UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2009 |

| ||||||

Item 1. Report to Shareholders

Filed herewith.

semi-annual report

june 30, 2009

government securities fund

income and equity fund

balanced fund

growth fund

multi-cap value fund

small cap fund

Pacific Advisors

table of contents

| Message from the Chairman | 1 | ||||||

| Government Securities Fund | 5 | ||||||

| Income and Equity Fund | 9 | ||||||

| Balanced Fund | 14 | ||||||

| Growth Fund | 19 | ||||||

| Multi-Cap Value Fund | 23 | ||||||

| Small Cap Fund | 28 | ||||||

| Statement of Investments | 34 | ||||||

| Statement of Assets and Liabilities | 58 | ||||||

| Statement of Operations | 60 | ||||||

| Statement of Changes in Net Assets | 62 | ||||||

| Notes to Financial Statements | 66 | ||||||

| Financial Highlights | 75 | ||||||

| Directors and Officers | 82 | ||||||

This Report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current effective prospectus of the Fund, which contains information concerning the investment policies of the Fund as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation, or a recommendation that any particular investor should purchase or sell any particular security. The statements in the Report are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change with market conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders,

This year, investors have been on an emotional roller coaster. The continuing credit crisis weighed on the markets during the first quarter. Uncertainty about the government's response to the economic and financial crises caused a "buyers strike" in the equity market. As a result, the equity markets dropped to significant lows in early March. The Dow Jones Industrial Average fell to 6,440 while the S&P 500 Index declined to 666, marking a loss of over 26% for each index since the beginning of the year. Fears of a "great depression" led many investors to "give up" on equities and sell into the market downturn.

The market downturn in the first quarter was the result of a lack of information rather than a significant change in economic conditions. While the credit markets were showing improvement, investors worried that conditions would deteriorate if governments and central banks failed to provide enough support through intervention. While the major market indices reached major lows in the first quarter, these numbers did not reflect the results of all market participants. Indeed, many companies did not return to the lows experienced last Fall. Trading volumes were also lower suggesting that many investors had moved to the sidelines. However, these statistics did little to give investors confidence in an eventual market rebound.

As governments around the world enacted economic stimulus programs and several banks pre- annnounced first quarter earnings, investors saw signs of encouragement. As they began to ease back into the equity markets, they were surprised when many companies beat earnings estimates. Opportunistic investors uncovered undervalued companies which, in some cases, had declined to levels anticipating bankruptcy. The strong market rally that followed caught the more cautious investors by surprise.

The equity markets posted impressive gains during the second quarter. While several factors contributed to the strong performance, the most prevalent was the growing sense that the global recession had begun to ease. As investors moved beyond fear, the "buyer's strike" that had crippled securities markets gave way to strategic investing. As confidence grew in response to early signs of economic recovery, investors were once again willing to accept risk.

The Funds' equity strategies, which focus on investments in high quality companies with experienced management teams; strong balance sheets; and solid growth prospects; trading at favorable valuations, were rewarded. While the strong rally might suggest that the market recovery is complete, the market remains well off of its October 2007 high. More significantly, stocks in strong companies are still trading at significantly depressed valuations. Such companies offer opportunities for long-term investors.

Market & Economic Review

The market rebound that began in March continued impressively through May. Investors were initially encouraged in mid-March when the Federal Reserve, Treasury, and FDIC announced programs to inject much-needed liquidity into the frozen credit markets. This unprecedented intervention sent a strong message that the government would take the steps necessary to stabilize the financial sector and the economy.

Additionally, packages implemented by foreign governments and central banks were important catalysts to reignite the global economy. In particular, China approved a massive package that will produce GDP growth of over 7% in 2009. This growth initiative triggered a recovery in basic materials which provided a foundation for global economic recovery.

The markets rallied in earnest at the end of March after Fed Chairman Ben Bernanke characterized the economy as exhibiting "green shoots" of recovery. This comment, followed by positive earnings pre-announcements by major banks and better-than-expected first quarter earnings, set in motion a wave of enthusiastic buying. The markets moved solidly higher in April and May as investors saw that stronger companies were surviving the downturn. These companies benefited from disciplined fiscal management,

Market Review

| June 30, 2009 | Close | YTD Return | |||||||||

| Dow Jones | 8,447.00 | -3.8 | % | ||||||||

| S&P 500 | 919.32 | 3.2 | % | ||||||||

| NASDAQ | 1,835.04 | 16.4 | % | ||||||||

| Russell 2000 (small cap) | 508.28 | 2.6 | % | ||||||||

| 06/30/09 | 06/30/08 | ||||||||||

| 10-Year T-Note Yield | 3.53 | % | 3.99 | % | |||||||

Data: The Wall Street Journal; Standard & Poor's; Russell Investments

1

Message

from the chairman continued

flexible business models and improved productivity which allowed them to implement cost controls to manage to new economic realities.

With the notable exception of unemployment, most official statistics pointed to a slower pace of economic contraction. Yet, while certain sectors of the economy showed signs of strength, others continued to lag. The market's bullish trend eased in June as investors turned their attention to second quarter earnings for better clarity on the direction of the economy. Nevertheless, the S&P 500 and other major indices ended the second quarter in positive territory for the year.

The market resumed its upward march in July as companies across a variety of sectors issued positive second quarter earnings reports. In another encouraging sign, companies began to report an uptick in business from the depressed levels in the first half of 2009. Through the end of July, the S&P 500 had gained a remarkable 48% from its March low.

Recovery Taking Shape

Growing evidence suggests that an economic recovery is under way, albeit at a slower pace than past recoveries. Positive signs include stabilization in the financial services sector; improved access to capital; low business inventories which will need replenishing; better-than-expected corporate earnings; a modest drop in unemployment claims; increases in home prices and sales; an increase in auto sales; and growing demand for commodities such as steel and coal.

A robust economic recovery, as seen after past recessions, is unlikely given the severity of the recession and credit crisis. The high cost of government spending and the projected deficits will likely result in higher federal and state taxes. These headwinds will probably continue for some time resulting in slow to moderate economic growth.

This economic environment creates opportunities for stronger businesses to strengthen their market positions and grow their franchises. This is accomplished as tighter industry economics force weaker competitors out of the market; distressed valuations create acquisition and consolidation opportunities; and companies with strong balance sheets opportunistically invest in new assets, new products, and new relationships. We believe these dynamics will result in a significant divergence between the strong and marginal performers in each industry.

Slower growth may have a dampening effect on the equity indices for the foreseeable future. Rather than a general recovery in which "a rising tide raises all boats," we expect that this recovery will reward the stronger companies. Therefore, individual stock selection will be an important factor in investment performance.

The benefits of the Funds' focused equity strategies are especially evident in this environment. Our focus on a relatively small number of companies enables us to closely monitor each holding to identify unusual market conditions and investment opportunities. As a result, market volatility can provide opportunities for timely investment decisions. The Funds' long-term horizon provides opportunities to realize significant returns as the market recovers.

Equity Investment Review

While broad-based, the market rally between March and May was driven by companies expected to benefit in the early stages of recovery. Many of these firms were in the Basic Materials, Technology, Consumer Discretionary, Industrial, and Energy sectors. Companies reacted to the economic slowdown by reassessing business operations, controlling costs and managing inventory levels. As a result, strong competitors have successfully weathered substantial revenue declines and reported better-than-expected earnings.

The rebound in the equity Funds during the quarter was the result of timely investment decisions as well as the strong market rally. While the market recovered from its March lows, many portfolio holdings significantly outperformed the overall market. The best performers included companies that we expected to benefit in the early recovery stage as well as companies that were industry leaders through the downturn.

The Funds' investment strategies continue to focus on holdings in stocks that traditionally perform well during slow economic periods; those that will benefit from the early stages of recovery as well as stocks which stand to benefit from economic stimulus programs. In addition to these themes which address the current

2

economic climate, we continue to target traditional value opportunities and special situations consistent with our core investment strategies. Given the extreme pressures of the credit crisis and the likelihood of a slow economic recovery, the growth opportunities for the best companies may occur as their weaker competitors lack the resources or capital necessary to recover.

We believe the portfolios are well-positioned to benefit from the developing economic recovery, with strong positions in Industrials, Energy, and Materials. A significant component of the Industrials sector is transportation stocks. Historically, transportation is generally a market leader in an economic recovery. We anticipate that trend will develop at slower pace to the benefit of the stronger companies. Many of the weaker companies have avoided bankruptcy or liquidation as creditors have been slow to repossess equipment in a weak market hoping an economic recovery will enable these companies to survive. This appears to be an unlikely scenario which may shrink supply and provide potentially strong growth in revenues to the surviving companies.

As economic recovery develops, we will increasingly focus on early recovery names, including Energy companies. Crude oil prices, while often volatile, are expected to move higher. As economies recover, the global appetite for energy will continue to grow. Investments in exploration and natural resource production will be rewarded. Additionally, we look to commodities, including energy products; copper; and steel, to provide a hedge against inflation. While oil prices fell to near $30 per barrel earlier this year, oil prices have recently moved higher to near $70 per barrel. We believe that, as economic conditions improve and supplies fall, higher oil prices are inevitable. Much of the world's oil supplies are in remote areas that require oil prices above $70 to $90 per barrel to be economicall y viable.

While many of the Financials stocks are beginning to rebound, we believe their primary focus for the remainder of this year will be to improve their balance sheets by raising capital, increasing deposits and writing off or selling problem loan portfolios. As stronger banks improve their balance sheets, they may seek opportunities for acquisitions or mergers with problem banks shut down by the FDIC. The larger banks are benefitting from their diversification through corporate debt financing and other investment banking business. During the recent quarter, several banks have been able to repay their government financing under TARP1 with new capital or earnings from improved business conditions.

Many of the companies in the portfolios are well positioned to experience strong growth even in a slower economy. They have aggressively cut costs, pared inventory and maintained strong balance sheets to initiate growth strategies. We believe these measures will enable them to leverage any improvement in business into more robust earnings. As economic conditions improve, we believe the upside potential for well managed companies is substantial.

Fixed Income Investment Review

The fixed income markets improved substantially over the six-month period. As access to the credit markets eased and investor appetite for risk increased, many companies responded with debt offerings. Recent downgrades of many corporate issues to lower investment grade levels have increased the interest rates on many new offerings.

Interest rates on government securities also trended higher during the period. At the height of the market panic in the first quarter, the rates on short-term Treasury Bills fell to zero, and even below zero. During the second quarter, the rate on the benchmark 10-year Treasury Note rose approximately 0.75% in response to the surging government debt. The interest rates demanded by investors to finance the stimulus spending have, so far, increased modestly. Much of the funding has been provided by foreign investors who currently hold approximately 55% of all U.S. Treasuries. The massive amounts of stimulus spending, however, are expected to test investor appetite for government bonds.

We expect interest rates to rise further as investors will demand higher returns on government bonds. As U.S. government bonds are a safe haven for many investors, we anticipate the stock market recovery will attract a significant amount of capital that has been invested in government bonds as a temporary investment vehicle. Any significant increase in rates will impact the economic recovery as interest rates for loans and mortgages will increase and inflationary pressures may reappear.

1 Troubled Asset Relief Program.

3

Message

from the chairman continued

Near-term, interest rates and the fixed income markets will remain volatile as economic recovery develops. As a result, the Funds' fixed income holdings remain concentrated in short to intermediate-term issues. We will continue to maintain this defensive strategy to protect capital while seeking reasonable income opportunities.

Looking Ahead

While uncertainties remain, we believe the market recovery is sustainable. We anticipate that the market will continue to "take two steps forward and one step back" in response to mixed economic data. Therefore, we expect performance will come from industry leaders rather than the overall market. Individual companies may post stellar returns as they successfully navigate a difficult economy. Our strategy will remain focused on these companies where we believe the best portfolio opportunities exist.

The past year has been particularly difficult. Investors feared that it would take years for their portfolios to recover from the global credit crisis and deep recession. We have encouraged investors to be patient and disciplined in maintaining their investment strategies. While the recovery is ongoing, the dramatic events during the first six months of the year demonstrate the ability of the equity markets to rapidly improve from their lows in a short period of time. We anticipate the global markets and global economies will continue to improve. We also recognize the importance of being diligent and will continue to adapt to changing market conditions consistent with the Funds' long-term investment strategies.

Sincerely,

George A. Henning

This report is for informational purposes only and is not a solicitation, or a recommendation that any investor should purchase or sell any particular security. Statements are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. Opinions are subject to change and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

4

Pacific Advisors

Government Securities Fund

Seeks to provide high current income, preservation of capital, and rising future income, consistent with prudent investment risk. Invests at least 80% of its assets in U.S. Government fixed income securities and may invest in other income-producing instruments including dividend paying common stocks, for income and capital appreciation.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2009 | For the fiscal year ended December 31, 2008 | ||||||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||||||

| Class A | 0.33 | % | Class A | 3.11 | % | 1.65 | % | ||||||||||||

| Class C | – 0.03 | % | Class C | 3.89 | % | 2.43 | % | ||||||||||||

| Barclays Capital U.S. Int T-Bond Index1 | – 1.52 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actua l returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's Board of Directors, but is expected to continue at current levels. Please see the Fund's most recent Annual Report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager

Thomas H. Hanson

Market Overview

Deteriorating economic conditions and continued fallout from the credit crisis put severe pressure on the markets at the beginning of the year. Industrial production, consumer spending and economic output continued to decline, while unemployment continued to rise. In addition, creditors remained reluctant to lend in light of ongoing instability in the economy and the financial sector. Seeking safety and liquidity, investors sold equities and other investments and flocked to U.S. government securities, especially short-term Treasuries. Strong demand pushed prices higher while Treasury rates dropped to historically low levels.

Throughout the first quarter, the U.S. government, Treasury and Federal Reserve continued to take dramatic steps to stimulate economic growth; ease credit conditions; and stabilize the financial sector. The Fed kept its target range for the federal funds rate at zero to 0.25% and stated that "economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period." In mid-March, the Fed announced plans to buy up to $300 billion in longer-term Treasuries to reduce the government's borrowing costs and stimulate lending by financial institutions. The Fed also expanded its efforts to support the housing markets; accommodate the credit needs of consumers and small businesses; and foster improved conditions in financial markets.

Late in the first quarter, the government's various efforts began to yield improved credit conditions and prospects for economic recovery. In turn, investor sentiment began to shift from acute pessimism to guarded optimism. This sparked a rally in the equity markets which continued in the second quarter. While

1 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity.

5

Pacific Advisors

Government Securities Fund continued

investors began to cautiously move back into equities and corporate bonds, demand for government securities remained relatively strong through the end of the second quarter.

Interest Rate Trends

During the first six months, Treasury rates were volatile in response to competing market forces. Broad economic weakness, aggressive government intervention, and increased investor demand put downward pressure on Treasury rates. Demand was particularly strong in the first quarter as investors fled the equity and fixed income markets for the safety of U.S. Treasuries. The desire to protect capital was so great that investors were willing to accept flat or negative rates on short-term Treasuries.

In mid-March, the tide began to turn when Fed Chairman Ben Bernanke characterized the economy as exhibiting "green shoots" of recovery. A number of factors subsequently pushed Treasury rates higher. Mounting data foreshadowing economic recovery; the threat of inflation; record-breaking Treasury auctions; and burgeoning federal deficits to fund stimulus initiatives put upward pressure on rates throughout the second quarter. Reflecting the diverging trends during the period, the rate on benchmark 10-year Treasury Note traded between a low of 2.12% in January and a high of 3.94% in June.

Fixed Income Strategy

We actively manage the portfolio with a conservative strategy designed to protect principal and provide current income. During the period, the Fund was primarily invested in intermediate-term government agencies. This strategy helped minimize the risk of depreciation in a rising interest rate environment. Additionally, intermediate-term bonds provided higher current income relative to short-term government securities.

In the first quarter, higher yielding bonds were limited due to the high demand for government securities. In order to maximize current income, the Fund primarily invested in continuously callable intermediate-term government agencies which offered higher coupon rates. Given the low interest rate environment, we anticipated that these bonds would be called back, providing the Fund with opportunities to purchase higher yielding bonds. As expected, many of these bonds were called during the period and proceeds were reinvested in intermediate-term government agencies with higher coupons.

As interest rates rose in second quarter, our strategy continued to emphasize preservation of capital to protect against market risk. As existing holdings were called away, we focused on purchasing government agencies with features to preserve principle. These purchases included bonds with coupon rates that gradually increase over the life of the bond. Furthermore, we purchased more government agencies with fixed call features. These bonds provided greater flexibility in managing the portfolio because, in comparison to continuously callable bonds, they are easier to sell in a rising interest rate environment. The Fund benefited from this strategy by preserving capital and enhancing income levels.

Equity Positioning

A relatively small portion of the portfolio is invested in high quality dividend paying common and preferred stocks to help provide a hedge against inflation and support total return. These investments provide additional current income and potential capital appreciation. During the period, the Fund maintained 4% to 5% of the portfolio in dividend paying common stocks and 4% to 5% in preferred stocks.

The severe market downturn in the first part of the year pushed equity valuations to extreme lows. We maintained the Fund' equity holdings as our internal research confirmed the underlying value and income potential of these well established companies. As anticipated, valuations for these holdings began to recover as the equity markets rebounded in the second quarter. In particular, the Fund benefited from a strong recovery in its preferred stock positions. For example, collectively, preferred stock in financial companies recovered 28% during the period in addition to providing strong dividend yield.

Despite the price recovery in the second quarter, we believe many of these holdings remain undervalued. The Fund's equity positions should see continued improvement as the economy recovers. We

6

believe the income and capital appreciation potential of these holdings will continue to contribute to the Fund's long-term total return objectives.

Fund Performance

As a conservative investment, the Fund seeks to preserve capital and provide current income. Risk management was paramount during the period given the volatile investment environment and trend toward rising interest rates. The Fund outperformed its benchmark during the period, which, unlike the Fund, is not actively managed to protect against risk. By actively managing the portfolio and concentrating holding in intermediate-term government agencies, we successfully managed risk while generating attractive income. Recovery in the Fund's preferred stock positions also contributed to the Fund's outperformance.

Looking Ahead

The significant stimulus initiatives by the government and the Fed have yielded an improving economic outlook. Recent data have confirmed a slowing in the pace of contraction while certain sectors of the economy are even demonstrating renewed strength. Likewise, the credit markets continue to improve in response to positive economic data and stabilization in the financial sector.

As economic recovery develops, investors will likely continue to gravitate from Treasuries toward other fixed income investments offering higher rates and greater appreciation potential. In response to this trend, rates on Treasuries and government agencies are expected to rise in order to remain competitive with other fixed income investments. Furthermore, concerns surrounding the burgeoning federal deficit and the strength of the U.S. dollar may also push rates higher.

At the same time, competing pressures may create continued interest rate volatility. While recovery is on the horizon, significant economic challenges remain including higher unemployment; continued weakness in the housing sector; moderate consumer spending; and higher mortgage and credit card default rates. For conservative investors, Treasuries may continue to provide attractive options. This popularity, if sufficiently widespread, may limit the upward pressure on interest rates. As the largest foreign holder of U.S. Treasuries, China's investment decisions may also influence the direction of Treasury rates.

In this environment, we will continue to implement a strategy focused on managing risk and protecting principal. The Fund will remain concentrated in short and intermediate-term government agencies many of which include call features. While we do not anticipate a significant change in the Fund's equity allocation, we will continue to utilize high quality dividend paying common and preferred stocks to increase income and capital appreciation potential. We will continue to actively manage the Fund's fixed income holdings in accordance with the market conditions to capture the most favorable return potential with the least vulnerability to the prevailing market risks.

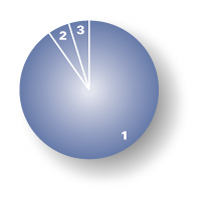

Portfolio Holdings as of 06/30/09 (Based on Total Investments)

| 1. | U.S. Government Agencies | 90.36 | % | ||||||||

| 2. | Preferred Stock | 5.10 | % | ||||||||

| 3. | Equities | 4.54 | % | ||||||||

7

Pacific Advisors

Government Securities Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2009 through June 30, 2009.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/09 | Ending Account Value 06/30/09 | Expense Paid During Period 01/01/09 – 06/30/09 | |||||||||||||

| Government Securities Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,003.30 | $ | 9.83 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 9.94 | |||||||||

| Government Securities Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 999.70 | $ | 13.54 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 13.71 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio of 1.98% for Class A shares and 2.73% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

8

Pacific Advisors

Income and Equity Fund

Seeks to provide current income and, secondarily, long-term capital appreciation. Invests primarily in investment grade fixed income securities and dividend paying stocks.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2009 | For the fiscal year ended December 31, 2008 | ||||||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||||||

| Class A | 4.94 | % | Class A | 2.80 | % | 2.05 | % | ||||||||||||

| Class C | 4.58 | % | Class C | 3.56 | % | 2.81 | % | ||||||||||||

| Barclays Capital U.S. Int Corp Bond Index1 | 9.04 | % | |||||||||||||||||

| S&P 500 Index2 | 3.16 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actua l returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's Board of Directors, but is expected to continue at current levels. Please see the Fund's most recent Annual Report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager

Thomas H. Hanson

Market Overview

The markets began 2009 mired in the crippling credit crisis. While short-term U.S. Treasuries and government agencies enjoyed unprecedented popularity, the corporate bond market was effectively closed. Lack of corporate finance opportunities impacted both businesses and consumers and placed enormous stress on the global economy. Investor sentiment swayed from one extreme to the other, causing tremendous volatility in both the fixed income and equity markets. In response, a series of forceful actions by the Treasury, Federal Reserve, and FDIC breathed life back into the credit markets and ignited a strong market rebound at the end of the first quarter.

Investor confidence improved in response to better-than-expected first quarter earnings and economic data which indicated a slowing in the pace of contraction. The market recovery extended through the second quarter benefiting all asset classes, including equities, fixed income, and commodities. Equities in particular staged an impressive comeback and seemed poised to extend their run.

1 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity.

2 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and The NASDAQ Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses.

9

Pacific Advisors

Income and Equity Fund continued

Corporate Bond Market

At the turn of the year, opportunities in the corporate bond market were in especially short supply. Limited access to debt financing and higher financing costs resulted in significantly fewer corporate issuances. Investment opportunities were further limited when rating agencies issued mass downgrades of corporate debt in a belated reaction to their role in the credit crisis and the weak economy. The corporate bond market was also challenged as investors fled to the safety of U.S. Treasuries and government agencies.

Volatility played a major role in portfolio management during the first half of 2009. Corporate bond prices fluctuated in response to fragile investor confidence and deteriorating economic conditions. However, in the midst of this challenging environment, unique opportunities arose. The ratings downgrades, coupled with a lack of investor demand, drove yields among investment grade bonds to abnormally high levels. In comparison to rates for Treasuries, corporate bonds were trading at attractive levels. We believed that the market was temporarily mispricing the risk of these issues. As a result, these bonds presented valuable investment opportunities.

In mid-February, credit conditions began to improve in response to various government initiatives. As investors gained confidence, they returned to the corporate bond market; as a result, yields on investment grade corporate debt began to fall. A wave of corporate refinancing activity ensued as companies took advantage of renewed investor demand and historically low interest rates. The impressive yields found earlier in the year were no longer available as prices for corporate bonds rose in response to heightened demand. Stabilization in the credit markets allowed portfolio managers to refocus on more traditional factors in fixed income analysis: interest rates and inflation.

Equity Market

The selloff in the equity market continued well into the first quarter of 2009. Stocks languished as the economic outlook remained clouded and investors questioned the administration's ability to handle the worst economic crisis in a generation. Bearish sentiment peaked in mid-March, as the S&P 500 Index fell to a 13-year low. Markets began to turn following the government's various initiatives aimed at recapitalizing banks and supporting critical credit markets.

The strong upward move in equities continued into the second quarter following better-than-expected first quarter earnings reports. A growing list of economic reports suggesting the recession was beginning to ease further contributed to the bullish mood. The strong momentum pushed equities into positive territory for the year. By the end of the second quarter, investors turned their focus to earnings results for clarity on the direction of the economy and the markets. Reports that many companies successfully weathered the economic decline with better-than-expected earnings confirmed to many investors that a sustainable market recovery is underway.

Fund Performance

The Fund performed well in the first half of the year given the extreme volatility in the fixed income and equity markets. While the Fund outperformed the overall market as measured by the S&P 500, performance was limited as a result of the Fund's conservative investment strategy. In particular, performance was impacted by the Fund's allocation to shorter-term bonds to protect principal as well as the continued impact of the credit market disruption on portfolio holdings in the Financials sector. We believe that the valuations of these holdings will continue to improve as the economic recovery develops.

Fund Strategy

The Fund seeks to provide current income and capital appreciation while maintaining a lower risk profile. Fixed income securities (corporate bonds and preferred stocks) typically make up at least 65% of the portfolio and provide a stable income base. The remainder of the portfolio is invested in high quality dividend paying stocks which contribute to current income and offer long-term capital appreciation potential.

10

The Fund's allocation to fixed income securities, at approximately 75%, was essentially unchanged during the first half of 2009. The mix of securities, however, changed when most of the Fund's U.S. government agency bonds were called or matured. At the beginning of the year, these agency bonds, which paid relatively high interest rates, represented almost 10% of the portfolio. With the proceeds, we expanded the Fund's portfolio of investment grade corporate bonds with new holdings in the Consumer Discretionary, Energy, Materials, Industrials and Technology sectors.

Preferred stocks represented approximately 7% of the portfolio while equity holdings varied during the period between 21% and 25%. The relatively modest allocation to equities was a direct reflection of the market upheaval. During periods of volatility and low valuations, the Fund will favor fixed income investing to mitigate the impact of price fluctuations.

Fixed Income Strategy

The first six months of the year presented two dramatically different investment environments. Suitable corporate bond investments were severely limited in the first part of the year. Corporations looking to issue debt faced higher financing costs in the wake of widespread ratings downgrades. Demand was also light as nervous investors avoided risk in favor of U.S. Treasuries. Nevertheless, we took advantage of select opportunities to purchase bonds of quality issuers such as Alcoa, Xerox and Staples. Reflecting the difficult environment, these investment grade bonds offered yields in excess of 7%, compared to 10-year Treasury rates of less than 3%.

As the credit markets stabilized in the second quarter and investor appetite for risk returned, many companies responded with debt offerings. Interest rates fluctuated within a fairly narrow range as investors weighed the pros and cons of an improving global economic outlook. The massive fiscal deficits taken on to combat the downturn also raised concerns about the threat of inflation and higher interest rates.

To minimize the potential impact of rising interest rates, the Fund focused new purchases in shorter-term bonds, primarily with maturities of two to five years. At the same time, we remain mindful that the pace of economic recovery is uncertain. Accordingly, we continued to hold the Fund's existing longer-term bonds to maintain current income.

Equity Strategy

We continued to maintain a focused but diversified portfolio with an emphasis on stocks that exhibit low volatility relative to the broader market. The Fund maintained a reduced equity exposure during the period to limit the impact of the equity downturn on the portfolio. As market conditions improved in the second quarter, we sold several positions in defensive stocks, including health care companies GlaxoSmithKline and Pfizer. The Fund's energy holdings, led by XTO Energy and Ultra Petroleum, performed well during the period.

The Fund continued to hold select securities despite lagging performance in the first quarter. For example, we maintained the Fund's position in Frontier Communications. The company owns and operates regional telecommunications lines and recently purchased assets from Verizon. Despite its recent difficulty, we believe that Frontier's experienced management team; strong dividend; and strong cash flows will positively impact performance.

Looking Ahead

Interest rates are likely to remain volatile as the economy recovers. Rates will be impacted by competing factors, such as the record supply of U.S. Treasuries to finance the stimulus programs and support the credit markets; the strong demand for government bonds; the emerging economic recovery; and the potential onset of inflation. As global economic conditions improve, however, interest rates are likely to begin a longer-term upward trend. Economic "green shoots" suggest the pace of global recession is easing. Although, given the severity of the recession and credit crisis, economic improvement is expected to progress at a slower rate than in recent recoveries.

11

Pacific Advisors

Income and Equity Fund continued

In this investment environment, the Fund's strategy will focus on actively managing the portfolio to minimize interest rate risk. We will seek to reduce the effect of higher rates by investing in shorter-term corporate bonds. These investment grade bonds will help minimize the impact of price volatility while limiting losses associated with changes in interest rates.

As the economy recovers, equities are poised to deliver favorable returns. Our equity strategy seeks to supplement the Fund's larger bond allocation by providing current income with the potential for capital appreciation. As fixed income securities mature, are called, or sold, we anticipate increasing the Fund's equity investments to approximately 30%. We expect to invest in sectors that should benefit from the developing recovery such as Technology, Energy, Materials and Consumer Discretionary. We will maintain our disciplined focus of selecting stocks with stable dividends and below average market volatility.

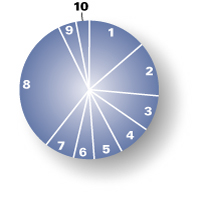

Portfolio Holdings as of 06/30/09 (Based on Total Investments)

| 1. | Corporate Bonds | 64.58 | % | ||||||||

| Equities | 21.64 | % | |||||||||

| 2. | Energy | 5.04 | % | ||||||||

| 3. | Health Care | 3.13 | % | ||||||||

| 4. | Telecommunication Services | 2.74 | % | ||||||||

| 5. | Industrials | 2.48 | % | ||||||||

| 6. | Utilities | 2.02 | % | ||||||||

| 7. | Consumer Staples | 1.99 | % | ||||||||

| 8. | Other Equities | 4.24 | % | ||||||||

| 9. | Preferred Stock | 7.35 | % | ||||||||

| 10. | Cash and Cash Equivalents | 4.95 | % | ||||||||

| 11. | U.S. Government Agencies | 1.48 | % | ||||||||

12

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2009 through June 30, 2009.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 60 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange aft er the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/09 | Ending Account Value 06/30/09 | Expense Paid During Period 01/01/09 – 06/30/09 | |||||||||||||

| Income & Equity Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,049.40 | $ | 12.45 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 12.30 | |||||||||

| Income & Equity Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,045.80 | $ | 16.23 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 16.07 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio of 2.45% for Class A shares and 3.20% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

13

Pacific Advisors

Balanced Fund

Seeks to achieve long-term capital appreciation and income consistent with reduced risk. Invests primarily in large and medium cap common stocks with at least 25% of its assets invested in fixed income securities and preferred stocks.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||

| For the six months ended June 30, 2009 | For the fiscal year ended December 31, 2008 | ||||||||||||||

| Class A | 4.11 | % | Class A | 2.31 | % | ||||||||||

| Class C | 3.68 | % | Class C | 3.09 | % | ||||||||||

| S&P 500 Index1 | 3.16 | % | |||||||||||||

| Barclays Capital U.S. Int Corp Bond Index2 | 9.04 | % | |||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actua l returns when shares are sold.

Discussion with Portfolio Managers

Thomas H. Hanson

George A. Henning

Samuel C. Coquillard

Market Overview

The equity and fixed income markets started 2009 mired in uncertainty. Fear surged on questions surrounding the extent of the global economic contraction, U.S. economic stimulus plans, and the stumbling credit markets. As investors sought safety in short-term U.S. Treasuries, stock valuations fell to levels not seen since 1996.

As signs of economic recovery emerged late in the first quarter, investor sentiment transitioned from extreme pessimism to cautious optimism. Government stimulus programs began to provide some relief to the financial, consumer and housing sectors. Capital injections by the Federal Reserve and foreign central banks improved liquidity in the credit markets. Additionally, first quarter earnings revealed that many companies were weathering the recession better than expected. An uptick in merger and acquisition activity and a rise in corporate bond offerings provided further evidence that corporate America was beginning to regain its footing. As investor confidence improved, capital moved back into the markets.

Equity Market

Stock prices tumbled in the first quarter on excessive fear as investors sold without regard for the actual strength of individual companies. While market volatility presented a major challenge, this environment also provided unique opportunities to invest in good companies at unprecedentedly low

1 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York Stock Exchange, American Stock Exchange and The NASDAQ Stock Market. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses.

2 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity.

14

prices. During the quarter, the Fed used every tool at its disposal to restore confidence in the financial sector, stimulate the languishing economy, and expand liquidity in the credit markets. Additionally, the U.S. Treasury implemented various stimulus initiatives and the administration provided greater detail on its economic recovery plans. These actions helped ignite a market rally late in the first quarter.

As concrete evidence of economic improvement mounted, investors began to revisit their risk assumptions. Domestically, most economic data pointed to a slowing rate of contraction. Internationally, China led the way by pouring massive amounts of capital into its economy to stimulate growth. Projects aimed at infrastructure building, industrial production and manufacturing put China on course for economic growth of 7% to 8% this year. Following China's lead, other countries injected more capital into their economies which improved the outlook for global economic recovery.

First quarter earnings further buoyed investor sentiment and strengthened the market recovery. Many companies demonstrated that they were effectively weathering the slowdown. Furthermore, stronger firms used the downturn to strategically position for future growth by streamlining operations, cutting costs, and expanding market share. Stock prices experienced a significant rebound in the second quarter as evidenced by the S&P 500 Index which recovered nearly 42% from its March low by June 30th.

Corporate Bond Market

The corporate bond market remained challenging in the first half of 2009. Fallout from the credit crisis continued to curtail new corporate bond issues. Additionally, bond investors found few opportunities to buy or sell as bonds in the secondary market were in short supply. Investors primarily chose safety over income. Short-term U.S. Treasuries were in high demand even though they offered zero or sometimes slightly negative returns.

In response to actions by the Fed and other government agencies, liquidity started to improve late in the first quarter. New corporate bond offerings subsequently increased during the second quarter. Additionally, firms took advantage of lower interest rates to refinance higher coupon, longer-term debt. Investors gradually began to reassess their appetite for risk as they gained confidence in the sustainability of the recovery. As interest rates ticked upward, capital began to move out of short-term Treasuries into other fixed income investments.

Fund Performance

The Fund outperformed the S&P 500 through the first half of the year. By maintaining a disciplined investment approach through the market downturn, the Fund was well positioned to benefit from the ensuing recovery. Performance was primarily supported by appreciation in the Fund's Energy and Basic Materials equity holdings. Higher yields on investment grade corporate paper and appreciation in the Fund's preferred stock holdings also supported total return. The Fund achieved this outperformance while maintaining lower risk and volatility than the S&P 500 as measured by the Fund's beta3 of 0.79 as of June 30th.

Fund Strategy

The Fund's equity and fixed income holdings are actively managed to seek capital appreciation while managing risk. In 2009, we maintained approximately 61% of the portfolio in equities which continued to offer the best opportunities for long-term growth. As corporate bonds matured, proceeds were reallocated into select equities. Equity and fixed income holdings remained diversified across sectors and industries to further manage risk.

3 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower volatility than the market or the benchmark; and a beta greater than 1.0 indicates greater volatility than the market or the benchmark.

15

Pacific Advisors

Balanced Fund continued

Equity Strategy

The Fund is designed to serve as a core holding and therefore uses a more conservative equity strategy. The Fund seeks to provide long-term growth while limiting risk and volatility. To this end, equities remained concentrated in dividend paying stocks from well established, larger cap companies.

The Fund continued to invest in fundamentally strong companies from a diverse mix of sectors and industries. Greater weight was given to holdings in stronger performing sectors such as Energy, Basic Materials, Information Technology and Health Care. Renewed demand for energy and other natural resources pushed energy and commodity prices higher during period. The Fund's Energy holdings performed especially well in the first half of the year. In particular, companies in energy related areas such as equipment and refining experienced good growth. This included Fund holdings Cameron International, which manufactures offshore oil and natural gas equipment; and Suncor Energy, a multinational oil producer and refiner. Cameron benefited from increased demand for offshore drilling in Brazil while Suncor benefited from the rise in oil prices during the second quarter.

Holdings in the Basic Materials sector also supported the Fund's investment objectives. This included, Reliance Steel & Aluminum, which is the largest distributor of metal products in the U.S. Reliance experienced price appreciation as global and domestic infrastructure projects increased demand for its products.

Fixed Income Strategy

The Fund's fixed income strategy seeks to achieve total return while mitigating risk. Given the risk for higher interest rates in 2009, to the Fund remained invested in short to intermediate-term investment grade corporate bonds. New purchases were concentrated in bonds with two to four-year maturities to protect against depreciation. Additionally, investment grade corporate bonds offered better yields than U.S. Treasuries or government agencies. This provided additional income to the Fund without significantly increasing risk.

The Fund also benefited from a recovery in its financial holdings. Specifically, preferred stock of financial firms saw marked price appreciation. Additionally, General Electric Capital bonds rebounded significantly as the market recovery took hold in the second quarter. At the same time, we further diversified the portfolio by investing new monies in bonds from well known Consumer Discretionary firms such as Staples and Ho me Depot.

Looking Ahead

While challenges to recovery remain, recent reports suggest that the worst of the recession may be over. Indeed, select sectors are showing signs of renewed growth. In particular, stimulus initiatives in the U.S., China and other countries should support demand in the Energy, Basic Materials and Industrials sectors. Investor confidence will continue to be a determining factor of market momentum. While the market will remain more volatile, continued economic improvement should create additional opportunities in the equity and fixed income markets.

We expect to modestly increase the Fund's equity allocation to approximately 65% to seek additional opportunities for capital appreciation. There will be opportunities for stronger, well positioned companies to grow their businesses, even in a slow-growth economy. Near-term, the Fund's equity portfolio will remain positioned to take advantage of sectors and companies benefiting from economic recovery.

Fixed income holdings will be managed to protect capital in anticipation of rising interest rates. We do not anticipate making any significant changes to the Fund's fixed income portfolio in the next six months. We will continue to manage the portfolio to maximize total return while limiting risk. Accordingly, the portfolio will remain primarily invested in short to intermediate-term, investment grade corporate bonds to manage volatility.

16

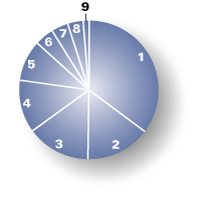

Portfolio Holdings as of 06/30/09 (Based on Total Investments)

| Equities | 60.73 | % | |||||||||

| 1. | Energy | 13.78 | % | ||||||||

| 2. | Industrials | 12.82 | % | ||||||||

| 3. | Consumer Staples | 8.18 | % | ||||||||

| 4. | Financials | 7.54 | % | ||||||||

| 5. | Health Care | 6.58 | % | ||||||||

| 6. | Information Technology | 4.92 | % | ||||||||

| 7. | Other Equities | 6.91 | % | ||||||||

| 8. | Corporate Bonds | 32.08 | % | ||||||||

| 9. | Preferred Stock | 4.40 | % | ||||||||

| 10. | Cash and Cash Equivalents | 2.79 | % | ||||||||

17

Pacific Advisors

Balanced Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2009 through June 30, 2009.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within six months of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within six months of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments, and (d) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/09 | Ending Account Value 06/30/09 | Expense Paid During Period 01/01/09 – 06/30/09 | |||||||||||||

| Balanced Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,041.10 | $ | 13.26 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 13.15 | |||||||||

| Balanced Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,036.80 | $ | 17.02 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,024.79 | $ | 16.92 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio of 2.62% for Class A shares and 3.37% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

18

Pacific Advisors

Growth Fund

Seeks to achieve long-term capital appreciation. Invests primarily in medium to large capitalization companies whose stocks are a part of the S&P 500 Index1 or the NASDAQ 100 Index2.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2009 | For the fiscal year ended December 31, 2008 | ||||||||||||||||||

| Expense Ratio | Net Expense Ratio | ||||||||||||||||||

| Class A | 5.07 | % | Class A | 3.65 | % | 2.62 | % | ||||||||||||

| Class C | 4.52 | % | Class C | 4.42 | % | 3.40 | % | ||||||||||||

| S&P 500 Index | 3.16 | % | |||||||||||||||||

| Russell 1000 Index3 | 4.32 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actua l returns when shares are sold.