UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811-05642 |

Nuveen Multi-Market Income Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: December 31, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | |

| | |  |

| Closed-End Funds | |

| | |

| | | Nuveen Investments |

| | | Closed-End Funds |

| | | | | | |

| | | | | | | Semi-Annual Report December 31, 2015 |

| | | |

| | | | | | |

| | | | | | | |

| JMM | | | | | | |

| Nuveen Multi-Market Income Fund | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| |

| | Life is Complex |

| |

| | Nuveen makes things e-simple. It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready – no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. |

| | |

| | Free e-Reports right to your e-mail! |

| |

| | www.investordelivery.com If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account. |

| |

| or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund dividends and statements directly from Nuveen. |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

For better or for worse, the financial markets spent most of the past year waiting for the U.S. Federal Reserve (Fed) to end its accommodative monetary policy. The policy has propped up stock and bond markets since the Great Recession, but the question remains: how will markets behave without its influence? This uncertainty was a considerable source of volatility for stock and bond prices for much of 2015, despite the Fed carefully conveying its intention to raise rates slowly and only when the economy shows evidence of readiness.

As was widely expected, the long-awaited Fed rate hike materialized in mid-December. While the move was interpreted as a vote of confidence on the U.S. economy’s underlying strength, the Fed emphasized that future rate increases will be gradual and guided by its ongoing assessment of financial conditions. Headwinds including rising borrowing costs, softer commodity prices, low inflation, a strong U.S. dollar and a stagnant global economy could necessitate keeping monetary conditions accommodative for longer. Meanwhile, policy makers in Europe and Japan are deploying their available tools to try to bolster their economies’ fragile growth, while Chinese authorities have stepped up efforts to manage China’s slowdown.

Although the new year began with a more pessimistic tone to investor sentiment and elevated volatility in the markets, we caution investors from making long-term decisions based on short-term news. In times like these, you can look to a professional investment manager with the experience and discipline to maintain the proper perspective on short-term events. And if the daily headlines do concern you, I encourage you to reach out to your financial advisor. Your financial advisor can help you evaluate your investment strategies in light of current events, your time horizon and risk tolerance.

On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

February 22, 2016

Portfolio Managers’

Comments

Nuveen Multi-Market Income Fund (JMM)

Nuveen Multi-Market Income Fund (JMM) is advised by Nuveen Fund Advisors, LLC (NFAL) and features portfolio management by Nuveen Asset Management, LLC (NAM). The portfolio management team includes Jason J. O’Brien, CFA, Chris J. Neuharth and John T. Fruit, CFA.

Here they discuss their portfolio management strategy and the performance of the Fund for the six-month reporting period ended December 31, 2015.

What key strategies were used to manage the Fund during this six-month reporting period ended December 31, 2015?

The Fund’s investment objective is to achieve high monthly income consistent with prudent risk to capital. The management team invests the Fund’s assets primarily in taxable fixed income securities including, but not limited to: U.S. agency and privately issued mortgage-backed securities; high yield and investment grade corporate bonds; and asset-backed securities.

How did the Fund perform during this six-month reporting period ended December 31, 2015?

The table in the Performance Overview and Holding Summaries section of this report provides total return performance for the Fund for the six-month, one-year, five-year and ten-year periods ended December 31, 2015. The Fund’s total return at net asset value (NAV) is compared with the performance of a corresponding market index. For the six-month reporting period ended December 31, 2015, JMM underperformed its blended benchmark, which is composed of 75% Barclays U.S. Government/Mortgage Index and 25% Barclays U.S. Corporate High-Yield Index.

The reporting period began with the U.S. economy showing resilience in the face of weaker growth experienced by the rest of the global economy. The key area of focus was China, which showed markedly slower manufacturing activity and uncertainty surrounding actual levels of consumption. Slower Chinese production and the ongoing weakness across emerging markets led to renewed volatility and weakness in commodity prices across the board. Oil prices were highly volatile throughout the reporting period, collapsing to a decade-low level of below $36-per-barrel level by December due to concerns over China’s slowdown, a global supply glut and the Organization of the Petroleum Exporting Countries (OPEC’s) decision to maintain current production levels. Fear over China and the uncertainty surrounding the Federal Reserve (Fed) policy normalization also caused market volatility to spike, spurring a significant sell-off in global equity markets beginning in mid-August. Despite broad speculation that it would increase rates in September for the first time in nearly a decade, the Fed decided to keep the federal funds rate near zero at that meeting. The nation’s relatively weak wage growth continued to be an area of keen interest for the Fed because it indicated that the U.S. economic recovery was far from robust. However, as the reporting period progressed, the U.S. economy continued to

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

expand at a moderate pace, while job growth improved with the unemployment rate falling to 5.0% in the final three months of the reporting period. Finally, at the Fed’s December meeting, policymakers began the long-awaited process of policy normalization by raising the federal funds rate by 0.25%, marking the end of a historically long period of low rates designed to boost the U.S. economic recovery. As a result, the Treasury yield curve flattened as rates for Treasuries with maturities of less than five years moved higher in earnest, while rates for intermediate- and long-term Treasuries fell modestly.

During the reporting period, spreads widened dramatically across all sectors as investors favored higher quality sectors of the market such as Treasuries and mortgage-backed securities, which outpaced corporate bonds, particularly high yield, by a wide margin. In the investment grade corporate market, commodity price volatility and heavy new issue supply kept technicals weak in higher risk sectors, causing lower quality bonds to underperform significantly. Analysts at ratings agencies reduced price forecasts for energy and metals, causing negative outlook changes for several issuers and exacerbating selling pressure in an already weak market. Market technicals were even weaker near the end of the year as dealers tried to keep inventory levels low, broadening declines across most industries. Merger and acquisition related financing also took a toll on the technical backdrop. However, financial spreads were steadier and this sector outperformed industrials by 121 basis points as the weakness in commodity-related bonds weighed down industrials. High yield bond prices were under extreme pressure as the risks of slower global growth, lower commodity prices and a hawkish Fed weighed on confidence. High yield spreads have been rising since mid-2014 and ended the reporting period trading well above their historical average as a percentage of the 10-year Treasury yield, reflecting the extremely negative sentiment. Lower quality bonds dramatically underperformed higher quality bonds as the flight to quality gained momentum.

Among the securitized sectors of the bond market, mortgage-backed securities (MBS) issued by government agencies such as Fannie Mae (FNMA), Ginnie Mae (GNMA) and Freddie Mac (FHLMC) performed well during the reporting period, posting positive excess returns versus Treasuries. Range-bound levels of implied volatility in the agency MBS segment were supportive from a fundamental perspective, while strong bank and money manager demand provided a solid technical backdrop. Homeowner refinancing activity was relatively subdued and MBS prepayments stabilized at historically low levels. The Fed implied that it will continue to re-invest MBS paydowns from its holdings until policy normalization is well under way, which gave investors comfort that technicals would remain favorable through much of 2016. Valuations were steady and investors embraced the combination of lower volatility and superior liquidity found in the agency MBS sector. Returns in the commercial mortgage-backed securities (CMBS) sector were lackluster during the reporting period as the segment underperformed Treasuries. Longer duration, newer vintage bonds struggled due to higher levels of new issuance and ongoing concerns about the quality of loans going into new deals. The valuation differential between CMBS deals became increasingly pronounced amid greater loan scrutiny in new deals. Traditional consumer asset-backed securities (ABS) generated positive excess returns over Treasuries as consumer credit trends remained favorable, although year-end balance sheet pressures and outflows from short-duration funds did create some technical pressure on the sector. ABS issuance was light given tepid investor demand for short, high quality paper as the Fed began the process of normalizing policy.

Our sector exposures generated mixed performance results, but overall were positive drivers of returns for the reporting period. The Fund’s performance benefited from our significant allocations to non-agency MBS and non-government mortgage-related ABS, which in aggregate represented between 35%-40% of its net assets during most of the reporting period. These segments once again outperformed the government and corporate sectors of the market. The Fund also maintained significant exposure to the CMBS sector, which underperformed Treasuries as excess returns were negative during the reporting period. Also, within the CMBS sector, lower rated investment grade securities lagged the broader index. Therefore, the Fund’s exposure to the CMBS sector and to the lower rated investment grade bonds within it were both detrimental to returns.

Conversely, our allocations to the credit sectors were modest contributors to investment results because the Fund had a small underweight to high yield credit throughout the reporting period. On the other hand, the Fund’s exposure to the metals/mining and energy sectors within credit held back investment performance.

In addition, we positioned the Fund with a defensive duration strategy in expectation of higher rates during the reporting period. While short-term rates rose modestly, long-term rates fell slightly and our interest rate strategy proved to be a slight drag on performance.

We anticipate the U.S. economy will continue to expand at a slightly below trend pace in 2016. Consumption is likely to remain supported by a healthy labor market and strong household balance sheets, while manufacturing and business spending continue to lag due to excess inventories, soft trade and volatility in the commodity sectors. Wage pressures are likely to remain contained. Along with subdued growth globally, the Fed will be able to slowly continue normalizing rates, likely at a pace even slower than its current official forecast. Therefore, we believe the Fed will remain very supportive of financial conditions, providing a constructive backdrop for corporate bonds. Outside of the United States, we believe central banks will likely remain highly accommodative. European growth is on track for continued improvement. Growth in emerging markets remains sluggish, burdened by China’s rebalancing, low and volatile commodity prices, diminished terms of trade and credit constraints in some regions.

Therefore, we continue to maintain the Fund’s emphasis on the non-agency MBS and CMBS sectors as both credit fundamentals and technicals remain supportive. We expect the high grade and high yield sectors of the corporate market will likely remain volatile, however, we increasingly believe that valuations are attractive enough to compensate investors for the slight deterioration in credit fundamentals and the current challenging liquidity environment. As always, we will continually evaluate relative value opportunities and shift the Fund’s exposures toward the segments of the market where we see the best long-term risk/reward equation. Because we expect rates to continue to gradually rise as 2016 progresses, we are maintaining a defensive bias with the Fund’s duration strategy.

We used U.S. Treasury futures as part of an overall portfolio construction strategy to manage portfolio duration and yield curve exposure. The effect of these activities during the reporting period was slightly negative. These derivative exposures are integrated with the overall portfolio construction and as such, losses and gains may be naturally related to and/or may offset impacts elsewhere in the portfolio.

Fund

Leverage

IMPACT OF THE FUND’S LEVERAGE STRATEGY ON PERFORMANCE

One important factor impacting the returns of the Fund relative to its benchmark was the Fund’s use of leverage through the use of reverse repurchase agreements and mortgage dollar rolls. The Fund uses leverage because our research has shown that, over time, leveraging provides opportunities for additional income and total return for common shareholders. However, use of leverage also can expose shareholders to additional volatility. For example, as the prices of securities held by the Fund decline, the negative impact of these valuation changes on NAV and total return is magnified by the use of leverage. Conversely, leverage may enhance common share returns during periods when the prices of securities held by the Fund generally are rising. The Fund’s use of leverage had a negative impact on performance during this reporting period.

As of December 31, 2015, the Fund’s percentages of leverage are shown in the accompanying table.

| | | | |

| | | JMM | |

Effective Leverage* | | | 29.21 | % |

Regulatory Leverage* | | | 0.00 | % |

| * | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

Share

Information

DISTRIBUTION INFORMATION

The following information regarding the Fund’s distributions is as of December 31, 2015. The Fund’s distribution levels may vary over time based on the Fund’s investment activity and portfolio investment value changes.

During the current reporting period, the Fund’s distributions to shareholders were as shown in the accompanying table.

| | | | |

| Ex-Dividend Date | | Per

Share

Amounts | |

July 2015 | | $ | 0.0400 | |

August | | | 0.0400 | |

September | | | 0.0400 | |

October | | | 0.0400 | |

November | | | 0.0400 | |

December 2015 | | | 0.0400 | |

Current Distribution Rate* | | | 6.76 | % |

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the amount of the Fund’s distributions, a return of capital for tax purposes. |

The Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit the Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s net asset value. Conversely, if the Fund has cumulatively paid in dividends more than it has earned, the excess will constitute a negative UNII that will likewise be reflected in the Fund’s net asset value. The Fund will, over time, pay all its net investment income as dividends to shareholders.

As of December 31, 2015, the Fund had a positive UNII balance, based upon our best estimate, for income tax purposes and a negative UNII balance for financial reporting purposes.

All monthly dividends paid by the Fund during the current reporting period, were paid from net investment income. If a portion of the Fund’s monthly distributions was sourced from or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders would have received a notice to that effect. For financial reporting purposes, the composition and per share amounts of the Fund’s dividends for the reporting period are presented in this report’s Statement of Changes in Net Assets and Financial Highlights, respectively. For income tax purposes, distribution information for the Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

SHARE REPURCHASES

During August 2015, the Fund’s Board of Trustees reauthorized an open-market share repurchase program, allowing the Fund to repurchase up to approximately 10% of its outstanding shares.

Share Information (continued)

As of December 31, 2015, and since the inception of the Fund’s repurchase program, the Fund has cumulatively repurchased and retired its outstanding shares as shown in the accompanying table.

| | | | |

| | | JMM | |

Shares cummulatively repurchased and retired | | | 1,800 | |

Approximate number of shares authorized for repurchase | | | 945,000 | |

During the current reporting period, the Fund repurchased and retired its common shares at a weighted average price per share and a weighted average discount per share as shown in the accompanying table.

| | | | |

| | | JMM | |

Shares repurchased and retired | | | 1,800 | |

Weighted average price per share repurchased and retired | | $ | 7.13 | |

Weighted average discount per share repurchased and retired | | | 14.62 | % |

OTHER SHARE INFORMATION

As of December 31, 2015, and during the current reporting period, the Fund’s common share price was trading at premium/(discount) to its NAV as shown in the accompanying table.

| | | | |

NAV | | $ | 8.00 | |

Share price | | $ | 7.10 | |

Premium/(Discount) to NAV | | | (11.25 | )% |

6-month average premium/(discount) to NAV | | | (13.33 | )% |

Risk

Considerations

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation.

Nuveen Multi-Market Income Fund (JMM)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. Investing in mortgage-backed securities entails credit risk, the risk that the servicer fails to perform its duties, liquidity risks, interest rate risks, structure risks, pre-payment risk, and geographical concentration risks. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. These and other risk considerations including hedging risk are described in more detail on the Fund’s web page at www.nuveen.com/JMM.

JMM

Nuveen Multi-Market Income Fund

Performance Overview and Holding Summaries as of December 31, 2015

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of December 31, 2015

| | | | | | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

| JMM at NAV | | | (1.94)% | | | | (0.55)% | | | | 5.43% | | | | 6.21% | |

| JMM at Share Price | | | 1.86% | | | | (1.21)% | | | | 3.61% | | | | 6.90% | |

| JMM Blended Benchmark | | | (1.02)% | | | | (0.26)% | | | | 3.42% | | | | 5.12% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

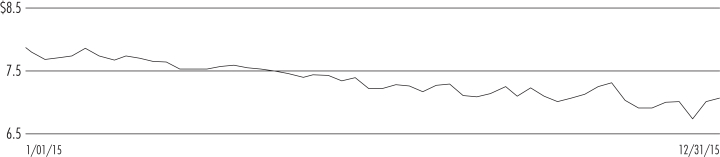

Share Price Performance — Weekly Closing Price

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Convertible Preferred Securities | | | 0.3% | |

| $25 Par (or similar) Retail Preferred | | | 0.5% | |

| Corporate Bonds | | | 31.0% | |

| $1,000 Par (or similar) Institutional Preferred | | | 0.4% | |

| Asset-Backed and Mortgage-Backed Securities | | | 106.6% | |

| Investment Companies | | | 0.6% | |

| Sovereign Debt | | | 0.2% | |

| Repurchase Agreements | | | 0.5% | |

| Other Assets Less Liabilities | | | (15.5)% | |

| Net Assets Plus Reverse Repurchase Agreements | | | 124.6% | |

| Reverse Repurchase Agreements | | | (24.6)% | |

| Net Assets | | | 100% | |

Portfolio Composition

(% of total investments)1

| | | | |

Asset-Backed and

Mortgage-Backed Securities | | | 76.1% | |

Oil, Gas & Consumable Fuels | | | 2.4% | |

Media | | | 1.9% | |

Banks | | | 1.7% | |

Health Care Providers & Services | | | 1.5% | |

Diversified Telecommunication Services | | | 1.5% | |

Other | | | 14.6% | |

Repurchase Agreements | | | 0.3% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term investments)1

| | | | |

AAA/U.S. Guaranteed | | | 24.1% | |

AA | | | 7.0% | |

A | | | 11.8% | |

BBB | | | 14.5% | |

BB or Lower | | | 26.7% | |

N/R (not rated) | | | 15.4% | |

N/A (not applicable) | | | 0.5% | |

Total | | | 100% | |

| 1 | Excluding investments in derivatives. |

JMM

| | |

Nuveen Multi-Market Income Fund | | |

Portfolio of Investments | | December 31, 2015 (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | Coupon | | | | | | Ratings (2) | | | Value | |

| | |

| | | | LONG-TERM INVESTMENTS – 139.6% (99.7% of Total Investments) | | | | | |

| | |

| | | | CONVERTIBLE PREFERRED SECURITIES – 0.3% (0.2% of Total Investments) | | | | | |

| | | | | |

| | | | Banks – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Bank of America Corporation | | | 7.250% | | | | | | | | BB+ | | | $ | 218,654 | |

| | | | Total Convertible Preferred Securities (cost $159,350) | | | | | | | | | | | | | | | 218,654 | |

| | | | | |

| Shares | | | Description (1) | | Coupon | | | | | | Ratings (2) | | | Value | |

| | |

| | | | $25 PAR (OR SIMILAR) RETAIL PREFERRED – 0.5% (0.3% of Total Investments) | | | | | |

| | | | | |

| | | | Banks – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 16,830 | | | Bank of America Corporation | | | 4.000% | | | | | | | | BB+ | | | $ | 361,508 | |

| | | | Total $25 Par (or similar) Retail Preferred (cost $279,946) | | | | | | | | | | | | | | | 361,508 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | |

| | | | CORPORATE BONDS – 31.0% (22.1% of Total Investments) | | | | | | | | | |

| | | | |

| | | | Aerospace & Defense – 0.4% | | | | | | | | | | |

| | | | | |

| $ | 200 | | | Bombardier Inc., 144A | | | 4.750% | | | | 4/15/19 | | | | B | | | $ | 164,500 | |

| | 200 | | | Triumph Group Inc. | | | 4.875% | | | | 4/01/21 | | | | Ba3 | | | | 161,125 | |

| | 400 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 325,625 | |

| | | | |

| | | | Auto Components – 0.3% | | | | | | | | | | |

| | | | | |

| | 200 | | | MPG Holdco I Inc. | | | 7.375% | | | | 10/15/22 | | | | B+ | | | | 202,000 | |

| | | | |

| | | | Automobiles – 0.2% | | | | | | | | | | |

| | | | | |

| | 100 | | | Ford Motor Company | | | 7.450% | | | | 7/16/31 | | | | BBB– | | | | 123,344 | |

| | | | | |

| | | | Banks – 1.4% | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Bank of America Corporation | | | 5.000% | | | | 5/13/21 | | | | A | | | | 546,338 | |

| | 500 | | | Citigroup Inc. | | | 4.500% | | | | 1/14/22 | | | | A | | | | 535,607 | |

| | 1,000 | | | Total Banks | | | | | | | | | | | | | | | 1,081,945 | |

| | | | | |

| | | | Building Products – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | NCI Building Systems, Inc., 144A | | | 8.250% | | | | 1/15/23 | | | | B+ | | | | 262,500 | |

| | | | | |

| | | | Capital Markets – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Goldman Sachs Group, Inc. | | | 5.750% | | | | 1/24/22 | | | | A | | | | 568,659 | |

| | | | | |

| | | | Chemicals – 1.2% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Hexion Inc. | | | 6.625% | | | | 4/15/20 | | | | B3 | | | | 78,250 | |

| | 200 | | | Huntsman International LLC | | | 4.875% | | | | 11/15/20 | | | | B1 | | | | 182,500 | |

| | 200 | | | Momentive Performance Materials Inc., (3), (4) | | | 8.875% | | | | 10/15/20 | | | | N/R | | | | — | |

| | 200 | | | Momentive Performance Materials Inc. | | | 3.880% | | | | 10/24/21 | | | | B | | | | 138,000 | |

| | 375 | | | NOVA Chemicals Corporation, 144A | | | 5.000% | | | | 5/01/25 | | | | BBB– | | | | 364,687 | |

| | 200 | | | Platform Specialty Products Corporation, 144A | | | 6.500% | | | | 2/01/22 | | | | B+ | | | | 173,000 | |

| | 1,275 | | | Total Chemicals | | | | | | | | | | | | | | | 936,437 | |

| | | | | |

| | | | Construction Materials – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 385 | | | Norbord Inc., 144A | | | 5.375% | | | | 12/01/20 | | | | Ba2 | | | | 385,000 | |

| | | | | |

| | | | Consumer Finance – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Covenant Surgical Partners Inc., 144A | | | 8.750% | | | | 8/01/19 | | | | B– | | | | 243,750 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Containers & Packaging – 0.3% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Cascades Inc., 144A | | | 5.500% | | | | 7/15/22 | | | | Ba3 | | | $ | 242,500 | |

| | | | | |

| | | | Diversified Financial Services – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | Fly Leasing Limited | | | 6.375% | | | | 10/15/21 | | | | BB | | | | 49,750 | |

| | 200 | | | James Hardie International Finance Limited, 144A | | | 5.875% | | | | 2/15/23 | | | | BBB– | | | | 204,000 | |

| | 185 | | | Nationstar Mortgage LLC Capital Corporation | | | 7.875% | | | | 10/01/20 | | | | B+ | | | | 177,045 | |

| | 435 | | | Total Diversified Financial Services | | | | | | | | | | | | | | | 430,795 | |

| | | | | |

| | | | Diversified Telecommunication Services – 2.1% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | CenturyLink Inc. | | | 6.750% | | | | 12/01/23 | | | | BB+ | | | | 234,375 | |

| | 200 | | | CenturyLink Inc. | | | 7.650% | | | | 3/15/42 | | | | BB+ | | | | 153,000 | |

| | 250 | | | Frontier Communications Corporation | | | 8.500% | | | | 4/15/20 | | | | BB | | | | 250,625 | |

| | 400 | | | IntelSat Jackson Holdings | | | 7.500% | | | | 4/01/21 | | | | B+ | | | | 348,000 | |

| | 200 | | | Neptune Finco Corporation, 144A | | | 10.875% | | | | 10/15/25 | | | | B2 | | | | 209,500 | |

| | 390 | | | SBA Tower Trust, 144A | | | 3.598% | | | | 4/15/43 | | | | BBB | | | | 388,643 | |

| | 1,690 | | | Total Diversified Telecommunication Services | | | | | | | | | | | | | | | 1,584,143 | |

| | | | | |

| | | | Electric Utilities – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 400 | | | Intergen NV, 144A | | | 7.000% | | | | 6/30/23 | | | | B+ | | | | 317,000 | |

| | 250 | | | PPL Energy Supply LLC, 144A | | | 6.500% | | | | 6/01/25 | | | | Ba3 | | | | 165,000 | |

| | 650 | | | Total Electric Utilities | | | | | | | | | | | | | | | 482,000 | |

| | | | | |

| | | | Energy Equipment & Services – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Compressco Partners LP / Compressco Finance Corporation | | | 7.250% | | | | 8/15/22 | | | | B | | | | 185,000 | |

| | 300 | | | Ensco PLC | | | 4.700% | | | | 3/15/21 | | | | BBB | | | | 241,660 | |

| | 550 | | | Total Energy Equipment & Services | | | | | | | | | | | | | | | 426,660 | |

| | | | | |

| | | | Food Products – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | JBS Investments GmbH, 144A | | | 7.250% | | | | 4/03/24 | | | | BB+ | | | | 181,500 | |

| | 200 | | | Pilgrim’s Pride Corporation, 144A | | | 5.750% | | | | 3/15/25 | | | | BB+ | | | | 194,500 | |

| | 400 | | | Total Food Products | | | | | | | | | | | | | | | 376,000 | |

| | | | | |

| | | | Gas Utilities – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | AmeriGas Finance LLC | | | 7.000% | | | | 5/20/22 | | | | Ba2 | | | | 193,500 | |

| | 300 | | | Ferrellgas LP | | | 6.750% | | | | 1/15/22 | | | | B+ | | | | 252,750 | |

| | 150 | | | Suburban Propane Partners LP | | | 5.750% | | | | 3/01/25 | | | | BB– | | | | 121,500 | |

| | 650 | | | Total Gas Utilities | | | | | | | | | | | | | | | 567,750 | |

| | | | | |

| | | | Health Care Equipment & Supplies – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 350 | | | Tenet Healthcare Corporation | | | 6.875% | | | | 11/15/31 | | | | B3 | | | | 283,500 | |

| | | | | |

| | | | Health Care Providers & Services – 2.1% | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Acadia Healthcare | | | 5.625% | | | | 2/15/23 | | | | B– | | | | 283,500 | |

| | 500 | | | Community Health Systems, Inc. | | | 6.875% | | | | 2/01/22 | | | | B+ | | | | 474,375 | |

| | 300 | | | Iasis Healthcare Capital Corporation | | | 8.375% | | | | 5/15/19 | | | | CCC+ | | | | 276,000 | |

| | 275 | | | Kindred Healthcare Inc. | | | 6.375% | | | | 4/15/22 | | | | B2 | | | | 228,250 | |

| | 400 | | | Select Medical Corporation | | | 6.375% | | | | 6/01/21 | | | | B– | | | | 350,000 | |

| | 1,775 | | | Total Health Care Providers & Services | | | | | | | | | | | | | | | 1,612,125 | |

| | | | | |

| | | | Hotels, Restaurants & Leisure – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Wynn Macau Limited, 144A | | | 5.250% | | | | 10/15/21 | | | | Ba2 | | | | 176,000 | |

| | | | | |

| | | | Household Durables – 1.2% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Brookfield Residential Properties Inc., 144A | | | 6.500% | | | | 12/15/20 | | | | BB– | | | | 240,937 | |

| | 200 | | | K. Hovnanian Enterprises Inc., 144A | | | 7.250% | | | | 10/15/20 | | | | B1 | | | | 172,000 | |

| | 250 | | | KB Home | | | 7.000% | | | | 12/15/21 | | | | B+ | | | | 246,562 | |

| | 200 | | | William Lyon Homes Incorporated | | | 8.500% | | | | 11/15/20 | | | | B– | | | | 211,500 | |

| | 900 | | | Total Household Durables | | | | | | | | | | | | | | | 870,999 | |

| | | | |

| JMM | | Nuveen Multi-Market Income Fund | | |

| | Portfolio of Investments (continued) | | December 31, 2015 (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | |

| | | | Independent Power & Renewable Electricity Producers – 0.6% | | | | | | | |

| | | | | |

| $ | 300 | | | GenOn Energy Inc. | | | 9.500% | | | | 10/15/18 | | | | B– | | | $ | 242,349 | |

| | 200 | | | NRG Energy Inc. | | | 6.625% | | | | 3/15/23 | | | | BB– | | | | 173,500 | |

| | 500 | | | Total Independent Power & Renewable Electricity Producers | | | | | | | | | | | | | | | 415,849 | |

| | | | | |

| | | | Insurance – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 190 | | | Genworth Holdings Inc. | | | 4.800% | | | | 2/15/24 | | | | Ba1 | | | | 128,250 | |

| | | | | |

| | | | Internet Software & Services – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 300 | | | EarthLink Inc. | | | 7.375% | | | | 6/01/20 | | | | Ba3 | | | | 305,250 | |

| | | | | |

| | | | IT Services – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 350 | | | Zayo Group LLC / Zayo Capital Inc. | | | 6.000% | | | | 4/01/23 | | | | B– | | | | 330,750 | |

| | | | | |

| | | | Media – 2.7% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Altice S.A, 144A | | | 7.750% | | | | 5/15/22 | | | | B | | | | 180,500 | |

| | 300 | | | CCO Safari II LLC, 144A | | | 4.908% | | | | 7/23/25 | | | | BBB– | | | | 299,705 | |

| | 250 | | | CSC Holdings Inc. | | | 8.625% | | | | 2/15/19 | | | | BB | | | | 266,250 | |

| | 300 | | | DIRECTV Holdings LLC | | | 3.800% | | | | 3/15/22 | | | | A– | | | | 302,079 | |

| | 200 | | | Dish DBS Corporation | | | 5.125% | | | | 5/01/20 | | | | BB– | | | | 198,000 | |

| | 200 | | | Quebecor Media Inc. | | | 5.750% | | | | 1/15/23 | | | | B+ | | | | 201,500 | |

| | 250 | | | Tribune Media Company, 144A | | | 5.875% | | | | 7/15/22 | | | | BB– | | | | 250,000 | |

| | 350 | | | WMG Acquisition Group, 144A | | | 6.000% | | | | 1/15/21 | | | | B1 | | | | 351,750 | |

| | 2,050 | | | Total Media | | | | | | | | | | | | | | | 2,049,784 | |

| | | | | |

| | | | Metals & Mining – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 325 | | | Alcoa Inc. | | | 5.400% | | | | 4/15/21 | | | | BBB– | | | | 316,062 | |

| | 175 | | | Allegheny Technologies Inc. | | | 5.950% | | | | 1/15/21 | | | | BB– | | | | 103,250 | |

| | 200 | | | AngloGold Holdings PLC | | | 5.125% | | | | 8/01/22 | | | | Baa3 | | | | 159,000 | |

| | 300 | | | Eldorado Gold Corporation, 144A | | | 6.125% | | | | 12/15/20 | | | | BB | | | | 262,500 | |

| | 500 | | | Freeport McMoRan, Inc. | | | 3.550% | | | | 3/01/22 | | | | BBB | | | | 290,000 | |

| | 200 | | | Lundin Mining Corporation, 144A | | | 7.500% | | | | 11/01/20 | | | | Ba2 | | | | 187,500 | |

| | 300 | | | Vale Overseas Limited | | | 4.375% | | | | 1/11/22 | | | | BBB | | | | 227,049 | |

| | 2,000 | | | Total Metals & Mining | | | | | | | | | | | | | | | 1,545,361 | |

| | | | | |

| | | | Oil, Gas & Consumable Fuels – 3.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Calumet Specialty Products | | | 7.625% | | | | 1/15/22 | | | | B+ | | | | 170,000 | |

| | 150 | | | Continental Resources Inc. | | | 7.375% | | | | 10/01/20 | | | | BBB– | | | | 138,000 | |

| | 200 | | | Crestwood Midstream Partners LP | | | 6.125% | | | | 3/01/22 | | | | BB | | | | 139,000 | |

| | 100 | | | EV Energy Partners LP / EV Energy Finance Corporation | | | 8.000% | | | | 4/15/19 | | | | B– | | | | 50,000 | |

| | 200 | | | Genesis Energy LP | | | 5.750% | | | | 2/15/21 | | | | B+ | | | | 169,000 | |

| | 245 | | | Gibson Energy, 144A | | | 6.750% | | | | 7/15/21 | | | | BB | | | | 234,588 | |

| | 250 | | | NGL Energy Partners LP/Fin Co | | | 5.125% | | | | 7/15/19 | | | | BB– | | | | 197,500 | |

| | 350 | | | Northern Tier Energy LLC | | | 7.125% | | | | 11/15/20 | | | | BB– | | | | 353,500 | |

| | 175 | | | Rose Rock Midstream LP / Rose Rock Finance Corporation | | | 5.625% | | | | 7/15/22 | | | | B1 | | | | 124,250 | |

| | 250 | | | Targa Resources Inc. | | | 5.000% | | | | 1/15/18 | | | | BB+ | | | | 231,250 | |

| | 500 | | | Transocean Inc. | | | 4.300% | | | | 10/15/22 | | | | BB+ | | | | 265,000 | |

| | 300 | | | Western Refining Inc. | | | 6.250% | | | | 4/01/21 | | | | B+ | | | | 288,000 | |

| | 175 | | | WPX Energy Inc. | | | 7.500% | | | | 8/01/20 | | | | Ba1 | | | | 141,750 | |

| | 3,095 | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 2,501,838 | |

| | | | | |

| | | | Paper & Forest Products – 1.1% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Domtar Corporation | | | 4.400% | | | | 4/01/22 | | | | BBB– | | | | 254,271 | |

| | 200 | | | Mercer International Inc. | | | 7.750% | | | | 12/01/22 | | | | B+ | | | | 202,000 | |

| | 200 | | | Millar Western Forest Products Ltd | | | 8.500% | | | | 4/01/21 | | | | B– | | | | 104,000 | |

| | 375 | | | Resolute Forest Products | | | 5.875% | | | | 5/15/23 | | | | BB– | | | | 272,812 | |

| | 1,025 | | | Total Paper & Forest Products | | | | | | | | | | | | | | | 833,083 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Personal Products – 0.3% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Albea Beauty Holdings SA, 144A | | | 8.375% | | | | 11/01/19 | | | | B | | | $ | 260,000 | |

| | | | | |

| | | | Real Estate Investment Trust – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 300 | | | CommomWealth REIT | | | 5.875% | | | | 9/15/20 | | | | BBB– | | | | 322,485 | |

| | 250 | | | iStar Inc. | | | 7.125% | | | | 2/15/18 | | | | B+ | | | | 258,750 | |

| | 550 | | | Total Real Estate Investment Trust | | | | | | | | | | | | | | | 581,235 | |

| | | | | |

| | | | Real Estate Management & Development – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 350 | | | Mattamy Group Corporation, 144A | | | 6.500% | | | | 11/15/20 | | | | BB | | | | 332,500 | |

| | | | | |

| | | | Road & Rail – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Watco Companies LLC Finance, 144A | | | 6.375% | | | | 4/01/23 | | | | B | | | | 295,500 | |

| | | | | |

| | | | Software – 1.4% | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Computer Sciences Corporation | | | 4.450% | | | | 9/15/22 | | | | BBB+ | | | | 1,025,884 | |

| | | | | |

| | | | Specialty Retail – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 150 | | | L Brands, Inc., 144A | | | 6.875% | | | | 11/01/35 | | | | BB+ | | | | 154,125 | |

| | 150 | | | Neiman Marcus Mariposa Borrower / Merger Sub LLC, 144A | | | 8.000% | | | | 10/15/21 | | | | CCC+ | | | | 111,000 | |

| | 300 | | | Total Specialty Retail | | | | | | | | | | | | | | | 265,125 | |

| | | | | |

| | | | Technology Hardware, Storage & Peripherals – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 175 | | | NCR Corporation | | | 4.625% | | | | 2/15/21 | | | | BB | | | | 166,688 | |

| | | | | |

| | | | Textiles, Apparel & Luxury Goods – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 225 | | | Levi Strauss & Company | | | 5.000% | | | | 5/01/25 | | | | BB | | | | 223,875 | |

| | | | | |

| | | | Wireless Telecommunication Services – 1.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Digicel Limited, 144A | | | 6.000% | | | | 4/15/21 | | | | B1 | | | | 168,500 | |

| | 275 | | | FairPoint Communications Inc., 144A | | | 8.750% | | | | 8/15/19 | | | | B | | | | 270,875 | |

| | 200 | | | Sprint Corporation | | | 7.250% | | | | 9/15/21 | | | | B+ | | | | 149,000 | |

| | 200 | | | T-Mobile USA Inc. | | | 6.731% | | | | 4/28/22 | | | | BB | | | | 208,500 | |

| | 200 | | | Wind Acquisition Finance SA, 144A | | | 4.750% | | | | 7/15/20 | | | | BB | | | | 198,000 | |

| | 1,075 | | | Total Wireless Telecommunication Services | | | | | | | | | | | | | | | 994,875 | |

| $ | 25,945 | | | Total Corporate Bonds (cost $25,852,059) | | | | | | | | | | | | | | | 23,437,579 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | $1,000 PAR (OR SIMILAR) INSTITUTIONAL PREFERRED – 0.4% (0.3% of Total Investments) | | | | | |

| | | | | |

| | | | Banks – 0.1% | | | | | | | | | | | | |

| | | | | |

| $ | 100 | | | Lloyd’s Banking Group PLC | | | 7.500% | | | | N/A (5) | | | | BB+ | | | $ | 106,500 | |

| | | | | |

| | | | Insurance – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 225 | | | Sirius International Group Limited, 144A | | | 7.506% | | | | N/A (5) | | | | BBB– | | | | 227,250 | |

| | | | Total $1,000 Par (or similar) Institutional Preferred (cost $341,491) | | | | | | | | 333,750 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES – 106.6% (76.1% of Total Investments) | | | | |

| | | | | |

| $ | 500 | | | 321 Henderson Receivables LLC, Series 2012-1A, 144A | | | 7.140% | | | | 2/15/67 | | | | A3 | | | $ | 574,704 | |

| | 415 | | | 321 Henderson Receivables LLC., Series 2010-1A, 144A | | | 9.310% | | | | 7/15/61 | | | | Aa2 | | | | 506,165 | |

| | 500 | | | 321 Henderson Receivables Trust Series 2012-2A, 144A | | | 6.770% | | | | 10/17/61 | | | | Baa1 | | | | 564,103 | |

| | 382 | | | ACE Securities Corporation, Manufactured Housing Trust

Series 2003-MH1, 144A | | | 6.208% | | | | 8/15/30 | | | | AA | | | | 417,012 | |

| | 750 | | | American Homes 4 Rent, Series 2015-SFR2, 144A | | | 5.036% | | | | 10/17/45 | | | | Baa2 | | | | 737,702 | |

| | | | |

| JMM | | Nuveen Multi-Market Income Fund | | |

| | Portfolio of Investments (continued) | | December 31, 2015 (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | | | | |

| $ | 1,747 | | | American Homes 4 Rent, Series 2015-SFR2 ,144A | | | 0.000% | | | | 10/17/45 | | | | N/R | | | $ | 2 | |

| | 405 | | | AmeriCold LLC Trust, Series 2010, 144A | | | 6.811% | | | | 1/14/29 | | | | A+ | | | | 456,672 | |

| | 220 | | | Bank of America Commercial Mortgage Inc., Commercial Mortgage Pass-Through Certificates, Series 2015-UBS7 | | | 3.167% | | | | 9/15/48 | | | | BBB– | | | | 160,081 | |

| | 174 | | | Bank of America Funding Trust, Mortgage Pass-Through Certificates, Series 2007-4 | | | 5.500% | | | | 6/25/37 | | | | C | | | | 39,934 | |

| | 428 | | | Barclays BCAP LLC Trust, Resecuritized Series 2009-RR14, 144A | | | 6.000% | | | | 5/26/37 | | | | BBB | | | | 448,769 | |

| | 500 | | | Barclays Commercial Mortgage, Mortgage Pass-Through Certificates, Series 2015-STP, 144A | | | 4.284% | | | | 9/10/28 | | | | BBB– | | | | 487,656 | |

| | 163 | | | Bayview Financial Acquisition Trust 2003-AA, 144A | | | 6.072% | | | | 2/25/33 | | | | AA | | | | 163,071 | |

| | 191 | | | Bayview Financial Acquisition Trust, Series 2006C | | | 5.852% | | | | 11/28/36 | | | | CCC | | | | 186,394 | |

| | 188 | | | Bayview Financial Acquisition Trust, Series 2006-C | | | 5.638% | | | | 11/28/36 | | | | Ba1 | | | | 187,542 | |

| | | | | |

| | 250 | | | Bayview Financial Acquisition Trust, Series 2006-D | | | 5.932% | | | | 12/28/36 | | | | A2 | | | | 243,692 | |

| | 66 | | | Bayview Financial Acquisition Trust, Series 2006-D | | | 5.660% | | | | 12/28/36 | | | | Aaa | | | | 65,687 | |

| | 149 | | | Bayview Financial Acquisition Trust, Series 2007-A | | | 6.205% | | | | 5/28/37 | | | | AA+ | | | | 156,135 | |

| | 750 | | | Bayview Financial Mortgage Pass-Through Trust, Mortgage Pass-Through Certificate Series 2005-D | | | 5.500% | | | | 12/28/35 | | | | BB+ | | | | 739,832 | |

| | 187 | | | Bayview Financial Mortgage Pass-Through Trust, Mortgage Pass-Through Certificate Series 2006-A | | | 5.704% | | | | 2/28/41 | | | | AAA | | | | 203,408 | |

| | 500 | | | CAM Mortgage Trust 2015-1, 144A | | | 4.750% | | | | 7/15/64 | | | | N/R | | | | 497,520 | |

| | 500 | | | CarFinance Capital Auto Trust, Automobile Receivables-Backed Notes, Series 2013-1, 144A | | | 3.450% | | | | 3/15/19 | | | | Aa3 | | | | 503,901 | |

| | 246 | | | Chase Funding Mortgage Loan Asset-Backed Certificates, Series 2003-3 | | | 4.660% | | | | 3/25/33 | | | | BBB– | | | | 251,302 | |

| | 500 | | | Citigroup Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2006-CD3 | | | 5.688% | | | | 10/15/48 | | | | B– | | | | 406,436 | |

| | 275 | | | Commercial Mortgage Pass-Through Certificates 2015-CR22 | | | 4.128% | | | | 3/10/48 | | | | A– | | | | 261,270 | |

| | 210 | | | Commercial Mortgage Pass-Through Certificates, Series 2015-CR26 | | | 4.496% | | | | 9/10/25 | | | | A– | | | | 198,404 | |

| | 291 | | | Countrywide Alternative Loan Trust 2005-86CB A10 | | | 5.500% | | | | 2/25/36 | | | | Caa3 | | | | 263,310 | |

| | 209 | | | Countrywide Alternative Loan Trust, Mortgage Pass-Through Certificates, Series 2004-J2 | | | 6.500% | | | | 3/25/34 | | | | A+ | | | | 219,326 | |

| | 261 | | | Countrywide Alternative Loan Trust, Mortgage Pass-Through Certificates, Series 2005-47CB | | | 5.500% | | | | 10/25/35 | | | | Caa3 | | | | 238,378 | |

| | 876 | | | Countrywide Alternative Loan Trust, Mortgage Pass-Through Certificates, Series 2007-6 A4 | | | 5.750% | | | | 4/25/47 | | | | Ca | | | | 772,978 | |

| | 315 | | | Countrywide Asset Backed Certificates, Series 2007-4 A2 | | | 5.397% | | | | 4/25/47 | | | | Caa1 | | | | 343,520 | |

| | 742 | | | Credit Suisse Commercial Mortgage Trust 2009-3R, 144A | | | 6.000% | | | | 1/27/37 | | | | BBB | | | | 768,113 | |

| | 400 | | | Credit Suisse CSMC Mortgage-Backed Trust, Pass-Through Certificates, Series 2006-7 | | | 6.000% | | | | 8/25/36 | | | | Caa3 | | | | 342,425 | |

| | 653 | | | Credit Suisse First Boston Mortgage Securities Corporation, Mortgage-Backed Pass-Through Certificates, Series 2003-8 | | | 6.189% | | | | 4/25/33 | | | | A | | | | 649,460 | |

| | 663 | | | Credit Suisse First Boston Mortgage Securities Corporation, Mortgage-Backed Pass-Through Certificates, Series 2005-11 6A7 | | | 6.000% | | | | 12/25/35 | | | | CC | | | | 183,259 | |

| | 405 | | | Credit Suisse First Boston Mortgage Securities, Home Equity Mortgage Pass-Through Certificates, Series 2004-6 | | | 5.821% | | | | 4/25/35 | | | | B1 | | | | 412,129 | |

| | 1,068 | | | Credit-Based Asset Servicing and Securitization Pool 2007-SP1, 144A | | | 6.020% | | | | 12/25/37 | | | | A+ | | | | 1,113,927 | |

| | 16 | | | Fannie Mae Mortgage Pool, (6) | | | 7.000% | | | | 7/01/17 | | | | Aaa | | | | 16,203 | |

| | 34 | | | Fannie Mae Mortgage Pool, (6) | | | 5.000% | | | | 11/01/18 | | | | Aaa | | | | 35,348 | |

| | 68 | | | Fannie Mae Mortgage Pool, (6) | | | 5.000% | | | | 2/01/21 | | | | Aaa | | | | 72,582 | |

| | 1,490 | | | Fannie Mae Mortgage Pool, (6) | | | 3.500% | | | | 12/01/26 | | | | Aaa | | | | 1,562,806 | |

| | 1,414 | | | Fannie Mae Mortgage Pool, (6) | | | 3.500% | | | | 1/01/27 | | | | Aaa | | | | 1,483,944 | |

| | — | (7) | | Fannie Mae Mortgage Pool | | | 3.224% | | | | 7/01/27 | | | | Aaa | | | | 221 | |

| | 60 | | | Fannie Mae Mortgage Pool, (6) | | | 6.000% | | | | 5/01/29 | | | | Aaa | | | | 67,782 | |

| | 28 | | | Fannie Mae Mortgage Pool, (6) | | | 7.000% | | | | 9/01/31 | | | | Aaa | | | | 31,000 | |

| | 36 | | | Fannie Mae Mortgage Pool, (6) | | | 5.500% | | | | 6/01/33 | | | | Aaa | | | | 40,817 | |

| | 97 | | | Fannie Mae Mortgage Pool, (6) | | | 6.000% | | | | 1/01/34 | | | | Aaa | | | | 109,878 | |

| | 193 | | | Fannie Mae Mortgage Pool, (6) | | | 5.500% | | | | 2/01/34 | | | | Aaa | | | | 219,021 | |

| | 134 | | | Fannie Mae Mortgage Pool, (6) | | | 6.000% | | | | 3/01/34 | | | | Aaa | | | | 147,999 | |

| | 123 | | | Fannie Mae Mortgage Pool, (6) | | | 6.000% | | | | 1/01/35 | | | | Aaa | | | | 140,367 | |

| | 89 | | | Fannie Mae Mortgage Pool, (6) | | | 5.000% | | | | 7/01/35 | | | | Aaa | | | | 98,503 | |

| | 46 | | | Fannie Mae Mortgage Pool, (6) | | | 5.500% | | | | 3/01/36 | | | | Aaa | | | | 51,732 | |

| | 172 | | | Fannie Mae Mortgage Pool, (6) | | | 6.000% | | | | 6/01/36 | | | | Aaa | | | | 194,802 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | | | | |

| $ | 146 | | | Fannie Mae Mortgage Pool, (6) | | | 5.500% | | | | 4/01/37 | | | | Aaa | | | $ | 162,892 | |

| | 207 | | | Fannie Mae Mortgage Pool, (6) | | | 5.000% | | | | 6/01/37 | | | | Aaa | | | | 227,462 | |

| | 143 | | | Fannie Mae Mortgage Pool, (6) | | | 5.500% | | | | 6/01/38 | | | | Aaa | | | | 159,486 | |

| | 2,373 | | | Fannie Mae Mortgage Pool, (6) | | | 3.500% | | | | 2/01/44 | | | | Aaa | | | | 2,449,806 | |

| | 139 | | | Fannie Mae REMIC Pass-Through Certificates | | | 6.335% | | | | 2/25/42 | | | | Aaa | | | | 160,344 | |

| | 663 | | | Fannie Mae REMIC Pass-Through Certificates | | | 4.224% | | | | 12/25/42 | | | | AAA | | | | 406,433 | |

| | 771 | | | Fannie Mae REMIC Pass-Through Certificates | | | 5.463% | | | | 7/25/44 | | | | Aaa | | | | 96,232 | |

| | 2,975 | | | Fannie Mae TBA Mortgage Pool, (MDR), (WI/DD) | | | 4.500% | | | | TBA | | | | N/R | | | | 3,212,082 | |

| | 4,605 | | | Fannie Mae TBA Mortgage Pool, (MDR), (WI/DD) | | | 4.000% | | | | TBA | | | | N/R | | | | 4,871,678 | |

| | 2,000 | | | Fannie Mae TBA Mortgage Pool, (MDR), (WI/DD) | | | 3.500% | | | | TBA | | | | N/R | | | | 2,062,792 | |

| | 2,500 | | | Fannie Mae TBA Mortgage Pool, (MDR), (WI/DD) | | | 3.000% | | | | TBA | | | | N/R | | | | 2,499,130 | |

| | 4,143 | | | Federal Home Loan Mortgage Corporation, Mortgage Pool, (6) | | | 3.000% | | | | 4/01/43 | | | | Aaa | | | | 4,144,137 | |

| | | | | |

| | 45 | | | First Horizon Alternative Mortgage Securities Trust, Pass-Through Certificates, Series 2005-FA5 | | | 5.500% | | | | 8/25/35 | | | | C | | | | 1,666 | |

| | 3,039 | | | Freddie Mac Gold Mortgage Pool, (6) | | | 3.000% | | | | 1/01/29 | | | | Aaa | | | | 3,134,319 | |

| | 40 | | | Freddie Mac Mortgage Pool, Various, (6) | | | 6.500% | | | | 11/01/28 | | | | Aaa | | | | 46,541 | |

| | 2,078 | | | Freddie Mac Mortgage Pool, (6) | | | 3.500% | | | | 1/01/44 | | | | Aaa | | | | 2,139,774 | |

| | 2,016 | | | Freddie Mac Mortgage Pool, (6) | | | 3.500% | | | | 2/01/44 | | | | Aaa | | | | 2,076,729 | |

| | 267 | | | Freddie Mac Mortgage Trust 2013-KF02, 144A | | | 3.422% | | | | 12/25/45 | | | | AAA | | | | 274,244 | |

| | 255 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage Pass-Through Certificates, Series 2012-K706, 144A | | | 4.167% | | | | 11/25/44 | | | | AA+ | | | | 261,449 | |

| | 500 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage Pass-Through Certificates, Series 2012-K706, 144A | | | 4.167% | | | | 11/25/44 | | | | AA+ | | | | 512,755 | |

| | 282 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage Pass-Through Certificates, Series 2012-K708, 144A | | | 3.754% | | | | 2/25/45 | | | | Aaa | | | | 286,710 | |

| | 500 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage Pass-Through Certificates, Series 2012-K708, 144A | | | 3.754% | | | | 2/25/45 | | | | Aaa | | | | 505,344 | |

| | 750 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage Pass-Through Certificates, Series 2013-K712, 144A | | | 3.371% | | | | 5/25/45 | | | | Aaa | | | | 742,076 | |

| | 750 | | | Freddie Mac Mortgage Trust, Multifamily Mortgage-Pass Through Certificates, Series 2012-K709, 144A | | | 3.741% | | | | 4/25/45 | | | | Aaa | | | | 763,633 | |

| | 250 | | | Freddie Mac Multifamily Mortgage Trust, Series 2011-K704, 144A | | | 4.535% | | | | 10/25/30 | | | | AA+ | | | | 260,144 | |

| | — | (7) | | Freddie Mac Non Gold Participation Certificates | | | 2.089% | | | | 9/01/18 | | | | Aaa | | | | 1 | |

| | 500 | | | GMAT Trust Mortgage Pool 2013-1A, 144A | | | 5.000% | | | | 11/25/43 | | | | N/R | | | | 473,036 | |

| | 1,000 | | | Goldman Sachs Mortgage Securities Corporation II, Commercial Mortgage Pass -Through Certificates, Series 2014-GSFL, 144A | | | 2.581% | | | | 7/15/31 | | | | A– | | | | 978,233 | |

| | 130 | | | Goldman Sachs Mortgage Securities Corporation, GSMPS Mortgage Pass-Through Certificates, Series 2001-2, 144A | | | 7.500% | | | | 6/19/32 | | | | B | | | | 133,806 | |

| | 898 | | | Goldman Sachs Mortgage Securities Corporation, GSMPS Mortgage Pass-Through Certificates, Series 2003-3, 144A | | | 7.000% | | | | 6/25/43 | | | | BBB | | | | 959,369 | |

| | 1,317 | | | Goldman Sachs Mortgage Securities Corporation, GSMPS Mortgage Pass-Through Certificates, Series 2006-RP2 B1 | | | 6.013% | | | | 4/25/36 | | | | CC | | | | 188,957 | |

| | 683 | | | Goldman Sachs Mortgage Securities Corporation, GSMPS Mortgage Pass-Through Certificates, Series 2006-RP2 B2 | | | 6.013% | | | | 4/25/36 | | | | C | | | | 28,170 | |

| | 1,187 | | | Goldman Sachs Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2003-1 B2, (3) | | | 6.643% | | | | 3/25/43 | | | | Ca | | | | 12 | |

| | 100 | | | Goldman Sachs Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2003-10 1A1 | | | 2.698% | | | | 10/25/33 | | | | BBB+ | | | | 100,138 | |

| | 471 | | | Goldman Sachs Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2005-RP2 1A2, 144A | | | 7.500% | | | | 3/25/35 | | | | B1 | | | | 518,106 | |

| | 469 | | | Goldman Sachs Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2005-RP3 1A2, 144A | | | 7.500% | | | | 9/25/35 | | | | B1 | | | | 517,607 | |

| | 500 | | | Goldman Sachs Mortgage Securities Trust, Mortgage Pass-Through Certificates, Series 2015-GC32 | | | 3.345% | | | | 7/10/48 | | | | BBB– | | | | 364,181 | |

| | 79 | | | Government National Mortgage Association Pool, (6) | | | 1.625% | | | | 12/20/22 | | | | Aaa | | | | 81,768 | |

| | 339 | | | Government National Mortgage Association Pool, (6) | | | 5.500% | | | | 8/15/33 | | | | Aaa | | | | 389,980 | |

| | 222 | | | Government National Mortgage Association Pool, (6) | | | 6.000% | | | | 7/15/34 | | | | Aaa | | | | 258,726 | |

| | 750 | | | Green Tree Agency Advance Funding Trust, Manufactured Housing Contract Pass-Through Certificates, Series 2015-T2, 144A | | | 4.669% | | | | 10/15/48 | | | | BBB | | | | 742,230 | |

| | 361 | | | Impac Secured Assets Corporation, Mortgage Pass-Through Certificates, Series 2000-3 | | | 8.000% | | | | 10/25/30 | | | | CCC | | | | 367,028 | |

| | 783 | | | IndyMac INDX Mortgage Loan Trust, Series 2006-AR13 A3 | | | 4.441% | | | | 7/25/36 | | | | Caa1 | | | | 665,130 | |

| | | | |

| JMM | | Nuveen Multi-Market Income Fund | | |

| | Portfolio of Investments (continued) | | December 31, 2015 (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | | | | |

| $ | 163 | | | IndyMac MBS Inc., Residential Asset Securitization Trust, Mortgage Pass-Through Certificates, Series 2004-A2 | | | 4.000% | | | | 5/25/34 | | | | A+ | | | $ | 163,526 | |

| | 445 | | | JPMorgan Alternative Loan Trust 2006-S1, Mortgage Pass-Through Certificates | | | 6.500% | | | | 3/25/36 | | | | D | | | | 384,750 | |

| | 750 | | | JPMorgan Chase Commercial Mortgage Securities Corporation, Commercial Mortgage Pass-Through Certificates, Series 2011-C4 C, 144A | | | 5.277% | | | | 7/15/46 | | | | A | | | | 792,115 | |

| | 270 | | | Lavender Trust, Mortgage Pass-Through Certificates, Series 2010-R10A, 144A | | | 6.250% | | | | 9/26/36 | | | | N/R | | | | 271,865 | |

| | 152 | | | Lehman ABS Manufactured Housing Contract Asset Backed Certificates, Series 2001B | | | 4.350% | | | | 4/15/40 | | | | AA | | | | 155,384 | |

| | 46 | | | Lehman Mortgage Trust, Mortgage Pass-Through Certificates, Series 2008-6 | | | 5.266% | | | | 7/25/47 | | | | BB+ | | | | 46,875 | |

| | | | | |

| | 500 | | | Master RePerforming Loan Trust 2005-1, 144A | | | 7.500% | | | | 8/25/34 | | | | Ba3 | | | | 520,328 | |

| | 481 | | | Master Resecuritization Trust 2009-1, 144A | | | 6.000% | | | | 10/25/36 | | | | A | | | | 503,159 | |

| | 458 | | | Merrill Lynch Alternative Note Asset, 2007-F1 2A7 | | | 6.000% | | | | 3/25/37 | | | | Caa3 | | | | 339,750 | |

| | 1,499 | | | Mid-State Capital Corporation Trust Notes, Series 2004-1 A | | | 6.005% | | | | 8/15/37 | | | | AAA | | | | 1,596,657 | |

| | 1,185 | | | Mid-State Capital Corporation Trust Notes, Series 2005-1 | | | 5.745% | | | | 1/15/40 | | | | AA | | | | 1,271,948 | |

| | 102 | | | Mid-State Trust 2004-A | | | 8.900% | | | | 8/15/37 | | | | BBB | | | | 113,275 | |

| | 266 | | | Mid-State Trust 2010-1, 144A | | | 7.000% | | | | 12/15/45 | | | | A | | | | 288,219 | |

| | 1,085 | | | Mid-State Trust 2010-1, 144A | | | 5.250% | | | | 12/15/45 | | | | AA | | | | 1,132,823 | |

| | 325 | | | Mid-State Trust VI | | | 7.790% | | | | 7/01/35 | | | | Baa1 | | | | 343,622 | |

| | 353 | | | Mid-State Trust XI | | | 5.598% | | | | 7/15/38 | | | | A+ | | | | 370,023 | |

| | 150 | | | Morgan Stanley Bank of America Merrill Lynch Trust, Series 2015-C22, 144A | | | 4.243% | | | | 4/15/48 | | | | BBB– | | | | 121,764 | |

| | 250 | | | Morgan Stanley Capital I Trust, Commercial Mortgage Pass-Through Certificates, Series 2011-C1 C, 144A | | | 5.438% | | | | 9/15/47 | | | | AA | | | | 271,413 | |

| | 200 | | | Morgan Stanley Mortgage Loan Trust, Pass-Through Certificates, 2006-2 | | | 5.750% | | | | 2/25/36 | | | | Caa2 | | | | 190,150 | |

| | 500 | | | Morgan Stanley Re REMIC Trust Series 2009-GG10, 144A | | | 5.794% | | | | 8/12/45 | | | | A | | | | 516,669 | |

| | 364 | | | Mortgage Asset Securitization Transaction Inc., Alternative Loan Trust Mortgage Pass-Through Certificates Series 2004-1 | | | 7.000% | | | | 1/25/34 | | | | BBB– | | | | 375,572 | |

| | 535 | | | Mortgage Asset Securitization Transaction Inc., Alternative Loan Trust Mortgage Pass-Through Certificates, 2004-5 6A1 | | | 7.000% | | | | 6/25/34 | | | | A+ | | | | 567,042 | |

| | 126 | | | Mortgage Asset Securitization Transaction Inc., Mortgage Pass-Through Certificates, Series 2003-5 | | | 5.000% | | | | 6/25/18 | | | | AA | | | | 129,138 | |

| | 525 | | | Nationstar Agency Fund Trust, Series 2013-T2A, 144A | | | 7.385% | | | | 2/18/48 | | | | B | | | | 526,040 | |

| | 350 | | | Nationstar Agency Fund Trust, Series 2013-T2A, 144A | | | 4.212% | | | | 2/18/48 | | | | BBB | | | | 350,959 | |

| | 500 | | | New Residential Advance Receivable Trust, Series 2015-T2, 144A | | | 4.679% | | | | 8/17/48 | | | | BBB | | | | 500,313 | |

| | 285 | | | New Residential Mortgage Loan Trust, Mortgage Pass-Through Certificates, Series 2014-2A, 144A | | | 3.750% | | | | 5/25/54 | | | | AAA | | | | 289,067 | |

| | 74 | | | Oakwood Mortgage Investors Inc., Series 1999-A | | | 6.090% | | | | 4/15/29 | | | | A | | | | 75,539 | |

| | 500 | | | OMART Receivables Trust, Series 2015-T3, 144A | | | 4.687% | | | | 11/15/47 | | | | BBB | | | | 499,226 | |

| | 166 | | | Origen Manufactured Housing Contract Trust Collateralized Notes Series 2004-B MI | | | 5.730% | | | | 11/15/35 | | | | AA | | | | 172,410 | |

| | 229 | | | Origen Manufactured Housing Contract Trust Collateralized Notes Series 2005A | | | 5.410% | | | | 6/15/36 | | | | AAA | | | | 236,449 | |

| | 350 | | | Origen Manufactured Housing Contract Trust Collateralized Notes Series 2005B | | | 5.990% | | | | 1/15/37 | | | | A+ | | | | 365,909 | |

| | 887 | | | Origen Manufactured Housing Contract Trust Notes, Series 2004A | | | 6.640% | | | | 1/15/35 | | | | A | | | | 953,951 | |

| | 457 | | | Renaissance Home Equity Loan Trust Asset Backed Certificates, Series 2005-4 A6 | | | 5.749% | | | | 2/25/36 | | | | Caa1 | | | | 428,250 | |

| | 516 | | | Residential Asset Mortgage Products Inc., Mortgage Asset-Backed Pass-Through Certificates, Series 2003-SL1 M2 | | | 7.352% | | | | 4/25/31 | | | | D | | | | 5 | |

| | 850 | | | Residential Asset Securities Corporation , Home Equity Mortgage Asset Backed Pass-Through Certificates, Series 2004-KS1 | | | 5.221% | | | | 2/25/34 | | | | BB+ | | | | 879,390 | |

| | 173 | | | Residential Funding Mortgage Securities II, Inc., Home Loan Backed Notes Trust 2003-HI4 | | | 6.030% | | | | 2/25/29 | | | | A+ | | | | 180,961 | |

| | 347 | | | Residential Funding Mortgage Trust I, 2007-S9 | | | 6.000% | | | | 10/25/37 | | | | D | | | | 291,190 | |

| | 285 | | | Salomon Brothers Commercial Mortgage Trust Pass-Through VII Certificates, Series 2003-1 A2, 144A | | | 6.000% | | | | 9/25/33 | | | | BB | | | | 282,977 | |

| | 500 | | | Springleaf Mortgage Loan Trust 2013-2A, 144A | | | 3.520% | | | | 12/25/65 | | | | AA | | | | 503,123 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | | | | |

| $ | 801 | | | Springleaf Mortgage Loan Trust, Series 2013-3A, 144A | | | 5.000% | | | | 9/25/57 | | | | BBB | | | $ | 822,233 | |

| | 500 | | | SPS Servicer Advance Receivables Trust, Series 2015-T3, 144A | | | 4.430% | | | | 7/15/47 | | | | BBB | | | | 499,720 | |

| | 500 | | | V Mortgage LLC, Pass-Through Certificate , Series 2014-NPL1, 144A | | | 4.750% | | | | 4/27/54 | | | | N/R | | | | 487,684 | |

| | 110 | | | Vanderbilt Acquisition Loan Trust, Series 2002-1 | | | 6.570% | | | | 5/07/27 | | | | AAA | | | | 112,520 | |

| | 496 | | | Vericrest Opportunity Loan Transferee, Series 2014-NPL7, 144A | | | 4.750% | | | | 8/27/57 | | | | N/R | | | | 493,237 | |

| | 499 | | | Vericrest Opportunity Loan Transferee, Series 2015-NLP4, 144A | | | 4.250% | | | | 2/25/55 | | | | N/R | | | | 480,915 | |

| | 500 | | | Vericrest Opportunity Loan Transferee, Series 2015-NP13, 144A | | | 4.875% | | | | 10/25/45 | | | | N/R | | | | 485,407 | |

| | 500 | | | Vericrest Opportunity Loan Transferee, Series 2015-NP14, 144A | | | 4.875% | | | | 11/27/45 | | | | N/R | | | | 484,508 | |

| | 179 | | | Wachovia Bank Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2007-C30 | | | 5.246% | | | | 12/15/43 | | | | AAA | | | | 179,197 | |

| | 359 | | | Walter Investment Management Company Capital Trust, Series 2012-AA, 144A | | | 4.549% | | | | 10/16/50 | | | | BBB | | | | 361,327 | |

| | 69 | | | Washington Mutual Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2003-MS1 | | | 5.250% | | | | 2/25/18 | | | | AA+ | | | | 69,759 | |

| | | | | |

| | 822 | | | Washington Mutual Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2003-MS4 | | | 5.500% | | | | 2/25/33 | | | | AA+ | | | | 831,346 | |

| | 56 | | | Washington Mutual Mortgage Securities Corporation, Mortgage Pass-Through Certificates, Series 2004-RA3 | | | 6.356% | | | | 8/25/38 | | | | AA | | | | 57,586 | |

| | 500 | | | Wells Fargo Commercial Mortgage Trust, Commercial Mortgage-Pass-Through Certificates, Series 2015-C26, 144A | | | 3.586% | | | | 2/15/48 | | | | BBB– | | | | 372,078 | |

| | 750 | | | Wells Fargo-RBS Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2011-C3, 144A | | | 5.335% | | | | 3/15/44 | | | | A2 | | | | 793,323 | |

| | 750 | | | Wells Fargo-RBS Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2013-C15, 144A | | | 4.480% | | | | 8/15/46 | | | | BBB– | | | | 690,226 | |

| | 250 | | | WF-RBS Commercial Mortgage Trust, Commercial Mortgage Pass-Through Certificates, Series 2011-C2, 144A | | | 5.392% | | | | 2/15/44 | | | | A1 | | | | 265,025 | |

| $ | 86,145 | | | Total Asset-Backed and Mortgage-Backed Securities (cost $82,523,960) | | | | | | | | 80,749,477 | |

| | | | | |

| Shares | | | Description (1), (8) | | | | | | | | | | | Value | |

| | | |

| | | | INVESTMENT COMPANIES – 0.6% (0.5% of Total Investments) | | | | | | | | | |

| | | | | |

| | 32,000 | | | Blackrock Credit Allocation Income Trust IV | | | | | | | | | | | | | | $ | 394,880 | |

| | 7,036 | | | Pioneer Floating Rate Trust | | | | | | | | | | | | | | | 76,341 | |

| | | | Total Investment Companies (cost $487,356) | | | | | | | | | | | | | | | 471,221 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | SOVEREIGN DEBT – 0.2% (0.2% of Total Investments) | | | | | |

| | | | | |

| | | | Uruguay – 0.2% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 123 | | | Republic of Uruguay | | | 8.000% | | | | 11/18/22 | | | | BBB | | | $ | 152,538 | |

| $ | 123 | | | Total Sovereign Debt (cost $125,900) | | | | | | | | | | | | | | | 152,538 | |

| | | | Total Long-Term Investments (cost $109,770,062) | | | | | | | | | | | | | | | 105,724,727 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | | | | Value | |

| | |

| | | | SHORT-TERM INVESTMENTS – 0.5% (0.3% of Total Investments) | | | | | |

| | |

| | | | REPURCHASE AGREEMENTS – 0.5% (0.3% of Total Investments) | | | | | |

| | | | | |

| $ | 347 | | | Repurchase Agreement with State Street Bank, dated 12/31/15,

repurchase price $347,040, collateralized by $330,000 U.S. Treasury Notes, 3.500%, due 5/15/20, value $355,988 | | | 0.010% | | | | 1/04/16 | | | | | | | $ | 347,040 | |

| | | | Total Short-Term Investments (cost $347,040) | | | | | | | | | | | | | | | 347,040 | |

| | | | Total Investments (cost $110,117,102) – 140.1% | | | | | | | | | | | | | | | 106,071,767 | |

| | | | Reverse Repurchase Agreements – (24.6)% | | | | | | | | | | | | | | | (18,604,000 | ) |

| | | | Other Assets Less Liabilities – (15.5)% (9) | | | | | | | | | | | | | | | (11,747,572 | ) |

| | | | Net Assets – 100% | | | | | | | | | | | | | | $ | 75,720,195 | |

| | | | |

| JMM | | Nuveen Multi-Market Income Fund | | |

| | Portfolio of Investments (continued) | | December 31, 2015 (Unaudited) |

Investments in Derivatives as of December 31, 2015

Futures Contracts outstanding:

| | | | | | | | | | | | | | | | | | | | | | | | |

| Description | | Contract

Position | | | Number of

Contracts | | | Contract

Expiration | | | Notional

Amount

at Value | | | Variation Margin

Receivable/(Payable) | | | Unrealized

Appreciation

(Depreciation) | |

U.S. Treasury 2-Year Note | | | Short | | | | (3 | ) | | | 3/16 | | | $ | (651,703 | ) | | $ | (141 | ) | | $ | 696 | |

U.S. Treasury 5-Year Note | | | Short | | | | (77 | ) | | | 3/16 | | | | (9,110,664 | ) | | | (10,828 | ) | | | 22,483 | |

U.S. Treasury 10-Year Note | | | Short | | | | (50 | ) | | | 3/16 | | | | (6,295,313 | ) | | | (14,844 | ) | | | 20,115 | |

| | | | | | | | | | | | | | | $ | (16,057,680 | ) | | $ | (25,813 | ) | | $ | 43,294 | |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets. |

| (2) | Ratings: Using the highest of Standard & Poor’s Group (“Standard & Poor’s”), Moody’s Investors Service, Inc. (“Moody’s”) or Fitch, Inc. (“Fitch”) rating. Ratings below BBB by Standard & Poor’s, Baa by Moody’s or BBB by Fitch are considered to be below investment grade. Holdings designated N/R are not rated by any of these national rating agencies. |

| (3) | As of, or subsequent to, the end of the reporting period this security is non-income producing. Non-income producing, in the case of a fixed-income security, generally denotes that the issuer has (1) defaulted on the payment of principal or interest, (2) is under the protection of the Federal Bankruptcy Court or (3) the Fund’s Adviser has concluded that the issue is not likely to meet its future interest payment obligations and has ceased accruing additional income on the Fund’s records. |

| (4) | Investment valued at fair value using methods determined in good faith by, or at the discretion of, the Board. For fair value measurement disclosure purposes, investment classified as Level 3. See Notes to Financial Statements, Note 2 – Investment Valuation and Fair Value Measurements for more information. |

| (5) | Perpetual security. Maturity date is not applicable. |

| (6) | Investment, or portion of investment, has been pledged to collateralize the net payment obligations for investments in reverse repurchase agreements. |

| (7) | Principal Amount (000) rounds to less than $1,000. |

| (8) | A copy of the most recent financial statements for these investment companies can be obtained directly from the Securities and Exchange Commission on its website at http://www.sec.gov. |

| (9) | Other assets less liabilities includes the unrealized appreciation (depreciation) of certain over-the-counter derivatives as presented on the Statement of Assets and Liabilities. The unrealized appreciation (depreciation) of exchange-cleared and exchange-traded derivatives is recognized as part of the cash collateral at brokers and/or the receivable or payable for variation margin as presented on the Statement of Assets and Liabilities, when applicable. |

| MDR | Denotes investment is subject to dollar roll transactions. |

| REIT | Real Estate Investment Trust |

| TBA | To be announced. Maturity date not known prior to settlement of this transaction. |

| 144A | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration, which are normally those transactions with qualified institutional buyers. |

| (WI/DD) | Investment, or portion of investment, purchased on a when-issued or delayed delivery basis. |

See accompanying notes to financial statements.

| | | | | | |

Statement of Assets and Liabilities | | December 31, 2015 (Unaudited) |

| | | | |

Assets | | | | |

Long-term investments, at value (cost $109,770,062) | | $ | 105,724,727 | |

Short-term investments, at value (cost approximates value) | | | 347,040 | |

Cash | | | 8,444 | |

Cash and cash equivalent collateral at broker[1] | | | 158,700 | |

Receivable for: | | | | |

Dividends | | | 6,623 | |

Interest | | | 822,030 | |

Paydowns | | | 114,614 | |

Other assets | | | 990 | |

Total assets | | | 107,183,168 | |

Liabilities | | | | |

Reverse repurchase agreements | | | 18,604,000 | |

Payable for: | | | | |

Investments purchased | | | 12,666,516 | |

Variation margin on futures contracts | | | 25,813 | |

Accrued expenses: | | | | |

Interest | | | 5,571 | |

Management fees | | | 70,949 | |

Trustees fees | | | 596 | |

Other | | | 89,528 | |

Total liabilities | | | 31,462,973 | |

Net assets | | $ | 75,720,195 | |

Shares outstanding | | | 9,462,350 | |

Net asset value (‘NAV’) per share outstanding | | $ | 8.00 | |

Net assets consist of: | | | | |

Shares, $0.01 par value per share | | $ | 94,624 | |

Paid-in surplus | | | 82,347,967 | |

Undistributed (Over-distribution of) net investment income | | | (338,426 | ) |

Accumulated net realized gain (loss) | | | (2,381,929 | ) |

Net unrealized appreciation (depreciation) | | | (4,002,041 | ) |

Net assets | | $ | 75,720,195 | |

Authorized shares | | | Unlimited | |