UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | June 30, 2014 |

| ||||||

Item 1. | Report to Shareholders |

| Filed herewith. |

semi-annual report

june 30, 2014

government securities fund

income and equity fund

balanced fund

large cap value fund

mid cap value fund

small cap value fund

Pacific Advisors

table of contents

Message from the Chairman | 1 | ||||||

Government Securities Fund | 5 | ||||||

Income and Equity Fund | 9 | ||||||

Balanced Fund | 14 | ||||||

Large Cap Value Fund | 19 | ||||||

Mid Cap Value Fund | 23 | ||||||

Small Cap Value Fund | 28 | ||||||

Schedule of Investments | 33 | ||||||

Statement of Assets and Liabilities | 56 | ||||||

Statement of Operations | 58 | ||||||

Statement of Changes in Net Assets | 60 | ||||||

Financial Highlights | 64 | ||||||

Notes to Financial Statements | 71 | ||||||

Directors and Officers | 81 | ||||||

This Report is submitted for the general information of the shareholders of Pacific Advisors Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by the Funds' current prospectus, which contains information concerning the investment policies of the Funds as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation or recommendation that any particular investor should purchase or sell any particular security. The statements in the Chairman's Letter and the discussions of the Funds' performance are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change at any time based on market or other conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders,

Equity markets faced a number of challenges during the first six months of 2014. At the beginning of the year, some investors locked in profits from the prior year and took time to assess the outlook for the New Year. Extremely harsh winter weather in the first quarter had a chilling effect on the markets as business activity was disrupted and consumer spending declined. Many feared that the early year selloff might trigger the long-predicted correction. Yet, the market began to recover in the second quarter as business conditions improved along with the weather.

Investors maintained a generally positive outlook on the direction of the economy; their measured optimism looked past issues such as geopolitical concerns in Ukraine and Iraq which, in other times, might well have been more disruptive. We believe that the energy revolution in the U.S., which has reduced our dependence on oil and gas imports, significantly influenced the markets' more sanguine attitude. The equity markets continued to inch higher as stocks seemingly followed the path of least resistance.

The market's upward bias continued even in the absence of any obvious catalysts. Economic data were generally positive, but not overwhelmingly so. Private sector employment and domestic motor vehicle sales reached pre-recession highs and the housing industry regained strength in the spring after weakening in the first quarter. However, first quarter GDP declined 2.9% and growth in the manufacturing sector eased. Yet, investors largely shrugged off the negative data.

The relatively benign economic conditions during the first six months provided an instructive reminder that, from time to time, positive or negative market momentum may propel stocks without any obvious reason. Markets may continue to behave unpredictably as the global economies transition from recession to growth. The Federal Reserve's prominent role in the recovery adds further ambiguity to markets' reaction to events. For example, the equity markets generally react positively to strong economic data; in the current environment, however, the markets may appear to disregard the data or may temporarily fall on fears that the Fed will raise interest rates sooner-than-expected. Conversely, the equity markets might rise on negative news which might suggest further monetary intervention.

In the second quarter, both the S&P 500® Index and Dow Jones Industrial Average reached record highs; while some areas of the market advanced, though, others lagged. The more conservative areas of the market outperformed. For example, large cap stocks significantly outperformed small cap stocks. Similarly, sectors with relatively stable growth and lower volatility, such as Utilities, outperformed. In contrast, sectors such as Retail, Restaurants and Transportation, offer significant growth opportunities as the economy expands but tend to underperform during periods of weakness or uncertainty. We believe the shift toward more conservative equities is temporary; stocks which respond to economic growth should regain traction as the recovery regains momentum.

Demand for bonds remained high in the first half of the year as fixed income investors preferred their relative safety in response to uneven global economic growth and geopolitical tensions. Interest rates remained low as economic data and geopolitical uncertainty provided no incentive for these investors to exit bonds. Many fixed income investors appeared content to await clear evidence of rising rates; over the next several months, though, they will pay close attention to economic reports and the actions of the Federal Reserve.

Investors continue to debate whether or not "the market" has run too far ahead of itself. Yet, these conversations are largely commentaries on investor sentiment rather than market fundamentals. To be sure, some stocks have likely risen beyond prices justified by their fundamental value; just as the high-flying technology and biotech companies came under pressure during the second quarter, these over-valued stocks may too sell off. The question, then, is not whether the market is overvalued or undervalued but whether the prices for individual stocks reflect their long-term appreciation potential. From this viewpoint, we remain encouraged by the growth initiatives among high-quality companies.

1

Message

from the chairman continued

Market Review

All of the major equity markets rose during the second quarter. The S&P 500® Index gained 5.23%, the Dow Jones Industrial Average rose 2.83% and the NASDAQ gained 5.32%. Smaller companies ended higher as well; the Russell Midcap® Index rose 4.97%, and the Russell 2000® Index gained 2.05%.1 The somewhat modest year-to-date returns reflect weak first quarter results followed by stronger second quarter performance.

Interest rates were, despite expectations for long-awaited increases, generally stable while decreasing slightly in the second quarter. Continued strong demand for fixed income investments has maintained downward pressure on rates. Another factor keeping interest rates low was the record-breaking purchase of $107.2 billion of U.S. Treasuries by the Chinese government during the first five months of 2014. These significant purchases were made with the intention of weakening the yuan to aid China's export-driven economy. The yield on the 10-year U.S. Treasury Note fell to a low of 2.44% at the end of May before increasing slightly and hovering below 2.66% for the remainder of the period. Rates on corporate bonds also fell; the combination of strong demand and limited supply tightened the already-narrow yield spread between U.S. Treasuries and corporate bonds. The narrow spread reflects the willingness of some investors to accept lower yields even as these positions expose holders to potential losses when rates increase.

Equity Investment Review

Many companies have strengthened their competitive positioning over the past several years to enhance their long-term growth prospects. The combination of the rebound in stock prices, low interest rates and an improving economic outlook has also rekindled growth through mergers and acquisitions. The significant increase in mergers and acquisitions is an important milestone; they reveal the growing conviction amongst corporate executives that economic conditions are improving. Often, strategic acquisitions provide immediate profitability to facilitate rapidly expanding businesses to quickly add scale to their operations. The severe winter weather delayed many projects for Energy and Industrial companies. Growth in these areas should recover over the remainder of the year. The synergy between Energy companies and various Industrials is an emerging economic trend: the lower cost, and ample supply, of oil and natural gas are emerging as significant catalysts for the U.S. economy; their impact in providing an incentive for companies to expand operations in North America can be felt across many sectors. Other areas, such as Transportation, performed well during the second quarter. Automobile and Truck manufacturers, suppliers and dealerships reported strong sales while trucking, rail and marine transportation continue to benefit from high demand and revenue growth.

Residential and commercial construction has gained momentum as low interest rates and economic growth created demand for remodeling and new construction. Even so, tighter credit conditions impede first time buyers in obtaining mortgages; but, we anticipate that, as employment trends improve and wages grow, home sales for these first timers will improve.

Five years after the "Great Recession," economic growth continues at a modest pace. Unlike many previous economic recoveries, companies and investors remain cautious; corporate executives carefully evaluate growth initiatives. Anxious Investors voice concerns about overvaluations or that geopolitical and economic events may disrupt the markets. We view these cautious attitudes positively as they provide a catalyst for a longer period of sustainable economic growth which should, in turn, provide continued momentum in the equity markets.

Fixed Income Investment Review

Interest rates declined as investors preferred the "safe haven" of fixed income assets. Demand for bonds rose in response to concerns that geopolitical events, economic trends and fears of an overvalued equity

Market Review • June 30, 2014

Index1 | Close | YTD Return | |||||||||

Dow Jones Industrial Avg | 16,826.60 | 2.68 | % | ||||||||

S&P 500® | 1,960.23 | 7.12 | % | ||||||||

NASDAQ | 4,408.18 | 6.20 | % | ||||||||

Russell 2000® (small cap) | 1,192.96 | 3.19 | % | ||||||||

06/30/14 | 06/30/13 | ||||||||||

| 10-Year T-Note Yield | 2.53 | % | 2.52 | % | |||||||

Data: Bloomberg; Federal Reserve

Index returns include reinvested dividends.

2

market might lead to a significant correction. The Fed however, continued to reduce its monthly bond-buying program; absent any major market disruptions, the central bank plans to conclude the program in October. Fed Chair Janet Yellen has also stated that if the labor market continues to improve more quickly than anticipated, the Fed may increase interest rates sooner than expected.

Our fixed income strategy focused on fundamentally-sound government and corporate bonds with shorter durations; as the fixed income markets transition from the Fed's low interest rate policies, these holdings offer the flexibility to identify timely opportunities to adapt to increasing interest rates.

Many factors, such as changes in Fed policies and unforeseen geopolitical or economic events, can affect interest rate movements. Consequently, we anticipate that interest rates will maintain an upward bias although they may also remain somewhat volatile.

Looking Ahead

Led by the U.S. and China, the major global economies are expanding; Europe and Japan continue to struggle with the economic reforms needed to successfully compete in the international markets. For both, growth in the near-to-intermediate-term may be anemic; concerns of a double dip recession, perhaps reminiscent of those voiced during the early stages of the U.S. recovery, may surface. Nevertheless, even modest growth will provide important momentum for the world economies.

In the U.S., businesses, having rebuilt their finances, are turning their focus toward growth initiatives. Companies are actively pursuing strategies to grow through mergers and acquisitions, investments in new plants and equipment and geographic expansions. This focus on capital spending is an important shift; in the last few years, many businesses emphasized less growth-oriented uses of capital such as stock buybacks and dividend increases. Historically, investors would have expected the upturn in plant and equipment spending to have occurred earlier in the economic recovery. However, businesses maintained a more cautious attitude in response to the lackluster economic growth. Their outlook is shifting with the overall improvement in the global economies and the pent-up demand for goods and services in the U.S. and Europe.

Along with an improving economy, the U.S. labor market is beginning to experience shortages; employees now have more willingness to leave for better paying jobs. Companies are reporting increased efforts to retain employees and attract new talent to support their growth initiatives. Customers are demonstrating willingness to accept pricing increases to cover the higher employee costs. In certain industries, companies are addressing shortages of skilled workers by expanding job training programs on their own or with local educational institutions. Increases in employee wages, which has been in abeyance during the economic recovery, will be an important catalyst for consumer spending growth.

Meanwhile, the "shale revolution" has been a game changer for the global energy industry and, in particular, for the competitiveness of the U.S. economy. Companies that are attracted to the prospect of cheap and secure domestic sources of oil and natural gas are bringing manufacturing facilities and jobs back home. These, and other activities that anticipate the benefits of low-cost energy, are in their early stages; they should contribute to economic growth for years, and perhaps decades, to come.

We expect a healthy recovery; yet, healthy does not suggest that we expect the growth rate to rapidly accelerate. Instead, we anticipate a "slower for longer" pace of economic expansion as households and businesses continue to proceed with caution. Today's investing environment requires a measured, sustainable approach. These conditions may temper the excesses that usually accompany rapid economic growth. Such an environment favors the strongest, most disciplined companies; they pursue growth initiatives while maintaining market-leading positions. Weaker competitors, on the other hand, typically benefit only when a rising tide of strong economic growth "lifts all boats." We believe, therefore, that the best-run companies will continue to outperform in a "slower for longer" growth period.

3

Message

from the chairman continued

The interviews which follow provide more detail on the investment strategies of each Fund and a detailed discussion of performance for individual companies and their growth potential. We believe that, even though the first half of 2014 was somewhat challenging, economic growth will continue to provide attractive investment opportunities for our Funds.

Sincerely,

George A. Henning

1 The Dow Jones Industrial Average is an unmanaged, price weighted measure of 30 U.S. stocks selected by the Averages Committee to represent the performance of all U.S. stocks outside the Transportation and Utilities sectors. The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is an unmanaged, market capitalization weighted measure of all domestic and international common stocks (currently over 3,000 stocks) listed on The Nasdaq Stock Market. The Russell 2000® Index is an unmanaged, market-weighted measure of the 2,000 smallest publicly traded companies of the Russell 3000® Index. The Russell Midcap® Index is an unmanaged, weighted measure of the 800 smallest companies within the Russell 1000® Index based on a combination of their market cap and current index membership. The Russell 2000® Growth Index includes those Russell 2000® Index companies with higher price-to-value ratios and higher forecasted growth values; the Russell 2000® Value Index includes those Russell 2000® Index companies with lower price-to-book ratios and lower forecasted growth values. These indices are not available for direct investment. Index returns assume the reinvestment of dividends.

Economic and performance information referenced is historical and past performance does not guarantee future results. The principal value and return of an investment will fluctuate so that an investor's shares may be worth less than the original cost when redeemed. For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money.

Shares of the Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The views expressed represent the opinions and beliefs at the time of this commentary and are not meant as a market forecast. These views are subject to change at any time based on market or other conditions. This information may not be relied on as investment advice or as an indication of trading intent on behalf of any Fund. Fund investments may change at any time.

4

Pacific Advisors

Government Securities Fund

Fund Objective: High current income, preservation of capital, and rising future income consistent with prudent investment risk.

Investment Invests at least 80% of its assets in U.S. Government fixed income securities.

Strategy: These include securities issued or guaranteed by the U.S. Treasury; issued by a U.S. Government agency; or issued by a Government-Sponsored Enterprise (GSE). May also invest in high quality dividend-paying common stocks.

Investor Profile: Conservative. Income-focused; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||||||||||

For the six months ended June 30, 2014 | Current | Prospectus | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | 0.44 | % | Class A | 3.24 | % | 6.06 | % | 3.39 | % | 6.09 | % | ||||||||||||||||

Class C | 0.00 | % | Class C | 3.97 | % | 6.79 | % | 4.16 | % | 6.82 | % | ||||||||||||||||

Barclays Capital U.S. Int T-Bond Index2 | 1.55 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings shown are for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager August 22, 2014

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

The Fund's investment strategy is to manage interest rate risk for both long-term and short-term investors seeking to protect principal. In response to the slow economic recovery and the extended period of low interest rates, the Fund's fixed income investments were concentrated in short- to intermediate-term bonds.

For the first half of the year, Class A shares of the Fund returned 0.44% compared to 1.55% for its benchmark, the Barclays Capital U.S. Intermediate T-Bond Index. Unlike the Fund, however, the benchmark is an unmanaged portfolio. Furthermore, the benchmark's longer average duration reflects a significantly greater exposure to interest rate risk.

During the period, the Fund maintained an average duration of approximately 0.7 years; in contrast, the benchmark's average duration was 3.6 years. Duration measures a portfolio's sensitivity to interest

1 "Current" expense ratio is annualized for the year-to-date as of 06/30/14. "Prospectus" expense ratio is for the fiscal year ended 12/31/13.

2 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity. It is not possible to invest directly in the Index.

5

Pacific Advisors

Government Securities Fund continued

rate movements; when interest rates increase by 1%, a portfolio with a 4-year duration would decline by approximately 4%. The Fund's short average duration reflected our commitment to minimize the negative effects of rising interest rates on bond portfolios. Also, the Fund's strategy to invest in shorter-term bonds provides price stability and the flexibility to respond timely as investment opportunities develop.

The Fund's investments include a small allocation to common stocks; these holdings contribute to total return by providing dividend income and the potential for price appreciation. The Fund selects high-quality, dividend-paying securities which help manage volatility by counteracting price changes in U.S. government securities holdings.

Market Overview

Most investors anticipated that interest rates, which had inched higher towards the end of 2013, would continue to rise as the Federal Reserve tapered its monthly bond-buying program. Instead, a confluence of issues kept the demand for U.S. Treasuries strong. Geopolitical tensions and mixed economic reports including a slowdown in factory output in China and, back at home, a negative reading for first quarter GDP provided no incentive for investors to exit bonds. Also, yields fell as record-breaking bond-purchasing activity by the Chinese government inflated bond prices. These purchases, totaling over $107 billion in the first five months of 2014, sought to aid China's export-driven economy by weakening the value of the Yuan. Stronger-than-expected domestic employment data and a rebound in Chinese manufacturing temporarily reversed the trend. Then, escalating tensions in Ukraine and accommodative monetary policies by the European Central Bank once again pressured rates. The yield on the 10-year U.S. Treasury Note, which closed 2013 at 3.04%, fell to 2.61% in early February. During the remainder of the period, Treasuries rose in February and March (reaching 2.82% in early April) before falling to 2.44% in May and closing the second quarter at 2.53%.

The Fed continued to reduce its monthly bond-buyback program although the effects of tapering were mostly overshadowed. Meanwhile, inflation remained subdued. The current interest rate environment is unusual in that the major central banks around the world are simultaneously utilizing low interest rates to spur growth; such a coordinated action on interest rate policy is virtually unprecedented. Nevertheless, prevailing interest rates are likely headed higher; changes in interest rates, though, will reflect investors' reactions to current events well in advance of central banks' policy changes. Consequently, we continue to invest in shorter-term government securities which offer principal protection as rates rise. Bonds with longer durations may offer higher yields, but we believe that the long-term risk tradeoff of higher yields versus falling prices is unfavorable. Indeed, when rates rose in 2013, portfolios that were invested in longer-term securities suffered significant losses.

Fund Strategy

Fixed Income Strategy

Over 80% of the Fund's holdings were invested in U.S. government agency bonds. These agency bonds offer higher coupon rates than U.S. Treasuries which enabled the Fund to increase income without materially increasing risk. The Fund captured additional yield by primarily purchasing callable government agency bonds with short-to-intermediate maturities. The callable bonds had higher coupon rates than non-callable bonds because they allowed the issuing agencies to call back the bonds on pre-set call dates. The Fund purchased callable bonds which included a "step-up" feature; here, the bonds' interest rates increase if the bonds are not called away. Also, the day-to-day prices for step-up callable bonds tend to be less volatile than for non-callable bonds. Even so, and given the low interest rate environment, we expected these bonds would be called back in less than a year. The frequent replacement of these callable bonds enabled the Fund to quickly respond to interest rate changes. As expected, many of these bonds were called and the proceeds were reinvested in other callable government agency bonds with step-up features.

The Fund does not employ higher-risk strategies to enhance return. For example, the Fund does not purchase bonds with extended durations, utilize leverage strategies or invest in mortgage-backed securities.

6

Equity Positioning

The Fund invests a minor portion of its portfolio (less than 18%) in high-quality, dividend-paying common stocks. Equity holdings focus on stocks that are relatively less sensitive than the overall market to economic disruptions while offering attractive dividends and the potential for price appreciation. Stock price appreciation added to the Fund's performance and offset the low interest rates on short- to intermediate-term U.S. government securities. We anticipate that the Fund's allocation to equities may be reduced as interest rates rise and the Fund repositions the portfolio toward longer-term U.S. government securities.

Several Fund holdings, including Unilever and Johnson & Johnson, performed well as investors favored the more conservative sectors of the market. During the period, the Fund took advantage of the equity markets' strong appreciation to trim positions in companies such as McDonald's, Chevron, and Microsoft; also, the Fund sold positions in Safeway and 3M.3 The Fund increased its positions in Unilever and Eli Lilly and added PepsiCo.

Looking Ahead

We expect that demand for U.S. government securities will, in the absence of major geopolitical turmoil, diminish somewhat in the second half of 2014. We also anticipate that investors will actively trade government bonds in response to various catalysts such as economic data, Fed policies and global concerns; as a result, interest rates will likely be volatile in the upcoming months. The Fed intends to conclude its quantitative easing ("QE") program in October; the central bank has also stated that it anticipates keeping the federal funds (or "fed funds") rate low for a considerable time after the QE program of bond purchasing ends. Fed officials expect to raise the fed funds rate sometime in 2015; even so, they may decide to raise the rate sooner should the labor market improve more quickly than anticipated. Moreover, the recent purchases of U.S. Treasuries by the Chinese are unlikely to continue at their record-high pace; the Chinese government now owns approximately 11% of the $12 trillion U.S. Treasury market. Interest rates will undoubtedly increase as these purchases decrease; clearly, though, the timing of these events is unknown and unpredictable. Also, the upcoming November elections for the U.S. Senate and House may add another element of uncertainty and volatility.

Investor response to the events and economic data over the remainder of the year will strongly influence interest rates. These reactions, however, are likely temporary; rates should resume their upward trend following the protracted period of historically low levels. As a result, we believe that the Fund's prudent strategy of investing in shorter-term U.S. government securities remains appropriate. We will monitor changing market conditions and manage the Fund accordingly. We expect to migrate the Fund's investments toward longer-term U.S. government securities to capture higher yields as interest rates increase. The Fund's adaptive strategy provides the flexibility to adjust portfolio holdings according to the market environment while keeping the current bias of increasing interest rates in mind.

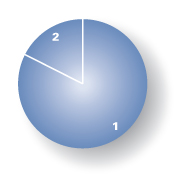

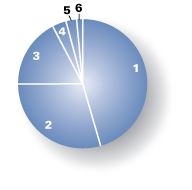

Portfolio Holdings as of 06/30/14 (Based on Total Investments)

1. | U.S. Government Securities | 82.29 | % | ||||||||

2. | Equities | 17.71 | % | ||||||||

3 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

7

Pacific Advisors

Government Securities Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2014 through June 30, 2014.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/14 | Ending Account Value 06/30/14 | Expense Paid During Period 01/01/14 – 06/30/14 | |||||||||||||

Government Secs Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,004.40 | $ | 16.10 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,008.73 | $ | 16.14 | |||||||||

Government Secs Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,000.00 | $ | 19.69 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,005.11 | $ | 19.74 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 3.24% for Class A shares and 3.97% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

8

Pacific Advisors

Income and Equity Fund

Fund Objective: Current income and, secondarily, long-term capital appreciation.

Investment Invests primarily in investment grade U.S. corporate bonds and in

Strategy: dividend-paying stocks.

Investor Profile: Conservative. Some current income required; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||||||||||

For the six months ended June 30, 2014 | Current | Prospectus | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | 4.09 | % | Class A | 1.93 | % | 2.68 | % | 2.23 | % | 2.98 | % | ||||||||||||||||

Class C | 3.59 | % | Class C | 2.68 | % | 3.43 | % | 3.03 | % | 3.78 | % | ||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index2 | 3.61 | % | |||||||||||||||||||||||||

S&P 500® Index3 | 7.12 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Managers August 22, 2014

Charles Suh, CFA

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

During the first half of the year, the Fund's conservative approach provided modest gains. Interest rates had hit historical lows in May 2013 before trending higher following the Federal Reserve's announced decision to begin tapering its accommodative monetary policies. The yield on the 10-year U.S. Treasury Note, which hit a low of 1.66% in early May, rose to end the year at 3.04%. Yet, in 2014, investor demand for Treasuries increased in response to the slow economic recovery and various geopolitical tensions. As a result, the much-anticipated increase in long-term interest rates temporarily reversed direction; rates ended the period at 2.53%. The Fund's fixed income strategy remained focused on short- to intermediate-term investment grade bonds; these conservative bonds provide not only valuable protection against price volatility but also better maintain their valuations as interest rates rise. Class A shares

1 "Current" expense ratio is annualized for the year-to-date as of 06/30/14. "Prospectus" expense ratio is for the fiscal year ended 12/31/13.

2 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

3 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

9

Pacific Advisors

Income and Equity Fund continued

of the Fund gained 4.09%. Notably, the Fund generated these returns with substantially less risk than the broader market as demonstrated by the Fund's one-year beta4 of 0.41, as of June 30th, versus the S&P 500® Index.

The average maturity of the Fund's fixed income holdings, at 3.6 years, reflects our strategy of protecting principal against volatility and rising interest rates. In comparison, the Fund's fixed income benchmark, the Barclays Capital U.S. Intermediate Corporate Bond Index, an unmanaged bond portfolio, maintains an average maturity of 5.0 years.

The Fund's equity portfolio benefitted from the strong performance of individual stocks as well as the solid gains in the stock market. Equity holdings remained concentrated in 30 to 40 high-quality, dividend-paying stocks with relatively low volatility and stable growth patterns; in contrast, the Fund's equity benchmark, the S&P 500® Index, is comprised of companies across a wide range of quality, risk factors and volatility. Also, the companies represented in the Fund are, on average, approximately three times larger than the companies in the Index.

Even though the Fund's fixed income and equity portfolios differ from their respective benchmarks, Fund performance is best compared to a blended return based on the two benchmarks. During the period, the blended return was 5.26%.

Fund Strategy

The Fund actively managed the allocation between fixed income and equity securities to find the most attractive, risk-appropriate opportunities for income and price appreciation. Corporate bond holdings remained at approximately 50% of the portfolio while the equity portion increased slightly to 46% during the period. The Fund's fixed income holdings in short- to intermediate-term investment grade corporate bonds provide both principal protection and the opportunity to reinvest at higher yields when interest rates rise. For the equity portfolio, Fund holdings include a diverse selection of dividend-paying blue-chip stocks; the relatively high dividends compensate for low yields offered by short- to intermediate-term corporate bonds. This equity strategy has been critical to the Fund's performance during the extended period of low interest rates as the dividend yields for portfolio stocks were often higher than the yields on corporate bonds issued by those same companies. We anticipate that the equity allocation may decrease as interest rates resume their upward trend and we reinvest capital in higher-yielding bonds.

Interest rates fell toward the beginning of the year as investors preferred the "safe haven" of U.S. Treasuries and quality corporate bonds. Demand rose in response to uneven global economic data, including the slowdown in China's manufacturing sector, and conflicts in Ukraine and elsewhere. Additionally, the Chinese government, in an attempt to weaken its own currency in order to encourage exports, purchased a record-breaking $107+ billion of U.S. Treasuries during the first five months of 2014. The continuing strong demand for bonds, combined with muted inflationary pressures, left fixed income investors inclined to maintain bonds holdings rather than migrate to riskier investments.

Fixed income investors sought both U.S. Treasuries and corporate bonds, which drove yields for Treasuries, investment grade and high-yield (or "junk" bonds) lower. And, the differences in yields (or "spread") between these types of bonds narrowed. During the first six months of 2014, the average yields of investment grade bonds fell 0.40% to 3.46% while the average yields on junk bonds fell 0.62% to 5.33%. The narrow spread reflects the willingness of some investors to accept lower yields on riskier bonds even though these higher-risk bonds have greater exposure to potential losses when rates increase. Not surprisingly, the inventory of quality bonds decreased as demand increased. Even so, the Fund does not use speculative or aggressive investments such as derivatives or leverage to enhance yield; and, no more than 5% of the Fund may be invested in below investment grade bonds. Consequently, the Fund selected bonds that we determined, after reviewing the financials, history and cash flow expectations of each company, presented attractive investment opportunities.

4 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark; a beta greater than 1.0 indicates higher risk than the market or the benchmark.

10

Fixed Income Strategy

The Fund's fixed income strategy anticipates that interest rates may remain somewhat volatile with an upward bias. Fixed income holdings, therefore, are focused on corporate bonds with short-to-intermediate maturities; these securities also provide the flexibility to identify timely investment opportunities as the fixed income market transitions to higher rates. Shorter-term bonds continued to enjoy strong demand as many institutional buyers, including other bond mutual fund managers, also favored these securities; as a result, the supply of attractive fixed income securities tightened further. As of June 30th, the average yield on 5-year investment grade U.S. corporate bonds was 2.29%; in this limited-supply, low-yield environment, the Fund also sought to enhance returns by identifying opportunities in good-quality corporate bonds with distinctive characteristics.

The Fund's strategy continued to utilize callable corporate bonds. Callable bonds are securities that can be bought back, or "called," by the issuer prior to maturity at predefined dates and at prices which generally include a premium over the bond's issue price. These types of bonds typically have higher yields due to their call features. The Fund's callable bonds provide higher returns and, when called, they enable the Fund to potentially reinvest in higher-yielding bonds. If, on the other hand, a callable bond is not called back, the Fund may have the opportunity to generate higher returns as the bond's yield increases.

The Fund may also purchase bonds with attractive yields due to company-specific issues or economic conditions. For example, in May, we purchased a callable bond maturing in 6 years that was issued by Ball Corporation.5 The yield until the first call date in early 2015 is approximately 1.75%; if the bond is not called on that date, the yield to maturity increases to 5.35%. The company, which supplies metal, plastic and glass packaging to the beverage, food and personal care industries, was under pressure as increasingly health-conscious consumers lessened the demand for carbonated soft drinks. Investors seemed somewhat disinterested in the company's bond offerings, yet our analysis concluded that the company's improving financials will likely continue to strengthen as the company expands into higher-margin products.

Equity Strategy

The Fund's equity holdings provide an important complement to corporate bonds especially during the current period of historically low interest rates. Our equity strategy focuses on total return through dividend income and capital appreciation. We select high-quality, blue-chip companies across a wide array of industries. During the period, we increased our allocation to companies which generally provide better growth opportunities during periods of global economic expansion; for example, we added to several industrial and telecommunications holdings.

We also continued to favor well-established stocks with attractive dividends. Lately, few firms have been inclined to increase dividend rates. Companies have been able to borrow or refinance at extremely low rates; as a result, the difference between a company's bond yield and its dividend yield may have narrowed. In some cases, the dividend yields of Fund holdings exceeded the yields of the corporate bonds issued by these same companies. For example, as of June 30th, Vodafone's dividend yield of 6.63% was significantly higher than the the approximate 2.46% yield of the company's corporate bond maturing in June 2019.

The weighted average yield for the Fund's equity holdings is 3.09% which is notably higher than the 2.29% average yield for 5-year investment grade corporate bonds. Stocks with a dividend yield over 4.5% included AT&T and Vodafone; companies with a dividend yield between 3.5% and 4.5% included Duke Energy, Verizon, Mattel, Xcel Energy and Public Services Enterprise Group.

We anticipate that, as the global economy further improves and interest rates trend higher, our allocations will adjust. We expect to manage portfolio risk and increase investment returns by reducing the Fund's equity holdings in favor of fixed income holdings with higher coupon yields as interest rates increase.

5 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

11

Pacific Advisors

Income and Equity Fund continued

Looking Ahead

Our outlook for the U.S. and global economies remains positive. Consistently strengthening economic data will enable the Fed to remain on track to end its monthly bond-buying program in October; improving employment statistics may spur the central bank to raise the federal funds rate sooner than later. Overall market conditions will determine how far, and how quickly, interest rates will rise. The shifting interest rate environment should prompt conservative investors to reevaluate their willingness to hold long-term bonds as interest rates increase.

The Fund's adaptive strategy provides the flexibility to manage the risk of higher interest rates. The approach also enables the Fund to gradually increase yield by reinvesting capital at the prevailing higher interest rates as bond holdings mature or are called away. Furthermore, the flexibility allows us to proactively adjust to changing market environments while acknowledging the upward bias of interest rates. We believe that the Fund is well-positioned for developing economic and market conditions including the transition from historically low interest rates to higher interest rates.

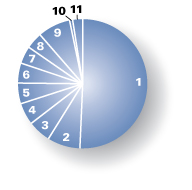

Portfolio Holdings as of 06/30/14 (Based on Total Investments)

1. | Corporate Bonds | 50.48 | % | ||||||||

Equities | 46.49 | % | |||||||||

2. | Consumer Staples | 8.25 | % | ||||||||

3. | Industrials | 5.76 | % | ||||||||

4. | Utilities | 5.61 | % | ||||||||

5. | Information Technology | 5.20 | % | ||||||||

6. | Consumer Discretionary | 4.88 | % | ||||||||

7. | Health Care | 4.43 | % | ||||||||

8. | Telecommunication Services | 4.19 | % | ||||||||

9. | Others | 8.17 | % | ||||||||

10. | Preferred Stock | 0.60 | % | ||||||||

11. | Cash and Cash Equivalents | 2.43 | % | ||||||||

12

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2014 through June 30, 2014.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 01/01/14 | Ending Account Value 06/30/14 | Expense Paid During Period 01/01/14 – 06/30/14 | |||||||||||||

Income & Equity Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,040.90 | $ | 9.77 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,015.22 | $ | 9.64 | |||||||||

Income & Equity Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,035.90 | $ | 13.53 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,011.50 | $ | 13.37 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 1.93% for Class A shares and 2.68% for Class C shares, multiplied by the average account value over the period, multiplied by 181/365 days to reflect the one-half year period.

13

Pacific Advisors

Balanced Fund

Fund Objective: Long-term capital appreciation and income consistent with reduced risk.

Investment Invests primarily in large cap common stocks and investment grade U.S. corporate

Strategy: bonds. Invests at least 25% of its assets in fixed income securities and preferred stocks and at least 25% in equities.

Investor Profile: Moderately conservative. Seeks combination of long-term growth, income, liquidity and reduced risk of price fluctuations.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||

For the six months ended June 30, 2014 | Current | Prospectus | |||||||||||||||||

Class A | –0.18 | % | Class A | 2.80 | % | 3.07 | % | ||||||||||||

Class C | –0.59 | % | Class C | 3.55 | % | 3.86 | % | ||||||||||||

S&P 500® Index2 | 7.12 | % | |||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index3 | 3.61 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Discussion with Portfolio Managers August 22, 2014

Charles Suh, CFA

Jingjing Yan, CFA

Samuel C. Coquillard

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Fund Performance

Overall performance reflects the combined results of the Fund's diversified "all cap" equity strategy and "total return" approach to fixed income investing. The Fund experienced mixed results in the first half of 2014; many of the Fund's large cap stocks performed well while several mid-cap and small cap holdings disappointed. Disappointing first quarter economic reports and escalating geopolitical tensions prompted investors to favor more conservative areas of the market, including large cap stocks and stocks with relatively high dividends. During the period, the Fund's fixed income holdings were concentrated in shorter-term investment grade corporate bonds; these bonds, which were selected to protect principal and minimize price volatility, trailed the fixed income benchmark which includes bonds with longer maturities. Bonds with shorter maturities typically underperform when interest rates fall as they did during the period.

1 "Current" expense ratio is annualized for the year-to-date as of 06/30/14. "Prospectus" expense ratio is for the fiscal year ended 12/31/13.

2 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

3 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

14

The Fund underperformed during the first half of the year; Class A shares declined slightly (–0.18%) to trail both the S&P 500® Index, which rose 7.12%, and the Barclays Capital U.S. Intermediate Corporate Bond Index, which rose 3.61%. The Fund's combination of equity and fixed income securities suggests that its performance would be best viewed against a blend of its equity and fixed income benchmarks. Fund volatility remained below average, with a one-year beta4 of 0.85, as of June 30th, compared to the S&P 500® Index. The Fund's bond holdings and, to a lesser extent, large cap equity holdings contributed to its relatively modest volatility; mid-cap and small cap holdings, however, experienced periods of heightened volatility during the period.

Fund Strategy

The Fund's conservative strategy seeks to provide long-term capital appreciation with limited risk and volatility. We actively manage the allocation between equity and fixed income investments to seek the best opportunities for long-term growth. The Fund combines high-quality stocks across all market capitalizations with fixed income holdings, primarily in investment grade corporate bonds, that provide income and appreciation potential. This balanced approach enables the Fund to take advantage of specific growth opportunities while reducing price volatility.

During the first quarter, economic growth stalled due primarily to unusually harsh winter weather. Business activity improved throughout the second quarter yet the increasing geopolitical tensions in Ukraine and Iraq contributed to a cautious equity market environment. Meanwhile, the Federal Reserve cited improved employment data and modest inflationary pressures in continuing to wind down its bond-buying program. Global conditions remained favorable, with an ongoing recovery in Europe, impressive growth in China and a gradually improving Japanese economy. Given the positive economic outlook, we maintained the Fund's equity allocation (71% of total assets) near the high end of its historical range.

Equity Strategy

The Fund's "all cap" equity strategy focuses on high-quality, well-managed companies that have proven track records of growth. Large cap stocks, which accounted for approximately 45% of the equity holdings, favor prominent global companies which provide a combination of stability and moderate growth potential. Mid-cap holdings, representing approximately 42% of the equity holdings, feature industry leaders benefiting from favorable trends and company-specific opportunities. Small cap holdings focus on established companies with long-term growth prospects.

Many of the Fund's large cap holdings benefitted from the market environment that favored large cap stocks. Individual stocks enjoyed strong performance; oilfield services companies Halliburton and National Oilwell Varco rose as activity related to the North American "shale revolution" and deepwater offshore drilling increased.5 The latter also completed the spinoff of its distribution operation which will enable the company to focus on more profitable business lines. Disney gained on impressive second quarter results led by strong box office and DVD sales of its animated film "Frozen." Truck engine manufacturer Cummins rose as companies are once again investing in and expanding their truck fleets; heavy duty commercial truck sales are on pace to grow more than 20% this year. And, shares of Microsoft rose on higher PC sales as corporations and consumers migrated to newer versions of Windows and Office.

Several of the Fund's mid-cap and small cap holdings lagged as investors sought to avoid risk; stocks which provided disappointing news or results were particularly hard-hit. Engineering and construction company Chicago Bridge & Iron sold off following criticism of its accounting treatment for last year's acquisition of Shaw Industries. Industrial parts distributor DXP Enterprises fell after a lackluster first quarter earnings report which headlined weak performance in a newly acquired business. And, home furnishings retailer Conn's slid when a slight deterioration in credit trends triggered a steep selloff in the shares. We believe these situations reflect the market's short-term orientation rather than significant setbacks for the

4 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark; a beta greater than 1.0 indicates higher risk than the market or the benchmark.

5 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

15

Pacific Advisors

Balanced Fund continued

companies. Accordingly, and in affirming our long-term positive view on these stocks, we added to our positions in Chicago Bridge & Iron, DXP Enterprises, and Conn's during the period.

The Fund added two new positions, Nike and Lithia Motors, during the quarter. Nike, the dominant franchise in the athletic apparel industry, benefits from advanced manufacturing capabilities and a sizable marketing budget. We believe that, with these advantages, the company will increase its global market share; China, in particular, represents a significant long-term growth opportunity. Lithia Motors, the eighth largest automotive retailer in the U.S., has typically operated in smaller towns where the company maintains market leadership. The recent acquisition of DCH Auto Group, which owns 27 new car facilities in New York, New Jersey, and California, expands the company's reach into faster growing metropolitan areas as well. We believe Nike and Lithia represent model Fund investments: Nike, as a dominant global franchise that should benefit from demographic and emerging market trends; and Lithia, as a medium-sized leader in an attractive industry with prospects for both near-term and long-term growth.

Fixed Income Strategy

The Fund's "total return" approach actively manages fixed income holdings in response to current interest rate trends. In selecting appropriate bonds, we examine each company's fundamentals including trends in cash flows, liquidity ratios, and debt maturity schedules. We then assess each bond's income and capital appreciation prospects based on its market price and yield. The extended period of low interest rates and our expectation that rates will rise contributed to our decision to maintain the Fund's fixed income allocation near the lower end of its historical range.

Rates on the 10-year U.S. Treasury Note declined from 3.04% at the end of 2013 to 2.53% by the end of June. Investors flocked to Treasuries in response to geopolitical concerns and the slow economy which stemmed, in part, from the harsh winter weather. Yet, another important but largely unreported factor in the decline was the record-breaking purchase of U.S. Treasuries by the Chinese government; during the first five months of the year, China purchased over $107 billion Treasuries to weaken its currency in order to support the country's export-based economy. Continued purchases of this magnitude may be unlikely; moreover, they may have temporarily distorted the market.

The decline in interest rates during the period benefitted bonds with longer maturities. As rates fell, longer-dated bonds gained in value. The Fund's shorter-term investment grade corporate bonds provided stability but less appreciation. Despite the underperformance, we continue to believe that the Fund's current positioning offers price protection should interest rates increase. Recent data point to a strengthening U.S. economy; and, the Fed is winding down its bond-buying program. Thus, current conditions suggest that interest rates are biased to the upside.

Looking Ahead

In the second half of the year, investors will likely focus on the eventual normalization of monetary policy as the Fed is expected to end its bond-buying program before the end of 2014. Further, most Fed watchers believe the first interest rate hikes will take place sometime in late 2015. Still, the low interest rate environment has persisted longer than most envisioned; indeed, the Fed may hold rates lower for longer, particularly in light of rising geopolitical risks and subdued inflation. Nevertheless, last year's "taper tantrum" is a stark reminder of how abruptly markets can change course; then, rates rose sharply as investors reacted to the Fed's decision to begin winding down its bond-buying program.

Importantly, the U.S. economy remains on firm footing and is expected to generate solid growth for the remainder of the year. Rising confidence in the economic outlook should support the Fund's equity investments in economically sensitive areas of the market, such as transportation. Railroad companies CSX and Kansas City Southern, for example, will handle increased shipments of merchandise, grains, and crude oil. Likewise, manufacturers, including General Electric, will benefit from higher capital spending as businesses invest for growth. In addition, long-term trends favoring the information technology and mobile computing industries should drive strong results at IBM and Qualcomm.

16

Smaller company shares underperformed during the first half of the year as investors pulled back from riskier areas of the market. Improved investor sentiment, supported by a healthy and expanding economy, could lead to a rebound in these stocks. Here, fast-growing companies such as Helix Energy, which owns and operates deepwater oilfield service rigs, and Team, which provides maintenance and repair services for refineries, should enjoy renewed investor interest. Thus, given our positive economic and market outlook, we believe that the Fund's emphasis towards equity holdings, in general, as well as its meaningful exposure to smaller and mid-sized companies, remains appropriate.

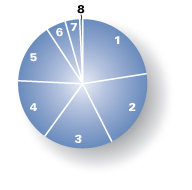

Portfolio Holdings as of 06/30/14 (Based on Total Investments)

Equities | 70.58 | % | |||||||||

1. | Industrials | 30.02 | % | ||||||||

2. | Consumer Discretionary | 11.83 | % | ||||||||

3. | Energy | 11.60 | % | ||||||||

4. | Financials | 6.71 | % | ||||||||

5. | Information Technology | 5.97 | % | ||||||||

6. | Consumer Staples | 4.45 | % | ||||||||

7. | Corporate Bonds | 29.42 | % | ||||||||

17

Pacific Advisors

Balanced Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2014 through June 30, 2014.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 5.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 180 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account, and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.