SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED: DECEMBER 30, 2006

COMMISSION FILE NUMBER: 0-17140

Tomkins plc

(Exact name of Registrant as specified in its charter)

England

(Jurisdiction of incorporation or organization)

East Putney House, 84 Upper Richmond Road

London SW15 2ST, United Kingdom

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange |

| Ordinary Shares, nominal value 5p per share | | New York Stock Exchange * |

| |

American Depositary Shares, each of which represents four Ordinary Shares | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act

None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as at the close of the period covered by the Annual Report:

| | |

Ordinary Shares, nominal value 5p per share | | 858,209,522 |

Convertible Cumulative Preference Shares, nominal value $50 per share | | 2,625,138 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which financial statement item the Registrant has elected to follow: Item 17 ¨ Item 18 x

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

| * | Not for trading, but only in connection with the registration of American Depositary Shares representing such Ordinary Shares |

TABLE OF CONTENTS

1

In this Annual Report (the “Annual Report”) on Form 20-F for the fiscal year ended December 30, 2006 (“fiscal 2006”), all references to “Tomkins”, the “Tomkins Group”, the “Group”, the “Company”, “we”, “us” and “our” include Tomkins plc and its consolidated subsidiaries, unless the context otherwise requires.

The consolidated financial statements of Tomkins plc appearing in this Annual Report are presented in US dollars (“$”) and are prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”).

In this Annual Report, references to “US dollars”, “$”, “cents” and “c” are to United States currency, references to “pounds sterling”, “£”, “pence” and “p” are to British currency, references to “Canadian dollars” are to Canadian currency, and “Euros” are to the currency of certain member states of the European Union.

Special Note Regarding Forward-Looking Statements

Pursuant to the meaning of forward-looking statements in Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), this Annual Report contains assumptions, anticipations, expectations and forecasts concerning the Company’s future business plans, products, services, financial results, performance, future events and information relevant to our business, industries and operating environments. When used in this document, the words “anticipate”, “believe”, “estimate”, “assume”, “could”, “should”, “expect” and similar expressions, as they relate to the Company or its management, are intended to identify forward-looking statements. Such statements reflect the current views of management with respect to future events and are subject to certain risks, uncertainties and assumptions. The forward-looking statements contained herein represent a good-faith assessment of our future performance for which we believe there is a reasonable basis. Many factors could cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements, including, among others, adverse changes or uncertainties in general economic conditions in the markets we serve, regulatory developments adverse to us or difficulties we may face in maintaining necessary licenses or other governmental approvals, changes in the competitive position or introduction of new competitors or new competitive products, lack of acceptance of new products or services by the Company’s targeted customers, changes in business strategy, any management level or large-scale employee turnover, any major disruption in production at our key facilities, adverse changes in foreign exchange rates, and acts of terrorism or war, and other risks described in Item 3D “Key Information – Risk factors”. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein as anticipated, believed, estimated or expected.

These forward-looking statements represent our view only as of the date they are made, and we disclaim any obligation to update forward-looking statements contained herein, except as may be otherwise required by law.

2

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

3

Item 3. Key Information

A. Selected financial data

The selected financial data set out below as at and for the fiscal years ended December 30, 2006, December 31, 2005 (“fiscal 2005”), January 1, 2005 (“fiscal 2004”), January 3, 2004 (“fiscal 2003”), the eight-month transition period ended December 31, 2002 and for the fiscal year ended April 30, 2002 has been derived from the audited consolidated financial statements of the Company. The audited consolidated financial statements for fiscal 2006 have been included as Item 18 to this Form 20-F. The selected financial data set forth below should be read in conjunction with, and are qualified in their entirety by reference to, such consolidated financial statements and Notes thereto and Item 5 “Operating and Financial Review and Prospects”.

Consolidated income statement data

| | | | | | | | | | | | | | | | | | |

| | | Fiscal Year Ended | |

| | | December 30,

2006(1) (364 days) | | | December 31,

2005(2) (3) (364 days) | | | January 1, 2005 (364 days) | | | January 3,

2004(4) (368 days) | | | December 31,

2002(5) (245 days) | | | April 30, 2002(6) (365 days) | |

| | | $ million | | | $ million | | | $ million | | | $ million | | | $ million | | | $ million | |

Net sales | | 5,418.7 | | | 5,108.9 | | | 4,688.0 | | | 4,210.9 | | | 2,593.3 | | | 3,794.5 | |

Operating income from continuing operations | | 439.2 | | | 483.6 | | | 457.8 | | | 372.2 | | | 216.8 | | | 328.9 | |

Income from continuing operations before cumulative effect of change in accounting principle | | 414.2 | | | 318.3 | | | 363.5 | | | 480.8 | | | 186.9 | | | 209.6 | |

(Loss)/income from discontinued operations, net of taxes | | (202.2 | ) | | (6.9 | ) | | 3.2 | | | (103.7 | ) | | (20.0 | ) | | (0.8 | ) |

| | | | | | | | | | | | | | | | | | |

Income from operations | | 212.0 | | | 311.4 | | | 366.7 | | | 377.1 | | | 166.9 | | | 208.8 | |

| | | | | | | | | | | | | | | | | | |

Gain/(loss) on disposal of discontinued operations, net of taxes | | 39.7 | | | 1.6 | | | 11.0 | | | 49.6 | | | (0.8 | ) | | 3.2 | |

Cumulative effect of change in accounting principle, net of taxes | | — | | | — | | | — | | | — | | | (47.3 | ) | | 2.6 | |

| | | | | | | | | | | | | | | | | | |

Net income | | 251.7 | | | 313.0 | | | 377.7 | | | 426.7 | | | 118.8 | | | 214.6 | |

| | | | | | | | | | | | | | | | | | |

Net income per common share (7) | | | | | | | | | | | | | | | | | | |

Basic | | | | | | | | | | | | | | | | | | |

Income from continuing operations before cumulative effect of change in accounting principle | | 48.19 | c | | 37.49 | c | | 43.47 | c | | 58.51 | c | | 19.37 | c | | 19.82 | c |

(Loss)/income from discontinued operations, net of taxes | | (24.10 | )c | | (0.89 | )c | | 0.42 | c | | (13.45 | )c | | (2.59 | )c | | (0.10 | )c |

Gain/(loss) on disposal of discontinued operations, net of taxes | | 4.73 | c | | 0.20 | c | | 1.42 | c | | 6.43 | c | | (0.11 | )c | | 0.41 | c |

| | | | | | | | | | | | | | | | | | |

Income before cumulative effect of change in accounting principle | | 28.82 | c | | 36.80 | c | | 45.31 | c | | 51.49 | c | | 16.67 | c | | 20.13 | c |

Cumulative effect of change in accounting principle, net of taxes | | — | | | — | | | — | | | — | | | (6.14 | )c | | 0.34 | c |

| | | | | | | | | | | | | | | | | | |

Net income | | 28.82 | c | | 36.80 | c | | 45.31 | c | | 51.49 | c | | 10.53 | c | | 20.47 | c |

| | | | | | | | | | | | | | | | | | |

Diluted | | | | | | | | | | | | | | | | | | |

Income from continuing operations before cumulative effect of change in accounting principle | | 46.92 | c | | 36.33 | c | | 41.43 | c | | 50.40 | c | | 18.75 | c | | 19.81 | c |

(Loss)/income from discontinued operations, net of taxes | | (22.90 | )c | | (0.79 | )c | | 0.36 | c | | (10.87 | )c | | (2.01 | )c | | (0.10 | )c |

Gain/(loss) on disposal of discontinued operations, net of taxes | | 4.49 | c | | 0.18 | c | | 1.26 | c | | 5.20 | c | | (0.07 | )c | | 0.41 | c |

| | | | | | | | | | | | | | | | | | |

Income before cumulative effect of change in accounting principle | | 28.51 | c | | 35.72 | c | | 43.05 | c | | 44.73 | c | | 16.67 | c | | 20.12 | c |

Cumulative effect of change in accounting principle, net of taxes | | — | | | — | | | — | | | — | | | (4.75 | )c | | 0.34 | c |

| | | | | | | | | | | | | | | | | | |

Net income | | 28.51 | c | | 35.72 | c | | 43.05 | c | | 44.73 | c | | 11.92 | c | | 20.46 | c |

| | | | | | | | | | | | | | | | | | |

Net income per American Depository Share(8) | | | | | | | | | | | | | | | | | | |

Basic | | 115.28 | c | | 147.20 | c | | 181.24 | c | | 205.96 | c | | 42.12 | c | | 81.88 | c |

| | | | | | | | | | | | | | | | | | |

Diluted(9) | | 114.04 | c | | 142.88 | c | | 172.20 | c | | 178.92 | c | | 47.68 | c | | 81.84 | c |

| | | | | | | | | | | | | | | | | | |

Average number of Ordinary Shares outstanding (‘000s) | | | | | | | | | | | | | | | | | | |

Basic | | 838,894 | | | 771,427 | | | 770,717 | | | 771,037 | | | 770,927 | | | 773,464 | |

| | | | | | | | | | | | | | | | | | |

Diluted(9) | | 882,807 | | | 876,141 | | | 877,299 | | | 953,989 | | | 996,607 | | | 774,017 | |

| | | | | | | | | | | | | | | | | | |

(1) – (9) Refer to notes on page 5.

4

Consolidated balance sheet data

| | | | | | | | | | | | |

| | | As at |

| | | December 30,

2006(10) | | December 31,

2005 | | January 1, 2005 | | January 3, 2004 | | December 31,

2002 | | April 30, 2002 |

| | | $ million | | $ million | | $ million | | $ million | | $ million | | $ million |

Total assets | | 5,780.4 | | 5,783.3 | | 5,736.0 | | 5,462.6 | | 5,202.6 | | 5,250.8 |

Ordinary share capital | | 62.9 | | 55.7 | | 55.6 | | 55.5 | | 55.5 | | 55.4 |

Shareholders’ equity | | 3,087.3 | | 3,034.4 | | 2,923.1 | | 2,697.0 | | 2,412.5 | | 2,555.7 |

Net assets | | 3,187.0 | | 3,117.7 | | 3,003.9 | | 2,756.6 | | 3,095.7 | | 3,227.2 |

(1) | The Group acquired Selkirk Americas L.P. on March 1, 2006, 60% of Gates Winhere LLC on July 19, 2006, ENZED Fleximak Ltd on August 4, 2006, Eastern Sheet Metal on October 19, 2006, and Heat-Fab Inc on October 26, 2006. |

(2) | The Group acquired Milcor Inc on January 27, 2005, L.E. Technologies on March 18, 2005, Eifeler Maschinenbau GmbH on July 1, 2005, and NRG Industries Inc. on September 23, 2005. |

(3) | The Group adopted SFAS123(R) using the modified prospective method with an effective date of January 2, 2005. |

(4) | The Group acquired Stackpole Limited on June 18, 2003. |

(5) | Change in accounting principle relates to the Group’s transitional adjustment in respect of the adoption of SFAS142 on May 1, 2002. |

(6) | Change in accounting principle relates to the Group’s transitional adjustment in respect of the adoption of SFAS133 on May 1, 2001. |

(7) | Net income per common share represents net income after deducting dividends payable on preferred shares. |

(8) | Net income and dividend per ADS is calculated per Ordinary Share multiplied by four, as discussed in Item 9C “Markets.” |

(9) | In the fiscal year ended April 30, 2002, the preferred shares were anti-dilutive and were therefore excluded from the calculation. |

(10) | The Group adopted the recognition provisions of SFAS158 with an effective date of December 30, 2006. |

Dividends

The Company has paid cash dividends on its Ordinary Shares, nominal value 5p per share (“Ordinary Shares”), in respect of every fiscal year since being first listed on the London Stock Exchange Limited (the “London Stock Exchange”) in 1950.

Dividends are paid to shareholders as of record dates that are fixed after consultation between the Company and the London Stock Exchange. For fiscal 2006, an interim dividend was declared by the Board of Directors (the “Board”) in August 2006 and was paid in November 2006. A final dividend was recommended by the Board following the end of fiscal 2006 and will, subject to approval by the shareholders at the Company’s annual general meeting on June 13, 2007, be paid on June 27, 2007.

The table below sets forth the amounts of interim, final and total dividends paid in respect of each fiscal year indicated and the eight month transition period ended December 31, 2002. The amounts are shown in US cents per Ordinary Share and in US cents per American Depositary Share (“ADS”) - each ADS represents four Ordinary Shares. The interim and final dividends below have been translated from pounds sterling into US dollars at the noon buying rate on each of the respective payment dates.

| | | | | | | | | | | | | | | | | | |

Fiscal Year Ended | | Cents per Ordinary Share(1) | | Cents per ADS(1) |

| | | Interim | | Second

Interim | | | Final | | Total | | Interim | | Second

Interim | | | Final | | Total |

April 30, 2002 | | 6.58 | | — | | | 11.58 | | 18.16 | | 26.33 | | — | | | 46.30 | | 72.63 |

May 1, 2002 – December 31, 2002(2) | | 7.13 | | 5.27 | (2) | | — | | 12.40 | | 28.52 | | 21.08 | (2) | | — | | 49.60 |

January 3, 2004 | | 7.70 | | — | | | 13.12 | | 20.82 | | 30.80 | | — | | | 52.49 | | 83.29 |

January 1, 2005 | | 8.96 | | — | | | 14.15 | | 23.11 | | 35.84 | | — | | | 56.60 | | 92.44 |

December 31, 2005 | | 8.80 | | — | | | 15.29 | | 24.09 | | 35.20 | | — | | | 61.16 | | 96.36 |

December 30, 2006(3) | | 10.14 | | — | | | 16.99 | | 27.13 | | 40.56 | | — | | | 67.96 | | 108.52 |

(1) | Translated at the noon buying rate on the date the dividend was paid (or, if not yet paid, translated at the noon buying rate on the convenience date). |

(2) | The Company’s fiscal year-end changed from April 30 to December 31 with effect from December 31, 2002. The resulting eight-month accounting period ended December 31, 2002 represented two-thirds of a normal twelve-month accounting period. In accordance with market practice in these circumstances, the Board elected to declare two interim dividends in lieu of an interim and a final dividend. |

(3) | The fiscal 2006 final dividend is subject to approval by the shareholders at the Company’s Annual General Meeting. |

The Company expects to continue to pay dividends in the future. The total amounts of future dividends will be determined by the Board and will depend on the Company’s results of operations, cash flow, financial and economic conditions and other factors. Management expects dividend payments to follow the same pattern in future years and anticipates the weighting of these payments to be approximately 40 percent for the interim dividend and 60 percent for the final dividend. Cash dividends are paid by the Company in pounds sterling, and fluctuations in the exchange rate between pounds sterling and US dollars will affect the US dollar amounts received by holders of American Depository Receipts (“ADRs”) upon conversion by The Bank of New York (the “Depositary”) of such dividends. Moreover, fluctuations in the exchange rates between the pound sterling and the US dollar will affect the US dollar equivalents of the pound sterling price of the Ordinary Shares on the London Stock Exchange and, as a result, are likely to affect the market prices of the ADSs which are quoted in US dollars. For a discussion of the historic effects of exchange rate fluctuations on the Company’s financial condition and results of operations, see Item 11 “Quantitative and Qualitative Disclosures about Market Risk” and Note 17 to the consolidated financial statements.

B. Capitalization and indebtedness

Not applicable.

C. Reasons for the offer and use of proceeds

Not applicable.

5

D. Risk factors

The Group’s business is affected by a number of risk factors, not all of which are in Tomkins’ control. This section highlights specific areas where Tomkins is particularly sensitive to business risk. The Group’s financial condition or results of operations could be materially and adversely affected by any of these risks. Additional risks not currently known to management, or risks that management currently regards as immaterial could also have a material adverse effect on the Group’s financial condition or results of operations.

As a part of the Performance Management Framework of the Group, each business considers strategic, operational, commercial and financial risks and identifies risk mitigation actions. Business unit managers maintain Risk Profiles, including mitigation strategies, which are updated at least annually. Periodically, each business unit reviews the risk profile. Management’s internal Risk and Assurance Services function performs a periodic risk assessment that is reviewed by senior management, who develop plans to mitigate significant identified risks. The findings and plans are presented to the Audit Committee. This framework provides a comprehensive list of key Group risk and control processes and allows the Board to assess the impact of those risks and the effectiveness of those processes. The Group has categorized its risks as those relating to:

| • | | the markets within which the Group operates; |

| • | | the competitive position of the Group and its businesses; and |

| • | | the financial position of the Group. |

Risk can be considered either as downside risk (the risk that something can go wrong and result in a financial loss or financial exposure for the Group) or as volatility risk (the risk associated with uncertainty, meaning there may be an opportunity for financial gain as well as potential for loss).

Risks relating to the markets within which the Group operates

There are a number of risks in the markets in which the Group operates which could have a material adverse effect on the Group’s business, financial condition or results of operations:

Cyclical nature of markets – The Group’s operating results depend on the conditions of the markets in which it operates, particularly the automotive and construction markets, where demand is ultimately affected by consumer spending and consumer preferences. Trends in these markets can be difficult to predict. In fiscal 2006, approximately 18 percent of the Group’s sales were to the automotive original equipment market. Because the production volumes of automotive original equipment manufacturers (“OEMs”) depend on general economic conditions and consumer spending levels, automotive production and sales can be highly cyclical. The volume of automotive production in the United States, the Group’s principal geographic segment, has fluctuated, sometimes significantly, from year to year, and such fluctuations give rise to fluctuations in the demand for the Group’s products. In fiscal 2006, approximately 29 percent of the Group’s sales were to the residential construction and non-residential construction markets in the United States. The construction industry in the United States slowed in the second half of 2006 and is expected to continue facing challenges in 2007 with the National Association of Home Builders forecasting that housing starts in 2007 will be approximately 15 percent lower in the United States than they were in 2006. The timing of a recovery in US residential housing now seems unlikely to occur until sometime in 2008, with this end-market showing greater weakness in the first quarter than commentators had predicted.

Loss of market share by US vehicle manufacturers – In recent years, General Motors, Ford and DaimlerChrysler (the “Detroit Three”) have seen a decline in their market share for vehicle sales, particularly in North America, with Asian automobile manufacturers increasing their market share. The automotive industry is characterized by overcapacity and fierce competition. In North America it is also affected by significant pension and healthcare liabilities. North American automobile manufacturers have recently announced production cuts for a number of platforms. Because a portion of the Group’s business is derived from the Detroit Three, if this trend of Detroit Three market share loss continues and the Group’s share of business with other vehicle manufacturers does not increase, the Group’s business could be materially and adversely affected.

Improvement in vehicle component life – The greater quality, performance and reliability of the components that the Group manufactures improves service life and could affect demand for the products the Group sells through the aftermarket business segment.

Regulatory environment – The Group is subject to a variety of environmental regulations in the industries in which it operates, particularly relating to waste water discharges, air emissions, solid waste management and hazardous chemical disposal. Management cannot give assurance that the Group has been or will be at all times in complete compliance with all of these requirements, or that it will not incur material costs or liabilities in connection with these requirements.

Operations in foreign and emerging markets – The Group operates in a number of geographic regions of the world, including emerging markets, and derives approximately 37 percent of its sales from markets outside the United States. Operations in foreign and emerging markets may subject the Group to the risks inherent in operating in such markets, such as economic and political instability, other disruption of markets, restrictive laws and actions of certain governments and difficulty in obtaining distribution and logistical resources. Should the Group fail to define and adequately execute its strategy in these markets effectively, it may not capitalize on growth opportunities that exist in these markets.

Risks relating to the competitive position of the Group and its businesses

There are a number of risks to the Group’s competitive position that could have a material adverse effect on its business, financial condition or results of operations.

Industry consolidation may result in more powerful competitors and fewer customers– Some of the Group’s customers and some of its competitors in a number of markets, particularly in the automotive aftermarket, and to a lesser extent in the markets of the Air Systems Components group, are consolidating to achieve greater scale or market share. Such changes could affect the negotiating leverage of the Group’s customers and their relationship with the Group. As the Group’s customers become larger and more concentrated, they could exert pricing pressure on all suppliers, including the Group, which may materially and adversely affect the Group’s margins.

6

Significance of revenues generated from the Detroit Three– Approximately 16 percent of the Industrial and Automotive group’s sales in fiscal 2006 came from direct sales to the Detroit Three. These customers have strong purchasing power as a result of high market concentration and the Group’s reliance on them subjects it to potential pressures on its sale prices that may reduce the Group’s profitability.

Price reductions by automotive customers – Approximately 18 percent of the Group’s sales are to OEMs. It is normal practice for such customers to seek reductions in their costs from their suppliers over the duration of any committed supply arrangement. To meet such requests for price reductions whilst maintaining profit margins, the Company has had to achieve corresponding cost savings in the business by strategic sourcing of raw materials and by improving production and manufacturing efficiencies. The Group may be unable to achieve such cost reductions in the future, which could result in lower margins or the loss of customers.

Increased competition from low-cost producers – The Group increasingly faces competition from low-cost sources in the developing economies of the world, leading to potential loss of market share and/or reduced margins.

Increasing raw material and energy costs– Steel, aluminum, oil based resins and energy are a significant part of the Group’s costs. If costs of these raw materials and energy increase, the Group may be unable to sustain margins if it is unable to pass such increases on to its customers. During fiscal 2006, the price of certain base metals more than doubled which had a particular adverse impact on the Wiper Systems and Fluid Systems businesses, as we were not able to increase prices to offset the increase in costs.

Reliance on certain raw materials and suppliers of key components – The Group’s productive processes require that arrangements are in place to ensure continuity of supply of certain raw materials and components. Disruption due to lack of availability of raw material and energy supplies may adversely affect our ability to service our customers and may erode our margins.

Dependence on strong relationships with manufacturers’ representatives, distributors and wholesalers–Deterioration in the relationships with manufacturers’ representatives, distributors and wholesalers or a change in the Group’s products’ distribution channels could materially and adversely affect the Group’s sales.

Product liability claims due to the nature of the Group’s products – The Group faces an inherent business risk of exposure to product liability claims. In the event that a failure of a product results in, or is alleged to result in, bodily injury, property damage or consequential loss, we could face significant liability.

Technological changes–The markets for the Group’s products and services are characterized by evolving industry standards and changing technology which may lead to commoditization of its products, allowing for low switching costs, increased pricing pressures and, potentially, loss of customers and reduced margins. Continual development of advanced technologies for new products and product enhancements is an important way in which the Group maintains acceptable pricing levels. If the Group’s core products are displaced or made obsolete, the Group may lose customers, which would have an adverse effect on its results of operations.

Dependence on investment and divestment decisions–If the Group were to make inappropriate investment and divestment decisions or fail to implement major projects, such as systems development, product development or plant closures, there may be destruction of value, returns below expectations and /or business interruption.

Dependence on human resources strategy–If the Group were to lack a human resources strategy or was to execute that strategy ineffectively there may be an adverse impact on the achievement of management’s long-term strategic objectives.

Dependence on the continued operation of the Group’s manufacturing facilities – While the Group is not heavily dependent on any single manufacturing facility, major disruptions at a number of the Group’s manufacturing facilities, due to labor unrest, natural disasters or mechanical failure of the Group’s facilities, could result in significant interruption of the Group’s business and potential loss of customers and sales.

Capacity, reliability and security of the Group’s computer hardware, software and telecommunications infrastructure – The Group currently secures its networks by means of back up, hardware, virus protection and other measures, but any systems interruption could lead to a reduction in performance or loss of services. The Group’s systems are vulnerable to damage or interruption caused by human error, network failure, natural disasters, sabotage, computer viruses and similar disruptive events. A breach of network security could result in loss of customers and reduced revenues.

Intellectual property rights – The Group’s proprietary technology is protected by patents and trade secrets which could be at risk if:

| | • | | competitors are able to develop similar technology independently; |

| | • | | patent applications are not approved; |

| | • | | steps taken to prevent misappropriation or infringement of intellectual property are not successful; or |

| | • | | the Group does not adequately protect its intellectual property. |

Work stoppages or other labor issues at our facilities or at our customers’ facilities – Some of the Group’s employees are members of labor unions. While the Group considers its relations with its employees and labor unions to be good, if the Group is unable to maintain these relations, there may be disputes and work stoppages that could affect production of the Group’s products. Some of the Group’s customers, particularly in the automotive industry, have highly unionized workforces and have been involved in major disputes in the past. If any of our customers experiences a work stoppage, that customer may halt or limit the purchase of the Group’s products which could, in turn, force the Group to shut down its own production facilities supplying these products.

Financial Risks

Certain financial risks could have a material adverse effect on the Group’s business, financial condition or results of operations.

Pension plans – The Group operates both defined benefit and defined contribution pension plans, the majority of which are in the United States and the United Kingdom. The schemes were in deficit by $259.8 million as at December 30, 2006. Deterioration in pension plan asset prices or changes to long-term interest rates could lead to an increase in the deficit or give rise to an additional funding requirement.

7

Cash flow from subsidiaries – The Company is a holding company with no independent operations or significant assets other than investments in, and advances to, subsidiaries. Accordingly, it depends upon the receipt of sufficient funds from its subsidiaries to meet its obligations, including its ability to repay any amounts it borrows under the Euro Medium Term Note (“EMTN”) Program or to pay its dividends. The ability of the Group to access that cash flow may be limited in some circumstances.

Health care and workers’ compensation–Healthcare and workers’ compensation are provided by certain subsidiaries to current and former employees in the United States. Healthcare costs in the United States are increasing at a faster rate than general cost inflation and these cost increases have to be absorbed in the business.

Tax cash outflows–Tomkins operates within multiple tax jurisdictions and is subject to audit in those jurisdictions. These audits can involve complex issues, which may require an extended period of time for resolution. Although provision has been made for such issues the ultimate resolution may result in additional tax charges and cash outflows.

Funding growth – The Group may require capital to expand its business, implement its strategic initiatives and remain competitive. At present, the Group’s established sources of funding are through equity, corporate bond markets (through the EMTN Program), bank debt and cash flow from operations. Management believes that the sources of funding currently available will be sufficient to fund the Group’s operations. If management’s plans or assumptions regarding the funding requirements change, the Group may need to seek other sources of financing, such as additional lines of credit with commercial banks or vendors or public financing, or to renegotiate existing bank facilities. It is possible that additional funding may not be available or may be available but not on commercially acceptable terms.

Bondholders’ rights – The Group has a EMTN Program under which Tomkins may issue bonds. The Group’s bondholders have the right to require the Group to redeem its outstanding bonds, at par, in the event of a change of control of Tomkins plc and also in the event that the Group’s credit rating falls below investment grade as a result of the Group making either acquisitions or disposals that comprise more than 25 percent of the Group’s operating profit in a twelve calendar month period. The Group may not have sufficient funds to repurchase such notes as required.

Fluctuations in currency exchange rates – The Group has manufacturing facilities in, and sells products to customers in, many countries worldwide. The principal currencies in which the Group trades are US dollars, Canadian dollars, Euros and pounds sterling. Currency exchange movements can give rise to the following risks:

| | • | | Transaction risk –arises where sales or purchases are denominated in foreign currencies and exchange rates can change between entering into a purchase or sale commitment and completing the transaction; |

| | • | | Translation risk – arises where the currency in which the results of an entity are reported differs from the underlying currency in which business is transacted; and |

| | • | | Economic risk – arises where the manufacturing cost base of a business is denominated in a currency different from the currency of the market into which the products are sold. |

Risks related to the securities market and ownership of ADSs and registered shares

Holders of ADSs may be restricted in their ability to exercise voting rights -Holders of ADSs will generally have the right under the deposit agreement to instruct the Depositary to exercise their voting rights for the registered shares represented by ADSs. At management’s request, the Depositary will mail to holders of ADSs any notice of any shareholders’ meeting received from the Company together with information explaining how to instruct the Depositary to exercise the voting rights of the securities represented by ADSs. If the Depositary receives voting instructions for a holder of ADSs on a timely basis, it is obligated to endeavor to vote the securities representing the holder’s ADSs in accordance with those voting instructions. The ability of the Depositary to carry out voting instructions, however, may be limited by practical limitations, such as time zone differences and delays in mailing.

ADS holders may be unable to participate in rights offerings and similar transactions in the future -US securities laws may restrict the ability of US persons who hold ADSs to participate in certain rights offerings or share or warrant dividend alternatives which the Company may undertake in the future in the event that the Company does not register such offerings under the US securities laws and is unable to rely on an exemption from registration under these laws. If the Company issues any securities of this nature in the future, it may issue such securities to the Depositary for the ADSs, which may sell those securities for the benefit of the holders of the ADSs. Management cannot offer any assurance as to the value, if any, the Depositary would receive upon the sale of those securities.

8

Item 4. Information on the Company

A. History and development of the Company

General

Tomkins plc was incorporated in England in 1925, converted from a private company into a public company in March 1950 and re-registered as a public limited company in February 1982. The Company’s Ordinary Shares are listed on the London Stock Exchange and have been listed on the New York Stock Exchange (the “NYSE”) in the form of ADSs evidenced by ADRs since February 1995. Prior to listing on the NYSE, the ADSs had been quoted on the Nasdaq National Market since November 1988. The Company is registered in England and Wales No. 203531 and operates under United Kingdom law. The Company’s registered office is East Putney House, 84 Upper Richmond Road, London SW15 2ST (Telephone: +44 (0) 20 8871 4544) and its website iswww.tomkins.co.uk.

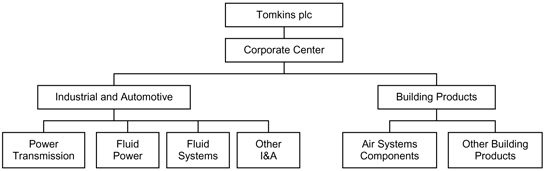

Tomkins plc is the ultimate parent of a large number of subsidiaries that are organized into two business groups:

| • | | Industrial and Automotive |

The Industrial and Automotive group manufactures a wide range of systems and components for the industrial and automotive markets through four operating segments, Power Transmission, Fluid Power, Fluid Systems and Other Industrial and Automotive. The group sells globally into the automotive original equipment market, the automotive aftermarket, the industrial original equipment market and the industrial aftermarket. Other markets include the recreational vehicle market and the manufactured housing market. Its brands include Gates, Dexter Axle, Trico and Schrader Electronics. Prior to fiscal 2006, an additional operating segment, Wiper Systems, was included in the Industrial and Automotive group. During fiscal 2006, Wiper Systems was classified as a discontinued operation and management expects that it will be sold during the fiscal year ending December 29, 2007 (“fiscal 2007”).

The Building Products group manufactures a wide range of air handling components, bathware, doors and windows and other building components for the residential and commercial construction industries through two business areas: Air Systems Components and Other Building Products. The group’s principal markets are the residential, industrial and commercial construction markets. Other markets include the recreational vehicle and manufactured housing market.

The Group is geographically diverse, operating 138 manufacturing facilities, 41 distribution centers and two dedicated research and development centers in 21 different countries across the Americas, Europe, Asia, and Australia.

The Industrial and Automotive group operates in all 21 countries in which the Group operates, while the Building Products group is located in the United States, Canada, Mexico, the United Kingdom and Thailand. Overall, 75 percent of revenue in fiscal 2006 came from the United States, 14 percent from Europe, 8 percent from Asia and 3 percent from the rest of the world.

Group sales in fiscal 2006 were to the following end markets:

| | | |

| | | Percentage of total sales | |

Automotive original equipment | | 17.5 | % |

Automotive aftermarket | | 18.6 | % |

Industrial original equipment | | 13.4 | % |

Industrial aftermarket | | 12.0 | % |

Residential construction | | 12.9 | % |

Non residential construction | | 15.8 | % |

Other markets | | 9.8 | % |

History

In fiscal 1984, Tomkins plc was a manufacturer and distributor of buckles and fasteners in the United Kingdom with net sales of $34.6 million. In the late 1980s, the Company made a number of acquisitions of engineering companies in both the United Kingdom and the United States. In 1992, the Group diversified into food manufacturing, with the acquisition of Ranks Hovis McDougall plc in the United Kingdom.

In fiscal 1996, the Group established the Industrial and Automotive group with the acquisition of The Gates Corporation for $1,160 million. This was satisfied by the issue of $633.4 million of 4.344 percent (net) redeemable convertible cumulative preference shares and $526.6 million of 5.56 percent (net) convertible cumulative preference shares. Stant Corporation was added to the Industrial and Automotive group in 1997 and ACD Tridon in 1999.

The redeemable convertible preference shares, issued as part consideration for the acquisition of The Gates Corporation, were redeemed in August 2003. During fiscal 2006, 74.4 percent of the convertible cumulative preference shares were converted into the Company’s Ordinary Shares. As at December 30, 2006, the carrying amount of the convertible cumulative preference shares was $131.3 million.

Between 1999 and 2005 a number of ‘add on acquisitions’ were made in the Industrial and Automotive and Building Products groups, the food manufacturing business was sold and a number of other divestments were made as part of a program to dispose of non-core businesses.

9

Principal acquisitions, disposals, and capital expenditures

This section should be read in conjunction with Item 5 “Operating and Financial Review and Prospects” and with Notes 4 and 5 to the consolidated financial statements presented under Item 18 “Financial Statements”.

Acquisitions and disposals

Fiscal 2006

In fiscal 2006, the Industrial and Automotive group acquired a 60 percent interest in Gates Winhere LLC (which, through a wholly-owned subsidiary, acquired the business and assets of a water pump manufacturer in China) and ENZED Fleximak Ltd, a supplier of engineering, fabrication, testing and service operations for flexible fluid transfer products in the Arabian Gulf region. The Building Products group acquired Selkirk Americas L.P., a manufacturer of chimney, venting and air distribution products, Eastern Sheet Metal (“ESM”), a manufacturer of commercial heating, ventilation and air conditioning systems and Heat-Fab Inc, a US-based manufacturer of high efficiency residential and commercial venting systems. The Group also acquired a 20 percent interest in e-business and logistics services provider, CoLinx LLC, which paved the way for the launch of an online store for industrial power transmission products in January 2007.

No businesses were sold in fiscal 2006. Subsequent to the year-end, on February 23, 2007, the Company completed the sale of Lasco Fittings Inc., a manufacturer of injection-molded fittings that was included in the Building Products group.

Fiscal 2005

In fiscal 2005, the Industrial and Automotive group acquired L.E. Technologies, a recreational vehicle frame manufacturer and Eifeler Maschinenbau GmbH (“EMB”), a manufacturer of high-performance hydraulic tube fittings, adapters and accessories. The Building Products group acquired Milcor Inc, a multi-brand manufacturer of building products and NRG Industries Inc., a multi brand manufacturer of commercial building accessories.

In fiscal 2005, the Industrial and Automotive group sold Unified Industries, Inc, the Air Springs division and the business and assets of the North American Curved Hose business. The Building Products group sold the business and assets of Gutter Helmet, part of the Hart & Cooley residential construction business.

Fiscal 2004

In fiscal 2004, the Industrial and Automotive group acquired the polyurethane power transmission and motion control belt business, assets and liabilities of Mectrol Corporation.

In fiscal 2004, the Group completed its exit from the valves, taps and mixers business with the disposal of the business and assets of Hattersley Newman Hender, and Pegler. In addition, Mayfran International Inc. was sold. Each of these businesses was included in the Company’s former Engineered & Construction Products group. In the Industrial and Automotive group, the sale of the European curved hose business in Nevers, France, was completed in November 2004 and the related closure of the European curved hose business in St Just, Spain was also completed in fiscal 2004.

Disposals in each of the above fiscal years were executed as part of management’s program to dispose of all non-core businesses.

Capital expenditure

Due to the diverse nature of the business, there is no individual item of capital expenditure that has had a material impact on the position of the Company and no individually significant capital expenditure project that is currently in progress.

10

B. Business overview

Segment contribution to net sales and operating income

The contribution of each segment to the Company’s net sales and operating income is set out below. The Company’s businesses are grouped for management reporting purposes according to the nature of their products and services. The Group’s operating segments are described later in this section.

The Company prepares its home country consolidated financial statements in accordance International Financial Reporting Standards (“IFRS”) adopted for use in the European Union.

SFAS131 “Disclosures about Segments of an Enterprise and Related Information” requires segment information provided in financial statements to reflect the information that was provided to the chief operating decision maker for purposes of making decisions about allocating resources within the Company and assessing the performance of each segment. The chief operating decision maker bases such decisions chiefly on “adjusted profit from operations” which comprises profit from operations before restructuring initiatives (restructuring expenses and gains and losses on disposals and on the exit of businesses) and the amortization of intangible assets arising on acquisition determined in accordance with IFRS.

Accordingly, the segment information presented below is prepared in accordance with IFRS. The information provided to the chief operating decision maker is presented in pounds sterling. In the tables that follow, pound sterling amounts have been translated into US dollars at the average exchange rate for the fiscal year which was as follows: fiscal 2006 £=$1.8336; fiscal 2005 £=$1.8156; fiscal 2004 £=$1.8257.

| | | | | | | | | |

Analysis by business segment (IFRS) | | Year ended December 30,

2006 | | | Year ended December 31,

2005 | | | Year ended January 1, 2005 | |

| | | $ million | | | $ million | | | $ million | |

Net sales | | | | | | | | | |

Industrial and Automotive | | | | | | | | | |

Power Transmission | | 1,851.3 | | | 1,761.0 | | | 1,668.1 | |

Fluid Power | | 703.7 | | | 650.0 | | | 591.0 | |

Fluid Systems | | 430.5 | | | 418.1 | | | 416.3 | |

Other Industrial and Automotive | | 981.7 | | | 919.4 | | | 845.8 | |

| | | | | | | | | |

| | 3,967.2 | | | 3,748.5 | | | 3,521.2 | |

| | | | | | | | | |

Building Products | | | | | | | | | |

Air Systems Components | | 1,070.6 | | | 881.3 | | | 772.3 | |

Other Building Products | | 691.5 | | | 723.3 | | | 673.3 | |

| | | | | | | | | |

| | 1,762.1 | | | 1,604.6 | | | 1,445.6 | |

| | | | | | | | | |

| | 5,729.3 | | | 5,353.1 | | | 4,966.8 | |

| | | | | | | | | |

Adjusted profit from operations | | | | | | | | | |

Industrial and Automotive | | | | | | | | | |

Power Transmission | | 258.2 | | | 234.8 | | | 250.3 | |

Fluid Power | | 63.1 | | | 66.6 | | | 62.3 | |

Fluid Systems | | 20.2 | | | 31.0 | | | 43.8 | |

Other Industrial and Automotive | | 100.1 | | | 111.0 | | | 86.4 | |

| | | | | | | | | |

| | 441.6 | | | 443.4 | | | 442.8 | |

| | | | | | | | | |

Building Products | | | | | | | | | |

Air Systems Components | | 106.3 | | | 90.8 | | | 86.9 | |

Other Building Products | | 47.3 | | | 51.9 | | | 41.4 | |

| | | | | | | | | |

| | 153.6 | | | 142.7 | | | 128.3 | |

| | | | | | | | | |

Unallocated corporate activities | | (52.6 | ) | | (45.2 | ) | | (43.1 | ) |

| | | | | | | | | |

| | 542.6 | | | 540.9 | | | 528.0 | |

| | | | | | | | | |

11

Reconciliations of net sales determined in accordance with IFRS to net sales determined in accordance with US GAAP and of adjusted profit from operations to operating income from continuing operations determined in accordance with US GAAP are set out below. An explanation of the differences between these measures is set forth in Note 7 to the consolidated financial statements presented under Item 18 “Financial Statements”.

Reconciliation of segmental information to US GAAP

| | | | | | | | | |

| | | Year ended December 30,

2006 | | | Year ended December 31,

2005 | | | Year ended January 1, 2005 | |

| | | $ million | | | $ million | | | $ million | |

Net sales (IFRS) | | 5,729.3 | | | 5,353.1 | | | 4,966.8 | |

Discontinued operations | | (310.6 | ) | | (244.2 | ) | | (278.8 | ) |

| | | | | | | | | |

Net sales (US GAAP) | | 5,418.7 | | | 5,108.9 | | | 4,688.0 | |

| | | | | | | | | |

Adjusted profit from operations (IFRS) | | 542.6 | | | 540.9 | | | 528.0 | |

Restructuring costs | | (23.8 | ) | | (7.6 | ) | | (23.0 | ) |

Gain on disposals and on the exit of businesses | | 5.7 | | | 15.4 | | | 4.6 | |

Amortization of intangible assets arising on acquisition | | (5.0 | ) | | (0.4 | ) | | — | |

| | | | | | | | | |

Profit from operations (IFRS) | | 519.5 | | | 523.2 | | | 518.2 | |

Reclassifications | | (20.0 | ) | | (16.7 | ) | | (4.7 | ) |

- Income from discontinued operations | | (6.1 | ) | | 3.6 | | | 1.1 | |

- (Gain)/loss on disposal of continuing operations | | (2.7 | ) | | (1.2 | ) | | (1.5 | ) |

- Equity in net income of associates | | (28.8 | ) | | (14.3 | ) | | (5.1 | ) |

Accounting differences: | | | | | | | | | |

- Acquired intangibles amortization | | (5.0 | ) | | (5.1 | ) | | (5.3 | ) |

- Impairment of acquired intangibles | | (3.1 | ) | | — | | | — | |

- Product development costs | | (0.6 | ) | | (0.7 | ) | | — | |

- Restructuring expenses | | (0.7 | ) | | (0.9 | ) | | (0.9 | ) |

- Capitalized interest | | (7.4 | ) | | (4.0 | ) | | (3.3 | ) |

- Inventory | | (5.5 | ) | | (7.4 | ) | | (1.3 | ) |

- Post retirement benefits | | (28.1 | ) | | (29.8 | ) | | (39.9 | ) |

- Share-based compensation | | (1.1 | ) | | (2.5 | ) | | 4.0 | |

| | | | | | | | | |

Operating income from continuing operations (US GAAP) | | 439.2 | | | 483.6 | | | 457.8 | |

| | | | | | | | | |

Analysis by geographical origin (US GAAP)

| | | | | | |

| | | Year ended December 30,

2006 | | Year ended December 31,

2005 | | Year ended January 1, 2005 |

| | | $ million | | $ million | | $ million |

Net sales | | | | | | |

United States | | 3,391.3 | | 3,291.6 | | 2,937.9 |

United Kingdom | | 256.7 | | 237.9 | | 255.0 |

Rest of Europe | | 641.2 | | 566.8 | | 539.5 |

Rest of the World | | 1,129.5 | | 1,012.6 | | 955.6 |

| | | | | | |

| | 5,418.7 | | 5,108.9 | | 4,688.0 |

| | | | | | |

12

Industrial and Automotive

| | | | | | | | |

Sales by end markets | | | Sales by major product category | |

Automotive original equipment | | 25.3 | % | | Power Transmission: | | | |

Automotive aftermarket | | 26.9 | % | | Belts and tensioners | | 40 | % |

Industrial original equipment | | 19.4 | % | | Powertrain | | 6 | % |

Industrial aftermarket | | 17.3 | % | | Fluid Power: | | | |

Other | | 11.1 | % | | Hydraulic and hose | | 18 | % |

| | | | | Fluid Systems: | | | |

| | | | | Remote Tire Pressure Monitoring System (“RTPMS”) | | 3 | % |

| | | | | Other Fluid Systems | | 8 | % |

| | | | | Other | | 25 | % |

The Industrial and Automotive group has corporate offices in Denver, Colorado, Rochester Hills, Michigan and Toronto, Canada. It supplies industrial and automotive parts, components and systems, serving a wide variety of industries, including the industrial and automotive original equipment and replacement markets, transportation, agricultural, mining, forestry, construction, office equipment, computer, and the food processing and handling markets.

In total, the Industrial and Automotive group operates 79 manufacturing facilities and 33 distribution centers in 21 countries. It has businesses in North America, Europe, Asia, South America, Australia and the Middle East. Most of the manufacturing facilities are in the Americas, with 40 manufacturing facilities in Canada and the United States, seven in Mexico and a further five in South America. European operations include 15 manufacturing facilities and the Asian operations involve 12 facilities, seven of which are in China.

The Industrial and Automotive group has four operating segments: Power Transmission, Fluid Power, Fluid Systems and Other Industrial and Automotive. These segments include divisions integrated from the acquisitions of Gates, Stant, Schrader and Stackpole. Together, these segments employed on average 20,776 people around the world in fiscal 2006. Products are sold directly to industrial and automotive OEMs and, through a network of approximately 150,000 distributors, dealers and jobbers worldwide, to the industrial and automotive replacement markets.

Prior to fiscal 2006, an additional operating segment, Wiper Systems, was included in the Industrial and Automotive group. This segment operated under the Trico and Tridon brands, manufacturing automotive windshield wiping systems and systems components. During fiscal 2006, the Wiper Systems business was classified as a discontinued operation and management expects that it will be sold during fiscal 2007.

Power Transmission

Power Transmission produces a comprehensive global product line ranging from synchronous belt and accessory belt drive systems for automotive applications to heavy-duty industrial belt drives. As a market leader in the power transmission industry, the Power Transmission segment provides a diverse product line encompassing V-belts, multi V-ribbed belts, synchronous belts, sheaves/sprockets, pulleys, tensioners, idlers, and crankshaft dampers and employs a variety of process and material technologies including rubber, polyurethane, and metals. A broad product line coupled with industry expertise allows this group to design, manufacture, market, and distribute complete power transmission systems to both OEM and replacement markets.

Power Transmission is globally integrated to standardize product and process technology, maximizing resource utilization across the Group. Product, material and enabling technology teams join forces in the development and commercialization of products and systems. Focusing on customer needs, the appropriate innovative technology is selected to create a sustainable competitive advantage in the market. Innovation, technology and product development are driven through three technical and product development centers located at Aachen, Germany, Seoul, Korea, and Nara, Japan, and a dedicated research and development center in Rochester Hills, Michigan. Each of these centers leads product development, engineering, and systems design with capabilities to focus on customer specific requirements.

Power Transmission supports and supplies customers on a global basis. Regional management in the Americas, Europe and Asia work to leverage the Group’s market strengths from one area to another utilizing common processes and global product lines.

13

Fluid Power

The Fluid Power segment is a manufacturer of engineered hose, fittings and accessories for hydraulic power transmission systems used in both mobile and stationary industrial equipment. The segment also manufactures industrial hose used to convey both liquids and bulk powder type materials, focused primarily in the petroleum, chemical and food/beverage sectors. The segment also produces a wide range of under-the-hood automotive, heavy duty truck and bus products used in engine cooling, power steering, braking, transmission and fuel system applications.

The Customer Solutions Center in Denver, Colorado has been established to promote customer focused innovation and global product development emphasizing integration of new products and design solutions into a value-added systems approach. The development of next generation products is focused on evolving the existing hose and connector product line into a full port-to-port sub-system capable of providing systems and design concepts that reduce leaks, warranty and assembly labor costs.

The segment has a global reach, serving customers in North America, South America, Europe, Asia and India. The acquisition of EMB in Germany has resulted in an expanded product range and geographic presence in Eastern Europe and Asia. Within Eastern Europe, India and China, restructuring has allowed Gates to focus and expand its efforts in these fast growing markets. Expansion plans being implemented over the next 12 to 24 months are expected to allow for localized supply of certain products within these regions.

Fluid Systems

The Fluid Systems segment, which comprises acquired businesses such as Stant Corporation and Schrader-Bridgeport International, is a designer, manufacturer and distributor of a broad range of automotive fluid conveyance and fluid management components and modules. Fluid Systems employs the latest technology in tire pressure monitoring components and fuel vapor management valves. Products are sold primarily for use as original equipment by manufacturers of cars and trucks and in the automotive replacement market as repair parts and accessories. Major customers include DaimlerChrysler, Ford, General Motors, Nissan, Renault and PSA, as well as a number of other major international OEMs. Fluid Systems products are also sold in wholesale and retail automotive parts and distribution outlets in North America, Europe and Latin America including the service departments of OEM dealers.

Through Schrader Electronics, the Fluid Systems segment is the technology leader in Remote Tire Pressure Monitoring Systems (“RTPMS”), a driver information and passenger security system that is economically and ergonomically integrated into vehicle electronic information systems. Fluid Systems also designs, manufactures and markets a variety of fuel vapor management valves and fuel, oil and radiator closure caps at its Stant Manufacturing Division. Stant complemented its existing fuel vapor management product offering in fiscal 2006 with the addition of carbon canisters and evaporative system integrity monitors for DaimlerChrysler. Standard-Thomson is a manufacturer of engine thermostats used in automotive cooling systems. Schrader-Bridgeport International provides a wide range of tire valve, hardware and specialty valve products worldwide. RTPMS, tire, and specialty valve products are sold under the “Schrader-Bridgeport” and “Schrader Electronics” trademarks. Closure cap and fuel management valve products are sold under the “Stant,” “Lev-R-Vent” and “Pre-Vent” trademarks. Engine thermostats are sold under the “Stant,” “Weir-stat,” and “Superstat” brand names. Many of these products are also sold to various private label customers bearing their own brand names.

Other Industrial and Automotive

Other Industrial and Automotive includes the trailer axles, materials handling and the aftermarket businesses.

Dexter Axle produces and markets its products primarily in the United States directly to OEMs and distributors. Dexter’s product line consists of a wide variety or trailer axles for the general utility, recreational vehicle, highway trailer and manufactured housing markets. Competition is based on price, quality, product performance and customer service.

Dexter’s trailer axles are available in capacities from 800 pounds to 30,000 pounds and specific trailer applications within its markets include horse and livestock trailers, equipment hauling trailers, enclosed cargo trailers, heavy hauling trailers, recreational vehicles, manufactured homes, portable equipment and highway trailers.

The Dexter Chassis Group (formerly LE Technologies) produces and markets its products in the United States directly to OEMs. The Dexter Chassis Group manufactures chassis and components for recreational vehicles and utility trailers, fabricated metal parts to commercial truck body builders, and high-end coatings for military and general industries. The Dexter Chassis Group provides engineering services for the products it builds based on its own designs or based on customers’ current designs. A complete line of recreational vehicle slide out rooms is currently offered as a value-added feature to the chassis.

Dearborn Mid-West Conveyor Company (“Dearborn”) designs, fabricates and installs overhead conveyor systems, inverted power and free conveyor systems, skillet systems, automatic electrified monorail systems, power roll conveyors and flat top conveyors for the automotive, commercial trucks, aircraft, appliance and heavy equipment industries; belt conveyors, stackers, hoppers, rotary plow feeders, belt feeders, barge/truck/rail loaders and unloaders and pipe conveyors for handling bulk materials servicing coal power generating plants, coal processing and cement manufacturing facilities; and various unit handling systems for parcel movement applications for the United States Postal Service, United Parcel Service and Fed-Ex. Dearborn is classified as a continuing operation under IFRS (and therefore for the purposes of the segment information provided in this Annual Report), but in fiscal 2006 it was classified as a discontinued operation under US GAAP. Management expects that Dearborn will be sold during fiscal 2007.

The Aftermarket business integrates the sales, marketing, distribution and manufacture of products destined for both the Industrial and Automotive original equipment and Aftermarket and sold under the Tridon, Ideal, Schrader, Plews Edelmann and numerous private brands. It designs and sells aftermarket automotive tools and fittings, power steering hose, transmission cooler lines, lubrication equipment, stainless and carbon steel hose clamps for both original equipment and parts applications.

The Aftermarket business also manufactures and distributes specialist components for the automotive industry. “Schrader” brand products include precision control valves and associated fluid conveyance and control modules for vehicle fluid system applications in fuel delivery, emission control, engine management, brake, steering, power transmission, coolant, air conditioning, windshield washing, PVC air hose, and ride control. Schrader, a leading brand of wheel valves for cars, medium

14

and heavy-duty trucks, agricultural vehicles and construction equipment, offers a full range of products, including tubeless tire valves, valves for inner tubes, cores, tubeless valves for large wheels and an assortment of specialty valves for virtually all global applications.

Wheel care products, air power pneumatic components and systems, and pressure-measuring devices are marketed to automotive channels worldwide. Wheel care products include “Camel” brand tire patch products, tools, chemicals and “Schrader” brand tire valves and cores. Air power systems include “Amflo” pneumatic couplers and plugs. Aftermarket’s “Syracuse” brand of pressure-measuring devices is a recognized market standard in North America. The Aftermarket business supplies “Amflo” pneumatic accessories to the home improvement retailer segment.

Building Products

| | | | | | | | |

Sales by end markets | | | Sales by major product category | |

Residential construction | | 41.9 | % | | Air handling components | | 63 | % |

Industrial & Commercial Construction | | 51.3 | % | | Bathtubs, showers and whirlpools | | 19 | % |

Other | | 6.8 | % | | Doors and windows | | 13 | % |

| | | | | Other | | 5 | % |

The Building Products group manufactures a range of products for residential and commercial buildings, supplying both the new-build and refurbishment sectors. Its product portfolio comprises air systems components (manufacturing a wide range of components for the heating, ventilation and air conditioning markets, principally in North America), bathware (manufacturing a range of baths, shower cubicles and luxury whirlpools for the North American residential market), and doors and windows (manufacturing uPVC doors and windows for the residential and manufactured housing markets in North America).

The Building Products group operates 59 manufacturing facilities and eight distribution centers in five countries. 55 of the manufacturing facilities are in the United States, Mexico and Canada, with three in the United Kingdom and one in Thailand. The distribution centers are all based in the United States.

Air Systems Components

The Air Systems Components segment’s products are primarily sold throughout the United States, Canada, Mexico and the United Kingdom. Competition is based principally on price, quality, service and breadth of product line. Just under half of the segment’s sales pass through manufacturers’ representatives and approximately 35 percent are sold through wholesalers, principally in the residential market. The balance of sales is direct to OEMs, national accounts and retail customers.

Hart & Cooley and Selkirk supply the residential and light commercial markets in the United States, Canada and Mexico with grilles, registers and diffusers. They also produce flexible air duct, chimney and gas venting systems which are marketed primarily through wholesale distributors and retail customers.

Air Systems designs and manufactures diffusers, variable air volume terminal boxes (with or without fan power), grilles, registers and fan coils for use in heating, ventilating and air conditioning systems in industrial, institutional and commercial applications. Air Systems also produces a comprehensive line of centrifugal and axial fans for both commercial and industrial applications comprising power roof ventilators, inline duct fans, ceiling fans, cabinet fans, propeller roof and wall fans, and fan accessories. These products are sold primarily to manufacturers’ representatives for resale to contractors.

Ruskin produces and markets commercial and industrial air control dampers, fire and smoke dampers, architectural louvers, sound absorbers, and air measuring stations for use in air conditioning, heating, ventilating and pollution control systems contained in office buildings, hotels, shopping centers, power plants, paper mills and other manufacturing plants. Ruskin also manufactures and supplies fans and blowers for residential and commercial forced air heating systems and air conditioners. These products are sold directly to manufacturers of heating, ventilating and air conditioning equipment and to contractors and commercial users principally through manufacturers’ representatives. Ruskin Air Management, a United Kingdom business, markets its damper, louver, grille, register, diffuser and fan coil products principally in the United Kingdom and continental Europe. This business gives the company important access to these markets for its other air distribution products.

Other Building Products

Lasco Bathware designs, manufactures and markets single piece and multi-piece fiberglass and acrylic showers, tub/shower combinations, soaking bathtubs, air tubs and whirlpools used in residential (including manufactured) housing and some commercial construction. Included in the product line are assisted care showers and tub/shower combinations designed both for new construction and remodeling applications, to meet the needs of senior citizens and the special requirements of the disabled. Products are sold in the United States, primarily through wholesale distributors and retail home improvement channels. Products are also sold directly to builders who use the company installation services. Aquatic Industries, a division of Lasco Bathware, is a maker of up-market acrylic whirlpools, principally for the dealer/distributor market in the United States and also supplies standard and customized products for hotel and resort developments internationally.

Lasco Fittings manufactures plastic fittings used in agricultural irrigation, turf irrigation, water works, swimming pools and spas, for commercial and industrial applications as well as for residential plumbing. Lasco Fittings is classified as a continuing operation under IFRS (and therefore for the purposes of the segment information provided in the Annual Report), but in fiscal 2006 it was classified as a discontinued operation under US GAAP. Lasco Fittings was sold on February 23, 2007.

15

Philips Products is a US producer of vinyl windows and sliding glass doors for the residential markets, principally for use in new on-site construction. These products are sold primarily through distributors to the builders. Philips sells to the window distributors through a company sales organization and, in certain regions, through independent sales representatives. Philips has recently introduced a new residential window series with appealing architectural and functional attributes that is targeted towards both the new construction and the remodeling markets. Additionally, Philips has received Florida/coastal state building code and hurricane approvals for its current residential vinyl window products allowing for growth in these regional coastal markets.

Philips Products also produces aluminum and vinyl windows, doors and venting products for the manufactured housing, recreational vehicle and specialty trailer markets. The majority of these products are sold to OEMs of manufactured housing, recreational vehicles, and specialty trailers. These products are also sold to manufactured housing and recreational vehicle after-market distributors. Philips makes sales to these OEMs and after-market distributors through a company sales organization.

Raw Materials and Energy Supplies

The Group purchases a broad range of raw materials, components and products from around the world in connection with its activities. The ability of the Group’s suppliers to meet performance and quality specifications and delivery schedules is important to its operations, but the Company is not dependent on any single source of supply for critical materials. In the past, the energy and materials required for the Group’s manufacturing operations have been readily available. However, basic raw materials such as steel, aluminum, nickel, polymers and resins used in the production of the Group’s products, can be subject to significant fluctuations in price. Where appropriate, the Group seeks to minimize the effect of fluctuations in prices of raw materials by entering into forward purchase contracts or options to fix the input cost of the raw material or product. During fiscal 2006, the price of certain base metals more than doubled which had an adverse impact on the Group’s Fluid Systems and Wiper Systems businesses. Generally, the Group has secured sales price increases that have enabled it to pass the increased cost of raw materials on to its customers. Where possible, the Group continues to endeavor to obtain raw materials from lower-cost sources and to find suitable lower-cost substitutes.

Seasonality

Industrial and Automotive

Sales to Automotive OEMs do not tend to exhibit seasonal patterns. Sales into the aftermarket are generally stronger during the winter months reflecting higher levels of demand for replacement parts for vehicles during this period. Sales to Industrial OEMs are strongest from October to April for outdoor power equipment and from February to June for agricultural equipment.

In the Fluid Power OEM segment, moderate seasonality is primarily driven by consumer demand and crop-related seasonal activities. Production of construction equipment declines in the summer months followed by a resurgence of activity in the late fall, early winter and spring. Farm equipment production levels are driven by purchases prior to the relevant planting and harvesting seasons. The remaining markets served by the Fluid Power segment do not exhibit significant seasonal patterns.

Building Products

Sales to the construction industry slow down in November and December before the Thanksgiving, Christmas and New Year holiday season and are generally stronger in the spring and summer months. Sales can also be affected regionally by severe weather. Heating product sales are more concentrated in the fall and cooling products in the spring.

Patents and Trademarks

Management believes that the Group’s operations are not dependent to any significant degree upon any single or series of related patents or licenses, or any single commercial or financial contract. Management also believes that the Group’s operations are also not dependent upon any single trademark or trade name, although trademarks and trade names are identified with a number of the Group’s products and services and are of importance in the sale and marketing of such products and services.

Governmental Regulation

The Company’s subsidiaries are regulated by governmental authorities in a number of countries. Many of the products produced by the Company’s subsidiaries are subject to governmental regulation regarding their production, sale, advertising, safety, labeling and raw materials. Management believes that the Company’s subsidiaries have taken sufficient measures to comply with applicable local or national regulations.

Some of the regulations applicable to the Company’s subsidiaries include regulations that would allow local, national or federal authorities to mandate product recalls, or provide for the seizure of products, as well as other sanctions. Management believes that the controls implemented by subsidiaries minimize the risk of the occurrence of such events and that such risks do not pose a material threat to the Company. It is standard practice for contracts with OEMs to limit compensation arising from product recalls to direct costs (recall notification and replacement). Warranty limitations and exclusions are printed on all customer-facing material.

The Company maintains worldwide insurance coverage for product liability claims and believes that its level of insurance coverage is adequate.

The Company’s subsidiaries are subject to regulation under various and changing federal, state and local laws and regulations relating to the environment and to employee safety and health. These environmental laws and regulations govern the generation, storage, transportation, disposal and emission of various substances. Permits are required for operation of certain businesses carried out by the Company’s subsidiaries (particularly air emission permits) and these permits are subject to renewal, modification and, in certain circumstances, revocation. Management believes that the Company’s subsidiaries are in substantial compliance with laws and regulations which could allow regulatory authorities to compel (or seek reimbursement for) clean up of environmental contamination at its subsidiary-owned sites and at facilities where its waste is stored or disposed of.

16

C. Organizational structure

Tomkins plc is the parent of a large number of subsidiaries that are organized into two principal business groups managed through a Corporate Center. The Group’s organizational structure is shown below (excluding the Wiper Systems operating segment that formed part of the Industrial & Automotive business group, but was classified as a discontinued operation during fiscal 2006). During fiscal 2006, Dearborn Mid-West Conveyor Company (that was included within the Other Industrial and Automotive operating segment) and Lasco Fittings Inc. (that was included within the Other Building Products operating segment) were also classified as discontinued operations.

A list of the Company’s significant subsidiaries, including name, country of incorporation and proportion of ownership, is set forth in Exhibit 8.1.

D. Property, plant and equipment

The Group’s principal executive offices are located in London, England. The Group’s plants, warehouses and offices are located in various countries throughout the world, with a large number in North America. The Group owns many of these properties and continues to improve and replace properties when considered appropriate to meet the needs of its individual operations. There are no individually significant properties that were underutilized during fiscal 2006.