UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-7062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2007 |

| ||||||

Item 1. Report to Shareholders

semi-annual report

june 30, 2007

government securities fund

income and equity fund

balanced fund

growth fund

multi-cap value fund

small cap fund

Pacific Advisors

table of contents

| Message from the Chairman | 1 | ||||||

| Government Securities Fund | 3 | ||||||

| Income and Equity Fund | 7 | ||||||

| Balanced Fund | 11 | ||||||

| Growth Fund | 15 | ||||||

| Multi-Cap Value Fund | 19 | ||||||

| Small Cap Fund | 23 | ||||||

| Statement of Investments | 29 | ||||||

| Statement of Assets and Liabilities | 54 | ||||||

| Statement of Operations | 56 | ||||||

| Statement of Changes in Net Assets | 58 | ||||||

| Notes to Financial Statements | 62 | ||||||

| Financial Highlights | 68 | ||||||

| Directors and Officers | 75 | ||||||

This Report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current effective prospectus of the Fund, which contains information concerning the investment policies of the Fund as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation, or a recommendation that any particular investor should purchase or sell any particular security. The statements in the Report are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change with market conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders:

Two steps forward and a half step back best described the equity markets during the first half of the year. In April and May, the market rallied in response to reports of stronger economic growth and consumer spending. In June, however, the market retreated somewhat as investors worried about higher inflation, a surge in oil prices, the impact of sub-prime debt defaults in the bond market, and potentially weaker second quarter earnings.

While the equity markets pulled back in response to market events in Asia and the deterioration of sub-prime debt portfolios, these market declines were brief. Overall, concerns about rising energy prices, a weak U.S. housing market, and troubled hedge funds were offset by stronger economic growth in the second quarter. Specific attention was paid to better-than-expected corporate profits, robust merger and acquisition activity, and strong consumer spending. As a result, the equity markets continued to advance.

Higher interest rates and the downturn in the housing market created a more bearish outlook for the credit markets. Low interest rates and lax loan underwriting in the mortgage, hedge fund and private equity markets provided capital for more aggressive investment strategies. As interest rates rose and the Federal Reserve showed no signs of easing interest rates, liquidity in the credit markets deteriorated. Borrowers whose collateral assets have declined in value or who are unable to fund their higher cost debt repayments bear the greatest risk. These events have negatively impacted both the equity and credit markets more recently.

Economic Review

In the first half of the year, the U.S. economy forged ahead at a moderate pace while the rate of growth worldwide exceeded 5%. However, economic growth rates varied widely, with countries such as Japan, Italy and France experiencing lackluster growth. In contrast, Germany and countries in the Eastern European bloc are experiencing strong economic growth as a result of lower corporate tax rates, business friendly labor policies, and significant increases in infrastructure spending. India and China continue to grow at rates exceeding 8% driven by soaring demand for goods and services and economic and infrastructure development in these countries and throughout Asia.

After growing at an anemic 0.7% rate in the first quarter, U.S. Gross Domestic Product (GDP) growth rebounded to 3.4% in the second quarter. The job market echoed this rebound with a historically low unemployment rate of 4.5% through June. Consumers remained confident and continued to spend despite rising energy prices and a downturn in the housing market. Additionally, a slowdown in the upward trend in core inflation eased broader concerns that the Fed would need to raise interest rates. While U.S. economic growth lagged in the first half of the year, it appears it should be stronger in the second half of the year. Overall growth for the year is expected to be at a moderate and sustainable rate in the range of 2.5% to 3.0%.

Market Review

| June 30, 2007 | Close | YTD Return | |||||||||

| Dow Jones | 13,408.62 | 7.59 | % | ||||||||

| S&P 500 | 1,503.35 | 6.96 | % | ||||||||

| NASDAQ | 2,603.23 | 7.78 | % | ||||||||

| Russell 2000 (small cap) | 833.69 | 6.45 | % | ||||||||

| 06/30/07 | 06/30/06 | ||||||||||

| 10-Year T-Note Yield | 5.03 | % | 5.15 | % | |||||||

Data: The Wall Street Journal

During the past year, the federal budget deficit has been reduced significantly by soaring tax revenues. The federal budget deficit as a percentage of GDP has fallen below 2%, which is significantly lower than the historical average of 2.5%. The Congressional Budget Office estimates that the U.S. budget deficit will be -$157 billion in 2007 compared to -$248 billion for 2006. A shrinking deficit would reduce the issuance of new government bonds and could even result in calling in existing bonds. These trends when coupled with lower demand for mortgage debt from lenders and government agencies could produce the benefit of lower interest rates in the coming year.

Equity Markets

The equity markets achieved strong gains as evidenced by the Dow Jones reaching several new highs over the second quarter and in July. Day-to-day market volatility remained high as news-of-the-day swayed market action up and down.

Until recently, the market had rallied without a significant correction during the past year. The current correction in the equity markets was overdue and its magnitude is not unusual for a normal bull market cycle. Interim pullbacks serve the purpose of removing excess speculation and providing a more stable base for

1

Message

from the chairman continued

continued growth. We believe the longer-term outlook for the equity markets remains positive. Near-term, the equity markets may take some time to rebound while the credit markets stabilize.

Currently, the market seems willing to accept a moderating economy, strong corporate profits, and stable interest rates as sufficient reasons to buy. Over the near-term, we will pay close attention to certain factors which may have a greater impact on the market. These factors include energy inflation as the price of oil has risen above $70 per barrel; further disruption in the sub-prime market and related derivative securities; and the severity of the downturn in the housing market. Any of these factors, could prompt the market to abruptly pull back further, especially if accompanied by disappointing third quarter corporate earnings. Furthermore, the threat of unexpected geopolitical events is always a market concern.

Fixed Income Investment Review

The Fed has continued to keep the fed funds rate at 5.25%. This policy has proven effective in keeping the economy moving ahead while controlling inflationary pressures. While the Fed left the fed funds rate unchanged, the U.S. bond market was active. The benchmark 10-year Treasury Note ranged from 4.50% to 5.26% during the first half of the year, a spread of over 60 basis points. The upward interest rate movement helped to normalize the yield curve where longer-term bonds pay more than shorter-term notes.

While the Fed chose to keep short-term rates unchanged, the bond market pushed intermediate and long-term interest rates higher. These dynamics created an opportunity to selectively purchase higher yielding fixed income instruments that included U.S. government agency bonds and preferred stock. While we view the upward yield movement in longer-term bonds as healthy, we continue to focus our fixed income strategy in shorter-term maturities of between 4 to 7 years. This shorter duration aims to protect invested capital while improving yields. We expect day-to-day volatility in the bond market to persist. Using the 10-year Treasury Note as a benchmark, we see the market establishing a new trading range going forward. In the past few months, yields have ranged from 4.60% to 5.25%. We now expect to see interest rates for the 10-year Treasury Note trading between 4.25% and 5.00% through the end of the year.

Looking Ahead

Overall, we maintain an optimistic outlook for the economy. The global economy remains strong and appears to be in a long-term growth pattern led by China, India and other developing countries in Asia and Eastern Europe. Domestically, interest rates are low by historical measures and inflation has been reasonable for this point in the economic cycle. As economic growth continues at a moderate pace, we expect to experience market volatility in reaction to fluctuations in economic indicators from time to time. Longer-term, however, we believe the economy can continue to expand and will reward a patient, longer-term investment strategy.

Near-term, the equity and bond markets continue to be challenging. Several catalysts could spark a directional change in the markets at any time. While the credit and liquidity problems are primarily impacting the fixed-income markets they have also affected the equity markets. Investors are concerned that the lack of liquidity may slow economic growth to a point where a recession might develop. It may take some time for the fixed income markets to stabilize. However, we believe that investors, financial institutions and the Fed can manage through these problems and return the fixed-income markets to a more balanced risk-reward credit environment. Longer-term this corrective period in the equity and fixed income markets should provide a more stable foundation for future growth.

At Pacific Advisors Fund, we seek to maintain disciplined, long-term investment strategies. Even though we are longer-term investors, we adapt to changing market and economic conditions. During periods of a market correction, we often find attractive investment opportunities that we believe will benefit the Funds in the future. While many investors regard volatility as a negative development, we believe it can be an important tool in implementing our buy and sell strategies. In the following interviews with our portfolio managers we discuss the investment strategies for each Fund in more detail.

Sincerely,

George A. Henning

2

Pacific Advisors

Government Securities Fund

Seeks to provide high current income, preservation of capital, and rising future income, consistent with prudent investment risk. Invests at least 80% of its assets in U.S. Government fixed income securities and may invest in other income-producing instruments including dividend paying common stocks, for income and capital appreciation.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||

| For the six months ended June 30, 2007 | For the fiscal year ended 12/31/06 | ||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||

| Class A | 2.45 | % | 3.17 | % | 2.51 | % | |||||||||

| Class C | 2.09 | % | 3.86 | % | 3.21 | % | |||||||||

For the six months ended June 30, 2007, the Fund's benchmark, the Lehman Intermediate Treasury Bond Index,1 rose 1.53%.

Figures shown are past performance and do not guarantee future results. Current performance may be higher or lower than the performance data quoted. For performance current to the most recent month-end call (800) 989-6693. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares and would be lower if the sales charge were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Expense ratios shown are for the Fund's most recent fiscal year ended December 31, 2006. The Fund's investment adviser is waiving a portion of its management fees. Results shown reflect the waiver, without which the results would have been lower. Expense ratios shown reflect the waiver, without which they would have been higher. Please see the Financial Highlights contained in this report for more details.

Interview with Portfolio Manager

Thomas H. Hanson

What factors contributed to rising interest rates during the first half of 2007?

Global and domestic economic expansion coupled with modest inflation propelled intermediate and long-term interest rates upward in 2007. Global economic growth continued at a robust pace in the first half of 2007. Rapid economic expansion increased competition for goods and services resulting in rising prices. Foreign central banks raised interest rates in an attempt to contain inflationary pressures and moderate economic growth to more sustainable levels.

The U.S. economy grew at a more moderate rate with rising energy costs, a cooling housing market, and problems in the sub-prime lending market keeping economic momentum in check. The Fed kept a close eye on inflationary pressures, but held short-term rates at 5.25% throughout the first half of the year. At the same time, however, the Fed quietly supported economic expansion by placing additional money into circulation to increase market liquidity. High levels of liquidity in the global and domestic marketplaces increased demand for bonds which also helped push rates higher.

How did rising interest rates impact the bond market?

The rise in rates brought a long anticipated return to a more normalized interest rate environment with longer-term bonds carrying higher rates than shorter-term bonds. Nevertheless, the bond market remained

1 The Lehman Intermediate Treasury Bond Index is an unmanaged index of intermediate term government bonds since 12/31/80.

3

volatile during the period as rates rose unevenly within a trading range. The benchmark 10-year Treasury Note traded between 4.50% and 5.26% during the first six months of the year.

Shorter-term securities typically experience less price volatility in response to interest rate changes. Therefore, longer-term bonds carried greater investment risk as interest rates ticked up in the first half of the year. Shorter-term bonds remained more attractive for their relative stability causing price depreciation in longer-term bonds.

The bond market was also significantly impacted by a notable decline in demand for U.S. treasuries by foreign investors. Foreign investors sought higher yielding fixed-income securities to combat the effects of inflation brought on by strong to moderate growth in their own economies. As a result of interest rate increases by foreign central banks, U.S. treasuries offered less attractive rates than their global counterparts. Prices declined on U.S. treasuries in order to remain competitive with foreign alternatives which also helped push rates higher. This competitive market drove the benchmark 10-Year Treasury Note to breakthrough its 13-year ceiling of 5.25% at the end of the second quarter.

The Fund outperformed its benchmark during the first six months of the year. How did the Fund successfully navigate the rising interest rate environment?

The Fund seeks total return by managing for income and capital appreciation. This investment approach gives the Fund the flexibility to actively manage risk in the bond market. Rising interest rates in the first half of the year continued to require a more defensive strategy to protect capital.

The Fund remained concentrated in intermediate-term bonds maintaining an average maturity in the portfolio of 5 to 6 years. Modest adjustments were made to the portfolio as interest rates ticked up, but the Fund did not make any broad strategic changes as evidenced by a low annualized turnover rate of 13% through June 30th. This strategy allowed the Fund to achieve a good total return for the period without exposing the portfolio to significant interest rate risk.

Over 80% of the Fund's portfolio remained invested in U.S. government agency issues. Government agency securities continued to offer higher coupon rates than U.S. treasuries which allowed the Fund to increase income without materially increasing the risk to the portfolio. The Fund captured additional yield by purchasing government agency bonds with callable features which offered attractive coupon rates. As these bonds were subsequently called away, capital was reinvested in intermediate-term (4 to 7 years) bonds to take advantage of rising interest rates.

The Fund also modestly increased its preferred stock holdings from 5% to 7% with well-known companies such as AT&T. These positions helped provide some protection against inflation through additional yield and capital appreciation potential. In addition, preferred stock provided liquidity which leaves the Fund positioned to take advantage of emerging opportunities in the bond market.

Should investors be concerned by the current rise in interest rates?

Interest rate movements are directly tied to the health of the domestic and global markets. Rising rates reflect sustained periods of economic expansion or rejuvenation. Interest rate increases, whether caused by central banks or market dynamics, often help to moderate unsustainably high economic growth rates and keep inflation in check.

Strong, but manageable, global economic growth is the main cause of the current rise in interest rates. While rates have risen in the U.S. and abroad, they have remained in a relatively low range by historical standards. Rising rates that stay within a healthy range, and are not driven by hyperinflation, represent a normal and healthy phase in the economic cycle.

4

What factors will impact interest rates and the Fund's investment strategy in the remainder of the year?

Domestic and global inflation will continue to have the greatest impact on interest rates in the last half of the year. Rising costs for energy, basic commodities and labor may continue to stoke inflationary pressures. Interest rates would also be impacted by any geopolitical events that disrupt international trade or cause price spikes, in oil for example.

While we do not believe interest rates will increase substantially worldwide, we will continue to monitor economic growth patterns. In particular, we are focused on assessing any policy changes made by central banks around the world. China, India and Eastern Europe continue to fuel the growth momentum in the global markets and any significant changes in their economies would impact fixed income markets worldwide.

In the U.S., concerns over the fallout in the sub-prime market will continue to impact the fixed income market for the near-term. In the normal course of the economic cycle, it is not unusual to experience some fallout in certain segments of the economy. While we cannot predict a specific timetable, we believe the credit markets will recover from current setbacks. Despite these setbacks, the U.S. economy remains well positioned to continue its moderate rate of growth.

In light of the problems in the bond market, it is uncertain whether the Fed will continue to hold short-term rates at their current level or consider reducing them to stabilize the credit markets. However, we believe sustained global economic growth and the high level of liquidity in the market will continue to produce a rise in intermediate and long-term rates. Given the continued uncertainty surrounding a variety of economic factors, we expect interest rates will continue to rise within a trading range.

In the last half of the year, the Fund will seek to evaluate long-term interest rates to identify the top of the new trading range and assess its likely duration. When it becomes clearer that interest rates are peaking, we will move into longer-term bonds to lock in higher coupons and capital appreciation potential. Until then, the Fund will maintain its defensive strategy to manage risk and preserve capital to achieve long-term growth.

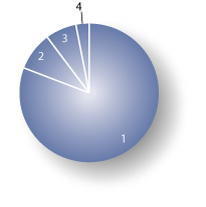

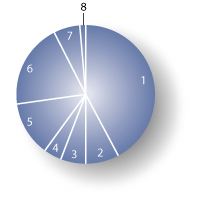

Portfolio Holdings as of 06/30/07 (Based on Total Investments)

| 1. | U.S. Government Agencies | 81.07 | % | ||||||||

| 2. | Equities | 8.89 | % | ||||||||

| 3. | Preferred Stock | 7.06 | % | ||||||||

| 4. | Cash and Cash Equivalents | 2.98 | % | ||||||||

5

Pacific Advisors

Government Securities Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2007 through June 30, 2007.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 1/1/2007 | Ending Account Value 6/30/2007 | Expense Paid During Period 01/01/07 – 06/30/07 | |||||||||||||

| Government Sec Class A | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,024.50 | $ | 8.93 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 8.94 | |||||||||

| Government Sec Class C | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,020.90 | $ | 12.68 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 12.70 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio of 1.78% for Class A shares and 2.53% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

6

Pacific Advisors

Income and Equity Fund

Seeks to provide current income and, secondarily, long-term capital appreciation. Invests primarily in investment grade fixed income securities and dividend paying stocks.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||

| For the six months ended June 30, 2007 | For the fiscal year ended 12/31/06 | ||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||

| Class A | 2.25 | % | 2.80 | % | 2.06 | % | |||||||||

| Class C | 1.94 | % | 3.56 | % | 2.81 | % | |||||||||

For the six months ended June 30, 2007, the Fund's benchmarks, the Lehman Intermediate Corporate Bond Index1 and the S&P 5002 Index, rose 1.27% and 6.96%, respectively.

Figures shown are past performance and do not guarantee future results. Current performance may be higher or lower than the performance data quoted. For performance current to the most recent month-end call (800) 989-6693. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares and would be lower if the sales charge were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Expense ratios shown are for the Fund's most recent fiscal year ended December 31, 2006. The Fund's investment adviser is waiving a portion of its management fees. Results shown reflect the waiver, without which the results would have been lower. Expense ratios shown reflect the waiver, without which they would have been higher. Please see the Financial Highlights contained in this report for more details.

Interview with Portfolio Manager

Thomas H. Hanson

How did the corporate bond market fare in the first half of 2007?

Economic conditions continued to create a challenging corporate bond market in the first half of the year. The Federal Reserve left short-term interest rates unchanged at 5.25%, citing stubborn inflationary pressures as the main threat to future economic growth. Nevertheless, intermediate and long-term rates ticked up in the U.S. and throughout the global marketplace. Despite this rise in interest rates, attractive corporate bond offerings remained scarce.

Many businesses remained flush with cash from growth in recent years and had little need to issue bonds to fund company growth. Ample cash reserves also allowed firms to refinance their existing debt obligations to improve their balance sheets and insulate their earnings from rising interest rates. With many companies choosing to forgo issuing new debt or refinancing existing debt, high-quality investment grade bonds remained in limited supply.

Global privatization added to the challenge of finding suitable corporate bond investments. Hedge funds, private equity firms and individual companies took a number of firms into the private sector. These acquisitions reduced investment opportunities in the bond market creating greater demand for an already dwindling supply of high-quality corporate bonds.

It is important to note that recent problems in the sub-prime lending market have had little impact on the Fund's fixed income strategy. The Fund is designed for more conservative investors. As we have discussed, the Fund seeks conservative investments in high-quality, investment grade bonds as opposed to the higher risk derivative type products.

1 The Lehman Intermediate Corporate Bond Index is an unmanaged index of intermediate term U.S. corporate bonds since 01/01/73.

2 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and The Nasdaq Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses.

7

Pacific Advisors

Income and Equity Fund continued

How did the Fund manage this challenging environment?

In the first half of the year, the Fund continued to maintain a larger portion of its holdings in U.S. government agency securities which offered attractive yields with a limited amount of risk. Corporate bonds typically pay higher interest rates which generally makes them more attractive than government agencies. Over the past year, however, the limited supply of corporate bonds has created a narrow difference (or 'spread') between interest rates on corporate bonds and government agencies making government agencies equally attractive investments.

In addition, the Fund maintained a greater portion of its portfolio in preferred stocks from high-quality companies such as AT&T and Deutsche Bank. Preferred stocks can be an attractive substitute for bonds because they pay a fixed dividend which provides a stable stream of income. Increasing its preferred stock holdings has allowed the Fund to maintain liquidity while providing the opportunity for capital appreciation and improved total return.

Additionally, the Fund allocated a small percentage of its portfolio to floating rate corporate bonds that are indexed to the Consumer Price Index (CPI). This tie to the widely-used inflation index provides some protection against risk from inflationary pressures.

Despite the overall trend toward higher rates, intermediate and long-term rates remained relatively volatile in the first six months of the year. The Fund continued to maintain an average maturity of 4 to 5 years in its bond portfolio to manage interest rate risk and protect capital. We will maintain this more defensive position until rates reach a definitive peak.

How did the Fund manage its investment allocation mix during the first six months of the year?

The Fund seeks to produce total return through income and capital appreciation. Managing risk and reward in both the fixed income and equity markets is a critical component of the Fund's total return strategy. By actively managing its asset allocation mix, the Fund seeks to capitalize on opportunities in the stronger performing areas of the markets while limiting exposure to risk in underperforming areas of the markets.

Throughout the first half of the year, the Fund maintained approximately 65% of its portfolio in fixed income securities and 35% in equities. Maintaining a higher allocation in equities enabled the Fund to benefit from continued strength in the equity markets in 2007. This added to the Fund's total return and helped offset more challenging conditions in the corporate bond market.

The Fund continued to concentrate its equity investments in dividend-paying stocks from large, well-established companies. This included consumer product companies such as Procter & Gamble and Home Depot; energy and basic materials firms such as British Petroleum and DuPont; and healthcare companies such as Pfizer and Johnson & Johnson. Concentrating in high-quality investments provides the opportunity for additional income and capital appreciation without significantly increasing volatility in the portfolio.

Why did the Fund reduce its holdings in the utilities sector?

Utility stocks are often viewed proxies for bonds because they typically pay high dividends and carry relatively low risk. In the past, the Fund has held substantial positions in utility stocks because of their ability to meet the conservative investor's need for stability and consistent income. However, the volatility and risk associated with these stocks can increase dramatically when interest rates rise. Utilities are capital intensive businesses which typically fund expenditures by issuing debt. This debt becomes more expensive as interest rates rise.

For the last 18 months, the utilities sector has been one of the strongest performing sectors in the economy given the low cost of borrowing. The Fund benefited from steady dividends, rising stock prices and limited risk by investing in utility stocks during this time. As interest rates rose in the first half of 2007, there was a growing potential for utility stocks to under-perform as the cost of issuing debt rose. The Fund trimmed its utilities holdings to limit this risk.

8

What is the expected trend in interest rates for the remainder of the year and how will this impact the Fund?

Interest rates are expected to remain somewhat volatile while continuing to push modestly higher through the end of the year. While rising interest rates are a normal and healthy part of the economic cycle, investment strategy is critical to protecting capital in this environment. The Fund will continue to manage for total return by seeking risk-appropriate opportunities for income and capital appreciation.

At this time, we expect to maintain the Fund's investment allocation mix in approximately 70% fixed income securities and 30% in high-quality equities. Until interest rates reach a clear peak, we will remain more defensive by keeping the portfolio's average maturity in a range of 4 to 6 years.

We expect the interest rate spread between corporate and government bonds will return to more historical norm once the markets move beyond the current liquidity crunch induced by fallout in the sub-prime lending market. However, given the strength of the U.S. and global economies and corporate balance sheets, high-quality corporate bonds will likely remain in relatively short supply. Therefore, we anticipate that the Fund will continue to seek additional total return opportunities in high-quality preferred stocks and government agency issues.

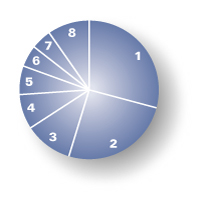

Portfolio Holdings as of 06/30/07 (Based on Total Investments)

| 1. | Corporate Bonds | 42.31 | % | ||||||||

| Equities | 30.63 | % | |||||||||

| 2. | Financials | 7.63 | % | ||||||||

| 3. | Energy | 5.98 | % | ||||||||

| 4. | Health Care | 4.27 | % | ||||||||

| 5. | Other Equities | 12.75 | % | ||||||||

| 6. | U.S. Government Agencies | 19.72 | % | ||||||||

| 7. | Preferred Stock | 6.17 | % | ||||||||

| 8. | Cash and Cash Equivalents | 1.17 | % | ||||||||

9

Pacific Advisors

Income and Equity Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2007 through June 30, 2007.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 1/1/2007 | Ending Account Value 6/30/2007 | Expense Paid During Period 01/01/07 – 06/30/07 | |||||||||||||

| Income Class A | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,022.50 | $ | 9.78 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 9.79 | |||||||||

| Income Class C | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,019.40 | $ | 13.52 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 13.56 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio of 1.95% for Class A shares and 2.70% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

10

Pacific Advisors

Balanced Fund

Seeks to achieve long-term capital appreciation and income consistent with reduced risk. Invests primarily in large and medium cap common stocks with at least 25% of its assets invested in fixed income securities and preferred stocks.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||

| For the six months ended June 30, 2007 | For the fiscal year ended 12/31/06 | ||||||||||

| Class A | 7.11 | % | 2.54 | % | |||||||

| Class C | 6.70 | % | 3.30 | % | |||||||

For the six months ended June 30, 2007, the Fund's benchmarks, the Lehman Intermediate Corporate Bond Index1 and the S&P 500 Index2, rose 1.27% and 6.96%, respectively.

Figures shown are past performance and do not guarantee future results. Current performance may be higher or lower than the performance data quoted. For performance current to the most recent month-end call (800) 989-6693. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares and would be lower if the sales charge were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. Expense ratios shown are for the Fund's most recent fiscal year ended December 31, 2006. Please see the Financial Highlights contained in this report for more details.

Interview with Portfolio Managers

Thomas H. Hanson

George A. Henning

Samuel C. Coquillard

Effective January 1, 2007, Mr. Hanson serves as lead portfolio manager for the Fund and Mr. Henning and Mr. Coquillard serve as portfolio managers with respect to the equity securities portion of the Fund.

What was the Fund's equity investment strategy in the first part of the year?

The equity markets have continued to offer better performance relative to the fixed income market in 2007. Therefore, the Fund maintained approximately 60% of its portfolio in equities and 40% in fixed income securities. Only minor adjustments were made to this mix to increase the potential for total return and position the Fund for long-term growth in response to changing market conditions. These strategies enabled the Fund to produce a solid total return and outperform its benchmarks in the first six months of the year.

The Fund's equity strategy focused on enhancing diversification to reduce volatility in the portfolio. We realized gains and selectively trimmed the Fund's energy exposure by pruning longer-term positions including Devon Energy, SunCor Energy and British Petroleum. This capital was used to increase the Fund's exposure to other sectors such as consumer staples and financials through positions in well-established, dividend-paying companies.

For example, the Fund took a new position in Procter & Gamble, a household name in personal care products. Procter & Gamble's stock was trading at a depressed price as a result of its recent acquisition of Gillette. This provided the Fund with an opportunity to invest in a well-established company with a good dividend rate at a discounted price. With the integration of Gillette largely complete, Procter & Gamble is on track to produce stronger earnings and revenue growth.

The Fund also enhanced diversification by selectively increasing its holdings in existing positions such as Chubb, which provides property and casualty insurance coverage to businesses and individuals. The company has achieved strong revenue and earnings growth over the last 5 years. Compelling long-term growth prospects, coupled with a respectable dividend rate, led the Fund to increase its position in the company.

1 The Lehman Intermediate Corporate Bond Index is an unmanaged index of intermediate term U.S. corporate bonds since 01/01/73.

2 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and The Nasdaq Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses.

11

Pacific Advisors

Balanced Fund continued

What changes were made in the Fund's fixed income investments in 2007?

The corporate bond market remained challenging in the first half of the year. Interest rate risk remained a concern in light of an overall rise in intermediate and long-term rates. In addition, high-quality, investment grade bonds continued to remain in short supply. Many corporations still possessed ample cash reserves giving them little need to issue debt while rising interest rates provided an incentive for companies to reduce existing debt.

Given the limited availability of investment-grade corporate bonds, the Fund maintained approximately 9% of its portfolio in U.S. government agency bonds. Government agency bonds are issued by agencies affiliated with the U.S. government and generally pay higher interest rates than U.S. Treasury securities. Government agency securities provided an attractive alternative to corporate bonds for their ability to offer competitive yields without increasing risk to the Fund.

The Fund's fixed income strategy also included adding select preferred stock holdings in well-known companies such as AT&T, ING Group and American International Group. Preferred stock, while typically considered an equity, acts like a bond by paying a fixed dividend rate. Recently, preferred stock issues have carried higher yields than many corporate bonds. This created an opportunity for the Fund to increase income and capital appreciation potential without exposing the portfolio to greater volatility.

The recent fallout in the sub-prime market has had little impact on the Fund's investment strategy. The Fund is designed for more conservative investors. As we have discussed, the Fund concentrates its fixed income investment in high-quality, investment grade securities as opposed to higher risk, derivative products.

How has global economic growth impacted the Fund's investment strategy?

The fluid exchange of goods, services and information between countries connects the world's economies like never before. As a result, long-term global trends can have a significant impact on U.S. companies with international exposure. In the first half of 2007, global economic growth topped 5% and this extraordinary pace is likely to continue as consumer and commercial demand increases around the world.

Much of this growth is tied to investment in commercial building and infrastructure which has dramatically increased the demand for basic materials such as concrete, steel, copper, and iron. The Fund benefited from global growth in this area through well-established multi-national companies including Rio Tinto, a copper and iron ore producer; Reliance Steel & Aluminum, a steel and metals processor; and Ingersoll-Rand, which makes construction equipment.

The Fund has also benefited from increased global demand for energy resources and energy-related services through positions in companies such as ConocoPhillips and British Petroleum. Growing energy consumption also translates into long-term growth across a variety of energy-related fields such as transportation, industrials and equipment. Holdings in companies such as GATX and Grant PrideCo have provided an opportunity for the Fund to capitalize on worldwide expansion in these areas.

How has the Balanced Fund capitalized on growth in the U.S. economy?

Many of the global trends discussed above are also driving U.S. economic growth. The Fund participated in the rising demand for energy in the U.S. through domestic natural gas firms Williams Companies and Spectra Energy Corporation. Furthermore, holdings in industrial equipment and services companies such as Cameron International and Ingersoll-Rand allowed the Fund to benefit from domestic infrastructure-related growth.

The Fund also maintained a focus on select areas of consumer spending. One such area is multi-media corporations which have benefited from the increased dependence on instant access to information, whether in the form of wireless data transmission, broadcast television, radio communications or internet resources. Holdings such as Time Warner; Walt Disney; CBS; and General Electric, with its subsidiary of

12

NBC Universal, provided exposure to several of the major U.S. entities which create and distribute news, information and entertainment. Maintaining positions in the media sector enables the Fund to capitalize on the technological advancements in the marketplace without taking on the higher risk associated with investments in technology, hardware and software manufacturers, or internet service providers.

Where do you see investment opportunities for the Fund going in the last half of 2007?

The global economy is expected to continue its strong rate of growth for the foreseeable future. The long-term outlook for the U.S. economy also remains positive, although growth is expected to continue at a more moderate rate. The Fund will continue to weight its portfolio toward equities with a focus on companies poised to benefit from this dual economic growth.

We expect that the energy sector will continue to lead the market and will continue to represent a significant portion of the Fund's equity holdings. At the same time, we also anticipate adding a limited number of new positions in areas such as healthcare equipment, industrials and basic materials for added diversification. The Fund will seek select opportunities in these areas through undervalued, dividend-paying, large cap companies with strong growth prospects.

We do not anticipate a significant change in the corporate bond market before the end of the year. The Fund will continue to remain defensively positioned in its fixed income holdings to manage ongoing risk and volatility in this area of the market. When it becomes clear that interest rates have reached a peak, the Fund will look to take advantage of opportunities to enhance long-term growth by locking in higher yields and capital appreciation potential.

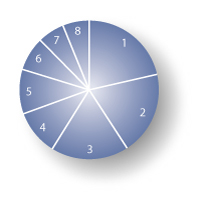

Portfolio Holdings as of 06/30/07 (Based on Total Investments)

| Equities | 62.39 | % | |||||||||

| 1. | Financials | 13.42 | % | ||||||||

| 2. | Energy | 12.84 | % | ||||||||

| 3. | Industrials | 9.92 | % | ||||||||

| 4. | Health Care | 6.26 | % | ||||||||

| 5. | Information Technology | 5.35 | % | ||||||||

| 6. | Materials | 4.92 | % | ||||||||

| 7. | Other Equities | 9.68 | % | ||||||||

| 8. | Corporate Bonds | 27.75 | % | ||||||||

| 9. | U.S. Government Agencies | 8.66 | % | ||||||||

| 10. | Preferred Stock | 1.14 | % | ||||||||

| 11. | Cash and Cash Equivalents | 0.06 | % | ||||||||

13

Pacific Advisors

Balanced Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2007 through June 30, 2007.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within six months of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within six months of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 1/1/2007 | Ending Account Value 6/30/2007 | Expense Paid During Period 01/01/07 – 06/30/07 | |||||||||||||

| Balanced Fund Class A | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,071.10 | $ | 11.71 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 11.45 | |||||||||

| Balanced Fund Class C | |||||||||||||||

| Actual | $ | 1,000 | $ | 1,067.00 | $ | 15.58 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000 | $ | 1,024.79 | $ | 15.26 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio of 2.28% for Class A shares and 3.04% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

14

Pacific Advisors

Growth Fund

Seeks to achieve long-term capital appreciation. Invests primarily in medium to large capitalization companies whose stocks are a part of the S&P 500 Index1 or the Nasdaq 100 Index2.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||

| For the six months ended June 30, 2007 | For the fiscal year ended 12/31/06 | ||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||

| Class A | 11.83 | % | 3.68 | % | 2.64 | % | |||||||||

| Class C | 11.41 | % | 4.44 | % | 3.40 | % | |||||||||

For the six months ended June 30, 2007, the Fund's benchmarks, the S&P 500 and the Russell 10003, rose 6.96% and 7.18%, respectively.

Figures shown are past performance and do not guarantee future results. Current performance may be higher or lower than the performance data quoted. For performance current to the most recent month-end call (800) 989-6693. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares and would be lower if the sales charge were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Expense ratios shown are for the Fund's most recent fiscal year ended December 31, 2006. The Fund's investment adviser is waiving a portion of its management fees. Results shown reflect the waiver, without which the results would have been lower. Expense ratios shown reflect the waiver, without which they would have been higher. Please see the Financial Highlights contained in this report for more details.

Interview with Portfolio Manager

Thomas H. Hanson

What economic trends influenced the Fund's investment strategy in the first half of 2007?

The first half of the year brought a continuation of the longer-term trends which have been developing in the global and domestic economies over the past year. The most influential trends included strong global economic growth; rising interest rates coupled with moderate inflation; and continued demand and competition for oil, energy, and other commodities. Continuing the investment strategy implemented in 2006, the Fund remained concentrated in those sectors and stocks positioned to benefit from these trends.

Throughout the first half of the year, the Fund remained oriented toward the energy, healthcare, industrials, and basic materials sectors. Investments in these sectors remained relatively stable throughout the period resulting in little turnover. While there were no pronounced sector rotations or shifts, minor adjustments were made in the portfolio to rebalance positions to reduce risk and achieve desired sector weightings.

Energy and energy related holdings such as ConocoPhillips and Apache Corp. performed well for the Fund as did industrial holdings such as Commercial Metals. The major demographic shift in the U.S. toward an aging population continued to make healthcare investments attractive, particularly in the healthcare equipment and services industries. Companies such as Zimmer Holdings, which specializes in hip and joint replacements, and St. Jude Medical, which produces replacement heart valves, continued to perform well for the Fund. Portfolio holdings also focused on other select sectors such as information technology which benefited from the rapid growth in the U.S. and Asian telecommunications markets.

1 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and The Nasdaq Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses.

2 The Nasdaq 100 Stock Index is an unmanaged, market capitalization weighted measure of the 100 largest non-financial domestic and international common stocks listed on The Nasdaq Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect management fees or expenses.

3 The Russell 1000 Stock Index is an unmanaged, market capitalization weighted measure of stock market performance. It contains the stocks of the 1,000 largest publicly traded companies within the Russell 3000 Index. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of capital gains, management fees, or expenses.

15

Pacific Advisors

Growth Fund continued

How does the Fund manage sector-specific risks?

The Fund takes a more conservative top-down investment approach that focuses on investments in the leading market sectors. We do not buy stocks based solely on share price momentum or price per earnings. Rather, we look for companies in those sectors with strong fundamentals and competitive advantages that offer solid growth potential at a reasonable price. The stock selection process takes into consideration the impact of longer-term economic trends and company-specific events.

Over the past year, the Fund has maintained a larger exposure to the industrials and basic materials sectors. Companies in the industrial and basic materials sectors – such as iron, copper, aluminum, and steel firms – provide the building blocks for economic growth and are the primary beneficiaries of global and domestic investments in infrastructure. In particular, these companies are expected to benefit from billions of dollars in future spending as a result of the emerging domestic trend to reinvest in infrastructure improvements on aging roads, sewer systems, and bridges.

Industrials and basic materials are examples of fast-paced sectors where sudden price shifts are commonplace. While the Fund avoids areas marked by speculative or short-term growth, some short-term volatility may be acceptable in exchange for the benefits offered by long-term growth potential. The Fund has strategically participated in the industrials and basic materials sectors through well-run companies, such as Chicago Bridge and Iron, which is positioned to participate in this multi-year growth cycle.

How has the Fund managed risk in light of slower economic growth in the U.S. economy?

The U.S. economy continued to grow at a more moderate rate in the first half of the year. As typical in a moderately growing economy, this period was marked by heightened market volatility in response to uneven economic data. The Fund actively managed this risk through diversification and strategic cash management.

The Fund's portfolio is diversified across various sectors to provide a counterbalance to the impact of sudden shifts in market or economic conditions. This includes maintaining positions in more defensive industries such as healthcare and consumer staples with holdings such as Johnson & Johnson and Chattem. The Fund also manages volatility through stock selection by focusing on companies with strong fundamentals that offer stable growth.

The Fund is unique in its use of cash to offset market volatility. Cash reserves tend to range between 5% and 10% of the Fund's portfolio. Cash levels may be temporarily increased as a hedge against volatility during periods of elevated market risk. As market volatility moderates, the Fund redeploys cash reserves into emerging opportunities. The Fund maintained approximately 9% of its portfolio in cash throughout the first six months of the year in light of continued market volatility.

How does a company's size factor into the Fund's stock selection?

The Fund focuses on large cap companies and complements these holdings with modest positions in mid and small cap companies within key sectors. This diversification strategy contributes to the Fund's total return by providing measured exposure to all market capitalizations. While maintaining its large cap orientation, the Fund looks for growth opportunities in mid and small cap stocks which shadow or mimic large cap companies.

For example, in the energy sector, large cap holdings such as Apache are supplemented by positions such as Carbo Ceramics, a smaller energy services company. In the healthcare sector, the Fund has invested in select mid cap companies that offer same growth potential and competitive advantages as many large caps such Quest Diagnostics, one of only two major medical lab testing companies in the U.S.

In addition, the Fund may utilize select small cap stocks to participate in growth within specialized industries. In the information technology sector, the Fund has benefited from its position in ITron, a small cap utility services provider. ITron provides wireless receivers that read water, electric, and gas meters from long distances which enables utilities to increase their productivity and shorten billing cycles.

16

How does a low portfolio turnover rate support the Fund's investment strategy?

Many growth funds shift sector allocations rapidly to follow market momentum which typically results in a high portfolio turnover rate. High portfolio turnover typically results in increased trading costs and tax consequences for a fund. While the Fund adapts to fundamental changes in market leadership, it does not chase short-term performance. As stated earlier, the Fund takes a long-term investment approach that seeks to invest in sectors and companies with sustainable, multi-year growth patterns. The Fund's more conservative growth-at-a-reasonable-price strategy enables it to seek above-average performance and manage risk. Unique from other g rowth funds, Fund has been able to achieve its investment objectives while maintaining a relatively low turnover rate.4

Where do you anticipate the best growth opportunities will be in the remainder of 2007?

We do not foresee a significant change in the global or domestic economic trends during the last half of the year. The U.S. economy is on track to achieve a moderate and sustainable growth rate for the year in the range of 21/2% to 3%. Strong balance sheets also leave corporate America well positioned for continued growth in the second half of 2007. As growth continues at a moderate pace, we expect to experience continued volatility in the market as economic indicators fluctuate from time to time.

The Fund will remain focused on sectors and stocks that offer long-term growth at a reasonable price. The energy, energy-related, and industrials sectors should continue to lead the market due to unprecedented global demand for oil and basic materials. We will continue to monitor the economic environment for changes in market leadership and new growth opportunities.

Portfolio Holdings as of 06/30/07 (Based on Total Investments)

| Equities | 90.40 | % | |||||||||

| 1. | Energy | 29.32 | % | ||||||||

| 2. | Health Care | 25.66 | % | ||||||||

| 3. | Industrials | 10.86 | % | ||||||||

| 4. | Information Technology | 8.32 | % | ||||||||

| 5. | Materials | 6.67 | % | ||||||||

| 6. | Other Equities | 4.96 | % | ||||||||

| 7. | Financials | 4.61 | % | ||||||||

| 8. | Cash and Cash Equivalents | 9.60 | % | ||||||||

4 The Fund had an annualized turnover ratio of 16.44% for the six months ended June 30, 2007; 22.80% for the year ended December 31, 2006; 30.54% for the year ended December 31, 2005; 12.96% for the year ended December 31, 2004; and 34.58% for the year ended December 31, 2003.

17

Pacific Advisors

Growth Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2007 through June 30, 2007.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within six months of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.