UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-06520

AMG Funds I

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203)299-3500

Date of fiscal year end: OCTOBER 31

Date of reporting period: NOVEMBER 1, 2018 – OCTOBER 31, 2019

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

| | |

| | ANNUALREPORT |

| | | | | | | | |

| | | | | AMG Funds October 31, 2019

AMG GW&K Core Bond ESG Fund (formerly AMG GW&K Core Bond Fund) |

| | | | | |

| | | | | Class N: MBGVX | | Class I: MBDFX | | Class Z: MBDLX |

| | | | | AMG GW&K Trilogy Emerging Wealth Equity Fund (formerly AMG Trilogy Emerging Wealth Equity Fund) |

| | | | | |

| | | | | Class N: TYWVX | | Class I: TYWSX | | Class Z: TYWIX |

| | | |

| | | | | AMG GW&K Trilogy Emerging Markets Equity Fund (formerly AMG Trilogy Emerging Markets Equity Fund) |

| | | | | |

| | | | | Class N: TLEVX | | Class I: TLESX | | Class Z: TLEIX |

| | | | | |

| | | | | | | | | |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (https://www.amgfunds.com/resources/order_literature.html), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting your financial intermediary or, if you invest directly with the Funds, by logging into your account at www.amgfunds.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1.800.548.4539 to inform the Funds that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds in the AMG Funds Family of Funds held in your account if you invest through your financial intermediary or all funds in the AMG Funds Family of Funds held with the fund complex if you invest directly with the Funds.

| | | | |

| amgfunds.com | | | | 103119 AR069 |

| | |

| | | AMG Funds Annual Report — October 31, 2019 |

| | | | | | |

| | | |

| | | | | | | |

| | | TABLE OF CONTENTS | | PAGE | |

| | | | |

| | | LETTER TO SHAREHOLDERS | | | 2 | |

| | | |

| | | ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| | | |

| | | PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| | | |

| | | AMG GW&K Core Bond ESG Fund | | | 4 | |

| | | |

| | | AMG GW&K Trilogy Emerging Wealth Equity Fund | | | 12 | |

| | | |

| | | AMG GW&K Trilogy Emerging Markets Equity Fund | | | 21 | |

| | | |

| | | FINANCIAL STATEMENTS | | | | |

| | | |

| | | Statement of Assets and Liabilities | | | 28 | |

| | | |

| | | Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | | | | |

| | | |

| | | Statement of Operations | | | 30 | |

| | | |

| | | Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| | | |

| | | Statements of Changes in Net Assets | | | 31 | |

| | | |

| | | Detail of changes in assets for the past two fiscal years | | | | |

| | | |

| | | Financial Highlights | | | 32 | |

| | | |

| | | Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| | | |

| | | Notes to Financial Statements | | | 41 | |

| | | |

| | | Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| | | |

| | | REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 48 | |

| | | |

| | | OTHER INFORMATION | | | 49 | |

| | | |

| | | TRUSTEES AND OFFICERS | | | 50 | |

| | | |

| | | ANNUAL RENEWAL OF INVESTMENT MANAGEMENT AND SUBADVISORY AGREEMENTS | | | 52 | |

| | | | | | | |

|

| Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds family of mutual funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. | |

| | |

| | Letter to Shareholders |

Dear Shareholder:

The U.S. bull market celebrated its 10-year anniversary during the fiscal year ended October 31, 2019, as stocks proved resilient in the face of global economic weakness, rising geopolitical tensions, and the ongoing trade war. Global stock markets swooned late in 2018 as hawkish U.S. Federal Reserve (Fed) policy and an escalation of the U.S./China trade war triggered a painful selloff. However, a dovish pivot from global central banks rescued investors and fueled a strong rebound early in 2019. Investors clung to hopes of a positive outcome from U.S./China trade negotiations, even as doubts about the durability of the economic cycle lingered, and the S&P 500® Index returned 14.33% for the fiscal year. International equities were also resistant to pressures facing the global economy and generated an 11.27% return as measured by the MSCI All Country World ex USA Index.

In total, ten out of eleven sectors of the S&P 500® Index were strongly positive during the prior twelve months. Investors sought the relative safety of defensive sectors, with utilities and real estate leading the index with returns of 26.73% and 23.71%, respectively. However, the higher growth information technology sector also generated a robust 22.60% return. Energy was the lone negative sector with a return of (11.40)% during the fiscal year. Growth stocks outperformed Value stocks for the full fiscal year with returns of 17.10% and 11.21% for the Russell 1000® Growth and Russell 1000® Value Indexes, respectively. The cycle of U.S. outperformance over international equities continued, but international developed and emerging markets still produced solidly positive returns, with the MSCI EAFE and MSCI Emerging Markets Index returning 11.04% and 11.86%, respectively, in the twelve months ending October 31, 2019.

Interest rates fell dramatically over the fiscal year and led to strong returns for bond investors as the Fed shifted to a more dovish policy stance early in 2019 and eventually cut short-term rates later in the year. The 10-year Treasury yield fell from a high of 3.24% last November to a yield of 1.69% as of October 31, 2019. The plunge in long-term interest rates caused the yield curve to briefly invert with 2-year yields rising higher than the 10-year yields. The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, ended the fiscal year with an 11.51% return. High yield bonds lagged the broader bond market and returned 8.38% as measured by the return of the Bloomberg Barclays U.S. Corporate High Yield Bond Index. Municipal bonds also performed strongly with a 9.42% return for the Bloomberg Barclays Municipal Bond Index.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. AMG Funds

provides access to a distinctive array of actively managed return-oriented investment strategies. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Keitha Kinne

President

AMG Funds

| | | | | | | | | | | | | | |

| Average Annual Total Returns | | Periods ended

October 31, 2019* | |

| | | | |

| Stocks: | | | | 1 Year | | | 3 Years | | | 5 Years | |

| | | | |

Large Caps | | (S&P 500® Index) | | | 14.33 | % | | | 14.91% | | | | 10.78% | |

| | | | |

Small Caps | | (Russell 2000® Index) | | | 4.90 | % | | | 10.96% | | | | 7.37% | |

| | | | |

International | | (MSCI All Country World Index ex USA) | | | 11.27 | % | | | 8.07% | | | | 3.82% | |

| Bonds: | | | | | | | | | | | |

| | | | |

Investment Grade | | (Bloomberg Barclays U.S. Aggregate Bond Index) | | | 11.51 | % | | | 3.29% | | | | 3.24% | |

| | | | |

High Yield | | (Bloomberg Barclays U.S. Corporate High Yield Bond Index) | | | 8.38 | % | | | 6.03% | | | | 5.18% | |

| | | | |

Tax-exempt | | (Bloomberg Barclays Municipal Bond Index) | | | 9.42 | % | | | 3.62% | | | | 3.55% | |

| | | | |

Treasury Bills | | (ICE BofAML U.S. 6-Month Treasury Bill Index) | | | 2.71 | % | | | 1.74% | | | | 1.21% | |

*Source: FactSet. Past performance is no guarantee of future results.

2

|

About Your Fund’s Expenses |

| | | | | | | | |

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below. ACTUAL EXPENSES The first line of the following table provides information about the actual account values and | | | | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | | | | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| | | | | | | | |

| | | | | | | | |

| | | | |

Six Months Ended October 31, 2019 | | Expense

Ratio for

the Period | | Beginning

Account

Value

05/01/19 | | Ending

Account

Value

10/31/19 | | Expenses

Paid

During

the Period* |

AMG GW&K Core Bond ESG Fund |

|

Based on Actual Fund Return |

| | | | |

Class N | | 0.88% | | $1,000 | | $1,058 | | $4.56 |

| | | | |

Class I | | 0.55% | | $1,000 | | $1,060 | | $2.86 |

| | | | |

Class Z | | 0.48% | | $1,000 | | $1,060 | | $2.49 |

|

Based on Hypothetical 5% Annual Return |

| | | | |

Class N | | 0.88% | | $1,000 | | $1,021 | | $4.48 |

| | | | |

Class I | | 0.55% | | $1,000 | | $1,022 | | $2.80 |

| | | | |

Class Z | | 0.48% | | $1,000 | | $1,023 | | $2.45 |

AMG GW&K Trilogy Emerging Wealth Equity Fund |

|

Based on Actual Fund Return |

| | | | |

Class N | | 1.35% | | $1,000 | | $959 | | $6.67 |

| | | | |

Class I | | 1.06% | | $1,000 | | $961 | | $5.24 |

| | | | |

Class Z | | 0.96% | | $1,000 | | $962 | | $4.75 |

|

Based on Hypothetical 5% Annual Return |

| | | | |

Class N | | 1.35% | | $1,000 | | $1,018 | | $6.87 |

| | | | |

Class I | | 1.06% | | $1,000 | | $1,020 | | $5.40 |

| | | | |

Class Z | | 0.96% | | $1,000 | | $1,020 | | $4.89 |

| | | | | | | | |

| | | | |

Six Months Ended October 31, 2019 | | Expense

Ratio for

the Period | | Beginning

Account

Value

05/01/19 | | Ending

Account

Value

10/31/19 | | Expenses

Paid

During

the Period* |

AMG GW&K Trilogy Emerging Markets Equity Fund |

|

Based on Actual Fund Return |

| | | | |

Class N | | 1.48% | | $1,000 | | $966 | | $7.34 |

| | | | |

Class I | | 1.13% | | $1,000 | | $968 | | $5.61 |

| | | | |

Class Z | | 0.92% | | $1,000 | | $969 | | $4.56 |

|

Based on Hypothetical 5% Annual Return |

| | | | |

Class N | | 1.48% | | $1,000 | | $1,018 | | $7.53 |

| | | | |

Class I | | 1.13% | | $1,000 | | $1,020 | | $5.75 |

| | | | |

Class Z | | 0.92% | | $1,000 | | $1,021 | | $4.69 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

|

AMG GW&K Core Bond ESG Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | |

For the 12 months ending October 31, 2019, the AMG GW&K Core Bond ESG Fund (Class I shares) (the “Fund”) returned 11.70%, compared to the return of 11.51% for the Bloomberg Barclays U.S. Aggregate Bond Index (the “Index”). On May 1, 2019, the AMG GW&K Core Bond Fund changed its name to the AMG GW&K Core Bond ESG Fund. While the Fund’s overall investment process remains the same, the Fund transitioned to an environmental, social, and governance (“ESG”) mandate. GW&K believes that responsible corporate behavior with respect to ESG factors can lead to positive and sustainable long-term financial performance and aligns with our pursuit of quality investments. GW&K has been incorporating ESG factors into our equity and fixed income analysis process for several years and as a signatory of the United Nations Principles for Responsible Investment (PRI), we are committed to incorporating the assessment of ESG issues into our fundamental research process. We believe ESG investing adds value to our investment process by improving our assessment of risk and enhancing our ability to identify high quality credits; aids our up-in-quality bias by improving identification of credits with less long-term volatility; limits our exposure to credit rating downgrades and negative events that are difficult to quantify; and deepens our fundamental credit analysis, leading to better outcomes by providing a more nuanced and complete picture. ESG considerations have long informed our process. We focus on business and credit fundamentals, relative valuation, and technical considerations. We believe ESG factors are important considerations in analyzing a company’s business and financial policy, as they highlight non-financial risks that can significantly affect a company’s financial health over the long term. Just as with credit risks, investors require additional compensation for ESG risks, leading to potential inefficiencies in valuation. MARKET OVERVIEW Investor sentiment deteriorated significantly at the end of 2018 as markets grew increasingly concerned about global growth, tightening U.S. Federal Reserve (“Fed”) policy and escalating trade tensions with China. These concerns took precedence over domestic economic data that, on balance, remained solid. The dominant narrative of synchronized global growth suddenly shifted to a serious debate around whether the post-crisis economic recovery was coming to an end—or worse. As expected, the Fed | | | | raised rates and tilted in a dovish direction, but not nearly enough for investors, who wanted a pause. Instead the Fed merely signaled a modestly slower pace of tightening along with continued balance sheet reduction. Volatility surged as a result, and risk assets sold off in a swift and decisive rebuke of Fed policy. Fixed income markets started 2019 on a strong note, helped by the unusual combination of a sharp rally in rates and a significant tightening in spreads. The Fed’s reduced growth outlook and dovish posture were the major drivers of the yield curve’s downward shift, reflecting softening U.S. economic data and renewed growth concerns out of Europe and China. Risk assets proved to be largely immune to these worries, benefiting instead from a fierce snapback in sentiment following a brutal fourth quarter. Corporates were also helped by a better-than-expected earnings season and a favorable technical backdrop. The rising tension between these competing risk-on/risk-off narratives underscores the high degree of investor uncertainty as the cycle continues to age, and volatility is likely to remain elevated until a clearer picture of the economy emerges. Having benefited from a second straight quarter of lower rates and tighter spreads, fixed income markets posted their strongest first-half returns in almost 25 years. Escalating trade rhetoric, decelerating industrial activity, and rising geopolitical tensions stoked concerns about a worldwide recession and drove a global flight to safety. In response, central banks around the world made clear their willingness to move forward with caution—if not provide outright stimulus as conditions warrant. In the U.S., this shift resulted in a massive collapse of the yield curve, driven by the perception that the Federal Open Market Committee (“FOMC”) had capitulated by removing the word “patient” from its post-meeting statement. This move had the perverse effect of both validating the risk aversion that drove the rally in rates and emboldening investors in risky assets, who promptly sent equities back to record highs. Fixed income markets endured a volatile third quarter amid the tumult of the trade war, mounting evidence of a global slowdown, and an increase in political tensions in the U.S. and abroad. Trade negotiations between the U.S. and China were the primary cause of uncertainty, as rhetoric escalated dramatically before calming in the closing days on hopes that tensions might be easing. This turmoil coincided with further signs of deterioration out of Europe, where both Germany and the U.K. posted | | | | negative Gross Domestic Product (“GDP”) readings. Against this already challenging backdrop, several other narratives weighed on investor sentiment: Saudi Arabia sustained an attack on its crude infrastructure, the overnight funding market required emergency intervention from the Fed, and talk of an impeachment inquiry began to gain traction. Interest rates finished October mixed following a sharp Fed-driven rally over the final two days of the month. The decision to cut the federal funds rate by another quarter point was not a surprise, nor was the messaging of a high bar set for further easing. Even so, Treasury yields fell, with a slight flattening bias, after Fed Chairman Jerome Powell stated in his post-meeting press conference that any increase in inflation would need to be “significant” and “persistent” before the Fed “would even consider” raising rates from here. The move reversed much of the October selloff that had preceded the meeting. All month long, rates had been rising and the curve re-steepening as investors took comfort from global monetary stimulus and receding concerns over trade and Brexit. The yield on the 10-year Treasury reached as high as 1.86% before rallying to close October 31, 2019, at 1.70%, up only 3 basis points on the month. The yield on the Long Bond finished up 7 basis points, while the two- and five-year fell 10 and 3 basis points, respectively. FUND REVIEW The Fund’s overweight to investment grade corporates, which outperformed the Index, was a significant contributor to performance. For the one-year period ending October 2019, interest rates decreased, and the corporate sector outperformed due to its longer duration and 8 basis points of spread tightening. Positive security selection within investment grade corporates was a key contributor to performance during the 12-month period, even as security selection overall contributed marginally. Corporate selection in the electric, insurance, and basic industry sectors were notable positives, while selection in consumer non-cyclicals and communications detracted. Treasuries were modest underperformers versus the Index, so our underweight was helpful. We were generally equal weight mortgage-backed securities, and our allocation decision had minimal impact, but our MBS selection underperformed in the rate rally given our preference for shorter duration seasoned mortgage pools. We overweighted taxable municipal bonds, a sector that benefited due to the decrease in rates, although security selection within the space was a small drag. The Fund’s overall yield curve positioning |

4

|

AMG GW&K Core Bond ESG Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | |

added to performance. The 5- to 10-year segment of the curve experienced the largest declines in rates, which is where the Fund had its largest exposure. Conversely, rates on the very short and long ends saw drops of a lesser degree and the Fund had underweights in those areas. OUTLOOK Investor sentiment improved notably as bright spots emerged on U.S.-Chinese trade and Brexit, reducing the perceived threat to global growth. A relatively healthy read on the labor market, the strength of Q3 GDP growth, and solid corporate earnings helped to confirm that the manufacturing recession was not | | | | spilling over into the broader economy. The Fed made it clear that while they stand ready to add accommodation if needed, such an outcome is likely unnecessary. In light of all of these factors, we believe the U.S. expansion will continue. A healthy consumer and labor market coupled with an improving outlook for global growth support our preference for high-quality spread product. We believe that corporate bonds with above average and/or improving ESG profiles offer an attractive alternative to the Treasury market in an environment where the Fed has made it clear they are focused on extending the credit cycle. We see value in the lower-rated segment of the investment grade space, | | | | where we believe the risk of ratings downgrades has received undue attention, especially in light of an accommodative Fed. The securitized sector remains a good hedge against the possibility of rising rates, offering a relatively attractive spread following the recent flurry of refinancing activity. The views expressed represent the opinions of GW&K Investment Management, LLC as of October 31, 2019, and are not intended as a forecast or guarantee of future results, and are subject to change without notice. |

5

|

AMG GW&K Core Bond ESG Fund Portfolio Manager’s Comments(continued) |

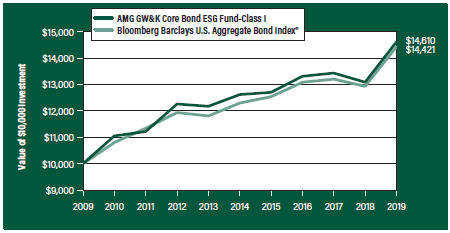

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG GW&K Core Bond ESG Fund’s (formerly AMG GW&K Core Bond Fund) cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the AMG GW&K Core Bond ESG Fund’s Class I shares on October 31, 2009 to a $10,000 investment made in the Bloomberg Barclays U.S. Aggregate Bond Index® for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG GW&K Core Bond ESG Fund and the Bloomberg Barclays U.S. Aggregate Bond Index® for the same time periods ended October 31, 2019.

| | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns1 | | One

Year | | | Five

Years | | | Ten

Years | | | Since

Inception | | | Inception

Date | |

AMG GW&K Core Bond ESG Fund2, 3, 4, 5, 6, 7, 8 | |

| | | | | |

Class N | | | 11.20% | | | | — | | | | — | | | | 2.70 | % | | | 05/08/15 | |

| | | | | |

Class I | | | 11.70% | | | | 2.99% | | | | 3.87% | | | | 5.85 | % | | | 04/30/93 | |

| | | | | |

Class Z | | | 11.71% | | | | — | | | | — | | | | 3.12 | % | | | 05/08/15 | |

| | | | | |

Bloomberg Barclays U.S. Aggregate Bond Index®9 | | | 11.51% | | | | 3.24% | | | | 3.73% | | | | 5.31 | % | | | 04/30/93 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and |

| | |

| | | capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of October 31, 2019. All returns are in U.S. dollars ($). 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. 4 Active and frequent trading of a fund may result in higher transaction costs and increased tax liability. 5 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. 6 The Fund may invest in derivatives such as options and futures; the complexity and rapidly changing structure of derivatives markets may increase the possibility of market losses. 7 Many bonds have call provisions which allow the debtors to pay them back before maturity. This is especially true with mortgage securities, which can be paid back anytime. Typically debtors prepay their debt when it is to their advantage (when interest rates drop making a new loan at current rates more attractive), and thus likely to the disadvantage of bondholders, who may have to reinvest prepayment proceeds in securities with lower yields. Prepayment risk will vary depending on the provisions of the security and current interest rates relative to the interest rate of the debt. |

| | | 8 Applying the Fund’s ESG investment criteria may result in the selection or exclusion of securities of certain issuers for reasons other than performance, and the Fund may underperform funds that do not utilize an ESG investment strategy. The application of this strategy may affect the Fund’s exposure to certain companies, sectors, regions, countries or types of investments, which could negatively impact the Fund’s performance depending on whether such investments are in or out of favor. Applying ESG crieria to investment decisions is qualitative and subjective by nature, and there is no guarantee that the criteria utilized by the Subadvisr or any judgment exercised by the Subadviser will reflect the beliefs or values of any particular investor. 9 The Bloomberg Barclays U.S. Aggregate Bond Index® is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds. Unlike the Fund, the |

6

|

AMG GW&K Core Bond ESG Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | |

Bloomberg Barclays U.S. Aggregate Bond Index® is unmanaged, is not available for investment, and does not incur expenses. Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of | | | | Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to | | | | be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. Not FDIC insured, nor bank guaranteed. May lose value. |

7

|

AMG GW&K Core Bond ESG Fund Fund Snapshots(unaudited) October 31, 2019 |

PORTFOLIO BREAKDOWN

| | |

| Category | | % of Net Assets |

| | |

U.S. Government and Agency Obligations | | 46.5 |

| | |

Corporate Bonds and Notes | | 43.7 |

| | |

Municipal Bonds | | 7.6 |

| | |

Short-Term Investments | | 1.6 |

| | |

Other Assets Less Liabilities | | 0.6 |

| |

| Rating | | % of Market Value1 |

| | |

U.S. Government and Agency Obligations | | 47.5 |

| | |

Aa | | 17.5 |

| | |

A | | 19.0 |

| | |

Baa | | 16.0 |

| 1 | Includes market value of long-term fixed-income securities only. |

TOP TEN HOLDINGS

| | |

| Security Name | | % of

Net Assets |

United States Treasury Notes, 2.000%, 11/30/22 | | 4.1 |

| | |

United States Treasury Bonds, 4.500%, 02/15/36 | | 4.0 |

| | |

FNMA, 4.500%, 06/01/41 | | 2.7 |

| | |

FNMA, 4.000%, 12/01/33 | | 2.6 |

| | |

FNMA, 4.500%, 04/01/39 | | 2.6 |

| | |

FNMA, 4.500%, 04/01/39 | | 2.6 |

| | |

FHLMC, 2.500%, 10/01/34 | | 2.5 |

| | |

FNMA, 3.500%, 03/01/48 | | 2.3 |

| | |

United States Treasury Notes, 6.250%, 08/15/23 | | 2.1 |

| | |

Verizon Communications, Inc., 3.875%, 02/08/29 | | 2.1 |

| | | |

| | |

Top Ten as a Group | | 27.6 |

| | |

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service, Inc. (“Moody’s”). These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

8

|

AMG GW&K Core Bond ESG Fund Schedule of Portfolio Investments October 31, 2019 |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

Corporate Bonds and Notes - 43.7% | | | | | | | | |

| | |

Financials - 19.2% | | | | | | | | |

| | |

Aircastle, Ltd. | | | | | | | | |

4.125%, 05/01/24 | | | $3,073,000 | | | | $3,216,002 | |

| | |

Ally Financial, Inc. | | | | | | | | |

8.000%, 11/01/31 | | | 1,535,000 | | | | 2,143,244 | |

| | |

American Tower Corp. | | | | | | | | |

3.375%, 10/15/26 | | | 1,628,000 | | | | 1,694,632 | |

| | |

Bank of America Corp., MTN | | | | | | | | |

3.875%, 08/01/25 | | | 3,534,000 | | | | 3,814,087 | |

| | |

The Bank of New York Mellon Corp., MTN | | | | | | | | |

2.450%, 08/17/26 | | | 1,049,000 | | | | 1,060,752 | |

| | |

Berkshire Hathaway, Inc. | | | | | | | | |

3.125%, 03/15/26 | | | 3,151,000 | | | | 3,353,565 | |

| | |

Boston Properties, LP | | | | | | | | |

3.400%, 06/21/29 | | | 2,045,000 | | | | 2,158,868 | |

| | |

Citigroup, Inc. | | | | | | | | |

(3 month LIBOR + 1.023%) | | | | | | | | |

4.044%, 06/01/241 | | | 3,485,000 | | | | 3,691,928 | |

| | |

CME Group, Inc. | | | | | | | | |

3.750%, 06/15/28 | | | 930,000 | | | | 1,044,330 | |

| | |

Crown Castle International Corp. | | | | | | | | |

4.000%, 03/01/27 | | | 2,021,000 | | | | 2,188,758 | |

| | |

The Goldman Sachs Group, Inc. | | | | | | | | |

3.500%, 11/16/26 | | | 3,141,000 | | | | 3,275,030 | |

| | |

Host Hotels & Resorts, LP | | | | | | | | |

Series C | | | | | | | | |

4.750%, 03/01/23 | | | 2,429,000 | | | | 2,591,609 | |

| | |

JPMorgan Chase & Co. | | | | | | | | |

2.950%, 10/01/26 | | | 2,163,000 | | | | 2,234,332 | |

| | |

Morgan Stanley, GMTN | | | | | | | | |

(3 month LIBOR + 1.628%) | | | | | | | | |

4.431%, 01/23/301 | | | 1,919,000 | | | | 2,156,854 | |

| | |

National Rural Utilities Cooperative | | | | | | | | |

Finance Corp., MTN | | | | | | | | |

3.250%, 11/01/25 | | | 2,072,000 | | | | 2,185,082 | |

| | |

Simon Property Group LP | | | | | | | | |

3.300%, 01/15/26 | | | 2,057,000 | | | | 2,181,628 | |

| | |

Visa, Inc., MTN | | | | | | | | |

3.150%, 12/14/25 | | | 2,574,000 | | | | 2,753,727 | |

| | |

Total Financials | | | | | | | 41,744,428 | |

| | |

Industrials - 23.5% | | | | | | | | |

| | |

Advocate Health & Hospitals Corp. | | | | | | | | |

4.272%, 08/15/48 | | | 2,006,000 | | | | 2,392,373 | |

| | |

AT&T, Inc. | | | | | | | | |

4.250%, 03/01/27 | | | 3,955,000 | | | | 4,347,273 | |

| | |

Automatic Data Processing, Inc. | | | | | | | | |

3.375%, 09/15/25 | | | 3,067,000 | | | | 3,299,268 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

Charter Communications Operating LLC/Charter Communications Operating Capital | | | | | | | | |

4.908%, 07/23/25 | | | $2,472,000 | | | | $2,725,640 | |

| | |

Cheniere Corpus Christi Holdings LLC | | | | | | | | |

5.875%, 03/31/25 | | | 2,889,000 | | | | 3,210,661 | |

| | |

CommonSpirit Health | | | | | | | | |

3.347%, 10/01/29 | | | 2,609,000 | | | | 2,634,527 | |

| | |

CVS Health Corp. | | | | | | | | |

5.125%, 07/20/45 | | | 1,899,000 | | | | 2,192,324 | |

| | |

Exelon Corp. | | | | | | | | |

3.400%, 04/15/26 | | | 2,016,000 | | | | 2,122,396 | |

| | |

Fidelity National Information Services, Inc. | | | | | | | | |

5.000%, 10/15/25 | | | 1,901,000 | | | | 2,173,985 | |

| | |

The George Washington University | | | | | | | | |

Series 2018 | | | | | | | | |

4.126%, 09/15/48 | | | 3,023,000 | | | | 3,611,447 | |

| | |

Georgia-Pacific LLC | | | | | | | | |

8.000%, 01/15/24 | | | 1,628,000 | | | | 1,997,610 | |

| | |

Kaiser Foundation Hospitals | | | | | | | | |

3.150%, 05/01/27 | | | 2,111,000 | | | | 2,235,768 | |

| | |

Kinder Morgan, Inc. | | | | | | | | |

4.300%, 03/01/28 | | | 1,967,000 | | | | 2,135,352 | |

| | |

McDonald’s Corp., MTN | | | | | | | | |

3.700%, 01/30/26 | | | 2,553,000 | | | | 2,758,619 | |

| | |

Parker-Hannifin Corp. | | | | | | | | |

3.250%, 06/14/29 | | | 2,089,000 | | | | 2,196,102 | |

| | |

RELX Capital, Inc. | | | | | | | | |

4.000%, 03/18/29 | | | 2,014,000 | | | | 2,216,215 | |

| | |

Rockwell Automation, Inc. | | | | | | | | |

3.500%, 03/01/29 | | | 2,027,000 | | | | 2,213,631 | |

| | |

Verizon Communications, Inc. | | | | | | | | |

3.875%, 02/08/29 | | | 4,042,000 | | | | 4,473,887 | |

| | |

Waste Management, Inc. | | | | | | | | |

3.450%, 06/15/29 | | | 2,007,000 | | | | 2,175,156 | |

| | |

Total Industrials | | | | | | | 51,112,234 | |

| | |

Utilities - 1.0% | | | | | | | | |

| | |

Northern States Power Co. | | | | | | | | |

2.900%, 03/01/50 | | | 2,197,000 | | | | 2,143,482 | |

| | |

Total Corporate Bonds and Notes | | | | | | | | |

(Cost $89,898,025) | | | | | | | 95,000,144 | |

| | |

Municipal Bonds - 7.6% | | | | | | | | |

| | |

California State General Obligation, | | | | | | | | |

School Improvements | | | | | | | | |

7.550%, 04/01/39 | | | 2,650,000 | | | | 4,351,751 | |

| | |

JobsOhio Beverage System, Series B | | | | | | | | |

4.532%, 01/01/35 | | | 1,890,000 | | | | 2,262,576 | |

| | |

Los Angeles Unified School District, | | | | | | | | |

School Improvements | | | | | | | | |

5.750%, 07/01/34 | | | 2,905,000 | | | | 3,787,452 | |

The accompanying notes are an integral part of these financial statements.

9

|

AMG GW&K Core Bond ESG Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

Metropolitan Transportation Authority | | | | | | | | |

6.687%, 11/15/40 | | | $1,875,000 | | | | $2,672,081 | |

| | |

University of California, University & College Improvements, Series BD | | | | | | | | |

3.349%, 07/01/29 | | | 3,215,000 | | | | 3,482,777 | |

| | |

Total Municipal Bonds | | | | | | | | |

(Cost $15,390,277) | | | | | | | 16,556,637 | |

| | |

| U.S. Government and Agency Obligations - 46.5% | | | | | | | | |

| | |

Fannie Mae - 27.2% | | | | | | | | |

| | |

FNMA | | | | | | | | |

3.000%, 09/01/46 to 11/01/46 | | | 4,984,012 | | | | 5,117,746 | |

3.500%, 03/01/30 to 03/01/48 | | | 11,702,567 | | | | 12,287,342 | |

4.000%, 12/01/33 to 11/01/48 | | | 16,007,970 | | | | 17,125,098 | |

4.500%, 04/01/39 to 06/01/41 | | | 18,508,594 | | | | 20,069,532 | |

5.000%, 08/01/40 | | | 4,038,968 | | | | 4,458,669 | |

| | |

Total Fannie Mae | | | | | | | 59,058,387 | |

| | |

Freddie Mac - 8.0% | | | | | | | | |

| | |

FHLMC | | | | | | | | |

2.500%, 10/01/34 | | | 5,303,091 | | | | 5,385,847 | |

| | |

FHLMC Gold Pool | | | | | | | | |

3.000%, 06/01/43 | | | 341,400 | | | | 353,734 | |

3.500%, 07/01/32 to 05/01/44 | | | 2,694,696 | | | | 2,833,689 | |

4.000%, 05/01/26 | | | 162,675 | | | | 169,673 | |

5.000%, 07/01/44 | | | 2,878,927 | | | | 3,182,505 | |

| | |

FHLMC Multifamily Structured Pass | | | | | | | | |

Through Certificates | | | | | | | | |

Series K071, Class A2 | | | | | | | | |

3.286%, 11/25/27 | | | 2,012,000 | | | | 2,177,365 | |

Series K062, Class A2 | | | | | | | | |

3.413%, 12/25/26 | | | 513,000 | | | | 559,348 | |

Series K063, Class A2 | | | | | | | | |

3.430%, 01/25/271 | | | 2,544,000 | | | | 2,767,785 | |

| | |

Total Freddie Mac | | | | | | | 17,429,946 | |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| |

U.S. Treasury Obligations - 11.3% | | | | | |

| | |

United States Treasury Bonds | | | | | | | | |

3.500%, 02/15/39 | | | $1,750,000 | | | | $2,173,042 | |

4.500%, 02/15/36 | | | 6,312,000 | | | | 8,648,919 | |

| | |

United States Treasury Notes | | | | | | | | |

2.000%, 11/30/22 | | | 8,892,000 | | | | 9,019,649 | |

6.250%, 08/15/23 | | | 3,947,000 | | | | 4,631,712 | |

Total U.S. Treasury Obligations | | | | | | | 24,473,322 | |

| | |

Total U.S. Government and Agency Obligations | | | | | | | | |

(Cost $98,781,344) | | | | | | | 100,961,655 | |

| | |

| | | Shares | | | | | |

| | |

Short-Term Investments - 1.6% | | | | | | | | |

| |

Other Investment Companies - 1.6% | | | | | |

| | |

Dreyfus Government Cash Management Fund, | | | | | | | | |

Institutional Shares, 1.73%2 | | | 1,153,067 | | | | 1,153,067 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 1.77%2 | | | 1,153,068 | | | | 1,153,068 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 1.75%2 | | | 1,188,010 | | | | 1,188,010 | |

| | |

Total Short-Term Investments

(Cost $3,494,145) | | | | | | | 3,494,145 | |

| | |

Total Investments - 99.4%

(Cost $207,563,791) | | | | | | | 216,012,581 | |

| |

Other Assets, less Liabilities - 0.6% | | | | 1,251,978 | |

| | |

Net Assets - 100.0% | | | | | | | $217,264,559 | |

| 1 | Variable rate security. The rate shown is based on the latest available information as of October 31, 2019. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

| 2 | Yield shown represents the October 31, 2019, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| GMTN | Global Medium-Term Notes |

| LIBOR | London Interbank Offered Rate |

The accompanying notes are an integral part of these financial statements.

10

|

AMG GW&K Core Bond ESG Fund Schedule of Portfolio Investments(continued) |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of October 31, 2019:

| | | | | | | | | | | | | | | | | | | | |

| | | Level 1 | | Level 2 | | Level 3 | | Total |

Investments in Securities | | | | | | | | | | | | | | | | | | | | |

Corporate Bonds and Notes† | | | | — | | | | | $95,000,144 | | | | | — | | | | | $95,000,144 | |

Municipal Bonds | | | | — | | | | | 16,556,637 | | | | | — | | | | | 16,556,637 | |

U.S. Government and Agency Obligations† | | | | — | | | | | 100,961,655 | | | | | — | | | | | 100,961,655 | |

Short-Term Investments | | | | | | | | | | | | | | | | | | | | |

Other Investment Companies | | | $ | 3,494,145 | | | | | — | | | | | — | | | | | 3,494,145 | |

| | | | | | | | | | | | | | | | | | | | |

Total Investments in Securities | | | $ | 3,494,145 | | | | $ | 212,518,436 | | | | | — | | | | $ | 216,012,581 | |

| | | | | | | | | | | | | | | | | | | | |

| † | All corporate bonds and notes and U.S. government and agency obligations held in the Fund are Level 2 securities. For a detailed breakout of corporate bonds and notes and U.S. government and agency obligations by major industry or agency classification, please refer to the Fund’s Schedule of Portfolio Investments. |

For the fiscal year ended October 31, 2019, there were no transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

11

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | |

MARKET OVERVIEW Global equity markets experienced sharp declines in the final quarter of 2018, with the MSCI All Country World Index posting the worst annual performance since the global financial crisis of 2008. Notably, after leading global markets down in the previous two quarters, the MSCI Emerging Markets Index displayed relative strength during December. In response to firm U.S. economic data, the U.S. Federal Reserve (the “Fed”) delivered its fourth rate hike in December, the ninth hike of the tightening cycle, while giving only modestly dovish guidance about its future intentions. Moving into 2019, emerging market equities participated in the strong global rally and posted a first quarter gain which was the largest advance since the first quarter of 2017, erasing the sharp decline of the previous quarter. The same factors that boosted global developed markets were also at play in emerging markets, such as dovish signals from key central banks (the Fed and the European Central Bank), optimism on U.S.-China trade negotiations, and early signs of stabilization in China’s economy. Overall, emerging market currencies held their ground against the U.S. dollar, while oil and industrial commodity prices firmed as concerns about the global economy began to ease. Although the MSCI Emerging Markets Index rose in the first quarter, it remained significantly below its peak level reached in January 2018 and lagged the first quarter gain of the MSCI All Country World Index. Following the strong rally in the first quarter, emerging market equities ended the second quarter of 2019 with relatively flat performance due to tepid economic reports and an escalation of trade tensions. The flat performance for the second quarter masked considerable volatility within the quarter as markets responded negatively to a breakdown in U.S.-China trade negotiations. Evidence mounted that the trade war was resulting in a significant slowdown in global manufacturing activity as supply chains were disrupted while businesses put capital spending plans on hold. However, emerging market equities were able to recover in June as investors correctly discounted that the U.S. and China would agree at the end of the month to postpone further tariff hikes and resume negotiations. Emerging market equities continued to lag developed markets, with developed market equities posting their strongest first-half gain since 1998. The wide performance spread between emerging and developed markets in 2019 reflects the differential impact of weaker global manufacturing | | | | activity and ongoing tension surrounding U.S.-China trade negotiations. The confrontational tone between the two countries has hit emerging market assets particularly hard. Emerging market equities posted a decline for the third quarter of 2019, but ended off the period’s worst levels. There were signs of an easing of U.S.-China tensions in September, with China resuming some purchases of U.S. agricultural goods in advance of formal trade talks. In addition, investors have been focusing on the tempering effect of central bank policy actions to offset the global slowdown. A total of 16 central banks cut rates in the third quarter, led by two cuts by the Fed. That said, China has so far refrained from aggressive monetary easing. Its future policy stance remains an important wild card since China accounts for about one-third of global growth. During the two prior global downturns of 2008 and 2016, inflections in global growth required strong stimulus by China. Finishing off the fiscal year, emerging market equities did well in October but continued to lag developed markets for the calendar-year-to-date period. Several factors contributed to the improved environment for emerging market equities. First, market participants took comfort from the continued broad-based monetary easing by central banks. Second, a de-escalation of trade issues between the U.S. and China helped market sentiment. On October 11, the U.S. and China reached a tentative “Phase One” agreement on key trade issues. The U.S. agreed to hold off on tariff hikes scheduled for October 15 and December 15. In exchange, China offered key concessions on agricultural purchases and financial sector opening. But no deal has been signed, so there remains the risk of last-minute histrionics. Finally, odds of a no-deal Brexit also declined. Brexit now looks likely to proceed on January 31 next year. FUND REVIEW For the one-year period ending October 31, 2019, the AMG GW&K Trilogy Emerging Wealth Equity Fund (the “Fund”) (Class Z shares) returned 21.34%, outperforming the MSCI Emerging Markets Index (the “Index”), which returned 11.86%. Looking at performance on a sector basis, stock selection in the financial, consumer staples, and health care sectors represented the largest contributors to relative performance. Although stock selection detracted from performance in the consumer discretionary sector, the Fund’s large overweight allocation more than offset it, resulting in a positive impact on performance. Finally, holdings in the materials sector added to relative performance for the year. These positives were partially offset by holdings in the | | | | communication services and information technology sectors, as well as an underweight allocation in information technology. Geographically, stock selection in Asia, particularly China, was by far the largest contributor to relative performance for the fiscal year. Stock selection and an underweight allocation in South Korea also helped performance versus the Index while an underweight allocation in Taiwan detracted from performance within the region. Within the Latin America and EMEA regions, stock selection and underweight allocations versus the Index helped on a relative basis. Finally, within developed markets, positive performance from U.S. holdings more than offset the negative returns in Germany and Denmark. OUTLOOK AND PORTFOLIO POSITION Looking forward, we see continued low inflation levels in most emerging market countries as supportive for further monetary easing and economic growth, albeit at more modest levels. As the third quarter earnings season progresses, business trends in the Fund’s consumer-focused companies remain healthy. We believe earnings growth for the Fund will be between 8% and 10% for 2019, followed by low-double-digit growth in 2020 and 2021, providing further support to already compelling valuations. Volatility will likely continue as investors balance political risks, trade discussions, and accommodative central bank policies globally. This continued volatility will create further opportunities to invest in best-in-class companies serving the emerging consumer. Ongoing discussions between the U.S. and China will most likely result in a trade agreement that will be executed in several phases over an extended period of time. In the meantime, the shift toward consumption in emerging markets remains undeterred. Not only do we continue to see high consumer confidence and strong consumption in China, despite the headline news, we also note that premium segments are growing at approximately twice the pace of overall Chinese consumption. In India, after broad monetary and fiscal stimulus, the government has now moved to support important labor-intensive industries including the auto industry, where a cash-for-clunkers program is under consideration. We continue to believe the combination of strong earnings growth and compelling valuations could present investors with a strong snap-back in emerging markets, and we would like to remind investors of the benefit of an emerging wealth allocation, as we believe the emerging consumer will be the most compelling growth story for the next couple of decades. |

12

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | |

Investors with a long-term investment horizon, as well as patience and focus on the underlying fundamentals of companies rather than the latest news, could reap sustainable excess returns in emerging markets as the world faces a scarcity of growth opportunities. We believe the underlying trends in emerging markets are very powerful for the companies within the Fund. Patience is required and we believe investors will be rewarded. With respect to the Fund’s structure, trading and market activity during the fiscal year resulted in increased exposures to the consumer discretionary, | | | | health care, information technology, materials, and industrial sectors while exposures to the consumer staples, communication services, and financial sectors decreased. At the close of the period, the Fund had overweight positions in the consumer discretionary and health care sectors and underweight positions in the energy, information technology, materials, communication services, industrial, real estate, utilities, and consumer staples sectors relative to the benchmark. Geographically, | | | | the portfolio finished the fiscal year with exposures of 68% in EM Asia, 22% in developed markets, 5% in EM EMEA, and 5% in EM Latin America. The views expressed represent the opinions of GW&K Investment Management, LLC as of October 31, 2019, and are not intended as a forecast or guarantee of future results, and are subject to change without notice. |

13

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Portfolio Manager’s Comments(continued) |

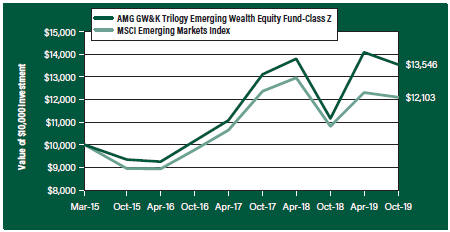

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG GW&K Trilogy Emerging Wealth Equity Fund’s (formerly AMG Trilogy Emerging Wealth Equity Fund) cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the AMG GW&K Trilogy Emerging Wealth Equity Fund’s Class Z shares on March 19, 2015 (inception date), to a $10,000 investment made in the MSCI Emerging Markets Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG GW&K Trilogy Emerging Wealth Equity Fund and the MSCI Emerging Markets Index for the same time periods ended October 31, 2019.

| | | | | | | | | | | | |

| Average Annual Total Returns1 | | One

Year | | | Since

Inception | | | Inception

Date | |

AMG GW&K Trilogy Emerging Wealth Equity Fund2, 3, 4, 5, 6, 7, 8 | | | | | | | | | | | | |

| | | |

Class N | | | 20.82 | % | | | 6.41 | % | | | 03/19/15 | |

| | | |

Class I | | | 21.15 | % | | | 6.69 | % | | | 03/19/15 | |

| | | |

Class Z | | | 21.34 | % | | | 6.79 | % | | | 03/19/15 | |

| | | |

MSCI Emerging Markets Index9 | | | 11.86 | % | | | 4.22 | % | | | 03/19/15 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.548.4539 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and |

| | |

| | | capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of October 31, 2019. All returns are in U.S. dollars ($). 2 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. These risks are magnified in emerging markets. 3 The Fund is subject to the risks associated with investments in emerging markets, such as erratic earnings patterns, economic and political instability, changing exchange controls, limitations on repatriation of foreign capital and changes in local governmental attitudes toward private investment, possibly leading to nationalization or confiscation of investor assets. 4 The Fund is subject to currency risk resulting from fluctuations in exchange rates that may affect the total loss or gain on a non-U.S. Dollar investment when converted back to U.S. Dollars. 5 The Fund may invest in derivatives such as options and futures; the complexity and rapidly changing structure of derivatives markets may increase the possibility of market losses. 6 The Fund is subject to risks associated with investments in mid-capitalization companies such as greater price volatility, lower trading volume, and less liquidity than the stocks of larger, more established companies. 7 The Fund is subject to risks associated with investments in small-capitalization companies, such as erratic earnings patterns, competitive conditions, limited earnings history and a reliance on one or a limited number of products. 8 Companies that are in similar businesses may be similarly affected by particular economic or market events; to the extent the Fund has substantial holdings within a particular sector, the risks associated with that sector increase. |

| | | 9 The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Please go to msci.com for most current list of countries represented by the index. Unlike the Fund, the MSCI Emerging Markets Index is unmanaged, is not available for investment and does not incur expenses. All MSCI data is provided “as is.” The products described herein are not sponsored or endorsed and have not been reviewed or passed on by MSCI. In no event shall MSCI, its affiliates or any MSCI data provider have any liability of any kind in connection with the MSCI data or the products described herein. |

14

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Portfolio Manager’s Comments(continued) |

| | | | | | | | |

Copying or redistributing the MSCI data is strictly prohibited. | | | | Not FIDC insured, not bank guaranteed. May lose value. | | | | |

15

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Fund Snapshots(unaudited) October 31, 2019 |

PORTFOLIO BREAKDOWN

| | |

| Sector | | % of Net Assets |

| | |

Consumer Discretionary | | 36.7 |

| | |

Financials | | 24.8 |

| | |

Information Technology | | 10.5 |

| | |

Communication Services | | 7.4 |

| | |

Health Care | | 6.3 |

| | |

Consumer Staples | | 5.3 |

| | |

Materials | | 3.4 |

| | |

Industrials | | 2.5 |

| | |

Short-Term Investments | | 5.6 |

| | |

Other Assets Less Liabilities | | (2.5) |

TOP TEN HOLDINGS

| | |

| Security Name | | % of

Net Assets |

Alibaba Group Holding, Ltd., Sponsored ADR (China) | | 6.0 |

| | |

Infineon Technologies AG (Germany) | | 5.8 |

| | |

Sands China, Ltd. (Macau) | | 4.9 |

| | |

Ping An Insurance Group Co. of China, Ltd., Class H (China) | | 4.7 |

| | |

HDFC Bank, Ltd., ADR (India) | | 4.3 |

| | |

Sberbank of Russia PJSC, Sponsored ADR (Russia) | | 4.0 |

| | |

AIA Group, Ltd. (Hong Kong) | | 4.0 |

| | |

QUALCOMM, Inc. | | 3.9 |

| | |

Tencent Holdings, Ltd. (China) | | 3.3 |

| | |

Trip.com Group, Ltd., ADR (China) | | 3.3 |

| | | |

| | |

Top Ten as a Group | | 44.2 |

| | |

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

16

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Schedule of Portfolio Investments October 31, 2019 |

| | | | | | | | |

| | | Shares | | | Value | |

| | |

Common Stocks - 96.9% | | | | | | | | |

| | |

Communication Services - 7.4% | | | | | | | | |

| | |

iQIYI, Inc., ADR (China)*,1 | | | 63,833 | | | | $1,112,609 | |

| | |

MultiChoice Group (South Africa)* | | | 37,798 | | | | 314,798 | |

| | |

Tencent Holdings, Ltd. (China) | | | 92,140 | | | | 3,737,467 | |

| | |

Tencent Music Entertainment Group, ADR (China)*,1 | | | 103,895 | | | | 1,437,907 | |

| | |

The Walt Disney Co. (United States) | | | 2,206 | | | | 286,604 | |

| | |

Zee Entertainment Enterprises, Ltd. (India) | | | 395,018 | | | | 1,451,339 | |

| | |

Total Communication Services | | | | | | | 8,340,724 | |

| | |

Consumer Discretionary - 36.7% | | | | | | | | |

| | |

Alibaba Group Holding, Ltd., Sponsored ADR (China)* | | | 38,781 | | | | 6,851,439 | |

| | |

Booking Holdings, Inc. (United States)* | | | 565 | | | | 1,157,555 | |

| | |

Eicher Motors, Ltd. (India) | | | 8,475 | | | | 2,686,988 | |

| | |

Hermes International (France) | | | 570 | | | | 410,601 | |

| | |

Huazhu Group Ltd., ADR (China)1 | | | 38,881 | | | | 1,472,035 | |

| | |

Jubilant Foodworks Ltd. (India) | | | 84,050 | | | | 1,894,594 | |

| | |

LVMH Moet Hennessy Louis Vuitton SE (France) | | | 3,660 | | | | 1,563,025 | |

| | |

MakeMyTrip, Ltd. (India)*,1 | | | 75,009 | | | | 1,726,707 | |

| | |

Maruti Suzuki India, Ltd. (India) | | | 30,688 | | | | 3,269,770 | |

| | |

Moncler SpA (Italy) | | | 37,312 | | | | 1,439,823 | |

| | |

Naspers, Ltd., N Shares (South Africa) | | | 5,353 | | | | 757,496 | |

| | |

New Oriental Education & Technology Group, Inc., Sponsored ADR (China)* | | | 7,148 | | | | 872,485 | |

| | |

NIKE, Inc., Class B (United States) | | | 6,301 | | | | 564,254 | |

| | |

Prosus, N.V. (Netherlands)* | | | 19,753 | | | | 1,362,147 | |

| | |

Sands China, Ltd. (Macau) | | | 1,131,000 | | | | 5,570,876 | |

| | |

Starbucks Corp. (United States) | | | 3,401 | | | | 287,589 | |

| | |

TAL Education Group, ADR (China)* | | | 28,850 | | | | 1,235,068 | |

| | |

Tiffany & Co. (United States)1 | | | 2,941 | | | | 366,184 | |

| | |

Titan Co., Ltd. (India) | | | 46,200 | | | | 866,771 | |

| | |

Trip.com Group, Ltd., ADR (China)* | | | 112,385 | | | | 3,707,581 | |

| | |

Yum China Holdings, Inc. (China) | | | 84,484 | | | | 3,590,570 | |

| | |

Total Consumer Discretionary | | | | | | | 41,653,558 | |

| | |

Consumer Staples - 5.3% | | | | | | | | |

| | |

The Estee Lauder Cos., Inc., Class A (United States) | | | 1,790 | | | | 333,423 | |

| | |

Kimberly-Clark de Mexico, SAB de CV, Class A (Mexico) | | | 135,260 | | | | 271,765 | |

| | |

Kweichow Moutai Co., Ltd., Class A (China) | | | 3,293 | | | | 551,469 | |

| | |

LG Household & Health Care, Ltd. (South Korea) | | | 2,490 | | | | 2,694,424 | |

| | |

Unilever NV (United Kingdom) | | | 3,439 | | | | 203,268 | |

| | |

Wal-Mart de Mexico, SAB de CV (Mexico) | | | 418,220 | | | | 1,253,366 | |

| | | | | | | | |

| | | Shares | | | Value | |

| | |

Wuliangye Yibin Co., Ltd., Class A (China) | | | 35,603 | | | | $666,411 | |

| | |

Total Consumer Staples | | | | | | | 5,974,126 | |

| | |

Financials - 24.8% | | | | | | | | |

| | |

AIA Group, Ltd. (Hong Kong) | | | 451,700 | | | | 4,498,130 | |

| | |

Bank Mandiri Persero Tbk PT (Indonesia) | | | 2,090,920 | | | | 1,045,187 | |

| | |

China Merchants Bank Co., Ltd., Class H (China) | | | 399,050 | | | | 1,903,162 | |

| | |

Credicorp, Ltd. (Peru) | | | 3,679 | | | | 787,453 | |

| | |

Grupo Financiero Banorte, S.A.B de CV (Mexico) | | | 374,370 | | | | 2,046,954 | |

| | |

HDFC Bank, Ltd., ADR (India) | | | 79,796 | | | | 4,874,738 | |

| | |

Kotak Mahindra (India) | | | 143,181 | | | | 3,175,711 | |

| | |

Ping An Insurance Group Co. of China, Ltd., Class H (China) | | | 459,000 | | | | 5,297,682 | |

| | |

Sberbank of Russia PJSC, Sponsored ADR (Russia) | | | 309,191 | | | | 4,553,243 | |

| | |

Total Financials | | | | | | | 28,182,260 | |

| | |

Health Care - 6.3% | | | | | | | | |

| | |

China Resources Sanjiu Medical & Pharmaceutical Co., Ltd., Class A (China) | | | 702,091 | | | | 2,937,827 | |

| | |

CSPC Pharmaceutical Group, Ltd. (China) | | | 238,000 | | | | 609,547 | |

| | |

Jiangsu Hengrui Medicine Co., Ltd., Class A (China) | | | 55,380 | | | | 714,469 | |

| | |

Novo Nordisk A/S, Class B (Denmark) | | | 13,509 | | | | 742,842 | |

| | |

Ping An Healthcare and Technology Co., Ltd. (China)*,1,2 | | | 314,300 | | | | 2,149,563 | |

| | |

Total Health Care | | | | | | | 7,154,248 | |

| | |

Industrials - 2.5% | | | | | | | | |

| | |

Copa Holdings, S.A., Class A (Panama) | | | 5,311 | | | | 540,341 | |

| | |

FANUC Corp. (Japan) | | | 9,230 | | | | 1,820,611 | |

| | |

Havells India, Ltd. (India) | | | 43,501 | | | | 423,841 | |

| | |

Total Industrials | | | | | | | 2,784,793 | |

| | |

Information Technology - 10.5% | | | | | | | | |

| | |

Infineon Technologies AG (Germany) | | | 339,205 | | | | 6,569,984 | |

| | |

Mastercard, Inc., Class A (United States) | | | 1,956 | | | | 541,440 | |

| | |

Pagseguro Digital, Ltd., Class A

(Brazil)*,1 | | | 10,240 | | | | 379,699 | |

| | |

QUALCOMM, Inc. (United States) | | | 55,266 | | | | 4,445,597 | |

| | |

Total Information Technology | | | | | | | 11,936,720 | |

| | |

Materials - 3.4% | | | | | | | | |

| | |

Asian Paints, Ltd. (India) | | | 62,004 | | | | 1,580,519 | |

| | |

Chr Hansen Holding A/S (Denmark) | | | 17,964 | | | | 1,379,200 | |

| | |

Novozymes A/S (Denmark) | | | 18,320 | | | | 863,597 | |

| | |

Total Materials | | | | | | | 3,823,316 | |

| | |

Total Common Stocks

| | | | | | | | |

(Cost $99,165,664) | | | | | | | 109,849,745 | |

The accompanying notes are an integral part of these financial statements.

17

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Schedule of Portfolio Investments(continued) |

| | | | | | | | |

| | | Principal

Amount | | | Value | |

| | |

Short-Term Investments - 5.6% | | | | | | | | |

| |

Joint Repurchase Agreements - 2.8%3 | | | | | |

| | |

Cantor Fitzgerald Securities, Inc., dated 10/31/19,due 11/01/19, 1.750% total to be received $1,000,049 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 9.000%, 11/25/19 - 10/20/68, totaling $1,020,041) | | | $1,000,000 | | | | $1,000,000 | |

| | |

Citigroup Global Markets, Inc., dated 10/31/19, due 11/01/19, 1.740% total to be received $1,000,048 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 2.500% - 8.000%, 12/01/20 - 01/01/59, totaling $1,020,000) | | | 1,000,000 | | | | 1,000,000 | |

| | |

Credit Suisse AG, dated 10/31/19, due 11/01/19, 1.730% total to be received $211,727 (collateralized by various U.S. Treasuries, 0.125% - 3.125%, 11/15/22 - 05/15/47, totaling $215,951) | | | 211,717 | | | | 211,717 | |

| | |

Guggenheim Securities LLC, dated 10/31/19, due 11/01/19, 1.760% total to be received $1,000,049 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 1.625% - 5.000%, 01/01/27 - 06/20/69, totaling $1,020,000) | | | 1,000,000 | | | | 1,000,000 | |

| | |

Total Joint Repurchase Agreements | | | | | | | 3,211,717 | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Other Investment Companies - 2.8% | | | | | |

| | |

Dreyfus Government Cash Management Fund, Institutional Shares, 1.73%4 | | | 1,035,029 | | | | $1,035,029 | |

| | |

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 1.77%4 | | | 1,035,029 | | | | 1,035,029 | |

| | |

JPMorgan U.S. Government Money Market Fund, IM Shares, 1.75%4 | | | 1,066,393 | | | | 1,066,393 | |

| | |

Total Other Investment Companies | | | | | | | 3,136,451 | |

| | |

Total Short-Term Investments | | | | | | | | |

(Cost $6,348,168) | | | | | | | 6,348,168 | |

| | |

Total Investments - 102.5% | | | | | | | | |

(Cost $105,513,832) | | | | | | | 116,197,913 | |

| |

Other Assets, less Liabilities - (2.5)% | | | | (2,793,817 | ) |

| | |

Net Assets - 100.0% | | | | | | | $113,404,096 | |

| * | Non-income producing security. |

| 1 | Some of these securities, amounting to $7,641,830 or 6.7% of net assets, were out on loan to various borrowers and are collateralized by cash and various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 2 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified buyers. At October 31, 2019, the value of these securities amounted to $2,149,563 or 1.9% of net assets. |

| 3 | Cash collateral received for securities lending activity was invested in these joint repurchase agreements. |

| 4 | Yield shown represents the October 31, 2019, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| ADR | American Depositary Receipt |

The accompanying notes are an integral part of these financial statements.

18

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Schedule of Portfolio Investments(continued) |

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of October 31, 2019:

| | | | | | | | | | | | | | | | | | | | |

| | | Level 1 | | Level 21 | | Level 3 | | Total |

Investments in Securities | | | | | | | | | | | | | | | | | | | | |

Common Stocks | | | | | | | | | | | | | | | | | | | | |

Consumer Discretionary | | | $ | 23,193,614 | | | | $ | 18,459,944 | | | | | — | | | | | $41,653,558 | |

Financials | | | | 7,709,145 | | | | | 20,473,115 | | | | | — | | | | | 28,182,260 | |

Information Technology | | | | 5,366,736 | | | | | 6,569,984 | | | | | — | | | | | 11,936,720 | |

Communication Services | | | | 4,288,459 | | | | | 4,052,265 | | | | | — | | | | | 8,340,724 | |

Health Care | | | | — | | | | | 7,154,248 | | | | | — | | | | | 7,154,248 | |

Consumer Staples | | | | 1,858,554 | | | | | 4,115,572 | | | | | — | | | | | 5,974,126 | |

Materials | | | | — | | | | | 3,823,316 | | | | | — | | | | | 3,823,316 | |

Industrials | | | | 540,341 | | | | | 2,244,452 | | | | | — | | | | | 2,784,793 | |

Short-Term Investments | | | | | | | | | | | | | | | | | | | | |

Joint Repurchase Agreements | | | | — | | | | | 3,211,717 | | | | | — | | | | | 3,211,717 | |

Other Investment Companies | | | | 3,136,451 | | | | | — | | | | | — | | | | | 3,136,451 | |

| | | | | | | | | | | | | | | | | | | | |

Total Investments in Securities | | | $ | 46,093,300 | | | | $ | 70,104,613 | | | | | — | | | | $ | 116,197,913 | |

| | | | | | | | | | | | | | | | | | | | |

| 1 | An external pricing service is used to reflect any impact on security value due to market movements between the time the Fund valued such foreign securities and the earlier closing of foreign markets. |

The following table below is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value at October 31, 2019:

| | | | | |

| | | Common

Stock |

Balance as of October 31, 2018 | | | | $244,523 | |

Accrued discounts (premiums) | | | | — | |

Realized gain (loss) | | | | — | |

Change in unrealized appreciation/depreciation | | | | — | |

Purchases | | | | — | |

Sales | | | | — | |

Transfers in to Level 3 | | | | — | |

Transfers out of Level 3 | | | | (244,523 | ) |

Balance as of October 31, 2019 | | | | — | |

| | | | | |

Net change in unrealized appreciation/depreciation on investments still held at October 31, 2019 | | | | — | |

The accompanying notes are an integral part of these financial statements.

19

|

AMG GW&K Trilogy Emerging Wealth Equity Fund Schedule of Portfolio Investments(continued) |

The country allocation in the Schedule of Portfolio Investments at October 31, 2019 is as follows:

| | | | |

| Country | | % of Long-Term

Investments |

Brazil | | | 0.3 | |

China | | | 35.4 | |

Denmark | | | 2.7 | |

France | | | 1.8 | |

Germany | | | 6.0 | |

Hong Kong | | | 4.1 | |

India | | | 20.0 | |

Indonesia | | | 0.9 | |

Italy | | | 1.3 | |

Japan | | | 1.7 | |

Macau | | | 5.1 | |

Mexico | | | 3.2 | |

Netherlands | | | 1.2 | |

Panama | | | 0.5 | |

Peru | | | 0.7 | |

Russia | | | 4.1 | |

South Africa | | | 1.0 | |

South Korea | | | 2.5 | |

United Kingdom | | | 0.2 | |

United States | | | 7.3 | |

| | | | | |

| |

| | | 100.0 | |

| | | | |

The accompanying notes are an integral part of these financial statements.

20

|

AMG GW&K Trilogy Emerging Markets Equity Fund Portfolio Manager’s Comments(unaudited) |

| | | | | | | | |