UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-07874

JPMorgan Insurance Trust

(Exact name of registrant as specified in charter)

270 Park Avenue

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta

270 Park Avenue

New York, NY 10017

(Name and Address of Agent for Service)

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: December 31

Date of reporting period: January 1, 2015 through June 30, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

Semi-Annual Report

JPMorgan Insurance Trust

June 30, 2015 (Unaudited)

JPMorgan Insurance Trust Core Bond Portfolio

| | | | |

NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

| | |  | |

CONTENTS

Investments in the Portfolio are not bank deposits or obligations of, or guaranteed or endorsed by, any bank and are not insured or guaranteed by the FDIC, the Federal Reserve Board or any other government agency. You could lose money if you sell when the Portfolio’s share price is lower than when you invested.

Past performance is no guarantee of future performance. The general market views expressed in this report are opinions based on market and other conditions through the end of the reporting period and are subject to change without notice. These views are not intended to predict the future performance of the Portfolio or the securities markets. References to specific securities and their issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Such views are not meant as investment advice and may not be relied on as an indication of trading intent on behalf of the Portfolio.

This Portfolio is intended to be a funding vehicle for variable annuity contracts and variable life insurance policies (collectively “Policies”) offered by the separate accounts of various insurance companies. Portfolio shares may also be offered to qualified pension and retirement plans and accounts permitting accumulation of assets on a tax-deferred basis (“Eligible Plans”). Individuals may not purchase shares directly from the Portfolio.

Prospective investors should refer to the Portfolio’s prospectus for a discussion of the Portfolio’s investment objective, strategies and risks. Call J.P. Morgan Funds Service Center at 1-800-480-4111 for a prospectus containing more complete information about the Portfolio, including management fees and other expenses. Please read it carefully before investing.

CEO’S LETTER

July 30, 2015 (Unaudited)

Dear Shareholder,

Central banks remained the dominant drivers of both the global economy and financial markets in the first half of 2015. In the U.S., the Federal Reserve (the “Fed”) held down interest rates in the face of slowing growth and faint inflationary pressure. Meanwhile, central banks in the European Union (EU), Japan and China took extraordinary steps to shore up financial markets and economic expansion. By the end of the six months ended June 30, 2015, the consensus outlook for slow but continued global growth became clouded by investor worries about China and to a lesser degree, Greece.

| | |

| | “While the 2015 investment climate had changed somewhat from January to June, interest rates remained low globally and central banks continued to provide significant support for economic growth.” |

Gross domestic product (GDP) in the U.S. rose by a tepid 0.6% in the first three months of the year, partly due to severe winter weather and a labor dispute that slowed operations at vital West Coast ports. The manufacturing sector of the U.S. economy showed particular weakness in first half of 2015 as a strong U.S. dollar hurt exports and weak oil prices curtailed energy sector projects. On the positive side, retail sales improved markedly in May and the unemployment rate fell to 5.3% in June from 5.7% in January, though wage growth showed little sign of improvement. U.S. GDP rebounded in the second quarter to 2.3%.

U.S equity markets held up well and the Standard & Poor’s 500 Index reached several record closing highs, but ended the six month period with a total return of just 1.2%. Moreover, the index’s high-to-low trading range was never wider than 7.7%, the narrowest six month range since 1994. Bond markets were mixed during the first half of the year. High-yield debt (also called “junk bonds”) rebounded to outperform investment grade debt securities for the reporting period. Meanwhile, the municipal bond market experienced increased volatility due to extra supply from a surge in new issuance of bonds, concerns about Puerto Rico’s debt crisis and a pension crisis in Illinois. Long-maturity debt securities, including U.S. Treasury bonds, were among the worst performers during the six month period as investors sought to avoid the risk of holding long-term debt ahead of an anticipated increase in interest rates by the Fed.

In the EU, the European Central Bank’s massive asset buying program and reassuring statements that it would take whatever actions necessary to sustain economic growth helped propel

equity markets higher. For the first three months of 2015, gross domestic product rose by 0.4% in the EU and unemployment dropped to its lowest level since March 2012, though it stubbornly remained above 11%. Indeed, mild improvement in economic data across Europe coupled with signs of slowing U.S. growth increased the relative attractiveness of European equities to investors.

While negotiations to resolve the Greek debt crisis was the focus of daily news reports throughout the first half of the year, the drawn-out nature of the crisis meant that investors were braced for either a deal or default and financial markets had “priced in” those outcomes. Thus the crisis appeared to have little impact on financial markets and domestic economies outside of Greece itself.

Japanese equity markets also benefitted from a strong U.S. dollar (which made Japanese goods relatively cheaper), improved corporate governance and government equity purchases. Japanese equities outperformed both U.S. and European equities for the six month period. The Nikkei 250 Index closed out the first half of the year at an 18-year high.

Chinese equities also produced strong returns for the first half of 2015, but volatility grew sharply in Shanghai, Shenzhen and Hong Kong markets. After reaching a peak on June 12, Chinese equity prices fell nearly 30% in the subsequent weeks and ended the month 17.4% down from that peak. On June 27, China’s central bank sought to bolster sagging equity prices by cutting interest rates and reducing the amount of required cash reserves at certain banks. When those efforts failed to halt the freefall, the Chinese government on June 29 granted local government pension funds permission to invest in the stock market, potentially funneling more than $160 billion into the equity market. Interestingly, by the end of June, about one-fourth of all companies listed on the Shanghai and Shenzhen stock exchanges had sought a suspension in trading of their shares rather than endure a further sell-off. The Shanghai Composite Index returned 32.2% for the first half of 2015.

While the global economy remained on a positive growth trajectory, the International Monetary Fund in July lowered its forecast for 2015 growth by 0.2% to 3.3%, citing slower growth in the U.S. Nevertheless, the U.S. economy continued to improve sufficiently to lead the Fed to signal it may raise interest rates in September for the first time since the 2008-09 financial crisis. While the 2015 investment climate had changed somewhat from January to June, interest rates remained low globally and central banks continued to provide significant support for economic growth. The changing investment climate and uncertainties about the pace of global economic expansion underscore the practicality of holding a properly diversified portfolio with long-range objectives.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 1 | |

CEO’S LETTER

July 30, 2015 (continued)

On behalf of everyone at J.P. Morgan Asset Management, thank you for your continued support. We look forward to managing your investment needs for years to come. Should you have any questions, please visit www.jpmorganfunds.com or contact the J.P. Morgan Funds Service Center at 1-800-480-4111.

Sincerely yours,

George C.W. Gatch

CEO, Global Funds Management

J.P. Morgan Asset Management

| | | | | | |

| | | |

| 2 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

SIX MONTHS ENDED JUNE 30, 2015 (Unaudited)

| | | | |

| REPORTING PERIOD RETURN: | |

| Portfolio (Class 1 Shares)* | | | 0.66% | |

| Barclays U.S. Aggregate Index | | | -0.10% | |

| |

| Net Assets as of 6/30/2015 | | $ | 210,722,621 | |

| Duration as of 6/30/2015 | | | 4.98 years | |

INVESTMENT OBJECTIVE**

The JPMorgan Insurance Trust Core Bond Portfolio (the “Portfolio”) seeks to maximize total return by investing primarily in a diversified portfolio of intermediate- and long-term debt securities.

HOW DID THE MARKET PERFORM?

The performance of bond markets was mixed during the first half of the year. U.S. Treasury bonds continued to prove attractive to investors and high-yield debt (also called “junk bonds”) rebounded to outperform investment grade debt securities for the reporting period. Meanwhile, the municipal bond market experienced increased volatility due to extra supply and concerns about Puerto Rico’s debt crisis and a pension crisis in Illinois. Long-maturity debt securities, including U.S. Treasury bonds, were among the worst performers during the reporting period as investors sought to avoid the risk of holding long-term debt ahead of an anticipated increase in interest rates by the U.S. Federal Reserve.

WHAT WERE THE MAIN DRIVERS OF THE PORTFOLIO’S PERFORMANCE?

The Portfolio outperformed the Barclays U.S. Aggregate Index (the “Benchmark”) for the six month period ending June 30, 2015.

The Portfolio’s shorter duration and positioning on the yield curve contributed to performance relative to the Benchmark. Compared with the Benchmark, the Portfolio was overweight in the 5-10 year part of the yield curve and underweight in the 20-plus year portion of the curve. Duration measures the price sensitivity of a bond or a portfolio of bonds to relative changes in interest rates. Generally, bonds with longer duration will experience a larger increase or decrease in price as interest

rates go down or up, respectively, versus bonds with shorter duration. The yield curve shows the relationship between yields and maturity dates for a set of similar bonds.

The Portfolio’s underweight position and security selection in the credit market was a slight contributor to relative performance during the first half of 2015. The Portfolio’s allocation and security selection in the mortgage-backed securities sector also contributed to relative performance.

The Portfolio’s underweight position in U.S. Treasury bonds was neutral to performance as was its exposure to the asset-backed securities and commercial mortgage-backed securities.

HOW WAS THE PORTFOLIO POSITIONED?

The Portfolio’s primary strategy continued to be security selection and relative value, which seeks to identify undervalued bonds among individual securities and across market sectors. The Portfolio managers used bottom-up fundamental research to construct what they believe to be a portfolio of undervalued fixed income securities. Portfolio construction is strategic in nature, so sector allocation changes should be gradual and a function of relative value.

The Portfolio remained underweight in U.S. Treasury securities, underweight in corporate credit debt and overweight in securitized sectors including asset-backed, commercial-backed, and mortgage-backed securities, which include both agency and non-agency debt. The Portfolio continued to be overweight in the intermediate part of the yield curve (5 to 10 year maturities) as the Portfolio’s managers believed that this had the most attractive risk/reward profile and its steepness would benefit the Portfolio as securities roll-down the yield curve. The Portfolio maintained a shorter duration posture versus the Benchmark during the six month period.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 3 | |

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

SIX MONTHS ENDED JUNE 30, 2015 (Unaudited) (continued)

| | | | |

PORTFOLIO COMPOSITION*** | |

| U.S. Treasury Obligations | | | 28.8 | % |

| Collateralized Mortgage Obligations | | | 20.3 | |

| Corporate Bonds | | | 15.8 | |

| U.S. Government Agency Securities | | | 13.8 | |

| Mortgage Pass-Through Securities | | | 9.8 | |

| Asset-Backed Securities | | | 4.5 | |

| Commercial Mortgage-Backed Securities | | | 2.0 | |

| Others (each less than 1.0%) | | | 0.6 | |

| Short-Term Investment | | | 4.4 | |

| * | | The return shown is based on net asset values calculated for shareholder transactions and may differ from the return shown in the financial highlights, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America. |

| ** | | The adviser seeks to achieve the Portfolio’s objective. There can be no guarantee it will be achieved. |

| *** | | Percentages indicated are based on total investments as of June 30, 2015. The Portfolio’s composition is subject to change. |

| | | | | | |

| | | |

| 4 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

JPMorgan Insurance Trust Core Bond Portfolio

PORTFOLIO COMMENTARY

SIX MONTHS ENDED JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | | | | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS AS OF JUNE 30, 2015 | |

| | | | | |

| | | INCEPTION DATE OF

CLASS | | 6 MONTHS* | | | 1 YEAR | | | 5 YEAR | | | 10 YEAR | |

CLASS 1 SHARES | | May 1, 1997 | | | 0.66 | % | | | 2.39 | % | | | 3.80 | % | | | 4.69 | % |

CLASS 2 SHARES | | August 16, 2006 | | | 0.49 | | | | 2.15 | | | | 3.53 | | | | 4.47 | |

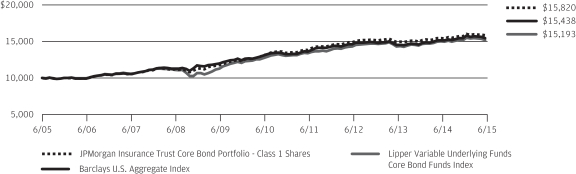

TEN YEAR PERFORMANCE (6/30/05 TO 6/30/15)

The performance quoted is past performance and is not a guarantee of future results. Mutual funds are subject to certain market risks. Investment returns and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data shown. For up-to-date month-end performance information please call 1-800-480-4111.

Returns for Class 2 Shares prior to its inception date are based on the performance of Class 1 Shares. The actual returns of Class 2 Shares would have been lower than those shown because Class 2 Shares have higher expenses than Class 1 Shares.

The graph illustrates comparative performance for $10,000 invested in Class 1 Shares of the JPMorgan Insurance Trust Core Bond Portfolio, the Barclays U.S. Aggregate Index and the Lipper Variable Underlying Funds Core Bond Funds Index from June 30, 2005 to June 30, 2015. The performance of the Portfolio assumes reinvestment of all dividends and capital gain distributions, if any. The performance of the Barclays U.S. Aggregate Index does not reflect the deduction of expenses associated with a mutual fund and has been adjusted to reflect reinvestment of all dividends and capital gain distributions of the securities included in the benchmark, if applicable. The performance of the Lipper

Variable Underlying Funds Core Bond Funds Index includes expenses associated with a mutual fund, such as investment management fees. These expenses are not identical to the expenses incurred by the Portfolio. The Barclays U.S. Aggregate Index is an unmanaged index that represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. The Lipper Variable Underlying Funds Core Bond Funds Index is an index based on the total returns of certain mutual funds within the Portfolio’s designated category as determined by Lipper, Inc. Investors cannot invest directly in an index.

Portfolio performance does not reflect any charges imposed by the Policies or Eligible Plans. If these charges were included, the returns would be lower than shown. Portfolio performance may reflect the waiver of the Portfolio’s fees and reimbursement of expenses for certain periods since the inception date. Without these waivers and reimbursements, performance would have been lower. The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights, which reflect adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 5 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Asset-Backed Securities — 4.5% | |

| | 159,951 | | | Ally Auto Receivables Trust, Series 2013-2, Class A3, 0.790%, 01/15/18 | | | 160,031 | |

| | | | American Credit Acceptance Receivables Trust, | | | | |

| | 73,784 | | | Series 2014-2, Class A, 0.990%,

10/10/17 (e) | | | 73,727 | |

| | 134,000 | | | Series 2015-2, Class A, 1.570%,

06/12/19 (e) | | | 133,889 | |

| | 250,000 | | | ARLP Securitization Trust, Series 2015-1, Class A1, SUB, 3.967%, 05/25/55 (e) | | | 250,000 | |

| | 99,590 | | | B2R Mortgage Trust, Series 2015-1, Class A1, 2.524%, 05/15/48 (e) | | | 99,062 | |

| | 100,000 | | | BA Credit Card Trust, Series 2015-A2, Class A, 1.360%, 09/15/20 | | | 99,661 | |

| | 17,362 | | | Bear Stearns Asset-Backed Securities Trust, Series 2006-SD1, Class A, VAR, 0.557%, 04/25/36 | | | 16,614 | |

| | 500,000 | | | CAM Mortgage LLC, Series 2015-1, Class A, SUB, 3.500%, 07/15/64 (e) | | | 500,000 | |

| | | | CarFinance Capital Auto Trust, | | | | |

| | 77,373 | | | Series 2014-1A, Class A, 1.460%, 12/17/18 (e) | | | 77,271 | |

| | 135,194 | | | Series 2014-2A, Class A, 1.440%,

11/16/20 (e) | | | 134,942 | |

| | | | CarMax Auto Owner Trust, | | | | |

| | 62,000 | | | Series 2013-4, Class A3, 0.800%, 07/16/18 | | | 61,996 | |

| | 55,000 | | | Series 2013-4, Class A4, 1.280%, 05/15/19 | | | 55,056 | |

| | 83,054 | | | Centex Home Equity Loan Trust, Series 2004-D, Class AF4, SUB, 4.680%, 06/25/32 | | | 84,851 | |

| | 200,000 | | | CPS Auto Trust, Series 2015-B, Class A, 1.650%, 11/15/19 (e) | | | 200,071 | |

| | 8,989 | | | CWABS Revolving Home Equity Loan Trust, Series 2004-K, Class 2A, VAR, 0.486%, 02/15/34 | | | 8,055 | |

| | | | CWABS, Inc. Asset-Backed Certificates, | | | | |

| | 1,056 | | | Series 2004-1, Class 3A, VAR, 0.747%, 04/25/34 | | | 987 | |

| | 86,511 | | | Series 2004-1, Class M1, VAR, 0.937%, 03/25/34 | | | 82,519 | |

| | 11,146 | | | Series 2004-1, Class M2, VAR, 1.012%, 03/25/34 | | | 10,286 | |

| | 163,000 | | | Drive Auto Receivables Trust, Series 2015-BA, Class B, 2.120%, 06/17/19 (e) | | | 163,412 | |

| | | | Exeter Automobile Receivables Trust, | | | | |

| | 52,935 | | | Series 2014-2A, Class A, 1.060%, 08/15/18 (e) | | | 52,856 | |

| | 128,475 | | | Series 2014-3A, Class A, 1.320%, 01/15/19 (e) | | | 128,479 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | 168,159 | | | Series 2015-2A, Class A, 1.540%,

11/15/19 (e) | | | 167,808 | |

| | 166,354 | | | FirstKey Lending Trust, Series 2015-SFR1, Class A, 2.553%, 03/09/47 (e) | | | 166,512 | |

| | | | Flagship Credit Auto Trust, | | | | |

| | 82,000 | | | Series 2014-1, Class A, 1.210%, 04/15/19 (e) | | | 81,895 | |

| | 148,159 | | | Series 2014-2, Class A, 1.430%,

12/16/19 (e) | | | 148,026 | |

| | 45,000 | | | Series 2014-2, Class B, 2.840%,

11/16/20 (e) | | | 45,330 | |

| | 22,000 | | | Series 2014-2, Class C, 3.950%,

12/15/20 (e) | | | 22,312 | |

| | 255,176 | | | GO Financial Auto Securitization Trust, Series 2015-1, Class A, 1.810%,

03/15/18 (e) | | | 254,945 | |

| | 90,805 | | | Gold Key Resorts LLC, Series 2014-A, Class A, 3.220%, 03/17/31 (e) | | | 91,199 | |

| | 180,000 | | | HLSS Servicer Advance Receivables Trust, Series 2013-T1, Class A2, 1.495%,

01/16/46 (e) | | | 179,820 | |

| | | | Hyundai Auto Receivables Trust, | | | | |

| | 68,050 | | | Series 2013-A, Class A3, 0.560%, 07/17/17 | | | 68,036 | |

| | 200,000 | | | Series 2013-A, Class A4, 0.750%, 09/17/18 | | | 199,786 | |

| | 459 | | | Lake Country Mortgage Loan Trust, Series 2006-HE1, Class A3, VAR, 0.537%, 07/25/34 (e) | | | 459 | |

| | | | Long Beach Mortgage Loan Trust, | | | | |

| | 104,076 | | | Series 2003-4, Class M1, VAR, 1.207%, 08/25/33 | | | 100,021 | |

| | 175,520 | | | Series 2004-1, Class M1, VAR, 0.937%, 02/25/34 | | | 166,865 | |

| | 12,580 | | | Series 2004-1, Class M2, VAR, 1.012%, 02/25/34 | | | 11,987 | |

| | 14,735 | | | Series 2006-WL2, Class 2A3, VAR, 0.387%, 01/25/36 | | | 14,197 | |

| | 200,000 | | | MarketPlace Loan Trust, Series 2015-OD1, Class A, 3.250%, 12/29/45 | | | 200,000 | |

| | 112,000 | | | Nationstar HECM Loan Trust,

Series 2015-1A, Class A, 3.844%, 05/25/18 (e) | | | 112,003 | |

| | 125,000 | | | New Century Home Equity Loan Trust, Series 2005-1, Class M1, VAR, 0.862%, 03/25/35 | | | 118,550 | |

| | 261,144 | | | Normandy Mortgage Loan Co. LLC,

Series 2013-NPL3, Class A, SUB, 4.949%, 09/16/43 (e) | | | 260,752 | |

| | 281,168 | | | NRPL Trust, Series 2015-2A, Class A1, VAR, 3.750%, 10/25/57 (e) | | | 279,831 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 6 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Asset-Backed Securities — continued | | | | |

| | 100,000 | | | Ocwen Freddie Advance Funding LLC,

Series 2015-T1, Class AT1, 2.062%, 11/15/45 (e) | | | 99,994 | |

| | 177,000 | | | Ocwen Freddie Advance Funding LLC Advance Receivables Backed Notes, Series 2015-T2, Class AT2, 2.014%, 09/15/45 (e) | | | 177,005 | |

| | | | OneMain Financial Issuance Trust, | | | | |

| | 276,000 | | | Series 2014-2A, Class A, 2.470%, 09/18/24 (e) | | | 277,466 | |

| | 230,000 | | | Series 2015-1A, Class A, 3.190%, 03/18/26 (e) | | | 233,268 | |

| | 350,000 | | | Series 2015-2A, Class A, 2.570%, 07/18/25 (e) | | | 350,229 | |

| | 100,000 | | | Series 2015-2A, Class B, 3.100%, 07/18/25 (e) | | | 100,191 | |

| | 54,826 | | | Park Place Securities, Inc. Asset-Backed Pass-Through Certificates, Series 2004-MCW1,

Class M1, VAR, 1.125%, 10/25/34 | | | 54,621 | |

| | 228,000 | | | Progress Residential Trust, Series 2015-SFR2,

Class A, 2.740%, 06/12/32 (e) | | | 224,233 | |

| | 6,951 | | | RASC Trust, Series 2003-KS9, Class A2B, VAR, 0.825%, 11/25/33 | | | 5,835 | |

| | 122,375 | | | RMAT LLC, Series 2015-NPL1, Class A1, SUB, 3.750%, 05/25/55 (e) | | | 122,375 | |

| | | | Santander Drive Auto Receivables Trust, | | | | |

| | 132,333 | | | Series 2015-S1, Class R1, 1.930%, 09/17/19 (e) | | | 132,329 | |

| | 110,044 | | | Series 2015-S7, Class R1, 1.970%, 03/16/21 (e) | | | 110,040 | |

| | 39,772 | | | SNAAC Auto Receivables Trust, Series 2014-1A, Class A, 1.030%, 09/17/18 (e) | | | 39,787 | |

| | | | SpringCastle America Funding LLC, | | | | |

| | 447,307 | | | Series 2014-AA, Class A, 2.700%, 05/25/23 (e) | | | 450,076 | |

| | 100,000 | | | Series 2014-AA, Class B, 4.610%, 10/25/27 (e) | | | 102,273 | |

| | | | Springleaf Funding Trust, | | | | |

| | 263,711 | | | Series 2013-AA, Class A, 2.580%, 09/15/21 (e) | | | 264,697 | |

| | 583,000 | | | Series 2014-AA, Class A, 2.410%, 12/15/22 (e) | | | 583,729 | |

| | 308,000 | | | Series 2015-AA, Class A, 3.160%, 11/15/24 (e) | | | 311,654 | |

| | 450,000 | | | VOLT XXV LLC, Series 2015-NPL8, Class A1, SUB, 3.500%, 06/26/45 (e) | | | 449,505 | |

| | 219,000 | | | VOLT XXXV LLC, Series 2015-NPL9, Class A1, SUB, 3.500%, 06/26/45 (e) | | | 218,781 | |

| | | | | | | | |

| | | | Total Asset-Backed Securities

(Cost $9,400,620) | | | 9,392,187 | |

| | | | | | | | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — 20.3% | | | | |

| | | | Agency CMO — 14.3% | | | | |

| | 109,774 | | | Federal Home Loan Mortgage Corp. - Government National Mortgage Association, Series 8,

Class ZA, 7.000%, 03/25/23 | | | 121,558 | |

| | | | Federal Home Loan Mortgage Corp. REMIC, | | | | |

| | 427 | | | Series 11, Class D, 9.500%, 07/15/19 | | | 433 | |

| | 2,090 | | | Series 22, Class C, 9.500%, 04/15/20 | | | 2,243 | |

| | 325 | | | Series 47, Class F, 10.000%, 06/15/20 | | | 360 | |

| | 290 | | | Series 99, Class Z, 9.500%, 01/15/21 | | | 321 | |

| | 519 | | | Series 1065, Class J, 9.000%, 04/15/21 | | | 601 | |

| | 31,233 | | | Series 1113, Class J, 8.500%, 06/15/21 | | | 32,723 | |

| | 2,823 | | | Series 1250, Class J, 7.000%, 05/15/22 | | | 3,152 | |

| | 6,916 | | | Series 1316, Class Z, 8.000%, 06/15/22 | | | 7,751 | |

| | 10,855 | | | Series 1324, Class Z, 7.000%, 07/15/22 | | | 12,101 | |

| | 47,672 | | | Series 1343, Class LA, 8.000%, 08/15/22 | | | 54,871 | |

| | 9,813 | | | Series 1343, Class LB, 7.500%, 08/15/22 | | | 11,321 | |

| | 7,063 | | | Series 1394, Class ID, IF, 9.566%, 10/15/22 | | | 8,743 | |

| | 6,386 | | | Series 1395, Class G, 6.000%, 10/15/22 | | | 6,947 | |

| | 4,565 | | | Series 1505, Class Q, 7.000%, 05/15/23 | | | 5,160 | |

| | 8,671 | | | Series 1518, Class G, IF, 8.885%, 05/15/23 | | | 10,309 | |

| | 8,308 | | | Series 1541, Class O, VAR, 1.610%, 07/15/23 | | | 8,426 | |

| | 217,943 | | | Series 1577, Class PV, 6.500%, 09/15/23 | | | 241,847 | |

| | 153,249 | | | Series 1584, Class L, 6.500%, 09/15/23 | | | 173,361 | |

| | 159,913 | | | Series 1633, Class Z, 6.500%, 12/15/23 | | | 176,173 | |

| | 182,491 | | | Series 1638, Class H, 6.500%, 12/15/23 | | | 209,168 | |

| | 2,387 | | | Series 1671, Class QC, IF, 10.000%, 02/15/24 | | | 3,545 | |

| | 26,131 | | | Series 1694, Class PK, 6.500%, 03/15/24 | | | 29,072 | |

| | 6,363 | | | Series 1700, Class GA, PO, 02/15/24 | | | 6,162 | |

| | 22,545 | | | Series 1798, Class F, 5.000%, 05/15/23 | | | 24,453 | |

| | 43,913 | | | Series 1863, Class Z, 6.500%, 07/15/26 | | | 50,335 | |

| | 4,026 | | | Series 1865, Class D, PO, 02/15/24 | | | 3,639 | |

| | 16,664 | | | Series 1981, Class Z, 6.000%, 05/15/27 | | | 18,409 | |

| | 23,065 | | | Series 1987, Class PE, 7.500%, 09/15/27 | | | 25,491 | |

| | 78,157 | | | Series 1999, Class PU, 7.000%, 10/15/27 | | | 88,999 | |

| | 128,554 | | | Series 2031, Class PG, 7.000%, 02/15/28 | | | 144,640 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 7 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Agency CMO — continued | | | | |

| | 5,040 | | | Series 2033, Class SN, HB, IF, 28.377%, 03/15/24 | | | 1,514 | |

| | 124,683 | | | Series 2035, Class PC, 6.950%, 03/15/28 | | | 142,989 | |

| | 8,852 | | | Series 2038, Class PN, IO, 7.000%, 03/15/28 | | | 1,349 | |

| | 27,666 | | | Series 2054, Class PV, 7.500%, 05/15/28 | | | 31,847 | |

| | 147,015 | | | Series 2057, Class PE, 6.750%, 05/15/28 | | | 165,596 | |

| | 32,743 | | | Series 2064, Class TE, 7.000%, 06/15/28 | | | 37,381 | |

| | 29,387 | | | Series 2075, Class PH, 6.500%, 08/15/28 | | | 32,820 | |

| | 93,682 | | | Series 2095, Class PE, 6.000%, 11/15/28 | | | 106,599 | |

| | 5,709 | | | Series 2132, Class SB, HB, IF, 29.753%, 03/15/29 | | | 10,456 | |

| | 7,673 | | | Series 2134, Class PI, IO, 6.500%, 03/15/19 | | | 718 | |

| | 47,468 | | | Series 2178, Class PB, 7.000%, 08/15/29 | | | 54,428 | |

| | 83,751 | | | Series 2182, Class ZB, 8.000%, 09/15/29 | | | 96,751 | |

| | 13,031 | | | Series 2247, Class Z, 7.500%, 08/15/30 | | | 15,086 | |

| | 190,784 | | | Series 2259, Class ZC, 7.350%, 10/15/30 | | | 219,180 | |

| | 3,472 | | | Series 2261, Class ZY, 7.500%, 10/15/30 | | | 4,002 | |

| | 35,355 | | | Series 2283, Class K, 6.500%, 12/15/23 | | | 39,338 | |

| | 6,050 | | | Series 2306, Class K, PO, 05/15/24 | | | 5,735 | |

| | 14,521 | | | Series 2306, Class SE, IF, IO, 8.360%, 05/15/24 | | | 1,986 | |

| | 17,509 | | | Series 2325, Class PM, 7.000%, 06/15/31 | | | 20,596 | |

| | 94,492 | | | Series 2344, Class ZD, 6.500%, 08/15/31 | | | 110,704 | |

| | 15,383 | | | Series 2344, Class ZJ, 6.500%, 08/15/31 | | | 17,575 | |

| | 8,819 | | | Series 2345, Class NE, 6.500%, 08/15/31 | | | 10,189 | |

| | 16,617 | | | Series 2345, Class PQ, 6.500%, 08/15/16 | | | 17,066 | |

| | 5,388 | | | Series 2355, Class BP, 6.000%, 09/15/16 | | | 5,500 | |

| | 56,472 | | | Series 2359, Class ZB, 8.500%, 06/15/31 | | | 66,959 | |

| | 137,707 | | | Series 2367, Class ME, 6.500%, 10/15/31 | | | 158,815 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Agency CMO — continued | | | | |

| | 12,977 | | | Series 2390, Class DO, PO, 12/15/31 | | | 12,284 | |

| | 7,940 | | | Series 2391, Class QR, 5.500%, 12/15/16 | | | 8,121 | |

| | 9,642 | | | Series 2394, Class MC, 6.000%, 12/15/16 | | | 9,910 | |

| | 25,260 | | | Series 2410, Class OE, 6.375%, 02/15/32 | | | 27,206 | |

| | 25,390 | | | Series 2410, Class QS, IF, 19.018%, 02/15/32 | | | 39,422 | |

| | 26,971 | | | Series 2410, Class QX, IF, IO, 8.465%, 02/15/32 | | | 8,593 | |

| | 30,027 | | | Series 2412, Class SP, IF, 15.729%, 02/15/32 | | | 44,083 | |

| | 55,560 | | | Series 2423, Class MC, 7.000%, 03/15/32 | | | 63,991 | |

| | 90,103 | | | Series 2423, Class MT, 7.000%, 03/15/32 | | | 103,840 | |

| | 193,885 | | | Series 2435, Class CJ, 6.500%, 04/15/32 | | | 224,941 | |

| | 35,105 | | | Series 2444, Class ES, IF, IO, 7.765%, 03/15/32 | | | 9,366 | |

| | 23,403 | | | Series 2450, Class SW, IF, IO, 7.815%, 03/15/32 | | | 6,282 | |

| | 78,865 | | | Series 2455, Class GK, 6.500%, 05/15/32 | | | 91,839 | |

| | 44,343 | | | Series 2484, Class LZ, 6.500%, 07/15/32 | | | 51,230 | |

| | 187,458 | | | Series 2500, Class MC, 6.000%, 09/15/32 | | | 214,029 | |

| | 6,462 | | | Series 2503, Class BH, 5.500%, 09/15/17 | | | 6,723 | |

| | 63,179 | | | Series 2527, Class BP, 5.000%, 11/15/17 | | | 65,344 | |

| | 63,077 | | | Series 2535, Class BK, 5.500%, 12/15/22 | | | 68,743 | |

| | 1,900,948 | | | Series 2543, Class YX, 6.000%, 12/15/32 | | | 2,143,881 | |

| | 129,047 | | | Series 2544, Class HC, 6.000%, 12/15/32 | | | 146,127 | |

| | 253,222 | | | Series 2575, Class ME, 6.000%, 02/15/33 | | | 277,783 | |

| | 514,276 | | | Series 2578, Class PG, 5.000%, 02/15/18 | | | 533,236 | |

| | 19,982 | | | Series 2586, Class WI, IO, 6.500%, 03/15/33 | | | 4,199 | |

| | 24,700 | | | Series 2626, Class NS, IF, IO, 6.365%, 06/15/23 | | | 1,593 | |

| | 27,992 | | | Series 2638, Class DS, IF, 8.415%, 07/15/23 | | | 33,274 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 8 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Agency CMO — continued | | | | |

| | 100,821 | | | Series 2647, Class A, 3.250%, 04/15/32 | | | 105,702 | |

| | 303,253 | | | Series 2651, Class VZ, 4.500%, 07/15/18 | | | 316,431 | |

| | 600,821 | | | Series 2656, Class BG, 5.000%, 10/15/32 | | | 629,649 | |

| | 61,958 | | | Series 2682, Class LC, 4.500%, 07/15/32 | | | 63,192 | |

| | 5,233 | | | Series 2780, Class JG, 4.500%, 04/15/19 | | | 5,366 | |

| | 289,767 | | | Series 2827, Class DG, 4.500%, 07/15/19 | | | 302,576 | |

| | 3,959 | | | Series 2989, Class PO, PO, 06/15/23 | | | 3,804 | |

| | 300,000 | | | Series 3047, Class OD, 5.500%, 10/15/35 | | | 338,096 | |

| | 143,233 | | | Series 3085, Class VS, HB, IF, 27.978%, 12/15/35 | | | 247,951 | |

| | 48,139 | | | Series 3117, Class EO, PO, 02/15/36 | | | 44,419 | |

| | 47,882 | | | Series 3260, Class CS, IF, IO, 5.955%, 01/15/37 | | | 7,980 | |

| | 105,539 | | | Series 3385, Class SN, IF, IO, 5.815%, 11/15/37 | | | 15,892 | |

| | 119,502 | | | Series 3387, Class SA, IF, IO, 6.235%, 11/15/37 | | | 17,771 | |

| | 81,771 | | | Series 3451, Class SA, IF, IO, 5.865%, 05/15/38 | | | 12,424 | |

| | 349,831 | | | Series 3455, Class SE, IF, IO, 6.015%, 06/15/38 | | | 49,491 | �� |

| | 313,603 | | | Series 3688, Class NI, IO, 5.000%, 04/15/32 | | | 24,005 | |

| | 110,639 | | | Series 3759, Class HI, IO, 4.000%, 08/15/37 | | | 9,619 | |

| | 131,066 | | | Series 3772, Class IO, IO, 3.500%, 09/15/24 | | | 4,994 | |

| | | | Federal Home Loan Mortgage Corp. STRIPS, | | | | |

| | 108,676 | | | Series 233, Class 11, IO, 5.000%, 09/15/35 | | | 23,986 | |

| | 128,634 | | | Series 239, Class S30, IF, IO, 7.515%, 08/15/36 | | | 26,407 | |

| | 417,837 | | | Series 262, Class 35, 3.500%, 07/15/42 | | | 429,404 | |

| | 430,137 | | | Series 299, Class 300, 3.000%, 01/15/43 | | | 437,963 | |

| | | | Federal Home Loan Mortgage Corp. Structured Pass-Through Securities, | | | | |

| | 14,647 | | | Series T-41, Class 3A, VAR, 6.152%, 07/25/32 | | | 16,656 | |

| | 97,646 | | | Series T-54, Class 2A, 6.500%, 02/25/43 | | | 114,573 | |

| | 44,991 | | | Series T-54, Class 3A, 7.000%, 02/25/43 | | | 54,659 | |

| | 196,960 | | | Series T-56, Class APO, PO, 05/25/43 | | | 157,028 | |

| | 25,235 | | | Series T-58, Class APO, PO, 09/25/43 | | | 20,376 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Agency CMO — continued | | | | |

| | | | Federal National Mortgage Association - ACES, | | | | |

| | 1,000,000 | | | Series 2014-M3, Class A2, VAR, 3.501%, 01/25/24 | | | 1,049,394 | |

| | 1,000,000 | | | Series 2015-M3, Class A2, 2.723%, 10/25/24 | | | 987,306 | |

| | 389,000 | | | Series 2015-M10, Class A2, VAR, 3.092%, 04/25/27 | | | 385,091 | |

| | | | Federal National Mortgage Association REMIC, | | | | |

| | 2,585 | | | Series 1988-16, Class B, 9.500%, 06/25/18 | | | 2,737 | |

| | 2,719 | | | Series 1989-83, Class H, 8.500%, 11/25/19 | | | 2,999 | |

| | 594 | | | Series 1990-1, Class D, 8.800%, 01/25/20 | | | 658 | |

| | 3,682 | | | Series 1990-10, Class L, 8.500%, 02/25/20 | | | 4,078 | |

| | 395 | | | Series 1990-93, Class G, 5.500%, 08/25/20 | | | 420 | |

| | 11 | | | Series 1990-140, Class K, HB, 652.145%, 12/25/20 | | | 76 | |

| | 757 | | | Series 1990-143, Class J, 8.750%, 12/25/20 | | | 858 | |

| | 16,561 | | | Series 1992-101, Class J, 7.500%, 06/25/22 | | | 18,477 | |

| | 6,599 | | | Series 1992-143, Class MA, 5.500%, 09/25/22 | | | 7,099 | |

| | 22,626 | | | Series 1993-146, Class E, PO, 05/25/23 | | | 21,720 | |

| | 51,845 | | | Series 1993-155, Class PJ, 7.000%, 09/25/23 | | | 59,073 | |

| | 1,672 | | | Series 1993-165, Class SD, IF, 13.414%, 09/25/23 | | | 2,204 | |

| | 8,338 | | | Series 1993-165, Class SK, IF, 12.500%, 09/25/23 | | | 9,836 | |

| | 71,262 | | | Series 1993-203, Class PL, 6.500%, 10/25/23 | | | 81,853 | |

| | 7,470 | | | Series 1993-205, Class H, PO, 09/25/23 | | | 7,158 | |

| | 317,455 | | | Series 1993-223, Class PZ, 6.500%, 12/25/23 | | | 346,710 | |

| | 73,274 | | | Series 1993-225, Class UB, 6.500%, 12/25/23 | | | 81,942 | |

| | 2,130 | | | Series 1993-230, Class FA, VAR, 0.787%, 12/25/23 | | | 2,162 | |

| | 9,729 | | | Series 1993-250, Class Z, 7.000%, 12/25/23 | | | 9,737 | |

| | 178,694 | | | Series 1994-37, Class L, 6.500%, 03/25/24 | | | 205,252 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 9 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Agency CMO — continued | | | | |

| | 1,495,151 | | | Series 1994-72, Class K, 6.000%, 04/25/24 | | | 1,697,081 | |

| | 15,975 | | | Series 1995-2, Class Z, 8.500%, 01/25/25 | | | 18,420 | |

| | 83,206 | | | Series 1995-19, Class Z, 6.500%, 11/25/23 | | | 95,572 | |

| | 3,132 | | | Series 1996-59, Class J, 6.500%, 08/25/22 | | | 3,402 | |

| | 100,033 | | | Series 1997-20, Class IB, IO, VAR, 1.840%, 03/25/27 | | | 4,451 | |

| | 15,734 | | | Series 1997-39, Class PD, 7.500%, 05/20/27 | | | 18,478 | |

| | 27,914 | | | Series 1997-46, Class PL, 6.000%, 07/18/27 | | | 31,349 | |

| | 70,114 | | | Series 1997-61, Class ZC, 7.000%, 02/25/23 | | | 78,697 | |

| | 11,367 | | | Series 1998-36, Class ZB, 6.000%, 07/18/28 | | | 12,916 | |

| | 25,836 | | | Series 1998-43, Class SA, IF, IO, 17.727%, 04/25/23 | | | 6,179 | |

| | 37,679 | | | Series 1998-46, Class GZ, 6.500%, 08/18/28 | | | 43,280 | |

| | 69,322 | | | Series 1998-58, Class PC, 6.500%, 10/25/28 | | | 78,024 | |

| | 161,667 | | | Series 1999-39, Class JH, IO, 6.500%, 08/25/29 | | | 22,901 | |

| | 5,026 | | | Series 2000-52, Class IO, IO, 8.500%, 01/25/31 | | | 1,033 | |

| | 61,304 | | | Series 2001-4, Class PC, 7.000%, 03/25/21 | | | 66,684 | |

| | 50,436 | | | Series 2001-30, Class PM, 7.000%, 07/25/31 | | | 57,547 | |

| | 181,179 | | | Series 2001-33, Class ID, IO, 6.000%, 07/25/31 | | | 27,153 | |

| | 77,064 | | | Series 2001-36, Class DE, 7.000%, 08/25/31 | | | 89,667 | |

| | 8,754 | | | Series 2001-44, Class PD, 7.000%, 09/25/31 | | | 9,909 | |

| | 2,529 | | | Series 2001-52, Class XN, 6.500%, 11/25/15 | | | 2,543 | |

| | 132,287 | | | Series 2001-61, Class Z, 7.000%, 11/25/31 | | | 149,686 | |

| | 10,772 | | | Series 2001-69, Class PG, 6.000%, 12/25/16 | | | 10,973 | |

| | 6,960 | | | Series 2001-71, Class QE, 6.000%, 12/25/16 | | | 7,120 | |

| | 18,298 | | | Series 2002-1, Class HC, 6.500%, 02/25/22 | | | 20,361 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Agency CMO — continued | | | | |

| | 6,965 | | | Series 2002-1, Class SA, HB, IF, 24.580%, 02/25/32 | | | 12,149 | |

| | 14,956 | | | Series 2002-2, Class UC, 6.000%, 02/25/17 | | | 15,404 | |

| | 11,879 | | | Series 2002-3, Class OG, 6.000%, 02/25/17 | | | 12,126 | |

| | 167,726 | | | Series 2002-13, Class SJ, IF, IO, 1.600%, 03/25/32 | | | 9,238 | |

| | 132,807 | | | Series 2002-15, Class PO, PO, 04/25/32 | | | 124,744 | |

| | 60,582 | | | Series 2002-28, Class PK, 6.500%, 05/25/32 | | | 67,695 | |

| | 110,763 | | | Series 2002-62, Class ZE, 5.500%, 11/25/17 | | | 115,145 | |

| | 120,192 | | | Series 2002-68, Class SH, IF, IO, 7.815%, 10/18/32 | | | 31,915 | |

| | 12,806 | | | Series 2002-77, Class S, IF, 14.140%, 12/25/32 | | | 17,203 | |

| | 61,917 | | | Series 2002-94, Class BK, 5.500%, 01/25/18 | | | 63,666 | |

| | 230,390 | | | Series 2003-7, Class A1, 6.500%, 12/25/42 | | | 268,053 | |

| | 293,000 | | | Series 2003-22, Class UD, 4.000%, 04/25/33 | | | 308,404 | |

| | 62,733 | | | Series 2003-44, Class IU, IO, 7.000%, 06/25/33 | | | 15,246 | |

| | 46,903 | | | Series 2003-47, Class PE, 5.750%, 06/25/33 | | | 53,228 | |

| | 10,230 | | | Series 2003-64, Class SX, IF, 13.290%, 07/25/33 | | | 12,707 | |

| | 13,998 | | | Series 2003-66, Class PA, 3.500%, 02/25/33 | | | 14,475 | |

| | 42,189 | | | Series 2003-71, Class DS, IF, 7.221%, 08/25/33 | | | 42,773 | |

| | 45,338 | | | Series 2003-80, Class SY, IF, IO, 7.463%, 06/25/23 | | | 2,864 | |

| | 599,709 | | | Series 2003-81, Class MC, 5.000%, 12/25/32 | | | 626,420 | |

| | 419,690 | | | Series 2003-82, Class VB, 5.500%, 08/25/33 | | | 433,155 | |

| | 19,107 | | | Series 2003-91, Class SD, IF, 12.188%, 09/25/33 | | | 24,112 | |

| | 167,364 | | | Series 2003-116, Class SB, IF, IO, 7.413%, 11/25/33 | | | 42,245 | |

| | 940,766 | | | Series 2003-128, Class DY, 4.500%, 01/25/24 | | | 1,003,586 | |

| | 9,478 | | | Series 2003-130, Class SX, IF, 11.240%, 01/25/34 | | | 11,452 | |

| | 24,583 | | | Series 2003-132, Class OA, PO, 08/25/33 | | | 21,785 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 10 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Agency CMO — continued | | | | |

| | 323,999 | | | Series 2004-2, Class OE, 5.000%, 05/25/23 | | | 330,681 | |

| | 79,899 | | | Series 2004-4, Class QM, IF, 13.826%, 06/25/33 | | | 98,648 | |

| | 41,700 | | | Series 2004-10, Class SC, HB, IF, 27.852%, 02/25/34 | | | 57,985 | |

| | 119,530 | | | Series 2004-36, Class SA, IF, 19.011%, 05/25/34 | | | 172,682 | |

| | 73,355 | | | Series 2004-46, Class SK, IF, 15.986%, 05/25/34 | | | 97,345 | |

| | 11,319 | | | Series 2004-51, Class SY, IF, 13.866%, 07/25/34 | | | 15,081 | |

| | 62,281 | | | Series 2004-61, Class SK, IF, 8.500%, 11/25/32 | | | 79,251 | |

| | 41,759 | | | Series 2004-76, Class CL, 4.000%, 10/25/19 | | | 43,200 | |

| | 182,660 | | | Series 2005-45, Class DC, HB, IF, 23.624%, 06/25/35 | | | 287,333 | |

| | 19,585 | | | Series 2005-52, Class PA, 6.500%, 06/25/35 | | | 20,724 | |

| | 312,603 | | | Series 2005-68, Class BC, 5.250%, 06/25/35 | | | 337,409 | |

| | 183,028 | | | Series 2005-84, Class XM, 5.750%, 10/25/35 | | | 198,564 | |

| | 350,308 | | | Series 2005-110, Class MN, 5.500%, 06/25/35 | | | 371,722 | |

| | 70,622 | | | Series 2006-22, Class AO, PO, 04/25/36 | | | 61,426 | |

| | 26,223 | | | Series 2006-46, Class SW, HB, IF, 23.514%, 06/25/36 | | | 35,147 | |

| | 42,047 | | | Series 2006-59, Class QO, PO, 01/25/33 | | | 41,436 | |

| | 77,558 | | | Series 2006-110, Class PO, PO, 11/25/36 | | | 67,067 | |

| | 121,483 | | | Series 2006-117, Class GS, IF, IO, 6.463%, 12/25/36 | | | 21,718 | |

| | 42,337 | | | Series 2007-7, Class SG, IF, IO, 6.313%, 08/25/36 | | | 9,123 | |

| | 205,845 | | | Series 2007-53, Class SH, IF, IO, 5.913%, 06/25/37 | | | 29,313 | |

| | 202,724 | | | Series 2007-88, Class VI, IF, IO, 6.353%, 09/25/37 | | | 30,915 | |

| | 161,571 | | | Series 2007-100, Class SM, IF, IO, 6.263%, 10/25/37 | | | 24,308 | |

| | 159,325 | | | Series 2008-1, Class BI, IF, IO, 5.723%, 02/25/38 | | | 21,325 | |

| | 39,157 | | | Series 2008-16, Class IS, IF, IO, 6.013%, 03/25/38 | | | 6,460 | |

| | 129,738 | | | Series 2008-46, Class HI, IO, VAR, 1.715%, 06/25/38 | | | 10,083 | |

| | 53,849 | | | Series 2008-53, Class CI, IF, IO, 7.013%, 07/25/38 | | | 10,404 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Agency CMO — continued | | | | |

| | 133,949 | | | Series 2009-112, Class ST, IF, IO, 6.063%, 01/25/40 | | | 20,764 | |

| | 74,132 | | | Series 2010-35, Class SB, IF, IO, 6.233%, 04/25/40 | | | 11,745 | |

| | 358,417 | | | Series 2013-128, Class PO, PO, 12/25/43 | | | 277,087 | |

| | 1,686 | | | Series G92-42, Class Z, 7.000%, 07/25/22 | | | 1,855 | |

| | 16,494 | | | Series G92-44, Class ZQ, 8.000%, 07/25/22 | | | 17,344 | |

| | 16,649 | | | Series G92-54, Class ZQ, 7.500%, 09/25/22 | | | 18,310 | |

| | 1,194 | | | Series G92-59, Class F, VAR, 1.380%, 10/25/22 | | | 1,212 | |

| | 3,427 | | | Series G92-61, Class Z, 7.000%, 10/25/22 | | | 3,910 | |

| | 8,057 | | | Series G92-66, Class KA, 6.000%, 12/25/22 | | | 8,787 | |

| | 38,105 | | | Series G92-66, Class KB, 7.000%, 12/25/22 | | | 42,376 | |

| | 10,123 | | | Series G93-1, Class KA, 7.900%, 01/25/23 | | | 11,556 | |

| | 10,792 | | | Series G93-17, Class SI, IF, 6.000%, 04/25/23 | | | 12,302 | |

| | | | Federal National Mortgage Association REMIC Trust, | | | | |

| | 47,462 | | | Series 1999-W1, Class PO, PO, 02/25/29 | | | 44,069 | |

| | 174,029 | | | Series 1999-W4, Class A9, 6.250%, 02/25/29 | | | 192,951 | |

| | 382,180 | | | Series 2002-W7, Class A4, 6.000%, 06/25/29 | | | 418,025 | |

| | 318,626 | | | Series 2003-W1, Class 1A1, VAR, 5.792%, 12/25/42 | | | 355,195 | |

| | 44,509 | | | Series 2003-W1, Class 2A, VAR, 6.475%, 12/25/42 | | | 51,706 | |

| | | | Federal National Mortgage Association STRIPS, | | | | |

| | 10,630 | | | Series 329, Class 1, PO, 4.047%,

01/25/33 (n) | | | 9,779 | |

| | 48,135 | | | Series 365, Class 8, IO, 5.500%, 05/25/36 | | | 11,344 | |

| | 38,061 | | | Federal National Mortgage Association Trust, Series 2004-W2, Class 2A2, 7.000%, 02/25/44 | | | 44,418 | |

| | | | Government National Mortgage Association, | | | | |

| | 128,404 | | | Series 1994-7, Class PQ, 6.500%, 10/16/24 | | | 146,670 | |

| | 77,832 | | | Series 1998-22, Class PD, 6.500%, 09/20/28 | | | 91,121 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 11 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Agency CMO — continued | | | | |

| | 24,799 | | | Series 1999-17, Class L, 6.000%, 05/20/29 | | | 27,905 | |

| | 125,143 | | | Series 2000-21, Class Z, 9.000%, 03/16/30 | | | 153,637 | |

| | 1,620 | | | Series 2000-36, Class IK, IO, 9.000%, 11/16/30 | | | 264 | |

| | 282,675 | | | Series 2000-36, Class PB, 7.500%, 11/16/30 | | | 337,578 | |

| | 858,992 | | | Series 2001-10, Class PE, 6.500%, 03/16/31 | | | 980,406 | |

| | 133,371 | | | Series 2001-22, Class PS, HB, IF, 20.526%, 03/17/31 | | | 211,737 | |

| | 59,918 | | | Series 2001-36, Class S, IF, IO, 7.865%, 08/16/31 | | | 19,035 | |

| | 7,165 | | | Series 2001-53, Class SR, IF, IO, 7.963%, 10/20/31 | | | 61 | |

| | 1,000,000 | | | Series 2001-64, Class PB, 6.500%, 12/20/31 | | | 1,146,343 | |

| | 9,918 | | | Series 2002-24, Class SB, IF, 11.648%, 04/16/32 | | | 13,353 | |

| | 4,804 | | | Series 2003-24, Class PO, PO, 03/16/33 | | | 4,045 | |

| | 245,925 | | | Series 2004-11, Class SW, IF, IO, 5.313%, 02/20/34 | | | 33,939 | |

| | 30,313 | | | Series 2004-28, Class S, IF, 19.154%, 04/16/34 | | | 43,764 | |

| | 166,491 | | | Series 2007-45, Class QA, IF, IO, 6.453%, 07/20/37 | | | 28,841 | |

| | 129,062 | | | Series 2007-76, Class SA, IF, IO, 6.343%, 11/20/37 | | | 22,525 | |

| | 126,455 | | | Series 2008-2, Class MS, IF, IO, 6.975%, 01/16/38 | | | 25,147 | |

| | 87,732 | | | Series 2008-55, Class SA, IF, IO, 6.013%, 06/20/38 | | | 13,313 | |

| | 63,946 | | | Series 2009-6, Class SA, IF, IO, 5.915%, 02/16/39 | | | 8,940 | |

| | 189,029 | | | Series 2009-6, Class SH, IF, IO, 5.853%, 02/20/39 | | | 27,843 | |

| | 132,632 | | | Series 2009-14, Class KI, IO, 6.500%, 03/20/39 | | | 28,993 | |

| | 94,501 | | | Series 2009-14, Class NI, IO, 6.500%, 03/20/39 | | | 18,503 | |

| | 274,889 | | | Series 2009-22, Class SA, IF, IO, 6.083%, 04/20/39 | | | 40,283 | |

| | 4,905 | | | Series 2009-31, Class ST, IF, IO, 6.163%, 03/20/39 | | | 736 | |

| | 248,425 | | | Series 2009-31, Class TS, IF, IO, 6.113%, 03/20/39 | | | 33,749 | |

| | 244,833 | | | Series 2009-64, Class SN, IF, IO, 5.915%, 07/16/39 | | | 30,579 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Agency CMO — continued | | | | |

| | 102,727 | | | Series 2009-79, Class OK, PO, 11/16/37 | | | 94,417 | |

| | 117,400 | | | Series 2009-102, Class SM, IF, IO, 6.215%, 06/16/39 | | | 11,030 | |

| | 426,344 | | | Series 2009-106, Class ST, IF, IO, 5.813%, 02/20/38 | | | 71,382 | |

| | 142,545 | | | Series 2010-130, Class CP, 7.000%, 10/16/40 | | | 169,066 | |

| | 265,297 | | | Series 2011-75, Class SM, IF, IO, 6.413%, 05/20/41 | | | 51,833 | |

| | 839,315 | | | Series 2013-H08, Class FC, VAR, 0.632%, 02/20/63 | | | 840,356 | |

| | 472,261 | | | Series 2013-H09, Class HA, 1.650%, 04/20/63 | | | 470,387 | |

| | 433,209 | | | Series 2014-H17, Class FC, VAR, 0.682%, 07/20/64 | | | 434,633 | |

| | | | Vendee Mortgage Trust, | | | | |

| | 51,852 | | | Series 1994-1, Class 1, VAR, 5.570%, 02/15/24 | | | 56,902 | |

| | 126,327 | | | Series 1996-1, Class 1Z, 6.750%, 02/15/26 | | | 143,943 | |

| | 69,470 | | | Series 1996-2, Class 1Z, 6.750%, 06/15/26 | | | 79,764 | |

| | 250,956 | | | Series 1997-1, Class 2Z, 7.500%, 02/15/27 | | | 294,231 | |

| | 68,007 | | | Series 1998-1, Class 2E, 7.000%, 03/15/28 | | | 81,150 | |

| | | | | | | | |

| | | | | | | 30,046,492 | |

| | | | | | | | |

| | | | Non-Agency CMO — 6.0% | |

| | 104,000 | | | Ajax Mortgage Loan Trust, Series 2015-B, Class A, SUB, 3.875%, 07/25/60 (e) | | | 103,782 | |

| | | | Alternative Loan Trust, | | | | |

| | 1,968,641 | | | Series 2004-2CB, Class 1A9, 5.750%, 03/25/34 | | | 1,983,699 | |

| | 513,908 | | | Series 2005-20CB, Class 3A8, IF, IO, 4.563%, 07/25/35 | | | 63,062 | |

| | 687,908 | | | Series 2005-22T1, Class A2, IF, IO, 4.883%, 06/25/35 | | | 103,253 | |

| | 741,150 | | | Series 2005-28CB, Class 1A4, 5.500%, 08/25/35 | | | 718,794 | |

| | 358,161 | | | Series 2005-54CB, Class 1A11, 5.500%, 11/25/35 | | | 327,200 | |

| | 464,261 | | | Series 2005-J1, Class 1A4, IF, IO, 4.913%, 02/25/35 | | | 43,081 | |

| | | | Banc of America Alternative Loan Trust, | | | | |

| | 245,706 | | | Series 2004-5, Class 3A3, PO, 06/25/34 | | | 206,546 | |

| | 26,482 | | | Series 2004-6, Class 15PO, PO, 07/25/19 | | | 25,650 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 12 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Non-Agency CMO — continued | |

| | | | Banc of America Funding Trust, | | | | |

| | 36,939 | | | Series 2004-1, Class PO, PO, 03/25/34 | | | 30,353 | |

| | 246,145 | | | Series 2005-6, Class 2A7, 5.500%, 10/25/35 | | | 242,517 | |

| | 40,902 | | | Series 2005-7, Class 30PO, PO, 11/25/35 | | | 33,031 | |

| | 148,854 | | | Series 2005-E, Class 4A1, VAR, 2.699%, 03/20/35 | | | 148,357 | |

| | | | Banc of America Mortgage Trust, | | | | |

| | 11,266 | | | Series 2003-8, Class APO, PO, 11/25/33 | | | 9,267 | |

| | 32,929 | | | Series 2004-3, Class 1A26, 5.500%, 04/25/34 | | | 33,512 | |

| | 7,966 | | | Series 2004-4, Class APO, PO, 05/25/34 | | | 6,936 | |

| | 132,417 | | | Series 2004-5, Class 2A2, 5.500%, 06/25/34 | | | 134,928 | |

| | 109,929 | | | Series 2004-6, Class 2A5, PO, 07/25/34 | | | 96,965 | |

| | 26,175 | | | Series 2004-6, Class APO, PO, 07/25/34 | | | 23,428 | |

| | 13,483 | | | Series 2004-7, Class 1A19, PO, 08/25/34 | | | 12,299 | |

| | 101,475 | | | Series 2004-J, Class 3A1, VAR, 2.862%, 11/25/34 | | | 99,503 | |

| | 81,561 | | | BCAP LLC Trust, Series 2011-RR5, Class 11A3, VAR, 0.335%, 05/28/36 (e) | | | 80,320 | |

| | | | Bear Stearns ARM Trust, | | | | |

| | 54,065 | | | Series 2003-7, Class 3A, VAR, 2.482%, 10/25/33 | | | 54,105 | |

| | 92,506 | | | Series 2005-5, Class A1, VAR, 2.160%, 08/25/35 | | | 93,175 | |

| | 316,138 | | | Series 2006-1, Class A1, VAR, 2.360%, 02/25/36 | | | 313,654 | |

| | | | CHL Mortgage Pass-Through Trust, | | | | |

| | 62,161 | | | Series 2004-7, Class 2A1, VAR, 2.506%, 06/25/34 | | | 60,894 | |

| | 38,225 | | | Series 2004-HYB1, Class 2A, VAR, 2.513%, 05/20/34 | | | 36,429 | |

| | 55,429 | | | Series 2004-HYB3, Class 2A, VAR, 2.294%, 06/20/34 | | | 52,637 | |

| | 53,737 | | | Series 2004-J8, Class 1A2, 4.750%, 11/25/19 | | | 55,022 | |

| | 5,484 | | | Series 2004-J8, Class POA, PO, 11/25/19 | | | 5,447 | |

| | 134,978 | | | Series 2005-16, Class A23, 5.500%, 09/25/35 | | | 132,144 | |

| | 289,762 | | | Series 2005-22, Class 2A1, VAR, 2.458%, 11/25/35 | | | 245,534 | |

| | 149,184 | | | Citigroup Mortgage Loan Trust, Series 2010-8, Class 6A6, 4.500%, 12/25/36 (e) | | | 152,182 | |

| | | | Citigroup Mortgage Loan Trust, Inc., | | | | |

| | 6,925 | | | Series 2003-UP3, Class A3, 7.000%, 09/25/33 | | | 7,167 | |

| | 8,687 | | | Series 2003-UST1, Class A1, 5.500%, 12/25/18 | | | 8,725 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Non-Agency CMO — continued | |

| | 2,487 | | | Series 2003-UST1, Class PO1, PO, 12/25/18 | | | 2,367 | |

| | 2,628 | | | Series 2003-UST1, Class PO3, PO, 12/25/18 | | | 2,543 | |

| | 93,962 | | | Series 2005-1, Class 2A1A, VAR, 2.620%, 04/25/35 | | | 73,624 | |

| | 4,177 | | | Credit Suisse First Boston Mortgage Securities Corp., Series 2004-5, Class 5P, PO, 08/25/19 | | | 4,140 | |

| | | | CSMC, | | | | |

| | 157,529 | | | Series 2010-11R, Class A6, VAR, 1.174%, 06/28/47 (e) | | | 151,652 | |

| | 30,837 | | | Series 2011-9R, Class A1, VAR, 2.174%, 03/27/46 (e) | | | 30,877 | |

| | 26,954 | | | FDIC Trust, Series 2013-N1, Class A, 4.500%, 10/25/18 (e) | | | 27,048 | |

| | 205,348 | | | First Horizon Alternative Mortgage Securities Trust, Series 2005-FA8, Class 1A19, 5.500%, 11/25/35 | | | 184,859 | |

| | | | First Horizon Mortgage Pass-Through Trust, | | | | |

| | 190,004 | | | Series 2004-AR7, Class 2A2, VAR, 2.583%, 02/25/35 | | | 190,510 | |

| | 149,104 | | | Series 2005-AR1, Class 2A2, VAR, 2.618%, 04/25/35 | | | 148,782 | |

| | | | GMACM Mortgage Loan Trust, | | | | |

| | 93,881 | | | Series 2003-AR1, Class A4, VAR, 2.917%, 10/19/33 | | | 92,696 | |

| | 90,982 | | | Series 2004-J5, Class A7, 6.500%, 01/25/35 | | | 94,844 | |

| | 470,379 | | | Series 2005-AR3, Class 3A4, VAR, 2.911%, 06/19/35 | | | 462,083 | |

| | | | GSR Mortgage Loan Trust, | | | | |

| | 77,291 | | | Series 2004-6F, Class 1A2, 5.000%, 05/25/34 | | | 78,072 | |

| | 317,979 | | | Series 2004-6F, Class 3A4, 6.500%, 05/25/34 | | | 342,532 | |

| | 90,992 | | | Series 2004-13F, Class 3A3, 6.000%, 11/25/34 | | | 94,475 | |

| | 55,190 | | | Impac Secured Assets Trust, Series 2006-1, Class 2A1, VAR, 0.537%, 05/25/36 | | | 53,413 | |

| | 101,756 | | | JP Morgan Mortgage Trust, Series 2006-A2, Class 5A3, VAR, 2.442%, 11/25/33 | | | 101,916 | |

| | 63,183 | | | MASTR Adjustable Rate Mortgages Trust, Series 2004-13, Class 2A1, VAR, 2.666%, 04/21/34 | | | 63,594 | |

| | | | MASTR Alternative Loan Trust, | | | | |

| | 86,402 | | | Series 2003-9, Class 8A1, 6.000%, 01/25/34 | | | 87,479 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 13 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Non-Agency CMO — continued | |

| | 152,704 | | | Series 2004-4, Class 10A1, 5.000%, 05/25/24 | | | 161,191 | |

| | 183,994 | | | Series 2004-6, Class 7A1, 6.000%, 07/25/34 | | | 187,255 | |

| | 22,029 | | | Series 2004-7, Class 30PO, PO, 08/25/34 | | | 16,999 | |

| | 89,159 | | | Series 2004-8, Class 6A1, 5.500%, 09/25/19 | | | 91,914 | |

| | 71,104 | | | Series 2004-10, Class 1A1, 4.500%, 09/25/19 | | | 72,201 | |

| | | | MASTR Asset Securitization Trust, | | | | |

| | 228,414 | | | Series 2003-11, Class 9A6, 5.250%, 12/25/33 | | | 240,231 | |

| | 7,168 | | | Series 2003-12, Class 15PO, PO, 12/25/18 | | | 7,119 | |

| | 22,247 | | | Series 2004-6, Class 15PO, PO, 07/25/19 | | | 22,059 | |

| | 12,748 | | | Series 2004-8, Class PO, PO, 08/25/19 | | | 11,922 | |

| | 37,299 | | | Series 2004-10, Class 15PO, PO, 10/25/19 | | | 35,246 | |

| | 95,485 | | | MASTR Resecuritization Trust, Series 2005-PO, Class 3PO, PO, 05/28/35 (e) | | | 76,388 | |

| | 55,591 | | | MortgageIT Trust, Series 2005-1, Class 1A1, VAR, 0.827%, 02/25/35 | | | 54,191 | |

| | 46,992 | | | NACC Reperforming Loan REMIC Trust, Series 2004-R2, Class A1, VAR, 6.500%, 10/25/34 (e) | | | 47,118 | |

| | 353,725 | | | PHH Alternative Mortgage Trust, Series 2007-2, Class 2X, IO, 6.000%, 05/25/37 | | | 89,436 | |

| | | | RALI Trust, | | | | |

| | 22,424 | | | Series 2002-QS8, Class A5, 6.250%, 06/25/17 | | | 22,629 | |

| | 706,321 | | | Series 2003-QR19, Class CB4, 5.750%, 10/25/33 | | | 743,976 | |

| | 7,148 | | | Series 2003-QS3, Class A2, IF, 16.089%, 02/25/18 | | | 7,855 | |

| | 53,187 | | | Series 2003-QS9, Class A3, IF, IO, 7.363%, 05/25/18 | | | 4,104 | |

| | 77,407 | | | Series 2003-QS14, Class A1, 5.000%, 07/25/18 | | | 78,483 | |

| | 25,089 | | | Series 2003-QS18, Class A1, 5.000%, 09/25/18 | | | 25,514 | |

| | 5,880 | | | Residential Asset Securitization Trust, Series 2003-A14, Class A1, 4.750%, 02/25/19 | | | 6,006 | |

| | 130,522 | | | RFMSI Trust, Series 2005-SA4, Class 1A1, VAR, 2.671%, 09/25/35 | | | 109,008 | |

| | 4,662 | | | SACO I, Inc., Series 1997-2, Class 1A5, 7.000%, 08/25/36 (e) | | | 4,725 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Non-Agency CMO — continued | |

| | | | Salomon Brothers Mortgage Securities VII, Inc., | | | | |

| | 62,175 | | | Series 2003-HYB1, Class A, VAR, 2.494%, 09/25/33 | | | 62,895 | |

| | 911 | | | Series 2003-UP2, Class PO1, PO, 12/25/18 | | | 806 | |

| | | | Springleaf Mortgage Loan Trust, | | | | |

| | 41,442 | | | Series 2012-2A, Class A, VAR, 2.220%, 10/25/57 (e) | | | 41,545 | |

| | 150,610 | | | Series 2013-1A, Class A, VAR, 1.270%, 06/25/58 (e) | | | 150,425 | |

| | 124,000 | | | Series 2013-1A, Class M1, VAR, 2.310%, 06/25/58 (e) | | | 124,353 | |

| | 108,000 | | | Series 2013-1A, Class M2, VAR, 3.140%, 06/25/58 (e) | | | 108,166 | |

| | 136,807 | | | Series 2013-2A, Class A, VAR, 1.780%, 12/25/65 (e) | | | 137,122 | |

| | 125,000 | | | Series 2013-2A, Class M1, VAR, 3.520%, 12/25/65 (e) | | | 127,296 | |

| | 90,615 | | | Structured Adjustable Rate Mortgage Loan Trust, Series 2004-6, Class 5A4, VAR, 2.357%, 06/25/34 | | | 90,172 | |

| | 94,767 | | | Structured Asset Securities Corp. Mortgage Pass-Through Certificates, Series 2003-33H, Class 1A1, 5.500%, 10/25/33 | | | 96,769 | |

| | | | WaMu Mortgage Pass-Through Certificates Trust, | | | | |

| | 17,658 | | | Series 2003-AR8, Class A, VAR, 2.384%, 08/25/33 | | | 18,122 | |

| | 84,200 | | | Series 2003-AR9, Class 1A6, VAR, 2.409%, 09/25/33 | | | 85,029 | |

| | 1,072 | | | Series 2003-S4, Class 3A, 5.500%, 06/25/33 | | | 1,070 | |

| | 31,233 | | | Series 2004-AR3, Class A2, VAR, 2.459%, 06/25/34 | | | 31,557 | |

| | | | Washington Mutual Mortgage Pass-Through Certificates WMALT Trust, | | | | |

| | 1,246,127 | | | Series 2005-2, Class 1A4, IF, IO, 4.863%, 04/25/35 | | | 188,326 | |

| | 381,536 | | | Series 2005-2, Class 2A3, IF, IO, 4.813%, 04/25/35 | | | 47,899 | |

| | 325,326 | | | Series 2005-3, Class CX, IO, 5.500%, 05/25/35 | | | 67,343 | |

| | 309,940 | | | Series 2005-4, Class CB7, 5.500%, 06/25/35 | | | 284,906 | |

| | 15,477 | | | Series 2005-4, Class DP, PO, 06/25/20 | | | 14,861 | |

| | 104,285 | | | Series 2005-6, Class 2A4, 5.500%, 08/25/35 | | | 99,997 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 14 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Collateralized Mortgage Obligations — continued | | | | |

| | | | Non-Agency CMO — continued | |

| | | | Wells Fargo Mortgage-Backed Securities Trust, | | | | |

| | 24,079 | | | Series 2003-K, Class 1A1, VAR, 2.490%, 11/25/33 | | | 24,170 | |

| | 48,157 | | | Series 2003-K, Class 1A2, VAR, 2.490%, 11/25/33 | | | 48,913 | |

| | 56,197 | | | Series 2004-EE, Class 3A1, VAR, 2.597%, 12/25/34 | | | 56,612 | |

| | 151,231 | | | Series 2004-P, Class 2A1, VAR, 2.626%, 09/25/34 | | | 151,763 | |

| | 282,219 | | | Series 2005-AR3, Class 1A1, VAR, 2.709%, 03/25/35 | | | 284,306 | |

| | 79,352 | | | Series 2005-AR8, Class 2A1, VAR, 2.623%, 06/25/35 | | | 79,724 | |

| | 67,189 | | | Series 2005-AR16, Class 2A1, VAR, 2.601%, 02/25/34 | | | 68,007 | |

| | | | | | | | |

| | | | | | | 12,638,828 | |

| | | | | | | | |

| | | | Total Collateralized Mortgage Obligations

(Cost $39,375,630) | | | 42,685,320 | |

| | | | | | | | |

| Commercial Mortgage-Backed Securities — 2.0% | |

| | | | A10 Securitization LLC, | | | | |

| | 55,832 | | | Series 2013-1, Class A, 2.400%, 11/15/25 (e) | | | 55,989 | |

| | 250,000 | | | Series 2015-1, Class A1, 2.100%, 04/15/34 (e) | | | 249,011 | |

| | 208,401 | | | A10 Term Asset Financing LLC, Series 2013-2, Class A, 2.620%, 11/15/27 (e) | | | 209,600 | |

| | 217,840 | | | Banc of America Commercial Mortgage Trust, Series 2006-4, Class A4, 5.634%, 07/10/46 | | | 223,530 | |

| | 37,752 | | | Banc of America Merrill Lynch Commercial Mortgage, Inc., Series 2005-3, Class AM, 4.727%, 07/10/43 | | | 37,829 | |

| | | | BB-UBS Trust, | | | | |

| | 100,000 | | | Series 2012-SHOW, Class A, 3.430%, 11/05/36 (e) | | | 99,484 | |

| | 100,000 | | | Series 2012-TFT, Class A, 2.892%, 06/05/30 (e) | | | 98,764 | |

| | 331,557 | | | Bear Stearns Commercial Mortgage Securities Trust, Series 2006-PW11, Class A4, VAR, 5.597%, 03/11/39 | | | 335,764 | |

| | 10,092,904 | | | CD Commercial Mortgage Trust, Series 2007-CD4, Class XC, IO, VAR, 0.548%, 12/11/49 (e) | | | 50,818 | |

| | 93,052 | | | Citigroup Commercial Mortgage Trust, Series 2013-SMP, Class A, 2.110%, 01/12/30 (e) | | | 93,933 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | COMM Mortgage Trust, | | | | |

| | 125,000 | | | Series 2013-SFS, Class A2, VAR, 3.086%, 04/12/35 (e) | | | 123,482 | |

| | 200,000 | | | Series 2014-CR19, Class A5, 3.796%, 08/10/47 | | | 207,744 | |

| | 511,494 | | | Commercial Mortgage Pass-Through Certificates, Series 2006-C1, Class A4, VAR, 5.609%, 02/15/39 | | | 515,371 | |

| | | | Federal Home Loan Mortgage Corp., Multifamily Structured Pass-Through Certificates, | | | | |

| | 229,000 | | | Series K038, Class A2, 3.389%, 03/25/24 | | | 238,812 | |

| | 250,000 | | | Series KPLB, Class A, 2.770%, 05/25/25 | | | 244,482 | |

| | 66,838 | | | GMAC Commercial Mortgage Securities, Inc. Trust, Series 2006-C1, Class A4, VAR, 5.238%, 11/10/45 | | | 67,188 | |

| | 122,000 | | | GS Mortgage Securities Corp. Trust, Series 2013-NYC5, Class A, 2.318%,

01/10/30 (e) | | | 123,399 | |

| | 3,156,991 | | | Morgan Stanley Capital I Trust, Series 2006-IQ12, Class X1, IO, VAR, 0.647%, 12/15/43 (e) | | | 17,445 | |

| | 583,593 | | | NCUA Guaranteed Notes Trust, Series 2010-C1, Class APT, 2.650%, 10/29/20 | | | 595,413 | |

| | 116,000 | | | UBS-BAMLL Trust, Series 2012-WRM, Class A, 3.663%, 06/10/30 (e) | | | 119,200 | |

| | 104,000 | | | UBS-Barclays Commercial Mortgage Trust, Series 2012-C2, Class A4, 3.525%, 05/10/63 | | | 107,758 | |

| | 200,000 | | | VNDO Mortgage Trust, Series 2013-PENN, Class A, 3.808%, 12/13/29 (e) | | | 210,886 | |

| | 15,977 | | | Wachovia Bank Commercial Mortgage Trust, Series 2004-C11, Class A5, VAR, 5.215%, 01/15/41 | | | 16,005 | |

| | 110,000 | | | WFRBS Commercial Mortgage Trust, Series 2011-C3, Class A4, 4.375%,

03/15/44 (e) | | | 119,189 | |

| | | | | | | | |

| | | | Total Commercial Mortgage-Backed Securities

(Cost $4,083,643) | | | 4,161,096 | |

| | | | | | | | |

| Corporate Bonds — 15.8% | | | | |

| | | | Consumer Discretionary — 1.3% | | | | |

| | | | Auto Components — 0.0% (g) | | | | |

| | 7,000 | | | Johnson Controls, Inc., 4.950%, 07/02/64 | | | 6,651 | |

| | | | | | | | |

| | | | Automobiles — 0.1% | |

| | 150,000 | | | Daimler Finance North America LLC, 1.875%, 01/11/18 (e) | | | 150,327 | |

| | | | | | | | |

| | | | Hotels, Restaurants & Leisure — 0.0% (g) | |

| | 28,000 | | | Starbucks Corp., 2.700%, 06/15/22 | | | 27,920 | |

| | | | | | | | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | | | |

| | | |

| JUNE 30, 2015 | | JPMORGAN INSURANCE TRUST | | | | | 15 | |

JPMorgan Insurance Trust Core Bond Portfolio

SCHEDULE OF PORTFOLIO INVESTMENTS

AS OF JUNE 30, 2015 (Unaudited) (continued)

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Corporate Bonds — continued | | | | |

| | | | Internet & Catalog Retail — 0.1% | |

| | | | Amazon.com, Inc., | | | | |

| | 66,000 | | | 3.300%, 12/05/21 | | | 66,870 | |

| | 65,000 | | | 4.800%, 12/05/34 | | | 64,564 | |

| | | | | | | | |

| | | | | | | 131,434 | |

| | | | | | | | |

| | | | Media — 1.0% | |

| | | | 21st Century Fox America, Inc., | | | | |

| | 50,000 | | | 6.650%, 11/15/37 | | | 60,846 | |

| | 50,000 | | | 7.250%, 05/18/18 | | | 57,648 | |

| | 150,000 | | | 7.300%, 04/30/28 | | | 185,886 | |

| | | | CBS Corp., | | | | |

| | 21,000 | | | 3.375%, 03/01/22 | | | 20,745 | |

| | 78,000 | | | 3.700%, 08/15/24 | | | 76,217 | |

| | 75,000 | | | Comcast Cable Holdings LLC, 10.125%, 04/15/22 | | | 101,505 | |

| | | | Comcast Corp., | | | | |

| | 39,000 | | | 4.200%, 08/15/34 | | | 37,614 | |

| | 87,000 | | | 4.250%, 01/15/33 | | | 84,965 | |

| | 50,000 | | | 6.450%, 03/15/37 | | | 61,790 | |

| | 30,000 | | | 6.500%, 01/15/17 | | | 32,451 | |

| | 35,000 | | | 6.500%, 11/15/35 | | | 43,548 | |

| | 20,000 | | | Cox Communications, Inc., 8.375%, 03/01/39 (e) | | | 25,496 | |

| | | | DIRECTV Holdings LLC/DIRECTV Financing Co., Inc., | | | | |

| | 25,000 | | | 3.800%, 03/15/22 | | | 25,144 | |

| | 125,000 | | | 4.600%, 02/15/21 | | | 133,168 | |

| | 42,000 | | | 5.000%, 03/01/21 | | | 45,480 | |

| | 125,000 | | | 6.000%, 08/15/40 | | | 129,719 | |

| | | | Discovery Communications LLC, | | | | |

| | 78,000 | | | 4.375%, 06/15/21 | | | 82,053 | |

| | 30,000 | | | 4.950%, 05/15/42 | | | 27,723 | |

| | 100,000 | | | Historic TW, Inc., 9.150%, 02/01/23 | | | 132,103 | |

| | 75,000 | | | NBCUniversal Media LLC, 5.950%, 04/01/41 | | | 87,866 | |

| | | | Thomson Reuters Corp., (Canada), | | | | |

| | 25,000 | | | 3.850%, 09/29/24 | | | 24,843 | |

| | 84,000 | | | 3.950%, 09/30/21 | | | 87,981 | |

| | | | Time Warner Cable, Inc., | | | | |

| | 50,000 | | | 6.550%, 05/01/37 | | | 52,051 | |

| | 50,000 | | | 6.750%, 07/01/18 | | | 55,748 | |

| | 50,000 | | | 7.300%, 07/01/38 | | | 56,335 | |

| | | | Time Warner Entertainment Co. LP, | | | | |

| | 50,000 | | | 8.375%, 03/15/23 | | | 62,156 | |

| | 25,000 | | | 8.375%, 07/15/33 | | | 30,685 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | |

| | | | Media — continued | |

| | | | Time Warner, Inc., | | | | |

| | 35,000 | | | 4.750%, 03/29/21 | | | 37,835 | |

| | 75,000 | | | 6.200%, 03/15/40 | | | 85,203 | |

| | 7,000 | | | 6.250%, 03/29/41 | | | 8,010 | |

| | 15,000 | | | 6.500%, 11/15/36 | | | 17,618 | |

| | | | Viacom, Inc., | | | | |

| | 15,000 | | | 2.750%, 12/15/19 | | | 14,999 | |

| | 22,000 | | | 3.250%, 03/15/23 | | | 20,907 | |

| | 43,000 | | | 3.875%, 12/15/21 | | | 43,620 | |

| | 20,000 | | | 4.500%, 02/27/42 | | | 16,722 | |

| | 16,000 | | | 4.850%, 12/15/34 | | | 14,797 | |

| | 5,000 | | | 6.250%, 04/30/16 | | | 5,220 | |

| | | | | | | | |

| | | | | | | 2,086,697 | |

| | | | | | | | |

| | | | Multiline Retail — 0.0% (g) | |

| | | | Macy’s Retail Holdings, Inc., | | | | |

| | 18,000 | | | 4.375%, 09/01/23 | | | 18,982 | |

| | 26,000 | | | 4.500%, 12/15/34 | | | 24,946 | |

| | 9,000 | | | 5.125%, 01/15/42 | | | 9,041 | |

| | | | | | | | |

| | | | | | | 52,969 | |

| | | | | | | | |

| | | | Specialty Retail — 0.1% | |

| | 28,000 | | | Gap, Inc. (The), 5.950%, 04/12/21 | | | 31,620 | |

| | | | Home Depot, Inc. (The), | | | | |

| | 34,000 | | | 4.250%, 04/01/46 | | | 33,015 | |

| | 70,000 | | | 5.400%, 03/01/16 | | | 72,210 | |

| | 75,000 | | | Lowe’s Cos., Inc., 7.110%, 05/15/37 | | | 97,492 | |

| | | | | | | | |

| | | | | | | 234,337 | |

| | | | | | | | |

| | | | Total Consumer Discretionary | | | 2,690,335 | |

| | | | | | | | |

| | | | Consumer Staples — 0.6% | | | | |

| | | | Beverages — 0.1% | | | | |

| | 23,000 | | | Anheuser-Busch InBev Worldwide, Inc., 7.750%, 01/15/19 | | | 27,300 | |

| | 38,000 | | | Brown-Forman Corp., 4.500%, 07/15/45 | | | 37,607 | |

| | 95,000 | | | Diageo Capital plc, (United Kingdom), 5.750%, 10/23/17 | | | 103,664 | |

| | 20,000 | | | Diageo Finance B.V., (Netherlands), 5.300%, 10/28/15 | | | 20,291 | |

| | | | | | | | |

| | | | | | | 188,862 | |

| | | | | | | | |

| | | | Food & Staples Retailing — 0.2% | | | | |

| | 21,000 | | | Costco Wholesale Corp., 2.250%, 02/15/22 | | | 20,388 | |

| | | | CVS Health Corp., | | | | |

| | 36,000 | | | 4.000%, 12/05/23 | | | 37,187 | |

| | 16,000 | | | 5.300%, 12/05/43 | | | 17,435 | |

SEE NOTES TO FINANCIAL STATEMENTS.

| | | | | | |

| | | |

| 16 | | | | JPMORGAN INSURANCE TRUST | | JUNE 30, 2015 |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| Corporate Bonds — continued | | | | |

| | | | Food & Staples Retailing — continued | |

| | | | Kroger Co. (The), | | | | |

| | 67,000 | | | 4.000%, 02/01/24 | | | 69,198 | |

| | 18,000 | | | 5.400%, 07/15/40 | | | 19,554 | |

| | 25,000 | | | 7.500%, 04/01/31 | | | 32,187 | |

| | 19,000 | | | Sysco Corp., 3.000%, 10/02/21 | | | 19,190 | |

| | 36,000 | | | Walgreens Boots Alliance, Inc.,

3.300%, 11/18/21 | | | 35,750 | |

| | 47,000 | | | 3.800%, 11/18/24 | | | 46,031 | |

| | 23,000 | | | 4.500%, 11/18/34 | | | 21,628 | |

| | 70,000 | | | Wal-Mart Stores, Inc., 6.500%, 08/15/37 | | | 89,958 | |

| | | | | | | | |

| | | | | | | 408,506 | |

| | | | | | | | |

| | | | Food Products — 0.3% | |

| | 25,000 | | | Archer-Daniels-Midland Co., 5.935%, 10/01/32 | | | 30,038 | |

| | 55,000 | | | Bunge Ltd. Finance Corp., 8.500%, 06/15/19 | | | 66,488 | |

| | 27,000 | | | Bunge N.A. Finance LP, 5.900%, 04/01/17 | | | 28,843 | |

| | 8,000 | | | ConAgra Foods, Inc., 2.100%, 03/15/18 | | | 7,922 | |

| | 33,000 | | | HJ Heinz Co., 5.000%, 07/15/35 (e) | | | 33,397 | |

| | 13,000 | | | Kellogg Co., 1.750%, 05/17/17 | | | 13,067 | |

| | | | Kraft Foods Group, Inc., | | | | |

| | 35,000 | | | 3.500%, 06/06/22 | | | 35,086 | |

| | 31,000 | | | 5.375%, 02/10/20 | | | 34,602 | |

| | 122,000 | | | 6.125%, 08/23/18 | | | 136,422 | |

| | 100,000 | | | 6.875%, 01/26/39 | | | 122,541 | |

| | 75,000 | | | Mondelez International, Inc., 4.000%, 02/01/24 | | | 77,679 | |

| | 49,000 | | | Tyson Foods, Inc., 3.950%, 08/15/24 | | | 49,359 | |

| | | | | | | | |

| | | | | | | 635,444 | |

| | | | | | | | |

| | | | Household Products — 0.0% (g) | | | | |

| | 57,242 | | | Procter & Gamble - ESOP, Series A, 9.360%, 01/01/21 | | | 69,574 | |

| | | | | | | | |

| | | | Total Consumer Staples | | | 1,302,386 | |

| | | | | | | | |

| | | | Energy — 2.0% | | | | |

| | | | Energy Equipment & Services — 0.1% | | | | |

| | 21,000 | | | Diamond Offshore Drilling, Inc., 4.875%, 11/01/43 | | | 16,644 | |

| | 9,000 | | | Ensco plc, (United Kingdom), 5.200%, 03/15/25 | | | 8,911 | |

| | 54,000 | | | Halliburton Co., 3.500%, 08/01/23 | | | 54,548 | |

| | 30,000 | | | Nabors Industries, Inc., 5.000%, 09/15/20 | | | 31,233 | |

| | | | Noble Holding International Ltd., (Cayman Islands), | | | | |

| | 5,000 | | | 3.950%, 03/15/22 | | | 4,607 | |

| | 6,000 | | | 4.000%, 03/16/18 | | | 6,143 | |

| | | | | | | | |

PRINCIPAL

AMOUNT($) | | | SECURITY DESCRIPTION | | VALUE($) | |

| | | | | | | | |

| | | | | | | | |

| | | | Energy Equipment & Services — continued | | | | |

| | 25,000 | | | 6.050%, 03/01/41 | | | 20,715 | |

| | 18,000 | | | 6.950%, 04/01/45 | | | 16,578 | |

| | | | Transocean, Inc., (Cayman Islands), | | | | |

| | 42,000 | | | 6.500%, 11/15/20 | | | 38,903 | |

| | 51,000 | | | 6.875%, 12/15/21 | | | 45,900 | |

| | 14,000 | | | 7.850%, 12/15/41 | | | 11,200 | |

| | | | | | | | |

| | | | | | | 255,382 | |

| | | | | | | | |

| | | | Oil, Gas & Consumable Fuels — 1.9% | | | | |

| | 50,000 | | | Apache Corp., 6.900%, 09/15/18 | | | 57,226 | |

| | 18,000 | | | Boardwalk Pipelines LP, 4.950%, 12/15/24 | | | 17,652 | |

| | | | BP Capital Markets plc, (United Kingdom), | | | | |

| | 121,000 | | | 2.750%, 05/10/23 | | | 115,730 | |

| | 15,000 | | | 3.506%, 03/17/25 | | | 14,792 | |

| | 150,000 | | | 4.742%, 03/11/21 | | | 165,520 | |

| | | | Buckeye Partners LP, | | | | |

| | 30,000 | | | 4.350%, 10/15/24 | | | 29,412 | |

| | 15,000 | | | 4.875%, 02/01/21 | | | 15,640 | |