UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2011 |

| ||||||

Item 1. | Report to Shareholders |

| Filed herewith. |

semi-annual report

june 30, 2011

government securities fund

income and equity fund

balanced fund

large cap value fund

mid cap value fund

small cap value fund

Pacific Advisors

table of contents

| Message from the Chairman | 1 | ||||||

| Government Securities Fund | 4 | ||||||

| Income and Equity Fund | 8 | ||||||

| Balanced Fund | 12 | ||||||

| Large Cap Value Fund | 16 | ||||||

| Mid Cap Value Fund | 20 | ||||||

| Small Cap Value Fund | 24 | ||||||

| Statement of Investments | 30 | ||||||

| Statement of Assets and Liabilities | 52 | ||||||

| Statement of Operations | 54 | ||||||

| Statement of Changes in Net Assets | 56 | ||||||

| Financial Highlights | 60 | ||||||

| Notes to Financial Statements | 67 | ||||||

| Directors and Officers | 76 | ||||||

This Report is submitted for the general information of the shareholders of Pacific Advisors Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by the Funds' copy of the prospectus, which contains information concerning the investment policies of the Funds as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation, or the Funds' recommendation that any particular investor should purchase or sell any particular security. The statements in the Chairman's Letter and the discussions of the Funds' performance are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change at any time based on market or other conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders,

Investor sentiment in the first half of the year seemed to be déjà vu all over again. In a repeat of 2010, the year began strongly as earnings results significantly beat market expectations. In May, however, the markets retreated largely in response to the Greek sovereign debt crisis. Investors also remained concerned about the prospects for economic growth and the completion of the Federal Reserve's QE2 stimulus package. Despite these headwinds, the markets rebounded as the first half of the year came to a close.

Disappointing economic data and the escalating European sovereign debt crisis tested investor fortitude. Yet, strong, well-managed companies continued to grow their businesses despite subdued economic growth; these companies were rewarded with higher market valuations. Dominant companies were able to benefit from industry growth, or, in some cases, from industry contraction as well as from geographic expansion; mergers and acquisitions; new product launches and operational improvements. Weaker counterparts were unable to keep pace.

Geopolitical and economic events around the world create a challenging investment environment. The cascade of headline news often paints a confusing picture. Investors must navigate a global economy that is highly interdependent even as individual countries govern their own economies. The resulting uncertainty reinforces the importance of a longer-term investment strategy focused on companies adept at managing in a diverse and ever-changing global economy. We believe the most capable firms are those with experienced management teams, solid financing and strong competitive positioning.

The slow recovery from the 2008 bear market continues to advance with ebbs and flows that are triggered by seemingly contradictory data. The volatility accompanying these events, while unsettling, can provide attractive opportunities to take profits or to buy at significant discounts. The specific investment discussions in the Fund commentaries highlight some of the situations that enabled the Funds to benefit from irrational market behavior.

Market & Economic Review

Markets enjoyed a solid first quarter as strong corporate profits inspired confidence in a global economic recovery. During the second quarter, various unsettling economic issues, sapped investor confidence and prompted a market pullback during the second quarter. These included the deterioration in domestic economic data, ongoing fears of a sovereign debt default in Europe, geopolitical unrest in North Africa, and the threat of a real estate bubble in China. Many investors, wary of taking on additional risk, moved from equities to safe-haven investments such as U.S. Treasuries. Then, at the end of June, the passage of austerity measures in Greece triggered a reversal of these trends and prompted a market rally during the final days of the quarter. In the first six months of 2011, the S&P 500 Index rose 6.02%.

GDP growth softened from 3.1% in the final quarter of 2010 to 0.4% in the first quarter. In the second quarter, GDP growth improved modestly but, at 1.3%, remained sluggish. Unusual factors, including severe weather disruptions in many parts of the country and supply chain constraints in Japan, likely distorted the underlying strength of the economy. At the same time, the economy faced continued challenges from the depressed housing market, rising inflationary pressures and persistently high unemployment. The Fed, in light of these trends, continued its accommodative monetary policy which kept interest rates at historic lows. Nervous investors, nevertheless, fled to the safety of U.S. government securities and investment grade corporate bonds. The increase in demand drove market interest rates lower.

Market Review – June 30, 2011

| Index1 | Close | YTD Return | |||||||||

| Dow Jones Industrial Avg | 12,414.34 | 7.20 | % | ||||||||

| S&P 500 | 1320.64 | 6.02 | % | ||||||||

| NASDAQ | 2773.52 | 4.55 | % | ||||||||

| Russell 2000 (small cap) | 827.43 | 6.21 | % | ||||||||

| 06/30/11 | 06/30/10 | ||||||||||

| 10-Year T-Note Yield | 3.18 | % | 2.97 | % | |||||||

Data: The Wall Street Journal

1 The Dow Jones Industrial Average is an unmanaged, price weighted measure of 30 U.S. stocks selected by the Averages Committee to represent the performance of all U.S. stocks outside the Transportation and Utilities sectors. The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy.The NASDAQ Composite Index is an unmanaged, market capitalization weighted measure of all domestic and international common stocks (currently over 3,000 stocks) listed on The Nasdaq Stock Market. The Russell 2000 Stock Index is an unmanaged, market-weighted measure of the 2,000 smallest publicly traded companies of the Russell 3000 Index. These indices are not available for direct investment. Index returns assume the reinvestment of dividends.

1

Message

from the chairman continued

Against a challenging economic backdrop, leading companies continued to deliver solid performance. Strong companies continued to benefit from diminished competition within their industries. Additionally, growing demand in certain markets provided opportunities for well-positioned firms. These trends reinforce the value of identifying companies with superior management teams. The ability of company management to navigate through challenges, identify opportunities and execute growth strategies is an important component in assessing a stock's appreciation potential.

Equity Investment Review

Performance of large, mid and small cap stocks varied during the first six months of 2011. By the end of June, however, their year-to-date performances were similar. Consistent with recent quarters, companies representing a range of industries contributed to portfolio gains for the Large Cap Value, Mid Cap Value and Small Cap Value Funds. In the first half of 2011, many companies began to shift their focus from cutting costs to implementing growth initiatives. The markets rewarded companies that demonstrated their ability to grow through acquisitions, new products, capital investments, or geographic expansion. The common characteristics among these companies are dominant positions in their markets, strong management teams and the financial resources to take advantage of growth opportunities.

In contrast, the slower pace of U.S. economic growth has taken its toll on weaker companies. In this recovery, they have not experienced the typical rebound in revenue; consequently, they have been unable to make the investments necessary to maintain market share. As a result, many sectors have contracted to a point where demand is exceeding supply.

For example, in the transportation industry, freight costs continue to escalate as carriers have regained pricing power from their customers. For car dealers, the decline in the number of U.S. dealerships has increased profitability in new and used car sales. We believe the slow growth economy will perpetuate this divergence.

Also, we are finding industry-specific opportunities. For example, higher energy prices reflect the increasing costs of finding oil. More supply is coming from offshore and remote locations which creates significant opportunities for specialized energy service companies. For investors, these examples are particularly important; investment performance will likely depend more on the quality of the individual portfolio holdings rather than on overall market performance.

Emerging countries remain the primary drivers of global economic growth. In addition to China, India and Brazil, as well as other Asian, South American and African nations are growing their economies. While the pace of growth in these countries may slow periodically, the opportunity for long-term growth is nevertheless substantial.

Geopolitical events will continue to play a significant role in the markets and in shaping the global economy. In particular, developments in the ongoing European financial crisis and unrest in the Middle East and North Africa will weigh heavily on the markets. Our investment focus, while not ignoring the relevance of these events, remains on individual companies that are well-positioned to grow despite the marketplace challenges. Many of these companies are still in the early stages of implementing their growth initiatives and, more importantly, of achieving their revenue and earnings growth potential.

Fixed Income Investment Review

Interest rate volatility continued throughout the first half of the year. Weaker U.S. economic data and international concerns had investors favoring U.S. government securities and high quality corporate bonds over equities for most of the period. The yield on the benchmark 10-year Treasury Note, which traded between 3.74% and 2.88% during the period, ended the second quarter at 3.18%.

Persistent uncertainty and the resulting interest rate volatility reinforce the importance of having active portfolio management. Fixed income holdings in the Funds were concentrated in short to intermediate-term bonds to protect against heightened interest rate volatility. Indeed, the significant spike in rates coinciding with the market rally at the end of June highlights the considerable risk of potential price depreciation on longer-term and higher yielding bonds. During the period, we continued to seek opportunities created by market volatility to purchase high quality bonds with attractive yields at discounted prices.

We expect interest rate volatility will persist as markets respond to uncertainty surrounding economic growth, inflation, and the European sovereign debt crisis. Longer-term, we believe market forces will ultimately drive a

2

Message

from the chairman

sustained rise in interest rates. Until a clear trend in interest rates emerges, however, we believe it is prudent to maintain a strategy of protecting principal by concentrating portfolios in high quality, shorter-term bonds.

Looking Ahead

Second quarter earnings season has seen many companies report strong growth and positive business outlooks. However, whatever optimism may have been generated by their commentaries has been overshadowed by other economic concerns. The debate over raising the U.S. debt ceiling has put more focus on growing budget deficits. And, not unlike a year ago, the slow pace of economic growth has also brought back the debate on a double dip recession.

In June, the Fed lowered its GDP growth expectations and raised its inflation forecast for 2011 and 2012. The slow housing market remains a drag on the economy and the unemployment levels. The reduction of government jobs has put additional pressure on employment conditions. Furthermore, smaller companies have been wary of aggressively hiring during the slow economic recovery; they continue to rely on fewer employees to get the job done. We believe, therefore, that a substantial improvement in employment will take some time.

Since the end of the second quarter, the equity markets have reversed course. Fears of a global recession re-emerged amid concerns about European banks' ability to manage the sovereign debt issues facing the most highly leveraged eurozone economies.

Near-term, the current slow-growth environment will likely persist; however, we do not believe a double dip recession is inevitable. Other factors portend a more positive environment in the second half of the year: a rapid recovery in Japan's manufacturing capacity should significantly contribute to global economic activity; the passage of pending trade pacts with South Korea, Colombia, and Panama would create new markets for American goods; and, business activity should bounce back in U.S. regions that were impacted by severe spring weather. However, we anticipate that the recovery will likely progress in fits and starts; as a result, overall market performance will likely remain unspectacular.

International economic and geopolitical concerns in Europe, the Middle East and Asia are contributing to heightened market volatility. Another significant contributor has been the emergence of High Frequency Trading which reportedly accounts for over 50% of daily trading volumes. These complex, automated computer trading platforms seek to take advantage of price movements. They can drive, and exacerbate, sharp movements in individual stocks or the overall market. Some estimates measure the average holding period for these 'investments' in seconds. The resulting wild market swings are disconcerting. These trading strategies, which do not consider company fundamentals, often distort the relationship between a company's value and its stock price. We believe that the proliferation of these short-term trading strategies will lead to a new norm of heightened volatility. Nevertheless, the Funds' long-term investment strategies can take advantage of this volatility to buy and sell at attractive prices.

We anticipate that companies' continued confidence in improving business conditions will drive increased investment and accelerated earnings growth. Leading companies remain significantly more competitive than industry laggards. This differential will likely widen as companies use cash reserves for strategic acquisitions and to expand their market presence. We believe many companies will continue to post solid results as they take advantage of industry-specific economic conditions to grow their businesses. Our investment strategy remains focused on the longer-term growth potential of the companies in the Funds' portfolios and their ability to manage through a variety of economic conditions. It is important to be vigilant to changing market conditions but respond in a manner consistent with the Funds' longer-term investment strategies. Over time, we believe this perspective will serve the Funds well.

Sincerely,

George A. Henning

The views expressed represent the opinions and beliefs at the time of this commentary and are not meant as a market forecast. These views are subject to change at any time based on market or other conditions. This information may not be relied on as investment advice or as an indication of trading intent on behalf of any Fund. Fund investments may change at any time. Economic and performance information referenced is historical and past performance does not guarantee future results.

3

Pacific Advisors

Government Securities Fund

Fund Objective: High current income, preservation of capital, and rising future income consistent with prudent investment risk.

Investment Invests at least 80% of its assets in U.S. Government fixed income

Strategy: securities. These include securities issued or guaranteed by the U.S. Treasury; issued by a U.S. Government agency; or issued by a Government-Sponsored Enterprise (GSE). May also invest in high quality dividend-paying common stocks.

Investor Profile: Conservative. Income-focused; capital preservation aim.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2011 | For the fiscal year ended December 31, 2010 | ||||||||||||||||||

| Net Expense Ratio | Expense Ratio | ||||||||||||||||||

| Class A | 0.66 | % | Class A | 2.09 | % | 3.69 | % | ||||||||||||

| Class C | 0.33 | % | Class C | 2.80 | % | 4.42 | % | ||||||||||||

| Barclays Capital U.S. Int T-Bond Index1 | 2.10 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Fund's most recent Annual Report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager August 19, 2011

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

The Fund is designed for conservative long-term investors and those with shorter investment horizons who need current income. Accordingly, the Fund seeks to protect capital while using a total return approach to provide current income. Economic uncertainty and the resulting interest rate volatility during the first half of the year reinforced the importance of active portfolio management. In implementing the Fund's strategy of preserving capital and minimizing portfolio volatility, holdings remained concentrated in short to intermediate-term bonds. This strategy was effective in reducing the Fund's sensitivity to interest rate changes.

The Fund's exposure to interest rate volatility can be measured by its "duration": the shorter the duration, the less sensitive an investment is to interest rate movements. For example, if market interest rates rise 0.75%, a portfolio with a 4-year duration would be expected to lose approximately 3% of its value. To protect principal, the Fund maintained an average duration of approximately 1 year.

1 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity. It is not possible to invest directly in the Index.

4

For the six-month period, the Fund's Class A shares returned 0.66% in comparison to 2.10% for its benchmark, the Barclay Capital U.S. Intermediate T-Bond Index. Unlike the Fund, however, the benchmark is an unmanaged portfolio. Also, with an average duration of 3.7 years, its exposure to interest rate changes is significantly greater than the Fund's.

Market Overview

Interest rates, under pressure from competing forces, remained volatile throughout the first half of the year. In the first quarter, the strength of the global economy and concerns about the U.S. fiscal deficit initially pushed interest rates higher. However, downward pressure on interest rates escalated throughout the quarter. Geopolitical unrest, the earthquake in Japan, and the European sovereign debt crisis heightened the demand for safety; as a result, investors' interest in U.S. government securities ballooned.

For most of the second quarter, weaker U.S. economic data and international concerns had investors favoring U.S. government securities over equities. Interest rates, however, spiked at the end of June when investors anticipated a resolution to the sovereign debt crisis in Greece. The yield on the benchmark 10-year Treasury Note, which traded between 3.74% and 2.88% during the first half of the year, ended the period at 3.18%.

Fund Strategy

Fixed Income Strategy

The turbulent interest rate environment continued to warrant a defensive strategy. Long-term bonds, which offered the most attractive yields, also carried the greatest risk of principal losses due to changes in interest rates. In order to protect principal, the Fund continued to concentrate in shorter-term government securities.

In particular, the Fund continued to focus on one-time callable government agency bonds. These bonds provided better yields than short-term Treasuries, yet, due to the call feature, they also have a short expected life. That is, these bonds can be called back on one specific date prior to maturity. If the bonds are not called back, they instead convert to non-callable bonds with higher interest rates. Investors face the risk that, if interest rates on the call date have fallen, or if they remained relatively unchanged, or even if they are modestly higher, the bonds would be called back. In exchange for the call feature, these investors received the benefit of a higher yield. The Fund also invested in shorter-term government agency bonds with yields that increase at fixed intervals over the life of the bond. These "step-up bonds" also help protect principal while providing increasing income.

Given the low interest rate environment, many other government funds have utilized more aggressive investments, such as leverage or mortgage-backed securities, to enhance return. We do not believe, however, that the risks associated with these strategies are appropriate for the Fund's more conservative investors. Alternatively, we continued to surface less well-known, risk-appropriate investments that provided the best total return potential in this challenging environment.

Equity Positioning

The Fund invests a minor portion of its portfolio in high quality, dividend-paying stocks. These equity holdings help provide stability for the Fund by counterbalancing price movements in the fixed income markets. In addition to providing meaningful income (with a current weighted average dividend yield of approximately 4.0%), the Fund's equity investments offer capital appreciation potential. As evidenced by the Fund's average one-year beta2 of 0.07, versus the S&P 500 Index3, these equity investments do not significantly increase risk.

2 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark and a beta greater than 1.0 indicates higher risk than the market or the benchmark.

3 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted measure of 500 widely held common stocks listed on the New York and American Stock Exchanges and The Nasdaq Stock Market. It is not possible to invest directly in the Index.

5

Pacific Advisors

Government Securities Fund continued

During the first half of the year, common stock holdings continued to represent approximately 12% of the portfolio. Higher dividend yields provided a conservative alternative to bonds and helped enhance total return. Equity investments included stocks such as AT&T and Consolidated Edison, with yields of 5.5% and 4.5%, respectively. Additionally, the Fund's equity investments include consumer staples companies, such as Kimberly-Clark, which are less sensitive to economic changes; and blue-chip stocks, such as Chevron, with excellent growth prospects and capital appreciation potential.

Looking Ahead

We expect interest rates will remain volatile in response to conflicting economic pressures. Near-term, interest rates may remain low. Concerns about inflation or the federal deficit would typically drive interest rates higher to compensate for increased risk. On the other hand, investors will likely respond to troubling economic and geopolitical developments by fleeing to the safety of U.S. Treasuries. Presently, however, investors' desire for safety will likely have a greater influence on interest rates.

Yet, as long as interest rates remain at historical lows the risk of a market-driven jump in interest rates remains significant. Ultimately, market forces will drive interest rates higher. The timing of, and catalyst for, the market reaction cannot be predicted; but history shows that rates typically rise quickly and with little warning. Furthermore, the significant spike in rates at the end of June highlights the considerable risk of price depreciation on longer-term and higher yielding bonds.

Given interest rate volatility, the Fund will maintain its strategy to protect principal by concentrating in shorter-term bonds. When a clear trend in interest rates emerges, we will reallocate to longer-term bonds to lock in higher yields and appreciation potential. In the interim, we anticipate maintaining the Fund's equity allocation to help minimize volatility while providing favorable dividend income and the potential for price appreciation.

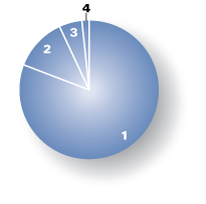

Portfolio Holdings as of 06/30/11 (Based on Total Investments)

| 1. U.S. Government Agencies | 80.95 | % | |||||

| 2. Equities | 12.34 | % | |||||

| 3. Preferred Stock | 5.30 | % | |||||

| 4. Cash and Cash Equivalents | 1.41 | % | |||||

6

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2011 through June 30, 2011.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/11 | Ending Account Value 06/30/11 | Expense Paid During Period 01/01/11 – 06/30/11 | |||||||||||||

| Government Securities Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,006.60 | $ | 12.09 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,012.74 | $ | 12.13 | |||||||||

| Government Securities Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,003.30 | $ | 15.80 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,009.03 | $ | 15.84 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 2.43% for Class A shares and 3.18% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

7

Pacific Advisors

Income and Equity Fund

Fund Objective: Current income and, secondarily, long-term capital appreciation.

Investment Invests primarily in investment grade U.S. corporate bonds and in dividend-paying

Strategy: stocks.

Investor Profile: Conservative. Some current income required; capital preservation aim.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2011 | For the fiscal year ended December 31, 2010 | ||||||||||||||||||

| Net Expense Ratio | Expense Ratio | ||||||||||||||||||

| Class A | 3.44 | % | Class A | 2.34 | % | 3.09 | % | ||||||||||||

| Class C | 3.09 | % | Class C | 3.07 | % | 3.82 | % | ||||||||||||

| Barclays Capital U.S. Int Corp Bond Index1 | 3.26 | % | |||||||||||||||||

| S&P 500 Index2 | 6.02 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Fund's most recent Annual Report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Managers August 19, 2011

Charles Suh, CFA

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

During the first half of 2011, the Fund effectively minimized the impact of interest rate volatility due to heightened global and domestic economic uncertainty. For the period, Class A shares returned 3.44%. The Fund achieved this performance with substantially reduced volatility in comparison to the broader market, as evidenced by its average one-year beta3 of 0.29 versus the S&P 500 Index.

Interest rate volatility combined with a low interest rate environment continued to warrant a conservative strategy. Fixed income holdings, therefore, remained concentrated in short to intermediate-term investment grade bonds. The Fund avoided longer-term bonds; while these bonds offered higher

1 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

2 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

3 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark and a beta greater than 1.0 indicates higher risk than the market or the benchmark.

8

yields, they represented too much risk to principal. High quality dividend-paying common stocks remained a risk-appropriate alternative to help support the Fund's total return.

The Fund's blend of fixed income and equity securities suggests that its performance be viewed against a blend of its benchmarks. Notably, the Fund outperformed Barclays Capital U.S. Intermediate Corporate Bond Index while maintaining a substantially shorter average maturity of 3.3 years. The average maturity for the Index was 5.2 years. The Fund's equity holdings are selected for stable growth. The concentration in these conservative, low volatility stocks accounted for the Fund's lower performance relative to the S&P 500 Index.

Fund Strategy

We actively manage the Fund's fixed income and equity allocations to take advantage of the best risk-appropriate opportunities for income and growth. We typically increase exposure to equities when a positive economic climate presents good capital appreciation opportunities and dividend income.

During the first half of 2011, interest rate volatility increased dramatically. Global uncertainty grew amid myriad economic crosswinds: the expiration of QE2; geopolitical unrest in North Africa and the Middle East; escalating inflationary pressures; an economic slowdown in China; fallout from the earthquake in Japan; and the European sovereign debt crisis. Interest rates spiked in response. The impact on bond prices posed a significant threat to longer-term bond holders. To protect against this volatility, the Fund's fixed income holdings remained concentrated in high-quality bonds with short maturities.

To minimize price volatility, and in response to a relatively positive economic outlook, we increased the Fund's equity allocation from approximately 41% to 44%. The higher equity allocation allowed the Fund to take advantage of opportunities in the equity market for capital appreciation and dividend income without significantly increasing risk. In fact, the Fund's average dividend rate is 3.74% with more than 60% of the Fund's equity holdings paying a dividend in excess of 3.0%. The Fund also benefited from capital appreciation in these superior companies. For example, AT&T appreciated 6.9% during the period in addition to paying a dividend of 5.50%. Other holdings with outstanding dividend rates in excess of 4.0% include Altria Group, Xcel Energy, Public Service Enterprise Group, and Duke Energy.

Fixed Income Strategy

Attractive investment opportunities in high quality corporate bonds remained limited. Low interest rates kept the spread between Treasuries and corporate bonds unusually narrow; as a result, corporate bonds offered low yields with higher risk in comparison to Treasuries. In this challenging environment, we were nevertheless able to benefit from temporary market unrest and purchase investment grade bonds at higher rates.

For example, with inflationary pressures rising, floating rate bonds linked to the Consumer Price Index (CPI) became more attractive in the first quarter. Our active management efforts surfaced a deeply discounted, CPI-linked bond from Prudential Financial with a current interest rate of 5.6%. Also, in the second quarter, we selectively added high-quality fixed rate bonds from solid companies including MDC Holdings and Reliance Steel. These bonds, each with approximately three to five-year maturities, provided yields of more than 4.0%.

Overall, the Fund remained focused on intermediate-term (approximately three to five years) investment grade corporate bonds. To protect principal, we actively managed the portfolio to maintain an average maturity of approximately 3.3 years. This strategy also provides the Fund with the flexibility to adapt to changes in the economic environment.

Consistent with its conservative orientation, the Fund did not invest in speculative or aggressive investments such as derivatives, leverage or high-yield "junk" bonds to enhance total return. Increasing the Fund's allocation to high quality dividend-paying stocks provided a more appropriate means to both seek additional income and capture price appreciation potential.

9

Pacific Advisors

Income and Equity Fund continued

Equity Strategy

The Fund's equity holdings focus on superior, well-established companies across various sectors and industries. The increase in the equity allocation during the first half of the year resulted from appreciation in the Fund's holdings as well as new acquisitions. In the first quarter, we took advantage of the market rally to trim positions in Johnson & Johnson and Home Depot. Proceeds from these sales were reallocated to new holdings such as Pitney Bowes, the world's largest provider of mailing solutions, and Vodafone, a telecommunications firm that owns a 45% stake in Verizon Wireless. These companies stand to benefit from renewed demand in their industries; they also pay dividend rates of 6.5% and 5.4%, respectively.

Several Fund holdings, including Pfizer, McDonald's, Automatic Data Processing and Sysco, also provided meaningful capital appreciation. In particular, McDonald's benefitted from increasing sales in the U.S. as well as emerging markets such as China. Automatic Data Processing shares appreciated substantially as demand for its payroll processing services rebounded.

Looking Ahead

We expect interest rate volatility will increase near-term. Market uncertainty surrounding economic growth, rising inflationary pressures, the European sovereign debt crisis, and Federal Reserve policy will likely continue to produce rapid, but short-lived, interest rate movements. This underlying uncertainty and the resulting volatility reinforce the importance of active portfolio management.

Long-term, we expect market forces will ultimately lead to a rise in interest rates. However, until a clear trend emerges, the Fund will maintain a strategy focused on protecting principal. To minimize the impact of interest changes, the fixed income portfolio will remain concentrated on shorter-term investment grade bonds; also, the Fund will maintain a higher equity allocation. We will continue to be opportunistic, seeking both high-quality corporate bonds with attractive yields and superior large cap stocks with outstanding dividend income.

Portfolio Holdings as of 06/30/11 (Based on Total Investments)

| 1. | Corporate Bonds | 48.27 | % | ||||||||

| Equities | 44.21 | % | |||||||||

| 2. | Consumer Discretionary | 8.51 | % | ||||||||

| 3. | Consumer Staples | 7.18 | % | ||||||||

| 4. | Industrials | 6.25 | % | ||||||||

| 5. | Health Care | 5.50 | % | ||||||||

| 6. | Telecommunication Services | 5.33 | % | ||||||||

| 7. | Utilities | 4.07 | % | ||||||||

| 8. | Information Technology | 3.78 | % | ||||||||

| 9. | Others | 3.59 | % | ||||||||

| 10. | Preferred Stock | 6.05 | % | ||||||||

| 11. | U.S. Government Agencies | 1.13 | % | ||||||||

| 12. | Cash and Cash Equivalents | 0.34 | % | ||||||||

10

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2011 through June 30, 2011.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/11 | Ending Account Value 06/30/11 | Expense Paid During Period 01/01/11 – 06/30/11 | |||||||||||||

| Income & Equity Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,034.40 | $ | 12.71 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,012.30 | $ | 12.57 | |||||||||

| Income & Equity Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,030.90 | $ | 16.47 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,008.58 | $ | 16.29 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 2.52% for Class A shares and 3.27% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

11

Pacific Advisors

Balanced Fund

Fund Objective: Long-term capital appreciation and income consistent with reduced risk.

Investment Invests primarily in large cap common stocks and investment grade

Strategy: U.S. corporate bonds. Invests at least 25% of its assets in fixed income securities and preferred stocks and at least 25% in equities.

Investor Profile: Moderately conservative. Seeks combination of long-term growth, income, liquidity and reduced risk of price fluctuations.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2011 | For the fiscal year ended December 31, 2010 | ||||||||||||||||||

| Class A | 4.81 | % | Class A | 2.77 | % | ||||||||||||||

| Class C | 4.41 | % | Class C | 3.50 | % | ||||||||||||||

| S&P 500 Index1 | 6.02 | % | |||||||||||||||||

| Barclays Capital U.S. Int Corp Bond Index2 | 3.26 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Discussion with Portfolio Managers August 19, 2011

Samuel C. Coquillard

Charles Suh, CFA

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

The Fund is designed to enable conservative investors to participate in the equity markets with limited risk. We actively manage the Fund's equity and fixed income allocations based on our general economic outlook and identification of risk-appropriate investments. We believe this approach provides opportunities to take advantage of specific growth opportunities in the market while also minimizing the Fund's price volatility.

During the first half of 2011, the Fund's Class A shares gained 4.81% which closely tracked the benchmarks. Overall market volatility remained elevated in reaction to geopolitical unrest in the Middle East and North Africa, the catastrophic earthquake and tsunami in Japan and the Greek sovereign debt crisis. Also, the markets reflected concerns over trends suggesting a modest economic slowdown in the U.S. and China. In contrast, the level of volatility in the Fund was significantly lower; the Fund's average one-year beta3 of 0.64 compared favorably to the S&P 500 Index.

1 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

2 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

3 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark and a beta greater than 1.0 indicates higher risk than the market or the benchmark.

12

The Fund's conservative strategy served it well in the first half of the year. Defensive equity and fixed income holdings acted as ballast during market pullbacks. At the same time, strong stock selection in sectors benefitting from economic recovery such as Energy and Industrials delivered favorable returns. Holdings including Halliburton, National Oilwell Varco, CSX, and Norfolk Southern contributed to strong gains in these areas. Financials also performed well; American Express, in particular, benefited from a recovery in consumer spending.

Fund Strategy

The Fund's conservative strategy seeks to provide long-term capital appreciation with reduced risk and volatility. We actively manage the allocation between equity and fixed income investments to seek the best opportunities for total return. In the first half of the year, the Fund's equity allocation remained at approximately 73%.

The Fund's equity investments focus on large, multinational companies that combine stability and growth. During the first half of 2011, and given continuing evidence of economic recovery, we marginally increased the Fund's exposure to those companies expected to benefit from an improving economy.

The Fund's fixed income investments primarily focus on investment grade corporate bonds supplemented by high quality preferred stocks. The fixed income portfolio is actively managed based on our outlook for interest rates. The Fund continued to invest in short-term debt instruments during the period; we believed that the risks associated with higher yielding instruments were inconsistent with the Fund's objectives.

Equity Strategy

The Fund utilizes a long-term, value-oriented equity strategy. Accordingly, it maintains a concentrated portfolio of high quality companies with dominant market positions, superior management teams, and exceptional growth prospects.

During the first half of the year, we continued to see evidence of a sustainable, albeit slow, economic recovery. Leading companies continue to significantly outperform industry laggards. This differential will likely widen as stronger companies use their cash reserves to expand their market positions through strategic acquisitions and other initiatives. Therefore, while economic challenges remain, our strategy of focusing on individual companies and identifiable industry trends has successfully identified growth opportunities.

The Fund added two new equity positions: Dow Chemical and Qualcomm. Dow Chemical is a leading manufacturer of industrial materials including plastics and petrochemicals. The recent acceleration of domestic natural gas supplies has significantly reduced the company's costs to power its plants; as a result, the company has gained a cost advantage in the global marketplace. Additionally, Dow has announced plans to expand and build new manufacturing plants to further capitalize on its position. Chip manufacturer Qualcomm is a primary beneficiary of the emerging smartphone and tablet PC trends; its technology increasingly powers the most popular devices, including the iPhone. We believe mobile computing represents the next evolution in personal and enterprise technology.

We also see significant value in existing holdings including Best Buy, CSX, Halliburton, and Microsoft. Best Buy's strategy is also capitalizing on emerging technology trends. In particular, the company is focused on delivering ease-of-use for connected devices such as mobile phones and home networks. CSX continues to enjoy strong volume and pricing gains due to improved railroad efficiency; also, high gas prices deter the use of long-haul trucks. Halliburton's North American land drilling activities are growing impressively while its international oil and gas markets are also strengthening. And, Microsoft recently released its Office 365 cloud-based productivity suite. In addition, it should begin to benefit from its partnership with Nokia on Windows Phone 7 in the second half of the year.

13

Pacific Advisors

Balanced Fund continued

Fixed Income Strategy

The Fund's fixed income portfolio is actively managed for total return. We utilize a combination of investment grade corporate bonds and high quality preferred stocks to provide current income and capital appreciation potential.

During the first half of 2011, geopolitical unrest in the Middle East and North Africa and the Greek sovereign debt crisis resulted in continued interest rate volatility. The Fund remained positioned in shorter-term investment grade bonds which offered modest income while protecting against market volatility. Furthermore, with rates remaining near historically low levels, the risks of owning higher yielding instruments outweighed the potential benefits. For example, long-term and non-investment grade corporate bonds offered appealing current income; however, they would have exposed the Fund to significant principal losses in the event of even modestly higher interest rates.

Persistently low interest rates and sustained interest rate volatility have created a challenging environment in which to identify attractive high quality bonds. While we continue to seek opportunities to obtain higher yields, we do so only when we believe the risks and rewards are properly balanced. Against this backdrop, we did not add to the fixed income portfolio during the first half of the year. However, we sold select bonds, such as TCI Communication and Estee Lauder, to lock in market appreciation.

We expect interest rates will remain volatile in response to global economic uncertainty and geopolitical events. Nevertheless, we anticipate interest rates will ultimately increase as other investments, such as equities, offer more attractive returns. Even a minor rise in interest rates can result in a substantial loss of principal on longer-term fixed income securities. Indeed, the significant spike in rates during the final week of the period, following the successful passing of austerity measures in Greece, highlights the significant risk underlying longer-term bonds.

Looking Ahead

Our favorable outlook on the broader economy contributes to our expectation that interest rates, while experiencing heightened volatility in the near to mid-term, will rise over time. We believe these conditions continue to warrant a conservative fixed income strategy; consequently, investments will likely remain focused in short to intermediate-term high quality corporate bonds and preferred stocks. When our assessment of interest rates changes, we expect to adjust our fixed income strategy to invest in longer-term bonds with attractive interest rates.

Consistent with our expectations for continued economic growth, we anticipate maintaining the Fund's higher allocation toward equities. We will continue to emphasize holdings in sectors poised to benefit from economic recovery while maintaining a significant allocation to defensive stocks for stability. As the economic recovery progresses, we see increasingly attractive investment opportunities in select industries including Energy, Industrials, and Technology. Our equity strategy remains focused on companies with dominant market positions, superior management teams, and exceptional growth outlooks.

Portfolio Holdings as of 06/30/11 (Based on Total Investments)

| Equities | 73.34 | % | |||||||||

| 1. | Industrials | 14.92 | % | ||||||||

| 2. | Information Technology | 14.69 | % | ||||||||

| 3. | Consumer Staples | 11.41 | % | ||||||||

| 4. | Energy | 8.96 | % | ||||||||

| 5. | Health Care | 8.39 | % | ||||||||

| 6. | Financials | 8.30 | % | ||||||||

| 7. | Consumer Discretionary | 5.16 | % | ||||||||

| 8. | Materials | 1.51 | % | ||||||||

| 9. | Corporate Bonds | 22.58 | % | ||||||||

| 10. | Preferred Stock | 4.08 | % | ||||||||

14

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2011 through June 30, 2011.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 180 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account, and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 180 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account, and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/11 | Ending Account Value 06/30/11 | Expense Paid During Period 01/01/11 – 06/30/11 | |||||||||||||

| Balanced Fund Class A | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,048.10 | $ | 14.63 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,010.51 | $ | 14.36 | |||||||||

| Balanced Fund Class C | |||||||||||||||

| Actual | $ | 1,000.00 | $ | 1,044.10 | $ | 18.40 | |||||||||

| Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,006.79 | $ | 18.06 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio of 2.88% for Class A shares and 3.63% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

15

Pacific Advisors

Large Cap Value Fund

Fund Objective: Long-term capital appreciation.

Investment Invests at least 80% of its assets in large cap companies that are, at the time of

Strategy: purchase, within the market cap range of companies in the S&P 500 Index1.

Investor Profile: Conservative equity. Growth-oriented with a long-term investment horizon.

| TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

| For the six months ended June 30, 2011 | For the fiscal year ended December 31, 2010 | ||||||||||||||||||

| Net Expense Ratio | Expense Ratio | ||||||||||||||||||

| Class A | 3.23 | % | Class A | 3.64 | % | 5.82 | % | ||||||||||||

| Class C | 2.83 | % | Class C | 4.37 | % | 6.57 | % | ||||||||||||

| S&P 500 Index | 6.02 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Returns do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Fund's most recent Annual Report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager August 19, 2011

Samuel C. Coquillard

Fund Performance

The Fund invests in leading blue-chip stocks with long-term capital appreciation potential and reduced price volatility. This stock selection approach focuses on purchasing high quality stocks with attractive dividend rates when those stocks are trading at advantageous prices. The Fund's conservative equity strategy delivered modest gains during the first half of the year; Class A shares returned 3.23%.

The Fund's strongest performers included:

• Kraft which gained 11.8% during the period on growth in its core businesses. We continue to like this long-term portfolio position for several reasons: in addition to its generous dividend yield of 3.33%, the company continues to benefit from its acquisition of Cadbury.

• IBM which rose 16.9% as it continued to capitalize on the global expansion of information technology. Despite its massive size, the company has, throughout its 100-year history, consistently reinvented itself. Continuing this track record, IBM is well positioned to take advantage of current growth trends

1 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

16

in cloud computing and in emerging markets such as China. Further, its focus on higher margin businesses, such as consulting and business software, continues to reap rewards for shareholders.

• McDonald's gained 9.9% as its value-priced offerings continued to resonate with cost-conscious consumers. At the same time, geographic expansions into new markets, such as China, are providing a new avenue of growth for the world's largest restaurant company.

Other notable Fund performers included: Dell, Intel, Sysco, Clorox, HJ Heinz, Time Warner, Cardinal Health, and Johnson & Johnson.

As a Fund designed for more conservative equity investors seeking stable growth, the portfolio is managed to minimize volatility. This orientation is evidenced by its average one-year beta2 of 0.83 versus the S&P 500 Index. With this emphasis on minimizing volatility, the Fund may grow at a slower rate in rising markets while providing better downside protection in falling markets.

Unlike its benchmark, the Fund primarily focuses on mega-cap companies with strong franchises and solid balance sheets whose size and strength typically result in more measured growth over time. In comparison, the S&P 500 Index is comprised of 500 widely-held companies across a variety of sectors and industries. In fact, the Fund's average market cap of approximately $100 billion is substantially greater than the $24 billion for the S&P 500 Index. The Fund, by concentrating on 30 to 50 of the most attractive companies, seeks to consistently provide superior risk-adjusted returns with lower volatility.

Fund Strategy

We believe that high quality, domestic large cap stocks offer significant value for equity investors. The Fund's portfolio predominantly consists of dividend paying stocks in areas of the market that are less sensitive to economic changes. We closely monitor investor behavior to take advantage of buying opportunities when large cap stocks are out-of-favor.

The first half of the year was a tale of two quarters for the Fund. In the market advance during the first quarter, investors favored small and mid-cap companies in areas most responsive to economic recovery. Stocks in the Energy, Industrials, Materials, Information Technology, and Financials sectors outperformed. The market paid little attention to high quality large cap stocks. Their financial strength, expanding global business opportunities, increasing dividend payments, and stock repurchase programs held little attraction. Against this backdrop, we took advantage of discounted pricing to increase the Fund's positions in firms such as Cisco Systems, Sysco and McDonald's. These firms enjoy large cash reserves which give them stability and the flexibility to strategically expand their businesses.