UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-6490 | |||||

|

| |||||

| Dreyfus Premier Investment Funds, Inc. |

| ||||

| (Exact name of Registrant as specified in charter) |

| ||||

|

|

| ||||

|

c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 |

| ||||

| (Address of principal executive offices) (Zip code) |

| ||||

|

|

| ||||

| Janette E. Farragher, Esq. 200 Park Avenue New York, New York 10166 |

| ||||

| (Name and address of agent for service) |

| ||||

| ||||||

Registrant's telephone number, including area code: | (212) 922-6000 | |||||

|

| |||||

Date of fiscal year end:

| 10/31 |

| ||||

Date of reporting period: | 10/31/12 |

| ||||

The following N-CSR relates only to the Registrant’s series listed below and does not affect the other series of the Registrant, which has a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR Form will be filed for this series, as appropriate.

DREYFUS PREMIER INVESTMENT FUNDS, INC.

-Dreyfus Diversified International Fund

-Dreyfus Emerging Asia Fund

- Dreyfus Greater China Fund

-Dreyfus India Fund

-Dreyfus Satellite Alpha Fund

1

Dreyfus

Diversified

International Fund

ANNUAL REPORT October 31, 2012

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Contents | |

THE FUND | |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 8 | Understanding Your Fund’s Expenses |

| 8 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 9 | Statement of Investments |

| 10 | Statement of Assets and Liabilities |

| 11 | Statement of Operations |

| 12 | Statement of Changes in Net Assets |

| 14 | Financial Highlights |

| 17 | Notes to Financial Statements |

| 26 | Report of Independent Registered Public Accounting Firm |

| 27 | Important Tax Information |

| 28 | Proxy Results |

| 29 | Information About the Renewal of the Fund’s Management Agreement |

| 34 | Board Members Information |

| 36 | Officers of the Fund |

FOR MORE INFORMATION | |

Back Cover |

Dreyfus

Diversified

International Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Diversified International Fund, covering the 12-month period from November 1, 2011, through October 31, 2012. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Despite pronounced stock market weakness during the spring of 2012, stocks generally advanced over the reporting period as investors responded to encouraging macroeconomic developments throughout the world. Employment gains in the United States, credible measures to prevent a more severe banking crisis in Europe, and the likelihood of a “soft landing” for China’s economy buoyed investor sentiment, as did aggressively accommodative monetary policies from central banks in the United States, Europe, Japan and China. Consequently, U.S. stocks across all capitalization ranges posted double-digit returns, on average, for the reporting period.

In light of the easy monetary policies adopted by many countries, we expect global growth to be slightly more robust in 2013 than in 2012.The U.S. economic recovery is likely to persist at subpar levels over the first half of the new year, as growth may remain constrained by uncertainties surrounding fiscal policy and tax reforms. However, successful resolution of the current fiscal debate may prompt corporate decision-makers to increase capital spending, which could have positive implications for the U.S. economy and domestic equity markets.As always, we encourage you to stay in touch with your financial advisor as new developments unfold.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

November 15, 2012

2

DISCUSSION OF FUND PERFORMANCE

For the period of November 1, 2011, through October 31, 2012, as provided by Richard B. Hoey,A. Paul Disdier and Keith L. Stransky, CFA, Portfolio Managers

Fund and Market Performance Overview

For the 12-month period ended October 31, 2012, Dreyfus Diversified International Fund’s Class A shares produced a total return of 6.39%, Class C shares returned 5.65% and Class I shares returned 6.82%.1 This compares with a 4.61% total return for the fund’s benchmark, the Morgan Stanley Capital International Europe, Australasia, Far East Index (the “MSCI EAFE Index” or the “Index”), during the same period.2

Despite bouts of heightened market volatility, improving economic sentiment in many parts of the world enabled global stock prices to end the reporting period with modest gains.The fund produced higher returns than its benchmark, largely due to strong contributions to relative performance from Dreyfus/Newton International Equity Fund, International Stock Fund, and Dreyfus International Equity Fund.

The Fund’s Investment Approach

The fund seeks long-term capital appreciation.To pursue its goal, the fund normally allocates its assets among other mutual funds advised by The Dreyfus Corporation (Dreyfus), or its affiliates, that invest primarily in stocks issued by foreign companies. The underlying funds are selected by the Dreyfus Investment Committee based on their investment objectives and management policies, portfolio holdings, risk/reward profiles, historical performance and other factors.The Dreyfus Investment Committee will rebalance the fund’s investments in the underlying funds at least annually, but may do so more often in response to market conditions.As of October 31, 2012, the fund’s assets were allocated as follows:

| Underlying Funds | (%) |

| International Stock Fund | 29 |

| Dreyfus International Equity Fund | 25 |

| Dreyfus International Value Fund | 11 |

| Dreyfus/Newton International Equity Fund | 26 |

| Dreyfus Emerging Markets Fund | 9 |

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

Markets Reacted to Changing Macroeconomic Developments

The reporting period began in the wake of major declines in stock markets throughout the world, resulting in attractive valuations across a number of market sectors in November 2011. Indeed, by the beginning of 2012 many equity markets were rallying amid encouraging macroeconomic developments, including U.S. employment gains, a quantitative easing program in Europe that forestalled a more severe banking crisis in the region, and less restrictive monetary and fiscal policies in China in an environment of reduced inflationary pressures. Meanwhile, corporate earnings generally remained strong, and many companies had shored up their balance sheets. Consequently, investors grew more tolerant of risks, and were able to focus more intently on business fundamentals and less on news headlines.

These positive influences were called into question during the spring, when the U.S. labor market’s rebound slowed, measures designed to relieve fiscal pressures in Europe encountered resistance, and the Chinese economy remained sluggish.The summer saw the markets’ rally resume amid more encouraging economic data, and international stocks and bonds ended the reporting period with respectable gains, on average.

A More Constructive Investment Posture

We are pleased that the fund produced higher returns with less volatility than its benchmark over the reporting period. Among the factors supporting the fund’s performance was underweighted exposure to troubled European markets across the fund’s underlying investments.

Although the fund began the reporting period with a relatively defensive stance, we soon adopted a more constructive posture as it became clearer that signs of global economic improvement were likely to be sustainable. In addition, we adjusted the fund’s allocations in response to our analysis of potential opportunities in global equity markets.

In January 2012, we regarded the emerging markets as undervalued compared to historical norms, and we shifted 2.6% of the fund’s assets from the relatively defensive International Stock Fund to the more aggressive Dreyfus Emerging Markets Fund. In June, we reversed course after the emerging markets had rallied, moving 2% of the fund’s assets from Dreyfus Emerging Markets Fund and 3% of assets from Dreyfus InternationalValue Fund into Dreyfus/Newton International Equity Fund.That move

4

was followed in July by a more modest reallocation of 1% of the fund’s assets from Dreyfus Emerging Asia Fund to Dreyfus Emerging Markets Fund. We repeated July’s move in August, when we shifted another 1% of the fund’s assets from Dreyfus Emerging Asia Fund to Dreyfus Emerging Markets Fund. Finally, in October, we sought to increase the fund’s participation in the depressed Chinese stock market by moving 2% of assets from International Stock Fund to Dreyfus Emerging Markets Fund.

Finding Opportunities in Worldwide Markets

Although heightened stock and bond market volatility is likely to persist over the near term in the face of ongoing global challenges, we have been encouraged recently by positive U.S. and global economic developments. In our analysis, emerging-markets stocks currently appear to be attractively valued, and we may increase the fund’s allocation to one or more of its underlying emerging-markets funds should economic and market conditions in developing countries continue to improve.

November 15, 2012

Equity funds are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the prospectus of the fund and that of each underlying fund.

The ability of the fund to achieve its investment goal depends, in part, on the ability of the Dreyfus Investment Committee to allocate effectively the fund’s assets among the underlying funds.There can be no assurance that the actual allocations will be effective in achieving the fund’s investment goal.

Each underlying fund’s performance will be influenced by political, social and economic factors affecting investments in foreign companies. Special risks associated with such companies include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards.These risks are higher in emerging market countries.

| 1 Total return includes reinvestment of dividends and any capital gains paid, and does not take into consideration the |

| maximum initial sales charge in the case of Class A shares, or the applicable contingent deferred sales charge imposed on |

| redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Past |

| performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, |

| fund shares may be worth more or less than their original cost. Return figures provided reflect the absorption of certain |

| fund expenses pursuant to an agreement by The Dreyfus Corporation through March 1, 2013, at which time it may |

| be extended, terminated or modified. Had these expenses not been absorbed, the fund’s returns would have been lower. |

| 2 SOURCE: LIPPER INC. — Reflects reinvestment of net dividends and, where applicable, capital gain distributions. |

| The Morgan Stanley Capital International Europe,Australasia, Far East (MSCI EAFE) Index is an unmanaged |

| index composed of a sample of companies representative of the market structure of European and Pacific Basin countries. |

The Fund 5

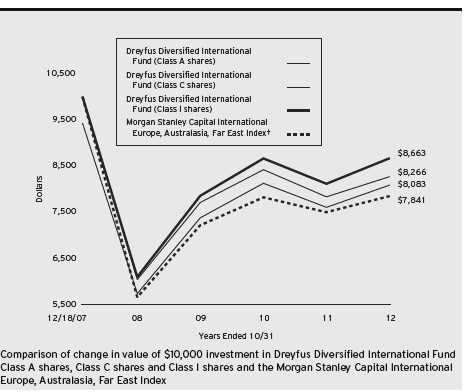

FUND PERFORMANCE

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in each of the Class A, Class C and Class I shares of Dreyfus Diversified International Fund on 12/18/07 (inception date) to a $10,000 investment made in the Morgan Stanley Capital International Europe,Australasia, Far East Index (the “Index”) on that date.All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses on all classes.The Index is an unmanaged index composed of a sample of companies representative of the market structure of European and Pacific Basin countries. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| Average Annual Total Returns as of 10/31/12 | |||||

| Inception | From | ||||

| Date | 1 | Year | Inception | ||

| Class A shares | |||||

| with maximum sales charge (5.75%) | 12/18/07 | 0.30 | % | –4.28 | % |

| without sales charge | 12/18/07 | 6.39 | % | –3.11 | % |

| Class C shares | |||||

| with applicable redemption charge † | 12/18/07 | 4.65 | % | –3.83 | % |

| without redemption | 12/18/07 | 5.65 | % | –3.83 | % |

| Class I shares | 12/18/07 | 6.82 | % | –2.90 | % |

| Morgan Stanley Capital International | |||||

| Europe, Australasia, Far East Index | 12/31/07 | 4.61 | % | –4.91 | %†† |

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

| † | The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the |

| date of purchase. | |

| †† | For comparative purposes, the value of the Index as of 12/31/07 is used as the beginning value on 12/18/07. |

The Fund 7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus Diversified International Fund from May 1, 2012 to October 31, 2012. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment

assuming actual returns for the six months ended October 31, 2012

| Class A | Class C | Class I | ||||

| Expenses paid per $1,000† | $ | 2.08 | $ | 5.77 | $ | .30 |

| Ending value (after expenses) | $ | 1,017.70 | $ | 1,013.60 | $ | 1,018.70 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment

assuming a hypothetical 5% annualized return for the six months ended October 31, 2012

| Class A | Class C | Class I | ||||

| Expenses paid per $1,000† | $ | 2.08 | $ | 5.79 | $ | .31 |

| Ending value (after expenses) | $ | 1,023.08 | $ | 1,019.41 | $ | 1,024.83 |

| † Expenses are equal to the fund’s annualized expense ratio of .41% for Class A, 1.14% for Class C and .06% |

| for Class I, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half |

| year period). |

8

STATEMENT OF INVESTMENTS

October 31, 2012

| Registered Investment Companies—100.1% | Shares | Value ($) | |||

| Dreyfus Emerging Markets Fund, Cl. I | 5,248,603 | a | 51,803,713 | ||

| Dreyfus International Equity Fund, Cl. I | 4,370,620 | a | 121,197,281 | ||

| Dreyfus International Value Fund, Cl. I | 5,060,229 | a | 51,310,718 | ||

| Dreyfus/Newton International Equity Fund, Cl. I | 7,129,108 | a | 119,982,886 | ||

| International Stock Fund, Cl. I | 9,124,547 | a | 127,287,436 | ||

| Total Investments (cost $423,815,050) | 100.1 | % | 471,582,034 | ||

| Liabilities, Less Cash and Receivables | (.1 | %) | (340,799 | ) | |

| Net Assets | 100.0 | % | 471,241,235 | ||

| a Investment in affiliated mutual fund. | |||||

| Portfolio Summary (Unaudited)† | |||||

| Value (%) | |||||

| Mutual Funds: Foreign | 100.1 | ||||

| † Based on net assets. | |||||

| See notes to financial statements. | |||||

The Fund 9

STATEMENT OF ASSETS AND LIABILITIES

October 31, 2012

| Cost | Value | |||

| Assets ($): | ||||

| Investments in affiliated issuers—See Statement of | ||||

| Investments—Note 1(c) | 423,815,050 | 471,582,034 | ||

| Receivable for investment securities sold | 344,488 | |||

| Receivable for shares of Common Stock subscribed | 212,799 | |||

| Prepaid expenses | 27,362 | |||

| 472,166,683 | ||||

| Liabilities ($): | ||||

| Due to The Dreyfus Corporation and affiliates—Note 3(c) | 6,965 | |||

| Cash overdraft due to Custodian | 203,969 | |||

| Payable for shares of Common Stock redeemed | 626,572 | |||

| Interest payable—Note 2 | 139 | |||

| Accrued expenses | 87,803 | |||

| 925,448 | ||||

| Net Assets ($) | 471,241,235 | |||

| Composition of Net Assets ($): | ||||

| Paid-in capital | 455,606,477 | |||

| Accumulated distributions in excess of investment income—net | (67,695 | ) | ||

| Accumulated net realized gain (loss) on investments | (32,064,531 | ) | ||

| Accumulated net unrealized appreciation | ||||

| (depreciation) on investments | 47,766,984 | |||

| Net Assets ($) | 471,241,235 | |||

| Net Asset Value Per Share | ||||

| Class A | Class C | Class I | ||

| Net Assets ($) | 8,674,538 | 116,492 | 462,450,205 | |

| Shares Outstanding | 886,883 | 12,021 | 47,122,299 | |

| Net Asset Value Per Share ($) | 9.78 | 9.69 | 9.81 | |

| See notes to financial statements. | ||||

10

| STATEMENT OF OPERATIONS | ||

| Year Ended October 31, 2012 | ||

| Investment Income ($): | ||

| Income: | ||

| Cash dividends from affiliated issuers | 9,354,045 | |

| Expenses: | ||

| Directors’ fees and expenses—Note 3(d) | 96,147 | |

| Legal fees | 45,390 | |

| Registration fees | 42,476 | |

| Auditing fees | 41,547 | |

| Shareholder servicing costs—Note 3(c) | 38,657 | |

| Prospectus and shareholders’ reports | 17,914 | |

| Custodian fees—Note 3(c) | 5,096 | |

| Loan commitment fees—Note 2 | 4,965 | |

| Interest expense—Note 2 | 3,689 | |

| Distribution fees—Note 3(b) | 1,566 | |

| Miscellaneous | 20,865 | |

| Total Expenses | 318,312 | |

| Less—reduction in expenses due to undertaking—Note 3(a) | (1,098 | ) |

| Less—reduction in fees due to earnings credits—Note 3(c) | (15 | ) |

| Net Expenses | 317,199 | |

| Investment Income—Net | 9,036,846 | |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | ||

| Net realized gain (loss) on investments in affiliated issuers | (31,125,363 | ) |

| Capital gain distributions from affiliated issuers | 4,856,296 | |

| Net Realized Gain (Loss) | (26,269,067 | ) |

| Net unrealized appreciation (depreciation) | ||

| on investments in affiliated issuers | 43,344,469 | |

| Net Realized and Unrealized Gain (Loss) on Investments | 17,075,402 | |

| Net Increase in Net Assets Resulting from Operations | 26,112,248 | |

| See notes to financial statements. | ||

The Fund 11

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended October 31, | ||||

| 2012 | 2011 | |||

| Operations ($): | ||||

| Investment income—net | 9,036,846 | 5,035,437 | ||

| Net realized gain (loss) on | ||||

| investments in affiliated issuers | (26,269,067 | ) | (2,491,387 | ) |

| Net unrealized appreciation (depreciation) | ||||

| on investments in affiliated issuers | 43,344,469 | (45,253,453 | ) | |

| Net Increase (Decrease) in Net Assets | ||||

| Resulting from Operations | 26,112,248 | (42,709,403 | ) | |

| Dividends to Shareholders from ($): | ||||

| Investment income—net: | ||||

| Class A Shares | (194,199 | ) | (104,433 | ) |

| Class C Shares | (5,620 | ) | (292 | ) |

| Class I Shares | (9,324,691 | ) | (5,921,143 | ) |

| Total Dividends | (9,524,510 | ) | (6,025,868 | ) |

| Capital Stock Transactions ($): | ||||

| Net proceeds from shares sold: | ||||

| Class A Shares | 1,663,492 | 4,777,705 | ||

| Class C Shares | 227,447 | 118,251 | ||

| Class I Shares | 151,019,904 | 238,791,647 | ||

| Dividends reinvested: | ||||

| Class A Shares | 189,297 | 104,360 | ||

| Class C Shares | 5,320 | 292 | ||

| Class I Shares | 1,239,699 | 973,208 | ||

| Cost of shares redeemed: | ||||

| Class A Shares | (3,939,062 | ) | (1,369,169 | ) |

| Class C Shares | (225,861 | ) | (63,143 | ) |

| Class I Shares | (180,962,996 | ) | (69,062,457 | ) |

| Increase (Decrease) in Net Assets | ||||

| from Capital Stock Transactions | (30,782,760 | ) | 174,270,694 | |

| Total Increase (Decrease) in Net Assets | (14,195,022 | ) | 125,535,423 | |

| Net Assets ($): | ||||

| Beginning of Period | 485,436,257 | 359,900,834 | ||

| End of Period | 471,241,235 | 485,436,257 | ||

| Undistributed (distributions in excess of) | ||||

| investment income–net | (67,695 | ) | — | |

12

| Year Ended October 31, | ||||

| 2012 | 2011 | |||

| Capital Share Transactions: | ||||

| Class A | ||||

| Shares sold | 180,699 | 469,196 | ||

| Shares issued for dividends reinvested | 21,808 | 10,025 | ||

| Shares redeemed | (415,349 | ) | (137,473 | ) |

| Net Increase (Decrease) in Shares Outstanding | (212,842 | ) | 341,748 | |

| Class C | ||||

| Shares sold | 25,121 | 11,177 | ||

| Shares issued for dividends reinvested | 614 | 28 | ||

| Shares redeemed | (25,351 | ) | (6,377 | ) |

| Net Increase (Decrease) in Shares Outstanding | 384 | 4,828 | ||

| Class I | ||||

| Shares sold | 16,045,955 | 22,911,074 | ||

| Shares issued for dividends reinvested | 142,658 | 93,488 | ||

| Shares redeemed | (19,633,403 | ) | (7,017,782 | ) |

| Net Increase (Decrease) in Shares Outstanding | (3,444,790 | ) | 15,986,780 | |

| See notes to financial statements. | ||||

The Fund 13

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| Year Ended October 31, | ||||||||||

| Class A Shares | 2012 | 2011 | 2010 | 2009 | 2008 | a | ||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 9.38 | 10.16 | 9.45 | 7.59 | 12.50 | |||||

| Investment Operations: | ||||||||||

| Investment income (loss)—netb | .16 | .09 | .09 | .16 | (.01 | ) | ||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | .42 | (.73 | ) | .86 | 1.96 | (4.90 | ) | |||

| Total from Investment Operations | .58 | (.64 | ) | .95 | 2.12 | (4.91 | ) | |||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.18 | ) | (.14 | ) | (.12 | ) | (.26 | ) | — | |

| Dividends from net realized | ||||||||||

| gain on investments | — | — | (.12 | ) | — | — | ||||

| Total Distributions | (.18 | ) | (.14 | ) | (.24 | ) | (.26 | ) | — | |

| Net asset value, end of period | 9.78 | 9.38 | 10.16 | 9.45 | 7.59 | |||||

| Total Return (%)c | 6.39 | (6.47 | ) | 10.18 | 28.80 | (39.28 | )d | |||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assetse | .41 | .40 | .40 | 1.89 | 14.57 | f | ||||

| Ratio of net expenses | ||||||||||

| to average net assetse | .41 | .24 | .30 | .37 | .31 | f | ||||

| Ratio of net investment income | ||||||||||

| (loss) to average net assetse | 1.70 | .90 | .92 | 2.01 | (.13 | )f | ||||

| Portfolio Turnover Rate | 30.63 | 16.15 | 20.78 | 36.68 | 25.65 | d | ||||

| Net Assets, end of period ($ x 1,000) | 8,675 | 10,310 | 7,701 | 4,578 | 1,646 | |||||

| a | From December 18, 2007 (commencement of operations) to October 31, 2008. |

| b | Based on average shares outstanding at each month end. |

| c | Exclusive of sales charge. |

| d | Not annualized. |

| e | Amounts do not include the activity of the underlying funds. |

| f | Annualized. |

See notes to financial statements.

14

| Year Ended October 31, | ||||||||||

| Class C Shares | 2012 | 2011 | 2010 | 2009 | 2008 | a | ||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 9.35 | 10.10 | 9.38 | 7.54 | 12.50 | |||||

| Investment Operations: | ||||||||||

| Investment income (loss)—netb | .17 | .01 | .08 | .14 | (.05 | ) | ||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | .34 | (.71 | ) | .78 | 1.90 | (4.91 | ) | |||

| Total from Investment Operations | .51 | (.70 | ) | .86 | 2.04 | (4.96 | ) | |||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.17 | ) | (.05 | ) | (.02 | ) | (.20 | ) | — | |

| Dividends from net realized | ||||||||||

| gain on investments | — | — | (.12 | ) | — | — | ||||

| Total Distributions | (.17 | ) | (.05 | ) | (.14 | ) | (.20 | ) | — | |

| Net asset value, end of period | 9.69 | 9.35 | 10.10 | 9.38 | 7.54 | |||||

| Total Return (%)c | 5.65 | (7.01 | ) | 9.21 | 27.73 | (39.68 | )d | |||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assetse | 1.47 | 1.48 | 1.63 | 3.33 | 15.79 | f | ||||

| Ratio of net expenses | ||||||||||

| to average net assetse | 1.17 | .70 | 1.07 | 1.12 | 1.06 | f | ||||

| Ratio of net investment income | ||||||||||

| (loss) to average net assetse | 1.71 | .13 | .85 | 1.76 | (.51 | )f | ||||

| Portfolio Turnover Rate | 30.63 | 16.15 | 20.78 | 36.68 | 25.65 | d | ||||

| Net Assets, end of period ($ x 1,000) | 116 | 109 | 69 | 84 | 39 | |||||

| a | From December 18, 2007 (commencement of operations) to October 31, 2008. |

| b | Based on average shares outstanding at each month end. |

| c | Exclusive of sales charge. |

| d | Not annualized. |

| e | Amounts do not include the activity of the underlying funds. |

| f | Annualized. |

See notes to financial statements.

The Fund 15

FINANCIAL HIGHLIGHTS (continued)

| Year Ended October 31, | ||||||||||

| Class I Shares | 2012 | 2011 | 2010 | 2009 | 2008 | a | ||||

| Per Share Data ($): | ||||||||||

| Net asset value, beginning of period | 9.39 | 10.18 | 9.47 | 7.61 | 12.50 | |||||

| Investment Operations: | ||||||||||

| Investment income—netb | .18 | .11 | .11 | .01 | .05 | |||||

| Net realized and unrealized | ||||||||||

| gain (loss) on investments | .44 | (.74 | ) | .86 | 2.12 | (4.94 | ) | |||

| Total from Investment Operations | .62 | (.63 | ) | .97 | 2.13 | (4.89 | ) | |||

| Distributions: | ||||||||||

| Dividends from investment income—net | (.20 | ) | (.16 | ) | (.14 | ) | (.27 | ) | — | |

| Dividends from net realized | ||||||||||

| gain on investments | — | — | (.12 | ) | — | — | ||||

| Total Distributions | (.20 | ) | (.16 | ) | (.26 | ) | (.27 | ) | — | |

| Net asset value, end of period | 9.81 | 9.39 | 10.18 | 9.47 | 7.61 | |||||

| Total Return (%) | 6.82 | (6.33 | ) | 10.34 | 28.89 | (39.12 | )c | |||

| Ratios/Supplemental Data (%): | ||||||||||

| Ratio of total expenses | ||||||||||

| to average net assetsd | .06 | .05 | .05 | .24 | 14.86 | e | ||||

| Ratio of net expenses | ||||||||||

| to average net assetsd | .06 | .04 | .04 | .08 | .06 | e | ||||

| Ratio of net investment income | ||||||||||

| to average net assetsd | 1.91 | 1.07 | 1.10 | .16 | .54 | e | ||||

| Portfolio Turnover Rate | 30.63 | 16.15 | 20.78 | 36.68 | 25.65 | c | ||||

| Net Assets, end of period ($ x 1,000) | 462,450 | 475,017 | 352,131 | 163,611 | 30 | |||||

| a | From December 18, 2007 (commencement of operations) to October 31, 2008. |

| b | Based on average shares outstanding at each month end. |

| c | Not annualized. |

| d | Amounts do not include the activity of the underlying funds. |

| e | Annualized. |

See notes to financial statements.

16

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus Diversified International Fund (the “fund”) is a separate diversified series of Dreyfus Premier Investment Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company currently offering eight series, including the fund.The fund’s investment objective is to seek long-term capital appreciation. The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of NewYork Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares.The fund is authorized to issue 400 million shares of $.001 par value Common Stock.The fund currently offers three classes of shares: Class A (200 million shares authorized), Class C (100 million shares authorized) and Class I (100 million shares authorized). Class A shares are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class I shares are sold at net asset value per share only to institutional investors. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Fund 17

NOTES TO FINANCIAL STATEMENTS (continued)

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

The Company enters into contracts that contain a variety of indemnifications.The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

18

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Investments are valued at the net asset value of each underlying fund determined as of the close of the NewYork Stock Exchange (generally 4 p.m., Eastern time) on the valuation date and are generally categorized within Level 1 of the fair value hierarchy.

The following is a summary of the inputs used as of October 31, 2012 in valuing the fund’s investments:

| Level 2—Other | Level 3— | |||

| Level 1— | Significant | Significant | ||

| Unadjusted | Observable | Unobservable | ||

| Quoted Prices | Inputs | Inputs | Total | |

| Assets ($) | ||||

| Investments in Securities: | ||||

| Mutual Funds | 471,582,034 | — | — | 471,582,034 |

| † See Statement of Investments for additional detailed categorizations. | ||||

At October 31, 2012, there were no transfers between Level 1 and Level 2 of the fair value hierarchy.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses

The Fund 19

NOTES TO FINANCIAL STATEMENTS (continued)

from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

(c) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” in the Act. Investments in affiliated investment companies for the period ended October 31, 2012 were as follows:

| Affiliated | ||||||||

| Investment | Value | Net Realized | ||||||

| Company | 10/31/2011 | ($) | Purchases ($)† | Sales ($) | Gain (Loss) ($) | |||

| Dreyfus Emerging | ||||||||

| Asia Fund, Cl. I | 9,271,508 | 1,970,075 | 10,156,994 | (4,437,025 | ) | |||

| Dreyfus Emerging | ||||||||

| Markets Fund, Cl. I | 37,334,770 | 41,588,810 | 21,489,051 | (7,425,878 | ) | |||

| Dreyfus International | ||||||||

| Equity Fund, Cl. I | 121,861,408 | 21,706,556 | 28,703,745 | (4,976,086 | ) | |||

| Dreyfus International | ||||||||

| Value Fund, Cl. I | 72,430,987 | 15,006,650 | 31,777,735 | (6,045,770 | ) | |||

| Dreyfus/Newton | ||||||||

| International Equity | ||||||||

| Fund, Cl. I | 96,234,584 | 42,638,181 | 26,183,277 | (3,525,271 | ) | |||

| International Stock | ||||||||

| Fund, Cl. I | 148,758,880 | 22,628,346 | 53,757,025 | (4,715,333 | ) | |||

| Total | 485,892,137 | 145,538,618 | 172,067,827 | (31,125,363 | ) | |||

| † Includes reinvested dividends/distributions. | ||||||||

| Change in Net | ||||||||

| Affiliated | Unrealized | |||||||

| Investment | Appreciation | Value | Net | Dividends/ | ||||

| Company | (Depreciation) ($) | 10/31/2012 | ($) | Assets (%) Distributions ($) | ||||

| Dreyfus Emerging | ||||||||

| Asia Fund, Cl. I | 3,352,436 | — | — | — | ||||

| Dreyfus Emerging | ||||||||

| Markets Fund, Cl. I | 1,795,062 | 51,803,713 | 11.0 | 3,875,288 | ||||

| Dreyfus International | ||||||||

| Equity Fund, Cl. I | 11,309,148 | 121,197,281 | 25.7 | 2,780,543 | ||||

| Dreyfus International | ||||||||

| Value Fund, Cl. I | 1,696,586 | 51,310,718 | 10.9 | 2,401,689 | ||||

| Dreyfus/Newton | ||||||||

| International Equity | ||||||||

| Fund, Cl. I | 10,818,669 | 119,982,886 | 25.5 | 3,445,867 | ||||

| International Stock | ||||||||

| Fund, Cl. I | 14,372,568 | 127,287,436 | 27.0 | 1,706,954 | ||||

| Total | 43,344,469 | 471,582,034 | 100.1 | 14,210,341 | ||||

20

(d) Dividends to shareholders: Dividends are recorded on the ex-dividend date. Dividends from investment income-net and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(e) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended October 31, 2012, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended October 31, 2012 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At October 31, 2012, the components of accumulated earnings on a tax basis were as follows: accumulated capital losses $19,174,282 and unrealized appreciation $34,876,735. In addition, the fund deferred for tax purposes late year ordinary losses of $67,695 to the first day of the following fiscal year.

Under the Regulated Investment Company Modernization Act of 2010 (the “2010 Act”), the fund is permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 (“post-enactment losses”) for an unlimited period. Furthermore, post-

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

enactment capital loss carryovers retain their character as either short-term or long-term capital losses rather than short-term as they were under previous statute.The 2010 Act requires post-enactment losses to be utilized before the utilization of losses incurred in taxable years prior to the effective date of the 2010 Act (“pre-enactment losses”).As a result of this ordering rule, pre-enactment losses may be more likely to expire unused.

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net realized capital gains, if any, realized subsequent to October 31, 2012. If not applied, $415,833 of the carryover expires in fiscal year 2018 and $943,756 expires in fiscal year 2019. The fund has $5,222,723 of post-enactment short-term capital losses and $12,591,970 of post-enactment long-term capital losses which can be carried forward for an unlimited period.

The tax character of distributions paid to shareholders during the fiscal periods ended October 31, 2012 and October 31, 2011 were as follows: ordinary income $9,524,510 and $6,025,868, respectively.

During the period ended October 31, 2012, as a result of permanent book to tax differences, primarily due to the tax treatment for short-term capital gain distributions from regulated investment company holdings, the fund increased accumulated undistributed investment income-net by $419,969 and decreased accumulated net realized gain (loss) on investments by the same amount. Net assets and net asset value per share were not affected by this reclassification.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $225 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of New York Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus, (each, a “Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. Effective October 10,

22

2012, the $225 million unsecured credit facility with Citibank, N.A., was decreased to $210 million. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended October 31, 2012, was approximately $311,200 with a related weighted average annualized interest rate of 1.19%.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement with the Manager, there is no management fee paid to the Manager. The fund invests in other mutual funds advised by the Manager. All fees and expenses of the underlying funds are reflected in the underlying funds’ net asset value.

The Dreyfus Corporation has contractually agreed, until March 1, 2013, to assume the expenses of the fund so that the total annual fund and underlying funds operating expenses of none of the classes (excluding Rule 12b-1 Distribution Plan fees, Shareholder Services Plan fees, taxes, interest expense, brokerage commissions, commitment fees on borrowings and extraordinary expenses) exceed 1.20% of the value of the fund’s average daily net assets.The reduction in expenses, pursuant to the undertaking, amounted to $1,098 during the period ended October 31, 2012.

During the period ended October 31, 2012, the Distributor retained $83 from commissions earned on sales of the fund’s Class A shares.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of the average daily net assets of Class C shares. During the period ended October 31, 2012, Class C shares were charged $1,566, pursuant to the Distribution Plan.

The Fund 23

NOTES TO FINANCIAL STATEMENTS (continued)

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services.The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts.The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry professionals) in respect of these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended October 31, 2012, Class A and Class C shares were charged $24,204 and $522 respectively, pursuant to the Shareholder Services Plan.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates DreyfusTransfer, Inc. (“DTI”), a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing transfer agency services for the fund and, since May 29, 2012, cash management services related to fund subscriptions and redemptions. During the period ended October 31, 2012, the fund was charged $4,069 for transfer agency services and $61 for cash management services. Cash management fees were partially offset by earnings credits of $7.These fees are included in Shareholder servicing costs in the Statement of Operations.

The fund compensatesThe Bank of NewYork Mellon under a custody agreement for providing custodial services for the fund. During the period ended October 31, 2012, the fund was charged $5,096 pursuant to the custody agreement.

Prior to May 29, 2012, the fund compensated The Bank of NewYork Mellon under a cash management agreement for performing cash management services related to fund subscriptions and redemptions.

24

During the period ended October 31, 2012, the fund was charged $227 pursuant to the cash management agreement, which is included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $8.

During the period ended October 31, 2012, the fund was charged $8,517 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: Distribution Plan fees $75, Shareholder Services Plan fees $1,887, custodian fees $1,679, Chief Compliance Officer fees $2,654 and transfer agency fees $670.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

(e) A 2% redemption fee is charged and retained by the fund on certain shares redeemed within sixty days following the date of issuance, subject to exceptions, including redemptions made through the use of the fund’s exchange privilege. During the period ended October 31, 2012, redemption fees charged and retained by the fund amounted to $187.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended October 31, 2012, amounted to $145,538,618 and $172,067,827, respectively.

At October 31, 2012, the cost of investments for federal income tax purposes was $436,705,299; accordingly, accumulated net unrealized appreciation on investments was $34,876,735, consisting of $49,229,624 gross unrealized appreciation and $14,352,889 gross unrealized depreciation.

The Fund 25

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Dreyfus Diversified International Fund

We have audited the accompanying statement of assets and liabilities, including the statement of investments, of Dreyfus Diversified International Fund (one of the series comprising Dreyfus Premier Investment Funds, Inc.) as of October 31, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2012 by correspondence with the custodian and others.We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus Diversified International Fund at October 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the indicated periods, in conformity with U. S. generally accepted accounting principles.

New York, New York

December 27, 2012

26

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund elects to provide each shareholder with their portion of the fund’s foreign taxes paid and the income sourced from foreign countries. Accordingly, the fund hereby reports the following information regarding its fiscal year ended October 31, 2012:

—the total amount of taxes paid to foreign countries was $1,287,547.

—the total amount of income sourced from foreign countries was $9,355,230.

For federal tax purposes, the fund hereby reports 98.22% of the ordinary dividends paid during the fiscal year ended October 31, 2012 as qualifying for the corporate dividends received deduction. Also certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $9,355,230 represents the maximum amount that may be considered qualified dividend income. Shareholders will receive notification in early 2013 of the percentage applicable to the preparation of their 2012 income tax returns.

The Fund 27

PROXY RESULTS (Unaudited)

The Company held a special meeting of shareholders on August 3, 2012.The proposal considered at the meeting, and the results, are as follows:

| Shares | |||

| Votes For | Authority Withheld | ||

| To elect additional Board Members: | |||

| Peggy C. Davis† | 125,042,328 | 610,092 | |

| Ehud Houminer† | 125,002,253 | 650,167 | |

| Martin Peretz† | 125,018,821 | 633,599 |

† Each new Board Member’s term commenced on September 1, 2012.

In addition, Joseph S. DiMartino, David P. Feldman, Lynn Martin, Robin A. Melvin and Philip L.Toia continue as Board Members of the Company.

28

INFORMATION ABOUT THE RENEWAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Directors held on June 28, 2012, the Board considered the renewal of the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below.The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund.The Board considered information previously provided to them in presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex, and Dreyfus representatives confirmed that there had been no material changes in this information. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex (such as retail direct or intermediary, in which intermediaries typically are paid by the fund and/or Dreyfus) and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each intermediary or distribution channel, as applicable to the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements.The Board also considered Dreyfus’ extensive administrative, accounting, and compliance infrastructures.

The Fund 29

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended May 31, 2012, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds. The Board discussed the results of the comparisons and noted that the fund’s total return performance was below the Performance Group medians and variously above and below the Performance Universe medians.The Board noted that the fund ranked in the fourth quartile of the Performance Group for all periods. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index, and it was noted that the fund’s return was above the return of the benchmark index in three of the four calendar years.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons. The

30

Board noted that, like the other funds in the Expense Group, the fund’s advisory fees are paid only at the underlying funds’ level.They further noted that the fund’s total expense ratio was below the Expense Group and Expense Universe medians.

Dreyfus representatives noted that Dreyfus has contractually agreed, until March 1, 2013, to assume the expenses of the fund so that the total annual fund and underlying funds operating expenses of none of the classes (excluding Rule 12b-1 Distribution Plan fees, Shareholder Services Plan fees, taxes, interest expense, brokerage commissions, commitment fees on borrowings and extraordinary expenses) exceed 1.20% of the fund’s average daily net assets.

Dreyfus representatives reviewed with the Board the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager(s) for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus does not receive direct profits from the fund’s management fee, as the fund pays no direct management fee. As such, the Board did not consider an evaluation of profitability or economies of scale to be relevant. The Board also considered potential benefits to Dreyfus from acting as investment adviser and noted that there were no soft dollar arrangements in effect for trading the fund’s investments.

The Fund 31

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

At a special Board meeting held on April 23, 2012, the Board approved consolidating the fund’s Board with the boards of certain other funds in The Dreyfus Family of Funds, effective September 1, 2012, subject to the election of the new Board members by shareholders of the fund (the “Board Consolidation”). It was noted that, to align the renewal dates of the Management Agreements of the funds involved in the Board Consolidation, management recommended changing the fund’s Management Agreement renewal date to March 30th, subject to shareholder election of the new Board members for the fund.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

The Board noted Dreyfus’ efforts to improve, and agreed to closely monitor, performance.

As described above, the Board did not consider profitability or economies of scale to be relevant since the fund does not pay a direct management fee.

In evaluating the Agreement, the Board considered these conclusions and determinations and also relied on its previous knowledge, gained through meetings and other interactions with Dreyfus and its affiliates, of the fund and the services provided to the fund by Dreyfus.The Board also relied on information received on a routine and regular basis

32

throughout the year relating to the operations of the fund and the investment management and other services provided under the Agreement, including information on the investment performance of the fund in comparison to similar mutual funds and benchmark performance indices; general market outlook as applicable to the fund; and compliance reports. In addition, it should be noted that the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of prior or similar agreements during which lengthy discussions took place between the Board and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board’s conclusions may be based, in part, on their consideration of the same or similar arrangements in prior years.The Board determined that renewal of the Agreement through March 30, 2013, subject to shareholder approval of the Board Consolidation as described above, was in the best interests of the fund and its shareholders.

The Fund 33

BOARD MEMBERS INFORMATION (Unaudited)

| Joseph S. DiMartino (69) |

| Chairman of the Board (1995) |

| Principal Occupation During Past 5Years: |

| • Corporate Director and Trustee |

| Other Public Company Board Memberships During Past 5Years: |

| • CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small |

| and medium size companies, Director (1997-present) |

| • Sunair Services Corporation, a provider of certain outdoor-related services to homes and |

| businesses, Director (2005-2009) |

| • The Newark Group, a provider of a national market of paper recovery facilities, paperboard |

| mills and paperboard converting plants, Director (2000-2010) |

| No. of Portfolios for which Board Member Serves: 157 |

| ——————— |

| Peggy C. Davis (69) |

| Board Member (2012) |

| Principal Occupation During Past 5Years: |

| • Shad Professor of Law, New York University School of Law (1983-present) |

| No. of Portfolios for which Board Member Serves: 63 |

| ——————— |

| David P. Feldman (72) |

| Board Member (1991) |

| Principal Occupation During Past 5Years: |

| • Corporate Director and Trustee |

| Other Public Company Board Memberships During Past 5Years: |

| • BBH Mutual Funds Group (4 registered mutual funds), Director (1992-present) |

| • QMed, Inc. a healthcare company, Director (1999-2007) |

| No. of Portfolios for which Board Member Serves: 46 |

| ——————— |

| Ehud Houminer (72) |

| Board Member (2012) |

| Principal Occupation During Past 5Years: |

| • Executive-in-Residence at the Columbia Business School, Columbia University (1992-present) |

| Other Public Company Board Memberships During Past 5Years: |

| • Avnet Inc., an electronics distributor, Director (1993-2012) |

| No. of Portfolios for which Board Member Serves: 73 |

34

| Lynn Martin (72) |

| Board Member (1993) |

| Principal Occupation During Past 5Years: |

| • President of The Martin Hall Group LLC, a human resources consulting firm, from January |

| 2005-present |

| Other Public Company Board Memberships During Past 5Years: |

| • AT&T Inc., a telecommunications company, Director (1999-2012) |

| • Ryder System, Inc., a supply chain and transportation management company, Director (1993-2012) |

| • The Proctor & Gamble Co., a consumer products company, Director (1994-2009) |

| • Constellation Energy Group Inc., Director (2003-2009) |

| No. of Portfolios for which Board Member Serves: 46 |

| ——————— |

| Robin A. Melvin (49) |

| Board Member (2011) |

| Principal Occupation During Past 5Years: |

| • Director, Boisi Family Foundation, a private family foundation that supports youth-serving orga- |

| nizations that promote the self sufficiency of youth from disadvantaged circumstances (1995-2012) |

| No. of Portfolios for which Board Member Serves: 83 |

| ——————— |

| Dr. Martin Peretz (73) |

| Board Member (2012) |

| Principal Occupation During Past 5Years: |

| • Editor-in-Chief Emeritus of The New Republic Magazine (2010-present) (previously, |

| Editor-in-Chief, 1974-2010) |

| • Director of TheStreet.com, a financial information service on the web (1996-present) |

| No. of Portfolios for which Board Member Serves: 46 |

| ——————— |

| Philip L. Toia (79) |

| Board Member (1997) |

| Principal Occupation During Past 5Years: |

| • Private Investor |

| No. of Portfolios for which Board Member Serves: 56 |

| ——————— |

| Once elected all Board Members serve for an indefinite term, but achieve Emeritus status upon reaching age 80.The |

| address of the Board Members and Officers is c/o The Dreyfus Corporation, 200 Park Avenue, NewYork, NewYork |

| 10166.Additional information about the Board Members is available in the fund’s Statement of Additional Information |

| which can be obtained from Dreyfus free of charge by calling this toll free number: 1-800-DREYFUS. |

| Daniel Rose, Emeritus Board Member |

| Sander Vanocur, Emeritus Board Member |

The Fund 35

OFFICERS OF THE FUND (Unaudited)

36

The Fund 37

Dreyfus

Emerging Asia Fund

ANNUAL REPORT October 31, 2012

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Contents | |

THE FUND | |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 8 | Understanding Your Fund’s Expenses |

| 8 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 9 | Statement of Investments |

| 12 | Statement of Assets and Liabilities |

| 13 | Statement of Operations |

| 14 | Statement of Changes in Net Assets |

| 15 | Financial Highlights |

| 18 | Notes to Financial Statements |

| 31 | Report of Independent Registered Public Accounting Firm |

| 32 | Important Tax Information |

| 33 | Proxy Results |

| 34 | Information About the Renewal of the Fund’s Management and Sub-Investment Advisory Agreements |

| 39 | Board Members Information |

| 41 | Officers of the Fund |

FOR MORE INFORMATION | |

Back Cover |

Dreyfus

Emerging Asia Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus Emerging Asia Fund, covering the 12-month period from November 1, 2011, through October 31, 2012. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

Despite pronounced stock market weakness during the spring of 2012, stocks generally advanced over the reporting period as investors responded to encouraging macroeconomic developments throughout the world. Employment gains in the United States, credible measures to prevent a more severe banking crisis in Europe, and the likelihood of a “soft landing” for China’s economy buoyed investor sentiment, as did aggressively accommodative monetary policies from central banks in the United States, Europe, Japan and China. Consequently, U.S. stocks across all capitalization ranges posted double-digit returns, on average, for the reporting period.

In light of the easy monetary policies adopted by many countries, we expect global growth to be slightly more robust in 2013 than in 2012.The U.S. economic recovery is likely to persist at subpar levels over the first half of the new year, as growth may remain constrained by uncertainties surrounding fiscal policy and tax reforms. However, successful resolution of the current fiscal debate may prompt corporate decision-makers to increase capital spending, which could have positive implications for the U.S. economy and domestic equity markets.As always, we encourage you to stay in touch with your financial advisor as new developments unfold.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

November 15, 2012

2

DISCUSSION OF FUND PERFORMANCE

For the period of November 1, 2011, through October 31, 2012, as provided by Hugh Simon, Raymond Chan and Abhijit Sarkar, Portfolio Managers of Hamon Asian Advisors LTD, Sub-Investment Adviser

Fund and Market Performance Overview

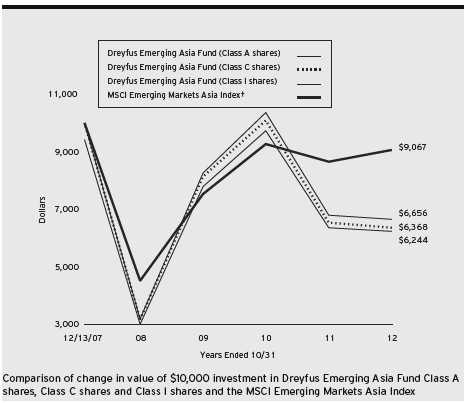

For the 12-month period ended October 31, 2012, Dreyfus Emerging Asia Fund’s Class A shares produced a total return of –1.90%, Class C shares returned –2.69% and Class I shares returned –2.12%.1 In comparison, the fund’s benchmark, the MSCI Emerging Markets Asia Index (the “Index”), produced a total return of 4.68% for the same period.2

Improving economic sentiment in the midst of accommodative policy initiatives in China and other Asian countries sent stocks higher over the reporting period.The fund produced lower returns than its benchmark, largely due to its overweighted exposure to small- and midcap stocks at a time when large-cap stocks fared better, as well as the weighting in the Chinese and Indian markets.

The Fund’s Investment Approach

The fund, which seeks long-term capital appreciation, normally invests at least 80% of its net assets in stocks of companies that are located or principally traded in Asian emerging market countries or other investments that are tied economically to Asian emerging markets. The fund may invest in the stocks of companies of any market capitalization. To determine where the fund will invest, we analyze several factors, including economic, demographic and political trends in Asian emerging market countries, the current financial condition and future prospects of individual companies and sectors in the Asian emerging markets, and the valuation of one market or company relative to that of another.

Accommodative Policies Drove Asian Equities Higher

The reporting period began in the wake of major stock market declines in Asia stemming from global economic weakness and inflation-fighting measures in China that threatened to derail the region’s economic growth.

Macroeconomic conditions appeared to improve in 2012, as Chinese policymakers felt more comfortable reducing short-term interest rates and injecting liquidity into the

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

local banking system. Although these stimulative measures took some time to have a significant impact on economic data, China began to post evidence of sustainable improvement during the third quarter of the year. In response, investment capital flowed back into emerging Asian equity markets, sparking rallies that erased previous losses and enabled the Index to produce a positive absolute return for the reporting period overall. However, the rebound was concentrated primarily among certain individual markets and large-cap stocks that comprise most of the benchmark, while small- and midcap stocks ended the reporting period with lower returns.

Small- and Midcap Focus Affected Relative Performance

An emphasis on smaller stocks helped the fund produce impressive results in previous reporting periods, but it proved counterproductive over the past year when cautious investors mainly focused on large, dividend-paying stocks. Consequently, some of the fund’s holdings remained out of favor. For example, Korean chemicals producer LG Chem lost value during the economic slowdown, but we believe the company is poised to advance as the regional economy improves. In India, industrial and building service consultancy SREI Infrastructure and financial services provider IFCI lost value early in the reporting period, when interest rates rose in response to central banks’ inflation-fighting policies. From an industry group perspective, the fund’s relative performance was hampered by disappointments in the information technology, materials and consumer discretionary sectors.

The fund achieved better results compared to its benchmark in the industrials sector, where China State Construction International Holdings advanced when the Chinese government made affordable housing a policy priority. Among consumer staples stocks, Indian beverages producer United Spirits received an acquisition offer from global giant Diageo at a premium to its stock price at the time. In other areas, Security Bank in the Philippines responded positively to its focus on a growing middle class of consumers, and luxury carmaker Brilliance China Automotive Holdings, a joint venture with Germany’s Bayerische Motoren Werke, gained value as higher end Chinese consumers flocked to the iconic BMW brand.

Emerging Asia Appears Poised for Growth

As of the reporting period’s end, we are optimistic regarding the region’s economic prospects.The recent adoption of policies designed to stimulate growth and promote

4

market liquidity in China are expected to produce encouraging results over the months ahead, and India has launched a number of tax and regulatory reforms that seem likely to boost foreign investment and drive its stock market higher. What’s more, equity valuations generally have declined to attractive levels and could rise as economic uncertainty wanes.

Therefore, we have retained the fund’s relatively constructive investment posture, including overweighted exposure to China and India. As of the reporting period’s end, we have favored interest rate-sensitive stocks that we believe will respond positively to lower rates, as well as consumer discretionary companies that are positioned to serve an expanding middle class. In contrast, we have identified relatively few stocks meeting our investment criteria in the utilities, telecommunications services and energy sectors.

November 15, 2012

Please note, the position in any security highlighted with italicized typeface was sold during the reporting period. Emerging markets tend to be more volatile than the markets of more mature economies, and generally have less diverse and less mature economic structures and less stable political systems than those of developed countries.The securities of companies located in emerging markets are often subject to rapid and large changes in price.An investment in this fund should be considered only as a supplement to a complete investment program for those investors willing to accept the greater risks associated with investing in emerging market countries.

Equity funds are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

The fund’s performance will be influenced by political, social and economic factors affecting investments in foreign companies. Special risks associated with investments in foreign companies include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards.These risks are enhanced in emerging market countries.