UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06279 |

|

Harris Associates Investment Trust |

(Exact name of registrant as specified in charter) |

|

Two North La Salle Street, Suite 500 Chicago, Illinois | | 60602-3790 |

(Address of principal executive offices) | | (Zip code) |

|

John R. Raitt

Harris Associates L.P.

Two North La Salle Street, #500

Chicago, Illinois 60602 | Cameron S. Avery

Bell, Boyd & Lloyd LLC

Three First National Plaza, #3100

Chicago, Illinois 60602 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (312) 621-0600 | |

|

Date of fiscal year end: | 09/30/06 | |

|

Date of reporting period: | 09/30/06 | |

| | | | | | | | | |

Item 1. Reports to Shareholders.

ANNUAL REPORT

SEPTEMBER 30, 2006

Advised by Harris Associates L.P.

THE OAKMARK FUNDS

2006 Annual Report

| President's Letter | | | 1 | | |

|

| Summary Information | | | 2 | | |

|

| Fund Expenses | | | 4 | | |

|

| Commentary on The Oakmark and Oakmark Select Funds | | | 6 | | |

|

| The Oakmark Fund | |

|

| Letter from the Portfolio Managers | | | 8 | | |

|

| Schedule of Investments | | | 9 | | |

|

| The Oakmark Select Fund | |

|

| Letter from the Portfolio Managers | | | 13 | | |

|

| Schedule of Investments | | | 14 | | |

|

| The Oakmark Equity and Income Fund | |

|

| Letter from the Portfolio Managers | | | 16 | | |

|

| Schedule of Investments | | | 18 | | |

|

| The Oakmark Global Fund | |

|

| Letter from the Portfolio Managers | | | 22 | | |

|

| Global Diversification Chart | | | 24 | | |

|

| Schedule of Investments | | | 25 | | |

|

| Commentary on The International and International Small Cap Funds | | | 30 | | |

|

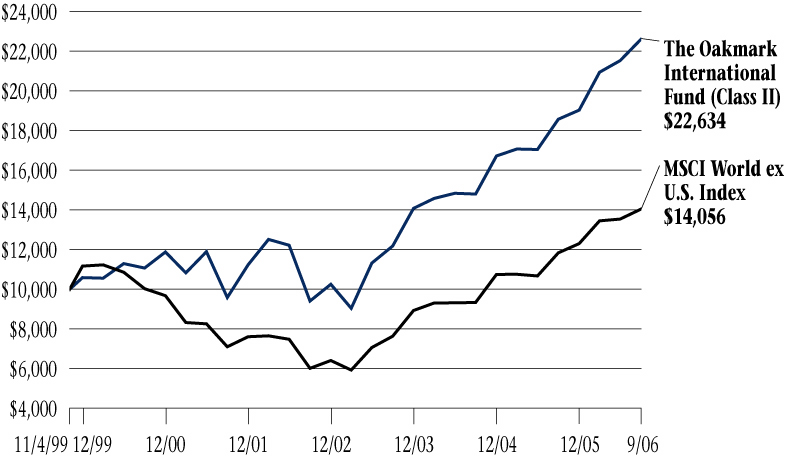

| The Oakmark International Fund | |

|

| Letter from the Portfolio Manager | | | 31 | | |

|

| International Diversification Chart | | | 33 | | |

|

| Schedule of Investments | | | 34 | | |

|

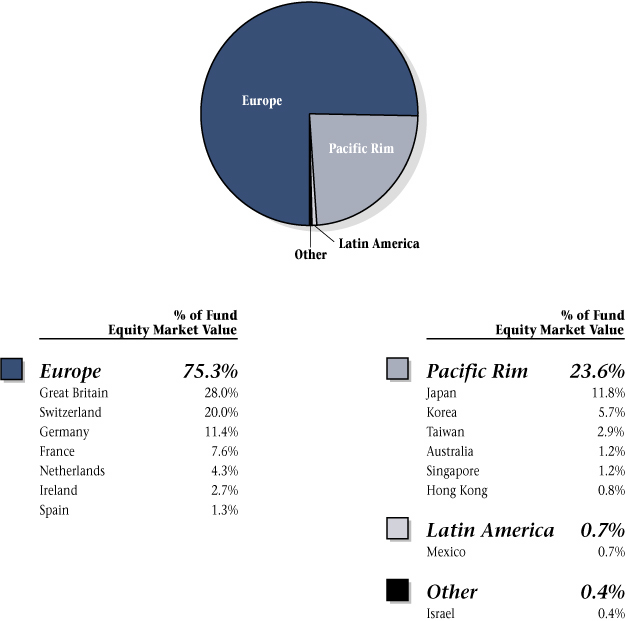

| The Oakmark International Small Cap Fund | |

|

| Letter from the Portfolio Managers | | | 40 | | |

|

| International Diversification Chart | | | 42 | | |

|

| Schedule of Investments | | | 43 | | |

|

| Financial Statements | |

|

| Statements of Assets and Liabilities | | | 50 | | |

|

| Statements of Operations | | | 52 | | |

|

| Statements of Changes in Net Assets | | | 54 | | |

|

| Notes to Financial Statements | | | 60 | | |

|

| Trustees and Officers | | | 80 | | |

|

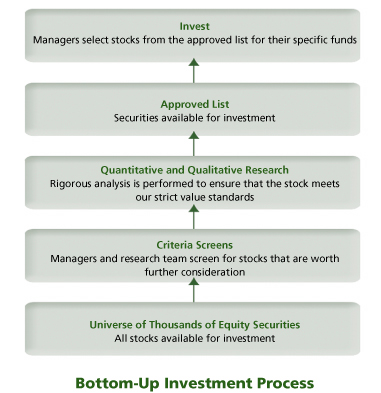

| Oakmark Philosophy and Process | | | 83 | | |

|

| The Oakmark Glossary | | | 84 | | |

|

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements". Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe", "plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

President's Letter

Dear Fellow Shareholders,

World markets rose strongly in the quarter ended September 30. All of our Funds also posted significant positive returns in the quarter. Compounding capital at positive rates of return over long periods is key to long-term wealth creation. Importantly, all of our Funds have produced solidly positive returns year-to-date.

Benchmarks, Over-diversification and Long Term Returns

Understanding a fund manager's investment process and strategy is essential to successful mutual fund investing, so we write about our investment process often. At Oakmark, we continuously search for businesses selling at large discounts to intrinsic value and try to fill our portfolios with the most undervalued of these ideas. We also believe that good investment ideas are scarce—so we concentrate our portfolios. That concentration occurs in two ways. First, the number of stocks in our portfolios is lower than our peers. Second, since we focus on owning the most undervalued ideas available, we often develop holdings that are concentrated in out of favor sectors or industries. We will also have few or even zero holdings in industries where we believe that stocks are fairly valued or overvalued. As a result, our portfolios tend to look quite different from most other funds and the broader market indexes.

Given our approach, we were interested to read of a recent study published by Professors Cremers and Petajisto from Yale University1. The professors' work focused on mutual fund performance, market indexes and how fund managers build their portfolios. As Bill Nygren discusses in his letter this quarter, many fund managers tend to over-diversify their holdings in an attempt to limit the impact of their mistakes. Along the way, however, they often become "closet indexers," owning so many stocks that it is mathematically difficult for their performance to differ much from the market averages. With returns destined to be average, it also becomes tricky for these managers to justify full management fees.

In focusing on this issue, Professors Cremers and Petajisto analyzed data across the mutual fund universe and created a statistic called "Active Share." Simply put, Active Share measures the portion of a mutual fund's portfolio that is different from the fund's benchmark index. Interestingly, the professors found that, while their returns might be more volatile, the funds with the highest Active Share significantly outperformed the market. At the same time, the funds with the lowest Active Share tended to underperform. Although the funds with a high Active Share generally do charge higher fees, the study found that these funds outperformed the market both before and after expenses. In other words, it has been worth paying for the extra cost of truly active portfolio management.

As one would expect from the description of the Oakmark stock selection process above, all of The Oakmark Funds have a high Active Share. The average U.S. equity mutual fund benchmarked against the S&P 5002, has an Active Share of 66%. As of September 30, four of six Oakmark Funds had an Active Share of over 90%, with the other two Funds above 80%. As we have discussed in past letters, our concentrated approach does increase the chance that our portfolios may lag behind the broader market indexes for several quarters or even years. However, we believe that concentrating on our best ideas greatly increases the chances for long-term Fund outperformance. These professors' research seems to indicate that we are on the right track.

Oakmark Offers a New Fund

On October 2, we launched a new Fund in the Oakmark family, The Oakmark Global Select Fund. Oakmark Global Select is a non-diversified, large company, global equity fund. The Fund is managed by David Herro and Bill Nygren, two of our most talented portfolio managers, and it will own the stocks of approximately 20 large companies from around the world. We believe that large, well run, high quality companies are attractively priced in both domestic and international markets. The Fund will be managed using the same value-oriented investment approach that is the hallmark of The Oakmark Funds. As with our other Funds, the portfolio managers and employees of Harris Associates L.P., Oakmark's adviser, have made significant personal investments in Oakmark Global Select.

Thank you for your continued investment and confidence in The Oakmark Funds. We welcome your comments and questions. You can reach us via e-mail at ContactOakmark@oakmark.com.

John R. Raitt

President of The Oakmark Funds

President and CEO of Harris Associates L.P.

1

THE OAKMARK FUNDS

Summary Information

Performance for Period

Ended September 30, 20063

(Unaudited) | | The Oakmark

Fund—Class I

(OAKMX) | | The Oakmark

Select Fund—Class I

(OAKLX) | | The Oakmark

Equity and Income

Fund—Class I

(OAKBX) | |

| 3 Months* | | | 5.56 | % | | | 3.02 | % | | | 2.36 | % | |

| 1 Year | | | 10.46 | % | | | 9.58 | % | | | 6.51 | % | |

Average Annual Total

Return for: | |

| 3 Year | | | 10.27 | % | | | 10.38 | % | | | 11.54 | % | |

| 5 Year | | | 7.43 | % | | | 8.07 | % | | | 10.59 | % | |

| 10 Year | | | 8.51 | % | | | N/A | | | | 13.46 | % | |

| Since inception | | | 15.25%

(8/5/91) | | | | 17.83%

(11/1/96) | | | | 13.36%

(11/1/95) | | |

Top Five Equity

Holdings as of

September 30, 20064

(Unaudited)

Company and % of Total

Net Assets | | | Washington

Mutual, Inc. 3.2%

McDonald's

Corporation 3.0%

Yum! Brands, Inc. 2.6%

Time Warner Inc. 2.5%

Baxter

International Inc. 2.4% | | | | Washington

Mutual, Inc. 15.0%

Yum! Brands, Inc. 7.6%

H&R Block, Inc. 5.7%

McDonald's

Corporation 5.5%

First Data

Corporation 5.0% | | | | XTO Energy, Inc. 4.0%

Nestle SA 3.1%

General Dynamics

Corporation 3.0%

EnCana Corp 2.7%

Diageo plc 2.6% | | |

Sector

Allocation as of

September 30, 2006

(Unaudited)

Sector and % of

Market Value | | | Consumer

Discretionary 42.6%

Financials 14.5%

Information

Technology 13.1%

Consumer Staples 12.6%

Health Care 9.0%

Industrials 6.9%

Energy 1.3% | | | | Consumer

Discretionary 49.2%

Financials 20.4%

Information

Technology 18.2%

Health Care 7.8%

Industrials 4.4% | | | | U.S. Government

Securities 32.6%

Consumer Staples 12.1%

Consumer

Discretionary 12.0%

Foreign Government

Securities 10.8%

Energy 10.5%

Industrials 7.6%

Financials 6.1%

Health Care 5.6%

Information

Technology 2.5%

Materials 0.2% | | |

The performance data quoted represents past performance. The above performance information for the Funds does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

THE OAKMARK FUNDS

2

Performance for Period

Ended September 30, 20063

(Unaudited) | | The Oakmark

Global Fund—Class I

(OAKGX) | | The Oakmark

International

Fund—Class I

(OAKIX) | | The Oakmark

International

Small Cap Fund—Class I

(OAKEX) | |

| 3 Months* | | | 5.58 | % | | | 5.09 | % | | | 8.42 | % | |

| 1 Year | | | 17.46 | % | | | 22.14 | % | | | 28.50 | % | |

Average Annual Total

Return for: | |

| 3 Year | | | 19.25 | % | | | 23.29 | % | | | 30.47 | % | |

| 5 Year | | | 22.18 | % | | | 19.12 | % | | | 26.58 | % | |

| 10 Year | | | N/A | | | | 11.99 | % | | | 14.64 | % | |

| Since inception | | | 16.67%

(8/4/99) | | | | 13.23%

(9/30/92) | | | | 14.88%

(11/1/95) | | |

Top Five Equity

Holdings as of

September 30, 20064

(Unaudited)

Company and % of Total

Net Assets | | | GlaxoSmithKline plc 3.5%

Snap-on

Incorporated 3.3%

Bayerische Motoren

Werke (BMW) AG 3.2%

Oracle Corporation 3.1%

Julius Baer Holding

Ltd., Class B 3.1% | | | | DaimlerChrysler AG 3.5%

GlaxoSmithKline plc 3.4%

British Sky

Broadcasting

Group plc 3.3%

Bayerische Motoren

Werke (BMW) AG 3.2%

Signet Group plc 3.0% | | | | Square Enix

Co., Ltd. 4.0%

MLP AG 4.0%

Sogecable SA 3.8%

JJB Sports plc 3.8%

Matalan PLC 3.8% | | |

Sector

Allocation as of

September 30, 2006

(Unaudited)

Sector and % of

Market Value | | | Consumer

Discretionary 27.7%

Information

Technology 17.6%

Health Care 11.0%

Financials 11.0%

Consumer Staples 10.8%

Telecommunication

Services 8.6%

Industrials 8.5%

Energy 2.8%

Materials 2.0% | | | | Consumer

Discretionary 34.5%

Financials 21.6%

Consumer Staples 13.9%

Telecommunication

Services 8.1%

Health Care 8.0%

Materials 5.8%

Industrials 5.2%

Information

Technology 2.6%

Energy 0.3% | | | | Consumer

Discretionary 34.0%

Information

Technology 17.9%

Industrials 17.7%

Financials 14.1%

Consumer Staples 6.3%

Health Care 5.4%

Materials 3.1%

Telecommunication

Services 1.5% | | |

THE OAKMARK FUNDS

3

FUND EXPENSES

A shareholder of each Fund incurs two types of costs: (1) transaction costs, such as redemption fees, and (2) ongoing costs, including investment advisory fees, transfer agent fees, and other fund expenses. The examples below are intended to help shareholders understand the ongoing cost (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses

The following table provides information about actual account values and actual fund expenses for Class I of each Fund. The table shows the expenses a Class I shareholder would have paid on a $1,000 investment in each Fund from April 1, 2006, to September 30, 2006, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. A Class I shareholder can estimate expenses incurred for the period by dividing the account value at September 30, 2006, by $1,000 and multiplying the result by the number in the Expenses Paid During Period row as shown below.

Certain accounts invested for 90 days or less may be charged a 2% redemption fee. Please consult the Funds' prospectus at oakmark.com for more information.

| | | The Oakmark Fund | | The Oakmark Select Fund | | The Oakmark Equity and Income Fund | | The Oakmark Global Fund | | The Oakmark International Fund | | The Oakmark International Small Cap Fund | |

Beginning

Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account Value | | $ | 1,051.80 | | | $ | 1,022.20 | | | $ | 1,039.60 | | | $ | 1,064.20 | | | $ | 1,081.40 | | | $ | 1,077.90 | | |

Expenses Paid

During Period* | | $ | 5.30 | | | $ | 4.97 | | | $ | 4.35 | | | $ | 6.05 | | | $ | 5.84 | | | $ | 7.03 | | |

Annualized

Expense Ratio | | | 1.03 | % | | | 0.98 | % | | | 0.85 | % | | | 1.17 | % | | | 1.12 | % | | | 1.35 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

4

FUND EXPENSES

Hypothetical Example for Comparison Purposes

The following table provides information about hypothetical account values and hypothetical expenses for Class I of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the third line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, the total costs would have been higher.

| | | The Oakmark Fund | | The Oakmark Select Fund | | The Oakmark Equity and Income Fund | | The Oakmark Global Fund | | The Oakmark International Fund | | The Oakmark International Small Cap Fund | |

Beginning

Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account Value | | $ | 1,019.90 | | | $ | 1,020.16 | | | $ | 1,020.81 | | | $ | 1,019.20 | | | $ | 1,019.45 | | | $ | 1,018.30 | | |

Expenses Paid

During Period* | | $ | 5.22 | | | $ | 4.96 | | | $ | 4.31 | | | $ | 5.92 | | | $ | 5.67 | | | $ | 6.83 | | |

Annualized

Expense Ratio | | | 1.03 | % | | | 0.98 | % | | | 0.85 | % | | | 1.17 | % | | | 1.12 | % | | | 1.35 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

5

THE OAKMARK AND OAKMARK SELECT FUNDS

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"If you think most stocks are attractively priced, how come you don't find as many to buy as most mutual funds do?"—Representative shareholder e-mail

Oakmark is one of few mutual fund families that makes their portfolio managers accessible via e-mail. I've often been asked why we "waste" our time answering these shareholder questions. I have three reasons: 1) We consider communicating with shareholders to be an opportunity to help them understand how we think and why we invest as we do. The better our shareholders understand us, the more likely they are to be long-term shareholders—and that is good for all of us. 2) Shareholders have been very respectful of our time. With the exception of a few 2:00 AM rants that senders often regret the next day, their questions are usually honest requests for better understanding. 3) Occasionally, a consistent theme develops from these e-mails that highlights an area where our communication needs to improve.

Such a theme has emerged recently regarding portfolio construction. I think we've done a pretty good job explaining how we select the stocks we own. Our three criteria—discount to value, growth in value, and owner-oriented management—appear at the top of each of these quarterly commentaries and are frequently topics for the reports. But we have not devoted nearly as much attention to an equally important topic: after identifying stocks that meet our criteria, how do we build the portfolio? And as the question at the top of the report shows, there is some confusion on this issue!

To make sense of how we structure a portfolio, we first need to identify our goals. First, the reason our Funds exist is to make money for our shareholders. So, we take great satisfaction when we report to you that a Fund has reached a new all-time high price. Some have commented that these new-high references are "cute" or even "corny." And given how sophisticated performance measurement has become, I can see why they think that. Simple as it may be, we think it is the most important thing we can say about our Funds' performance. We view new highs as a reminder that our primary objective is to increase your capital. We're pleased that even during the past three years, when other funds have increased more than we have, Oakmark has reached a new high in nine of those twelve quarters, and Oakmark Select did so in eight. (And both have already hit new highs again this quart er.)

Another important goal is to outperform passive management. An index fund can match the stock market's return at almost no cost to its shareholders. This is important because a broad-based index, such as the S&P 5002, has historically provided a return that was superior to most investment alternatives. Matching that return creates a pretty high hurdle, and if we—or any other active managers—are going to justify our fees, then over long periods of time we either have to earn a higher return than the market or deliver a similar return but with less risk. We believe our three investment criteria simultaneously address both goals—higher than average returns and lower than average risk. As active managers, we must balance the potential risk that an individual stock could perform meaningfully worse than the market with the potential benefit of concentrating our assets in the stocks we deem most attractive.

A typical mutual fund manager today spreads portfolio assets across more than 100 stocks. As a competing fund manager I was seated next to for a panel discussion once said, "We keep our position sizes small enough so that our mistakes don't hurt us." That pretty much sums up the positive case for diversification—minimize the cost of your mistakes. Though the logic of that approach is sound, it is tough, if not impossible, to diversify your way to superior performance. The law of large numbers says that the more stocks you own, the more likely it becomes that your portfolio performs like the average of all stocks. And if you are content with an average outcome, a passive portfolio, or index fund, is a lower cost solution.

Since we believe our approach can identify above-average stocks, we take a very different tack. The problem with owning so many stocks that mistakes don't matter, is that successes won't matter then either. At Oakmark, we want to own enough of each of our stocks so that our successes do matter.

The Oakmark Fund is the more diversified of the two Funds I work on. But even Oakmark is much more concentrated than the average mutual fund. At most times our portfolio is invested in about 50-60 stocks, roughly half the average fund's number of holdings. A typical position for us is just under 2% of assets, and it is unusual to have a position as high as 4% of assets. We keep Oakmark this diversified so that we are comfortable when a long-term investor tells us

THE OAKMARK AND OAKMARK SELECT FUNDS

6

they have put most of their stock market investments in The Oakmark Fund.

The Oakmark Select Fund owns less than half as many stocks as The Oakmark Fund does—usually about 20 stocks. It is a non-diversified fund, and because of that, we routinely caution that it is a high-risk strategy to use it as your only mutual fund. With only 20 stocks, a normal position for Oakmark Select is about 4% of assets (bigger than Oakmark's largest position), and our top holdings are usually a double-digit percentage of the portfolio. For example, both Funds' largest position today is Washington Mutual. It represents 3% of Oakmark's assets and 15% of Select's. If Washington Mutual continues to be a profitable stock, then it will be an important positive for Oakmark, but it will be far more important to Select. And if it doesn't, Select will suffer more than Oakmark does. We believe that the risk is worth taking, but we need Select's shareholders to understand the volatility they could experience.

So when we find lots of attractive stocks, why don't we just add them all to our portfolios? Most investors define "attractive" relative to cash. When we think about adding a new stock to our portfolios, the hurdle isn't just cash, but rather all the other stocks we already own. Since our portfolios are normally close to fully invested, adding a new stock needs to be funded by selling some existing holdings. Even if we thought hundreds of stocks were priced to produce attractive returns, we wouldn't increase our number of holdings. We believe that the twenty stocks in The Oakmark Select Fund will average a higher return than the fifty stocks in The Oakmark Fund, but the offset is that the portfolio will have higher risk. Our next favorite fifty stocks, the most attractive stocks we don't own, are, in our judgment, likely to average decent returns, just not quite as high as the stocks we already own. We don't believe that further diversificat ion of The Oakmark Fund—say to 100 stocks—would reduce risk by enough to justify accepting a lower expected return.

Outperforming the market with a value approach requires discipline and patience to get through the inevitable periods when other investors enjoy more rapid price appreciation than we do. That patience is needed not just by the investment adviser, but also by the shareholders. We trust that our commitment to answering your questions will help you be patient as we work to continue increasing the value of your investments.

Best wishes,

William C. Nygren, CFA

Portfolio Manager

bnygren@oakmark.com

THE OAKMARK AND OAKMARK SELECT FUNDS

7

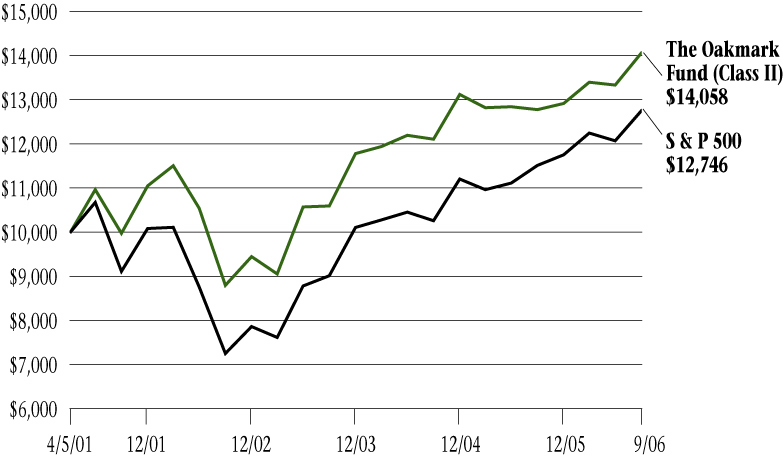

THE OAKMARK FUND

Report from Bill Nygren and Kevin Grant, Portfolio Managers

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK FUND FROM ITS INCEPTION (8/5/91) TO PRESENT (9/30/06) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX2 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 9/30/06) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(8/5/91) | |

| Oakmark Fund (Class I) | | | 5.56 | % | | | 10.46 | % | | | 7.43 | % | | | 8.51 | % | | | 15.25 | % | |

| S&P 500 | | | 5.67 | % | | | 10.79 | % | | | 6.97 | % | | | 8.59 | % | | | 10.74 | % | |

| Dow Jones Average5 | | | 5.35 | % | | | 13.14 | % | | | 8.06 | % | | | 9.21 | % | | | 11.89 | % | |

Lipper Large Cap

Value Index6 | | | 5.81 | % | | | 12.59 | % | | | 8.01 | % | | | 8.60 | % | | | 10.66 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

For the quarter ended September 30, both The Oakmark Fund and the S&P 500 increased by 6%. Though we are never fully satisfied with market-matching returns, an absolute return of 6% in a quarter is always pleasing. And unlike the S&P 500, The Oakmark Fund did again achieve a new all-time-high during the quarter, extending our new-high streak to three consecutive quarters. For the fiscal year, the story was similar. We trailed the S&P 500 by a fraction of a percentage point, but still achieved a double-digit return of just over 10%.

During the quarter nearly one-third of our stocks (17 of 52) achieved gains above 10%, and none suffered declines of that magnitude. Our best performer was Baxter International, up 24%. We added Baxter to our portfolio in the first quarter of 2003. At the time, the stock had lost more than half its value due to short-term concerns about their products and longer-term concerns about their management. Baxter's Earnings Per Share bottomed in 2003 while new management was working toward increasing sales and improving operating margins. Our earnings forecast for next year is 65% higher than that 2003 trough. Now selling at 18x projected earnings, Baxter is no longer the bargain it was in 2003, but it is still priced at a more modest premium than we believe is deserved.

During the quarter we did not add or eliminate any positions. That's the first time that's happened since we assumed management of the Fund over six years ago. The lack of activity is neither good nor bad. Turnover creates transaction costs, and those costs reduce investment returns. In that sense, it is good that we tend to have low turnover. On the other hand, no turnover also means that none of our holdings increased enough in price so that other stocks appeared to offer better return potential. We continue to believe that our current portfolio, with more large cap and higher quality businesses than we typically own, is appropriate for a market that is showing little price differentiation between low and high quality businesses.

Best wishes,

William C. Nygren, CFA

Portfolio Manager

bnygren@oakmark.com | | Kevin G. Grant, CFA

Portfolio Manager

kgrant@oakmark.com | |

|

THE OAKMARK FUND

8

THE OAKMARK FUND

Schedule of Investments—September 30, 2006

Name | |

Shares Held | |

Market Value | |

| Common Stocks—94.9% | |

| Apparel Retail—3.9% | |

| Limited Brands | | | 4,628,047 | | | $ | 122,596,965 | | |

| The Gap, Inc. | | | 5,066,700 | | | | 96,013,965 | | |

| | | | 218,610,930 | | |

| Broadcasting & Cable TV—7.3% | |

| Comcast Corporation, Special Class A (a) | | | 3,225,000 | | | $ | 118,712,250 | | |

| The DIRECTV Group, Inc. (a) | | | 5,850,000 | | | | 115,128,000 | | |

| EchoStar Communications Corporation, Class A (a) | | | 2,525,000 | | | | 82,668,500 | | |

| Liberty Media Holding Corporation - Capital, Class A (a) | | | 739,970 | | | | 61,839,293 | | |

| Discovery Holding Company, Class A (a) | | | 1,740,140 | | | | 25,162,425 | | |

| | | | 403,510,468 | | |

| Catalog Retail—1.4% | |

| Liberty Media Holding Corporation - Interactive, Class A (a) | | | 3,699,850 | | | $ | 75,402,943 | | |

| Department Stores—2.2% | |

| Kohl's Corporation (a) | | | 1,850,000 | | | $ | 120,102,000 | | |

| Home Improvement Retail—1.9% | |

| The Home Depot, Inc. | | | 2,881,500 | | | $ | 104,512,005 | | |

| Homebuilding—2.0% | |

| Pulte Homes, Inc. | | | 3,500,000 | | | $ | 111,510,000 | | |

| Household Appliances—2.0% | |

| The Black & Decker Corporation | | | 1,400,000 | | | $ | 111,090,000 | | |

| Housewares & Specialties—1.9% | |

| Fortune Brands, Inc. | | | 1,400,000 | | | $ | 105,154,000 | | |

| Leisure Products—0.7% | |

| Mattel, Inc. | | | 2,074,300 | | | $ | 40,863,710 | | |

| Motorcycle Manufacturers—2.4% | |

| Harley-Davidson, Inc. | | | 2,100,000 | | | $ | 131,775,000 | | |

| Movies & Entertainment—6.3% | |

| Time Warner, Inc. | | | 7,447,700 | | | $ | 135,771,571 | | |

| Viacom, Inc., Class B (a) | | | 2,939,745 | | | | 109,299,719 | | |

| The Walt Disney Company | | | 3,300,000 | | | | 102,003,000 | | |

| | | | 347,074,290 | | |

| Publishing—0.7% | |

| Gannett Co., Inc. | | | 684,500 | | | $ | 38,900,135 | | |

THE OAKMARK FUND

9

THE OAKMARK FUND

Schedule of Investments—September 30, 2006 cont.

Name | |

Shares Held | |

Market Value | |

| Common Stocks—94.9% (cont.) | |

| Restaurants—5.6% | |

| McDonald's Corporation | | | 4,250,000 | | | $ | 166,260,000 | | |

| Yum! Brands, Inc. | | | 2,724,000 | | | | 141,784,200 | | |

| | | | 308,044,200 | | |

| Specialized Consumer Services—2.1% | |

| H&R Block, Inc. | | | 5,358,600 | | | $ | 116,495,964 | | |

| Brewers—3.8% | |

| Anheuser-Busch Companies, Inc. | | | 2,250,000 | | | $ | 106,897,500 | | |

| InBev NV (b) | | | 1,850,000 | | | | 101,858,652 | | |

| | | | 208,756,152 | | |

| Distillers & Vintners—1.6% | |

| Diageo plc (c) | | | 1,271,000 | | | $ | 90,291,840 | | |

| Hypermarkets & Super Centers—1.9% | |

| Wal-Mart Stores, Inc. | | | 2,100,000 | | | $ | 103,572,000 | | |

| Packaged Foods & Meats—3.5% | |

| General Mills, Inc. | | | 1,756,000 | | | $ | 99,389,600 | | |

| H.J. Heinz Company | | | 2,250,000 | | | | 94,342,500 | | |

| | | | 193,732,100 | | |

| Soft Drinks—1.1% | |

| The Coca-Cola Company | | | 1,398,700 | | | $ | 62,493,916 | | |

| Integrated Oil & Gas—1.3% | |

| ConocoPhillips | | | 1,200,373 | | | $ | 71,458,205 | | |

| Asset Management & Custody Banks—1.4% | |

| The Bank of New York Company, Inc. | | | 2,150,000 | | | $ | 75,809,000 | | |

| Diversified Banks—2.1% | |

| U.S. Bancorp | | | 3,450,000 | | | $ | 114,609,000 | | |

| Life & Health Insurance—1.5% | |

| AFLAC Incorporated | | | 1,767,000 | | | $ | 80,857,919 | | |

| Other Diversified Financial Services—4.4% | |

| JPMorgan Chase & Co. | | | 2,700,000 | | | $ | 126,792,000 | | |

| Citigroup, Inc. | | | 2,400,000 | | | | 119,208,000 | | |

| | | | 246,000,000 | | |

| Thrifts & Mortgage Finance—4.4% | |

| Washington Mutual, Inc. | | | 4,037,300 | | | $ | 175,501,431 | | |

| MGIC Investment Corporation | | | 1,090,600 | | | | 65,403,282 | | |

| | | | 240,904,713 | | |

THE OAKMARK FUND

10

THE OAKMARK FUND

Schedule of Investments—September 30, 2006 cont.

Name | | Shares Held/

Par Value | |

Market Value | |

| Common Stocks—94.9% (cont.) | |

| Health Care Equipment—2.4% | |

| Baxter International, Inc. | | | 2,900,000 | | | $ | 131,834,000 | | |

| Pharmaceuticals—6.2% | |

| Abbott Laboratories | | | 2,487,300 | | | $ | 120,783,288 | | |

| Bristol-Myers Squibb Company | | | 4,500,000 | | | | 112,140,000 | | |

| Schering-Plough Corporation | | | 4,960,200 | | | | 109,570,818 | | |

| | | | 342,494,106 | | |

| Aerospace & Defense—3.5% | |

| Raytheon Company | | | 2,450,000 | | | $ | 117,624,500 | | |

| Honeywell International, Inc. | | | 1,900,000 | | | | 77,710,000 | | |

| | | | 195,334,500 | | |

| Building Products—1.7% | |

| Masco Corporation | | | 3,433,600 | | | $ | 94,149,312 | | |

| Industrial Conglomerates—1.3% | |

| Tyco International Ltd. (b) | | | 2,558,000 | | | $ | 71,598,420 | | |

| Computer Hardware—5.3% | |

| Hewlett-Packard Company | | | 2,925,000 | | | $ | 107,318,250 | | |

| Sun Microsystems, Inc. (a) | | | 19,270,000 | | | | 95,771,900 | | |

| Dell Inc. (a) | | | 4,000,000 | | | | 91,360,000 | | |

| | | | 294,450,150 | | |

| Data Processing & Outsourced Services—2.0% | |

| First Data Corporation | | | 2,575,000 | | | $ | 108,150,000 | | |

| Office Electronics—1.5% | |

| Xerox Corporation (a) | | | 5,272,400 | | | $ | 82,038,544 | | |

| Semiconductors—3.6% | |

| Intel Corp. | | | 4,900,000 | | | $ | 100,793,000 | | |

| Texas Instruments Incorporated | | | 3,000,000 | | | | 99,750,000 | | |

| | | | 200,543,000 | | |

| Total Common Stocks (Cost: $3,733,386,310) | | | | | | | 5,242,122,522 | | |

| Short Term Investments—4.9% | |

| U.S. Government Agencies—1.8% | |

| Federal Home Loan Bank, 5.14% due 10/18/2006 | | $ | 100,000,000 | | | $ | 99,757,278 | | |

| Total U.S. Government Agencies (Cost: $99,757,278) | | | | | 99,757,278 | | |

THE OAKMARK FUND

11

THE OAKMARK FUND

Schedule of Investments—September 30, 2006 cont.

Name | | Par Value | |

Market Value | |

| Short Term Investments—4.9% (cont.) | |

| Repurchase Agreement—3.1% | |

IBT Repurchase Agreement, 5.16% dated 9/29/2006

due 10/2/2006, repurchase price $172,284,634,

collateralized by Government National Mortgage

Association Bonds with rates of 6.400%, with maturity

dates from 4/20/2034 - 2/20/2035, and with an aggregate

market value plus accrued interest of $96,329,384, and by

Small Business Administration Bonds, with rates of

6.000% - 9.000%, with maturities from

4/25/2027 - 9/25/2030, and with an aggregate market

value plus accrued interest of $84,491,728 | | $ | 172,210,583 | | | $ | 172,210,583 | | |

| Total Repurchase Agreement (Cost: $172,210,583) | | | | | 172,210,583 | | |

| Total Short Term Investments (Cost: $271,967,861) | | | | | 271,967,861 | | |

| Total Investments (Cost $4,005,354,171)—99.8% | | | | $ | 5,514,090,383 | | |

| Other Assets In Excess Of Other Liabilities—0.2% | | | | | 9,568,540 | | |

| Total Net Assets—100% | | | | $ | 5,523,658,923 | | |

(a) Non-income producing security.

(b) Represents a foreign domiciled corporation.

(c) Represents an American Depository Receipt.

THE OAKMARK FUND

See accompanying Notes to Financial Statements.

12

THE OAKMARK SELECT FUND

Report from Bill Nygren and Henry Berghoef, Portfolio Managers

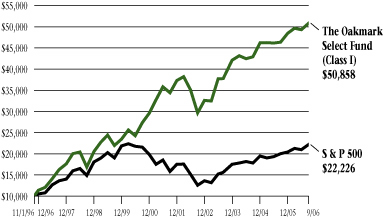

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK SELECT FUND FROM ITS INCEPTION (11/1/96) TO PRESENT (9/30/06) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX2 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 9/30/06) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | Since

Inception

(11/1/96) | |

| Oakmark Select Fund (Class I) | | | 3.02 | % | | | 9.58 | % | | | 8.07 | % | | | 17.83 | % | |

| S&P 500 | | | 5.67 | % | | | 10.79 | % | | | 6.97 | % | | | 8.39 | % | |

| S&P MidCap 4007 | | | -1.08 | % | | | 6.56 | % | | | 13.08 | % | | | 13.46 | % | |

| Lipper Mid Cap Value Index8 | | | 2.61 | % | | | 9.20 | % | | | 13.64 | % | | | 10.91 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Select Fund gained 3% for the quarter, bringing the fiscal year gain to 10%. Though good on an absolute basis, the Fund's returns fell short of the S&P 500's 6% for the quarter and 11% for the fiscal year. Despite underperforming for the quarter, we believe the month of September, when oil prices fell by more than 10%, finally demonstrated the positive relative performance we expect to see if commodity prices fall. In September, Oakmark Select gained 5% while the S&P gained only 3%. We continue to believe that most of the attractive stocks today are in businesses that are less economically sensitive and would benefit from declining prices for energy and other basic materials.

During the quarter, the strongest contributor to our positive performance was McDonald's. In addition to achieving good results at its restaurants, McDonald's announced a creative approach for spinning-off their ownership in Chipotle. Chipotle is a restaurant chain that is a small, marginally profitable, but rapidly growing business—characteristics that often appeal to different investors than those who own McDonald's. By requiring shareholders to exchange their McDonald's shares to obtain Chipotle shares, McDonald's is effectively using its Chipotle ownership to fund a share repurchase. Good things happen to per-share-value when earnings are increasing while shares outstanding are decreasing! We much prefer investing with managements who evaluate their success using per-share metrics, thinking like shareholders, than with those who use corporate metrics, thinking like professional managers.

For the fiscal year, the Fund's largest holding, Washington Mutual, was also the largest contributor to our return. Increasing 15%, Washington Mutual was not our best performer (another bank, JP Morgan was), but because of our large weighting, its performance helped the Fund the most. We continue to believe that retail banking has good growth prospects, and with both Washington Mutual and JP Morgan selling at below average P/E9 multiples, we believe they will continue to be good long-term performers.

Best wishes,

William C. Nygren, CFA

Portfolio Manager

bnygren@oakmark.com | | Henry R. Berghoef, CFA

Portfolio Manager

berghoef@oakmark.com | |

|

THE OAKMARK SELECT FUND

13

THE OAKMARK SELECT FUND

Schedule of Investments—September 30, 2006

Name | |

Shares Held | |

Market Value | |

| Common Stocks—95.6% | |

| Apparel Retail—7.0% | |

| Limited Brands | | | 9,280,981 | | | $ | 245,853,187 | | |

| The Gap, Inc. | | | 8,560,000 | | | | 162,212,000 | | |

| | | | 408,065,187 | | |

| Broadcasting & Cable TV—2.7% | |

| Discovery Holding Company, Class A (a) | | | 10,809,500 | | | $ | 156,305,370 | | |

| Catalog Retail—4.6% | |

| Liberty Media Holding Corporation - Interactive, Class A (a) | | | 13,050,000 | | | $ | 265,959,000 | | |

| Homebuilding—2.8% | |

| Pulte Homes, Inc. | | | 5,224,200 | | | $ | 166,443,012 | | |

| Leisure Products—2.4% | |

| Mattel, Inc. | | | 7,070,900 | | | $ | 139,296,730 | | |

| Movies & Entertainment—8.6% | |

| Time Warner, Inc. | | | 15,340,000 | | | $ | 279,648,200 | | |

| Viacom, Inc., Class B (a) | | | 5,975,000 | | | | 222,150,500 | | |

| | | | 501,798,700 | | |

| Restaurants—13.1% | |

| Yum! Brands, Inc. | | | 8,557,000 | | | $ | 445,391,850 | | |

| McDonald's Corporation | | | 8,200,000 | | | | 320,784,000 | | |

| | | | 766,175,850 | | |

| Specialized Consumer Services—5.7% | |

| H&R Block, Inc. (b) | | | 15,419,600 | | | $ | 335,222,104 | | |

| Other Diversified Financial Services—4.4% | |

| JPMorgan Chase & Co. | | | 5,500,000 | | | $ | 258,280,000 | | |

| Thrifts & Mortgage Finance—15.0% | |

| Washington Mutual, Inc. | | | 20,167,400 | | | $ | 876,676,878 | | |

| Health Care Technology—3.8% | |

| IMS Health Incorporated | | | 8,303,441 | | | $ | 221,203,668 | | |

| Pharmaceuticals—3.6% | |

| Bristol-Myers Squibb Company | | | 8,490,200 | | | $ | 211,575,784 | | |

| Diversified Commercial and Professional Services—4.2% | |

| The Dun & Bradstreet Corporation (a)(b) | | | 3,284,900 | | | $ | 246,334,651 | | |

| Computer Hardware—3.5% | |

| Dell Inc. (a) | | | 9,000,000 | | | $ | 205,560,000 | | |

| Data Processing & Outsourced Services—5.4% | |

| First Data Corporation (c) | | | 7,015,400 | | | $ | 294,646,800 | | |

| Western Union Company, When Issued (a)(d) | | | 1,100,000 | | | | 21,043,000 | | |

| | | | 315,689,800 | | |

| Office Electronics—4.4% | |

| Xerox Corporation (a) | | | 16,446,400 | | | $ | 255,905,984 | | |

THE OAKMARK SELECT FUND

14

THE OAKMARK SELECT FUND

Schedule of Investments—September 30, 2006 cont.

Name | | Shares Held/

Par Value | |

Market Value | |

| Common Stocks—95.6% (cont.) | |

| Semiconductors—4.4% | |

| Intel Corp. | | | 12,500,000 | | | $ | 257,125,000 | | |

| Total Common Stocks (Cost: $3,912,760,962) | | | | | | | 5,587,617,718 | | |

| Short Term Investments—4.9% | |

| U.S. Government Agencies—2.1% | |

| Fannie Mae, 5.08% due 10/26/2006 | | $ | 25,000,000 | | | $ | 24,911,806 | | |

| Federal Home Loan Bank, 5.14% due 10/18/2006 | | | 100,000,000 | | | | 99,757,278 | | |

| Total U.S. Government Agencies (Cost: $124,669,084) | | | | | | | 124,669,084 | | |

| Repurchase Agreement—2.8% | |

IBT Repurchase Agreement, 5.16% dated 9/29/2006

due 10/2/2006, repurchase price $162,245,766,

collateralized by Government National Mortgage

Association Bonds with a rate of 6.400%, with

maturities from 5/20/2034 - 10/20/2034, and with an

aggregate market value plus accrued interest of

$52,934,905, and by Small Business Administration

Bonds, with rates of 7.650% - 8.500%, with maturities

from 3/25/2023 - 9/25/2030, and with an aggregate

market value plus accrued interest of $117,349,926 | | $ | 162,176,030 | | | $ | 162,176,030 | | |

| Total Repurchase Agreement (Cost: $162,176,030) | | | | | | | 162,176,030 | | |

| Total Short Term Investments (Cost: $286,845,114) | | | | | | | 286,845,114 | | |

| Total Investments (Cost $4,199,606,076)—100.5% | | | | | | $ | 5,874,462,832 | | |

| Common Stocks Sold Short—(0.4%) | |

| Data Processing & Outsourced Services—(0.4%) | |

| First Data Corporation, When Issued (e) | | | (950,000 | ) | | $ | (21,840,500 | ) | |

Total Common Stocks Sold Short

(Proceeds Received: $(21,737,301)) | | | | | | | (21,840,500 | ) | |

| Other Liabilities In Excess Of Other Assets—(0.1%) | | | | | | | (7,928,046 | ) | |

| Total Net Assets—100% | | | | | | $ | 5,844,694,286 | | |

(a) Non-income producing security.

(b) See footnote number five in the Notes to Financial Statements regarding investments in affiliated issuers.

(c) A portion of this security is designated as collateral in connection with common stocks sold short.

(d) Security purchased on a when issued or delayed delivery basis.

(e) Security sold on a when issued or delayed delivery basis.

See accompanying Notes to Financial Statements.

THE OAKMARK SELECT FUND

15

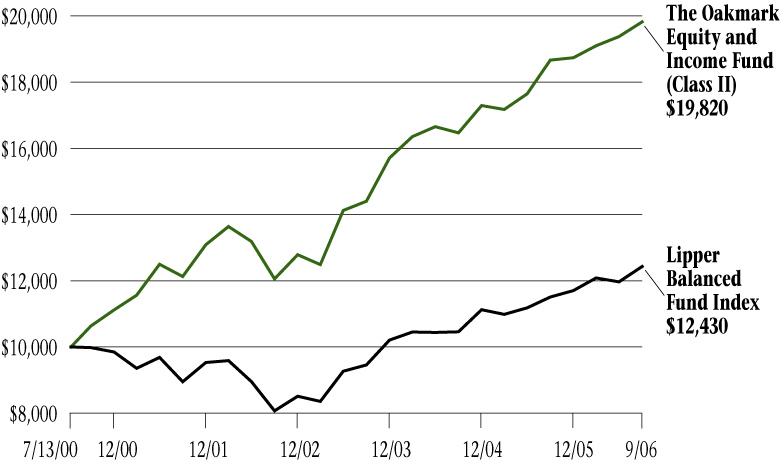

THE OAKMARK EQUITY AND INCOME FUND

Report from Clyde S. McGregor and Edward A. Studzinski, Portfolio Managers

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK EQUITY AND INCOME FUND FROM ITS INCEPTION (11/1/95) TO PRESENT (9/30/06) AS COMPARED TO THE LIPPER BALANCED FUND INDEX10 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 9/30/06) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/95) | |

Oakmark Equity &

Income Fund (Class I) | | | 2.36 | % | | | 6.51 | % | | | 10.59 | % | | | 13.46 | % | | | 13.36 | % | |

Lipper Balanced

Fund Index | | | 3.87 | % | | | 8.02 | % | | | 6.79 | % | | | 7.49 | % | | | 7.92 | % | |

| S&P 5002 | | | 5.67 | % | | | 10.79 | % | | | 6.97 | % | | | 8.59 | % | | | 9.67 | % | |

Lehman Govt./

Corp. Bond11 | | | 3.91 | % | | | 3.33 | % | | | 4.96 | % | | | 6.47 | % | | | 6.17 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter and Fiscal Year Review

The Equity and Income Fund earned 2% in the quarter ended September 30. This is a solid return, but it nevertheless lags behind the 4% result of the Lipper Balanced Fund Index. The comparison for the fiscal year ended September 30 is 7% for the Fund and 8% for the Lipper Balanced Fund Index. As always, we are pleased to report a positive rate of return for the Fund, even when the comparison with Lipper is uninspiring. It especially pleases us that in the recent quarter the fixed income segment of the portfolio contributed meaningfully. When the quarter began, the Fund's duration (a measure of sensitivity to changes in interest rates) was a very low 1.8 years, meaning that we had positioned that portfolio segment defensively. During the quarter the Federal Reserve broke its string of 17 consecutive hikes in short-term interest rates. Believing that the risk in longer term fixed income securities had diminished, we increased the portfolio's du ration to 3.2 years by quarter's end. The extension of maturity produced a significantly favorable effect on the Fund's return in the quarter.

Many of our investors wrote to us earlier in the year expressing concern about the fixed income outlook and the Fund's bond holdings. These correspondents argued that continued upward pressure on short-term rates would inevitably result in deterioration in bond prices. As we noted two letters ago, during the time that the Fed increased short-term rates 17 times, long-term bond prices stayed remarkably stable. Now that the Federal Reserve has either paused or perhaps completed its cycle of increasing rates, longer term bonds have rallied vigorously. Markets often move in a fashion designed to frustrate the maximum amount of investors, and this appears to have happened in the bond market.

Earnings Season

In late July, the writer of this letter was awaiting the arrival of his commuter train when an investing professional from a competitor asked, "How is your earnings season going?" Your letter writer stumbled to construct a response, attempting to hide the fact that he did not know that our industry now designates the period in a quarter when the majority of companies report earnings as "earnings season." As most of our regular readers know (and those who don't can infer from our pictures), your Fund managers have labored long enough in the investment management industry to observe our industry pursue many fads. In the early 1980s, for example, the weekly money supply figures were the data du jour, and many professionals made good livings simply forecasting these numbers. The current obsession with quarterly earnings announcements and mid-quarter "earnings guidance" strikes us as a similar fad,

THE OAKMARK EQUITY AND INCOME FUND

16

because quarterly earnings reports rarely contain information that changes a business's intrinsic value.

This fad may be losing momentum, however. In July the Business Roundtable Institute for Corporate Ethics and the CFA Institute issued a joint report calling for business leaders to stop issuing quarterly earnings guidance. [The National Investor Relations Institute estimates that just over half of U.S. public companies provide earnings guidance each quarter.] The report argues that regular three-month forecasts distract management from concentrating on their businesses' long-term health. We agree and often share this opinion with the management teams that we meet. We should note, though, that the stock market's focus on short-term earnings benefits our investing style by generating stock price volatility unconnected to long-term fundamental value.

Shortly after the Business Roundtable issued its report, New York Times columnist Joe Nocera wrote a piece titled "A Defense of Short-Termism."12 He argued that before the investment community forced corporate management teams to focus on quarterly results, managers often avoided making tough decisions and could appear lethargic. He points out that "Having sailed through the post-war era without much in the way of global competition, there were plenty of American industries that desperately needed to be shaken up in a tougher, more competitive era." It may be that Mr. Nocera is correct, that the obsession with short-term earnings has been necessary for reinvigorating the U.S. economy. But we believe that this phase has persisted too long. In any event, you may rest assured that your managers will continue to ignore the noise of the moment and focus on understanding long-term business value.

Passage of Time

Notwithstanding the previous section of this report, we do charge our security analysts with the task of developing annual earnings forecasts for the companies that they cover. Every August we require them to extend their estimates another year into the future. While the analysts may grumble about the difficulty of forecasting so far out, the point is simply to keep their focus very long term.

As the analysts review their earnings projections, they often increase their estimates for intrinsic value because of the "passage of time." This brings to mind an experience we had with a client many years ago who sold his business for cash and hired us to manage some of the proceeds. All too soon he terminated his account. When asked why, he explained his reasons. Before the sale of his business, he had never owned a stock nor paid any attention to the stock market. Once he began to pay attention, however, the daily volatility of stock prices shocked him. He remarked that when he owned his business, he knew that every evening when he left the office the business was worth more than when the day began. The daily price movements in the stock market were not just disconnected from economic reality (as he saw it), they were completely irrational!

As value investors, we simply try to answer two questions about an investment: "What is it worth?" and "What is its current price?" If our former client's understanding of the world—where every security properly reflected its intrinsic value—prevailed, we would have to change careers! As it is, however, the securities markets provide us with enough irrational pricing to continue to employ our value investing approach. Here's to irrationality in the stock market!

As always, we thank you for entrusting us with your assets.

Clyde S. McGregor, CFA

Portfolio Manager

mcgregor@oakmark.com | | Edward A. Studzinski, CFA

Portfolio Manager

estudzinski@oakmark.com | |

|

THE OAKMARK EQUITY AND INCOME FUND

17

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—September 30, 2006

Name | |

Shares Held | |

Market Value | |

| Equity and Equivalents—54.3% | |

| Common Stocks—54.3% | |

| Apparel Retail—1.8% | |

| The TJX Companies, Inc. | | | 7,240,000 | | | $ | 202,937,200 | | |

| Broadcasting & Cable TV—4.7% | |

| EchoStar Communications Corporation, Class A (a) | | | 8,250,000 | | | $ | 270,105,000 | | |

| The E.W. Scripps Company, Class A | | | 4,750,000 | | | | 227,667,500 | | |

| CBS Corporation, Class A | | | 910,000 | | | | 25,680,200 | | |

| | | | 523,452,700 | | |

| Movies & Entertainment—1.8% | |

| News Corporation, Class B | | | 9,735,100 | | | $ | 200,932,464 | | |

| Publishing—1.9% | |

| The Washington Post Company, Class B | | | 280,000 | | | $ | 206,360,000 | | |

| PRIMEDIA Inc. (a) | | | 3,500,000 | | | | 5,320,000 | | |

| | | | 211,680,000 | | |

| Restaurants—1.1% | |

| McDonald's Corporation | | | 3,000,000 | | | $ | 117,360,000 | | |

| Specialty Stores—0.2% | |

| Zale Corporation (a) | | | 940,000 | | | $ | 26,075,600 | | |

| Brewers—1.0% | |

| InBev NV (b) | | | 2,100,000 | | | $ | 115,623,335 | | |

| Distillers & Vintners—2.6% | |

| Diageo plc (c) | | | 4,100,000 | | | $ | 291,264,000 | | |

| Hypermarkets & Super Centers—0.9% | |

| Costco Wholesale Corporation | | | 2,100,000 | | | $ | 104,328,000 | | |

| Packaged Foods & Meats—3.8% | |

| Nestle SA (c)(d) | | | 3,900,000 | | | $ | 339,959,100 | | |

| Smithfield Foods, Inc. (a) | | | 2,985,000 | | | | 80,654,700 | | |

| | | | 420,613,800 | | |

| Personal Products—1.6% | |

| Avon Products, Inc. | | | 5,719,000 | | | $ | 175,344,540 | | |

| Tobacco—1.7% | |

| UST, Inc. | | | 3,500,000 | | | $ | 191,905,000 | | |

| Integrated Oil & Gas—2.4% | |

| ConocoPhillips | | | 4,500,000 | | | $ | 267,885,000 | | |

THE OAKMARK EQUITY AND INCOME FUND

18

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—September 30, 2006 cont.

Name | |

Shares Held | |

Market Value | |

| Equity and Equivalents—54.3% (cont.) | |

| Oil & Gas Exploration & Production—7.7% | |

| XTO Energy, Inc. | | | 10,561,338 | | | $ | 444,949,170 | | |

| EnCana Corp (b) | | | 6,500,000 | | | | 303,485,000 | | |

| St. Mary Land & Exploration Company (e) | | | 2,900,000 | | | | 106,459,000 | | |

| | | | 854,893,170 | | |

| Property & Casualty Insurance—5.4% | |

| SAFECO Corporation | | | 4,610,000 | | | $ | 271,667,300 | | |

| MBIA Inc. | | | 2,918,300 | | | | 179,300,352 | | |

| The Progressive Corporation | | | 6,239,500 | | | | 153,117,330 | | |

| | | | 604,084,982 | | |

| Reinsurance—0.5% | |

| PartnerRe, Ltd. (b) | | | 800,000 | | | $ | 54,056,000 | | |

| Biotechnology—1.7% | |

| MedImmune, Inc. (a) | | | 6,500,800 | | | $ | 189,888,368 | | |

| Health Care Equipment—0.7% | |

| Hospira, Inc. (a) | | | 1,350,000 | | | $ | 51,664,500 | | |

| Medtronic, Inc. | | | 500,000 | | | | 23,220,000 | | |

| | | | 74,884,500 | | |

| Health Care Services—2.3% | |

| Caremark Rx, Inc. | | | 4,500,000 | | | $ | 255,015,000 | | |

| Life Science Tools & Services—0.7% | |

| Varian, Inc. (a)(e) | | | 1,649,400 | | | $ | 75,657,978 | | |

| Aerospace & Defense—6.3% | |

| General Dynamics Corporation | | | 4,700,000 | | | $ | 336,849,000 | | |

| Raytheon Company | | | 3,599,700 | | | | 172,821,597 | | |

| Alliant Techsystems, Inc. (a) | | | 1,325,000 | | | | 107,404,500 | | |

| Honeywell International, Inc. | | | 1,889,500 | | | | 77,280,550 | | |

| Rockwell Collins, Inc. | | | 150,000 | | | | 8,226,000 | | |

| | | | 702,581,647 | | |

| Industrial Conglomerates—0.8% | |

| Walter Industries, Inc. | | | 2,075,000 | | | $ | 88,561,000 | | |

| Industrial Machinery—0.2% | |

| Mueller Water Products, Inc (a) | | | 1,700,000 | | | $ | 24,837,000 | | |

| Application Software—0.4% | |

| Mentor Graphics Corporation (a) | | | 3,288,318 | | | $ | 46,299,518 | | |

| Data Processing & Outsourced Services—1.0% | |

| Ceridian Corporation (a) | | | 4,800,000 | | | $ | 107,328,000 | | |

THE OAKMARK EQUITY AND INCOME FUND

19

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—September 30, 2006 cont.

Name | | Shares Held/

Par Value | |

Market Value | |

| Equity and Equivalents—54.3% (cont.) | |

| Semiconductors—0.3% | |

| International Rectifier Corporation (a) | | | 1,089,700 | | | $ | 37,965,148 | | |

| Technology Distributors—0.7% | |

| CDW Corporation | | | 1,200,000 | | | $ | 74,016,000 | | |

| Paper Products—0.1% | |

| Schweitzer-Mauduit International, Inc. | | | 350,000 | | | $ | 6,643,000 | | |

| Total Common Stocks (Cost: $4,470,336,150) | | | | | | | 6,046,112,950 | | |

| Total Equity and Equivalents (Cost: $4,470,336,150) | | | | | | | 6,046,112,950 | | |

| Fixed Income—41.9% | |

| Corporate Bonds—0.2% | |

| Paper Packaging—0.2% | |

| Sealed Air Corporation, 144A, 5.625% due 7/15/2013 (f) | | $ | 20,000,000 | | | $ | 19,679,180 | | |

| Total Corporate Bonds (Cost: $20,173,684) | | | | | | | 19,679,180 | | |

| Government and Agency Securities—41.7% | |

| Canadian Government Bonds—10.0% | |

| Canada Government, 4.25% due 12/1/2008 | | CAD | 250,000,000 | | | $ | 225,229,255 | | |

| Canada Government, 4.00% due 9/1/2010 | | CAD | 250,000,000 | | | | 224,553,791 | | |

| Canada Government, 3.25% due 12/1/2006 | | CAD | 250,000,000 | | | | 223,316,931 | | |

| Canada Government, 3.00% due 6/1/2007 | | CAD | 250,000,000 | | | | 222,075,598 | | |

| Canada Government, 2.75% due 12/1/2007 | | CAD | 250,000,000 | | | | 220,509,953 | | |

| | | | 1,115,685,528 | | |

| France Government Bonds—0.4% | |

France Government, 3.00%

due 7/25/2012, Inflation Indexed | | EUR | 33,028,200 | | | $ | 45,213,913 | | |

| U.S. Government Notes—31.3% | |

| United States Treasury Notes, 4.875% due 2/15/2012 (g) | | | 500,000,000 | | | $ | 506,972,500 | | |

| United States Treasury Notes, 5.125% due 6/30/2008 | | | 500,000,000 | | | | 503,203,000 | | |

| United States Treasury Notes, 4.875% due 5/15/2009 | | | 500,000,000 | | | | 502,890,500 | | |

| United States Treasury Notes, 4.875% due 8/15/2016 | | | 375,000,000 | | | | 382,089,750 | | |

United States Treasury Notes, 3.375% due 1/15/2007,

Inflation Indexed | | | 273,530,340 | | | | 271,158,285 | | |

| United States Treasury Notes, 5.125% due 6/30/2011 | | | 250,000,000 | | | | 255,517,500 | | |

| United States Treasury Notes, 4.875% due 5/31/2011 | | | 250,000,000 | | | | 252,871,000 | | |

| United States Treasury Notes, 4.75% due 3/31/2011 | | | 250,000,000 | | | | 251,533,250 | | |

| United States Treasury Notes, 4.875% due 5/31/2008 | | | 250,000,000 | | | | 250,468,750 | | |

THE OAKMARK EQUITY AND INCOME FUND

20

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—September 30, 2006 cont.

Name | | Par Value | |

Market Value | |

| Fixed Income—41.9% (cont.) | |

| U.S. Government Notes—31.3% (cont.) | |

| United States Treasury Notes, 4.50% due 2/15/2016 | | $ | 250,000,000 | | | $ | 247,490,250 | | |

United States Treasury Notes, 3.625% due 1/15/2008,

Inflation Indexed | | | 62,969,500 | | | | 63,473,760 | | |

| | | | 3,487,668,545 | | |

| Total Government and Agency Securities (Cost: $4,560,095,037) | | | | | | | 4,648,567,986 | | |

| Total Fixed Income (Cost: $4,580,268,721) | | | | | | | 4,668,247,166 | | |

| Short Term Investments—3.0% | |

| Repurchase Agreement—3.0% | |

IBT Repurchase Agreement, 5.16% dated 9/29/2006

due 10/2/2006, repurchase price $334,312,156,

collateralized by Government National Mortgage

Association Bonds with rates of 5.250% - 6.400%,

with maturities from 8/20/2032 - 4/20/2035, and

with an aggregate market value plus accrued

interest of $69,050,520, and by Small Business

Administration Bonds, with rates of 7.000% - 10.500%,

with maturities from 10/25/2016 - 8/25/2030, and

with an aggregate market value plus accrued

interest of $281,826,368 | | $ | 334,168,464 | | | $ | 334,168,464 | | |

| Total Repurchase Agreement (Cost: $334,168,464) | | | | | | | 334,168,464 | | |

| Total Short Term Investments (Cost: $334,168,464) | | | | | | | 334,168,464 | | |

| Total Investments (Cost $9,384,773,335)—99.2% | | | | | | $ | 11,048,528,580 | | |

| Other Assets In Excess Of Other Liabilities—0.8% | | | | | | | 84,088,324 | | |

| Total Net Assets—100% | | | | | | $ | 11,132,616,904 | | |

(a) Non-income producing security.

(b) Represents a foreign domiciled corporation.

(c) Represents an American Depository Receipt.

(d) Market value is determined in accordance with procedures established in good faith by the Board of Trustees.

(e) See footnote number five in the Notes to Financial Statements regarding investments in affiliated issuers.

(f) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

(g) A portion of security out on loan.

Key to abbreviations:

CAD: Canadian Dollar

EUR: Euro Dollar

See accompanying Notes to Financial Statements.

THE OAKMARK EQUITY AND INCOME FUND

21

THE OAKMARK GLOBAL FUND

Report from Clyde S. McGregor and Robert A. Taylor, Portfolio Managers

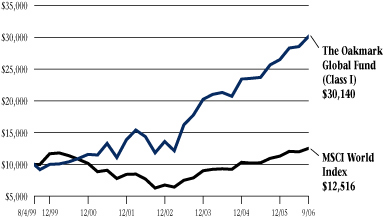

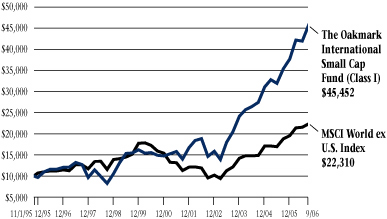

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK GLOBAL FUND FROM ITS INCEPTION (8/4/99) TO PRESENT (9/30/06) AS COMPARED TO THE MSCI WORLD INDEX13 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 9/30/06) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | Since

Inception

(8/4/99) | |

| Oakmark Global Fund (Class I) | | | 5.58 | % | | | 17.46 | % | | | 22.18 | % | | | 16.67 | % | |

| MSCI World | | | 4.47 | % | | | 14.18 | % | | | 10.01 | % | | | 3.19 | % | |

| Lipper Global Fund Index14 | | | 4.06 | % | | | 14.36 | % | | | 10.63 | % | | | 5.17 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter and Fiscal Year Review

A strong recovery in world stock markets helped to propel The Oakmark Global Fund to a pleasing 6% gain in the quarter ended September 30. Both the Lipper Global Fund Index and the MSCI World Index reported 4% for the period. September 30 also is the end of the Fund's fiscal year. For that 12-month period the Fund earned 17%, which contrasts to 14% for the Lipper Global Fund Index as well as the MSCI World Index. Most importantly, the Fund since inception has compounded at approximately 17% per year, measured against 3% per year for the MSCI World Index and 5% for the Lipper Global Fund Index.

While several stocks in the Fund lost ground during the quarter, every country in which we invested Fund assets contributed positively. The Netherlands, Italy, and Mexico provided the highest percentage total return. We ended the quarter with the portfolio divided roughly 40/60 between U.S. stocks and foreign-domiciled issues. As we have often stated, we build the portfolio from the bottom up. Each individual name fights for space within the portfolio. The resulting split between the U.S. and international simply captures a snapshot view of where we have identified dominant investment ideas. Consultants may tell us that we are "underweight" a country or an industry, but this has little meaning for our investment process. We go wherever we believe value to be taking us, and currently that means a lot of Europe and the U.S., some Asia, and a small position in the emerging markets.

Japan—The New Frontier

The changes that have taken place in Japan over the past decade have been dramatic. Deflation has ended, interest rates are on the rise, capital spending is booming, the banks are back from the brink, and the real estate market is experiencing a renaissance. Also, very importantly, management teams are starting to care about shareholders. Meeting a CEO or CFO is becoming common compared to dealing only with the investor relations department in the past. Companies are truly restructuring, and share repurchases are more than just an announcement. Average returns, measured by return on equity, have jumped from low single-digit levels to almost 10% today. The recent apex was the bid by OJI Paper for Hokuetsu Paper, which marked the first time a blue-chip Japanese company attempted a hostile takeover of a competitor. While the attempt was unsuccessful, it illustrates how things have changed from the keiretsu-dominated business relationships in Ja pan.

It is interesting to note that despite these positives, Japan has been one of the worst performing

THE OAKMARK GLOBAL FUND

22

equity markets for the year. We see this as an opportunity. Close to 12% of the Fund is invested in Japan because of changes mentioned above, the owner-oriented management teams of our holdings, and our holdings' respective discounts to fair value. The management teams at Rohm, Takeda, Meitec and Uni-Charm share our belief in this discount to intrinsic value and are executing meaningful share repurchases. We are pleased that our Japanese holdings have been some of the biggest contributors for the Fund quarter and year-to-date. Even after these price moves we remain excited about our Japanese holdings.

Portfolio Changes

We kept the number of stocks in the portfolio constant during the quarter, adding two new names and eliminating another two. As noted above, every holding in the portfolio fights for space, and ConocoPhillips (received in exchange for the Fund's Burlington Resources shares) and Santen Pharmaceutical lost that fight. Both, however, are solid companies that could easily return to the portfolio in the future.

Our two new purchases are Intel and Kinetic Concepts, both U.S.-domiciled concerns. Intel, the world's largest microprocessor company, typifies the opportunity to buy a great company at a good price, which we always desire but rarely see. In the summer, market share losses to a major competitor combined with poor personal computer industry conditions to push Intel's stock price down to 1997 levels. Intel's market share position has experienced many cycles, and we believe that the current share loss will prove to be temporary. The company introduced several important new products in the third quarter, and more are on the way. Not only does Intel spend more than four times as much on research and development than its nearest competitor, but also the company sets the standard, in our opinion, for state of the art manufacturing in its industry.

In contrast to the very well known Intel, Kinetic Concepts is a somewhat obscure mid-size company that develops and manufactures health care products. The company has long been known for its specialty hospital beds, but wound care products now dominate corporate revenues. Kinetic Concepts controls a patented technology named Vacuum Assisted Closure that speeds healing for difficult wounds. Demographics are favorable for this product because two rapidly growing populations (diabetics and nursing home residents) are primary customers. Usually, specialty medical device companies trade at prices that we find too expensive, and this is usually the case for Kinetic Concepts. However, when a patent infringement trial produced an unexpected outcome, Kinetic Concepts' share price decreased, and we saw an investment opportunity. As with Intel, we believe that the stock market has overreacted to ambiguous news.

In closing, we note that the Fund passed its seventh anniversary during the quarter. While the Fund has grown in size over the years, it has not changed in its character. We thank you for your support and patience, and we welcome your e-mailed questions and comments.

Clyde S. McGregor, CFA

Portfolio Manager

mcgregor@oakmark.com | | Robert A. Taylor, CFA

Portfolio Manager

rtaylor@oakmark.com | |

|

THE OAKMARK GLOBAL FUND

23

THE OAKMARK GLOBAL FUND

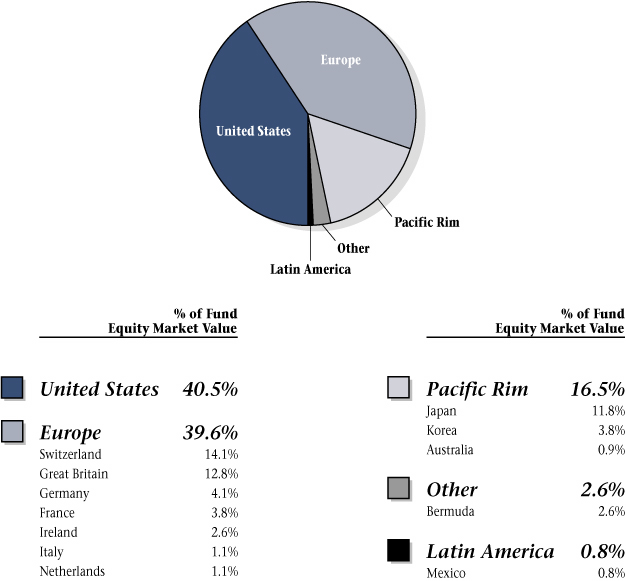

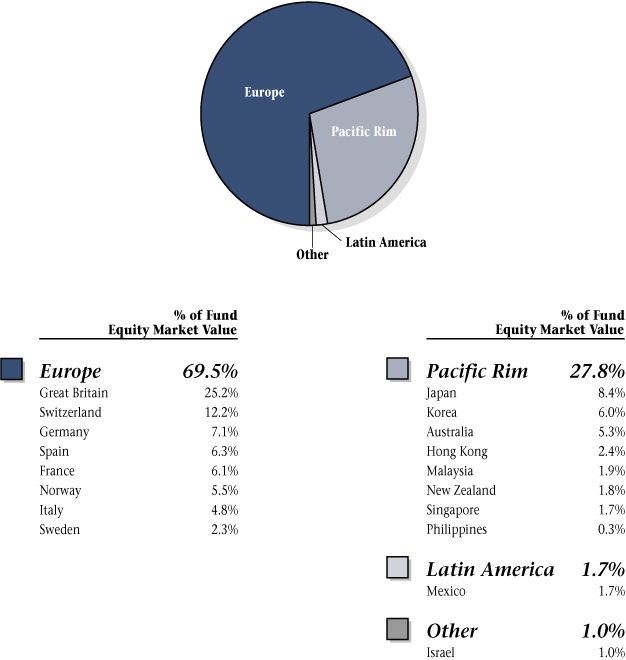

Global Diversification—September 30, 2006 (Unaudited)

THE OAKMARK GLOBAL FUND

24

THE OAKMARK GLOBAL FUND

Schedule of Investments—September 30, 2006

| Name | | Description | | Shares Held | | Market Value | |

| Common Stocks—97.9% | |

| Apparel Retail—2.0% | |

The TJX Companies, Inc.

(United States) | | Discount Apparel & Home

Fashion Retailer | | | 1,689,000 | | | $ | 47,342,670 | | |

| Apparel, Accessories & Luxury Goods—1.1% | |

| Bulgari S.p.A. (Italy) | | Jewelry Manufacturer & Retailer | | | 1,946,000 | | | $ | 24,774,958 | | |

| Automobile Manufacturers—3.2% | |

Bayerische Motoren

Werke (BMW) AG

(Germany) | | Luxury Automobile Manufacturer | | | 1,424,000 | | | $ | 76,272,903 | | |

| Broadcasting & Cable TV—3.7% | |

CBS Corporation, Class B

(United States) | | Radio & Television Broadcasting | | | 1,585,000 | | | $ | 44,649,450 | | |

Discovery Holding

Company, Class A

(United States) (a) | | Media Management &

Network Services | | | 2,913,700 | | | | 42,132,102 | | |

| | | | 86,781,552 | | |

| Household Appliances—3.3% | |

Snap-on Incorporated

(United States) | | Tool & Equipment Manufacturer | | | 1,760,000 | | | $ | 78,408,000 | | |

| Leisure Products—1.2% | |

Brunswick Corp.

(United States) | | Leisure & Recreation

Products Manufacturer | | | 877,000 | | | $ | 27,353,630 | | |

| Motorcycle Manufacturers—3.0% | |

Harley-Davidson, Inc.

(United States) | | Motorcycle Manufacturer | | | 1,126,000 | | | $ | 70,656,500 | | |

| Movies & Entertainment—6.2% | |

Time Warner, Inc.

(United States) | | | | | 2,117,000 | | | $ | 38,592,910 | | |

Vivendi Universal SA

(France) | | Music, Games, Television, Film, &

Telecommunications | | | 1,051,500 | | | | 37,907,271 | | |

News Corporation,

Class B (United States) | | International Multimedia &

Entertainment Company | | | 1,726,500 | | | | 35,634,960 | | |

Viacom, Inc., Class B

(United States) (a) | | | | | 944,000 | | | | 35,097,920 | | |

| | | | 147,233,061 | | |

THE OAKMARK GLOBAL FUND

25

THE OAKMARK GLOBAL FUND

Schedule of Investments—September 30, 2006 cont.

| Name | | Description | | Shares Held | | Market Value | |

| Common Stocks—97.9% (cont.) | |

| Publishing—3.4% | |

The Washington Post

Company, Class B

(United States) | | Newspaper & Magazine Publishing | | | 61,418 | | | $ | 45,265,066 | | |

Trinity Mirror plc

(Great Britain) | | Newspaper Publishing | | | 4,078,900 | | | | 36,352,731 | | |

| | | | 81,617,797 | | |

| Distillers & Vintners—2.9% | |

| Diageo plc (Great Britain) | | Beverages, Wines, &

Spirits Manufacturer | | | 3,902,500 | | | $ | 68,940,091 | | |

| Household Products—2.5% | |

Uni-Charm Corporation

(Japan) | | Toiletry Products Manufacturer | | | 397,400 | | | $ | 22,069,367 | | |

| Henkel KGaA (Germany) | | Consumer Chemical

Products Manufacturer | | | 154,000 | | | | 19,057,346 | | |

Kimberly-Clark de

Mexico S.A. de C.V

(Mexico) | | Hygiene Products Manufacturer,

Marketer & Distributor | | | 4,391,000 | | | | 17,669,442 | | |

| | | | 58,796,155 | | |

| Packaged Foods & Meats—4.2% | |

| Nestle SA (Switzerland) | | Food & Beverage Manufacturer | | | 175,500 | | | $ | 61,192,371 | | |

Cadbury Schweppes plc

(Great Britain) | | Beverage & Confectionary

Manufacturer | | | 3,493,000 | | | | 37,180,574 | | |

| | | | 98,372,945 | | |

| Soft Drinks—1.0% | |

Lotte Chilsung

Beverage Co., Ltd.

(Korea) | | Soft Drinks, Juices & Sports

Drinks Manufacturer | | | 16,680 | | | $ | 22,616,053 | | |

| Oil & Gas Exploration & Production—2.7% | |

XTO Energy, Inc.

(United States) | | Oil & Natural Gas Exploration &

Production | | | 1,509,000 | | | $ | 63,574,170 | | |

| Asset Management & Custody Banks—3.1% | |

Julius Baer Holding AG-B

(Switzerland) | | Asset Management | | | 729,300 | | | $ | 72,845,432 | | |

| Diversified Banks—3.4% | |

| Bank of Ireland (Ireland) | | Commercial Bank | | | 3,032,000 | | | $ | 59,285,700 | | |

Australia and New Zealand

Banking Group Limited

(Australia) | | Commercial Bank | | | 1,095,000 | | | | 21,920,540 | | |

| | | | 81,206,240 | | |

THE OAKMARK GLOBAL FUND

26

THE OAKMARK GLOBAL FUND

Schedule of Investments—September 30, 2006 cont.

| Name | | Description | | Shares Held | | Market Value | |

| Common Stocks—97.9% (cont.) | |

| Diversified Capital Markets—3.0% | |

Credit Suisse Group

(Switzerland) | | Investment Services & Insurance | | | 1,228,400 | | | $ | 71,074,205 | | |

| Investment Banking & Brokerage—1.3% | |

Daiwa Securities Group,

Inc. (Japan) | | Stock Broker | | | 2,558,000 | | | $ | 29,840,626 | | |

| Health Care Equipment—1.5% | |

Kinetic Concepts, Inc.

(United States) (a) | | Health Care Equipment & Supplies | | | 1,115,100 | | | $ | 35,081,046 | | |

| Health Care Services—2.6% | |

Laboratory Corporation of

America Holdings

(United States) (a) | | Medical Laboratory & Testing

Services | | | 920,000 | | | $ | 60,324,400 | | |

| Pharmaceuticals—6.7% | |

GlaxoSmithKline plc

(Great Britain) | | Pharmaceuticals | | | 3,055,000 | | | $ | 81,338,816 | | |

| Novartis AG (Switzerland) | | Pharmaceuticals | | | 899,600 | | | | 52,517,734 | | |

Takeda Pharmaceutical