| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

Investment Company Act file number 811- 6490

| Dreyfus Premier Investment Funds, Inc. |

| (Exact name of Registrant as specified in charter) |

| c/o The Dreyfus Corporation | ||

| 200 Park Avenue | ||

| New York, New York 10166 | ||

| (Address of principal executive offices) | (Zip code) | |

| Michael A. Rosenberg, Esq. |

| 200 Park Avenue |

| New York, New York 10166 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (212) 922-6000 | |||

| Date of fiscal year end: | 12/31 | |||

| Date of reporting period: | 12/31/08 | |||

The following N-CSR relates only to the Registrant’s series listed below and does not affect the other series of the Registrant, which has a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR Form will be filed for this series, as appropriate.

| DREYFUS PREMIER INVESTMENT FUNDS, INC. | ||

| - | Dreyfus Enhanced Income Fund | |

| - | Dreyfus Global Real Estate Securities Fund | |

| - | Dreyfus Large Cap Equity Fund | |

| - | Dreyfus Large Cap Growth Fund | |

| - | Dreyfus Large Cap Value Fund | |

| FORM N-CSR |

Item 1. Reports to Stockholders.

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured Not Bank-Guaranteed May Lose Value

| Contents | ||

| THE FUND | ||

| 2 | A Letter from the CEO | |

| 3 | Discussion of Fund Performance | |

| 6 | Fund Performance | |

| 8 | Understanding Your Fund’s Expenses | |

| 8 | Comparing Your Fund’s Expenses | |

| With Those of Other Funds | ||

| 9 | Statement of Investments | |

| 12 | Statement of Assets and Liabilities | |

| 13 | Statement of Operations | |

| 14 | Statement of Changes in Net Assets | |

| 16 | Financial Highlights | |

| 18 | Notes to Financial Statements | |

| 28 | Report of Independent Registered | |

| Public Accounting Firm | ||

| 29 | Important Tax Information | |

| 30 | Information About the Review and Approval | |

| of the Fund’s Management Agreement | ||

| 34 | Board Members Information | |

| 37 | Officers of the Fund | |

| FOR MORE INFORMATION | ||

| Back Cover | ||

| The Fund |

| Dreyfus Enhanced Income Fund |

| A LETTER FROM THE CEO Dear Shareholder: |

We present to you this annual report for Dreyfus Enhanced Income Fund, covering the 12-month period from January 1, 2008, through December 31, 2008.

2008 was the most difficult year in decades for the financial markets. A credit crunch that began in 2007 exploded in mid-2008 into a global financial crisis, resulting in the failures of major financial institutions, a deep and prolonged recession and lower investment values across a broad range of asset classes. Governments and regulators throughout the world moved aggressively to curtail the damage, implementing unprecedented reductions of short-term interest rates, massive injections of liquidity into the banking system, government bailouts of struggling companies and plans for massive economic stimulus programs. U.S. government securities generally fared well in the ensuing “flight to quality,” but riskier bond market sectors suffered sharp price declines.

Although we expect the U.S. and global economies to remain weak until longstanding imbalances have worked their way out of the system, the financial markets currently appear to have priced in investors’ generally low expectations. In previous recessions, however, the markets have tended to anticipate economic improvement before it occurs, potentially leading to major rallies when few expected them. That’s why it makes sense to remain disciplined, maintain a long-term perspective and adopt a consistent asset allocation strategy that reflects one’s future goals and attitudes toward risk. As always, we urge you to consult with your financial advisor, who can recommend the course of action that is right for you.

For information about how the fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance given by the fund’s Portfolio Managers.

Thank you for your continued confidence and support.

| Jonathan R. Baum Chief Executive Officer The Dreyfus Corporation |

| 2 |

| January 15, 2009 |

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2008, through December 31, 2008, as provided by Laurie Carroll and Theodore Bair, Jr., Portfolio Managers

Notice to Shareholders: On September 12, 2008, BNY Hamilton Enhanced Income Fund (the “predecessor fund”) completed a tax-free reorganization into the fund, and performance for the fund’s Institutional and Investor shares for periods prior to September 12, 2008, reflects the performance of the predecessor fund’s Institutional and Class A shares, respectively.

Fund and Market Performance Overview

For the 12-month period ended December 31, 2008, Dreyfus Enhanced Income Fund’s Institutional shares achieved a total return of –8.69% and the fund’s Investor shares achieved a total return of –9.49% .1 In comparison, the Merrill Lynch U.S. Dollar LIBOR 3-Month Constant Maturity Index (the “Index”), the fund’s benchmark, achieved a total return of 3.83% .2 At the start of 2008, the fund was overweight in mortgage-backed and asset-backed securities. However, as liquidity concerns grew, the returns on these issues significantly lagged those of Treasuries as the year progressed. While we attempted to reduce our exposure during the second half of the year, increased investor demand for Treasuries and the diminished capacity for demand of asset-backed securities hampered our efforts to reduce the fund’s exposure to these assets.

The Fund’s Investment Approach

The fund seeks a high level of current income as is consistent with the preservation of capital and the maintenance of liquidity.To pursue this goal, the fund normally invests at least 80% of its assets in fixed-income securities of U.S. and foreign issuers rated investment grade or the unrated equivalent as determined by Dreyfus.

These may include securities issued or guaranteed by the U.S. government or its agencies or instrumentalities (including securities that are neither insured or guaranteed by the U.S. government), debt securities and securities with debt-like characteristics issued by domestic and foreign private issuers (including corporations, partnerships, trusts or similar entities), foreign governments and their subdivisions, agencies and sponsored enterprises and supranational entities, municipal securities, convertible securities, preferred stock, guaranteed investment contracts, asset-based securities, and mortgage-related securities.

The Fund 3

| DISCUSSION OF FUND PERFORMANCE (continued) |

The fund seeks to provide a high degree of share price stability.To help manage share price volatility and preserve shareholders’ capital, we attempt to keep the fund’s average effective duration, under normal market conditions, between three and 13 months. However, we may adjust the fund’s holdings based on actual or anticipated changes in interest rates or credit quality, and may shorten the fund’s duration below three months based on our interest rate outlook or adverse market conditions. Of course, the fund is not a money-market fund and does not seek to maintain a stable $1 price per share.

Contending with Challenging Conditions

To describe the past year in the financial markets as eventful would be an understatement.The first half of 2008 was, for the most part, a frustrating period in the financial markets, marked by a sweeping liquidity crisis. Investors became increasingly wary of any risk, and staged a massive flight to quality in which Treasuries outperformed virtually every other bond sector.The Federal Reserve engaged in an aggressive series of interest-rate cuts and initiated other measures to shore up liquidity and restore confidence to the marketplace.

In the second half of the year, the breakdown of the financial system accelerated. The year’s third quarter was largely defined by a shocking series of events in September. In the span of just a few weeks, we saw the takeover of Fannie Mae and Freddie Mac by the U.S. government, the bankruptcy filing of Lehman Brothers, Bank of America’s hastily arranged purchase of Merrill Lynch, the government bailout of global insurer AIG, the seizure of Washington Mutual by federal regulators, and the contemplation of a sweeping bailout plan to stabilize the markets. In this environment, already-tight credit became even more constrained. Banks were not only wary of lending to consumers and corporations; they even became reluctant to lend to one another, as it became difficult to assess which institutions might fail next.The predictable result of these unexpected developments was another, even greater flight to quality. Investors shunned virtually every other type of asset in favor ofTreasuries, even as the Federal Reserve slashed short-term rate targets to near-zero.

The Lehman Collapse Was Widespread and Significant

The Lehman bankruptcy on its own sparked a deep crisis of confidence. Lehman’s role as counterparty to many transactions, and the exposure of many money market funds to Lehman assets, heightened the impact of the institution’s failure.

In this environment, the market’s preference for Treasuries was so overpowering that the yield on three-month Treasuries approached zero. Treasury yields across the yield spectrum also dropped dramatically, while

4

yields on comparable-maturity securities, such as commercial paper, corporate securities, and asset-backed securities, rose in accordance with the extreme selling pressure they came under.

Our Approach to a Difficult Market

Our efforts to improve the fund’s diversification and reduce its mortgage-backed and asset-backed exposure have left the fund better-positioned than it was a year ago, even if market conditions did not allow us to make all the changes we wanted.When we were able to diversify earlier in the year, we moved the fund into short-term industrial credits, which were less volatile and also offered a yield advantage over Treasury securities. As the economic news worsened late in the year, we reduced our positions in short-term industrial credits and also utility-related securities. At that point, we added money market instruments such as commercial paper and U.S. agency-related securities. We also shortened the fund’s duration, or sensitivity to interest-rate shifts, over the reporting period. The fund’s duration now ranges between 120 and 140 days.

Our Outlook

We anticipate that we could see more of the volatility we saw in the past year, and believe investors are likely to maintain their very risk-averse stance.

The push is already on for the new Presidential administration and Congress to provide a major stimulus package, which should be able to gain acceptance by including some assistance for troubled homeowners. The government will probably also be called upon to take more steps to help restore market liquidity, which remains problematic.Those efforts will only be able to achieve maximum effectiveness, however, if banks become more willing to lend.

January 15, 2009

| 1 | Total return includes reinvestment of dividends and any capital gains paid, and, for the fund’s Investor shares for periods prior to September 12, 2008, do not take into consideration the maximum initial sales charge imposed on the predecessor fund’s Class A shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. |

| Share price, yield and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figures provided reflect the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an agreement in effect through September 30, 2010, for the fund’s Institutional shares, and September 30, 2009, for the fund’s Investor shares, at which time they may be extended, terminated or modified. Had these expenses not been absorbed, the fund’s returns would have been lower. | |

| 2 | SOURCE: BLOOMBERG — Reflects reinvestment of dividends and, where applicable, capital gain distributions.The Merrill Lynch U.S. Dollar LIBOR 3-Month Constant Maturity Index is an unmanaged index that measures current interest rates on 3-month constant maturity dollar- denominated deposits.The index does not reflect fees and expenses to which the fund is subject. |

The Fund 5

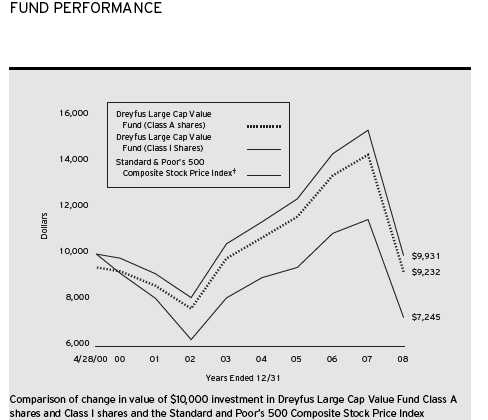

| FUND PERFORMANCE |

| Average Annual Total Returns as of 12/31/08 | ||||||||

| Inception | From | |||||||

| Date | 1 Year | 5 Years | Inception | |||||

| Investor shares | 5/07/02 | (9.49)% | (0.22)% | 0.28% | ||||

| Institutional shares | 5/01/02 | (8.69)% | 0.05% | 0.56% | ||||

† Source: Lipper Inc. Source: Bloomberg L.P.

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The above graph compares a $10,000 investment made in Investor shares and Institutional shares of Dreyfus Enhanced Income Fund on 5/1/02 (inception date for Institutional shares) and 5/7/02 (inception date for Investor shares) to a $10,000 investment made in the Barclays Capital 9-12 Month Treasury Note Index (the “Barclays Capital Index”) and the Merrill Lynch U.S. Dollar LIBOR 3-Month Constant Maturity Index (the “Merrill Lynch Index”) on that date. All dividends and capital gain distributions are reinvested.

6

As of the close of business on September 12, 2008, substantially all of the assets of another investment company advised by an affiliate of the fund’s investment adviser, BNY Hamilton Enhanced Income Fund (the “predecessor fund”), a series of BNY Hamilton Funds, Inc., were transferred to Dreyfus Enhanced Income Fund in a tax-free reorganization.The predecessor fund has the same investment objective, policies, guidelines and restrictions as Dreyfus Enhanced Income Fund. The performance figures for the fund’s Investor shares represent the performance of the predecessor fund’s Class A shares prior to the commencement of operations for Dreyfus Enhanced Income Fund and the performance of Dreyfus Enhanced Income Fund’s Investor shares thereafter.The performance figures for the fund’s Institutional shares represent the performance of the predecessor fund’s Institutional shares prior to the commencement of operations for Dreyfus Enhanced Income Fund and the performance of the Dreyfus Enhanced Income Fund’s Institutional shares thereafter.

The fund’s performance shown in the line graph takes into account all applicable fees and expenses.The Barclays Capital Index is an unmanaged index designed to measure the performance of U.S.Treasury notes and bonds with remaining maturities of from nine up to but not including twelve months.The Merrill Lynch Index is an unmanaged index that measures current interest rates on 3-month constant maturity dollar-denominated deposits. Unlike a mutual fund, both indices are not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

The Fund 7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Enhanced Income Fund from July 1, 2008 to December 31, 2008. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment assuming actual returns for the six months ended December 31, 2008

| Institutional | Investor | |||

| Expenses paid per $1,000† | $ 3.30 | $ 6.90 | ||

| Ending value (after expenses) | $962.10 | $959.90 |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment assuming a hypothetical 5% annualized return for the six months ended December 31, 2008

| Institutional | Investor | |||

| Expenses paid per $1,000† | $ 3.40 | $ 7.10 | ||

| Ending value (after expenses) | $1,021.77 | $1,018.10 |

| † Expenses are equal to the fund’s annualized expense ratio of .67% for Institutional Shares and 1.40% for |

| Investor shares, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the |

| one-half year period). |

8

| STATEMENT OF INVESTMENTS | ||||||||||

| December 31, 2008 | ||||||||||

| Coupon | Maturity | Principal | ||||||||

| Bonds and Notes—52.8% | Rate (%) | Date | Amount ($) | Value ($) | ||||||

| Asset-Backed Ctfs./ | ||||||||||

| Auto Receivables—.9% | ||||||||||

| Capital Auto Receivables Asset | ||||||||||

| Trust, Ser. 2007-3, Cl. A2A | 5.11 | 11/16/09 | 40,449 | 40,413 | ||||||

| WFS Financial Owner Trust, | ||||||||||

| Ser. 2005-2, Cl. A4 | 4.39 | 11/19/12 | 34,977 | 34,883 | ||||||

| 75,296 | ||||||||||

| Asset-Backed Ctfs./ | ||||||||||

| Home Equity Loans—3.1% | ||||||||||

| Securitized Asset Backed | ||||||||||

| Receivables, Ser. 2006-WM4, | ||||||||||

| Cl. A2C | 0.63 | 11/25/36 | 1,000,000 | a | 273,224 | |||||

| Banks—4.0% | ||||||||||

| US Bancorp, | ||||||||||

| Sr. Unscd. Notes | 3.11 | 5/6/10 | 355,000 | a | 348,073 | |||||

| Electric—Integrated—1.7% | ||||||||||

| Public Service Electricity & Gas, | ||||||||||

| First Mortgage Bonds | 2.97 | 3/12/10 | 150,000 | a | 148,339 | |||||

| Health Care—.9% | ||||||||||

| Abbott Laboratories, | ||||||||||

| Sr. Unscd. Notes | 5.60 | 5/15/11 | 70,000 | 73,950 | ||||||

| Residential Mortgage | ||||||||||

| Pass-Through Ctfs.—6.1% | ||||||||||

| Indymac Index Mortgage Loan Trust, | ||||||||||

| Ser. 2006-AR35, Cl. 2A2 | 0.57 | 1/25/37 | 193,205 | a | 182,730 | |||||

| Structured Adjustable Rate | ||||||||||

| Mortgage Loan Trust, | ||||||||||

| Ser. 2005-23, Cl. 1A1 | 5.45 | 1/25/36 | 820,627 | a | 347,536 | |||||

| 530,266 | ||||||||||

| U.S. Government Agencies—2.6% | ||||||||||

| Federal Home Loan Mortgage Corp., | ||||||||||

| Notes | 5.63 | 3/15/11 | 210,000 | b | 228,997 | |||||

The Fund 9

| STATEMENT OF INVESTMENTS (continued) |

| Principal | ||||

| Bonds and Notes (continued) | Amount ($) | Value ($) | ||

| U.S. Government Agencies/ | ||||

| Mortgage-Backed—33.5% | ||||

| Government National Mortgage Association I: | ||||

| Ser. 2007-20, Cl. FA, 0.81%, 4/20/37 | 1,685,959 a | 1,648,726 | ||

| Ser. 2006-58, Cl. FL, 1.24%, 10/16/36 | 1,312,571 a | 1,275,710 | ||

| 2,924,436 | ||||

| Total Bonds and Notes | ||||

| (cost $5,883,821) | 4,602,581 | |||

| Short-Term Investments—37.2% | ||||

| Commercial Paper—13.7% | ||||

| Barclays US Funding | ||||

| 3.07%, 2/13/09 | 500,000 | 498,166 | ||

| ING US Funding | ||||

| 2.06%, 3/4/09 | 200,000 | 199,290 | ||

| Monta Blanc Capital | ||||

| 1.80%, 1/22/09 | 100,000 | 99,895 | ||

| Praxair | ||||

| 0.40%, 2/17/09 | 250,000 | 249,869 | ||

| Royal Bank of Scotland | ||||

| 1.30%, 1/8/09 | 150,000 | 149,962 | ||

| 1,197,182 | ||||

| U.S. Government Agencies—23.5% | ||||

| Federal Home Loan Banks, Discount | ||||

| Notes, 3.15%, 1/28/09 | 880,000 | 878,231 | ||

| Federal Home Loan Mortgage Corp., | ||||

| Discount Notes, 1.25%, 6/25/09 | 450,000 b | 447,266 | ||

| Federal National Mortgage | ||||

| Association, Discount Notes, 1.24%, 7/1/09 | 450,000 b | 449,156 | ||

| Federal Natonal Mortgage | ||||

| Association, Discount Notes, 1.15%, 12/1/09 | 280,000 b | 277,013 | ||

| 2,051,666 | ||||

| Total Short-Term Investments | ||||

| (cost $3,246,864) | 3,248,848 | |||

10

| Other Investment—12.4% | Shares | Value ($) | ||

| Registered Investment Company; | ||||

| Dreyfus Institutional Preferred | ||||

| Plus Money Market Fund | ||||

| (cost $1,083,000) | 1,083,000 c | 1,083,000 | ||

| Total Investments (cost $10,213,685) | 102.4% | 8,934,429 | ||

| Liabilities, Less Cash and Receivables | (2.4%) | (210,947) | ||

| Net Assets | 100.0% | 8,723,482 | ||

| a | Variable rate security—interest rate subject to periodic change. |

| b | On September 7, 2008, the Federal Housing Finance Agency (FHFA) placed Federal National Mortgage Association and Federal Home Loan Mortgage Corporation into conservatorship with FHFA as the conservator. As such, the FHFA will oversee the continuing affairs of these companies. |

| c | Investment in affiliated money market mutual fund. |

| Portfolio Summary (Unaudited)† | ||||||

| Value (%) | Value (%) | |||||

| Short-Term/ | Asset/Mortgage-Backed | 10.1 | ||||

| Money Market Investments | 49.6 | Corporate Bonds | 6.6 | |||

| U.S. Government & Agencies | 36.1 | 102.4 | ||||

| † Based on net assets. | ||||||

| See notes to financial statements. | ||||||

The Fund 11

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2008

| Cost | Value | |||

| Assets ($): | ||||

| Investments in securities—See Statement of Investments: | ||||

| Unaffiliated issuers | 9,130,685 | 7,851,429 | ||

| Affiliated issuers | 1,083,000 | 1,083,000 | ||

| Receivable for shares of Common Stock subscribed | 58,241 | |||

| Dividends and interest receivable | 11,619 | |||

| Prepaid expenses | 9,150 | |||

| Due from The Dreyfus Corporation and affiliates—Note 3(c) | 1,404 | |||

| 9,014,843 | ||||

| Liabilities ($): | ||||

| Cash overdraft due to Custodian | 308 | |||

| Payable for shares of Common Stock redeemed | 233,439 | |||

| Accrued expenses | 57,614 | |||

| 291,361 | ||||

| Net Assets ($) | 8,723,482 | |||

| Composition of Net Assets ($): | ||||

| Paid-in capital | 18,270,785 | |||

| Accumulated net realized gain (loss) on investments | (8,268,039) | |||

| Accumulated net unrealized appreciation | ||||

| (depreciation) on investments | (1,279,264) | |||

| Net Assets ($) | 8,723,482 | |||

| Net Asset Value Per Share | ||||

| Institutional Shares | Investor Shares | |||

| Net Assets ($) | 8,697,162 | 26,320 | ||

| Shares Outstanding | 5,213,445 | 15,767 | ||

| Net Asset Value Per Share ($) | 1.67 | 1.67 | ||

| See notes to financial statements. | ||||

12

| STATEMENT OF OPERATIONS | ||

| Year Ended December 31, 2008 | ||

| Investment Income ($): | ||

| Income: | ||

| Interest | 850,473 | |

| Cash dividends; | ||

| Affiliated issuers | 10,516 | |

| Total Income | 860,989 | |

| Expenses: | ||

| Management fee—Note 3(a) | 24,105 | |

| Administration fee—Note 3(a) | 12,889 | |

| Auditing fees | 30,154 | |

| Registration fees | 29,815 | |

| Shareholder servicing costs—Note 3(c) | 24,475 | |

| Directors’ fees and expenses—Note 3(d) | 14,799 | |

| Custodian fees—Note 3(c) | 7,175 | |

| Prospectus and shareholders’ reports | 4,471 | |

| Distribution fees—Note 3(b) | 2,823 | |

| Miscellaneous | 20,535 | |

| Total Expenses | 171,241 | |

| Less—expense reimbursement due to undertakings—Note 3(a) | (95,591) | |

| Less—reduction in fees due to earnings credits—Note 1(b) | (36) | |

| Net Expenses | 75,614 | |

| Investment Income—Net | 785,375 | |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | ||

| Net realized gain (loss) on investments | (2,434,358) | |

| Net unrealized appreciation (depreciation) on investments | (479,951) | |

| Net Realized and Unrealized Gain (Loss) on Investments | (2,914,309) | |

| Net (Decrease) in Net Assets Resulting from Operations | (2,128,934) | |

| See notes to financial statements. | ||

The Fund 13

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended December 31, | ||||

| 2008a,b | 2007b,c | |||

| Operations ($): | ||||

| Investment income—net | 785,375 | 4,083,651 | ||

| Net realized gain (loss) on investments | (2,434,358) | (1,379,497) | ||

| Net unrealized appreciation | ||||

| (depreciation) on investments | (479,951) | (767,647) | ||

| Net Increase (Decrease) in Net Assets | ||||

| Resulting from Operations | (2,128,934) | 1,936,507 | ||

| Dividends to Shareholders from ($): | ||||

| Investment income—net: | ||||

| Institutional Shares | (804,662) | (3,950,560) | ||

| Investor Shares | (43,561) | (143,594) | ||

| Class C Shares | — | (20) | ||

| Total Dividends | (848,223) | (4,094,174) | ||

| Capital Stock Transactions ($): | ||||

| Net proceeds from shares sold: | ||||

| Institutional Shares | 14,845,975 | 63,360,069 | ||

| Investor Shares | 34,806 | 724,628 | ||

| Dividends reinvested: | ||||

| Institutional Shares | 516,643 | 2,007,961 | ||

| Investor Shares | 37,400 | 143,594 | ||

| Class C Shares | — | 20 | ||

| Cost of shares redeemed: | ||||

| Institutional Shares | (40,946,772) | (91,711,116) | ||

| Investor Shares | (1,739,439) | (1,786,114) | ||

| Class C Shares | — | (21,046) | ||

| Increase (Decrease) in Net Assets | ||||

| from Capital Stock Transactions | (27,251,387) | (27,282,004) | ||

| Total Increase (Decrease) in Net Assets | (30,228,544) | (29,439,671) | ||

| Net Assets ($): | ||||

| Beginning of Period | 38,952,026 | 68,391,697 | ||

| End of Period | 8,723,482 | 38,952,026 | ||

| Undistributed investment income—net | — | 56,290 | ||

14

| Year Ended December 31, | ||||

| 2008a,b | 2007b,c | |||

| Capital Share Transactions: | ||||

| Institutional Shares | ||||

| Shares sold | 8,200,191 | 32,042,477 | ||

| Shares issued for dividends reinvested | 288,194 | 1,019,157 | ||

| Shares redeemed | (22,756,542) | (46,616,628) | ||

| Net Increase (Decrease) in Shares Outstanding | (14,268,157) | (13,554,994) | ||

| Investor Shares | ||||

| Shares sold | 21,497 | 365,982 | ||

| Shares issued for dividends reinvested | 20,637 | 73,165 | ||

| Shares redeemed | (1,001,452) | (907,202) | ||

| Net Increase (Decrease) in Shares Outstanding | (959,318) | (468,055) | ||

| Class C Shares | ||||

| Shares sold | — | — | ||

| Shares issued for dividends reinvested | — | 13 | ||

| Shares redeemed | — | (10,629) | ||

| Net Increase (Decrease) in Shares Outstanding | — | (10,616) | ||

| a | The fund commenced offering two classes of shares on the close of business September 12, 2008.The existing shares were redesignated. |

| b | Represents information for the the funds’s predecessor, BNY Hamilton Enhanced Income Fund through September 12, 2008. |

| c | Prior to January 1, 2007, Class C share accounts had been closed. On January 3, 2007, residual Class C shares remaining were redeemed. |

| See notes to financial statements. |

The Fund 15

FINANCIAL HIGHLIGHTS

Please note that the financial highlights information in the following tables for the fund’s Institutional and Investor shares represents the financial highlights of the Institutional and Class A shares, respectively, of the fund’s predecessor, BNY Hamilton Enhanced Income Fund (“Enhanced Income Fund”), before the fund commenced operations as of the close of business on September 12, 2008, and represents the performance of the fund’s Institutional and Investor shares thereafter. Before the fund commenced operations, all of the assets of the Enhanced Income Fund were transferred to the fund in exchange for Institutional and Investor shares of the fund in a tax-free reorganization. Total return shows how much an investment in the fund would have increased (or decreased), assuming all dividends and distributions were reinvested. These figures have been derived from the fund’s and the fund’s predecessor’s financial statements.

| Year Ended December 31, | ||||||||||

| Institutional Shares† | 2008 | 2007 | 2006 | 2005 | 2004 | |||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 1.90 | 1.98 | 1.98 | 1.98 | 2.00 | |||||

| Investment Operations: | ||||||||||

| Investment income—neta | .07 | .10 | .09 | .05 | .03 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | (.23) | (.08) | — | .01 | (.02) | |||||

| Total from Investment Operations | (.16) | .02 | .09 | .06 | .01 | |||||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.07) | (.10) | (.09) | (.06) | (.03) | |||||

| Net asset value, end of period | 1.67 | 1.90 | 1.98 | 1.98 | 1.98 | |||||

| Total Return (%) | (8.69) | 1.09 | 4.77 | 2.88 | .76 | |||||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assets | .80 | .33 | .34 | .29 | .27 | |||||

| Ratio of net expenses | ||||||||||

| to average net assets | .33 | .25 | .25 | .25 | .25 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets | 3.63 | 5.24 | 4.67 | 2.90 | 1.51 | |||||

| Portfolio Turnover Rate | 72 | 104 | 126 | 51 | 105 | |||||

| Net Assets, end of period ($ x 1,000) | 8,697 | 37,092 | 65,511 | 87,151 | 324,670 | |||||

- Represents information for Institutional Shares of the fund’s predecessor, Enhanced Income Fund through September 12, 2008.

| a Based on average shares outstanding at each month end. See notes to financial statements. |

16

| Year Ended December 31, | ||||||||||

| Investor Shares† | 2008 | 2007 | 2006 | 2005 | 2004 | |||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 1.91 | 1.98 | 1.98 | 1.99 | 2.00 | |||||

| Investment Operations: | ||||||||||

| Investment income—neta | .06 | .10 | .09 | .05 | .03 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | (.24) | (.07) | — | (.01) | (.01) | |||||

| Total from Investment Operations | (.18) | .03 | .09 | .04 | .02 | |||||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.06) | (.10) | (.09) | (.05) | (.03) | |||||

| Net asset value, end of period | 1.67 | 1.91 | 1.98 | 1.98 | 1.99 | |||||

| Total Return (%)b | (9.49) | 1.36 | 4.50 | 2.10 | 1.02 | |||||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assets | .62 | .58 | .59 | .54 | .52 | |||||

| Ratio of net expenses | ||||||||||

| to average net assets | .59 | .50 | .50 | .50 | .50 | |||||

| Ratio of net investment income | ||||||||||

| to average net assets | 3.32 | 4.97 | 4.43 | 2.92 | 1.30 | |||||

| Portfolio Turnover Rate | 72 | 104 | 126 | 51 | 105 | |||||

| Net Assets, end of period ($ x 1,000) | 26 | 1,860 | 2,860 | 2,473 | 7,966 | |||||

| † Represents information for Class A Shares of the fund’s predecessor, Enhanced Income Fund through |

| September 12, 2008. |

| a | Based on average shares outstanding at each month end. |

| b | Exclusive of sales charge. |

| See notes to financial statements. |

The Fund 17

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Enhanced Income Fund (the “fund”) is a separate diversified series of Dreyfus Premier Investment Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering nine series, including the fund.The fund commenced operations on September 13, 2008. The fund’s investment objective is high current income with preservation of capital and maintenance of liquidity. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

As of the close of business on September 12, 2008, pursuant to an Agreement and Plan of Reorganization previously approved by the fund’s Board of Directors, all of the assets, subject to the liabilities, of BNY Hamilton Enhanced Income Fund (“Enhanced Income Fund”), a series of BNY Hamilton Funds, were transferred to the fund in exchange for corresponding class of shares of Common Stock of the fund of equal value. Shareholders of Institutional shares and Class A of Enhanced Income Fund received Institutional shares and Investor shares of the fund, respectively, in each case in an amount equal to the aggregate net asset value of their investment in Enhanced Income Fund at the time of the exchange. The net asset value of the fund’s shares on the close of business September 12, 2008, after the reorganization was $1.74 for Institutional shares and $1.75 for Investor shares, and a total of 7,358,435 Institutional shares and 787,846 Investor shares, representing net assets of $14,198,125 (including $787,393 net unrealized depreciation on investments) were issued to shareholders of Hamilton Enhanced Income Fund shareholders in the exchange.The exchange was a tax-free event to shareholders. Enhanced Income Fund is the accounting survivor and its historical performance is presented for periods through September 12, 2008.

18

Effective July 1, 2008, BNY Mellon reorganized and consolidated a number of its banking and trust company subsidiaries.As a result of the reorganization, any services previously provided to the fund by Mellon Bank, N.A. or Mellon Trust of New England, N.A. are now provided by The Bank of NewYork Mellon (formerly,The Bank of NewYork).

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the funds’ shares, which are sold to the public without a sales charge.The fund is authorized to issue 50 million shares of $.001 Common Stock in each of the following classes of shares: Institutional and Investor. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

As of December 31, 2008, MBC Investments Corp., an indirect subsidiary of BNY Mellon, held 5,714 Investor shares of the fund.

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations: expenses which are applicable to all series are allocated among them on a pro rata basis.

The fund’s financial statements are prepared in accordance with U.S. generally accepted accounting principles, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

The Fund 19

| NOTES TO FINANCIAL STATEMENTS (continued) |

(a) Portfolio valuation: Investments in securities excluding short-term investments (other than U.S. Treasury Bills), are valued each business day by an independent pricing service (the “Service”) approved by the Board of Directors. Investments for which quoted bid prices are readily available and are representative of the bid side of the market in the judgment of the Service are valued at the mean between the quoted bid prices (as obtained by the Service from dealers in such securities) and asked prices (as calculated by the Service based upon its evaluation of the market for such securities). Other investments (which constitute a majority of the portfolio securities) are valued as determined by the Service, based on methods which include consideration of: yields or prices of securities of comparable quality, coupon, maturity and type; indications as to values from dealers; and general market conditions. Restricted securities, as well as securities or other assets for which recent market quotations are not readily available, that are not valued by a pricing service approved by the Board of Directors, or are determined by the fund not to reflect accurately fair value, are valued at fair value as determined in good faith under the direction of the Board of Directors.The factors that may be considered when fair valuing a security include fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold and public trading in similar securities of the issuer or comparable issuers. Short-term investments, excluding U.S.Treasury Bills, are carried at amortized cost, which approximates value. Registered investment companies that are not traded on an exchange are valued at their net asset value. Financial futures and options, which are traded on an exchange, are valued at the last sales price on the securities exchange on which such securities are primarily traded or at the last sales price on the national securities market on each business day. Options traded over-the-counter are priced at the mean between the bid and the asked price.

The fund adopted Statement of Financial Accounting Standards No. 157 “FairValue Measurements” (“FAS 157”). FAS 157 establishes an author-

20

itative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the fund’s investments relating to FAS 157.These inputs are summarized in the three broad levels listed below.

Level 1—quoted prices in active markets for identical securities. Level 2—other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used as of December 31, 2008 in valuing the fund’s investments carried at fair value:

| Investments in | Other Financial | |||

| Valuation Inputs | Securities ($) | Instruments ($)† | ||

| Level 1—Quoted Prices | 1,083,000 | 0 | ||

| Level 2—Other Significant | ||||

| Observable Inputs | 7,851,429 | 0 | ||

| Level 3—Significant | ||||

| Unobservable Inputs | 0 | 0 | ||

| Total | 8,934,429 | 0 |

| † | Other financial instruments include derivative instruments such as futures, forward currency | |

| exchange contracts and swap contracts, which are valued at the unrealized appreciation | ||

| (depreciation) on the instrument and written options contracts which are shown at value. |

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

The Fund 21

| NOTES TO FINANCIAL STATEMENTS (continued) |

The fund has arrangements with the custodian and cash management banks whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset custody and cash management fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

(c) Affiliated issuers: Investments in other investment companies advised by the Manager are defined as “affiliated” in the Act.

(d) Concentration of risk: The fund invests primarily in debt securities. Failure of an issuer of the debt securities to make timely interest or principal payments, or a decline or the perception of a decline in the credit quality of a debt security, can cause the debt security’s price to fall, potentially lowering the fund’s share price. High yield (“junk”) bonds involve greater credit risk, including the risk of default, than investment grade bonds, and are considered predominantly speculative with respect to the issuer’s continuing ability to make principal and interest payments. In addition, the value of debt securities may decline due to general market conditions that are not specifically related to a particular company, such as real or perceived adverse economic conditions, changes in outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment. They may also decline because of factors that affect a particular industry.

(e) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains.

(f) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable pro-

22

visions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended December 31, 2008, the fund did not have any liabilities for any unrecognized tax positions. The fund recognizes interest and penalties, if any, related to unrecognized tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended December 31, 2008 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At December 31, 2008, the components of accumulated earnings on a tax basis were as follows: accumulated capital losses $8,267,615 and unrealized depreciation $1,279,688.

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net securities profits, if any, realized subsequent to December 31, 2008. If not applied $205,618 of the carryover expires in fiscal 2011, $1,689,718 expires in fiscal 2012, $2,085,448 expires in fiscal 2013, $482,656 expires in fiscal 2014, $45,761 expires in fiscal 2015 and $3,758,414 expires in fiscal 2016.

The tax character of distributions paid to shareholders during the fiscal periods ended December 31, 2008 and December 31, 2007 were as follows: ordinary income $848,223 and $4,094,174, respectively.

During the period ended December 31, 2008, as a result of permanent book to tax differences, primarily due to the tax treatment for amortization of premiums and paydown gains and losses, the fund increased accumulated undistributed investment income-net by $6,558, increased accumulated net realized gain (loss) on investments by $3,795 and decreased paid in capital by $10,353. Net assets and net asset value per share were not affected by this reclassification.

The Fund 23

| NOTES TO FINANCIAL STATEMENTS (continued) |

NOTE 2—Bank Line of Credit:

Effective October 15, 2008, the fund participates with other Dreyfus managed funds in a $145 million redemption credit facility (the “Facility”) to be utilized for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay commitment fees on its pro rata portion of the Facility. Interest is charged to the fund based on prevailing market rates in effect at the time of borrowing. During the period ended December 31, 2008, the fund did not borrow under the Facility.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a Management Agreement (“Agreement”) with the Manager, the management fee is computed at an annual rate of .17% of the value of the fund’s average daily net assets and is payable monthly. Prior to September 12, 2008,The Bank of NewYork (the “Advisor”) was the advisor for Enhanced Income Fund.The Advisor's fee was based on the value of Enhanced Income Fund’s average daily net assets and was computed at the following annual rates .10% of the first $2 billion, .095% of the next $3 billion, .09% of the next $5 billion and .085% in excess of $10 billion. The fee was payable monthly. During the period ended December 31, 2008, the Advisor and Manager earned $18,413 and $5,692, respectively.

Dreyfus has contractually agreed, through September 30, 2010, to waive receipt of its fees and/or assume the expenses of the fund so that the direct expenses of the Institutional shares (excluding taxes, interest, brokerage commissions, commitment fees on borrowings and extraordinary expenses) do not exceed .37%.

Dreyfus has agreed from September 24, 2008 through May 1, 2009, to waive receipt of its fees and/or assume the expenses of the fund so that the direct expenses of the Investor shares (excluding taxes, interest, brokerage commissions, commitment fees on borrowings, extraordinary expenses and shareholder services fees) do not exceed .65%.

24

The expense reimbursement, pursuant to the undertakings, amounted to $95,591 during the period ended December 31, 2008.

The Bank of New York Mellon served as Administrator to Enhanced Income Fund pursuant to an Administration Agreement. The Administrator received from Enhanced Income Fund a monthly fee equal to an annual rate of .07% of the average daily net assets of Enhanced Income Fund.The administration fee amounted to $12,889 for the period ended September 12, 2008.This agreement was terminated as of the close of business on September 12, 2008, due to the reorganization.

(b) Under the prior Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class A shares paid BNY Hamilton Distributors Inc. for distributing their shares at an annual rate of .25% of the value of the average daily net assets of Class A. During the period January 1, 2008 through September 12, 2008, Class A shares were charged $2,823.This agreement was terminated as of the close of business on September 12, 2008.

(c) Under the Shareholder Services Plan, Investor shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (a securities dealer, financial institution or other industry professional) in respect of these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended December 31, 2008, Investor shares were charged $114, pursuant to the Shareholder Services Plan.

The fund compensates Dreyfus Transfer, Inc., a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing personnel and facilities to perform transfer agency services for the

The Fund 25

| NOTES TO FINANCIAL STATEMENTS (continued) |

fund. During the period ended December 31, 2008, the fund was charged $4,775 pursuant to the transfer agency agreement.

The fund compensates The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, under a cash management agreement for performing cash management services related to fund subscriptions and redemptions. During the period ended December 31, 2008, the fund was charged $36 pursuant to the cash management agreement.

The fund compensates The Bank of New York Mellon under a custody agreement for providing custodial services for the fund. During the period ended December 31, 2008, the fund was charged $7,175 pursuant to the custody agreement.

During the period ended December 31, 2008, the fund was charged $1,197 for services performed by the Chief Compliance Officer.

The components of “Due fromThe Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: an expense reimbursement of $11,162, which is offset by management fees $1,330, shareholder services plan fees $5, custodian fees $2,819, chief compliance officer fees $1,197 and transfer agency per account fees $4,407.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales (including paydowns) of investment securities, excluding short-term securities, during the period ended December 31, 2008, amounted to $11,036,126 and $38,049,242, respectively.

26

At December 31, 2008, the cost of investments for federal income tax purposes was $10,214,117; accordingly, accumulated net unrealized depreciation on investments was $1,279,688, consisting of $12,726 gross unrealized appreciation and $1,292,414 gross unrealized depreciation.

In March 2008, the FASB released Statement of Financial Accounting Standards No. 161, “Disclosures about Derivative Instruments and Hedging Activities” (“FAS 161”). FAS 161 requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of gains and losses on derivative instruments, and disclosures about credit-risk-related contingent features in derivative agreements.The application of FAS 161 is required for fiscal years and interim periods beginning after November 15, 2008. At this time, management is evaluating the implications of FAS 161 and its impact on the financial statements and the accompanying notes has not yet been determined.

The Fund 27

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

| Shareholders and Board of Directors Dreyfus Enhanced Income Fund |

We have audited the accompanying statement of assets and liabilities, including the statement of investments, of Dreyfus Enhanced Income Fund (one of the series comprising Dreyfus Premier Investment Funds, Inc.) as of December 31, 2008, and the related statements of operations and changes in net assets for the year then ended and financial highlights for the year then ended and for the year ended December 31,2004.These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The statement of changes in net assets for the year ended December 31, 2007 and the financial highlights for the years ended December 31, 2007, 2006 and 2005 were audited by other auditors whose report dated February 28, 2008, expressed an unqualified opinion on such statement of changes in net assets and financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2008 by correspondence with the custodian and others. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above and audited by us present fairly, in all material respects, the financial position of Dreyfus Enhanced Income Fund at December 31, 2008, the results of its operations and the changes in its net assets for the year then ended and the financial highlights for the year then ended and for the year ended December 31, 2004, in conformity with U.S. generally accepted accounting principles.

28

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes the fund hereby designates 100% of ordinary income dividends paid during the fiscal year ended December 31, 2008 as qualifying “interest related dividends”.

The Fund 29

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited)

At the March 18, 2008, Board meeting, the Board members established the Fund as a separate series of Dreyfus Premier Investment Funds, Inc. (the “Company”), and authorized the Company, on behalf of the Fund, to enter into an agreement and plan of reorganization to acquire all of the assets and liabilities of BNY Hamilton Enhanced Income Fund (the “BNY Fund”) in a tax-free reorganization in exchange for shares of the Fund and the assumption by the Fund of the BNY Fund’s stated liabilities. The Fund was established solely for the purpose of effecting the BNY Fund’s reorganization and, as a result, the Fund adopted the same or substantially similar investment objective and policies as the BNY Fund and expected to inherit the performance and financial records of the BNY Fund.

At the meeting, the Board considered the approval of, with respect to the Fund, the management agreement, between the Company and Dreyfus (the “Agreement”) through July 30, 2010.The Board members who are not “interested persons” (as defined in the Act) of the Company were assisted in their review by independent legal counsel and met with counsel in executive session separate from representatives of Dreyfus.

Analysis of Nature, Extent and Quality of Services To Be Provided to the Fund. The Board members received a presentation from representatives of Dreyfus regarding services provided to the funds in the Dreyfus fund complex, and discussed the nature, extent and quality of the services to be provided to the Fund pursuant to the Agreement. The Board members also referenced information provided and discussed at the meeting regarding the fund’s distribution of accounts, the relationships Dreyfus has with various intermediaries and the different needs of each, the diversity of distribution among the funds in the Dreyfus fund complex, and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each of the funds’ distribution channels.

The Board members also considered Dreyfus’ research and portfolio management capabilities and that Dreyfus provides oversight of day-to-day fund operations, including fund accounting and administration

30

and assistance in meeting legal and regulatory requirements.The Board members also considered Dreyfus’ extensive administrative, accounting and compliance infrastructure.

Comparative Analysis of the Fund’s Performance, Management Fee, and Expense Ratio. As the Fund had not yet commenced operations, the Board members were not able to review the Fund’s performance. The Board was advised, however, that the Fund was expected to inherit the BNY Fund’s performance record upon the closing of the reorganization. The Board members received a presentation from Dreyfus that described, among other matters, the BNY Fund’s average annual total returns for the various periods ended December 31, 2007. The Board discussed with the Dreyfus representatives the Fund’s investment objective and policies and portfolio management team, and noted that the team responsible for managing the BNY Fund will continue to manage the Fund.

The Board members reviewed the Fund’s proposed management fee and estimated expense ratio, and reviewed the range of management fees and expense ratios of the funds in the Lipper Ultra Short Obligations Funds category, the average and median management fees of the funds in that Lipper category and management fees of a subset of those funds.

The Board also noted that Dreyfus has contractually agreed to waive receipt of its fees and/or assume the expenses of the Fund’s Institutional and Investor shares so that the direct expenses of the Institutional and Investor shares (excluding taxes, interest, brokerage commissions, commitment fees on borrowings and extraordinary expenses) do not exceed 0.37% and 0.62%, respectively.This expense undertaking will continue in effect for the Fund’s Institutional shares for at least two years after the reorganization of the BNY Fund, and for the Fund’s Investor shares until such Investor shares received by holders of Class A shares of the BNY Fund are converted to Institutional shares of the Fund.

The Fund 31

INFORMATION ABOUT THE REVIEW AND APPROVAL OF THE FUND’S MANAGEMENT AGREEMENT (Unaudited) (continued)

Representatives of Dreyfus reviewed with the Board members the fees paid to Dreyfus or its affiliates by mutual funds and/or separate accounts managed by Dreyfus with similar investment objectives, policies and strategies as the Fund (the “Similar Accounts”), and explained the nature of the Similar Accounts and the differences, from Dreyfus’ perspective, in providing services to the Similar Accounts as compared to the Fund.The Dreyfus representatives also reviewed the costs associated with distribution through intermediaries. The Board analyzed differences in fees paid to Dreyfus and its affiliates by the Similar Accounts and discussed the relationship of the advisory fee to be paid in light of the services to be provided by Dreyfus.The Board members considered the relevance of the fee information provided for the Similar Accounts managed by Dreyfus, to evaluate the appropriateness and reasonableness of the Fund’s management fees. The Board acknowledged that differences in fees paid by the Similar Accounts seemed to be consistent with the services to be provided.

Analysis of Profitability and Economies of Scale. As the Fund had not yet commenced operations, Dreyfus’ representatives were not able to review the dollar amount of expenses allocated and profit received by Dreyfus. The Board members were presented with a schedule of the estimated profitability of the Fund prepared by Dreyfus. The Board members also considered potential benefits to Dreyfus from acting as investment adviser and noted the unlikelihood of soft dollar arrangements in the future with respect to trading the Fund’s portfolio. The Board also considered whether the Fund would be able to participate in any economies of scale that Dreyfus may experience in the event that the Fund attracts a large amount of assets.The Board members noted the uncertainty of the estimated asset levels, and discussed the renewal requirements for advisory agreements and their ability to review the management fee annually after an initial term of the Agreement.

32

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to approving the Agreement. Based on the discussions and considerations as described above, the Board made the following conclusions and determinations.

- The Board concluded that the nature, extent and quality of the ser- vices to be provided by Dreyfus are adequate and appropriate.

- The Board concluded that the fee to be paid by the Fund to Dreyfus was reasonable, in light of the services to be provided, comparative expense and advisory fee information, and benefits anticipated to be derived by Dreyfus from its relationship with the Fund.

- The Board determined that because the Fund had not commenced investment operations, economies of scale were not a factor and that, to the extent in the future it were to be determined that material economies of scale had not been shared with the Fund, the Board would seek to have those economies of scale shared with the Fund.

The Board members considered these conclusions and determinations, and, without any one factor being dispositive, the Board determined that approval of the Agreement was in the best interests of the Fund.

The Fund 33

NOTES

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured Not Bank-Guaranteed May Lose Value

| Contents | ||

| THE FUND | ||

| 2 | A Letter from the CEO | |

| 3 | Discussion of Fund Performance | |

| 6 | Fund Performance | |

| 8 | Understanding Your Fund’s Expenses | |

| 8 | Comparing Your Fund’s Expenses | |

| With Those of Other Funds | ||

| 9 | Statement of Investments | |

| 13 | Statement of Assets and Liabilities | |

| 14 | Statement of Operations | |

| 15 | Statement of Changes in Net Assets | |

| 17 | Financial Highlights | |

| 21 | Notes to Financial Statements | |

| 33 | Report of Independent Registered | |

| Public Accounting Firm | ||

| 34 | Important Tax Information | |

| 35 | Information About the Review and Approval | |

| of the Fund’s Management Agreement | ||

| 39 | Board Members Information | |

| 42 | Officers of the Fund | |

| FOR MORE INFORMATION | ||

| Back Cover | ||

The Fund

| Dreyfus |

| Global Real Estate |

| Securities Fund |

A LETTER FROM THE CEO

Dear Shareholder:

We present to you this annual report for Dreyfus Global Real Estate Securities Fund, covering the 12-month period from January 1, 2008, through December 31, 2008.

2008 was the most difficult year in decades for the world’s financial markets. A credit crunch that began in 2007 in the U.S. sub-prime mortgage market exploded in mid-2008 into a global financial crisis, resulting in the failures of major financial institutions, a deep and prolonged recession and lower investment values across a broad range of asset classes. Governments and regulators throughout the world moved aggressively to curtail the damage, implementing unprecedented reductions of short-term interest rates, massive injections of liquidity into the banking system, government bailouts of struggling companies and plans for massive economic stimulus programs. After several years of strong relative returns, international stocks generally declined more sharply than their U.S. counterparts.

Although we expect the U.S. and global economies to remain weak until longstanding imbalances have worked their way out of the system, the financial markets currently appear to have priced in investors’ generally low expectations. In previous recessions, however, the markets have tended to anticipate economic improvement before it occurs, potentially leading to major rallies when few expected them. That’s why it makes sense to remain disciplined, maintain a long-term perspective and adopt a consistent asset allocation strategy that reflects one’s future goals and attitudes toward risk. As always, we urge you to consult with your financial advisor, who can recommend the course of action that is right for you.

For information about how the fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance given by the fund’s Portfolio Managers.

Thank you for your continued confidence and support.

| Jonathan R. Baum Chief Executive Officer The Dreyfus Corporation January 15, 2009 |

2

DISCUSSION OF FUND PERFORMANCE

For the period of January 1, 2008, through December 31, 2008, as provided by Peter Zabierek, Dean Frankel and Todd Briddell, Portfolio Managers

Fund and Market Performance Overview

For the 12-month period ended December 31, 2008, Dreyfus Global Real Estate Securities Fund’s Class A shares achieved a total return of –43.60% and Class I shares returned –43.38% ..1 In comparison, the FTSE EPRA/NAREIT Global Real Estate Securities Index (the “Index”), the fund’s benchmark, achieved a total return of –47.72% for the same period.2 For the period of September 13, 2008, through December 31, 2008, Class C shares returned –34.92%, and Class T shares returned –34.94% .1 In comparison, for that period, the Index returned –38.20% .2 The fund’s outperformance of the Index is attributable to our conservative positioning of the portfolio in a very volatile period for real estate, and our individual security selection in keeping with that positioning.Although we can’t say we predicted the full depth of the industry’s troubles, in 2007 we saw what we considered to be clear signs of more difficult conditions ahead. This led us to move away from more speculative names with large development pipelines and highly-levered private funds, and toward more conservative positions in well-managed companies.

The Fund’s Investment Approach

The fund seeks to maximize total return consisting of capital appreciation and current income. To pursue this goal, the fund normally invests at least 80% of its assets in publicly traded equity securities of companies principally engaged in the real estate sector. The fund’s equity investments may include common stocks, preferred stocks, convertible securities, warrants, equity interests in foreign investment funds or trusts, depositary receipts and other equity investments. Under normal conditions, the fund expects to invest at least 40% of its assets in companies whose principal place of business is located outside the United States, and will invest in at least 10 different countries (including the United States). Although the fund invests primarily in developed markets, it also may invest in equity securities of companies located in emerging markets, and may invest in equity securities of companies of any market capitalization, including smaller companies.

The Fund 3

| DISCUSSION OF FUND PERFORMANCE (continued) |

In selecting investments for the fund’s portfolio, we use a proprietary approach to quantify investment opportunity both from a real estate and stock perspective. We combine a bottom-up real estate research with a Relative Value Model that includes regular and direct contact with the companies in the fund’s investable universe. These research efforts are supported by extensive sell side and independent research.

Economic Difficulties Were Far-Reaching

The dark cloud that followed the global real estate market in 2008 was the same one that followed every market — and that was the global credit crunch.There were very few corners of the world that were able to avoid the crisis this year.The real estate markets were hit by a bit of a double whammy. First, the credit crunch created recessionary conditions around the world, and as usual, weaker economies reduced demand for residential, commercial, and industrial real estate. Second, banks’ tightening of credit sapped liquidity from the market and made it difficult to buy and to sell commercial real estate properties. So at the same time revenues were going down, it became more difficult to create value through buying and selling properties.

In this environment, we sought out reliable, income-producing securities that weren’t taking a lot of risk with building new projects. Specifically, we looked for companies that had relatively low levels of debt, access to capital, and established management teams with a record of success. This approach served us relatively well during this past year, not only because of the companies it led us to buy, but also those it led us not to buy; we were able to avoid a number of stocks in the benchmark that fell precipitously during the year.

A Variety of Positions Benefited the Fund

One of the stocks that performed well for the fund was Unibail-Redamco, a French company. Although this company posted a double-digit loss for the year, its losses were far less than the market’s. Unibail had a very large development pipeline, but was among the first to realize that development risk was mounting. Thus, while many of its competitors moved forward with development pipelines and then had trouble leasing them up, Unibail actually put a lot of its development sites on hold. Another solid performer was U.S.-based Public Storage, which was up 12%.The company has almost no debt. In addition, because many people use storage facilities during times of economic dislocation —when they may need to move unexpectedly or downsize their home, for example — demand for these facilities can actually perform well when the economy weakens.

4

The strongest-performing global market in 2008 was Switzerland, which posted a mild single-digit decline. Our overweighting in this country helped our relative performance.The country has a very strong banking system and operates outside the Eurozone, which gives it control of its own monetary policy.The commercial real estate market in Switzerland didn’t rise up as steeply as many of its peers around the world early in the decade, so it hasn’t had as far to fall during the recent contraction.

One of our weakest markets, relative to the benchmark, was Canada. In hindsight, we probably weren’t conservative enough with our positioning in this market. It’s hard to pick two bigger stories this year — the wind coming out of energy’s sails and the fall of the auto industries —and Canada has been hit hard by both of them. The economy in the western part of the country is largely tied to the price of oil, which stumbled in the year’s second half, while the economy in the eastern part of the country is exposed to the automotive industry, which of course struggled mightily throughout the year.

Our Outlook for the Year Ahead

We anticipate some difficult months to come, but we believe we are closer to the bottom than the top in terms of valuations.With this market down so steeply in 2008, we are seeing what we believe to be some compelling valuations. In various parts of the world, many stocks are trading at a 40% to 50% discount to their net asset value, with cash-flow multiples at or near all-time lows and dividend yields at or near all-time highs. In short, we see opportunity for high-quality real estate in major institutional markets.

January 15, 2009

| 1 | The total return figures presented for Class A and I shares of the fund reflect the performance of BNY Hamilton Global Real Estate Securities Fund’s (the “predecessor fund”) Class A shares and Institutional shares, respectively, prior to 9/13/08. Performance for each share class includes returns for the predecessor fund (Class A and Class I only) and the current maximum sales load, and reflects current distribution and servicing fees in effect only since the reorganization date. |

| Investors should consider, when deciding whether to purchase a particular class of shares, the investment amount, anticipated holding period and other relevant factors. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. Return figures provided reflect the absorption of certain fund expenses by The Dreyfus Corporation pursuant to an undertaking in effect for Classes A, C, and T through May 1, 2009, and in effect for Class I through September 30, 2010, at which time it may be extended, terminated or modified. Had these expenses not been absorbed, the fund’s returns would have been lower. | |

| 2 | SOURCE: BLOOMBERG — Reflects reinvestment of net dividends and, where applicable, capital gain distributions.The FTSE European Public Real Estate Association (EPRA) National Association of Real Estate Investment Trusts (NAREIT) Global Real Estate Securities Index is an unmanaged index designed to track the performance of listed real estate companies and REITs worldwide. |

The Fund 5

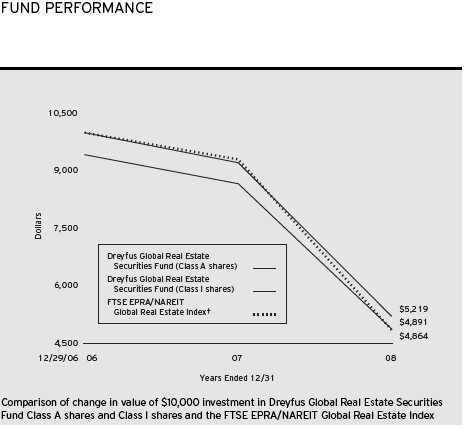

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in Class A and Class I shares of Dreyfus Global Real Estate Securities Fund on 12/29/06 (inception date) to a $10,000 investment made in the FTSE EPRA/NAREIT Global Real Estate Index (the “Index”) on that date. For comparative purposes, the value of the Index on 12/31/06 is used the beginning value on 12/29/06. All dividends and capital gain distributions are reinvested.

As of the close of business on September 12, 2008, substantially all of the assets of another investment company advised by an affiliate of the fund’s investment adviser, BNY Hamilton Global Real Estate Securities Fund (the “predecessor fund”), a series of BNY Hamilton Funds, Inc., were transferred to Dreyfus Global Real Estate Securities Fund in a tax-free reorganization.The predecessor fund has the same investment objective, policies, guidelines and restrictions as Dreyfus Global Real Estate Securities Fund.The performance of the fund’s Class A, Class C, Class I and Class T shares represent the performance of the predecessor fund’s Class A and Institutional shares prior to the commencement of operations for Dreyfus Global Real Estate Securities Fund and the performance of Dreyfus Global Real Estate Securities Fund’s Class A, Class C, Class I and Class T shares thereafter.

The fund’s performance shown in the line graph takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses.The Index is an unmanaged market-capitalization weighted index designed to measure the performance of exchange-listed real estate companies and REITs worldwide. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| Average Annual Total Returns as of 12/31/08 | ||||||

| Inception | From | |||||

| Date | 1 Year | Inception | ||||

| Class A shares | ||||||