fed scaled back its 2017 inflation forecast but still expected inflation to move closer to its 2% target over the medium term. Further tightening in the labor market should help, although wage gains have been modest.

Over the period, the broad U.S. equity market (as measured by the Russell 3000 Index) returned nearly 19%. U.S. stock market performance was broad-based; nine of 11 market sectors advanced, led by financials, materials, and industrials. Growth stocks outperformed their value counterparts, small-capitalization stocks topped large-caps, and international and emerging-market equities outperformed their U.S. peers.

Many other countries posted decent growth, but major central banks such as the Bank of Japan, the Bank of England, and the European Central Bank remained in accommodative policy mode as they struggled to balance growth and inflation concerns. Even with a weaker U.S. dollar, comparatively low yields across many developed markets kept U.S. bonds attractive to international investors.

7

Investment objective and strategy

Although it’s important to understand how overall performance is affected by the macroeconomic factors we’ve described, our strategy focuses on company-specific fundamentals—not technical analysis. Our stock selection model evaluates companies within our investment universe to identify those with attractive characteristics that we believe will outperform over the long run.

To do this, we use a strict quantitative process that focuses on a combination of five key themes: high quality—healthy balance sheets and consistent cash-flow generation; effective use of capital—sound investment policies that favor internal over external funding; consistent earnings growth—a demonstrated ability to grow earnings year after year; strong market sentiment—market confirmation of our view; and reasonable valuation—avoidance of overpriced stocks.

The interaction of these themes generates an opinion on all the stocks in our universe each day. We monitor our portfolio based on those rankings and adjust when appropriate. Our approach also includes a dynamic weighting process that shifts the relative importance of the themes over time. Using the results of our model, we then construct our portfolio with the goal of maximizing expected return, while minimizing exposure to risks that our research indicates do not improve returns, such as industry selection and other risks relative to our benchmark.

Our successes and failures

The fund’s outperformance was driven by our valuation signal, especially in the beginning of the period, and our growth signal. The sentiment and management decisions signals contributed to a lesser degree.

Stock selection results were positive in seven sectors, with information technology, materials, and health care leading the way. Energy and consumer discretionary were among the sectors that detracted the most.

Our overweighting of semiconductor manufacturer NVIDIA contributed significantly to our strength in information technology. AK Steel, Chemours, Advanced Micro Devices, and Bank of America were also top contributors.

Energy sector companies such as Denbury Resources, Newfield Exploration, Sanchez Energy, and Chesapeake Energy hurt most.

Portfolio Managers:

James P. Stetler

Binbin Guo, Principal,

Head of Alpha Equity Investments

Vanguard Quantitative Equity Group

October 12, 2017

8

U.S. Value Fund

Fund Profile

As of September 30, 2017

| | | |

| Portfolio Characteristics | | |

| | | | DJ |

| | | | U.S. |

| | | Russell | Total |

| | | 3000 | Market |

| | | Value | FA |

| | Fund | Index | Index |

| Number of Stocks | 230 | 2,110 | 3,808 |

| Median Market Cap | $36.6B | $55.2B | $61.4B |

| Price/Earnings Ratio | 18.0x | 18.8x | 21.9x |

| Price/Book Ratio | 2.1x | 1.9x | 2.9x |

| Return on Equity | 11.5% | 10.9% | 15.1% |

| Earnings Growth | | | |

| Rate | 7.4% | 6.3% | 9.6% |

| Dividend Yield | 2.2% | 2.3% | 1.8% |

| Foreign Holdings | 0.2% | 0.0% | 0.0% |

| Turnover Rate | 95% | — | — |

| Ticker Symbol | VUVLX | — | — |

| Expense Ratio1 | 0.23% | — | — |

| 30-Day SEC Yield | 2.07% | — | — |

| Short-Term Reserves | 0.2% | — | — |

| | | |

| Sector Diversification (% of equity exposure) |

| | | Russell | DJ |

| | | 3000 | U.S. Total |

| | | Value | Market |

| | Fund | Index | FA Index |

| Consumer Discretionary | 7.0% | 7.0% | 12.3% |

| Consumer Staples | 8.3 | 8.2 | 7.3 |

| Energy | 10.4 | 10.5 | 5.8 |

| Financials | 26.2 | 26.4 | 15.0 |

| Health Care | 13.3 | 13.3 | 14.0 |

| Industrials | 8.9 | 8.8 | 10.8 |

| Information Technology | 8.4 | 8.3 | 22.3 |

| Materials | 2.9 | 3.0 | 3.4 |

| Real Estate | 5.4 | 5.3 | 4.0 |

| Telecommunication | | | |

| Services | 3.0 | 3.0 | 2.0 |

| Utilities | 6.2 | 6.2 | 3.1 |

| | |

| Volatility Measures | | |

| | Russell | DJ |

| | 3000 | U.S. Total |

| | Value | Market |

| | Index | FA Index |

| R-Squared | 0.94 | 0.86 |

| Beta | 1.01 | 0.98 |

These measures show the degree and timing of the fund’s

fluctuations compared with the indexes over 36 months.

| | |

| Ten Largest Holdings (% of total net assets) |

| Exxon Mobil Corp. | Integrated Oil & Gas | 3.1% |

| JPMorgan Chase & Co. | Diversified Banks | 3.1 |

| Chevron Corp. | Integrated Oil & Gas | 2.2 |

| Procter & Gamble Co. | Household Products | 2.2 |

| Berkshire Hathaway Inc. Multi-Sector | |

| | Holdings | 2.1 |

| Pfizer Inc. | Pharmaceuticals | 2.1 |

| Bank of America Corp. | Diversified Banks | 2.1 |

| Citigroup Inc. | Diversified Banks | 2.1 |

| AT&T Inc. | Integrated | |

| | Telecommunication | |

| | Services | 2.0 |

| Johnson & Johnson | Pharmaceuticals | 1.9 |

| Top Ten | | 22.9% |

The holdings listed exclude any temporary cash investments and

equity index products.

Investment Focus

Sector categories are based on the Global Industry Classification

Standard (“GICS”), except for the “Other” category (if applicable),

which includes securities that have not been provided a GICS

classification as of the effective reporting period.

1 The expense ratio shown is from the prospectus dated January 26, 2017, and represents estimated costs for the current fiscal year. For the fiscal year ended September 30, 2017, the expense ratio was 0.23%.

9

U.S. Value Fund

Performance Summary

All of the returns in this report represent past performance, which is not a guarantee of future results that may be achieved by the fund. (Current performance may be lower or higher than the performance data cited. For performance data current to the most recent month-end, visit our website at vanguard.com/performance.) Note, too, that both investment returns and principal value can fluctuate widely, so an investor’s shares, when sold, could be worth more or less than their original cost. The returns shown do not reflect taxes that a shareholder would pay on fund distributions or on the sale of fund shares.

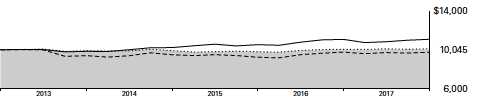

Cumulative Performance: September 30, 2007, Through September 30, 2017

Initial Investment of $10,000

| | | | | |

| | | Average Annual Total Returns | |

| | | Periods Ended September 30, 2017 | |

| | | | | | Final Value |

| | | One | Five | Ten | of a $10,000 |

| | | Year | Years | Years | Investment |

| | U.S. Value Fund* | 17.87% | 14.01% | 6.53% | $18,830 |

| • • • • • • • • | Russell 3000 Value Index | 15.53 | 13.20 | 6.01 | 17,926 |

| – – – – | Multi-Cap Value Funds Average | 16.69 | 12.32 | 5.39 | 16,908 |

| | Dow Jones U.S. Total Stock Market | | | | |

| | Float Adjusted Index | 18.67 | 14.15 | 7.64 | 20,887 |

| Multi-Cap Value Funds Average: Derived from data provided by Lipper, a Thomson Reuters Company. | | |

See Financial Highlights for dividend and capital gains information.

10

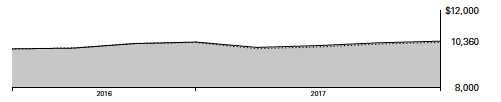

U.S. Value Fund

Fiscal-Year Total Returns (%): September 30, 2007, Through September 30, 2017

11

U.S. Value Fund

Financial Statements

Statement of Net Assets

As of September 30, 2017

The fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter-ends. For the second and fourth fiscal quarters, the lists appear in the fund’s semiannual and annual reports to shareholders. For the first and third fiscal quarters, the fund files the lists with the Securities and Exchange Commission on Form N-Q. Shareholders can look up the fund’s Forms N-Q on the SEC’s website at sec.gov. Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room (see the back cover of this report for further information).

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| Common Stocks (99.5%)1 | | |

| Consumer Discretionary (7.0%) | |

| | Best Buy Co. Inc. | 184,448 | 10,506 |

| | Comcast Corp. Class A | 263,023 | 10,121 |

| | Coach Inc. | 232,498 | 9,365 |

| | Lear Corp. | 54,053 | 9,356 |

| | Carnival Corp. | 141,480 | 9,135 |

| * | Liberty Media Corp- | | |

| | Liberty SiriusXM Class | | |

| | A Shares | 210,839 | 8,834 |

| * | Burlington Stores Inc. | 87,400 | 8,343 |

| * | Discovery | | |

| | Communications Inc. | | |

| | Class A | 299,521 | 6,377 |

| | New York Times Co. | | |

| | Class A | 316,333 | 6,200 |

| | General Motors Co. | 143,549 | 5,797 |

| | Royal Caribbean | | |

| | Cruises Ltd. | 47,745 | 5,660 |

| | Hasbro Inc. | 41,730 | 4,076 |

| * | Cooper-Standard | | |

| | Holdings Inc. | 26,268 | 3,046 |

| | Twenty-First Century | | |

| | Fox Inc. Class A | 108,834 | 2,871 |

| | MDC Holdings Inc. | 84,154 | 2,795 |

| | Office Depot Inc. | 601,483 | 2,731 |

| | Ralph Lauren Corp. | | |

| | Class A | 25,591 | 2,259 |

| | Twenty-First Century | | |

| | Fox Inc. | 52,971 | 1,366 |

| | Target Corp. | 19,185 | 1,132 |

| ^ | Big 5 Sporting Goods | | |

| | Corp. | 145,850 | 1,116 |

| | Time Warner Inc. | 10,030 | 1,028 |

| * | Iconix Brand Group Inc. | 175,125 | 996 |

| | Aaron’s Inc. | 20,592 | 898 |

| | Tailored Brands Inc. | 59,475 | 859 |

| * | Gray Television Inc. | 36,005 | 565 |

| | | |

| | KB Home | 23,075 | 557 |

| | Toll Brothers Inc. | 11,389 | 472 |

| | | | 116,461 |

| Consumer Staples (8.2%) | | |

| | Procter & Gamble Co. | 397,545 | 36,169 |

| | Philip Morris | | |

| | International Inc. | 213,172 | 23,664 |

| | Wal-Mart Stores Inc. | 274,463 | 21,447 |

| | Walgreens Boots | | |

| | Alliance Inc. | 148,670 | 11,480 |

| | Conagra Brands Inc. | 289,686 | 9,774 |

| | Sanderson Farms Inc. | 57,160 | 9,232 |

| | Hershey Co. | 64,543 | 7,046 |

| | PepsiCo Inc. | 44,280 | 4,934 |

| | Bunge Ltd. | 55,176 | 3,832 |

| * | Pilgrim’s Pride Corp. | 112,317 | 3,191 |

| | CVS Health Corp. | 39,202 | 3,188 |

| | Universal Corp. | 19,523 | 1,119 |

| * | HRG Group Inc. | 57,067 | 891 |

| | Campbell Soup Co. | 17,676 | 828 |

| | Kimberly-Clark Corp. | 7,010 | 825 |

| | | | 137,620 |

| Energy (10.4%) | | |

| | Exxon Mobil Corp. | 640,325 | 52,494 |

| | Chevron Corp. | 316,482 | 37,187 |

| | Valero Energy Corp. | 174,527 | 13,426 |

| | Halliburton Co. | 220,379 | 10,144 |

| | Williams Cos. Inc. | 333,707 | 10,015 |

| *,^ | Chesapeake Energy | | |

| | Corp. | 1,809,458 | 7,781 |

| | Devon Energy Corp. | 168,409 | 6,182 |

| | Baker Hughes a GE Co. | 134,641 | 4,931 |

| ^ | RPC Inc. | 197,635 | 4,899 |

| * | Newfield Exploration Co. | 157,753 | 4,680 |

| * | Peabody Energy Corp. | 155,297 | 4,505 |

| | Phillips 66 | 43,157 | 3,954 |

| | Schlumberger Ltd. | 49,084 | 3,424 |

| * | Exterran Corp. | 99,487 | 3,145 |

12

U.S. Value Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| * | Laredo Petroleum Inc. | 149,318 | 1,931 |

| * | Abraxas Petroleum Corp. | 516,877 | 972 |

| | Delek US Holdings Inc. | 31,474 | 841 |

| * | Denbury Resources Inc. | 602,127 | 807 |

| * | W&T Offshore Inc. | 257,786 | 786 |

| * | SandRidge Energy Inc. | 32,793 | 659 |

| * | McDermott International | | |

| | Inc. | 76,382 | 555 |

| * | REX American Resources | | |

| | Corp. | 5,003 | 469 |

| | CVR Energy Inc. | 17,177 | 445 |

| | | | 174,232 |

| Financials (26.1%) | | |

| | JPMorgan Chase & Co. | 540,838 | 51,655 |

| * | Berkshire Hathaway Inc. | | |

| | Class B | 193,497 | 35,472 |

| | Bank of America Corp. | 1,388,345 | 35,181 |

| | Citigroup Inc. | 475,238 | 34,569 |

| | Wells Fargo & Co. | 464,484 | 25,616 |

| | Goldman Sachs Group Inc. | 85,230 | 20,216 |

| | PNC Financial Services | | |

| | Group Inc. | 128,872 | 17,368 |

| | Morgan Stanley | 356,198 | 17,158 |

| | Bank of New York | | |

| | Mellon Corp. | 293,952 | 15,585 |

| | State Street Corp. | 137,477 | 13,135 |

| | Aflac Inc. | 148,012 | 12,047 |

| | Regions Financial Corp. | 764,727 | 11,647 |

| | Citizens Financial | | |

| | Group Inc. | 307,046 | 11,628 |

| | Allstate Corp. | 123,602 | 11,360 |

| | Lincoln National Corp. | 151,072 | 11,101 |

| | T. Rowe Price Group Inc. | 120,522 | 10,925 |

| | Unum Group | 206,536 | 10,560 |

| | Comerica Inc. | 127,670 | 9,736 |

| | Everest Re Group Ltd. | 42,594 | 9,728 |

| | Ameriprise Financial Inc. | 61,656 | 9,157 |

| | Assured Guaranty Ltd. | 224,235 | 8,465 |

| * | Walker & Dunlop Inc. | 130,529 | 6,831 |

| | Discover Financial | | |

| | Services | 105,159 | 6,781 |

| | Zions Bancorporation | 143,376 | 6,764 |

| | Leucadia National Corp. | 211,444 | 5,339 |

| | Universal Insurance | | |

| | Holdings Inc. | 217,019 | 4,991 |

| | American Express Co. | 51,238 | 4,635 |

| | SunTrust Banks Inc. | 57,003 | 3,407 |

| | CNO Financial Group Inc. | 138,788 | 3,239 |

| | Torchmark Corp. | 28,164 | 2,256 |

| | US Bancorp | 40,502 | 2,170 |

| | East West Bancorp Inc. | 32,318 | 1,932 |

| | Primerica Inc. | 19,997 | 1,631 |

| | Raymond James | | |

| | Financial Inc. | 10,558 | 890 |

| | Ally Financial Inc. | 35,344 | 857 |

| | | |

| * | Credit Acceptance Corp. | 3,036 | 851 |

| | Principal Financial Group | | |

| | Inc. | 12,925 | 832 |

| | American Financial Group | | |

| | Inc. | 7,995 | 827 |

| | Federal Agricultural | | |

| | Mortgage Corp. | 10,908 | 793 |

| | Capital One Financial Corp. | 6,843 | 579 |

| | | | 437,914 |

| Health Care (13.3%) | | |

| | Pfizer Inc. | 991,878 | 35,410 |

| | Johnson & Johnson | 250,973 | 32,629 |

| | Merck & Co. Inc. | 457,173 | 29,273 |

| | Bristol-Myers Squibb Co. | 251,719 | 16,044 |

| | Anthem Inc. | 75,730 | 14,380 |

| * | Centene Corp. | 108,191 | 10,470 |

| | Agilent Technologies Inc. | 158,181 | 10,155 |

| | Cigna Corp. | 50,260 | 9,396 |

| | Humana Inc. | 35,454 | 8,638 |

| * | WellCare Health Plans Inc. | 49,772 | 8,548 |

| * | Quintiles IMS Holdings Inc. | 89,051 | 8,466 |

| | Baxter International Inc. | 134,006 | 8,409 |

| | Aetna Inc. | 49,648 | 7,894 |

| * | Express Scripts Holding Co. 124,595 | 7,889 |

| | Medtronic plc | 56,027 | 4,357 |

| | Amgen Inc. | 22,337 | 4,165 |

| | Abbott Laboratories | 39,877 | 2,128 |

| * | Exelixis Inc. | 60,640 | 1,469 |

| * | INC Research Holdings | | |

| | Inc. Class A | 17,240 | 902 |

| | Allergan plc | 3,939 | 807 |

| * | OraSure Technologies Inc. | 26,786 | 603 |

| | | | 222,032 |

| Industrials (8.8%) | | |

| | Honeywell International | | |

| | Inc. | 99,030 | 14,037 |

| | General Electric Co. | 570,370 | 13,792 |

| | Oshkosh Corp. | 121,671 | 10,043 |

| | Spirit AeroSystems | | |

| | Holdings Inc. Class A | 128,241 | 9,967 |

| | Caterpillar Inc. | 79,655 | 9,934 |

| | Owens Corning | 122,641 | 9,486 |

| * | United Rentals Inc. | 67,229 | 9,327 |

| | Lockheed Martin Corp. | 29,826 | 9,255 |

| | SkyWest Inc. | 179,152 | 7,865 |

| | Quad/Graphics Inc. | 301,013 | 6,806 |

| * | United Continental | | |

| | Holdings Inc. | 101,363 | 6,171 |

| | Global Brass & Copper | | |

| | Holdings Inc. | 177,763 | 6,008 |

| | Copa Holdings SA Class A | 42,473 | 5,289 |

| | Waste Management Inc. | 56,484 | 4,421 |

| | Wabash National Corp. | 183,039 | 4,177 |

| * | Meritor Inc. | 147,959 | 3,848 |

| | Timken Co. | 67,507 | 3,277 |

13

U.S. Value Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| * | Rush Enterprises Inc. | | |

| | Class A | 60,929 | 2,820 |

| | United Technologies Corp. | 20,219 | 2,347 |

| | GATX Corp. | 32,163 | 1,980 |

| * | Hawaiian Holdings Inc. | 44,826 | 1,683 |

| | American Airlines | | |

| | Group Inc. | 34,805 | 1,653 |

| | Allison Transmission | | |

| | Holdings Inc. | 32,313 | 1,213 |

| * | Harsco Corp. | 54,845 | 1,146 |

| | Rockwell Automation Inc. | 4,662 | 831 |

| | CECO Environmental Corp. | 46,275 | 392 |

| | | | 147,768 |

| Information Technology (8.3%) | |

| | Intel Corp. | 362,945 | 13,821 |

| | HP Inc. | 670,001 | 13,373 |

| | Cisco Systems Inc. | 376,386 | 12,658 |

| | Applied Materials Inc. | 188,617 | 9,825 |

| | Booz Allen Hamilton | | |

| | Holding Corp. Class A | 247,213 | 9,243 |

| *,^ | VMware Inc. Class A | 84,151 | 9,188 |

| *,^ | Advanced Micro Devices | | |

| | Inc. | 626,522 | 7,988 |

| | Oracle Corp. | 160,329 | 7,752 |

| | CDW Corp. | 115,793 | 7,642 |

| * | TTM Technologies Inc. | 463,242 | 7,120 |

| * | Extreme Networks Inc. | 443,102 | 5,268 |

| | DXC Technology Co. | 59,226 | 5,086 |

| | Travelport Worldwide Ltd. | 273,100 | 4,288 |

| * | CACI International Inc. | | |

| | Class A | 27,637 | 3,851 |

| | SYNNEX Corp. | 27,238 | 3,446 |

| * | ON Semiconductor Corp. | 140,265 | 2,591 |

| * | Anixter International Inc. | 29,302 | 2,491 |

| * | Amkor Technology Inc. | 234,081 | 2,470 |

| * | Dell Technologies Inc. | | |

| | Class V | 31,693 | 2,447 |

| | Western Digital Corp. | 21,144 | 1,827 |

| * | Micron Technology Inc. | 34,667 | 1,363 |

| | QUALCOMM Inc. | 26,000 | 1,348 |

| * | Ultra Clean Holdings Inc. | 40,914 | 1,253 |

| * | Sigma Designs Inc. | 165,961 | 1,046 |

| | Convergys Corp. | 23,908 | 619 |

| * | Unisys Corp. | 58,504 | 497 |

| * | Alpha & Omega | | |

| | Semiconductor Ltd. | 19,824 | 327 |

| * | Sykes Enterprises Inc. | 9,568 | 279 |

| | | | 139,107 |

| Materials (2.9%) | | |

| * | Freeport-McMoRan Inc. | 697,621 | 9,794 |

| | Huntsman Corp. | 342,172 | 9,382 |

| | Chemours Co. | 182,453 | 9,234 |

| * | Owens-Illinois Inc. | 345,192 | 8,685 |

| * | Louisiana-Pacific Corp. | 312,512 | 8,463 |

| | | |

| * | AdvanSix Inc. | 43,990 | 1,749 |

| | DowDuPont Inc. | 19,627 | 1,359 |

| * | Alcoa Corp. | 9,095 | 424 |

| | | | 49,090 |

| Real Estate (5.4%) | | |

| ^ | Omega Healthcare | | |

| | Investors Inc. | 284,946 | 9,093 |

| | Hospitality Properties | | |

| | Trust | 308,949 | 8,802 |

| | Lexington Realty Trust | 705,509 | 7,210 |

| | Senior Housing | | |

| | Properties Trust | 348,210 | 6,808 |

| | CoreCivic Inc. | 229,070 | 6,132 |

| | Sabra Health Care | | |

| | REIT Inc. | 270,866 | 5,943 |

| | GEO Group Inc. | 219,073 | 5,893 |

| *,2 | Forestar Group Inc. | 274,347 | 4,719 |

| | Xenia Hotels & Resorts | | |

| | Inc. | 216,625 | 4,560 |

| | Sunstone Hotel Investors | | |

| | Inc. | 283,139 | 4,550 |

| | CorEnergy Infrastructure | | |

| | Trust Inc. | 117,483 | 4,153 |

| | Government Properties | | |

| | Income Trust | 211,584 | 3,971 |

| | LaSalle Hotel Properties | 134,889 | 3,914 |

| | Select Income REIT | 119,680 | 2,803 |

| | Prologis Inc. | 35,223 | 2,235 |

| | NorthStar Realty Europe | | |

| | Corp. | 153,722 | 1,969 |

| ^ | Uniti Group Inc. | 116,709 | 1,711 |

| | National Health | | |

| | Investors Inc. | 20,588 | 1,591 |

| | Getty Realty Corp. | 35,690 | 1,021 |

| | Essex Property Trust Inc. | 3,629 | 922 |

| | Ashford Hospitality | | |

| | Trust Inc. | 128,054 | 854 |

| | Park Hotels & Resorts Inc. | 15,667 | 432 |

| | Chesapeake Lodging Trust | 12,749 | 344 |

| | Tier REIT Inc. | 17,398 | 336 |

| | | | 89,966 |

| Telecommunication Services (3.0%) | |

| | AT&T Inc. | 841,647 | 32,967 |

| * | T-Mobile US Inc. | 144,633 | 8,918 |

| * | Sprint Corp. | 496,059 | 3,859 |

| | Verizon Communications | | |

| | Inc. | 72,669 | 3,597 |

| | | | 49,341 |

| Utilities (6.1%) | | |

| | NextEra Energy Inc. | 114,889 | 16,837 |

| | PG&E Corp. | 187,919 | 12,795 |

| | CenterPoint Energy Inc. | 349,101 | 10,197 |

| | FirstEnergy Corp. | 320,282 | 9,874 |

| | Entergy Corp. | 129,275 | 9,872 |

14

U.S. Value Fund

| | | |

| | | | Market |

| | | | Value• |

| | | Shares | ($000) |

| | Ameren Corp. | 170,225 | 9,846 |

| | National Fuel Gas Co. | 154,473 | 8,745 |

| | NRG Energy Inc. | 239,855 | 6,138 |

| | DTE Energy Co. | 51,184 | 5,495 |

| | MDU Resources Group Inc. | 179,041 | 4,646 |

| | Xcel Energy Inc. | 76,688 | 3,629 |

| | PNM Resources Inc. | 56,434 | 2,274 |

| | AES Corp. | 146,749 | 1,617 |

| | Avangrid Inc. | 19,456 | 923 |

| | | | 102,888 |

| Total Common Stocks | | |

| (Cost $1,407,471) | | 1,666,419 |

| Temporary Cash Investments (1.4%)1 | |

| Money Market Fund (1.3%) | | |

| 3,4 | Vanguard Market Liquidity | | |

| | Fund, 1.223% | 222,053 | 22,210 |

| |

| | | Face | |

| | | Amount | |

| | | ($000) | |

| U. S. Government and Agency Obligations (0.1%) |

| 5 | United States Cash | | |

| | Management Bill, | | |

| | 1.048%, 1/2/18 | 1,000 | 997 |

| 5 | United States Treasury Bill, | | |

| | 1.107%, 12/28/17 | 400 | 399 |

| | | | 1,396 |

| Total Temporary Cash Investments | |

| (Cost $23,604) | | 23,606 |

| Total Investments (100.9%) | | |

| (Cost $1,431,075) | | 1,690,025 |

| |

| | Amount |

| | ($000) |

| Other Assets and Liabilities (-0.9%) | |

| Other Assets | |

| Receivables for Investment Securities Sold | 265 |

| Investment in Vanguard | 102 |

| Receivables for Accrued Income | 1,947 |

| Receivables for Capital Shares Issued | 597 |

| Variation Margin Receivable-Futures | |

| Contracts | 32 |

| Other Assets | 3,202 |

| Total Other Assets | 6,145 |

| Liabilities | |

| Payables for Investment Securities | |

| Purchased | (6,724) |

| Collateral for Securities on Loan | (11,837) |

| Payables for Capital Shares Redeemed | (914) |

| Payables to Vanguard | (1,380) |

| Other Liabilities | (4) |

| Total Liabilities | (20,859) |

| Net Assets (100%) | |

| Applicable to 85,358,971 outstanding | |

| $.001 par value shares of beneficial | |

| interest (unlimited authorization) | 1,675,311 |

| Net Asset Value Per Share | $19.63 |

15

U.S. Value Fund

| |

| At September 30, 2017, net assets consisted of: |

| | Amount |

| | ($000) |

| Paid-in Capital | 1,301,912 |

| Undistributed Net Investment Income | 23,033 |

| Accumulated Net Realized Gains | 91,362 |

| Unrealized Appreciation (Depreciation) | |

| Investment Securities | 258,950 |

| Futures Contracts | 54 |

| Net Assets | 1,675,311 |

• See Note A in Notes to Financial Statements.

* Non-income-producing security.

^ Includes partial security positions on loan to broker-dealers.

The total value of securities on loan is $11,344,000.

1 The fund invests a portion of its cash reserves in equity

markets through the use of index futures contracts. After

giving effect to futures investments, the fund’s effective

common stock and temporary cash investment positions

represent 100.0% and 0.9%, respectively, of net assets.

2 Security value determined using significant unobservable

inputs.

3 Affiliated money market fund available only to Vanguard funds

and certain trusts and accounts managed by Vanguard. Rate

shown is the 7-day yield.

4 Includes $11,837,000 of collateral received for securities

on loan.

5 Securities with a value of $509,000 have been segregated as

initial margin for open futures contracts.

REIT—Real Estate Investment Trust.

| | | | |

| Derivative Financial Instruments Outstanding as of Period End | | |

| |

| Futures Contracts | | | | |

| | | | | ($000) |

| | | | | Value and |

| | | Number of | | Unrealized |

| | | Long (Short) | Notional | Appreciation |

| | Expiration | Contracts | Amount | (Depreciation) |

| Long Futures Contracts | | | | |

| E-mini S&P 500 Index | December 2017 | 69 | 8,681 | 54 |

Unrealized appreciation (depreciation) on open futures contracts is required to be treated as realized gain (loss) for tax purposes.

See accompanying Notes, which are an integral part of the Financial Statements.

16

U.S. Value Fund

| |

| Statement of Operations | |

| |

| | Year Ended |

| | September 30, 2017 |

| | ($000) |

| Investment Income | |

| Income | |

| Dividends | 39,716 |

| Interest1 | 79 |

| Securities Lending—Net | 725 |

| Total Income | 40,520 |

| Expenses | |

| The Vanguard Group—Note B | |

| Investment Advisory Services | 1,034 |

| Management and Administrative | 2,146 |

| Marketing and Distribution | 270 |

| Custodian Fees | 24 |

| Auditing Fees | 35 |

| Shareholders’ Reports and Proxy | 87 |

| Trustees’ Fees and Expenses | 2 |

| Total Expenses | 3,598 |

| Net Investment Income | 36,922 |

| Realized Net Gain (Loss) | |

| Investment Securities Sold1 | 99,442 |

| Futures Contracts | 1,349 |

| Realized Net Gain (Loss) | 100,791 |

| Change in Unrealized Appreciation (Depreciation) | |

| Investment Securities1 | 109,838 |

| Futures Contracts | 38 |

| Change in Unrealized Appreciation (Depreciation) | 109,876 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 247,589 |

1 Interest income, realized net gain (loss), and change in unrealized appreciation (depreciation) from an affiliated company of the fund were $74,000, $3,000, and $0, respectively.

See accompanying Notes, which are an integral part of the Financial Statements.

17

U.S. Value Fund

| | |

| Statement of Changes in Net Assets | | |

| |

| | Year Ended September 30, |

| | 2017 | 2016 |

| | ($000) | ($000) |

| Increase (Decrease) in Net Assets | | |

| Operations | | |

| Net Investment Income | 36,922 | 34,546 |

| Realized Net Gain (Loss) | 100,791 | 23,090 |

| Change in Unrealized Appreciation (Depreciation) | 109,876 | 81,526 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 247,589 | 139,162 |

| Distributions | | |

| Net Investment Income | (30,933) | (26,754) |

| Realized Capital Gain1 | (22,230) | (48,800) |

| Total Distributions | (53,163) | (75,554) |

| Capital Share Transactions | | |

| Issued | 422,683 | 306,212 |

| Issued in Lieu of Cash Distributions | 50,256 | 71,550 |

| Redeemed | (365,711) | (282,648) |

| Net Increase (Decrease) from Capital Share Transactions | 107,228 | 95,114 |

| Total Increase (Decrease) | 301,654 | 158,722 |

| Net Assets | | |

| Beginning of Period | 1,373,657 | 1,214,935 |

| End of Period2 | 1,675,311 | 1,373,657 |

1 Includes fiscal 2017 and 2016 short-term gain distributions totaling $0 and $0, respectively. Short-term gain distributions are treated as ordinary income dividends for tax purposes.

2 Net Assets—End of Period includes undistributed (overdistributed) net investment income of $23,033,000 and $20,151,000.

See accompanying Notes, which are an integral part of the Financial Statements.

18

| | | | | |

| U.S. Value Fund | | | | | |

| |

| |

| Financial Highlights | | | | | |

| |

| |

| For a Share Outstanding | | | Year Ended September 30, |

| Throughout Each Period | 2017 | 2016 | 2015 | 2014 | 2013 |

| Net Asset Value, Beginning of Period | $17.25 | $16.48 | $16.95 | $14.41 | $11.89 |

| Investment Operations | | | | | |

| Net Investment Income | . 4371 | .440 | .355 | .299 | .304 |

| Net Realized and Unrealized Gain (Loss) | | | | | |

| on Investments | 2.606 | 1.341 | (.543) | 2.531 | 2.506 |

| Total from Investment Operations | 3.043 | 1.781 | (.188) | 2.830 | 2.810 |

| Distributions | | | | | |

| Dividends from Net Investment Income | (. 386) | (. 358) | (. 282) | (. 290) | (. 290) |

| Distributions from Realized Capital Gains | (.277) | (.653) | — | — | — |

| Total Distributions | (. 663) | (1.011) | (. 282) | (. 290) | (. 290) |

| Net Asset Value, End of Period | $19.63 | $17.25 | $16.48 | $16.95 | $14.41 |

| |

| Total Return2 | 17.87% | 11.09% | -1.18% | 19.89% | 24.16% |

| |

| Ratios/Supplemental Data | | | | | |

| Net Assets, End of Period (Millions) | $1,675 | $1,374 | $1,215 | $1,117 | $829 |

| Ratio of Total Expenses to Average Net Assets | 0.23% | 0.23% | 0.26% | 0.29% | 0.29% |

| Ratio of Net Investment Income to | | | | | |

| Average Net Assets | 2.36% | 2.63% | 2.10% | 1.92% | 2.26% |

| Portfolio Turnover Rate | 95% | 76% | 66% | 57% | 75% |

1 Calculated based on average shares outstanding.

2 Total returns do not include account service fees that may have applied in the periods shown. Fund prospectuses provide information about any applicable account service fees.

See accompanying Notes, which are an integral part of the Financial Statements.

19

U.S. Value Fund

Notes to Financial Statements

Vanguard U.S. Value Fund is registered under the Investment Company Act of 1940 as an open-end investment company, or mutual fund.

A. The following significant accounting policies conform to generally accepted accounting principles for U.S. investment companies. The fund consistently follows such policies in preparing its financial statements.

1. Security Valuation: Securities are valued as of the close of trading on the New York Stock Exchange (generally 4 p.m., Eastern time) on the valuation date. Equity securities are valued at the latest quoted sales prices or official closing prices taken from the primary market in which each security trades; such securities not traded on the valuation date are valued at the mean of the latest quoted bid and asked prices. Securities for which market quotations are not readily available, or whose values have been materially affected by events occurring before the fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the board of trustees to represent fair value. Investments in Vanguard Market Liquidity Fund are valued at that fund’s net asset value. Temporary cash investments are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services.

2. Futures Contracts: The fund uses index futures contracts to a limited extent, with the objective of maintaining full exposure to the stock market while maintaining liquidity. The fund may purchase or sell futures contracts to achieve a desired level of investment, whether to accommodate portfolio turnover or cash flows from capital share transactions. The primary risks associated with the use of futures contracts are imperfect correlation between changes in market values of stocks held by the fund and the prices of futures contracts, and the possibility of an illiquid market. Counterparty risk involving futures is mitigated because a regulated clearinghouse is the counterparty instead of the clearing broker. To further mitigate counterparty risk, the fund trades futures contracts on an exchange, monitors the financial strength of its clearing brokers and clearinghouse, and has entered into clearing agreements with its clearing brokers. The clearinghouse imposes initial margin requirements to secure the fund’s performance and requires daily settlement of variation margin representing changes in the market value of each contract.

Futures contracts are valued at their quoted daily settlement prices. The notional amounts of the contracts are not recorded in the Statement of Net Assets. Fluctuations in the value of the contracts are recorded in the Statement of Net Assets as an asset (liability) and in the Statement of Operations as unrealized appreciation (depreciation) until the contracts are closed, when they are recorded as realized futures gains (losses).

During the year ended September 30, 2017, the fund’s average investments in long and short futures contracts represented less than 1% and 0% of net assets, respectively, based on the average of the notional amounts at each quarter-end during the period.

3. Federal Income Taxes: The fund intends to continue to qualify as a regulated investment company and distribute all of its taxable income. Management has analyzed the fund’s tax positions taken for all open federal income tax years (September 30, 2014–2017), and has concluded that no provision for federal income tax is required in the fund’s financial statements.

20

U.S. Value Fund

4. Distributions: Distributions to shareholders are recorded on the ex-dividend date.

5. Securities Lending: To earn additional income, the fund lends its securities to qualified institutional borrowers. Security loans are subject to termination by the fund at any time, and are required to be secured at all times by collateral in an amount at least equal to the market value of securities loaned. Daily market fluctuations could cause the value of loaned securities to be more or less than the value of the collateral received. When this occurs, the collateral is adjusted and settled on the next business day. The fund further mitigates its counterparty risk by entering into securities lending transactions only with a diverse group of prequalified counterparties, monitoring their financial strength, and entering into master securities lending agreements with its counterparties. The master securities lending agreements provide that, in the event of a counterparty’s default (including bankruptcy), the fund may terminate any loans with that borrower, determine the net amount owed, and sell or retain the collateral up to the net amount owed to the fund; however, such actions may be subject to legal proceedings. While collateral mitigates counterparty risk, in the event of a default, the fund may experience delays and costs in recovering the securities loaned. The fund invests cash collateral received in Vanguard Market Liquidity Fund, and records a liability in the Statement of Net Assets for the return of the collateral, during the period the securities are on loan. Securities lending income represents fees charged to borrowers plus income earned on invested cash collateral, less expenses associated with the loan. During the term of the loan, the fund is entitled to all distributions made on or in respect of the loaned securities.

6. Credit Facility: The fund and certain other funds managed by The Vanguard Group (“Vanguard”) participate in a $3.1 billion committed credit facility provided by a syndicate of lenders pursuant to a credit agreement that may be renewed annually; each fund is individually liable for its borrowings, if any, under the credit facility. Borrowings may be utilized for temporary and emergency purposes, and are subject to the fund’s regulatory and contractual borrowing restrictions. The participating funds are charged administrative fees and an annual commitment fee of 0.10% of the undrawn amount of the facility; these fees are allocated to the funds based on a method approved by the fund’s board of trustees and included in Management and Administrative expenses on the fund’s Statement of Operations. Any borrowings under this facility bear interest at a rate based upon the higher of the one-month London Interbank Offered Rate, federal funds effective rate, or overnight bank funding rate plus an agreed-upon spread.

The fund had no borrowings outstanding at September 30, 2017, or at any time during the period then ended.

7. Other: Dividend income is recorded on the ex-dividend date. Interest income includes income distributions received from Vanguard Market Liquidity Fund and is accrued daily. Premiums and discounts on debt securities purchased are amortized and accreted, respectively, to interest income over the lives of the respective securities. Security transactions are accounted for on the date securities are bought or sold. Costs used to determine realized gains (losses) on the sale of investment securities are those of the specific securities sold.

B. In accordance with the terms of a Funds’ Service Agreement (the “FSA”) between Vanguard and the fund, Vanguard furnishes to the fund investment advisory, corporate management, administrative, marketing, and distribution services at Vanguard’s cost of operations (as defined by the FSA). These costs of operations are allocated to the fund based on methods and guidelines approved by the board of trustees. Vanguard does not require reimbursement in the current period

21

U.S. Value Fund

for certain costs of operations (such as deferred compensation/benefits and risk/insurance costs); the fund’s liability for these costs of operations is included in Payables to Vanguard on the Statement of Net Assets.

Upon the request of Vanguard, the fund may invest up to 0.40% of its net assets as capital in Vanguard. At September 30, 2017, the fund had contributed to Vanguard capital in the amount of $102,000, representing 0.01% of the fund’s net assets and 0.04% of Vanguard’s capitalization. The fund’s trustees and officers are also directors and employees, respectively, of Vanguard.

C. Various inputs may be used to determine the value of the fund’s investments. These inputs are summarized in three broad levels for financial statement purposes. The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

Level 1—Quoted prices in active markets for identical securities.

Level 2—Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—Significant unobservable inputs (including the fund’s own assumptions used to determine the fair value of investments). Any investments valued with significant unobservable inputs are noted on the Statement of Net Assets.

The following table summarizes the market value of the fund’s investments as of September 30, 2017, based on the inputs used to value them:

| | | |

| | Level 1 | Level 2 | Level 3 |

| Investments | ($000) | ($000) | ($000) |

| Common Stocks | 1,661,700 | — | 4,719 |

| Temporary Cash Investments | 22,210 | 1,396 | — |

| Futures Contracts—Assets1 | 32 | — | — |

| Total | 1,683,942 | 1,396 | 4,719 |

| 1 Represents variation margin on the last day of the reporting period. | | | |

D. Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain, or loss are recognized in different periods for financial statement and tax purposes. These differences will reverse at some time in the future. Differences in classification may also result from the treatment of short-term gains as ordinary income for tax purposes.

The fund used a tax accounting practice to treat a portion of the price of capital shares redeemed during the year as distributions from net investment income and realized capital gains. Accordingly, the fund has reclassified $3,107,000 from undistributed net investment income, and $8,471,000 from accumulated net realized gains, to paid-in capital.

For tax purposes, at September 30, 2017, the fund had $46,927,000 of ordinary income and $68,731,000 of long-term capital gains available for distribution.

22

U.S. Value Fund

At September 30, 2017, the cost of investment securities for tax purposes was $1,431,075,000. Net unrealized appreciation of investment securities for tax purposes was $258,950,000, consisting of unrealized gains of $285,019,000 on securities that had risen in value since their purchase and $26,069,000 in unrealized losses on securities that had fallen in value since their purchase.

E. During the year ended September 30, 2017, the fund purchased $1,564,356,000 of investment securities and sold $1,473,193,000 of investment securities, other than temporary cash investments.

F. Capital shares issued and redeemed were:

| | |

| | Year Ended September 30, |

| | 2017 | 2016 |

| | Shares | Shares |

| | (000) | (000) |

| Issued | 22,746 | 18,669 |

| Issued in Lieu of Cash Distributions | 2,714 | 4,339 |

| Redeemed | (19,713) | (17,113) |

| Net Increase (Decrease) in Shares Outstanding | 5,747 | 5,895 |

G. Management has determined that no material events or transactions occurred subsequent to September 30, 2017, that would require recognition or disclosure in these financial statements.

23

Report of Independent Registered

Public Accounting Firm

To the Board of Trustees of Vanguard Malvern Funds and the Shareholders of Vanguard U.S.

Value Fund

In our opinion, the accompanying statement of net assets and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Vanguard U.S. Value Fund (constituting a separate portfolio of Vanguard Malvern Funds, hereafter referred to as the “Fund”) as of September 30, 2017, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities as of September 30, 2017 by correspondence with the custodian and brokers and by agreement to the underlying ownership records of the transfer agent, provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Philadelphia, Pennsylvania

November 13, 2017

Special 2017 tax information (unaudited) for Vanguard U.S. Value Fund

This information for the fiscal year ended September 30, 2017, is included pursuant to provisions

of the Internal Revenue Code.

The fund distributed $28,657,000 as capital gain dividends (20% rate gain distributions)

to shareholders during the fiscal year.

The fund distributed $27,329,000 of qualified dividend income to shareholders during the

fiscal year.

For corporate shareholders, 54.7% of investment income (dividend income plus short-term gains,

if any) qualifies for the dividends-received deduction.

24

Your Fund’s After-Tax Returns

This table presents returns for your fund both before and after taxes. The after-tax returns are shown in two ways: (1) assuming that an investor owned the fund during the entire period and paid taxes on the fund’s distributions, and (2) assuming that an investor paid taxes on the fund’s distributions and sold all shares at the end of each period.

Calculations are based on the highest individual federal income tax and capital gains tax rates in effect at the times of the distributions and the hypothetical sales. State and local taxes were not considered. After-tax returns reflect any qualified dividend income, using actual prior-year figures and estimates for 2017. (In the example, returns after the sale of fund shares may be higher than those assuming no sale. This occurs when the sale would have produced a capital loss. The calculation assumes that the investor received a tax deduction for the loss.)

Please note that your actual after-tax returns will depend on your tax situation and may differ from those shown. Also note that if you own the fund in a tax-deferred account, such as an individual retirement account or a 401(k) plan, this information does not apply to you. Such accounts are not subject to current taxes.

Finally, keep in mind that a fund’s performance—whether before or after taxes—does not guarantee future results.

| | | |

| Average Annual Total Returns: U.S. Value Fund | | | |

| Periods Ended September 30, 2017 | | | |

| | One | Five | Ten |

| | Year | Years | Years |

| Returns Before Taxes | 17.87% | 14.01% | 6.53% |

| Returns After Taxes on Distributions | 16.85 | 13.23 | 5.71 |

| Returns After Taxes on Distributions and Sale of Fund Shares | 10.79 | 11.15 | 5.07 |

25

About Your Fund’s Expenses

As a shareholder of the fund, you incur ongoing costs, which include costs for portfolio management, administrative services, and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund.

A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in your fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The accompanying table illustrates your fund’s costs in two ways:

• Based on actual fund return. This section helps you to estimate the actual expenses that you paid over the period. The ”Ending Account Value“ shown is derived from the fund‘s actual return, and the third column shows the dollar amount that would have been paid by an investor who started with $1,000 in the fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for your fund under the heading ”Expenses Paid During Period.“

• Based on hypothetical 5% yearly return. This section is intended to help you compare your fund‘s costs with those of other mutual funds. It assumes that the fund had a yearly return of 5% before expenses, but that the expense ratio is unchanged. In this case—because the return used is not the fund’s actual return—the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to calculate expenses based on a 5% return. You can assess your fund’s costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that the expenses shown in the table are meant to highlight and help you compare ongoing costs only and do not reflect transaction costs incurred by the fund for buying and selling securities. Further, the expenses do not include any purchase, redemption, or account service fees described in the fund prospectus. If such fees were applied to your account, your costs would be higher. Your fund does not carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

You can find more information about the fund’s expenses, including annual expense ratios, in the Financial Statements section of this report. For additional information on operating expenses and other shareholder costs, please refer to your fund’s current prospectus.

26

| | | |

| Six Months Ended September 30, 2017 | | | |

| | Beginning | Ending | Expenses |

| | Account Value | Account Value | Paid During |

| U.S. Value Fund | 3/31/2017 | 9/30/2017 | Period |

| Based on Actual Fund Return | $1,000.00 | $1,046.93 | $1.13 |

| Based on Hypothetical 5% Yearly Return | 1,000.00 | 1,023.97 | 1.12 |

The calculations are based on expenses incurred in the most recent six-month period. The fund’s annualized six-month expense ratio for that period is 0.22%. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period, then divided by the number of days in the most recent 12-month period (183/365).

27

Glossary

30-Day SEC Yield. A fund’s 30-day SEC yield is derived using a formula specified by the U.S. Securities and Exchange Commission. Under the formula, data related to the fund’s security holdings in the previous 30 days are used to calculate the fund’s hypothetical net income for that period, which is then annualized and divided by the fund’s estimated average net assets over the calculation period. For the purposes of this calculation, a security’s income is based on its current market yield to maturity (for bonds), its actual income (for asset-backed securities), or its projected dividend yield (for stocks). Because the SEC yield represents hypothetical annualized income, it will differ—at times significantly—from the fund’s actual experience. As a result, the fund’s income distributions may be higher or lower than implied by the SEC yield.

Beta. A measure of the magnitude of a fund’s past share-price fluctuations in relation to the ups and downs of a given market index. The index is assigned a beta of 1.00. Compared with a given index, a fund with a beta of 1.20 typically would have seen its share price rise or fall by 12% when the index rose or fell by 10%. For this report, beta is based on returns over the past 36 months for both the fund and the index. Note that a fund’s beta should be reviewed in conjunction with its R-squared (see definition). The lower the R-squared, the less correlation there is between the fund and the index, and the less reliable beta is as an indicator of volatility.

Dividend Yield. Dividend income earned by stocks, expressed as a percentage of the aggregate market value (or of net asset value, for a fund). The yield is determined by dividing the amount of the annual dividends by the aggregate value (or net asset value) at the end of the period. For a fund, the dividend yield is based solely on stock holdings and does not include any income produced by other investments.

Earnings Growth Rate. The average annual rate of growth in earnings over the past five years for the stocks now in a fund.

Equity Exposure. A measure that reflects a fund’s investments in stocks and stock futures. Any holdings in short-term reserves are excluded.

Expense Ratio. A fund’s total annual operating expenses expressed as a percentage of the fund’s average net assets. The expense ratio includes management and administrative expenses, but does not include the transaction costs of buying and selling portfolio securities.

Foreign Holdings. The percentage of a fund represented by securities or depositary receipts of companies based outside the United States.

Inception Date. The date on which the assets of a fund (or one of its share classes) are first invested in accordance with the fund’s investment objective. For funds with a subscription period, the inception date is the day after that period ends. Investment performance is measured from the inception date.

Median Market Cap. An indicator of the size of companies in which a fund invests; the midpoint of market capitalization (market price x shares outstanding) of a fund’s stocks, weighted by the proportion of the fund’s assets invested in each stock. Stocks representing half of the fund’s assets have market capitalizations above the median, and the rest are below it.

Price/Book Ratio. The share price of a stock divided by its net worth, or book value, per share.

For a fund, the weighted average price/book ratio of the stocks it holds.

28

Price/Earnings Ratio. The ratio of a stock’s current price to its per-share earnings over the past year. For a fund, the weighted average P/E of the stocks it holds. P/E is an indicator of market expectations about corporate prospects; the higher the P/E, the greater the expectations for a company’s future growth.

R-Squared. A measure of how much of a fund’s past returns can be explained by the returns from the market in general, as measured by a given index. If a fund’s total returns were precisely synchronized with an index’s returns, its R-squared would be 1.00. If the fund’s returns bore no relationship to the index’s returns, its R-squared would be 0. For this report, R-squared is based on returns over the past 36 months for both the fund and the index.

Return on Equity. The annual average rate of return generated by a company during the past five years for each dollar of shareholder’s equity (net income divided by shareholder’s equity). For a fund, the weighted average return on equity for the companies whose stocks it holds.

Short-Term Reserves. The percentage of a fund invested in highly liquid, short-term securities that can be readily converted to cash.

Turnover Rate. An indication of the fund’s trading activity. Funds with high turnover rates incur higher transaction costs and may be more likely to distribute capital gains (which may be taxable to investors). The turnover rate excludes in-kind transactions, which have minimal impact on costs.

29

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard and Poor’s, a division of McGraw-Hill Companies, Inc. (“S&P”), and is licensed for use by Vanguard. Neither MSCI, S&P nor any third party involved in making or compiling the GICS or any GICS classification makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of its affiliates or any third party involved in making or compiling the GICS or any GICS classification have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

30

The People Who Govern Your Fund

The trustees of your mutual fund are there to see that the fund is operated and managed in your best interests since, as a shareholder, you are a part owner of the fund. Your fund’s trustees also serve on the board of directors of The Vanguard Group, Inc., which is owned by the Vanguard funds and provides services to them on an at-cost basis.

A majority of Vanguard’s board members are independent, meaning that they have no affiliation with Vanguard or the funds they oversee, apart from the sizable personal investments they have made as private individuals. The independent board members have distinguished backgrounds in business, academia, and public service. Each of the trustees and executive officers oversees 198 Vanguard funds.

Information for each trustee and executive officer of the fund appears below. The mailing address of the trustees and officers is P.O. Box 876, Valley Forge, PA 19482. More information about the trustees is in the Statement of Additional Information, which can be obtained, without charge, by contacting Vanguard at 800-662-7447, or online at vanguard.com.

Interested Trustee1

F. William McNabb III

Born 1957. Trustee Since July 2009. Chairman of the Board. Principal Occupation(s) During the Past Five Years and Other Experience: Chairman of the Board of The Vanguard Group, Inc., and of each of the investment companies served by The Vanguard Group, since January 2010; Chief Executive Officer and Director of The Vanguard Group and President and Chief Executive Officer of each of the investment companies served by The Vanguard Group, since 2008; Director of Vanguard Marketing Corporation; President of The Vanguard Group (2008–2017); Managing Director of The Vanguard Group (1995–2008).

Independent Trustees

Emerson U. Fullwood

Born 1948. Trustee Since January 2008. Principal Occupation(s) During the Past Five Years and Other Experience: Executive Chief Staff and Marketing Officer for North America and Corporate Vice President (retired 2008) of Xerox Corporation (document management products and services);

Executive in Residence and 2009–2010 Distinguished Minett Professor at the Rochester Institute of Technology; Lead Director of SPX FLOW, Inc. (multi-industry manufacturing); Director of the United Way of Rochester, the University of Rochester Medical Center, Monroe Community College Foundation, North Carolina A&T University, and Roberts Wesleyan College; Trustee of the University of Rochester.

Rajiv L. Gupta

Born 1945. Trustee Since December 2001.2 Principal Occupation(s) During the Past Five Years and Other Experience: Chairman and Chief Executive Officer (retired 2009) and President (2006–2008) of Rohm and Haas Co. (chemicals); Director of Arconic Inc. (diversified manufacturer), HP Inc. (printer and personal computer manufacturing), and Delphi Automotive plc (automotive components); Senior Advisor at New Mountain Capital.

Amy Gutmann

Born 1949. Trustee Since June 2006. Principal Occupation(s) During the Past Five Years and Other Experience: President of the University of Pennsylvania; Christopher H. Browne

1 Mr. McNabb is considered an “interested person,” as defined in the Investment Company Act of 1940, because he is an officer of the Vanguard funds.

2 December 2002 for Vanguard Equity Income Fund, the Vanguard Municipal Bond Funds, and the Vanguard State Tax-Exempt Funds.

Distinguished Professor of Political Science, School of Arts and Sciences, and Professor of Communication, Annenberg School for Communication, with secondary faculty appointments in the Department of Philosophy, School of Arts and Sciences, and at the Graduate School of Education, University of Pennsylvania; Trustee of the National Constitution Center.

JoAnn Heffernan Heisen

Born 1950. Trustee Since July 1998. Principal Occupation(s) During the Past Five Years and Other Experience: Corporate Vice President and Member of the Executive Committee (1997–2008), Chief Global Diversity Officer (retired 2008), Vice President and Chief Information Officer (1997–2006), Controller (1995–1997), Treasurer (1991–1995), and Assistant Treasurer (1989–1991) of Johnson & Johnson (pharmaceuticals/medical devices/ consumer products); Director of Skytop Lodge Corporation (hotels) and the Robert Wood Johnson Foundation; Member of the Advisory Board of the Institute for Women’s Leadership at Rutgers University.

F. Joseph Loughrey

Born 1949. Trustee Since October 2009. Principal Occupation(s) During the Past Five Years and Other Experience: President and Chief Operating Officer (retired 2009) of Cummins Inc. (industrial machinery); Chairman of the Board of Hillenbrand, Inc. (specialized consumer services), Oxfam America, and the Lumina Foundation for Education; Director of the V Foundation for Cancer Research; Member of the Advisory Council for the College of Arts and Letters and Chair of the Advisory Board to the Kellogg Institute for International Studies, both at the University of Notre Dame.

Mark Loughridge

Born 1953. Trustee Since March 2012. Principal Occupation(s) During the Past Five Years and Other Experience: Senior Vice President and Chief Financial Officer (retired 2013) at IBM (information technology services); Fiduciary Member of IBM’s Retirement Plan Committee (2004–2013); Member of the Council on Chicago Booth.

Scott C. Malpass

Born 1962. Trustee Since March 2012. Principal Occupation(s) During the Past Five Years and Other Experience: Chief Investment Officer and Vice President at the University of Notre Dame; Assistant Professor of Finance at the Mendoza College of Business at Notre Dame; Member of the Notre Dame 403(b) Investment Committee, the Board of Advisors for Spruceview Capital Partners, the Board of Catholic Investment Services, Inc. (investment advisor), and the Board of Superintendence of the Institute for the Works of Religion; Chairman of the Board of TIFF Advisory Services, Inc. (investment advisor).

André F. Perold

Born 1952. Trustee Since December 2004. Principal Occupation(s) During the Past Five Years and Other Experience: George Gund Professor of Finance and Banking, Emeritus at the Harvard Business School (retired 2011); Chief Investment Officer and Co-Managing Partner of HighVista Strategies LLC (private investment firm); Overseer of the Museum of Fine Arts Boston.

Peter F. Volanakis

Born 1955. Trustee Since July 2009. Principal Occupation(s) During the Past Five Years and Other Experience: President and Chief Operating Officer (retired 2010) of Corning Incorporated (communications equipment); Chairman of the Board of Trustees of Colby-Sawyer College; Member of the Board of Hypertherm, Inc. (industrial cutting systems, software, and consumables).

Executive Officers

Glenn Booraem

Born 1967. Investment Stewardship Officer Since February 2017. Principal Occupation(s) During the Past Five Years and Other Experience: Principal of The Vanguard Group, Inc.; Treasurer (2015–2017), Controller (2010–2015), and Assistant Controller (2001–2010) of each of the investment companies served by The Vanguard Group.

Thomas J. Higgins

Born 1957. Chief Financial Officer Since September 2008. Principal Occupation(s) During the Past Five Years and Other Experience: Principal of The Vanguard Group, Inc.; Chief Financial Officer of each of the investment companies served by The Vanguard Group; Treasurer of each of the investment companies served by The Vanguard Group (1998–2008).

Peter Mahoney