SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM MAY 1, 2002 TO DECEMBER 31, 2002

COMMISSION FILE NUMBER: 0-17140

Tomkins plc

(Exact name of Registrant as specified in its charter)

England

(Jurisdiction of incorporation or organization)

East Putney House, 84 Upper Richmond Road

London SW15 2ST, United Kingdom

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange |

| Ordinary Shares, nominal value 5p per share | | New York Stock Exchange * |

| American Depositary Shares, each of which represents four Ordinary Shares | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act

None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Transition report:

Ordinary Shares, nominal value 5p per share | | 772,973,339 |

Convertible Cumulative Preference Shares, nominal value US$50 per share | | 10,507,478 |

Redeemable Convertible Cumulative Preference Shares, nominal value US$50 per share | | 12,438,282 |

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No ¨

Indicate by check mark which financial statement item the Registrant has elected to follow: Item 17 x Item 18 ¨

| * | | Not for trading, but only in connection with the registration of American Depositary Shares representing such Ordinary Shares |

TABLE OF CONTENTS

In this Transition Report (the “Transition Report”) on Form 20-F for the eight month period from May 1, 2002 to December 31, 2002 (“eight months ended December 31, 2002”), all references to “Tomkins”, the “Tomkins Group”, the “Group”, the “Company”, “we”, “us” and “our” include Tomkins plc and its consolidated subsidiaries, unless the context otherwise requires.

The consolidated financial statements of Tomkins plc appearing in this Transition Report are presented in pounds sterling (“£”) and are prepared in accordance with accounting principles generally accepted in the United Kingdom (“U.K. GAAP”). U.K. GAAP differs in certain respects from accounting principles generally accepted in the United States of America (“U.S. GAAP”). The significant differences between U.K. GAAP and U.S. GAAP relevant to Tomkins plc are explained in Note 27 of Notes to the consolidated financial statements.

In this Transition Report, references to “U.S. dollars”, “$”, “cents” and “c” are to United States currency and references to “pounds sterling”, “£”, “pence” and “p” are to British currency. Solely for the convenience of the reader, this Transition Report contains translations of certain pound sterling amounts into U.S. dollars. These translations should not be construed as representations that the pound sterling amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rates indicated or at any other rates. Unless otherwise stated, the translations of pounds sterling into U.S. dollars have been made at $1.6095 to £1.00, the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York (the “Noon Buying Rate”) on December 31, 2002, provided, however, that the amounts associated with acquisitions and dispositions are translated at the Noon Buying Rate on the date of completion. On June 6, 2003, the Noon Buying Rate was $1.6622 to £1.00.

Pursuant to the meaning of forward-looking statements in Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), this Transition Report contains assumptions, anticipations, expectations and forecasts concerning the Company’s future business plans, products, services, financial results, performance, future events and information relevant to our business, industries and operating environments. When used in this document, the words “anticipate”, “believe”, “estimate”, “assume”, “could”, “should”, “expect” and similar expressions, as they relate to the Company or its management, are intended to identify forward-looking statements. Such statements reflect the current views of Tomkins with respect to future events and are subject to certain risks, uncertainties and assumptions. The forward-looking statements contained herein represent a good-faith assessment of our future performance for which we believe there is a reasonable basis. Many factors could cause the actual results, performance or achievements of Tomkins to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements, including, among others, adverse changes or uncertainties in general economic conditions in the markets we serve, regulatory developments adverse to us or difficulties we may face in maintaining necessary licenses or other governmental approvals, changes in the competitive position or introduction of new competitors or new competitive products, lack of acceptance of new products or services by the Company’s targeted customers, changes in business strategy, any management level or large-scale employee turnover, any major disruption in production at our key facilities, adverse changes in foreign exchange rates, and acts of terrorism or war, and various other factors, both referenced and not referenced in this Transition Report. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein as anticipated, believed, estimated or expected. For more discussion of the risks affecting us, please refer to Item 3.D. “Key Information—Risk factors”.

These forward-looking statements represent our view only as of the date they are made, and we disclaim any obligation to update forward-looking statements contained herein, except as may be otherwise required by law.

1

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. Selected financial data

The selected financial data set out below as of and for the eight month Transition Period ended December 31, 2002 and for the fiscal years ended April 30, 2002 and April 30, 2001 has been derived from the audited consolidated financial statements of the Company, which appear elsewhere in this Form 20-F. The selected financial data as of and for the fiscal years ended April 29, 2000, May 1, 1999 and May 2, 1998 has been derived from the audited financial statements of the Company appearing in our historical annual reports as filed with the Securities and Exchange Commission (the “SEC”). The selected financial data set forth below should be read in conjunction with, and are qualified in their entirety by reference to, such consolidated financial statements and Notes thereto and Item 5 – “Operating and Financial Review and Prospects”. The selected financial data does not comprise “statutory accounts” within the meaning of Section 240 of the Companies Act 1985 of England and Wales (the “Companies Act”), but have been based upon the full published accounts of the Company for the eight month period ended December 31, 2002 and the five fiscal years ended April 30, 2002. The published accounts for the eight month period ended December 31, 2002 and for the five fiscal years ended April 30, 2002, upon which unqualified auditors’ reports have been given, have each been delivered to the Registrar of Companies in England and Wales with the exception of the accounts for the eight month period ended December 31, 2002, which will be delivered prior to the relevant filing deadline of July 31, 2003. The consolidated financial statements of the Company are prepared in accordance with U.K. GAAP, which differs in certain significant respects from U.S. GAAP. The principal differences between U.K. GAAP and U.S. GAAP, as they relate to the Company, are presented in Note 27 to the consolidated financial statements.

Consolidated income statement data

| | | Fiscal Year Ended

| |

| | | December 31, 2002(1)

(245 days)

| | | December 31,

2002 (245 days)

| | | April 30,

2002 (365 days)

| | | April 30,

2001

(366 days)

| | | April 29,

2000 (364 days)

| | | May 1, 1999 (364

days)

| | | May 2, 1998 (364

days)

| |

| | | (In millions except per Ordinary Share and per ADS data) | |

| | | $ | | | £ | | | £ | | | £ | | | £ | | | £ | | | £ | |

Amounts in accordance with U.K.GAAP | | | | | | | | | | | | | | | | | | | | | |

Net sales | | | | | | | | | | | | | | | | | | | | | |

Continuing operations | | 3,375.4 | | | 2,097.2 | | | 3,373.8 | | | 3,335.1 | | | 3,161.7 | | | 2,818.2 | | | 2,710.2 | |

Discontinued operations | | — | | | — | | | — | | | 770.4 | | | 2,478.7 | | | 2,541.1 | | | 2,351.9 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

| | | 3,375.4 | | | 2,097.2 | | | 3,373.8 | | | 4,105.5 | | | 5,640.4 | | | 5,359.3 | | | 5,062.1 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Operating income | | | | | | | | | | | | | | | | | | | | | |

Continuing operations | | 230.3 | | | 143.1 | | | 256.1 | | | 299.2 | | | 336.5 | | | 298.7 | | | 281.5 | |

Discontinued operations | | — | | | — | | | — | | | 11.2 | | | 182.9 | | | 196.6 | | | 195.8 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

| | | 230.3 | | | 143.1 | | | 256.1 | | | 310.4 | | | 519.4 | | | 495.3 | | | 477.3 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before taxes and minority interests | | 246.4 | | | 153.1 | | | 264.4 | | | 144.0 | | | 252.6 | | | 461.6 | | | 500.4 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before preference dividend | | 189.6 | | | 117.8 | | | 187.5 | | | 53.3 | | | 105.1 | | | 296.7 | | | 316.7 | |

Preference share dividend | | (39.4 | ) | | (24.5 | ) | | (39.3 | ) | | (37.6 | ) | | (34.4 | ) | | (34.2 | ) | | (34.5 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income attributable to Ordinary Shareholders | | 150.2 | | | 93.3 | | | 148.2 | | | 15.7 | | | 70.7 | | | 262.5 | | | 282.2 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Basic net income: | | | | | | | | | | | | | | | | | | | | | |

Per ordinary share | | 19.48 | c | | 12.10 | p | | 19.16 | p | | 1.83 | p | | 7.46 | p | | 22.69 | p | | 23.80 | p |

Per ADS(2) | | 77.90 | c | | 48.40 | p | | 76.64 | p | | 7.32 | p | | 29.84 | p | | 90.76 | p | | 95.20 | p |

Diluted net income: | | | | | | | | | | | | | | | | | | | | | |

Per ordinary share | | 19.02 | c | | 11.82 | p | | 18.78 | p | | 1.83 | p | | 11.07 | p | | 21.44 | p | | 22.30 | p |

Per ADS(2) | | 76.10 | c | | 47.28 | p | | 75.12 | p | | 7.32 | p | | 44.28 | p | | 85.76 | p | | 89.20 | p |

Dividends: | | | | | | | | | | | | | | | | | | | | | |

Per ordinary share | | 12.88 | c | | 8.00 | p | | 12.00 | p | | 12.00 | p | | 17.45 | p | | 15.15 | p | | 13.17 | p |

Per ADS(2) | | 51.50 | c | | 32.00 | p | | 48.00 | p | | 48.00 | p | | 69.80 | p | | 60.60 | p | | 52.68 | p |

| |

| | | (in thousands) | |

Average number of ordinary shares outstanding—basic | | 770,927 | | | 770,927 | | | 773,464 | | | 857,686 | | | 947,774 | | | 1,156,877 | | | 1,185,873 | |

Average number of ordinary shares outstanding—diluted | | 996,607 | | | 996,607 | | | 998,355 | | | 857,712 | | | 949,793 | | | 1,383,752 | | | 1,420,178 | |

| (1) | | The Noon Buying Rate on December 31, 2002 of $1.6095 = £1.00 has been used to provide a convenience translation into U.S. dollars solely for the convenience of the reader. |

| (2) | | Net income and dividend per ADS is calculated per Ordinary Share multiplied by four, as discussed in Item 9.C. “Markets.” |

2

Consolidated income statement data (continued)

| | | Fiscal Year Ended

| |

| | | December 31, 2002(1) (245 days)

| | | December 31, 2002(6) (245 days)

| | | April 30,

2002(5) (365 days)

| | | April 30,

2001(4) (366 days)

| | | April 29,

2000(3) (364 days)

| | | May 1, 1999 (364 days)

| | | May 2, 1998 (364 days)

| |

| | | (In millions except per Ordinary Share and per ADS data) | |

| | | $ | | | £ | | | £ | | | £ | | | £ | | | £ | | | £ | |

Amounts in accordance with U.S.GAAP | | | | | | | | | | | | | | | | | | | | | |

Net sales | | 3,375.4 | | | 2,097.2 | | | 3,373.8 | | | 4,105.5 | | | 5,640.4 | | | 5,359.3 | | | 5,062.1 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Operating income from continuing operations | | 274.9 | | | 170.8 | | | 228.6 | | | 284.8 | | | 323.8 | | | 275.7 | | | 261.6 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Operating income | | 274.9 | | | 170.8 | | | 228.6 | | | 296.0 | | | 479.4 | | | 455.1 | | | 420.4 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before change in accounting principle | | 176.7 | | | 109.8 | | | 147.8 | | | 64.4 | | | 193.5 | | | 256.7 | | | 259.6 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Effects of change in accounting principle, net of tax | | (52.6 | ) | | (32.7 | ) | | 1.8 | | | — | | | — | | | — | | | — | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income | | 124.1 | | | 77.1 | | | 149.6 | | | 64.4 | | | 193.5 | | | 256.7 | | | 259.6 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income per Ordinary Share | | | | | | | | | | | | | | | | | | | | | |

Basic: | | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations before change in accounting principle | | 17.80 | c | | 11.06 | p | | 14.03 | p | | 16.27 | p | | 13.04 | p | | 10.78 | p | | 9.59 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before change in accounting principle | | 17.80 | c | | 11.06 | p | | 14.03 | p | | 3.12 | p | | 16.79 | p | | 19.23 | p | | 18.98 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Cumulative effect of change in accounting principle | | (6.82 | )c | | (4.24 | )p | | 0.23 | p | | — | | | — | | | — | | | — | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income | | 10.98 | c | | 6.82 | p | | 14.26 | p | | 3.12 | p | | 16.79 | p | | 19.23 | p | | 18.98 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Diluted: | | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations before change in accounting principle | | 17.74 | c | | 11.02 | p | | 14.02 | p | | 16.27 | p | | 13.01 | p | | 10.75 | p | | 9.52 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before change in accounting principle | | 17.74 | c | | 11.02 | p | | 14.02 | p | | 3.12 | p | | 16.75 | p | | 19.17 | p | | 18.84 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Cumulative effect of change in accounting principle | | (5.28 | )c | | (3.28 | )p | | 0.23 | p | | — | | | — | | | — | | | — | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income | | 12.46 | c | | 7.74 | p | | 14.25 | p | | 3.12 | p | | 16.75 | p | | 19.17 | p | | 18.84 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income per ADS(2) | | | | | | | | | | | | | | | | | | | | | |

Basic: | | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations before change in accounting principle | | 71.20 | c | | 44.24 | p | | 56.12 | p | | 65.08 | p | | 52.16 | p | | 43.12 | p | | 38.36 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before change in accounting principle | | 71.20 | c | | 44.24 | p | | 56.12 | p | | 12.48 | p | | 67.16 | p | | 76.92 | p | | 75.92 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Cumulative effect of change in accounting principle | | (27.30 | c) | | (16.96 | )p | | 0.92 | p | | — | | | — | | | — | | | — | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income | | 43.90 | c | | 27.28 | p | | 57.04 | p | | 12.48 | p | | 67.16 | p | | 76.92 | p | | 75.92 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Diluted: | | | | | | | | | | | | | | | | | | | | | |

Income from continuing operations before change in accounting principle | | 70.95 | c | | 44.08 | p | | 56.08 | p | | 65.08 | p | | 52.04 | p | | 43.00 | p | | 38.08 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Income before change in accounting principle | | 70.95 | c | | 44.08 | p | | 56.08 | p | | 12.48 | p | | 67.00 | p | | 76.68 | p | | 75.36 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Cumulative effect of change in accounting principle | | (21.12 | )c | | (13.12 | )p | | 0.92 | p | | — | | | — | | | — | | | — | |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Net income | | 49.83 | c | | 30.96 | p | | 57.00 | p | | 12.48 | p | | 67.00 | p | | 76.68 | p | | 75.36 | p |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Dividends per ordinary share | | 12.88 | c | | 8.00 | p | | 12.00 | p | | 12.00 | p | | 17.45 | p | | 15.15 | p | | 13.17 | p |

Dividends per ADS(2) | | 51.50 | c | | 32.00 | p | | 48.00 | p | | 48.00 | p | | 69.80 | p | | 60.60 | p | | 52.68 | p |

| |

| | | (in thousands) | |

Average number of ordinary shares outstanding—basic | | 770,927 | | | 770,927 | | | 773,464 | | | 857,686 | | | 947,774 | | | 1,156,877 | | | 1,185,873 | |

Average number of ordinary shares outstanding—diluted(7) | | 996,607 | | | 996,607 | | | 774,017 | | | 857,712 | | | 949,793 | | | 1,383,752 | | | 1,420,178 | |

| (1) | | The Noon Buying Rate on December 31, 2002 of $1.6095 = £1.00 has been used to provide a convenience translation into U.S. dollars solely for the convenience of the reader. |

| (2) | | Net income and dividend per ADS is calculated per Ordinary Share multiplied by four, as discussed in Item 9.C. “Markets.” |

| (3) | | Tomkins acquired ACD Tridon Inc. and Hart & Cooley on June 25, 1999 and December 30, 1999 respectively. |

| (4) | | The sale of the Food Manufacturing business segment was completed on August 31, 2000. |

| (5) | | Change in accounting principle relates to Tomkins transitional adjustment in respect of the adoption of SFAS No. 133 on May 1, 2001. |

| (6) | | Change in accounting principle relates to Tomkins transitional adjustment in respect of the adoption of SFAS No. 142 on May 1, 2002. |

| (7) | | In fiscal year ended April 30, 2002, the preference shares were anti-dilutive and were therefore excluded from the calculation. |

3

Consolidated balance sheet data

| | | As of

|

| | | December 31, 2002(1)

| | December 31,

2002

| | April 30,

2002

| | April 30,

2001

| | April 29,

2000

| | May 1, 1999

| | May 2, 1998

|

| | | (In millions) |

| | | $ | | £ | | £ | | £ | | £ | | £ | | £ |

Amounts in accordance with U.K. GAAP | | | | | | | | | | | | | | |

Net assets | | 1,734.2 | | 1,077.5 | | 1,141.1 | | 1,118.9 | | 760.4 | | 675.1 | | 1,092.6 |

Total assets | | 3,751.4 | | 2,330.8 | | 2,564.7 | | 2,765.7 | | 3,885.1 | | 3,289.9 | | 3,151.8 |

Ordinary share capital | | 62.3 | | 38.7 | | 38.6 | | 39.1 | | 47.5 | | 47.5 | | 58.8 |

Shareholders’ funds | | 1,673.1 | | 1,039.5 | | 1,106.9 | | 1,084.9 | | 726.4 | | 646.8 | | 1,073.9 |

| | | | | | | |

Amounts in accordance with U.S. GAAP | | | | | | | | | | | | | | |

Net assets | | 2,371.4 | | 1,473.4 | | 1,805.8 | | 1,866.1 | | 2,280.9 | | 2,245.7 | | 2,712.6 |

Total assets | | 5,173.1 | | 3,214.1 | | 3,602.9 | | 3,794.9 | | 5,641.1 | | 5,095.2 | | 5,013.0 |

Shareholders’ equity | | 2,438.1 | | 1,514.8 | | 1,771.6 | | 1,832.7 | | 2,247.4 | | 2,217.7 | | 2,693.9 |

| (1) | | The Noon Buying Rate on December 31, 2002 of $1.6095 = £1.00 has been used to provide a convenience translation into U.S. dollars solely for the convenience of the reader. |

Dividends

The Company has paid cash dividends on its ordinary shares, nominal value 5p per share (“Ordinary Shares”), in respect of every fiscal year since being first listed on the London Stock Exchange Limited (the “London Stock Exchange”) in 1950.

Dividends are paid to shareholders as of record dates that are fixed after consultation between the Company and the London Stock Exchange. Prior to changing our fiscal year end, an interim dividend was normally declared by the Board of Directors (the “Board”) in January of each year and paid in March or April. A final dividend is recommended by the Board following the end of each fiscal year and is subject to approval by the shareholders at the Company’s annual general meeting. The final dividend was paid in October. For the current year ending on December 31, 2003 and thereafter, we intend to pay an interim dividend in November and a final dividend in the following May, in accordance with market practice. In normal circumstances we anticipate the weighting of these payments to be approximately 40 percent for the interim dividend and 60 percent for the final dividend.

The table below sets forth the amounts of interim, final and total dividends paid in respect of each fiscal year indicated and the Transition Period ending December 31, 2002. The amounts are shown both in pence per Ordinary Share and translated, solely for convenience, into U.S. cents per American Depositary Share (each representing four Ordinary Shares) at the Noon Buying Rate on each of the respective payment dates for such interim and final dividends.

Fiscal Year Ended

| | Pence per Ordinary Share

| | Translated into U.S. cents per ADS(2)

|

| | | Interim

| | | Second

Interim

| | Final

| | Total

| | Interim

| | Second

Interim

| | Final

| | Total

|

May 2, 1998 | | 3.50 | (1) | | — | | 9.67 | | 13.17 | | 23.48 | | — | | 66.47 | | 89.95 |

May 1, 1999 | | 4.00 | (1) | | — | | 11.15 | | 15.15 | | 25.83 | | — | | 73.69 | | 99.52 |

April 29, 2000 | | 4.60 | | | — | | 12.85 | | 17.45 | | 29.12 | | — | | 74.44 | | 103.56 |

April 30, 2001 | | 4.60 | | | — | | 7.40 | | 12.00 | | 26.46 | | — | | 43.79 | | 70.25 |

April 30, 2002 | | 4.60 | | | — | | 7.40 | | 12.00 | | 26.33 | | — | | 46.30 | | 72.63 |

May 1, 2002 – December 31, 2002 | | 4.60 | | | 3.40 | | — | | 8.00 | | 28.52 | | 21.08 | | — | | 49.60 |

| (1) | | Of which 3.06p was paid in the form of a foreign income dividend. |

| (2) | | Translated at the noon buying rate on the date the dividend was paid. |

The Company expects to continue to pay dividends in the future. The total amounts of future dividends will be determined by the Board and will depend on the Company’s results of operations, cash flow, financial and economic conditions and other factors.

The Company’s fiscal year end changed from April 30 to December 31 with effect for the year ending December 31, 2002. The change to our accounting reference date has given rise to an eight month accounting period, which represents two-thirds of a normal twelve month accounting period. In accordance with market practice in these circumstances, the Board has elected to declare two interim dividends in lieu of an interim and a final dividend.

4

The first interim dividend of 4.6 pence per ordinary share was declared on January 14, 2003. The Board declared a second interim dividend of 3.4 pence per ordinary share on March 4, 2003 in lieu of a final dividend. Taken together, these interim dividends bring the total dividend payable for this eight month accounting period to 8.0 pence per ordinary share, which represents two-thirds of the total dividends paid in respect of the last fiscal year ended April 30, 2002. Both the first and the second interim dividends were paid on April 7, 2003 to shareholders of record on March 14, 2003. Tomkins ordinary shares went ex-dividend on the London Stock Exchange in respect of both dividends on March 12, 2003.

The Board has decided not to offer a dividend reinvestment plan option for the first and second interim dividends due to the change in the dividend timetable. We will consider whether to offer such an option for dividends payable in respect of the year ending December 31, 2003.

Cash dividends are paid by the Company in pounds sterling, and fluctuations in the exchange rate between pounds sterling and U.S. dollars will affect the U.S. dollar amounts received by holders of American Depository Receipts (“ADRs”) upon conversion by The Bank of New York (the “Depositary”) of such dividends. Moreover, fluctuations in the exchange rates between the pound sterling and the U.S. dollar will affect the dollar equivalents of the pound sterling price of the Ordinary Shares on the London Stock Exchange and, as a result, are likely to affect the market prices of the American Depositary Shares (“ADSs”) in the United States. For information regarding the exchange rates for pounds sterling into U.S. dollars for the five most recent fiscal years, see “Exchange Rates” below. For a discussion of the historic effects of exchange rate fluctuations on the Company’s financial condition and results of operations, see Item 11. “Quantitative and Qualitative Disclosures about Market Risk” and Note 26 to the consolidated financial statements.

Exchange Rates

The following table sets forth, for the fiscal years indicated, the average, high, low and period end Noon Buying Rates for pounds sterling, expressed in U.S. dollars per £1.00:

Fiscal Year Ended

| | Average*

| | High

| | Low

| | Period End

|

May 2, 1998 | | 1.65 | | 1.70 | | 1.58 | | 1.67 |

May 1, 1999 | | 1.64 | | 1.72 | | 1.59 | | 1.61 |

April 29, 2000 | | 1.60 | | 1.68 | | 1.55 | | 1.56 |

April 30, 2001 | | 1.47 | | 1.56 | | 1.40 | | 1.43 |

April 30, 2002 | | 1.43 | | 1.48 | | 1.37 | | 1.46 |

Eight months ended December 31, 2002 | | 1.55 | | 1.61 | | 1.45 | | 1.61 |

Jan 1, 2003 through June 6, 2003 | | 1.62 | | 1.66 | | 1.55 | | 1.62 |

| * | | The average of the Noon Buying Rates on the last day of each month during the period. |

The following table sets forth, for the months indicated high and low Noon Buying Rates for pounds sterling, expressed in U.S. dollars per £1.00:

Month

| | High

| | Low

|

December 2002 | | 1.6044 | | 1.5555 |

January 2003 | | 1.6482 | | 1.5975 |

February 2003 | | 1.6480 | | 1.5727 |

March 2003 | | 1.6129 | | 1.5624 |

April 2003 | | 1.6000 | | 1.5500 |

May 2003 | | 1.6484 | | 1.5930 |

June 2003 (through June 6, 2003) | | 1.6622 | | 1.6278 |

See “Operating results” in Item 5. “Operating and Financial Review and Prospects” concerning the effect of fluctuations in the exchange rate between the pound sterling and the U.S. dollar on the Company’s results of operations.

B. Capitalization and indebtedness

Not applicable.

C. Reasons for the offer and use of proceeds

Not applicable.

5

D. Risk factors

In addition to the other information contained in this Transition Report, investors in our securities should consider carefully the risks described below. Our financial condition or results of operations could be materially adversely affected by any of these risks. The risks described below are not the only risks facing us. Additional risks not currently known to us, or risks that we currently regard as immaterial could also have a material adverse effect on our financial condition or results of operations.

The following discussion contains a number of forward-looking statements. Please refer to the “Forward-Looking Statements” discussion at the front of this Transition Report for cautionary information.

As a part of the planning, control and performance management framework of the Group, each business considers strategic, operational, commercial and financial risks and identifies risk mitigation actions. The Group has categorized the foregoing risks as those relating to:

| | • | | the markets within which the Group operates; |

| | • | | the competitive position of the Group and its businesses; |

| | • | | the financial position of the Group; and |

| | • | | the securities markets and ownership of ADSs and registered shares. |

Risk can be considered either as downside risk, the risk that something can go wrong and result in a financial loss or financial exposure for the Group, or volatility risk. Volatility risk is the risk associated with uncertainty, which means there may be an opportunity for financial gain as well as potential for loss.

The risks listed primarily relate to potential downside risks. The nature of the Group’s business means that risks will change as a result of controllable and uncontrollable events occurring in the future.

Risks relating to the markets within which the Group operates

The cyclical nature of automotive production and sales could adversely affect our business.

Approximately a quarter of our net sales are to automotive manufacturers in various parts of the world. Sales and production in the automotive industry are cyclical and depend on general economic conditions and other factors, including consumer spending and preferences. A significant reduction in automotive production and sales by our customers could have an adverse effect on our business, financial condition or results of operations.

A continuing improvement in vehicle component life could adversely affect our important aftermarket business.

The success of component manufacturers including ourselves in improving product quality and performance and the demand from the automotive original equipment makers for ever greater service life and reliability could lower demand in the aftermarket business segment which could have an adverse effect on our business, financial condition or results of operations.

A potentially changing regulatory environment could limit our business opportunities and profitability.

Changes in existing laws, regulations, licenses, decisions, policies or interpretations thereof by the courts, or by regulators, may have a material adverse impact on our business, financial condition or results of operations.

In particular, the industries in which we operate are subject to a variety of environmental regulations, particularly relating to waste water discharges, air emissions, solid waste management and hazardous chemical disposal. These regulations have generally become stricter in recent years and may continue to become more stringent in the future. Any future changes to existing environmental legislation or regulation could have a material adverse effect on our business, financial condition or results of operations. There is a risk that our activities will not continue to be in substantial compliance in the future with applicable environmental legislation or regulation and we are unable to predict the costs of compliance with changes in legislation or regulation.

In certain countries we are required to secure and maintain operating licenses. If we experience difficulties or delays in obtaining or maintaining licenses in the future or if the cost of such licenses increases significantly, this could adversely affect our business, financial condition or results of operations.

Our operations in foreign and emerging markets expose us to risks associated with conditions in those markets.

We operate principally in the automotive, industrial and construction related markets in a number of geographic regions of the world, including emerging markets. Operations in emerging markets present risks that are not encountered in countries with better established economic and political systems, including: economic and political instability within these markets; boycotts and embargoes imposed by the international community; significant fluctuations in interest rates and currency exchange rates; the imposition of unexpected taxes or other levies on our revenues in these markets; the inability to expatriate revenues or dividends; limitations on foreign

6

investments and foreign capital participation in certain industries or regions; and the introduction of exchange, customs or trade controls and other restrictions by foreign governments.

In addition, the legal and regulatory systems of foreign and emerging markets identified above are often less formalized and less consistently enforced than in industrialized countries. Therefore, our ability to protect our intellectual property and our contractual and other legal rights in those regions could be limited. Changes in demand in any of these markets may have an adverse affect on our business, financial condition or results of operations.

Public health issues, in particular SARS may adversely impact our business and particularly the operations of our customers in East Asia.

The recent Severe Acute Respiratory Syndrome (“SARS”) outbreak has been most notable in Asia, in particular China and Singapore. While the long-term impact of the SARS outbreak is unclear at this time, the prolonged existence of the SARS outbreak, or the perception that the SARS outbreak has not been contained, may have an adverse effect on the trade and industries as well as on the economies and financial markets of certain countries in Asia. Since a number of our customers are located in Asia, the commercialization of our products could suffer from any economic downturn resulting therefrom. In addition, our business could also be harmed if travel to or from Asia is restricted or inadvisable.

Risks relating to the competitive position of the Group and its businesses

Industry consolidation could result in more powerful competitors and fewer customers.

Our customers and competitors in some of our markets, especially in the automotive aftermarket, and to a lesser extent in the markets of the Air Systems Components group, are consolidating to achieve greater scale or market share. Such changes could affect our customers and their relationship with us. If one of our competitors acquires any of our customers, we may lose its business. Additionally, as our customers become larger and more concentrated, they could exert pricing pressure on all suppliers, including us.

Some of our customers are experiencing lower levels of business.

Lower levels of economic activity have resulted in a number of our customers reducing demand compared to past years levels for some of our products and some rescheduling of orders. Lower levels of demand resulting from lower levels of business that may be experienced by our customers could have an adverse effect on our business, financial condition or results of operations.

Our automotive customers may seek to obtain price reductions from their suppliers and we may be unable to achieve corresponding reductions in costs.

Approximately a quarter of our sales are to automotive manufacturers. It is normal practice for such customers to seek reductions in their costs from their suppliers over the duration of any committed supply arrangement. To meet any such requests for price reductions, we would have to achieve corresponding cost savings in our business by strategic sourcing of raw materials and by improving production and manufacturing efficiencies. The failure to achieve future cost savings to meet the committed price reductions could adversely affect our business, financial condition or results of operations.

Reliance on certain raw materials and suppliers for key components could destabilize our productivity levels.

To the extent not reflected in prices for our products, an unexpected increase in the cost of certain raw materials, especially polymers, steel, aluminum and chemical resins, could lead to lower profit margins. The failure of our key suppliers to maintain and increase production levels could result in our inability to fulfill orders, which could damage relationships with current and prospective customers and have an adverse effect on our business, financial condition or results of operations.

Our business could be adversely affected if we are unable to obtain adequate supplies or equipment in a timely manner from our current suppliers or any alternative supplier, or if there were significant increases in the costs of such equipment.

We are dependent upon our strong relationships with manufacturers’ representatives, distributors and wholesalers.

Many of our businesses have strong established relationships with manufacturers’ representatives, distributors and wholesalers and these relationships are an important ingredient of our strong competitive positions in a number of our markets. Deterioration in these relationships, or a change in our product’s route to market, could have an adverse effect on our business, financial condition or results from operations.

Product liability claims may arise due to the nature of our products.

We face an inherent business risk of exposure to product liability claims in the event that a failure of a product results in, or is alleged to result in, bodily injury, property damage or result in consequential losses as a result of a product recall. Any material product liability losses in the future or costs to defend any alleged failures of our products may have a material adverse effect on our business, financial condition or results of operations.

7

If we are unable to implement our strategic initiatives successfully, our ability to achieve optimal market performance may be impaired.

We are pursuing a number of strategic initiatives aimed to ensure that we continue to focus on value creating areas, provide the appropriate value offerings to our customers, achieve superior execution of business processes and maintain a low cost position. A number of initiatives are also in place to achieve future growth by developing relationships with global customers, investing in product innovation, expanding into new geographic regions and product adjacent markets. The success of the strategic initiatives depends in part on the changing competitive dynamics of the markets in which we operate and management can provide no assurance that each of the strategic initiatives will be successful in achieving improvement in our financial performance.

If we experience difficulty in implementing our strategic initiatives it may have an adverse effect on our business, financial condition or results from operations.

We operate in very competitive markets and could be adversely affected if we fail to keep pace with technological changes.

We operate in very competitive environments in several geographical markets and product areas. The markets for our products and services are characterized by evolving industry standards, rapidly changing technology and increased competition. The continual development of advanced technologies for new products and product enhancements is an important way in which we maintain acceptable pricing levels. If we fail to keep pace with technological changes in the industrial sectors that we serve, we may experience price erosion and lower margins.

Our success is dependent in large part on our ability to:

| | • | | anticipate our customers’ needs and provide products and services to meet those needs; |

| | • | | develop new products and services that are accepted by our customers; |

| | • | | enhance and upgrade our existing products and services; and |

| | • | | price our products and services competitively. |

Many of our competitors are sophisticated companies with many resources that may develop products and services that are superior to our products and services or may adapt more quickly than we do to new technologies, industry changes or evolving customer requirements. Our failure to anticipate or respond adequately to technological developments or customer requirements, and any delay in accomplishing these goals, could adversely affect our business, financial condition or results of operations.

We are dependent on the continued operation of our manufacturing facilities.

Our manufacturing facilities are based principally in the United States and Europe. A major disruption of our critical manufacturing facilities could result in significant interruption of our business and potential loss of customers and sales, which could have an adverse effect on our business, financial condition or results of operations.

If we are unable to protect our intellectual property rights, the future success of our business could suffer.

Our proprietary technology is protected by patents and trade secrets which could be at risk if:

| | • | | competitors are able to develop similar technology independently; |

| | • | | our patent applications are not approved; |

| | • | | steps taken to prevent misappropriation or infringement of our intellectual property are not successful; or |

| | • | | we do not adequately protect our intellectual property. |

From time to time we may need to litigate in order to enforce our patents, copyrights or other intellectual property rights, to protect our trade secrets, to determine the validity and scope of the proprietary rights of others or to defend against significant claims of infringement. Any such litigation, the outcome of which will be uncertain, or its threat, could result in costs and a diversion of our resources.

We have a number of businesses in the various regions of the world, which provide additional management challenges.

We operate in many countries around the world, which requires us to take account of cultural and language differences and to assimilate different business practices. Failure to effectively manage our geographically diverse operations could have an adverse effect on our operations, financial condition or results from operations.

We have a number of employees who are members of trade unions or other employment organizations.

Some of our employees are members of trade unions and over many years we have been able to maintain successful relationships with the unions and employment organizations. A deterioration of these relationships in the future may have an adverse effect on our business, financial condition or results from operations.

8

Risks relating to the financial position of the Group

Tomkins plc is a holding company that is dependent upon cash flow from its subsidiaries to meet its obligations.

Tomkins plc is a holding company with no independent operations or significant assets other than investments in, and advances to, subsidiaries. Accordingly, it depends upon the receipt of sufficient funds from its subsidiaries to meet its obligations, including its ability to repay any amounts it borrows under its Medium Term Note program or to pay its dividends. The ability of Tomkins plc to access that cash flow may be limited in some circumstances. For instance, the terms of existing and future indebtedness of its subsidiaries and the laws and jurisdictions under which those subsidiaries are organized may limit the payment of dividends, loan repayments and other distributions to Tomkins plc. Any such limitations could have an adverse affect on our business, financial condition or results of operations.

Approximately 25 percent of our total revenues are generated from 10 major customers.

Approximately 25 percent of our total revenues come from the top ten customers of our Industrial & Automotive business. The loss of, or a significant decrease in demand from, one or more of these customers could result in an adverse effect on our business, financial condition or results of operations.

We operate pension plans throughout the world, covering the majority of employees, which expose us to the risk of fluctuations in the world’s financial markets.

We operate both defined benefit and defined contribution schemes, the majority of which are in the United States of America and the United Kingdom. The schemes were in deficit by £194.8 million as of December 31, 2002 as detailed in Note 24 to the consolidated financial statements. Deterioration in asset prices or changes to long term interest rates could adversely affect the deficit and have an adverse effect on our business, financial condition or results of operations.

The rising costs of providing health care and workers compensation may erode margins.

Healthcare is provided by certain US subsidiaries to current and former employees. We strive to cover increases in this expense and in the cost of workers compensation, by reducing overheads in other areas. If the cost of heath care and workers compensation increases to the extent that we are unable to achieve adequate savings elsewhere, operating margins may be eroded

Deferred consideration in respect of disposals may not be repaid in accordance with original terms.

In May 2001, we disposed of Smith & Wesson Corp. through a stock purchase agreement, which contains deferred terms in respect of $30 million of the proceeds from disposal, which will be repaid over the seven years commencing in May 2004. If the purchaser is unable to fulfill its payment obligations in the future, a provision against the deferred consideration receivable would be charged to the income statement of the Company.

We may not be able to raise sufficient additional capital necessary to fund our growth.

We may require significant amounts of capital to expand our business, implement our strategic initiatives and remain competitive. At present, our established sources of funding are through equity, corporate bond markets (through the Medium Term Note program) bank debt and cash flow from operations. We believe that the sources of funding currently available will be sufficient to fund our operations. If our plans or assumptions regarding our funding requirements change, however, we may need to seek other sources of financing, such as additional lines of credit with commercial banks or vendors or public financing, or to renegotiate existing bank facilities. There is a risk that we will not be able to obtain financing from these or other sources, or renegotiate our existing financing on a timely basis, on favorable terms, or at all. If we are unable to obtain financing from these sources, or unable to renegotiate our existing financing on a timely basis or on favorable terms, we may have to delay or abandon some of our development plans or strategic initiatives. Any or all of these developments could have an adverse affect on our business, financial condition or results of operations.

Our international operations expose us to the risk of fluctuations in currency exchange rates.

We have manufacturing facilities in, and sell products to, many countries worldwide. Consequently, our results can be affected by changes in the currency exchange rates. The principal currencies in which we trade are U.S. Dollars, Euros and Pounds Sterling. Currency exchange movements can give rise to the following risks:

Transaction risk—this arises where sales or purchases are denominated in foreign currencies and exchange rates can change between entering into a purchase or sale commitment and completing the transaction;

Translation risk—this arises where the currency in which the results of an entity are reported differs from the underlying currency in which business is transacted; and

Economic risk—this arises where the manufacturing cost base of a business is denominated in a currency different from the currency of the market into which the products are sold.

9

Short-term volatility and long-term realignments of currency exchange rates may have an adverse affect on our business, financial condition or results of operations.

Risks related to the securities market and ownership of ADSs and registered shares

Holders of ADSs may be restricted in their ability to exercise voting rights.

Holders of ADSs will generally have the right under the deposit agreement to instruct the Depositary to exercise their voting rights for the registered shares represented by ADSs.

At our request, the Depositary will mail to holders of ADSs any notice of any shareholders’ meeting received from us together with information explaining how to instruct the Depositary to exercise the voting rights of the securities represented by ADSs. If the Depositary receives voting instructions for a holder of ADSs on a timely basis, it is obligated to endeavor to vote the securities representing the holder’s ADSs in accordance with those voting instructions. The ability of the Depositary to carry out voting instructions, however, may be limited by practical limitations, such as time zone differences and delays in mailing.

ADS holders may be unable to participate in rights offerings and similar transactions in the future.

U.S. securities law may restrict the ability of U.S. persons who hold ADSs to participate in certain rights offerings or share or warrant dividend alternatives which we may undertake in the future in the event we are unable to, or choose not to, register those securities under the U.S. securities laws and are unable to rely on an exemption from registration under these laws. If we issue any securities of this nature in the future, we may issue such securities to the Depositary for the ADSs, which may sell those securities for the benefit of the holders of the ADSs. We cannot offer any assurance as to the value, if any, the Depositary would receive upon the sale of those securities.

10

Item 4. Information on the Company

A. History and development of the Company

General

Tomkins plc was incorporated in England in 1925, converted from a private company into a public company in March 1950 and re-registered as a public limited company in February 1982. The Company’s Ordinary Shares are listed on the London Stock Exchange and have been listed on the New York Stock Exchange (the “NYSE”) in the form of ADSs evidenced by ADRs since February 1995. Prior to listing on the NYSE, the ADSs had been quoted on the Nasdaq National Market since November 1988. Tomkins plc is registered in England and Wales No. 203531. Its registered office is East Putney House, 84 Upper Richmond Road, London SW15 2ST (Telephone: +44 (0) 20 8871 4544).

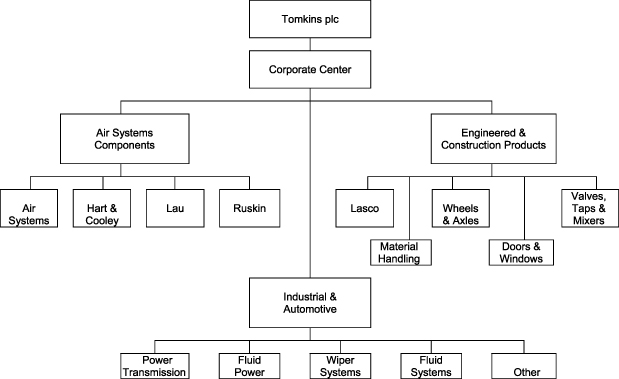

Tomkins is a global engineering and manufacturing group with market and technical leadership. Its activities report in three business segments:

Industrial & Automotive

The Industrial & Automotive segment manufactures systems and components for the industrial and automotive markets. The segment has four main business areas: Power Transmission; Fluid Power; Wiper Systems; and Fluid Systems. Sales are to original equipment manufacturers (“OEMs”) and the replacement markets around the world under leading brand names such as Gates, Trico, Stant and Schrader. We also have a number of discrete businesses that manufacture products primarily for the automotive replacement markets.

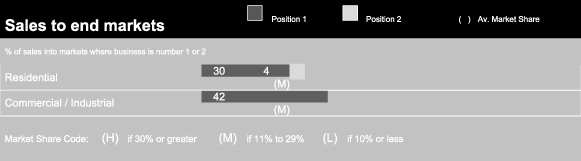

Air Systems Components

The Air Systems Components segment is the leading manufacturer of air handling components in North America. We supply the heating, ventilation and air conditioning (HVAC) market with a range of products including fans, grilles, registers, diffusers, fan coils and terminal units for residential and commercial applications, as well as dampers for architectural, commercial and industrial use. Our products are sold under the industry’s leading brand names: Hart & Cooley, Ruskin, Lau, Titus, Krueger and Actionair.

Engineered & Construction Products

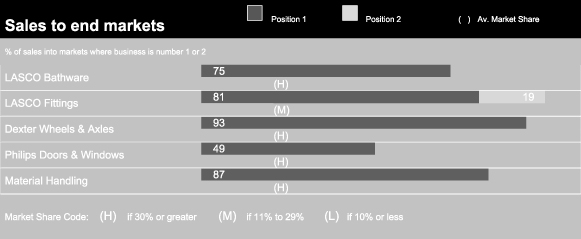

The Engineered & Construction Products segment manufactures products for a range of markets including construction, truck and trailer and automotive industries. It is divided into five main business areas: Lasco, Philips Doors & Windows, Material Handling, Dexter Wheels & Axles and Valves, Taps and Mixers. Each benefits from long-established relationships in its channels to market, a strongly branded product offering and a low manufacturing cost base. Over 90 percent of the segment’s sales are within North America.

The Company’s continuing operating units manufacture and distribute products throughout the world, including the United States, the United Kingdom, Canada, France, Belgium, the Republic of South Africa, Germany, Mexico, Brazil, Spain, The Netherlands, Korea, Australia, Singapore, Argentina, India, Japan, China, Poland and Thailand. The Company’s operating units are based principally in North America, Europe and Asia, employing approximately 40,000 people on average, worldwide, during the eight month period ended December 31, 2002.

Strategy

During the eight month period ended December 31, 2002, Tomkins focused on a number of strategic initiatives aimed at modernizing its business, implementing new technologies and manufacturing practices and expanding its markets. These initiatives include:

Technology and product innovation

The Company is committed to identifying, developing and applying new technologies with the commercial potential to realize tangible benefits for its customers.

Manufacturing excellence

The Company recognizes the importance of becoming the lowest-cost manufacturer of quality products in its market places. Progress is being made through a combination of lean manufacturing (which focuses on production efficiency and quality), and strategic manufacturing initiatives (“SMIs”) (that rationalize capacity and relocate productive capacity to low cost areas).

Industrial & automotive aftermarket

Tomkins already has a significant presence in the global industrial and automotive aftermarkets. Sales in these markets are typically more stable and achieve higher margins than in the original equipment market.

11

The Company aims to build on this platform by cutting its logistics costs, reducing inventory and increasing the rate of new product introductions. It is also aiming to increase further its presence outside the North American market, particularly in Europe and Asia.

Acquisitions and disposals

Tomkins recently strengthened its corporate finance team with a view to making further value-enhancing acquisitions and extending its technology. An overriding criteria is that acquisitions must add value to the Group by providing a return in excess of our weighted average cost of capital. The Company will also continue to dispose of non-core businesses where we believe that they can achieve higher returns elsewhere.

Role of the Corporate Center

The role of the Corporate Center at Tomkins is to assist the attainment of growth in value. The center supports operations as well as maintaining the framework of efficient financial reporting. It encourages the Company-wide implementation of best practice in manufacturing and other areas such as purchasing and human resource management. It develops incentive schemes for managers that aligns their compensation with the interests of shareholders, making them act more as owners of their businesses. It also directs the allocation of resources by ensuring that we only invest in opportunities that add value by providing returns in excess of our weighted average cost of capital.

The road ahead

Going forward Tomkins will be concentrating on:

| | • | | bringing innovative new products to market; |

| | • | | extending the Company’s product offering and geographic presence in both the industrial and automotive aftermarkets; |

| | • | | reducing the Company’s cost base still further through strategic manufacturing initiatives and lean manufacturing; and |

| | • | | using the Company’s financial strength to make value-enhancing acquisitions to its existing businesses. |

Principal acquisitions, disposals, and capital expenditures

This section should be read in conjunction with Item 5. “Operating and Financial Review and Prospects” and with Note 3 to the consolidated financial statements.

May 1, 2002 to December 31, 2002

Tomkins acquired the business, assets and liabilities of Ward Industries Inc. and the heating, ventilating and air conditioning dampers division of Johnson Controls Inc. on September 11, 2002 and September 30, 2002, respectively, for a combined cash consideration of $17.6 million (£11.3 million) of which $0.7 million (£0.4 million) is deferred. Goodwill of £6.9 million arising on these acquisitions was capitalized. The value of the assets acquired is still being assessed and therefore the calculation of goodwill is provisional. These acquisitions were included within the Air Systems Components group.

The consumer and industrial division of Gates (U.K.) Limited, and the business and assets of Fedco Automotive Components Inc. were sold on May 15, 2002 and December 30, 2002 respectively for a total cash consideration of £33.0 million. Lasco Composites was sold on May 24, 2002 for an adjusted cash consideration of $43.1 million (£29.6 million).

Fiscal 2002

On May 11, 2001 Tomkins sold Smith & Wesson Corp. for consideration of $15.0 million (£10.6 million). The purchaser also paid $20.0 million (£14.1 million) of an outstanding loan of $73.8 million (£52.0 million) due from Smith & Wesson Corp. to Tomkins Corporation. Of the remaining $53.8 million (£37.9 million), $30 million (£21 million) will be repaid on an amortizing basis over the seven years commencing in May 2004 and $23.8 million (£16.8 million) was included in the equity capital acquired by the purchaser. Interest on the outstanding loan balance will continue at nine percent per annum.

Totectors Limited and The Northern Rubber Company Limited were sold on May 25, 2001 and September 11, 2001, respectively, for a total consideration, net of costs, of £23.0 million. Sunvic Controls Limited was sold on July 27, 2001 for total consideration, net of costs, of £1.8 million.

Tomkins acquired American Metal Products Company and the business and assets of Superior Rex on November 13, 2001 and November 19, 2001, respectively, for combined consideration of $45.0 million (£31.2 million). These acquisitions were included within the Air Systems Components group.

On December 17, 2001, Tomkins sold the bellows business of Standard-Thomson Corporation for cash consideration, net of costs, of $1.6 million (£1.1 million).

12

Fiscal 2001

The Company sold the Red Wing Company Inc. on July 14, 2000 for cash consideration, net of costs, of $140.9 million (£93.8 million). The Company completed the sale of the remaining Food Manufacturing business segment on August 31, 2000 for total cash consideration of £1,138.0 million. The loss on disposal totaled £216.8 million, of which £215.0 million had been provided for in fiscal 2000.

The Company sold Murray Inc and Hayter Limited on October 5, 2000 for consideration of $219.3 million (£148.3 million). Of the proceeds, the Company has received $206.3 million (£139.5 million) in cash and $13.0 million (£8.8 million) in a secured subordinated loan note, repayable in 2006. The loss on disposal was £76.2 million.

On November 3, 2000, the Company acquired the business and net assets of Care Free Aluminum Products, Inc. for a cash consideration of $11.2 million (£7.8 million). The Company sold Homer of Redditch Limited, Twiflex Limited and T. A. Knight Limited on May 18, 2000, June 23, 2000 and February 16, 2001, respectively, for total cash consideration, net of costs, of £3.1 million. The loss on disposal totaled £1.8 million.

Fiscal 2000

Tomkins sold Shipham and Company Limited and The Premier Screw and Repetition Company Limited on April 17, 2000 and April 27, 2000, respectively, for total consideration of £2.6 million.

On June 25, 1999, the Company completed the acquisition of ACD Tridon, a manufacturer of fully integrated windshield wiper systems, for CAD$159 million (£68.7 million) including acquired debt of CAD$105 million (£45.2 million) and on August 9, 1999 completed the acquisition of Hayden’s Bakeries Limited, a high quality patisserie and dessert manufacturer, for £5.2 million, including the repayment of £1.7 million debt.

On November 10, 1999, Tomkins acquired the 14 percent of the ordinary shares in Anand Gates (India) Private Limited held by a minority shareholder of that company for cash consideration of £0.8 million.

On December 30, 1999, Tomkins acquired the assets of Hart & Cooley, a leading U.S. producer of grilles, registers and diffusers used in residential and light commercial applications, for cash consideration of $322 million (£197.5 million) including acquired debt. On January 9, 2000, the Company completed the acquisition of Air Diffusion Limited, and the business of Actionair, both of which have a leading position market in the U.K. air handling industry for cash consideration of £8.0 million and acquired debt of £2.8 million.

Recent events

On January 27, 2003, Tomkins sold Milliken Valve Company Inc. for a cash consideration of $7.3 million (£4.5 million), resulting in a small gain on disposal.

Tomkins plc announced on April 30, 2003, the planned transfer of the valve production from Ormskirk, Lancashire to an existing manufacturing facility in Doncaster. The integration of these two facilities will provide a more competitive cost base whilst preserving the market-leading brand of Hattersley Newman Hender.

Tomkins plc announced on June 18, 2003 that, at the expiry on June 17, 2003 of the offer dated May 12, 2003, made by Ontario Inc. (the “Offeror”), an indirect wholly owned subsidiary of Tomkins plc, to acquire all the outstanding common shares of Stackpole Limited, in excess of 97% of the outstanding common shares of Stackpole Limited (on a fully diluted basis) had been deposited to the offer. In addition, the other conditions to the offer had been satisfied or waived and 2023103 Ontario Inc. had instructed its depository to take up and pay for the common shares deposited to the offer. Tomkins plc also announced that the Offeror intends to acquire the remaining common shares of Stackpole Limited not deposited to the offer by exercise of the Offeror’s compulsory acquisition right under the Ontario Business Corporations Act. Shareholders of Stackpole Limited who did not tender to the offer will be offered Cdn $33.25 per common share, the same price that was offered to shareholders under the original offer.

13

B. Business overview

Segment contribution to net sales and operating income

The contribution of each segment to the Company’s net sales and operating income under U.K. GAAP is set out below.

| | | Transition Period Ended

| | Fiscal Year Ended

|

By Business Segment

| | December 31

2002 (245 days)

| | April 30, 2002 (365 days)

| | April 30, 2001 (366 days)

| | April 29, 2000 (364 days)

|

| | | In £ millions |

| | | | | | | | | |

Industrial & Automotive | | | | | | | | |

Net Sales | | 1,263.9 | | 1,985.9 | | 1,968.3 | | 1,921.3 |

Operating Income | | 91.6 | | 146.1 | | 190.2 | | 198.2 |

Air Systems Components | | | | | | | | |

Net Sales | | 325.7 | | 516.4 | | 487.9 | | 321.6 |

Operating Income | | 20.0 | | 45.2 | | 47.7 | | 39.9 |

Engineered & Construction Products | | | | | | | | |

Net Sales | | 507.6 | | 871.5 | | 878.9 | | 918.8 |

Operating Income | | 46.7 | | 77.4 | | 85.3 | | 119.7 |

Food Manufacturing | | | | | | | | |

Net Sales | | — | | — | | 562.1 | | 1,898.6 |

Operating Income | | — | | — | | 25.5 | | 160.5 |

Professional, Garden & Leisure Products | | | | | | | | |

Net Sales | | — | | — | | 208.3 | | 580.1 |

Operating (Loss)/Income | | — | | — | | (14.3) | | 22.4 |

Central Costs (1) | | | | | | | | |

Net Sales | | — | | — | | — | | — |

Operating Loss | | (15.2) | | (12.6) | | (24.0) | | (21.3) |

Total | | | | | | | | |

Net Sales | | 2,097.2 | | 3,373.8 | | 4,105.5 | | 5,640.4 |

Operating Income | | 143.1 | | 256.1 | | 310.4 | | 519.4 |

| | | | | | | | |

By Geographic Region

| | Net Sales

| | % of Total

| | Net Sales

| | % of Total

| | Net Sales

| | % of Total

| | Net Sales

| | % of Total

|

United States | | 1,470.1 | | 70.1 | | 2,380.5 | | 70.6 | | 2,498.1 | | 60.9 | | 2,884.3 | | 51.1 |

United Kingdom | | 125.6 | | 6.0 | | 237.7 | | 7.0 | | 787.4 | | 19.2 | | 1,908.6 | | 33.8 |

Rest of Europe | | 191.1 | | 9.1 | | 290.3 | | 8.6 | | 309.8 | | 7.5 | | 341.0 | | 6.1 |

Rest of World | | 310.4 | | 14.8 | | 465.3 | | 13.8 | | 510.2 | | 12.4 | �� | 506.5 | | 9.0 |

| | |

| |

| |

| |

| |

| |

| |

| |

|

| | | 2,097.2 | | 100.0 | | 3,373.8 | | 100.0 | | 4,105.5 | | 100.0 | | 5,640.4 | | 100.0 |

| (1) | | Includes the cost of the corporate center, which carries out corporate functions for the Company as a whole. |

Tomkins exited the Food Manufacturing and Professional, Garden and Leisure Products segments during the year ended April 30, 2001 with the disposal of the Red Wing Company Inc. on July, 14, 2000 and the sale if the remainder of the Food Manufacturing business segment on August 31, 2000. The Professional, Garden and Leisure Products segment was disposed of on October 5, 2000.

Notes 5(a), 5(b) and 5(c) of the consolidated financial statements provide more detailed business segment and geographic information concerning the Company’s operations.

14

Industrial & Automotive

Business unit

| | Proportion of

net sales for

the eight

months

ended

December 31,

2002

| | Products

| | Primary markets

|

Power

Transmission | | 41% | | • Synchronous belts, V-belts, multi V-ribbed belts, accessory drive systems, synchronous drive systems | | • Automotive original equipment and aftermarket (timing and accessory drives); industrial original equipment and aftermarket (outdoor power equipment, office machines etc.) |

| | | |

Fluid Power | | 17% | | • High pressure fluid power connectors, hose and assemblies • Industrial transfer and automotive coolant hoses | | • Mobile original equipment (construction, agriculture, etc.); industrial aftermarket (mobile and MRO); automotive original equipment and aftermarket (coolant hose) |

| | | |

Wiper

Systems | | 15% | | • Wiper systems and components | | • Automotive original equipment and aftermarket |

| | | |

Fluid Systems | | 12% | | • Fuel products • Valve products • Thermostats • Automotive hose | | • Automotive and industrial—fuel valves/caps and radiator caps for cars and trucks; curved hose for mobile markets |

| | | |

Other | | 15% | | • Automotive accessories, radiator cores • Clamps and formed fiber | | • Automotive and industrial aftermarkets |

The Industrial & Automotive segment has corporate offices in Denver, Colorado, Rochester Hills, Michigan and Dayton, Ohio. It is one of the world’s largest suppliers of automotive parts, components and systems, serving a wide variety of industries, including the industrial and automotive original equipment and replacement markets, transportation, agricultural, mining, forestry, construction, office equipment, computer, and the food processing and handling markets.

In total, the segment operates 67 factories and 33 distribution centers in 21 countries. It is the only non-tire polymer-based products company with development centers and manufacturing operations in North America, Europe, Asia and South America. No other belt and hose company has significant operations in all of the world’s major automotive development centers.

The segment operates 36 manufacturing plants in Canada and the U.S., and a further 12 in Latin America. European operations include 14 manufacturing plants and 8 distribution centers, which provide customers with Tomkins products and technology. There are also operations in Asia and the Pacific Rim including Singapore, Australia and India, with joint venture manufacturing facilities in South Korea, Japan, China, and Thailand.

The Industrial & Automotive group operates five global strategic enterprise groups: power transmission, fluid power, wiper systems, fluid systems and other aftermarket products. These groups include divisions integrated from the acquisitions of Gates, Stant, Trico, Tridon and Schrader. Together, these operations employed on average 22,637 people around the world in the eight month period ended December 31, 2002. Products are sold directly to industrial and automotive original equipment manufacturers and through a network of approximately 150,000 distributors, dealers and jobbers worldwide, to the industrial and automotive replacement markets.

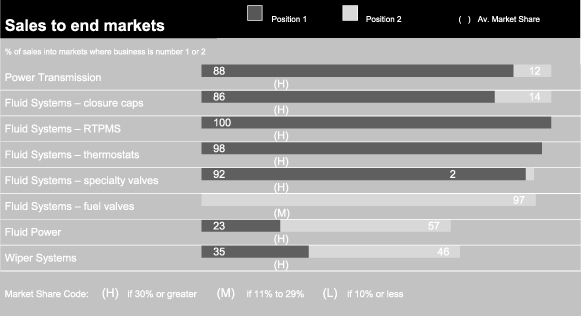

Power Transmission

The Power Transmission group produces a comprehensive global product line ranging from synchronous belt and accessory belt drive systems for automotive applications to heavy-duty industrial belt drives. Its eight major product lines include V-belts, multi V-ribbed belts, synchronous belts, sheaves/sprockets, pulleys, tensioners, idlers, and crankshaft dampers.

Power Transmission is globally integrated in order to standardize products, process technology, and to maximize resource utilization across the group. Core technology centers (“CTCs”) associated with each product line are responsible for global product development. Manufacturing development centers are responsible for the commercialization process and for implementing best practices throughout the group’s facilities in their respective regions for a particular product line. Two global research centers are responsible for identifying new technologies and locating materials to meet the CTCs’ requirements. There are three Automotive Technical Centers (“ATCs”) located at Aachen in Germany, Rochester Hills in the USA and Nara in Japan, which lead

15

product and systems design and engineering. The ATCs also perform customer specific component or system testing.

Power Transmission supports and supplies customers on a regional and global basis. Regional management in the Americas, Europe and Asia work to leverage the group’s market strengths from one area to another utilizing common processes and global product lines.

Fluid Power

The Fluid Power group is a leading manufacturer of high-pressure connectors, hoses and assemblies for mobile equipment and heavy industrial applications. The group also produces a wide range of Industrial hoses for the transfer of liquids, gases and solids (petroleum, chemical, food/beverage materials etc.). In addition, the group produces a complete range of Automotive cooling system hoses.

The group has major strength in the North American market, and also has a significant presence in European and Brazilian markets. The existing Asian presence is being augmented with expansion plans being implemented over the next 24 to 36 months.

The Fluid Power group is focused on delivering value added design, engineering and logistics support with a complete range of fluid power connectors, hoses and assemblies to mobile equipment manufacturers globally.

Wiper Systems

The Wiper Systems group comprises Trico and Tridon operations and is one of the world’s largest manufacturers of automotive windshield wiping systems and systems components, producing arms, blades, linkage mechanisms, modules, motors and electronic components. Modular systems combine the linkages, arms, blades, motors and electronic circuitry produced by the Wiper Systems group with plastic housings, manifold assemblies and other components purchased from supplier partners. Systems are sold directly to OEMs as ready-to-install modules. Wiper blades are produced in sizes ranging from 10 to 40 inches and over 50 different types of wiper arms are manufactured. Wiper blades and arms are sold for use as original equipment and in the aftermarket under the “Trico,” “Roberk,” and “Tridon” brand names. Over 25 different types of linkages are produced and sold for use as original equipment.

Fluid Systems

The Automotive Fluid Systems group, made up of divisions acquired as Stant Corporation and Schrader-Bridgeport International, is a leading designer, manufacturer and distributor of a broad range of automotive fluid conveyance and fluid management components and modules. This includes the latest technology in tire pressure monitoring components and fuel vapor management valves. Products are sold primarily for use as original equipment by manufacturers of cars and trucks and in the automotive replacement market as repair parts and accessories. Major customers include DaimlerChrysler, Ford, General Motors, Nissan, Renault and PSA, as well as a number of other major international OEMs. Products from Tomkins Automotive Fluid Systems group are also sold in a vast majority of wholesale and retail automotive parts and distribution outlets in North America, Europe and Latin America including the service departments of OEM dealers.

Through Schrader Electronics, the Automotive Fluid Systems group is the technology and market leader in Remote Tire Pressure Monitoring Systems (“RTPMS”), a driver information and passenger security system that is economically and ergonomically integrated into vehicle electronic information systems. The company also designs, manufactures and markets a variety of fuel vapor management valves and fuel, oil and radiator closure caps at its Stant Manufacturing Division. Standard-Thomson is the leading manufacturer of engine thermostats used in automotive cooling systems. Schrader-Bridgeport International provides a wide range of tire valve, hardware and specialty valve products worldwide. RTPMS, tire, and specialty valve products are sold under the “Schrader-Bridgeport” and “Schrader Electronics” trademarks. Closure cap and fuel management valve products are sold under the “Stant,” “Lev-R-Vent” and “Pre-Vent” trademarks. Engine thermostats are sold under the “Stant,” “Weir-stat,” and “Superstat” brand names. Many of these products are also sold to various private label customers bearing their unique brand names.

Other

The Aftermarket group integrates the sales, marketing, distribution and manufacture of products destined for both the Industrial and Automotive original equipment and Aftermarket and sold under the Gates, Stant, Trico, Tridon, Ideal, Schrader and numerous private brands. It designs and sells aftermarket automotive tools and fittings, power steering hose, lubrication equipment, stainless and carbon steel hose clamps for both original equipment and parts applications.

The Aftermarket group also manufactures and distributes specialist components for the automotive industry. Schrader-brand products include precision control valving and associated fluid conveyance and control modules for vehicle fluid system applications in fuel delivery, emission control, engine management, brake, steering, power transmission, coolant, air conditioning, windshield washing, PVC air hose, and ride control. Schrader, a leading brand of wheel valving for cars, medium- and heavy-duty trucks, agricultural vehicles and construction

16