UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-07338

Capital World Growth and Income Fund, Inc.

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: November 30

Date of reporting period: November 30, 2012

Vincent P. Corti

Capital World Growth and Income Fund, Inc.

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

Copies to:

Kathryn A. Sanders

O’Melveny & Myers LLP

400 South Hope Street, 10th Floor

Los Angeles, California 90071

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

Capital World Growth

and Income Fund®

Special feature

Far and wide: pursuing value in a low-growth world

See page 6

Annual report for the year ended November 30 , 2012

Capital World Growth and Income Fund seeks long-term growth of capital while providing current income. It invests on a global basis in a diversified portfolio consisting primarily of common stocks and other equity securities.

This fund is one of more than 40 offered by American Funds, which is one of the nation’s largest mutual fund families. For more than 80 years, Capital Research and Management Company,SM the American Funds adviser, has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

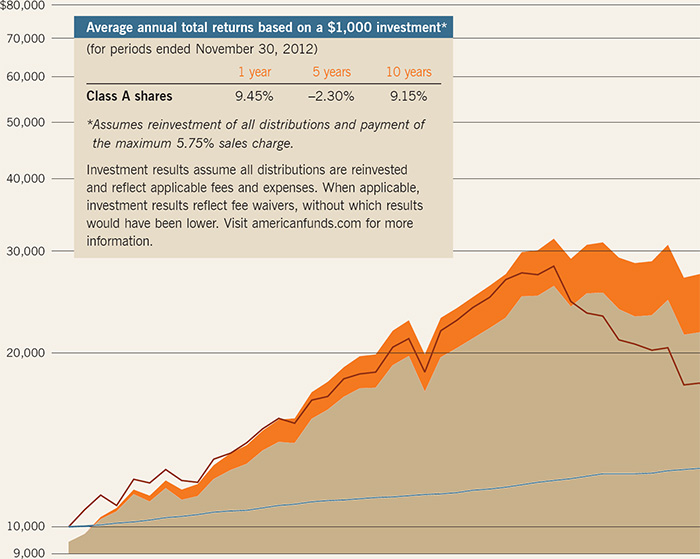

Here are the average annual total returns on a $1,000 investment with all distributions reinvested for periods ended December 31, 2012 (the most recent calendar quarter-end):

| | | | | | | | |

| Class A shares | | 1 year | | 5 years | | 10 years | |

| | | | | | | | |

| Reflecting 5.75% maximum sales charge | | 12.27% | | –1.84% | | 9.58% | |

The total annual fund operating expense ratio is 0.82% for Class A shares as of the prospectus dated February 1, 2013 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

The fund’s 30-day yield for Class A shares as of December 31, 2012, reflecting the 5.75% maximum sales charge and calculated in accordance with the U.S. Securities and Exchange Commission formula, was 2.18%.

Results for other share classes can be found on page 31.

Investing outside the United States may be subject to risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Fellow investors:

Global equity markets rallied during the second half of Capital World Growth and Income Fund’s fiscal year despite considerable volatility, uncertainty over fiscal problems in Europe and the United States, and a slowdown in China. The fund overcame a sluggish first half to produce a strong return for the full 12 months.

For the year ended November 30, 2012, the fund delivered a gain of 16.1%. That result surpassed the fund’s relevant benchmarks. The unmanaged MSCI All Country World Index, which measures a broad range of developed- and developing-country stock markets, rose 13.3%.* The Lipper Global Funds Index, a measure of the fund’s peer group, recorded a 10.7% return.

The fund’s total return includes the reinvestment of dividends, which totaled 97 cents a share during the fiscal year. These dividends represented an income return of 3.0%. As you can see in the table below, Capital World Growth and Income Fund continues to compare favorably to its peers and benchmarks over longer time frames.

The global investing environment

Most of the world’s stock markets ended the fiscal year substantially higher as investors welcomed additional stimulus measures from major central banks, including in the U.S. and Europe. Later in the period, concerns about moderating growth in China gave way to renewed optimism about the longer term economic outlook for the country.

In Europe, stocks generally rallied during the second half. On a U.S. dollar-adjusted basis, the MSCI All Country Europe Index surged 13.6% and most European countries registered double-digit gains for

| | |

| * | Unless otherwise noted, MSCI indexes are stated in U.S. dollars and their results reflect dividends net of withholding taxes. |

Results at a glance

For periods ended November 30, 2012, with all distributions reinvested

| | | | | | | | | | | | | | |

| | | Total returns | | Average annual total returns | |

| | |

| |

|

|

| | | 1 year | | 5 years | | 10 years | | Lifetime

(since 3/26/93) | |

|

|

|

|

|

|

|

|

|

|

| Capital World Growth and Income Fund (Class A shares) | | 16.14 | % | | –1.14 | % | | 9.80 | % | | 10.71 | % | |

| MSCI All Country World Index† | | 13.33 | | | –1.82 | | | 7.34 | | | 6.73 | | |

| Lipper Global Funds Index | | 10.69 | | | –1.84 | | | 6.83 | | | 6.72 | | |

| | |

| † | The market index is unmanaged and, therefore, has no expenses. Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

| | |

| In this report |

| | |

| | Special feature |

| | |

| 6 | Far and wide: pursuing value in a low-growth world |

| | |

| | Even as global economic growth slows, the fund’s portfolio counselors are finding companies around the world with what they believe are good prospects for sales and profit growth. |

| | |

| | Contents |

| | |

| 1 | Letter to investors |

| | |

| 4 | The value of a long-term perspective |

| | |

| 12 | Summary investment portfolio |

| | |

| 18 | Financial statements |

| | |

| 35 | Board of directors and other officers |

| | |

| Capital World Growth and Income Fund | 1 |

(as of November 30, 2012)

| | | | | | | | | | |

| Company | | Country | | Percent of

net assets | | 12-month

return | |

|

|

|

|

|

|

|

|

| | |

| Novartis | | Switzerland | | 2.99 | % | | 14.68 | % | |

| Philip Morris International | | United States | | 2.51 | | | 17.89 | | |

| BP | | United Kingdom | | 2.00 | | | –4.90 | | |

| Bayer | | Germany | | 1.84 | | | 37.68 | | |

| Altria | | United States | | 1.81 | | | 17.85 | | |

| Amgen | | United States | | 1.67 | | | 53.34 | | |

| Home Depot | | United States | | 1.49 | | | 65.91 | | |

| Microsoft | | United States | | 1.37 | | | 4.07 | | |

| Royal Dutch Shell | | United Kingdom | | 1.09 | | | –4.09 | | |

| National Grid | | United Kingdom | | 1.07 | | | 14.96 | | |

the fiscal year. Among the few markets to sustain declines were fiscally troubled European nations Greece (–2.3%), Spain (–3.4%) and Portugal (–9.7%).

Despite signs of slowing corporate profits and mixed economic data, U.S. stocks rose 16.1%, as measured by Standard & Poor’s 500 Composite Index. Following November’s election, pledges from President Obama and Congressional leaders to work together on a compromise budget appeared to encourage investors. On January 1, following the close of the fund’s fiscal year, the White House and lawmakers agreed to raise taxes on affluent Americans, averting the so-called fiscal cliff. However, scheduled budget cuts were delayed for a few months, so a number of issues remain unresolved going into 2013.

Although growth slowed in China and other developing countries, the developing world continued to experience relatively healthy economic activity. However, results for equities were mixed. China and India’s stock markets rose 20.0% and 18.4%, respectively, but Russia declined 4.3%. While Brazilian equities were positive during the year, a slide in the Brazilian real versus the dollar resulted in a loss of 8.9% for U.S. investors.

Inside the portfolio

While country returns provide a useful backdrop, the investment professionals who manage Capital World Growth and Income Fund do not focus on particular geographies or market sectors. Rather, they build the portfolio one company at a time through careful fundamental research. The fund’s strong result in both absolute and relative terms was supported by a broad diversity of companies, many of which were among the largest holdings in the portfolio.

As you can see in the table above, a number of the fund’s 10 largest holdings produced double-digit gains; these included home improvement retailer Home Depot, biotechnology company Amgen and European pharmaceutical makers Bayer and Novartis (the fund’s top holding). The only holdings in the top 10 to lose ground were oil companies BP and Royal Dutch Shell, partly reflecting a slide in energy prices during the period.

Consumer discretionary companies, which represented the fund’s largest sector weighting, accounted for 12.3% of the portfolio at fiscal year-end. Holdings in this sector contributed some of the strongest returns of the period. In addition to Home Depot, the fund was supported by double-digit gains from U.S. cable operators Comcast (+64.0%) and Time Warner Cable (+56.9%), auto components maker Michelin (+45.7%) and Virgin Media (+58.7%). Several investments in the basic materials and industrials sectors also bolstered results.

Other holdings that dampened returns included HTC Corp. (–44.3%) and French utility GDF SUEZ (–19.9%).

A look ahead

As we look forward, a number of serious fiscal challenges around the world — particularly in the U.S. and Europe — have yet to be fully resolved. Despite some signs of progress in recent months, leaders in the U.S. still must address longer term budget concerns. European leaders, likewise, continue to grapple with the region’s structural problems and also are confronted with a difficult economic outlook.

Despite these challenges, we are encouraged by a number of developments. In a sluggish global economy, corporate profits have been remarkably resilient. In the U.S., we believe a dramatic transformation in U.S. energy supply and a housing market turnaround are leading to greater opportunity, and while Europe’s troubles will not be resolved quickly, we have seen a number of companies in Europe adjust to the changing landscape. We are further encouraged by what we believe are reasonable valuations in several areas.

Growth has clearly slowed in China as the nation’s leaders seek to transition toward a more domestic-focused economy. However, we believe China can continue to be a leading contributor to overall global growth.

And while global economic growth may remain muted, particularly in the world’s indebted developed nations, we believe there will continue to be opportunities to invest in companies experiencing vibrant

| | |

| 2 | Capital World Growth and Income Fund |

profit growth. We invite you to read our feature on page 6, “Far and wide: pursuing value in a low-growth world,” to learn more about how the fund’s portfolio counselors and analysts look for growth in a sluggish economy.

Our focus remains on investing in sound companies that we believe can provide long-term capital appreciation — regardless of where they are domiciled — and that often reward investors with regular dividend payments.

As always, we thank you, our fellow investors, for your continued support of Capital World Growth and Income Fund and we look forward to reporting back to you in six months’ time.

Cordially,

Michael Thawley

Vice Chairman of the Board

Mark E. Denning

President

January 9, 2013

For current information about the fund, visit americanfunds.com.

| | | | | | | | |

| Where the fund’s assets were invested* |

| | | | | | | | |

| | | Capital World Growth

and Income Fund | | MSCI All Country

World Index† | |

|

|

|

|

|

|

| | | | | | | | |

| Europe | | 37.2 | % | | 25.4 | % | |

| United Kingdom | | 11.1 | | | 8.4 | | |

| Switzerland | | 6.2 | | | 3.3 | | |

| France | | 5.1 | | | 3.5 | | |

| Germany | | 4.8 | | | 3.2 | | |

| Sweden | | 3.6 | | | 1.2 | | |

| Belgium | | 1.3 | | | .4 | | |

| Finland | | 1.0 | | | .3 | | |

| Russia | | .8 | | | .7 | | |

| Netherlands | | .8 | | | .9 | | |

| Italy | | .6 | | | .8 | | |

| Other Europe | | 1.9 | | | 2.7 | | |

| The Americas | | 37.8 | | | 53.3 | | |

| United States | | 35.7 | | | 46.3 | | |

| Canada | | 1.0 | | | 4.3 | | |

| Mexico | | .6 | | | .7 | | |

| Brazil | | .5 | | | 1.5 | | |

| Other Americas | | — | | | .5 | | |

| Asia/Pacific | | 17.0 | | | 20.1 | | |

| Hong Kong | | 3.6 | | | 1.2 | | |

| China | | 2.6 | | | 2.3 | | |

| Australia | | 2.2 | | | 3.3 | | |

| Japan | | 2.1 | | | 7.2 | | |

| South Korea | | 1.9 | | | 1.9 | | |

| Singapore | | 1.5 | | | .7 | | |

| Thailand | | 1.1 | | | .3 | | |

| Other Asia/Pacific | | 2.0 | | | 3.2 | | |

| Other | | 1.0 | | | 1.2 | | |

| Bonds & notes, short-term securities & other assets less liabilities | | 7.0 | | | — | | |

| Total | | 100.0 | % | | 100.0 | % | |

| | |

| * | Percent of net assets by country as of November 30, 2012. |

| † | The MSCI All Country World Index is weighted by market capitalization. |

| | |

| Capital World Growth and Income Fund | 3 |

The value of a long-term perspective

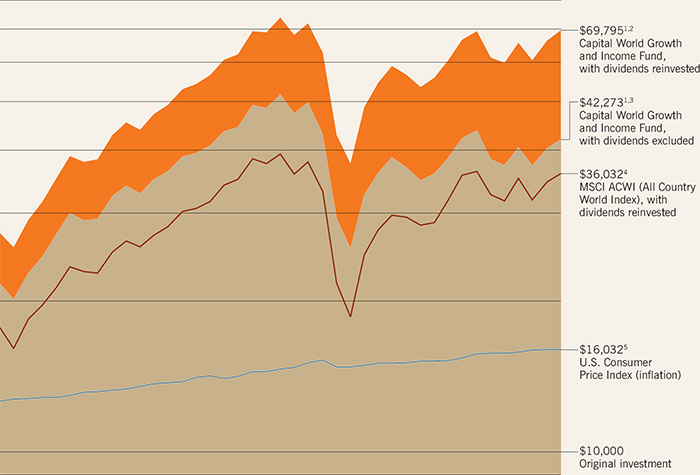

How a $10,000 investment has grown since March 26, 1993

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Year ended

November 30 | | 1993 | 6 | 1994 | | 1995 | | 1996 | | 1997 | | 1998 | | 1999 | | 2000 | | 2001 | | 2002 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total value | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Dividends reinvested | | $ | 144 | | | 295 | | | 421 | | | 506 | | | 488 | | | 478 | | | 440 | | | 577 | | | 578 | | | 569 | |

| Value at year-end | | $ | 10,782 | | | 11,592 | | | 13,841 | | | 17,118 | | | 19,917 | | | 23,007 | | | 27,396 | | | 29,142 | | | 28,613 | | | 27,405 | |

| WGI total return | | | 7.8 | % | | 7.5 | | | 19.4 | | | 23.7 | | | 16.4 | | | 15.5 | | | 19.1 | | | 6.4 | | | (1.8 | ) | | (4.2 | ) |

| | |

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | Includes reinvested dividends of $18,706 and reinvested capital gain distributions of $20,534. |

| 3 | Results calculated with capital gains reinvested. |

| | |

| 4 | Capital World Growth and Income Fund |

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.1 Thus, the net amount invested was $9,425. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Average

annual total

return for

fund’s lifetime

10.4%2 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 679 | | | 914 | | | 1,043 | | | 1,315 | | | 1,633 | | | 1,918 | | | 1,711 | | | 1,555 | | | 1,633 | | | 1,809 | | |

| | 35,220 | | | 43,044 | | | 49,405 | | | 60,955 | | | 73,901 | | | 43,044 | | | 59,179 | | | 60,701 | | | 60,096 | | | 69,795 | | |

| | 28.5 | | | 22.2 | | | 14.8 | | | 23.4 | | | 21.2 | | | (41.8 | ) | | 37.5 | | | 2.6 | | | (1.0 | ) | | 16.1 | ► | |

| | |

| 4 | The market index is unmanaged and, therefore, has no expenses. Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

| 5 | Computed from data supplied by the U.S. Department of Labor, Bureau of Labor Statistics. |

| 6 | For the period March 26, 1993 (when the fund began operations), through November 30, 1993. |

The results shown are before taxes on fund distributions and sale of fund shares.

| | |

| Capital World Growth and Income Fund | 5 |

| | |

| 6 | Capital World Growth and Income Fund |

Far and wide: pursuing value in a low-growth world

Even as global economic growth slows, the portfolio counselors who manage your fund believe they are finding companies around the world with good prospects for sales and profit growth. In the following pages, we look at how these investment professionals seek to build long-term value for investors despite the cloudy horizon.

Economic news has been less than encouraging lately. As leaders in Europe, the United States and other advanced nations wrestled over lingering fiscal troubles, growth in their economies was sluggish. At the same time, the pace of expansion in China, India and Brazil slowed considerably.

Investors may be faced with more of the same in coming years. The International Monetary Fund recently lowered its forecast for 2013 global growth to 3.6%. It expects gross domestic product (GDP) for the world’s developed nations to rise a modest 1.5%. However, the organization predicts a healthier 5.6% growth for the developing world. In fact, many economists expect growth to remain relatively low for a number of years as the developed world reduces its debt, and China and other developing nations seek a balance between exports and domestic demand.

“A look at historical data has shown that economic growth and stock market returns are not related. China has been a great example of that.”

Does this mean investors should expect weak equity returns going forward? Not necessarily, says Mark Denning, president of Capital World Growth and Income Fund and a portfolio counselor. “A look at historical data has shown that economic growth and stock market returns are not related. China has been a great example of that. Its economy has been among the strongest in the world in recent years, yet stock market returns there have been uneven.”

Consider, for example, that in 2011 China’s economy expanded at a 9.2% rate, yet the Chinese stock market, as measured by the MSCI China Index, dropped 18.4%. During the same period, the U.S. economy grew 1.8% while its stock market rose 2.1% as measured by the S&P 500. Why the disconnect? Simply put, prospects for companies are not necessarily tied to the changing fate of the local or regional economy where they are based. Nor are local companies necessarily the best positioned to participate in the growth of their home economies.

“Even in an environment of generally slower growth, there will be some areas of vibrant growth — and there will be companies that are going to do well,” says Michael Thawley, vice chairman of the fund. “Some people might avoid stocks because they are concerned about a particular crisis or discouraging economic data. But there are companies that will adapt to difficult conditions. They will adjust their focus, rethink their strategies and change their product offerings. What we try to do is invest in those companies that can thrive as conditions change.”

Indeed, rather than invest in economies, countries or particular sectors of the market, the investment professionals who manage Capital World Growth and Income Fund build the portfolio one company at a time. Through intensive fundamental research, they seek to identify companies with long-term growth potential. While the fund’s portfolio counselors have broad flexibility, they focus on larger, established companies that often pay dividends. Many of these are companies with global operations that can benefit from growth opportunities around the world. “Periods of intense stress also tend to be periods of restructuring,” says Michael. “This means great opportunity for investors who can recognize companies with the vision, initiative, leadership and other attributes to benefit from new trends.” Here are some examples of where they are looking for growth.

| | |

| Capital World Growth and Income Fund | 7 |

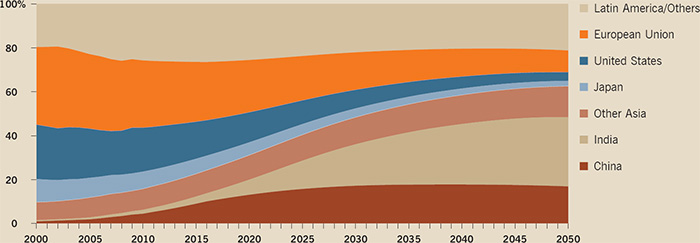

Developing countries: driving future middle-class consumption

The relative proportions of global middle-class consumption are changing dramatically. In the chart below, the width of each band of color for a given year indicates the percentages of consumption for a given region. By 2030, for example, India and China are expected to collectively account for about one-third of the middle class’s consumption of goods and services.

Share of global middle-class consumption

Sources: The New Global Middle Class: A Cross-Over from West to East, 2010, Homi Kharas and Geoffrey Gertz; The Emerging Middle Class in Developing Countries, 2010, Homi Kharas.

“ Even in an environment of generally slower growth, there will be some areas of vibrant growth — and there will be companies that are going to do well.”

A rising consumer class

China and other developing economies have experienced slower growth recently, but many of these areas are expected to continue experiencing growth at a faster rate than the global average. What’s more, millions of people living in developing nations are seeing their standards of living rise substantially.

“Economic cycles will ebb and flow, but this is an undeniable, powerful phenomenon with long-term implication for investors,” says Mark. The McKinsey Global Institute estimates that the global consumer class will grow from 2.4 billion people today to 4.2 billion by 2025, when the world’s population is expected to be about 7.9 billion. As you can see in the chart above, China, India, Latin America and other developing areas are expected to account for a much larger share of global consumption in the coming years.

With their increased spending power, these rising middle-class populations are already driving demand for products ranging from food and beverages and better health care to smartphones, automobiles and various types of luxury goods. “As consumers in these markets see their purchasing power increase, there will be opportunities for growth in a broad range of industries and sectors,” says Mark. “The challenge for investors is to identify companies with strong products, recognizable brands and the flexibility to tap into growth potential around the world, whether they are domiciled in the developing or developed world.”

Developed but developing

In fact, as trade has become increasingly globalized, the country or region where a company is based has become less important. In many cases, multinational companies based in developed markets are in a position to benefit from the rising consumer demand in developing markets.

Consider, for example, industrial conglomerate Jardine Matheson Holdings, a holding in the fund. This Fortune Global 500 company has business interests in property management, automobile distribution, financial services, supermarkets and restaurants. Based in Hong Kong, the company trades on the London and Singapore exchanges, but has significant operations in developing Asian markets including Indonesia and China.

“Jardines is a large, multinational company

| | |

| 8 | Capital World Growth and Income Fund |

whose shares trade in advanced markets, which gives investors the potential benefits of liquidity and transparency,” says Mark. “But much of its growth potential comes from businesses serving consumers in Southeast Asia.” One example: Jardines has a controlling interest in Astra International, the largest automobile distributor in Indonesia. Because of low penetration, the Indonesian auto market has strong potential for growth, Mark says. Despite robust sales in recent months, only 4% of Indonesia’s 240 million residents have a car. “Certainly, Astra will face challenges, including increased competition, but I believe the company can grow its earnings by 10% to 15% over the next few years,” says Amol Gogate, a Hong Kong-based investment analyst who covers the company.

A convergence of trends

Despite the murky economic picture in recent years, a combination of factors has led to an explosion in wireless communication around the world. This has been driven by rising consumer demand in developing markets, but also by the advent of faster LTE (fourth-generation) networks in the U.S. and other advanced markets.

“In places like Africa and other developing areas, basic voice and simple text-type communication is still very much a growth industry,” says portfolio counselor Sung Lee. “And the development of smartphones and the LTE service in places like the U.S. has been a real boon to the service operators. All around the world, with some exceptions, a lot of telecom companies that were thought to be beyond their growth stage have seen very robust revenue growth during a period of general economic malaise.”

What’s more, because wireless service businesses often generate strong cash flows, Sung believes such investments can help the fund meet both of its primary objectives — long-term capital appreciation and current income. Consider, for example, AT&T and Verizon Communications, both among the fund’s top 20 holdings. As of November 30, they paid dividend yields of 5.3% and 4.7%, respectively. “Over the last couple of years, both of these stocks have been strong investments in terms of capital appreciation — and all along they have paid relatively high dividends, providing a measure of stability for investors.”

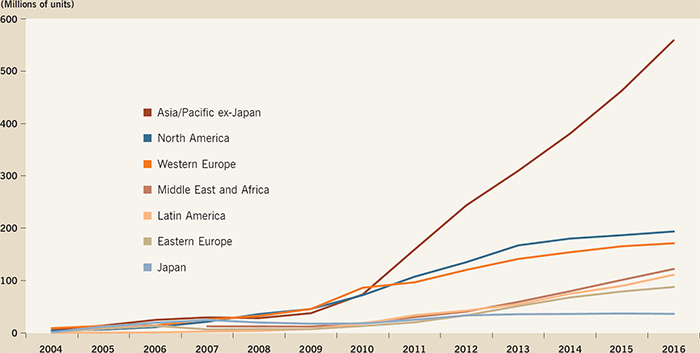

The demand for mobile data communication has also translated into strong growth in mobile phone sales, a trend that is expected to continue. Global sales of handsets will rise from 649.1 million in 2012 to 1.2 billion in 2016, according to research firm Gartner. As you can see in the chart on page 10, most of that growth is expected to come from the Asia/Pacific region. Also, as sales growth slows in North America and Western Europe, it is expected to pick up pace in Africa and Latin America.

One beneficiary of the rising demand for smartphones has been Samsung

| | |

| Capital World Growth and Income Fund | 9 |

As the income of the global consumer has risen, phone sales have gone into high gear

Source: Gartner, Inc.; data from 2012 to 2016 are estimates.

“Samsung has executed incredibly well to emerge as a primary beneficiary of the movement toward smartphones in the past couple of years.”

Electronics, one of the top holdings of the fund. “Samsung has executed incredibly well to emerge as a primary beneficiary of the movement toward smartphones in the past couple of years,” says Sung.

Resistant to economic fluctuations

In his search for growth, portfolio counselor Alfonso Barroso tends to focus on companies with essential products and services that aren’t sensitive to the ups and downs of economic cycles. This includes companies in so-called defensive areas of utilities and businesses focused on health care. “I look for companies that can grow by gaining market share, expanding into new markets and launching new products and services,” says Alfonso, who is based in London.

Swiss pharmaceutical maker Novartis, the fund’s top holding, provides one such example. The company, which has recently introduced medicines to treat multiple sclerosis, leukemia and other types of cancer, also makes a variety of consumer drugs such as Excedrin and Theraflu. With operations in more than 140 countries, including India, China and Russia, Novartis also could benefit from rising consumer demand in developing markets.

“Novartis is attractively valued relative to both the broader market and the pharmaceuticals industry largely because of concerns about patent expirations,” says Alfonso. “But I believe the negative impact of the patent expirations should abate starting in 2013.”

U.S. biotechnology company Amgen, the fund’s sixth-largest holding, has also focused on introducing new medicines and has developed a fairly robust pipeline. Its primary offerings include medicines for anemia, bone diseases, inflammatory conditions and the stimulation of white blood cells in chemotherapy patients. Alfonso believes the medicines that the company is developing have the potential to benefit investors regardless of the health of the macroeconomy.

“Both Amgen and Novartis, in my view, are well-positioned to potentially grow earnings by 5% to 10% a year over the next five years even if global economic growth remains subdued,” says Alfonso. “What’s more, both companies have stable and highly cash flow generative-based businesses that have supported predictable and rising dividend payments.”

Connecting the dots

Looking beneath the broad macroeconomic

| | |

| 10 | Capital World Growth and Income Fund |

picture often reveals that particular industries or areas are picking up momentum while others are stagnating or slowing down. In the U.S., the emerging natural gas boom is impacting various areas of the U.S. economy.

“There are a lot of investment implications for shale gas in the United States, some of which are related to a recovery from low gas prices,” says portfolio counselor Eric Richter, who often looks for growth potential in industries that appear to be coming off a cyclical bottom. “But the best opportunity is not necessarily through a natural gas company.”

In fact, research has led Eric not only to direct investment in a natural gas company but also in companies that stand to benefit indirectly. One example: railroads. As natural gas became more abundant early last year, prices dropped substantially. “Because natural gas and coal can serve as substitutes for one another, the cheaper gas drove down demand for coal,” explains Eric. “This hurt railroads, which generate much of their profits from transporting coal.” More recently, gas prices have begun to recover as manufacturing and other activity in the U.S. pick up momentum. “As natural gas prices recover, it provides an incentive for utilities to use more coal, which in turn can benefit the railroads,” Eric continues. “So, I have looked for opportunities to invest not just in natural gas companies directly, which generally don’t have great yields, but also indirectly through railroads that carry coal and often offer a good dividend yield.”

Flexible and focused

Nearly 20 years ago, Capital World Growth and Income Fund was created to provide investors with a conservative approach to global investing. Our investment professionals have pursued the fund’s growth-and-income objective by remaining flexible and focused on the long term. They have relied on fundamental research to build a portfolio of companies that they believe can endure and thrive in the long run. This approach has served investors over time.

“Truly, despite the economic headwinds and fiscal problems around the world, there is a great deal of opportunity,” says portfolio counselor Jeanne Carroll. “I see potential for growth in both the developed and developing worlds. But it is important to dig in and do the research to find the companies that can best take advantage of economic growth and demographic trends.”

Mark agrees. “Do I think there are individual companies that are going to do well even in troubled areas like Europe? I do. And that connects directly with what we do. We don’t invest in markets. We carefully scrutinize companies, including those that others have stopped looking at, perhaps because they are avoiding troubled countries or regions or sectors. By remaining flexible and looking for opportunity around the world, we have the potential to benefit from growth wherever it arises.” ■

| | |

| Capital World Growth and Income Fund | 11 |

Summary investment portfolio November 30, 2012

The following summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

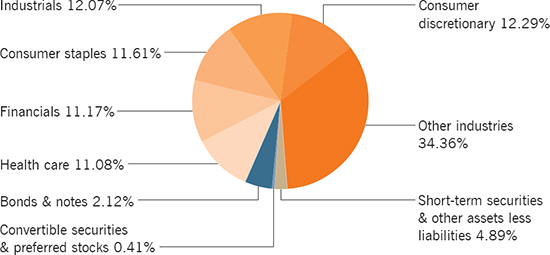

Industry sector diversification (percent of net assets)

| | | | | |

| Country diversification | | Percent of

net assets | |

|

|

|

|

| United States | | | 35.7 | % |

|

|

|

|

|

| Euro zone* | | | 14.6 | |

|

|

|

|

|

| United Kingdom | | | 11.1 | |

|

|

|

|

|

| Switzerland | | | 6.2 | |

|

|

|

|

|

| Hong Kong | | | 3.6 | |

|

|

|

|

|

| Sweden | | | 3.6 | |

|

|

|

|

|

| China | | | 2.6 | |

|

|

|

|

|

| Australia | | | 2.2 | |

|

|

|

|

|

| Japan | | | 2.1 | |

|

|

|

|

|

| South Korea | | | 1.9 | |

|

|

|

|

|

| Other countries | | | 9.4 | |

|

|

|

|

|

| Bonds & notes, short-term securities & other assets less liabilities | | | 7.0 | |

|

|

|

|

|

| | |

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Austria, Belgium, Finland, France, Germany, Ireland, Italy, the Netherlands, Portugal and Spain. |

| | | | | | | | | | | |

| Common stocks — 92.58% | | Shares | | Value

(000) | | Percent of

net assets | |

| Consumer discretionary — 12.29% | | | | | | | | | | |

| Home Depot, Inc. | | | 16,095,800 | | $ | 1,047,354 | | | 1.49 | % |

| The world’s largest home improvement retailer. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Comcast Corp., Class A | | | 13,567,900 | | | 504,454 | | | .72 | |

| The largest cable TV provider in the U.S. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| General Motors Co.1 | | | 18,646,450 | | | 482,570 | | | .69 | |

| U.S.-based auto manufacturer of brands such as Buick, Cadillac, Chevrolet and GMC. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Virgin Media Inc. | | | 11,495,500 | | | 404,297 | | | .58 | |

| United Kingdom-based provider of television, Internet, mobile phone and fixed-line telephone services. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| DIRECTV1 | | | 7,873,000 | | | 391,288 | | | .56 | |

| Digital television services provider in the United States, Latin America and the Caribbean. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Cie. Générale des Établissements Michelin, Class B | | | 4,000,000 | | | 372,009 | | | .53 | |

| One of the world’s largest tire makers. Its brands include Uniroyal and Goodrich. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Amazon.com, Inc.1 | | | 1,397,400 | | | 352,215 | | | .50 | |

| Major online retailer of books, CDs, DVDs, toys, apparel, home furnishings and other products. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 5,068,558 | | | 7.22 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 8,622,745 | | | 12.29 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Industrials — 12.07% | | | | | | | | | | |

| ASSA ABLOY AB, Class B | | | 19,660,007 | | | 711,245 | | | 1.01 | |

| Manufactures mechanical, electromagnetic and electronic locks and security systems. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| AB Volvo, Class B | | | 41,589,080 | | | 589,142 | | | .84 | |

| One of Sweden’s major manufacturers of trucks, buses, and marine and aerospace engines. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| KONE Oyj, Class B | | | 6,185,000 | | | 463,329 | | | .66 | |

| Finland-based manufacturer of elevators and escalators, as well as automatic building doors. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Jardine Matheson Holdings Ltd. | | | 7,748,000 | | | 457,287 | | | .65 | |

| Hong Kong-based diversified trading company operating in numerous industries, including supermarkets, real estate, hotels, restaurants, financial services, construction and mining. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| | |

| 12 | Capital World Growth and Income Fund |

| | | | | | | | | | | |

| Common stocks | | Shares | | Value

(000) | | Percent of

net assets | |

|

|

|

|

|

|

|

|

|

|

|

| United Parcel Service, Inc., Class B | | | 5,200,000 | | $ | 380,172 | | | .54 | % |

| The world’s largest package delivery company and express carrier. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| General Electric Co. | | | 17,500,000 | | | 369,775 | | | .53 | |

| Global operator of infrastructure, technology, energy and finance businesses. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 5,499,932 | | | 7.84 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 8,470,882 | | | 12.07 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Consumer staples — 11.61% | | | | | | | | | | |

| Philip Morris International Inc. | | | 19,606,300 | | | 1,762,214 | | | 2.51 | |

| One of the world’s largest international tobacco companies. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Altria Group, Inc. | | | 37,619,300 | | | 1,271,909 | | | 1.81 | |

| One of the world’s largest tobacco companies. The group also owns a large interest in the global brewer SABMiller. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Anheuser-Busch InBev NV | | | 7,924,534 | | | 694,538 | | | .99 | |

| Anheuser-Busch InBev NV, VVPR STRIPS1 | | | 3,247,475 | | | 4 | | | |

| One of the world’s largest brewers. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Wesfarmers Ltd. | | | 16,071,520 | | | 596,253 | | | .85 | |

| Australia-based retailer that operates home improvement and convenient stores, and has a presence in coal and natural gas production, and insurance. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Lorillard, Inc. | | | 4,314,988 | | | 522,804 | | | .75 | |

| U.S.-based tobacco company. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Nestlé SA | | | 7,310,030 | | | 478,422 | | | .68 | |

| Global packaged food and beverage company based in Switzerland. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 2,819,435 | | | 4.02 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 8,145,579 | | | 11.61 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Financials — 11.17% | | | | | | | | | | |

| Société Générale1 | | | 14,946,365 | | | 540,487 | | | .77 | |

| Has retail, corporate and investment banking operations around the world, with particular strength in Europe. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| HSBC Holdings PLC (Hong Kong) | | | 26,720,033 | | | 271,503 | | | .69 | |

| HSBC Holdings PLC (United Kingdom) | | | 20,476,231 | | | 209,204 | | | |

| One of the world’s largest international banking and financial services organizations. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Industrial and Commercial Bank of China Ltd., Class H | | | 676,073,470 | | | 456,229 | | | .65 | |

| A state-owned commercial bank in China and one of the world’s largest banks. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Prudential PLC | | | 29,060,000 | | | 421,354 | | | .60 | |

| Major life insurance and pension provider with operations in the U.S., U.K. and Asia-Pacific region. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| AIA Group Ltd. | | | 95,215,796 | | | 370,411 | | | .53 | |

| Life insurance and financial services provider in the Asia-Pacific region. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Siam Commercial Bank PCL | | | 66,634,100 | | | 352,820 | | | .50 | |

| Commercial bank based in Thailand. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 5,214,773 | | | 7.43 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 7,836,781 | | | 11.17 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Health care — 11.08% | | | | | | | | | | |

| Novartis AG | | | 33,907,063 | | | 2,098,381 | | | 2.99 | |

| One of the world’s largest pharmaceutical companies. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Bayer AG | | | 14,267,026 | | | 1,290,499 | | | 1.84 | |

| Makes pharmaceuticals and over-the-counter medicines, and develops medical diagnostic equipment. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Amgen Inc. | | | 13,159,758 | | | 1,168,587 | | | 1.67 | |

| The world’s largest biotechnology company. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| | |

| Capital World Growth and Income Fund | 13 |

| | | | | | | | | | | |

| Common stocks | | Shares | | Value

(000) | | Percent of

net assets | |

| Health care (continued) | | | | | | | | | | |

| Abbott Laboratories | | | 10,999,300 | | $ | 714,954 | | | 1.02 | % |

| Major health care company that develops drugs, drug-delivery systems, diagnostic tools and nutritional supplements. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Gilead Sciences, Inc.1 | | | 9,430,000 | | | 707,250 | | | 1.01 | |

| Develops drugs to treat infectious diseases and cancer. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Roche Holding AG | | | 2,014,000 | | | 396,410 | | | .56 | |

| A world leader in pharmaceuticals and diagnostic research. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 1,393,786 | | | 1.99 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 7,769,867 | | | 11.08 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Telecommunication services — 7.39% | | | | | | | | | | |

| AT&T Inc. | | | 20,610,000 | | | 703,419 | | | 1.01 | |

| Global provider of telecommunication services, including local and long-distance, Internet and wireless communications. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Verizon Communications Inc. | | | 15,119,500 | | | 667,072 | | | .95 | |

| Major broadband and telecommunication services provider. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| SOFTBANK CORP. | | | 13,509,700 | | | 506,399 | | | .72 | |

| Internet and telecommunications conglomerate and distributor of digital media and software. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| TeliaSonera AB | | | 71,210,054 | | | 477,563 | | | .68 | |

| Telecommunications company serving the Nordic and Baltic regions, and mobile communications provider serving northern and eastern Europe and Spain. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Vodafone Group PLC | | | 179,857,500 | | | 464,368 | | | .66 | |

| One of the leading global operators of mobile telephone services. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 2,363,964 | | | 3.37 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 5,182,785 | | | 7.39 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Information technology — 6.52% | | | | | | | | | | |

| Microsoft Corp. | | | 36,085,019 | | | 960,583 | | | 1.37 | |

| A world leader in software and Internet technologies. Its products include the Windows operating system and Office software. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Samsung Electronics Co. Ltd. | | | 556,400 | | | 722,444 | | | 1.03 | |

| Korea’s top electronics manufacturer and a global leader in semiconductor production. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Oracle Corp. | | | 13,337,000 | | | 428,118 | | | .61 | |

| Major supplier of database management software. Also develops business applications and provides consulting and support. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 2,463,349 | | | 3.51 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 4,574,494 | | | 6.52 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Energy — 5.67% | | | | | | | | | | |

| BP PLC | | | 203,283,213 | | | 1,405,679 | | | 2.00 | |

| One of the world’s largest oil companies. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Royal Dutch Shell PLC, Class B | | | 17,620,746 | | | 608,238 | | | 1.09 | |

| Royal Dutch Shell PLC, Class A (ADR) | | | 1,127,500 | | | 75,509 | | | |

| Royal Dutch Shell PLC, Class A | | | 1,686,000 | | | 56,507 | | | |

| Royal Dutch Shell PLC, Class B (ADR) | | | 344,800 | | | 23,819 | | | |

| A global group of energy and oil companies. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 1,809,862 | | | 2.58 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 3,979,614 | | | 5.67 | |

| | | | | |

|

|

|

|

| |

| | |

| 14 | Capital World Growth and Income Fund |

| | | | | | | | | | | |

| Common stocks | | Shares | | Value

(000) | | Percent of

net assets | |

| Utilities — 5.24% | | | | | | | | | | |

| National Grid PLC | | | 66,484,639 | | $ | 750,955 | | | 1.07 | % |

| Operates electricity networks in the U.K. and U.S. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| GDF SUEZ | | | 20,468,329 | | | 460,394 | | | .66 | |

| Major natural gas and electricity company based in France. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| SSE PLC | | | 18,545,336 | | | 423,402 | | | .60 | |

| One of the U.K.’s largest gas and electricity companies. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| PT Perusahaan Gas Negara (Persero) Tbk | | | 831,120,000 | | | 392,017 | | | .56 | |

| Explores for and produces oil and gas in Indonesia. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 1,648,930 | | | 2.35 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 3,675,698 | | | 5.24 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Materials — 4.74% | | | | | | | | | | |

| Dow Chemical Co. | | | 16,047,000 | | | 484,459 | | | .69 | |

| A major producer of plastics, chemicals, herbicides and pesticides. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| BASF SE | | | 4,429,000 | | | 396,873 | | | .57 | |

| The largest chemical company in the world. | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 2,442,728 | | | 3.48 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 3,324,060 | | | 4.74 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Miscellaneous — 4.80% | | | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | 3,366,079 | | | 4.80 | |

| | | | | |

|

|

|

|

| |

| Total common stocks (cost: $52,120,377,000) | | | | | | 64,948,584 | | | 92.58 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Preferred stocks — 0.01% | | | | | | | | | | |

| Financials — 0.01% | | | | | | | | | | |

| Other securities | | | | | | 10,271 | | | .01 | |

| | | | | |

|

|

|

|

| |

| Total preferred stocks (cost: $9,150,000) | | | | | | 10,271 | | | .01 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Convertible securities — 0.40% | | | | | | | | | | |

| Other — 0.40% | | | | | | | | | | |

| Other securities | | | | | | 277,431 | | | .40 | |

| | | | | |

|

|

|

|

| |

| Total convertible securities (cost: $262,002,000) | | | | | | 277,431 | | | .40 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Bonds & notes — 2.12% | | Principal amount

(000) | | | | | | | |

| | | | | | | | | | | |

| U.S. Treasury bonds & notes — 0.57% | | | | | | | | | | |

| U.S. Treasury 0.25%–1.875% 20142 | | $ | 393,000 | | | 399,162 | | | .57 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Energy — 0.15% | | | | | | | | | | |

| BP Capital Markets PLC 3.875%–5.25% 2013–2015 | | | 10,655 | | | 11,305 | | | .02 | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 93,220 | | | .13 | |

| | | | | |

|

|

|

|

| |

| | | | | | | 104,525 | | | .15 | |

| | | | | |

|

|

|

|

| |

| | |

| Capital World Growth and Income Fund | 15 |

| | | | | | | | | | | |

| Bonds & notes | | Principal amount

(000) | | Value

(000) | | Percent of

net assets | |

| Health care — 0.01% | | | | | | | | | | |

| Amgen Inc. 5.375% 2043 | | $ | 9,625 | | $ | 11,396 | | | .01 | % |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Other — 1.39% | | | | | | | | | | |

| Other securities | | | | | | 975,094 | | | 1.39 | |

| | | | | |

|

|

|

|

| |

| Total bonds & notes (cost: $1,295,392,000) | | | | | | 1,490,177 | | | 2.12 | |

| | | | | |

|

|

|

|

| |

| | | | | | | | | | | |

| Short-term securities — 4.62% | | | | | | | | | | |

| | | | | | | | | | | |

| U.S. Treasury Bills 0.11%–0.195% due 12/6/2012–7/25/2013 | | | 1,163,800 | | | 1,163,380 | | | 1.66 | |

|

|

|

|

|

|

|

|

|

|

|

| Fannie Mae 0.13%–0.175% due 1/2–4/10/2013 | | | 534,329 | | | 534,186 | | | .76 | |

|

|

|

|

|

|

|

|

|

|

|

| Federal Home Loan Bank 0.124%–0.20% due 12/10/2012–4/17/2013 | | | 381,900 | | | 381,780 | | | .55 | |

|

|

|

|

|

|

|

|

|

|

|

| Other securities | | | | | | 1,160,022 | | | 1.65 | |

| | | | | |

|

|

|

|

| |

| Total short-term securities (cost: $3,238,984,000) | | | | | | 3,239,368 | | | 4.62 | |

| | | | | |

|

|

|

|

| |

| Total investment securities (cost: $56,925,905,000) | | | | | | 69,965,831 | | | 99.73 | |

| Other assets less liabilities | | | | | | 189,643 | | | .27 | |

| | | | | |

|

|

|

|

| |

| Net assets | | | | | $ | 70,155,474 | | | 100.00 | % |

| | | | | |

|

|

|

|

| |

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio, including securities which were valued under fair value procedures adopted by authority of the board of directors. The total value of all such securities was $110,936,000, which represented .16% of the net assets of the fund. Some of “Other securities” (with an aggregate value of $939,074,000, which represented 1.34% of the net assets of the fund) were acquired in transactions exempt from registration under Rule 144A or section 4(2) of the Securities Act of 1933 and may be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers.

The descriptions of the companies shown in the summary investment portfolio, which were obtained from published reports and other sources believed to be reliable, are supplemental and are not covered by the Report of Independent Registered Public Accounting Firm.

Forward currency contracts

The fund has entered into forward currency contracts to sell currencies as shown in the following table. The open forward currency contracts shown are generally indicative of the level of activity over the prior 12-month period.

| | | | | | | | | | | | | | | | | |

| | | | | | | Contract amount | | Unrealized appreciation

(depreciation)

at 11/30/2012

(000) | |

| | | | | | |

| | |

| | | Settlement

date | | Counterparty | | Receive

(000) | | Deliver

(000) | | |

|

|

|

|

|

|

|

|

|

|

|

|

| | | | | | | | | | | | |

| Sales: | | | | | | | | | | | | | | |

| Australian dollars | | 1/8/2013 | | Barclays Bank PLC | | $ | 145,116 | | A$ | 139,000 | | | $ | 509 | | |

| Euros | | 12/10/2012 | | JPMorgan Chase | | $ | 224,322 | | € | 175,000 | | | | (3,295 | ) | |

| Euros | | 12/14/2012 | | UBS AG | | $ | 222,656 | | € | 175,000 | | | | (4,972 | ) | |

| Euros | | 12/18/2012 | | HSBC Bank | | $ | 159,356 | | € | 125,000 | | | | (3,244 | ) | |

| Euros | | 12/19/2012 | | UBS AG | | $ | 49,824 | | € | 39,000 | | | | (908 | ) | |

| Euros | | 12/20/2012 | | Citibank | | $ | 151,721 | | € | 119,000 | | | | (3,077 | ) | |

| | | | | | | | | | | | | |

|

| | |

| | | | | | | | | | | | | | $ | (14,987 | ) | |

| | | | | | | | | | | | | |

|

| | |

| | |

| 16 | Capital World Growth and Income Fund |

Investments in affiliates

A company is considered to be an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund’s holdings in affiliated companies is included in “Other securities” under the respective industry sectors in the summary investment portfolio. Further details on these holdings and related transactions during the year ended November 30, 2012, appear below.

| | | | | | | | | | | | | | | | | | | | |

| | | Beginning shares

or principal

amount | | Additions | | Reductions | | Ending shares

or principal

amount | | Dividend

or interest

income

(000) | | Value

of affiliates

at 11/30/2012

(000) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| | | | | | | | | | | | | | |

| ComfortDelGro Corp. Ltd. | | | 135,100,000 | | | — | | | — | | | 135,100,000 | | $ | 6,744 | | $ | 190,375 | |

| Qantas Airways Ltd.1 | | | 125,158,600 | | | — | | | — | | | 125,158,600 | | | — | | | 173,066 | |

| Darty PLC3 | | | 26,593,098 | | | — | | | 2,000,000 | | | 24,593,098 | | | 1,212 | | | — | |

| OPAP SA3 | | | 16,055,910 | | | — | | | 16,055,910 | | | — | | | 5,775 | | | — | |

| Virgin Media Inc.3 | | | 15,757,000 | | | — | | | 4,261,500 | | | 11,495,500 | | | 2,521 | | | — | |

| Virgin Media Inc. 6.50% convertible notes 20163 | | $ | 7,100,000 | | | — | | $ | 3,600,000 | | $ | 3,500,000 | | | 431 | | | — | |

| | | | | | | | | | | | | | |

|

|

|

|

| |

| | | | | | | | | | | | | | | $ | 16,683 | | $ | 363,441 | |

| | | | | | | | | | | | | | |

|

|

|

|

| |

The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item.

| | |

| 1 | Security did not produce income during the last 12 months. |

| 2 | A portion of this security was pledged as collateral for net losses on unsettled forward currency contracts with certain counterparties. The total value of pledged collateral was $4,444,000, which represented .01% of the net assets of the fund. |

| 3 | Unaffiliated issuer at 11/30/2012. |

| |

| Key to abbreviation and symbols |

| ADR = American Depositary Receipts |

| A$ = Australian dollars |

| € = Euros |

See Notes to Financial Statements

| | |

| Capital World Growth and Income Fund | 17 |

Financial statements

| | | | | | | | | | | |

| Statement of assets and liabilities | | | | | | | | | | |

| at November 30, 2012 | | | | | (dollars in thousands) | |

| | | | | | | | | | | |

| Assets: | | | | | | | | | | |

| Investment securities, at value: | | | | | | | | | | |

| Unaffiliated issuers (cost: $56,504,187) | | | | | $ | 69,602,390 | | | | |

| Affiliated issuers (cost: $421,718) | | | | | | 363,441 | | $ | 69,965,831 | |

| | | | | |

|

| | | | |

| Cash denominated in currencies other than U.S. dollars (cost: $7,464) | | | | | | | | | 7,464 | |

| Cash | | | | | | | | | 54 | |

| Unrealized appreciation on open forward currency contracts | | | | | | | | | 509 | |

| Receivables for: | | | | | | | | | | |

| Sales of investments | | | | | | 243,045 | | | | |

| Sales of fund’s shares | | | | | | 75,930 | | | | |

| Dividends and interest | | | | | | 217,991 | | | 536,966 | |

| | | | | |

|

| |

|

| |

| | | | | | | | | | 70,510,824 | |

| Liabilities: | | | | | | | | | | |

| Unrealized depreciation on open forward currency contracts | | | | | | | | | 15,496 | |

| Payables for: | | | | | | | | | | |

| Purchases of investments | | | | | | 156,763 | | | | |

| Repurchases of fund’s shares | | | | | | 116,109 | | | | |

| Investment advisory services | | | | | | 21,389 | | | | |

| Services provided by related parties | | | | | | 43,436 | | | | |

| Directors’ deferred compensation | | | | | | 1,108 | | | | |

| Other | | | | | | 1,049 | | | 339,854 | |

| | | | | |

|

| |

|

| |

| Net assets at November 30, 2012 | | | | | | | | $ | 70,155,474 | |

| | | | | | | | |

|

| |

| | | | | | | | | | | |

| Net assets consist of: | | | | | | | | | | |

| Capital paid in on shares of capital stock | | | | | | | | $ | 71,095,540 | |

| Undistributed net investment income | | | | | | | | | 624,411 | |

| Accumulated net realized loss | | | | | | | | | (14,587,790 | ) |

| Net unrealized appreciation | | | | | | | | | 13,023,313 | |

| | | | | | | | |

|

| |

| Net assets at November 30, 2012 | | | | | | | | $ | 70,155,474 | |

| | | | | | | | |

|

| |

| | | | | | | | | | | |

| (dollars and shares in thousands, except per-share amounts) | |

| | | | | | | | | | | |

Total authorized capital stock — 4,000,000 shares,

$.01 par value (1,911,925 total shares outstanding) | | | | | | | | | | |

| | | | | | | | | | | |

| | | Net assets | | Shares

outstanding | | Net asset value

per share | |

|

|

|

|

|

|

|

|

| Class A | | $ | 46,323,249 | | | 1,260,556 | | $ | 36.75 | |

| Class B | | | 1,432,804 | | | 39,226 | | | 36.53 | |

| Class C | | | 4,373,176 | | | 120,271 | | | 36.36 | |

| Class F-1 | | | 3,177,453 | | | 86,624 | | | 36.68 | |

| Class F-2 | | | 1,856,614 | | | 50,530 | | | 36.74 | |

| Class 529-A | | | 2,298,584 | | | 62,718 | | | 36.65 | |

| Class 529-B | | | 114,978 | | | 3,148 | | | 36.52 | |

| Class 529-C | | | 582,064 | | | 15,957 | | | 36.48 | |

| Class 529-E | | | 99,115 | | | 2,709 | | | 36.59 | |

| Class 529-F-1 | | | 78,157 | | | 2,131 | | | 36.68 | |

| Class R-1 | | | 276,101 | | | 7,581 | | | 36.42 | |

| Class R-2 | | | 1,149,854 | | | 31,637 | | | 36.35 | |

| Class R-3 | | | 2,335,321 | | | 63,925 | | | 36.53 | |

| Class R-4 | | | 2,158,731 | | | 58,865 | | | 36.67 | |

| Class R-5 | | | 1,381,022 | | | 37,559 | | | 36.77 | |

| Class R-6 | | | 2,518,251 | | | 68,488 | | | 36.77 | |

See Notes to Financial Statements

| | |

| 18 | Capital World Growth and Income Fund |

| | | | | | | | |

| Statement of operations | | | | | | | |

| for the year ended November 30, 2012 | | (dollars in thousands) | |

| | | | | | | | |

| Investment income: | | | | | | | |

| Income: | | | | | | | |

| Dividends (net of non-U.S. taxes of $144,246; also includes $16,252 from affiliates) | | $ | 2,198,517 | | | | |

| Interest (includes $431 from affiliates) | | | 96,357 | | $ | 2,294,874 | |

| | |

|

| | | | |

| | | | | | | | |

| Fees and expenses*: | | | | | | | |

| Investment advisory services | | | 260,673 | | | | |

| Distribution services | | | 217,325 | | | | |

| Transfer agent services | | | 107,382 | | | | |

| Administrative services | | | 14,729 | | | | |

| Reports to shareholders | | | 3,913 | | | | |

| Registration statement and prospectus | | | 922 | | | | |

| Directors’ compensation | | | 585 | | | | |

| Auditing and legal | | | 204 | | | | |

| Custodian | | | 7,821 | | | | |

| State and local taxes | | | 565 | | | | |

| Other | | | 3,400 | | | 617,519 | |

| | |

|

| |

|

| |

| Net investment income | | | | | | 1,677,355 | |

| | | | | | | | |

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency: | | | | | | | |

| Net realized gain (loss) on: | | | | | | | |

| Investments (net of non-U.S. taxes of $295; also includes $384,211 net loss from affiliates) | | | 235,372 | | | | |

| Forward currency contracts | | | 45,490 | | | | |

| Currency transactions | | | (2,197 | ) | | 278,665 | |

| | |

|

| | | | |

| Net unrealized appreciation (depreciation) on: | | | | | | | |

| Investments | | | 8,279,678 | | | | |

| Forward currency contracts | | | (14,318 | ) | | | |

| Currency translations | | | (2,495 | ) | | 8,262,865 | |

| | |

|

| |

|

| |

| Net realized gain and unrealized appreciation on investments, forward currency contracts and currency | | | | | | 8,541,530 | |

| | | | | |

|

| |

| Net increase in net assets resulting from operations | | | | | $ | 10,218,885 | |

| | | | | |

|

| |

| | | | | | | | |

| *Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements. |

| | | | | | | | |

| Statements of changes in net assets | | | | | | | |

| | | (dollars in thousands) | |

| | | | |

| | | Year ended November 30 | |

| | | 2012 | | 2011 | |

| | |

|

|

| |

| Operations: | | | | | | | |

| Net investment income | | $ | 1,677,355 | | $ | 1,987,803 | |

| Net realized gain on investments, forward currency contracts and currency transactions | | | 278,665 | | | 837,186 | |

| Net unrealized appreciation (depreciation) on investments, forward currency contracts and currency translations | | | 8,262,865 | | | (3,205,256 | ) |

| | |

|

| |

|

| |

| Net increase (decrease) in net assets resulting from operations | | | 10,218,885 | | | (380,267 | ) |

| | |

|

| |

|

| |

| | | | | | | | |

| Dividends paid to shareholders from net investment income | | | (1,889,680 | ) | | (1,908,500 | ) |

| | | | | | | | |

| Net capital share transactions | | | (6,354,159 | ) | | (6,453,000 | ) |

| | |

|

| |

|

| |

| | | | | | | | |

| Total increase (decrease) in net assets | | | 1,975,046 | | | (8,741,767 | ) |

| | | | | | | | |

| Net assets: | | | | | | | |

| Beginning of year | | | 68,180,428 | | | 76,922,195 | |

| | |

|

| |

|

| |

| End of year (including undistributed net investment income: | | | | | | | |

| $624,411 and $642,459, respectively) | | $ | 70,155,474 | | $ | 68,180,428 | |

| | |

|

| |

|

| |

See Notes to Financial Statements

| | |

| Capital World Growth and Income Fund | 19 |

Notes to financial statements

1. Organization

Capital World Growth and Income Fund, Inc. (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital while providing current income. It invests on a global basis in a diversified portfolio consisting primarily of common stocks and other equity securities. Shareholders approved a proposal to reorganize the fund from a Maryland corporation to a Delaware statutory trust. The reorganization may be completed in 2013; however, the fund reserves the right to delay the implementation.

The fund has 16 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and six retirement plan share classes (Classes R-1, R-2, R-3, R-4, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are further described below:

| | | | | | | |

| Share class | | Initial sales charge | | Contingent deferred sales

charge upon redemption | | Conversion feature |

|

|

|

|

|

|

|

| | | | | | | |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None |

|

|

|

|

|

|

|

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years |

|

|

|

|

|

|

|

| Class C | | None | | 1% for redemptions

within one year of purchase | | Class C converts to Class F-1

after 10 years |

|

|

|

|

|

|

|

| Class 529-C | | None | | 1% for redemptions

within one year of purchase | | None |

|

|

|

|

|

|

|

| Class 529-E | | None | | None | | None |

|

|

|

|

|

|

|

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None |

|

|

|

|

|

|

|

Classes R-1, R-2, R-3, R-4,

R-5 and R-6 | | None | | None | | None |

|

|

|

|

|

|

|

* Class B and 529-B shares of the fund are not available for purchase.

Holders of all share classes have equal pro rata rights to assets, dividends and liquidation proceeds. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, administrative and shareholder services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each class.

2. Significant accounting policies

The financial statements have been prepared to comply with accounting principles generally accepted in the United States of America. These principles require management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described below, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, administrative and shareholder services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions paid to shareholders are recorded on the ex-dividend date.

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. On the

| | |

| 20 | Capital World Growth and Income Fund |

accompanying financial statements, the effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by accounting principles generally accepted in the United States of America. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities purchased with more than 60 days left to maturity, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| | | |

| Fixed-income class | | Examples of standard inputs |

|

|

|

| |

| All | | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

|

|

|

| Corporate bonds & notes; convertible securities | | Standard inputs and underlying equity of the issuer |

|

|

|

| Bonds & notes of governments & government agencies | | Standard inputs and interest rate volatilities |

|

|

|