UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-07338

Capital World Growth and Income Fund

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: November 30

Date of reporting period: November 30, 2016

Michael W. Stockton

Capital World Growth and Income Fund

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

ITEM 1 – Reports to Stockholders

Global flexibility:

Following opportunity

anywhere.

Special feature page 6

| | Capital World Growth

and Income Fund®

Annual report

for the year ended

November 30, 2016 |

Capital World Growth and Income Fund seeks to provide you with long-term growth of capital while providing current income.

This fund is one of more than 40 offered by one of the nation’s largest mutual fund families, American Funds, from Capital Group. For 85 years, Capital has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

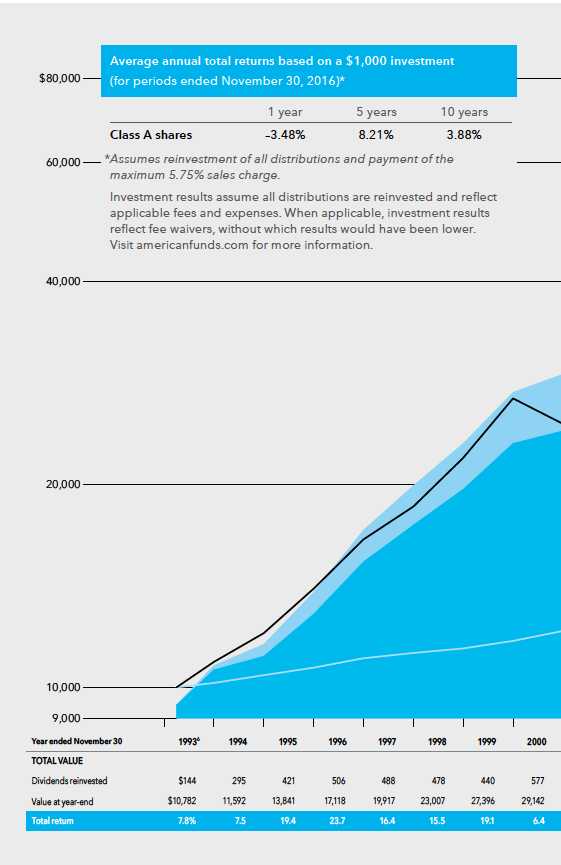

Here are the average annual total returns on a $1,000 investment with all distributions reinvested for periods ended December 31, 2016 (the most recent calendar quarter-end):

| Class A shares | 1 year | 5 years | 10 years |

| | | | |

| Reflecting 5.75% maximum sales charge | 0.36% | 8.72% | 3.78% |

For other share class results, visit americanfunds.com and americanfundsretirement.com.

The total annual fund operating expense ratio is 0.79% for Class A shares as of the prospectus dated February 1, 2017 (unaudited).

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. When applicable, investment results reflect fee waivers, without which results would have been lower. Visit americanfunds.com for more information.

The fund’s 30-day yield for Class A shares as of December 31, 2016, reflecting the 5.75% maximum sales charge and calculated in accordance with the U.S. Securities and Exchange Commission formula, was 2.02%.

Investing outside the United States may be subject to risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. Refer to the fund prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

Fellow investors:

Global stock markets produced modest gains during Capital World Growth and Income Fund’s fiscal year, a period characterized by unexpected political developments, aggressive monetary stimulus in markets around the world and improving growth in the United States.

Against this backdrop, the fund generated a total return of 2.42% for the 12 months ended November 30, 2016. This result lagged the 3.68% gain of the fund’s primary benchmark, the MSCI ACWI (All Country World Index). The Lipper Global Funds Index, a peer group measure, recorded a 3.28% total return. It is worth noting that the fund has consistently outpaced both of these indexes over longer time frames, as shown in the table below.

Capital World Growth and Income Fund seeks to provide investors with current income and long-term growth of capital. The fund paid dividends totaling $1.04 per share for the 12 months, as well as capital gains distributions totaling 71 cents paid in December. For the year, investors who reinvested dividends recorded an income return of 2.34%.

The global macroeconomic environment

The fiscal year was characterized by volatile swings from gains to losses, starting with a selloff in the early months after the U.S. Federal Reserve raised interest rates in December 2015 and investors focused on plummeting oil prices and China’s slowing growth. After bouncing back, equities fell sharply in June after U.K. voters surprised markets by choosing to leave the European Union. The declines were short-lived however, as markets rebounded after European economic data remained resilient following the referendum. The British Pound declined sharply against the U.S. dollar. Political uncertainty weighed on European markets throughout the period, as investors considered the impact of the Brexit vote, the election of Donald Trump as U.S. president and a pending Italian referendum on constitutional reform, positioned by Prime Minister Matteo Renzi as an initiative to streamline government. Shortly after the close of the fiscal year, Italian voters rejected the measure. For the 12 months, the MSCI EU Index fell 7.80% in U.S. dollar terms. In the U.K., British exporters were bolstered by the declining pound but U.K. shares ended 7.83% lower for U.S. investors as a result of the currency weakness.

In Japan, equity prices were similarly volatile amid a strengthening yen and persistent deflationary pressures. In the third quarter, Japan’s economy grew at a faster-than-expected 2.2%, supported by higher exports. In October, industrial output climbed for the third consecutive

Results at a glance

For periods ended November 30, 2016, with all distributions reinvested

| | | Cumulative

total returns | | Average annual total returns |

| | | 1 year | | 5 years | | 10 years | | Lifetime

(since 3/26/93) |

| | | | | | | | | |

| Capital World Growth and Income Fund (Class A shares) | | | 2.42 | % | | | 9.50 | % | | | 4.50 | % | | | 10.23 | % |

| MSCI ACWI* | | | 3.68 | | | | 8.85 | | | | 3.57 | | | | 6.90 | |

| Lipper Global Funds Index† | | | 3.28 | | | | 9.24 | | | | 3.74 | | | | 7.08 | |

| * | Results for the MSCI ACWI reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. This index is a free float-adjusted market capitalization-weighted index that is designed to measure results of more than 40 developed and emerging equity markets. It is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index. |

| † | Lipper indexes track the largest mutual funds (no more than 30), represented by one share class per fund, in the corresponding Lipper category. |

| | |

| Capital World Growth and Income Fund | 1 |

Largest equity holdings

(as of November 30, 2016)

| Company | | Country of domicile | | Percent of

net assets | | 12-month

return† |

| Amgen | | United States | | | 2.3 | | | | –10.57 | % |

| AbbVie | | United States | | | 2.1 | | | | 4.56 | % |

| Novartis | | Switzerland | | | 2.1 | | | | –19.34 | % |

| Verizon Communications | | United States | | | 1.6 | | | | 9.79 | % |

| Philip Morris International | | United States | | | 1.5 | | | | 1.02 | % |

| Prudential | | United Kingdom | | | 1.5 | | | | –16.67 | % |

| Imperial Brands | | United Kingdom | | | 1.4 | | | | –20.64 | % |

| Altria | | United States | | | 1.3 | | | | 10.99 | % |

| Royal Dutch Shell* | | United Kingdom | | | 1.3 | | | | 2.89 | % |

| Barclays | | United Kingdom | | | 1.1 | | | | –19.70 | % |

| * | 12-month return for Royal Dutch Shell represents Class A shares only. |

| † | Returns shown are on a share price basis. |

month and household spending was relatively stable, but wage growth remained sluggish and core consumer prices fell for the eighth consecutive month. Japanese shares edged up 1.72% for U.S. investors.

After an uneven start, U.S. equities ended with solid gains, as the U.S. presidential election result brightened prospects for tax cuts, infrastructure spending and an easier regulatory environment. The U.S. economy continued to strengthen throughout the period. Third-quarter GDP was revised up to a 3.5% annualized gain and the unemployment rate fell below 5%. In October, new home construction reached a nine-year high, and durable goods orders and capital expenditures rose.

Results for emerging market stocks were generally upbeat, supported by firmer commodities prices, new stimulus measures in China and stronger growth in the U.S. However, volatility was renewed toward the end of the fiscal year with the prospect of higher interest rates in the U.S. and questions about the future of global trade after the U.S. election. Brazilian equities soared 56.49% on hopes of economic reform under new political leadership. A proposal by President Michel Temer to cap government spending won preliminary support from legislators. Results for stocks in India were essentially flat, weighed down by the government’s surprise move to pull 86% of the country’s currency from circulation as part of an effort to curb tax evasion. Russian equities soared 23.54%, fueled by rising oil prices and prospects for improved relations with the U.S. In Mexico, stocks tumbled 14.27% as the peso slid against the U.S. dollar and investors worried that the prospect for changes in U.S. trade policy could stifle exports.

Inside the portfolio

The fund received some of its strongest contributions from holdings in more economically sensitive areas of the market, most notably the materials and energy sectors. Brazilian mining company Vale (+179.9%) and Fortescue Metals Group (+209.9%) soared on higher commodities prices and, in the case of the former, optimism about political and economic reform in Brazil. Canadian Natural Resources, an independent crude oil and natural gas producer with operations in North America, the North Sea and off the coast of Africa, rose on higher oil prices and progress on cost cutting. Royal Dutch Shell, the fund’s ninth-largest holding, rose 2.9%.

Select holdings in information technology stocks also supported the fund’s overall positive total return. Japanese game maker Nintendo shares advanced 59.6%, as the company pushed into mobile gaming, most notably with its Pokémon Go game. U.S. semiconductor maker Texas Instruments (+27.2%), rose on earnings that beat estimates.

Health care holdings, the second-largest sector concentration in the fund, proved to be a drag on the fund’s overall result. Top-holding Amgen (–10.6%), a U.S. biotech company, and Swiss drug maker Novartis (–19.3%), the fund’s third-largest holding, declined as drug makers came under pressure amid political criticism and greater scrutiny of drug pricing practices. However, No. 2 holding AbbVie (+4.6%), a U.S. biopharmaceuticals company, recorded positive results for the fiscal year. Among the fund’s financial holdings, U.K. insurer Prudential (–16.7%) and British bank Barclays (–19.7%) both declined amid Brexit worries.

Elsewhere among the fund’s top-10 holdings, U.S. telecom company Verizon Communications (+9.8%) and tobacco companies Altria (+11.0%) and Philip Morris International (+1.0%) all advanced, while British tobacco maker Imperial Brands (–20.6%) lost ground.

Looking forward

Given that market leadership during the past 12 months has been largely composed of U.S. growth-oriented companies, we are pleased with the fund’s overall positive result. Largely for valuation reasons, the fund’s managers have been focused on what they believe are top companies in non-U.S. markets. We continue to believe that, over time, attractively valued, profitable businesses will tend to outpace businesses with less attractive valuations.

The global economy remains on a path of slow growth, as a number of challenges remain. We have seen some positive developments in Europe, but markets could experience volatility in the coming

| * | Unless otherwise noted, country stock returns are based on MSCI indexes, expressed in U.S. dollars, and assume the reinvestment of dividends. Results reflect dividends net of withholding taxes. |

| | |

| 2 | Capital World Growth and Income Fund |

months due to Brexit fallout and other political developments. The consequences of Italian voters’ rejection of a constitutional referendum aimed at streamlining the government remain unclear. In addition, several European countries are holding key elections in 2017, including Germany and France. Similarly, in the U.S. questions remain about the future direction of trade policy under President Trump. That said, the economy continues to gain momentum and investors have been encouraged by the prospect of corporate tax reform and infrastructure spending under the new administration. With the U.S. economy improving steadily, we expect the U.S. Federal Reserve to raise rates gradually in the near future. With commodity prices on the rise, and global economic growth finding its footing, the backdrop for emerging markets has also brightened.

We believe that our disciplined dividend orientation can continue to generate value for our investors over the long term, and we remain focused on seeking out what we consider to be superior businesses in markets around the world.

We thank you for your commitment to Capital World Growth and Income Fund and look forward to reporting back to you in six months.

Cordially,

Mark E. Denning

Vice Chairman and President

Michael Cohen

Senior Vice President

January 10, 2017

For current information about the fund, visit americanfunds.com.

Where the fund’s assets are invested*

(percent invested by country of domicile)

| | | Capital World Growth

and Income Fund | | MSCI All Country

World Index† |

| | | | | |

| Europe | | | 28.8 | % | | | 20.7 | % |

| United Kingdom | | | 11.1 | | | | 5.9 | |

| Switzerland | | | 5.3 | | | | 2.8 | |

| France | | | 4.6 | | | | 3.2 | |

| Germany | | | 1.7 | | | | 2.9 | |

| Spain | | | 1.8 | | | | 1.0 | |

| Netherlands | | | .9 | | | | 1.1 | |

| Sweden | | | .6 | | | | .9 | |

| Other Europe | | | 2.8 | | | | 2.9 | |

| | | | | | | | | |

| The Americas | | | 45.6 | | | | 58.6 | |

| United States | | | 40.3 | | | | 54.0 | |

| Canada | | | 4.0 | | | | 3.3 | |

| Brazil | | | .9 | | | | .8 | |

| Other Americas | | | .4 | | | | .5 | |

| | | | | | | | | |

| Asia/Pacific | | | 18.4 | | | | 19.6 | |

| Japan | | | 4.3 | | | | 7.9 | |

| Hong Kong | | | 3.6 | | | | 1.2 | |

| China | | | 2.1 | | | | 2.9 | |

| India | | | 1.8 | | | | .9 | |

| South Korea | | | 1.7 | | | | 1.6 | |

| Thailand | | | 1.6 | | | | .2 | |

| Australia | | | 1.2 | | | | 2.4 | |

| Taiwan | | | 1.1 | | | | 1.3 | |

| Singapore | | | .6 | | | | .4 | |

| Other Asia/Pacific | | | .4 | | | | .8 | |

| | | | | | | | | |

| Other | | | 1.4 | | | | 1.1 | |

| | | | | | | | | |

| Bonds, notes & other debt instruments, short-term securities & other assets less liabilities | | | 5.8 | | | | — | |

| | | | | | | | | |

| Total | | | 100.0 | % | | | 100.0 | % |

| * | Percent of net assets by country as of November 30, 2016. |

| † | The MSCI All Country World Index is weighted by market capitalization. |

| Capital World Growth and Income Fund | 3 |

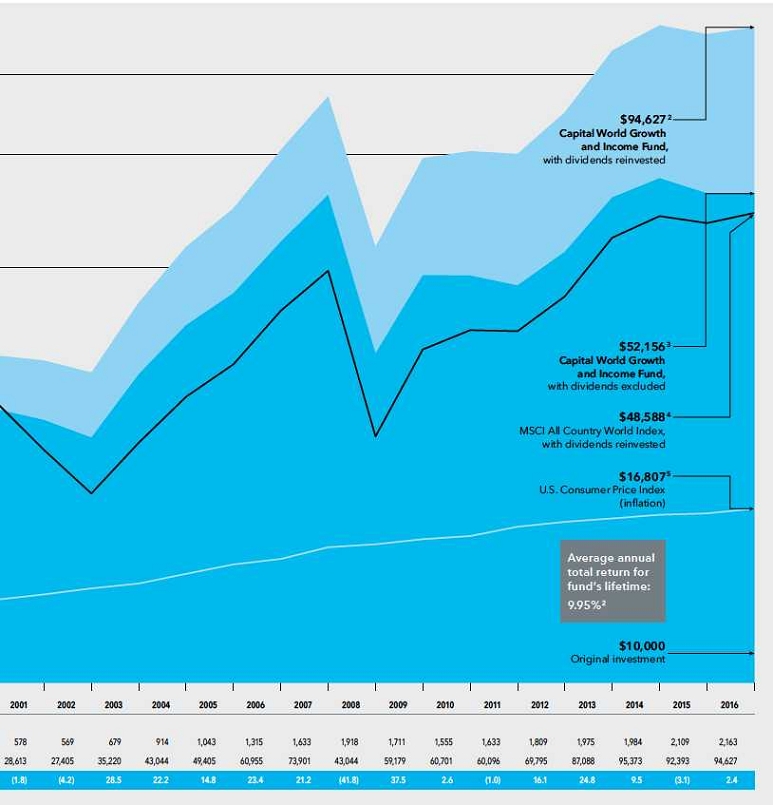

The value of a long-term perspective

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.1 Thus, the net amount invested was $9,425. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

The results shown are before taxes on fund distributions and sale of fund shares.

| 1 | As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

| 2 | Includes reinvested dividends of $26,938 and reinvested capital gain distributions of $21,981. |

| 3 | Results calculated with capital gains reinvested. |

| 4 | The market index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index. Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. |

| 5 | Computed from data supplied by the U.S. Department of Labor, Bureau of Labor Statistics. |

| 6 | For the period from March 26, 1993, commencement of fund operations, through November 30, 1993. |

| 4 | Capital World Growth and Income Fund |

How a $10,000 investment has grown

While notable for their volatility in recent years, financial markets have tended to reward investors over the long term. Active management — bolstered by experience and careful research — can add even more value. As the chart shows, over its lifetime, Capital World Growth and Income Fund has done demonstrably better than its relevant benchmark.

| Capital World Growth and Income Fund | 5 |

Global flexibility:

Following opportunity anywhere.

Change these days seems to be picking up speed at a dizzying pace. Technological advancements are altering the way people live and disrupting whole industries. New global companies rise in relatively short order to take a dominant market share from long-established businesses. Global supply chains quickly snap into action to meet the shifting demands of an evolving marketplace.

Whether it’s a shakeup in the euro zone triggered by recent election results, the ascendancy of Donald Trump to the U.S. presidency, or unprecedented steps taken by major central banks around the world to stimulate growth, nearly every week brings news of developments that promise to transform the global investment landscape.

Change, of course, is not new. In the 23 years since Capital World Growth and Income Fund began operations, investors have witnessed the introduction of the euro currency, the formation of the World Trade Organization and the emergence of China as the world’s second-largest economy. Borders have been redrawn, technology has brought the world closer together and investment opportunity has opened up to a degree few could have foreseen back in 1993.

Through all these changes, the fund has proved to be relatively resilient, and over its lifetime it has outpaced its primary benchmark, the MSCI ACWI. One important reason why the fund has adapted well to a rapidly changing environment is its flexible investment approach.

“When we started the fund 23 years ago, we believed very strongly that the fund’s dual growth-and-income objective was relevant for most investors,” explains Mark Denning, the fund’s president and a founding manager. “We anticipated that businesses and economies outside the U.S. would expand at a rapid pace, providing growth and diversification opportunities for our investors. We also believed a focus on established dividend payers around the world could help mitigate some of the risks of global investing. In today’s environment, where we can look to China and other developing markets for opportunity — and we can find some Japanese companies that have higher payout ratios than many U.S. companies — I look at our global growth-and-income approach as more relevant than ever.”

In the following pages, we take a closer look at the fund’s broad flexibility and how it serves the fund’s managers as they seek to achieve the fund’s objectives.

Go where the opportunity is

Perhaps the clearest manifestation of the fund’s flexibility is its ability to invest in companies based in virtually any market in the world. Thanks to the flourishing of global trade and the maturation of many of the world’s developing economies, today there are many more markets — and many more global companies — open to investment than there were two decades ago. As measured by the MSCI ACWI Index, a broad measure of the world’s stock markets, nearly half of the world’s investment opportunities lie outside the United States.

“The fund’s flexibility allows it to take advantage of the best values around the world, in any market and in any industry,” said Mark. “Focusing on companies based on geography would limit us in our choices and potentially restrict us from

| 6 | Capital World Growth and Income Fund |

“The fund’s flexibility allows it to take advantage of the best values around the world, in any market and in any industry.”

Mark Denning, president

| Capital World Growth and Income Fund | 7 |

investing in what we consider to be the most attractively valued companies.”

Primarily for valuation reasons, the fund has been invested largely outside the U.S. At the close of the fiscal year, nearly 60% of the fund’s assets were invested in companies domiciled abroad, including about 29% in Europe. “But there have been periods in the fund’s history when we have deemed U.S. stocks to be much more attractive in terms of relative valuation, and the fund had much higher exposure to U.S.-domiciled companies,” Mark explains.

Focus on companies, not countries

Clearly not all opportunities are equal. Indeed, the fund’s managers do not invest in markets or countries but focus on building the portfolio one investment at a time, selecting individual companies based on their underlying fundamentals and business prospects. In today’s increasingly global market, there are world-class companies domiciled in countries all over the world.

By having the flexibility to cross borders, for example, the fund’s managers can invest in leading innovators in any industry. While U.S. technology companies rank among the world’s most innovative businesses, innovation can be found across regions, nations and economies. Consider that today the latest advancements in screen technology for smart phones are being developed by Samsung Electronics, based in Suwon, South Korea, and a holding in the fund.

“Samsung is widely known for making the Galaxy smartphone, but it also has a division that is leading the development of a display technology called OLED that allows for flexible screens,” says Alfonso Barroso, a fund manager based in London. This technology allows for the construction of wraparound screens that extend from the front, around the side edges to the back of the phone. Ultimately the technology is intended to result in folding screens for devices such as tablets and televisions. “One day you may have a device in your pocket that you will be able to fold out to the size of a phone, and then unfold to the size of a notebook, then fold back down to fit in your pocket,” explains Alfonso.

In 2017, both Samsung and Apple are expected to introduce new models with wraparound screens. As the only company producing the OLED screens in large quantities, Samsung has contracted to supply screens for both its Galaxy S8 and the iPhone 8. “Without the flexibility to invest in Korea, we might miss the opportunity to invest directly in what we believe to be a major technological shift from flat to flexible display,” says Alfonso. “Of course this technology has the potential to put the “wow” factor back into the handset replacement cycle. Because of the fund’s global flexibility we can also invest in Apple and other companies that might benefit by adopting the technology.”

A holistic view

In addition to providing worldwide access to investment opportunity, the fund’s global approach also allows the fund’s managers to think holistically about global industries and individual companies within those industries. “Rather than stitching together a patchwork of investments from the U.S., international and emerging markets, or by style or market cap, or whatever other segmentation you might think of, we can take a truly holistic approach in choosing the best company in terms of growth prospects, earnings, cash flows and general market positioning,” says Michael Cohen, senior vice president of the fund and a portfolio manager. “That is something

| 8 | Capital World Growth and Income Fund |

“The fund does set a yield target, meaning a level of income that the overall portfolio must generate. But there are a variety of paths I can take to meet that target.”

Sung Lee, fund manager

that investments in separate U.S. and international funds might not provide in combination,” he adds.

Consider the global auto industry. Most leading automakers are global businesses operating largely in the same markets. The fund’s managers can look at individual companies in the U.S., Japan, Europe and emerging markets, consider each company’s merits relative to the competition and decide which to invest in. “If your mandate covers only the U.S., for example, and you have a constructive view on autos, you might feel compelled to invest in General Motors in that context,” says Michael. “Within Capital World Growth and Income Fund, we can consider all the major automakers and invest in only the best company. We could also decide to invest in all of them — or none of them.”

Many paths to income

In their pursuit of the fund’s growth and income objectives, the fund’s managers naturally focus on well-established companies with a track record of paying regular dividends. That said, the fund does not have strict guidelines on the types of companies that managers must invest in. “The fund does set a yield target, meaning a level of income that the overall portfolio must generate,” says Sung Lee, a fund manager in Singapore. “But there are a variety of paths I can take to meet that target.”

In putting together a portfolio that offers a reasonable dividend yield, managers can explore a wide spectrum of alternatives, from purely income-focused investments with fairly modest growth to companies with no dividends but very rapid growth, or troubled companies with the potential for a turn-around. While the fund is chiefly

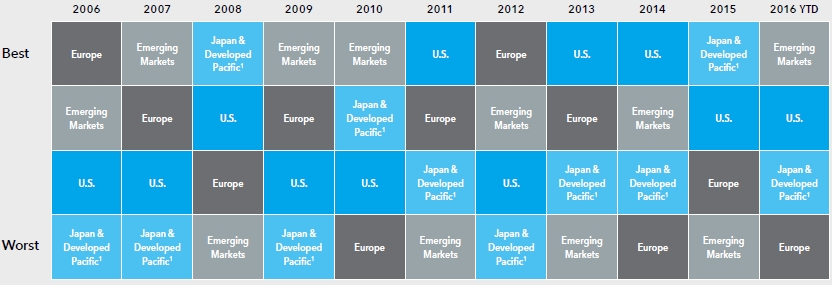

Yearly MSCI Index Performance by Region in U.S. Dollars (Best to Worst)

A flexible approach to investing across regions and economies may help investors capitalize on broader investment themes that transcend narrower investment approaches. Since 2006, emerging market stocks have had the strongest returns for four years, U.S. stocks for three years, and Europe and Japan & developed Pacific for two years each.

Sources: MSCI, RIMES. As of 12/5/16.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

| Capital World Growth and Income Fund | 9 |

The New Geography of Investing®

Fifty years ago, companies tended to do business solely within their own borders. Globalization, however, has made that less and less true. Where a company is headquartered or where its stock is listed have become less meaningful proxies.

Equity portion breakdown by revenue (%)

| | Region | | Fund | | Index |

| United States | | | 38 | % | | | 41 | % |

| Canada | | | 4 | | | | 3 | |

| Europe | | | 21 | | | | 17 | |

| Japan | | | 4 | | | | 8 | |

| Asia-Pacific ex. Japan | | | 5 | | | | 4 | |

| Emerging markets | | | 28 | | | | 27 | |

| | Total | | | 100 | % | | | 100 | % |

Equity portion breakdown by domicile (%)

| | Region | | Fund | | Index |

| | United States | | | 43 | % | | | 54 | % |

| | Canada | | | 4 | | | | 3 | |

| | Europe | | | 32 | | | | 20 | |

| | Japan | | | 4 | | | | 8 | |

| | Asia-Pacific ex. Japan | | | 6 | | | | 4 | |

| | Emerging markets | | | 11 | | | | 11 | |

| | Total | | | 100 | % | | | 100 | % |

Source: Capital Group (as of November 30, 2016).

Compared with the MSCI ACWI (All Country World Index) as a percent of net assets.

All figures include convertible securities.

focused on global equity markets, managers have the added flexibility of investing in some bonds. “Some of the fund’s managers may choose to invest primarily in companies whose dividend yields are close to the target, but I take another approach,” says Sung, a growth-oriented investor with investments in U.S. online retailer Amazon and streaming video service Netflix. “I am a big believer that Amazon and Netflix are doing things that are really changing people’s lives in a lot of ways.”

Blending multiple perspectives

Another facet of the fund’s flexibility can be found in its system of investment management. Known as The Capital System,SM it combines high-conviction investing and individual accountability with diverse perspectives and teamwork. The fund is divided into portions that are managed independently by nine investment professionals with varied backgrounds and investment approaches. An additional fund segment is managed by a group of analysts. Each manager is able to focus on only those ideas he or she feels are most compelling. As a result, there is broad diversification across the individual portfolios that comprise the fund.

“Under The Capital System, I have the flexibility to hold concentrated positions not only in specific companies but also in specific sectors that I like, and to hold little or nothing in major sectors of the global market,” says Eric Richter, a portfolio manager based in Washington, D.C. “So I can have a portfolio that includes my best ideas, knowing all of us together will produce diversification.”

Because he has spent most of his career as an investor living in the U.S., Eric tends to focus on U.S. companies. “On the other

| 10 | Capital World Growth and Income Fund |

“We will continue to work hard to generate value for our investors by searching in markets all around the world for world-class companies.”

Michael Cohen, senior vice president

hand, Asia is the geographic area where I rely the most heavily on the research organization and other colleagues who have much greater knowledge of specific country and company conditions that often I don’t have a history with,” Eric adds.

At the other end of the spectrum is Harold La, a portfolio manager in Hong Kong who has spent much of his career covering emerging markets (EM) in Asia and tends to have a heavy concentration in EM companies. “I see more EM companies, I am closer to them, so I am more comfortable investing in them,” says Harold.

Because he lives in Hong Kong, Harold has made dozens of visits to China and India to meet with company managements and gain an in-depth understanding of the local political, economic and business climate. “I am probably more comfortable investing in Indian companies, for example, than a U.S. colleague who is far away and might only see them once or twice a year at best. By being on the ground in local markets, I am less affected by news headlines.”

Among the fund’s holdings is HDFC Bank, the second-largest private bank in India. In November, in an effort to crack down on corruption and drive citizens into the formal economy, India’s Prime Minister Narendra Modi announced a demonetization effort that would render much of the country’s currency null and void. HDFC shares, along with other banks, fell sharply on the news. The fund held onto its investment. “I have been covering banks in Asia for 15 years, and HDFC is one of the strongest banks I have encountered,” Harold says.

Global presence, local knowledge

At the heart of the fund’s broad flexibility and multifaceted investment approach is an extensive global research network. The fund’s nine managers are supported by dozens of investment analysts based in local markets all around the world, many of whom have spent years — even decades — covering the same companies and industries. They also develop relationships with politicians, regulators and central bankers. “Our strong presence of locally domiciled analysts and portfolio managers gives us a differentiated depth of knowledge of local markets,” says Alfonso.

The knowledge acquired by both local specialists and the analysts who follow industries globally is widely shared so that the fund’s managers can look at valuations and competitive conditions in a context that a single market investor might not have. “Because we share local research, we can observe developments in one market, identify the trends which other countries or regions are likely to experience, and determine possible outcomes in other markets,” said Sung. “We can identify what we believe the implications are for the stocks in different segments of the value chain, whether it is parts makers or service providers.”

Consider, for example, Netflix, whose streaming video service has disrupted the cable television business in the United States. “Netflix has had a great impact on people’s viewing behavior, and the cable cord-cutting, I think, has started to happen much more quickly than people expected,” says Sung. “We can take that information and look at other markets where a similar service may soon be introduced and use that knowledge to determine how legacy businesses in that market might be impacted.”

Globalization reconsidered

The globalization of the world’s economy and markets over the past 20 years has boosted global trade and expanded opportunities for both businesses and investors. More recently, global trade has slowed, and recent election results around the world suggest, in part, a populist backlash against the impact of globalization. The U.K.’s “Brexit” vote in June to leave the European Union, and the rejection of a constitutional referendum in Italy shortly after the close of the fund’s fiscal year, have raised questions about the future direction of the EU. Similarly, the election of Donald Trump as U.S. president in November has raised some questions about the future direction of U.S. trade policy.

That said, globalization is likely to only accelerate going forward, says Mark. “Once the glass has been smashed, it can be very hard to put things back the way they were,” he says. “Some things are too difficult to reverse. I don’t think we are going to see a major reversal of global supply chains. At the margin, we may see some things come back to certain countries domestically.”

For the investment professionals who manage Capital World Growth and Income Fund, the key to successful global investing will be a continuation along the path they are on: working hard to understand shifting economic and political dynamics, and seeking to make sound judgments about the ability of companies to operate successfully as circumstances evolve. Observes Michael: “We will continue to work hard to generate value for our investors by searching in markets all around the world for world-class companies.” ■

| Capital World Growth and Income Fund | 11 |

Summary investment portfolio November 30, 2016

| Industry sector diversification | Percent of net assets |

| Country diversification by domicile | | Percent of

net assets |

| United States | | 40.26 | % |

| Euro zone* | | 11.33 | |

| United Kingdom | | 11.14 | |

| Switzerland | | 5.31 | |

| Japan | | 4.27 | |

| Canada | | 3.98 | |

| Hong Kong | | 3.60 | |

| China | | 2.11 | |

| India | | 1.77 | |

| Other countries | | 10.44 | |

| Bonds, notes & other debt instruments, short-term securities & other assets less liabilities | | 5.79 | |

| * | Countries using the euro as a common currency; those represented in the fund’s portfolio are Austria, Belgium, Finland, France, Germany, Ireland, Italy, the Netherlands, Portugal and Spain. |

| Common stocks 94.08% | | Shares | | | Value

(000) | |

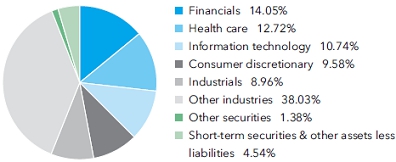

| Financials 14.05% | | | | | | | | |

| Prudential PLC1 | | | 61,356,400 | | | $ | 1,185,481 | |

| Barclays PLC1 | | | 345,242,756 | | | | 931,822 | |

| UBS Group AG1 | | | 55,859,786 | | | | 888,416 | |

| HDFC Bank Ltd.1 | | | 36,585,126 | | | | 734,563 | |

| HDFC Bank Ltd. (ADR) | | | 569,900 | | | | 36,770 | |

| American International Group, Inc. | | | 11,688,800 | | | | 740,252 | |

| Société Générale1 | | | 17,051,989 | | | | 731,253 | |

| AIA Group Ltd.1 | | | 89,997,196 | | | | 548,023 | |

| Siam Commercial Bank PCL1 | | | 132,758,855 | | | | 543,960 | |

| Other securities | | | | | | | 5,042,978 | |

| | | | | | | | 11,383,518 | |

| | | | | | | | | |

| Health care 12.72% | | | | | | | | |

| Amgen Inc. | | | 12,684,841 | | | | 1,827,505 | |

| AbbVie Inc. | | | 28,019,095 | | | | 1,703,561 | |

| Novartis AG1 | | | 24,150,054 | | | | 1,661,950 | |

| Stryker Corp. | | | 6,807,000 | | | | 773,684 | |

| Medtronic PLC | | | 8,179,000 | | | | 597,149 | |

| Teva Pharmaceutical Industries Ltd. (ADR) | | | 15,112,050 | | | | 569,724 | |

| Takeda Pharmaceutical Co. Ltd.1 | | | 12,717,200 | | | | 526,993 | |

| UnitedHealth Group Inc. | | | 3,117,100 | | | | 493,499 | |

| Other securities | | | | | | | 2,156,656 | |

| | | | | | | | 10,310,721 | |

| | | | | | | | | |

| Information technology 10.74% | | | | | | | | |

| Alphabet Inc., Class A2 | | | 636,880 | | | | 494,143 | |

| Alphabet Inc., Class C2 | | | 555,867 | | | | 421,369 | |

| Samsung Electronics Co., Ltd.1 | | | 457,799 | | | | 677,345 | |

| Intel Corp. | | | 19,380,000 | | | | 672,486 | |

| Taiwan Semiconductor Manufacturing Co., Ltd.1 | | | 108,673,000 | | | | 622,677 | |

| Texas Instruments Inc. | | | 8,311,200 | | | | 614,447 | |

| Nintendo Co., Ltd.1 | | | 2,405,832 | | | | 590,427 | |

| Oracle Corp. | | | 13,726,000 | | | | 551,648 | |

| Apple Inc. | | | 4,776,829 | | | | 527,935 | |

| Tencent Holdings Ltd.1 | | | 18,149,500 | | | | 451,903 | |

| Other securities | | | | | | | 3,075,877 | |

| | | | | | | | 8,700,257 | |

| 12 | Capital World Growth and Income Fund |

| | | Shares | | | Value

(000) | |

| Consumer discretionary 9.58% | | | | | | | | |

| Netflix, Inc.2 | | | 7,076,089 | | | $ | 827,902 | |

| Amazon.com, Inc.2 | | | 919,883 | | | | 690,437 | |

| Other securities | | | | | | | 6,248,052 | |

| | | | | | | | 7,766,391 | |

| | | | | | | | | |

| Industrials 8.96% | | | | | | | | |

| Boeing Co. | | | 5,483,000 | | | | 825,520 | |

| Lockheed Martin Corp. | | | 2,884,400 | | | | 765,087 | |

| Union Pacific Corp. | | | 5,383,140 | | | | 545,474 | |

| General Dynamics Corp. | | | 2,919,700 | | | | 511,969 | |

| Abertis Infraestructuras, SA, Class A1 | | | 34,657,935 | | | | 463,010 | |

| Other securities | | | | | | | 4,153,738 | |

| | | | | | | | 7,264,798 | |

| | | | | | | | | |

| Consumer staples 8.44% | | | | | | | | |

| Philip Morris International Inc. | | | 13,653,300 | | | | 1,205,313 | |

| Imperial Brands PLC1 | | | 26,137,100 | | | | 1,120,833 | |

| Altria Group, Inc. | | | 15,989,700 | | | | 1,022,222 | |

| Nestlé SA1 | | | 9,260,052 | | | | 622,984 | |

| Reynolds American Inc. | | | 9,292,528 | | | | 502,726 | |

| Thai Beverage PCL1 | | | 746,930,900 | | | | 455,135 | |

| Other securities | | | | | | | 1,914,927 | |

| | | | | | | | 6,844,140 | |

| | | | | | | | | |

| Energy 7.71% | | | | | | | | |

| Royal Dutch Shell PLC, Class B1 | | | 16,907,953 | | | | 451,172 | |

| Royal Dutch Shell PLC, Class A (GBP denominated)1 | | | 17,697,975 | | | | 450,611 | |

| Royal Dutch Shell PLC, Class A (ADR) | | | 945,123 | | | | 48,296 | |

| Royal Dutch Shell PLC, Class A (EUR denominated)1 | | | 1,784,000 | | | | 45,577 | |

| Royal Dutch Shell PLC, Class B (ADR) | | | 344,800 | | | | 18,678 | |

| Canadian Natural Resources, Ltd. | | | 25,377,830 | | | | 856,381 | |

| Suncor Energy Inc. | | | 22,412,717 | | | | 713,777 | |

| EOG Resources, Inc. | | | 5,541,587 | | | | 568,123 | |

| TOTAL SA1 | | | 11,841,645 | | | | 566,780 | |

| BP PLC1 | | | 84,002,150 | | | | 487,318 | |

| Other securities | | | | | | | 2,039,457 | |

| | | | | | | | 6,246,170 | |

| | | | | | | | | |

| Materials 4.81% | | | | | | | | |

| Vale SA, Class A, preferred nominative | | | 57,362,000 | | | | 433,346 | |

| Vale SA, Class A, preferred nominative (ADR) | | | 15,444,600 | | | | 115,835 | |

| Other securities | | | | | | | 3,346,985 | |

| | | | | | | | 3,896,166 | |

| | | | | | | | | |

| Utilities 4.79% | | | | | | | | |

| SSE PLC1 | | | 38,157,269 | | | | 704,200 | |

| Dominion Resources, Inc. | | | 6,238,422 | | | | 457,214 | |

| Other securities | | | | | | | 2,723,244 | |

| | | | | | | | 3,884,658 | |

| | | | | | | | | |

| Telecommunication services 4.33% | | | | | | | | |

| Verizon Communications Inc. | | | 26,791,053 | | | | 1,336,874 | |

| Other securities | | | | | | | 2,169,498 | |

| | | | | | | | 3,506,372 | |

| | | | | | | | | |

| Real estate 3.14% | | | | | | | | |

| Cheung Kong Property Holdings Ltd.1 | | | 78,990,856 | | | | 539,776 | |

| Other securities | | | | | | | 2,008,023 | |

| | | | | | | | 2,547,799 | |

| | | | | | | | | |

| Miscellaneous 4.81% | | | | | | | | |

| Other common stocks in initial period of acquisition | | | | | | | 3,901,001 | |

| | | | | | | | | |

| Total common stocks (cost: $65,073,701,000) | | | | | | | 76,251,991 | |

| Capital World Growth and Income Fund | 13 |

| Convertible stocks 0.13% | | Shares | | | Value

(000) | |

| Miscellaneous 0.13% | | | | | | | | |

| Other convertible stocks in initial period of acquisition | | | | | | $ | 102,000 | |

| | | | | | | | | |

| Total convertible stocks (cost: $79,932,000) | | | | | | | 102,000 | |

| | | | | | | | | |

| Bonds, notes & other debt instruments 1.25% | Principal amount

(000) | | | | | |

| Corporate bonds & notes 0.91% | | | | | | | | |

| Other 0.91% | | | | | | | | |

| Other securities | | | | | | | 738,446 | |

| | | | | | | | | |

| | | | | | | | | |

| Bonds & notes of governments & government agencies outside the U.S. 0.26% | | | | | | | | |

| Other securities | | | | | | | 211,072 | |

| | | | | | | | | |

| U.S. Treasury bonds & notes 0.08% | | | | | | | | |

| U.S. Treasury 0.08% | | | | | | | | |

| Other securities | | | | | | | 64,594 | |

| | | | | | | | | |

| Total bonds, notes & other debt instruments (cost: $975,592,000) | | | | | | | 1,014,112 | |

| | | | | | | | | |

| Short-term securities 4.48% | | | | | | | | |

| Federal Home Loan Bank 0.31%–0.65% due 12/2/2016–5/23/2017 | | $ | 810,000 | | | | 809,388 | |

| Other securities | | | | | | | 2,822,148 | |

| | | | | | | | | |

| Total short-term securities (cost: $3,631,139,000) | | | | | | | 3,631,536 | |

| Total investment securities 99.94% (cost: $69,760,364,000) | | | | | | | 80,999,639 | |

| Other assets less liabilities 0.06% | | | | | | | 50,105 | |

| | | | | | | | | |

| Net assets 100.00% | | | | | | $ | 81,049,744 | |

This summary investment portfolio is designed to streamline the report and help investors better focus on the fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

As permitted by U.S. Securities and Exchange Commission regulations, “Miscellaneous” securities include holdings in their first year of acquisition that have not previously been publicly disclosed.

“Other securities” includes all issues that are not disclosed separately in the summary investment portfolio. Some of these securities (with an aggregate value of $2,020,714,000, which represented 2.49% of the net assets of the fund) were acquired in transactions exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933 and may be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. “Other securities” also includes securities which were pledged as collateral. The total value of pledged collateral was $3,705,000, which represented less than .01% of the net assets of the fund.

Forward currency contracts

The fund has entered into forward currency contracts as shown in the following table. The average month-end notional amount of open forward currency contracts while held was $1,431,108,000.

| | | | | | | Contract amount | | Unrealized

(depreciation)

appreciation | |

| | | Settlement date | | Counterparty | | Receive

(000) | | Deliver

(000) | | at 11/30/2016

(000) | |

| Sales: | | | | | | | | | | | | |

| British pounds | | 12/7/2016 | | JPMorgan Chase | | $170,961 | | £140,000 | | | $(4,222 | ) |

| British pounds | | 12/16/2016 | | Citibank | | $101,514 | | £82,718 | | | (2,032 | ) |

| British pounds | | 12/20/2016 | | Bank of America, N.A. | | $29,261 | | £23,465 | | | (117 | ) |

| British pounds | | 1/11/2017 | | Citibank | | $199,978 | | £160,000 | | | (482 | ) |

| British pounds | | 1/19/2017 | | UBS AG | | $156,180 | | £124,850 | | | (266 | ) |

| British pounds | | 1/19/2017 | | JPMorgan Chase | | $153,543 | | £122,746 | | | (268 | ) |

| British pounds | | 1/19/2017 | | Bank of America, N.A. | | $156,177 | | £124,849 | | | (270 | ) |

| British pounds | | 1/19/2017 | | Bank of America, N.A. | | $199,545 | | £160,160 | | | (1,148 | ) |

| Euros | | 12/7/2016 | | JPMorgan Chase | | $41,165 | | €37,790 | | | 1,104 | |

| Euros | | 12/7/2016 | | Citibank | | $32,448 | | €29,788 | | | 870 | |

| Euros | | 12/19/2016 | | HSBC Bank | | $35,259 | | €31,842 | | | 1,475 | |

| 14 | Capital World Growth and Income Fund |

| | | | | | | Contract amount | | Unrealized

(depreciation)

appreciation | |

| | | Settlement date | | Counterparty | | Receive

(000) | | Deliver

(000) | | at 11/30/2016

(000) | |

| Euros | | 12/20/2016 | | Bank of America, N.A. | | $128,048 | | €120,640 | | | $ 43 | |

| Euros | | 12/20/2016 | | HSBC Bank | | $67,384 | | €63,533 | | | (28 | ) |

| Euros | | 1/19/2017 | | Citibank | | $57,979 | | €53,783 | | | 818 | |

| South African rand | | 1/6/2017 | | Barclays Bank PLC | | $15,985 | | ZAR223,100 | | | 260 | |

| South African rand | | 1/6/2017 | | Barclays Bank PLC | | $15,940 | | ZAR223,100 | | | 215 | |

| South African rand | | 1/6/2017 | | Barclays Bank PLC | | $18,165 | | ZAR255,858 | | | 132 | |

| | | | | | | | | | | | $(3,916 | ) |

Investments in affiliates

A company is an affiliate of the fund under the Investment Company Act of 1940 if the fund’s holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund’s affiliated-company holdings is either shown in the summary investment portfolio or included in the value of “Other securities” under the respective industry sectors. Further details on such holdings and related transactions during the year ended November 30, 2016, appear below.

| | | | Beginning

shares | | | | Additions | | | | Reductions | | | | Ending

shares | | | Dividend

income

(000) | | | Value of

affiliates at

11/30/2016

(000) | |

| Greene King PLC1 | | | 16,727,000 | | | | 33,403 | | | | — | | | | 16,760,403 | | | $ | 7,265 | | | $ | 143,858 | |

| Golar LNG Ltd. | | | 5,180,000 | | | | 242,000 | | | | — | | | | 5,422,000 | | | | 3,132 | | | | 132,297 | |

| Ocado Group PLC1,2 | | | 23,970,000 | | | | 15,110,197 | | | | — | | | | 39,080,197 | | | | — | | | | 132,022 | |

| American Campus Communities, Inc.3 | | | 6,763,000 | | | | 518,000 | | | | 4,431,000 | | | | 2,850,000 | | | | 1,165 | | | | — | |

| ComfortDelGro Corp. Ltd.1,3 | | | 148,490,000 | | | | — | | | | 130,792,761 | | | | 17,697,239 | | | | 4,313 | | | | — | |

| Kingfisher PLC1,3 | | | 121,513,199 | | | | 1,018,000 | | | | 90,512,393 | | | | 32,018,806 | | | | 15,793 | | | | — | |

| | | | | | | | | | | | | | | | | | | $ | 31,668 | | | $ | 408,177 | |

| 1 | Valued under fair value procedures adopted by authority of the board of trustees. The total value of all such securities, including those in “Miscellaneous” and “Other securities,” was $37,914,674,000, which represented 46.78% of the net assets of the fund. This amount includes $37,179,723,000 related to certain securities trading outside the U.S. whose values were adjusted as a result of significant market movements following the close of local trading. |

| 2 | Security did not produce income during the last 12 months. |

| 3 | Unaffiliated issuer at 11/30/2016. |

Key to abbreviations and symbols

ADR = American Depositary Receipts

EUR/€ = Euros

GBP/£ = British pounds

ZAR = South African rand

See Notes to Financial Statements

| Capital World Growth and Income Fund | 15 |

Financial statements

| Statement of assets and liabilities | | | | | | | | |

| at November 30, 2016 | (dollars in thousands) |

| | |

| Assets: | | | | | | | | |

| Investment securities, at value: | | | | | | | | |

| Unaffiliated issuers (cost: $69,074,503) | | $ | 80,591,462 | | | | | |

| Affiliated issuers (cost: $685,861) | | | 408,177 | | | $ | 80,999,639 | |

| Cash | | | | | | | 372 | |

| Cash denominated in currencies other than U.S. dollars (cost: $11,859) | | | | | | | 11,863 | |

| Unrealized appreciation on open forward currency contracts | | | | | | | 4,917 | |

| Receivables for: | | | | | | | | |

| Sales of investments | | | 175,595 | | | | | |

| Sales of fund’s shares | | | 73,779 | | | | | |

| Dividends and interest | | | 225,899 | | | | | |

| Other | | | 59 | | | | 475,332 | |

| | | | | | | | 81,492,123 | |

| Liabilities: | | | | | | | | |

| Unrealized depreciation on open forward currency contracts | | | | | | | 8,833 | |

| Payables for: | | | | | | | | |

| Purchases of investments | | | 234,732 | | | | | |

| Repurchases of fund’s shares | | | 123,169 | | | | | |

| Closed forward currency contracts | | | 3,408 | | | | | |

| Investment advisory services | | | 24,862 | | | | | |

| Services provided by related parties | | | 29,524 | | | | | |

| Trustees’ deferred compensation | | | 1,468 | | | | | |

| Other | | | 16,383 | | | | 433,546 | |

| Net assets at November 30, 2016 | | | | | | $ | 81,049,744 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Capital paid in on shares of beneficial interest | | | | | | $ | 67,384,671 | |

| Undistributed net investment income | | | | | | | 328,176 | |

| Undistributed net realized gain | | | | | | | 2,111,019 | |

| Net unrealized appreciation | | | | | | | 11,225,878 | |

| Net assets at November 30, 2016 | | | | | | $ | 81,049,744 | |

(dollars and shares in thousands, except per-share amounts)

Shares of beneficial interest issued and outstanding (no stated par value) —

unlimited shares authorized (1,818,544 total shares outstanding)

| | | Net assets | | | Shares outstanding | | | Net asset

value per share | |

| Class A | | $ | 50,454,104 | | | | 1,130,902 | | | $ | 44.61 | |

| Class B | | | 72,237 | | | | 1,624 | | | | 44.49 | |

| Class C | | | 2,938,354 | | | | 66,603 | | | | 44.12 | |

| Class F-1 | | | 3,286,067 | | | | 73,802 | | | | 44.53 | |

| Class F-2 | | | 5,646,040 | | | | 126,618 | | | | 44.59 | |

| Class 529-A | | | 2,859,340 | | | | 64,288 | | | | 44.48 | |

| Class 529-B | | | 10,508 | | | | 236 | | | | 44.46 | |

| Class 529-C | | | 658,959 | | | | 14,891 | | | | 44.25 | |

| Class 529-E | | | 117,289 | | | | 2,641 | | | | 44.41 | |

| Class 529-F-1 | | | 115,354 | | | | 2,591 | | | | 44.52 | |

| Class R-1 | | | 223,205 | | | | 5,052 | | | | 44.18 | |

| Class R-2 | | | 919,499 | | | | 20,864 | | | | 44.07 | |

| Class R-2E | | | 16,144 | | | | 363 | | | | 44.47 | |

| Class R-3 | | | 1,908,834 | | | | 43,066 | | | | 44.32 | |

| Class R-4 | | | 1,747,709 | | | | 39,262 | | | | 44.51 | |

| Class R-5E | | | 8,666 | | | | 194 | | | | 44.59 | |

| Class R-5 | | | 1,116,877 | | | | 25,020 | | | | 44.64 | |

| Class R-6 | | | 8,950,558 | | | | 200,527 | | | | 44.64 | |

See Notes to Financial Statements

| 16 | Capital World Growth and Income Fund |

| Statement of operations | | | | | | | | |

| for the year ended November 30, 2016 | | (dollars in thousands) |

| | | |

| Investment income: | | | | | | | | |

| Income: | | | | | | | | |

| Dividends (net of non-U.S. taxes of $88,913; also includes $31,668 from affiliates) | | $ | 2,334,901 | | | | | |

| Interest (net of non-U.S. taxes of $1,201) | | | 88,833 | | | $ | 2,423,734 | |

| Fees and expenses*: | | | | | | | | |

| Investment advisory services | | | 304,681 | | | | | |

| Distribution services | | | 202,924 | | | | | |

| Transfer agent services | | | 98,993 | | | | | |

| Administrative services | | | 19,885 | | | | | |

| Reports to shareholders | | | 3,877 | | | | | |

| Registration statement and prospectus | | | 1,973 | | | | | |

| Trustees’ compensation | | | 466 | | | | | |

| Auditing and legal | | | 4,259 | | | | | |

| Custodian | | | 8,642 | | | | | |

| Other | | | 3,279 | | | | 648,979 | |

| Net investment income | | | | | | | 1,774,755 | |

| | | | | | | | | |

| Net realized gain and unrealized depreciation: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments (net of non-U.S. taxes of $1,041; also includes $50,060 net gain from affiliates) | | | 2,215,950 | | | | | |

| Forward currency contracts | | | 216,336 | | | | | |

| Currency transactions | | | (11,968 | ) | | | 2,420,318 | |

| Net unrealized depreciation on: | | | | | | | | |

| Investments (net of non-U.S. taxes of $6,232) | | | (2,307,033 | ) | | | | |

| Forward currency contracts | | | (3,266 | ) | | | | |

| Currency translations | | | (1,065 | ) | | | (2,311,364 | ) |

| Net realized gain and unrealized depreciation | | | | | | | 108,954 | |

| Net increase in net assets resulting from operations | | | | | | $ | 1,883,709 | |

| * | Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements. |

| Statements of changes in net assets | | | | | | | | |

| | | (dollars in thousands) |

| | | |

| | | Year ended November 30 | |

| | | 2016 | | | 2015 | |

| Operations: | | | | | | | | |

| Net investment income | | $ | 1,774,755 | | | $ | 1,658,631 | |

| Net realized gain | | | 2,420,318 | | | | 4,774,514 | |

| Net unrealized depreciation | | | (2,311,364 | ) | | | (9,218,680 | ) |

| Net increase (decrease) in net assets resulting from operations | | | 1,883,709 | | | | (2,785,535 | ) |

| | | | | | | | | |

| Dividends and distributions paid to shareholders: | | | | | | | | |

| Dividends from net investment income | | | (1,920,044 | ) | | | (1,933,803 | ) |

| Distributions from net realized gain on investments | | | (1,318,506 | ) | | | — | |

| Total dividends and distributions paid to shareholders | | | (3,238,550 | ) | | | (1,933,803 | ) |

| | | | | | | | | |

| Net capital share transactions | | | (1,900,242 | ) | | | (401,335 | ) |

| | | | | | | | | |

| Total decrease in net assets | | | (3,255,083 | ) | | | (5,120,673 | ) |

| | | | | | | | | |

| Net assets: | | | | | | | | |

| Beginning of year | | | 84,304,827 | | | | 89,425,500 | |

| End of year (including undistributed net investment income: $328,176 and $367,603, respectively) | | $ | 81,049,744 | | | $ | 84,304,827 | |

See Notes to Financial Statements

| Capital World Growth and Income Fund | 17 |

Notes to financial statements

1. Organization

Capital World Growth and Income Fund (the “fund”) is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital while providing current income.

The fund has 18 share classes consisting of five retail share classes (Classes A, B and C, as well as two F share classes, F-1 and F-2), five 529 college savings plan share classes (Classes 529-A, 529-B, 529-C, 529-E and 529-F-1) and eight retirement plan share classes (Classes R-1, R-2, R-2E, R-3, R-4, R-5E, R-5 and R-6). The 529 college savings plan share classes can be used to save for college education. The retirement plan share classes are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described further in the following table:

| Share class | | Initial sales

charge | | Contingent deferred sales

charge upon redemption | | Conversion feature |

| Classes A and 529-A | | Up to 5.75% | | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | | None |

| Classes B and 529-B* | | None | | Declines from 5% to 0% for redemptions within six years of purchase | | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years |

| Class C | | None | | 1% for redemptions within one year of purchase | | Class C converts to Class F-1 after 10 years |

| Class 529-C | | None | | 1% for redemptions within one year of purchase | | None |

| Class 529-E | | None | | None | | None |

| Classes F-1, F-2 and 529-F-1 | | None | | None | | None |

| Classes R-1, R-2, R-2E, R-3, R-4, R-5E, R-5 and R-6 | | None | | None | | None |

| * | Class B and 529-B shares of the fund are not available for purchase. |

Holders of all share classes have equal pro rata rights to the assets, dividends and liquidation proceeds of the fund. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses (“class-specific fees and expenses”), primarily due to different arrangements for distribution, transfer agent and administrative services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each share class.

2. Significant accounting policies

The fund is an investment company that applies the accounting and reporting guidance issued in Topic 946 by the U.S. Financial Accounting Standards Board. The fund’s financial statements have been prepared to comply with U.S. generally accepted accounting principles (“U.S. GAAP”). These principles require the fund’s investment adviser to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. Subsequent events, if any, have been evaluated through the date of issuance in the preparation of the financial statements. The fund follows the significant accounting policies described in this section, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income — Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations — Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, transfer agent and administrative services, are charged directly to the respective share class.

Dividends and distributions to shareholders — Dividends and distributions to shareholders are recorded on the ex-dividend date.

| 18 | Capital World Growth and Income Fund |

Currency translation — Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments in the fund’s statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

3. Valuation

Capital Research and Management Company (“CRMC”), the fund’s investment adviser, values the fund’s investments at fair value as defined by U.S. GAAP. The net asset value of each share class of the fund is generally determined as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs — The fund’s investment adviser uses the following methods and inputs to establish the fair value of the fund’s assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market on which the security trades.

Fixed-income securities, including short-term securities, are generally valued at prices obtained from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive, and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities; and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

| Mortgage-backed; asset-backed obligations | Standard inputs and cash flows, prepayment information, default rates, delinquency and loss assumptions, collateral characteristics, credit enhancements and specific deal information |

When the fund’s investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or deemed to be not representative), fixed-income securities will be valued in good faith at the mean quoted bid and ask prices that are reasonably and timely available (or bid prices, if ask prices are not available) or at prices for securities of comparable maturity, quality and type.

Securities with both fixed-income and equity characteristics, or equity securities traded principally among fixed-income dealers, are generally valued in the manner described for either equity or fixed-income securities, depending on which method is deemed most appropriate by the fund’s investment adviser. Forward currency contracts are valued at the mean of representative quoted bid and ask prices, generally based on prices supplied by one or more pricing vendors.

Securities and other assets for which representative market quotations are not readily available or are considered unreliable by the fund’s investment adviser are fair valued as determined in good faith under fair valuation guidelines adopted by authority of the fund’s board of trustees as further described. The investment adviser follows fair valuation guidelines, consistent with U.S. Securities and Exchange Commission rules and guidance, to consider relevant principles and factors when making fair value determinations. The investment adviser considers relevant indications of value that are reasonably and timely available to it in determining the fair value to be assigned to a particular security, such as the type and cost of the security; contractual or legal restrictions on resale of the security; relevant financial or business developments of the issuer; actively traded similar or related securities; conversion or exchange rights on the security; related corporate actions; significant events occurring after the close of trading in the security; and changes in overall market conditions. In addition, the closing prices of equity securities that trade in markets outside U.S. time zones may be adjusted to reflect significant events

| Capital World Growth and Income Fund | 19 |

that occur after the close of local trading but before the net asset value of each share class of the fund is determined. Fair valuations and valuations of investments that are not actively trading involve judgment and may differ materially from valuations that would have been used had greater market activity occurred.

Processes and structure — The fund’s board of trustees has delegated authority to the fund’s investment adviser to make fair value determinations, subject to board oversight. The investment adviser has established a Joint Fair Valuation Committee (the “Fair Valuation Committee”) to administer, implement and oversee the fair valuation process, and to make fair value decisions. The Fair Valuation Committee regularly reviews its own fair value decisions, as well as decisions made under its standing instructions to the investment adviser’s valuation teams. The Fair Valuation Committee reviews changes in fair value measurements from period to period and may, as deemed appropriate, update the fair valuation guidelines to better reflect the results of back testing and address new or evolving issues. The Fair Valuation Committee reports any changes to the fair valuation guidelines to the board of trustees with supplemental information to support the changes. The fund’s board and audit committee also regularly review reports that describe fair value determinations and methods.

The fund’s investment adviser has also established a Fixed-Income Pricing Review Group to administer and oversee the fixed-income valuation process, including the use of fixed-income pricing vendors. This group regularly reviews pricing vendor information and market data. Pricing decisions, processes and controls over security valuation are also subject to additional internal reviews, including an annual control self-evaluation program facilitated by the investment adviser’s compliance group.

Classifications — The fund’s investment adviser classifies the fund’s assets and liabilities into three levels based on the inputs used to value the assets or liabilities. Level 1 values are based on quoted prices in active markets for identical securities. Level 2 values are based on significant observable market inputs, such as quoted prices for similar securities and quoted prices in inactive markets. Certain securities trading outside the U.S. may transfer between Level 1 and Level 2 due to valuation adjustments resulting from significant market movements following the close of local trading. Level 3 values are based on significant unobservable inputs that reflect the investment adviser’s determination of assumptions that market participants might reasonably use in valuing the securities. The valuation levels are not necessarily an indication of the risk or liquidity associated with the underlying investment. For example, U.S. government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market. The following tables present the fund’s valuation levels as of November 30, 2016 (dollars in thousands):

| | | Investment securities | |

| | | Level 1 | | | Level 2* | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | | | | | |

| Common stocks: | | | | | | | | | | | | | | | | |

| Financials | | $ | 2,916,370 | | | $ | 8,467,148 | | | $ | — | | | $ | 11,383,518 | |

| Health care | | | 7,288,415 | | | | 3,022,306 | | | | — | | | | 10,310,721 | |

| Information technology | | | 5,543,702 | | | | 3,156,555 | | | | — | | | | 8,700,257 | |

| Consumer discretionary | | | 3,692,661 | | | | 4,073,730 | | | | — | | | | 7,766,391 | |

| Industrials | | | 4,341,342 | | | | 2,923,456 | | | | — | | | | 7,264,798 | |

| Consumer staples | | | 3,481,426 | | | | 3,362,714 | | | | — | | | | 6,844,140 | |

| Energy | | | 4,058,899 | | | | 2,187,271 | | | | — | | | | 6,246,170 | |

| Materials | | | 1,002,785 | | | | 2,893,381 | | | | — | | | | 3,896,166 | |

| Utilities | | | 1,303,856 | | | | 2,580,802 | | | | — | | | | 3,884,658 | |

| Telecommunication services | | | 1,848,177 | | | | 1,658,195 | | | | — | | | | 3,506,372 | |

| Real estate | | | 1,018,580 | | | | 1,529,219 | | | | — | | | | 2,547,799 | |

| Miscellaneous | | | 1,841,103 | | | | 2,059,898 | | | | — | | | | 3,901,001 | |

| Convertible stocks | | | 102,000 | | | | — | | | | — | | | | 102,000 | |

| Bonds, notes & other debt instruments | | | — | | | | 1,014,112 | | | | — | | | | 1,014,112 | |

| Short-term securities | | | — | | | | 3,631,536 | | | | — | | | | 3,631,536 | |

| Total | | $ | 38,439,316 | | | $ | 42,560,323 | | | $ | — | | | $ | 80,999,639 | |

| 20 | Capital World Growth and Income Fund |

| | | Other investments† | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Assets: | | | | | | | | | | | | | | | | |

| Unrealized appreciation on open forward currency contracts | | $ | — | | | $ | 4,917 | | | $ | — | | | $ | 4,917 | |

| Liabilities: | | | | | | | | | | | | | | | | |

| Unrealized depreciation on open forward currency contracts | | | — | | | | (8,833 | ) | | | — | | | | (8,833 | ) |

| Total | | $ | — | | | $ | (3,916 | ) | | $ | — | | | $ | (3,916 | ) |

| * | Securities with a value of $37,179,723,000, which represented 45.87% of the net assets of the fund, were classified as Level 2 due to significant market movements following the close of local trading. |

| † | Forward currency contracts are not included in the investment portfolio. |

4. Risk factors

Investing in the fund may involve certain risks including, but not limited to, those described below.

Market conditions — The prices of, and the income generated by, the common stocks and other securities held by the fund may decline – sometimes rapidly or unpredictably – due to various factors, including events or conditions affecting the general economy or particular industries; overall market changes; local, regional or global political, social or economic instability; governmental or governmental agency responses to economic conditions; and currency exchange rate, interest rate and commodity price fluctuations.

Issuer risks — The prices of, and the income generated by, securities held by the fund may decline in response to various factors directly related to the issuers of such securities, including reduced demand for an issuer’s goods or services, poor management performance and strategic initiatives such as mergers, acquisitions or dispositions and the market response to any such initiatives.

Investing outside the U.S. — Securities of issuers domiciled outside the United States, or with significant operations or revenues outside the United States, may lose value because of adverse political, social, economic or market developments (including social instability, regional conflicts, terrorism and war) in the countries or regions in which the issuers operate or generate revenue. These securities may also lose value due to changes in foreign currency exchange rates against the U.S. dollar and/or currencies of other countries. Issuers of these securities may be more susceptible to actions of foreign governments, such as the imposition of price controls or punitive taxes, that could adversely impact the value of these securities. Securities markets in certain countries may be more volatile and/or less liquid than those in the United States. Investments outside the United States may also be subject to different accounting practices and different regulatory, legal and reporting standards and practices, and may be more difficult to value, than those in the United States. In addition, the value of investments outside the United States may be reduced by foreign taxes, including foreign withholding taxes on interest and dividends. Further, there may be increased risks of delayed settlement of securities purchased or sold by the fund. The risks of investing outside the United States may be heightened in connection with investments in emerging markets.

Investing in emerging markets — Investing in emerging markets may involve risks in addition to and greater than those generally associated with investing in the securities markets of developed countries. For instance, developing countries may have less developed legal and accounting systems than those in developed countries. The governments of these countries may be less stable and more likely to impose capital controls, nationalize a company or industry, place restrictions on foreign ownership and on withdrawing sale proceeds of securities from the country, and/or impose punitive taxes that could adversely affect the prices of securities. In addition, the economies of these countries may be dependent on relatively few industries that are more susceptible to local and global changes. Securities markets in these countries can also be relatively small and have substantially lower trading volumes. As a result, securities issued in these countries may be more volatile and less liquid, and may be more difficult to value, than securities issued in countries with more developed economies and/or markets. Less certainty with respect to security valuations may lead to additional challenges and risks in calculating the fund’s net asset value. Additionally, there may be increased settlement risks for transactions in local securities.

Investing in growth-oriented stocks — Growth-oriented common stocks and other equity-type securities (such as preferred stocks, convertible preferred stocks and convertible bonds) may involve larger price swings and greater potential for loss than other types of investments.

Investing in income-oriented stocks — Income provided by the fund may be reduced by changes in the dividend policies of, and the capital resources available for dividend payments at, the companies in which the fund invests.

Management — The investment adviser to the fund actively manages the fund’s investments. Consequently, the fund is subject to the risk that the methods and analyses employed by the investment adviser in this process may not produce the desired results. This could cause the fund to lose value or its investment results to lag relevant benchmarks or other funds with similar objectives.

| Capital World Growth and Income Fund | 21 |

5. Certain investment techniques

Forward currency contracts — The fund has entered into forward currency contracts, which represent agreements to exchange currencies on specific future dates at predetermined rates. The fund’s investment adviser uses forward currency contracts to manage the fund’s exposure to changes in exchange rates. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from possible movements in exchange rates.

On a daily basis, the fund’s investment adviser values forward currency contracts and records unrealized appreciation or depreciation for open forward currency contracts in the fund’s statement of assets and liabilities. Realized gains or losses are recorded at the time the forward currency contract is closed or offset by another contract with the same broker for the same settlement date and currency.

Closed forward currency contracts that have not reached their settlement date are included in the respective receivables or payables for closed forward currency contracts in the fund’s statement of assets and liabilities. Net realized gains or losses from closed forward currency contracts and net unrealized appreciation or depreciation from open forward currency contracts are recorded in the fund’s statement of operations.