Washington, D.C. 20549

W. Lee H. Dunham, Esq.

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

THE DAVENPORT FUNDS LETTER TO SHAREHOLDERS | |

Equity markets roared higher in the quarter ended March 31, 2013. The S&P 500 Index gained 10.61%, the Dow Jones Industrial Average advanced 11.93% and the Russell 2000 Index surged 12.39%. The Dow and S&P have both been hitting fresh all-time highs. Early in the quarter, markets bounced as fear of an acute event associated with the “fiscal cliff” waned. In fact, the S&P 500 posted its best January since 1997. Subsequently, markets shrugged off fears surrounding sequestration in the U.S. (i.e. mandated government spending cuts), a slowdown in domestic consumer spending, and fresh budget woes in Europe.

Why the rally? For one, economic and corporate fundamentals appear to be improving. Credit Suisse First Boston (CSFB) recently noted: “The idea that the cliff, or the election, held back the economy heading into year-end is everywhere but in the actual data.” Corporate earnings have generally exceeded expectations, implying estimates for 2013 earnings could move upward. The unemployment rate has continued to decline, the housing market is rebounding sharply, and consumer spending has proven resilient in the face of higher gas prices and payroll taxes. Furthermore, the financial system is on much stronger footing as evidenced by most banks’ solid showing in the recent “stress test.”

We’ve also begun to see a pickup in mergers & acquisitions, with deal value up 14% year-over-year according to CSFB. Further takeout activity makes sense given that deal value is still running 36% below its 10-year average in the U.S. and 64% below average in Europe. Given depressed financing costs and leverage levels near a 20-year low, most companies certainly have the capacity to look at opportunities. Alternatively, many of these companies may look to repurchase their own stock. CSFB points out that more optimal leverage could allow companies to buy back 9% of the market capitalization of the U.S. Both takeouts and share repurchase activity shrink the available supply of equities and are generally supportive for the market.

Perhaps most notable, we’ve begun to see money flows shift. After five years of bond inflows dwarfing stock inflows, billions have flowed into equity funds year-to-date as fear has abated and stocks have flexed their muscle as a relatively attractive asset class. Many investors and money managers have been under-exposed to equities; hence, improving market conditions have created somewhat of a “buying panic.” At times in the past, such a surge of money into stocks has been a warning signal. But we’re hopeful that it can last more than three months (especially when considering how long it went the other way). We’re also comforted by the fact that valuations remain reasonable by historical standards (S&P trades for 14.5x earnings) and, while we are close to all-time highs, we’re just getting back to the prior market peaks of 2000 and 2007.

As always, there are factors that could derail the market’s momentum. The U.S. budget deficit, peaking corporate profit margins, fiscal issues in Europe, and slowing growth in China are threats that come to mind. However, the “elephant in the room” appears to be the threat of a shift in interest rates. Interest rates have been declining for many years alongside a secular bull market for bonds and remain depressed (a 10-year Treasury currently yields 1.9%) due in great

part to monetary policy. Ironically, we seem to run the risk of things getting too good. That is, if economic momentum builds too quickly, we are likely to see policy shift and interest rates hit a much anticipated inflection point.

BCA Research points out that U.S. stocks have historically suffered swift corrections following the end of long bull cycles for Treasuries (for more information, please visit www.bcaresearch.com). When looking at four prior cycles, they note that stocks have seen mean declines exceeding 20% over just 10 months once the bull cycle ends and interest rates turn upward. This is clearly an alarming statistic; however, BCA also notes that equities go on to generate robust long-term returns. In fact, the 10-year compound annual growth rate for equities after the end of those same cycles was roughly 9%. In other words, investors were rewarded with substantial long-term gains after some short-term pain. We acknowledge the world seems to be floating on “cheap money” and recognize higher rates may ultimately put a damper on the market, but this could prove very difficult to time and history suggests we shouldn’t try.

In sum, we still think the big picture for equities looks pretty good. When we started the year, we suggested stocks seemed positioned to enjoy a good 2013, albeit probably not as good as 2012. Now, we find ourselves in the interesting predicament of having squeezed a lot of return into a short period of time. Such gains can’t be sustained at this pace and we suspect a hiccup is forthcoming. While our antennas are up, we aren’t market timers and will continue to focus on the simple but time-tested strategy of owning shares of good businesses for an extended period.

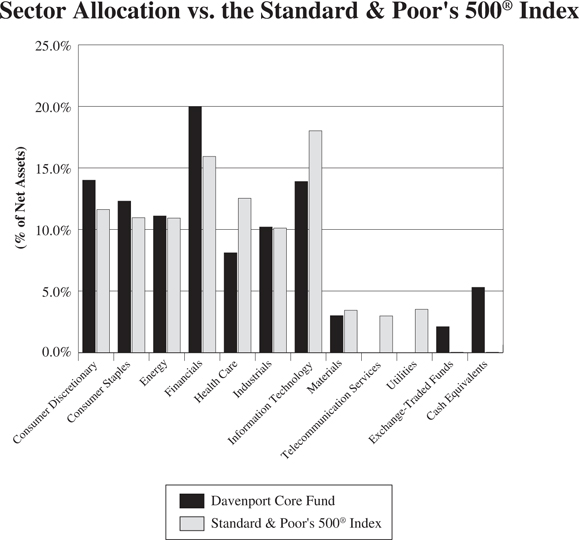

Davenport Core Fund

The following chart represents Davenport Core Fund (the “Core Fund”) performance and the performance of the S&P 500 Index*, the Core Fund’s primary benchmark, for the periods ended March 31, 2013.

| | | | | | | Fiscal Year 2013 Expense Ratio |

| Core Fund | 9.34% | 12.47% | 12.34% | 5.39% | 8.76% | 5.29% | 0.95% |

| S&P 500 Index* | 10.61% | 13.96% | 12.67% | 5.81% | 8.53% | 5.25% | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An index is not available for direct investment; therefore, its performance does not reflect the expenses, fees and taxes generally paid with the active management of an actual portfolio. |

| | |

| ** | Annualized. |

The Core Fund advanced 12.47% during the year ended March 31, 2013, slightly lagging the 13.96% gain for the S&P 500 Index. Though we lagged the benchmark slightly, we are very pleased to have had such a strong year of absolute returns. Furthermore, we were especially encouraged to close the fiscal year with strong fourth quarter results.

Though most of the Energy sector struggled throughout the fiscal year, leading oil refiner, Valero Energy (VLO), was the Core Fund’s top performer as it became evident that the company is a key beneficiary of increasing domestic oil production. Other key contributors included the Fund’s holdings in Visa (V), CarMax (KMX), and News Corp. (NWSA). Ironically, in what was one of the best quarters of all time for the S&P 500, historically defensive sectors such as Consumer Staples and Health Care produced the biggest gains during the fourth quarter. In Consumer Staples, Walgreen (WAG), J.M. Smucker (SJM) and PepsiCo (PEP) were standouts. WAG gained nearly 30% in Q4 on the heels of better results and a major distribution announcement with recently purchased drug distribution and logistics company, AmerisourceBergen (ABC). Despite serving as a headwind for much of the fiscal year, being underweight Apple (AAPL) contributed positively to relative performance as the shares pulled back. We feel the shares look much more reasonably valued at current levels, reflecting some of the challenges inherent in maintaining a high rate of profitability and revenue growth.

Within the Financials sector, we made various opportunistic transactions that we believe have repositioned the Core Fund’s exposure to this sector positively. For one, we elected to sell names such as Fiserv (FISV), Bank of America (BAC) and T. Rowe Price (TROW), all of which were hitting new highs and seemed to be more fairly valued. With the proceeds from these transactions, we were able to add to high-conviction ideas such as Markel (MKL) and Capital One (COF), both of which had fallen under pressure. In the case of MKL, the stock sold off meaningfully following a major acquisition announcement. As a result, we were able to purchase the shares around book value, which we thought was very attractive in light of the company’s track record of compounding book value at an impressive rate over the last 20 years. In terms of COF, the stock had weakened in response to disappointing results and asset sales that surprised investors. While disappointed in these developments, we believed the resulting valuation discount to peers was simply too excessive given the company’s significant earnings power.

Near the end of the year, we elected to add to the Fund’s position in Danaher Corp. (DHR). We have long regarded DHR as one of the highest quality names in the Industrials sector due to management’s impressive track record of cash generation and above-average returns on capital. The stock has performed well over the years and currently sits near all time highs; however, we feel the shares are attractively valued at current levels given the company’s best-in-class management team, high quality portfolio of assets, and free cash flow yield in the high single digits. While we believe management will continue to wring out efficiencies from its current portfolio of businesses (pushing free cash flow and returns higher), we also note that the company is well positioned to deploy significant amounts of incremental capital via acquisitions and buybacks. Given management’s virtually unrivaled success with acquisitions over the decades, we believe further Mergers & Acquisitions (M&A) can be meaningfully accretive to shareholder value over time.

In conclusion, we are pleased with recent results and remain constructive on the outlook for the coming year. Though we are doubtful that the pace of gains seen in the fiscal fourth quarter can continue, we are comfortable with the Core Fund’s positioning and continue to think large cap stocks look attractive.

New Positions

Amgen, Inc. (AMGN) is a leading biotechnology firm with core franchises in nephrology, oncology and inflammatory diseases.

AmerisourceBergen Corporation (ABC) is a leading drug distribution and logistics company. After our initial purchase, we subsequently increased the Fund’s position in ABC.

General Electric Company (GE) is an industrial conglomerate with exposure to core markets such as energy, aerospace, health care, transportation and finance.

Increased Positions

Aon plc (AON)** is an insurance brokerage and human resources outsourcing firm.

Danaher Corporation (DHR) is a large, well-diversified manufacturing company with a long track record of achieving best-in-class returns through acquiring smaller competitors and improving operations though Danaher Business System.

Markel Corporation (MKL) is a Richmond, VA-based specialty insurer.

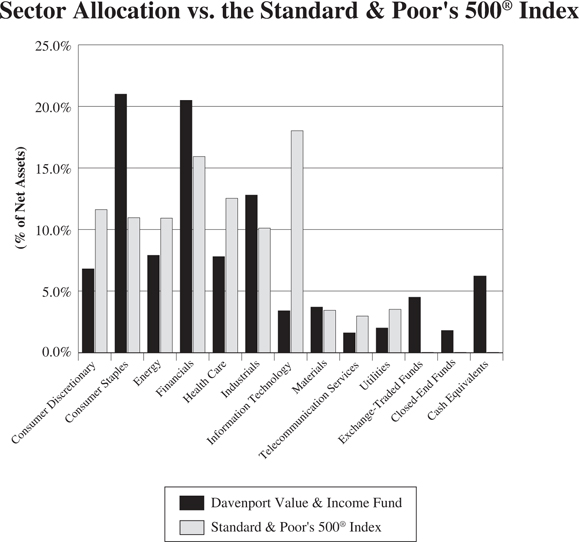

Davenport Value & Income Fund

The following chart represents Davenport Value & Income Fund (the “Value & Income Fund”) performance and the performance of the S&P 500 Index, the Value & Income Fund’s primary benchmark, and the Lipper Equity Income Index for the periods ended March 31, 2013.

| | | Since Inception** 12/31/2010 | Fiscal Year 2013 Expense Ratio |

| Value & Income Fund | 12.61% | 18.69% | 16.28% | 0.96% |

| S&P 500 Index* | 10.61% | 13.96% | 12.78% | — |

| Lipper Equity Income Index* | 10.59% | 15.06% | 12.03% | — |

30-Day SEC Yield: 1.81%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Lipper Equity Income Index is an unmanaged index of the 30 largest funds, based on total year-end net asset value, in the Lipper Equity Income Index. An index is not available for direct investment; therefore, its performance does not reflect the expenses, fees and taxes generally paid with the active management of an actual portfolio. |

| | |

| ** | Annualized. |

The Value & Income Fund advanced 18.69% during the year ended March 31, 2013, nicely exceeding the 13.96% and 15.06% gain for the S&P 500 Index and the Lipper Equity Income Index, respectively. After taking a bit of a breather to close 2012, it was impressive to see the strategy close the year with a 12.61% gain in fiscal Q4. As retail fund flows finally started to move towards equity funds to close the year, it was clear that income is still a top priority on investors’ wish list. The Value & Income Fund’s 30-day SEC yield as of March 31, 2013 was 1.81%.

Housing related companies exhibited strong performance during the fiscal year as improving industry data coupled with the Federal Reserve System’s announcement of QE3 fueled gains across the group. Weyerhaeuser (WY) and Fidelity National Financial (FNF) were top performers as each company benefitted from the aforementioned developments. The Fund also benefitted from strong performance within the REIT sector, where holdings such as Sun Communities (SUI) and W.P. Carey (WPC) posted strong gains. Despite a very good year from Johnson & Johnson (JNJ), the Health Care sector was a key detractor from relative performance given relatively weak results from the Fund’s holdings in GlaxoSmithKline (GSK) and WellPoint (WLP).

The Energy sector was a source of strength during the fiscal year, with Marathon Petroleum (MPC) and Tortoise Energy Infrastructure (TYG) emerging as top performers. Despite our belief in the long-term attractiveness of the domestic refining industry, we elected to chip the Fund’s position in MPC given the stock’s sharp move and considering the extreme volatility of the refining industry. In addition to the chip of MPC, the fiscal fourth quarter saw a lot of activity in the Energy space. As a result, the Fund’s exposure to the sector has decreased slightly and has become more focused on companies with what we believe is above-average potential for dividend growth.

In keeping with this theme, we added to the Fund’s position in BP plc (BP) and sold the position in Royal Dutch Shell (RDS’B). RDS’B has lagged the Energy sector amid disappointing results and concerns regarding the company’s increasing capital expenditure profile. Though we are confident in the company’s ability to maintain its healthy dividend (yields over 5%), we are concerned that increasing capital expenditures will limit future dividend growth. While BP has a similar dividend yield (5.1%), we feel the steps the company has taken to restructure the business could lead to significant increases in returns, cash flows and the dividend in coming years. Although there is still ample headline risk related to the ongoing Macondo spill civil trial, we believe decidedly negative outcomes have already been priced into the shares. As such, any resolution of the matter should remove an overhang and allow the stock to move higher.

Later in the year, we purchased a position in regional gaming operator Penn National Gaming (PENN). On Nov 15th, the company announced that it intends to split its real estate and operating assets into two separate companies. To summarize the transaction, one entity will be structured as a REIT, which we anticipate will pay an attractive dividend and have substantial growth opportunity, while the other entity will be a smaller casino operator that could grow significantly. We have a long history with the company and view management as being among the sharpest value creators we’ve encountered. This new structure (first of its kind in the industry) could be another feather in their cap. Insider ownership is high and management acts more like shareholders/owners as a result. Further, we were excited to see the company’s CFO purchase a substantial amount of stock in the high $40’s after the deal was announced. Ultimately, we think the value of the combined entity could have significant price appreciation as the transaction comes closer to being consummated in early 2014. Also, bear in mind this will ultimately be two separate positions, one of which we anticipate will pay a meaningful dividend (approximately 8.5% yield implied by the valuation at the time of purchase), and both of which could have attractive long-term growth opportunities.

While we are certainly happy with this year’s performance, we remain thoughtful about the Value & Income Fund’s positioning and are vigilantly committed to finding new ideas. Though we will always focus on high-quality companies with above-average payouts, we continue to seek a balance between higher yielding defensive stocks and those that have the ability to grow their dividends over time.

New Positions

Capital One Financial Corporation (COF) is a credit card and consumer banking franchise. After our initial purchase, we subsequently increased the Fund’s position in COF. Current yield: 0.4%.

Penn National Gaming, Inc. (PENN) is a regional casino operator with an attractive portfolio of 19 casinos throughout the United States. Current yield: N/A. PENN is currently in the process of becoming a REIT.

WisdomTree Japan Hedged Equity Fund (DXJ) Current yield: 1.3%.

Increased Positions

BP plc (BP)** is headquartered in the United Kingdom and is a one of the world’s leading integrated energy companies with operations in over one hundred countries worldwide. Current yield: 5.1%.

The Dow Chemical Company (DOW) is a global chemical innovator and producer. Current yield: 4.0%.

General Electric Company (GE) is an industrial conglomerate with exposure to core markets such as energy, aerospace, health care, transportation and finance. Current yield: 3.3%.

Hartford Financial Services Group, Inc. (HIG) is a multi-line insurer. Current yield: 1.6%.

LinnCo, LLC (LNCO) is a C-Corp formed for the sole purpose to invest in the units of upstream oil and gas Master Limited Partnership (MLP) Linn Energy (LINE). Current yield: 7.3%.

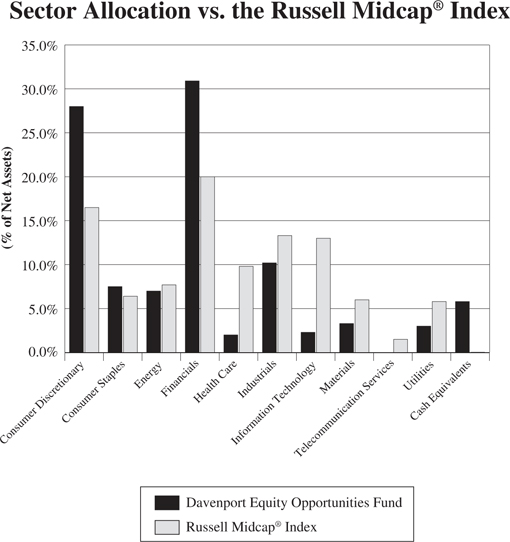

Davenport Equity Opportunities Fund

The following chart represents Davenport Equity Opportunities Fund (the “Equity Opportunities Fund”) performance and the performance of the Russell Midcap Index, the Fund’s primary benchmark, and the S&P 500 Index for the periods ended March 31, 2013.

| | | Since Inception** 12/31/2010 | Fiscal Year 2013 Expense Ratio |

| Equity Opportunities Fund | 11.33% | 18.77% | 17.11% | 1.01% |

| Russell Midcap Index* | 12.96% | 17.30% | 12.55% | — |

| S&P 500 Index* | 10.61% | 13.96% | 12.78% | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000, which represent approximately 25% of the total market capitalization of the Russell 1000. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An index is not available for direct investment; therefore, its performance does not reflect the expenses, fees and taxes generally paid with the active management of an actual portfolio. |

| | |

| ** | Annualized. |

The Equity Opportunities Fund advanced 18.77% during the year ended March 31, 2013. This compares to gains of 17.30% and 13.96%, respectively, for the Russell Midcap Index and S&P 500 Index. Not surprisingly, a few holdings that finished 2012 on an unusually strong note lagged a bit as we entered 2013. Nonetheless, we managed to participate nicely in the market’s upside. It is fun to report such results, but most quarters won’t resemble fiscal Q4 and we are much more focused on generating attractive multi-year returns. Below, we discuss recent performance and a few recent transactions.

Dollar Tree (DLTR) and Markel (MKL) were among the top contributors in the fiscal fourth quarter and for the fiscal year. Their performance was particularly gratifying since we recently added to both positions when the stocks were under pressure. Further, it displays the benefits of adding to quality franchises when they are out of favor with investors for short-term reasons. Delta Air Lines (DAL) also took flight. Its shares gained roughly 42% in the fourth quarter. We probably seemed crazy when we bought this stock given the airline industry’s checkered past (as far as investors are concerned). Thus far, however, our outlook for renewed operating discipline, declining debt levels and higher returns on capital has come to fruition nicely. The biggest disappointment was Capital One (COF), which declined 9% in February as a subdued 2013 outlook and uncertainty about the benefit of recent acquisitions weighed on the name. We are frustrated with the stock’s action, but it remains a top holding and we think the risk/reward from here is very favorable.

We’ve recently built positions in a couple of depressed energy stocks. We aren’t particularly bullish on oil and gas prices given growing supplies, but each stock has a unique story and seems to possess little downside risk. The first is CONSOL Energy (CNX), which is a domestic coal and natural gas producer. Most analysts and investors focus on the company’s coal business, which has struggled in the face of lower coal prices and may face secular headwinds. We are more focused on the company’s growing base of natural gas assets, which are positioned in some of the lowest cost and most prolific shale plays in the U.S. These assets seem somewhat unappreciated and currently contribute little to earnings, but could be a significant source of value in coming years even in the absence of material improvement in gas prices.

Another is National Oilwell Varco (NOV), which is a bellwether name in the oil services industry. With a 50%+ market share, NOV is the dominant provider of equipment for drilling rigs. Recently, the stock has struggled due to a declining earnings outlook for the company’s North American land business as producers have curtailed drilling for conventional natural gas. We believe this presents an opportunity to purchase a cash generative business with high barriers to entry at a very reasonable price. While the North American land business may remain weak, NOV’s deepwater rig equipment business has a bright outlook with high international oil prices prompting new build rig orders. Also, the company has a strong balance sheet and record $12 billion backlog. Finally, we’ve been pleased to see that Berkshire Hathaway has been accumulating the stock over the past year.

We have also established a position in American International Group (AIG), which is a name that causes many people to cringe. The company’s epic collapse and subsequent bailout by the U.S. Government continue to leave a bad taste in many investors’ mouths. Hence, this appears to be one of the most “under-owned” and misunderstood names around. Meanwhile, not only are insurance rates firming industry-wide, but AIG has become more focused on disciplined underwriting and cost efficiencies. Further, the company’s capital position has been bolstered by asset sales and the United States Treasury recently exited its stake in the company. With the stock now trading at roughly 50% of book value, we think the risk/reward here is very favorable. This adds to our kitty of insurance names, which also includes Markel (MKL), Aon (AON) and Safety Insurance Group (SAFT). Each company has unique drivers, but all could benefit from improved pricing dynamics.

We chipped and sold a few positions during the fourth quarter. Strength in names such as Lamar Advertising (LAMR), Colfax (CFX) and Rockwell Collins (COL) prompted us to take some gains. We like each company, but outsized returns in a short period led us to believe there were better opportunities elsewhere. In another case, Check Point Software (CHKP), we sold the Fund’s position given changing competitive dynamics and decelerating revenue growth. The Fund remains underweight in the Information Technology sector, where we struggle with rapid change, pricing pressure and product obsolescence. In fact, it often seems today’s high flyers are tomorrow’s has-beens. Such rapid change may be good for consumers, but is troublesome for us as investors and we’d much rather own companies with a higher degree of visibility. Take J.M. Smucker (SJM) for example. While we can’t say how CHKP will be positioned in five years, we’re pretty certain SJM’s jams, peanut butter and coffee will stand the test of time.

New Positions

American International Group, Inc. (AIG) is a leading global insurance company with a focus on property and casualty lines of business.

National Oilwell Varco, Inc. (NOV) is a leading oilfield services company that makes and sells systems and components used in oil and gas drilling and production.

Valero Energy Corporation (VLO) is the world’s largest independent oil refiner, with 2.3 million barrels of refining capacity.

Increased Positions

CONSOL Energy, Inc. (CNX) is a coal producer in the Northeast United States with considerable natural gas assets in the Marcellus and Utica shales.

Dollar Tree, Inc. (DLTR) is a leading discount retailer based in Chesapeake, VA.

We are pleased that The Davenport Funds are off to a good start thus far in 2013. We thank you for your trust and look forward to reporting back as we proceed through the year.

Sincerely,

John P. Ackerly, IV

President, The Davenport Funds

DAVENPORT CORE FUND PERFORMANCE INFORMATION (Unaudited) |

| | Average Annual Total Returns(a) (for years ended March 31, 2013) |

| | 1 Year | 5 Years | 10 Years |

| Davenport Core Fund | 12.47% | 5.39% | 8.76% |

Standard & Poor’s 500® Index | 13.96% | 5.81% | 8.53% |

(a) The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

DAVENPORT VALUE & INCOME FUND PERFORMANCE INFORMATION (Unaudited) |

| | Average Annual Total Returns(a) (for periods ended March 31, 2013) |

| | 1 Year | Since Inception(b) |

| Davenport Value & Income Fund | 18.69% | 16.28% |

Standard & Poor’s 500® Index | 13.96% | 12.78% |

| Lipper Equity Income Index | 15.06% | 12.02% |

(a) The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| |

(b) Commencement of operations was December 31, 2010. |

DAVENPORT EQUITY OPPORTUNITIES FUND PERFORMANCE INFORMATION (Unaudited) |

| | Average Annual Total Returns(a) (for periods ended March 31, 2013) |

| | 1 Year | Since Inception(b) |

| Davenport Equity Opportunities Fund | 18.77% | 17.11% |

Russell Midcap® Index | 17.30% | 12.55% |

(a) The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| |

(b) Commencement of operations was December 31, 2010. |

DAVENPORT CORE FUND PORTFOLIO INFORMATION March 31, 2013 (Unaudited) |

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Johnson & Johnson | 3.0% |

| CarMax, Inc. | 2.9% |

| Markel Corporation | 2.9% |

| Berkshire Hathaway, Inc. - Class B | 2.6% |

| Brookfield Asset Management, Inc. - Class A | 2.6% |

| Danaher Corporation | 2.5% |

| Capital One Financial Corporation | 2.5% |

| Wells Fargo & Company | 2.3% |

| Exxon Mobil Corporation | 2.3% |

| J.M. Smucker Company (The) | 2.3% |

DAVENPORT VALUE & INCOME FUND PORTFOLIO INFORMATION March 31, 2013 (Unaudited) |

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| JPMorgan Chase & Company | 2.7% |

| Travelers Companies, Inc. (The) | 2.6% |

| Walgreen Company | 2.6% |

| Johnson & Johnson | 2.6% |

| General Electric Company | 2.6% |

| W.P. Carey, Inc. | 2.5% |

SPDR EURO STOXX 50® ETF | 2.4% |

| Wells Fargo & Company | 2.4% |

| Sun Communities, Inc. | 2.4% |

| Dow Chemical Company (The) | 2.3% |

DAVENPORT EQUITY OPPORTUNITIES FUND PORTFOLIO INFORMATION March 31, 2013 (Unaudited) |

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Penn National Gaming, Inc. | 6.0% |

| Markel Corporation | 5.5% |

| CarMax, Inc. | 5.4% |

| Dollar Tree, Inc. | 4.6% |

| O'Reilly Automotive, Inc. | 4.0% |

| Brookfield Asset Management, Inc. - Class A | 4.0% |

| Aon plc | 3.9% |

| Sun Communities, Inc. | 3.7% |

| Albemarle Corporation | 3.3% |

| International Game Technology | 3.3% |

DAVENPORT CORE FUND SCHEDULE OF INVESTMENTS March 31, 2013 | |

| | | | | | |

| Consumer Discretionary — 14.0% | | | | | | |

Amazon.com, Inc. (a) | | | 15,073 | | | $ | 4,016,804 | |

CarMax, Inc. (a) | | | 148,617 | | | | 6,197,329 | |

General Motors Company (a) | | | 125,945 | | | | 3,503,790 | |

Lowe's Companies, Inc. | | | 93,816 | | | | 3,557,503 | |

McDonald's Corporation | | | 41,990 | | | | 4,185,983 | |

News Corporation - Class A | | | 128,851 | | | | 3,932,532 | |

Walt Disney Company (The) | | | 70,778 | | | | 4,020,190 | |

| | | | | | | | 29,414,131 | |

| Consumer Staples — 12.3% | | | | | | | | |

Anheuser-Busch InBev SA/NV - ADR | | | 34,645 | | | | 3,448,910 | |

J.M. Smucker Company (The) | | | 48,862 | | | | 4,845,156 | |

Nestle SA - ADR | | | 39,993 | | | | 2,898,293 | |

PepsiCo, Inc. | | | 47,176 | | | | 3,732,094 | |

Procter & Gamble Company (The) | | | 38,639 | | | | 2,977,521 | |

Walgreen Company | | | 81,700 | | | | 3,895,456 | |

Wal-Mart Stores, Inc. | | | 54,557 | | | | 4,082,500 | |

| | | | | | | | 25,879,930 | |

| Energy — 11.1% | | | | | | | | |

Chevron Corporation | | | 36,387 | | | | 4,323,503 | |

Exxon Mobil Corporation | | | 54,567 | | | | 4,917,032 | |

National Oilwell Varco, Inc. | | | 53,750 | | | | 3,802,813 | |

Occidental Petroleum Corporation | | | 40,104 | | | | 3,142,950 | |

Schlumberger Ltd. | | | 42,338 | | | | 3,170,693 | |

Valero Energy Corporation | | | 91,046 | | | | 4,141,683 | |

| | | | | | | | 23,498,674 | |

| Financials — 20.0% | | | | | | | | |

American Tower Corporation | | | 47,658 | | | | 3,665,853 | |

Aon plc | | | 69,605 | | | | 4,280,708 | |

Berkshire Hathaway, Inc. - Class B (a) | | | 52,476 | | | | 5,467,999 | |

| Brookfield Asset Management, Inc. - Class A | | | 147,924 | | | | 5,397,747 | |

Capital One Financial Corporation | | | 95,642 | | | | 5,255,528 | |

Goldman Sachs Group, Inc. (The) | | | 25,625 | | | | 3,770,719 | |

JPMorgan Chase & Company | | | 69,728 | | | | 3,309,291 | |

Markel Corporation (a) | | | 12,023 | | | | 6,053,580 | |

Wells Fargo & Company | | | 133,129 | | | | 4,924,442 | |

| | | | | | | | 42,125,867 | |

| Health Care — 8.1% | | | | | | | | |

AmerisourceBergen Corporation | | | 79,700 | | | | 4,100,565 | |

Amgen, Inc. | | | 32,555 | | | | 3,337,213 | |

Johnson & Johnson | | | 78,248 | | | | 6,379,559 | |

WellPoint, Inc. | | | 50,390 | | | | 3,337,330 | |

| | | | | | | | 17,154,667 | |

DAVENPORT CORE FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 92.6% (Continued) | | | | | | |

| Industrials — 10.2% | | | | | | |

Danaher Corporation | | | 85,872 | | | $ | 5,336,944 | |

General Electric Company | | | 127,965 | | | | 2,958,551 | |

Illinois Tool Works, Inc. | | | 45,699 | | | | 2,784,897 | |

Stanley Black & Decker, Inc. | | | 39,738 | | | | 3,217,586 | |

Union Pacific Corporation | | | 23,690 | | | | 3,373,693 | |

United Technologies Corporation | | | 41,779 | | | | 3,903,412 | |

| | | | | | | | 21,575,083 | |

| Information Technology — 13.9% | | | | | | | | |

Accenture plc - Class A | | | 56,144 | | | | 4,265,260 | |

Apple, Inc. | | | 6,635 | | | | 2,936,850 | |

Automatic Data Processing, Inc. | | | 49,175 | | | | 3,197,359 | |

Google, Inc. - Class A (a) | | | 4,279 | | | | 3,397,654 | |

| International Business Machines Corporation | | | 21,957 | | | | 4,683,428 | |

Microsoft Corporation | | | 105,598 | | | | 3,021,159 | |

QUALCOMM, Inc. | | | 47,820 | | | | 3,201,549 | |

Visa, Inc. - Class A | | | 26,593 | | | | 4,516,555 | |

| | | | | | | | 29,219,814 | |

| Materials — 3.0% | | | | | | | | |

Albemarle Corporation | | | 55,483 | | | | 3,468,797 | |

Praxair, Inc. | | | 26,046 | | | | 2,905,171 | |

| | | | | | | | 6,373,968 | |

| | | | | | | | | |

Total Common Stocks (Cost $136,401,294) | | | | | | $ | 195,242,134 | |

EXCHANGE-TRADED FUNDS — 2.1% | | | | | | |

| iShares Nasdaq Biotechnology Index Fund (Cost $3,875,987) | | | 27,372 | | | $ | 4,377,604 | |

MONEY MARKET FUNDS — 3.1% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (b) (Cost $6,599,017) | | | 6,599,017 | | | $ | 6,599,017 | |

| | | | | | | | | |

Total Investments at Value — 97.8% (Cost $146,876,298) | | | | | | $ | 206,218,755 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 2.2% | | | | | | | 4,680,250 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 210,899,005 | |

| ADR - American Depositary Receipt. |

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of March 31, 2013. |

| See accompanying notes to financial statements. |

DAVENPORT VALUE & INCOME FUND SCHEDULE OF INVESTMENTS March 31, 2013 | |

| | | | | | |

| Consumer Discretionary — 6.8% | | | | | | |

Cracker Barrel Old Country Store, Inc. | | | 34,950 | | | $ | 2,825,708 | |

Darden Restaurants, Inc. | | | 47,950 | | | | 2,478,056 | |

McDonald's Corporation | | | 39,210 | | | | 3,908,845 | |

Penn National Gaming, Inc. (a) | | | 75,805 | | | | 4,126,066 | |

| | | | | | | | 13,338,675 | |

| Consumer Staples — 21.0% | | | | | | | | |

Altria Group, Inc. | | | 78,906 | | | | 2,713,577 | |

Anheuser-Busch InBev SA/NV - ADR | | | 36,210 | | | | 3,604,706 | |

Archer-Daniels-Midland Company | | | 93,310 | | | | 3,147,346 | |

Coca-Cola Company (The) | | | 93,800 | | | | 3,793,272 | |

Diageo plc - ADR | | | 23,175 | | | | 2,916,342 | |

Dr. Pepper Snapple Group, Inc. | | | 57,372 | | | | 2,693,616 | |

H.J. Heinz Company | | | 39,430 | | | | 2,849,606 | |

PepsiCo, Inc. | | | 49,355 | | | | 3,904,474 | |

Philip Morris International, Inc. | | | 38,940 | | | | 3,610,128 | |

Procter & Gamble Company (The) | | | 38,720 | | | | 2,983,763 | |

Walgreen Company | | | 106,780 | | | | 5,091,270 | |

Wal-Mart Stores, Inc. | | | 53,552 | | | | 4,007,296 | |

| | | | | | | | 41,315,396 | |

| Energy — 7.9% | | | | | | | | |

BP plc - ADR | | | 92,820 | | | | 3,930,927 | |

Chevron Corporation | | | 34,956 | | | | 4,153,472 | |

LinnCo, LLC | | | 93,695 | | | | 3,658,790 | |

Marathon Petroleum Corporation | | | 42,485 | | | | 3,806,656 | |

| | | | | | | | 15,549,845 | |

| Financials — 20.5% | | | | | | | | |

Capital One Financial Corporation | | | 71,385 | | | | 3,922,606 | |

Fidelity National Financial, Inc. - Class A | | | 143,320 | | | | 3,615,963 | |

Hartford Financial Services Group, Inc. | | | 156,025 | | | | 4,025,445 | |

JPMorgan Chase & Company | | | 113,380 | | | | 5,381,015 | |

Sun Communities, Inc. | | | 95,113 | | | | 4,691,924 | |

Travelers Companies, Inc. (The) | | | 60,810 | | | | 5,119,594 | |

W.P. Carey, Inc. | | | 72,204 | | | | 4,866,549 | |

Wells Fargo & Company | | | 128,540 | | | | 4,754,695 | |

Weyerhaeuser Company | | | 129,634 | | | | 4,067,915 | |

| | | | | | | | 40,445,706 | |

| Health Care — 7.8% | | | | | | | | |

GlaxoSmithKline plc - ADR | | | 85,535 | | | | 4,012,447 | |

Johnson & Johnson | | | 62,445 | | | | 5,091,141 | |

Merck & Company, Inc. | | | 70,405 | | | | 3,114,013 | |

WellPoint, Inc. | | | 47,935 | | | | 3,174,735 | |

| | | | | | | | 15,392,336 | |

DAVENPORT VALUE & INCOME FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 87.5% (Continued) | | | | | | |

| Industrials — 12.8% | | | | | | |

3M Company | | | 31,085 | | | $ | 3,304,646 | |

Eaton Corporation plc | | | 64,297 | | | | 3,938,191 | |

General Electric Company | | | 220,000 | | | | 5,086,400 | |

Illinois Tool Works, Inc. | | | 41,920 | | | | 2,554,605 | |

Norfolk Southern Corporation | | | 44,775 | | | | 3,451,257 | |

Raytheon Company | | | 57,316 | | | | 3,369,608 | |

Watsco, Inc. | | | 40,845 | | | | 3,438,332 | |

| | | | | | | | 25,143,039 | |

| Information Technology — 3.4% | | | | | | | | |

Automatic Data Processing, Inc. | | | 57,810 | | | | 3,758,806 | |

Microsoft Corporation | | | 105,800 | | | | 3,026,938 | |

| | | | | | | | 6,785,744 | |

| Materials — 3.7% | | | | | | | | |

Dow Chemical Company (The) | | | 141,030 | | | | 4,490,395 | |

E.I. du Pont de Nemours and Company | | | 56,665 | | | | 2,785,652 | |

| | | | | | | | 7,276,047 | |

| Telecommunication Services — 1.6% | | | | | | | | |

Vodafone Group plc - ADR | | | 114,525 | | | | 3,253,655 | |

| | | | | | | | | |

| Utilities — 2.0% | | | | | | | | |

Dominion Resources, Inc. | | | 66,205 | | | | 3,851,807 | |

| | | | | | | | | |

Total Common Stocks (Cost $144,747,782) | | | | | | $ | 172,352,250 | |

EXCHANGE-TRADED FUNDS — 4.5% | | | | | | |

SPDR EURO STOXX 50® ETF | | | 145,830 | | | $ | 4,818,223 | |

WisdomTree Japan Hedged Equity Fund | | | 90,855 | | | | 3,923,119 | |

Total Exchange-Traded Funds (Cost $7,942,048) | | | | | | $ | 8,741,342 | |

| | | | | | |

| Tortoise Energy Infrastructure Corporation (Cost $2,827,624) | | | 70,735 | | | $ | 3,492,894 | |

DAVENPORT VALUE & INCOME FUND SCHEDULE OF INVESTMENTS (Continued) | |

MONEY MARKET FUNDS — 2.8% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (b) (Cost $5,604,664) | | | 5,604,664 | | | $ | 5,604,664 | |

| | | | | | | | | |

Total Investments at Value — 96.6% (Cost $161,122,118) | | | | | | $ | 190,191,150 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 3.4% | | | | | | | 6,698,721 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 196,889,871 | |

| ADR - American Depositary Receipt. |

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of March 31, 2013. |

| See accompanying notes to financial statements. |

DAVENPORT EQUITY OPPORTUNITIES FUND SCHEDULE OF INVESTMENTS March 31, 2013 | |

| | | | | | |

| Consumer Discretionary — 28.0% | | | | | | |

CarMax, Inc. (a) | | | 133,410 | | | $ | 5,563,197 | |

Dollar Tree, Inc. (a) | | | 97,200 | | | | 4,707,396 | |

Hanesbrands, Inc. (a) | | | 60,990 | | | | 2,778,705 | |

International Game Technology | | | 202,660 | | | | 3,343,890 | |

Lamar Advertising Company - Class A (a) | | | 42,995 | | | | 2,089,987 | |

O'Reilly Automotive, Inc. (a) | | | 40,505 | | | | 4,153,788 | |

Penn National Gaming, Inc. (a) | | | 112,845 | | | | 6,142,153 | |

| | | | | | | | 28,779,116 | |

| Consumer Staples — 7.5% | | | | | | | | |

Church & Dwight Company, Inc. | | | 32,930 | | | | 2,128,266 | |

J.M. Smucker Company (The) | | | 31,725 | | | | 3,145,851 | |

Walgreen Company | | | 50,705 | | | | 2,417,614 | |

| | | | | | | | 7,691,731 | |

| Energy — 7.0% | | | | | | | | |

CONSOL Energy, Inc. | | | 91,920 | | | | 3,093,108 | |

National Oilwell Varco, Inc. | | | 28,745 | | | | 2,033,709 | |

Valero Energy Corporation | | | 45,455 | | | | 2,067,748 | |

| | | | | | | | 7,194,565 | |

| Financials — 30.9% | | | | | | | | |

American International Group, Inc. (a) | | | 50,485 | | | | 1,959,828 | |

American Tower Corporation | | | 33,640 | | | | 2,587,589 | |

Aon plc | | | 65,940 | | | | 4,055,310 | |

| Brookfield Asset Management, Inc. - Class A | | | 111,610 | | | | 4,072,649 | |

Capital One Financial Corporation | | | 60,006 | | | | 3,297,330 | |

Fidelity National Financial, Inc. - Class A | | | 74,855 | | | | 1,888,592 | |

Markel Corporation (a) | | | 11,275 | | | | 5,676,962 | |

Safety Insurance Group, Inc. | | | 49,830 | | | | 2,449,144 | |

Sun Communities, Inc. | | | 78,055 | | | | 3,850,453 | |

SunTrust Banks, Inc. | | | 64,900 | | | | 1,869,769 | |

| | | | | | | | 31,707,626 | |

| Health Care — 2.0% | | | | | | | | |

Henry Schein, Inc. (a) | | | 22,455 | | | | 2,078,210 | |

| | | | | | | | | |

| Industrials — 10.2% | | | | | | | | |

Colfax Corporation (a) | | | 42,445 | | | | 1,975,390 | |

Delta Air Lines, Inc. (a) | | | 152,555 | | | | 2,518,683 | |

Pall Corporation | | | 29,590 | | | | 2,023,068 | |

Rockwell Collins, Inc. | | | 32,300 | | | | 2,038,776 | |

Watsco, Inc. | | | 22,510 | | | | 1,894,892 | |

| | | | | | | | 10,450,809 | |

| Information Technology — 2.3% | | | | | | | | |

Intuit, Inc. | | | 37,005 | | | | 2,429,378 | |

DAVENPORT EQUITY OPPORTUNITIES FUND SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 94.2% (Continued) | | | | | | |

| Materials — 3.3% | | | | | | |

Albemarle Corporation | | | 54,180 | | | $ | 3,387,334 | |

| | | | | | | | | |

| Utilities — 3.0% | | | | | | | | |

ITC Holdings Corporation | | | 34,240 | | | | 3,056,262 | |

| | | | | | | | | |

Total Common Stocks (Cost $78,600,744) | | | | | | $ | 96,775,031 | |

MONEY MARKET FUNDS — 2.8% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (b) (Cost $2,825,594) | | | 2,825,594 | | | $ | 2,825,594 | |

| | | | | | | | | |

Total Investments at Value — 97.0% (Cost $81,426,338) | | | | | | $ | 99,600,625 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 3.0% | | | | | | | 3,078,370 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 102,678,995 | |

| (a) | Non-income producing security. |

| (b) | The rate shown is the 7-day effective yield as of March 31, 2013. |

| See accompanying notes to financial statements. |

THE DAVENPORT FUNDS STATEMENTS OF ASSETS AND LIABILITIES March 31, 2013 | |

| | | | | Davenport Value & Income Fund | | | Davenport Equity Opportunities Fund | |

| ASSETS | | | | | | | | | |

| Investments in securities: | | | | | | | | | |

At acquisition cost | | $ | 146,876,298 | | | $ | 161,122,118 | | | $ | 81,426,338 | |

At market value (Note 2) | | $ | 206,218,755 | | | $ | 190,191,150 | | | $ | 99,600,625 | |

Cash | | | 32,345 | | | | 5,220,499 | | | | 3,364,270 | |

Dividends receivable | | | 225,873 | | | | 530,660 | | | | 76,719 | |

Receivable for capital shares sold | | | 757,451 | | | | 1,292,034 | | | | 391,600 | |

Receivable for securities sold | | | 5,829,385 | | | | — | | | | 1,445,076 | |

Other assets | | | 12,279 | | | | 7,529 | | | | 6,974 | |

TOTAL ASSETS | | | 213,076,088 | | | | 197,241,872 | | | | 104,885,264 | |

| | | | | | | | | | | | | |

| LIABILITIES | | | | | | | | | | | | |

Payable for investment securities purchased | | | 1,901,845 | | | | — | | | | 2,026,453 | |

Payable for capital shares redeemed | | | 97,292 | | | | 201,442 | | | | 96,552 | |

Accrued investment advisory fees (Note 4) | | | 145,951 | | | | 123,184 | | | | 66,057 | |

Payable to administrator (Note 4) | | | 24,900 | | | | 22,600 | | | | 13,050 | |

Other accrued expenses and liabilities | | | 7,095 | | | | 4,775 | | | | 4,157 | |

TOTAL LIABILITIES | | | 2,177,083 | | | | 352,001 | | | | 2,206,269 | |

| | | | | | | | | | | | | |

NET ASSETS | | $ | 210,899,005 | | | $ | 196,889,871 | | | $ | 102,678,995 | |

| | | | | | | | | | | | | |

| Net assets consist of: | | | | | | | | | | | | |

Paid-in capital | | $ | 150,421,112 | | | $ | 164,586,438 | | | $ | 82,116,288 | |

Undistributed net investment income | | | 11,648 | | | | 3,121 | | | | 25,889 | |

Accumulated net realized gains from

security transactions | | | 1,123,788 | | | | 3,231,280 | | | | 2,362,531 | |

Net unrealized appreciation on investments | | | 59,342,457 | | | | 29,069,032 | | | | 18,174,287 | |

Net assets | | $ | 210,899,005 | | | $ | 196,889,871 | | | $ | 102,678,995 | |

| | | | | | | | | | | | | |

Shares of beneficial interest outstanding

(unlimited number of shares authorized,

$0.01 par value) | | | 12,594,528 | | | | 14,936,637 | | | | 7,409,101 | |

| | | | | | | | | | | | | |

Net asset value, offering price and redemption

price per share (Note 2) | | $ | 16.75 | | | $ | 13.18 | | | $ | 13.86 | |

| See accompanying notes to financial statements. |

THE DAVENPORT FUNDS STATEMENTS OF OPERATIONS Year Ended March 31, 2013 | |

| | | | | Davenport Value & Income Fund | | | Davenport Equity Opportunities Fund | |

| INVESTMENT INCOME | | | | | | | | | |

Dividends | | $ | 3,092,980 | | | $ | 4,635,894 | | | $ | 918,533 | |

Foreign withholding taxes on dividends | | | (46,538 | ) | | | (2,497 | ) | | | (13,292 | ) |

Interest | | | 136 | | | | — | | | | — | |

TOTAL INVESTMENT INCOME | | | 3,046,578 | | | | 4,633,397 | | | | 905,241 | |

| | | | | | | | | | | | | |

| EXPENSES | | | | | | | | | | | | |

Investment advisory fees (Note 4) | | | 1,372,583 | | | | 1,040,060 | | | | 547,147 | |

Administration fees (Note 4) | | | 245,401 | | | | 189,617 | | | | 110,238 | |

Custodian and bank service fees | | | 18,536 | | | | 24,235 | | | | 12,106 | |

Professional fees | | | 19,038 | | | | 16,818 | | | | 16,818 | |

Compliance service fees (Note 4) | | | 19,865 | | | | 16,502 | | | | 11,593 | |

Registration and filing fees | | | 17,786 | | | | 14,541 | | | | 13,335 | |

Trustees’ fees and expenses (Note 4) | | | 9,275 | | | | 9,275 | | | | 9,275 | |

Printing of shareholder reports | | | 14,309 | | | | 5,960 | | | | 4,738 | |

Insurance expense | | | 11,709 | | | | 6,830 | | | | 4,520 | |

Other expenses | | | 10,869 | | | | 10,113 | | | | 10,563 | |

TOTAL EXPENSES | | | 1,739,371 | | | | 1,333,951 | | | | 740,333 | |

| | | | | | | | | | | | | |

NET INVESTMENT INCOME | | | 1,307,207 | | | | 3,299,446 | | | | 164,908 | |

| | | | | | | | | | | | | |

REALIZED AND UNREALIZED

GAINS ON INVESTMENTS | | | | | | | | | | | | |

Net realized gains from security transactions | | | 9,676,207 | | | | 6,183,266 | | | | 4,578,353 | |

Net change in unrealized appreciation/

depreciation on investments | | | 12,010,397 | | | | 18,460,679 | | | | 10,165,302 | |

| | | | | | | | | | | | | |

NET REALIZED AND UNREALIZED

GAINS ON INVESTMENTS | | | 21,686,604 | | | | 24,643,945 | | | | 14,743,655 | |

| | | | | | | | | | | | | |

NET INCREASE IN NET ASSETS

FROM OPERATIONS | | $ | 22,993,811 | | | $ | 27,943,391 | | | $ | 14,908,563 | |

| See accompanying notes to financial statements. |

DAVENPORT CORE FUND STATEMENTS OF CHANGES IN NET ASSETS | |

| | | | | | |

| FROM OPERATIONS | | | | | | |

Net investment income | | $ | 1,307,207 | | | $ | 1,034,589 | |

Net realized gains from security transactions | | | 9,676,207 | | | | 2,194,465 | |

Net change in unrealized appreciation/

depreciation on investments | | | 12,010,397 | | | | 12,450,152 | |

Net increase in net assets from operations | | | 22,993,811 | | | | 15,679,206 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | (1,315,956 | ) | | | (1,036,002 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 32,795,331 | | | | 17,735,914 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 1,246,351 | | | | 972,757 | |

Payments for shares redeemed | | | (19,718,238 | ) | | | (18,348,617 | ) |

Net increase in net assets from capital share transactions | | | 14,323,444 | | | | 360,054 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 36,001,299 | | | | 15,003,258 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

Beginning of year | | | 174,897,706 | | | | 159,894,448 | |

End of year | | $ | 210,899,005 | | | $ | 174,897,706 | |

| | | | | | | | | |

UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 11,648 | | | $ | 20,397 | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 2,156,214 | | | | 1,299,210 | |

Shares reinvested | | | 82,322 | | | | 73,427 | |

Shares redeemed | | | (1,300,040 | ) | | | (1,362,591 | ) |

Net increase in shares outstanding | | | 938,496 | | | | 10,046 | |

Shares outstanding at beginning of year | | | 11,656,032 | | | | 11,645,986 | |

Shares outstanding at end of year | | | 12,594,528 | | | | 11,656,032 | |

| See accompanying notes to financial statements. |

DAVENPORT VALUE & INCOME FUND STATEMENTS OF CHANGES IN NET ASSETS | |

| | | | | | |

| FROM OPERATIONS | | | | | | |

Net investment income | | $ | 3,299,446 | | | $ | 1,533,671 | |

Net realized gains (losses) from security transactions | | | 6,183,266 | | | | (989,066 | ) |

Net change in unrealized appreciation/

depreciation on investments | | | 18,460,679 | | | | 9,378,913 | |

Net increase in net assets from operations | | | 27,943,391 | | | | 9,923,518 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | (3,316,928 | ) | | | (1,522,098 | ) |

From net realized gains from security transactions | | | (1,962,920 | ) | | | (71,734 | ) |

Decrease in net assets from distributions to shareholders | | | (5,279,848 | ) | | | (1,593,832 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 85,076,371 | | | | 44,865,899 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 4,722,338 | | | | 1,359,339 | |

Payments for shares redeemed | | | (14,329,788 | ) | | | (4,628,047 | ) |

Net increase in net assets from capital share transactions | | | 75,468,921 | | | | 41,597,191 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 98,132,464 | | | | 49,926,877 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

Beginning of year | | | 98,757,407 | | | | 48,830,530 | |

End of year | | $ | 196,889,871 | | | $ | 98,757,407 | |

| | | | | | | | | |

| UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 3,121 | | | $ | 20,603 | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 7,171,909 | | | | 4,240,900 | |

Shares reinvested | | | 398,116 | | | | 130,856 | |

Shares redeemed | | | (1,212,247 | ) | | | (444,451 | ) |

Net increase in shares outstanding | | | 6,357,778 | | | | 3,927,305 | |

Shares outstanding at beginning of year | | | 8,578,859 | | | | 4,651,554 | |

Shares outstanding at end of year | | | 14,936,637 | | | | 8,578,859 | |

| See accompanying notes to financial statements. |

DAVENPORT EQUITY OPPORTUNITIES FUND STATEMENTS OF CHANGES IN NET ASSETS | |

| | | | | | |

| FROM OPERATIONS | | | | | | |

Net investment income (loss) | | $ | 164,908 | | | $ | (99,423 | ) |

Net realized gains (losses) from security transactions | | | 4,578,353 | | | | (469,701 | ) |

Net change in unrealized appreciation/

depreciation on investments | | | 10,165,302 | | | | 6,678,341 | |

Net increase in net assets from operations | | | 14,908,563 | | | | 6,109,217 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | (139,019 | ) | | | — | |

From net realized gains from security transactions | | | (1,731,142 | ) | | | (163,030 | ) |

Decrease in net assets from distributions to shareholders | | | (1,870,161 | ) | | | (163,030 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 33,820,160 | | | | 23,587,122 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 1,800,189 | | | | 157,487 | |

Payments for shares redeemed | | | (5,114,447 | ) | | | (4,931,526 | ) |

Net increase in net assets from capital share transactions | | | 30,505,902 | | | | 18,813,083 | |

| | | | | | | | | |

TOTAL INCREASE IN NET ASSETS | | | 43,544,304 | | | | 24,759,270 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

Beginning of year | | | 59,134,691 | | | | 34,375,421 | |

End of year | | $ | 102,678,995 | | | $ | 59,134,691 | |

| | | | | | | | | |

UNDISTRIBUTED NET INVESTMENT INCOME | | $ | 25,889 | | | $ | — | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 2,737,625 | | | | 2,186,580 | |

Shares reinvested | | | 145,972 | | | | 15,593 | |

Shares redeemed | | | (419,552 | ) | | | (464,812 | ) |

Net increase in shares outstanding | | | 2,464,045 | | | | 1,737,361 | |

Shares outstanding at beginning of year | | | 4,945,056 | | | | 3,207,695 | |

Shares outstanding at end of year | | | 7,409,101 | | | | 4,945,056 | |

| See accompanying notes to financial statements. |

DAVENPORT CORE FUND FINANCIAL HIGHLIGHTS | |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Year | |

| | | | |

| | | | | | | | | | | | | | | |

| Net asset value at beginning of year | | $ | 15.00 | | | $ | 13.73 | | | $ | 12.05 | | | $ | 8.36 | | | $ | 13.82 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.11 | | | | 0.09 | | | | 0.07 | | | | 0.08 | | | | 0.11 | |

Net realized and unrealized gains

(losses) on investments | | | 1.75 | | | | 1.27 | | | | 1.68 | | | | 3.69 | | | | (5.17 | ) |

| Total from investment operations | | | 1.86 | | | | 1.36 | | | | 1.75 | | | | 3.77 | | | | (5.06 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.11 | ) | | | (0.09 | ) | | | (0.07 | ) | | | (0.08 | ) | | | (0.11 | ) |

| Distributions from net realized gains | | | — | | | | — | | | | — | | | | — | | | | (0.29 | ) |

Total distributions | | | (0.11 | ) | | | (0.09 | ) | | | (0.07 | ) | | | (0.08 | ) | | | (0.40 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net asset value at end of year | | $ | 16.75 | | | $ | 15.00 | | | $ | 13.73 | | | $ | 12.05 | | | $ | 8.36 | |

| | | | | | | | | | | | | | | | | | | | | |

Total return (a) | | | 12.47% | | | | 9.99% | | | | 14.61% | | | | 45.20% | | | | (36.85% | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net assets at end of year (000’s) | | $ | 210,899 | | | $ | 174,898 | | | $ | 159,894 | | | $ | 132,662 | | | $ | 92,358 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratio of total expenses to average net assets | | | 0.95% | | | | 0.96% | | | | 0.99% | | | | 1.00% | | | | 1.00% | |

| | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income

to average net assets | | | 0.71% | | | | 0.66% | | | | 0.58% | | | | 0.75% | | | | 0.98% | |

| | | | | | | | | | | | | | | | | | | | | |

Portfolio turnover rate | | | 26% | | | | 19% | | | | 34% | | | | 25% | | | | 39% | |

| (a) | Total return is a measure of the change in value of an investment in the Fund over the years covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| See accompanying notes to financial statements. |

DAVENPORT VALUE & INCOME FUND FINANCIAL HIGHLIGHTS | |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period | |

| | | | | | | | Period Ended March 31, 2011 (a) | |

| Net asset value at beginning of period | | $ | 11.51 | | | $ | 10.50 | | | $ | 10.00 | |

| | | | | | | | | | | | | |

| Income from investment operations: | | | | | | | | | | | | |

| Net investment income | | | 0.28 | | | | 0.23 | | | | 0.04 | |

| Net realized and unrealized gains on investments | | | 1.81 | | | | 1.02 | | | | 0.49 | |

| Total from investment operations | | | 2.09 | | | | 1.25 | | | | 0.53 | |

| | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.27 | ) | | | (0.23 | ) | | | (0.03 | ) |

| Distributions from net realized gains | | | (0.15 | ) | | | (0.01 | ) | | | — | |

| Total distributions | | | (0.42 | ) | | | (0.24 | ) | | | (0.03 | ) |

| | | | | | | | | | | | | |

| Net asset value at end of period | | $ | 13.18 | | | $ | 11.51 | | | $ | 10.50 | |

| | | | | | | | | | | | | |

Total return (b) | | | 18.69% | | | | 12.23% | | | | 5.35% | (c) |

| | | | | | | | | | | | | |

| Net assets at end of period (000’s) | | $ | 196,890 | | | $ | 98,757 | | | $ | 48,831 | |

| | | | | | | | | | | | | |

| Ratio of total expenses to average net assets | | | 0.96% | | | | 1.04% | | | | 1.25% | (d) |

| | | | | | | | | | | | | |

| Ratio of net investment income to average net assets | | | 2.43% | | | | 2.30% | | | | 1.99% | (d) |

| | | | | | | | | | | | | |

| Portfolio turnover rate | | | 29% | | | | 27% | | | | 10% | (c) |

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

| (b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| See accompanying notes to financial statements. |

DAVENPORT EQUITY OPPORTUNITIES FUND FINANCIAL HIGHLIGHTS | |

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period | |

| | | | | | | | Period Ended March 31, 2011 (a) | |

| Net asset value at beginning of period | | $ | 11.96 | | | $ | 10.72 | | | $ | 10.00 | |

| | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | |

| Net investment income (loss) | | | 0.03 | | | | (0.02 | ) | | | (0.01 | ) |

| Net realized and unrealized gains on investments | | | 2.17 | | | | 1.30 | | | | 0.73 | |

| Total from investment operations | | | 2.20 | | | | 1.28 | | | | 0.72 | |

| | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.02 | ) | | | — | | | | — | |

| Distributions from net realized gains | | | (0.28 | ) | | | (0.04 | ) | | | — | |

| Total distributions | | | (0.30 | ) | | | (0.04 | ) | | | — | |

| | | | | | | | | | | | | |

| Net asset value at end of period | | $ | 13.86 | | | $ | 11.96 | | | $ | 10.72 | |

| | | | | | | | | | | | | |

Total return (b) | | | 18.77% | | | | 12.00% | | | | 7.20% | (c) |

| | | | | | | | | | | | | |

| Net assets at end of period (000’s) | | $ | 102,679 | | | $ | 59,135 | | | $ | 34,375 | |

| | | | | | | | | | | | | |

| Ratio of total expenses to average net assets | | | 1.01% | | | | 1.10% | | | | 1.25% | (d) |

| | | | | | | | | | | | | |

| Ratio of net investment income (loss) to average net assets | | | 0.23% | | | | (0.22% | ) | | | (0.40% | )(d) |

| | | | | | | | | | | | | |

| Portfolio turnover rate | | | 41% | | | | 35% | | | | 6% | (c) |

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

| (b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| See accompanying notes to financial statements. |

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS

1. Organization

Davenport Core Fund, Davenport Value & Income Fund and Davenport Equity Opportunities Fund (individually, a “Fund,” and, collectively, the “Funds”) are each a no-load, diversified series of the Williamsburg Investment Trust (the “Trust”), an open-end management investment company registered under the Investment Company Act of 1940. The Trust was organized as a Massachusetts business trust on July 18, 1988. Other series of the Trust are not incorporated in this report. Davenport Core Fund began operations on January 15, 1998. Davenport Value & Income Fund and Davenport Equity Opportunities Fund each began operations on December 31, 2010.

Davenport Core Fund’s investment objective is long term growth of capital.

Davenport Value & Income Fund’s investment objective is to achieve long term growth while generating current income through dividend payments on portfolio securities.

Davenport Equity Opportunities Fund’s investment objective is long term capital appreciation.

2. Significant Accounting Policies

The following is a summary of the Funds’ significant accounting policies. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Securities valuation — The Funds’ portfolio securities are valued as of the close of business of the regular session of the New York Stock Exchange (normally 4:00 p.m., Eastern time). Securities traded on a national stock exchange are valued based upon the closing price on the principal exchange where the security is traded. Securities which are quoted by NASDAQ are valued at the NASDAQ Official Closing Price. Securities which are traded over-the-counter are valued at the last sales price, if available, otherwise, at the last quoted bid price. Fixed income securities will ordinarily be traded in the over-the-counter market and common stocks will ordinarily be traded on a national securities exchange, but may also be traded in the over-the-counter market.

When market quotations are not readily available, securities may be valued on the basis of prices provided by an independent pricing service. The prices provided by the pricing service are determined with consideration given to institutional bid and last sale prices and take into account securities prices, yields, maturities, call features, ratings, institutional trading in similar groups of securities and developments related to specific securities. If a pricing service cannot provide a valuation or the investment adviser believes the price received from the pricing service is not indicative of fair value, securities will be valued in good faith at fair value using methods consistent with those determined by the Board of Trustees and will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Such methods of fair valuation may include, but are not limited to: multiple of earnings, multiple of book value,

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

discount from market of a similar freely traded security, purchase price of the security, subsequent private transactions in the security or related securities, or a combination of these and other factors.

Short-term instruments (those with remaining maturities of 60 days or less) may be valued at amortized cost, which approximates market value. Money market funds have been determined to be represented at amortized cost which approximates fair value, absent unusual circumstances.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Funds’ investments. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – other significant observable inputs

• Level 3 – significant unobservable inputs

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Funds’ investments as of March 31, 2013 by security type:

| | | | | | | | | | | | |

Common Stocks | | $ | 195,242,134 | | | $ | — | | | $ | — | | | $ | 195,242,134 | |

Exchange-Traded Funds | | | 4,377,604 | | | | — | | | | — | | | | 4,377,604 | |

Money Market Funds | | | 6,599,017 | | | | — | | | | — | | | | 6,599,017 | |

Total | | $ | 206,218,755 | | | $ | — | | | $ | — | | | $ | 206,218,755 | |

Davenport Value & Income Fund | | | | | | | | | | | | |

Common Stocks | | $ | 172,352,250 | | | $ | — | | | $ | — | | | $ | 172,352,250 | |

Exchange-Traded Funds | | | 8,741,342 | | | | — | | | | — | | | | 8,741,342 | |

Closed-End Funds | | | 3,492,894 | | | | — | | | | — | | | | 3,492,894 | |

Money Market Funds | | | 5,604,664 | | | | — | | | | — | | | | 5,604,664 | |

Total | | $ | 190,191,150 | | | $ | — | | | $ | — | | | $ | 190,191,150 | |

Davenport Equity Opportunities Fund | | | | | | | | | | | | |

Common Stocks | | $ | 96,775,031 | | | $ | — | | | $ | — | | | $ | 96,775,031 | |

Money Market Funds | | | 2,825,594 | | | | — | | | | — | | | | 2,825,594 | |

Total | | $ | 99,600,625 | | | $ | — | | | $ | — | | | $ | 99,600,625 | |

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

Refer to each Fund’s Schedule of Investments for a listing of the securities valued by sector type. As of March 31, 2013, the Funds did not have any transfers in and out of any Level. There were no Level 2 or Level 3 securities or derivative instruments held by the Funds as of March 31, 2013. It is the Funds’ policy to recognize transfers into and out of any Level at the end of the reporting period.

Repurchase agreements — The Funds may enter into repurchase agreements. The repurchase agreement, which is collateralized by U.S. Government obligations, is valued at cost which, together with accrued interest, approximates market value. At the time a Fund enters into the repurchase agreement, the Fund takes possession of the underlying securities and the seller agrees that the value of the underlying securities, including accrued interest, will at all times be equal to or exceed the face amount of the repurchase agreement. In addition, the Funds actively monitor and seek additional collateral, as needed. If the seller defaults, the fair value of the collateral may decline and realization of the collateral by the Funds may be delayed or limited.

Share valuation — The net asset value per share of each Fund is calculated daily by dividing the total value of its assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of each Fund is equal to the net asset value per share.

Investment income — Interest income is accrued as earned. Dividend income is recorded on the ex-dividend date. Discounts and premiums on fixed-income securities purchased are amortized using the interest method.

Security transactions — Security transactions are accounted for on trade date for financial reporting purposes. Gains and losses on securities sold are determined on a specific identification basis.

Common expenses — Common expenses of the Trust are allocated among the funds within the Trust based on relative net assets of each fund or the nature of the services performed and the relative applicability to each fund.

Distributions to shareholders — Dividends arising from net investment income, if any, are declared and paid quarterly to shareholders of Davenport Core Fund and Davenport Value & Income Fund; and declared and paid annually to shareholders of Davenport Equity Opportunities Fund. Net realized short-term capital gains, if any, may be distributed throughout the year and net realized long-term capital gains, if any, are distributed at least once each year. The amount of distributions from net investment income and net realized gains are determined in accordance with federal income tax regulations which may differ from GAAP. Dividends and distributions are recorded on the ex-dividend date.

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

The tax character of distributions paid during the years ended March 31, 2013 and March 31, 2012 is as follows:

| | | | | | | | | | |

| Davenport Core Fund | 3/31/13 | | $ | 1,315,956 | | | $ | — | | | $ | 1,315,956 | |

| | 3/31/12 | | $ | 1,036,002 | | | $ | — | | | $ | 1,036,002 | |

| Davenport Value & Income Fund | 3/31/13 | | $ | 3,316,928 | | | $ | 1,962,920 | | | $ | 5,279,848 | |

| | 3/31/12 | | $ | 1,593,832 | | | $ | — | | | $ | 1,593,832 | |

| Davenport Equity Opportunities Fund | 3/31/13 | | $ | 505,327 | | | $ | 1,364,834 | | | $ | 1,870,161 | |

| | 3/31/12 | | $ | 163,030 | | | $ | — | | | $ | 163,030 | |

Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax — It is each Fund’s policy to comply with the special provisions of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. As provided therein, in any fiscal year in which a Fund so qualifies and distributes at least 90% of its taxable net income, the Fund (but not the shareholders) will be relieved of federal income tax on the income distributed. Accordingly, no provision for income taxes has been made.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also each Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of March 31, 2013:

| | | | | Davenport Value & Income Fund | | | Davenport Equity Opportunities Fund | |

Cost of portfolio investments | | $ | 147,207,987 | | | $ | 161,144,316 | | | $ | 81,479,572 | |

Gross unrealized appreciation | | $ | 59,689,594 | | | $ | 29,613,649 | | | $ | 18,231,524 | |

Gross unrealized depreciation | | | (678,826 | ) | | | (566,815 | ) | | | (110,471 | ) |

Net unrealized appreciation | | | 59,010,768 | | | | 29,046,834 | | | | 18,121,053 | |

Undistributed ordinary income | | | 11,648 | | | | 598,977 | | | | 36,859 | |

Undistributed long-term gains | | | 1,455,477 | | | | 2,657,623 | | | | 2,404,795 | |

Total distributable earnings | | $ | 60,477,893 | | | $ | 32,303,434 | | | $ | 20,562,707 | |

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

The difference between the federal income tax cost and the financial statement cost for the Funds is due to certain timing differences in the recognition of capital gains and losses under income tax regulations and GAAP. These timing differences are temporary in nature and are due to the tax deferral of losses on wash sales and adjustments to basis on public traded partnerships.

During the year ended March 31, 2013, Davenport Core Fund and Davenport Value & Income Fund utilized short-term capital loss carryforwards in the amount of $8,216,252 and $510,828, respectively, to offset current year realized gains.

The Funds recognize the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the tax positions taken on Federal income tax returns for all applicable open tax years (tax years ended March 31, 2010 through March 31, 2013) of each Fund and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements.

3. Investment Transactions

During the year ended March 31, 2013, the cost of purchases and proceeds from sales and maturities of investment securities, other than short-term investments and U.S. Government securities, totaled $52,113,492 and $45,242,839, respectively, for Davenport Core Fund; $102,713,211 and $38,444,311, respectively, for Davenport Value & Income Fund; and $53,302,882 and $28,526,903, respectively, for Davenport Equity Opportunities Fund.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENTS

Each Fund’s investments are managed by Davenport & Company LLC (the “Adviser”) under the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, each Fund pays the Adviser a fee, which is computed and accrued daily and paid monthly, at an annual rate of .75% on its average daily net assets.

Certain officers of the Trust are also officers of the Adviser.

MUTUAL FUND SERVICES AGREEMENT

Under the terms of a Mutual Fund Services Agreement between the Trust and Ultimus Fund Solutions, LLC (“Ultimus”), Ultimus provides administrative, pricing, accounting, dividend disbursing, shareholder servicing and transfer agent services for the Funds. For these services, Ultimus receives a monthly fee from each Fund at an annual rate of .15% on its average daily net assets up to $25 million, .125% on the next $25 million of such assets and .10% on such assets in excess of $50 million, subject to a minimum monthly fee of $4,000, plus a shareholder recordkeeping fee at the annual rate of $10 per shareholder account in excess of 1,000 accounts. In addition, the Funds pay out-of-pocket expenses including, but not limited to, postage, supplies and costs of pricing the Funds’ portfolio securities.

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

Certain officers of the Trust are also officers of Ultimus, or of Ultimus Fund Distributors, LLC (the “Distributor”), the principal underwriter of the Funds’ shares and an affiliate of Ultimus. The Distributor is compensated by the Adviser (not the Funds) for acting as principal underwriter.

COMPLIANCE CONSULTING AGREEMENT

Under the terms of a Compliance Consulting Agreement between the Trust and Ultimus, Ultimus provides an individual to serve as the Trust’s Chief Compliance Officer and to administer the Trust’s compliance policies and procedures. For these services, the Funds pay Ultimus an annual base fee of $18,600 plus an asset-based fee equal to 0.01% per annum on the Funds’ aggregate average net assets in excess of $100 million. In addition, the Funds reimburse Ultimus for any reasonable out-of-pocket expenses, if any, incurred in providing these services.

COMPENSATION OF TRUSTEES