UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06114

Cavanal Hill Funds

(Exact name of registrant as specified in charter)

| Citi Fund Services Ohio, Inc., 4400 Easton Commons, Suite 200, Columbus, OH 43219 |

| (Address of principal executive offices) | (Zip code) |

Citi Fund Services Ohio, Inc., 4400 Easton Commons, Suite 200, Columbus, OH 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-762-7085

Date of fiscal year end: 8/31

Date of reporting period: 8/31/22

Item 1. Reports to Stockholders.

Annual Report

August 31, 2022

U.S. Treasury Fund

Government Securities Money Market Fund

Limited Duration Fund

Moderate Duration Fund

Bond Fund

Strategic Enhanced Yield Fund

Ultra Short Tax-Free Income Fund

Mid Cap Diverse Leadership Fund

Opportunistic Fund

World Energy Fund

Hedged Income Fund

On January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Fund’s website (www.cavanalhillfunds.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling (800) 762-7085.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund you can call (800) 762-7085 to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the fund complex if you invest directly with the Fund.

Table of Contents

Management Discussion of Fund Performance

3

Statements of Assets and Liabilities

22

Statements of Operations

26

Statements of Changes in Net Assets

30

Schedules of Portfolio Investments

36

Notes to the Financial Statements

66

Financial Highlights

76

Report of Independent Registered Public Accounting Firm

98

Additional Fund Information

100

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to the portfolio securities and information during the most recent 12-month period ended June 30th is available without charge, upon request, by calling 1-800-762-7085 or on the Securities and Exchange Commission’s website at http://www.sec.gov.

A complete schedule of each non-Money Market Fund’s portfolio holdings for the first and third fiscal quarter of each fiscal year is filed with the Securities and Exchange Commission on Form N-PORT. The Money Market Funds file completed Schedules of Portfolio Holdings with the Securities and Exchange Commission on Form N-NMFP. Schedules of Portfolio Holdings for the funds are available without charge on the Securities and Exchange Commission’s website at http://www.sec.gov. In addition, the schedules may be reviewed and copied at the Securities and Exchange Commission’s Public Reference Room in Washington D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

This report is authorized for distribution to prospective investors only when preceded or accompanied by a prospectus or summary prospectus. An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing or sending money. This and other important information about the investment company can be found in the Fund’s prospectus or summary prospectus. To obtain a prospectus or summary prospectus, please call 1-800-762-7085. Please read the prospectus carefully before investing.

Cavanal Hill Distributors, Inc., member FINRA, serves as the distributor for the Cavanal Hill Funds.

Shares of the Funds are not deposits or obligations of, or guaranteed or endorsed by, BOKF, NA, any of its affiliates or the Distributor. Shares are NOT FDIC INSURED, nor are they insured by any other government agency. An investment in the Funds involves investment risk, including possible loss of principal.

This document may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act and Section 21E of the Securities Exchange Act. Forward-looking statements give our current expectations of forecasts of future events. They include statements regarding our anticipated future operating and financial performance. Although we believe the expectations and statements reflected in these and other forward-looking statements are reasonable, we can give no assurance they will prove to have been correct. They can be affected by inaccurate assumptions, by inaccurate information from third parties, or by known or unknown risks and uncertainties.

Glossary of Terms

Bloomberg 1-Year Municipal Bond Index includes bonds with a minimum credit rating of BAA3, are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million, and have maturities of 1 to 2 years.

Bloomberg Asset-Backed Securities (ABS) Index includes pass-through, bullet, and controlled amortization structures. The ABS Index includes only the senior class of each ABS issue and the ERISA-eligible B and C tranche.

Bloomberg U.S. Aggregate Bond Index measures the investment-grade, USD-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-through), ABS, and CMBS.

Bloomberg U.S. CMBS Investment Grade Index measures the market of U.S. Agency and US Non-Agency conduit and fusion CMBS deals with a minimum current deal size of $300m. The index is divided into two subcomponents: the U.S. Aggregate-eligible component, which contains bonds that are ERISA eligible under the underwriter’s exemption, and the non-US Aggregate-eligible component, which consists of bonds that are not ERISA eligible.

Bloomberg U.S. Corporate High Yield Bond Index measures the USD-denominated, high-yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/ BB+ or below. Bonds from issuers with an emerging markets (EM) country of risk, based on Barclays EM country definition, are excluded.

Bloomberg U.S. Corporate Investment-Grade Index covers all publicly issued U.S. corporate, non-corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements, to qualify, bonds must be SEC-registered.

Bloomberg U.S. Intermediate Aggregate Bond Index is representative of investment-grade debt issues with maturities from one year up to (but not including) 10 years.

Bloomberg U.S. Mortgage-Backed Securities tracks agency mortgage pass-through securities (no longer incorporates hybrid ARM) guaranteed by Ginnie Mae (GNMA), Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon and vintage.

Bloomberg U.S. Treasury 20+ Year Index measures U.S. dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 20+ years to maturity. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

Bloomberg U.S. Treasury Index is an index of the public obligations of the U.S. Treasury with a remaining maturity of one year or more are non-convertible and are denominated in U.S. dollars. Securities must be rated investment-grade (Baa3/BBB- or higher) by at least two of the following ratings agencies: Moody’s, S&P, and Fitch. If only two of the three agencies rate the security, the lower rating is used to determine index eligibility. If only one of the three agencies rates a security, the rating must be investment grade.

CBOE S&P 500 BuyWrite Index is designed to show the hypothetical performance of a portfolio that engages in a buywrite strategy using S&P 500 index call options.

Hedge Fund Research, Inc. (HFR) utilizes a UCITSIII compliant methodology to construct the HFRX Hedge Fund Indices. The methodology is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize representation of the Hedge Fund Universe. HFRX Indices utilize state-of-the-art quantitative techniques and analysis; multi-level screening, cluster analysis, Monte-Carlo simulations, and optimization techniques ensure that each Index is a pure representation of its corresponding investment focus.

ICE BofA Merrill Lynch 1-5 Year U.S. Corporate/Government Index is comprised of investment-grade government and corporate debt securities with maturities between one- and five-years.

MSCI World Energy Index captures the large- and mid-cap segments across 23 developed markets and includes securities classified in the energy sector per Global Industry Classification Standard.

Russell 1000® Index is designed to represent the performance of companies within specific sectors of the Russell 1000® Index. Methodology equally weights securities within each sector, mitigating security specific risk an offering balanced exposure to particular sectors.

Russell 2000® Index is designed to represent the performance of companies within specific sectors of the Russell 2000® Index. Methodology equally weights securities within each sector, mitigating security specific risk and offering balanced exposure to particular sectors.

Russell 3000® Index is designed to represent the performance of companies within specific sectors of the Russell 3000® Index. Methodology equally weights securities within each sector, mitigating security specific risk and offering balanced exposure to particular sectors.

Russell 3000® Growth Index is a market capitalization weighted index based on the Russell 3000® Index. The Russell 3000® Growth Index includes companies that display signs of above average growth, exhibit higher price-to-book, and forecasted earnings.

Russell 3000® Value Index is a market capitalization weighted equity index maintained by the Russell Investment Group and based on the Russell 3000® Index, included in the index are stocks from the Russell 3000 with lower price-to-book ratios and lower expected growth rates.

Russell Midcap® Index tracks the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 27% of the total market capitalization of the Russell 1000 companies.

Secured Overnight Financing Rate (SOFR) is a measure of the cost of borrowing cash overnight collateralized by Treasury securities, the benchmark is fully transaction based, founded on a robust underlying market–actual transaction level data is provided by Bank of New York Mellon and an affiliate of the Depository Trust & Clearing Corporation, DTCC Solutions LLC.

Securities Industry and Financial Markets Association (SIFMA) Municipal Swap Index is produced by Municipal Market Data (MMD), which is a 7-day high-grade market index comprised of tax-exempt variable rate demand obligations (VRDO’s) from MMD’s extensive database. SIFMA is a leading securities industry trade group representing securities firms, banks, and asset management companies in the U.S. and Hong Kong.

Standard & Poor 500 Index (S&P 500 Index) is regarded as a gauge of the U.S. equities market; this index includes 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 focuses on the large-cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market.

The above indices are unmanaged and do not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Gross Domestic Product (GDP) measures the market value of the goods and services produced by labor and property within the respective country/economic region.

Yield to Worst (YTW) is lowest potential bond yield received without the issuer defaulting, it assumes the worst-case scenario, or earliest redemption possible under terms of the bond.

Organization of Petroleum Exporting Countries (OPEC) is a permanent intergovernmental organization of 14 oil-exporting developing nations that coordinates and unifies the petroleum policies of its Member Countries.

Money Market Funds (Unaudited)

Investment Concerns

You could lose money by investing in the funds. Although each Fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the funds is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The sponsor has no legal obligation to provide financial support to the funds, and you should not expect that the sponsor will provide financial support to the funds at any time.

Market Conditions

The skies finally cleared for the money market fund industry this year as the Federal Open Market Committee (FOMC) began to roll back the monetary accommodation triggered by the COVID 19 pandemic in March 2020. In March 2022, the FOMC raised the federal funds target rate range 25 basis points (0.25%) to 0.25 - 0.50%. It continued to raise rates at each subsequent meeting, including 75-basis-point moves in June and July. The Crane 100 Money Fund Index ended August at 2%, the highest level since June 2019. Additional interest rate hikes are expected as current inflation expectations far exceed those of only six months ago.

Russia’s unanticipated invasion of Ukraine in February had severe macroeconomic shocks for Europe, particularly as it concerned energy. But it did not deter the FOMC from raising short-term rates.

Before beginning to raise rates in early 2022, the Fed anchored interest rates near zero making it difficult to generate yield. The Securities and Exchange Commission (SEC) is expected to announce its final rule regarding new money market reforms in October. While the full effect is yet unknown, some large money market sponsors are urging the SEC to modify the proposed rule.

The U.S. Treasury Fund and the Government Securities Money Market Fund

Both of our money market funds had short weighted average maturities (WAM’s) going into the current rising rate environment. This allows each interest rate increase to be quickly reflected in portfolio yields. In the Government Securities Money Market Fund, we also maintained an allocation to Secured Overnight Financing Rate (SOFR) floating rate notes, which also quickly reflect interest rate moves. According to Money Fund Intelligence, the weighted average maturity for taxable money market funds was 18 days at the end of August, down from 36 days at the start of the year and the lowest level ever.

While interest rates were anchored near zero, earning any yield at all was a struggle, and with expenses taken into consideration, most money market funds yielded zero or almost zero until the FOMC began its interest rate increase campaign. We believed that rates would rise in 2022, and toward the end of 2021 we began preparing the funds for that possibility, with very sizable amounts of cash in overnight repurchase agreements and floating rate notes. Once the FOMC began raising rates in March, we kept maturities short so as to seek to capture each subsequent increase quickly.*

While interest rates were almost zero, we occasionally extended duration out the curve but there was little value to be had. Keeping the portfolios relatively short prepared them for rising rates.*

Overnight repurchase agreements and floating rate notes quickly reflected rising rates. This summer, our Government Securities Money Market Fund began investing in repo with the Federal Reserve Bank of New York, which has a somewhat higher interest rate than many corporate issuers.*

Longer duration securities, purchased before interest rates began going up, acted as a drag on returns once levels started rising.*

Outlook

Over the near term, markets reflect the assumption that interest rates will keep rising into next year, and we share that assumption. The FOMC still has work to do on the inflationary front, and more increases will be required.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

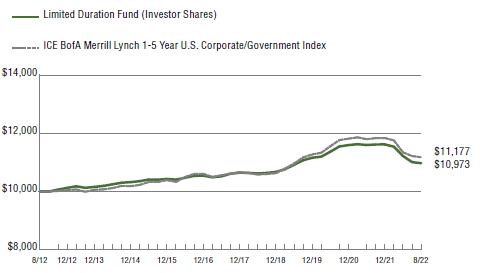

Limited Duration Fund (Unaudited)

Fund Goal

We pursue a strategy of broad diversification in order to benefit from investments in both corporate and government fixed-income securities as well as mortgage-backed securities (MBS) and asset-backed securities (ABS), with the Fund maintaining a dollar-weighted average duration of no longer than 3.5 years.

For the year ended August 31, 2022, the Limited Duration Fund A Shares (at NAV) returned -5.63%; Investor Shares returned -5.72%, while the Institutional Shares returned -5.51%. The Fund’s benchmark, the ICE BofA Merrill Lynch 1-5 Year U.S. Corporate/Government Index1 posted a total return of -5.82%.

Market Conditions

The 12-month period ended August 31, 2022 provided a stark contrast to the year prior in the financial markets. The highest inflation readings seen in a generation pushed the Federal Reserve to reverse course and begin implementing more restrictive monetary policy. In the face of tighter Fed policy, nearly all financial assets suffered steep declines over the period.

With the backdrop of high inflation and rising rates, fixed income assets delivered historically poor returns. Credit spreads also widened during the period as economic growth weakened, causing credit sectors to underperform. Conservatively positioned portfolios with respect to both duration and credit exposure (short duration and higher credit quality) provided the best opportunity to outperform.

Fund Strategy

The Fund maintained a shorter duration than its benchmark during the year, which was the primary driver of its modest outperformance versus the benchmark as interest rates rose sharply. Though the Fund maintained a high quality bias, the benchmark is heavily underweighted to government sectors so any overweight to credit sectors resulted in headwinds as credit spreads widened during the period. The Fund had fairly large allocations to the non-agency residential mortgage-backed securities and non-agency asset-backed securities sectors, which modestly detracted as both sectors experienced spread widening.*

We expect economic growth and inflation to slow over the near to medium term. Accordingly, we believe it is wise to move portfolios into higher credit quality and more liquid securities and we continue to do so. We also favor selectively adding to duration as interest rates have risen significantly. We believe the Fund should perform well in a slowing growth and slowing inflation environment.*

Outlook

With the Fed already well into its rate-hiking campaign and further increases priced into the market, we believe that most of the price declines on the longer end of the yield curve should now be behind us. The Fed is increasing interest rates in an economy that has already decelerated and the lagged nature of the impact from rising interest rates portends a more significant slowdown ahead.

Though inflation readings remain very high, the relatively aggressive tightening of monetary policy from the Fed should eventually be effective at bringing inflation down. The strong U.S. dollar combined with deceleration in rate-sensitive sectors of the economy (housing and autos) should have a strong deflationary impact over the near and medium term.

With economic growth weakening and the Fed following through on its goal of getting inflation back down to 2%, the environment for fixed income assets appears very constructive. With interest rates near their highest levels in more than a decade, expected returns from fixed income look relatively attractive. If the economy does indeed slow further and if inflation recedes, then there also appears to be the potential for price appreciation.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Limited Duration Fund (Unaudited)

Index Description

The performance of the Limited Duration Fund is measured against the ICE BofA Merrill Lynch 1-5 Year U.S. Corporate/Government Index, an unmanaged index that is comprised of investment-grade government and corporate debt securities with maturities between one- and five-years. The index does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Investment Risks

Fixed income securities are subject to interest rate risks. The principal value of a bond falls when interest rates rise and rise when interest rates fall. During periods of rising interest rates, the value of a bond investment is at greater risk than during periods of stable or falling rates. Short-term investment-grade bonds offer less risk and generally a lower rate of return than longer-term higher-yielding bonds. Bond funds will tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price, especially for longer-term issues and in environments of changing interest rates.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Funds’ prospectus.

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return |

| For the periods ended 8/31/2022 | | 1 Year | | | 5 years | | | 10 Year | |

| A Shares (at NAV)1 | | | (5.63)% | | | | 0.58% | | | | 0.97% | |

| A Shares (with 2.00% maximum load)1 | | | (7.54)% | | | | 0.16% | | | | 0.77% | |

| Investor Shares | | | (5.72)% | | | | 0.54% | | | | 0.93% | |

| Institutional Shares | | | (5.51)% | | | | 0.80% | | | | 1.19% | |

| ICE BofA ML 1-5 Year US Corporate/Government Index | | | (5.82)% | | | | 0.89% | | | | 1.12% | |

| Lipper Short Investment Grade Debt Funds Average2 | | | (4.54)% | | | | 0.99% | | | | 1.11% | |

| | | | | | | | | | | | | |

| Expense Ratios | | | | | | | | | | | | |

| | | | | | | | | | | | Gross | |

| A Shares | | | | | | | | | | | 0.86% | |

| Investor Shares | | | | | | | | | | | 1.01% | |

| Institutional Shares | | | | | | | | | | | 0.76% | |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. This performance reflects the Fund’s no-Load Investor class (“Investor Shares”) for periods prior to May 2, 2011 for the A Shares. The A Shares began presenting performance linked to the Investor Class in September of 2011. Unlike Institutional Shares, Investor Shares and A Shares bear a 12b-1 fee of 0.25%. Investor Shares and Institutional Shares are subject to a Shareholder Servicing Fee of 0.25%, whereas the Shareholder Servicing Fee for A Shares is 0.10%. As indicated in the table, A Shares are also subject to a sales charge (Load). Each of these differences is reflected in the performance information. Accordingly, had the A Shares of the Fund been offered for periods before May 2, 2011, the performance information would have been different as a result of differing annual operating expenses. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. |

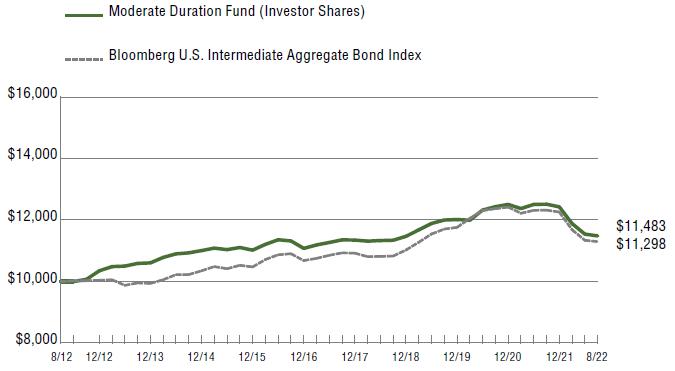

Moderate Duration Fund (Unaudited)

Fund Goal

We pursue a strategy of broad diversification in order to benefit from investments in both corporate and government fixed-income securities as well as mortgage-backed securities (MBS) and asset-backed securities (ABS), with the Fund maintaining a dollar-weighted average duration of no longer than five years.

For the year ended August 31, 2022, the Moderate Duration Fund A Shares (at NAV) returned -8.54%; Investor Shares returned -8.63%, while the Institutional Shares returned -8.31%. The Fund’s benchmark, the Bloomberg U.S. Intermediate Aggregate Bond Index1, showed total return of -8.76%.

Market Conditions

The 12-month period ended August 31, 2022 provided a stark contrast to the year prior in the financial markets. The highest inflation readings seen in a generation pushed the Federal Reserve to reverse course and begin implementing more restrictive monetary policy. In the face of tighter Fed policy, nearly all financial assets suffered steep declines over the period.

With the backdrop of high inflation and rising rates, fixed income assets delivered historically poor returns. Credit spreads also widened during the period as economic growth weakened, causing credit sectors to underperform. Conservatively positioned portfolios with respect to both duration and credit exposure (short duration and higher credit quality) provided the best opportunity to outperform.

Fund Strategy

The Fund maintained a shorter duration than its benchmark during the year, which was the primary driver of its modest outperformance versus the benchmark as interest rates rose sharply. Though the Fund maintained a high quality bias, the benchmark is heavily underweighted to government sectors so any overweight to credit sectors resulted in headwinds as credit spreads widened during the period. The Fund had fairly large allocations to the taxable municipal and non-agency asset-backed securities sectors, which modestly detracted as both sectors experienced spread widening.*

We expect economic growth and inflation to slow over the near to medium term. Accordingly, we believe it is wise to move portfolios into higher credit quality and more liquid securities and we continue to do so. We also favor selectively adding to duration as interest rates have risen significantly. We believe the Fund should perform well in a slowing growth and slowing inflation environment.*

Outlook

With the Fed already well into its rate-hiking campaign and further increases priced into the market, we believe that most of the price declines on the longer end of the yield curve should now be behind us. The Fed is increasing interest rates in an economy that has already decelerated and the lagged nature of the impact from rising interest rates portends a more significant slowdown ahead.

Though inflation readings remain very high, the relatively aggressive tightening of monetary policy from the Fed should eventually be effective at bringing inflation down. The strong U.S. dollar combined with deceleration in rate-sensitive sectors of the economy (housing and autos) should have a strong deflationary impact over the near and medium term.

With economic growth weakening and the Fed following through on its goal of getting inflation back down to 2%, the environment for fixed income assets appears very constructive. With interest rates near their highest levels in more than a decade, expected returns from fixed income look relatively attractive. If the economy does indeed slow further and if inflation recedes, then there also appears to be the potential for price appreciation.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Moderate Duration Fund (Unaudited)

Index Description

The performance of the Moderate Duration Fund is measured against the Bloomberg U.S. Intermediate Aggregate Bond Index, an unmanaged index that is representative of investment-grade debt issues with maturities from one year up to (but not including) 10 years. The index does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Investment Risks

Fixed income securities are subject to interest rate risks. The principal value of a bond falls when interest rates rise and rise when interest rates fall. During periods of rising interest rates, the value of a bond investment is at greater risk than during periods of stable or falling rates. Intermediate-term investment-grade bonds offer less risk and generally a lower rate of return than longer-term higher-yielding bonds. Bond funds will tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price, especially for longer-term issues and in environments of changing interest rates.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Fund’s prospectus.

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return |

| For the periods ended 8/31/2022 | | 1 Year | | | 5 years | | | 10 Year | |

| A Shares (at NAV)1 | | | (8.54)% | | | | 0.19% | | | | 1.43% | |

| A Shares (with 2.00% maximum load)1 | | | (10.37)% | | | | (0.20)% | | | | 1.22% | |

| Investor Shares | | | (8.63)% | | | | 0.17% | | | | 1.39% | |

| Institutional Shares | | | (8.31)% | | | | 0.44% | | | | 1.66% | |

| Bloomberg U.S. Intermediate Aggregate Bond Index | | | (8.76)% | | | | 0.58% | | | | 1.23% | |

| Lipper Short-Intermediate Investment Grade Debt Funds Average2 | | | (6.18)% | | | | 0.82% | | | | 1.10% | |

| | | | | | | | | | | | | |

| Expense Ratios |

| | | | | | | | | | | | Gross | |

| A Shares | | | | | | | | | | | 1.15% | |

| Investor Shares | | | | | | | | | | | 1.29% | |

| Institutional Shares | | | | | | | | | | | 1.04% | |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. This performance reflects the Fund’s no-Load Investor class (“Investor Shares”) for periods prior to May 2, 2011 for the A Shares. The A Shares began presenting performance linked to the Investor Class in September of 2011. Unlike Institutional Shares, Investor Shares and A Shares bear a 12b-1 fee of 0.25%. Investor Shares and Institutional Shares are subject to a Shareholder Servicing Fee of 0.25%, whereas the Shareholder Servicing Fee for A Shares is 0.10%. As indicated in the table, A Shares are also subject to a sales charge (Load). Each of these differences is reflected in the performance information. Accordingly, had the A Shares of the Fund been offered for periods before May 2, 2011, the performance information would have been different as a result of differing annual operating expenses. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. |

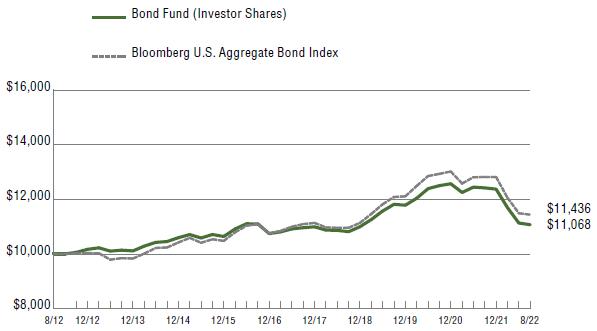

Bond Fund (Unaudited)

Fund Goal

We pursue a strategy of broad diversification in order to benefit from investments in both corporate and government fixed-income securities as well as mortgage-backed securities (MBS) and asset-backed securities (ABS), with the Fund maintaining a dollar-weighted average maturity of three years or more and generally no longer than 10 years.

For the year ended August 31, 2022, the Bond Fund A Shares (at NAV) returned -11.63%; the Investor Shares returned -11.63%; and the Institutional Shares returned -11.35%. The Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index1, showed a total return of -11.52%.

Market Conditions

The 12-month period ended August 31, 2022 provided a stark contrast to the year prior in the financial markets. The highest inflation readings seen in a generation pushed the Federal Reserve to reverse course and begin implementing more restrictive monetary policy. In the face of tighter Fed policy, nearly all financial assets suffered steep declines over the period.

With the backdrop of high inflation and rising rates, fixed income assets delivered historically poor returns. Credit spreads also widened during the period as economic growth weakened, causing credit sectors to underperform. Conservatively positioned portfolios with respect to both duration and credit exposure (short duration and higher credit quality) provided the best opportunity to outperform.

Fund Strategy

The Fund maintained a shorter duration than its benchmark during the year, which helped mitigate the underperformance versus the benchmark, as interest rates rose sharply. Though the Fund maintained a high quality bias, the benchmark is heavily underweighted to government sectors so any overweight to credit sectors resulted in headwinds as credit spreads widened during the period. The Fund had fairly large allocations to the taxable municipal and non-agency asset-backed securities sectors, which modestly detracted as both sectors experienced spread widening.*

We expect economic growth and inflation to slow over the near to medium term. Accordingly, we believe it is wise to move portfolios into higher credit quality and more liquid securities and we continue to do so. We also favor selectively adding to duration as interest rates have risen significantly. We believe the Fund should perform well in a slowing growth and slowing inflation environment.*

Outlook

With the Fed already well into its rate-hiking campaign and further increases priced into the market, we believe that most of the price declines on the longer end of the yield curve should now be behind us. The Fed is increasing interest rates in an economy that has already decelerated and the lagged nature of the impact from rising interest rates portends a more significant slowdown ahead.

Though inflation readings remain very high, the relatively aggressive tightening of monetary policy from the Fed should eventually be effective at bringing inflation down. The strong U.S. dollar combined with deceleration in rate-sensitive sectors of the economy (housing and autos) should have a strong deflationary impact over the near and medium term.

With economic growth weakening and the Fed following through on its goal of getting inflation back down to 2%, the environment for fixed income assets appears very constructive. With interest rates near their highest levels in more than a decade, expected returns from fixed income look relatively attractive. If the economy does indeed slow further and if inflation recedes, then there also appears to be the potential for price appreciation.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Bond Fund (Unaudited)

Index Description

The performance of the Bond Fund is measured against the Bloomberg U.S. Aggregate Bond Index, an unmanaged index that is a market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of at least one year. The index does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these value-added services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Investment Risks

Fixed income securities are subject to interest rate risks. The principal value of a bond falls when interest rates rise and rise when interest rates fall. During periods of rising interest rates, the value of a bond investment is at greater risk than during periods of stable or falling rates. Bond funds will tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price, especially for longer-term issues and in environments of changing interest rates.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Fund’s prospectus.

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return | | | | | | |

| For the periods ended 8/31/2022 | | 1 Year | | 5 years | | 10 Year |

| A Shares (at NAV)1 | | (11.63)% | | 0.07% | | 1.04% |

| A Shares (with 2.00% maximum load)1 | | (13.36)% | | (0.33)% | | 0.84% |

| Investor Shares | | (11.63)% | | 0.04% | | 1.02% |

| Institutional Shares | | (11.35)% | | 0.31% | | 1.27% |

| Bloomberg U.S. Aggregate Bond Index | | (11.52)% | | 0.52% | | 1.35% |

| Lipper Core Bond Funds Average2 | | (11.94)% | | 0.52% | | 1.38% |

| | | | | | | |

| Expense Ratios | | | | | | |

| | | | | | | Gross |

| A Shares | | | | | | 0.82% |

| Investor Shares | | | | | | 0.97% |

| Institutional Shares | | | | | | 0.72% |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. This performance reflects the Fund’s no-Load Investor class (“Investor Shares”) for periods prior to May 2, 2011 for the A Shares. The A Shares began presenting performance linked to the Investor Class in September of 2011. Unlike Institutional Shares, Investor Shares and A Shares bear a 12b-1 fee of 0.25%. Investor Shares and Institutional Shares are subject to a Shareholder Servicing Fee of 0.25%, whereas the Shareholder Servicing Fee for A Shares is 0.10%. As indicated in the table, A Shares are also subject to a sales charge (Load). Each of these differences is reflected in the performance information. Accordingly, had the A Shares of the Fund been offered for periods before May 2, 2011, the performance information would have been different as a result of differing annual operating expenses. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. |

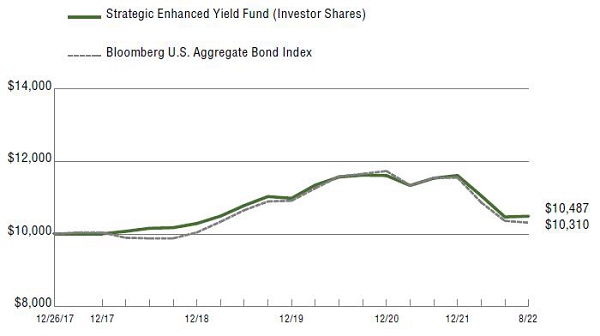

Strategic Enhanced Yield Fund (Unaudited)

Fund Goal

We pursue a strategy of broad diversification in order to achieve optimal risk-adjusted return by tapping into multi-sector opportunities created by market inefficiencies. We focus on out-of-favor sectors, searching for individual securities that we believe are likely to outperform the market. The Fund typically has a substantial allocation to mortgage- backed securities and other securitized products. We have the freedom to invest in a broad range of credit ratings and durations.

For the year ended August 31, 2022, the Strategic Enhanced Yield Fund A Shares (at NAV) returned -9.91% the Investor Shares returned -9.93% and the Institutional Shares returned -9.78%. The Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index1, showed a total return of -11.52%.

Market Conditions

The 12-month period ended August 31, 2022 provided a stark contrast to the year prior in the financial markets. The highest inflation readings seen in a generation pushed the Federal Reserve to reverse course and begin implementing more restrictive monetary policy. In the face of tighter Fed policy, nearly all financial assets suffered steep declines over the period.

With the backdrop of high inflation and rising rates, fixed income assets delivered historically poor returns. Credit spreads also widened during the period as economic growth weakened, causing credit sectors to underperform. Conservatively positioned portfolios with respect to both duration and credit exposure (short duration and higher credit quality) provided the best opportunity to outperform.

Fund Strategy

The Fund maintained a shorter duration than its benchmark during the year, which was the primary driver of its outperformance versus the benchmark as interest rates rose sharply. The Fund had a heavy weighting to the non-agency mortgage-backed securities and non-agency asset-backed securities markets. It also has a large allocation to the corporate sector. These allocations were headwinds as all three sectors experienced spread widening.*

We expect economic growth and inflation to slow over the near to medium term. Accordingly, we believe it is wise to move portfolios into higher credit quality and more liquid securities and we continue to do so. We also favor selectively adding to duration as interest rates have risen significantly. We believe the Fund should perform well in a slowing growth and slowing inflation environment.*

Outlook

With the Fed already well into its rate-hiking campaign and further increases priced into the market, we believe that most of the price declines on the longer end of the yield curve should now be behind us. The Fed is increasing interest rates in an economy that has already decelerated and the lagged nature of the impact from rising interest rates portends a more significant slowdown ahead.

Though inflation readings remain very high, the relatively aggressive tightening of monetary policy from the Fed should eventually be effective at bringing inflation down. The strong U.S. dollar combined with deceleration in rate-sensitive sectors of the economy (housing and autos) should have a strong deflationary impact over the near and medium term.

With economic growth weakening and the Fed following through on its goal of getting inflation back down to 2%, the environment for fixed income assets appears very constructive. With interest rates near their highest levels in more than a decade, expected returns from fixed income look relatively attractive. If the economy does indeed slow further and if inflation recedes, then there also appears to be the potential for price appreciation.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Strategic Enhanced Yield Fund (Unaudited)

Index Description

The performance of the Strategic Enhanced Yield Fund is measured against the Bloomberg U.S. Aggregate Bond Index, an unmanaged index that is a market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of at least one year. The index does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these value-added services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Investment Risks

Fixed income securities are subject to interest rate risks. The principal value of a bond falls when interest rates rise and rise when interest rates fall. During periods of rising interest rates, the value of a bond investment is at greater risk than during periods of stable or falling rates. Short-term investment-grade bonds offer less risk and generally a lower rate of return than longer-term higher-yielding bonds. Bond funds will tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price, especially for longer-term issues and in environments of changing interest rates. High-yield bonds have a higher risk of default or other adverse credit events, but have the potential to pay higher earnings over investment-grade bonds. The higher risk of default, or the inability of the creditor to repay its debt, is the primary reason for the higher interest rates on high-yield bonds.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Fund’s prospectus.

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return | | | | |

| For the periods ended 8/31/2022 | | 1 Year | | Since

Inception

(12/26/2017) |

| A Shares (at NAV)1 | | (9.91)% | | 0.95% |

| A Shares (with 2.00% maximum load)1 | | (11.70)% | | 0.52% |

| Investor Shares | | (9.93)% | | 1.02% |

| Institutional Shares | | (9.78)% | | 1.18% |

| Bloomberg U.S. Aggregate Bond Index | | (11.52)% | | 0.65% |

| Lipper Multi-Sector Income Funds Average2 | | (9.69)% | | 1.14% |

| Expense Ratios | | | | |

| | | | | Gross |

| A Shares | | | | 1.53% |

| Investor Shares | | | | 1.67% |

| Institutional Shares | | | | 1.43% |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. Since inception value calculated from December 31, 2017. |

Ultra Short Tax-Free Income Fund (Unaudited)

Fund Goal

We seek to generate current income that is exempt from federal income taxes by investing primarily in a diversified portfolio of municipal securities, with at least 65% of the Fund’s assets invested in securities that are rated within the three highest long-term or highest short-term rating categories at the time of purchase. The Fund normally maintains a dollar-weighted average maturity of one day to one year.

For the year ended August 31, 2022, the Ultra Short Tax-Free Fund A Shares (at NAV) returned -0.85%; the Investor Shares returned -0.95% and the Institutional Shares returned -0.74%. The Fund’s benchmark, the Bloomberg 1-Year Municipal Bond Index1, showed a total return of -1.59%.

Market Conditions

The Federal Reserve’s pledge to fight the rising inflation rate was the biggest economic story for the period. Price stability is one of the Fed’s mandates and the central bank was faced with a consumer price index (CPI) that increased steadily during the year, ultimately hitting a year-over-year increase of 9.1% in June, the largest gain since the end of 1981. Although the reading fell to 8.5% in July, it is still well above the Fed’s target of 2% inflation.

In response to the rampant increase in inflation, the Fed announced at the beginning of 2022 that it would begin raising the overnight lending rate and initiated an aggressive tightening cycle at the March meeting of the Federal Open Market Committee. The rate hikes at subsequent meetings brought the total increase to 2.25% through the end of the Fund’s fiscal year. In addition to price stability, the Fed’s other mandate is full employment and that aspect of the economy continued to be quite strong. The unemployment rate ended the period at 3.7% and nonfarm payrolls grew by a monthly average of 487,000 through the year.

The short end of the municipal market responded as expected to the Fed’s aggressive tightening, as yields moved considerably higher throughout the period. The SIFMA index, which is an average of yields on variable rate demand notes (VRDNs), started the period at a paltry 0.02%, but began rising in the spring of 2022 and ultimately reached 1.83% in August, the highest level since April 2020. The fixed rate portion in the short end of the muni market also rose dramatically in the period, as yields in the one-year maturity range moved up about 200 basis points (2.0%).

Although the Russian invasion of Ukraine initially rattled global financial markets, it ultimately had very little impact on the short end of the muni market.

While the rapid rise in rates caused some uneasiness in early 2022 in the short end of the muni market, investors eventually appreciated higher yields after enduring the low-rate environment of recent years. Buying opportunities surfaced throughout the year as rates rose. The VRDN yields rose in conjunction with the Fed’s tightening cycle and investors were also able to lock in fixed-rate paper at attractive levels as rates rose.

The biggest challenge in a rising rate environment is deciding how aggressive to be in purchasing fixed paper. VRDNs provide a nice alternative for investors while they wait on fixed-rate opportunities, as variable rates tend to rise with either a daily or weekly reset.

Fund Strategy

The Fund’s relatively short duration proved to be very effective for the period as the Fund outperformed the benchmark. The mix of VRDNs and fixed-rate paper was a successful strategy in a rising rate environment.*

Outlook

The Fed has maintained its stance of continuing to raise rates until the inflation rate shows signs of getting closer to the 2% target. We expect yields in the short end of the muni market to move higher in conjunction with the overnight lending rate.

The Fund will continue to look for opportunities to lock in fixed-rate paper at attractive levels, while maintaining a core position of VRDNs, as those rates can be expected to reset higher as the Fed maintains its tightening cycle.

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Ultra Short Tax-Free Income Fund (Unaudited)

Index Description

The performance of the Ultra Short Tax-Free Fund is measured against the Bloomberg 1-Year Municipal Bond Index, an unmanaged index that includes bonds with a minimum credit rating of BAA3, are issued as part of a deal of at least $50 million, have an amount outstanding of at least $5 million, and have maturities of 1 to 2 years. The index does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these value-added services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investors cannot invest directly in an index.

Investment Risks

Fixed income securities are subject to interest rate risks. The principal value of a bond falls when interest rates rise and rise when interest rates fall. During periods of rising interest rates, the value of a bond investment is at greater risk than during periods of stable or falling rates. Short-term investment-grade bonds offer less risk and generally a lower rate of return than longer-term higher yielding bonds. Bond funds will tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price, especially for longer-term issues and in environments of changing interest rates. The Fund’s income may be subject to certain state and local taxes and, depending on one’s tax status, to the federal alternative minimum tax.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Fund’s prospectus.

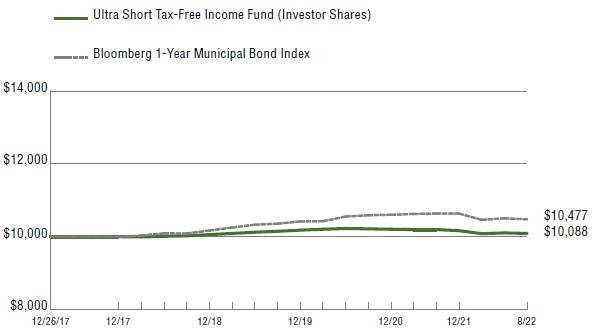

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return | | | | |

| For the periods ended 8/31/2022 | | 1 Year | | Since

Inception

(12/26/2017) |

| A Shares (at NAV)1 | | (0.85)% | | (0.01)% |

| A Shares (with 2.00% maximum load)1 | | (1.83)% | | (0.22)% |

| Investor Shares | | (0.95)% | | 0.19% |

| Institutional Shares | | (0.74)% | | 0.49% |

| Bloomberg 1-Year Municipal Bond Index | | (1.59)% | | 1.00% |

| Lipper Short Municipal Debt Funds Average2 | | (2.75)% | | 0.67% |

| Expense Ratios | | | | |

| | | | | Gross |

| A Shares | | | | 0.92% |

| Investor Shares | | | | 1.07% |

| Institutional Shares | | | | 0.82% |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. Since inception value calculated from December 31, 2017. |

Mid Cap Diverse Leadership Fund (Unaudited)

Fund Goal

We seek to provide positive investment return, net of taxes, by investing at least 80% of net assets in a diversified portfolio of common stocks of Mid Cap U.S. companies that demonstrate governance diversity and leadership. The Fund defines mid-cap securities as those that are included in the Russell MidCap® Index1 at the time of purchase.

For the year ended August 31, 2022, the Mid Cap Diverse Leadership Fund A Shares (at NAV) returned -9.33%; C Shares returned -9.97% and Investor Shares returned -9.32%, while the Institutional Shares returned -9.05%. The Fund’s benchmark, the Russell MidCap® Index1, showed total return of -14.82%.

Market Conditions

During the Fund’s fiscal year, from September 2021 through August 2022, the dominant themes included persistent and rising inflation, concerns regarding central banks pivoting on monetary policy and beginning to aggressively raise interest rates, and ongoing shortages of global goods and labor.

Despite earlier expectations that inflation would be transitory, the Federal Reserve finally admitted that rising prices were persisting. Consequently, in 2022, the Fed pivoted hard and played an aggressive game of catch-up. In addition to quantitative tightening by reducing assets from its balance sheet, the Fed’s four interest rate hikes from March through July raised the federal funds rate from near zero in January to a range of 2.25% to 2.50% by July, with another 0.75-percentage-point hike anticipated for September.

The economic recovery that was still strong late in 2021 gave way to two consecutive quarters of declining real U.S. gross domestic product in the first half of 2022. Despite a robust U.S. labor market and ongoing strength in consumer spending, the uneven global economic recovery was hampered by the impact of ongoing supply chain disruptions and a persistent COVID-19-related labor shortage.

The Russian invasion of Ukraine sent alreadysoaring oil prices even higher. This exacerbated the economic slowdown already underway outside the U.S. along with global inflationary forces.

In this historically difficult environment, value stocks and mega-cap stocks outperformed. On a sector basis, energy stocks outperformed, rising 75% for the annual period through August 31, 2022, in stark contrast to the 11% decline in the S&P 500 Index. Utilities, a classic defensive sector, also did well, gaining 11%. On the flip side, small caps and growth stocks underperformed. Among sectors, communication services stocks trailed significantly, declining 35%.

Fund Strategy

The surge in inflationary pressures and the Federal Reserve’s actions to contain it were the main drivers of financial markets for the end of 2021 and the first half of 2022. In addition, the Russian invasion of Ukraine only added to problems as a significant amount of global energy supply was taken off line, driving oil and natural gas prices higher. Our exposure to the energy sector during this period served as a tailwind and our preference for highquality, profitable businesses though the market downturn helped to reduce some of the potential drawdowns seen in riskier parts of the market.*

From a market cap perspective, we are in line with the benchmark. Our sector allocations varied significantly over the past 12 months; but, as a whole, we leaned on over-weights to technology, consumer discretionary, financials, and industrials. Conversely, we had under-weights to materials, utilities, communication services, and health care. Sector performance reversed course during the early 2022 market sell-off with consumer sensitive and technology industries turning especially negative. Overall, we benefited from the technology and industrial overweights but the underweights in other sectors were more punitive. In total, about 27 basis points (0.27%) of performance were detracted versus the benchmark due to sector allocations.

Our style allocation generated positive performance over the past 12 months. Owning more valueoriented stocks, with lower earnings multiples relative to the benchmark, contributed around 50 basis points. Likewise, a bias towards higherquality, lower-risk names added another 20 basis points. In terms of detractors, the benchmark’s cap-weighting methodology helped to shield it from some of the market volatility relative to the fund. This subtracted around 20 basis points. However, in total, style allocations added roughly 70 basis points for the year.

We managed our exposure to the cyclical areas of the market, including the energy and industrials sectors, as the economy continued to rebound after the pandemic shutdowns. In particular, our top individual contributor was an energy stock that jumped as oil and gas prices surged higher in 2022. As well, stocks in the technology and semiconductor industries added to performance. Stock selection was the biggest factor in the past 12 months of outperformance. Holding on to high-quality assets in this down-market environment helped to add more than 500 basis points versus the benchmark.

Stocks that were highly sensitive to consumer spending and those with the highest valuations produced the greatest drag on the portfolio over the past year. However, the bulk of that underperformance came in the market sell-off, when growth companies were punished the most in response to interest rate hikes.

Outlook

Macroeconomic data will likely continue to slow from here. However, the U.S. still appears to be in a better position than other markets. The primary source of uncertainty is over where the struggle between the economy, inflation, and the Fed will eventually land. Until more clarity arrives on that subject, we are maintaining a fairly neutral sector weighting. In terms of factor themes, however, we are maintaining our preference for high quality companies going forward.*

| 1 | For additional information, please refer to the Glossary of Terms. |

| * | The composition of the Funds’ portfolio is subject to change. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Mid Cap Diverse Leadership Fund (Unaudited)

Index Description

The performance of the Mid Cap Diverse Leadership Fund is measured against the Russell Midcap® Index, which tracks the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap® Index is a subset of the Russell 1000® Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap® Index represents approximately 27% of the total market capitalization of the Russell 1000 companies. The index is unmanaged and does not reflect the deduction of the expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services, but does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investor cannot invest directly in an index.

Investment Risks

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The value of the Fund’s investments may decline due to an increase in interest rates. In general, the longer a security’s maturity, the greater the interest rate risk. The Fund’s yield may decrease due to a decline in interest rates. International investing involves increased risk and volatility. Mid- and small-cap companies may be more vulnerable to adverse business or economic developments.

For a complete description of these and other risks associated with investing in a mutual fund, please refer to the Fund’s prospectus.

Value of a $10,000 Investment

The growth of $10,000 investment chart represents a hypothetical investment in the indicated share class versus a similar investment in the Fund’s benchmark, and represents the reinvestment of distributions and capital gains.

| Average Annual Total Return |

| For the periods ended 8/31/2022 | | 1 Year | | 5 Years | | Since

Inception

(12/30/2016) |

| A Shares (at NAV)1 | | (9.33)% | | 8.83% | | 8.48% |

| A Shares (with 2.00% maximum load)1 | | (11.16)% | | 8.39% | | 8.10% |

| C Shares1 | | (9.97)% | | 8.01% | | 7.55% |

| Investor Shares | | (9.32)% | | 8.80% | | 8.44% |

| Institutional Shares | | (9.05)% | | 9.11% | | 8.71% |

| Russell MidCap Index | | (14.82)% | | 9.17% | | 9.65% |

| Lipper Mid-Cap Core Funds Average2 | | (9.01)% | | 7.72% | | 7.91% |

| | | | | | | |

| Expense Ratios |

| | | | | | | Gross |

| A Shares | | | | | | 12.13% |

| C Shares | | | | | | 13.03% |

| Investor Shares | | | | | | 12.28% |

| Institutional Shares | | | | | | 12.03% |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month end, please call 1-800-762-7085 or visit www.cavanalhillfunds.com.

Investment performance for the Fund’s classes reflects fee waivers that have been in effect during the applicable periods. Without such waivers, the performance would have been lower. Contractual fee waivers are in effect through December 31, 2022.

The above expense ratios are from the Funds’ prospectus dated December 28, 2021. Additional information pertaining to the Funds’ expense ratios for the year ended August 31, 2022 can be found in the Financial Highlights.

| 1 | Class A Shares and C Shares are subject to a 1.00% Maximum Deferred Sales Charge on shares purchased without an initial sales charge and redeemed within 12 months of purchase. Performance data does not reflect the Maximum Deferred Sales Charge. If reflected, one year performance quoted would be lower. |

| 2 | The Lipper Mutual Funds Average is an equally weighted average of the mutual funds within their respective Lipper classification, adjusted for reinvestment of capital gains distributions and income dividends. Since inception value calculated from December 31, 2016. |

Opportunistic Fund (Unaudited)

Fund Goal

We pursue positive investment returns by opportunistically investing in equities, real estate investment trusts (REITs), fixed income securities, preferred stocks, exchange traded funds (ETFs), which may include leveraged and inverse ETFs, options, commodities, and money market funds. The Fund's management team will consider all asset classes and may invest in domestic as well as international securities. The team pursues investment opportunities with the most attractive risk/return profiles.

For the year ended August 31, 2022, the Opportunistic Fund’s A Shares (at NAV) returned -18.79%; the C Shares returned -19.41%; the Investor Shares returned -18.75%, and the Institutional Shares returned -18.53%. The Fund’s benchmarks, the S&P 500 Index1 and the HFRX Equity Hedge Index1, posted total returns of -11.23% and -0.78%, for the same time period.

Market Conditions

During the Fund’s fiscal year, from September 2021 through August 2022, the dominant themes included persistent and rising inflation, concerns regarding central banks pivoting on monetary policy and beginning to aggressively raise interest rates, and ongoing shortages of global goods and labor.

Despite earlier expectations that inflation would be transitory, the Federal Reserve finally admitted that rising prices were persisting. Consequently, in 2022, the Fed pivoted hard and played an aggressive game of catch-up. The Fed’s four interest rate hikes from March through July raised the federal funds rate from near zero in January to a range of 2.25% to 2.50% by July, with another 0.75-percentage-point hike anticipated for September. Additionally, the Fed initiated its quantitative tightening program and began reducing assets from its balance sheet.

The economic recovery that was still strong late in 2021 gave way to two consecutive quarters of declining real U.S. gross domestic product in the first half of 2022. Despite a robust U.S. labor market and ongoing strength in consumer spending, the uneven global economic recovery was hampered by the impact of ongoing supply chain disruptions and a persistent COVID-19-related labor shortage.

The Russian invasion of Ukraine sent alreadysoaring oil prices even higher. This exacerbated the economic slowdown already underway outside the U.S. along with global inflationary forces.

In this historically difficult environment, value stocks and mega-cap stocks outperformed. On a sector basis, energy stocks outperformed, rising 75% for the annual period through August 31, 2022, in stark contrast to the 11% decline in the S&P 500 Index. Utilities, a classic defensive sector, also did well, gaining 11%.

On the flip side, small caps and growth stocks underperformed. Among sectors, communication services stocks trailed significantly, declining 35%.

Fund Strategy

We believe attractive investment opportunities often arise where Wall Street research is lacking. We use bottom-up research to identify opportunities and we adjust the Fund’s level of exposure to risk assets accordingly, which can lead to fluctuations of the Fund’s net risk exposure over time.*

We may use ETFs to hedge the Fund’s long positions, and we may use options on indices or ETFs to hedge a portion of the portfolio. When opportunities are scarce, we also may raise cash to lower our net market exposure. We track and modulate the Fund’s stock market exposure based on our view of market conditions and investment opportunities.*

The institutional shares of the Fund returned -18.53% for the year, compared with the Fund’s benchmark, the HFRX Equity Hedge Index, which declined less than 1%. The Fund’s peers evidently neutralized their market exposure, as reflected by a generally flat return for the 12-month period.*

We increased market exposure during the back half of calendar 2021 while decreasing it during the course of calendar 2022. Additionally, we positioned the Fund defensively with regard to market capitalization, beta (market risk exposure), and sector allocations. The Fund’s defensive positioning was a major headwind during the two-month-long bear market rally that began in June 2022. However, that headwind then reversed as the market began to sell off in mid-August.*

The greatest positive impact on performance came from our large overweight to energy, along with stock selection in energy and technology.*