UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-6563

CALVERT WORLD VALUES FUND, INC.

(Exact name of registrant as specified in charter)

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Address of Principal Executive Offices)

William M. Tartikoff, Esq.

4550 Montgomery Avenue

Suite 1000N

Bethesda, Maryland 20814

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (301) 951-4800

Date of fiscal year end: September 30

Date of reporting period: Twelve months ended September 30, 2012

Item 1. Report to Stockholders.

[Calvert International Equity Fund Annual Report]

and

[Calvert Capital Accumulation Fund Annual Report]

and

[Calvert International Opportunities Fund Annual Report]

Choose Planet-friendly E-delivery!

Sign up now for on-line statements, prospectuses, and fund reports. In less than five minutes you can help reduce paper mail and lower fund costs.

Just go to www.calvert.com. If you already have an online account at Calvert, click on My Account, and select the documents you would like to receive via e-mail.

If you’re new to online account access, click on Login/Register to open an online account. Once you’re in, click on the E-delivery sign-up at the bottom of the Account Portfolio page and follow the quick, easy steps. Note: if your shares are not held directly at Calvert but through a brokerage firm, you must contact your broker for electronic delivery options available through their firm.

Dear Shareholder:

Stock markets ended the 2012 annual reporting period sharply higher as the Standard & Poor’s (S&P) 500 Index returned 30.20% versus 1.14% for the 12 months through September 30, 2011. While the two periods shared many commonalities--such as a softening of economic indicators, mounting concerns about sovereign debt in the eurozone, and relatively strong corporate profits--there were some key differences.

Financial markets around the world breathed a sigh of relief after the European Central Bank committed to saving the euro this summer and offered to support the debt markets for any euro member government seeking a new financial bailout. And while the disasters in Japan and strife in the Middle East and North Africa weighed heavily on investor confidence last year, uncertainty closer to home rattled investors this year, primarily as a result of the presidential election and looming “fiscal cliff” in January 2013 that could raise taxes for many Americans. The good news is both situations should see some resolution by the end of 2012.

The U.S. economy’s relative strength was also more evident in this annual reporting period. The divergence with foreign stock market returns widened as the S&P 500 Index more than doubled the 14.33% return of the MSCI EAFE Index for the 12-month period ending September 30, 2012. In the 12 months ending September 30, 2011, the S&P 500 barely eked out a positive return compared with -8.94% for the MSCI EAFE for the same period.

A Truly Uneven Recovery

Within the United States, the economic recovery was also uneven, with some consumers and businesses feeling left behind in the midst of an “improving” economy. For example, growth in northeastern metropolitan areas lagged, while metro areas out west, particularly those in natural gas or high-tech centers, rebounded strongly.1 Also, the housing market finally turned the corner, as national home prices rose 3.6% year-over-year for the past 12 months. However, they surged 9.4% in the western U.S. while notching up only 0.9% in the northeast.2 In employment, more than 70% of jobs lost in service industries during the recession have returned, but only 15% of jobs lost in manufacturing, construction, and other goods-producing industries have come back. The differences are stark even within industries, where retail general merchandisers such as Costco recouped 92% while department stores regained just 41% of lost jobs.3 Overall, we remain cautiously optimistic about the economic recovery ahead. As both citizens and investors, we hope that government legislators return to the negotiating table after the election and give us all the gift of more certainty before the holidays.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 4

Making Strides in Board Diversity

Calvert continued its advocacy efforts in many areas, including board diversity. The United Nations Gender Equality for Sustainable Business Event in March marked the two-year anniversary of the U.N.’s Women’s Empowerment Principles (WEP), which were adapted from the Calvert’s Women Principles®, and emphasized the business case for promoting gender equality and women’s empowerment in the workplace. Calvert also joined the newly formed WEP Leadership Group to expand implementation of the Principles.

On March 21, we testified before the Senate Democratic Steering and Outreach Committee about the importance of gender equity in economic empowerment and job creation, highlighting research showing the inclusion of women in corporate management correlates with higher shareholder value and better operating results.

Creating “The Future We Want” in Rio

Finally, I had the pleasure of representing Calvert by speaking at several events at the Rio + 20 Summit about board oversight of sustainability, social enterprise and impact investing, the role of business in promoting gender equality, the business case for the green economy, and establishing value for natural capital.

The first Earth Summit in Rio de Janeiro 20 years ago created climate and biodiversity conventions and set the stage for frameworks to address global environmental degradation, climate change, and poverty. However, global economic uncertainty weighed heavily on the Rio + 20 Summit. While negotiations continued to advance toward 2015, we’re disappointed by the lack of concrete commitments needed for substantial progress on critical sustainability issues.

However, side events sponsored by private-sector and non-governmental organizations sparked many innovative initiatives and positive outcomes. A number of major companies made significant commitments on water, energy, renewable materials, and deforestation. Corporate and investor disclosure of environmental, social, and governance (ESG) impacts took a real step forward as well. In fact, NASDAQ will now encourage companies on its exchange to report on ESG issues, or explain why they do not.

While these efforts can’t substitute for binding governmental commitments, we are happy to see so many companies and investors stepping up to the plate and believe the private sector will remain a key driver of progress on sustainability issues over the next few years.

Stay Informed in the Months Ahead

Maintaining a well-diversified mix of stocks, bonds, and cash appropriate for your goals and risk tolerance is one of the best ways to mitigate the effects of an uneven economic recovery. We also recommend discussing any changes in your financial situation with your investment advisor.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 5

A financial services consulting firm recently named Calvert as one of the Top Social Media Leaders in 2012 for using Facebook to share valuable content with investors and advisors.4 Join the dialogue at www.facebook.com/calvert.

We also invite you to visit our website, www.calvert.com, for fund information, portfolio updates, and commentary from Calvert professionals. You can now get the same information on the go with our new iPhone® app, available free at iTunes.

As always, we thank you for investing with Calvert.

Barbara Krumsiek

President and CEO of Calvert Investments, Inc.

October 2012

1. Brookings Institution, Metro Monitor - September 2012, www.brookings.edu/research/

interactives/metromonitor#overall

2. Clear Capital, “June Home Prices Provide Further Evidence of Budding Recovery. Forecast

Indicates Further Increases Through 2012,” July 2012 Market Report, http://clearcapital.com/

company/MarketReport.cfm?month=July&year=2012

3. Paul Davison and Barbara Hansen, “Service Businesses Lead Uneven Jobs Recovery,” USA

Today, July 15, 2012, www.usatoday.com/money/economy/story/2012-07-15/jobs-recov-

ered/56242656/1

4. kasina ranked Calvert fifth of 53 asset management and insurance companies for using

Facebook to tell a compelling brand story and share valuable content with investors and advi

sors. The ranking was based on kasina’s three-tier methodology that ranked firms based on

content, branding, interactivity, and usability on each social platform. For more information,

visit www.kasina.com.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 6

Landmark Rules on Conflict Minerals

After a complicated and controversial two-year rulemaking process, the Securities and Exchange Commission (SEC) released final rules under the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) Section 1502, which require companies to file and publish reports on their efforts to eliminate the use of “conflict minerals” that have fueled a violent 14-year conflict in the Eastern Democratic Republic of the Congo (DRC).

Calvert played a leading role among investors during the rulemaking process and is pleased with the progress. However, the two- to four-year timeline for compliance and exclusion of mining companies from reporting requirements was disappointing. We will continue to press all companies involved with conflict minerals to step up their efforts to address these issues.

New Standards Will Nearly Double Fuel Efficiency by 2025

Newly finalized corporate average fuel economy (CAFE) standards require cars and light-duty trucks to reach the equivalent of 54.5 mpg by 2025. Experts estimate the new standards will reduce oil consumption by 12 billion barrels while saving consumers $1.7 trillion. The major U.S. automakers supported the new standards and have already begun incorporating them into future vehicles.

The higher standards should boost both the competitiveness of American automakers and U.S. policy efforts to mitigate climate change, since more than 90% of a vehicle’s contribution to climate change through greenhouse gas emissions (GHGs) is related to fuel consumption.1 Calvert has long advocated for higher standards in public testimony to Environmental Protection Agency, meetings with Obama administration officials, dialogues with the auto industry, and the media and will continue to do so.

Helping Companies Combat Climate Change Risks

Economic and insured losses from natural catastrophes set new records last year, driving home the very real physical climate risks for investors. Extreme weather events accounted for 90% of the disasters and eight of the 10 most costly events, causing overall losses of more than $148 billion.

To that end, Calvert co-authored two reports to help companies evaluate their exposure to climate risks and protect shareholder value. Oxfam America and Ceres joined us to create Physical Risks from Climate Change: A guide for companies and investors on disclosure and management of climate impacts.

We also developed Value Chain Climate Resilience: A guide to managing climate impacts in companies and communities, a first-of-its-kind guide to help businesses assess and prepare for the risks and opportunities posed by climate change, with other leading companies from the Partnership for Resilience and Environmental Preparedness (PREP).

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 7

Exercising Our Say on Pay

Calvert fought for the new “say on pay” rule, which requires publicly traded U.S. companies to allow shareholders to vote on the compensation awarded to senior management the previous year. We built on that success this year by creating a strict set of voting guidelines on executive compensation for the proxy season. We also shared our reasons for voting against the proposals to management at key companies.

Overall, Calvert votes against compensation packages that do not align management and shareholder interests and do not incentivize the company’s long-term performance. In May, this meant voting against company compensation packages 34% of the time. This includes Gilead Sciences, Safeway, and Plains Exploration and Production, all of which rewarded CEOs with high pay in 2011 despite lackluster shareholder returns.

Even before the May announcement of a massive trading loss, we rejected the $23 million pay package for JPMorgan Chase Chairman and CEO Jamie Dimon due to its discretionary nature and inherent lack of accountability to long-term financial goals. The weaknesses in risk oversight evident by the company’s failed hedging strategy only reinforced our decision.

Other Shareholder Advocacy Efforts

This spring, Calvert filed 24 shareholder resolutions to keep the sustainability issues with a real impact on profits, people, and the planet front and center. Six were voted upon by shareholders, including resolutions on: -- Board diversity at Urban Outfitters, which received 39% support (up from 22% last year). Despite owning popular women’s retail brands Anthropologie and Free People, the company does not have any women or minorities on its board of directors.

-- Disclosure of water scarcity and pollution risks at Fossil, which received 31% support. As an apparel company, Fossil relies on water- and energy-intensive processes for producing cotton, leather, and other products. These processes can also pollute water supplies, especially in developing countries.

-- Sustainability reports at Gentex, which received 32% support. This supplier for the automotive, aerospace, and commercial fire protection industries currently provides no information on its efforts to manage resource efficiency and environmental impacts—despite increasing demands from its key clients for sustainability data.

Promoting Privacy on the Internet

In 2006, Calvert joined other investors, human rights advocacy organizations, academic experts and companies to develop the multi-stakeholder Global Network Initiative (GNI) to help information and communication technology (ICT) companies address freedom of expression and privacy issues. In early 2012, GNI’s path to becoming a fully global standard leapt forward as the first three GNI companies—Yahoo, Google, and Microsoft— completed the second phase of the assessment process.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 8

In addition, Facebook became a GNI observer in May, opening the door to its participation in GNI policy and advocacy discussions for one year as it evaluates the potential commitment of implementing the GNI principles. We welcome the opportunity to work with Facebook, particularly in protecting against privacy violations that can endanger members using it as an instrument of freedom of expression and political dissent across the world.

Community Investments

Many of our Funds participate in Calvert’s High Social Impact Investing program, which is administered through the Calvert Foundation. This community investment program may allocate a small percentage of Fund assets at below-market interest rates to investments that provide economic opportunity for struggling populations.2 One such investment through the Foundation is FMM Popayan, which offers financial services to more than 400,000 clients in some of the poorest areas of Columbia. Women comprise 66% of their client base.

We also supported the Triodos Sustainable Trade Fund, which seeks to improve the economic position of farmers in emerging markets and stimulate development in the sustainable agriculture sector. It does this by providing pre-export value chain financing to farmer cooperatives—with a specific focus on fair trade and organic farming.

Special Equities

A modest but important portion of certain funds is allocated to small private companies developing products or services that address important sustainability or environmental issues facing our society.

One example of a recent investment is Ivy Capital/All Life Insurance Company of South Africa, which insures people living with HIV.3 The company uses online support systems to help clients comply with their medical requirements in order to live a longer life. This provides enormous security to their families and employers and seems to be a rather unique business model in fighting the scourge of AIDS.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 9

1. ACEEE, Automobiles and the Environment, www.greenercars.org/guide_environment.

htm

2. As of September 30, 2012, Calvert Social Investment Foundation (“Calvert

Foundation” or “Foundation”) Community Investment Notes represented the follow-

ing percentages of Fund net assets: Calvert Capital Accumulation Fund 0.51%, Calvert

International Equity Fund 1.29%, and Calvert Small Cap Fund 0.48%. The Calvert

Foundation is a 501(c)(3) nonprofit organization. The Foundation’s Community

Investment Note Program is not a mutual fund and should not be confused with any

Calvert Investments-sponsored investment product.

3. As of September 30, 2012, Ivy Capital All Life Insurance represented 0.02% of

Calvert Equity Portfolio. Holdings are subject to change.

As of September 30, 2012, the following companies represented 0% of net assets in the

Fund: Gilead Sciences, Safeway, Plains Exploration and Production, JPMorgan Chase,

Urban Outfitters, Fossil, Gentex, Yahoo, Google, Microsoft and Facebook. Holdings are

subject to change.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 10

Investment Performance

Calvert International Equity Fund Class A shares (at NAV) gained 15.34% for the 12-month period ended September 30, 2012, outperforming the 14.17% return of the MSCI EAFE Investable Market Index due to strong stock selection.

Investment Climate

Gradually improving U.S. economic data, healthy corporate earnings, and some policy steps toward mitigation of the sovereign debt crisis in Europe provided support for equities worldwide during the fiscal year. Global inflation remained tame, and aggressive, accommodative monetary policy by central banks around the globe helped equity markets rally hard off their lows posted last fall, albeit on low volume.

For the trailing 12-month period, the Standard and Poor’s (S&P) 500, Russell 1000, and Russell 2000 Indices returned 30.20%, 30.06%, and 31.91% respectively. Negative headwinds from the eurozone and an economic slowdown in China led to a divergence in performance by international

| CALVERT |

| INTERNATIONAL |

| EQUITY FUND |

| September 30, 2012 |

| INVESTMENT PERFORMANCE | | | |

| (total return at NAV*) | | | |

| | 6 Months | | 12 Months | |

| | ended | | ended | |

| | 9/30/12 | | 9/30/12 | |

| Class A | -1.24 | % | 15.34 | % |

| Class B | -1.89 | % | 13.93 | % |

| Class C | -1.76 | % | 14.23 | % |

| Class I | -0.89 | % | 16.16 | % |

| Class Y | -1.04 | % | 15.80 | % |

| |

| MSCI EAFE Investable | | | |

| Market Index (IMI) | -0.45 | % | 14.17 | % |

| |

| Lipper International | | | | |

| Multi-Cap Growth | | | | |

| Funds Average | -0.72 | % | 17.09 | % |

| TEN LARGEST | % of | |

| STOCK HOLDINGS | Net Assets | |

| adidas AG | 2.3 | % |

| Novartis AG | 2.1 | % |

| Check Point Software | | |

| Technologies Ltd. | 2.0 | % |

| Pearson plc | 1.9 | % |

| BG Group plc | 1.9 | % |

| Canadian National Railway Co. | 1.9 | % |

| Air Liquide SA | 1.8 | % |

| Toyota Motor Corp. | 1.8 | % |

| Kingfisher plc | 1.6 | % |

| Reckitt Benckiser Group plc | 1.6 | % |

| Total | 18.9 | % |

*Investment performance/return at NAV does not reflect the deduction of the Fund’s maximum 4.75%

front-end sales charge or any deferred sales charges.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 11

stocks with the MSCI EAFE and MSCI Emerging Markets Indices returning 14.33% and 17.33%, respectively.

Value stocks slightly outperformed growth stocks during the fiscal year, and within the Russell 1000 Index, Consumer Discretionary, Telecommunication Services, and Financials were the top-performing sectors, while the Utilities, Consumer Staples, and Energy sectors lagged.

The U.S. economy continued to proceed on the path of gradual recovery. The U.S. corporate sector remained strong and provided some upside surprises for investors. The top-line numbers driven by the economic recovery were encouraging. Improvement in employment numbers were also a welcome, positive sign, though the decline in the unemployment rate was, unfortunately, primarily due to a drop in the labor force participation rate.

U.S. inflation remained low, bank lending continued to improve, and a weak U.S. dollar, thanks to the especially accommodative monetary policy in the U.S., helped U.S. exports and supported the rebuilding of the domestic manufacturing and industrial base. Vehicle sales and production also looked encouraging.

The manufacturing sector continued to provide a boost to employment and the U.S. economy, but accelerating recession in Europe and the overall slowdown in the global economy will de-emphasize the contribution of exports to U.S. GDP. Therefore, the continued recovery of the U.S. consumer will be important for a self-sustained U.S. economic recovery. More recently, the service sector has been showing signs of improvement. Consumer spending patterns remained promising and consumer confidence, helped by strength in the housing market, a falling unemploy-

| CALVERT |

| INTERNATIONAL |

| EQUITY FUND |

| September 30, 2012 |

| |

| | % of Total | |

| ECONOMIC SECTORS | Investments | |

| Consumer Discretionary | 19.5 | % |

| Consumer Staples | 8.4 | % |

| Energy | 5.0 | % |

| Financials | 18.6 | % |

| Health Care | 8.1 | % |

| Industrials | 10.3 | % |

| Information Technology | 7.8 | % |

| Limited Partnership Interest | 0.7 | % |

| Materials | 4.9 | % |

| Short-Term Investment | 9.9 | % |

| Telecommunication Services | 5.0 | % |

| Utilities | 1.4 | % |

| Venture Capital | 0.4 | % |

| Total | 100 | % |

ment rate, and improving equity markets, has also shown signs of improvement.

The U.S. housing market continued its bottoming-out process into early 2012 and showed significant improvement in the second and third quarters of 2012. With mortgage rates at record lows, housing activity picked up throughout the fiscal year. Housing can provide a positive surprise for the U.S. economy and equity markets through the powerful multiplier effect it can have on the consumer and, therefore, the economy.

The stance of the Federal Reserve (Fed) remained that it was ready to act should economic conditions in the U.S. deteriorate. This so-called “Bernanke put” provided support for U.S. equity markets throughout the fiscal year with investors believing the Fed would provide future liquidity injections in the event the economy faltered. A third round of quantitative easing (QE3)

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 12

materialized in September with the Federal Reserve’s Open Market Committee (FOMC) announcing an open-ended commitment to purchase $40 billion of mortgage-backed securities each month until substantial improvements in the labor market were seen. This came on top of the FOMC’s announcement earlier in the year to extend “Operation Twist” in an effort to further reduce long-term interest rates.

With global economic challenges keeping inflation in check, policymakers around the globe also continued their efforts toward easing monetary policies. On the flip side, the easing cycle has been inflating the balance sheets of the world’s six biggest central banks, which have more than doubled since 2006.

In the eurozone, the economic picture looked increasingly grim throughout the fiscal year, with peripheral economies firmly in a recessionary spiral and core economies coming under stress. Manufacturing in the region continued to fall deeper into contraction territory while consumer confidence in the eurozone reached its lowest level since early 2009 and the unemployment rate hit a record high.

As we anticipated, markets seemed to overestimate the efficacy of the policy action in Europe and underestimated the possibility of a more severe economic recession in the eurozone.

China cut its economic growth target from 8.0% to 7.5% during the first quarter of 2012, signaling the country’s need to transition from an export-driven to a more sustainable, consumer-driven, economic model. Nevertheless, the Chinese economy continued to decelerate during the fiscal year as foreign direct investment (FDI), one of the major drivers of economic growth in China, continued to decline and China’s HSBC Manufacturing Purchasing Managers Index (PMI) was in contraction territory for 11 consecutive months as exports continued to weaken.

A slower inflation trend allowed the Chinese government to reposition its economic policy from contractionary for most of 2011 to stimulative. A hard landing in China is not out of the question and could significantly impact global growth while making the overall macroeconomic backdrop riskier for the next several quarters.

Portfolio Strategy

The Fund is based upon a multi-manager approach with allocations managed by each of the two sub-advisors, Thornburg Investment Management and Martin Currie Inc., as well as the advisor, Calvert Investment Management, Inc., with the latter also overseeing the general strategy and overall allocations to the managers.

On a Fund level, stock selection drove performance, particularly in the Consumer Discretionary and Industrials sectors. Stock selection was largely positive across all sectors with the exception of Financials. Names like Canadian National Railway, Assa Abloy, Natura Cosmeticos, and adidas Group were top contributors to Fund performance for the reporting period.

Sector allocation was an overall detractor from performance. The Fund’s underweight to Financials and the beverage industry detracted most significantly, while the Fund’s

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 13

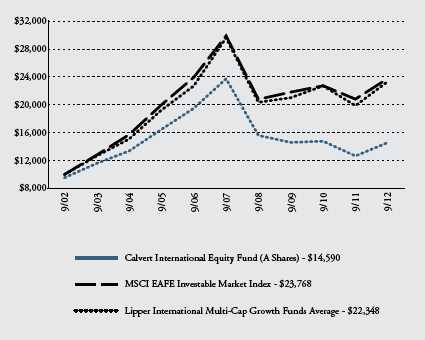

Growth of $10,000

The graph below shows the value of a hypothetical $10,000 investment in the Fund over the past 10 fiscal year periods. The results shown are for Classes A shares and reflect the deduction of the maximum front-end sales charge of 4.75%, and assume the reinvestment of dividends. The result is compared with benchmarks that include a broad based market index and a Lipper peer group average. Market indexes are unmanaged and their results do not reflect the effect of expenses or sales charges. The Lipper average reflects the deduction of the category’s average front-end sales charge. The value of an investment in a different share class would be different.

All performance data shown, including the graph above and the adjacent table, represents past performance, does not guarantee future results, assumes reinvestment of dividends and distributions and does not reflect the deduction of taxes that a shareholder would pay on the Fund’s distributions or the redemption of the Fund shares. All performance data reflects fee waivers and/or expense limitations, if any are in effect; in their absence performance would be lower. See Note B in Notes to Financial Statements. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted; for current performance data visit www.calvert.com. The gross expense ratio from the current prospectus for Class A shares is 1.82%. This number may differ from the expense ratio shown elsewhere in this report because it is based on a different time period and, if applicable, does not include fee or expense waivers. Performance data quoted already reflects the deduction of the Fund’s operating expenses.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 14

underweight position in Utilities was an offsetting lift. Country allocation was also a positive contributor, driven primarily by an underweight position in Japan, which added 1.60 percentage points of relative return.

Outlook

Despite healthy corporate earnings and continued gradual economic recovery in the United States, looming developments in the political landscape could have a negative impact on U.S. GDP growth and are likely to be a source of volatility for the markets in the coming months. However, once we have more visibility into the “fiscal cliff” scenarios, market participants may feel better about investing in risky assets for the long term.

We see continued challenges in the global macro backdrop leaving equity markets vulnerable to negative news, especially given that most of the positive catalysts are out and the markets had a healthy run through September 30, 2012. Any negative news from Europe or China or a soft earnings season in the United States. will likely trigger a risk aversion trade.

October 2012

As of September 30, 2012, the following holdings accounted for the following percentages of Fund net assets: Canadian National Railway 0.92%, Assa Abloy 1.00%, Natura Cosmeticos 1.28%, and adidas Group 2.13%. Holdings are subject to change.

| CALVERT |

| INTERNATIONAL |

| EQUITY FUND |

| September 30, 2012 |

| | |

| AVERAGE ANNUAL TOTAL RETURNS | |

| |

| CLASS A SHARES | (with max. load) | |

| One year | 9.87 | % |

| Five year | -10.18 | % |

| Ten year | 3.85 | % |

| |

| CLASS B SHARES | (with max. load) | |

| One year | 8.93 | % |

| Five year | -10.51 | % |

| Ten year | 3.19 | % |

| |

| CLASS C SHARES | (with max. load) | |

| One year | 13.23 | % |

| Five year | -10.09 | % |

| Ten year | 3.45 | % |

| |

| CLASS I SHARES | | |

| One year | 16.16 | % |

| Five year | -8.62 | % |

| Ten year | 5.15 | % |

| |

| CLASS Y SHARES* | | |

| One year | 15.80 | % |

| Five year | -8.99 | % |

| Ten year | 4.53 | % |

* Calvert International Equity Fund first offered Class Y Shares on October 31, 2008.

Performance prior to that date reflects the performance of Class A Shares at net asset value (NAV). Actual Class Y Share performance would have been different.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 15

SHAREHOLDER EXPENSE EXAMPLE

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2012 to September 30, 2012).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 16

| | | |

| | BEGINNING | ENDING ACCOUNT | EXPENSES PAID |

| | ACCOUNT VALUE | VALUE | DURING PERIOD* |

| | 4/1/12 | 9/30/12 | 4/1/12 - 9/30/12 |

| CLASS A | | | |

| Actual | $1,000.00 | $987.60 | $8.97 |

| Hypothetical | $1,000.00 | $1,015.98 | $9.10 |

| (5% return per | | | |

| year before expenses) | | | |

| | | | |

| CLASS B | | | |

| Actual | $1,000.00 | $981.10 | $14.71 |

| Hypothetical | $1,000.00 | $1,010.15 | $14.93 |

| (5% return per | | | |

| year before expenses) | | | |

| | | | |

| CLASS C | | | |

| Actual | $1,000.00 | $982.40 | $13.39 |

| Hypothetical | $1,000.00 | $1,011.50 | $13.58 |

| (5% return per | | | |

| year before expenses) | | | |

| | | | |

| CLASS I | | | |

| Actual | $1,000.00 | $991.10 | $5.30 |

| Hypothetical | $1,000.00 | $1,019.68 | $5.38 |

| (5% return per | | | |

| year before expenses) | | | |

| |

| CLASS Y | | | |

| Actual | $1,000.00 | $989.60 | $6.93 |

| Hypothetical | $1,000.00 | $1,018.04 | $7.03 |

| (5% return per | | | |

| year before expenses) | | | |

* Expenses are equal to the Fund’s annualized expense ratio of 1.80%, 2.97%, 2.70%, 1.06%, and 1.39% for Class A, Class B, Class C, Class I, and Class Y, respectively, multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period).

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 17

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors of Calvert World Values Fund, Inc.

and Shareholders of Calvert International Equity Fund:

We have audited the accompanying statement of net assets of Calvert International Equity Fund (the Fund), a series of the Calvert World Values Fund, Inc., as of September 30, 2012, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2012, by correspondence with the custodian and brokers or by performing other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Calvert International Equity Fund as of September 30, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

Philadelphia, Pennsylvania

November 29, 2012

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 18

| | | |

| STATEMENT OF NET ASSETS |

| SEPTEMBER 30, 2012 |

| |

| |

| EQUITY SECURITIES - 94.4% | SHARES | | VALUE |

| Australia - 1.0% | | | |

| Amcor Ltd. (ADR) | 3,181 | $ | 101,926 |

| QR National Ltd. | 442,455 | | 1,567,236 |

| Santos Ltd. | 91,149 | | 1,075,576 |

| Sims Metal Management Ltd. (ADR) | 36,251 | | 358,885 |

| | | | 3,103,623 |

| |

| Austria - 0.0% | | | |

| Erste Group Bank AG (ADR)* | 5,237 | | 57,188 |

| Telekom Austria AG (ADR) | 271 | | 3,862 |

| Verbund AG (ADR) | 507 | | 2,119 |

| | | | 63,169 |

| |

| Belgium - 0.0% | | | |

| Ageas (ADR) | 205 | | 4,891 |

| Delhaize Group SA (ADR) | 2,364 | | 91,156 |

| | | | 96,047 |

| |

| Brazil - 2.8% | | | |

| BM&FBOVESPA SA | 122,893 | | 742,290 |

| Itau Unibanco Holding SA (ADR) | 239,200 | | 3,654,976 |

| Natura Cosmeticos SA | 157,199 | | 4,282,454 |

| | | | 8,679,720 |

| |

| Canada - 5.5% | | | |

| Canadian National Railway Co.: | | | |

| New York Exchange | 16,907 | | 1,491,704 |

| Toronto Exchange | 66,724 | | 5,900,199 |

| Cenovus Energy, Inc. | 80,300 | | 2,800,603 |

| EnCana Corp. New York Exchange | 29,499 | | 646,618 |

| Potash Corporation of Saskatchewan, Inc. | 101,544 | | 4,409,041 |

| Suncor Energy, Inc.: | | | |

| New York Exchange | 6,475 | | 212,704 |

| Toronto Exchange | 46,600 | | 1,531,938 |

| | | | 16,992,807 |

| |

| China - 0.5% | | | |

| China Merchants Bank Co. Ltd | 911,915 | | 1,533,569 |

| |

| Denmark - 1.5% | | | |

| Danske Bank A/S (ADR)* | 15,792 | | 140,075 |

| H Lundbeck A/S (ADR)* | 3,480 | | 63,858 |

| Novo Nordisk A/S, Series B | 28,742 | | 4,542,789 |

| Novozymes A/S (ADR) | 1,844 | | 51,171 |

| | | | 4,797,893 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 19

| | | |

| EQUITY SECURITIES - cont’d | SHARES | | VALUE |

| Finland - 0.1% | | | |

| Metso Oyj (ADR) | 420 | $ | 15,099 |

| Nokia Oyj (ADR) | 7,964 | | 20,468 |

| Sampo Oyj (ADR) | 6,861 | | 105,865 |

| | | | 141,432 |

| |

| France - 9.1% | | | |

| Air France-KLM (ADR)* | 2,564 | | 16,492 |

| Air Liquide SA | 46,511 | | 5,767,635 |

| Air Liquide SA (ADR) | 8,449 | | 209,704 |

| AXA SA (ADR) | 18,230 | | 271,627 |

| BNP Paribas SA (ADR) | 7,862 | | 186,408 |

| Cap Gemini SA (ADR) | 207 | | 4,368 |

| Carrefour SA (ADR) | 27,123 | | 111,475 |

| Cie Generale des Etablissements Michelin | 51,079 | | 4,003,384 |

| Cie Generale d’Optique Essilor International SA (ADR) | 1,395 | | 65,760 |

| Credit Agricole SA (ADR)* | 33,364 | | 113,137 |

| Danone SA | 70,666 | | 4,352,878 |

| Danone SA (ADR) | 27,083 | | 331,767 |

| Dassault Systemes SA | 17,521 | | 1,841,788 |

| L’Oreal SA (ADR) | 4,044 | | 99,887 |

| Publicis Groupe | 86,900 | | 4,865,728 |

| Sanofi SA | 36,379 | | 3,103,356 |

| Sanofi SA (ADR) | 11,115 | | 478,612 |

| Schneider Electric SA | 33,923 | | 2,008,681 |

| Schneider Electric SA (ADR) | 11,305 | | 133,738 |

| Suez Environnement Co. (ADR) | 1,758 | | 9,792 |

| Valeo SA (ADR) | 5,507 | | 127,102 |

| Veolia Environnement SA (ADR) | 21,929 | | 237,272 |

| | | | 28,340,591 |

| |

| Germany - 9.7% | | | |

| adidas AG | 86,947 | | 7,136,534 |

| Aixtron SE (ADR) | 23,607 | | 312,085 |

| Allianz SE | 21,736 | | 2,587,519 |

| Allianz SE (ADR) | 70,176 | | 832,989 |

| Brenntag AG | 12,313 | | 1,576,751 |

| Celesio AG (ADR) | 942 | | 3,288 |

| Commerzbank AG (ADR)* | 999 | | 1,768 |

| Continental AG | 19,166 | | 1,877,700 |

| Continental AG (ADR) | 61 | | 6,010 |

| Deutsche Bank AG | 31,100 | | 1,229,348 |

| Deutsche Post AG (ADR) | 7,514 | | 147,500 |

| Henkel AG & Co. KGaA | 24,363 | | 1,590,295 |

| K+S AG (ADR) | 1,685 | | 41,805 |

| Kabel Deutschland Holding AG* | 46,200 | | 3,297,259 |

| Merck KGaA (ADR) | 345 | | 14,141 |

| ProSiebenSat.1 Media AG, Preferred | 58,863 | | 1,483,710 |

| SAP AG | 57,535 | | 4,076,640 |

| SAP AG (ADR) | 17,919 | | 1,278,162 |

| Volkswagen AG, Preferred | 13,307 | | 2,428,597 |

| Volkswagen AG (ADR), Preferred | 9,371 | | 343,541 |

| | | | 30,265,642 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 20

| | | |

| EQUITY SECURITIES - cont’d | SHARES | | VALUE |

| Greece - 0.0% | | | |

| National Bank of Greece SA (ADR)* | 49,475 | $ | 118,740 |

| |

| Hong Kong - 3.7% | | | |

| AIA Group Ltd. | 645,700 | | 2,394,088 |

| Bank of East Asia Ltd. (ADR) | 3,753 | | 13,699 |

| China Merchants Holdings International Co. Ltd. | 914,000 | | 2,823,080 |

| City Telecom HK Ltd. (ADR) | 58,461 | | 273,013 |

| Esprit Holdings Ltd. (ADR) | 62,073 | | 190,564 |

| Hang Lung Properties Ltd. (ADR) | 67,965 | | 1,151,327 |

| Hang Seng Bank Ltd. (ADR) | 1,110 | | 16,905 |

| Hong Kong Exchanges and Clearing Ltd. | 209,546 | | 3,164,519 |

| Hong Kong Exchanges and Clearing Ltd. (ADR) | 3,389 | | 50,733 |

| Johnson Electric Holdings Ltd. (ADR) | 1,074 | | 6,884 |

| Li & Fung Ltd. (ADR) | 22,086 | | 66,258 |

| PCCW Ltd. (ADR) | 2,456 | | 10,168 |

| SJM Holdings Ltd. | 681,000 | | 1,478,974 |

| | | | 11,640,212 |

| |

| Indonesia - 0.5% | | | |

| Bank Mandiri Persero Tbk PT | 1,904,500 | | 1,631,860 |

| |

| Ireland - 2.2% | | | |

| Accenture plc | 35,200 | | 2,465,056 |

| Covidien plc | 38,400 | | 2,281,728 |

| Experian plc (ADR) | 11,240 | | 187,708 |

| Kerry Group plc | 37,457 | | 1,919,116 |

| WPP plc (ADR) | 667 | | 45,443 |

| | | | 6,899,051 |

| |

| Israel - 2.0% | | | |

| Check Point Software Technologies Ltd.* | 129,231 | | 6,223,765 |

| |

| Italy - 0.6% | | | |

| Intesa Sanpaolo SpA (ADR) | 10,926 | | 98,443 |

| Prysmian SpA | 92,657 | | 1,653,513 |

| | | | 1,751,956 |

| |

| Japan - 12.2% | | | |

| Advantest Corp. (ADR) | 4,514 | | 58,366 |

| Aeon Co. Ltd. (ADR) | 3,305 | | 37,611 |

| Asahi Glass Co. Ltd. (ADR) | 24,499 | | 161,694 |

| Astellas Pharma, Inc | 37,900 | | 1,928,561 |

| Canon, Inc | 28,100 | | 899,763 |

| Canon, Inc. (ADR) | 30,411 | | 973,456 |

| Dai Nippon Printing Co. Ltd. (ADR) | 22,230 | | 152,720 |

| Daiwa House Industry Co. Ltd. (ADR) | 489 | | 70,660 |

| Denso Corp. (ADR) | 6,160 | | 96,897 |

| Eisai Co. Ltd. (ADR) | 254 | | 11,460 |

| FANUC Corp | 21,761 | | 3,513,262 |

| Fujitsu Ltd. (ADR) | 11,218 | | 209,216 |

| Honda Motor Co. Ltd. (ADR) | 36,718 | | 1,134,586 |

| KDDI Corp. | 41,200 | | 3,204,209 |

| Konami Corp. (ADR) | 2,378 | | 53,838 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 21

| | | |

| EQUITY SECURITIES - cont’d | SHARES | | VALUE |

| Japan - Cont’d | | | |

| Kubota Corp. (ADR) | 7,329 | $ | 370,261 |

| Lawson, Inc | 21,600 | | 1,663,244 |

| Mitsubishi Estate Co. Ltd. | 101,000 | | 1,936,525 |

| Mitsui Fudosan Co. Ltd | 101,256 | | 2,031,098 |

| Mizuho Financial Group, Inc. (ADR) | 201,536 | | 650,961 |

| MS&AD Insurance Group Holdings (ADR) | 34,938 | �� | 298,021 |

| Nippon Yusen KK (ADR) | 89,927 | | 308,450 |

| Nissan Motor Co. Ltd. (ADR)* | 51,937 | | 884,357 |

| Nitto Denko Corp. (ADR) | 15,966 | | 375,680 |

| Nomura Holdings, Inc. (ADR) | 161,596 | | 575,282 |

| NSK Ltd. (ADR) | 1,607 | | 18,497 |

| NTT DoCoMo, Inc | 857 | | 1,392,405 |

| ORIX Corp | 15,890 | | 1,598,789 |

| ORIX Corp. (ADR) | 7,678 | | 384,745 |

| Panasonic Corp. (ADR) | 77,651 | | 510,167 |

| Sega Sammy Holdings, Inc. (ADR) | 6,279 | | 29,637 |

| Seiko Epson Corp. (ADR) | 9,704 | | 29,209 |

| Sekisui House Ltd. | 191,000 | | 1,899,705 |

| Sharp Corp. (ADR) | 27,019 | | 67,548 |

| Sony Corp. | 51,400 | | 606,219 |

| Sony Corp. (ADR) | 38,955 | | 455,773 |

| Sumitomo Mitsui Trust Holdings, Inc. (ADR) | 40,720 | | 118,495 |

| Tokyo Gas Co. Ltd. | 389,118 | | 2,147,340 |

| Toyota Motor Corp. | 144,882 | | 5,652,480 |

| Toyota Motor Corp. (ADR) | 17,903 | | 1,405,565 |

| | | | 37,916,752 |

| |

| Luxembourg - 1.0% | | | |

| Nielsen Holdings NV* | 105,400 | | 3,159,892 |

| |

| Mexico - 0.6% | | | |

| FINAE, Series D, Preferred (b)(i)* | 1,962,553 | | 237,661 |

| Grupo Financiero Banorte SAB de CV | 262,200 | | 1,482,732 |

| | | | 1,720,393 |

| |

| Netherlands - 2.7% | | | |

| ASML Holding NV | 2,469 | | 132,536 |

| BE Semiconductor Industries NV | 4,208 | | 28,951 |

| Gemalto NV | 15,856 | | 1,395,426 |

| ING Groep NV (CVA)* | 246,482 | | 1,948,631 |

| Koninklijke Philips Electronics NV | 45,962 | | 1,077,809 |

| PostNL NV (ADR)* | 15,105 | | 52,867 |

| TNT Express NV (ADR) | 13,119 | | 137,094 |

| Yandex NV* | 93,700 | | 2,259,107 |

| Ziggo NV | 43,049 | | 1,464,235 |

| | | | 8,496,656 |

| |

| Norway - 1.3% | | | |

| DnB ASA | 159,611 | | 1,955,966 |

| Petroleum Geo-Services ASA | 105,666 | | 1,745,571 |

| Yara International ASA (ADR) | 8,545 | | 426,823 |

| | | | 4,128,360 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 22

| | | |

| EQUITY SECURITIES - cont’d | SHARES | | VALUE |

| Philippines - 0.6% | | | |

| Philippine Long Distance Telephone Co. (ADR) | 29,053 | $ | 1,917,789 |

| |

| Portugal - 0.1% | | | |

| Portugal Telecom SGPS SA (ADR) | 29,155 | | 144,609 |

| |

| Singapore - 0.7% | | | |

| City Developments Ltd. (ADR) | 479 | | 4,608 |

| Oversea-Chinese Banking Corp. Ltd | 252,830 | | 1,925,656 |

| Singapore Telecommunications Ltd. (ADR) | 11,258 | | 292,145 |

| | | | 2,222,409 |

| |

| South Africa - 1.4% | | | |

| African Bank Investments Ltd. (ADR) | 169 | | 3,346 |

| Aspen Pharmacare Holdings Ltd.* | 118,131 | | 2,037,417 |

| Clicks Group Ltd.* | 238,800 | | 1,667,028 |

| MTN Group Ltd. (ADR) | 21,938 | | 424,500 |

| Nedbank Group Ltd. (ADR) | 3,939 | | 86,658 |

| Tiger Brands Ltd. (ADR) | 1,994 | | 65,383 |

| | | | 4,284,332 |

| |

| Spain - 0.3% | | | |

| Banco Bilbao Vizcaya Argentaria SA (ADR) | 43,088 | | 333,932 |

| Banco Santander SA (ADR) | 74,002 | | 552,055 |

| International Consolidated Airlines Group SA (ADR)* | 678 | | 8,048 |

| | | | 894,035 |

| |

| Sweden - 4.1% | | | |

| Assa Abloy AB, Series B | 103,400 | | 3,356,560 |

| Atlas Copco AB | 70,045 | | 1,634,956 |

| Atlas Copco AB (ADR) | 2,340 | | 55,130 |

| Hennes & Mauritz AB, B Shares | 116,454 | | 4,046,288 |

| SKF AB (ADR) | 650 | | 14,063 |

| Svenska Cellulosa AB (ADR) | 3,578 | | 66,329 |

| Svenska Handelsbanken AB | 99,100 | | 3,713,402 |

| | | | 12,886,728 |

| |

| Switzerland - 5.5% | | | |

| Adecco SA (ADR)* | 277 | | 6,576 |

| Compagnie Financiere Richemont SA | 33,600 | | 2,016,000 |

| Credit Suisse Group AG (ADR) | 33,797 | | 714,807 |

| Julius Baer Group Ltd.* | 72,413 | | 2,526,751 |

| Nobel Biocare Holding AG (ADR)* | 495 | | 2,445 |

| Novartis AG | 105,005 | | 6,428,764 |

| Roche Holding AG (ADR) | 39,128 | | 1,838,625 |

| STMicroelectronics NV | 16,908 | | 91,303 |

| Swatch Group AG, Bearer Shares | 7,300 | | 2,913,787 |

| Zurich Insurance Group AG (ADR)* | 18,785 | | 470,189 |

| | | | 17,009,247 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 23

| | | |

| EQUITY SECURITIES - cont’d | SHARES | | VALUE |

| Taiwan - 0.6% | | | |

| Taiwan Semiconductor Manufacturing Co. Ltd. (ADR) | 121,600 | $ | 1,923,712 |

| |

| Thailand - 0.6% | | | |

| Kasikornbank PCL | 309,700 | | 1,836,266 |

| |

| United Kingdom - 21.9% | | | |

| Aon plc | 34,600 | | 1,809,234 |

| ARM Holdings plc | 162,806 | | 1,510,172 |

| Aviva plc (ADR) | 17,740 | | 184,673 |

| Barclays plc (ADR) | 20,253 | | 280,909 |

| BG Group plc (s) | 294,893 | | 5,946,517 |

| BG Group plc (ADR) | 42,482 | | 862,385 |

| British Land Co. plc (ADR) | 543 | | 4,502 |

| British Sky Broadcasting Group plc | 152,978 | | 1,834,840 |

| BT Group plc (ADR) | 27,414 | | 1,019,801 |

| Bunzl plc (ADR) | 631 | | 56,588 |

| Capita plc | 151,344 | | 1,890,927 |

| Centrica plc | 312,006 | | 1,649,909 |

| Centrica plc (ADR) | 9,287 | | 195,863 |

| GlaxoSmithKline plc | 117,049 | | 2,695,454 |

| HSBC Holdings plc | 376,775 | | 3,484,594 |

| HSBC Holdings plc (ADR) | 22,325 | | 1,037,220 |

| Inmarsat plc | 199,779 | | 1,901,472 |

| J Sainsbury plc (ADR) | 7,617 | | 169,554 |

| Johnson Matthey plc | 46,528 | | 1,811,180 |

| Johnson Matthey plc (ADR) | 134 | | 10,496 |

| Kingfisher plc | 1,153,187 | | 4,914,968 |

| Legal & General Group plc (ADR) | 608 | | 6,408 |

| Man Group plc (ADR) | 39,306 | | 52,670 |

| Old Mutual plc (ADR) | 895 | | 19,644 |

| Pearson plc | 307,583 | | 6,003,933 |

| Persimmon plc | 161,493 | | 1,976,048 |

| Petrofac Ltd. | 71,634 | | 1,843,181 |

| Prudential plc | 166,759 | | 2,156,160 |

| Prudential plc (ADR) | 60,796 | | 1,580,696 |

| Reckitt Benckiser Group plc | 84,817 | | 4,877,874 |

| Reckitt Benckiser Group plc (ADR) | 18,380 | | 210,635 |

| Rexam plc | 165,949 | | 1,164,266 |

| Royal Bank of Scotland Group plc* | 210,550 | | 872,924 |

| Sage Group plc (ADR) | 7,701 | | 157,254 |

| Smith & Nephew plc (ADR) | 15,944 | | 878,833 |

| Spirax-Sarco Engineering plc | 22,945 | | 773,981 |

| SSE plc (ADR) | 18,076 | | 408,518 |

| Tate & Lyle plc | 138,435 | | 1,486,217 |

| Tesco plc | 415,586 | | 2,225,805 |

| Tesco plc (ADR) | 44,802 | | 724,896 |

| Unilever plc (ADR) | 44,310 | | 1,618,201 |

| United Utilities Group plc (ADR) | 4,302 | | 100,022 |

| Vodafone Group plc | 1,451,777 | | 4,116,076 |

| Vodafone Group plc (ADR) | 23,339 | | 665,045 |

| Willis Group Holdings plc | 31,900 | | 1,177,748 |

| | | | 68,368,293 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 24

| | | | |

| EQUITY SECURITIES - cont’d | | SHARES | | VALUE |

| United States - 1.6% | | | | |

| ACCO Brands Corp.* | | 14,679 | $ | 95,267 |

| Bristol-Myers Squibb Co. | | 25,205 | | 850,669 |

| H.J. Heinz Co | | 29,200 | | 1,633,740 |

| MeadWestvaco Corp | | 44,502 | | 1,361,761 |

| Powerspan Corp.: | | | | |

| Series A, Convertible Preferred (b)(i)* | | 45,455 | | — |

| Series B, Convertible Preferred (b)(i)* | | 20,000 | | — |

| Series C, Convertible Preferred (b)(i)* | | 239,764 | | — |

| Series D, Convertible Preferred (b)(i)* | | 45,928 | | — |

| Series D, Preferred Warrants (strike price $3.44/share, | | | | |

| expires 12/31/12) (b)(i)* | | 2,347 | | — |

| Pricesmart, Inc. | | 10,028 | | 759,320 |

| Sealed Air Corp | | 26,185 | | 404,820 |

| | | | | 5,105,577 |

| |

| Total Equity Securities (Cost $277,782,148) | | | | 294,295,127 |

| |

| |

| VENTURE CAPITAL LIMITED | | ADJUSTED | | |

| PARTNERSHIP INTEREST - 0.8% | | BASIS | | |

| Balkan Financial Sector Equity Fund CV (b)(i)* | $ | 587,411 | | 523,175 |

| Blackstone Cleantech Venture Partners (b)(i)* | | 64,896 | | 47,330 |

| China Environment Fund 2004 (b)(i)* | | - | | 324,950 |

| Emerald Sustainability Fund I (b)(i)* | | 441,425 | | 294,571 |

| gNet Defta Development Holdings LLC (a)(b)(i)* | | 400,000 | | 318,510 |

| SEAF Central and Eastern European Growth Fund LLC (a)(b)(i)* | | 347,969 | | 569,717 |

| SEAF India International Growth Fund (b)(i)* | | 346,209 | | 280,391 |

| ShoreCap International LLC (b)(i)* | | - | | 186,502 |

| Terra Capital (b)(i)* | | 469,590 | | 1 |

| |

| Total Venture Capital Limited Partnership Interest (Cost $2,657,500) | | 2,545,147 |

| |

| |

| VENTURE CAPITAL DEBT | | PRINCIPAL | | |

| OBLIGATIONS - 0.2% | | AMOUNT | | |

| FINAE: | | | | |

| Note I, 6.50%, 12/10/15 (b)(i) | | 250,000 | | 250,000 |

| Note II, 6.50%, 2/29/16 (b)(i) | | 500,000 | | 500,000 |

| Mayer Laboratories, Inc., 6.00%, 12/31/01 (b)(i)(w) | | 11,056 | | 2,764 |

| Windhorse International-Spring Health Water Ltd., 8.00%, 3/13/13 (b)(i) 70,000 | | 70,000 |

| |

| Total Venture Capital Debt Obligations (Cost $831,056) | | | | 822,764 |

| |

| |

| HIGH SOCIAL IMPACT INVESTMENTS - 1.4% | | | | |

| Calvert Social Investment Foundation Notes, 1.04%, 7/1/14 (b)(i)(r) | | 4,431,583 | | 4,313,969 |

| |

| Total High Social Impact Investments (Cost $4,431,583) | | | | 4,313,969 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 25

| | | | | |

| PRINCIPAL | | | |

| TIME DEPOSIT - 10.6% | | AMOUNT | | VALUE | |

| State Street Bank Time Deposit, 0.113%, 10/1/12 | $ | 33,082,395 | $ | 33,082,395 | |

| |

| Total Time Deposit (Cost $33,082,395) | | | | 33,082,395 | |

| |

| |

| |

| TOTAL INVESTMENTS (Cost $318,784,682) - 107.4% | | 335,059,402 | |

| Other assets and liabilities, net - (7.4%) | | | | (23,204,801 | ) |

| NET ASSETS - 100% | | | $ | 311,854,601 | |

| |

| |

| |

| NET ASSETS CONSIST OF: | | | | | |

| Paid-in capital applicable to the following shares of common stock with | | | | | |

| 250,000,000 shares of $0.01 par value shares authorized: | | | | | |

| Class A: 13,613,546 shares outstanding | | | $ | 310,238,153 | |

| Class B: 302,101 shares outstanding | | | | 10,644,007 | |

| Class C: 1,359,397 shares outstanding | | | | 33,698,755 | |

| Class I: 6,970,052 shares outstanding | | | | 153,365,461 | |

| Class Y: 528,830 shares outstanding | | | | 7,742,740 | |

| Undistributed net investment income | | | | 2,995,904 | |

| Accumulated net realized gain (loss) on investments and foreign currency transactions | | (223,084,584 | ) |

| Net unrealized appreciation (depreciation) on investments, foreign | | | | | |

| currencies,and assets and liabilities denominated in foreign currencies | | | | 16,254,165 | |

| |

| |

| NET ASSETS | | | $ | 311,854,601 | |

| |

| |

| NET ASSET VALUE PER SHARE | | | | | |

| Class A (based on net assets of $183,587,896) | | | $ | 13.49 | |

| Class B (based on net assets of $3,607,055) | | | $ | 11.94 | |

| Class C (based on net assets of $15,921,608) | | | $ | 11.71 | |

| Class I (based on net assets of $101,203,366) | | | $ | 14.52 | |

| Class Y (based on net assets of $7,534,676 ) | | | $ | 14.25 | |

See notes to financial statements.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 26

| | | |

| RESTRICTED SECURITIES | ACQUISITION DATES | | COST |

| Balkan Financial Sector Equity Fund CV LP | 1/12/06 - 6/27/12 | $ | 587,411 |

| Blackstone Cleantech Venture Partners LP | 7/29/10 - 8/10/12 | | 64,896 |

| Calvert Social Investment Foundation Notes, 1.04%, 7/1/14 | 7/1/11 | | 4,431,583 |

| China Environment Fund 2004 LP | 9/15/05 - 4/1/09 | | - |

| Emerald Sustainability Fund I LP | 7/19/01 - 5/17/11 | | 441,425 |

| FINAE: | | | |

| Series D, Preferred | 2/28/11 | | 252,686 |

| Note I, 6.50%, 12/10/15 | 12/10/10 | | 250,000 |

| Note II, 6.50%, 2/29/16 | 2/24/11 | | 500,000 |

| gNet Defta Development Holdings LLC, LP | 8/30/05 | | 400,000 |

| Mayer Laboratories, Inc., 6.00%, 12/31/01 | 12/22/06 | | 11,056 |

| Powerspan Corp.: | | | |

| Series A, Convertible Preferred | 8/20/97 | | 250,000 |

| Series B, Convertible Preferred | 10/5/99 | | 200,000 |

| Series C, Convertible Preferred | 12/21/04 - 6/12/08 | | 273,331 |

| Series D, Convertible Preferred | 6/20/08 | | 157,996 |

| Series D, Preferred Warrants (strike price | | | |

| $3.44/share, expires 12/31/12) | 12/5/07 - 6/20/08 | | - |

| SEAF Central and Eastern European Growth Fund LLC, LP | 8/10/00 - 8/26/11 | | 347,969 |

| SEAF India International Growth Fund LP | 3/22/05 - 5/24/10 | | 346,209 |

| ShoreCap International LLC, LP | 8/12/04 - 12/15/08 | | - |

| Terra Capital LP | 11/23/98 - 3/14/06 | | 469,590 |

| Windhorse International-Spring Health Water Ltd., | | | |

| 8.00%, 3/13/13 | 9/13/11 - 7/10/12 | | 70,000 |

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 27

(a) Affiliated company.

(b) This security was valued by the Board of Directors. See Note A.

(i) Restricted securities represent 2.5% of net assets of the Fund.

(r) The coupon rate shown on floating or adjustable rate securities represents the rate at period end.

(s) 135,000 shares of BG Group plc have been soft segregated in order to cover outstanding commitments to

certain limited partnerships investments within the Fund. There are no restrictions on the trading of this

security.

(w) Mayer Laboratories, Inc. is in default for principal and interest. Past due accrued interest as of September

30, 2012 totaled $166.

* Non-income producing security.

Abbreviations:

ADR: American Depositary Receipts

CVA: Certificaten Van Aandelen

LLC: Limited Liability Corporation

plc: Public Limited Company

See notes to financial statements.

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 28

| | | |

| STATEMENT OF OPERATIONS |

| YEAR ENDED SEPTEMBER 30, 2012 |

| |

| |

| NET INVESTMENT INCOME | | | |

| Investment Income: | | | |

| Dividend income (net of foreign taxes withheld of $628,682) | $ | 8,262,769 | |

| Interest income | | 119,448 | |

| Total investment income | | 8,382,217 | |

| |

| Expenses: | | | |

| Investment advisory fee | | 2,265,331 | |

| Transfer agency fees and expenses | | 668,530 | |

| Administrative fees | | 872,048 | |

| Distribution Plan expenses: | | | |

| Class A | | 451,192 | |

| Class B | | 41,151 | |

| Class C | | 163,509 | |

| Directors’ fees and expenses | | 37,826 | |

| Custodian fees | | 207,618 | |

| Registration fees | | 67,787 | |

| Reports to shareholders | | 165,019 | |

| Professional fees | | 36,111 | |

| Miscellaneous | | 63,536 | |

| Total expenses | | 5,039,658 | |

| Reimbursement from Advisor: | | | |

| Class A | | (66,615 | ) |

| Class B | | (8,690 | ) |

| Class C | | (4,504 | ) |

| Class I | | (29,563 | ) |

| Class Y | | (5,082 | ) |

| Fees paid indirectly | | (101 | ) |

| Net expenses | | 4,925,103 | |

| |

| |

| NET INVESTMENT INCOME | | 3,457,114 | |

| |

| REALIZED AND UNREALIZED GAIN (LOSS) | | | |

| Net realized gain (loss) on: | | | |

| Investments | | (15,183,849 | ) |

| Foreign currency transactions | | (391,815 | ) |

| | | (15,575,664 | ) |

| |

| Change in unrealized appreciation (depreciation) on: | | | |

| Investments and foreign currencies | | 56,135,558 | |

| Assets and liabilities denominated in foreign currencies | | 52,620 | |

| | | 56,188,178 | |

| |

| NET REALIZED AND UNREALIZED GAIN (LOSS) | | 40,612,514 | |

| |

| INCREASE (DECREASE) IN NET ASSETS | | | |

| RESULTING FROM OPERATIONS | $ | 44,069,628 | |

See notes to financial statements.www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 29

| | | | |

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | Year ended | | Year ended | |

| | September 30, | | September 30, | |

| INCREASE (DECREASE) IN NET ASSETS | 2012 | | 2011 | |

| Operations: | | | | |

| Net investment income | $3,457,114 | | $4,177,788 | |

| Net realized gain (loss) | (15,575,664 | ) | 1,597,366 | |

| Change in unrealized appreciation (depreciation) | 56,188,178 | | (54,531,070 | ) |

| |

| |

| INCREASE (DECREASE) IN NET ASSETS | | | | |

| RESULTING FROM OPERATIONS | 44,069,628 | | (48,755,916 | ) |

| |

| Distributions to shareholders from: | | | | |

| Net investment income: | | | | |

| Class A shares | (2,117,749 | ) | (655,710 | ) |

| Class C shares | (14,293 | ) | — | |

| Class I shares | (1,414,874 | ) | (542,675 | ) |

| Class Y shares | (79,164 | ) | (3,993 | ) |

| Total distributions | (3,626,080 | ) | (1,202,378 | ) |

| |

| Capital share transactions: | | | | |

| Shares sold: | | | | |

| Class A shares | 25,698,704 | | 37,038,781 | |

| Class B shares | 17,463 | | 95,958 | |

| Class C shares | 994,621 | | 1,483,373 | |

| Class I shares | 20,757,214 | | 31,388,444 | |

| Class Y shares | 1,229,161 | | 8,008,040 | |

| Reinvestment of distributions: | | | | |

| Class A shares | 1,891,096 | | 608,387 | |

| Class C shares | 11,391 | | — | |

| Class I shares | 1,274,329 | | 483,830 | |

| Class Y shares | 35,166 | | 419 | |

| Redemption fees: | | | | |

| Class A shares | 6,002 | | 4,506 | |

| Class C shares | 15 | | 249 | |

| Class I shares | — | | 669 | |

| Class Y shares | 14 | | 6 | |

| Shares redeemed: | | | | |

| Class A shares | (41,319,982 | ) | (79,188,924 | ) |

| Class B shares | (1,476,972 | ) | (1,646,677 | ) |

| Class C shares | (3,469,843 | ) | (4,408,325 | ) |

| Class I shares | (23,295,875 | ) | (14,266,871 | ) |

| Class Y shares | (2,119,332 | ) | (1,831,646 | ) |

| Total capital share transactions | (19,766,827 | ) | (22,229,781 | ) |

| |

| TOTAL INCREASE (DECREASE) IN NET ASSETS | 20,676,721 | | (72,188,075 | ) |

| |

| |

| NET ASSETS | | | | |

| Beginning of year | 291,177,880 | | 363,365,955 | |

| End of year (including undistributed net investment income | | | | |

| of $2,995,904 and $3,608,275, respectively) | $311,854,601 | | $291,177,880 | |

See notes to financial statements. www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 30

| | | | |

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | Year ended | | Year ended | |

| | September 30, | | September 30, | |

| CAPITAL SHARE ACTIVITY | 2012 | | 2011 | |

| Shares sold: | | | | |

| Class A shares | 2,002,914 | | 2,582,076 | |

| Class B shares | 1,516 | | 7,466 | |

| Class C shares | 88,845 | | 119,086 | |

| Class I shares | 1,510,443 | | 2,086,100 | |

| Class Y shares | 90,952 | | 527,710 | |

| Reinvestment of distributions: | | | | |

| Class A shares | 156,677 | | 42,634 | |

| Class C shares | 1,079 | | — | |

| Class I shares | 98,632 | | 31,789 | |

| Class Y shares | 2,767 | | 28 | |

| Shares redeemed: | | | | |

| Class A shares | (3,233,923 | ) | (5,606,048 | ) |

| Class B shares | (129,393 | ) | (130,029 | ) |

| Class C shares | (308,966 | ) | (353,754 | ) |

| Class I shares | (1,656,401 | ) | (929,886 | ) |

| Class Y shares | (158,957 | ) | (125,742 | ) |

| Total capital share activity | (1,533,815 | ) | (1,748,570 | ) |

See notes to financial statements.

www. calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 31

NOTES TO FINANCIAL STATEMENTS

NOTE A — SIGNIFICANT ACCOUNTING POLICIES

General: The Calvert International Equity Fund (the “Fund”), a series of Calvert World Values Fund, Inc., is registered under the Investment Company Act of 1940 as a diversified, open-end management investment company. The Calvert World Values Fund, Inc. is comprised of three separate series. The operations of each series are accounted for separately. The Fund offers five classes of shares of capital stock - Classes A, B, C, I, and Y. Class A shares are sold with a maximum front-end sales charge of 4.75%. Class B shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge at the time of redemption, depending on how long investors have owned the shares. Class B shares are no longer offered for purchase, except through reinvestment of dividends and/or distributions and through certain exchanges. Class C shares are sold without a front-end sales charge and, with certain exceptions, will be charged a deferred sales charge on shares sold within one year of purchase. Class B and Class C shares have higher levels of expenses than Class A shares. Class I shares require a minimum account balance of $1,000,000. The $1 million minimum initial investment may be waived for certain institutional accounts where it is believed to be in the best interest of the Fund and its shareholders. Class I shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Class Y shares are generally only available to wrap or similar fee-based programs offered by financial intermediaries that have entered into an agreement with the Fund’s Distributor to offer Class Y shares. Class Y shares have no front-end or deferred sales charge and have lower levels of expenses than Class A shares. Each class has different: (a) dividend rates, due to differences in Distribution Plan expenses and other class-specific expenses, (b) exchange privileges and (c) class-specific voting rights.

Security Valuation: Net asset value per share is determined every business day as of the close of the regular session of the New York Stock Exchange (generally 4:00 p.m. Eastern time). The Fund uses independent pricing services approved by the Board of Directors (“the Board”) to value its investments wherever possible. Investments for which market quotations are not available or deemed not reliable are fair valued in good faith under the direction of the Board.

The Board has adopted Valuation Procedures (the “Procedures”) to determine the fair value of securities and other financial instruments for which market prices are not readily available or which may not be reliably priced. The Board has delegated the day-to-day responsibility for determining the fair value of assets of the Fund, except Special Equities investments, to Calvert Investment Management, Inc. (the “Advisor” or “Calvert”) and has provided these Procedures to govern Calvert in its valuation duties. Special Equities investments, as described in the Fund’s prospectus and statement of additional informa-tioin, are fair valued by the Board’s Special Equities Committee.

Calvert has chartered an internal Valuation Committee to oversee the implementation of these Procedures and to assist it in carrying out the valuation responsibilities that the Board has delegated.

The Valuation Committee meets on a regular basis to review illiquid securities and other investments which may not have readily available market prices. The Valuation Committee’s fair valuation determinations are subject to review, approval and ratification by the Board at its next regularly scheduled meeting covering the calendar quarter in

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 32

which the fair valuation was determined.

The Valuation Committee utilizes various methods to measure the fair value of the Fund’s investments. Generally Accepted Accounting Principles (GAAP) establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

Level 1 – quoted prices in active markets for identical securities

Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned level within the hierarchy during the period. Valuation techniques used to value the Funds’ investments by major category are as follows: Equity securities, including restricted securities and venture capital securities, for which market quotations are readily available, are valued at the last reported sale price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded and are categorized as Level 1 in the hierarchy. In the event there were no sales during the day or closing prices are not available, securities are valued at the last quoted bid price or using the last available price and are categorized as Level 2 in the hierarchy. Foreign securities are valued based on quotations from the principal market in which such securities are normally traded. If events occur after the close of the principal market in which foreign securities are traded, and before the close of business of the Fund, that are expected to materially affect the value of those securities, then they are valued at their fair value taking these events into account. The Fund has retained a third party fair value pricing service to quantitatively analyze the price movement of its holdings on foreign exchanges and to automatically fair value if the variation from the prior day’s closing price exceeds specified parameters. Such securities would be categorized as Level 2 in the hierarchy in these circumstances. Utilizing this technique may result in transfers between Level 1 and Level 2. For restricted securities and private placements where observable inputs are limited, assumptions about market activity and risk are used and such securities are categorized as Level 3 in the hierarchy.

Venture capital securities for which market quotations are not readily available are fair valued by the Fund’s Board of Directors and are categorized as Level 3 in the hierarchy. Venture capital direct equity securities are generally valued using the most appropriate and applicable method to measure fair value in light of each company’s situation. Methods may include market, income or cost approaches with discounts as appropriate based on assumptions of liquidation or exit risk. Examples of the market approach are subsequent rounds of financing, comparable transactions, and revenue times an industry multiple. An example of the income approach is the discounted cash flow. Examples of the cost approach are replacement cost, salvage value, or net asset percentage. Venture capital limited partnership (“LP”) securities

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 33

are valued at the fair value reported by the general partner of the partnership adjusted as necessary to reflect subsequent capital calls and distributions and any other available information. In the absence of a reported LP unit value, fair value may be estimated based on the Fund’s percentage equity in the partnership and/or other balance sheet information and portfolio value for the most recently available period reported by the general partner. In some cases adjustments may be made to account for daily pricing of material public holdings within the partnership. Venture capital debt securities are valued based on assumptions of credit and market risk. For venture capital securities denominated in foreign currency, the fair value is marked to the daily exchange rate.

Debt securities, including restricted securities, are valued based on evaluated prices received from independent pricing services or from dealers who make markets in such securities and are generally categorized as Level 2 in the hierarchy. Short-term securities of sufficient credit quality with remaining maturities of sixty days or less for which quotations are not readily available are valued at amortized cost, which approximates fair value, and are categorized as Level 2 in the hierarchy.

When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing matrices which consider similar factors that would be used by independent pricing services. These are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances.

If a market value cannot be determined for a security using the methodologies described above, or if, in the good faith opinion of the Advisor, the market value does not constitute a readily available market quotation, or if a significant event has occurred that would materially affect the value of the security, the security will be fair valued as determined in good faith by the Valuation Committee or with respect to Special Equities investments, by the Special Equities Committee using the venture capital methodologies described above.

The Valuation Committee considers a number of factors, including significant unobservable valuation inputs when arriving at fair value. It considers all significant facts that are reasonably available and relevant to the determination of fair value.

The Valuation Committee primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. When more appropriate, the fund may employ an income-based or cost approach. An income-based valuation approach discounts anticipated future cash flows of the investment to calculate a present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. A cost based approach is based on the amount that currently would be required to replace the service capacity of an asset (current replacement cost). From the seller’s perspective, the price that would be received for the asset is determined based on the cost to a buyer to acquire or construct a substitute asset of comparable utility, adjusted for obsolescence.

The values assigned to fair value investments are based on available information and do not necessarily represent amounts that might ultimately be realized. Further, due to the inherent uncertainty of valuations of such investments, the fair values may differ sig-

www.calvert.com CALVERT INTERNATIONAL EQUITY FUND ANNUAL REPORT 34

nificantly from the values that would have been used had an active market existed, and the differences could be material. The Valuation Committee employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis and reviews of any related market activity.

At September 30, 2012, securities valued at $7,919,541, or 2.5% of net assets, were fair valued in good faith under the direction of the Board.

The following is a summary of the inputs used to value the Fund’s net assets as of September 30, 2012:

| | | VALUATION INPUTS | | |

| |

| Investments in Securities | Level 1 | Level 2 | | Level 3 | Total | |

| Equity securities* | $294,057,466 | — | | — | $294,057,466 | ** |

| Other debt obligations | — | $37,396,364 | | — | 37,396,364 | |

| Venture capital | — | — | $ | $3,605,572 | 3,605,572 | |

| |

| TOTAL | $294,057,466 | $37,396,364 | $ | $3,605,572 | $335,059,402 | |

* For further breakdown of equity securities by country, please refer to the Statement of Net Assets.

** Exclusive of $237,661 venture capital equity shown in venture capital heading.

The following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value:

| | | | |

| | VENTURE CAPITAL | | TOTAL | |

| Balance as of 9/30/11 | $8,898,945 | | $8,898,945 | |

| Accrued discounts/premiums | - | | - | |

| Realized gain (loss) | 22,504 | | 22,504 | |

| Change in unrealized appreciation (depreciation) | (49,433 | ) | (49,433 | ) |

| Purchases | 61,812 | | 61,812 | |

| Sales | (1,014,287 | ) | (1,014,287 | ) |

| Transfers in and/or out of Level 31 | (4,313,969 | )2 | (4,313,969 | ) |

| Balance as of 9/30/12 | $3,605,572 | | $3,605,572 | |