| OMB APPROVAL |

OMB Number: 3235-0570 Expires: August 31, 2020 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-07076 | |

| Wilshire Mutual Funds, Inc. |

| (Exact name of registrant as specified in charter) |

| 1299 Ocean Avenue, Suite 700 Santa Monica, CA | 90401-1085 |

| (Address of principal executive offices) | (Zip code) |

Jason A. Schwarz

| Wilshire Associates Incorporated, 1299 Ocean Avenue, Suite 700, Santa Monica, CA 90401-1085 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (310) 451-3051 | |

| Date of fiscal year end: | December 31 | |

| | | |

| Date of reporting period: | December 31, 2017 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Wilshire Mutual Funds, Inc. |

ANNUAL REPORT Large Company Growth Portfolio Large Company Value Portfolio Small Company Growth Portfolio Small Company Value Portfolio Wilshire 5000 Indexsm Fund Wilshire International Equity Fund Wilshire Income Opportunities Fund |

December 31, 2017 |

http://advisor.wilshire.com

Wilshire Mutual Funds, Inc. Table of Contents |

|

Letter to Shareholders | 1 |

Commentary: | |

Large Company Growth Portfolio | 4 |

Large Company Value Portfolio | 8 |

Small Company Growth Portfolio | 12 |

Small Company Value Portfolio | 16 |

Wilshire 5000 IndexSM Fund | 20 |

Wilshire International Equity Fund | 24 |

Wilshire Income Opportunities Fund | 30 |

Disclosure of Fund Expenses | 36 |

Schedules of Investments/Condensed Schedules of Investments: | |

Large Company Growth Portfolio | 39 |

Large Company Value Portfolio | 41 |

Small Company Growth Portfolio | 43 |

Small Company Value Portfolio | 45 |

Wilshire 5000 IndexSM Fund | 47 |

Wilshire International Equity Fund | 49 |

Wilshire Income Opportunities Fund | 52 |

Statements of Assets and Liabilities | 71 |

Statements of Operations | 74 |

Statements of Changes in Net Assets | 76 |

Financial Highlights: | |

Large Company Growth Portfolio | 81 |

Large Company Value Portfolio | 83 |

Small Company Growth Portfolio | 85 |

Small Company Value Portfolio | 87 |

Wilshire 5000 IndexSM Fund | 89 |

Wilshire International Equity Fund | 91 |

Wilshire Income Opportunities Fund | 93 |

Notes to Financial Statements | 95 |

Report of Independent Registered Public Accounting Firm | 121 |

Additional Fund Information | 122 |

Tax Information | 125 |

Board Approval of Advisory and Subadvisory Agreements | 127 |

This report is for the general information of the shareholders of Large Company Growth Portfolio, Large Company Value Portfolio, Small Company Growth Portfolio, Small Company Value Portfolio, Wilshire 5000 IndexSM Fund, Wilshire International Equity Fund and Wilshire Income Opportunities Fund. Its use in connection with any offering of a Portfolio’s shares is authorized only if accompanied or preceded by the Portfolio’s current prospectus.

Wilshire Mutual Funds, Inc. are distributed by Ultimus Fund Distributors, LLC.

Wilshire Mutual Funds, Inc. Letter to Shareholders (Unaudited) |

|

Dear Wilshire Mutual Fund Shareholder:

We are pleased to present this annual report to all shareholders of the Wilshire Mutual Funds. This report covers the period from January 1, 2017 to December 31, 2017, for all share classes of Large Company Growth Fund, Large Company Value Fund, Small Company Growth Fund, Small Company Value Fund, Wilshire 5000 IndexSM Fund, Wilshire International Equity Fund and Wilshire Income Opportunities Fund.

MARKET ENVIRONMENT

U.S. Equity Market

The US stock market, represented by the Wilshire 5000 Total Market IndexSM, was up 6.4% for the fourth quarter and 21.0% for 2017. This marks the Index’s ninth straight annual gain. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades.

During the year, large-cap stocks outpaced small-cap stocks, with the Wilshire US Large-Cap IndexSM and the Wilshire US Small-Cap IndexSM returning 21.8% and 13.5%, respectively. The strong overall return for the Wilshire 5000 Total Market Index masked a wide performance dispersion between investment styles and among industries for the year. Growth oriented stocks handedly outpaced growth stocks across the capitalization spectrum. The Wilshire US Large-Cap Growth IndexSM and the Wilshire US. Small-Cap Growth IndexSM outpaced their growth oriented counterparts by 940 basis points and 1,213 basis points, respectively. Sector-wise, renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth.

International Equity Market

Markets rallied in 2017 behind synchronized global growth, strong corporate earnings growth, improved investor sentiment and signs of diminishing political risks globally. After four years lagging US equities, international equities outperformed US equities during the year with the MSCI ACWI ex US Index returning 27.2%. The US dollar weakened in 2017, providing a boost for US investors holding foreign currencies – the MSCI ACWI ex US Index in local currency terms returned 18.2%.

For the second year in a row, emerging markets outpaced foreign developed markets with the MSCI Emerging Markets Index returning 37.3%, largely driven by a weakening US dollar, strong profits from technology companies, strengthening global economy and rising commodities prices. 2017’s return was the strongest year for broad emerging markets equity since they recovered from the global financial crisis in 2009.

1

Wilshire Mutual Funds, Inc. Letter to Shareholders (Unaudited) - (Continued) |

|

Bond Market

The US fixed income market was positive for 2017 with the Bloomberg Barclays US Aggregate Bond Index returning 3.5%. Investment grade corporate securities led the rally during the year as credit overall did well over the period. The ICE Bank of America US High Yield Index returned 4.5% as spreads continued to tighten and remain near historical lows. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink its $4.5T balance sheet starting in October 2017.

During the first quarter, anticipation for quick and swift fiscal policy reforms from the Trump Administration fueled Treasury yields higher and the 10 Year US Treasury yield peaked at just over 2.60% in mid-March before falling to end the first quarter. The US Treasury curve continued to flatten over the remainder of the year with the bellwether 10-year Treasury yield ended the quarter at 2.40%, up slightly but approximately equal to year-end 2016. Globally, continued accommodative monetary policy, a weaker US Dollar, positive economic outlooks and subdued inflation boosted global fixed income. The Bloomberg Barclays Global Aggregate ex US Index returned 10.5% for the year.

Fund Performance Review

The Large Company Growth Portfolio Institutional Class returned 27.35%, underperforming the Russell 1000 Growth Index by 2.86%. The Large Company Value Portfolio Institutional Class returned 14.99%, outperforming the Russell 1000 Value Index by 1.33%. The Small Company Growth Portfolio Institutional Class returned 13.96%, underperforming the Russell 2000 Growth Index by 8.21%. The Small Company Value Portfolio Institutional Class returned 8.97%, outperforming the Russell 2000 Value Index by 1.13%. The Wilshire 5000 IndexSM Fund Institutional Class returned 20.57%, underperforming the Wilshire 5000 Total Market Index by 0.43%. The Wilshire International Equity Fund Institutional Class returned 25.92%, underperforming the MSCI All Country World ex-US Index by 1.27%. The Wilshire Income Opportunities Fund Institutional Class returned 5.84%, outperforming the Bloomberg Barclays US Universal Index by 1.75%. We are pleased with the Funds’ performance for 2017 and we are confident that each Fund is well positioned for future growth.

As always, we sincerely appreciate your continued support and confidence in Wilshire Associates.

Sincerely,

Jason Schwarz

President, Wilshire Mutual Funds

2

Wilshire Mutual Funds, Inc. Letter to Shareholders (Unaudited) - (Continued) | |

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Returns assume reinvestment of all distributions.

Index returns are for illustrative purposes only and do not represent actual Fund performance. Index performance returns do not reflect any management fees, transactions costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise.

In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. Investments in smaller companies typically exhibit higher volatility.

Investing involves risk including loss of principal. This report identifies each Portfolio’s investments on December 31, 2017. These holdings are subject to change. Not all investments in each Portfolio performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across developed markets countries around the world, excluding the U.S. and Canada.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

The Wilshire 5000 Total Market IndexSM is widely accepted as the definitive benchmark for the U.S. equity market, and measures performance of all U.S. equity securities with readily available price data.

3

Large Company Growth Portfolio Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 26.93% |

Five Years Ended 12/31/17 | 14.38% |

Ten Years Ended 12/31/17 | 7.34% |

RUSSELL 1000® GROWTH INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 30.21% |

Five Years Ended 12/31/17 | 17.33% |

Ten Years Ended 12/31/17 | 10.00% |

COMPARATIVE PERFORMANCE

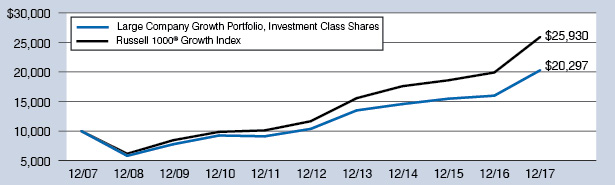

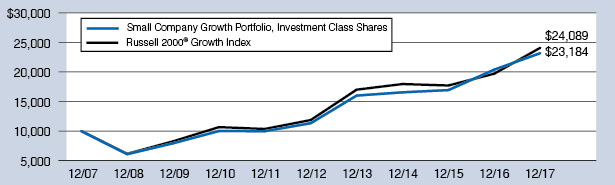

Comparison of Change in Value of $10,000 Investment in Shares of Large Company Growth Portfolio, Investment Class Shares and the Russell 1000® Growth Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| (1) | The Russell 1000® Growth Index is an unmanaged index that measures the performance of the largest 1,000 U.S. companies with higher price-to-book ratios and higher forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

4

Large Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 27.35% |

Five Years Ended 12/31/17 | 14.74% |

Ten Years Ended 12/31/17 | 7.68% |

RUSSELL 1000® GROWTH INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 30.21% |

Five Years Ended 12/31/17 | 17.33% |

Ten Years Ended 12/31/17 | 10.00% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Large Company Growth Portfolio, Institutional Class Shares and the Russell 1000® Growth Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| (1) | The Russell 1000® Growth Index is an unmanaged index that measures the performance of the largest 1,000 U.S. companies with higher price-to-book ratios and higher forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

5

Large Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

The Wilshire 5000 Total Market IndexSM returned 21.0% in 2017 marking the ninth consecutive year of positive gains for the broad US equity market. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink their $4.5T balance sheet starting in October 2017. For the year, growth securities strongly outperformed value stocks and large capitalization stocks outperformed their smaller capitalization counterparts marking a sharp reversal from calendar year 2016 when value meaningfully outperformed growth across market capitalizations.

Sector performance for the Wilshire 5000 Total Market Index was mostly positive for 2017. Renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth. Conversely, Energy (-2.5%) was the worst performing sector. After retracting to start the year, crude oil prices moved higher towards the end of the year pushing above the $60-per-barrel mark by the end of the period. However, weak natural gas prices and concerns about companies’ ability to replace production with new reserves weighed on performance.

The Wilshire Large Company Growth Portfolio Institutional Class returned 27.35% in 2017, underperforming the Russell 1000 Growth Index return of 30.21% by 2.86%. The Portfolio was weighed down by weak stock selection in the Health Care and Industrials sectors as well as an underweight allocation to the Energy sector. Conversely, strong stock selection in the Consumer Staples and Materials sectors helped mitigate relative underperformance.

Despite the Portfolio’s underperformance versus its benchmark, we believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical issues.

6

Large Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

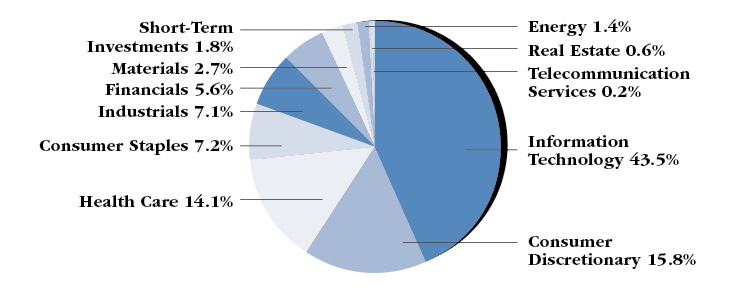

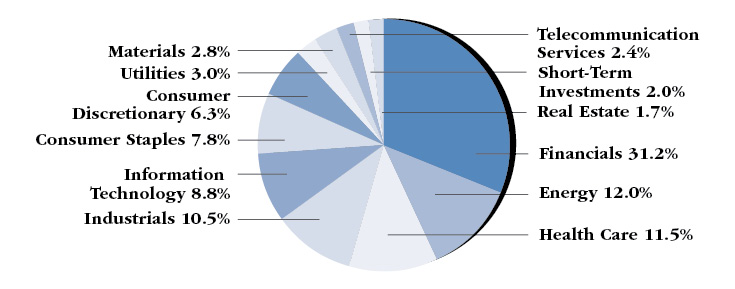

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Portfolio’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

7

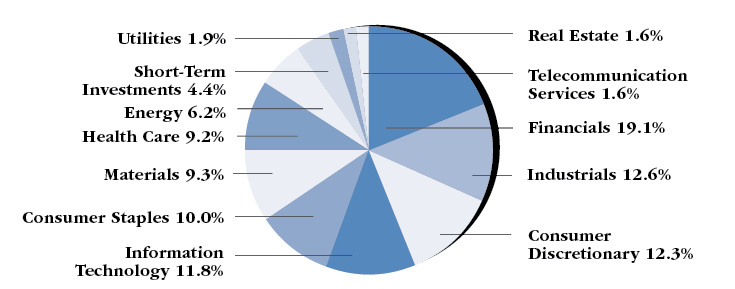

Large Company Value Portfolio Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 14.64% |

Five Years Ended 12/31/17 | 13.69% |

Ten Years Ended 12/31/17 | 6.13% |

RUSSELL 1000® VALUE INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 13.66% |

Five Years Ended 12/31/17 | 14.04% |

Ten Years Ended 12/31/17 | 7.10% |

COMPARATIVE PERFORMANCE

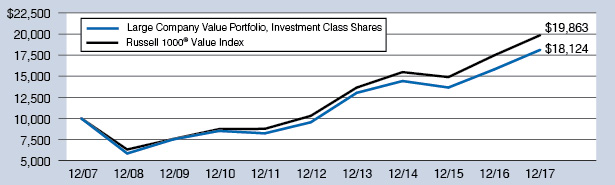

Comparison of Change in Value of $10,000 Investment in Shares of Large Company Value Portfolio, Investment Class Shares and the Russell 1000® Value Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| (1) | The Russell 1000® Value Index is an unmanaged index that measures the performance of the largest 1,000 U.S. companies with lower price-to-book ratios and lower forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

8

Large Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 14.99% |

Five Years Ended 12/31/17 | 13.94% |

Ten Years Ended 12/31/17 | 6.36% |

RUSSELL 1000® VALUE INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 13.66% |

Five Years Ended 12/31/17 | 14.04% |

Ten Years Ended 12/31/17 | 7.10% |

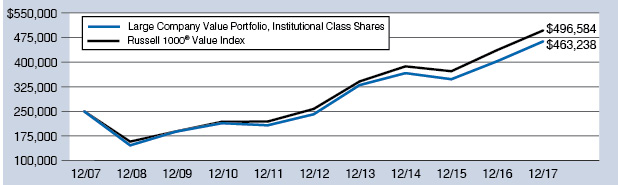

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Large Company Value Portfolio, Institutional Class Shares and the Russell 1000® Value Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| (1) | The Russell 1000® Value Index is an unmanaged index that measures the performance of the largest 1,000 U.S. companies with lower price-to-book ratios and lower forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

9

Large Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

The Wilshire 5000 Total Market IndexSM returned 21.0% in 2017 marking the ninth consecutive year of positive gains for the broad US equity market. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink their $4.5T balance sheet starting in October 2017. For the year, growth securities strongly outperformed value stocks and large capitalization stocks outperformed their smaller capitalization counterparts marking a sharp reversal from calendar year 2016 when value meaningfully outperformed growth across market capitalizations.

Sector performance for the Wilshire 5000 Total Market Index was mostly positive for 2017. Renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth. Conversely, Energy (-2.5%) was the worst performing sector. After retracting to start the year, crude oil prices moved higher towards the end of the year pushing above the $60-per-barrel mark by the end of the period. However, weak natural gas prices and concerns about companies’ ability to replace production with new reserves weighed on performance.

The Wilshire Large Company Value Portfolio Institutional Class returned 14.99% in 2017, outperforming the Russell 1000 Value Index return of 13.66% by 1.33%. The Portfolio benefited from strong stock selection in the Energy, Industrials and Consumer Staples sectors. Conversely, weak stock selection in the Financials and Information Technology sectors detracted from relative performance.

We are pleased with the Portfolio’s outperformance for 2017 and believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical uncertainties.

10

Large Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Portfolio’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

11

Small Company Growth Portfolio Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 13.66% |

Five Years Ended 12/31/17 | 15.39% |

Ten Years Ended 12/31/17 | 8.77% |

RUSSELL 2000® GROWTH INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 22.17% |

Five Years Ended 12/31/17 | 15.21% |

Ten Years Ended 12/31/17 | 9.19% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $10,000 Investment in Shares of Small Company Growth Portfolio, Investment Class Shares and the Russell 2000® Growth Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| * | During the ten years ended December 31, 2017, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements (excluding fees paid indirectly), historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.16% of average net assets. |

| (1) | The Russell 2000® Growth Index is an unmanaged index that measures the performance of the 2,000 smallest U.S. companies with higher price-to-book ratios and higher forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

12

Small Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 13.96% |

Five Years Ended 12/31/17 | 15.70% |

Ten Years Ended 12/31/17 | 9.04% |

RUSSELL 2000® GROWTH INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 22.17% |

Five Years Ended 12/31/17 | 15.21% |

Ten Years Ended 12/31/17 | 9.19% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Small Company Growth Portfolio, Institutional Class Shares and the Russell 2000® Growth Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| * | During the ten years ended December 31, 2017, certain fees and expenses were waived or reimbursed. Without waivers and reimbursements (excluding fees paid indirectly), historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.11% of average net assets. |

| (1) | The Russell 2000® Growth Index is an unmanaged index that measures the performance of the 2,000 smallest U.S. companies with higher price-to-book ratios and higher forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

13

Small Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

The Wilshire 5000 Total Market IndexSM returned 21.0% in 2017 marking the ninth consecutive year of positive gains for the broad US equity market. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink their $4.5T balance sheet starting in October 2017. For the year, growth securities strongly outperformed value stocks and large capitalization stocks outperformed their smaller capitalization counterparts marking a sharp reversal from calendar year 2016 when value meaningfully outperformed growth across market capitalizations.

Sector performance for the Wilshire 5000 Total Market Index was mostly positive for 2017. Renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth. Conversely, Energy (-2.5%) was the worst performing sector. After retracting to start the year, crude oil prices moved higher towards the end of the year pushing above the $60-per-barrel mark by the end of the period. However, weak natural gas prices and concerns about companies’ ability to replace production with new reserves weighed on performance.

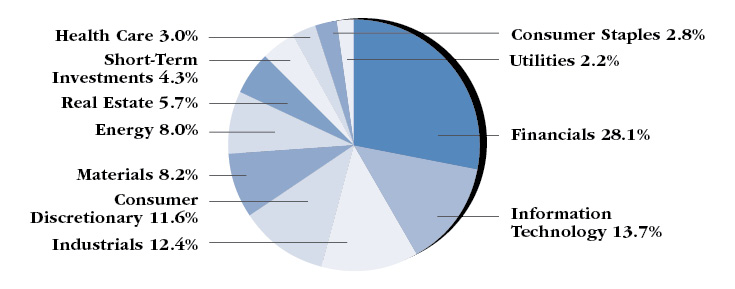

The Wilshire Small Company Growth Portfolio Institutional Class returned 13.96% in 2017, underperforming the Russell 2000 Growth Index return of 22.17% by 8.21%. The Portfolio was weighed down by weak stock selection in the Health Care, Financials, and Consumer Discretionary sectors. Conversely, strong stock selection in the Consumer Staples, Industrials, and Information Technology sectors boosted absolute performance.

Despite the Portfolio’s underperformance versus its benchmark, we believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical issues.

14

Small Company Growth Portfolio Commentary (Unaudited) - (Continued) |

|

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

† | Based on percent of the Portfolio’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

15

Small Company Value Portfolio Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 8.65% |

Five Years Ended 12/31/17 | 14.77% |

Ten Years Ended 12/31/17 | 8.21% |

RUSSELL 2000® VALUE INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 7.84% |

Five Years Ended 12/31/17 | 13.01% |

Ten Years Ended 12/31/17 | 8.17% |

COMPARATIVE PERFORMANCE

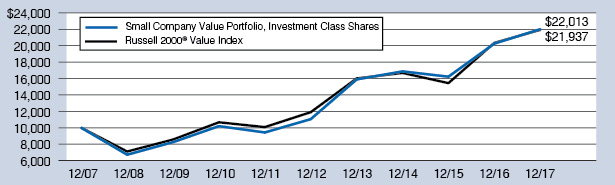

Comparison of Change in Value of $10,000 Investment in Shares of Small Company Value Portfolio, Investment Class Shares and the Russell 2000® Value Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

* | During the ten years ended December 31, 2017, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements (excluding fees paid indirectly), historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.22% of average net assets. |

(1) | The Russell 2000® Value Index is an unmanaged index that measures the performance of the 2,000 smallest U.S. companies with lower price-to-book ratios and lower forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

16

Small Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 8.97% |

Five Years Ended 12/31/17 | 15.10% |

Ten Years Ended 12/31/17 | 8.56% |

RUSSELL 2000® VALUE INDEX(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 7.84% |

Five Years Ended 12/31/17 | 13.01% |

Ten Years Ended 12/31/17 | 8.17% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Small Company Value Portfolio, Institutional Class Shares and the Russell 2000® Value Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or the redemption of Portfolio shares.

| * | During the ten years ended December 31, 2017, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements (excluding fees paid indirectly), historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.16% of average net assets. |

| (1) | The Russell 2000® Value Index is an unmanaged index that measures the performance of the 2,000 smallest U.S. companies with lower price-to-book ratios and lower forecasted growth values. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

17

Small Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

The Wilshire 5000 Total Market IndexSM returned 21.0% in 2017 marking the ninth consecutive year of positive gains for the broad US equity market. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink their $4.5T balance sheet starting in October 2017. For the year, growth securities strongly outperformed value stocks and large capitalization stocks outperformed their smaller capitalization counterparts marking a sharp reversal from calendar year 2016 when value meaningfully outperformed growth across market capitalizations.

Sector performance for the Wilshire 5000 Total Market Index was mostly positive for 2017. Renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth. Conversely, Energy (-2.5%) was the worst performing sector. After retracting to start the year, crude oil prices moved higher towards the end of the year pushing above the $60-per-barrel mark by the end of the period. However, weak natural gas prices and concerns about companies’ ability to replace production with new reserves weighed on performance.

The Wilshire Small Company Value Portfolio Institutional Class returned 8.97% in 2017, outperforming the Russell 2000 Value Index return of 7.84% by 1.13%. The Portfolio benefited from strong selection in the Information Technology and Materials sectors. Conversely, weak stock selection in the Consumer Staples sector as well as an underweight allocation to Health Care detracted from relative performance.

We are pleased with the Portfolio’s outperformance for 2017 and believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical uncertainties.

18

Small Company Value Portfolio Commentary (Unaudited) - (Continued) |

|

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Portfolio’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

19

Wilshire 5000 Indexsm Fund Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 20.20% |

Five Years Ended 12/31/17 | 14.98% |

Ten Years Ended 12/31/17 | 8.00% |

WILSHIRE 5000 INDEXSM(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 21.00% |

Five Years Ended 12/31/17 | 15.67% |

Ten Years Ended 12/31/17 | 8.64% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $10,000 Investment in Shares of Wilshire 5000 IndexSM Fund, Investment Class Shares and the Wilshire 5000 IndexSM through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| (1) | The Wilshire 5000 IndexSM is an unmanaged index that measures the performance of all U.S. headquartered equity securities with readily available price data. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

20

Wilshire 5000 Indexsm Fund Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 20.57% |

Five Years Ended 12/31/17 | 15.28% |

Ten Years Ended 12/31/17 | 8.25% |

WILSHIRE 5000 INDEXSM(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 21.00% |

Five Years Ended 12/31/17 | 15.67% |

Ten Years Ended 12/31/17 | 8.64% |

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Wilshire 5000 IndexSM Fund, Institutional Class Shares and the Wilshire 5000 IndexSM through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| (1) | The Wilshire 5000 IndexSM is an unmanaged index that measures the performance of all U.S. headquartered equity securities with readily available price data. Index performance is presented for general comparative purposes. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot directly invest in any index. |

21

Wilshire 5000 Indexsm Fund Commentary (Unaudited) - (Continued) |

|

The Wilshire 5000 Total Market IndexSM returned 21.0% in 2017 marking the ninth consecutive year of positive gains for the broad US equity market. Several factors contributed to this success, including a rebound in global economic growth and continued strength domestically. Investors also responded positively to the largest overhaul of the US tax system in 30 years. What also made the past year particularly impressive was the relative lack of volatility. The largest drawdown for the year was -2.75%, and there were only four trading days where the market was down 1% or more, making 2017 one of the least volatile years in nearly four decades. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink their $4.5T balance sheet starting in October 2017. For the year, growth securities strongly outperformed value stocks and large capitalization stocks outperformed their smaller capitalization counterparts marking a sharp reversal from calendar year 2016 when value meaningfully outperformed growth across market capitalizations.

Sector performance for the Wilshire 5000 Total Market Index was mostly positive for 2017. Renewed enthusiasm over long-term growth prospects and strong earnings growth expectations drove Information Technology (+37.4%) and Health Care (+23.9%) higher. Materials (+24.2%) and Industrials (+22.1%) also had strong performance on a brighter outlook for global economic growth. Conversely, Energy (-2.5%) was the worst performing sector. After retracting to start the year, crude oil prices moved higher towards the end of the year pushing above the $60-per-barrel mark by the end of the period. However, weak natural gas prices and concerns about companies’ ability to replace production with new reserves weighed on performance.

The Wilshire 5000 Index Fund Institutional Class returned 20.57% in 2017, underperforming the Wilshire 5000 Index return of 21.00% by 0.43%. Underperformance is attributable to Portfolio expenses and is well within the range of historical experiences.

22

Wilshire 5000 Indexsm Fund Commentary (Unaudited) - (Continued) |

|

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Fund’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

23

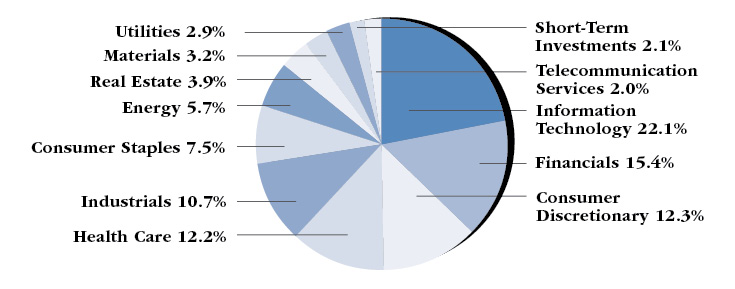

Wilshire International Equity Fund Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 25.54% |

Five Years Ended 12/31/17 | 6.99% |

Ten Years Ended 12/31/17 | 2.40% |

MSCI ALL COUNTRY WORLD INDEX EX-U.S.(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 27.19% |

Five Years Ended 12/31/17 | 6.80% |

Ten Years Ended 12/31/17 | 1.84% |

On April 2, 2013, the Wilshire International Equity Fund’s investment strategy was changed. Consequently, prior period performance may have been different if the new investment strategy had been in effect during these periods.

| * | During the ten years ended December 31, 2017, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements, historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.04% of average net assets. |

| (1) | The MSCI All Country World Ex-U.S. Index is an unmanaged capitalization-weighted measure of stock markets of developed and emerging markets, with the exception of U.S.-based companies. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot invest directly in an index. Index performance is presented for general comparative purposes. |

24

Wilshire International Equity Fund Commentary (Unaudited) - (Continued) |

|

COMPARATIVE PERFORMANCE

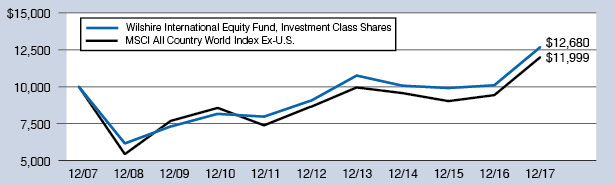

Comparison of Change in Value of $10,000 Investment in Shares of Wilshire International Equity Fund, Investment Class Shares and the MSCI All Country World Index Ex-U.S. through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

25

Wilshire International Equity Fund Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 25.92% |

Five Years Ended 12/31/17 | 7.24% |

Ten Years Ended 12/31/17 | 2.67% |

MSCI ALL COUNTRY WORLD INDEX EX-U.S.(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 27.19% |

Five Years Ended 12/31/17 | 6.80% |

Ten Years Ended 12/31/17 | 1.84% |

On April 2, 2013, the Wilshire International Equity Fund’s investment strategy was changed. Consequently, prior period performance may have been different if the new investment strategy had been in effect during these periods.

| * | During the ten years ended December 31, 2017, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements, historical total returns would have been lower. For the year ended December 31, 2017, the investment adviser did not reduce its fees or reimburse expenses. |

| (1) | The MSCI All Country World Ex-U.S. Index is an unmanaged capitalization-weighted measure of stock markets of developed and emerging markets, with the exception of U.S.-based companies. Unlike a mutual fund, the performance of an index assumes no transaction costs, management fees or other expenses. An individual cannot invest directly in an index. Index performance is presented for general comparative purposes. |

26

Wilshire International Equity Fund Commentary (Unaudited) - (Continued) |

|

COMPARATIVE PERFORMANCE

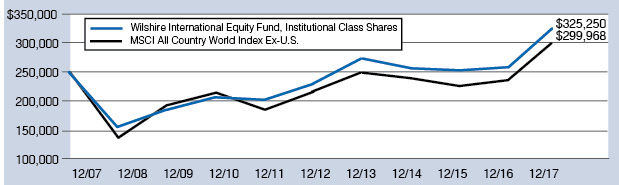

Comparison of Change in Value of $250,000 Investment in Shares of Wilshire International Equity Fund, Institutional Class Shares and the MSCI All Country World Index Ex-U.S. through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

27

Wilshire International Equity Fund Commentary (Unaudited) - (Continued) |

|

Markets rallied in 2017 behind synchronized global growth, strong corporate earnings growth, improved investor sentiment and signs of diminishing political risks globally. After four years lagging US equities, international equities outperformed US equities during the year with the MSCI ACWI ex US Index returning 27.2%. The US dollar weakened in 2017, providing a boost for US investors holding foreign currencies – the MSCI ACWI ex US Index in local currency terms returned 18.2%. The first half of the year was marked by increasing political risks as the U.K. officially triggered Article 50 launching the process to formally withdraw from the European Union and centrist Emmanuel Macron defeated anti-European Union nationalist Marine Le Pen in the French presidential election. The second half of the year saw rising political tensions in North Korea, however the market advanced higher amidst these concerns. In the third quarter investors cheered the re-election of German Chancellor Angela Merkel as she won her fourth term in office. For the second year in a row, emerging markets outpaced foreign developed markets with the MSCI Emerging Markets Index returning 37.3%, largely driven by a weakening US dollar, strong profits from technology companies, strengthening global economy and rising commodities prices. 2017’s return was the strongest year for broad emerging markets equity since they recovered from the global financial crisis in 2009.

All sectors of the MSCI ACWI ex US Index had positive performance in 2017. Information Technology (+50.5%) was the top performing sector lead by securities such as Chinese companies Alibaba Group and Tencent Holdings as well as Samsung Electronics (South Korea) and Nintendo (Japan). Materials (+32.6%) and Industrials (29.8%) also performed well as most commodities prices advanced for the year. Additionally, Energy closed out the second half of the year strong after being the worst performing, and only negatively returning, sector in the first half of the year. Energy returned 21.5% over the last six months of 2017 and 17.3% for the year.

The Wilshire International Equity Fund Institutional Class returned 25.92% in 2017, underperforming the MSCI ACWI ex US Index return of 27.19% by 1.27%. The Portfolio was weighed down by weak stock selection in the Consumer Discretionary and Industrials sectors and regionally within Japan. Additionally, an underweight allocation to emerging markets hurt performance. Conversely, strong stock selection in the Health Care and Materials sectors and regionally within Hong Kong and Australia helped mitigate relative underperformance.

Despite the Portfolio’s underperformance versus its benchmark, we believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical issues.

28

Wilshire International Equity Fund Commentary (Unaudited) - (Continued) |

|

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Fund’s total investments in securities at value. Includes investments held as collateral for securities on loan (see Note 7 in Notes to Financial Statements). |

29

Wilshire Income Opportunities Fund Commentary (Unaudited) |

|

INVESTMENT CLASS SHARES

Average Annual Total Returns*

One Year Ended 12/31/17 | 5.60% |

Inception (03/30/16) through 12/31/17 | 5.43% |

Bloomberg Barclays U.S. Universal Index(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 4.09% |

Inception (03/30/16) through 12/31/17 | 2.92% |

| * | During certain periods since inception, certain fees and expenses were reduced or reimbursed. Without fee reductions and expense reimbursements, historical returns would have been lower. For the year ended December 31, 2017, the investment adviser reduced its fees or reimbursed expenses in the amount of 0.06% of average net assets. |

| (1) | The Bloomberg Barclays U.S. Universal Index represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index. The index covers USD-denominated, taxable bonds that are rated either investment grade or high-yield. Some U.S. Universal Index constituents may be eligible for one or more of its contributing subcomponents that are not mutually exclusive. The Bloomberg Barclays U.S. Universal Index includes Treasury securities, Government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in U.S. |

30

Wilshire Income Opportunities Fund Commentary (Unaudited) - (Continued) |

|

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $10,000 Investment in Shares of Wilshire Income Opportunities Fund, Investment Class Shares and the Bloomberg Barclays U.S. Universal Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

31

Wilshire Income Opportunities Fund Commentary (Unaudited) - (Continued) |

|

INSTITUTIONAL CLASS SHARES

Average Annual Total Returns

One Year Ended 12/31/17 | 5.84% |

Inception (03/30/16) through 12/31/17 | 5.52% |

Bloomberg Barclays U.S. Universal Index(1)

Average Annual Total Returns

One Year Ended 12/31/17 | 4.09% |

Inception (03/30/16) through 12/31/17 | 2.92% |

| (1) | The Bloomberg Barclays U.S. Universal Index represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index. The index covers USD-denominated, taxable bonds that are rated either investment grade or high-yield. Some U.S. Universal Index constituents may be eligible for one or more of its contributing subcomponents that are not mutually exclusive. The Bloomberg Barclays U.S. Universal Index includes Treasury securities, Government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in U.S. |

32

Wilshire Income Opportunities Fund Commentary (Unaudited) - (Continued) |

|

COMPARATIVE PERFORMANCE

Comparison of Change in Value of $250,000 Investment in Shares of Wilshire Income Opportunities Fund, Institutional Class Shares and the Bloomberg Barclays U.S. Universal Index through 12/31/17.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month end may be obtained at http://advisor.wilshire.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. The table above does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

33

Wilshire Income Opportunities Fund Commentary (Unaudited) - (Continued) |

|

The US fixed income market was positive for 2017 with the Bloomberg Barclays US Aggregate Bond Index returning 3.5%. Investment grade corporate securities led the rally during the year as credit overall did well over the period. The ICE Bank of America US High Yield Index returned 4.5% as spreads continued to tighten and remain near historical lows. Reflecting an improved outlook for growth, the Federal Reserve pushed forward with its plan to normalize short-term interest rates and raised the federal funds rate by 0.25% at its March, June and December meetings of its Federal Open Market Committee increasing the overnight rate to a range of 1.25% to 1.50% by the end of 2017. Additionally, the Federal Open Market Committee began to shrink its $4.5T balance sheet starting in October 2017. During the first quarter, anticipation for quick and swift fiscal policy reforms from the Trump Administration fueled Treasury yields higher and the 10 Year US Treasury yield peaked at just over 2.60% in mid-March before falling to end the first quarter. The US Treasury curve continued to flatten over the remainder of the year with the bellwether 10-year Treasury yield ending the year at 2.40%, up slightly but approximately equal to year-end 2016. Globally, continued accommodative monetary policy, a weaker US Dollar, positive economic outlooks and subdued inflation boosted global fixed income. The Bloomberg Barclays Global Aggregate ex US Index returned 10.5% for the year.

The Wilshire Income Opportunities Fund Institutional Class returned 5.84% for the year, outperforming the Bloomberg Barclays US Universal Index return of 4.09%. Positive yield carry, spread compression, particularly in RMBS, and positioning in high yield and investment grade corporates boosted overall performance. Holdings in bank loans weighed on performance for the period.

We are pleased with the Portfolio’s outperformance for 2017 and believe the Portfolio is well positioned going into 2018 as the market deals with ongoing macroeconomic and geopolitical uncertainties.

34

Wilshire Income Opportunities Fund Commentary (Unaudited) - (Continued) |

|

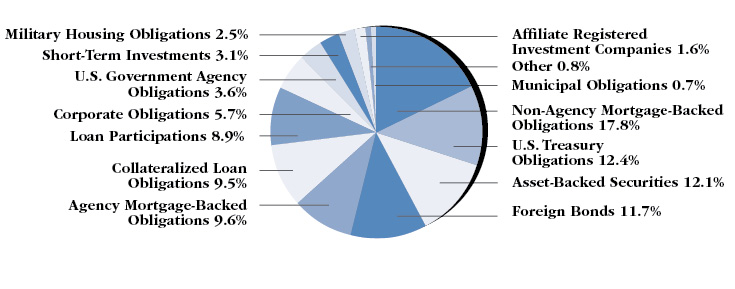

PORTFOLIO SECTOR WEIGHTING†

(As of December 31, 2017)

| † | Based on percent of the Fund’s total investments in securities at value. |

35

Wilshire Mutual Funds, Inc. Disclosure of Fund Expenses (Unaudited) |

|

All mutual funds have operating expenses. As a shareholder of a portfolio (or a “fund”), you incur ongoing costs, which include costs for investment advisory, administrative services, distribution and/or shareholder services and shareholder reports (like this one), among others. Operating expenses, which are deducted from a fund’s gross income, directly reduce the investment return of the fund. A fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing fees (in dollars) of investing in the Portfolios and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period and held for the entire period from July 1, 2017 to December 31, 2017.

The table on the next page illustrates the Portfolios’ costs in two ways:

Actual Fund Return: This section helps you to estimate the actual expenses, after any applicable fee waivers, that you paid over the period. The “Ending Account Value” shown is derived from each Portfolio’s actual return for the period. The “Expense Ratio” column shows the period’s annualized expense ratio and the “Expenses Paid During Period” column shows the dollar amount that would have been paid by an investor who started with $1,000 in the Portfolios at the beginning of the period.

You may use the information here, together with your account value, to estimate the expenses that you paid over the period. To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Portfolio in the first line under the heading entitled “Expenses Paid During Period.”

Hypothetical 5% Return: This section is intended to help you compare the Portfolios’ costs with those of other mutual funds. The “Ending Account Value” shown is derived from hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and assumed rate of return. It assumes that each Portfolio had an annual return of 5% before expenses, but that the expense ratio is unchanged. In this case, because the return used is not each Portfolio’s actual return, the results do not apply to your investment. This example is useful in making comparisons to other mutual funds because the Securities and Exchange Commission (“SEC”) requires all mutual funds to calculate expenses based on an assumed 5% annual return. You can assess the Portfolios’ ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare your ongoing costs only and do not reflect any transactional costs such as sales charges (loads), redemption fees, or exchange fees. Wilshire Mutual Funds, Inc. has no such charges, but these may be present in other funds to which you compare this data. Therefore, the hypothetical portions of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

36

Wilshire Mutual Funds, Inc. Disclosure of Fund Expenses (Unaudited) - (Continued) |

|

| | Beginning

Account

Value

07/01/2017 | Ending

Account

Value

12/31/2017 | Net

Expense

Ratio(1) | Expenses Paid

During Period

07/01/17-12/31/17(2) |

Large Company Growth Portfolio |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,108.30 | 1.29% | $ 6.86 |

Institutional Class | $ 1,000.00 | $ 1,110.00 | 0.97% | $ 5.16 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,018.70 | 1.29% | $ 6.56 |

Institutional Class | $ 1,000.00 | $ 1,020.32 | 0.97% | $ 4.94 |

Large Company Value Portfolio |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,095.40 | 1.25% | $ 6.60 |

Institutional Class | $ 1,000.00 | $ 1,096.60 | 0.98% | $ 5.18 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 |

Institutional Class | $ 1,000.00 | $ 1,020.27 | 0.98% | $ 4.99 |

Small Company Growth Portfolio |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,079.20 | 1.47% | $ 7.70 |

Institutional Class | $ 1,000.00 | $ 1,080.60 | 1.20% | $ 6.29 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,017.80 | 1.47% | $ 7.48 |

Institutional Class | $ 1,000.00 | $ 1,019.16 | 1.20% | $ 6.11 |

Small Company Value Portfolio |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,095.20 | 1.43% | $ 7.55 |

Institutional Class | $ 1,000.00 | $ 1,097.00 | 1.17% | $ 6.18 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,018.00 | 1.43% | $ 7.27 |

Institutional Class | $ 1,000.00 | $ 1,019.31 | 1.17% | $ 5.96 |

37

Wilshire Mutual Funds, Inc. Disclosure of Fund Expenses (Unaudited) - (Continued) |

|

| | Beginning

Account

Value

07/01/2017 | Ending

Account

Value

12/31/2017 | Net

Expense

Ratio(1) | Expenses Paid

During Period

07/01/17-12/31/17(2) |

Wilshire 5000 IndexSM Fund |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,109.60 | 0.61% | $ 3.24 |

Institutional Class | $ 1,000.00 | $ 1,110.80 | 0.32% | $ 1.70 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,022.13 | 0.61% | $ 3.11 |

Institutional Class | $ 1,000.00 | $ 1,023.59 | 0.32% | $ 1.63 |

Wilshire International Equity Fund |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,102.20 | 1.51% | $ 8.00 |

Institutional Class | $ 1,000.00 | $ 1,103.80 | 1.26% | $ 6.68 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,017.59 | 1.51% | $ 7.68 |

Institutional Class | $ 1,000.00 | $ 1,018.85 | 1.26% | $ 6.41 |

Wilshire Income Opportunities Fund |

Based on Actual Fund Return | | | | |

Investment Class | $ 1,000.00 | $ 1,019.80 | 1.16% | $ 5.91 |

Institutional Class | $ 1,000.00 | $ 1,020.10 | 0.96% | $ 4.89 |

Based on Hypothetical 5% Return | | | | |

Investment Class | $ 1,000.00 | $ 1,019.36 | 1.16% | $ 5.90 |

Institutional Class | $ 1,000.00 | $ 1,020.37 | 0.96% | $ 4.89 |

| (1) | Annualized, based on the Portfolio’s most recent fiscal half-year expenses. |

| (2) | Expenses are equal to the Portfolio’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

38

Wilshire Mutual Funds, Inc. Large Company Growth Portfolio Condensed Schedule of Investments | December 31, 2017 |

|

| | | Shares | | | Value | |

| COMMON STOCKS — 98.9% (a) |

| Consumer Discretionary — 15.9% |

| Amazon.com, Inc. (b) | | | 11,301 | | | $ | 13,216,181 | |

| Priceline Group, Inc. (The) (b) | | | 1,965 | | | | 3,414,659 | |

| Starbucks Corp. | | | 40,875 | | | | 2,347,452 | |

| TJX Cos., Inc. (The) | | | 32,400 | | | | 2,477,304 | |

| Ulta Beauty, Inc. (b) | | | 9,425 | | | | 2,107,996 | |

| Yum! Brands, Inc. | | | 25,902 | | | | 2,113,863 | |

| Other Securities (c) (d) | | | | | | | 11,638,801 | |

| | | | | | | | 37,316,256 | |

| Consumer Staples — 7.2% | | | | | | | | |

| Coca-Cola Co. (The) | | | 61,907 | | | | 2,840,293 | |

| Danone S.A. - ADR (d) | | | 169,441 | | | | 2,841,526 | |

| Monster Beverage Corp. (b) | | | 107,045 | | | | 6,774,878 | |

| Procter & Gamble Co. (The) | | | 25,655 | | | | 2,357,182 | |

| Other Securities (c) (d) | | | | | | | 2,154,018 | |

| | | | | | | | 16,967,897 | |

| Energy — 1.5% | | | | | | | | |

| Schlumberger Ltd. | | | 40,815 | | | | 2,750,522 | |

| Other Securities (c) | | | | | | | 672,579 | |

| | | | | | | | 3,423,101 | |

| Financials — 5.7% | | | | | | | | |

| Charles Schwab Corp. (The) | | | 35,300 | | | | 1,813,361 | |

| First Republic Bank | | | 22,650 | | | | 1,962,396 | |

| Goldman Sachs Group, Inc. (The) | | | 6,725 | | | | 1,713,261 | |

| SEI Investments Co. | | | 39,931 | | | | 2,869,441 | |

| Other Securities (c) | | | | | | | 4,950,357 | |

| | | | | | | | 13,308,816 | |

| Health Care — 14.1% | | | | | | | | |

| Alexion Pharmaceuticals, Inc. (b) | | | 15,625 | | | | 1,868,594 | |

| Align Technology, Inc. (b) | | | 13,933 | | | | 3,095,773 | |

| Celgene Corp. (b) | | | 19,035 | | | | 1,986,493 | |

| Cerner Corp. (b) | | | 27,458 | | | | 1,850,395 | |

| Edwards Lifesciences Corp. (b) | | | 20,875 | | | | 2,352,821 | |

| Novartis AG - ADR | | | 18,777 | | | | 1,576,517 | |

| Novo Nordisk A/S - ADR | | | 54,960 | | | | 2,949,702 | |

| Regeneron Pharmaceuticals, Inc. (b) | | | 6,163 | | | | 2,317,040 | |

| Varian Medical Systems, Inc. (b) | | | 17,425 | | | | 1,936,789 | |

| Zoetis, Inc. | | | 33,025 | | | | 2,379,121 | |

| Other Securities (c) | | | | | | | 10,911,108 | |

| | | | | | | | 33,224,353 | |

| Industrials — 7.1% | | | | | | | | |

| CSX Corp. | | | 41,375 | | | | 2,276,039 | |

| Deere & Co. | | | 21,839 | | | | 3,418,021 | |

| Expeditors International of Washington, Inc. | | | 38,512 | | | | 2,491,342 | |

| United Parcel Service, Inc. - Class B | | | 16,435 | | | | 1,958,230 | |

| Other Securities (c) | | | | | | | 6,622,250 | |

| | | | | | | | 16,765,882 | |

| Information Technology — 43.8% |

| Activision Blizzard, Inc. | | | 42,805 | | | | 2,710,413 | |

| Adobe Systems, Inc. (b) | | | 12,215 | | | | 2,140,557 | |

| Alibaba Group Holding Ltd. - ADR (b) (d) | | | 31,128 | | | | 5,367,401 | |

| Alphabet, Inc. - Class A (b) | | | 4,148 | | | | 4,369,503 | |

| Alphabet, Inc. - Class C (b) | | | 8,154 | | | | 8,532,346 | |

| Apple, Inc. | | | 33,932 | | | | 5,742,312 | |

| Applied Materials, Inc. | | | 45,175 | | | | 2,309,346 | |

| Arista Networks, Inc. (b) | | | 8,325 | | | | 1,961,204 | |

| Autodesk, Inc. (b) | | | 28,897 | | | | 3,029,273 | |

| Cisco Systems, Inc. | | | 110,305 | | | | 4,224,681 | |

| Cognex Corp. | | | 35,350 | | | | 2,162,006 | |

| Facebook, Inc. - Class A (b) | | | 73,137 | | | | 12,905,755 | |

| Microsoft Corp. | | | 74,840 | | | | 6,401,813 | |

| NVIDIA Corp. | | | 11,906 | | | | 2,303,811 | |

| Oracle Corp. | | | 95,569 | | | | 4,518,501 | |

| PayPal Holdings, Inc. (b) | | | 41,285 | | | | 3,039,402 | |

| QUALCOMM, Inc. | | | 43,396 | | | | 2,778,211 | |

| Red Hat, Inc. (b) | | | 26,125 | | | | 3,137,612 | |

| Salesforce.com, Inc. (b) | | | 23,465 | | | | 2,398,827 | |

| ServiceNow, Inc. (b) | | | 11,950 | | | | 1,558,161 | |

| Visa, Inc. - Class A (d) | | | 84,725 | | | | 9,660,344 | |

| Other Securities (c) (d) | | | | | | | 11,643,555 | |

| | | | | | | | 102,895,034 | |

| Materials — 2.8% | | | | | | | | |

| Sherwin-Williams Co. (The) | | | 6,500 | | | | 2,665,260 | |

| Other Securities (c) (d) | | | | | | | 3,779,906 | |

| | | | | | | | 6,445,166 | |

| Real Estate — 0.6% | | | | | | | | |

| Other Securities (c) | | | | | | | 1,367,480 | |

| | | | | | | | | |

| Telecommunication Services — 0.2% | | | | | | | | |

| Other Securities (c) | | | | | | | 427,621 | |

| | | | | | | | | |

| Utilities — 0.0% (e) | | | | | | | | |

| Other Securities (c) | | | | | | | 17,658 | |

| | | | | | | | | |

| Total Common Stocks (Cost $148,649,726) | | | | | | | 232,159,264 | |

See Notes to Financial Statements.

39

Wilshire Mutual Funds, Inc. Large Company Growth Portfolio Condensed Schedule of Investments - (Continued) | December 31, 2017 |

|

| | | Shares | | | Value | |

| MONEY MARKET FUNDS — 1.8% | | | |

| Northern Trust Institutional Government Select Portfolio - Institutional Class, 1.13% (f) | | | 2,635,435 | | | $ | 2,635,435 | |

| Northern Trust Institutional Liquid Asset Portfolio - Institutional Class, 1.09% (f) (g) | | | 1,614,019 | | | | 1,614,019 | |

| | | | | | | | | |

| Total Money Market Funds (Cost $4,249,454) | | | | | | | 4,249,454 | |

| | | | | | | | | |

| Total Investments at Value — 100.7% (Cost $152,899,180) | | | | | | | 236,408,718 | |

| | | | | | | | | |

| Liabilities in Excess of Other Assets — (0.7%) | | | | | | | (1,570,391 | ) |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 234,838,327 | |

The Condensed Schedule of Investments does not reflect the complete portfolio holdings. It includes the Portfolio’s 50 largest holdings and each investment of any issue that exceeds 1% of the Portfolio’s net assets. “Other Securities” represent all issues not required to be disclosed under the rules adopted by the U.S. Securities and Exchange commission (“SEC”). The complete schedule of portfolio holdings is available (i) without charge, upon request, by calling (800)607-2200; (ii) on the SEC’s website at http://www.sec.gov; and (iii) on our website at http://advisor.wilshire.com.

ADR — American Depositary Receipt.

(a) | More narrow industries are utilized for compliance purposes, whereas broad sectors are utilized for reporting purposes. |

(b) | Non-income producing security. |

(c) | Represents issuers not identified as a top 50 holding in terms of market value and issues or issuers not exceeding 1% of net assets individually or in the aggregate, respectively, as of December 31, 2017. |

(d) | This security or a partial position of this security is on loan at December 31, 2017. The total value of securities on loan at December 31, 2017 was $15,985,353 (Note 7). |

(e) | Percentage rounds to less than 0.1%. |

(f) | The rate shown is the 7-day effective yield as of December 31, 2017. |

(g) | This security was purchased with cash collateral held from securities on loan. The total value of such securities as of December 31, 2017 was $1,614,019. Securities on loan are also collateralized by various U.S. Treasury obligations in the amount of $14,796,474 (Note 7). |

See Notes to Financial Statements.

40

Wilshire Mutual Funds, Inc. Large Company Value Portfolio Condensed Schedule of Investments | December 31, 2017 |

|

| | | Shares | | | Value | |

| COMMON STOCKS — 97.9% (a) |

| Consumer Discretionary — 6.3% |

| Omnicom Group, Inc. | | | 17,637 | | | $ | 1,284,502 | |

| Target Corp. (b) | | | 16,600 | | | | 1,083,149 | |

| Other Securities (b) (c) | | | | | | | 7,592,608 | |

| | | | | | | | 9,960,259 | |

| Consumer Staples — 7.8% | | | | | | | | |

| Altria Group, Inc. | | | 22,800 | | | | 1,628,148 | |

| CVS Health Corp. | | | 19,395 | | | | 1,406,138 | |

| Philip Morris International, Inc. | | | 23,706 | | | | 2,504,539 | |

| Wal-Mart Stores, Inc. | | | 37,643 | | | | 3,717,246 | |

| Other Securities (b) (c) | | | | | | | 3,107,644 | |

| | | | | | | | 12,363,715 | |

| Energy — 12.0% | | | | | | | | |

| BP plc - ADR | | | 75,697 | | | | 3,181,544 | |

| Chevron Corp. | | | 14,999 | | | | 1,877,725 | |

| ConocoPhillips | | | 26,697 | | | | 1,465,398 | |

| Exxon Mobil Corp. | | | 35,958 | | | | 3,007,527 | |

| Halliburton Co. | | | 21,916 | | | | 1,071,035 | |

| Occidental Petroleum Corp. | | | 22,400 | | | | 1,649,984 | |

| Phillips 66 | | | 17,600 | | | | 1,780,240 | |

| Royal Dutch Shell plc - Class A - ADR (b) | | | 35,705 | | | | 2,381,881 | |

| Other Securities (b) (c) | | | | | | | 2,545,648 | |

| | | | | | | | 18,960,982 | |

| Financials — 31.2% | | | | | | | | |

| American Express Co. | | | 21,068 | | | | 2,092,263 | |

| American International Group, Inc. | | | 23,065 | | | | 1,374,213 | |

| Bank of America Corp. | | | 164,175 | | | | 4,846,446 | |

| Berkshire Hathaway, Inc. - Class B (d) | | | 6,282 | | | | 1,245,219 | |

| Capital One Financial Corp. | | | 19,481 | | | | 1,939,918 | |

| Citigroup, Inc. | | | 32,621 | | | | 2,427,329 | |

| Franklin Resources, Inc. | | | 38,834 | | | | 1,682,677 | |

| Goldman Sachs Group, Inc. (The) | | | 5,810 | | | | 1,480,156 | |

| JPMorgan Chase & Co. | | | 50,843 | | | | 5,437,149 | |

| Loews Corp. | | | 28,000 | | | | 1,400,840 | |

| MetLife, Inc. | | | 21,133 | | | | 1,068,484 | |

| Morgan Stanley | | | 25,386 | | | | 1,332,003 | |

| State Street Corp. | | | 25,529 | | | | 2,491,886 | |

| UBS Group AG (b) | | | 57,466 | | | | 1,056,800 | |

| Voya Financial, Inc. | | | 24,747 | | | | 1,224,234 | |

| Wells Fargo & Co. | | | 72,054 | | | | 4,371,516 | |

| XL Group Ltd. | | | 51,619 | | | | 1,814,925 | |

| Other Securities (b) (c) | | | | | | | 12,117,477 | |

| | | | | | | | 49,403,535 | |

| Health Care — 11.5% | | | | | | | | |

| Cigna Corp. | | | 6,106 | | | | 1,240,068 | |

| Express Scripts Holding Co. (d) | | | 17,200 | | | | 1,283,808 | |

| Johnson & Johnson | | | 21,465 | | | | 2,999,090 | |

| McKesson Corp. | | | 6,935 | | | | 1,081,513 | |

| Merck & Co., Inc. | | | 50,811 | | | | 2,859,135 | |

| Mylan N.V. (d) | | | 37,572 | | | | 1,589,671 | |

| Pfizer, Inc. | | | 110,487 | | | | 4,001,839 | |

| Other Securities (c) | | | | | | | 3,234,508 | |

| | | | | | | | 18,289,632 | |

| Industrials — 10.5% | | | | | | | | |

| Dover Corp. | | | 14,222 | | | | 1,436,280 | |

| Johnson Controls International plc | | | 40,216 | | | | 1,532,632 | |

| Southwest Airlines Co. | | | 20,300 | | | | 1,328,635 | |

| Stanley Black & Decker, Inc. | | | 14,038 | | | | 2,382,108 | |

| United Technologies Corp. | | | 16,205 | | | | 2,067,271 | |

| Other Securities (c) | | | | | | | 7,900,707 | |