We are pleased to report on your Funds and their investments for the annual period ended March 31, 2010.

What a difference a year can make. Last year at this time we were just recovering from one of the most difficult bear markets in history and were in the grips of a worldwide recession. Today, most economies have improved and we are enjoying a very powerful stock market rally. The S&P 500 Index returned 49.77% over the twelve months ended March 31, 2010 - one of the best years on record. This has been quite a recovery, but not surprising considering the low levels reached in early of March of 2009. Every sector in the S&P 500 Index posted positive returns, with Financials producing the strongest gains. Again not surprising as this was the most devastated sector during the bear market.

The FBP Value Fund and the FBP Balanced Fund each produced very strong returns over this period, rising 62.84% and 44.01%, respectively. The key to achieving these results was staying true to our investment philosophy and process. We believed that tremendous values had been created during the weakness of the bear market. By sticking with our disciplines, we were able to stay invested a year ago when others may have become too conservative. Our investment team worked to improve the quality of the equity holdings and to maintain sufficient equity exposure in the Balanced Fund. Therefore, as the recovery has unfolded, the performance of the equities in the Funds drove the Funds’ returns. And just as with the S&P 500 Index, all sectors held by the Funds produced positive results. The Energy sector was the strongest performer, dri ven by Pioneer Natural Resources (+243%) and BJ Services (+122%). Industrials were quite strong relative to the S&P 500 Index with Ingersoll-Rand (+157%) a large contributor. Financials were also a major contributor. We had reduced the exposure to the Financials sector early in 2009, but the Funds maintained a higher weight than the S&P 500 Index and produced a higher return. JPMorgan Chase (+69%) and Lincoln National (+360%) provided the most lift in this sector. Two sectors, Materials and Consumer Staples, contributed negatively on a relative basis. While both sectors were up nicely, a combination of weighting and relative return produced the slight detraction. The best individual stock was Wyndham Worldwide (+521%), just recently eliminated from the Funds, and the worst was Watson Pharmaceuticals (+2%), which was sold early in the fiscal year.

Just as investors began to feel more comfortable with the equity markets, several significant events occurred: The rise in risk premiums due to Greece’s financial problems and market weakness in China seem to be tipping points, and most likely are accompanying a near-term correction in equity prices. We are not surprised; as we believed the markets had been due to adjust following the past year’s powerful run. The exaggerated price swings witnessed on May 7th have unnerved many and will surely lead to some changes in trading rules, hopefully to minimize such occurrences in the future. The public turmoil in opposition to necessary austerity measures resulting from Greece’s large debt load is indeed troubling. The rest of Europe has prepared a financial

rescue package to allow Greece to work out of its difficulties over time. But this should be a warning signal to any country that takes on too much debt, whatever its reason.

While the recession most likely ended sometime in the second half of 2009 and economic growth is improved, the strength and longevity of this cycle remain uncertain. We expect domestic GDP growth to be in the 3% to 3.5% range for the calendar year, a decent economic environment. Unemployment remains high at 9.7%, but is down from its seasonally-adjusted peak last year of 10.1%. We expect the unemployment rate, which is traditionally a lagging indicator, to improve gradually as the economy continues to gain traction. Some evidence of this improvement is already appearing, with unemployment claims recently making an 18-month low. Understandably, consumer spending remains subdued, and consumers are continuing to deleverage their balance sheets. Expectations for spending are very low, so even minor upticks in retail sales numbers are being favorably received by investors. We believe a pickup in corporate spending will be a key driver of the economic recovery. During the uncertainty of the recession, companies became reluctant to spend and began hoarding cash. We expect that, as managements see continued economic improvement, they will loosen their purse strings and invest in capital projects, technology and payrolls. The credit markets have normalized, but there are signs that bank lending hasn’t returned to normal levels yet. As bank balance sheets continue to improve over time, lending should pick up and provide additional fuel for the recovering economy.

With interest rates at historically low levels, equity valuation levels reasonable, skepticism still abundant and a decade of very low returns behind us, we are quite optimistic about the potential for stocks to perform well over the long term. During the downturn, many companies cut costs and should be better positioned to generate relatively strong earnings in a gradually improving economic environment. Our focus is to build the Funds’ portfolios with companies trading at substantial discounts to our estimated values. We want to understand the businesses we invest in and to understand the drivers of future value. Strong financial flexibility, excess cash flow generation, revenue and margin potential and competitive position are some of the key factors we consider.

The bond market is ending a multiyear period of relatively strong performance, just as one would expect with interest rates moving to record low levels. As the economy improves, the potential for interest rates to rise is quite likely, which will offer an unattractive return profile for bonds, whose prices move inversely to interest rates. Our current strategy is to maintain short maturities to protect principal value. With government yields so low, our focus will be more on opportunities in investment-grade corporate bonds through which we can generate higher income for the Balanced Fund.

This month we are celebrating our twenty-fifth year as Flippin, Bruce & Porter. Much has changed over the years. Our firm has grown and as a result we have more depth and experience. We have had the pleasure of working with many excellent employees and seeing their families grow up among us. The dynamics of the markets change through time. Now both domestic and global events shape the markets, and we are constantly challenged to understand what is occurring and to invest accordingly. What will never

change, however, is our dedication to you, our clients, who have placed your confidence and trust in us. We appreciate you as our client and look forward each day to come to work on your behalf.

Please visit our website at www.fbpfunds.com for information on your Funds and the investment philosophy and process we utilize to achieve their investment objectives.

John T. Bruce, CFA

Data presented reflects past performance, which is no guarantee of future results. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Due to market volatility, current performance may be higher or lower than the performance shown. Updated performance information, current through the most recent month-end, is available by contacting the Funds at 1-866-738-1127.

This report is submitted for the general information of the shareholders of the Funds. It reflects our views, opinions and portfolio holdings as of March 31, 2010, the end of the reporting period. These views are subject to change at any time based upon market or other conditions. For more current information throughout the year please visit www.fbpfunds.com or call the Funds at 1-866-738-1127. This report is not authorized for distribution to prospective investors in the Funds unless accompanied by a current prospectus. Distributed by Ultimus Fund Distributors, LLC

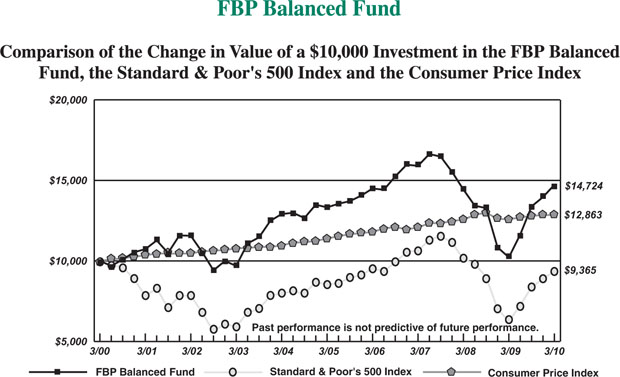

Performance for each Fund is compared to the most appropriate broad-based index, the S&P 500 Index, an unmanaged index of 500 large common stocks. Over time, this index has the potential to outpace the FBP Balanced Fund, which normally maintains at least 25% of its investable assets in bonds. Balanced funds have the growth potential to outpace inflation, but they will typically lag a 100% stock index over the long term because of the bond portion of their portfolios. However, the advantage of the bond portion is that it can make the return and principal of a balanced fund more stable than a portfolio completely invested in stocks. Results are also compared to the Consumer Price Index, a measure of inflation.

Average Annual Total Returns(a) (for periods ended March 31, 2010) |

| | 1 Year | 5 Years | 10 Years |

| FBP Value Fund | 62.84% | -0.17% | 2.71% |

| FBP Balanced Fund | 44.01% | 2.02% | 3.94% |

| Standard & Poor’s 500 Index | 49.77% | 1.92% | -0.65% |

| Consumer Price Index | 2.13% | 2.47% | 2.55% |

| (a) | Total returns are a measure of the change in value of an investment in the Funds over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Funds. Returns do not reflect the deduction of taxes a shareholder would pay on the Funds’ distributions or the redemption of Fund shares. |

FBP VALUE FUND PORTFOLIO INFORMATION MARCH 31, 2010 (Unaudited) |

| General Information | | Asset Allocation |

| Net Asset Value Per Share | $19.42 | |

| Total Net Assets (Millions) | $28.6 |

| Current Expense Ratio | 1.07% |

| Portfolio Turnover | 21% |

| Fund Inception Date | 7/30/93 |

| | | |

| Stock Characteristics | FBP Value Fund | S&P 500 Index |

| Number of Stocks | 43 | 500 |

| Weighted Avg Market Capitalization (Billions) | $63.4 | $82.1 |

Price-to-Earnings Ratio (IBES 1 Yr. Forecast EPS) | 12.6 | 14.2 |

| Price-to-Book Value | 2.0 | 2.2 |

| Sector Diversification vs. the S&P 500 Index |

| Ten Largest Equity Holdings | % of Net Assets |

| JPMorgan Chase & Company | 4.7% |

| Travelers Companies, Inc. (The) | 3.8% |

| McGraw-Hill Companies, Inc. (The) | 3.1% |

| SUPERVALU, Inc. | 3.0% |

| Sealed Air Corporation | 3.0% |

| Johnson & Johnson | 3.0% |

| Willis Group Holdings plc | 3.0% |

| Devon Energy Corporation | 2.9% |

| Hewlett-Packard Company | 2.8% |

| Ingersoll-Rand plc | 2.7% |

FBP BALANCED FUND PORTFOLIO INFORMATION MARCH 31, 2010 (Unaudited) |

| General Information | | Asset Allocation |

| Net Asset Value Per Share | $15.49 | |

| Total Net Assets (Millions ) | $45.5 |

| Current Expense Ratio | 1.00% |

| Portfolio Turnover | 24% |

| Fund Inception Date | 7/3/89 |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

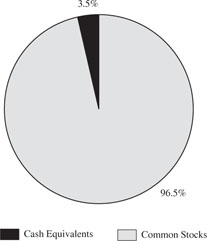

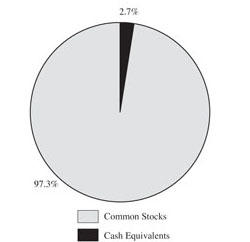

| Common Stock Portfolio (72.5% of Net Assets) |

| Number of Stocks | 52 | | Ten Largest Equity Holdings | % of Net Assets |

| Weighted Avg Market Capitalization (Billions) | $64.2 | | JPMorgan Chase & Company | 3.0% |

| Price-to-Earnings Ratio (IBES 1 Yr. Forecast EPS) | 12.4 | | International Business Machines Corporation | 2.7% |

| Price-to-Book Value | 2.0 | | Travelers Companies, Inc. (The) | 2.5% |

| | | | McGraw-Hill Companies, Inc. (The) | 2.0% |

| Five Largest Sectors | % of Net Assets | | Johnson & Johnson | 2.0% |

| Information Technology | 12.6% | | SUPERVALU, Inc. | 2.0% |

| Financials | 11.1% | | Devon Energy Corporation | 2.0% |

| Consumer Staples | 10.5% | | Sealed Air Corporation | 1.9% |

| Industrials | 9.1% | | Willis Group Holdings plc | 1.9% |

| Consumer Discretionary | 7.7% | | Hewlett-Packard Company | 1.9% |

| Fixed-Income Portfolio (20.7% of Net Assets) |

| Number of Fixed-Income Securities | 12 | | |

| Average Quality | A | U.S. Treasury | 1.7% |

| Average Weighted Maturity | 1.9 yrs | U.S. Government Agency | 1.7% |

| Average Effective Duration | 1.8 yrs | Corporate | 17.3% |

FBP VALUE FUND SCHEDULE OF INVESTMENTS March 31, 2010 |

| | | | | | |

| Consumer Discretionary — 11.4% | | | | | | |

| H&R Block, Inc. | | | 16,000 | | | $ | 284,800 | |

| Home Depot, Inc. (The) | | | 21,000 | | | | 679,350 | |

| KB Home | | | 23,000 | | | | 385,250 | |

Kohl's Corporation (a) | | | 8,000 | | | | 438,240 | |

| Macy's, Inc. | | | 26,500 | | | | 576,905 | |

| McGraw-Hill Companies, Inc. (The) | | | 25,000 | | | | 891,250 | |

| | | | | | | | 3,255,795 | |

| Consumer Staples — 14.3% | | | | | | | | |

| Avon Products, Inc. | | | 11,600 | | | | 392,892 | |

| CVS Caremark Corporation | | | 16,500 | | | | 603,240 | |

| Kimberly-Clark Corporation | | | 9,000 | | | | 565,920 | |

| SUPERVALU, Inc. | | | 52,000 | | | | 867,360 | |

| Sysco Corporation | | | 10,000 | | | | 295,000 | |

| Walgreen Company | | | 19,000 | | | | 704,710 | |

| Wal-Mart Stores, Inc. | | | 12,000 | | | | 667,200 | |

| | | | | | | | 4,096,322 | |

| Energy — 8.5% | | | | | | | | |

| Chevron Corporation | | | 3,800 | | | | 288,154 | |

| Devon Energy Corporation | | | 13,100 | | | | 844,033 | |

| Pioneer Natural Resources Company | | | 12,800 | | | | 720,896 | |

| Royal Dutch Shell plc - Class A - ADR | | | 10,000 | | | | 578,600 | |

| | | | | | | | 2,431,683 | |

| Financials — 16.9% | | | | | | | | |

| Comerica, Inc. | | | 14,000 | | | | 532,560 | |

| First American Corporation | | | 10,000 | | | | 338,400 | |

| JPMorgan Chase & Company | | | 30,000 | | | | 1,342,500 | |

| Lincoln National Corporation | | | 23,000 | | | | 706,100 | |

| Travelers Companies, Inc. (The) | | | 20,000 | | | | 1,078,800 | |

| Willis Group Holdings plc | | | 27,000 | | | | 844,830 | |

| | | | | | | | 4,843,190 | |

| Health Care — 10.8% | | | | | | | | |

Amgen, Inc. (a) | | | 8,400 | | | | 501,984 | |

| Johnson & Johnson | | | 13,000 | | | | 847,600 | |

| Merck & Company, Inc. | | | 16,000 | | | | 597,600 | |

| Pfizer, Inc. | | | 42,000 | | | | 720,300 | |

WellPoint, Inc. (a) | | | 6,300 | | | | 405,594 | |

| | | | | | | | 3,073,078 | |

| Industrials — 13.2% | | | | | | | | |

| Avery Dennison Corporation | | | 17,900 | | | | 651,739 | |

| FedEx Corporation | | | 5,800 | | | | 541,720 | |

| General Electric Company | | | 33,000 | | | | 600,600 | |

| Ingersoll-Rand plc | | | 22,500 | | | | 784,575 | |

| Lockheed Martin Corporation | | | 7,900 | | | | 657,438 | |

| Masco Corporation | | | 35,000 | | | | 543,200 | |

| | | | | | | | 3,779,272 | |

FBP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 96.5% (Continued) | | | | | | |

| Information Technology — 18.4% | | | | | | |

Cisco Systems, Inc. (a) | | | 22,000 | | | $ | 572,660 | |

Computer Sciences Corporation (a) | | | 14,000 | | | | 762,860 | |

Dell, Inc. (a) | | | 50,000 | | | | 750,500 | |

Flextronics International Ltd. (a) | | | 84,000 | | | | 658,560 | |

| Hewlett-Packard Company | | | 15,000 | | | | 797,250 | |

| International Business Machines Corporation | | | 6,000 | | | | 769,500 | |

| Microsoft Corporation | | | 23,000 | | | | 673,210 | |

| Western Union Company (The) | | | 16,900 | | | | 286,624 | |

| | | | | | | | 5,271,164 | |

| Materials — 3.0% | | | | | | | | |

| Sealed Air Corporation | | | 41,100 | | | | 866,388 | |

| | | | | | | | | |

Total Common Stocks (Cost $22,054,024) | | | | | | $ | 27,616,892 | |

MONEY MARKET FUNDS — 2.2% | | | | | | |

Fidelity Institutional Money Market Government Portfolio - Class I, 0.04% (b) (Cost $632,035) | | | 632,035 | | | $ | 632,035 | |

| | | | | | | | | |

Total Investments at Value — 98.7% (Cost $22,686,059) | | | | | | $ | 28,248,927 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 1.3% | | | | | | | 367,673 | |

| | | | | | | | | |

| Total Net Assets — 100.0% | | | | | | $ | 28,616,600 | |

| ADR - American Depositary Receipt |

| |

| (a) | Non-income producing security. |

| | |

| (b) | Variable rate security. The rate shown is the 7-day effective yield as of March 31, 2010. |

| | |

| See accompanying notes to financial statements. |

FBP BALANCED FUND SCHEDULE OF INVESTMENTS March 31, 2010 |

| | | | | | |

| Consumer Discretionary — 7.7% | | | | | | |

| H&R Block, Inc. | | | 17,000 | | | $ | 302,600 | |

| Home Depot, Inc. (The) | | | 23,000 | | | | 744,050 | |

| KB Home | | | 26,000 | | | | 435,500 | |

Kohl's Corporation (a) | | | 7,500 | | | | 410,850 | |

| Macy's, Inc. | | | 32,000 | | | | 696,640 | |

| McGraw-Hill Companies, Inc. (The) | | | 26,000 | | | | 926,900 | |

| | | | | | | | 3,516,540 | |

| Consumer Staples — 10.5% | | | | | | | | |

| Avon Products, Inc. | | | 12,000 | | | | 406,440 | |

| CVS Caremark Corporation | | | 17,500 | | | | 639,800 | |

| Kimberly-Clark Corporation | | | 9,300 | | | | 584,784 | |

| Philip Morris International, Inc. | | | 6,500 | | | | 339,040 | |

| SUPERVALU, Inc. | | | 54,000 | | | | 900,720 | |

| Sysco Corporation | | | 11,600 | | | | 342,200 | |

| Walgreen Company | | | 22,000 | | | | 815,980 | |

| Wal-Mart Stores, Inc. | | | 13,500 | | | | 750,600 | |

| | | | | | | | 4,779,564 | |

| Energy — 7.5% | | | | | | | | |

| BP plc - ADR | | | 5,000 | | | | 285,350 | |

| Chevron Corporation | | | 4,000 | | | | 303,320 | |

| ConocoPhillips | | | 12,500 | | | | 639,625 | |

| Devon Energy Corporation | | | 13,900 | | | | 895,577 | |

| Pioneer Natural Resources Company | | | 13,000 | | | | 732,160 | |

| Royal Dutch Shell plc - Class A - ADR | | | 10,000 | | | | 578,600 | |

| | | | | | | | 3,434,632 | |

| Financials — 11.1% | | | | | | | | |

| Comerica, Inc. | | | 15,000 | | | | 570,600 | |

| First American Corporation | | | 11,000 | | | | 372,240 | |

| JPMorgan Chase & Company | | | 31,000 | | | | 1,387,250 | |

| Lincoln National Corporation | | | 22,700 | | | | 696,890 | |

| Travelers Companies, Inc. (The) | | | 21,000 | | | | 1,132,740 | |

| Willis Group Holdings plc | | | 28,000 | | | | 876,120 | |

| | | | | | | | 5,035,840 | |

| Health Care — 7.6% | | | | | | | | |

Amgen, Inc. (a) | | | 8,850 | | | | 528,876 | |

| Eli Lilly & Company | | | 6,000 | | | | 217,320 | |

| Johnson & Johnson | | | 14,000 | | | | 912,800 | |

| Merck & Company, Inc. | | | 15,600 | | | | 582,660 | |

| Pfizer, Inc. | | | 46,000 | | | | 788,900 | |

WellPoint, Inc. (a) | | | 6,500 | | | | 418,470 | |

| | | | | | | | 3,449,026 | |

FBP BALANCED FUND SCHEDULE OF INVESTMENTS (Continued) |

COMMON STOCKS — 72.5% (Continued) | | | | | | |

| Industrials — 9.1% | | | | | | |

| Avery Dennison Corporation | | | 19,000 | | | $ | 691,790 | |

| FedEx Corporation | | | 6,400 | | | | 597,760 | |

| General Electric Company | | | 39,000 | | | | 709,800 | |

| Ingersoll-Rand plc | | | 24,000 | | | | 836,880 | |

| Lockheed Martin Corporation | | | 8,400 | | | | 699,048 | |

| Masco Corporation | | | 39,000 | | | | 605,280 | |

| | | | | | | | 4,140,558 | |

| Information Technology — 12.6% | | | | | | | | |

Cisco Systems, Inc. (a) | | | 25,000 | | | | 650,750 | |

Computer Sciences Corporation (a) | | | 14,000 | | | | 762,860 | |

Dell, Inc. (a) | | | 35,000 | | | | 525,350 | |

Flextronics International Ltd. (a) | | | 85,000 | | | | 666,400 | |

| Hewlett-Packard Company | | | 16,000 | | | | 850,400 | |

| International Business Machines Corporation | | | 9,500 | | | | 1,218,375 | |

| Microsoft Corporation | | | 27,000 | | | | 790,290 | |

| Western Union Company (The) | | | 17,000 | | | | 288,320 | |

| | | | | | | | 5,752,745 | |

| Materials — 3.9% | | | | | | | | |

| E.I. du Pont de Nemours and Company | | | 18,000 | | | | 670,320 | |

| RPM International, Inc. | | | 10,000 | | | | 213,400 | |

| Sealed Air Corporation | | | 42,000 | | | | 885,360 | |

| | | | | | | | 1,769,080 | |

| Telecommunication Services — 0.5% | | | | | | | | |

| Verizon Communications, Inc. | | | 7,500 | | | | 232,650 | |

| | | | | | | | | |

| Utilities — 2.0% | | | | | | | | |

| American Electric Power Company, Inc. | | | 14,000 | | | | 478,520 | |

| Duke Energy Corporation | | | 26,000 | | | | 424,320 | |

| | | | | | | | 902,840 | |

| | | | | | | | | |

Total Common Stocks (Cost $25,126,647) | | | | | | $ | 33,013,475 | |

| | | | | | |

| BB&T Capital Trust VII (Cost $550,000) | | | 22,000 | | | $ | 586,080 | |

U.S. GOVERNMENT & AGENCY OBLIGATIONS — 3.4% | | | | | | |

| U.S. Treasury Notes — 1.7% | | | | | | |

| 4.50%, due 11/15/2010 | | $ | 750,000 | | | $ | 769,570 | |

| | | | | | | | | |

| Federal Home Loan Bank — 1.7% | | | | | | | | |

| 4.375%, due 10/22/2010 | | | 750,000 | | | | 765,751 | |

| | | | | | | | | |

Total U.S. Government & Agency Obligations (Cost $1,505,741) | | | | | | $ | 1,535,321 | |

FBP BALANCED FUND SCHEDULE OF INVESTMENTS (Continued) |

| | | | | | |

| Consumer Staples — 1.7% | | | | | | |

| Kraft Foods, Inc., 5.625%, due 11/01/2011 | | $ | 750,000 | | | $ | 796,575 | |

| | | | | | | | | |

| Financials — 3.5% | | | | | | | | |

| Berkley (W.R.) Corporation, 5.60%, due 05/15/2015 | | | 750,000 | | | | 770,667 | |

| Prudential Financial, Inc., 5.80%, due 06/15/2012 | | | 750,000 | | | | 804,952 | |

| | | | | | | | 1,575,619 | |

| Health Care — 1.7% | | | | | | | | |

| UnitedHealth Group, Inc., 5.25%, due 03/15/2011 | | | 750,000 | | | | 778,804 | |

| | | | | | | | | |

| Industrials — 5.2% | | | | | | | | |

| Eaton Corporation, 5.95%, due 03/20/2014 | | | 750,000 | | | | 828,548 | |

| Ryder System, Inc., 5.00%, due 04/01/2011 | | | 750,000 | | | | 772,965 | |

| Union Pacific Corporation, 3.625%, due 06/01/2010 | | | 750,000 | | | | 753,488 | |

| | | | | | | | 2,355,001 | |

| Information Technology — 1.7% | | | | | | | | |

| Analog Devices, Inc., 5.00%, due 07/01/2014 | | | 750,000 | | | | 792,080 | |

| | | | | | | | | |

| Utilities — 3.5% | | | | | | | | |

| Ohio Power Company, 5.30%, due 11/01/2010 | | | 750,000 | | | | 769,136 | |

| SBC Communications, Inc., 5.875%, due 02/01/2012 | | | 750,000 | | | | 804,807 | |

| | | | | | | | 1,573,943 | |

| | | | | | | | | |

Total Corporate Bonds (Cost $7,498,721) | | | | | | $ | 7,872,022 | |

MONEY MARKET FUNDS — 5.0% | | | | | | |

Fidelity Institutional Money Market Government Portfolio - Class I, 0.04% (b) (Cost $2,252,232) | | | 2,252,232 | | | $ | 2,252,232 | |

| | | | | | | | | |

Total Investments at Value — 99.5% (Cost $36,933,341) | | | | | | $ | 45,259,130 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 0.5% | | | | | | | 247,604 | |

| | | | | | | | | |

| Total Net Assets — 100.0% | | | | | | $ | 45,506,734 | |

| ADR - American Depositary Receipt |

| |

| (a) | Non-income producing security. |

| | |

| (b) | Variable rate security. The rate shown is the 7-day effective yield as of March 31, 2010. |

| | |

| See accompanying notes to financial statements. |

THE FLIPPIN, BRUCE & PORTER FUNDS STATEMENTS OF ASSETS AND LIABILITIES March 31, 2010 |

| | | | | | |

| ASSETS | | | | | | |

| Investments in securities: | | | | | | |

| At acquisition cost | | $ | 22,686,059 | | | $ | 36,933,341 | |

| At value (Note 1) | | $ | 28,248,927 | | | $ | 45,259,130 | |

| Dividends and interest receivable | | | 36,106 | | | | 179,295 | |

Receivable for investment securities sold | | | 640,820 | | | | 427,688 | |

| Receivable for capital shares sold | | | 425 | | | | — | |

| Other assets | | | 6,270 | | | | 4,732 | |

| TOTAL ASSETS | | | 28,932,548 | | | | 45,870,845 | |

| | | | | | | | | |

| LIABILITIES | | | | | | | | |

| Distributions payable | | | 1,225 | | | | 24,299 | |

Payable for investment securities purchased | | | 287,810 | | | | 289,514 | |

| Payable for capital shares redeemed | | | 214 | | | | 10,130 | |

Accrued investment advisory fees (Note 3) | | | 16,064 | | | | 27,143 | |

| Payable to administrator (Note 3) | | | 4,700 | | | | 6,000 | |

| Other accrued expenses | | | 5,935 | | | | 7,025 | |

| TOTAL LIABILITIES | | | 315,948 | | | | 364,111 | |

| | | | | | | | | |

| NET ASSETS | | $ | 28,616,600 | | | $ | 45,506,734 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Paid-in capital | | $ | 27,379,006 | | | $ | 39,485,070 | |

| Undistributed (distributions in excess of) net investment income | | | (1,225 | ) | | | 4,877 | |

| Accumulated net realized losses from security transactions | | | (4,324,049 | ) | | | (2,309,002 | ) |

Net unrealized appreciation on investments | | | 5,562,868 | | | | 8,325,789 | |

| Net assets | | $ | 28,616,600 | | | $ | 45,506,734 | |

| | | | | | | | | |

| Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | | | 1,473,711 | | | | 2,937,816 | |

| | | | | | | | | |

| Net asset value, offering price and redemption price per share (Note 1) | | $ | 19.42 | | | $ | 15.49 | |

| See accompanying notes to financial statements. |

THE FLIPPIN, BRUCE & PORTER FUNDS STATEMENTS OF OPERATIONS Year Ended March 31, 2010 |

| | | | | | |

| INVESTMENT INCOME | | | | | | |

| Interest | | $ | 8 | | | $ | 534,653 | |

| Dividends | | | 480,639 | | | | 689,724 | |

Foreign withholding taxes on dividends | | | (6,432 | ) | | | (7,005 | ) |

TOTAL INVESTMENT INCOME | | | 474,215 | | | | 1,217,372 | |

| | | | | | | | | |

| EXPENSES | | | | | | | | |

| Investment advisory fees (Note 3) | | | 183,733 | | | | 294,117 | |

| Administration fees (Note 3) | | | 48,000 | | | | 58,821 | |

| Professional fees | | | 17,740 | | | | 19,240 | |

| Trustees’ fees and expenses | | | 14,702 | | | | 14,702 | |

| Registration fees | | | 11,664 | | | | 8,340 | |

| Compliance service fees (Note 3) | | | 8,400 | | | | 8,400 | |

| Custodian and bank service fees | | | 7,672 | | | | 8,923 | |

| Postage and supplies | | | 6,825 | | | | 5,868 | |

| Printing of shareholder reports | | | 5,125 | | | | 3,586 | |

| Insurance expense | | | 3,129 | | | | 4,725 | |

| Other expenses | | | 6,029 | | | | 8,365 | |

| TOTAL EXPENSES | | | 313,019 | | | | 435,087 | |

Fees voluntarily waived by the Adviser (Note 3) | | | (32,170 | ) | | | (14,920 | ) |

| NET EXPENSES | | | 280,849 | | | | 420,167 | |

| | | | | | | | | |

| NET INVESTMENT INCOME | | | 193,366 | | | | 797,205 | |

| | | | | | | | | |

| REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | | | | | | |

| Net realized gains on security transactions | | | 1,048,186 | | | | 1,458,838 | |

| Net realized gains on option contracts written | | | 28,944 | | | | 32,808 | |

| Net change in unrealized appreciation/depreciation on investments | | | 10,893,329 | | | | 12,459,369 | |

| | | | | | | | | |

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | | | 11,970,459 | | | | 13,951,015 | |

| | | | | | | | | |

NET INCREASE IN NET ASSETS FROM OPERATIONS | | $ | 12,163,825 | | | $ | 14,748,220 | |

| See accompanying notes to financial statements. |

THE FLIPPIN, BRUCE & PORTER FUNDS STATEMENTS OF CHANGES IN NET ASSETS |

| | | | | | | |

| | | | | | | | | | | | |

| FROM OPERATIONS | | | | | | | | | | | | |

| Net investment income | | $ | 193,366 | | | $ | 495,561 | | | $ | 797,205 | | | $ | 1,039,325 | |

| Net realized gains (losses) on: | | | | | | | | | | | | | | | | |

| Security transactions | | | 1,048,186 | | | | (5,387,493 | ) | | | 1,458,838 | | | | (3,859,162 | ) |

| Option contracts written | | | 28,944 | | | | (13,686 | ) | | | 32,808 | | | | 78,285 | |

| Net change in unrealized appreciation/depreciation on investments | | | 10,893,329 | | | | (11,397,617 | ) | | | 12,459,369 | | | | (12,251,683 | ) |

| Net increase (decrease) in net assets from operations | | | 12,163,825 | | | | (16,303,235 | ) | | | 14,748,220 | | | | (14,993,235 | ) |

| | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | | | | | | | | | |

| From net investment income | | | (205,334 | ) | | | (472,135 | ) | | | (838,744 | ) | | | (963,884 | ) |

| | | | | | | | | | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | | | | | | | | | |

| Proceeds from shares sold | | | 811,111 | | | | 1,826,232 | | | | 1,129,444 | | | | 1,127,417 | |

| Net asset value of shares issued in reinvestment of distributions to shareholders | | | 199,289 | | | | 459,482 | | | | 747,349 | | | | 868,323 | |

| Payments for shares redeemed | | | (4,957,268 | ) | | | (7,976,893 | ) | | | (4,478,899 | ) | | | (6,834,380 | ) |

| Net decrease in net assets from capital share transactions | | | (3,946,868 | ) | | | (5,691,179 | ) | | | (2,602,106 | ) | | | (4,838,640 | ) |

| | | | | | | | | | | | | | | | | |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | | | 8,011,623 | | | | (22,466,549 | ) | | | 11,307,370 | | | | (20,795,759 | ) |

| | | | | | | | | | | | | | | | | |

| NET ASSETS | | | | | | | | | | | | | | | | |

| Beginning of year | | | 20,604,977 | | | | 43,071,526 | | | | 34,199,364 | | | | 54,995,123 | |

| End of year | | $ | 28,616,600 | | | $ | 20,604,977 | | | $ | 45,506,734 | | | $ | 34,199,364 | |

| | | | | | | | | | | | | | | | | |

| UNDISTRIBUTED (DISTRIBUTIONS IN EXCESS OF) NET INVESTMENT INCOME | | $ | (1,225 | ) | | $ | 303 | | | $ | 4,877 | | | $ | 26,645 | |

| | | | | | | | | | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | | | | | | | | | |

| Shares sold | | | 50,497 | | | | 115,697 | | | | 83,529 | | | | 85,110 | |

| Shares reinvested | | | 12,030 | | | | 29,288 | | | | 53,343 | | | | 66,451 | |

| Shares redeemed | | | (303,238 | ) | | | (482,157 | ) | | | (317,389 | ) | | | (504,104 | ) |

| Net decrease in shares outstanding | | | (240,711 | ) | | | (337,172 | ) | | | (180,517 | ) | | | (352,543 | ) |

| Shares outstanding at beginning of year | | | 1,714,422 | | | | 2,051,594 | | | | 3,118,333 | | | | 3,470,876 | |

| Shares outstanding at end of year | | | 1,473,711 | | | | 1,714,422 | | | | 2,937,816 | | | | 3,118,333 | |

| See accompanying notes to financial statements. |

FBP VALUE FUND FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | |

| | | | |

| | | | | | | | | | | | | | | |

| Net asset value at beginning of year | | $ | 12.02 | | | $ | 20.99 | | | $ | 27.30 | | | $ | 26.60 | | | $ | 25.73 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.12 | | | | 0.27 | | | | 0.32 | | | | 0.33 | | | | 0.32 | |

| Net realized and unrealized gains (losses) on investments | | | 7.41 | | | | (8.98 | ) | | | (4.43 | ) | | | 2.71 | | | | 2.70 | |

| Total from investment operations | | | 7.53 | | | | (8.71 | ) | | | (4.11 | ) | | | 3.04 | | | | 3.02 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.13 | ) | | | (0.26 | ) | | | (0.32 | ) | | | (0.33 | ) | | | (0.32 | ) |

| Distributions from net realized gains | | | — | | | | — | | | | (1.68 | ) | | | (2.01 | ) | | | (1.83 | ) |

| Return of capital | | | — | | | | — | | | | (0.20 | ) | | | — | | | | — | |

| Total distributions | | | (0.13 | ) | | | (0.26 | ) | | | (2.20 | ) | | | (2.34 | ) | | | (2.15 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net asset value at end of year | | $ | 19.42 | | | $ | 12.02 | | | $ | 20.99 | | | $ | 27.30 | | | $ | 26.60 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return (a) | | | 62.84% | | | | (41.78% | ) | | | (16.33% | ) | | | 11.57% | | | | 12.03% | |

| | | | | | | | | | | | | | | | | | | | | |

Net assets at end of year (000’s) | | $ | 28,617 | | | $ | 20,605 | | | $ | 43,072 | | | $ | 60,233 | | | $ | 59,611 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratio of net expenses to average net assets | | | 1.07% | (b) | | | 1.07% | (b) | | | 1.01% | | | | 1.01% | | | | 1.01% | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratio of net investment income to average net assets | | | 0.74% | | | | 1.59% | | | | 1.21% | | | | 1.19% | | | | 1.17% | |

| | �� | | | | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 21% | | | | 16% | | | | 26% | | | | 16% | | | | 15% | |

| (a) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| | |

| (b) | Absent investment advisory fees voluntarily waived by the Adviser, the ratio of expenses to average net assets would have been 1.19% and 1.18% for the years ended March 31, 2010 and 2009, respectively (Note 3). |

| | |

| See accompanying notes to financial statements. |

FBP BALANCED FUND FINANCIAL HIGHLIGHTS |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | |

| | | | |

| | | | | | | | | | | | | | | |

| Net asset value at beginning of year | | $ | 10.97 | | | $ | 15.84 | | | $ | 18.95 | | | $ | 18.39 | | | $ | 18.06 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.27 | | | | 0.32 | | | | 0.38 | | | | 0.37 | | | | 0.33 | |

| Net realized and unrealized gains (losses) on investments | | | 4.53 | | | | (4.89 | ) | | | (2.01 | ) | | | 1.39 | | | | 1.22 | |

| Total from investment operations | | | 4.80 | | | | (4.57 | ) | | | (1.63 | ) | | | 1.76 | | | | 1.55 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.28 | ) | | | (0.30 | ) | | | (0.39 | ) | | | (0.37 | ) | | | (0.32 | ) |

| Distributions from net realized gains | | | — | | | | — | | | | (1.02 | ) | | | (0.83 | ) | | | (0.90 | ) |

| Return of capital | | | — | | | | — | | | | (0.07 | ) | | | — | | | | — | |

| Total distributions | | | (0.28 | ) | | | (0.30 | ) | | | (1.48 | ) | | | (1.20 | ) | | | (1.22 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net asset value at end of year | | $ | 15.49 | | | $ | 10.97 | | | $ | 15.84 | | | $ | 18.95 | | | $ | 18.39 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return (a) | | | 44.01% | | | | (29.15% | ) | | | (9.27% | ) | | | 9.70% | | | | 8.81% | |

| | | | | | | | | | | | | | | | | | | | | |

| Net assets at end of year (000’s) | | $ | 45,507 | | | $ | 34,199 | | | $ | 54,995 | | | $ | 66,358 | | | $ | 62,781 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratio of net expenses to average net assets | | | 1.00% | (b) | | | 1.00% | (b) | | | 0.96% | | | | 0.97% | | | | 0.99% | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratio of net investment income to average net assets | | | 1.90% | | | | 2.36% | | | | 2.05% | | | | 1.95% | | | | 1.75% | |

| | | | | | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 24% | | | | 24% | | | | 29% | | | | 17% | | | | 24% | |

| (a) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| | |

| (b) | Absent investment advisory fees voluntarily waived by the Adviser, the ratio of expenses to average net assets would have been 1.03% and 1.05% for the years ended March 31, 2010 and 2009 (Note 3). |

| | |

| See accompanying notes to financial statements. |

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS March 31, 2010 |

1. Organization and Significant Accounting Policies

The FBP Value Fund and the FBP Balanced Fund (the “Funds”) are no-load, diversified series of the Williamsburg Investment Trust (the “Trust”), an open-end management investment company registered under the Investment Company Act of 1940. The Trust was organized as a Massachusetts business trust on July 18, 1988. Other series of Williamsburg Investment Trust are not included in this report.

The FBP Value Fund seeks long term growth of capital through investment in a diversified portfolio comprised primarily of equity securities, with current income as a secondary objective.

The FBP Balanced Fund seeks long term capital appreciation and current income through investment in a balanced portfolio of equity and fixed income securities assuming a moderate level of investment risk.

The following is a summary of the Funds’ significant accounting policies:

Securities valuation — The Funds’ portfolio securities are valued as of the close of business of the regular session of the New York Stock Exchange (normally 4:00 p.m., Eastern time). Securities traded on a national stock exchange are valued based upon the closing price on the principal exchange where the security is traded. Securities which are quoted by NASDAQ are valued at the NASDAQ Official Closing Price. Securities which are traded over-the-counter are valued at the last sales price, if available, otherwise, at the last quoted bid price. It is expected that fixed income securities will ordinarily be traded in the over-the-counter market, and common stocks will ordinarily be traded on a national securities exchange, but may also be traded in the over-the-counter market. Call options written by the Funds are valued at t he then current market quotation, using the ask price as of the close of each day on the principal exchanges on which they are traded. Short-term instruments (those with remaining maturities of 60 days or less) may be valued at amortized cost, which approximates market value.

When market quotations are not readily available, securities may be valued on the basis of prices provided by an independent pricing service. The prices provided by the pricing service are determined with consideration given to institutional bid and last sale prices and take into account securities prices, yields, maturities, call features, ratings, institutional trading in similar groups of securities and developments related to specific securities. If a pricing service cannot provide a valuation, securities will be valued in good faith at fair value using methods consistent with those determined by the Board of Trustees. Such methods of fair valuation may include, but are not limited to: multiple of earnings, multiple of book value, discount from market of a similar freely traded security, purchase price of security, subsequent priva te transactions in the security or related securities, or a combination of these and other factors.

Accounting principles generally accepted in the United States (“GAAP”) establish a single authoritative definition of fair value, set out a framework for measuring fair value and require additional disclosures about fair value measurements. Various inputs are used in determining the value of each Fund’s investments. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – other significant observable inputs

• Level 3 – significant unobservable inputs

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities.

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS (Continued) |

The following is a summary of the inputs used to value each Fund’s investments as of March 31, 2010 by security type:

| FBP Value Fund | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | $ | 27,616,892 | | | $ | — | | | $ | — | | | $ | 27,616,892 | |

| Money Market Funds | | | — | | | | 632,035 | | | | — | | | | 632,035 | |

| Total | | $ | 27,616,892 | | | $ | 632,035 | | | $ | — | | | $ | 28,248,927 | |

| FBP Balanced Fund | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | $ | 33,013,475 | | | $ | — | | | $ | — | | | $ | 33,013,475 | |

| Preferred Stocks | | | 586,080 | | | | — | | | | — | | | | 586,080 | |

| U.S. Government & Agency Obligations | | | — | | | | 1,535,321 | | | | — | | | | 1,535,321 | |

| Corporate Bonds | | | — | | | | 7,872,022 | | | | — | | | | 7,872,022 | |

| Money Market Funds | | | — | | | | 2,252,232 | | | | — | | | | 2,252,232 | |

| Total | | $ | 33,599,555 | | | $ | 11,659,575 | | | $ | — | | | $ | 45,259,130 | |

Refer to each Fund’s Schedule of Investments for a listing of the common stocks and corporate bonds valued using Level 1 and Level 2 inputs by sector type.

Share valuation — The net asset value per share of each Fund is calculated daily by dividing the total value of its assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of each Fund is equal to its net asset value per share.

Investment income — Interest income is accrued as earned. Dividend income is recorded on the ex-dividend date. Discounts and premiums on fixed income securities purchased are amortized using the interest method.

Repurchase agreements — Each Fund may enter into repurchase agreements. A repurchase agreement, which is collateralized by U.S. Government obligations, is valued at cost which, together with accrued interest, approximates market value. At the time a Fund enters into a repurchase agreement, the Fund takes possession of the underlying securities and the seller agrees that the value of the underlying securities, including accrued interest, will at all times be equal to or exceed the face amount of the repurchase agreement. In addition, the Funds actively monitor and seek additional collateral, as needed. If the seller defaults, the fair value of the collateral may decline and realization of the collateral by the Funds may be delayed or limited.

Distributions to shareholders — Dividends arising from net investment income are declared and paid quarterly to shareholders of each Fund. Net realized short-term capital gains, if any, may be distributed throughout the year and net realized long-term capital gains, if any, are distributed at least once each year. The amount of distributions from net investment income and net realized gains are determined in accordance with federal income tax regulations, which may differ from GAAP. These “book/tax” differences are either temporary or permanent in nature.

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS (Continued) |

The tax character of distributions paid by each Fund during the years ended March 31, 2010 and March 31, 2009 is ordinary income.

Security transactions — Security transactions are accounted for on trade date. Gains and losses on securities sold are determined on a specific identification basis.

Common expenses — Common expenses of the Trust are allocated among the funds of the Trust based on relative net assets of each fund or the nature of the services performed and the relative applicability to each fund.

Options transactions — When the Funds’ investment adviser believes that individual portfolio securities held by the Funds are approaching the top of the adviser’s growth and price expectations, the Funds may write covered call options for which premiums are received and are recorded as liabilities, and are subsequently valued daily at the closing prices on their primary exchanges. Premiums received from writing options which expire are treated as realized gains. Premiums received from writing options which are exercised increase the proceeds used to calculate the realized gain or loss on the sale of the security. If a closing purchase transaction is used to terminate a Fund’s obligation on a call option, a gain or loss will be realized, depending upon whether the price of the closing purchase transaction is more or less than the premium previously received on the call option written.

Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax — It is each Fund’s policy to comply with the special provisions of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. As provided therein, in any fiscal year in which a Fund so qualifies and distributes at least 90% of its taxable net income, the Fund (but not the shareholders) will be relieved of federal income tax on the income distributed. Accordingly, no provision for income taxes has been made.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also each Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS (Continued) |

The following information is computed on a tax basis for each item as of March 31, 2010:

| | | FBP Value Fund | | | FBP Balanced Fund | |

| Cost of portfolio investments | | $ | 22,686,059 | | | $ | 36,929,609 | |

| Gross unrealized appreciation | | $ | 7,725,547 | | | $ | 10,494,345 | |

| Gross unrealized depreciation | | | (2,162,679 | ) | | | (2,164,824 | ) |

| Net unrealized appreciation | | | 5,562,868 | | | | 8,329,521 | |

| Undistributed ordinary income | | | — | | | | 25,444 | |

| Capital loss carryforwards | | | (4,324,049 | ) | | | (2,309,002 | ) |

| Other temporary differences | | | (1,225 | ) | | | (24,299 | ) |

| Total distributable earnings | | $ | 1,237,594 | | | $ | 6,021,664 | |

The difference between the federal income tax cost of portfolio investments and the financial statement cost for the FBP Balanced Fund is due to certain differences in the recognition of capital gains and losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to differing methods in the amortization of discounts and premiums on fixed income securities.

As of March 31, 2010, the Funds had the following capital loss carryforwards for federal income tax purposes:

| Expires March 31, | | FBP Value Fund | | | FBP Balanced Fund | |

| 2017 | | $ | 2,475,616 | | | $ | 1,823,332 | |

| 2018 | | | 1,848,433 | | | | 485,670 | |

| | | $ | 4,324,049 | | | $ | 2,309,002 | |

These capital loss carryforwards may be utilized in future years to offset net realized capital gains, if any, prior to distributing such gains to shareholders.

For the year ended March 31, 2010, the FBP Balanced Fund reclassified accumulated net realized gains from security transactions of $19,771 against undistributed net investment income on the Statements of Assets and Liabilities. For the year ended March 31, 2010, the FBP Value Fund reclassified distributions in excess of net investment income of $10,440 against paid-in capital on the Statements of Assets and Liabilities. Such reclassifications, the result of permanent differences between the financial statement and income tax reporting requirements, has no effect on the Funds’ net assets or net asset value per share.

The Funds recognize the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the tax positions taken on Federal income tax returns for all open tax years (tax years ended March 31, 2007 through March 31, 2010) of each Fund and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements.

2. Investment Transactions

During the year ended March 31, 2010, cost of purchases and proceeds from sales and maturities of investment securities, other than short-term investments and U.S. government securities, totaled $5,368,537 and $9,716,518, respectively, for the FBP Value Fund and $9,586,131 and $11,966,725, respectively, for the FBP Balanced Fund.

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS (Continued) |

3. Transactions with Affiliates

INVESTMENT ADVISORY AGREEMENT

The Funds’ investments are managed by Flippin, Bruce & Porter, Inc. (the “Adviser”) under the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, each Fund pays the Adviser a fee, which is computed and accrued daily and paid monthly, at an annual rate of .70% of its average daily net assets up to $250 million; .65% of the next $250 million of such assets; and .50% of such assets in excess of $500 million.

During the year ended March 31, 2010, the Adviser voluntarily waived $32,170 and $14,920 of its investment advisory fees from the FBP Value Fund and the FBP Balanced Fund, respectively.

Certain officers of the Trust are also officers of the Adviser.

MUTUAL FUND SERVICES AGREEMENT

Under the terms of a Mutual Fund Services Agreement between the Trust and Ultimus Fund Solutions, LLC (“Ultimus”), Ultimus provides administrative, pricing, accounting, dividend disbursing, shareholder servicing and transfer agent services for the Funds. For these services, Ultimus receives a monthly fee from each Fund at an annual rate of .15% of its average daily net assets up to $25 million, .125% of the next $25 million of such assets, and .10% of such assets in excess of $50 million, subject to a minimum monthly fee of $4,000; plus a shareholder recordkeeping fee at the annual rate of $10 per shareholder account in excess of 1,000 accounts. In addition, each Fund pays out-of-pocket expenses including, but not limited to, postage, supplies and costs of pricing portfolio securities. Certain officers of the Trust are also officers of Ultimus, or of Ultimus Fund Distributors, LLC (the “Distributor”), the principal underwriter of each Fund’s shares. The Distributor is compensated by the Adviser (not the Funds) for acting as principal underwriter.

COMPLIANCE CONSULTING AGREEMENT

Under the terms of a Compliance Consulting Agreement between the Trust and Ultimus, Ultimus provides an individual to serve as the Trust’s Chief Compliance Officer and to administer the Funds’ compliance policies and procedures. For these services, the Funds pay Ultimus an annual base fee of $16,800 plus an asset-based fee equal to 0.01% per annum on the Funds’ aggregate net assets in excess of $100 million. In addition, the Funds reimburse Ultimus for reasonable out-of-pocket expenses, if any, incurred in connection with these services.

4. Covered Call Options

Transactions in option contracts written by the Funds during the year ended March 31, 2010 were as follows:

| | | FBP Value Fund | | | FBP Balanced Fund | |

| | | Option Contracts | | | Option Premiums | | | Option Contracts | | | Option Premiums | |

| Options outstanding at beginning of year | | | — | | | $ | — | | | | — | | | $ | — | |

| Options written | | | 350 | | | | 101,574 | | | | 395 | | | | 105,185 | |

| Options expired | | | (145 | ) | | | (28,709 | ) | | | (170 | ) | | | (32,613 | ) |

| Options exercised | | | (205 | ) | | | (72,865 | ) | | | (225 | ) | | | (72,572 | ) |

| Options outstanding at end of year | | | — | | | $ | — | | | | — | | | $ | — | |

The average monthly notional amount of option contracts during the year ended March 31, 2010 was $840,958 and $882,917, respectively, for the FBP Value Fund and the FBP Balanced Fund.

THE FLIPPIN, BRUCE & PORTER FUNDS NOTES TO FINANCIAL STATEMENTS (Continued) |

5. Contingencies and Commitments

The Funds indemnify the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Funds. Additionally, in the normal course of business the Funds enter into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Funds’ maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Funds that have not yet occurred. However, based on experience, the Funds expect the risk of loss to be remote.

6. Subsequent Events

The Funds are required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statements of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Funds are required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

7. Recent Accounting Pronouncement

In January 2010, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2010-06 “Improving Disclosures about Fair Value Measurements.” ASU No. 2010-06 amends FASB Accounting Standards Codification Topic 820, Fair Value Measurements and Disclosures, to require additional disclosures regarding fair value measurements. Certain disclosures required by ASU No. 2010-06 are effective for interim and annual reporting periods beginning after December 31, 2009 and others for fiscal years beginning after December 15, 2010 and for interim periods within those fiscal years. Management is currently evaluating the impact ASU No. 2010-06 will have on the Funds’ financial statement disclosures.

THE FLIPPIN, BRUCE & PORTER FUNDS REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

The Board of Trustees and Shareholders of

the FBP Value Fund and the FBP Balanced Fund

of the Williamsburg Investment Trust

We have audited the accompanying statements of assets and liabilities, including the schedules of investments, of the FBP Value Fund and the FBP Balanced Fund (the “Funds”) (each a series of the Williamsburg Investment Trust), as of March 31, 2010, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Funds’ internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclo sures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of March 31, 2010, by correspondence with the custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the FBP Value Fund and the FBP Balanced Fund at March 31, 2010, the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Cincinnati, Ohio

May 27, 2010

THE FLIPPIN, BRUCE & PORTER FUNDS BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) |

Overall responsibility for management of the Fund rests with the Board of Trustees. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement or removal. The Trustees, in turn, elect the officers of the Fund. The officers have been elected for an annual term. The following are the Trustees and executive officers of the Fund:

| | Trustee | Address | Age | Position Held with the Trust | Length of Time Served |

| * | Charles M. Caravati, Jr. | 931 Broad Street Road Manakin-Sabot, VA | 73 | Chairman and Trustee | Since June 1991 |

| * | Austin Brockenbrough III | 1802 Bayberry Court, Suite 400 Richmond, VA | 73 | Trustee | Since September 1988 |

| * | John T. Bruce | 800 Main Street Lynchburg, VA | 56 | Trustee | Since September 1988 |

| | Robert S. Harris | 100 Darden Boulevard Charlottesville, VA | 60 | Trustee | Since January 2007 |

| | J. Finley Lee, Jr. | 448 Pond Apple Drive North Naples, FL | 70 | Trustee | Since September 1988 |

| | Richard L. Morrill | University of Richmond Richmond, VA | 70 | Trustee | Since March 1993 |

| | Harris V. Morrissette | 100 Jacintoport Boulevard Saraland, AL | 50 | Trustee | Since March 1993 |

| | Samuel B. Witt III | 302 Clovelly Road Richmond, VA | 74 | Trustee | Since November 1988 |

| | John M. Flippin | 800 Main Street Lynchburg, VA | 68 | Vice President | Since September 1988 |

| | R. Gregory Porter III | 800 Main Street Lynchburg, VA | 68 | Vice President | Since September 1988 |

| | John H. Hanna IV | 800 Main Street Lynchburg, VA | 54 | Vice President | Since February 2007 |

| | David J. Marshall | 800 Main Street Lynchburg, VA | 53 | Vice President | Since February 2007 |

| | Robert G. Dorsey | 225 Pictoria Drive, Suite 450 Cincinnati, OH | 53 | Vice President | Since November 2000 |

| | Mark J. Seger | 225 Pictoria Drive, Suite 450 Cincinnati, OH | 48 | Treasurer | Since November 2000 |

| | John F. Splain | 225 Pictoria Drive, Suite 450 Cincinnati, OH | 53 | Secretary | Since November 2000 |

| | Tina H. Bloom | 225 Pictoria Drive, Suite 450 Cincinnati, OH | 41 | Chief Compliance Officer | Since August 2006 |

| * | Messrs. Bruce and Brockenbrough, as affiliated persons of investment advisers to the Trust, are “interested persons” of the Trust within the meaning of Section 2(a)(19) of the Investment Company Act of 1940. Charles M. Caravati, Jr. is the father of Charles M. Caravati III, an officer of The Jamestown Funds, which are other series of the Trust. |

THE FLIPPIN, BRUCE & PORTER FUNDS BOARD OF TRUSTEES AND EXECUTIVE OFFICERS (Unaudited) (Continued) |

Each Trustee oversees nine portfolios of the Trust, including the Fund. The principal occupations of the Trustees and executive officers of the Fund during the past five years and public directorships held by the Trustees are set forth below:

Charles M. Caravati, Jr. is a retired physician. He is also the retired President of Dermatology Associates of Virginia, P.C.

Austin Brockenbrough III is President and Managing Director of Lowe, Brockenbrough & Company, Inc. (an investment advisory firm). He is a member of the Board of Directors of Tredegar Corporation (a plastics manufacturer) and Wilkinson O’Grady & Co., Inc. (a global asset manager).

John T. Bruce is a Principal of Flippin, Bruce & Porter, Inc. (an investment advisory firm).

Robert S. Harris is the C. Stewart Sheppard Professor of Business Administration at The Darden Graduate School of Business Administration at the University of Virginia. He was previously the dean at Darden. Professor Harris has published widely on corporate finance, financial markets and mergers and acquisitions and has served as a consultant to corporations and government agencies.

J. Finley Lee, Jr. is a financial consultant and the Julian Price Professor Emeritus at the University of North Carolina.

Richard L. Morrill serves as President of the Teagle Foundation (charitable foundation) and Chancellor of the University of Richmond. He is also a member of the Board of Directors of Tredegar Corporation and Albemarle Corporation (specialty chemical manufacturer).

Harris V. Morrissette is President of China Doll Rice and Beans Inc. and Dixie Lily Foods. He is a member of the Board of Directors of BancTrust Financial Group, Inc. (a bank holding company). In addition, he is Chairman of Azalea Aviation, Inc. (an airplane fueling company).

Samuel B. Witt III is the retired Senior Vice President and General Counsel of Stateside Associates, Inc. He is also a member of the Board of Directors of The Swiss Helvetia Fund, Inc. (a closed-end investment company).

John M. Flippin is a Principal of the Adviser.

R. Gregory Porter III is a Principal of the Adviser.

John H. Hanna IV is a Principal of the Adviser.

David J. Marshall is a Principal of the Adviser.

Robert G. Dorsey is a Managing Director of Ultimus Fund Solutions, LLC and Ultimus Fund Distributors, LLC.

Mark J. Seger is a Managing Director of Ultimus Fund Solutions, LLC and Ultimus Fund Distributors, LLC.

John F. Splain is a Managing Director of Ultimus Fund Solutions, LLC and Ultimus Fund Distributors, LLC.

Tina H. Bloom is Vice President of Administration of Ultimus Fund Solutions, LLC.

Additional information about members of the Board of Trustees and executive officers is available in the Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call 1-800-281-3217.

THE FLIPPIN, BRUCE & PORTER FUNDS ABOUT YOUR FUNDS’ EXPENSES (Unaudited) |

We believe it is important for you to understand the impact of costs on your investment. All mutual funds have operating expenses. As a shareholder of the Funds, you incur ongoing costs, including management fees and other operating expenses. These ongoing costs, which are deducted from each Fund’s gross income, directly reduce the investment return of the Funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The examples below are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period (October 1, 2009 through March 31, 2010).

The table below illustrates each Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from each Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Funds. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Funds under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Funds’ ongoing costs with those of other mutual funds. It assumes that each Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the returns used are not the Funds’ actual returns, the results do not apply to your investment. The example is useful in making comparisons because the Securities and Exchange Commission (“SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess each Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Funds do not charge sales loads or redemption fees, nor do they carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

More information about the Funds’ expenses, including annual expense ratios for the past five fiscal years, can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Funds’ prospectus.

FBP Value Fund

| | Beginning Account Value October 1, 2009 | Ending Account Value March 31, 2010 | Expenses Paid During Period* |

Based on Actual Fund Return | $1,000.00 | $1,127.40 | $5.68 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,019.60 | $5.39 |

| * | Expenses are equal to the FBP Value Fund’s annualized expense ratio of 1.07% for the period, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

THE FLIPPIN, BRUCE & PORTER FUNDS ABOUT YOUR FUNDS’ EXPENSES (Unaudited) (Continued) |

FBP Balanced Fund

| | Beginning Account Value October 1, 2009 | Ending Account Value March 31, 2010 | Expenses Paid During Period* |

Based on Actual Fund Return | $1,000.00 | $1,099.70 | $5.23 |

| Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,019.95 | $5.04 |

| * | Expenses are equal to the FBP Balanced Fund’s annualized expense ratio of 1.00% for the period, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

OTHER INFORMATION (Unaudited) |

The Trust files a complete listing of portfolio holdings for the Funds with the SEC as of the first and third quarters of each fiscal year on Form N-Q. The filings are available upon request, by calling 1-800-327-9375. Furthermore, you may obtain a copy of these filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-800-327-9375, or on the SEC’s website at http://www.sec.gov. Information regarding how the Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is also available without charge upon request by calling toll-free 1-800-327-9375, or on the SEC’s website at http://www.sec.gov.

FEDERAL TAX INFORMATION (Unaudited) |

In accordance with federal tax requirements, the following provides shareholders with information concerning distributions from ordinary income made by the Funds during the year ended March 31, 2010. For the fiscal year ended March 31, 2010, certain dividends paid by the Funds may be subject to a maximum tax rate of 15%, as provided by the Jobs and Growth Tax Relief Reconciliation Act of 2003. The FBP Value Fund and the FBP Balanced Fund intend to designate up to a maximum amount of $205,334 and $838,744, respectively, as taxed at a maximum rate of 15%. Additionally, for the fiscal year ended March 31, 2010, 100% and 73% of the dividends paid from ordinary income by the FBP Value Fund and the FBP Balanced Fund, respectively, qualified for the dividends received deduction for corporations. As required by federal regulations, complete in formation will be computed and reported in conjunction with your 2010 Form 1099-DIV.

THE FLIPPIN, BRUCE & PORTER FUNDS DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) |

At an in-person meeting held on February 9, 2010, the Board of Trustees, including a majority of the Independent Trustees, approved the continuance for a one-year period of the Investment Advisory Agreements with the Adviser on behalf of the FBP Value Fund and the FBP Balanced Fund. Below is a discussion of the factors considered by the Board of Trustees along with their conclusions with respect thereto that formed the basis for the Board’s approvals.

In selecting the Adviser and approving the continuance of the Investment Advisory Agreements, the Trustees considered all information they deemed reasonably necessary to evaluate the terms of the Agreements. The principal areas of review by the Trustees were the nature, extent and quality of the services provided by the Adviser and the reasonableness of the fees charged for those services. These matters were considered by the Independent Trustees consulting with experienced counsel for the Independent Trustees, who is independent of the Adviser.

The Trustees’ evaluation of the quality of the Adviser’s services took into account their knowledge and experience gained through meetings with and reports of the Adviser’s senior management over the course of the preceding year. Both short-term and long-term investment performance of the Funds was considered. Each Fund’s performance was compared to its performance benchmark and to that of competitive funds with similar investment objectives and to the Adviser’s comparably managed private accounts. The Trustees also considered the scope and quality of the in-house capabilities of the Adviser and other resources dedicated to performing services for the Funds. The quality of administrative and other services, including the Adviser’s role in coordinating the activities of the Funds’ other service providers, were considered in light of the Funds’ compliance with investment policies and applicable laws and regulations and of related reports by management and the Funds’ independent public accounting firm in periodic meetings with the Trust’s Audit Committee. The Trustees also considered the business reputation of the Adviser, the qualifications of its key investment and compliance personnel, and its financial resources.

In reviewing the fees payable under the Investment Advisory Agreements, the Trustees compared the advisory fees and overall expense levels of each Fund with those of competitive funds with similar investment objectives as well as the private accounts managed by the Adviser. The Trustees considered information provided by the Adviser concerning the Adviser’s profitability with respect to each Fund, including the assumptions and methodology used in preparing the profitability information, in light of applicable case law relating to advisory fees. For these purposes, the Trustees took into account not only the fees paid by the Funds, but also so-called “fallout” benefits to the Adviser, such as the benefits of research made available to the Adviser by reason of brokerage commissions generated by the Funds’ securiti es transactions. The Trustees also reviewed the revenue sharing arrangements relating to the Funds, whereby fees are paid by the Adviser to various intermediaries that direct assets to the Funds. In evaluating the Funds’ advisory fees, the Trustees took into account the complexity and quality of the investment management of the Funds.

Based upon their review of this information, the Independent Trustees concluded that: (i) based upon the performance of each Fund during 2009, which exceeded the returns of its primary benchmark and Lipper peer group average, as well as the longer term performance of each Fund, and the services provided to shareholders, the Adviser has provided quality services to the Funds as compared to similarly managed funds; (ii) although the contractual advisory fee rates for each Fund are in the higher range of fees for other comparably managed funds, the Independent Trustees believe the fees to be reasonable given the scope and

THE FLIPPIN, BRUCE & PORTER FUNDS DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued) |

quality of services provided by the Adviser; (iii) the total operating expense ratio of each Fund is lower than the average expense ratio for comparably managed funds, according to statistics derived from Morningstar, Inc.; and (iv) the Adviser’s voluntary waivers of a portion of its advisory fees has enabled each Fund to further increase returns for shareholders. The Board noted that the Adviser’s profitability analysis indicated that the Adviser did not derive any profits from its management of the Funds over the past year. Given the current size of the Funds and their expected growth, the Independent Trustees did not believe that at the present time it would be relevant to consider the extent to which economies of scale would be realized as the Funds grow, and whether fee levels reflect these economies of scale. The Inde pendent Trustees also considered the “fallout” benefits to the Adviser with respect to the Funds, but given the amounts involved viewed these as secondary factors in connection with the evaluation of the reasonableness of the advisory fees paid by the Funds.

No single factor was considered in isolation or to be determinative to the decision of the Trustees to approve continuance of the Investment Advisory Agreements. Rather the Trustees concluded, in light of a weighing and balancing of all factors considered, that it was in the best interests of each Fund and its shareholders to continue its Investment Advisory Agreement without modification to its terms, including the fees charged for services thereunder.

| | | | | | | |

| | | | | | | |

| | | |

| | | |

| | | | Investment Adviser Flippin, Bruce & Porter, Inc. 800 Main Street, Second Floor P.O. Box 6138 Lynchburg, Virginia 24505 Toll-Free 1-800-327-9375 www.fbpinc.com

Administrator Ultimus Fund Solutions, LLC P.O. Box 46707 Cincinnati, Ohio 45246-0707 Toll-Free 1-866-738-1127

Custodian US Bank NA 425 Walnut Street Cincinnati, Ohio 45202

Independent Registered Public Accounting Firm Ernst & Young LLP 1900 Scripps Center 312 Walnut Street Cincinnati, Ohio 45202 | Legal Counsel Sullivan & Worcester LLP One Post Office Square Boston, Massachusetts 02109

Officers John T. Bruce, President and Portfolio Manager John M. Flippin, Vice President R. Gregory Porter, III, Vice President John H. Hanna, IV, Vice President David J. Marshall, Vice President

Trustees Austin Brockenbrough, III John T. Bruce Charles M. Caravati, Jr. Robert S. Harris J. Finley Lee, Jr. Richard L. Morrill Harris V. Morrissette Samuel B. Witt, III | | | |

| | | | | | | |

| | | | | | | | |

| | | | | | | |

THE GOVERNMENT STREET FUNDS No-Load Mutual Funds Annual Report March 31, 2010 |

The Government Street Equity Fund The Government Street Mid-Cap Fund The Alabama Tax Free Bond Fund |

| LETTER FROM THE PRESIDENT | May 13, 2010 |

Dear Fellow Shareholders:

We are enclosing for your review the Annual Report for The Government Street Funds for the year ended March 31, 2010.

The Government Street Equity Fund

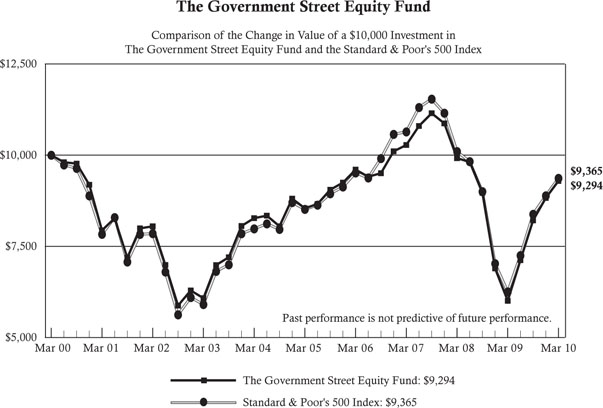

The Government Street Equity Fund had a positive 54.71% total return for the fiscal year ended March 31, 2010. By comparison, the S&P 500 Index and the Morningstar Large Blend Equity category were up 49.77% and 50.08%, respectively. In direct contrast to the previous year, the returns were products of an equity market that was positive across all capitalizations and economic sectors. “A rising tide was lifting all ships.”

The current Administration and the Congress have ratified tremendous economic stimulus plans to activate the economy. The amounts of absolute debt incurred in the process are unprecedented. It is certain that these actions have given a reprieve to financial institutions on the brink of fiscal disaster. The result appears to have set the nation’s economy on a slow and arduous recovery. At this point the stock market, as reflected in the explosive positive return, seems to have bought into the prospect of recovery. There is little doubt that such activities will be manifested in a myriad of reactions and counter-reactions that will directly impact investment returns in the future.