1

Annual Report

Franklin India Growth Fund

Your Fund’s Goal and Main Investments: Franklin India Growth Fund seeks long-term capital appreciation by investing under normal market conditions at least 80% of its net assets in securities of “Indian companies,” which are defined as those organized under the laws of, with a principal office in, or for which the principal trading market for their securities is in India, that derive 50% or more of total revenue or profit from goods or services produced or sales made in India, or that have 50% or

more of their assets in India.1

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

This annual report for Franklin India Growth Fund covers the fiscal year ended October 31, 2012.

Performance Overview

Franklin India Growth Fund – Class A had a -6.02% cumulative total return for the fiscal year ended October 31, 2012. The Fund underperformed the -4.73% total return of the benchmark MSCI India Index, which is designed to measure stock market performance in India.2 You can find more of the Fund’s performance data in the Performance Summary beginning on page 7.

Economic and Market Overview

India’s economy expanded at a modest pace during the review period. Real gross domestic product growth averaged 5.9% over the four quarters ended June 2012, compared to an annualized expansion rate of 8.3% over the five years ended December 2011.3 Weak investment spending and tight monetary policy stifled growth, which was visibly slower in the industrial and infrastructure sectors, mainly because of limited central bank policy options and a slowdown in project approvals. News reports and investors focused for most of the year on many of the near-term headwinds.

1. The Fund currently invests indirectly in Indian companies through FT (Mauritius) Offshore Investments Limited, a wholly owned, collective investment vehicle registered in the Republic of Mauritius.

2. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

3. Source: Ministry of Statistics and Programme Implementation.

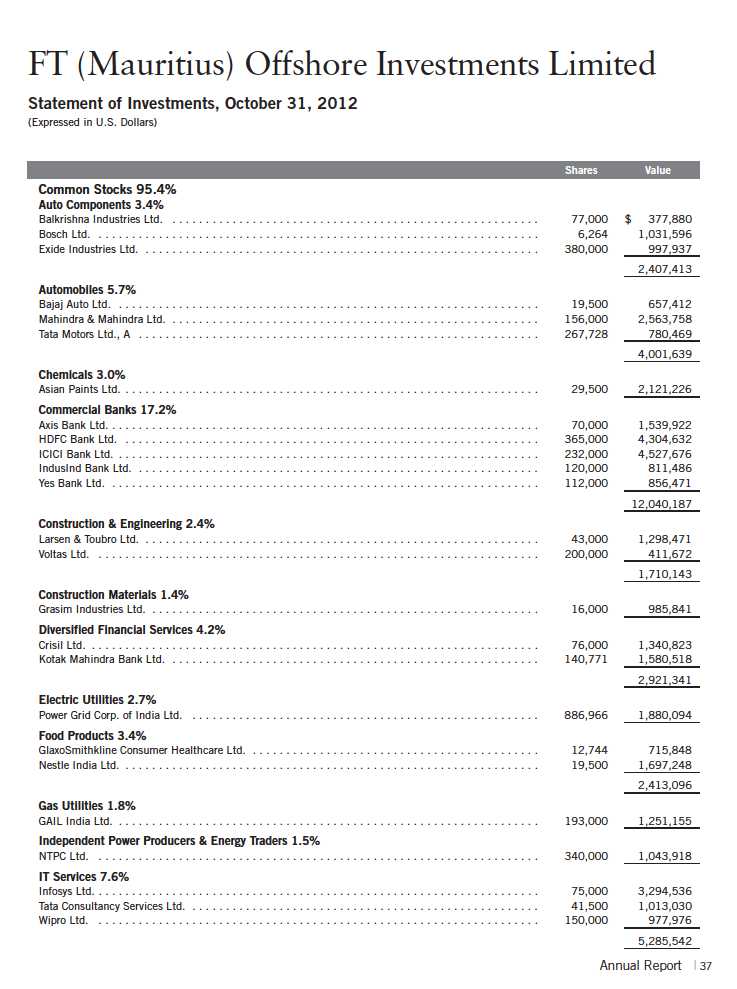

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 16.

Annual Report | 3

Despite the country’s moderating growth rate, the Reserve Bank of India maintained a cautious monetary policy stance. The central bank cut its benchmark policy rate 50 basis points in April 2012 to 8% from 8.50%, but has since refrained as inflation levels remained elevated. More importantly, the bank has been concerned about a high fiscal deficit and widening current account gap. The central bank has, however, reduced reserve requirements for banks to boost systemic liquidity and promote credit flow to productive sectors of the economy. This move helped corporate borrowing costs ease from peaks.

A key positive factor throughout the period was Indian corporations’ sustained strength. Although many Indian companies continued to report reasonably strong revenue growth, higher input and borrowing costs weighed on profitability. However, third quarter 2012 earnings data suggested margin pressures were peaking amid easing borrowing costs and raw material prices.

In September 2012, the government stepped up policy action and announced measures focused on boosting foreign capital investment and managing the fiscal deficit. The improved policy environment helped local equity markets and the rupee rebound. Strong foreign portfolio inflows also supported Indian stocks as a fresh round of stimulus from key developed market central banks and receding eurozone worries boosted global investor risk appetite. In terms of sectors, consumer staples and health care stocks generally outperformed broad markets during the period, while the metal and energy sectors declined in value.

Investment Strategy

We are research-driven, fundamental investors pursuing a growth strategy. As bottom-up investors focusing primarily on individual securities, we seek to invest in companies whose current market price, in our opinion, does not reflect future growth prospects. We choose companies that have identifiable drivers of future earnings growth and that present, in our opinion, the best trade-off between earnings growth potential, business and financial risk, and valuation. We rely on a team of analysts to help provide in-depth industry expertise and use both qualitative and quantitative analyses to evaluate companies for distinct and sustainable competitive advantages through leading-edge products, intellectual property, product positioning, unique market niches, brand identity, solid management teams, strong balance sheets, above-average or rising margins, and strong returns on capital invested in the business. In choosing equity investments, we also consider such factors as the company’s financial strength, management’s expertise, the company’s growth potential within the industry, and the industry’s growth potential.

4 | Annual Report

Manager’s Discussion

Our overall strategy has been to build a diversified portfolio covering the full market capitalization spectrum of companies we believe are well positioned to take advantage of Indian economic growth. The Fund has focused on companies that have been delivering growth across market cycles and benefiting from India’s structural growth drivers, consumption and investment.

The Fund’s absolute performance during the period was bolstered by gains from financials and industrials holdings.4 The top individual contributors to performance over the 12-month period included private banking firm HDFC Bank, personal care products company Marico and machinery firm Cummins India. HDFC Bank’s strong, low-cost deposit base and good asset quality profile helped the company maintain robust earnings. Hopes surrounding monetary easing also helped the stock rally along with other financial companies.

A combination of factors helped Marico stock appreciate during the period under review, including investor preference for defensive sectors such as consumer staples with a strong earnings profile. In addition, the firm purchased the personal care portfolio of Paras Pharmaceuticals in an effort to lay the foundation for the next level of growth. Strong demand for Cummins power generation equipment, along with stringent focus on costs, helped the company do well relative to its peers and benefited Fund performance.

In contrast, the Fund’s performance was hampered by declines for certain telecommunication services and information technology (IT) holdings.5 Regulatory issues continued to weigh on telecommunication stocks, and a slowdown in target markets dampened growth momentum for Indian IT services companies. As a result, wireless telecommunications industry leader Bharti Airtel and IT services firm Infosys were among the Fund’s largest detractors.

Reliance Industries’ stock price also declined. The company is one of India’s largest conglomerates with interests in upstream (exploration, development and production) oil and gas, refining and related petrochemicals. Reliance experienced issues with raising output at its key gas production block in the Krishna-Godavari basin. Notwithstanding the recent declines, at period-end these detractors remained among our favored long-term positions, and we believe their underlying fundamentals remain robust.

4. The financials sector comprises commercial banks and diversified financial services in the SOI. The industrials sector comprises construction and engineering, machinery and transportation infrastructure in the SOI.

5. The telecommunication services sector comprises wireless telecommunication services in the SOI. The IT sector comprises IT services in the SOI.

Annual Report | 5

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the 12 months ended October 31, 2012, the U.S. dollar rose in value relative to the Indian rupee. As a result, the Fund’s performance was negatively affected by the portfolio’s investment predominantly in securities denominated in the Indian rupee.

Thank you for your continued participation in Franklin India Growth Fund.

We look forward to serving your future investment needs.

6 | Annual Report

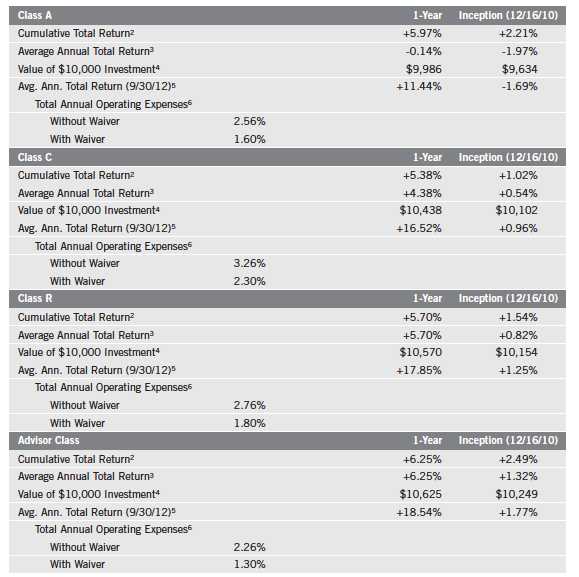

Performance Summary as of 10/31/12

Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table and graphs do not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses.

Annual Report | 7

Performance Summary (continued)

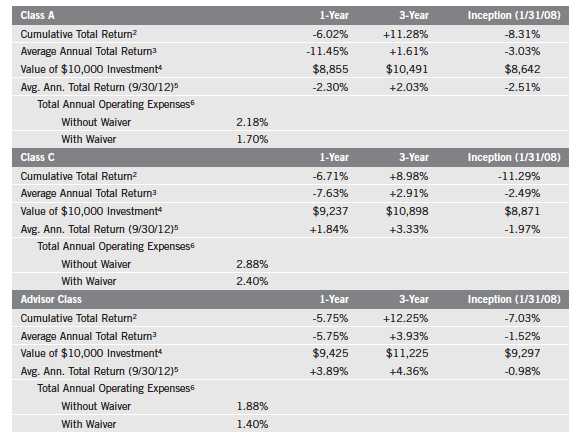

Performance1

Cumulative total return excludes sales charges. Average annual total returns and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class C: 1% contingent deferred sales charge in first year only; Advisor Class: no sales charges.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to franklintempleton.com or call (800) 342-5236.

The investment manager and administrator have contractually agreed to waive or assume certain expenses so that the common expenses (including the expenses of FT (Mauritius) Offshore Investments Limited but excluding Rule 12b-1 fees) for each class of the Fund do not exceed 1.40% (other than certain nonroutine expenses) until 2/28/13.

8 | Annual Report

Performance Summary (continued)

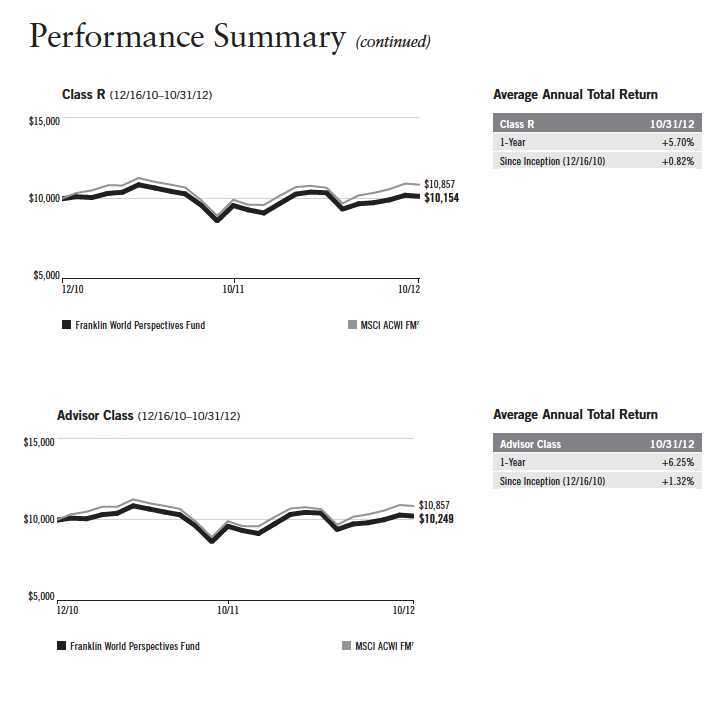

Total Return Index Comparison for a Hypothetical $10,000 Investment1

Total return represents the change in value of an investment over the periods shown. It includes any applicable maximum sales charge, Fund expenses, account fees and reinvested distributions. The unmanaged index includes reinvestment of any income or distributions. It differs from the Fund in composition and does not pay management fees or expenses. One cannot invest directly in an index.

Annual Report | 9

10 | Annual Report

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs:

- Transaction costs, including sales charges (loads) on Fund purchases; and

- Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

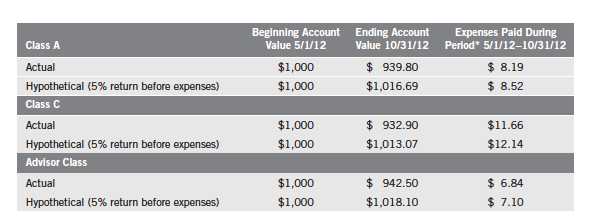

The following table shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and expenses. The “Ending Account Value” is derived from the Fund’s actual return, which includes the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course, your account value and expenses will differ from those in this illustration:

| 1. | Divide your account value by $1,000. |

| | If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6. |

| 2. | Multiply the result by the number under the heading “Expenses Paid During Period.” |

| | If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50. |

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare ongoing costs of investing in the Fund with those of other mutual funds. This information may not be used to estimate the actual ending account balance or expenses you paid during the period. The hypothetical “Ending Account Value” is based on the actual expense ratio for each class and an assumed 5% annual rate of return before expenses, which does not represent the Fund’s actual return. The figure under the heading “Expenses Paid During Period” shows the hypothetical expenses your account would have incurred under this scenario. You can compare this figure with the 5% hypothetical examples that appear in shareholder reports of other funds.

Annual Report | 11

Your Fund’s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

*Expenses are calculated using the most recent six-month expense ratio, net of expense waivers, annualized for each class (A: 1.68%; C: 2.40%; and Advisor: 1.40%), multiplied by the average account value over the period, multiplied by 184/366 to reflect the one-half year period.

12 | Annual Report

Franklin Templeton International Trust

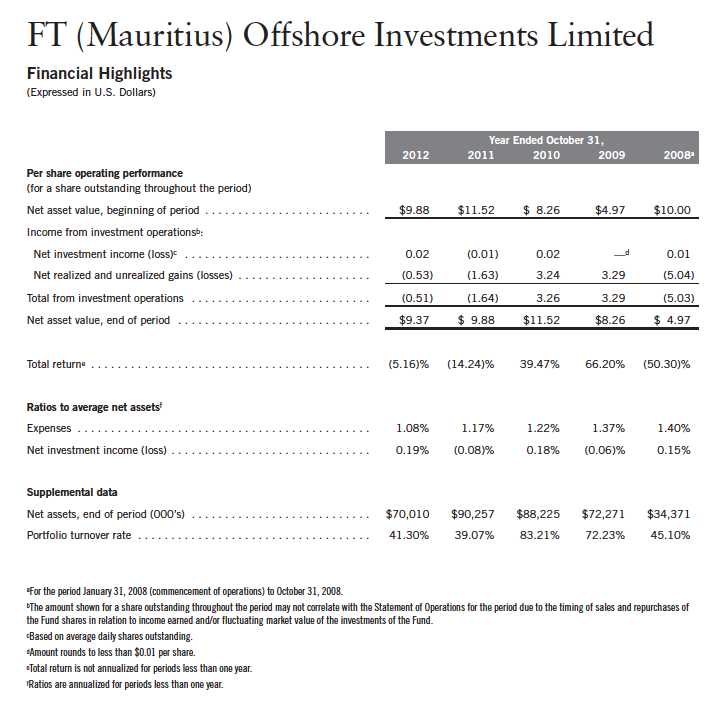

Financial Highlights

Annual Report | The accompanying notes are an integral part of these financial statements. | 13

Franklin Templeton International Trust

Financial Highlights (continued)

14 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Templeton International Trust

Financial Highlights (continued)

Annual Report | The accompanying notes are an integral part of these financial statements. | 15

Franklin Templeton International Trust

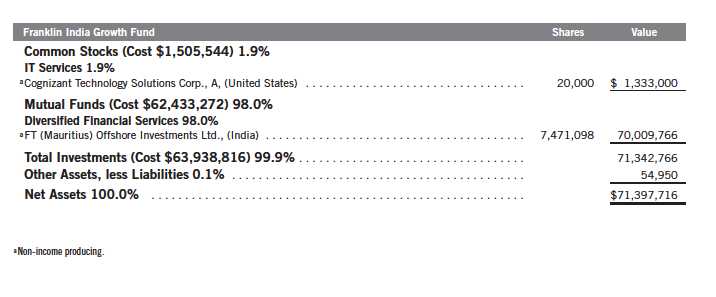

Statement of Investments, October 31, 2012

16 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Templeton International Trust

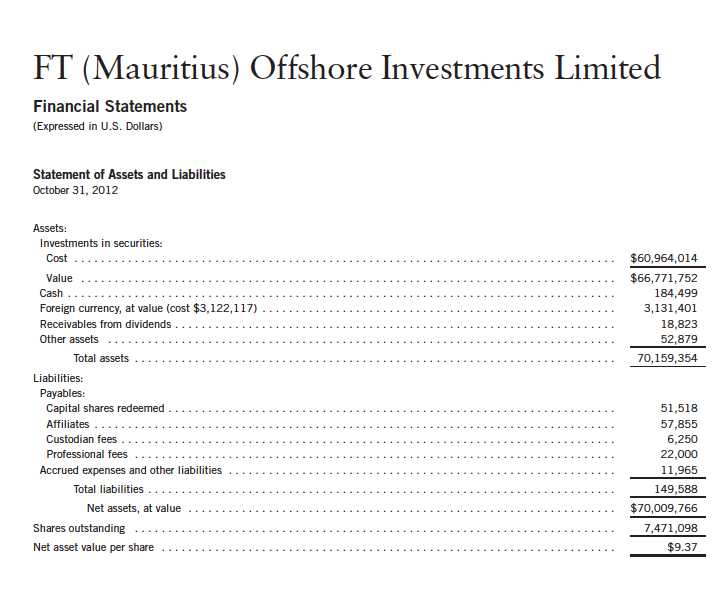

Financial Statements

aRedemption price is equal to net asset value less contingent deferred sales charges, if applicable.

Annual Report | The accompanying notes are an integral part of these financial statements. | 17

Franklin Templeton International Trust

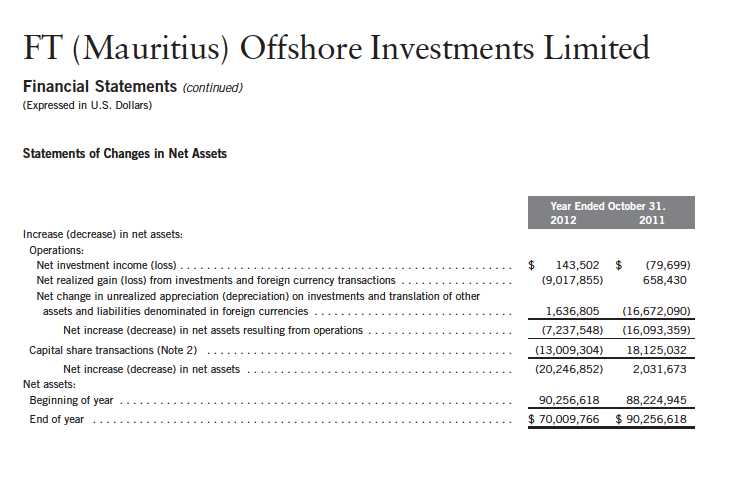

Financial Statements (continued)

18 | The accompanying notes are an integral part of these financial statements. | Annual Report

Franklin Templeton International Trust

Financial Statements (continued)

Annual Report | The accompanying notes are an integral part of these financial statements. | 19

Franklin Templeton International Trust

Notes to Financial Statements

Franklin India Growth Fund

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

Franklin Templeton International Trust (Trust) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as an open-end investment company, consisting of four separate funds. The Franklin India Growth Fund (Fund) is included in this report. The financial statements of the remaining funds in the Trust are presented separately. The Fund offers three classes of shares: Class A, Class C, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, distribution fees, voting rights on matters affecting a single class and its exchange privilege.

The Fund operates using a “master fund/feeder fund” structure and primarily invests indirectly in the securities of Indian companies through FT (Mauritius) Offshore Investments Limited (Portfolio), an entity registered with and regulated by the Mauritius Financial Services Commission, which shares the same investment objective as the Fund. The accounting policies of the Portfolio, including the Portfolio’s security valuation policies, will directly affect the recorded value of the Fund’s investment in the Portfolio. The financial statements of the Portfolio, including the Statement of Investments, are included elsewhere in this report and should be read in conjunction with the Fund’s financial statements. At October 31, 2012, the Fund owned 100% of the outstanding shares of the Portfolio.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Trustees (the Board), the Fund’s administrator, investment manager and other affiliates have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Over-the-counter (OTC) securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities.

20 | Annual Report

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

The Fund has procedures to determine the fair value of financial instruments for which market prices are not reliable or readily available. Under these procedures, the VLOC convenes on a regular basis to review such financial instruments and considers a number of factors, including significant unobservable valuation inputs, when arriving at fair value. The VLOC primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. An income-based valuation approach may also be used in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. The VLOC employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis, and reviews of any related market activity.

The Fund’s investment in the Portfolio shares is valued at the Portfolio’s net asset value per share. Valuation of securities by the Portfolio is discussed in Note 1(a) of the Portfolio’s Notes to Financial Statements, which are included elsewhere in this report.

b. Income Taxes

It is the Fund’s policy to qualify as a regulated investment company under the Internal Revenue Code. The Fund intends to distribute to shareholders substantially all of its taxable income and net realized gains to relieve it from federal income and excise taxes. As a result, no provision for U.S. federal income taxes is required.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is “more likely than not” to be sustained upon examination by the tax authorities based on the technical merits of the tax position. As of October 31, 2012, and for all open tax years, the Fund has determined that no liability for unrecognized tax benefits is required in the Fund’s financial statements related to uncertain tax positions taken on a tax return (or expected to be taken on future tax returns). Open tax years are those that remain subject to examination and are based on each tax jurisdiction statute of limitation.

The Fund’s investment in the Portfolio may be subject to income and withholding taxes in Mauritius and/or India which are discussed in Note 1(c) of the Portfolio’s Notes to Financial Statements.

Annual Report | 21

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| c. | Security Transactions, Investment Income, Expenses and Distributions |

Security transactions, including investments in the Portfolio, are accounted for on trade date. Realized gains and losses on security transactions are determined on a specific identification basis. Estimated expenses are accrued daily. Dividend income is recorded on the ex-dividend date. Distributions to shareholders are recorded on the ex-dividend date and are determined according to income tax regulations (tax basis). Distributable earnings determined on a tax basis may differ from earnings recorded in accordance with accounting principles generally accepted in the United States of America. These differences may be permanent or temporary. Permanent differences are reclassified among capital accounts to reflect their tax character. These reclassifications have no impact on net assets or the results of operations. Temporary differences are not reclassified, as they may reverse in subsequent periods.

Common expenses incurred by the Trust are allocated among the funds based on the ratio of net assets of each fund to the combined net assets of the Trust. Fund specific expenses are charged directly to the fund that incurred the expense.

Realized and unrealized gains and losses and net investment income, not including class specific expenses, are allocated daily to each class of shares based upon the relative proportion of net assets of each class. Differences in per share distributions, by class, are generally due to differences in class specific expenses.

The Fund records its proportionate share of the Portfolio’s income, expenses and realized and unrealized gains and losses daily. In addition, the Fund accrues its own expenses.

d. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

e. Guarantees and Indemnifications

Under the Trust’s organizational documents, its officers and directors are indemnified by the Trust against certain liabilities arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust, on behalf of the Fund, enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred. Currently, the Trust expects the risk of loss to be remote.

22 | Annual Report

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

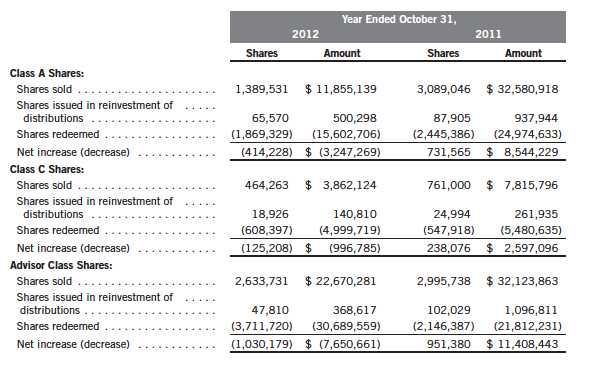

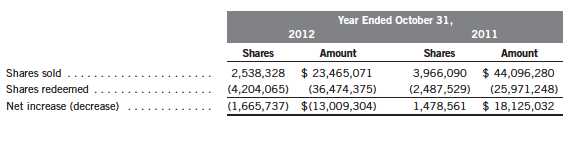

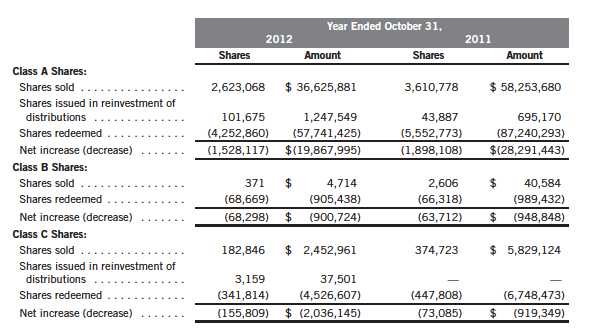

2. SHARES OF BENEFICIAL INTEREST

At October 31, 2012, there were an unlimited number of shares authorized (without par value).

Transactions in the Fund’s shares were as follows:

3. TRANSACTIONS WITH AFFILIATES

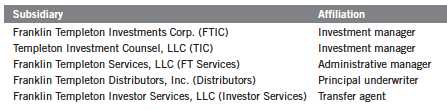

Franklin Resources, Inc. is the holding company for various subsidiaries that together are referred to as Franklin Templeton Investments. Certain officers and trustees of the Trust are also officers and/or directors of the Portfolio and of the following subsidiaries:

Annual Report | 23

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

| 3. | TRANSACTIONS WITH AFFILIATES (continued) |

| a. | Management Fees |

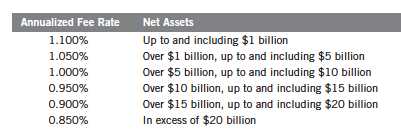

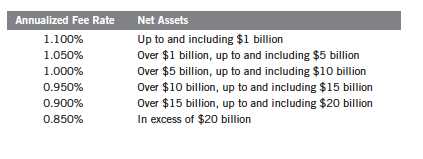

The Fund pays an investment management fee to Advisers equal to 20% of the total management fee with the remainder to be paid by the Portfolio. The total management fee is paid based on the average daily net assets of the Fund as follows:

Under a subadvisory agreement, FT India, an affiliate of Advisers, provides subadvisory services to the Fund. The subadvisory fee is paid by Advisers based on the average daily net assets, and is not an additional expense of the Fund.

b. Administrative Fees

The Fund pays an administrative fee to FT Services of 0.20% per year of the average daily net assets of the Fund.

c. Distribution Fees

The Board has adopted distribution plans for each share class, with the exception of Advisor Class shares, pursuant to Rule 12b-1 under the 1940 Act. Distribution fees are not charged on shares held by affiliates. Under the Fund’s Class A reimbursement distribution plan, the Fund reimburses Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate. Under the Class A reimbursement distribution plan, costs exceeding the maximum for the current plan year cannot be reimbursed in subsequent periods. In addition, under the Fund’s Class C compensation distribution plan, the Fund pays Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate.

The maximum annual plan rates, based on the average daily net assets, for each class, are as follows:

The Board has set the current rate at 0.30% per year for Class A shares until further notice and approval by the Board.

24 | Annual Report

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

| 3. | TRANSACTIONS WITH AFFILIATES (continued) |

| d. | Sales Charges/Underwriting Agreements |

Front-end sales charges and contingent deferred sales charges (CDSC) do not represent expenses of the Fund. These charges are deducted from the proceeds of sales of Fund shares prior to investment or from redemption proceeds prior to remittance, as applicable. Distributors has advised the Fund of the following commission transactions related to the sales and redemptions of the Fund’s shares for the year:

e. Transfer Agent Fees

For the year ended October 31, 2012, the Fund paid transfer agent fees of $172,468, of which $92,047 was retained by Investor Services.

f. Waiver and Expense Reimbursements

Advisers and FT Services have contractually agreed in advance to waive or limit their respective fees and to assume as their own expense certain expenses otherwise payable by the Fund so that the common expenses (i.e. a combination of management fees, administrative fees, transfer agent fees, and other expenses, including the Fund’s share of the Portfolio’s allocated expenses, but excluding distribution fees, and acquired fund fees and expenses) for each class of the Fund do not exceed 1.40% (other than certain non-routine expenses or costs, including those relating to litigation, indemnification, reorganizations, and liquidations) until February 28, 2013.

4. EXPENSE OFFSET ARRANGEMENT

The Fund has entered into an arrangement with its custodian whereby credits realized as a result of uninvested cash balances are used to reduce a portion of the Fund’s custodian expenses. During the year ended October 31, 2012, there were no credits earned.

5. INCOME TAXES

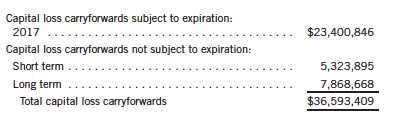

For tax purposes, capital losses may be carried over to offset future capital gains, if any. Under the Regulated Investment Company Modernization Act of 2010, capital losses incurred by the Fund in taxable years beginning after December 22, 2010 are not subject to expiration and such

Annual Report | 25

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

5. INCOME TAXES (continued)

losses retain their character as short-term or long-term. At October 31, 2012, capital loss carry-forwards were as follows:

For tax purposes, the Fund may elect to defer any portion of a late-year ordinary loss to the first day of the following fiscal year. At October 31, 2012, the Fund deferred late-year ordinary losses of $127,609.

The tax character of distributions paid during the years ended October 31, 2012 and 2011, was as follows:

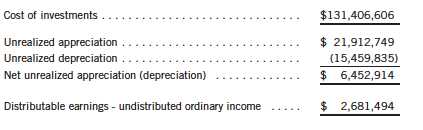

At October 31, 2012, the cost of investments, net unrealized appreciation (depreciation), including the holdings of the Portfolio for income tax purposes were as follows:

The Portfolio is a disregarded entity for United States Federal income tax purposes.

Differences between income and/or capital gains as determined on a book basis and a tax basis are primarily due to differing treatments of foreign currency transactions, non-deductible expenses, organization costs and wash sales.

6. INVESTMENT TRANSACTIONS

Purchases and sales of investments including transactions from the Portfolio (excluding short term securities) for the year ended October 31, 2012, aggregated $29,140,205 and $38,237,753, respectively.

26 | Annual Report

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

7. CONCENTRATION OF RISK

Investing in Indian equity securities through the Portfolio may include certain risks and considerations not typically associated with investing in U.S. securities, such as fluctuating currency values, less liquidity, expropriation, confiscatory taxation, nationalization, exchange control regulations (including currency blockage), differing legal standards and changing local and regional economic, political and social conditions, which may result in greater market volatility.

8. CREDIT FACILITY

The Fund, together with other U.S. registered and foreign investment funds (collectively, Borrowers), managed by Franklin Templeton Investments, are borrowers in a joint syndicated senior unsecured credit facility totaling $1.5 billion (Global Credit Facility) which matures on January 18, 2013. This Global Credit Facility provides a source of funds to the Borrowers for temporary and emergency purposes, including the ability to meet future unanticipated or unusually large redemption requests.

Under the terms of the Global Credit Facility, the Fund shall, in addition to interest charged on any borrowings made by the Fund and other costs incurred by the Fund, pay its share of fees and expenses incurred in connection with the implementation and maintenance of the Global Credit Facility, based upon its relative share of the aggregate net assets of all of the Borrowers, including an annual commitment fee of 0.08% based upon the unused portion of the Global Credit Facility, which is reflected in other expenses on the Statement of Operations. During the year ended October 31, 2012, the Fund did not use the Global Credit Facility.

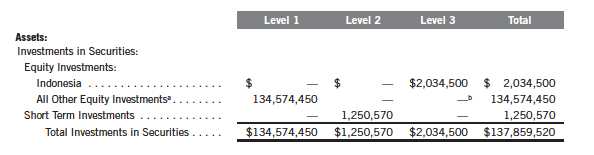

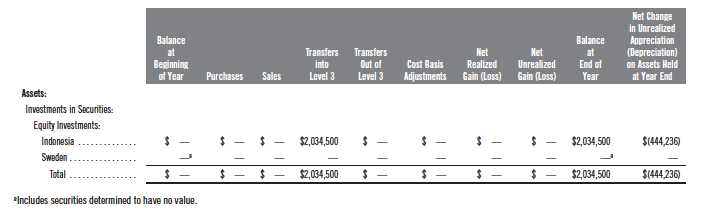

9. FAIR VALUE MEASUREMENTS

The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund’s financial instruments and are summarized in the following fair value hierarchy:

- Level 1 – quoted prices in active markets for identical financial instruments

- Level 2 – other significant observable inputs (including quoted prices for similar financial instruments, interest rates, prepayment speed, credit risk, etc.)

- Level 3 – significant unobservable inputs (including the Fund’s own assumptions in deter- mining the fair value of financial instruments)

The inputs or methodology used for valuing financial instruments are not an indication of the risk associated with investing in those financial instruments.

Annual Report | 27

Franklin Templeton International Trust

Notes to Financial Statements (continued)

Franklin India Growth Fund

9. FAIR VALUE MEASUREMENTS (continued)

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

At October 31, 2012, all of the Fund’s investments in financial instruments and in financial instruments through the Portfolio carried at fair value were valued using Level 1 inputs. For detailed categories, see the accompanying Statement of Investments.

10. NEW ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2011-11, Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities. The amendments in the ASU enhance disclosures about offsetting of financial assets and liabilities to enable investors to understand the effect of these arrangements on a fund’s financial position. The ASU is effective for interim and annual reporting periods beginning on or after January 1, 2013. The Fund believes the adoption of this ASU will not have a material impact on its financial statements.

11. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the issuance of the financial statements and determined that no events have occurred that require disclosure.

28 | Annual Report

Franklin Templeton International Trust

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of Franklin India Growth Fund

In our opinion, the accompanying statement of assets and liabilities, including the statement of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Franklin India Growth Fund (the “Fund”) at October 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2012 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

December 17, 2012

Annual Report | 29

Franklin Templeton International Trust

Tax Information (unaudited)

Franklin India Growth Fund

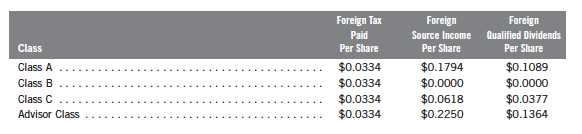

Under Section 852(b)(3)(C) of the Internal Revenue Code (Code), the Fund hereby reports the maximum amount allowable but no less than $1,085,215 as a long term capital gain dividend for the fiscal year ended October 31, 2012.

Under Section 854(b)(1)(B) of the Code, the Fund hereby reports the maximum amount allowable but no less than $748,567 as qualified dividends for purposes of the maximum rate under Section 1(h)(11) of the Code for the fiscal year ended October 31, 2012. Distributions, including qualified dividend income, paid during calendar year 2012 will be reported to shareholders on Form 1099-DIV by mid-February 2013. Shareholders are advised to check with their tax advisors for information on the treatment of these amounts on their individual income tax returns.

30 | Annual Report

Franklin Templeton International Trust

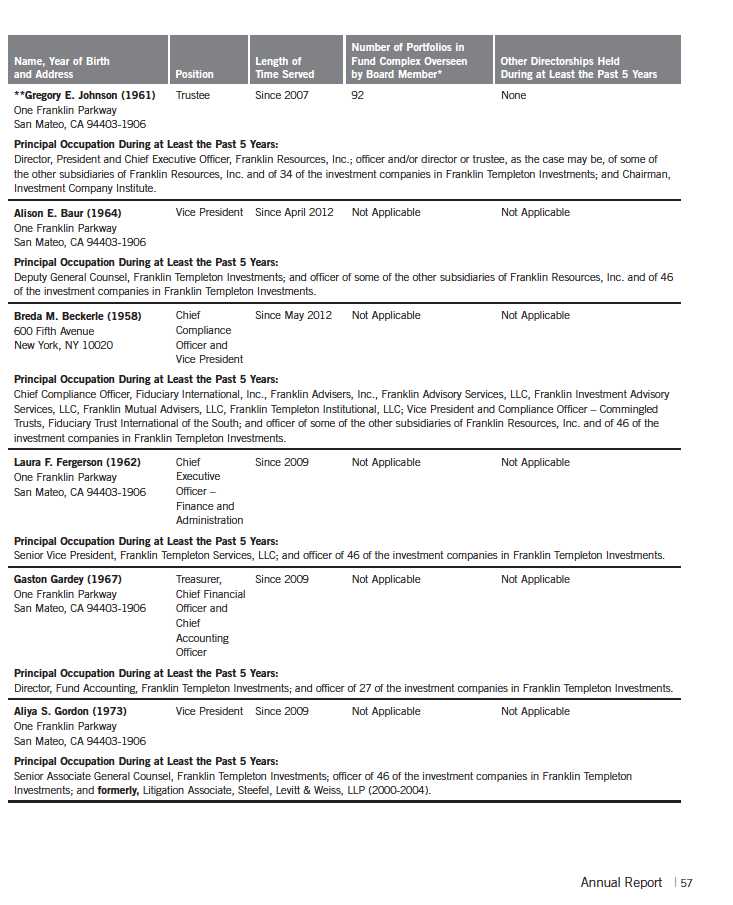

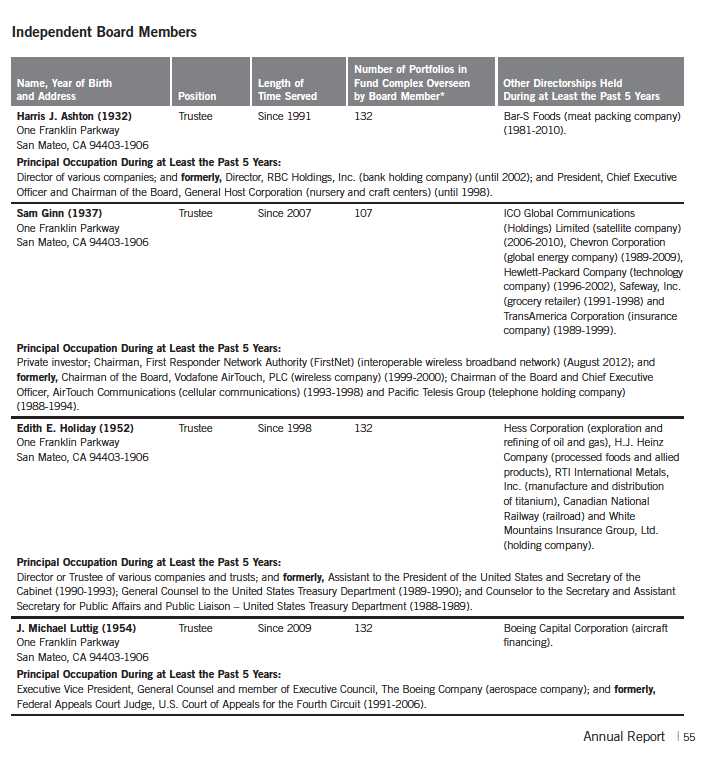

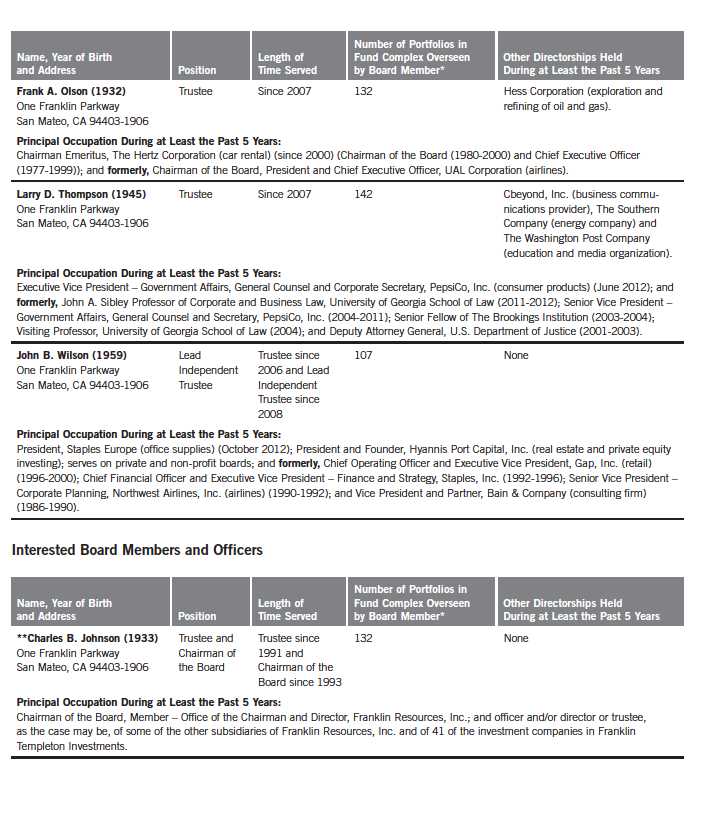

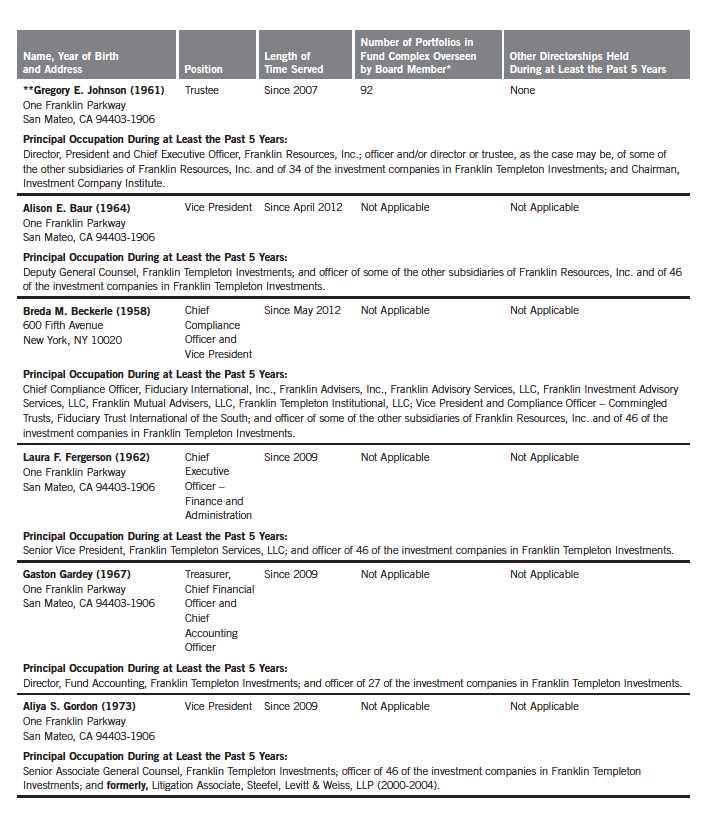

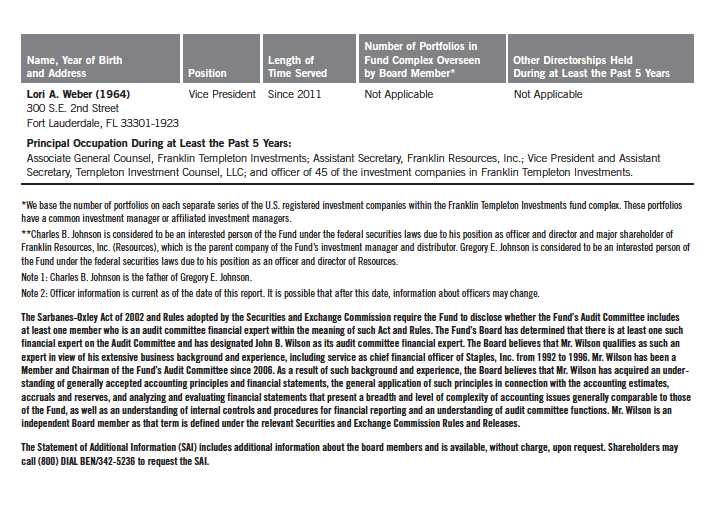

Board Members and Officers

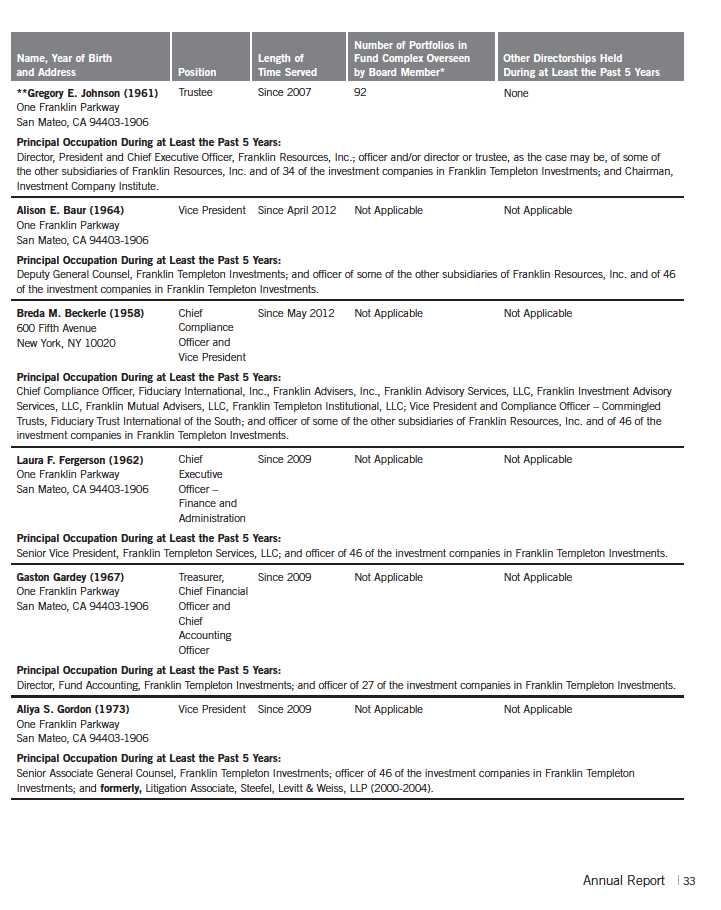

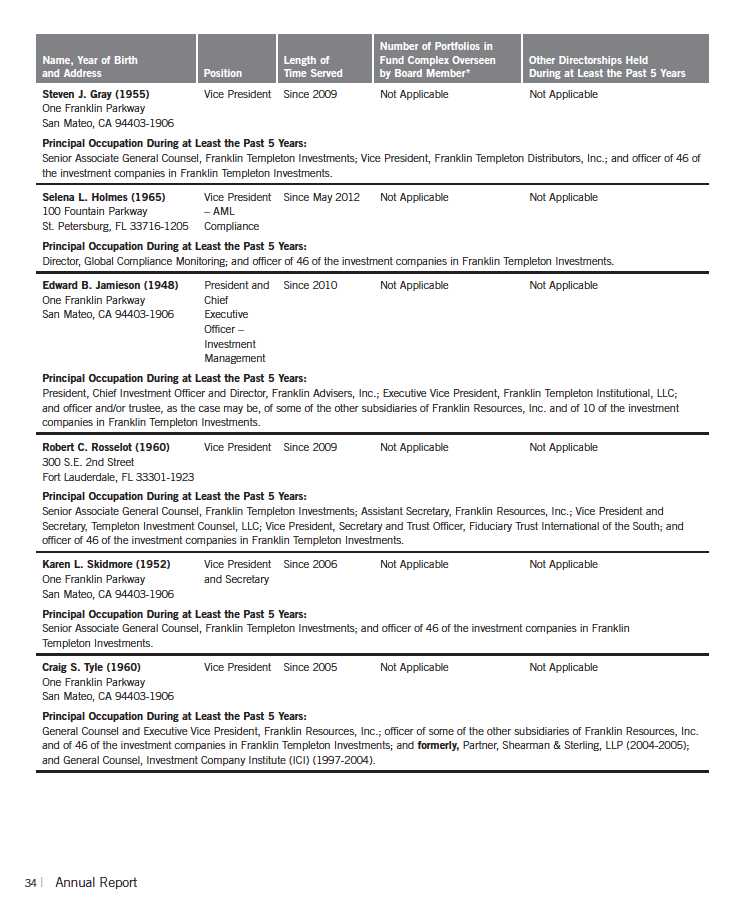

The name, year of birth and address of the officers and board members, as well as their affiliations, positions held with the Trust, principal occupations during at least the past five years and number of portfolios overseen in the Franklin Templeton Investments fund complex are shown below. Generally, each board member serves until that person’s successor is elected and qualified.

32 | Annual Report

Annual Report | 35

36 | The accompanying notes are an integral part of these financial statements. | Annual Report

38 | The accompanying notes are an integral part of these financial statements. | Annual Report

Annual Report | The accompanying notes are an integral part of these financial statements. | 39

40 | The accompanying notes are an integral part of these financial statements. | Annual Report

Annual Report | The accompanying notes are an integral part of these financial statements. | 41

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements

(Expressed in U.S. Dollars)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

FT (Mauritius) Offshore Investments Limited (Portfolio) is registered with and regulated by the Mauritius Financial Services Commission. The Portfolio was formed for the purpose of facilitating the Franklin India Growth Fund’s (Fund) purchase of securities of a wide selection of Indian companies, consistent with the Fund’s investment strategies and has elected to be treated as a disregarded entity for United States federal income tax purposes.

At October 31, 2012, the Fund owned 100% of the Portfolio.

The following summarizes the Portfolio’s significant accounting policies.

a. Financial Instrument Valuation

The Portfolio’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Trustees (the Board), the Fund’s administrator, investment manager and other affiliates have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Portfolio’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Portfolio to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter (OTC) securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities.

The Portfolio follows the Fund’s procedures to determine the fair value of financial instruments for which market prices are not reliable or readily available. Under these procedures, the VLOC convenes on a regular basis to review such financial instruments and considers a number of factors, including significant unobservable valuation inputs, when arriving at fair value. The VLOC primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. An income-based valuation approach may also be used in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such

42 | Annual Report

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

investments, the fair values may differ significantly from the values that would have been used had an active market existed. The VLOC employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis, and reviews of any related market activity.

Trading in securities on foreign securities stock exchanges and OTC markets may be completed before the daily close of business on the NYSE. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Portfolio. As a result, differences may arise between the value of the Portfolio’s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the VLOC monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depositary Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for each specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Portfolio. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

b. Foreign Currency Translation

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Portfolio may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Portfolio securities and assets and liabilities denominated in foreign currencies contain risks that those currencies will decline in value relative to the U.S. dollar. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by the Board.

The Portfolio does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments on the Statement of Operations.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and

Annual Report | 43

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| b. | Foreign Currency Translation (continued) |

the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

c. Income Taxes

The Portfolio conducts its investment activities in India as a tax resident of Mauritius and expects to obtain benefits under the double taxation treaty between Mauritius and India (Treaty). To obtain benefits under the Treaty, the Portfolio must meet certain tests and conditions, including the establishment of Mauritius tax residence and related requirements. The Portfolio has obtained a certificate from the Mauritius tax authorities and believes that such certification is evidence that it is a resident of Mauritius under the Treaty. A company which is a tax resident in Mauritius under the Treaty and has no branch or permanent establishment in India, will not be subject to capital gains tax in India on the sale of Indian securities but is subject to Indian withholding tax on interest earned on Indian securities at the rate of 21.012% (which includes surcharges). There is no withholding tax in India in respect of dividends paid by Indian companies and such dividends are exempt in the hands of the shareholders.

The Portfolio holds a Category 1 Global Business License for the purpose of the Financial Services Act 2007 and under current laws and regulations, is subject to tax in Mauritius at the rate of 15% on its net income. However, the Portfolio is entitled to a deemed tax credit equivalent to the higher of actual foreign tax suffered or a presumed foreign tax equivalent of 80% of the Mauritian tax on its foreign source income. Thus, the effective tax rate in Mauritius should not exceed 3% (i.e. 15% less 80% of 15%). Indian companies making distributions are, however, liable to a dividend distribution tax equivalent to 16.225% of the dividends distributed. A company holding at least 5% of the share capital of an Indian company and receiving dividends from that Indian company may claim a credit for tax paid by the Indian company on its profits out of which the dividends were distributed including the dividend distribution tax. No Mauritian capital gains tax is payable on profits arising from sale of securities, and any dividends and redemption proceeds paid by the Portfolio to its shareholders will be exempt from withholding or other tax.

The Portfolio continues to: (i) comply with the requirements of the Treaty; (ii) be a tax resident of Mauritius; and (iii) maintain that its central management and control resides in Mauritius, and therefore management believes that the Portfolio will be able to obtain the benefits of the Treaty. Accordingly, no provision for Indian income taxes has been made in the accompanying financial statements of the Portfolio for taxes related to capital gains or dividends.

44 | Annual Report

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| c. | Income Taxes (continued) |

The Indian Finance Minister announced the introduction of a General Anti Avoidance Rule (“GAAR”) in the Indian tax law in the 2012/2013 budget. Subsequently, following representations made by stakeholders, the implementation of the GAAR provisions has been deferred until April 1, 2013. A Committee has also been constituted by the Indian government to produce a set of rules and guidelines (Guidelines) with a view to providing clarity and certainty on the application of GAAR. Draft Guidelines and the Shome Report have since been issued, with a view to analyzing, finalizing and bringing more clarity to the GAAR provisions. In particular, it is noteworthy that the Shome Report has recommended that GAAR provisions should not be invoked to examine the genuineness of the residency of entities in Mauritius. However, as the reports are still under consideration, management is not in a position to assess the implications of any GAAR provisions on the Portfolio, including any potential Indian capital gains tax claim in 2013 until such time a formal stand is taken by the Government of India.

The Portfolio’s accounting policy in accordance with accounting principles generally accepted in the United States of America (U.S. GAAP) is to account for changes in tax laws when the laws are enacted.

The India tax law also includes provisions that impose tax on certain transfers of shares of non-Indian companies that substantially derive their value from Indian assets. Uncertainty exists with respect to the application of this law on investment structures such as the Portfolio and the Fund. However, based on judgment and analysis of the facts and circumstances, management currently believes that the provisions are not likely to have a material impact on the Portfolio and the Fund.

d. Security Transactions, Investment Income and Expenses

Security transactions are accounted for on trade date. Realized gains and losses on security transactions are determined on a specific identification basis. Estimated expenses are accrued daily. Dividend income is recorded on the ex-dividend date except that certain dividends from foreign securities are recognized as soon as the Portfolio is notified of the ex-dividend date.

e. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Annual Report | 45

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| f. | Guarantees and Indemnifications |

Under the Portfolio’s organizational documents, the Portfolio’s officers and directors are indemnified by the Portfolio against certain liabilities arising out of the performance of their duties to the Portfolio. Additionally, in the normal course of business, the Portfolio enters into contracts with service providers that contain general indemnification clauses. The Portfolio’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Portfolio that have not yet occurred. Currently, the Portfolio expects the risk of loss to be remote.

2. SHARES OF BENEFICIAL INTEREST

At October 31, 2012, there were an unlimited number of shares authorized (without par value).

Transactions in the Portfolio’s shares were as follows:

3. TRANSACTIONS WITH AFFILIATES

Franklin Resources, Inc. is the holding company of Franklin Advisers, Inc. (Advisers) which is the investment manager of the Portfolio.

a. Management Fees

The Portfolio pays an investment management fee to Advisers equal to 80% of the total management fee with the remainder to be paid by the Fund based on the average daily net assets of the Fund as follows:

46 | Annual Report

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

| 3. | TRANSACTIONS WITH AFFILIATES (continued) |

| b. | Administrative Fees |

The Portfolio pays an administrative fee to International Financial Services Limited (IFS), a Mauritius company, an annual fee of $30,000 plus reimbursement of certain expenses. Certain directors of the Portfolio are also directors of IFS.

4. INVESTMENT TRANSACTIONS

Purchases and sales of investments (excluding short term securities) for the year ended October 31, 2012, aggregated $29,140,205 and $38,237,753, respectively.

5. CONCENTRATION OF RISK

Investing in Indian equity securities through the Portfolio may include certain risks and considerations not typically associated with investing in U.S. securities, such as fluctuating currency values, less liquidity, expropriation, confiscatory taxation, nationalization, exchange control regulations (including currency blockage), differing legal standards and changing local and regional economic, political and social conditions, which may result in greater market volatility.

6. FAIR VALUE MEASUREMENTS

The Portfolio follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Portfolio’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Portfolio’s financial instruments and are summarized in the following fair value hierarchy:

- Level 1 – quoted prices in active markets for identical financial instruments

- Level 2 – other significant observable inputs (including quoted prices for similar financial instruments, interest rates, prepayment speed, credit risk, etc.)

- Level 3 – significant unobservable inputs (including the Portfolio’s own assumptions in determining the fair value of financial instruments)

The inputs or methodology used for valuing financial instruments are not an indication of the risk associated with investing in those financial instruments.

For movements between the levels within the fair value hierarchy, the Portfolio has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

At October 31, 2012, all of the Portfolio’s investments in financial instruments carried at fair value were valued using Level 1 inputs. For detailed categories, see the accompanying Statement of Investments.

Annual Report | 47

FT (Mauritius) Offshore Investments Limited

Notes to Financial Statements (continued)

(Expressed in U.S. Dollars)

7. NEW ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2011-11, Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities. The amendments in the ASU enhance disclosures about offsetting of financial assets and liabilities to enable investors to understand the effect of these arrangements on a fund’s financial position. The ASU is effective for interim and annual reporting periods beginning on or after January 1, 2013. The Portfolio believes the adoption of this ASU will not have a material impact on its financial statements.

8. SUBSEQUENT EVENTS

The Portfolio has evaluated subsequent events through the issuance of the financial statements and determined that no events have occurred that require disclosure.

48 | Annual Report

FT (Mauritius) Offshore Investments Limited

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of FT (Mauritius) Offshore Investments Limited

In our opinion, the accompanying statement of assets and liabilities, including the statement of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of FT (Mauritius) Offshore Investments Limited (the “Portfolio”) at October 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at October 31, 2012 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

San Francisco, California

December 17, 2012

Annual Report | 49

Franklin Templeton International Trust

Shareholder Information

Franklin India Growth Fund

Proxy Voting Policies and Procedures

The Fund’s investment manager has established Proxy Voting Policies and Procedures (Policies) that the Fund uses to determine how to vote proxies relating to portfolio securities. Shareholders may view the Fund’s complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301, Attention: Proxy Group. Copies of the Fund’s proxy voting records are also made available online at franklintempleton.com and posted on the U.S. Securities and Exchange Commission’s website at sec.gov and reflect the most recent 12-month period ended June 30.

Quarterly Statement of Investments

The Fund files a complete statement of investments with the U.S. Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission’s website at sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling (800) SEC-0330.

Householding of Reports and Prospectuses

You will receive the Fund’s financial reports every six months as well as an annual updated summary prospectus (prospectus available upon request). To reduce Fund expenses, we try to identify related shareholders in a household and send only one copy of the financial reports and summary prospectus. This process, called “householding,” will continue indefinitely unless you instruct us otherwise. If you prefer not to have these documents householded, please call us at (800) 632-2301. At any time you may view current prospectuses/summary prospectuses and financial reports on our website. If you choose, you may receive these documents through electronic delivery.

50 | Annual Report

This page intentionally left blank.

This page intentionally left blank.

| 1

Annual Report

Franklin World Perspectives Fund

Your Fund’s Goal and Main Investments: Franklin World Perspectives Fund seeks long-term capital appreciation. Under normal market conditions, the Fund invests primarily in equity securities in developed, emerging and frontier markets across the entire market capitalization spectrum.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. Please visit franklintempleton.com or call (800) 342-5236 for most recent month-end performance.

This annual report for Franklin World Perspectives Fund covers the fiscal year ended October 31, 2012.

Performance Overview

Franklin World Perspectives Fund – Class A delivered a +5.97% cumulative total return for the 12-month period ended October 31, 2012. The Fund under-performed the +9.13% total return of its benchmark, the MSCI All Country World Index Plus Frontier Markets Index (ACWI FM), which measures stock performance in developed, emerging and frontier markets.1 You can find more of the Fund’s performance data in the Performance Summary beginning on page 14.

Economic and Market Overview

The global economy slowed during the 12 months under review, but emerging and frontier market economies generally continued to grow faster than their developed market counterparts. Nonetheless, economic reports from the largest economies proved inconsistent with some dire predictions of a severe global economic slowdown. Fears of European sovereign debt default and China’s potential “hard landing” dominated financial headlines in the first half of the period, contributing to heightened market volatility that led global stocks to a 2012 low in early June. Despite ongoing uncertainty, eurozone leaders made meaningful progress and began to implement policy solutions aimed at correcting structural issues. Globally, central bankers continued to pursue historically accommodative monetary policies. Among developed markets, the Bank of Japan and U.S. Federal Reserve Board (Fed) maintained their

1. Source: © 2012 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. The index is unmanaged and includes reinvested dividends. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

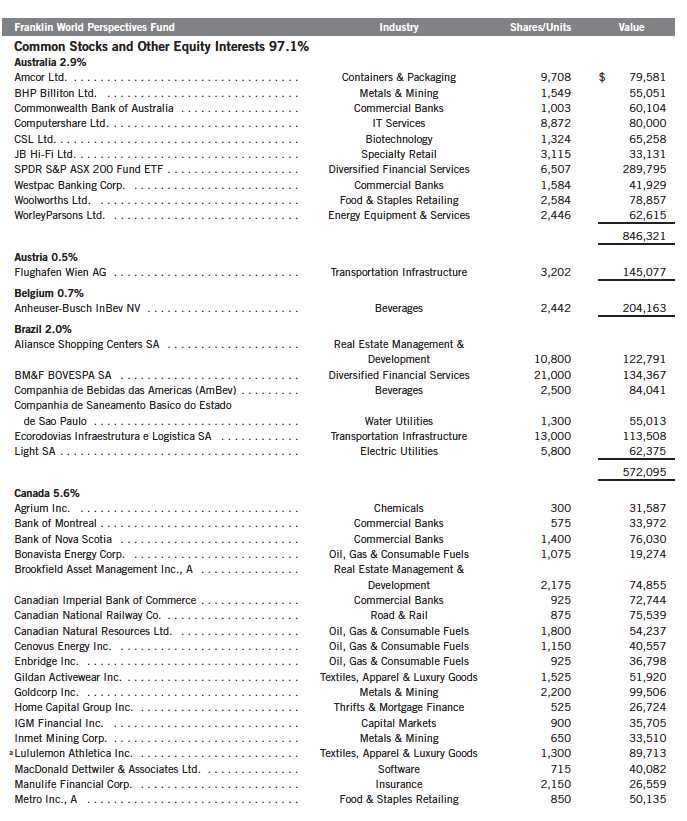

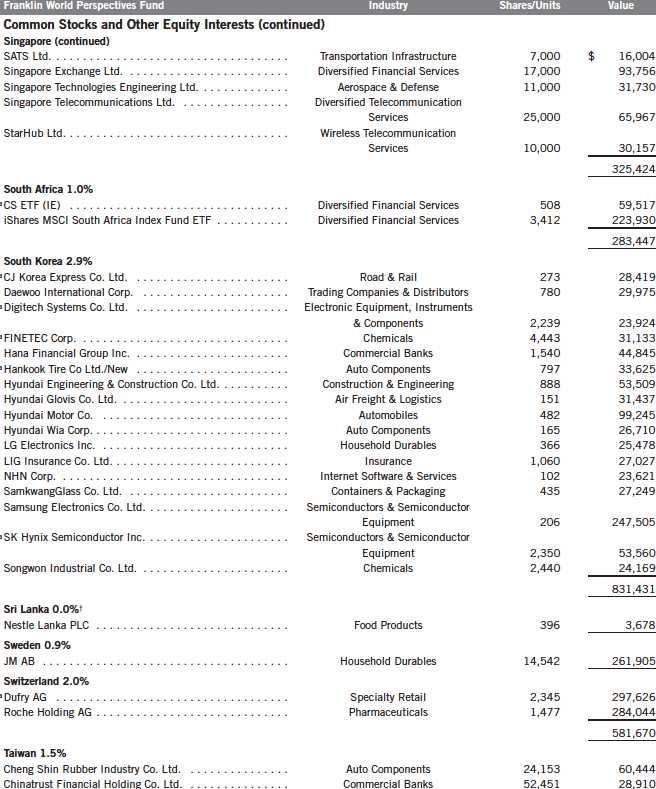

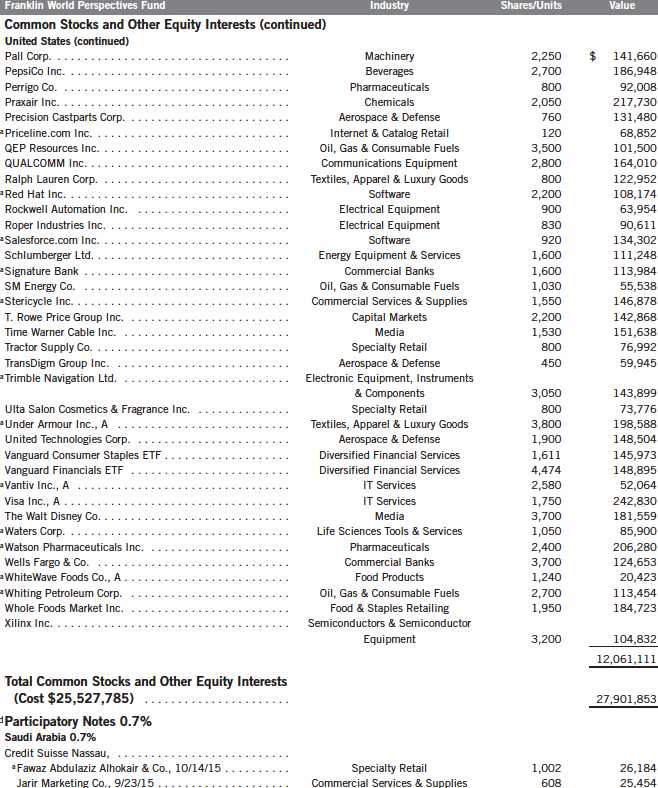

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 25.

Annual Report | 3

respective policy rates, while the European Central Bank (ECB) implemented a series of rate reductions.

In addition to rate adjustments, many central bankers employed a variety of policy tools. The Fed increased the average maturity of its Treasury holdings and in September announced plans to increase mortgage-backed securities holdings in a third round of quantitative easing. In September, the ECB announced its Outright Monetary Transactions program, which was designed to allow the central bank to purchase government bonds on the secondary market with the aim of easing borrowing pressures in the eurozone. The Bank of England and Bank of Japan expanded their respective asset purchase programs. Among emerging market countries, Brazil, China and India announced fiscal and monetary easing measures to support economic growth. Brazil unveiled a 133 billion real (approximately $66 billion) stimulus package in August. In addition to adopting a monetary easing policy and reducing the reserve requirement ratio, China launched a 1 trillion yuan (approximately $158 billion) stimulus package in September. The Indian government announced a series of reforms in September to boost investment and stimulate economic growth.

Global markets reached a period high in mid-September as investors became optimistic that monetary easing policies and fiscal stimulus measures would boost economic growth. However, momentum faltered toward period-end amid renewed investor concerns about economic growth, triggered by manufacturing weakness in some parts of Asia and Europe. Further weighing on investor sentiment was the U.S. “fiscal cliff,” when spending cuts and tax increases will take effect in January 2013 unless the U.S. Congress acts, which could threaten the fragile global economic health. Although global economic indicators remained generally weak throughout the period, U.S. data offered some relief, with increased consumer spending and notable improvements in housing and labor markets helping to offset slower manufacturing growth. Additionally, manufacturing in Canada and several emerging market countries, particularly Mexico, Russia and India, improved near period-end. In this environment, commodities and the euro declined for the period, while U.S. Treasuries and the U.S. dollar gained. Global developed, emerging and frontier market stocks, as represented by the MSCI ACWI FM, generated healthy returns for the 12 months ended October 31, 2012.

Investment Strategy

We manage the Fund using a multi-manager approach. While we have overall responsibility for the Fund’s investments, we consult with Franklin Templeton’s

4 | Annual Report

local asset management teams (subadvisors) to determine regional and country allocations, and each subadvisor is responsible for selecting investments for that portion of the Fund’s portfolio allocated to it. We work closely with the sub-advisors to develop local portfolios of securities seeking to outperform the relevant market of each region and combine those portfolios into a single global growth equity fund. The Fund’s actual exposure to various regions and markets will vary from time to time according to our and the subadvisors’ opinions as to the prevailing conditions and prospects for these markets.

Using a growth-oriented investment style, we seek to invest in growth-oriented equity securities of companies in developed, emerging and frontier regions and countries around the world. When choosing equity investments for the Fund, we and the subadvisors, with the benefit of local knowledge and market insight, apply a research-driven, bottom-up, fundamental long-term approach. We focus on the market price of a company’s securities relative to our and the sub-advisors’ evaluations of the company’s long-term earnings, asset value and cash flow potential. We seek to invest in financially strong companies with favorable growth potential and sustainable competitive advantages and also consider a company’s price/earnings ratio, profit margins and liquidation value.

Manager’s Discussion

Global markets seemingly remained driven primarily by economic headlines and investor expectations of the effects of monetary easing programs implemented by many developed and emerging market countries rather than by any clear indication of significant structural economic reforms. Although the investment climate was challenging, the backdrop seemed to improve toward period-end as data releases suggested potential stabilization in the global economy. Global manufacturing showed signs of improvement in September and October as the manufacturing sector in several countries expanded. Economic recovery in many developed market countries, however, remained somewhat restrained due to ongoing deleveraging, fiscal restraint and persistent pressure on sovereign debt markets, particularly in the eurozone.

Developed market stocks, led largely by the U.S., generally outperformed their emerging and frontier market counterparts for the 12 months ended October 31, 2012. As investor sentiment swung across the risk spectrum, emerging market stocks generally exhibited greater volatility than developed and frontier market stocks but still ended the period with positive returns. Within emerging markets, Asia Pacific (excluding Japan) generally outperformed Latin America and Europe, with the Philippines, Thailand and Malaysia among the best performers. In line with the broader equity markets, the Fund’s developed market

Annual Report | 5

holdings generally outperformed their emerging market counterparts. The Fund’s frontier market holdings delivered strong performance overall.

Europe

Stock selection in Europe was a key contributor to the Fund’s absolute and relative performance, compared with the MSCI ACWI FM, particularly in the U.K., the Netherlands, Italy and Switzerland. The Fund’s regional allocation was also favorable, notably the lack of exposure to Spain, whose market declined during the period, as well as an overweighted allocation to Belgium, one of the best performing European markets. In addition, our overweighted allocations to Denmark and Ireland helped relative performance as their markets outperformed the index. From a sector standpoint, key contributors included the Fund’s overweighting and stock selection in the U.K.’s financials and consumer discretionary sectors, as well as portfolio positioning in Belgium’s consumer staples, Italy’s industrials and the Netherlands’ energy sectors.2

The Fund’s off-benchmark holding in the U.K.-based short-term financing company International Personal Finance was a leading individual contributor to performance relative to the benchmark. After declining sharply in the second half of 2011, the company’s share price advanced in 2012 largely because of expanding customer and credit volumes. Following its report of encouraging earnings results, the company maintained its optimistic outlook that it expects to weather the global economic turmoil. An off-benchmark position in consumer discretionary company Carpetright, a U.K.-based floor covering specialist and carpet retailer, was another strong performer during the period. Although the company reported weak 2011 sales and profit margins resulting from delays in U.K. home purchases and remodeling, its share price rallied in the first half of 2012 as a result of optimism regarding the European Central Bank’s (ECB’s) monetary policy moves. In our assessment, Carpetright’s strengths included its balance sheet and leading position, which improved as many competitors struggled in the recent economic environment. The Fund also benefited from the strong share price gain of Belgium-based beverage company Anheuser-Busch InBev as it generated strong earnings and higher net profits attributable to its acquisition of a Chinese brewery, continued sales growth in Asia-Pacific

2. The financials sector comprises capital markets, commercial banks, consumer finance, diversified financial services, insurance, real estate investment trusts, real estate management and development, and thrifts and mortgage finance in the SOI. The consumer discretionary sector comprises auto components; automobiles; diversified consumer services; hotels, restaurants and leisure; household durables; Internet and catalog retail; leisure equipment and products; media; multiline retail; specialty retail; and textiles, apparel and luxury goods in the SOI. The consumer staples sector comprises beverages, food and staples retailing, food products, household products, personal products and tobacco in the SOI. The industrials sector comprises aerospace and defense, air freight and logistics, building products, commercial services and supplies, construction and engineering, electrical equipment, industrial conglomerates, machinery, road and rail, trading companies and distributors, and transportation infrastructure in the SOI. The energy sector comprises energy equipment and services; and oil, gas and consumable fuels in the SOI.

6 | Annual Report

beverage markets, and price increases in the U.S. and Brazil. The company announced in late June that it had reached an agreement to acquire the remaining stake in Grupo Modelo3 in a $20.1 billion deal expected to close in the first quarter of 2013, which will augment the world’s biggest brewer’s position in the fast-growing Mexican market. An off-benchmark holding in Savills, a U.K.-based property advisory company, also gained in value, largely from ongoing expansion into the U.S. real estate market amid increased interest in investment properties.

In contrast, stock selection in France weighed on relative performance, particularly our position in Neopost, a France-based information technology (IT) company, as its shares lost value during the first half of 2012.4 Neopost provides mailing and logistics solutions such as customized mail processing systems to corporate customers worldwide. Elsewhere, our off-benchmark position in Homeserve,3 a U.K. home repair and emergency services provider, declined in value during the first half of 2012 after the company decided to suspend all telephone sales and marketing activities and the Financial Services Authority announced it would launch an investigation into Homeserve’s sales practices.

Although the ECB implemented some programs during the period that we believe could help certain European countries surmount some longstanding sovereign debt issues, we still expect that many national governments will face some uncertainties ahead. Even though austerity measures fueled protests in Europe, increased investor optimism for improvement in the region’s sovereign debt crisis was evident amid the ECB’s commitment to buy government bonds of troubled countries in an unrestricted capacity. During the reporting period, we slightly increased our weighting in Europe and at fiscal year-end had a relatively neutral position relative to the benchmark. In particular, we increased our allocations to France, Italy and Switzerland. Conversely, we decreased our weightings in the Netherlands, Ireland and Austria.

North America

The Fund’s positioning in the North American materials sector and stock selection in the financials sector benefited relative performance as did our overweighted allocation to the U.S. industrials, consumer discretionary and IT sectors.5 On a security level, our overweighting in Apple, one of the top U.S. performers during the period, aided the Fund’s results. An off-benchmark

3. No longer held at period-end.

4. The IT sector comprises communications equipment; computers and peripherals; electronic equipment, instruments and components; Internet software and services; IT services; office electronics; semiconductors and semiconductor equipment; and software in the SOI.

5. The materials sector comprises chemicals, containers and packaging, and metals and mining in the SOI.

Annual Report | 7

position in Under Armour also helped performance as the sporting goods company reported increased sales, earnings and operating margins. The company’s higher 2012 guidance further supported the stock.

However, the Fund’s underweighted allocation to the U.S. detracted from relative returns, as U.S. stocks rallied amid investor optimism about the country’s economic recovery and stimulus measures announced by the U.S. Fed and other central banks. Additionally, one of the biggest overall detractors from the Fund’s relative returns was stock selection in the U.S., particularly in the IT, consumer discretionary, energy and industrials sectors. Among the holdings that hurt relative and absolute results were off-benchmark positions in software company Informatica3 and oil and gas company SM Energy. Informatica’s revenue and earnings were pressured by sales weakness in Europe. SM Energy’s share price suffered from a slowdown in crude oil demand stemming from weaker global economic growth.

Outside of the U.S., stock selection in Canada helped the Fund’s relative performance. Individual contributors included an off-benchmark position in energy equipment and services company URS Flint (formerly known as Flint Energy Services).3 In contrast, generally falling precious metals prices weighed on mining company Goldcorp’s share price, which hindered relative Fund performance.

Although the Fund’s U.S. allocation was less than the benchmark’s at fiscal year-end, we increased the weighting during the period, particularly in the health care, financials, consumer staples and consumer discretionary sectors.6 We continued to have no exposure to the telecommunication services and utilities sectors.7 In Canada, we remained overweighted throughout the reporting period as we increased our allocation to the consumer discretionary sector, reduced our allocation to energy, and continued to have no exposure to health care and utilities.

The U.S. market outperformed many of its developed market peers during the 12-month period, providing support to global equity indexes. In October, the Bureau of Economic Analysis released an estimate of third-quarter U.S. gross domestic product (GDP) growth that showed the economy improved as a result of stronger consumer spending, a recovering housing sector and increased