UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06241

Loomis Sayles Funds II

(Exact name of Registrant as specified in charter)

888 Boylston Street, Suite 800 Boston, Massachusetts 02199-8197

(Address of principal executive offices) (Zip code)

Susan McWhan Tobin, Esq.

Natixis Distribution, LLC

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2139

Date of fiscal year end: September 30

Date of reporting period: September 30, 2023

Item 1. Reports to Stockholders.

(a) The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Annual Report

September 30, 2023

Loomis Sayles Core Plus Bond Fund |

Loomis Sayles Credit Income Fund |

Loomis Sayles Global Allocation Fund |

Loomis Sayles Growth Fund |

Loomis Sayles Intermediate Duration Bond Fund |

Loomis Sayles Limited Term Government and Agency Fund |

Loomis Sayles Core Plus Bond Fund

|

|

|

|

|

Loomis, Sayles & Company, L.P. |

Investment GoalThe Fund seeks high total investment return through a combination of current income and capital appreciation.

Market Conditions

The US fixed income market produced a narrow gain in the 12 months ended September 30, 2023, albeit with a high level of volatility along the way. The majority of positive return occurred in the early part of the period. During this time, signs of cooling inflation and slightly more dovish commentary from US Federal Reserve (Fed) officials raised hopes that the central bank was approaching the end of its long series of interest rate hikes, even as the Fed continued to raise rates. This backdrop changed for the worse as crude oil prices surged to their highest level since July 2022, raising the possibility that inflation—which had been ticking lower since late last year—would begin to reaccelerate. In addition to being hurt by the prospect of rising rates, US Treasuries faced pressure from increased supply due to the need to fund the nation’s burgeoning debt load. Later in the period, the possibility of a government shutdown emerged as an additional source of instability for the market.

Investment grade corporate bonds logged robust, broad-based gains and strongly outperformed Treasuries. The category was helped by both its yield advantage and a decline in its yield spread relative to government issues. Lower-rated bonds, shorter-term debt, and economically sensitive issues exhibited leadership. High yield corporate bonds delivered a strong, double-digit gain and finished well ahead of the investment grade market, mostly due to its lower degree of sensitivity to interest rates. A large contribution from yield helped results, as did a decline in yield spreads brought about by investors’ elevated appetite for risk.

Floating rate securitized credit sectors displayed outperformance versus corporates and the broader fixed income markets. Agency mortgage-backed securities (MBS) continued to suffer from unfavorable supply/demand dynamics. Despite elevated levels of rate volatility, agency MBS outperformed US Treasuries over the period.

Performance Results

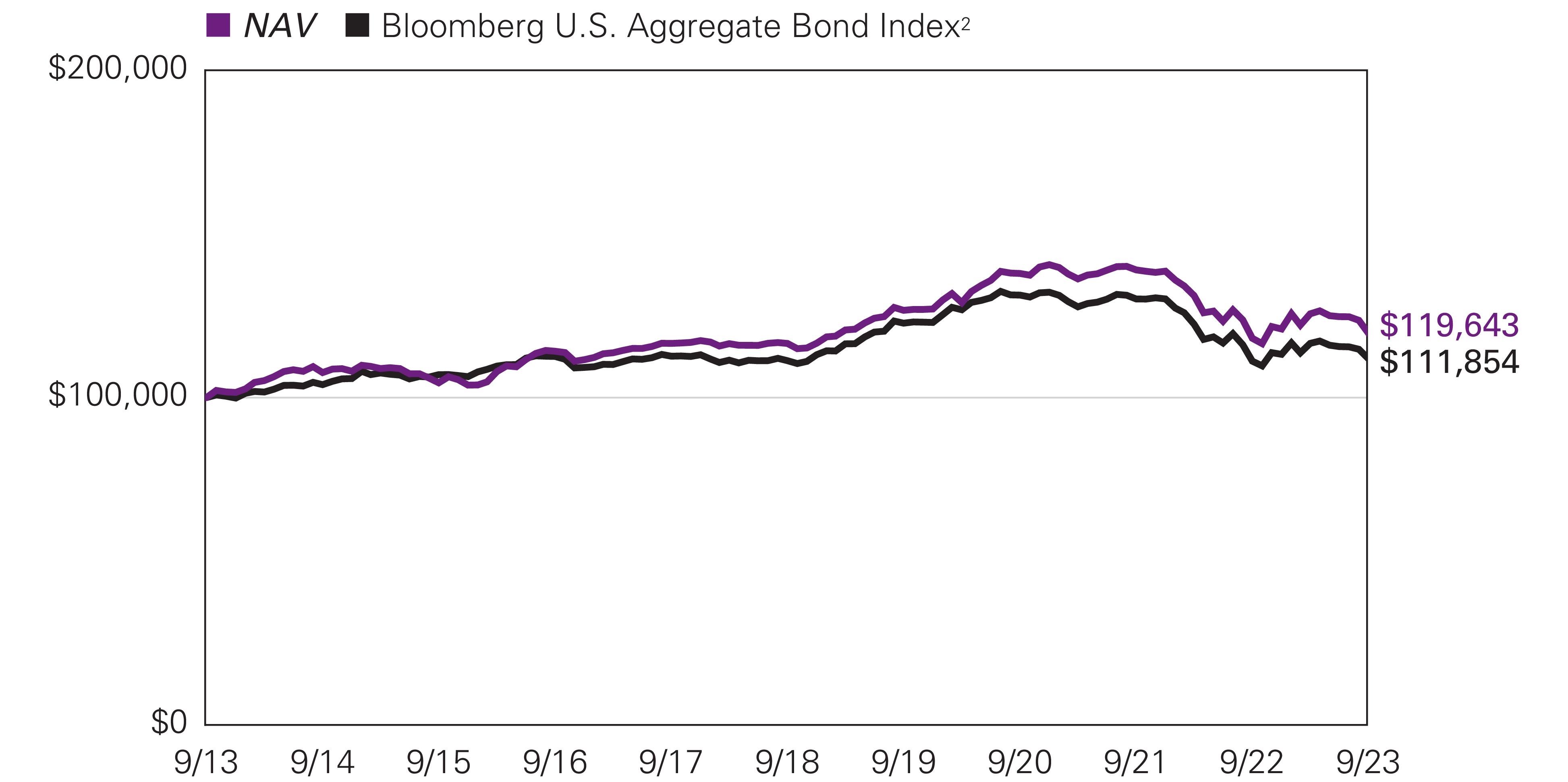

For the 12 months ended September 30, 2023, Class Y shares of the Loomis Sayles Core Plus Bond Fund returned 1.28% at net asset value. The Fund outperformed its benchmark, the Bloomberg US Aggregate Bond Index, which returned 0.64%.

Explanation of Fund Performance

The Fund’s excess returns over the trailing twelve months were primarily driven by sector allocation. Out-of-benchmark positions in “plus” sectors were the most impactful. We currently hold non-US dollar local government emerging market bonds in Mexico and Uruguay, which has been an important source of diversification and yield. Our allocation to high yield was also additive, due to spread tightening over the period and its lower interest rate sensitivity in general. Allocations to floating rate bank loans and collateralized loan obligations (CLOs) contributed positively, also a result of lower interest rate sensitivity. Within the “core” sectors, the Fund’s market value underweight to US Treasuries contributed to positive relative performance, while the underweight to investment grade corporates was a detractor.

Security selection over the period was also positive, as our relative value process identified issues and issuers which outperformed the benchmark across investment grade corporate, securitized credit, government-related, and securitized agency sectors. Securities held within the finance companies, banking, and electric utilities industries contributed the most to corporate-specific returns. Within government-related, our security selection in sovereigns was a contributor, while our decision not to own supranationals detracted. A 2% allocation to non-agency commercial mortgage-backed securities (CMBS), diversified across retail, office, and hospitality, also detracted.

The primary detractor from relative performance was due to duration and yield curve positioning. The Fund’s interest rate risk, as measured by duration, was higher than that of the benchmark by 1.3 years. This detracted from relative value in an environment of rising yields. Additionally, our decision to concentrate in the belly of the yield curve modestly detracted from relative returns. We are

Loomis Sayles Core Plus Bond Fund

expressing our duration and curve views through US Treasuries and utilizing interest rate futures to make adjustments efficiently. Exposure to Ultra Bond interest rate futures, which effectively increased the Fund’s allocation to the long end of the curve, detracted from performance.

Outlook

We continue to believe that we remain in the very late expansion phase of the credit cycle1, and that the significant increase in rates is now starting to impact business and consumer spending decisions. Corporate and consumer balance sheets have begun to show some signs of strain, and we expect the lagged effects of tighter credit conditions on the real economy will eventually translate to employment pressure and corporate profit degradation. Should growth and inflation sufficiently moderate over the coming three-to-six-month period, we think the Fed can pause hiking at or near the current 5.5% fed funds rate, and then consider easing policy somewhat starting in early summer 2024. This "soft landing" scenario is also currently the stated goal of the Fed. Recession risk could continue to be a factor if incoming economic data obscures the true impact of higher rates and restrictive monetary policy pushes the economy into downturn. We believe interest rates are likely to fall in either of those scenarios and are positioned with more interest rate risk in the portfolio relative to our benchmark. Our yield curve positioning continues to be concentrated in the five-to-ten-year part of the curve, an expression of our view that the yield curve will steepen, with short-term rates falling more sharply than long-term rates. The primary risk we face is that inflation remains above the Fed’s target, and doesn't moderate as we forecast, in which case we could see more rate hikes, and a peak fed funds rate of 6% or higher.

Portfolio liquidity remains at cycle highs, with nearly 40% of the portfolio in US Treasuries and cash equivalents. Looking ahead, we expect Treasury valuations to be supported by slowing economic activity and decelerating inflation. Additionally, Treasuries are a source of significant liquidity for re-entering credit sectors, should tangible signs of economic weakness cause credit spreads to widen from current levels. Weaker agency MBS valuations provided an opportunity to add to the sector in August, although we remain modestly underweight. In our view, MBS remain an attractive alternative to credit securities given their high current yield, return potential and the full backing of the US agencies. Within investment grade corporate credit, we remain approximately 8% market value underweight. We have a modest bias towards BBB-rated securities for incremental carry and tend to favor industries that we believe are less economically sensitive.

We have a large overweight to investment grade securitized credit, primarily in the front end of the yield curve for more defensive, non-corporate yield. We continue to favor higher-rated asset-backed securities (ABS) related to consumer receivables, as well as whole loan ABS, and have minimal exposure to commercial real estate.

Within the plus sectors, we have continued to reduce our overall allocation to high yield, which is currently approximately 5% in fixed rate high yield corporates, including just over 1% in emerging market high yield corporates. We have been incrementally reducing high yield exposure in response to the Fed's aggressive tightening path along with growing signs of economic slowdown. We have rotated bank loan exposure to high quality, investment grade CLOs, which are now at approximately 3%. We currently hold a 3.3% allocation to non-US dollar, now evenly split between Mexico and Uruguay, after monetizing a portion of our Mexican exposure to lock in significant gains.

1 A credit cycle is a cyclical pattern that follows credit availability and corporate health.

Loomis Sayles Core Plus Bond Fund

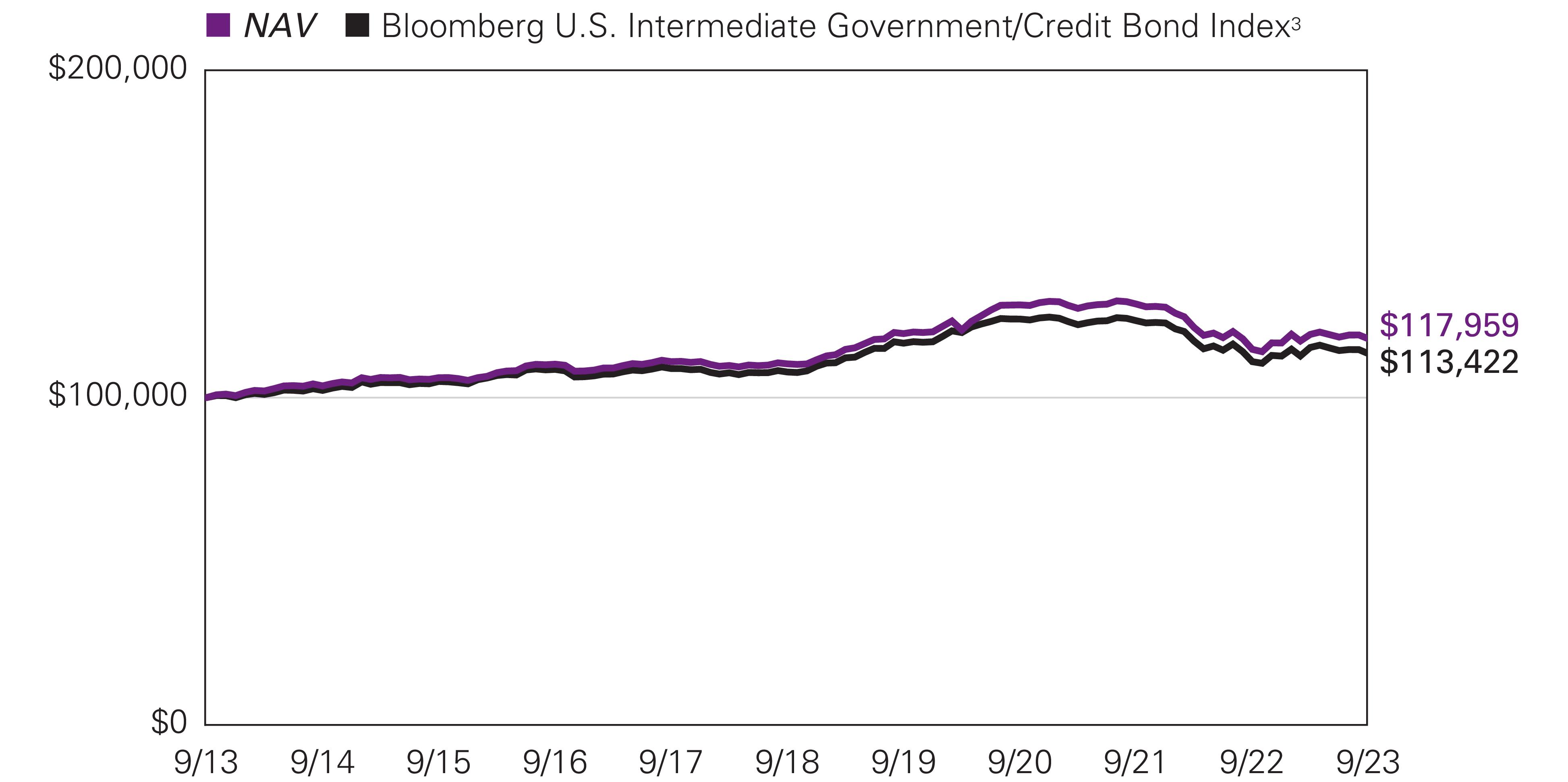

Hypothetical Growth of $100,000 Investment in Class Y Shares1 |

September 30, 2013 through September 30, 2023 |

Loomis Sayles Core Plus Bond Fund

Average Annual Total Returns — September 30, 20231 |

| | | | |

| | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

With 4.25% Maximum Sales Charge | | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

Bloomberg U.S. Aggregate Bond Index2 | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Bloomberg U.S. Aggregate Bond Index is a broad-based index that covers the U.S. dollar-denominated, investment-grade, fixed-rate, taxable bond market of SEC- registered securities. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed securities, asset-backed securities, and collateralized mortgage-backed securities sectors. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 1/31/24. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 5 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase, and includes automatic conversion to Class A shares after eight years. |

Loomis Sayles Credit Income Fund

|

|

|

|

|

Loomis, Sayles & Company, L.P. |

| Effective June 30, 2023, Peter Sheehan serves as portfolio manager of the Fund. |

Investment GoalThe Fund seeks high current income with a secondary objective of capital growth.

Market Conditions

The US fixed income market produced a narrow gain in the 12 months ended September 30, 2023, albeit with a high level of volatility along the way. The majority of the positive return occurred in the early part of the period. During this time, signs of cooling inflation and slightly more dovish commentary from US Federal Reserve (Fed) officials raised hopes that the central bank was approaching the end of its long series of interest rate hikes. While the Fed continued to raise rates—with a total of 1.25 percentage points of increases in late 2022, followed by four quarter-point hikes in 2023—investors appeared encouraged by hopes that the Fed was nearing the end of its hiking cycle.

This backdrop changed for the worse in the final three months of the period, leading to a downturn that significantly dampened 12-month returns. Crude oil prices surged to their highest level since July 2022, raising the possibility that inflation—which had been ticking lower since late last year—would begin to reaccelerate. In addition, the Fed made it clear that although its pace of interest rate increases slowed in 2023, it remained open to further hikes if necessary. These developments fed through to longer-term expectations, with the futures markets beginning to factor in fewer rate cuts in 2024 than was the case earlier in the year.

US Treasuries posted a loss and underperformed the more credit-oriented areas of the bond market in the annual period. Performance was mixed across the curve: while the two and five-year issues produced positive total returns, the 10-year note lost ground and the 30-year bond suffered a double-digit loss. In terms of yield movements, the two-year climbed from 4.22% at the start of the period to 5.03% on the final trading day of September 2023, and the 10-year rose from 3.83% to 4.57%.

Notably, the yield curve remained inverted throughout the period (meaning that short-term yields traded above those on longer-term debt). At the end of June, in fact, the curve was at its highest degree of inversion on the last day of a calendar quarter in history. Although an inverted yield curve has often been a precursor to a recession historically, economic growth stayed in positive territory.

Investment grade corporate bonds logged robust, broad-based gains and strongly outperformed Treasuries. The category was helped by both its yield advantage and a decline in its yield spread relative to government issues. The ICE BofA US Corporate Index Option-Adjusted Spread opened the period at 1.67 over Treasuries and closed at 1.23, indicating outperformance. Lower-rated bonds, shorter-term debt, and economically sensitive issues exhibited leadership, providing a tailwind for the category.

High yield corporate bonds delivered a strong, double-digit gain and finished well ahead of the investment-grade market, mostly due to the lower duration of high yield. A large contribution from yield helped results, as did a decline in yield spreads brought about by investors’ elevated appetite for risk. Senior loans, which typically feature floating rates, benefited from the rising-rate environment and were one of the top-performing segments of the bond market.

Over the prior year, securitized assets produced largely positive total returns, with the exception of non-agency commercial mortgage-backed securities (CMBS) and agency mortgage-backed securities (MBS). Collateralized loan obligations (CLOs) and commercial asset-backed securities (ABS) provided particularly strong returns over the period, with portions of the residential mortgage-backed securities (RMBS) market also outperforming. Headwinds facing the commercial real estate sector emerged in the first half of 2023, negatively impacting non-agency CMBS performance over the period. The shorter duration in most securitized credit sectors led to outperformance versus corporates and the broader Bloomberg US Aggregate Bond Index. A challenging technical backdrop negatively impacted agency MBS returns as elevated levels of rate volatility continued. However, agency MBS did outperform US Treasuries over the period.

Loomis Sayles Credit Income Fund

Developed market government bonds weakened in local currency terms given the challenging rate environment. However, emerging market bonds gained ground, reflecting both positive local market performance and favorable currency translation.

Performance Results

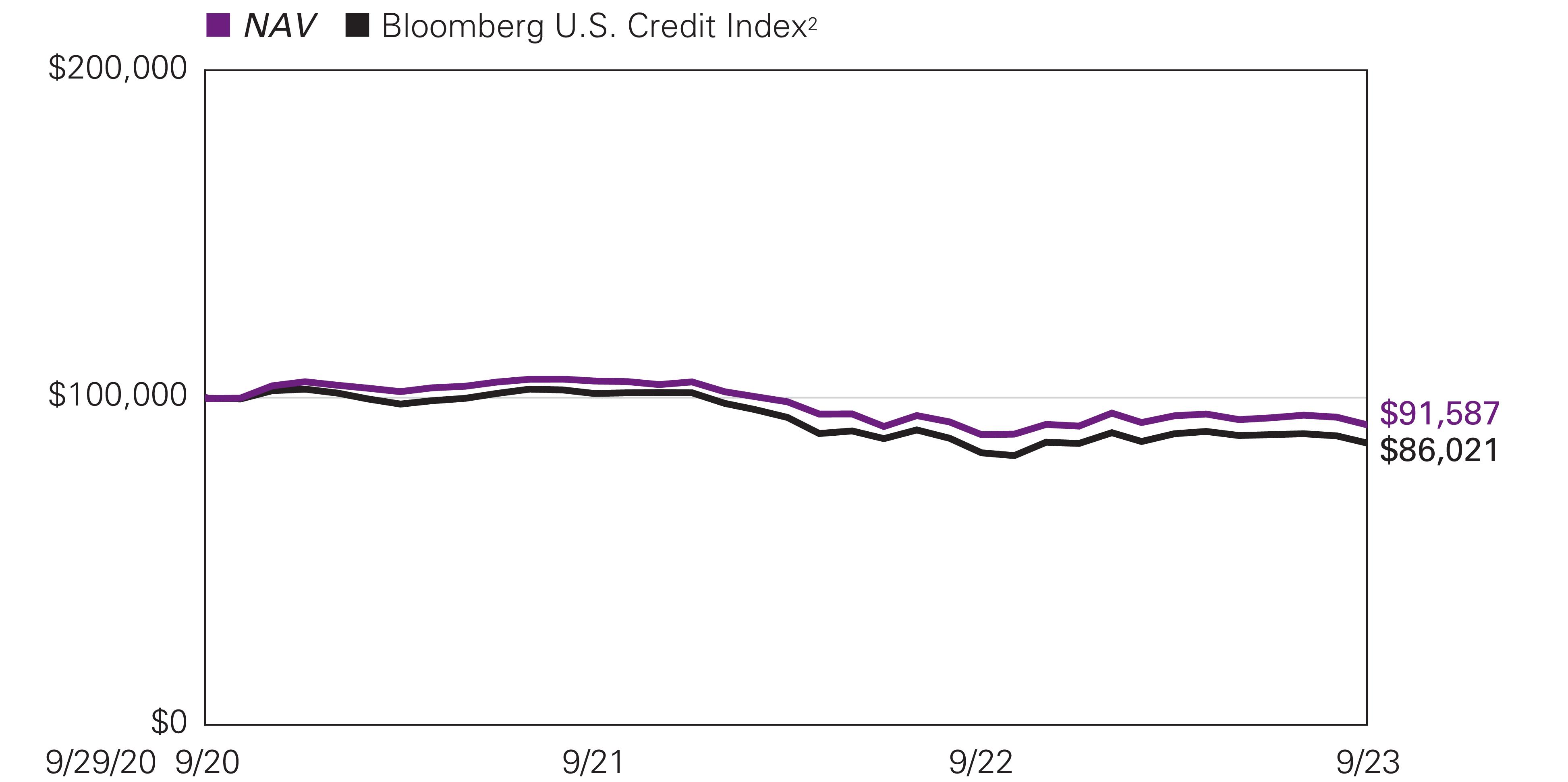

For the 12 months ended September 30, 2023, Class Y shares of the Loomis Sayles Credit Income Fund returned 3.27% at net asset value. The Fund underperformed its benchmark, the Bloomberg US Credit Index, which returned 3.47%.

Explanation of Fund Performance

The year brought continued volatility as the positive returns investors realized in the first half of the year were erased by the rise in US long-term yields during the third quarter of 2023. Due to this volatility, the Fund underperformed its index during the period. Duration positioning in US Treasuries was the main detractor from performance, and the team continued to use Treasury futures to manage overall portfolio duration, which had a negative impact. The Fund began the period with shorter duration relative to the benchmark but brought overall duration positioning closer to neutral (increased duration) during the year as we believed the Fed could be nearing the end of its hiking cycle. Given this positioning, the rise in interest rates in 2023 led to the majority of negative returns.

Both high yield and investment grade credit were strong contributors to performance over the year. Within high yield credit, our higher conviction names in the consumer cyclical and communications space were beneficial. For investment grade credit, names in banking and consumer cyclical were positive. Securitized credit was also beneficial given the asset class’ shorter duration profile. Here, holdings in CLOs aided returns. Finally, performance was aided by defensive, reserve-like positions.

Outlook

A rise in US long-term yields during the third quarter erased the overall positive returns realized in the first half of the year across most sectors of the global fixed income market. Inflation — while still above the Fed’s 2% target — continued to decline from its mid-2022 peak and helped create optimism early in the year that central banks would be able to conclude their long series of interest rate hikes. More recently, a re-pricing of expectations for growth (resilient), inflation (stickier) and Fed policy (higher for longer), as well as concern for significant US Treasury issuance over the coming 12-24 months, pushed yields higher. Since hitting a low of 3.31% for the year on April 6, the 10-year US Treasury yield climbed higher, ending September at 4.57%. As a result, performance of high quality, long duration bonds suffered. Sectors that have less interest rate sensitivity, such as high yield corporates and bank loans, continue to be bright spots on a year-to-date return basis.

In our view, the credit cycle1is firmly in the late cycle stage. Monetary policy is restrictive and lending standards have tightened; however, the economic backdrop has remained resilient and forecasts are reflecting better-than-expected growth for the remainder of 2023. Most notably, resiliency can be seen in areas such as services/housing, while manufacturing has also experienced a bounce from more depressed levels witnessed late last year. While the risk of downturn remains, at this time we do not expect a technical recession of back-to-back quarters with negative GDP. Our base case calls for below trend US growth and our view is dependent on a strong consumer and stable corporate fundamentals. The consumer appears to maintain strong levels of excess savings and continues to spend at a healthy rate. Shifts in hiring and firing dynamics, including labor hoarding, have led to employment remaining robust. We believe these factors should help support consumer confidence and spending going forward. Monetary policy has helped to cool employment, but it is still growing, and investors have likely had to reassess how much flexibility the Fed may have in the near term.

Corporate fundamentals appear stable, highlighted by strong leverage and interest coverage ratios, and specific to the high yield market, a maturity wall that seems manageable, in our opinion, through 2025. We are carefully monitoring the pace of corporate earnings growth. Earnings have contracted over the past three quarters, putting us in the midst of a “profits recession.” While we believe earnings will trough at the end of 2023, if this trend continues, or accelerates as pricing power fades and margins come under further pressure, companies may need to aggressively cut costs (via job cuts). This could lead to an environment where the pace of earnings growth declines materially and ultimately leads to recession. Under this scenario, we believe a healthy consumer combined with stable corporate fundamentals should serve to minimize the potential for a hard landing by providing a floor to economic activity that could result in a mild or shallow recession.

While inflation has peaked and positive real rates should have the effect of slowing growth and rolling inflation down over time, in our opinion inflation will continue to be sticky. We believe inflation will remain elevated and above the Fed's target through the end of 2023 and into 2024 as services inflation remains high, which is worrisome because services inflation is currently stickier than goods inflation. Rising wages may be a major factor that keeps inflation elevated and constrains Fed policy in the near term. In addition, we foresee longer-term structural concerns that could support higher levels of inflation, including the impact of de-globalization, de-carbonization, aging demographics and growing government deficits. We anticipate the Fed will be driven by how firm evidence is that inflation continues to moderate. The potential for an extended Fed pause and short-term rates that stay “higher for longer” remains; in our view, policymakers will be slow to react to the onset of a downturn and will likely tolerate a rise in unemployment, particularly

Loomis Sayles Credit Income Fund

while inflation is above target. We believe value has returned to US fixed income markets and a combination of discount-to-par, favorable yields and an increase in issuer performance dispersion is helping to create opportunities in bonds. We expect defaults/losses to remain relatively low, while slowly increasing to more normal levels associated with a late cycle environment. With the potential for a downturn in 2024, we have been holding larger-than-average liquid reserves. We are comfortable with how we are being compensated by short-term yields as we patiently wait for opportunities to potentially develop. If volatility increases and we see what we view as more attractive yields and spreads, we would consider re-deploying reserves. Overall, we are maintaining an up-in-quality bias and are focused on credits that we believe can weather a slowdown, or credits that will benefit from the transition of goods to services spending. We are mindful of the risks going forward, such as tighter financial conditions and their impact on the financial system, slower Chinese growth, geopolitical risk, and the broader economic impact of a further decline in the commercial real estate market. Much of the turmoil leaves us with a wide range of potential outcomes for growth, inflation and central bank policy response. Based on the uncertain backdrop, we feel it is prudent to maintain a balanced risk profile between interest rate and spread risk. We believe the 10-year US Treasury range is currently around 3.75% - 4.75%, with a potential path to 5% over the long term. We have structured our portfolios for a steeper yield curve, which we believe will be primarily driven by a fall in short-term rates as inflation moderates, combined with secular trends that could potentially keep a floor under long-term yields.

The Fund closed as of November 6, 2023, and as it closed, primary consideration was given to clients and their interests. There was no unusual market action that affected our trading of the portfolio during liquidation. All Fund assets were subsequently redeemed or distributed to Fund shareholders.

1 A credit cycle is a cyclical pattern that follows credit availability and corporate health.

Hypothetical Growth of $100,000 Investment in Class Y Shares1 |

September 29, 2020 (inception) through September 30, 2023 |

Loomis Sayles Credit Income Fund

Average Annual Total Returns — September 30, 20231 |

| | | |

| | |

Class Y (Inception 9/29/20) | | | | |

| | | | |

Class A (Inception 9/29/20) | | | | |

| | | | |

With 4.25% Maximum Sales Charge | | | | |

Class C (Inception 9/29/20) | | | | |

| | | | |

| | | | |

Class N (Inception 9/29/20) | | | | |

| | | | |

| | | | |

Bloomberg U.S. Credit Index2 | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Bloomberg U.S. Credit Index measures the investment grade, U.S. dollar-denominated, fixed-rate, taxable corporate and government-related bond markets. It is composed of the U.S. Corporate Index and a non-corporate component that includes non-U.S. agencies, sovereigns, supranationals and local authorities. The Index was called the U.S. Corporate Index until July 2000, when it was renamed to reflect its inclusion of both corporate and non-corporate issuers. The Index is a subset of the U.S. Government/Credit Index and U.S. Aggregate Index. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 1/31/24. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 5 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

Loomis Sayles Global Allocation Fund

|

|

|

|

|

Loomis, Sayles & Company, L.P |

Investment GoalThe Fund seeks high total investment return through a combination of capital appreciation and current income.

Market Conditions

The past 12-month period was characterized by “risk on” sentiment, with credit and equity markets outperforming global government bonds. One reason for the favorable showing from risk assets was timing: when the reporting period began in October 2022, risk assets were near the end of a protracted, 10-month decline brought about by the US Federal Reserve’s (Fed) aggressive interest rate increases. By the fourth quarter of 2022, however, cooler inflation prompted investors to begin looking ahead to when the central bank could shift to a neutral policy. Although the Fed continued to raise rates throughout 2023, the slower pace of tightening fostered persistent optimism about the longer-term outlook. The markets were further cheered by economic data and corporate earnings that consistently exceeded the depressed expectations that were in place in late 2022.

While total returns were generally positive for the full period, the backdrop became less supportive in August and September of 2023. A sharp increase in oil prices raised fears that inflation would reaccelerate and lead the Fed and other central banks to maintain tight monetary policies for longer than the markets had been expecting. Signs of slowing growth, particularly in Europe and China, further weighed on sentiment by raising the odds that the world economy could enter a period of stagflation.

The US fixed-income market posted a narrow gain for the 12 months ended September 30, 2023, albeit with a high level of volatility along the way. US Treasuries suffered losses and underperformed the more credit-oriented areas of the bond market. Performance was mixed across the yield curve: while the two- and five-year issues produced positive total returns, the 10-year note lost ground and the 30-year bond experienced a double-digit decline. Global developed market government bonds weakened in local currency terms, but currency translation helped results. The credit-sensitive segments of the market—investment grade corporate high-yield bonds, senior loans, and emerging-market issues—finished with healthy gains and strongly outpaced government debt thanks in part to the “risk-on” market in the first half of 2023.

The US dollar posted mixed results, initially falling sharply in late 2022 on expectations that the Fed would shift to a less aggressive policy stance. However, once investors began to see “higher-for-longer” as being the most likely scenario, the dollar staged an impressive rally in the third calendar quarter of 2023 and made up for most of its earlier losses. For the full period, the euro and British pound appreciated relative to the dollar while the Japanese yen struggled against the dollar.

Despite the late downturn, equities delivered robust gains over the full 12 months. Growth stocks in general, and US mega-cap technology companies in particular, generated meaningful outperformance. Mid- and small-cap stocks, while finishing behind large caps, also posted solid gains. The developed international markets were an additional source of positive performance, with Europe leading the way higher. Value stocks, defensive sectors, and the emerging markets gained ground in absolute terms but underperformed the broad-based indexes. The emerging markets were hurt by the weak showing for China, which experienced a slower-than-expected economic recovery after reopening from the government’s extended Covid-19 lockdowns.

Performance Results

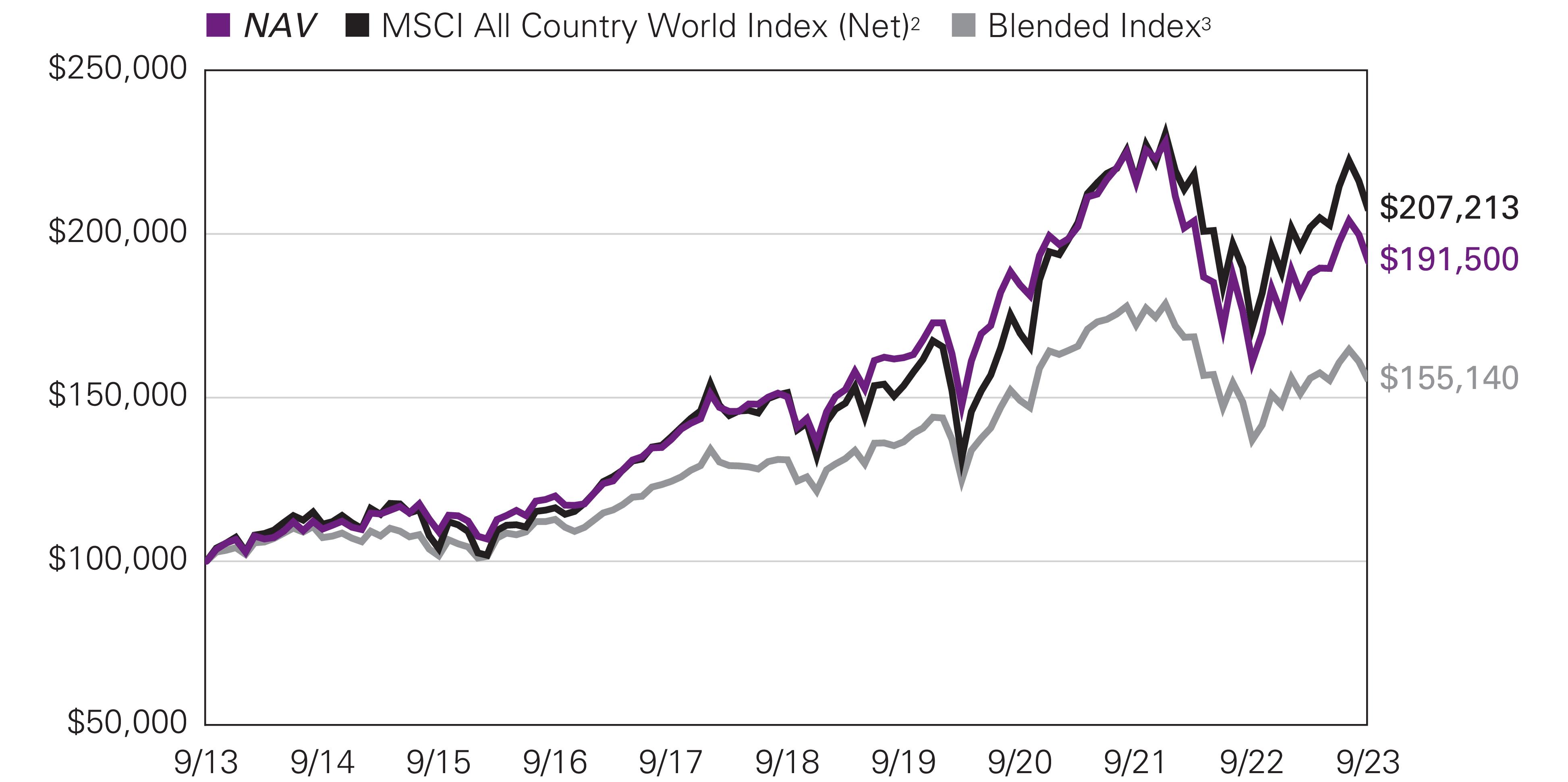

For the 12 months ended September 30, 2023, Class Y shares of the Loomis Sayles Global Allocation Fund returned 19.00% at net asset value. The Fund underperformed its primary benchmark, the MSCI All Country World Index (Net), which returned 20.80%. The Fund outperformed its secondary blended index (60% MSCI All Country World Index (Net)/40% Bloomberg Global Aggregate Bond Index) which returned 13.18%.

Explanation of Fund Performance

In equities, the largest detractors from performance were Zions Bank, Estee Lauder and Danaher.

Zions Bank is a high-quality regional bank with a client base dominated by small to mid-size businesses (SME’s) in the western US. It has a strong franchise in its home base of Utah, where it has the leading market share, and in higher growth southern and western

Loomis Sayles Global Allocation Fund

states. Zions has a high-quality management team; since 2018, management’s strategy has shifted away from acquisitions and towards better allocation of excess capital generation, including share buybacks. Its focus on SME’s provides it with low-cost funding, as it has a relatively high proportion of non-interest bearing commercial deposits. The bank has made significant improvements since the Global Financial Crisis, better managing its expenses and materially improving its efficiency ratio to bring it more in line with peers. Zions has also improved its credit risk management through diversifying its loan book, primarily by reducing the proportion of real estate and energy loans. We believe the bank is well placed to benefit in a rising interest rate environment due to its strong base of non-interest bearing deposits. We also think Zions has an opportunity to further improve its operations by increasing its fee income through wealth management and capital market services. The stock is attractively valued under our discounted cash flow methodology.

Shares of Zions fell just under 40% in the first quarter; investors were concerned about midsize regional bank deposit outflows and rising cost of deposits that could put pressure on profitability. These concerns were exacerbated by the failure of Silicon Valley Bank and another regional bank in March, following deposit runs amid scrutiny of banks’ unrealized losses in their securities portfolios. The stock recovered in the third quarter on signs of the regional banking crisis receding. Zions also announced second quarter results which showed stable credit quality and some signs that the downward pressure on net interest margins is easing.

Shares of Estee Lauder, a multi-national manufacturer and marketer of prestige beauty products, underperformed. We eliminated our position due to concerns regarding the company's ability to grow its intrinsic value. There has been significant erosion of the company's earning power due to an oversupply of inventory in the Asia-Pacific region and a slowdown in developed markets, with limited ability to forecast a path to recovery. Additionally, we have been finding better risk/reward opportunities to include in the portfolio and had been trimming the position size prior to exiting.

Danaher is a technology-focused health care company with a highly durable portfolio. Approximately three quarters of its businesses are healthcare-centric (life sciences and diagnostics) and are supported by secular drivers, such as an aging population, growth of chronic disease and rising healthcare costs. Its other businesses, under the umbrella of “Environmental & Applied Solutions,” sell products geared toward water quality where demand is underpinned by increasing regulatory and safety requirements. Shares retreated in the third quarter after the company reduced its full-year revenue and profit guidance on lower expectations for bioprocessing growth. The adjusted growth forecast stemmed from a decline in pandemic-related demand; we believe these Covid revenue streams will be fully replaced over the next two years driven by strong demand for bioprocessing instruments consumables as well as a recovery in demand for non-Covid molecular tests as patient volume returns. We believe Danaher is well positioned to manage any economic slowdown with three-quarters of its revenue recurring and over 85% of revenue attributable to healthcare end markets. Longer-term, we expect Danaher to continue apply the Danaher Business System continuous improvement strategy to consolidate the life science and tools industry, to right-size acquired companies and to deliver attractive returns to shareholders. Danaher’s shares are attractively valued based on our discounted cash flow methodology.

Within fixed income, while yield curve exposure as a whole contributed to performance, allocations to the US dollar (particularly the five- and ten-year segments) and euro-pay markets detracted. Both the Fed and European Central Bank (ECB) continued aggressive monetary tightening over the year in order to tame persistently high inflation.

Within corporate credit, select holdings in the communications and technology sectors detracted from performance. Within communications, cable satellite provider CSC and media entertainment company IHRT were the biggest detractors, while within technology Commscope was a notable underperformer.

In equities, the largest contributors to performance were Nvidia, ASML and Linde.

Nvidia's origins are in hardware and the gaming end market; it created the world’s first discrete graphics processing unit (GPU) in 1999. The company has since evolved into a larger ecosystem of products with the GPU at its core; its accelerators are used in the gaming, professional visualization, data center and automotive markets. The company created a singular platform across all products and updates are fully compatible, making for seamless transitions for their customers. Nvidia has only one GPU competitor, and holds a 70% or higher market share across all of its end markets. The company has continued to grow by creating new uses for its hardware and software. Specifically, the recent artificial intelligence (AI) renaissance is increasingly leveraging GPUs rather than CPUs, leading to new and larger opportunities in the data center and automotive markets. The company is starting to explore options to monetize its software (currently it is "free" with its hardware) via licensing and subscription models. Nvidia’s gross margin has been on an upward trajectory over the last decade as its business mix shifts towards the more profitable data center business; we expect this trend to continue as standalone software sales and new markets provide a lift. Capital allocation is strong with dividends, repurchases and select M&A, while maintaining a net cash position.

Shares of Nvidia outperformed over the period. In the company’s first quarter earnings release, management noted their view of the data center market had improved given the excitement around ChatGPT (an AI tool). Management also introduced AI as a Service which will provide access to sophisticated AI tools otherwise not affordable to many. In the second quarter, shares continued to outperform; the company announced first quarter revenue above consensus expectations while raising guidance materially. The rapid

Loomis Sayles Global Allocation Fund

rise in AI utilization and popularity of generative AI tools such as ChatGPT has been a significant tailwind for Nvidia, as the company is a critical supplier to the industry.

Shares of ASML, a leader in photolithography (the process in which a light source is used to etch a pattern on a silicon wafer) outperformed. We believe ASML is uniquely positioned in the utilization of extreme ultraviolet (EUV), the next generation technology which allows chipmakers to continue to make chips smaller while maintaining their power (i.e., Moore’s law). The barriers to entry are high given the required technical expertise (EUV was in development for ten years) and associated R&D spending. ASML partners with its customers, aligning its product roadmap with their needs, which we believe has led to a symbiotic relationship. ASML is moving toward a value-based service model under which it will be paid according to the wafer output of its machines, which should be more profitable. Under this model, ASML agrees to meet a set level of output, and if it is not met ASML is obligated to fix the issues at no additional cost to the customer. Assuming their machines are delivering as promised, we believe the company should enjoy a solid revenue stream based on chip output.

Linde is one of the largest industrial gases companies in the world, formed in 2018 as the result of a merger between Linde and Praxair. Linde’s industrial gases are used across industries – from high purity gases in semiconductor production to natural gas liquefaction plants in the energy sector. The company rates highly across our quality criteria. Industrial gases are critical products in many applications, driving pricing power. Contracts are long-term in nature and switching costs are high, particularly for large customers with on-site plants, which provides revenue visibility. We believe the company has meaningful scale, holding the top one or two positions in every market globally, where density is a competitive advantage; the market structure is also consolidated creating a disciplined market environment. With regard to ESG initiatives, we believe greenhouse gas emissions reduction presents a material opportunity for the company. Linde continues to lower its carbon footprint internally and, most importantly, we believe it also has an opportunity externally as the company continues to expand its hydrogen portfolio, which can help lower the carbon footprint of its customers. We expect revenue growth, operating margin expansion and capital allocation to be among the key drivers of intrinsic value growth. The company’s strong free cash flow generation and appetite to repurchase shares over time further add to our intrinsic value growth outlook. The stock outperformed over the period as business execution around top line, margin expansion and capital deployment continued to be strong.

In fixed income, credit positioning was a top contributor to performance over the period. In particular, allocations to the consumer non-cyclical, consumer cyclical and finance company industries contributed over the period. Holdings of pharmaceutical and healthcare companies such as Teva Pharmaceuticals and Teladoc Health were top drivers of returns. Exposure to Uber contributed positively to performance within the consumer cyclical sector.

Currency allocation also contributed to performance over the period. In particular, exposure to the euro, Brazilian real and Polish zloty contributed over the period, as those currencies appreciated against the US dollar.

Outlook

Currently, our core view is that the global economy is in a vulnerable position and therefore at risk of entering the downturn phase of the credit cycle1. However, asset valuations are generally reflecting a “soft landing” scenario. As we view the probability of this outcome as only around 20%, we find risk assets optimistically priced.

While earnings for companies in the S&P 500 Index were negative for the past three quarters, they did not collapse to the point where companies began to shed jobs – a scenario that typically heralds a downturn in the economy. Corporations have been losing pricing power, and economic growth appears set to continue slowing. We believe top-line revenue growth will be more challenging to generate, and we suspect that further profit margin compression is ahead. We view credit spreads as tight and likely to widen over the next six-to-twelve months. In our view, growth expectations are too high as bond yields have surged, the US dollar has strengthened and energy prices have increased.

China’s economic growth has been a disappointment for the last few months. It wasn’t long ago that the market was incredibly bullish on the country’s post-Covid recovery story, but that optimistic scenario has failed to play out. Since China is a large source of external demand for the rest of the global economy, its continued economic underperformance would weigh on total global economic growth. However, the most recent data prints in the country have shown evidence of stabilization.

We are watching 2024 GDP growth expectations closely. Bloomberg consensus estimates are calling for growth of 0.9% in the United States in the coming year, while the Fed sees an expansion of 1.5%. In our view, growth expectations are too high given the combination of higher bond yields, the strong US dollar and rising energy prices. In this vein, leading indicators have continued to show a stagnant economic environment in the euro area. Manufacturing purchasing managers indexes (PMIs) in the region remained weak, and services PMIs also dropped into contraction territory. At its September 14 meeting, the ECB revised down its 2023 growth forecasts due to weaker second quarter growth and the slowdown in China. The ECB acknowledged that tighter financial conditions

Loomis Sayles Global Allocation Fund

have had an increasing impact on activity, and that core inflation pressure has begun to ease. This is in line with our expectation that the ECB will soon shift from aggressive hiking to a more neutral posture.

Globally, inflation remains far above central banks’ typical 2% targets. In our view, this adds to a growing belief that the economy is entering a higher-for-longer interest rate environment. The Fed’s September forecasts boosted the median expected fed funds rate in 2024 from 4.6% to 5.1%. The central bank’s September Summary of Economic Projections included higher GDP growth forecasts for 2023 and 2024, further suggesting that rates could remain elevated for some time.

1 A credit cycle is a cyclical pattern that follows credit availability and corporate health.

Top Ten Holdings as of September 30, 2023 |

| |

1 Alphabet, Inc., Class A | |

| |

3 Mastercard, Inc., Class A | |

| |

| |

6 UnitedHealth Group, Inc. | |

| |

| |

| |

10 Atlas Copco AB, Class A | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Hypothetical Growth of $100,000 Investment in Class Y Shares1 |

September 30, 2013 through September 30, 2023 |

See notes to chart on page 13.

Loomis Sayles Global Allocation Fund

Average Annual Total Returns — September 30, 20231 |

| | | | | |

| | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

With 5.75% Maximum Sales Charge | | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

Class N (Inception 2/2/17) | | | | | | |

| | | | | | |

| | | | | | |

MSCI All Country World Index (Net)2 | | | | | | |

| | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| MSCI All Country World Index (Net) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. |

| Blended Index is an unmanaged, blended index composed of the following weights: 60% MSCI All Country World Index (Net) and 40% Bloomberg Global Aggregate Bond Index. The Bloomberg Global Aggregate Bond Index provides a broad-based measure of the global investment-grade fixed income markets. The four major components of this index are the U.S. Aggregate, the Pan-European Aggregate, the Asian-Pacific Aggregate, and the Canadian Aggregate Indices. The Index also includes Eurodollar and Euro-Yen corporate bonds, Canadian government, agency and corporate securities, and USD investment grade 144A securities. |

| Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense limitations set to expire on 1/31/25. When a Fund’s expenses are below the limitation, gross and net expense ratios will be the same. See Note 5 of the Notes to Financial Statements for more information about the Fund’s expense limitations. |

| Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase, and includes automatic conversion to Class A shares after eight years. |

Loomis Sayles Growth Fund

|

Aziz V. Hamzaogullari, CFA® |

Loomis, Sayles & Company, L.P. |

Investment GoalThe Fund seeks long-term growth of capital.

Market Conditions

US equities produced strong performance in the 12 months ended September 30, 2023. When the reporting period began in October 2022, stocks were near the end of a protracted, ten-month decline brought about in part by the US Federal Reserve’s (Fed) aggressive interest rate increases. By the fourth quarter of 2022, however, cooler inflation prompted the Fed to begin decelerating the pace of rate hikes, which provided relief to markets. Although the Fed continued to raise rates throughout 2023, its slower pace of tightening may have fostered renewed optimism about the longer-term outlook. Investors may have been further encouraged by economic data and corporate earnings that consistently exceeded the depressed expectations that were in place in late 2022. While the backdrop became less favorable in August and September, the US market finished firmly in positive territory on the strength of its earlier gains. Growth stocks in general, and US mega-cap technology companies in particular, delivered meaningful outperformance. Mid- and small-cap stocks, while finishing behind large caps, also posted solid gains.

Performance Results

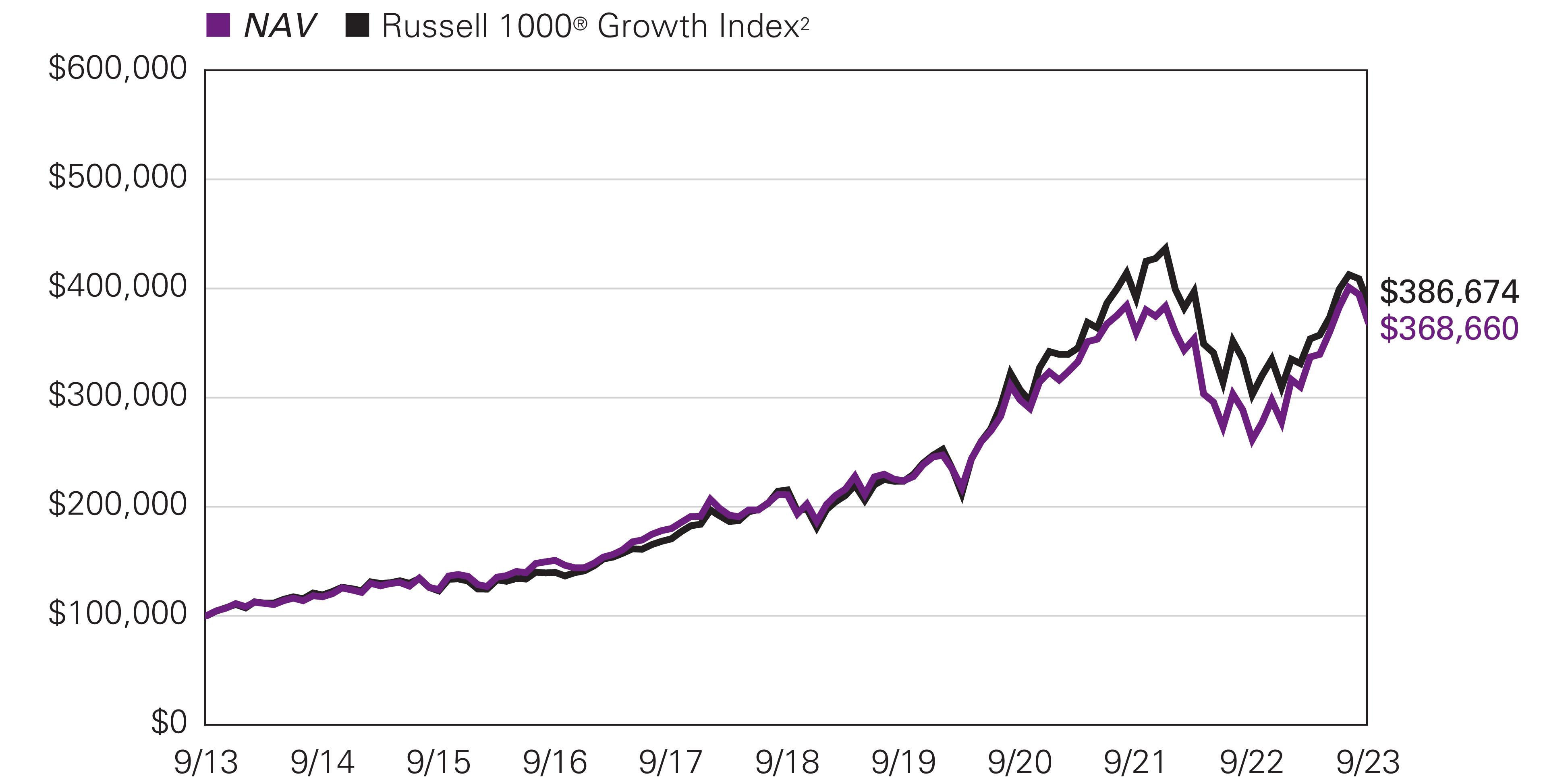

For the 12 months ended September 30, 2023, Class Y shares of the Loomis Sayles Growth Fund returned 40.97% at net asset value. The Fund outperformed its benchmark, the Russell 1000® Growth Index, which returned 27.72%.

Explanation of Fund Performance

We are an active manager with a long-term, private equity approach to investing. Through our proprietary bottom-up research framework, we look to invest in those few high-quality businesses with sustainable competitive advantages and profitable growth when they trade at a significant discount to intrinsic value. Given the rare confluence of quality, growth, and valuation, we may study dozens of companies but may only invest in a select few businesses each year. We believe identifying those few businesses with these characteristics is an art, not a science. As a result of this rigorous approach, ours is a selective, high-conviction portfolio of typically 30-40 names.

The Fund’s positions in Nvidia, Meta Platforms, and Boeing contributed the most to performance. Stock selection in the information technology, communication services, industrials, consumer staples, consumer discretionary, and healthcare sectors, along with our allocations in the communication services, consumer staples, consumer discretionary, healthcare, and industrials sectors, contributed positively to relative performance.

Nvidia is the world leader in artificial intelligence (AI) computing, which enable computers to mimic human-like intelligence for problem solving and decision-making capabilities. We believe the company’s competitive advantages include its intellectual property, brands, and a large and growing ecosystem of developers and applications utilizing its GPU (graphic processing unit) technology. A portfolio holding since January 2019, after shares were under pressure throughout most of 2022 given a weak market backdrop, shares rebounded substantially over the past 12 months, with gains accelerating following the company’s first quarter earnings report in May. Nvidia reported financial results that were well above consensus expectations, as AI applications, including generative AI, are driving strong demand for GPUs by companies looking to leverage these capabilities and drive competitive differentiation. The company also provided revenue guidance that was substantially higher than consensus expectations, resulting in a material increase in expectations for revenue, profits, and free cash flow for its full fiscal year. Revenue in the company’s gaming segment has been depressed, which we believe reflected global demand for PCs returning to pre-pandemic levels after a period of excess, and the impact of macroeconomic weakness and Covid-19 restrictions on China consumer spending. However, we believe the company has done a good job of clearing existing inventory in its retail channels, which contributed to the gaming business returning to growth in the most recent quarter. In the company’s data center business, we believe the company’s decades of focused investment, cumulative know-how, and robust software platform and architecture that has attracted millions of developers, position the company to benefit from several secular long-term growth drivers, including continued growth in use cases for artificial intelligence. To further drive adoption by enterprises, Nvidia is also partnering with cloud service providers including Oracle, Microsoft, and Google to offer AI services via the cloud. We believe Nvidia remains strongly positioned to benefit from secular growth in gaming and is still in the early stages of growth in its data center business, which has the potential to be much larger in the long term. We believe Nvidia’s strong growth prospects are not currently

Loomis Sayles Growth Fund

reflected in its share price. As a result, we believe the company’s shares are trading at a significant discount to our estimate of intrinsic value, offering a compelling reward-to-risk opportunity.

Meta Platforms operates online social networking platforms that allow people to connect, share, and interact with friends and communities. With 3.9 billion monthly users, 200 million businesses, and 10 million advertisers worldwide using its family of apps – Facebook, Messenger, WhatsApp, and Instagram – the scale and reach of Meta’s network is unrivaled. A strategy holding since its IPO in 2012, Meta’s shares were under pressure throughout most of 2022, due to a perceived lack of discipline in the company’s capital expenditures – especially with respect to the metaverse – that coincided with what we believed was temporary fundamental weakness arising from the company’s transition to a new advertising format and maneuvering around privacy changes imposed by Apple in 2021. Our analysis suggested that Meta was being priced as if a high-quality, high-returning, growth company – whose returns on capital were many times larger than its cost of capital – would become a low-quality business that ceased to grow and would henceforth generate low margins and low returns on invested capital. We took advantage of near-term price weakness to add to our holdings on multiple occasions during this period, most recently in October and November 2022. Despite ongoing macroeconomic pressure on advertising spending, Meta has since posted three consecutive quarters of better-than-expected financial results, including accelerating revenue growth in the second half of the period. Following this period of temporary weakness and elevated investment spending, Meta announced a set of efficiency measures that have already led to significant improvements in margins and lower capital expenditure plans, and shares responded positively to the company’s increased focus on productivity and cost management. We believe founder and CEO Mark Zuckerberg has always managed the company with a long-term focus and strong strategic vision. Over the past ten years, Meta has spent over $125 billion on research and development and $110 billion on capital expenditures – a level of investment that few firms can match and which creates high barriers to entry for competitors that are further compounded by the growth of cumulative knowledge over time. The successful development of a metaverse is not an explicit part of our investment thesis for Meta. However, given the potential size of the opportunity, which we estimate could impact over $1 trillion of spending over the long term, and Meta’s positioning with billions of users and hundreds of millions of businesses, we believe Meta’s current balanced approach to its forward-looking investments make sense. We expect that corporations will continue to allocate an increasing proportion of their advertising spending online, and Meta remains one of very few platforms where advertisers can reach consumers at such scale in such a targeted and effective fashion. We believe Meta’s brands, network, and targeting advantage position the company to take increasing share of the industry’s profit pool and grow its market share from 6% currently to approximately 10% of the total global advertising market over our investment time horizon. On the basis of its core business alone, we believe the company is substantially undervalued and trades at a significant to our estimate of intrinsic value. In the second half of the period, we trimmed our position on multiple occasions as it reached our maximum allowable position size of eight percent due to market appreciation.

Founded in 1916, Boeing is a global leader in the commercial and defense aerospace industries. Along with Airbus, Boeing is part of a global duopoly that accounts for almost all commercial planes sold with greater than 125 seats – the largest market segment. A holding since March 2020, Boeing’s financial results during the period were mixed and largely below consensus expectations from an income statement standpoint. However, shares responded positively to the company’s significantly improved free cash flow (FCF) generation and outlook for substantial further FCF growth. While the company has previously faced execution issues across several programs that temporarily paused aircraft deliveries, it is increasing production of both its 737 MAX and 787 Dreamliner models, and will resume production of the 777x earlier than anticipated, with expected entry into service in 2025. Despite the near-term challenges, we did not view the issues as structural and believed the long-term earnings power of the company remained unchanged and significantly underappreciated. Boeing has also made significant progress with the 737 MAX, which is now cleared to fly in almost all countries, including China. However, while over 90% of the MAX fleet in China is back in service, there has not been any concrete progress with respect to pending deliveries, and Boeing has remarked over one-third of planes originally earmarked for Chinese customers to other customers. We estimate that Boeing has approximately $38 billion of aircraft currently in inventory that will generate substantial revenue and cash flow as they are likely delivered over the next 12-to-24 months. As of June quarter-end, backlog of $440 billion, or approximately 4,900 aircraft, was up 18% year over year. Despite still uneven quarterly results, air traffic recovery is underway and absent further issues with the MAX and 787, we believe the company’s long-term earnings power remains intact. In the interim, Boeing’s financial results remain impacted by the decline in global air travel that began with Covid-19. At its low point in April 2020, travel demand, as measured by revenue passenger kilometer (RPK), which represents distance flown by paying passengers, had declined 94% from April 2019. And while demand year to date has returned to 89% of pre-pandemic levels, with domestic travel exceeding 2019 levels, international travel remains at 83%, due primarily to China. We believe the impact of Covid-19, along with the grounding of the MAX, the fourth generation of its most profitable airplane model, represented temporary, not structural, issues that created the opportunity to initiate our position. We believe Boeing’s strong and sustainable competitive advantages include its significant cumulative knowledge and experience in aeronautical development, scale, and a client base that faces switching costs due to plane-specific operational and maintenance issues, which collectively result in significant barriers to entry. Global growth in air travel is the primary secular growth driver for Boeing. Over our long-term investment horizon, we believe demand for global air travel will continue to grow at a mid-single-digit rate, as it has for the past four decades. We believe Boeing is one of only two companies globally which possess the requisite expertise and scale to profitably serve the global demand for commercial aircraft. We believe the current

Loomis Sayles Growth Fund

market price embeds expectations for aircraft deliveries and margins that are well below our long-term assumptions. As a result, we believe the company is selling at a significant discount to our estimate of intrinsic value and offers a compelling reward-to-risk opportunity. We took advantage of near-term price weakness to add to our position on several occasions during the year.

The Fund’s positions in PayPal, Walt Disney, and Illumina detracted the most from performance. Stock selection in the financials sector, along with our allocations in the information technology and financials sectors, detracted from relative performance.

PayPal is a leading technology platform that enables digital payments and simplifies commerce experiences on behalf of consumers and merchants, globally. The company operates a “two-sided” network that connects almost 400 million consumers with 35 million merchants across more than 200 markets around the world. The company provides its solutions through a family of brands that span several areas of payment solutions and include Braintree, Honey, Zettle, Venmo, and Xoom. While the majority of its transactions take place online, PayPal offers customers the ability to move money in digital form from any device when sending payments or getting paid. PayPal provides merchants with an end-to-end payments solution that provides authorization and settlement capabilities, as well as instant access to funds. A strategy holding since the first quarter of 2022, PayPal reported fundamentally solid financial results that were generally above or in-line with consensus expectations during the period. However, shares responded negatively to a modest reduction in the company’s target for year-end operating margin expansion, as well as lower-than-expected transaction margins in its most recent quarterly report. We believe the decline in margins was due to short-term factors that do not impact our structural investment thesis for the company. We took advantage of near-term price weakness to add to our position during the period. We believe PayPal’s strong and sustainable competitive advantages include its two-sided network, scale, and brand advantages. We believe the company’s biggest advantage is its rare two-sided network, which very few companies have been able to replicate. The network is sustained by the high value proposition offered to both consumers and merchants. Consumers benefit from a secure digital wallet that enables seamless checkout across devices, platforms, and merchants, along with solutions to manage and move money domestically and internationally, and access to credit and alternative payment solutions. Merchants benefit from the ability to enable all aspects of digital checkouts online and in store, as well as credit solutions, risk management and fraud prevention tools, and other value-added services to attract new customers and increase sales. As PayPal’s already massive two-sided network grows, we believe it becomes increasingly attractive to new participants, which we believe will enable the company to grow its digital checkout volumes from approximately 1.5% of global personal consumption expenditures today to approximately 3% over our long-term investment horizon. Collectively, we believe PayPal can generate compounded annual revenue growth in the low-double-digits. As the company continues to grow, we expect it will realize operating leverage in general and administrative, customer support, and operations expenses that will enable operating margins to expand. As a result, we expect operating profits and free cash flows will grow faster than revenues, in the low-to-mid teens. We believe the assumptions embedded in PayPal’s share price underestimate the company’s significant long-term growth opportunities and the sustainability of its business model. We believe the company’s shares currently sell at a significant discount to our estimate of intrinsic value and thereby offer a compelling reward-to-risk opportunity.

Founded almost 100 years ago, Disney is one of the largest and most renowned vertically integrated media companies in the world, with iconic entertainment brands and decades of film and TV content that it leverages across its media networks, theme parks, motion picture studios, and direct-to-consumer (DTC) businesses. A holding since the second quarter of 2020, Disney’s share price has been volatile over the past year due in part to activist investor campaigns, the surprise return of Bob Iger as CEO, greater than expected losses in the company’s DTC business, and continued weakness in linear networks. In the second half of the period, shares also responded negatively to lower-than-expected subscriptions to the company’s core Disney+ DTC platform, due in part to pricing increases implemented in the beginning of the year in North America (NA). The price hikes contributed to a modest decline in NA subscribers, but also to healthy growth in NA average revenue per user (ARPU). We believe the market continues to underappreciate the long-term opportunity for subscriber growth, pricing increases, and margin expansion in the company’s DTC platform. Globally, subscribers to its DTC streaming services declined 1% year over year, driven by subscriber declines at Disney Hotstar, where last year the company walked away from the digital rights to broadcast Indian Premiere League (IPL) cricket, which had been an important customer acquisition tool for the service. ARPU at Hotstar was over six-times lower than Disney’s core markets, and the company has been re-evaluating its level of investment spending in markets with lower profitability. Following the November 2019 launch of its Disney+ service, the company surpassed its five-year goal of attaining 130 million global subscribers in just 12 months, which we believe underscores the global appeal of its unique content and brands. Recently, operating losses of $512 million in the company’s DTC segment narrowed from $1.1 billion in the prior-year quarter, benefiting from price increases for both Disney+ and ESPN+, as well as lower content and marketing spending. We believe Disney’s strong and sustainable competitive advantages include its iconic brands, content, and intellectual property (IP), its massive scale in the media, entertainment, and leisure industries, and a structural cost advantage that directly benefits its streaming business. We believe the company is pursuing a well-articulated strategy to optimize distribution for its high-quality, best-in-class brands and franchises through a multi-pronged DTC approach that we believe will be central to the company’s media strategy over the next decade. Over our long-term investment horizon, we believe the company’s portfolio of iconic brands, its massive scale and geographic reach, and nearly impossible-to-replicate guest experiences, leave the company well positioned to benefit from secular growth in global entertainment spending. We believe current market expectations

Loomis Sayles Growth Fund

substantially underestimate the uniqueness of the company’s IP, the opportunity to monetize that IP across several global business segments, and its ability to generate sustainable growth in free cash flow. As a result we believe the shares trade at a substantial discount to our estimate of intrinsic value and offer a compelling reward-to-risk opportunity. We took advantage of near-term price weakness to add to our position on multiple occasions during the period.

Founded in 1998, Illumina is the industry leader in fast-growing field of sequencing for genetic and genomic analysis, supporting research, clinical, and consumer genetics applications. The company’s customers include leading genomic research centers, academic institutions, government laboratories, hospitals, pharmaceutical and biotechnology companies, commercial molecular diagnostic laboratories, and consumer genomics companies. Because genes determine cell function and characteristics, understanding genetic sequencing and variation can provide valuable information in fields ranging from disease treatment to crop optimization. A strategy holding since March 2020, Illumina’s shares have been pressured during the period due to lower-than-expected results in its core business, ongoing uncertainty regarding its acquisition of GRAIL, and an activist investor campaign that succeeded in ousting the Chairman of the Board and later prompted the resignation of CEO Francis DeSouza. The company did report strong orders for its newest sequencing platform, NovaSeq X, including over 260 orders from approximately 30 countries that led it to increase its full-year projected shipments. However, the company’s recent results and guidance are below our long-term expectations. While the launch of a new platform typically results in an initial slowdown in revenues as customers exhaust existing inventory while evaluating the new platform, we believe the company’s acquisition of GRAIL has detracted from near-term focus and returns. GRAIL was founded by Illumina in 2016 and was spun out as a standalone company in 2017, with Illumina retaining an equity interest that represented approximately 15% ownership. The company reacquired GRAIL in August 2021, but uncertainty remains as the company closed the transaction prior to receiving approval from the EU, which has since ordered that the business be divested. Illumina is challenging divestiture rulings from both the EU and FTC. We believe the legal challenges should conclude by the first quarter of 2024. GRAIL is an early leader in asymptomatic cancer screening through liquid biopsies, which utilize Illumina’s Next Generation Sequencing technology to detect tumor DNA in the bloodstream before it could otherwise be sampled via a traditional biopsy. To date, GRAIL has produced increasingly compelling data in support of its screening technology, and we believe continued reduction in sequencing costs is broadening the accessible market opportunity that we estimate to be in excess of $20 billion. We believe the combination with Illumina provides GRAIL with structural operating and distribution advantages relative to competitors that potentially position it to become the standard of care. And while realizing the acquisition’s potential will take substantial ongoing investment that will depress Illumina’s near-term financial results, we believe successful execution could yield significant value to Illumina. However, our structural investment thesis for Illumina is not premised on a successful completion of the GRAIL acquisition. While the process is likely to remain a distraction over the coming year, we believe Illumina’s core business remains highly attractive on a reward-to-risk basis and remains substantially discounted to intrinsic value regardless of the GRAIL outcome. As we do with all regulatory developments, we continue to monitor and assess any potential structural impact to our investment thesis for Illumina. The activist investor campaign was seeking three board seats. They succeeded in securing one seat while the Chairman, John Thompson, was voted off the board. About two weeks following the annual meeting, CEO Francis DeSouza submitted his resignation. The timing of the leadership turnover comes at an inopportune moment. Illumina is in the early stages of a major platform launch while simultaneously facing more competition than in recent years. They are also involved in legal disputes with regulators both home and abroad. Though this level of management uncertainty is not a desirable situation, we believe it presents an opportunity for the business to redouble its focus on the significant opportunity in its core markets and reinvigorate operational execution - which appears to have diminished over last several quarters under DeSouza. In September, the company named Jacob Thaysen, Ph.D. as its new CEO. Thaysen previously served as President of the Life Sciences and Applied Markets Group at Agilent, a well-regarded life sciences company. Jacob brings a background in research and development (R&D) as well as experience operating in genetics and clinical end markets. In addition to the activist sponsored candidate, Illumina also added two new board members with significant experience at innovative, market-expanding healthcare businesses that we believe should contribute positively to Illumina’s to return to growth. Despite the near term uncertainty, we believe Illumina remains advantageously positioned in a high quality industry benefitting from long-term, secular growth. We believe Illumina is at the forefront of a multi-decade transformation that will see genetic analysis incorporated into multiple facets of our lives. While demand today is still predominantly from large life sciences research facilities, over the next decade we believe democratization of gene sequencing technology and greater practical application will result in the equipment becoming ubiquitous in clinical settings as well, with oncology offering the largest market opportunity. We believe Illumina is a dominant competitor whose sequencing technology represents the critical enabling technology that ideally positions it to capitalize on an approximately $100 billion market opportunity. We believe Illumina’s shares embed expectations for key revenue and cash flow growth drivers that are well below our long-term assumptions. As a result, we believe the company is selling at a significant discount to our estimate of its intrinsic value and offers a compelling reward-to-risk opportunity. We added to our position on multiple occasions during the period.

All aspects of our quality-growth-valuation investment thesis must be present simultaneously for us to make an investment. Often our research is completed well in advance of the opportunity to invest. We are patient investors and maintain coverage of high-quality businesses in order to take advantage of meaningful price dislocations if and when they occur. During the period, we initiated a new

Loomis Sayles Growth Fund

positions in Thermo Fisher Scientific. We added to our existing holdings in Amazon, Block, Disney, Illumina, Meta Platforms, PayPal, and Tesla. We trimmed our existing positions in Deere, Monster Beverage, Novartis, Regeneron Pharmaceuticals, Roche, Vertex Pharmaceuticals, and Yum China. We also trimmed our positions in Meta Platforms and Nvidia as they reached our maximum allowable position size due to market appreciation.

Outlook

Our investment process is characterized by bottom-up, fundamental research and a long-term investment time horizon. The nature of the process leads to a lower-turnover portfolio in which sector positioning is the result of stock selection. As of September 30, we were overweight in the communication services, financials, healthcare, and industrials sectors and equal weight in the consumer discretionary sector. We were underweight in the information technology and consumer staples sectors. We held no positions in the real estate, energy, materials, or utilities sectors.

Top Ten Holdings as of September 30, 2023 |

| |

1 Meta Platforms, Inc., Class A | |

| |

| |

| |

| |

| |

| |

| |

9 Alphabet, Inc., Class A | |

| |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced. The holdings listed exclude any temporary cash investments, are presented on an individual security basis and do not represent holdings of the issuer. |

Loomis Sayles Growth Fund

Hypothetical Growth of $100,000 Investment in Class Y Shares1 |

September 30, 2013 through September 30, 2023 |

Loomis Sayles Growth Fund

Average Annual Total Returns — September 30, 20231 |

| | | | |

| | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

With 5.75% Maximum Sales Charge | | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

Russell 1000® Growth Index2 | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| Russell 1000® Growth Index is an unmanaged index that measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® Index companies with higher price-to-book ratios and higher forecasted growth values. |