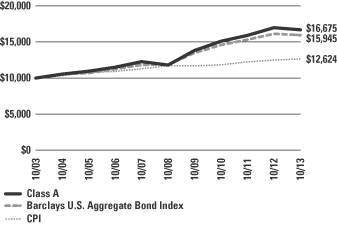

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06017

Aberdeen Global Select Opportunities Fund Inc.

(Exact name of registrant as specified in charter)

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

(Address of principal executive offices) (Zip code)

Ms. Andrea Melia

c/o Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 387-6977

Date of fiscal year end: October 31st

Date of reporting period: October 31, 2013

Item 1. Reports to Shareholders.

Aberdeen Investment Funds

Aberdeen Global Select Opportunities Fund Inc.

Annual Report

October 31, 2013

Aberdeen Global Select Opportunities Fund Inc.

Aberdeen Select International Equity Fund

Aberdeen Select International Equity Fund II

Aberdeen Total Return Bond Fund

Aberdeen Global High Income Fund

Table of Contents

Investors should carefully consider a fund’s investment objectives, risks, fees, and expenses before investing any money. To obtain this and other fund information, please call 1-800-387-6977 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Investment Funds and Aberdeen Global Select Opportunities Fund Inc. are distributed by Aberdeen Fund Distributors, LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (AAMI) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23,1995.

Statement Regarding Availability of Quarterly Portfolio Schedule.

Aberdeen Investment Funds and Aberdeen Global Select Opportunities Fund Inc. file complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “Commission”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the Commission’s website at http://www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330; and the Funds make their most recent Forms N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-800-387-6977. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the Commission’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-800-387-6977; and (ii) on the Commission’s website at www.sec.gov.

Letter to Shareholders

October 31, 2013

Dear Shareholder:

Welcome to the Aberdeen Investment Funds and Aberdeen Global Select Opportunities Fund Inc. Annual Report covering the activities for the twelve-month period ended October 31, 2013.

Market overview

During the reporting period, global equity markets continued their bull run amid widespread dovish monetary policy by central banks and growing optimism toward the end of the summer that the U.S. Federal Reserve’s (Fed) quantitative easing policy would continue at least through the first quarter of 2014. On the other hand, global investment-grade fixed income markets posted mostly negative returns as U.S. Treasury yields spiked and markets experienced a sharp sell-off in risk assets amid confused rhetoric from the Fed in early summer.

Going forward, we believe the overall global economic recovery remains fragile and any action in the form of tapering by the Fed needs to be carefully calculated. We believe that central banks around the world continue to walk the fine line between the fiscal conservatism necessary to tighten up balance sheets in heavily indebted Western nations and the continued stimulus that is necessary to support growth. Given President Obama’s recent nomination of Janet Yellen as the next Fed Chief, we expect policy to likely remain fairly dovish for the short-to-medium term, allowing equity markets to continue their strong run and investment-grade fixed income markets to correct. Therefore, we believe that now is the time for investors to consider diversifying their portfolios globally to gain access to the growth potential of Asia and emerging markets as well as securities that are less interest rate sensitive than U.S. dollar-denominated securities.*

Anne Richards, Aberdeen Group’s Chief Investment Officer, provides you with a detailed insight on the investment marketplace in the Global Market Review and Outlook on the following page.

Aberdeen Developments

In May 2013, Aberdeen Group completed the acquisition of Artio Global Investors Inc., a U.S. publicly-listed asset manager. This acquisition expands Aberdeen’s U.S. business, deepens our distribution network in the U.S., and adds to our existing fixed income capabilities. Artio’s Global High Yield and Total Return Bond teams, including lead portfolio managers Greg Hopper and Don Quigley, have comfortably migrated their teams to Aberdeen’s New York City office.

In June 2013, Aberdeen hosted the second annual U.S. Investment Conference at the TimeWarner Center in New York City. Approximately 200 financial advisors gathered to observe panels of Aberdeen fund managers and guest speakers, including keynote speaker Todd Buchholz, discuss the main theme, “Navigating a New Investment Reality.” Toward the end of the reporting period in October 2013, Aberdeen held its Annual Investment Conference in London, where institutional investors and financial advisors from around the world gathered to observe panel discussions from different Aberdeen investment teams and guest speakers on the outlook for central bank monetary policy and other key economic issues against the backdrop of “Investing in Different Tomorrows.”

During the reporting period, Aberdeen’s global marketing team won a total of 11 STAR Awards from the Mutual Fund Education Association for our mutual fund client and marketing communications. We are pleased and proud to be so recognized.

Additionally, Aberdeen has launched a global campaign to educate investors about how fixed income should be viewed in the current global economic context and to promote Aberdeen’s wide range of fixed income capabilities. This campaign largely promotes the Aberdeen Global High Income Fund and the Aberdeen Total Return Bond Fund as well as our other strategies and funds. To learn more about the campaign and Aberdeen’s fixed income capabilities, visit www.aberdeen-asset.us/fixedincome.

Thank you for choosing Aberdeen Investment Funds and Aberdeen Global Select Opportunities Fund Inc. We value your investment with us.

Yours sincerely,

Gary Marshall

President

Aberdeen Investment Funds

Aberdeen Global Select Opportunities Fund, Inc.

| * | | Diversification does not ensure a profit or eliminate the risk of loss. |

2013 Annual Report

1

Market Review

Major global equity market indices rose sharply during the 12-month period ended October 31, 2013, buoyed mainly by coordinated global central bank monetary policy. The developed markets significantly outperformed their emerging markets counterparts for the period. The U.S. broader-market S&P 500 Index and the MSCI All Country World ex-U.S. Index gained 27.2% and 20.3%, respectively, versus the 6.9% return of the MSCI Emerging Markets Index over the annual period. Investors appeared to be preoccupied initially by the U.S. presidential election in November 2012, and then focused on a succession of impending crises fueled by the ongoing political wrangling in Washington, DC over federal spending and debt management – including a partial shutdown of the U.S. government in October 2013. Elsewhere, there were signs of economic recovery in Europe, albeit a modest upturn, and China rebounded from a comparative slowdown earlier in the annual period, buoyed mainly by loose monetary policy.

Shares of U.S. companies posted healthy gains during the annual period amid the release of modestly improving U.S. economic data and with the support of continued accommodative monetary policy. At first, the uncertain fiscal situation across Europe and the upcoming U.S. presidential election dominated the news, swiftly followed by the impending fiscal cliff and the eventual reality of across-the-board U.S. federal spending cuts. The Federal Reserve (Fed) then assumed the spotlight, as global financial markets clamored for a sign from the central bank as to when it would begin to slow the pace of its monetary easing. Major market indices moved higher after the Fed announced at its September 2013 meeting that it would keep policy unchanged. Late in the period, markets appeared to be preoccupied with the 15-day U.S. government shutdown which began on October 1 after politicians failed to agree on a budget for the 2014 fiscal year. By the end of the reporting period, Congress had reached an accord on temporary funding of government operations and suspending the nation’s debt ceiling until early 2014.

Japan was the strongest performer among the major developed equity markets for the annual period attributable largely to the Bank of Japan’s aggressive monetary easing policy, as well as a notable decline in the yen versus most major global currencies – which was a boon to exports. Europe emerged from recession in the third quarter of 2013 after six consecutive quarters of contraction, while UK gross domestic product (GDP) growth accelerated. The European Central Bank (ECB) lowered its benchmark interest rate in May 2013 and asserted that it could implement negative deposit rates in an effort to encourage banks to lend. However, as of the end of the reporting period, the ECB had not taken additional actions, although ECB President Mario Draghi indicated that all policy options remained on the table.

Emerging market equities provided only modest returns for much of the period until rallying in September and October 2013. Performance initially was dampened by concerns about slowing economic growth in the developing markets, along with the ongoing monetary policy tightening in China. Emerging markets suffered a significant correction in June after the Fed began communicating a timeline for the withdrawal of its quantitative easing program, which has supplied copious amounts of liquidity to emerging economies. The upturn late in the annual period was spurred mainly by an increase in investor risk appetite, as well as improvement in Chinese economic growth. China’s GDP grew 7.8% year over year in the third quarter, up from the 7.5% rate for the previous three-month period, bolstered by the manufacturing sector. Nonetheless, there was a slowdown in infrastructure investment, which we believe may signal that the momentum of the economic rebound is fading, particularly if credit growth continues to decline. In Latin America, economic data over the reporting period generally did not meet expectations. The governments of Brazil, Chile, Colombia and Mexico all downgraded their full-year GDP forecasts. Additionally, the Brazilian central bank embarked on a rate-tightening cycle in an effort to stem inflation.

There was quite a different performance story in the global investment-grade fixed income markets. The Barclays Capital Global Aggregate Bond Index, the broad investment-grade fixed income market benchmark, returned -1.5% for the annual period. The markets were well-supported through May 2013 by central bank asset purchases in Japan and the West, signs of a stalling global economic recovery, and receding inflation. Subsequently, however, U.S. monetary policy dynamics came to the fore in driving market sentiment. Fears that the Fed was about to reduce its stimulus program led to a spike in U.S. Treasury yields, and consequently, a sharp sell-off across other markets. Income investors were not completely “left out in the cold,” however, as positive returns could be found further down on the credit quality ladder, with both the U.S. and global high yield markets posting gains for the annual period. High yield bonds historically have outperformed versus their investment-grade counterparts in rising interest-rate environments.

Outlook

The Fed’s recent deferral of monetary policy tapering has provided some relief for bond markets; however, we think that this is merely a short term reprieve. We maintain our expectation of bond yields gradually rising from their current, historic lows once monetary tightening begins, most likely in the first half of 2014. Due to the vast scale and reach of the U.S. quantitative easing program (dubbed “QE3”), we see the likely impact being felt across global bond markets. In our view, global equities are well-positioned to gain from improving economic activity in the developed world, particularly given the current healthy balance sheets and margins of many companies. We are, however, conscious of the significant rise in company valuations that has occurred, particularly in developed equity markets, and we note the need for an improvement in earnings growth to substantiate further re-rating. Looking ahead, we believe the markets will remain highly sensitive to Fed policy-induced capital outflows, and growth in emerging economies generally should exceed that of the developed world, yet with more volatility. We believe that both demographics and the scope for productivity growth remain positive in emerging markets, and that the fundamentals remain attractive over a longer time horizon.

Anne Richards

Chief Investment Officer

Aberdeen Asset Management

Annual Report 2013

2

Aberdeen Global Select Opportunities Fund Inc. (Unaudited)

Aberdeen Global Select Opportunities Fund Inc. (Class A shares at net asset value net of fees) returned 15.02% for the 12-month period ended October 31, 2013, versus 23.29% for its benchmark, the MSCI All Country World Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of Global Multi-Cap Growth Funds (consisting of 232 funds) was 25.89% for the period.

Market review

Global equities rallied significantly during the reporting period. Following investors’ risk aversion in the second quarter of 2013, equity markets climbed higher, supported by coordinated monetary policy. Sentiment was further boosted as Japanese policymakers explicitly targeted an inflation rate of 2%. The U.S. presidential election and China’s leadership change proceeded smoothly, supporting risk appetite as well. However, the warning in May 2013 from Federal Reserve (Fed) Chairman Ben Bernanke that U.S. monetary policy would be tightened in the near future unsettled markets. Core government bond yields rose sharply, while equity markets, especially in developing countries, corrected. After the initial volatility, Bernanke calmed markets by emphasizing the link of the reduction in quantitative easing (QE) to employment data, thereby suggesting that the degree of future tapering would be measured. Subsequently, he surprised investors by announcing that the Fed was keeping stimulus unchanged following the Federal Open Market Committee meeting in September, which caused markets to rally. Towards the end of the review period, U.S. politicians failed to agree on the federal budget. Consequently, the U.S. government began its first partial shutdown in 17 years. A temporary solution was found by mid-October, but this simply deferred the problems of the budget and federal debt ceiling to early 2014.

Aberdeen’s equity investment process

Aberdeen’s investment approach is based on bottom-up company analysis. We believe that, given the inefficiency of markets, strong long-term returns are achieved by identifying good-quality stocks, buying them at reasonable prices and holding them for the long run. In our view, sound fundamentals drive stock prices over time. As a consequence of our rigorous selection criteria, we introduce new stocks infrequently, the result of which is reflected in our portfolios’ typically low annual turnover rates. Our research process relies primarily on gathering information from meetings with company management and public filings. We prepare a written analysis after each management meeting in a standard Aberdeen format used by our regional teams worldwide. Investment in a new company is made only after our investment managers have met with management, prepared written detailed research reports and thoroughly discussed the merits of the company in a team-based setting. We do not actively seek to overweight or underweight companies in a benchmark index. Instead, we focus on each investment on its own merit. We will not own a stock due solely to its sizeable position in an index.

After Aberdeen Asset Management Inc. was appointed as investment adviser of the Fund effective May 22, 2013, the Aberdeen Global Equity team began to position the Fund in accordance with Aberdeen’s investment process.

Fund positioning and outlook

As bottom-up stock pickers, our country and sector allocations are driven by where we believe that we can find quality companies with attractive valuations. This approach may lead to significant deviations from the MSCI All Country World Index benchmark.

At the end of the reporting period, the Fund was most overweight relative to the benchmark in Switzerland and the UK.

Switzerland – In our view, the Swiss market is home to some of Europe’s best-run companies. The Fund holds substantial positions in food conglomerate Nestle, pharmaceutical companies Roche and Novartis, as well as insurer Zurich Insurance.

UK – We believe that this market has a broad array of diverse companies that benefit from a range of growth drivers that underpins their prospects and earnings. The Fund has positions in Vodafone, Standard Chartered, HSBC, Royal Dutch Shell, BHP Billiton and British American Tobacco, which generate significant portions of their revenue from overseas. We also hold utility Centrica, which is more directly exposed to UK gas consumption.

The Fund’s largest underweight positions were in the U.S., Japan and Germany.

U.S. – We believe that excessive risk and leverage in the banking sector have hobbled the U.S. economy. Recovery is likely to be tenuous, in our opinion, as the country works through its massive imbalances. However, we hold several firms that we think are well-managed, including energy company Schlumberger.

Japan – Although Japan is Asia’s biggest market, we feel that quite a few domestically-oriented corporations remain unattractive due to an inherent lack of competitiveness amid a sluggish domestic economy. The recent stock market rally has been fuelled by hope and expectation surrounding political rhetoric, in our view, rather than evidence of improving fundamentals at the company level.

Germany – The Fund is underweight in this market as we believe that there are better opportunities elsewhere.

The Fund’s most notable sector overweights versus the benchmark were energy and consumer staples.

Energy –The Fund holds a broad range of exposures within this sector covering energy and energy service companies with operations spread around the world. Holdings include Eni and Royal Dutch Shell.

Consumer Staples – The Fund is overweight in this sector as a result of our bottom-up, stock-driven investment process. Holdings in this sector include British American Tobacco, Philip Morris International, and Nestle. We are attracted to the strong characteristics and sound cash flows of the underlying businesses and, in many cases, the exposure these companies have to domestic demand growth in emerging markets.

Conversely, the Fund was most underweight relative to the benchmark in the consumer discretionary and financials sectors.

2013 Annual Report

3

Aberdeen Global Select Opportunities Fund Inc. (Unaudited) (concluded)

Consumer Discretionary – The Fund has only a small position in this sector, which is dominated by developed-market companies exposed to the over-indebted western consumer, in our view.

Financials – Although the Fund holds a diverse range of stocks both in the context of geography and end-market exposure, the position is underweight in comparison to the benchmark.

While the Fund used derivatives during the reporting period, they had minimal impact on performance. The Fund had no derivative positions open as of October 31, 2013.

In our view, investors realize that financial markets are approaching a period of transition, from unconventional U.S. monetary policy towards a more normalized environment. While the initial reaction to the Fed announcement on the likely delay of quantitative easing (QE) tapering was significant, we see indications of growing Fed confidence in U.S. economic growth. In our opinion, it would seem premature for Fed officials to begin managing investor expectations if they still believed that the economic upturn was in doubt. While global economic data continue to improve, the recovery remains uneven. With a lot of positive news already discounted, equity markets require healthy earnings growth to progress meaningfully from these levels. We therefore believe that there will be higher levels of volatility in the medium term.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 800-387-6977 or visiting www.aberdeen-asset.us.

Total returns assume the reinvestment of all distributions. Investment performance reflects fee waivers and, in the absence of such waivers, returns would have been lower. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Annual Report 2013

4

Aberdeen Global Select Opportunities Fund Inc. (Unaudited)

| | | | | | | | | | | | |

Average Annual Total Return (For periods ended October 31, 2013) | | 1 Yr. | | | 5 Yr. | | | Inception | |

Class A1 | | | 15.02% | | | | 8.83% | | | | 5.36% | |

Class I2 | | | 15.23% | | | | 9.08% | | | | 3.87% | |

| 1 | | Class commenced operations on July 01, 2004. |

| 2 | | Class commenced operations on March 14, 2005. |

2013 Annual Report

5

Aberdeen Global Select Opportunities Fund Inc. (Unaudited)

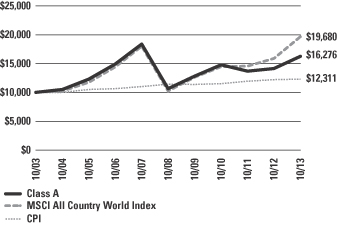

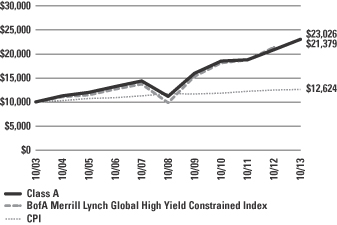

Performance of a $10,000 Investment (as of October 31, 2013)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Global Select Opportunities Fund Inc., Morgan Stanley Capital International (MSCI) All Country World Index and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2013. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI All Country World Index is a free float-adjusted, market capitalization-weighted index that captures large and mid cap representation across 24 developed markets countries including: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK and the US.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Portfolio Summary (as a percentage of net assets)

October 31, 2013 (Unaudited)

| | | | |

| Asset Allocation | | | |

Common Stocks | | | 88.9% | |

Preferred Stocks | | | 9.4% | |

Repurchase Agreement | | | 2.1% | |

Liabilities in excess of other assets | | | (0.4% | ) |

| | | | 100.0% | |

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry. As of October 31, 2013, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by Morgan Stanley Capital International’s and Standard & Poor’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| | | | |

| Top Sectors | | | |

Financials | | | 18.4% | |

Energy | | | 17.6% | |

Consumer Staples | | | 16.6% | |

Health Care | | | 12.9% | |

Information Technology | | | 8.8% | |

Materials | | | 8.5% | |

Industrials | | | 8.0% | |

Telecommunication Services | | | 4.5% | |

Utilities | | | 1.9% | |

Consumer Discretionary | | | 1.1% | |

Other | | | 1.7% | |

| | | | 100.0% | |

| | | | |

| Top Holdings* | | | |

Roche Holding AG | | | 4.0% | |

British American Tobacco PLC | | | 3.7% | |

Philip Morris International, Inc. | | | 3.6% | |

Vodafone Group PLC | | | 3.5% | |

Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 3.1% | |

Johnson & Johnson | | | 3.0% | |

CVS Caremark Corp. | | | 3.0% | |

Novartis AG | | | 3.0% | |

Royal Dutch Shell PLC, B Shares | | | 3.0% | |

Standard Chartered PLC | | | 2.9% | |

Other | | | 67.2% | |

| | | | 100.0% | |

| | | | |

| Top Countries | | | |

United States | | | 29.1% | |

United Kingdom | | | 18.6% | |

Switzerland | | | 11.8% | |

Brazil | | | 6.5% | |

Italy | | | 5.6% | |

Japan | | | 4.4% | |

Sweden | | | 4.2% | |

Canada | | | 4.0% | |

Taiwan | | | 3.1% | |

Republic of South Korea | | | 2.9% | |

Other | | | 9.8% | |

| | | | 100.0% | |

| * | | For the purpose of listing top holdings, repurchase agreements included as part of Other. |

Annual Report 2013

6

Statement of Investments

October 31, 2013

Aberdeen Global Select Opportunities Fund Inc.

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

COMMON STOCKS (88.9%) | | | | | | | | |

AUSTRALIA (1.4%) | | | | | | | | |

Financials (1.4%) | | | | | | | | |

QBE Insurance Group Ltd. | | | 8,300 | | | $ | 116,323 | |

CANADA (4.0%) | | | | | | | | |

Industrials (2.1%) | | | | | | | | |

Canadian National Railway Co. | | | 1,600 | | | | 175,749 | |

Materials (1.9%) | | | | | | | | |

Potash Corp. of Saskatchewan, Inc. | | | 5,000 | | | | 155,344 | |

| | | | | | | | 331,093 | |

CHINA (1.5%) | | | | | | | | |

Energy (1.5%) | | | | | | | | |

PetroChina Co. Ltd., H Shares | | | 106,000 | | | | 121,408 | |

FRANCE (1.0%) | | | | | | | | |

Industrials (1.0%) | | | | | | | | |

Schneider Electric SA | | | 1,000 | | | | 84,357 | |

HONG KONG (2.5%) | | | | | | | | |

Financials (2.5%) | | | | | | | | |

AIA Group Ltd. | | | 25,500 | | | | 129,423 | |

Swire Pacific Ltd., Class A | | | 7,000 | | | | 80,942 | |

| | | | | | | | 210,365 | |

ITALY (5.6%) | | | | | | | | |

Energy (5.6%) | | | | | | | | |

Eni SpA | | | 8,800 | | | | 223,121 | |

Tenaris SA, ADR | | | 5,100 | | | | 238,731 | |

| | | | | | | | 461,852 | |

JAPAN (4.4%) | | | | | | | | |

Financials (1.0%) | | | | | | | | |

Daito Trust Construction Co. Ltd. | | | 800 | | | | 81,623 | |

Industrials (1.5%) | | | | | | | | |

FANUC Corp. | | | 800 | | | | 128,182 | |

Materials (1.9%) | | | | | | | | |

Shin-Etsu Chemical Co. Ltd. | | | 2,800 | | | | 157,823 | |

| | | | | | | | 367,628 | |

MEXICO (1.8%) | | | | | | | | |

Consumer Staples (1.8%) | | | | | | | | |

Fomento Economico Mexicano SAB de CV, ADR | | | 1,600 | | | | 149,280 | |

SINGAPORE (1.0%) | | | | | | | | |

Financials (1.0%) | | | | | | | | |

City Developments Ltd. | | | 10,000 | | | | 83,041 | |

SOUTH AFRICA (1.0%) | | | | | | | | |

Telecommunication Services (1.0%) | | | | | | | | |

MTN Group Ltd. | | | 4,200 | | | | 83,761 | |

SWEDEN (4.2%) | | | | | | | | |

Financials (2.0%) | | | | | | | | |

Nordea Bank AB | | | 13,000 | | | | 166,743 | |

Industrials (1.4%) | | | | | | | | |

Atlas Copco AB, A Shares | | | 4,100 | | | | 113,920 | |

Information Technology (0.8%) | | | | | | | | |

Telefonaktiebolaget LM Ericsson, B Shares | | | 6,000 | | | | 71,719 | |

| | | | | | | | 352,382 | |

SWITZERLAND (11.8%) | | | | | | | | |

Consumer Staples (2.1%) | | | | | | | | |

Nestle SA | | | 2,400 | | | | 173,596 | |

Financials (2.7%) | | | | | | | | |

Zurich Insurance Group AG * | | | 800 | | | | 221,656 | |

Health Care (7.0%) | | | | | | | | |

Novartis AG | | | 3,200 | | | | 248,954 | |

Roche Holding AG | | | 1,200 | | | | 332,880 | |

| | | | | | | | 581,834 | |

| | | | | | | | 977,086 | |

TAIWAN (3.1%) | | | | | | | | |

Information Technology (3.1%) | | | | | | | | |

Taiwan Semiconductor Manufacturing Co. Ltd., ADR | | | 13,800 | | | | 254,058 | |

UNITED KINGDOM (18.6%) | | | | | | | | |

Consumer Staples (3.7%) | | | | | | | | |

British American Tobacco PLC | | | 5,600 | | | | 309,136 | |

Energy (3.0%) | | | | | | | | |

Royal Dutch Shell PLC, B Shares | | | 7,100 | | | | 246,331 | |

Financials (4.9%) | | | | | | | | |

HSBC Holdings PLC | | | 14,900 | | | | 163,284 | |

Standard Chartered PLC | | | 10,100 | | | | 243,319 | |

| | | | | | | | 406,603 | |

Materials (1.6%) | | | | | | | | |

BHP Billiton PLC | | | 4,300 | | | | 133,366 | |

Telecommunication Services (3.5%) | | | | | | | | |

Vodafone Group PLC | | | 79,600 | | | | 287,103 | |

Utilities (1.9%) | | | | | | | | |

Centrica PLC | | | 27,600 | | | | 156,705 | |

| | | | | | | | 1,539,244 | |

UNITED STATES (27.0%) | | | | | | | | |

Consumer Discretionary (1.1%) | | | | | | | | |

Comcast Corp., Class A | | | 1,900 | | | | 90,402 | |

Consumer Staples (9.0%) | | | | | | | | |

CVS Caremark Corp. | | | 4,000 | | | | 249,040 | |

PepsiCo, Inc. | | | 2,400 | | | | 201,816 | |

Philip Morris International, Inc. | | | 3,300 | | | | 294,096 | |

| | | | | | | | 744,952 | |

See accompanying notes to financial statements.

2013 Annual Report

7

Statement of Investments (concluded)

October 31, 2013

Aberdeen Global Select Opportunities Fund Inc.

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

Energy (5.9%) | | | | | | | | |

Chevron Corp. | | | 1,000 | | | $ | 119,960 | |

EOG Resources, Inc. | | | 1,100 | | | | 196,240 | |

Schlumberger Ltd. | | | 1,800 | | | | 168,696 | |

| | | | | | | | 484,896 | |

Health Care (5.9%) | | | | | | | | |

Baxter International, Inc. | | | 1,800 | | | | 118,566 | |

Johnson & Johnson | | | 2,700 | | | | 250,047 | |

Quest Diagnostics, Inc. | | | 2,000 | | | | 119,820 | |

| | | | | | | | 488,433 | |

Industrials (2.0%) | | | | | | | | |

United Technologies Corp. | | | 1,600 | | | | 170,000 | |

Information Technology (2.0%) | | | | | | | | |

Oracle Corp. | | | 5,000 | | | | 167,500 | |

Materials (1.1%) | | | | | | | | |

Praxair, Inc. | | | 700 | | | | 87,297 | |

| | | | | | | | 2,233,480 | |

Total Common Stocks | | | | | | | 7,365,358 | |

PREFERRED STOCKS (9.4%) | | | | | | | | |

BRAZIL (6.5%) | | | | | | | | |

Energy (1.6%) | | | | | | | | |

Petroleo Brasileiro SA, ADR, Preferred Shares | | | 7,200 | | | | 130,752 | |

Financials (2.9%) | | | | | | | | |

Banco Bradesco SA, ADR, Preferred Shares | | | 16,500 | | | | 237,930 | |

Materials (2.0%) | | | | | | | | |

Vale SA, ADR, Preferred Shares | | | 11,500 | | | | 168,360 | |

| | | | | | | | 537,042 | |

REPUBLIC OF SOUTH KOREA (2.9%) | | | | | | | | |

Information Technology (2.9%) | | | | | | | | |

Samsung Electronics Co. Ltd., GDR, Preferred Shares (a) | | | 500 | | | | 239,550 | |

Total Preferred Stocks | | | | | | | 776,592 | |

REPURCHASE AGREEMENT (2.1%) | | | | | | | | |

UNITED STATES (2.1%) | | | | | | | | |

State Street Bank, 0.00%, dated 10/31/2013, due 11/01/2013, repurchase price $171,625 collateralized by Federal Home Loan Mortgage Corp., maturity 09/10/2015; total market value of $180,031 | | $ | 171,625 | | | | 171,625 | |

Total Repurchase Agreement | | | | | | | 171,625 | |

Total Investments

(Cost $8,056,448) (b)—100.4% | | | | | | | 8,313,575 | |

| | |

Liabilities in excess of other assets—(0.4)% | | | | | | | (35,350 | ) |

Net Assets—100.0% | | | $ | 8,278,225 | |

| * | | Non-income producing security. |

| (a) | | Denotes a security issued under Regulation S or Rule 144A. |

| (b) | | See notes to financial statements for tax unrealized appreciation/depreciation of securities. |

| ADR | | American Depositary Receipt |

| GDR | | Global Depositary Receipt |

See accompanying notes to financial statements.

Annual Report 2013

8

Aberdeen Select International Equity Fund (Unaudited)

Aberdeen Select International Equity Fund (Class A shares at net asset value net of fees) returned 20.70% for the 12-month period ended October 31, 2013, versus 20.29% for its benchmark, the MSCI All Country World ex-U.S. Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of International Multi-Cap Growth Funds (consisting of 335 funds) was 21.94% for the period.

Market review

Global equities rallied significantly during the reporting period. Following investors’ risk aversion in the second quarter of 2013, equity markets climbed higher, supported by coordinated monetary policy. Sentiment was further boosted as Japanese policymakers explicitly targeted an inflation rate of 2%. The U.S. presidential election and China’s leadership change proceeded smoothly, supporting risk appetite as well. However, the warning in May 2013 from Federal Reserve (Fed) Chairman Ben Bernanke that U.S. monetary policy would be tightened in the near future unsettled markets. Core government bond yields rose sharply, while equity markets, especially in developing countries, corrected. After the initial volatility, Bernanke calmed markets by emphasizing the link of the reduction in quantitative easing (QE) to employment data, thereby suggesting that the degree of future tapering would be measured. Subsequently, he surprised investors by announcing that the Fed was keeping stimulus unchanged following the Federal Open Market Committee meeting in September, which caused markets to rally. Towards the end of the review period, U.S. politicians failed to agree on the federal budget. Consequently, the U.S. government began its first partial shutdown in 17 years. A temporary solution was found by mid-October, but this simply deferred the problems of the budget and federal debt ceiling to early 2014.

Aberdeen’s equity investment process

Aberdeen’s investment approach is based on bottom-up company analysis. We believe that, given the inefficiency of markets, strong long-term returns are achieved by identifying good-quality stocks, buying them at reasonable prices and holding them for the long run. In our view, sound fundamentals drive stock prices over time. As a consequence of our rigorous selection criteria, we introduce new stocks infrequently, the result of which is reflected in our portfolios’ typically low annual turnover rates. Our research process relies primarily on gathering information from meetings with company management and public filings. We prepare a written analysis after each management meeting in a standard Aberdeen format used by our regional teams worldwide. Investment in a new company is made only after our investment managers have met with management, prepared written detailed research reports and thoroughly discussed the merits of the company in a team-based setting. We do not actively seek to overweight or underweight companies in a benchmark index. Instead, we focus on each investment on its own merit. We will not own a stock due solely to its sizeable position in an index.

After Aberdeen Asset Management Inc. was appointed as investment adviser of the Fund effective May 22, 2013, the Aberdeen Global Equity team began to position the Fund in accordance with Aberdeen’s investment process.

Fund positioning and Outlook

As bottom-up stock pickers, our country and sector allocations are driven by where we believe that we can find quality companies with attractive valuations. This approach may lead to significant deviations from the benchmark MSCI All Country World ex-U.S. Index.

At the end of the reporting period, the Fund was most overweight relative to the benchmark in Switzerland and the UK.

Switzerland – In our view, the Swiss market is home to some of Europe’s best-run companies. The Fund holds substantial positions in food conglomerate Nestle, pharmaceutical companies Roche and Novartis, as well as insurer Zurich Insurance.

UK – We believe that this market has a broad array of diverse companies that benefit from a range of growth drivers that underpins their prospects and earnings. The Fund has positions in Vodafone, Standard Chartered, HSBC, Royal Dutch Shell, BHP Billiton and British American Tobacco, which generate significant portions of their revenue from overseas. We also hold utility Centrica, which is more directly exposed to UK gas consumption.

The Fund’s largest underweight positions were in Japan and Germany.

Japan – Although Japan is Asia’s biggest market, we feel that quite a few domestically-oriented corporations remain unattractive due to an inherent lack of competitiveness amid a sluggish domestic economy. The recent stock market rally has been fuelled by hope and expectation surrounding political rhetoric, in our view, rather than evidence of improving fundamentals at the company level.

Germany – The Fund is underweight in this market as we believe that there are better opportunities elsewhere.

The Fund’s most notable sector overweights versus the benchmark were energy and consumer staples.

Energy – The Fund holds a broad range of exposures within this sector covering energy and energy service companies with operations spread around the world. Holdings include Eni and Royal Dutch Shell.

Consumer Staples – The Fund is overweight in this sector as a result of our bottom-up, stock-driven investment process. Holdings in this sector include British American Tobacco, Philip Morris International, and Nestle. We are attracted to the strong characteristics and sound cash flows of the underlying businesses and, in many cases, the exposure these companies have to domestic demand growth in emerging markets.

Conversely, the Fund was most underweight relative to the benchmark in the consumer discretionary and financials sectors.

Consumer Discretionary – The Fund has only a small position in this sector, which is dominated by developed-market companies exposed to the over-indebted western consumer, in our view.

2013 Annual Report

9

Aberdeen Select International Equity Fund (Unaudited) (concluded)

Financials – Although the Fund holds a diverse range of stocks both in the context of geography and end-market exposure, the position is underweight in comparison to the benchmark.

The Fund’s use of total return swaps, forward foreign exchange contracts and futures contracts positively contributed to the performance of the Fund during the year. The Fund had no derivative positions open as of October 31, 2013.

In our view, investors realize that financial markets are approaching a period of transition, from unconventional U.S. monetary policy towards a more normalized environment. While the initial reaction to the Fed announcement on the likely delay of quantitative easing (QE) tapering was significant, we see indications of growing Fed confidence in U.S. economic growth. In our opinion, it would seem premature for Fed officials to begin managing investor expectations if they still believed that the economic upturn was in doubt. While global economic data continue to improve, the recovery remains uneven. With a lot of positive news already discounted, equity markets require healthy earnings growth to progress meaningfully from these levels. We therefore believe that there will be higher levels of volatility in the medium term.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 800-387-6977 or visiting www.aberdeen-asset.us.

Total returns assume the reinvestment of all distributions. Investment performance reflects fee waivers and, in the absence of such waivers, returns would have been lower. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Annual Report 2013

10

Aberdeen Select International Equity Fund (Unaudited)

| | | | | | | | | | | | |

Average Annual Total Return (For periods ended October 31, 2013) | | 1 Yr. | | | 5 Yr. | | | 10 Yr. | |

Class A | | | 20.70% | | | | 5.97% | | | | 6.26% | |

Class I | | | 21.04% | | | | 6.23% | | | | 6.52% | |

2013 Annual Report

11

Aberdeen Select International Equity Fund (Unaudited)

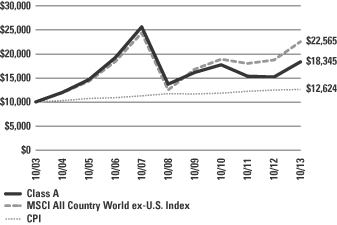

Performance of a $10,000 Investment (as of October 31, 2013)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund, Morgan Stanley Capital International All Country World ex-U.S. Index (MSCI ACWI ex-US), and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2013. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-US is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets excluding the US.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Portfolio Summary (as a percentage of net assets)

October 31, 2013 (Unaudited)

| | | | |

| Asset Allocation | | | |

Common Stocks | | | 87.3% | |

Preferred Stocks | | | 11.6% | |

Government Bonds | | | 0.3% | |

Exchange Traded Funds | | | 0.2% | |

Repurchase Agreement | | | 0.1% | |

Other assets in excess of liabilities | | | 0.5% | |

| | | | 100.0% | |

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry. As of October 31, 2013, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by Morgan Stanley Capital International’s and Standard & Poor’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| | | | |

| Top Sectors | | | |

Financials | | | 20.6% | |

Energy | | | 14.2% | |

Consumer Staples | | | 14.0% | |

Materials | | | 10.8% | |

Industrials | | | 9.9% | |

Information Technology | | | 9.4% | |

Health Care | | | 9.2% | |

Telecommunication Services | | | 7.9% | |

Utilities | | | 2.9% | |

Other | | | 1.1% | |

| | | | 100.0% | |

| | | | |

| Top Holdings* | | | |

Roche Holding AG | | | 4.9% | |

Samsung Electronics Co. Ltd., Preferred Shares | | | 4.6% | |

British American Tobacco PLC | | | 4.3% | |

Novartis AG | | | 4.3% | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 3.9% | |

Nestle SA | | | 3.9% | |

Vodafone Group PLC | | | 3.6% | |

Eni SpA | | | 3.3% | |

Royal Dutch Shell PLC, B Shares | | | 3.2% | |

Standard Chartered PLC | | | 3.0% | |

Other | | | 61.0% | |

| | | | 100.0% | |

| | | | |

| Top Countries | | | |

United Kingdom | | | 24.3% | |

Switzerland | | | 16.9% | |

Brazil | | | 7.0% | |

Japan | | | 6.6% | |

Italy | | | 6.3% | |

Canada | | | 5.4% | |

Republic of South Korea | | | 4.6% | |

Sweden | | | 4.5% | |

France | | | 4.3% | |

Taiwan | | | 3.9% | |

Other | | | 16.2% | |

| | | | 100.0% | |

| * | | For the purpose of listing top holdings, repurchase agreements included as part of Other. |

Annual Report 2013

12

Statement of Investments

October 31, 2013

Aberdeen Select International Equity Fund

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

COMMON STOCKS (87.3%) | | | | | | | | |

AUSTRALIA (1.5%) | | | | | | | | |

Financials (1.5%) | | | | | | | | |

QBE Insurance Group Ltd. | | | 705,600 | | | $ | 9,888,885 | |

BULGARIA (0.3%) | | | | | | | | |

Financials (0.2%) | | | | | | | | |

LEV Insurance (a)(b)(c) | | | 4,078,860 | | | | 1,933,107 | |

Industrials (0.1%) | | | | | | | | |

Sparki Eltos AD-Lovech (a)(b)(c) | | | 1,321,370 | | | | 358,219 | |

| | | | | | | | 2,291,326 | |

CANADA (5.4%) | | | | | | | | |

Industrials (2.3%) | | | | | | | | |

Canadian National Railway Co. | | | 138,300 | | | | 15,191,317 | |

Materials (2.0%) | | | | | | | | |

Potash Corp. of Saskatchewan, Inc. | | | 434,100 | | | | 13,486,925 | |

Telecommunication Services (1.1%) | | | | | | | | |

TELUS Corp. | | | 208,100 | | | | 7,267,586 | |

| | | | | | | | 35,945,828 | |

CHINA (1.5%) | | | | | | | | |

Energy (1.5%) | | | | | | | | |

PetroChina Co. Ltd., H Shares | | | 8,943,200 | | | | 10,243,145 | |

FRANCE (4.3%) | | | | | | | | |

Consumer Staples (2.3%) | | | | | | | | |

Casino Guichard-Perrachon SA | | | 133,200 | | | | 15,013,781 | |

Industrials (1.0%) | | | | | | | | |

Schneider Electric SA | | | 80,200 | | | | 6,765,425 | |

Utilities (1.0%) | | | | | | | | |

GDF Suez | | | 281,000 | | | | 7,006,234 | |

| | | | | | | | 28,785,440 | |

GERMANY (1.0%) | | | | | | | | |

Materials (1.0%) | | | | | | | | |

Linde AG | | | 34,700 | | | | 6,602,088 | |

HONG KONG (3.3%) | | | | | | | | |

Financials (3.3%) | | | | | | | | |

AIA Group Ltd. | | | 2,924,400 | | | | 14,842,564 | |

Swire Pacific Ltd., Class A | | | 588,900 | | | | 6,809,563 | |

| | | | | | | | 21,652,127 | |

ITALY (6.3%) | | | | | | | | |

Energy (6.3%) | | | | | | | | |

Eni SpA | | | 865,600 | | | $ | 21,946,993 | |

Tenaris SA, ADR | | | 433,100 | | | | 20,273,411 | |

| | | | | | | | 42,220,404 | |

JAPAN (6.6%) | | | | | | | | |

Consumer Staples (1.0%) | | | | | | | | |

Japan Tobacco, Inc. | | | 194,700 | | | | 7,045,001 | |

Financials (1.1%) | | | | | | | | |

Daito Trust Construction Co. Ltd. | | | 69,600 | | | | 7,101,172 | |

Industrials (2.0%) | | | | | | | | |

FANUC Corp. | | | 82,500 | | | | 13,218,836 | |

Materials (2.5%) | | | | | | | | |

Shin-Etsu Chemical Co. Ltd. | | | 291,800 | | | | 16,447,396 | |

| | | | | | | | 43,812,405 | |

LATVIA (0.0%) | | | | | | | | |

Financials (0.0%) | | | | | | | | |

AS Parex Banka* (c) | | | 1,424,182 | | | | – | |

MEXICO (2.5%) | | | | | | | | |

Consumer Staples (2.5%) | | | | | | | | |

Fomento Economico Mexicano SAB de CV, ADR | | | 176,100 | | | | 16,430,130 | |

SERBIA (0.2%) | | | | | | | | |

Financials (0.2%) | | | | | | | | |

Komercijalna Banka ad Beograd* | | | 95,073 | | | | 1,382,962 | |

Industrials (0.0%) | | | | | | | | |

Toza Markovic ad Kikinda* (a)(b)(c) | | | 78,160 | | | | 80,145 | |

| | | | | | | | 1,463,107 | |

SINGAPORE (3.7%) | | | | | | | | |

Financials (1.6%) | | | | | | | | |

City Developments Ltd. | | | 1,253,000 | | | | 10,405,047 | |

Telecommunication Services (2.1%) | | | | | | | | |

Singapore Telecommunications Ltd. | | | 4,570,600 | | | | 13,929,027 | |

| | | | | | | | 24,334,074 | |

SOUTH AFRICA (1.1%) | | | | | | | | |

Telecommunication Services (1.1%) | | | | | | | | |

MTN Group Ltd. | | | 362,600 | | | | 7,231,343 | |

SWEDEN (4.5%) | | | | | | | | |

Financials (2.1%) | | | | | | | | |

Nordea Bank AB | | | 1,107,500 | | | | 14,205,191 | |

Industrials (1.5%) | | | | | | | | |

Atlas Copco AB, A Shares | | | 350,700 | | | | 9,744,301 | |

Information Technology (0.9%) | | | | | | | | |

Telefonaktiebolaget LM Ericsson, B Shares | | | 505,500 | | | | 6,042,362 | |

| | | | | | | | 29,991,854 | |

SWITZERLAND (16.9%) | | | | | | | | |

Consumer Staples (3.9%) | | | | | | | | |

Nestle SA | | | 355,500 | | | | 25,713,931 | |

Financials (2.8%) | | | | | | | | |

Zurich Insurance Group AG* | | | 68,000 | | | | 18,840,704 | |

Health Care (9.2%) | | | | | | | | |

Novartis AG | | | 365,600 | | | | 28,442,957 | |

Roche Holding AG | | | 118,600 | | | | 32,899,697 | |

| | | | | | | | 61,342,654 | |

See accompanying notes to financial statements.

2013 Annual Report

13

Statement of Investments (concluded)

October 31, 2013

Aberdeen Select International Equity Fund

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

Industrials (1.0%) | | | | | | | | |

Schindler Holding AG | | | 46,800 | | | $ | 6,651,383 | |

| | | | | | | | 112,548,672 | |

TAIWAN (3.9%) | | | | | | | | |

Information Technology (3.9%) | | | | | | | | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 6,932,000 | | | | 25,836,178 | |

UNITED KINGDOM (24.3%) | | | | | | | | |

Consumer Staples (4.3%) | | | | | | | | |

British American Tobacco PLC | | | 521,300 | | | | 28,777,229 | |

Energy (4.7%) | | | | | | | | |

John Wood Group PLC | | | 779,600 | | | | 10,170,351 | |

Royal Dutch Shell PLC, B Shares | | | 600,800 | | | | 20,844,487 | |

| | | | | | | | 31,014,838 | |

Financials (5.1%) | | | | | | | | |

HSBC Holdings PLC | | | 1,263,700 | | | | 13,848,417 | |

Standard Chartered PLC | | | 841,900 | | | | 20,282,200 | |

| | | | | | | | 34,130,617 | |

Industrials (2.0%) | | | | | | | | |

Weir Group PLC (The) | | | 366,500 | | | | 13,277,876 | |

Materials (2.7%) | | | | | | | | |

BHP Billiton PLC | | | 572,400 | | | | 17,753,236 | |

Telecommunication Services (3.6%) | | | | | | | | |

Vodafone Group PLC | | | 6,702,500 | | | | 24,174,709 | |

Utilities (1.9%) | | | | | | | | |

Centrica PLC | | | 2,174,500 | | | | 12,346,221 | |

| | | | | | | | 161,474,726 | |

VENEZUELA (0.0%) | | | | | | | | |

Financials (0.0%) | | | | | | | | |

Banco Provincial SA-Banco Universal (a)(c) | | | 18,422 | | | | 281,236 | |

Banco Venezolano de Credito SA* (a)(c) | | | 156 | | | | – | |

| | | | | | | | 281,236 | |

Industrials (0.0%) | | | | | | | | |

Cemex Venezuela SACA-I* (a)(c) | | | 15,843,815 | | | | – | |

Materials (0.0%) | | | | | | | | |

Siderurgica Venezolana Sivensa SACA, ADR (c) | | | 2,847,910 | | | | – | |

| | | | | | | | 281,236 | |

Total Common Stocks | | | | | | | 581,032,968 | |

EXCHANGE TRADED FUNDS (0.2%) | | | | | | | | |

RUSSIA (0.2%) | | | | | | | | |

Renaissance Pre-IPO Fund* (a)(c) | | | 92,634 | | | | 1,389,510 | |

Total Exchange Traded Funds | | | | | | | 1,389,510 | |

GOVERNMENT BONDS (0.3%) | | | | | | | | |

VENEZUELA (0.3%) | | | | | | | | |

Bonos de la Deuda Publica Nacional (VEF), 17.25%, 12/31/2015 (a)(c) | | $ | 10,000,000 | | | | 232,811 | |

Bonos de la Deuda Publica Nacional (VEF), 16.00%, 08/23/2018 (a)(c) | | | 49,500,000 | | | | 1,142,969 | |

Bonos de la Deuda Publica Nacional (VEF), 18.00%, 04/12/2018 (a)(c) | | | 20,000,000 | | | | 473,255 | |

| | | | | | | | 1,849,035 | |

Total Government Bonds | | | | | | | 1,849,035 | |

PREFERRED STOCKS (11.6%) | | | | | | | | |

BRAZIL (7.0%) | | | | | | | | |

Energy (1.7%) | | | | | | | | |

Petroleo Brasileiro SA, ADR, Preferred Shares | | | 611,600 | | | | 11,106,656 | |

Financials (2.7%) | | | | | | | | |

Banco Bradesco SA, ADR, Preferred Shares | | | 1,237,800 | | | | 17,849,076 | |

Materials (2.6%) | | | | | | | | |

Vale SA, ADR, Preferred Shares | | | 1,198,100 | | | | 17,540,184 | |

| | | | | | | | 46,495,916 | |

REPUBLIC OF SOUTH KOREA (4.6%) | | | | | | | | |

Information Technology (4.6%) | | | | | | | | |

Samsung Electronics Co. Ltd., Preferred Shares | | | 32,100 | | | | 30,987,886 | |

Total Preferred Stocks | | | | | | | 77,483,802 | |

REPURCHASE AGREEMENT (0.1%) | | | | | | | | |

UNITED STATES (0.1%) | | | | | | | | |

State Street Bank, 0.00%, dated 10/31/2013, due 11/01/2013, repurchase price $1,007,688 collateralized by Federal Home Loan Bank, maturity 01/08/2016; total market value of $1,031,288 | | $ | 1,007,687 | | | | 1,007,687 | |

Total Repurchase Agreement | | | | | | | 1,007,687 | |

Total Investments

(Cost $724,940,260) (d)—99.5% | | | | | | | 662,763,002 | |

| | |

Other assets in excess of liabilities—0.5% | | | | | | | 3,051,990 | |

Net Assets—100.0% | | | | | | $ | 665,814,992 | |

| * | | Non-income producing security. |

| (a) | | The Fund’s adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. Illiquid securities held by the Fund represent 0.88% of net assets as of October 31, 2013. (unaudited) |

| (b) | | Investment in affiliate. |

| (c) | | Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Board of Trustees. See Note 2(a) of the accompanying notes to financial statements. |

| (d) | | See notes to financial statements for tax unrealized appreciation/depreciation of securities. |

| ADR | | American Depositary Receipt |

See accompanying notes to financial statements.

Annual Report 2013

14

Aberdeen Select International Equity Fund II (Unaudited)

Aberdeen Select International Equity Fund II (Class A shares at net asset value net of fees) returned 20.00% for the 12-month period ended October 31, 2013, versus 20.29% for its benchmark, the MSCI All Country World ex-U.S. Index, during the same period. For broader comparison, the average return of the Fund’s Lipper peer category of International Large-Cap Growth Funds (consisting of 142 funds) was 20.76% for the period.

Market review

Global equities rallied significantly during the reporting period. Following investors’ risk aversion in the second quarter of 2013, equity markets climbed higher, supported by coordinated monetary policy. Sentiment was further boosted as Japanese policymakers explicitly targeted an inflation rate of 2%. The U.S. presidential election and China’s leadership change proceeded smoothly, supporting risk appetite as well. However, the warning in May 2013 from Federal Reserve (Fed) Chairman Ben Bernanke that U.S. monetary policy would be tightened in the near future unsettled markets. Core government bond yields rose sharply, while equity markets, especially in developing countries, corrected. After the initial volatility, Bernanke calmed markets by emphasizing the link of the reduction in quantitative easing (QE) to employment data, thereby suggesting that the degree of future tapering would be measured. Subsequently, he surprised investors by announcing that the Fed was keeping stimulus unchanged following the Federal Open Market Committee meeting in September, which caused markets to rally. Towards the end of the review period, U.S. politicians failed to agree on the federal budget. Consequently, the U.S. government began its first partial shutdown in 17 years. A temporary solution was found by mid-October, but this simply deferred the problems of the budget and federal debt ceiling to early 2014.

Aberdeen’s equity investment process

Aberdeen’s investment approach is based on bottom-up company analysis. We believe that, given the inefficiency of markets, strong long-term returns are achieved by identifying good-quality stocks, buying them at reasonable prices and holding them for the long run. In our view, sound fundamentals drive stock prices over time. As a consequence of our rigorous selection criteria, we introduce new stocks infrequently, the result of which is reflected in our portfolios’ typically low annual turnover rates. Our research process relies primarily on gathering information from meetings with company management and public filings. We prepare a written analysis after each management meeting in a standard Aberdeen format used by our regional teams worldwide. Investment in a new company is made only after our investment managers have met with management, prepared written detailed research reports and thoroughly discussed the merits of the company in a team-based setting. We do not actively seek to overweight or underweight companies in a benchmark index. Instead, we focus on each investment on its own merit. We will not own a stock due solely to its sizeable position in an index.

After Aberdeen Asset Management Inc. was appointed as investment adviser of the Fund effective May 22, 2013, the Aberdeen Global Equity team began to position the Fund in accordance with Aberdeen’s investment process.

Fund positioning and Outlook

As bottom-up stock pickers, our country and sector allocations are driven by where we believe that we can find quality companies with attractive valuations. This approach may lead to significant deviations from the benchmark MSCI All Country World ex-U.S. Index.

At the end of the reporting period, the Fund was most overweight relative to the benchmark in Switzerland and the UK.

Switzerland – In our view, the Swiss market is home to some of Europe’s best-run companies. The Fund holds substantial positions in food conglomerate Nestle, pharmaceutical companies Roche and Novartis, as well as insurer Zurich Insurance.

UK – We believe that this market has a broad array of diverse companies that benefit from a range of growth drivers that underpins their prospects and earnings. The Fund has positions in Vodafone, Standard Chartered, HSBC, Royal Dutch Shell, BHP Billiton and British American Tobacco, which generate significant portions of their revenue from overseas. We also hold utility Centrica, which is more directly exposed to UK gas consumption.

The Fund’s largest underweight positions were in Japan and Germany.

Japan – Although Japan is Asia’s biggest market, we feel that quite a few domestically-oriented corporations remain unattractive due to an inherent lack of competitiveness amid a sluggish domestic economy. The recent stock market rally has been fuelled by hope and expectation surrounding political rhetoric, in our view, rather than evidence of improving fundamentals at the company level.

Germany – The Fund is underweight this market as we believe that there are better opportunities elsewhere.

The Fund’s most notable sector overweights versus the benchmark were energy and consumer staples.

Energy – The Fund holds a broad range of exposures within this sector covering energy and energy service companies with operations spread around the world. Holdings include Eni and Royal Dutch Shell.

Consumer Staples – The Fund is overweight in this sector as a result of our bottom-up, stock-driven investment process. Holdings in this sector include British American Tobacco, Philip Morris International, and Nestle. We are attracted to the strong characteristics and sound cash flows of the underlying businesses and, in many cases, the exposure these companies have to domestic demand growth in emerging markets.

Conversely, the Fund was most underweight relative to the benchmark in the consumer discretionary and financials sectors.

Consumer Discretionary – The Fund has only a small position in this sector, which is dominated by developed-market companies exposed to the over-indebted western consumer, in our view.

2013 Annual Report

15

Aberdeen Select International Equity Fund II (Unaudited) (concluded)

Financials – Although the Fund holds a diverse range of stocks both in the context of geography and end-market exposure, the position is underweight in comparison to the benchmark.

The Fund’s use of total return swaps, forward foreign exchange contracts and futures contracts positively contributed to the performance of the Fund during the year. The Fund had no derivative positions open as of October 31, 2013.

In our view, investors realize that financial markets are approaching a period of transition, from unconventional U.S. monetary policy towards a more normalized environment. While the initial reaction to the Fed announcement on the likely delay of quantitative easing (QE) tapering was significant, we see indications of growing Fed confidence in U.S. economic growth. In our opinion, it would seem premature for Fed officials to begin managing investor expectations if they still believed that the economic upturn was in doubt. While global economic data continue to improve, the recovery remains uneven. With a lot of positive news already discounted, equity markets require healthy earnings growth to progress meaningfully from these levels. We therefore believe that there will be higher levels of volatility in the medium term.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 800-387-6977 or visiting www.aberdeen-asset.us.

Total returns assume the reinvestment of all distributions. Investment performance reflects fee waivers and, in the absence of such waivers, returns would have been lower. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and political and economic risks. These risks are enhanced in emerging markets countries.

Equity stocks of small and mid-cap companies carry greater risk, and more volatility than equity stocks of larger, more established companies.

Please read the prospectus for more detailed information regarding these and other risks.

Annual Report 2013

16

Aberdeen Select International Equity Fund II (Unaudited)

| | | | | | | | | | | | |

Average Annual Total Return (For periods ended October 31, 2013) | | 1 Yr. | | | 5 Yr. | | | Inception1 | |

Class A | | | 20.00% | | | | 6.55% | | | | 4.36% | |

Class I | | | 20.36% | | | | 6.84% | | | | 4.65% | |

| 1 | | Fund commenced operations on May 04, 2005. |

2013 Annual Report

17

Aberdeen Select International Equity Fund II (Unaudited)

Performance of a $10,000 Investment (as of October 31, 2013)

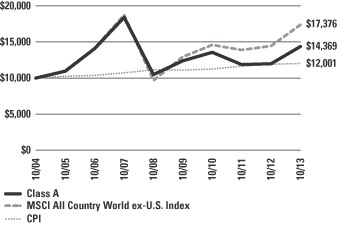

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund II, Morgan Stanley Capital International All Country World ex-U.S. Index (MSCI ACWI ex-US), and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2013. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-US is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets excluding the US.

The CPI represents changes in prices of a basket of goods and services purchased for consumption by urban households.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

Portfolio Summary (as a percentage of net assets)

October 31, 2013 (Unaudited)

| | | | |

| Asset Allocation | | | |

Common Stocks | | | 86.5% | |

Preferred Stocks | | | 11.9% | |

Other assets in excess of liabilities | | | 1.6% | |

| | | | 100.0% | |

The following chart summarizes the composition of the Fund’s portfolio, in industry classification standard sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry. As of October 31, 2013, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by Morgan Stanley Capital International’s and Standard & Poor’s Global Industry Classification Standard Sectors, are comprised of several industry groups.

| | | | |

| Top Sectors | | | |

Financials | | | 20.2% | |

Energy | | | 14.3% | |

Consumer Staples | | | 14.3% | |

Materials | | | 10.8% | |

Industrials | | | 9.8% | |

Information Technology | | | 9.2% | |

Health Care | | | 9.1% | |

Telecommunication Services | | | 7.7% | |

Utilities | | | 3.0% | |

Other | | | 1.6% | |

| | | | 100.0% | |

| | | | |

| Top Holdings | | | |

Roche Holding AG | | | 4.9% | |

Samsung Electronics Co. Ltd., Preferred Shares | | | 4.6% | |

British American Tobacco PLC | | | 4.4% | |

Novartis AG | | | 4.2% | |

Nestle SA | | | 3.7% | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 3.6% | |

Vodafone Group PLC | | | 3.5% | |

Eni SpA | | | 3.3% | |

Royal Dutch Shell PLC, B Shares | | | 3.1% | |

Tenaris SA, ADR | | | 3.1% | |

Other | | | 61.6% | |

| | | | 100.0% | |

| | | | |

| Top Countries | | | |

United Kingdom | | | 24.4% | |

Switzerland | | | 16.6% | |

Brazil | | | 7.3% | |

Japan | | | 6.8% | |

Italy | | | 6.4% | |

Canada | | | 5.4% | |

Republic of South Korea | | | 4.6% | |

Sweden | | | 4.5% | |

France | | | 4.3% | |

Taiwan | | | 3.6% | |

Other | | | 16.1% | |

| | | | 100.0% | |

Annual Report 2013

18

Statement of Investments

October 31, 2013

Aberdeen Select International Equity Fund II

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

COMMON STOCKS (86.5%) | | | | | | | | |

AUSTRALIA (1.6%) | | | | | | | | |

Financials (1.6%) | | | | | | | | |

QBE Insurance Group Ltd. | | | 371,100 | | | $ | 5,200,914 | |

CANADA (5.4%) | | | | | | | | |

Industrials (2.3%) | | | | | | | | |

Canadian National Railway Co. | | | 69,100 | | | | 7,590,166 | |

Materials (1.9%) | | | | | | | | |

Potash Corp. of Saskatchewan, Inc. | | | 199,700 | | | | 6,204,421 | |

Telecommunication Services (1.2%) | | | | | | | | |

TELUS Corp. | | | 112,100 | | | | 3,914,927 | |

| | | | | | | | 17,709,514 | |

CHINA (1.7%) | | | | | | | | |

Energy (1.7%) | | | | | | | | |

PetroChina Co. Ltd., H Shares | | | 4,796,000 | | | | 5,493,126 | |

FRANCE (4.3%) | | | | | | | | |

Consumer Staples (2.3%) | | | | | | | | |

Casino Guichard-Perrachon SA | | | 66,200 | | | | 7,461,804 | |

Industrials (1.0%) | | | | | | | | |

Schneider Electric SA | | | 39,500 | | | | 3,332,099 | |

Utilities (1.0%) | | | | | | | | |

GDF Suez | | | 130,000 | | | | 3,241,318 | |

| | | | | | | | 14,035,221 | |

GERMANY (1.0%) | | | | | | | | |

Materials (1.0%) | | | | | | | | |

Linde AG | | | 16,837 | | | | 3,203,440 | |

HONG KONG (3.1%) | | | | | | | | |

Financials (3.1%) | | | | | | | | |

AIA Group Ltd. | | | 1,361,600 | | | | 6,910,694 | |

Swire Pacific Ltd., Class A | | | 272,500 | | | | 3,150,970 | |

| | | | | | | | 10,061,664 | |

ITALY (6.4%) | | | | | | | | |

Energy (6.4%) | | | | | | | | |

Eni SpA | | | 428,700 | | | | 10,869,542 | |

Tenaris SA, ADR | | | 213,600 | | | | 9,998,616 | |

| | | | | | | | 20,868,158 | |

JAPAN (6.8%) | | | | | | | | |

Consumer Staples (1.3%) | | | | | | | | |

Japan Tobacco, Inc. | | | 112,200 | | | | 4,059,831 | |

Financials (1.0%) | | | | | | | | |

Daito Trust Construction Co. Ltd. | | | 33,400 | | | | 3,407,746 | |

Industrials (2.0%) | | | | | | | | |

FANUC Corp. | | | 40,900 | | | | 6,553,338 | |

Materials (2.5%) | | | | | | | | |

Shin-Etsu Chemical Co. Ltd. | | | 142,800 | | | | 8,048,966 | |

| | | | | | | | 22,069,881 | |

MEXICO (2.6%) | | | | | | | | |

Consumer Staples (2.6%) | | | | | | | | |

Fomento Economico Mexicano SAB de CV, ADR | | | 89,100 | | | | 8,313,030 | |

SINGAPORE (3.5%) | | | | | | | | |

Financials (1.5%) | | | | | | | | |

City Developments Ltd. | | | 596,000 | | | | 4,949,248 | |

Telecommunication Services (2.0%) | | | | | | | | |

Singapore Telecommunications Ltd. | | | 2,162,000 | | | | 6,588,753 | |

| | | | | | | | 11,538,001 | |

SOUTH AFRICA (1.0%) | | | | | | | | |

Telecommunication Services (1.0%) | | | | | | | | |

MTN Group Ltd. | | | 165,900 | | | | 3,308,549 | |

SWEDEN (4.5%) | | | | | | | | |

Financials (2.1%) | | | | | | | | |

Nordea Bank AB | | | 543,300 | | | | 6,968,560 | |

Industrials (1.4%) | | | | | | | | |

Atlas Copco AB, A Shares | | | 165,100 | | | | 4,587,351 | |

Information Technology (1.0%) | | | | | | | | |

Telefonaktiebolaget LM Ericsson, B Shares | | | 263,100 | | | | 3,144,897 | |

| | | | | | | | 14,700,808 | |

SWITZERLAND (16.6%) | | | | | | | | |

Consumer Staples (3.7%) | | | | | | | | |

Nestle SA | | | 168,200 | | | | 12,166,197 | |

Financials (2.8%) | | | | | | | | |

Zurich Insurance Group AG* | | | 33,200 | | | | 9,198,697 | |

Health Care (9.1%) | | | | | | | | |

Novartis AG | | | 176,000 | | | | 13,692,452 | |

Roche Holding AG | | | 57,000 | | | | 15,811,828 | |

| | | | | | | | 29,504,280 | |

Industrials (1.0%) | | | | | | | | |

Schindler Holding AG | | | 22,500 | | | | 3,197,781 | |

| | | | | | | | 54,066,955 | |

TAIWAN (3.6%) | | | | | | | | |

Information Technology (3.6%) | | | | | | | | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 3,192,000 | | | | 11,896,867 | |

UNITED KINGDOM (24.4%) | | | | | | | | |

Consumer Staples (4.4%) | | | | | | | | |

British American Tobacco PLC | | | 258,100 | | | | 14,247,847 | |

Energy (4.6%) | | | | | | | | |

John Wood Group PLC | | | 381,500 | | | | 4,976,897 | |

Royal Dutch Shell PLC, B Shares | | | 294,300 | | | | 10,210,607 | |

| | | | | | | | 15,187,504 | |

See accompanying notes to financial statements.

2013 Annual Report

19

Statement of Investments (concluded)

October 31, 2013

Aberdeen Select International Equity Fund II

| | | | | | | | |

| | | Shares or

Principal

Amount | | | Value | |

Financials (5.1%) | | | | | | | | |

HSBC Holdings PLC | | | 608,600 | | | $ | 6,669,420 | |

Standard Chartered PLC | | | 412,302 | | | | 9,932,762 | |

| | | | | | | | 16,602,182 | |

Industrials (2.1%) | | | | | | | | |

Weir Group PLC (The) | | | 188,800 | | | | 6,840,008 | |

Materials (2.7%) | | | | | | | | |

BHP Billiton PLC | | | 279,800 | | | | 8,678,119 | |

Telecommunication Services (3.5%) | | | | | | | | |

Vodafone Group PLC | | | 3,180,100 | | | | 11,470,048 | |

Utilities (2.0%) | | | | | | | | |

Centrica PLC | | | 1,164,000 | | | | 6,608,876 | |

| | | | | | | | 79,634,584 | |

Total Common Stocks | | | | | | | 282,100,712 | |

PREFERRED STOCKS (11.9%) | | | | | | | | |

BRAZIL (7.3%) | | | | | | | | |

Energy (1.6%) | | | | | | | | |

Petroleo Brasileiro SA, ADR, Preferred Shares | | | 288,300 | | | | 5,235,528 | |

Financials (3.0%) | | | | | | | | |

Banco Bradesco SA, ADR, Preferred Shares | | | 676,400 | | | | 9,753,688 | |

Materials (2.7%) | | | | | | | | |

Vale SA, ADR, Preferred Shares | | | 593,100 | | | | 8,682,984 | |

| | | | | | | | 23,672,200 | |

REPUBLIC OF SOUTH KOREA (4.6%) | | | | | | | | |

Information Technology (4.6%) | | | | | | | | |

Samsung Electronics Co. Ltd., Preferred Shares | | | 15,600 | | | | 15,059,533 | |

Total Preferred Stocks | | | | | | | 38,731,733 | |

Total Investments

(Cost $308,013,257) (a)—98.4% | | | | | | | 320,832,445 | |

| | |

Other assets in excess of liabilities—1.6% | | | | | | | 5,071,923 | |

Net Assets—100.0% | | | $ | 325,904,368 | |

| * | | Non-income producing security. |

| (a) | | See notes to financial statements for tax unrealized appreciation/depreciation of securities. |

| ADR | | American Depositary Receipt |

See accompanying notes to financial statements.

Annual Report 2013