| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | August 31, 2011 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . 18.9 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07986 |

|

The Alger Institutional Funds |

(Exact name of registrant as specified in charter) |

|

111 Fifth Avenue New York, New York | | 10003 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes Fred Alger Management, Inc. 111 Fifth Avenue New York, New York 10003 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | October 31, 2010 | |

| | | | | | | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

The Alger

Institutional Funds

ANNUAL REPORT | |

October 31, 2010 | |

Table of Contents

THE ALGER INSTITUTIONAL FUNDS

Letter to Our Shareholders (Unaudited) | 1 |

| |

Fund Highlights (Unaudited) | 10 |

| |

Portfolio Summary (Unaudited) | 14 |

| |

Schedules of Investments | 15 |

| |

Statements of Assets and Liabilities | 36 |

| |

Statements of Operations | 38 |

| |

Statements of Changes in Net Assets | 40 |

| |

Financial Highlights | 42 |

| |

Notes to Financial Statements | 50 |

| |

Report of Independent Registered Public Accounting Firm | 64 |

| |

Additional Information (Unaudited) | 65 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Dear Shareholders, | | December 3, 2010 |

Equities Rally on Corporate Earnings

Sometimes the strongest drivers of market performance receive the least amount of media attention. That was clearly the case during the 12-month period ended October 31, 2010. As the period progressed, soothsayers of gloom increasingly basked in the limelight of the media to discuss the possibility of the U.S. slipping into a double-dip recession. Other pundits discussed persistently high unemployment and the possibility of America being hit with deflation. Yet as the media embraced an increasingly negative economic outlook, corporations continued to announce strong quarterly results, continuing a trend of surprisingly resilient earnings, high levels of free cash flow, and strong incremental profit margins. The markets, we believe, responded to these fundamentals of investing with the S&P 500 Index posting a 16.52% return for the reporting period.

During the 12-month period, mid and small cap equities outperformed large cap stocks while growth stocks outperformed value. The Russell Midcap Index posted a 27.71% return, compared to the 26.58% return of the small cap Russell 2000 Index and to the 17.67% return of the large cap Russell 1000 Index. Among small caps, the Russell 2000 Growth Index return of 28.67% outpaced the 24.43% return of the Russell 2000 Value Index. In mid caps, growth returned 28.03% as measured by the Russell Midcap Growth Index, outpacing the 27.49% return of the Russell Midcap Value Index. In the large cap category, the Russell 1000 Growth Index posted a 19.65% return, substantially outperforming the 15.71% return of the Russell 1000 Value Index.

Market Volatility Thrives

Despite solid market gains for the 12-month period, volatility thrived with the S&P 500 Index declining 11.4% during the second quarter of 2010. Volatility was driven, in large part, by fears of a slowing U.S. economic recovery. The country’s unemployment rate lingered at or above 9.5% and weakness in real estate persisted, despite mortgage rates dropping to record low levels. Investors’ concerns over health care reform, proposed regulations of financial firms, and the military conflict in Afghanistan also drove volatility. In Europe, meanwhile, the sovereign debt crisis lingered, even as countries such as Ireland, Portugal, Greece, and Spain launched austerity programs to improve their ability to make bond payments.

The volatility was no surprise to the Alger investment team. Indeed, in the later portion of 2009 and in August of this year, we conveyed our belief that ongoing market volatility would create opportunities to purchase attractively valued growth companies during market dips and that equities would advance in the foreseeable future. Our summer observation was timely as the S&P 500 gained 8.92% in September. Our forecast for long-term market gains, meanwhile, is also on track, with the S&P 500 index having gained 80.96% from the market low of March 9, 2009.

1

Corporations Produce Strong Earnings

Against the backdrop of a challenging economy, corporations generated strong earnings during the 12-month period. Many companies continued to benefit from cost cutting measures, improvements in operating efficiency, and growing revenues from overseas markets. In the process, they produced strong levels of free cash flow and they accumulated impressive amounts of cash. Indeed, by the end of March, non-financial corporations held $1.8 trillion in liquid assets, which is comparable to the combined amount of stimulus spending approved by Congress and the White House in 2008 and 2009.

What is even more encouraging is that manufacturers and other corporations started using their cash to make strategic acquisitions, launch share buyback programs, increase dividends, and engage in capital expenditures. This continuation of increased corporate spending in capital expenditures, sales initiatives, and marketing activities is a strong positive for many industries and a reminder that while the U.S. economy is no longer dominated by manufacturing companies, the sector is far from irrelevant. Additionally, business spending on PCs, data storage equipment, and software continued to strengthen during the 12-month period. Encouragingly, our analysts’ research suggests that equipment orders for leading machinery, industrial, and engineering companies will continue to be in the “recovery mode.”

Throughout the reporting period, we maintained that U.S. equity valuations were highly attractive. This view was supported by those who would know best: the CEOs and boards of corporate America. With historically low interest rates and corporations’ deep coffers, U.S. companies have been making investments in something they know better than anyone: their own equities. So far this year, for example, corporations have announced nearly $243 billion in share buybacks, compared to $125 billion for all of last year, according to data from equity research firm Birinyi Associates, Inc.

An increase in merger and acquisition activity also supports our view that equities are attractively valued. Deals announced during the first 11 months of 2010 had a total value of $2.08 trillion, up from $1.70 trillion for the first 11 months of 2009, according to Bloomberg data. Of particular interest was the bidding war between Hewlett-Packard Co. and Dell Inc. for storage specialist 3Par during the third quarter. Hewlett-Packard won with a bid exceeding $2.35 billion. Other deals included Intel Corp.’s acquisition of security-software maker McAfee Inc. and consumer-goods company Unilever’s acquisition of hair care products company Alberto-Culver Co.

Some analysts have said that deals are being completed at excessively high valuations. For example, Hewlett-Packard paid about 10 times the value of 3Par’s estimated annual sales to acquire the company, according to investment banking firm Kaufman Bros. By comparison, EMC Corp. and NetApp Inc., two of the leading (but also large) storage specialists trade at three to four times their sales.

2

Yet, we maintain that viewing recent deal valuations as excessive fails to consider the adverse impacts upon companies that fail to execute in high growth markets. When considering such adverse impact, the strategic significance of acquisitions of high growth companies like 3Par becomes clear. By failing to internally develop capabilities or to make acquisitions, the “missed opportunity” for HP or Dell is not simply slower growth, but the “enhanced risk” that the new high growth market served by 3Par will erode either company’s present business in data storage, for example. Winners and losers today are created faster than ever, and in this competitive landscape, sitting still is not an option. While technology as a tool is a primary agent for the transmission of “creative destruction” within an industry at a faster and more devastating pace than ever before, this phenomenon occurs in every industry today. Indeed, retailers like Barnes & Noble, Inc. or Mervyn’s department stores and media giants such as newspaper publishers and radio broadcasters that failed to respond aggressively to the rise of new forms of competition for their goods, services and advertising platforms suffered from a serious decline in their core business and they missed strong growth opportunities. Thus, the value of entry and of position at the table of a high growth market is both future growth opportunities and, likely, the ability to manage (but not avoid) the decline of a core business.

Finally, on the financial ledgers, corporate America looks not only strong, but willing to share with stakeholders. The benefits of large cash balances were reflected in dividends. Many companies implemented dividends and a flurry of other companies with dividend programs said they will increase the amount that they pay. In fact, some 37% of S&P 500 companies either started dividend payments in 2010 or announced that they will increase their dividends, according to data from FactSet. Dividend payments, of course, will help stimulate the economy by increasing income for shareholders. Perhaps more importantly, dividends will begin to compete for investing dollars with the paltry bond yields in the market today. Why own a 10-year bond yielding 2.4% when you can own stock with a 2% dividend and earnings or free cash flow yields of 8%, 9%, or 10%?

Investors Look to the Fed

Strong corporate earnings clearly drove equity gains during the 12-month period, but stocks also received additional support from expectations that the Federal Reserve would roll out additional stimulus. As the 12-month period progressed, continuing weakness in real estate, the labor market and GDP growth caused the expectations to grow, helping the S&P 500 climb 3.7% in October.

The Road Ahead

Going forward, we believe uncertainty over economic growth will continue to drive equity market volatility, while the sovereign debt crisis in Europe may also provoke angst among investors. Yet, we are encouraged to observe that European countries are pushing forward with austerity programs to improve their ability to service debt and that the European Financial Stability Facility (the Facility), which was created to assist in the crisis, has received preliminary credit ratings of AAA from Moody’s Investors Service Inc, Standard & Poor’s [a division of McGraw-Hill Companies], and Fitch Inc. The Facility currently has 440 billion euros in assets while the

3

International Monetary Fund has earmarked an additional 750 billion euros to assist governments that may be in danger of defaulting.

Domestically, we also expect investors to remain concerned about high rates of unemployment and weakness in real estate. We note, however, that job creation and improvements in real estate often occur in the later stages of economic recoveries, so while we would like to see those areas strengthen, we do not believe they point to a decline in the health of the U.S. At the same time, pockets of improvement in real estate exist. In Jacksonville, Florida, for example, vacancy rates for office and industrial properties declined during the third quarter, while in Manhattan, residential sales climbed. We also note that on both sides of the Atlantic, central bankers remain highly vigilant and, we are confident, ready to act to support the recovery today and for quite a while.

Robust emerging markets growth, meanwhile, may help lift the U.S. economy and markets. China may lead the process with its gross domestic product for this year expected to grow 10.5%, according to the International Monetary Fund. Strong growth won’t be limited to China: The IMF expects overall GDP for emerging markets to grow 6.5% this year. India, Brazil, and other emerging markets similarly support our long-held view that “global growth” is an investable theme for U.S. equity investors.

In closing, we continue to believe that research is the cornerstone of superior portfolio management, regardless of economic conditions. We believe our proven and disciplined process for identifying companies experiencing Positive Dynamic Change will continue to produce superior long-term investment results for our clients.

Portfolio Matters

Alger Capital Appreciation Institutional Fund

The Alger Capital Appreciation Institutional Fund returned 17.69% for the 12-month period ended October 31, 2010, compared to the Russell 3000 Growth Index return of 20.31%.

During the period, the largest sector weightings in the Fund were in Information Technology and Health Care sectors. The largest sector overweight for the period was in Information Technology and the largest sector underweight for the period was in Consumer Staples. Relative outperformance in the Materials and Information Technology sectors was the most important contributor to performance, while sectors that detracted from the portfolio included Health Care and Consumer Staples.

Among the most important contributors to relative performance were Skyworks Solutions Inc., Patriot Coal Corp., Cliffs Natural Resources Inc., Seagate Technology PLC, and Focus Media Holding Ltd. Conversely, detracting from overall results on a relative basis were Hewlett-Packard Co., Brocade Communications Systems Inc., International Business Machines Corp., Baxter International Inc., and Oracle Corp.

4

Alger Large Cap Growth Institutional Fund

The Alger Large Cap Growth Institutional Fund returned 17.09% for the 12-month period ended October 31, 2010, compared to the 19.65% return of the Russell 1000 Growth Index.

During the period, the largest portfolio weightings in the Fund were in the Information Technology and Health Care sectors. The largest sector overweight for the period was in Financials and the largest sector underweight for the period was in Consumer Discretionary. Relative outperformance in the Materials and Utilities sectors was the most important contributor to performance. Sectors that detracted from performance included Financials and Consumer Discretionary.

Among the most important relative contributors were Burlington Northern, Potash Corporation of Saskatchewan Inc., Carnival Corp., The Boeing Co., and Cognizant Technology Solutions Corp. Conversely, detracting from overall results on a relative basis were Exxon Mobil Corp., Transocean Inc., International Business Machines Corp., Caterpillar Inc., and Baxter International Inc.

Alger Mid Cap Growth Institutional Fund

The Alger Mid Cap Growth Institutional Fund returned 22.75% for the 12-month period ended October 31, 2010, compared to the 28.03% return of the Russell Midcap Growth Index.

During the period, the largest sector weightings for the Fund were in Information Technology and Consumer Discretionary. The largest sector overweight for the period was in Information Technology and the largest sector underweight for the period was in Consumer Staples. Relative outperformance in the Information Technology and Energy sectors was the most important contributor to performance. Sectors that detracted from performance included Industrials and Health Care.

Among the most important contributors to relative performance were Skyworks Solutions Inc., Cliffs Natural Resources Inc., OpenTable Inc., NetFlix Inc., and Human Genome Sciences Inc. Conversely, detracting from overall results on a relative basis were Duoyuan Global Water Inc., NuVasive Inc., Brocade Communications Systems Inc. Select Medical Holdings Corporation, and SmartHeat Inc.

Alger Small Cap Growth Institutional Fund

For the 12-month period ended October 31, 2010, the Alger Small Cap Growth Institutional Fund returned 27.04%, compared to 28.67% return of the Russell 2000 Growth Index.

During the period, the largest sector weightings in the Alger Small Cap Growth Institutional Fund were in Information Technology and Health Care. The largest sector overweight for the period was in Industrials and the largest sector underweight for the period was in Information Technology. Relative outperformance in the

5

Industrials and Energy sectors was the most important contributor to performance. Sectors that detracted from performance included Financials and Health Care.

Among the most important contributors to relative performance were BE Aerospace Inc., Dollar Thrifty Automotive Group Inc., VanceInfo Technologies Inc., Informatica Corp., and OpenTable Inc. Conversely, detracting from overall results on a relative basis were InterMune Inc., Brocade Communications Systems Inc., Sykes Enterprises Inc., VeriFone Systems Inc., and PMI Group Inc.

Respectfully submitted,

Daniel C. Chung, CFA

Chief Investment Officer

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Funds unless proceeded or accompanied by an effective prospectus for the Funds. Funds returns represent the fiscal 12-month period return of Class I shares. The performance data quoted represents past performance, which is not an indication or guarantee of future results. Standardized performance results can be found on the following pages. The investment return and principal value of an investment in a fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Recent performance has been impacted by an unusually strong period in the U.S. equity market and there is no g uarantee that such conditions will be repeated. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the Funds’ management in this report are as of the date of the Shareholders letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable; however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including without limitation, in re sponse to cash flows, inclusion in a benchmark, and risk control. The reference to a

6

specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a portfolio. Please refer to the Schedules of Investments for each fund that is included in this report for a complete list of fund holdings as of October 31, 2010. Securities mentioned in the Shareholders Letter, if not found in the Schedule of Investments, may have been held by the Funds during the fiscal period.

A Word about Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies’ earnings and may be more sensitive to market, political and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small and mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Funds that participate in leveraging, such as the Capital Appreciation Institutional Fund, are subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the Funds’ net asset value can decrease more quickly than if the Funds had not borrowed. For a more detail ed discussion of the risks associated with these Funds, please see the Funds’ Prospectus.

Before investing, carefully consider a fund’s investment objective, risks, charges, and expenses. For a prospectus or a summary prospectus containing this and other information about The Alger Institutional Funds call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

Definitions:

· Standard & Poor’s 500 Index (S&P 500 Index) is an index of 500 leading companies in leading industries in the United States.

· The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on the total market capitalization, which represents 99% of the U.S. Equity Market. The Russell 3000 Growth Index is an unmanaged index designed to measure the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values.

· The Russell 1000 Index measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 92% of the Russell 3000 Index. The Russell 1000 Growth Index is an unmanaged index designed to measure the performance of the largest 1,000 companies in the Russell 3000 Index with higher price-to-book ratios and higher

7

forecasted growth values. The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower expected growth values.

· The Russell Midcap Index measures the performance of the mid-cap segment of the U.S. equity universe. The Russell Midcap Index is a subset of the Russell 1000 Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Russell Midcap Growth Index measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap Value Index measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap Index companies with lower price-to-book ratios and lower forecasted growth valu es.

· The Russell 2500 Index measures the performance of the small to mid-cap segment of the U.S. equity universe, commonly referred to as “smid” cap. The Russell 2500 Index is a subset of the Russell 3000 Index. The Russell 2500 Growth Index measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2500. Growth Index is an unmanaged index designed to measure the performance of the 2,500 smallest companies in the Russell 3000 Index with higher price-to-book ratios and higher forecasted growth values. The Russell 2500 Value Index measures the performance of the small to mid-cap value segment of the U.S. equi ty universe. It includes those Russell 2500 companies with lower price-to-book ratios and lower forecasted growth values.

· The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index representing approximately 8% of the total market capitalization of that index. The Russell 2000 Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Value Index measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower forecasted growth values.

· Observations of buying opportunities during market dips were provided in the Annual Report to Alger Institutional Fund Shareholders, October 31, 2009.

· Bond values are subject to interest rate movements; their market values tend to fall when interest rates rise and to rise when interest rates fall. Bond values may also decline as a result of an issue’s falling credit rating or actual default, and bonds that are backed by assets are subject to prepayment risk; thus the average life of the security may be less than maturity.

· Birinyi Associates, Inc. is a stock market research firm.

· FactSet is a firm that provides market data and analytics to investment firms.

· Bloomberg is a financial publisher and provider of financial data.

8

· Moody’s Investors Service, Standard & Poor’s and Fitch Ratings are credit rating agencies.

· The following companies represented the stated percentage of firm wide assets as of October 31, 2010: Hewlett-Packard, 2.11%; Dell, 0.00%; 3Par, 0.00%; McAfee, 0.00%; Intel, 0.07%; Unilever, 0.00%; Alberto-Culver, 0.00%; Barnes & Noble, Inc., 0.00%; Mervyn’s, 0.00%; EMC Corp., 0.78% and NetApp Inc., 0.13%.

FUND PERFORMANCE AS OF 9/30/10 (Unaudited)

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | SINCE

INCEPTION | |

Alger Capital Appreciation Class I (Inception 11/8/93) | | 8.33 | % | 6.66 | % | (0.82 | )% | 10.86 | % |

Alger Capital Appreciation Class R* (Inception 1/27/03) | | 7.75 | % | 6.11 | % | (1.32 | )% | 10.30 | % |

| | | | | | | | | |

Alger Large Cap Growth Class I (Inception 11/8/93) | | 9.91 | % | (0.59 | )% | (2.94 | )% | 6.80 | % |

Alger Large Cap Growth Class R* (Inception 1/27/03) | | 9.17 | % | (1.12 | )% | (3.44 | )% | 6.26 | % |

| | | | | | | | | |

Alger Mid Cap Growth Class I (Inception 11/8/93) | | 11.47 | % | (0.23 | )% | 0.52 | % | 11.68 | % |

Alger Mid Cap Growth Class R* (Inception 1/27/03) | | 10.95 | % | (0.71 | )% | 0.03 | % | 11.13 | % |

| | | | | | | | | |

Alger Small Cap Growth Class I (Inception 11/8/93) | | 15.74 | % | 3.60 | % | (0.42 | )% | 8.51 | % |

Alger Small Cap Growth Class R* (Inception 1/27/03) | | 15.26 | % | 3.11 | % | (0.89 | )% | 7.99 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

9

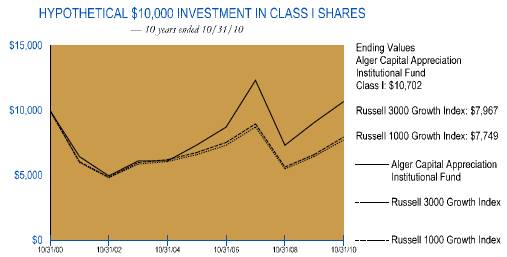

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Fund Highlights Through October 31, 2010 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 3000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2010. Figures for the Alger Capital Appreciation Institutional Fund Class I shares and the Russell 3000 Growth Index include reinvestment of dividends. Performance for the Alger Capital Appreciation Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 10/31/10

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | SINCE

INCEPTION | |

Class I (Inception 11/8/93) | | 17.69 | % | 7.79 | % | 0.68 | % | 11.08 | % |

Class R* (Inception 1/27/03) | | 17.09 | % | 7.24 | % | 0.17 | % | 10.52 | % |

Russell 3000 Growth Index | | 20.31 | % | 3.28 | % | (2.25 | )% | 6.63 | % |

Russell 1000 Growth Index | | 19.65 | % | 3.21 | % | (2.52 | )% | 6.92 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

10

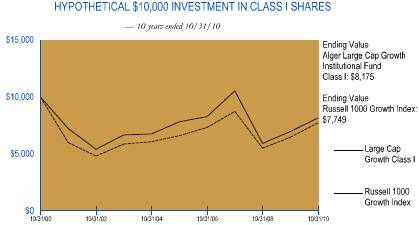

ALGER LARGE CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2010 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Large Cap Growth Institutional Fund Class I shares and the Russell 1000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2010. The figures for the Alger Large Cap Growth Institutional Fund Class I shares and the Russell 1000 Growth Index include reinvestment of dividends. Performance for the Alger Large Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 10/31/10

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | SINCE

INCEPTION | |

Class I (Inception 11/8/93) | | 17.09 | % | 0.87 | % | (1.99 | )% | 7.06 | % |

Class R* (Inception 1/27/03) | | 16.25 | % | 0.32 | % | (2.51 | )% | 6.51 | % |

Russell 1000 Growth Index | | 19.65 | % | 3.21 | % | (2.52 | )% | 6.92 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

11

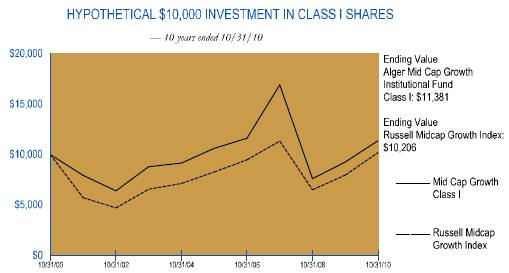

ALGER MID CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2010 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2010 Figures for the Alger Mid Cap Growth Institutional Fund Class I shares and the Russell Midcap Growth Index include reinvestment of dividends. Performance for the Alger Mid Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 10/31/10

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | SINCE

INCEPTION | |

Class I (Inception 11/8/93) | | 22.75 | % | 1.39 | % | 1.30 | % | 11.86 | % |

Class R* (Inception 1/27/03) | | 22.17 | % | 0.89 | % | 0.80 | % | 11.31 | % |

Russell Midcap Growth Index | | 28.03 | % | 4.28 | % | 0.20 | % | 8.06 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

12

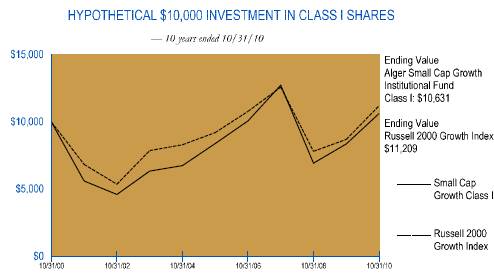

ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Fund Highlights Through October 31, 2010 (Unaudited)

The chart above illustrates the change in value of a hypothetical $10,000 investment made in the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index (an unmanaged index of common stocks) for the ten years ended October 31, 2010. The figures for the Alger Small Cap Growth Institutional Fund Class I shares and the Russell 2000 Growth Index include reinvestment of dividends. Performance for the Alger Small Cap Growth Institutional Fund Class R shares may vary from the results shown above due to differences in expenses the class bears.

PERFORMANCE COMPARISON AS OF 10/31/10

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | SINCE

INCEPTION | |

Class I (Inception 11/8/93) | | 27.04 | % | 4.83 | % | 0.61 | % | 8.67 | % |

Class R* (Inception 1/27/03) | | 26.37 | % | 4.32 | % | 0.14 | % | 8.15 | % |

Russell 2000 Growth Index | | 28.67 | % | 3.99 | % | 1.15 | % | 5.17 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

* | Performance figures prior to 1/27/03, inception of Class R shares, are those of the Fund’s Class I Shares. The performance figures prior to 1/27/03 have been adjusted to reflect the higher operating expenses of Class R shares. |

13

PORTFOLIO SUMMARY*

October 31, 2010 (Unaudited)

SECTORS | | Alger Capital

Appreciation

Institutional Fund | | Alger Large Cap

Growth

Institutional Fund | | Alger Mid Cap

Growth

Institutional Fund | | Alger Small Cap

Growth

Institutional Fund | |

Consumer Discretionary | | 12.6 | % | 10.4 | % | 19.1 | % | 19.0 | % |

Consumer Staples | | 4.8 | | 9.5 | | 1.4 | | 2.7 | |

Energy | | 10.3 | | 8.5 | | 7.9 | | 4.1 | |

Financials | | 5.3 | | 6.6 | | 8.5 | | 3.5 | |

Health Care | | 9.6 | | 11.0 | | 15.3 | | 17.4 | |

Industrials | | 15.3 | | 11.9 | | 15.8 | | 19.0 | |

Information Technology | | 34.1 | | 31.7 | | 25.0 | | 24.5 | |

Materials | | 5.5 | | 4.5 | | 4.6 | | 4.5 | |

Telecommunication Services | | 0.0 | | 0.5 | | 1.3 | | 1.4 | |

Utilities | | 0.0 | | 0.9 | | 0.0 | | 1.1 | |

Short-Term Investments and Net Other Assets | | 2.5 | | 4.5 | | 1.1 | | 2.8 | |

| | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % |

* Based on net assets for each Fund.

14

THE ALGER INSTITUTIONAL FUNDS |

ALGER CAPITAL APPRECIATION INSTITUTIONAL FUND

Schedule of Investments‡ October 31, 2010

| | SHARES | | VALUE | |

COMMON STOCKS—97.5% | | | | | |

ADVERTISING—1.8% | | | | | |

Focus Media Holding Ltd.#* | | 719,800 | | $ | 17,815,050 | |

| | | | | |

AEROSPACE & DEFENSE—1.1% | | | | | |

Goodrich Corp. | | 25,500 | | 2,092,785 | |

United Technologies Corp. | | 110,600 | | 8,269,562 | |

| | | | 10,362,347 | |

AIR FREIGHT & LOGISTICS—3.0% | | | | | |

FedEx Corp. | | 109,900 | | 9,640,428 | |

United Parcel Service Inc., Cl. B | | 307,800 | | 20,727,252 | |

| | | | 30,367,680 | |

AIRLINES—0.9% | | | | | |

United Continental Holdings Inc.* | | 305,100 | | 8,860,104 | |

| | | | | |

APPLICATION SOFTWARE—1.5% | | | | | |

Adobe Systems Inc. * | | 225,100 | | 6,336,565 | |

Mentor Graphics Corp. * | | 522,300 | | 5,640,840 | |

Nice Systems Ltd. #* | | 91,700 | | 3,071,033 | |

| | | | 15,048,438 | |

AUTO PARTS & EQUIPMENT—1.0% | | | | | |

Johnson Controls Inc. | | 46,100 | | 1,619,032 | |

Lear Corp. * | | 92,700 | | 8,194,680 | |

| | | | 9,813,712 | |

BIOTECHNOLOGY—1.7% | | | | | |

Celgene Corp. * | | 65,500 | | 4,065,585 | |

Cephalon Inc. * | | 82,500 | | 5,481,300 | |

Human Genome Sciences Inc. * | | 256,900 | | 6,905,472 | |

| | | | 16,452,357 | |

COAL & CONSUMABLE FUELS—1.4% | | | | | |

Peabody Energy Corp. | | 266,200 | | 14,081,980 | |

| | | | | |

COMMODITY CHEMICALS—0.5% | | | | | |

Celanese Corp. | | 143,900 | | 5,130,035 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—3.4% | | | | | |

Cisco Systems Inc. * | | 546,700 | | 12,481,161 | |

Qualcomm Inc. | | 457,600 | | 20,651,488 | |

| | | | 33,132,649 | |

COMPUTER HARDWARE—10.7% | | | | | |

Apple Inc. * | | 170,900 | | 51,418,683 | |

Hewlett-Packard Co. | | 1,276,600 | | 53,693,796 | |

| | | | 105,112,479 | |

COMPUTER STORAGE & PERIPHERALS—1.6% | | | | | |

EMC Corp.* | | 724,000 | | 15,211,240 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—2.1% | | | | | |

ArvinMeritor Inc. * | | 335,400 | | 5,560,932 | |

Caterpillar Inc. | | 115,400 | | 9,070,440 | |

Cummins Inc. | | 63,100 | | 5,559,110 | |

| | | | 20,190,482 | |

| | | | | | |

15

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

DATA PROCESSING & OUTSOURCED SERVICES—1.2% | | | | | |

Mastercard Inc. | | 48,700 | | $ | 11,690,922 | |

| | | | | |

DEPARTMENT STORES—0.5% | | | | | |

Kohl’s Corp.* | | 101,900 | | 5,217,280 | |

| | | | | |

DIVERSIFIED CHEMICALS—0.3% | | | | | |

Dow Chemical Co., /The | | 95,200 | | 2,935,016 | |

| | | | | |

DIVERSIFIED METALS & MINING—1.9% | | | | | |

Cliffs Natural Resources Inc. | | 169,900 | | 11,077,480 | |

Freeport-McMoRan Copper & Gold Inc. | | 78,700 | | 7,451,316 | |

| | | | 18,528,796 | |

DRUG RETAIL—0.5% | | | | | |

CVS Caremark Corp. | | 155,200 | | 4,674,624 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—0.1% | | | | | |

Emerson Electric Co. | | 18,300 | | 1,004,670 | |

| | | | | |

ENVIRONMENTAL & FACILITIES SERVICES—0.5% | | | | | |

Republic Services Inc. | | 155,400 | | 4,632,474 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—1.3% | | | | | |

CF Industries Holdings Inc. | | 45,400 | | 5,562,862 | |

Mosaic Co., /The | | 98,600 | | 7,213,576 | |

| | | | 12,776,438 | |

FOOTWEAR—0.5% | | | | | |

NIKE Inc., Cl. B | | 60,800 | | 4,951,552 | |

| | | | | |

GOLD—1.1% | | | | | |

Goldcorp Inc. | | 173,700 | | 7,745,283 | |

Yamana Gold Inc. | | 273,100 | | 3,001,369 | |

| | | | 10,746,652 | |

HEALTH CARE EQUIPMENT—1.6% | | | | | |

Covidien PLC | | 329,540 | | 13,138,760 | |

Insulet Corp. * | | 133,500 | | 2,129,325 | |

| | | | 15,268,085 | |

HEALTH CARE FACILITIES—1.0% | | | | | |

Universal Health Services Inc., Cl. B | | 246,600 | | 10,177,182 | |

| | | | | |

HEALTH CARE SERVICES—1.2% | | | | | |

Medco Health Solutions Inc.* | | 231,700 | | 12,171,201 | |

| | | | | |

HOME ENTERTAINMENT SOFTWARE—1.0% | | | | | |

Activision Blizzard Inc. | | 863,400 | | 9,903,198 | |

| | | | | |

HOME IMPROVEMENT RETAIL—1.0% | | | | | |

Lowe’s Companies, Inc. | | 441,100 | | 9,408,663 | |

| | | | | |

HOTELS RESORTS & CRUISE LINES—1.6% | | | | | |

Carnival Corp. | | 101,600 | | 4,386,072 | |

Wyndham Worldwide Corporation | | 397,500 | | 11,428,125 | |

| | | | 15,814,197 | |

HOUSEHOLD APPLIANCES—0.4% | | | | | |

Stanley Black & Decker Inc. | | 60,800 | | 3,767,776 | |

| | | | | | |

16

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HUMAN RESOURCE & EMPLOYMENT SERVICES—0.5% | | | | | |

Towers Watson & Co. | | 96,170 | | $ | 4,945,061 | |

| | | | | |

HYPERMARKETS & SUPER CENTERS—0.9% | | | | | |

Wal-Mart Stores Inc. | | 159,210 | | 8,624,406 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—1.9% | | | | | |

3M Co. | | 97,700 | | 8,228,294 | |

Tyco International Ltd. | | 262,300 | | 10,040,844 | |

| | | | 18,269,138 | |

INDUSTRIAL MACHINERY—2.6% | | | | | |

Flowserve Corp. | | 68,500 | | 6,850,000 | |

Illinois Tool Works Inc. | | 120,100 | | 5,488,570 | |

Ingersoll-Rand PLC | | 341,500 | | 13,424,365 | |

| | | | 25,762,935 | |

INTEGRATED OIL & GAS—2.3% | | | | | |

Chevron Corp. | | 144,800 | | 11,961,928 | |

ConocoPhillips | | 183,200 | | 10,882,080 | |

| | | | 22,844,008 | |

INTERNET RETAIL—2.4% | | | | | |

Amazon.com Inc. * | | 85,900 | | 14,185,526 | |

Expedia Inc. | | 294,300 | | 8,519,985 | |

| | | | 22,705,511 | |

INTERNET SOFTWARE & SERVICES—6.6% | | | | | |

Google Inc., Cl. A * | | 43,000 | | 26,358,570 | |

GSI Commerce Inc. * | | 570,250 | | 13,925,505 | |

IAC/InterActiveCorp. * | | 149,800 | | 4,179,420 | |

Sina Corp. * | | 88,530 | | 4,984,239 | |

VistaPrint Ltd. * | | 150,900 | | 6,348,363 | |

Yahoo! Inc. * | | 544,700 | | 8,992,997 | |

| | | | 64,789,094 | |

INVESTMENT BANKING & BROKERAGE—0.9% | | | | | |

Lazard Ltd., Cl. A | | 134,500 | | 4,963,050 | |

Morgan Stanley | | 164,900 | | 4,101,063 | |

| | | | 9,064,113 | |

IT CONSULTING & OTHER SERVICES—0.7% | | | | | |

International Business Machines Corp. | | 45,100 | | 6,476,360 | |

| | | | | |

LEISURE PRODUCTS—1.6% | | | | | |

Phillips-Van Heusen Corp. | | 256,800 | | 15,752,112 | |

| | | | | |

LIFE & HEALTH INSURANCE—0.9% | | | | | |

MetLife Inc. | | 215,900 | | 8,707,247 | |

| | | | | |

LIFE SCIENCES TOOLS & SERVICES—1.0% | | | | | |

Thermo Fisher Scientific Inc.* | | 197,700 | | 10,165,734 | |

| | | | | |

MANAGED HEALTH CARE—0.4% | | | | | |

Aetna Inc. | | 60,000 | | 1,791,600 | |

WellPoint Inc. * | | 33,100 | | 1,798,654 | |

| | | | 3,590,254 | |

| | | | | | |

17

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

METAL & GLASS CONTAINERS—0.4% | | | | | |

Ball Corp. | | 63,400 | | $ | 4,080,424 | |

| | | | | |

MOVIES & ENTERTAINMENT—0.7% | | | | | |

Walt Disney Co., /The | | 199,300 | | 7,196,723 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—2.5% | | | | | |

Halliburton Company | | 121,500 | | 3,870,990 | |

National Oilwell Varco Inc. | | 176,400 | | 9,483,264 | |

Schlumberger Ltd. | | 162,900 | | 11,385,081 | |

| | | | 24,739,335 | |

OIL & GAS EXPLORATION & PRODUCTION—4.1% | | | | | |

Concho Resources Inc., /Restricted *,(L2),(a) | | 161,985 | | 10,444,976 | |

Devon Energy Corp. | | 165,900 | | 10,786,818 | |

Nexen Inc. | | 514,100 | | 10,945,189 | |

Plains Exploration & Production Co. * | | 248,600 | | 6,928,482 | |

| | | | 39,105,465 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—1.6% | | | | | |

BM&F Bovespa SA | | 551,500 | | 4,620,693 | |

JPMorgan Chase & Co. | | 280,200 | | 10,543,926 | |

| | | | 15,164,619 | |

PHARMACEUTICALS—2.7% | | | | | |

Abbott Laboratories | | 145,700 | | 7,477,324 | |

Allergan Inc. | | 71,700 | | 5,191,797 | |

Auxilium Pharmaceuticals Inc. * | | 137,400 | | 3,400,650 | |

Pfizer Inc. | | 450,000 | | 7,830,000 | |

Teva Pharmaceutical Industries Ltd. # | | 41,900 | | 2,174,610 | |

| | | | 26,074,381 | |

PROPERTY & CASUALTY INSURANCE—0.7% | | | | | |

Travelers Cos., Inc., /The | | 124,800 | | 6,888,960 | |

| | | | | |

RAILROADS—1.3% | | | | | |

CSX Corp. | | 175,800 | | 10,802,910 | |

Union Pacific Corp. | | 23,900 | | 2,095,552 | |

| | | | 12,898,462 | |

REAL ESTATE SERVICES—0.4% | | | | | |

CB Richard Ellis Group, Inc.* | | 209,400 | | 3,842,490 | |

| | | | | |

RESEARCH & CONSULTING SERVICES—0.3% | | | | | |

Verisk Analytic Inc., Cl. A* | | 114,100 | | 3,401,321 | |

| | | | | |

RESTAURANTS—1.1% | | | | | |

McDonald’s Corp. | | 143,700 | | 11,175,549 | |

| | | | | |

SEMICONDUCTOR EQUIPMENT—1.2% | | | | | |

Lam Research Corp.* | | 259,499 | | 11,882,459 | |

| | | | | |

SEMICONDUCTORS—4.1% | | | | | |

Applied Micro Circuits Corporation * | | 156,800 | | 1,578,976 | |

Broadcom Corp., Cl. A | | 84,800 | | 3,454,752 | |

Marvell Technology Group Ltd. * | | 749,960 | | 14,481,728 | |

NXP Semiconductor NV * | | 118,300 | | 1,560,377 | |

ON Semiconductor Corp. * | | 133,000 | | 1,020,110 | |

| | | | | | |

18

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

SEMICONDUCTORS—(CONT.) | | | | | |

Skyworks Solutions Inc. * | | 402,400 | | $ | 9,218,984 | |

Texas Instruments Inc. | | 298,400 | | 8,823,688 | |

| | | | 40,138,615 | |

SOFT DRINKS—2.3% | | | | | |

Coca-Cola Co., /The | | 113,800 | | 6,978,216 | |

PepsiCo Inc. | | 252,800 | | 16,507,840 | |

| | | | 23,486,056 | |

SPECIALIZED FINANCE—0.8% | | | | | |

CME Group Inc. | | 27,229 | | 7,886,880 | |

| | | | | |

SYSTEMS SOFTWARE—2.1% | | | | | |

Oracle Corp. | | 708,400 | | 20,826,960 | |

| | | | | |

TOBACCO—1.1% | | | | | |

Philip Morris International Inc. | | 182,650 | | 10,685,025 | |

| | | | | |

TRUCKING—1.0% | | | | | |

Hertz Global Holdings Inc.* | | 831,900 | | 9,417,108 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $909,494,974) | | | | 955,834,084 | |

| | | | | |

Total Investments

(Cost $909,494,974)(b) | | 97.5 | % | 955,834,084 | |

Other Assets in Excess of Liabilities | | 2.5 | | 24,977,700 | |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 980,811,784 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

| |

* | Non-income producing security. |

# | American Depository Receipts. |

(a) | Restricted Security - Investment in security pending registration under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on October 7, 2010 for a cost of $7,337,921 and represents 1.1% of the net assets of the Fund. |

(b) | At October 31, 2010, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $914,788,184 amounted to $41,045,900 which consisted of aggregate gross unrealized appreciation of $76,829,447 and aggregate gross unrealized depreciation of $35,783,547. |

(L2) | Security classified as Level 2 for ASC 820 disclosure purposes based on valuation inputs. |

Industry classifications are unaudited.

See Notes to Financial Statements.

19

THE ALGER INSTITUTIONAL FUNDS | ALGER LARGE CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ October 31, 2010

| | SHARES | | VALUE | |

COMMON STOCKS—95.5% | | | | | |

AEROSPACE & DEFENSE—3.0% | | | | | |

Boeing Co., /The | | 2,550 | | $ | 180,132 | |

General Dynamics Corp. | | 3,600 | | 245,232 | |

Lockheed Martin Corp. | | 2,900 | | 206,741 | |

United Technologies Corp. | | 3,600 | | 269,171 | |

| | | | 901,276 | |

AIR FREIGHT & LOGISTICS—2.1% | | | | | |

FedEx Corp. | | 3,550 | | 311,406 | |

United Parcel Service Inc., Cl. B | | 4,450 | | 299,663 | |

| | | | 611,069 | |

AIRLINES—0.5% | | | | | |

Delta Air Lines Inc.* | | 9,650 | | 134,039 | |

| | | | | |

APPLICATION SOFTWARE—1.4% | | | | | |

Adobe Systems Inc. * | | 10,600 | | 298,390 | |

Salesforce.com Inc. * | | 900 | | 104,463 | |

| | | | 402,853 | |

ASSET MANAGEMENT & CUSTODY BANKS—0.6% | | | | | |

BlackRock Inc. | | 1,100 | | 188,089 | |

| | | | | |

BIOTECHNOLOGY—1.5% | | | | | |

Celgene Corp. * | | 4,050 | | 251,384 | |

Gilead Sciences Inc. * | | 4,800 | | 190,416 | |

| | | | 441,800 | |

COAL & CONSUMABLE FUELS—1.0% | | | | | |

Peabody Energy Corp. | | 5,650 | | 298,885 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—3.6% | | | | | |

Cisco Systems Inc. * | | 25,750 | | 587,872 | |

Qualcomm Inc. | | 10,050 | | 453,556 | |

| | | | 1,041,428 | |

COMPUTER HARDWARE—7.0% | | | | | |

Apple Inc. * | | 4,700 | | 1,414,088 | |

Hewlett-Packard Co. | | 14,450 | | 607,767 | |

| | | | 2,021,855 | |

COMPUTER STORAGE & PERIPHERALS—1.5% | | | | | |

EMC Corp.* | | 20,150 | | 423,352 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—0.5% | | | | | |

Deere & Co. | | 1,900 | | 145,920 | |

| | | | | |

CONSUMER FINANCE—0.5% | | | | | |

American Express Co. | | 3,700 | | 153,402 | |

| | | | | |

DATA PROCESSING & OUTSOURCED SERVICES—2.0% | | | | | |

Mastercard Inc. | | 1,400 | | 336,084 | |

Visa Inc., Cl. A | | 3,150 | | 246,236 | |

| | | | 582,320 | |

DEPARTMENT STORES—1.0% | | | | | |

Kohl’s Corp.* | | 5,700 | | 291,840 | |

| | | | | | |

20

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

DIVERSIFIED CHEMICALS—0.7% | | | | | |

EI Du Pont de Nemours & Co. | | 4,350 | | $ | 205,668 | |

| | | | | |

DIVERSIFIED METALS & MINING—1.2% | | | | | |

Cliffs Natural Resources Inc. | | 3,650 | | 237,980 | |

Freeport-McMoRan Copper & Gold Inc. | | 1,250 | | 118,350 | |

| | | | 356,330 | |

DRUG RETAIL—1.6% | | | | | |

CVS Caremark Corp. | | 7,700 | | 231,924 | |

Walgreen Co. | | 6,900 | | 233,772 | |

| | | | 465,696 | |

ELECTRIC UTILITIES—0.9% | | | | | |

Southern Co. | | 6,650 | | 251,836 | |

| | | | | |

ENVIRONMENTAL & FACILITIES SERVICES—0.9% | | | | | |

Republic Services Inc. | | 8,850 | | 263,819 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—1.1% | | | | | |

Monsanto Co. | | 3,050 | | 181,231 | |

Potash Corporation of Saskatchewan Inc. | | 900 | | 130,581 | |

| | | | 311,812 | |

FOOTWEAR—0.5% | | | | | |

NIKE Inc., Cl. B | | 1,700 | | 138,448 | |

| | | | | |

GENERAL MERCHANDISE STORES—0.8% | | | | | |

Target Corp. | | 4,250 | | 220,745 | |

| | | | | |

GOLD—0.9% | | | | | |

Goldcorp Inc. | | 6,000 | | 267,540 | |

| | | | | |

HEALTH CARE EQUIPMENT—1.8% | | | | | |

Covidien PLC | | 6,850 | | 273,110 | |

Stryker Corp. | | 2,600 | | 128,674 | |

Zimmer Holdings Inc. * | | 2,400 | | 113,856 | |

| | | | 515,640 | |

HEALTH CARE SERVICES—1.2% | | | | | |

Medco Health Solutions Inc.* | | 6,400 | | 336,192 | |

| | | | | |

HOME ENTERTAINMENT SOFTWARE—1.6% | | | | | |

Activision Blizzard Inc. | | 25,500 | | 292,485 | |

Electronic Arts Inc. * | | 11,650 | | 184,653 | |

| | | | 477,138 | |

HOME IMPROVEMENT RETAIL—1.0% | | | | | |

Lowe’s Companies, Inc. | | 13,600 | | 290,088 | |

| | | | | |

HOTELS RESORTS & CRUISE LINES—1.0% | | | | | |

Carnival Corp. | | 6,700 | | 289,239 | |

| | | | | |

HOUSEHOLD APPLIANCES—0.6% | | | | | |

Stanley Black & Decker Inc. | | 2,600 | | 161,122 | |

| | | | | |

HOUSEHOLD PRODUCTS—1.3% | | | | | |

Procter & Gamble Co., /The | | 5,900 | | 375,063 | |

| | | | | |

HYPERMARKETS & SUPER CENTERS—1.6% | | | | | |

Wal-Mart Stores Inc. | | 8,500 | | 460,445 | |

| | | | | | |

21

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

INDUSTRIAL CONGLOMERATES—2.1% | | | | | |

3M Co. | | 3,700 | | $ | 311,614 | |

Tyco International Ltd. | | 7,700 | | 294,756 | |

| | | | 606,370 | |

INDUSTRIAL GASES—0.6% | | | | | |

Praxair Inc. | | 1,900 | | 173,546 | |

| | | | | |

INDUSTRIAL MACHINERY—1.7% | | | | | |

Danaher Corp. | | 5,400 | | 234,144 | |

Illinois Tool Works Inc. | | 5,450 | | 249,065 | |

| | | | 483,209 | |

INTEGRATED OIL & GAS—3.4% | | | | | |

Chevron Corp. | | 6,500 | | 536,965 | |

Exxon Mobil Corp. | | 6,600 | | 438,702 | |

| | | | 975,667 | |

INTEGRATED TELECOMMUNICATION SERVICES—0.5% | | | | | |

Verizon Communications Inc. | | 4,900 | | 159,103 | |

| | | | | |

INTERNET RETAIL—1.6% | | | | | |

Amazon.com Inc. * | | 2,450 | | 404,593 | |

Expedia Inc. | | 2,550 | | 73,823 | |

| | | | 478,416 | |

INTERNET SOFTWARE & SERVICES—5.3% | | | | | |

eBay Inc. * | | 10,950 | | 326,419 | |

Google Inc., Cl. A * | | 1,502 | | 920,710 | |

Yahoo! Inc. * | | 17,950 | | 296,355 | |

| | | | 1,543,484 | |

INVESTMENT BANKING & BROKERAGE—1.0% | | | | | |

Charles Schwab Corp., /The | | 9,850 | | 151,690 | |

Goldman Sachs Group Inc., /The | | 950 | | 152,903 | |

| | | | 304,593 | |

IT CONSULTING & OTHER SERVICES—2.4% | | | | | |

Cognizant Technology Solutions Corp., Cl. A * | | 2,800 | | 182,532 | |

International Business Machines Corp. | | 3,550 | | 509,780 | |

| | | | 692,312 | |

LEISURE PRODUCTS—0.5% | | | | | |

Coach Inc. | | 2,950 | | 147,500 | |

| | | | | |

LIFE & HEALTH INSURANCE—1.0% | | | | | |

Aflac Inc. | | 2,650 | | 148,109 | |

MetLife Inc. | | 3,750 | | 151,237 | |

| | | | 299,346 | |

LIFE SCIENCES TOOLS & SERVICES—0.8% | | | | | |

Thermo Fisher Scientific Inc.* | | 4,700 | | 241,674 | |

| | | | | |

MANAGED HEALTH CARE—0.7% | | | | | |

UnitedHealth Group Inc. | | 5,600 | | 201,880 | |

| | | | | |

MOVIES & ENTERTAINMENT—1.7% | | | | | |

Viacom Inc., Cl. B | | 6,150 | | 237,328 | |

| | | | | | |

22

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

MOVIES & ENTERTAINMENT—(CONT.) | | | | | |

Walt Disney Co., /The | | 7,650 | | $ | 276,241 | |

| | | | 513,569 | |

OIL & GAS EQUIPMENT & SERVICES—1.7% | | | | | |

Schlumberger Ltd. | | 5,950 | | 415,845 | |

Weatherford International Ltd. * | | 4,150 | | 69,762 | |

| | | | 485,607 | |

OIL & GAS EXPLORATION & PRODUCTION—2.4% | | | | | |

Devon Energy Corp. | | 6,300 | | 409,626 | |

Nexen Inc. | | 13,650 | | 290,609 | |

| | | | 700,235 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—1.4% | | | | | |

Bank of America Corp. | | 8,100 | | 92,664 | |

JPMorgan Chase & Co. | | 7,800 | | 293,513 | |

| | | | 386,177 | |

PACKAGED FOODS & MEATS—0.8% | | | | | |

Kraft Foods Inc., Cl. A | | 7,250 | | 233,958 | |

| | | | | |

PERSONAL PRODUCTS—0.2% | | | | | |

Avon Products Inc. | | 2,350 | | 71,558 | |

| | | | | |

PHARMACEUTICALS—5.0% | | | | | |

Abbott Laboratories | | 5,350 | | 274,562 | |

Allergan Inc. | | 3,000 | | 217,230 | |

Johnson & Johnson | | 4,800 | | 305,615 | |

Pfizer Inc. | | 15,900 | | 276,660 | |

Roche Holding AG # | | 4,150 | | 152,513 | |

Teva Pharmaceutical Industries Ltd. # | | 4,700 | | 243,930 | |

| | | | 1,470,510 | |

PROPERTY & CASUALTY INSURANCE—0.6% | | | | | |

Travelers Cos., Inc., /The | | 2,950 | | 162,840 | |

| | | | | |

RAILROADS—1.1% | | | | | |

CSX Corp. | | 5,200 | | 319,540 | |

| | | | | |

RESTAURANTS—1.1% | | | | | |

McDonald’s Corp. | | 4,150 | | 322,746 | |

| | | | | |

SEMICONDUCTORS—3.3% | | | | | |

Broadcom Corp., Cl. A | | 5,650 | | 230,181 | |

Intel Corp. | | 15,200 | | 305,064 | |

Marvell Technology Group Ltd. * | | 17,150 | | 331,166 | |

Texas Instruments Inc. | | 3,050 | | 90,189 | |

| | | | 956,600 | |

SOFT DRINKS—2.9% | | | | | |

Coca-Cola Co., /The | | 5,700 | | 349,524 | |

PepsiCo Inc. | | 7,600 | | 496,279 | |

| | | | 845,803 | |

SPECIALIZED FINANCE—1.0% | | | | | |

CME Group Inc. | | 1,012 | | 293,126 | |

| | | | | | |

23

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

SPECIALIZED REITS—0.5% | | | | | |

Weyerhaeuser Company | | 8,267 | | $ | 134,091 | |

| | | | | |

SPECIALTY STORES—0.6% | | | | | |

Staples Inc. | | 8,650 | | 177,066 | |

| | | | | |

SYSTEMS SOFTWARE—3.6% | | | | | |

Microsoft Corp. | | 20,200 | | 538,128 | |

Oracle Corp. | | 17,000 | | 499,800 | |

| | | | 1,037,928 | |

TOBACCO—1.1% | | | | | |

Philip Morris International Inc. | | 5,400 | | 315,900 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $26,571,527) | | | | 27,759,303 | |

| | | | | |

Total Investments

(Cost $26,571,527)(a) | | 95.5 | % | 27,759,303 | |

Other Assets in Excess of Liabilities | | 4.5 | | 1,311,572 | |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 29,070,875 | |

‡ Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted.

* Non-income producing security.

# American Depository Receipts.

(a) At October 31, 2010, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $26,601,684 amounted to $1,157,619 which consisted of aggregate gross unrealized appreciation of $2,832,222 and aggregate gross unrealized depreciation of $1,674,603.

Industry classifications are unaudited.

See Notes to Financial Statements.

24

THE ALGER INSTITUTIONAL FUNDS | ALGER MID CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ October 31, 2010

| | SHARES | | VALUE | |

COMMON STOCKS—96.9% | | | | | |

ADVERTISING—0.8% | | | | | |

Focus Media Holding Ltd.#* | | 262,500 | | $ | 6,496,875 | |

| | | | | |

AEROSPACE & DEFENSE—1.9% | | | | | |

Goodrich Corp. | | 186,600 | | 15,314,262 | |

| | | | | |

AIRLINES—0.8% | | | | | |

United Continental Holdings Inc.* | | 213,400 | | 6,197,136 | |

| | | | | |

APPAREL RETAIL—2.9% | | | | | |

Chico’s FAS Inc. | | 482,500 | | 4,689,900 | |

J Crew Group Inc. * | | 186,900 | | 5,978,931 | |

TJX Cos., Inc. | | 174,300 | | 7,998,627 | |

Urban Outfitters Inc. * | | 126,100 | | 3,880,097 | |

| | | | 22,547,555 | |

APPLICATION SOFTWARE—5.6% | | | | | |

Adobe Systems Inc. * | | 558,900 | | 15,733,035 | |

Informatica Corp. * | | 157,000 | | 6,388,330 | |

Intuit Inc. * | | 125,200 | | 6,009,600 | |

Nice Systems Ltd. #* | | 261,300 | | 8,750,937 | |

Salesforce.com Inc. * | | 61,000 | | 7,080,270 | |

| | | | 43,962,172 | |

ASSET MANAGEMENT & CUSTODY BANKS—2.2% | | | | | |

BlackRock Inc. | | 44,300 | | 7,574,857 | |

T. Rowe Price Group Inc. | | 182,900 | | 10,108,883 | |

| | | | 17,683,740 | |

BIOTECHNOLOGY—4.2% | | | | | |

Alexion Pharmaceuticals Inc. * | | 41,100 | | 2,807,130 | |

Cephalon Inc. * | | 60,200 | | 3,999,688 | |

China Nuokang Bio-Pharmaceutical Inc. #* | | 735,262 | | 3,418,968 | |

Human Genome Sciences Inc. * | | 375,400 | | 10,090,752 | |

Metabolix Inc. * | | 960,468 | | 13,408,133 | |

| | | | 33,724,671 | |

BROADCASTING & CABLE TV—1.0% | | | | | |

Discovery Communications Inc., Series C* | | 205,900 | | 8,001,274 | |

| | | | | |

COAL & CONSUMABLE FUELS—1.0% | | | | | |

Patriot Coal Corp.* | | 574,700 | | 7,752,703 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—0.7% | | | | | |

Finisar Corp.* | | 326,500 | | 5,553,765 | |

| | | | | |

COMPUTER & ELECTRONICS RETAIL—0.5% | | | | | |

GameStop Corp., Cl. A* | | 216,100 | | 4,248,526 | |

| | | | | |

COMPUTER HARDWARE—0.6% | | | | | |

Teradata Corp.* | | 117,800 | | 4,636,608 | |

| | | | | |

COMPUTER STORAGE & PERIPHERALS—1.5% | | | | | |

NetApp Inc. * | | 151,300 | | 8,056,725 | |

Seagate Technology PLC * | | 281,000 | | 4,116,650 | |

| | | | 12,173,375 | |

CONSTRUCTION & ENGINEERING—1.7% | | | | | |

Aecom Technology Corp. * | | 299,300 | | 7,928,457 | |

| | | | | | |

25

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

CONSTRUCTION & ENGINEERING—(CONT.) | | | | | |

Chicago Bridge & Iron Co., NV #* | | 213,500 | | $ | 5,382,335 | |

| | | | 13,310,792 | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.2% | | | | | |

Bucyrus International Inc. | | 52,200 | | 3,557,952 | |

Westport Innovations Inc. * | | 331,300 | | 6,003,156 | |

| | | | 9,561,108 | |

DATA PROCESSING & OUTSOURCED SERVICES—1.5% | | | | | |

Echo Global Logistics Inc. * | | 258,285 | | 3,667,647 | |

Fiserv Inc. * | | 146,800 | | 8,003,536 | |

| | | | 11,671,183 | |

DIVERSIFIED METALS & MINING—2.8% | | | | | |

Cliffs Natural Resources Inc. | | 224,100 | | 14,611,320 | |

Ivanhoe Mines Ltd. * | | 82,100 | | 1,976,147 | |

Walter Energy, Inc. | | 68,600 | | 6,034,056 | |

| | | | 22,621,523 | |

ELECTRICAL COMPONENTS & EQUIPMENT—2.6% | | | | | |

AMETEK Inc. | | 164,800 | | 8,907,440 | |

General Cable Corp. * | | 414,800 | | 11,589,512 | |

| | | | 20,496,952 | |

ENVIRONMENTAL & FACILITIES SERVICES—0.9% | | | | | |

Stericycle Inc.* | | 97,900 | | 7,023,346 | |

| | | | | |

GOLD—1.8% | | | | | |

Yamana Gold Inc. | | 1,258,600 | | 13,832,014 | |

| | | | | |

HEALTH CARE EQUIPMENT—2.5% | | | | | |

Insulet Corp. * | | 147,000 | | 2,344,650 | |

Intuitive Surgical Inc. * | | 11,400 | | 2,997,630 | |

Mindray Medical International Ltd. # | | 214,100 | | 6,204,618 | |

NuVasive Inc. * | | 295,500 | | 7,742,100 | |

| | | | 19,288,998 | |

HEALTH CARE FACILITIES—2.2% | | | | | |

Community Health Systems Inc. * | | 127,400 | | 3,832,192 | |

Select Medical Holdings Corp. * | | 424,200 | | 3,173,016 | |

Universal Health Services Inc., Cl. B | | 203,200 | | 8,386,064 | |

VCA Antech Inc. * | | 92,600 | | 1,914,042 | |

| | | | 17,305,314 | |

HOME ENTERTAINMENT SOFTWARE—1.5% | | | | | |

Activision Blizzard Inc. | | 1,002,000 | | 11,492,940 | |

| | | | | |

HOME FURNISHING RETAIL—0.8% | | | | | |

Bed Bath & Beyond Inc.* | | 134,500 | | 5,904,550 | |

| | | | | |

HOMEBUILDING—0.9% | | | | | |

Lennar Corp., Cl. A | | 489,000 | | 7,095,390 | |

| | | | | |

HOTELS RESORTS & CRUISE LINES—6.2% | | | | | |

Ctrip.com International Ltd. #* | | 230,100 | | 11,981,307 | |

Home Inns & Hotels Management Inc. #* | | 152,700 | | 7,812,132 | |

Interval Leisure Group * | | 398,000 | | 5,711,300 | |

Morgans Hotel Group Co. * | | 252,800 | | 2,040,096 | |

| | | | | | |

26

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HOTELS RESORTS & CRUISE LINES—(CONT.) | | | | | |

Orient-Express Hotels Ltd., Cl. A * | | 413,900 | | $ | 5,239,974 | |

Royal Caribbean Cruises Ltd. * | | 226,500 | | 8,955,810 | |

Wyndham Worldwide Corporation | | 269,700 | | 7,753,875 | |

| | | | 49,494,494 | |

HOUSEHOLD APPLIANCES—0.5% | | | | | |

Stanley Black & Decker Inc. | | 61,600 | | 3,817,352 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—0.5% | | | | | |

McDermott International Inc.* | | 271,600 | | 4,190,788 | |

| | | | | |

INDUSTRIAL MACHINERY—3.9% | | | | | |

Duoyuan Global Water Inc. #* | | 67,899 | | 849,416 | |

Flowserve Corp. | | 102,600 | | 10,260,000 | |

SmartHeat Inc. * | | 876,800 | | 5,690,432 | |

SPX Corp. | | 202,100 | | 13,552,826 | |

| | | | 30,352,674 | |

INTERNET RETAIL—2.0% | | | | | |

Expedia Inc. | | 251,000 | | 7,266,450 | |

NetFlix Inc. * | | 46,700 | | 8,102,450 | |

| | | | 15,368,900 | |

INTERNET SOFTWARE & SERVICES—3.4% | | | | | |

GSI Commerce Inc. * | | 229,000 | | 5,592,180 | |

OpenTable Inc. * | | 247,100 | | 15,159,585 | |

Yahoo! Inc. * | | 356,300 | | 5,882,513 | |

| | | | 26,634,278 | |

INVESTMENT BANKING & BROKERAGE—0.9% | | | | | |

Greenhill & Co., Inc. | | 93,100 | | 7,231,077 | |

| | | | | |

IT CONSULTING & OTHER SERVICES—1.7% | | | | | |

Cognizant Technology Solutions Corp., Cl. A* | | 200,600 | | 13,077,114 | |

| | | | | |

LEISURE PRODUCTS—2.0% | | | | | |

Coach Inc. | | 174,800 | | 8,740,000 | |

Polo Ralph Lauren Corp., Cl. A | | 70,700 | | 6,849,416 | |

| | | | 15,589,416 | |

LIFE SCIENCES TOOLS & SERVICES—0.9% | | | | | |

ICON PLC#* | | 376,059 | | 7,276,742 | |

| | | | | |

MANAGED HEALTH CARE—0.5% | | | | | |

Aetna Inc. | | 123,400 | | 3,684,724 | |

| | | | | |

OIL & GAS DRILLING—1.3% | | | | | |

Helmerich & Payne Inc. | | 91,800 | | 3,927,204 | |

Nabors Industries Ltd. * | | 286,800 | | 5,994,120 | |

| | | | 9,921,324 | |

OIL & GAS EQUIPMENT & SERVICES—1.4% | | | | | |

Cameron International Corp. * | | 153,300 | | 6,706,875 | |

National Oilwell Varco Inc. | | 76,550 | | 4,115,328 | |

| | | | 10,822,203 | |

OIL & GAS EXPLORATION & PRODUCTION—4.3% | | | | | |

Concho Resources Inc., /Restricted *,(L2),(a) | | 198,500 | | 12,799,504 | |

| | | | | | |

27

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

OIL & GAS EXPLORATION & PRODUCTION—(CONT.) | | | | | |

Nexen Inc. | | 598,957 | | $ | 12,751,795 | |

Plains Exploration & Production Co. * | | 308,200 | | 8,589,534 | |

| | | | 34,140,833 | |

OTHER DIVERSIFIED FINANCIAL SERVICES—1.6% | | | | | |

BM&F Bovespa SA | | 1,505,887 | | 12,616,939 | |

| | | | | |

PACKAGED FOODS & MEATS—0.5% | | | | | |

McCormick & Co., Inc. | | 82,700 | | 3,656,994 | |

| | | | | |

PHARMACEUTICALS—4.3% | | | | | |

Auxilium Pharmaceuticals Inc. * | | 229,800 | | 5,687,550 | |

Medicis Pharmaceutical Corp., Cl. A | | 176,069 | | 5,238,053 | |

Mylan Inc. * | | 648,300 | | 13,173,456 | |

Optimer Pharmaceuticals Inc. * | | 631,674 | | 5,931,419 | |

Shire PLC # | | 50,900 | | 3,568,090 | |

| | | | 33,598,568 | |

RAILROADS—1.0% | | | | | |

CSX Corp. | | 121,700 | | 7,478,465 | |

| | | | | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—0.8% | | | | | |

BR Malls Participacoes SA | | 622,840 | | 5,950,817 | |

| | | | | |

REAL ESTATE SERVICES—1.2% | | | | | |

CB Richard Ellis Group, Inc. * | | 399,500 | | 7,330,825 | |

E-House China Holdings Ltd. # | | 107,200 | | 1,791,312 | |

| | | | 9,122,137 | |

RESEARCH & CONSULTING SERVICES—1.3% | | | | | |

Verisk Analytic Inc., Cl. A* | | 341,700 | | 10,186,077 | |

| | | | | |

RESTAURANTS—1.5% | | | | | |

Darden Restaurants Inc. | | 132,800 | | 6,070,288 | |

McCormick & Schmick’s Seafood Restaurants Inc. * | | 615,976 | | 5,500,666 | |

| | | | 11,570,954 | |

SEMICONDUCTOR EQUIPMENT—1.7% | | | | | |

Lam Research Corp.* | | 287,200 | | 13,150,888 | |

| | | | | |

SEMICONDUCTORS—6.2% | | | | | |

Altera Corp. | | 352,700 | | 11,007,767 | |

Applied Micro Circuits Corporation * | | 748,300 | | 7,535,381 | |

Atheros Communications Inc. * | | 150,735 | | 4,678,814 | |

Marvell Technology Group Ltd. * | | 550,900 | | 10,637,879 | |

Netlogic Microsystems Inc. * | | 225,200 | | 6,769,512 | |

Skyworks Solutions Inc. * | | 389,700 | | 8,928,027 | |

| | | | 49,557,380 | |

SPECIALIZED FINANCE—1.8% | | | | | |

CME Group Inc. | | 35,400 | | 10,253,610 | |

IntercontinentalExchange Inc. * | | 34,300 | | 3,940,041 | |

| | | | 14,193,651 | |

SYSTEMS SOFTWARE—0.5% | | | | | |

Red Hat Inc.* | | 94,200 | | 3,980,892 | |

| | | | | | |

28

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

THRIFTS & MORTGAGE FINANCE—0.0% | | | | | |

Ocwen Financial Corp.* | | 14,400 | | $ | 124,272 | |

| | | | | |

TOBACCO—0.9% | | | | | |

ITC Ltd.* | | 1,971,500 | | 7,561,309 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $733,636,638) | | | | 762,248,034 | |

| | | | | |

CONVERTIBLE PREFERRED STOCK—0.7% | | | | | |

BIOTECHNOLOGY—0.7% | | | | | |

Merrimack Pharmaceuticals Inc., Cl. B, /Restricted *,(L3),(b) | | 586,714 | | 3,395,901 | |

Merrimack Pharmaceuticals Inc., Cl. C, /Restricted *,(L3),(c) | | 611,759 | | 2,294,096 | |

| | | | 5,689,997 | |

TOTAL CONVERTIBLE PREFERRED STOCK

(Cost $5,689,997) | | | | 5,689,997 | |

| | | | | | |

| | PRINCIPAL

AMOUNT | | | |

CONVERTIBLE CORPORATE BONDS—1.3% | | | | | |

WIRELESS TELECOMMUNICATION SERVICES—1.3% | | | | | |

SBA Communications Corp., 4.00%, 10/1/14(L2)

(Cost $8,920,564) | | 7,266,000 | | 10,590,195 | |

| | | | | |

Total Investments

(Cost $748,247,199)(d) | | 98.9 | % | 778,528,226 | |

Other Assets in Excess of Liabilities | | 1.1 | | 8,587,183 | |

| | | | | |

NET ASSETS | | 100.0 | % | $ | 787,115,409 | |

| | | | | | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

| |

* | Non-income producing security. |

# | American Depository Receipts. |

(a) | Restricted Security - Investment in security pending registration under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on October 7, 2010 for a cost of $8,992,050 and represents 1.6% of the net assets of the Fund. |

(b) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $3,395,901 and represents 0.4% of the net assets of the Fund. |

(c) | Restricted Security - Investment in security not registered under the Securities Act of 1933. The investment is deemed to be illiquid and may be sold only to qualified institutional buyers. Security was acquired on August 25, 2010 for a cost of $2,294,096 and represents 0.3% of the net assets of the Fund. |

(d) | At October 31, 2010, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $752,314,231 amounted to $26,213,995 which consisted of aggregate gross unrealized appreciation of $74,346,616 and aggregate gross unrealized depreciation of $48,132,621. |

(L2) | Security classified as Level 2 for ASC 820 disclosure purposes based on valuation inputs. |

(L3) | Security classified as Level 3 for ASC 820 disclosure purposes based on valuation inputs. |

Industry classifications are unaudited.

See Notes to Financial Statements.

29

THE ALGER INSTITUTIONAL FUNDS | ALGER SMALL CAP GROWTH INSTITUTIONAL FUND

Schedule of Investments‡ October 31, 2010

| | SHARES | | VALUE | |

COMMON STOCKS—97.2% | | | | | |

AEROSPACE & DEFENSE—2.4% | | | | | |

AAR Corp. * | | 152,550 | | $ | 3,362,202 | |

BE Aerospace Inc. * | | 283,955 | | 10,438,186 | |

Esterline Technologies Corp. * | | 232,375 | | 14,044,745 | |

| | | | 27,845,133 | |

AIRLINES—0.9% | | | | | |

Airtran Holdings Inc.* | | 1,466,290 | | 10,850,546 | |

| | | | | |

APPAREL RETAIL—2.9% | | | | | |

Aeropostale Inc. * | | 227,125 | | 5,537,308 | |

AnnTaylor Stores Corp. * | | 600,050 | | 13,981,164 | |

Childrens Place Retail Stores Inc., /The * | | 257,700 | | 11,354,261 | |

Coldwater Creek Inc. * | | 1,079,550 | | 3,638,084 | |

| | | | 34,510,817 | |

APPLICATION SOFTWARE—9.0% | | | | | |

Cadence Design Systems, Inc. * | | 1,105,150 | | 9,360,621 | |

Concur Technologies Inc. * | | 214,900 | | 11,093,138 | |

Informatica Corp. * | | 301,950 | | 12,286,345 | |

Nice Systems Ltd. #* | | 424,655 | | 14,221,695 | |

Pegasystems Inc. | | 177,586 | | 4,803,701 | |

QLIK Technologies Inc. * | | 335,450 | | 8,376,187 | |

Solera Holdings Inc. | | 289,200 | | 13,896,059 | |

Taleo Corp., Cl. A * | | 338,100 | | 9,700,089 | |

Ultimate Software Group Inc. * | | 268,300 | | 11,102,254 | |

VanceInfo Technologies Inc. #* | | 312,750 | | 11,374,718 | |

| | | | 106,214,807 | |

AUTO PARTS & EQUIPMENT—1.2% | | | | | |

Dana Holding Corp.* | | 963,650 | | 13,635,648 | |

| | | | | |

BIOTECHNOLOGY—2.2% | | | | | |

Acorda Therapeutics Inc. * | | 129,250 | | 3,494,920 | |

Cubist Pharmaceuticals Inc. * | | 198,200 | | 4,614,096 | |

Incyte Corp., Ltd. * | | 207,050 | | 3,449,453 | |

Savient Pharmaceuticals Inc. * | | 408,800 | | 5,073,208 | |

United Therapeutics Corp. * | | 145,330 | | 8,719,800 | |

| | | | 25,351,477 | |

CASINOS & GAMING—0.7% | | | | | |

WMS Industries Inc.* | | 196,450 | | 8,571,114 | |

| | | | | |

COAL & CONSUMABLE FUELS—0.8% | | | | | |

Patriot Coal Corp.* | | 653,900 | | 8,821,111 | |

| | | | | |

COMMERCIAL PRINTING—0.3% | | | | | |

Warnaco Group Inc., /The* | | 62,900 | | 3,340,619 | |

| | | | | |

COMMODITY CHEMICALS—0.5% | | | | | |

STR Holdings Inc.* | | 240,650 | | 5,980,153 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—3.3% | | | | | |

Acme Packet Inc. * | | 127,300 | | 5,034,715 | |

Aruba Networks Inc. * | | 545,450 | | 11,950,809 | |

Finisar Corp. * | | 699,450 | | 11,897,645 | |

| | | | | | |

30

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

COMMUNICATIONS EQUIPMENT—(CONT.) | | | | | |

Riverbed Technology Inc. * | | 178,050 | | $ | 10,244,997 | |

| | | �� | 39,128,166 | |

COMPUTER STORAGE & PERIPHERALS—0.8% | | | | | |

QLogic Corp. * | | 339,900 | | 5,972,043 | |

Smart Technologies Inc., Cl. A * | | 268,100 | | 3,482,619 | |

| | | | 9,454,662 | |

CONSTRUCTION & ENGINEERING—0.7% | | | | | |

Aecom Technology Corp.* | | 323,700 | | 8,574,813 | |

| | | | | |

DATA PROCESSING & OUTSOURCED SERVICES—1.0% | | | | | |

Wright Express Corp.* | | 312,685 | | 11,791,351 | |

| | | | | |

DISTRIBUTORS—1.1% | | | | | |

LKQ Corp.* | | 610,740 | | 13,277,488 | |

| | | | | |

DIVERSIFIED CHEMICALS—0.3% | | | | | |

Solutia Inc.* | | 215,700 | | 3,906,327 | |

| | | | | |

EDUCATION SERVICES—1.2% | | | | | |

American Public Education Inc. * | | 240,700 | | 6,729,972 | |

Grand Canyon Education, Inc. * | | 362,700 | | 6,822,387 | |

| | | | 13,552,359 | |

ELECTRIC UTILITIES—1.1% | | | | | |

ITC Holdings Corp. | | 215,385 | | 13,485,255 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—2.2% | | | | | |

GrafTech International Ltd. * | | 722,700 | | 11,902,869 | |

Woodward Governor Co. | | 453,550 | | 14,214,257 | |

| | | | 26,117,126 | |

ENVIRONMENTAL & FACILITIES SERVICES—2.7% | | | | | |

Clean Harbors, Inc. * | | 148,950 | | 10,500,975 | |

Tetra Tech Inc. * | | 331,350 | | 6,978,231 | |

Waste Connections Inc. | | 355,600 | | 14,487,144 | |

| | | | 31,966,350 | |

FOOD DISTRIBUTORS—0.6% | | | | | |

United Natural Foods Inc.* | | 209,600 | | 7,495,296 | |

| | | | | |

FOREST PRODUCTS—0.6% | | | | | |

Louisiana-Pacific Corp.* | | 941,450 | | 7,286,823 | |

| | | | | |