UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06652

Aberdeen Investment Funds

Exact name of registrant as specified in charter:

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Address of principal executive offices:

Ms. Andrea Melia

Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

Name and address of agent for service:

Registrant’s telephone number, including area code: 866-667-9231

Date of fiscal year end: October 31

Date of reporting period: October 31, 2018

Item 1. Reports to Shareholders.

Aberdeen Investment Funds

Annual Report

October 31, 2018

Aberdeen Select International Equity Fund

Aberdeen Select International Equity Fund II

Aberdeen Total Return Bond Fund

Aberdeen Global High Income Fund

| Page 1 | ||||

| Page 3 | ||||

| Page 10 | ||||

| Page 16 | ||||

| Page 28 | ||||

| Page 38 | ||||

| Page 52 | ||||

| Page 72 | ||||

| Page 73 | ||||

| Page 74 | ||||

| Page 75 | ||||

| Page 79 | ||||

Investors should carefully consider a fund’s investment objectives, risks, fees, and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at www.aberdeen-asset.us. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Select International Equity Fund, Aberdeen Select International Equity Fund II, Aberdeen Total Return Bond Fund, and Aberdeen Global High Income Fund, (each a “Fund” and collectively the “Funds”) are distributed by Aberdeen Fund Distributors, LLC, Member FINRA, 1735 Market Street, 32nd Floor, Philadelphia, PA 19103.

Aberdeen Asset Management Inc. (AAMI) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23,1995. Registration with the Securities and Exchange Commission does not imply any certain level of skill or training.

Statement Regarding Availability of Quarterly Portfolio Schedule.

The complete schedule of portfolio holdings for the Aberdeen Investment Funds is included in the Funds’ semi-annual and annual reports to shareholders. The Funds file complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the “SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at http://www.sec.gov. The Funds’ Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330. The Funds make their most recent Forms N-Q available to shareholders on www.aberdeen-asset.us or upon request without charge.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 866-667-9231. The information is also included in the Funds’ Statement of Additional Information, which is available on the Funds’ website at www.aberdeen-asset.us and on the SEC’s website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 866-667-9231; and (ii) on the SEC’s website at www.sec.gov.

Global financial markets weathered numerous bouts of significant volatility during the 12-month period ended October 31, 2018, capped off by a major downturn in October 2018. Global stock markets in aggregate gained ground for the first few months of the period, as generally upbeat corporate earnings reports, tax reform in the U.S., and relatively steady economic growth buoyed investors’ confidence. However, market sentiment soon turned negative amid concerns that rising inflation could lead to more aggressive global central bank monetary policy, as well as fears of a possible global trade war spurred by tensions between the U.S and China. Global equities recovered during the third quarter of 2018, led by the U.S., with the broader-market Standard and Poor’s (S&P) 500 Index1 climbing 7.7% – its strongest quarterly performance since 2013. Nonetheless, in an apparent case of “financial whiplash,” global markets declined sharply towards the end of the reporting period in October. Investors were rattled by concerns ranging from lower corporate earnings estimates to the impact of continued monetary policy normalization. There also was a spike in U.S. Treasury yields during the month, triggered by expectations of further U.S. Federal Reserve (Fed) interest-rate increases. Shares of technology companies tumbled as higher interest rates led to investors’ apprehension about the rising valuations in the sector.

There was divergent performance among the regional stock markets during the 12-month reporting period. The Morgan Stanley Capital International (MSCI) World Index,2 a global equity market benchmark, posted a modest gain of 1.7% for the period, despite the vast majority of its constituents recording losses for the period. The U.S. was the lone major developed market to garner a positive return, while European stocks declined and were the weakest performers. Global emerging equity markets, as represented by the MSCI Emerging Markets Index,3 fell 12.2% over the reporting period, hampered by the strengthening U.S. dollar, which weighed on vulnerable economies with substantial foreign debt. The escalating trade tensions between the U.S. and China had a negative impact on Asia-Pacific stock markets, which declined 11.8% for the period, as measured by the MSCI All Country (AC) Asia Pacific ex Japan Index.4

While shares of U.S. companies could not avoid the sell-off in the global financial markets in October 2018, they finished the 12-month reporting period in positive territory. The U.S. market was bolstered for most of the period by generally positive economic data and corporate earnings reports, as well as the tax reform legislation that was enacted in late 2017. Many large-cap companies responded to the reduction of the top U.S. corporate tax rate from 35% to 21% by increasing their dividend payments and accelerating share repurchases. Late in the period, however, as investors worried that rising wage pressure and inflation could force the Fed to tighten monetary policy more aggressively than previously forecast. U.S. large-cap stocks, as represented by the S&P 500 Index, gained 7.4% during the reporting period, substantially outperforming the corresponding 2.8% and 1.9% returns of their mid- and small-cap counterparts, as measured by the Russell Midcap5 and Russell 20006 indices, respectively.

Shares of large-cap companies in the Asia-Pacific region fell sharply over the reporting period, hampered in part by investors’ concerns about a possible U.S.-China trade war. In June 2018, the administration of U.S. President Donald Trump assessed tariffs on US$50 billion in Chinese imports. Three months later, the U.S. placed an additional US$200 billion of levies on Chinese imports. China responded without escalating rhetoric while allowing its currency, the renminbi, to depreciate further against the U.S. dollar. Additionally, the weak investor sentiment in mainland China was compounded by fears over the country’s moderating economic growth.

One of the key reasons for the weakness in emerging-market equities was the liquidity squeeze on the U.S. dollar, stemming from the U.S. tax reforms that encouraged U.S. companies to repatriate7 their cash, as well as the Fed’s hawkish monetary policy stance. Turkey bore the brunt of the downturn amid worries about the central bank’s unwillingness to adopt orthodox economic policies and the government’s deteriorating relations with the U.S. In Mexico, Andres Lopez Obrador, the left-wing candidate, won Mexico’s presidential election in July 2018. While this outcome was expected, the market has become increasingly concerned with his plans to unwind some of the reforms that had occurred under his predecessor, Pena Nieto. Japan’s longest economic growth streak in 28 years stalled in the first quarter of 2018, but the economy subsequently resumed its momentum. An upgrade of second-quarter 2018 gross domestic product (GDP) data was attributable to an increase in capital investments. This was partly the result of the tight Japanese labor market, which saw the unemployment rate reach its lowest since the 1990s, boosting investments in labor-saving technologies.

Regarding the global fixed-income markets during the reporting period, capital outflows from emerging markets quickened due to the Fed’s ongoing rate-hike cycle and rising U.S. Treasury yields. As monetary policy normalization accelerated in the West, the easing cycle also came to an end in most parts of Asia. Indonesia’s central bank led the charge, raising its benchmark interest rate five times over the reporting period in a bid to stem the falling Indonesian rupiah as most emerging-market currencies succumbed to broad U.S.-dollar strength. Central banks in the Philippines and India also increased interest rates, but more in response to rising inflation, given the threat posed by higher global oil prices after U.S. President Trump reimposed economic sanctions on Iran. Yields on U.S. Treasuries rose, with two-, five- and ten year yields increasing by 127, 97 and 77 basis points (bps), respectively, over the reporting period, and this pressured higher-quality, lower-yielding and longer duration8 credit. U.S. and European high-yield markets saw marginal gains over the reporting period. Corporate earnings remained supported by generally positive economic growth, while default rates remained low. Supply was also lower than that in 2017 as companies, faced with rising borrowing costs, responded by reducing new issuance. However, investor sentiment in the U.S. deteriorated towards the end of the reporting period as trade tensions with China worsened and businesses began to forecast more conservative revenues and profitability in the ensuing quarters.

| 2018 Annual Report | 1 |

Market Review (concluded)

Global real estate equity markets faced a challenging environment during the reporting period. While the Financial Times Stock Exchange European Public Real Estate Association/National Association of Real Estate Investment Trusts (FTSE EPRA/NAREIT) Global Real Estate Index9 ended the period with a modest negative return, there were considerable variations in country-level returns. The performance of real estate markets in developed countries was modestly positive, while emerging markets generally posted negative returns for the reporting period.

Outlook

As we near the end of 2018, global financial markets are beset by worries over rising interest rates, trade tensions and a slowing global economy. Although the U.S. market initially appeared to be indifferent to these concerns, the technology rally which had underpinned the current bull market appears to have faltered. Other threats remain, including Italy’s fiscal problems and political uncertainty in Europe caused by negotiations surrounding the UK’s exit from the EU (“Brexit”), which have yet to provide clarity on what the outcome will be for the UK or Europe.

The UK remains a member of the EU until the legally established departure date of March 29, 2019 and, until such date, all existing EU-derived laws and regulations continue to apply in the UK. Those laws may continue to apply for a transitional period, depending on whether a deal is struck and, if so, what that deal is. In any event, the UK’s on-shoring of EU legislation currently envisages no policy changes to EU law. However, the EU has not yet provided any material cushion from the effects of Brexit for financial services as a matter of EU law. Whether or not a Fund invests in securities of issuers located in Europe (whether the EU, Eurozone or UK) or with significant exposure to European, EU, Eurozone or UK issuers or countries, the unavoidable uncertainties and events related to Brexit could negatively affect the value and liquidity of a Fund’s investments, increase taxes and costs of business and cause volatility in currency exchange rates and interest rates. Brexit could adversely affect the performance of contracts in existence at the date of Brexit and European, UK or worldwide political, regulatory, economic or market conditions and could contribute to instability in political institutions, regulatory agencies and financial markets. Brexit could also lead to legal uncertainty and politically divergent national laws and regulations as a new relationship between the UK and EU is defined and the UK determines which EU laws to replace or replicate. Any of these effects of Brexit, and others that cannot be anticipated, could adversely affect a Fund’s business, results of operations and financial condition. In addition, the risk that Standard Life Aberdeen plc, the parent of the companies that provide investment advisory and sub-advisory services to the Funds and which is headquartered in the UK, fails to adequately prepare for Brexit could have significant customer, reputation and capital impacts for Standard Life Aberdeen plc and its subsidiaries, including those providing services to the Funds; however, we have detailed contingency planning in place to seek to manage the consequences of Brexit on the Funds and to avoid any disruption on the Funds and to the services we provide. Given the fluidity and complexity of the situation, however, we cannot assure that the Funds will not be adversely impacted despite our preparations.

We remain cautious on the growing divergence across global markets, with strength in U.S. macroeconomic data contrasting with slowing growth across other economies and markets. With the U.S. economy gradually moving closer towards full capacity, the Federal Reserve maintains its monetary policy tightening stance and is expected to continue to raise interest rates into 2019. In Asia, China continues to balance further trade-related responses towards the U.S. with managing and maintaining its closely monitored economic growth rates.

Aberdeen Standard Investments

| 1 | The S&P 500 Index is an unmanaged index considered representative of the U.S. stock market. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | The MSCI World Index tracks the performance of large- and mid-cap stocks across 23 developed-market countries. |

| 3 | The MSCI Emerging Markets Index tracks the performance of large- and mid-cap stocks across 24 emerging-market countries. |

| 4 | The MSCI AC Asia Pacific ex Japan Index tracks the performance of large and mid-cap representation across two of three developed-market countries (excluding Japan) and nine emerging-market countries in Asia. |

| 5 | The Russell Midcap Index is an unmanaged index considered representative of U.S. mid-cap stocks. |

| 6 | The Russell 2000 Index is an unmanaged index considered representative of U.S. small-cap stocks. |

| 7 | Repatriation refers to a corporation’s conversion of any offshore capital back to the currency of the country in which the corporation is based. |

| 8 | Duration is an estimate of bond price sensitivity to changes in interest rates. The higher the duration, the greater the change (i.e., higher risk) in relation to interest-rate movements. |

| 9 | The FTSE EPRA/NAREIT Index is an unmanaged index considered representative of real estate companies and REITs outside the U.S. |

| 2 | Annual Report 2018 |

Aberdeen Select International Equity Fund (Unaudited)

The Aberdeen Select International Equity Fund (Institutional Class shares net of fees) returned -11.71% for the 12-month period ended October 31, 2018, versus -7.80% for its benchmark, the MSCI All Country (AC) World ex-USA Index, during the same period. For broader comparison, the average return of the Fund’s peer category of International Large-Cap Growth Funds (comprising 71 funds), as measured by Lipper, Inc., was -8.01%.

International equities declined over the reporting period. Investors were initially optimistic towards global economic growth, but investor sentiment turned more negative as the period progressed. Worries that rising inflation could compel more aggressive monetary policy, and a flare-up in trade tensions – especially as U.S.-China trade relations deteriorated amid rounds of brinkmanship – led to higher market volatility. The U.S. broader-market Standard & Poor’s (S&P) 500 Index1 initially shrugged off these concerns to record its longest bull run in history, supported by strong corporate earnings growth and a strengthening U.S. dollar. However, a spike in U.S. Treasury yields at the end of the reporting period triggered a slide in share prices as investors reassessed global stock valuations. Emerging markets also came under pressure due to the appreciating U.S. dollar.

The Fund underperformed its benchmark, the MSCI AC World ex-USA Index, for the reporting period due to negative stock selection.

At the stock level, South Korean beauty and cosmetics firm AmorePacific Group was a key detractor from the Fund’s relative performance, as the company’s shares declined after its results generally missed the market’s expectations. We are monitoring the stock’s performance. Shares of German pharmaceutical and life sciences group Bayer declined following an adverse court decision against weed-killers made by Monsanto, which the company recently acquired. While the damages have been reduced on appeal as we expected, the guilty verdict was upheld. We continue to monitor the situation closely. Brazilian fuel distributor Ultrapar Participacoes S.A.’s stock price moved lower eased in tandem with the broader Brazilian equity market, which declined due to an extended strike by truckers and concerns over economic reforms. We subsequently exited the Fund’s position in the company.

Conversely, the Fund’s position in Italy-listed Tenaris S.A., which supplies steel pipes for the energy industry, was a key positive contributor to the relative performance for the reporting period as its shares were buoyed by the rising oil price. German industrial gas supplier Linde plc was a key contributor to relative performance for the reporting period. The company’s stock price advanced on its positive operating profits as well as progress towards the completion of its US$45 billion merger with rival Praxair. Shares of UK exchange-listed consumer credit information services company Experian plc rose on robust results for its 2017 fiscal year and a favorable outlook for 2018.

Regarding portfolio activity over the period, we initiated a holding in Yum China, a leading restaurant-chain operator, as we like its mix of brands and believe that it may potentially benefit from attractive business prospects in China. We trimmed the Fund’s holdings in Shin-Etsu Chemical Co. and Taiwan Semiconductor Manufacturing Co. in an effort to diversify2 the Fund’s exposure to the semiconductor industry by reinvesting the sales proceeds into a new position in Infineon Technologies. We believe that Infineon Technologies is a high-quality business with a net-cash balance sheet that is well-established in automotive end-markets, and also serves the industrial automation market. Additionally, we initiated holdings in Chinese internet giant Tencent Holdings, as we think that the business offers good long-term growth opportunities and brings further diversification to the Fund, and Deutsche Boerse, as we believe that it is a well-managed securities exchange trading at an attractive valuation. We also established new positions in Swiss security group Dormakaba, which in our view possesses solid presence in various global markets and good financial metrics; Auckland International Airport, the largest airport in New Zealand, which we believe has a solid regional position and an effective strategy for medium- and long-term growth; Australia-based wine-maker Treasury Wine Estates, as we believe that it is well-positioned to benefit from growth internationally and its expansion of the premium range; British speciality chemicals company Croda, which in our view is a high-quality business poised to benefit from increasing demand for natural ingredients; and luxury products maker LVMH Moët Hennessy Louis Vuitton S.E., which as we think that it has a healthy diversified portfolio of brands and a good track record.

In contrast, we exited the Fund’s position in Canadian telecommunications company Telus Corp. to fund what we believed were better opportunities elsewhere. We sold the Fund’s shares in Hong Kong rail and property firm MTR Corporation. In our view, the stock’s valuation has captured many of the positives within the business, but not some of the risks associated with expanding the rail franchise beyond its core geographical areas. We also sold the Fund’s shares in Tenaris, as we considered the stock to be fully valued; hospitality chain Whitbread following its plans to sell its Costa Coffee business; and Ultrapar due to its deteriorating fundamentals and increased regulatory constraint. Furthermore, we exited the Fund’s position in South African telecom MTN Group given rising political risk attributable to a proposed fine by the Nigerian government, which alleged that the company illegally moved funds out of that country. Finally, we exited the positions in Singapore telecom Singtel due to the intense competition that the company faces, and Australia-based global mining giant BHP Billiton, as we believed that there were better opportunities elsewhere.

Global markets are beset by worries over rising interest rates, trade tensions and a slowing global economy. Although the U.S. market

| 1 | The S&P 500 Index is an unmanaged index considered representative of the U.S. stock market. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | Diversification does not ensure a profit or protect against a loss in a declining market. |

| 2018 Annual Report | 3 |

Aberdeen Select International Equity Fund (Unaudited)

initially appeared to be indifferent to these concerns, the technology rally which had underpinned the current bull market appears to have faltered. Other threats remain, including political uncertainty in Europe caused by tumultuous Brexit negotiations and Italy’s fiscal problems.

While the continued health of corporate earnings goes some way in calming investors’ nerves, we think that politics is increasingly overshadowing central bank policy to become the main driving force of market sentiment. In our view, shifting political alliances may keep markets on their toes but, at the same time, may provide discerning investors with opportunities to take advantage of mispricing of stocks. Amid such periods of uncertainty, we think that investors increasingly will seek high-quality stocks with defensive characteristics, which we believe should bode well for the Fund’s performance.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Stocks issued by large cap companies subject the Fund to the risk that those stocks may underperform stocks issued by companies with smaller capitalizations or the market as a whole.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 4 | Annual Report 2018 |

Aberdeen Select International Equity Fund (Unaudited)

| Average Annual Total Return* (For periods ended October 31, 2018) | 1 Yr. | 5 Yr. | 10 Yr. | |||||||

Class A** | (11.93%) | (0.71% | ) | 2.58% | ||||||

Institutional Class** | (11.71%) | (0.46% | ) | 2.83% | ||||||

| * | Performance shown for periods after December 16, 2016 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2008) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”). The receipt of these extraordinary payments increased the Fund’s performance for all periods that include December 2016 and February 2017 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. For Class A, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (11.93)%, (1.81)%, and 2.01%, respectively, for the 1-year, 5-year, and 10-year periods ended October 31, 2018. For Institutional Class, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (11.71)%, (1.55)%, and 2.26%, respectively, for the 1-year, 5-year, and 10-year periods ended October 31, 2018. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see Note 2(g) and the Fund’s prospectus dated February 28, 2018 for further information. |

| ** | Class A shares and Institutional Class shares are not subject to any sales charges. |

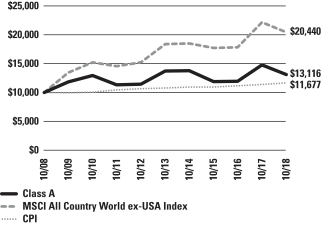

Performance of a $10,000 Investment (as of October 31, 2018)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund, Morgan Stanley Capital International All Country World ex-US Index (MSCI ACWI ex-USA Index), and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2018. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States (U.S.) and 24 Emerging Markets (EM) countries). With 2,163 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

| 2018 Annual Report | 5 |

Aberdeen Select International Equity Fund (Unaudited) (concluded)

Portfolio Summary (as a percentage of net assets)

October 31, 2018 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 94.3% | |||

Preferred Stocks | 8.7% | |||

Short-Term Investment | 0.3% | |||

Government Bonds | –% | |||

Liabilities in Excess of Other Assets | (3.3%) | |||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 69 industries and 158 sub-industries. As of October 31, 2018, the Fund did not have more than 25% of its assets invested in any single industry or industry group.

| Top Sectors | ||||

Financials | 18.3% | |||

Consumer Staples | 17.7% | |||

Industrials | 15.1% | |||

Health Care | 13.3% | |||

Information Technology | 12.2% | |||

Consumer Discretionary | 7.0% | |||

Materials | 6.5% | |||

Communication Services | 6.2% | |||

Real Estate | 4.0% | |||

Energy | 2.7% | |||

Other | (3.0%) | |||

| 100.0% | ||||

| Top Holdings* | ||||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.2% | |||

AIA Group Ltd. | 3.2% | |||

Samsung Electronics Co. Ltd., Preferred Shares | 3.1% | |||

Novartis AG | 2.8% | |||

Banco Bradesco SA, ADR, Preferred Shares, 1.94% | 2.8% | |||

Henkel AG & Co. KGaA, Preferred Shares, 1.33% | 2.7% | |||

Roche Holding AG | 2.7% | |||

Jardine Matheson Holdings Ltd. | 2.7% | |||

Royal Dutch Shell PLC, B Shares | 2.7% | |||

Japan Tobacco, Inc. | 2.6% | |||

Other | 71.5% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

United Kingdom | 19.3% | |||

Japan | 14.5% | |||

Germany | 11.8% | |||

Switzerland | 9.1% | |||

Hong Kong | 6.9% | |||

China | 4.3% | |||

South Korea | 4.2% | |||

Taiwan | 3.2% | |||

Canada | 3.2% | |||

Sweden | 3.1% | |||

Other | 20.4% | |||

| 100.0% | ||||

| 6 | Annual Report 2018 |

Statement of Investments

October 31, 2018

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (94.3%) | ||||||||

AUSTRALIA (2.6%) | ||||||||

Consumer Staples (1.0%) | ||||||||

Treasury Wine Estates Ltd. (a) | 144,744 | $ | 1,557,961 | |||||

Health Care (1.6%) | ||||||||

CSL Ltd. (a) | 18,500 | 2,469,697 | ||||||

| 4,027,658 | ||||||||

CANADA (3.2%) | ||||||||

Industrials (1.5%) | ||||||||

Ritchie Bros Auctioneers, Inc. | 69,000 | 2,320,878 | ||||||

Materials (1.7%) | ||||||||

Nutrien Ltd. | 48,640 | 2,574,896 | ||||||

| 4,895,774 | ||||||||

CHINA (4.3%) | ||||||||

Communication Services (1.8%) | ||||||||

Tencent Holdings Ltd. (a) | 81,400 | 2,788,704 | ||||||

Consumer Discretionary (2.5%) | ||||||||

Yum China Holdings, Inc. | 104,100 | 3,755,928 | ||||||

| 6,544,632 | ||||||||

FRANCE (2.7%) | ||||||||

Consumer Discretionary (1.1%) | ||||||||

LVMH Moet Hennessy Louis Vuitton SA (a) | 5,500 | 1,668,730 | ||||||

Consumer Staples (1.6%) | ||||||||

L’Oreal SA (a) | 11,200 | 2,523,430 | ||||||

| 4,192,160 | ||||||||

GERMANY (9.0%) | ||||||||

Financials (1.2%) | ||||||||

Deutsche Boerse AG (a) | 14,200 | 1,794,490 | ||||||

Health Care (4.4%) | ||||||||

Bayer AG (a) | 38,226 | 2,930,116 | ||||||

Fresenius Medical Care AG & Co. KGaA (a) | 49,100 | 3,855,160 | ||||||

| 6,785,276 | ||||||||

Information Technology (1.4%) | ||||||||

Infineon Technologies AG (a) | 110,600 | 2,216,080 | ||||||

Materials (2.0%) | ||||||||

Linde PLC (b) | 18,172 | 2,981,378 | ||||||

| 13,777,224 | ||||||||

HONG KONG (6.9%) | ||||||||

Financials (3.2%) | ||||||||

AIA Group Ltd. (a) | 636,400 | 4,841,122 | ||||||

Industrials (2.7%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 71,300 | 4,117,105 | ||||||

Real Estate (1.0%) | ||||||||

Swire Pacific Ltd., Class A (a) | 151,500 | 1,573,886 | ||||||

| 10,532,113 | ||||||||

INDIA (1.7%) | ||||||||

Financials (1.7%) | ||||||||

HDFC Bank Ltd., ADR | 28,600 | 2,542,826 | ||||||

ISRAEL (2.2%) | ||||||||

Information Technology (2.2%) | ||||||||

Check Point Software Technologies Ltd. (b) | 30,400 | 3,374,400 | ||||||

JAPAN (14.5%) | ||||||||

Consumer Discretionary (1.5%) | ||||||||

Shimano, Inc. (a) | 17,200 | 2,349,093 | ||||||

Consumer Staples (2.6%) | ||||||||

Japan Tobacco, Inc. (a) | 154,000 | 3,957,077 | ||||||

Financials (1.9%) | ||||||||

Japan Exchange Group, Inc. (a) | 164,400 | 2,944,521 | ||||||

Health Care (1.8%) | ||||||||

Sysmex Corp. (a) | 39,700 | 2,784,538 | ||||||

Industrials (1.6%) | ||||||||

FANUC Corp. (a) | 14,000 | 2,435,537 | ||||||

Information Technology (2.3%) | ||||||||

Keyence Corp. (a) | 7,200 | 3,517,341 | ||||||

Materials (1.7%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (a) | 30,800 | 2,573,663 | ||||||

Real Estate (1.1%) | ||||||||

Daito Trust Construction Co. Ltd. (a) | 12,700 | 1,674,347 | ||||||

| 22,236,117 | ||||||||

LATVIA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

AS Parex Banka (a)(b)(c)(d) | 1,424,182 | – | ||||||

MEXICO (2.4%) | ||||||||

Consumer Staples (2.4%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 42,700 | 3,632,489 | ||||||

NEW ZEALAND (1.1%) | ||||||||

Industrials (1.1%) | ||||||||

Auckland International Airport Ltd. (a) | 370,300 | 1,693,407 | ||||||

PHILIPPINES (1.9%) | ||||||||

Real Estate (1.9%) | ||||||||

Ayala Land, Inc. (a) | 3,919,300 | 2,908,135 | ||||||

SINGAPORE (2.1%) | ||||||||

Financials (2.1%) | ||||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 410,358 | 3,187,846 | ||||||

SOUTH KOREA (1.1%) | ||||||||

Consumer Staples (1.1%) | ||||||||

Amorepacific Group (a) | 30,800 | 1,688,160 | ||||||

SWEDEN (3.1%) | ||||||||

Industrials (3.1%) | ||||||||

Atlas Copco AB, A Shares (a) | 129,500 | 3,201,467 | ||||||

Epiroc AB, Class A (b) | 181,000 | 1,589,435 | ||||||

| 4,790,902 | ||||||||

See accompanying Notes to Financial Statements.

| 2018 Annual Report | 7 |

Statement of Investments (continued)

October 31, 2018

Aberdeen Select International Equity Fund

| Shares or Principal Amount | Value | |||||||

SWITZERLAND (9.1%) | ||||||||

Consumer Staples (2.4%) | ||||||||

Nestle SA (a) | 43,700 | $ | 3,689,289 | |||||

Health Care (5.5%) | ||||||||

Novartis AG (a) | 49,400 | 4,326,071 | ||||||

Roche Holding AG (a) | 17,000 | 4,137,161 | ||||||

| 8,463,232 | ||||||||

Industrials (1.2%) | ||||||||

dormakaba Holding AG (a)(b) | 2,446 | 1,764,645 | ||||||

| 13,917,166 | ||||||||

TAIWAN (3.2%) | ||||||||

Information Technology (3.2%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 657,000 | 4,932,352 | ||||||

THAILAND (2.0%) | ||||||||

Financials (2.0%) | ||||||||

Kasikornbank PCL (a) | 522,100 | 3,143,875 | ||||||

UNITED KINGDOM (19.3%) | ||||||||

Communication Services (4.4%) | ||||||||

Inmarsat PLC (a) | 559,700 | 3,254,896 | ||||||

Vodafone Group PLC (a) | 1,861,400 | 3,500,434 | ||||||

| 6,755,330 | ||||||||

Consumer Staples (3.8%) | ||||||||

British American Tobacco PLC (a) | 70,300 | 3,047,524 | ||||||

Diageo PLC (a) | 77,700 | 2,686,207 | ||||||

| 5,733,731 | ||||||||

Energy (2.7%) | ||||||||

Royal Dutch Shell PLC, B Shares (a) | 124,800 | 4,070,093 | ||||||

Financials (3.4%) | ||||||||

Prudential PLC (a) | 161,600 | 3,235,819 | ||||||

Standard Chartered PLC (a) | 285,100 | 1,998,182 | ||||||

| 5,234,001 | ||||||||

Industrials (3.9%) | ||||||||

Experian PLC (a) | 153,200 | 3,523,477 | ||||||

Rolls-Royce Holdings PLC (a) | 229,700 | 2,463,345 | ||||||

| 5,986,822 | ||||||||

Materials (1.1%) | ||||||||

Croda International PLC (a) | 27,471 | 1,692,092 | ||||||

| 29,472,069 | ||||||||

UNITED STATES (1.9%) | ||||||||

Consumer Discretionary (1.9%) | ||||||||

Samsonite International SA (a)(b)(e) | 990,900 | 2,857,737 | ||||||

VENEZUELA (0.0%) | ||||||||

Financials (0.0%) | ||||||||

Banco Venezolano de Credito SA (b)(c)(d) | 156 | – | ||||||

Industrials (0.0%) | ||||||||

Cemex Venezuela SACA-I (b)(c)(d) | 15,843,815 | – | ||||||

| – | ||||||||

Total Common Stocks | 144,347,040 | |||||||

GOVERNMENT BONDS (0.0%) | ||||||||

VENEZUELA (0.0%) | ||||||||

Bonos de la Deuda Publica Nacional (VEF), 0.00%, (b)(c)(d) | 69,500,000 | – | ||||||

Total Government Bonds | – | |||||||

PREFERRED STOCKS (8.7%) | ||||||||

BRAZIL (2.8%) | ||||||||

Financials (2.8%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares, 1.94% | 468,481 | 4,295,971 | ||||||

GERMANY (2.8%) | ||||||||

Consumer Staples (2.8%) | ||||||||

Henkel AG & Co. KGaA, Preferred Shares, 1.33% (a) | 38,200 | 4,173,531 | ||||||

SOUTH KOREA (3.1%) | ||||||||

Information Technology (3.1%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | 150,900 | 4,761,005 | ||||||

UNITED KINGDOM (0.0%) | ||||||||

Industrials (0.0%) | ||||||||

Rolls-Royce Holdings PLC, C Shares (b) | 10,566,200 | 13,505 | ||||||

Total Preferred Stocks | 13,244,012 | |||||||

SHORT-TERM INVESTMENT (0.3%) | ||||||||

UNITED STATES (0.3%) | ||||||||

State Street Institutional U.S. Government Money Market Fund, Premier Class, | $ | 451,376 | 451,376 | |||||

Total Short-Term Investment | 451,376 | |||||||

Total Investments | 158,042,430 | |||||||

Liabilities in Excess of Other Assets—(3.3)% | (5,026,551 | ) | ||||||

Net Assets—100.0% | $ | 153,015,879 | ||||||

| (a) | Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. Unless otherwise noted, securities are valued by applying valuation factors to the exchange traded price. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | The Fund’s adviser has deemed this security to be illiquid based upon procedures approved by the Board of Trustees. Illiquid securities held by the Fund represent 0.00% of net assets as of October 31, 2018. |

| (d) | Level 3 security. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (e) | Denotes a security issued under Regulation S or Rule 144A. |

See accompanying Notes to Financial Statements.

| 8 | Annual Report 2018 |

Statement of Investments (concluded)

October 31, 2018

Aberdeen Select International Equity Fund

| (f) | Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of October 31, 2018. |

| (g) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

See accompanying Notes to Financial Statements.

| 2018 Annual Report | 9 |

Aberdeen Select International Equity Fund II (Unaudited)

The Aberdeen Select International Equity Fund II (Institutional Class shares net of fees) returned -11.23% for the 12-month period ended October 31, 2018, versus -7.80% for its benchmark, the MSCI All Country (AC) World ex-USA Index, during the same period. For broader comparison, the average return of the Fund’s peer category of International Large-Cap Growth Funds (comprising 71 funds), as measured by Lipper, Inc., was –8.01%.

International equities declined over the reporting period. Investors were initially optimistic towards global economic growth, but investor sentiment turned more negative as the period progressed. Worries that rising inflation could compel more aggressive monetary policy, and a flare-up in trade tensions–especially as U.S.-China trade relations deteriorated amid rounds of brinkmanship–led to higher market volatility. The U.S. broader-market Standard & Poor’s (S&P) 500 Index1 initially shrugged off these concerns to record its longest bull run in history, supported by strong corporate earnings growth and a strengthening U.S. dollar. However, a spike in U.S. Treasury yields at the end of the reporting period triggered a slide in share prices as investors reassessed global stock valuations. Emerging markets also came under pressure due to the appreciating U.S. dollar.

The Fund underperformed its benchmark, the MSCI AC World ex-USA Index, for the reporting period due to negative stock selection.

At the stock level, South Korean beauty and cosmetics firm AmorePacific Group was a key detractor from the Fund’s relative performance, as the company’s shares declined after its results generally missed the market’s expectations. We are monitoring the stock’s performance. Shares of German pharmaceutical and life sciences group Bayer declined following an adverse court decision against weed-killers made by Monsanto, which the company recently acquired. While the damages have been reduced on appeal as we expected, the guilty verdict was upheld. We continue to monitor the situation closely. Brazilian fuel distributor Ultrapar Participacoes S.A.’s stock price moved lower eased in tandem with the broader Brazilian equity market, which declined due to an extended strike by truckers and concerns over economic reforms. We subsequently exited the Fund’s position in the company.

Conversely, the Fund’s position in German industrial gas supplier Linde plc was a key contributor to relative performance for the reporting period. The company’s stock price advanced on its positive operating profits as well as progress towards the completion of its US$45 billion merger with rival Praxair. Shares of UK exchange-listed consumer credit information services company Experian plc rose on robust results for its 2017 fiscal year and a favorable outlook for 2018. The stock price of Italy-listed Tenaris S.A., which supplies steel pipes for the energy industry, was buoyed by the rising oil price.

Regarding portfolio activity over the period, we initiated a holding in Yum China, a leading restaurant-chain operator, as we like its mix of brands and believe that it may potentially benefit from attractive business prospects in China. We trimmed the Fund’s holdings in Shin-Etsu Chemical Co. and Taiwan Semiconductor Manufacturing Co. in an effort to diversify2 the Fund’s exposure to the semiconductor industry by reinvesting the sales proceeds into a new position in Infineon Technologies. We believe that Infineon Technologies is a high-quality business with a net-cash balance sheet that is well-established in automotive end-markets, and also serves the industrial automation market. Additionally, we initiated holdings in Chinese internet giant Tencent Holdings, as we think that the business offers good long-term growth opportunities and brings further diversification to the Fund, and Deutsche Boerse, as we believe that it is a well-managed securities exchange trading at an attractive valuation. We also established new positions in Swiss security group Dormakaba, which in our view possesses solid presence in various global markets and good financial metrics; Auckland International Airport, the largest airport in New Zealand, which we believe has a solid regional position and an effective strategy for medium- and long-term growth; Australia-based wine-maker Treasury Wine Estates, as we believe that it is well-positioned to benefit from growth internationally and its expansion of the premium range; British speciality chemicals company Croda, which in our view is a high-quality business poised to benefit from increasing demand for natural ingredients; and luxury products maker LVMH Moët Hennessy Louis Vuitton S.E., which as we think that it has a healthy diversified portfolio of brands and a good track record.

In contrast, we exited the Fund’s position in Canadian telecommunications company Telus Corp. to fund what we believed were better opportunities elsewhere. We sold the Fund’s shares in Hong Kong rail and property firm MTR Corporation. In our view, the stock’s valuation has captured many of the positives within the business, but not some of the risks associated with expanding the rail franchise beyond its core geographical areas. We also sold the Fund’s shares in Tenaris, as we considered the stock to be fully valued; hospitality chain Whitbread following its plans to sell its Costa Coffee business; and Ultrapar due to its deteriorating fundamentals and increased regulatory constraint. Furthermore, we exited the Fund’s position in South African telecom MTN Group given rising political risk attributable to a proposed fine by the Nigerian government, which alleged that the company illegally moved funds out of that country. Finally, we exited the positions in Singapore telecom Singtel due to the intense competition that the company faces, and Australia-based global mining giant BHP Billiton, as we believed that there were better opportunities elsewhere.

| 1 | The S&P 500 Index is an unmanaged index considered representative of the U.S. stock market. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | Diversification does not ensure a profit or protect against a loss in a declining market. |

| 10 | Annual Report 2018 |

Aberdeen Select International Equity Fund II (Unaudited)

Global markets are beset by worries over rising interest rates, trade tensions and a slowing global economy. Although the U.S. market initially appeared to be indifferent to these concerns, the technology rally which had underpinned the current bull market appears to have faltered. Other threats remain, including political uncertainty in Europe caused by tumultuous Brexit negotiations and Italy’s fiscal problems.

While the continued health of corporate earnings goes some way in calming investors’ nerves, we think that politics is increasingly overshadowing central bank policy to become the main driving force of market sentiment. In our view, shifting political alliances may keep markets on their toes but, at the same time, may provide discerning investors with opportunities to take advantage of mispricing of stocks. Amid such periods of uncertainty, we think that investors increasingly will seek high-quality stocks with defensive characteristics, which we believe should bode well for the Fund’s performance.

Portfolio Management:

Aberdeen Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance quoted represents past performance, which does not guarantee future results. Class A Shares have up to a 0.25% 12b-1 fee. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 866-667-9231 or visiting www.aberdeen-asset.us.

Investing in mutual funds involves risk, including the possible loss of principal. There is no assurance that the investment objective of any fund will be achieved. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Lipper is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

Risk Considerations

Foreign securities may be more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and currency exchange rate, political and economic risks. Fluctuation in currency exchange rates may impact a Fund’s returns more greatly to the extent a Fund does not hedge currency exposure or hedging techniques are unsuccessful. The foregoing risks are enhanced in emerging market countries.

Equity stocks of small- and mid-cap companies carry greater risk and more volatility than equity stocks of larger, more established companies.

Stocks issued by large cap companies subject the Fund to the risk that those stocks may underperform stocks issued by companies with smaller capitalizations or the market as a whole.

Investing a significant portion of the Fund’s assets in securities of companies conducting business in a broadly related group of industries within an economic sector may make the Fund more vulnerable to unfavorable developments in that sector.

Please read the prospectus for more detailed information regarding these and other risks.

| 2018 Annual Report | 11 |

Aberdeen Select International Equity Fund II (Unaudited)

Average Annual Total Return* (For periods ended October 31, 2018) | 1 Yr. | 5 Yr. | 10 Yr. | |||||||

Class A** | (11.48%) | (0.91% | ) | 2.75% | ||||||

Institutional Class** | (11.23%) | (0.66% | ) | 3.02% | ||||||

| * | Performance shown for periods after February 1, 2017 reflect the Fund’s receipt of payment from some European jurisdictions related to prior years (2005-2009) in accordance with European Union law under Article 63 of the Treaty on the Functioning of the European Union (the “Article 63 EU Tax Reclaims”). The receipt of these extraordinary payments increased the Fund’s performance for all periods that include February 2017 in a manner that may not recur in the future, and the Fund’s performance was significantly higher than it would have been absent receipt of the Article 63 EU Tax Reclaims. For Class A, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (11.73)%, (1.63)% and 2.38%, respectively, for the 1-year, 5-year, and 10-year periods ended October 31, 2018. For Institutional Class, the average annual total return excluding the receipt of Article 63 EU Tax Reclaims was (11.48)%, (1.37) and 2.65%, respectively, for the 1-year, 5-year, and 10-year periods ended October 31, 2018. There can be no assurance that the Fund will receive additional Article 63 EU Tax Reclaim payments or maintain this level of performance in the future. Please see the Fund’s prospectus dated February, 28, 2018 for further information. |

| ** | Class A shares and Institutional Class shares are not subject to any sales charges. |

Performance of a $10,000 Investment (as of October 31, 2018)

Comparative performance of $10,000 invested in Class A shares of the Aberdeen Select International Equity Fund II, Morgan Stanley Capital International All Country World ex-US Index (MSCI ACWI ex-USA Index), and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2018. Unlike the Fund’s returns, the returns for these unmanaged indexes do not reflect any fees or expenses. Investors cannot invest directly in market indexes.

The MSCI ACWI ex-USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the United States (U.S.) and 24 Emerging Markets (EM) countries). With 2,163 constituents, the index covers approximately 85% of the global equity opportunity set outside the U.S.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and performance graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions.

| 12 | Annual Report 2018 |

Aberdeen Select International Equity Fund II (Unaudited) (concluded)

Portfolio Summary (as a percentage of net assets)

October 31, 2018 (Unaudited)

| Asset Allocation | ||||

Common Stocks | 92.9% | |||

Preferred Stocks | 8.7% | |||

Short-Term Investment | 0.5% | |||

Liabilities in Excess of Other Assets | (2.1%) | |||

| 100.0% | ||||

The following table summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets. The GICS structure consists of 11 sectors, 24 industry groups, 69 industries and 158 sub-industries. As of October 31, 2018, the Fund did not have more than 25% of its assets invested in any single industry or industry group.

| Top Sectors | ||||

Financials | 18.2% | |||

Consumer Staples | 17.3% | |||

Industrials | 14.9% | |||

Health Care | 13.1% | |||

Information Technology | 12.2% | |||

Consumer Discretionary | 6.8% | |||

Materials | 6.3% | |||

Communication Services | 6.2% | |||

Real Estate | 4.0% | |||

Energy | 2.6% | |||

Other | (1.6%) | |||

| 100.0% | ||||

| Top Holdings* | ||||

Samsung Electronics Co. Ltd., Preferred Shares | 3.2% | |||

Taiwan Semiconductor Manufacturing Co. Ltd. | 3.2% | |||

AIA Group Ltd. | 3.1% | |||

Novartis AG | 2.8% | |||

Banco Bradesco SA, ADR, Preferred Shares, 1.94% | 2.8% | |||

Jardine Matheson Holdings Ltd. | 2.7% | |||

Henkel AG & Co. KGaA, Preferred Shares, 1.33% | 2.7% | |||

Roche Holding AG | 2.6% | |||

Royal Dutch Shell PLC, B Shares | 2.6% | |||

Japan Tobacco, Inc. | 2.5% | |||

Other | 71.8% | |||

| 100.0% | ||||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | ||||

United Kingdom | 18.9% | |||

Japan | 14.4% | |||

Germany | 11.6% | |||

Switzerland | 9.0% | |||

Hong Kong | 6.8% | |||

South Korea | 4.3% | |||

China | 4.2% | |||

Taiwan | 3.2% | |||

Sweden | 3.1% | |||

Canada | 3.1% | |||

Other | 21.4% | |||

| 100.0% | ||||

| 2018 Annual Report | 13 |

Statement of Investments

October 31, 2018

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

COMMON STOCKS (92.9%) | ||||||||

AUSTRALIA (2.5%) | ||||||||

Consumer Staples (1.0%) | ||||||||

Treasury Wine Estates Ltd. (a) | 59,850 | $ | 644,199 | |||||

Health Care (1.5%) | ||||||||

CSL Ltd. (a) | 7,000 | 934,480 | ||||||

| 1,578,679 | ||||||||

CANADA (3.1%) | ||||||||

Industrials (1.4%) | ||||||||

Ritchie Bros Auctioneers, Inc. | 27,000 | 908,170 | ||||||

Materials (1.7%) | ||||||||

Nutrien Ltd. | 20,400 | 1,079,931 | ||||||

| 1,988,101 | ||||||||

CHINA (4.2%) | ||||||||

Communication Services (1.8%) | ||||||||

Tencent Holdings Ltd. (a) | 33,700 | 1,154,537 | ||||||

Consumer Discretionary (2.4%) | ||||||||

Yum China Holdings, Inc. | 43,300 | 1,562,264 | ||||||

| 2,716,801 | ||||||||

FRANCE (2.7%) | ||||||||

Consumer Discretionary (1.1%) | ||||||||

LVMH Moet Hennessy Louis Vuitton SA (a) | 2,300 | 697,833 | ||||||

Consumer Staples (1.6%) | ||||||||

L’Oreal SA (a) | 4,700 | 1,058,939 | ||||||

| 1,756,772 | ||||||||

GERMANY (8.9%) | ||||||||

Financials (1.2%) | ||||||||

Deutsche Boerse AG (a) | 5,900 | 745,598 | ||||||

Health Care (4.4%) | ||||||||

Bayer AG (a) | 16,034 | 1,229,045 | ||||||

Fresenius Medical Care AG & Co. KGaA (a) | 20,000 | 1,570,330 | ||||||

| 2,799,375 | ||||||||

Information Technology (1.4%) | ||||||||

Infineon Technologies AG (a) | 45,900 | 919,693 | ||||||

Materials (1.9%) | ||||||||

Linde PLC (b) | 7,546 | 1,238,030 | ||||||

| 5,702,696 | ||||||||

HONG KONG (6.8%) | ||||||||

Financials (3.1%) | ||||||||

AIA Group Ltd. (a) | 264,800 | 2,014,345 | ||||||

Industrials (2.7%) | ||||||||

Jardine Matheson Holdings Ltd. (a) | 30,000 | 1,732,302 | ||||||

Real Estate (1.0%) | ||||||||

Swire Pacific Ltd., Class A (a) | 62,000 | 644,099 | ||||||

| 4,390,746 | ||||||||

INDIA (1.6%) | ||||||||

Financials (1.6%) | ||||||||

HDFC Bank Ltd., ADR | 11,800 | 1,049,138 | ||||||

ISRAEL (2.2%) | ||||||||

Information Technology (2.2%) | ||||||||

Check Point Software Technologies Ltd. (b) | 12,600 | 1,398,600 | ||||||

JAPAN (14.4%) | ||||||||

Consumer Discretionary (1.5%) | ||||||||

Shimano, Inc. (a) | 7,100 | 969,684 | ||||||

Consumer Staples (2.5%) | ||||||||

Japan Tobacco, Inc. (a) | 63,200 | 1,623,943 | ||||||

Financials (2.1%) | ||||||||

Japan Exchange Group, Inc. (a) | 75,000 | 1,343,303 | ||||||

Health Care (1.8%) | ||||||||

Sysmex Corp. (a) | 16,600 | 1,164,316 | ||||||

Industrials (1.6%) | ||||||||

FANUC Corp. (a) | 5,800 | 1,009,008 | ||||||

Information Technology (2.2%) | ||||||||

Keyence Corp. (a) | 2,900 | 1,416,707 | ||||||

Materials (1.6%) | ||||||||

Shin-Etsu Chemical Co. Ltd. (a) | 12,700 | 1,061,218 | ||||||

Real Estate (1.1%) | ||||||||

Daito Trust Construction Co. Ltd. (a) | 5,300 | 698,743 | ||||||

| 9,286,922 | ||||||||

MEXICO (2.3%) | ||||||||

Consumer Staples (2.3%) | ||||||||

Fomento Economico Mexicano SAB de CV, ADR | 17,600 | 1,497,232 | ||||||

NEW ZEALAND (1.1%) | ||||||||

Industrials (1.1%) | ||||||||

Auckland International Airport Ltd. (a) | 153,100 | 700,137 | ||||||

PHILIPPINES (1.9%) | ||||||||

Real Estate (1.9%) | ||||||||

Ayala Land, Inc. (a) | 1,630,100 | 1,209,540 | ||||||

SINGAPORE (2.1%) | ||||||||

Financials (2.1%) | ||||||||

Oversea-Chinese Banking Corp. Ltd. (a) | 177,899 | 1,382,000 | ||||||

SOUTH KOREA (1.1%) | ||||||||

Consumer Staples (1.1%) | ||||||||

Amorepacific Group (a) | 12,800 | 701,573 | ||||||

SWEDEN (3.1%) | ||||||||

Industrials (3.1%) | ||||||||

Atlas Copco AB, A Shares (a) | 53,900 | 1,332,503 | ||||||

Epiroc AB, Class A (b) | 75,300 | 661,240 | �� | |||||

| 1,993,743 | ||||||||

See accompanying Notes to Financial Statements.

| 14 | Annual Report 2018 |

Statement of Investments (concluded)

October 31, 2018

Aberdeen Select International Equity Fund II

| Shares or Principal Amount | Value | |||||||

SWITZERLAND (9.0%) | ||||||||

Consumer Staples (2.4%) | ||||||||

Nestle SA (a) | 18,400 | $ | 1,553,385 | |||||

Health Care (5.4%) | ||||||||

Novartis AG (a) | 20,400 | 1,786,474 | ||||||

Roche Holding AG (a) | 7,000 | 1,703,537 | ||||||

| 3,490,011 | ||||||||

Industrials (1.2%) | ||||||||

dormakaba Holding AG (a)(b) | 1,034 | 745,970 | ||||||

| 5,789,366 | ||||||||

TAIWAN (3.2%) | ||||||||

Information Technology (3.2%) | ||||||||

Taiwan Semiconductor Manufacturing Co. Ltd. (a) | 271,000 | 2,034,501 | ||||||

THAILAND (2.0%) | ||||||||

Financials (2.0%) | ||||||||

Kasikornbank PCL (a) | 215,800 | 1,299,460 | ||||||

UNITED KINGDOM (18.9%) | ||||||||

Communication Services (4.4%) | ||||||||

Inmarsat PLC (a) | 232,800 | 1,353,832 | ||||||

Vodafone Group PLC (a) | 777,500 | 1,462,119 | ||||||

| 2,815,951 | ||||||||

Consumer Staples (3.7%) | ||||||||

British American Tobacco PLC (a) | 29,300 | 1,270,163 | ||||||

Diageo PLC (a) | 32,300 | 1,116,660 | ||||||

| 2,386,823 | ||||||||

Energy (2.6%) | ||||||||

Royal Dutch Shell PLC, B Shares (a) | 51,600 | 1,682,827 | ||||||

Financials (3.3%) | ||||||||

Prudential PLC (a) | 67,400 | 1,349,592 | ||||||

Standard Chartered PLC (a) | 112,300 | 787,078 | ||||||

| 2,136,670 | ||||||||

Industrials (3.8%) | ||||||||

Experian PLC (a) | 63,800 | 1,467,348 | ||||||

Rolls-Royce Holdings PLC (a) | 95,500 | 1,024,160 | ||||||

| 2,491,508 | ||||||||

Materials (1.1%) | ||||||||

Croda International PLC (a) | 11,306 | 696,400 | ||||||

| 12,210,179 | ||||||||

UNITED STATES (1.8%) | ||||||||

Consumer Discretionary (1.8%) | ||||||||

Samsonite International SA (a)(b)(c) | 411,700 | 1,187,335 | ||||||

Total Common Stocks | 59,873,521 | |||||||

PREFERRED STOCKS (8.7%) | ||||||||

BRAZIL (2.8%) | ||||||||

Financials (2.8%) | ||||||||

Banco Bradesco SA, ADR, Preferred Shares, 1.94% | 193,567 | 1,775,009 | ||||||

GERMANY (2.7%) | ||||||||

Consumer Staples (2.7%) | ||||||||

Henkel AG & Co. KGaA, Preferred Shares, 1.33% (a) | 15,800 | 1,726,225 | ||||||

SOUTH KOREA (3.2%) | ||||||||

Information Technology (3.2%) | ||||||||

Samsung Electronics Co. Ltd., Preferred Shares (a) | 65,500 | 2,066,573 | ||||||

UNITED KINGDOM (0.0%) | ||||||||

Industrials (0.0%) | ||||||||

Rolls-Royce Holdings PLC, C Shares (b) | 4,393,000 | 5,615 | ||||||

Total Preferred Stocks | 5,573,422 | |||||||

SHORT-TERM INVESTMENT (0.5%) | ||||||||

UNITED STATES (0.5%) | ||||||||

State Street Institutional U.S. Government Money Market Fund, Premier Class, 2.09% (d) | 332,172 | 332,172 | ||||||

Total Short-Term Investment | 332,172 | |||||||

Total Investments | 65,779,115 | |||||||

Liabilities in Excess of Other Assets—(2.1)% | (1,338,076 | ) | ||||||

Net Assets—100.0% | $ | 64,441,039 | ||||||

| (a) | Fair Values are determined pursuant to procedures approved by the Fund’s Board of Trustees. Unless otherwise noted, securities are valued by applying valuation factors to the exchange traded price. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (b) | Non-income producing security. |

| (c) | Denotes a security issued under Regulation S or Rule 144A. |

| (d) | Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of October 31, 2018. |

| (e) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

See accompanying Notes to Financial Statements.

| 2018 Annual Report | 15 |

Aberdeen Total Return Bond Fund (Unaudited)

The Aberdeen Total Return Bond Fund (Institutional Class shares net of fees) returned -2.96% for the 12-month period ended October 31, 2018, versus the -2.05% return of its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, for the same period. For broader comparison, the average return of the Fund’s Lipper peer category of Core Bond Funds (comprising 221 funds) was -2.01% for the period.

Following a relatively calm period in 2017, volatility returned to global financial markets in the first quarter of 2018, with a major expansion of U.S. fiscal policy, some nascent signs of inflation, and fear of a trade war. U.S. economic growth remained solid over the 12-month reporting period, with momentum and expectations accelerating and then receding somewhat. The labor market continued to tighten, with U.S. payrolls expanding by a monthly average of 210,000 during the 12-month reporting period, and the unemployment rate dipped 0.4 percentage point to 3.7% – its lowest level since December 1969.1 The labor force participation rate2 rose 0.2 percentage point, ending the reporting period at 62.9%.3 With such tight labor supply and the Consumer Price Index (CPI), an inflation indicator, approaching the U.S. Federal Reserve’s (Fed’s) annualized target rate of 2%, the economy received an unusual and large late-cycle fiscal boost, as the Republican majority in the U.S. Congress enacted tax reform legislation in December 2017. The tax reform bill cuts tax rates for corporations and individuals and reduces or eliminates some personal deductions, with estimated cost of more than $1.5 trillion over 10 years. The package is very favorable to corporations, which we believe should be supportive of credit markets as well as business and consumer sentiment. Congress also passed a budget that includes a $400 billion fiscal stimulus package.

The Fed, under the leadership of new Chair Jerome Powell, who succeeded Janet Yellen in early February 2018, appeared to be increasingly confident that the U.S. economy can withstand higher interest rates. Over the reporting period, the central bank raised its benchmark interest rate in four increments of 25 basis points (bps) to a range of 2.00% to 2.25% following its meetings in December 2017, and March, June and September 2018, and revised upward its expectations for the pace at which it will increase rates in 2019. U.S. companies generally reported strong fourth-quarter 2017 earnings results as they began to communicate the effect of the recently implemented U.S. tax cuts on their profits, while estimates of profit growth rose. Investors’ exuberance was curtailed by several economic data releases indicating signs of higher wages and inflation. Political uncertainty further unsettled the markets as the administration of President Donald Trump ramped up its threat of trade wars amid White House cabinet reshuffling. The U.S. announced tariffs on $50 billion in Chinese imports, and the Chinese government responded more promptly than expected. The threat of escalation of geopolitical hotspots also exacerbated the jittery market.

In the second quarter of 2018, the global financial markets were dominated by increasing concerns about trade conflicts, political discords in Europe and Japan, as well as an anticipation of reduced monetary stimuli. U.S. President Donald Trump upped the ante, introducing or proposing broader import tariffs in a faster and larger fashion against China and other regions. Italian bonds weakened significantly versus comparable-duration4 German Bunds as Euroskeptic5 political parties formed a government. In Germany, Chancellor Angela Merkel’s coalition government was under increasing strain. Prime Minister Mariano Rajoy of Spain was forced to resign and was replaced by Socialist party leader Pedro Sánchez. In the UK, Brexit negotiations appeared increasingly fraught for the government as deadlines for critical decisions loom. In Japan, the ruling Liberal Democratic Party (LDP) government was mired in a cronyism scandal in which Prime Minister Shinzo Abe’s popularity plummeted. U.S. Treasury yields reversed their uptrend as investors sought safe-haven assets against mounting political risks.

The U.S. was the bright spot and dominant force in global economic and financial markets and political developments in the third quarter. The U.S. saw strong economic growth, a very tight labor market and signs of moderate inflation uplift. Corporate earnings were robust, with mergers-and-acquisition (M&A) activity reaching a post-global credit crisis high, while monetary policy remained relatively easy. The U.S. Federal Open Market Committee (FOMC) became more confident in signaling a steady path of interest-rate increases that led to a another 25-bps increase and a higher expected terminal rate.6 Meanwhile, a quasi-trade war materialized, with U.S. President Donald Trump dominating the conversation. The U.S. started to levy tariffs on an additional US$200 billion of Chinese imports and is seeking to implement another US$260 billion. China responded in kind without escalating rhetoric while allowing its currency, the renminbi, depreciate a further 3.7% against the U.S. dollar. President Trump also threatened to impose up to a 25% tariff on autos manufactured in European Union (EU) member nations, which his meeting with EU President Donald Tusk defused the chance of imminent action. Toward the end of the quarter, the U.S. finally reached an agreement with Mexico on the modification of the North American Free Trade Agreement (NAFTA), as well as a new trade agreement with Korea.

Despite continued threats from trade, growth stabilized above-historical trend levels across Europe, with purchasing managers indexes (PMIs) hovering in the mid-50s (indicating economic expansion). Eurozone inflation readings remained subdued, with only

| 1,3 | Source: U.S. Department of Labor, November 2018. |

| 2 | The labor force participation rate comprises the percentage of the U.S. population aged 16 years and older working or actively seeking work. |

| 4 | Duration is an estimate of bond price sensitivity to changes in interest rates. The higher the duration, the greater the change (i.e., higher risk) in relation to interest-rate movements. |

| 5 | Euroskeptics are opposed to increasing the powers of the European Union. |

| 6 | The terminal rate is the federal funds rate that is consistent with full employment and capacity utilization and stable prices. |

| 16 | Annual Report 2018 |

Aberdeen Total Return Bond Fund (Unaudited)

pockets of wage growth in the core markets, which enabled the European Central Bank (ECB) to double down on dovish monetary policy guidance. Italian budgetary fears have kept Italian yields elevated and core bonds well bid. While we think that the fundamental outlook for the UK remains uncertain due to Brexit headwinds, third-quarter 2018 data broadly have surprised to the upside relative to the markets’ expectations, allowing the Monetary Policy Committee (MPC) to hike its benchmark interest rate in August. At its July meeting the Bank of Japan (BoJ) tweaked the language around yield curve control7 to increase the flexibility around the 0% 10-year yield target. Policy sustainability is cited as the driving rationale, and the Japanese government bond (JGB) yield curve bear steepened.8 Trade tensions exacerbated existing growth challenges in China. Fixed investment and retail sales slowed along with credit growth. However, the Chinese government began to expand fiscal and regulatory measures in addition to loosening monetary policy.

The Fund’s international exposure to both bonds and currencies significantly hampered relative performance for the quarter. The Fund’s investments in the commodity market segment were the main source of its underperformance, as local currency government bonds in South Africa and Russia experienced substantial declines. Local currency Norwegian government bonds lagged comparable-duration U.S. Treasuries, while the benefits from the currency exposure in Chile was not enough to cushion losses from the Colombian peso and Australian dollar. Within the Fund’s low correlation segment,9 the Indian rupee was hard hit as oil prices rose sharply during the quarter. Indonesian government bonds declined notably, but our currency-hedging activities offset some of the losses. The Fund’s exposure in its major market segment was limited to the Japanese yen, which failed to act as a safe-haven asset as trade war rhetoric expanded. The euro declined and its neighboring currencies experienced collateral damage; the Fund’s Swedish krona position recorded a negative return for the quarter despite strong economic growth as inflation in that nation remained subdued. The holding in the Czech koruna marginally detracted from Fund performance as well, even though its central bank hiked interest rates due to strong growth.

Conversely, the Fund’s investments in its U.S. core market contributed to the performance relative to the benchmark index for the quarter. Sector allocation decisions produced positive results, particularly from the exposure to collateralized mortgage obligations (CMOs). Overall security selection also generated positive alpha,10 with corporate bonds posting strong performance largely from banks and energy names, which was augmented by gains from our emphasis on short-maturity asset-backed securities (ABS).

Fund performance also benefited from the addition of risk exposure to corporate and securitized credits that we had implemented in the second quarter and in August 2018, when spreads had widened with volatility. Specifically, the primary contributor was the compression of the Libor overnight indexed swap (OIS) spread,11 which drove short-end spreads tighter as we had expected and where the Fund had heavy exposure. Moreover, the Fund’s sizable underweight in the weakest-performing sector over the quarter, agency MBS, had a positive impact on performance. Unfortunately, the Fund’s investments in local currency foreign bonds continued to underperform, as the strong U.S. dollar remained a significant headwind. We added exposure, particularly in emerging markets (EMs), when contagion from Italy and a few problematic high-yielding EM countries affected global markets. When numerous countries were hit in waves without regard to their fundamentals, we increased the Fund’s weighting in a few conviction trades since we believe that a reasonable amount of recession-like risk has been priced into these markets.

We employed derivatives over the reporting period, including U.S. Treasury futures, in an effort to manage the Fund’s overall yield-curve and interest-rate exposure, and protect the Fund from sharply rising yields. We utilized foreign exchange forwards12 in an effort to gain exposure to foreign markets efficiently and to hedge currency risks from sovereign bond holdings. Our use of futures bolstered the Fund’s performance in global interest-rate allocation and yield-curve positioning. The derivatives positions did not have a significant impact on Fund performance for the reporting period.

We believe that the global economy will be strong in the near term, but may slow over the next year or two to historical trend levels, driven by fading fiscal and monetary stimuli. In our opinion, the extent of the slowdown will depend on the magnitude of monetary tightening and its impact on financial conditions, as well as

| 7 | The Bank of Japan employs yield curve control to keep the 10-year Japanese government bond yield at zero in an effort to steepen the yield curve, thereby increasing the difference between the yields of short- and long-term term bonds. |

| 8 | A bear steepener is the widening of the yield curve caused by long-term rates increasing at a faster rate than short-term rates, leading to a larger spread between the two rates. |

| 9 | The Fund’s investment universe includes six global fixed-income market segments: Core (U.S. investment-grade fixed income); Major (Eurozone, Japan and the UK, among others); Satellites (including, but not limited to Canada, Hong Kong and Switzerland); Convergence (Czech Republic, Hungary and Poland, among others); Commodity (including, but not limited to, Australia, Chile and Russia); and Low Correlation (Brazil, China and Mexico, among others). |

| 10 | Alpha is a measure of performance that takes the volatility of a mutual fund and compares its risk-adjusted performance to a benchmark index. |

| 11 | The London Interbank Offered Rate (Libor) is the most common benchmark interest rate index used to make adjustments to variable-rate loans and credit cards. Global banks use Libor when charging each other for short-term loans. The overnight indexed swap (OIS) is an interest rate swap in which the overnight rate being exchanged for a fixed interest rate. |

| 12 | A foreign exchange forward is a binding contract in the foreign exchange market that locks in the exchange rate for the purchase or sale of a currency on a future date. |

| 2018 Annual Report | 17 |

Aberdeen Total Return Bond Fund (Unaudited)

developments on trade and other geopolitical events, although we think that the probability of a recession has increased. We feel that the deceleration of economic growth in emerging markets, particularly in China, is not as dire as that market appears to be pricing in. Despite the limitation from high leverage, we believe that the Chinese government will loosen fiscal and regulatory measures to counter the headwind from trade conflicts, in addition to further easing monetary policy. There are other levers and non-tariff measures that China can use in response to an aggressive stance by the U.S., including an outside risk of currency devaluation. Populist governments pose risks with late-cycle fiscal expansion. The instability of the Italian government and Brexit in the UK represent many geopolitical risks facing the markets. The mismatch between the politicians’ promises and what they can do to keep the deficit in a range acceptable to the EU will be challenging though not unachievable, in our view. We think that the most likely outcome for Brexit is to kick the can down the road, though the odds that there will be no deal have increased.