Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8194

FINANCIAL INVESTORS TRUST

(exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

JoEllen L. Legg, Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: May 1, 2010 - October 31, 2010

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

Table of Contents

October 31, 2010

|

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

For the six months ended October 31, 2010, the ALPS | GNI Long-Short Fund - Class A Shares (exclusive of applicable sales loads) returned

-0.25%.

Great news, though: The recession that began in December 2007 technically ended in June 2009, so said the National Bureau of Economic Research (NBER), the group of economists that officially dates the inflection points in the economic cycle, in late September. But in the next breath, Robert Hall, Chairman of the NBER’s Business Cycle Dating Committee was quoted as saying, “The economy is not in good shape.” Somehow, we think the 15 million unemployed Americans probably concur and aren’t rejoicing just yet.*

The U.S. economic rebound, as we’ve noted a few times before, was mostly cosmetic, manufactured almost entirely by temporary and unsustainable growth drivers: unprecedented levels of government stimulus using borrowed money and inventory restocking. The upturn itself, in terms of real final demand, goes down as one of the weakest on record. The economic apocalypse was avoided – and for that we should all be grateful – but we’ve yet to see any meaningful private-sector demand in the U.S.

With interest rates near zero percent, the Federal Reserve (“the Fed”) has taken to unconventional ways to affect monetary policy, like quantitative easing (QE), increasing the supply of money by dramatically expanding its own balance sheet by buying financial assets. But QE is no cure-all. Despite the Fed spending $1.7 trillion to purchase Treasuries, mortgage-backed securities and housing agency bonds, the economy remains fragile and estimates for both economic growth and corporate earnings continue to get nudged lower.

That hasn’t discouraged our central bankers, though. In a monetary experiment with an uncertain outcome, another round of quantitative easing (QE2) is imminent. This will probably lead to a temporary boost in asset prices, but it’s unclear whether it will have the intended effect on the real economy. In anticipation of QE2, Treasury yields have fallen to 2.4%, gold has rallied up to $1,350/oz, equities had their strongest September since 1939 and the dollar has fallen like a stone.**

With a bleak labor market, a still-troubled housing sector where demand is not even stimulated by record-low mortgage rates, a huge debt overhang and a household sector that is still struggling, we believe the macro backdrop is far from rosy.

So how does this poor fundamental backdrop but extreme liquidity translate into our portfolio construction? We remain bullish on the long-term prospects for gold, because to date the government’s only economic plan has been to increase deficit spending and to systematically debase the currency through quantitative easing.

We’re also finding opportunities on the long side in higher quality, larger companies, mostly within the technology and consumer staples areas, many of which have very attractive dividend yields and derive much of their revenue from non-dollar countries. Demand for staples like food and household products is relatively stable regardless of economic activity, and we believe currency diversification in this era of mass debasement is essential.

On the short side, we have more cyclicality and have targeted more fundamentally flawed companies. We also have maintained broad index-related short exposure, especially in small-cap indexes where we expect underperformance relative to large caps. We have increased our net exposure to 20-30% net long as we attempt to participate in the “risk on” trade, but will remain vigilant in our risk controls because we believe any boost in asset prices due to QE will likely be short lived.

During the third quarter, the official government account on the causes and culprits of May’s Flash Crash was released. Though the full report is 104 pages long, it basically attributes the events of May 6 to a single trade by an overeager futures seller. Unfortunately, this report fails to mention the fundamental conditions that might lead to an environment where a crash becomes possible, and it fails to account for the near daily mini-crashes still occurring in individual securities.

Near-zero interest rate environments are unique. Discounting projected cash flows of an investment requires a discount rate, and when the dividend growth rate (or the interest rate) on a security is greater than the discount rate, the fundamental valuation formula becomes meaningless. The projected value becomes infinite, as something close to zero is in the denominator.

As a practical matter, this means we are in a speculative regime with an extreme sensitivity to slight changes in the near-zero interest rates. As the Federal Reserve drives interest rates down to zero, stocks can take on an almost infinite value. However, the process can also work in reverse.

1 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

In our opinion, it’s not a coincidence that the Flash Crash occurred two months after the end of the first round of quantitative easing, causing the market to drop over 10% in a few minutes. Many stocks returned to the same trading levels that existed before the Federal Reserve started quantitative easing, but those trades were later erased off the tape. The free market wasn’t broken in March 2009, the government and the banks just didn’t like the prices. They didn’t like the prices in that May swoon either, so they expunged those trades.

Every bubble we have ever studied rises on increasing leverage, then crashes on the reality that it cannot be maintained. Sometimes that process takes a couple of years; sometimes it takes a day. Currently, government leverage as measured by the size of the Federal Reserve’s balance sheet and the federal government’s debt is increasing dramatically. That increasing leverage is raising the prices of securities, but that can all end in a flash as it almost did this May.

We are always grateful for the trust you’ve placed in us with the management of your assets. We cannot be sure how long the current disparity between high quality companies and low quality companies will persist. We cannot be sure of the effects or duration of another round of quantitative easing. But we do believe the current environment is setting up for exciting opportunities for long/short portfolios and we look forward to seeking to capitalize on them on your behalf.

Sincerely,

Charles L. Norton, CFA | Principal

Allen R. Gillespie, CFA | Principal

| * | The National Bureau of Economic Research and The Globe and Mail, “Slow U.S. recovery follows the Great Recession,” Sept. 20, 2010. |

| ** | Financial Times, “US stocks post best September since 1939,” Oct. 1, 2010. |

2 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

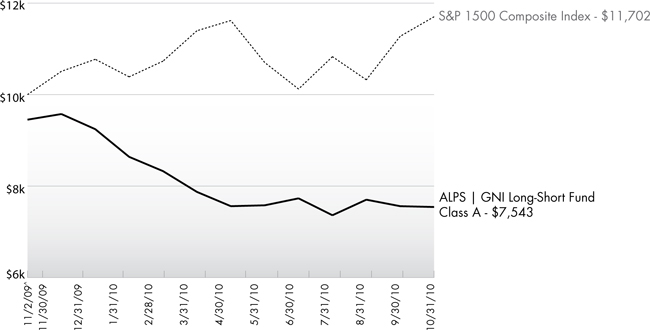

Performance of $10,000 Initial Investment (as of October 31, 2010)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

3 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

Cumulative Return (as of October 31, 2010)

| 6 month | Since Inception^ | Gross Expense Ratio | Net Expense Ratio* | |||||

Class A (NAV)1 | -0.25% | -20.20% | 26.75% | 3.13% | ||||

Class A (MOP)2 | -5.79% | -24.57% | ||||||

Class I | 0.00% | -19.80% | 2.96% | 2.83% | ||||

S&P 1500 Composite Index3 | 0.72% | 17.03% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 90 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data please call (866) 759-5679.

Subject to investment risks, including possible loss of the principal amount invested. Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the funds original investment.

1 Net Asset Value (NAV) is the share price without sales charges. 2 Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%. 3 S&P Composite 1500: an equity benchmark that combines three leading indices, the S&P 500®, the S&P MidCap 400 and the S&P SmallCap 600 to cover approximately 90% of the U.S. market capitalization. It is designed for investors seeking to replicate the performance of the U.S. equity market or benchmark against a representative universe of tradable stocks. You cannot invest directly in the index. ^ Fund inception date of 11/02/09. * ALPS Advisors, Inc. (the “Adviser”) has given a contractual agreement to the Fund to limit the amount of the Fund’s total annual expenses, exclusive of distribution and service (12b-1) fees, shareholder service fees, acquired fund fees and expenses, short-sale dividend expenses, brokerage expenses, interest expenses, taxes and extraordinary expenses, to 2.00% of the Fund’s average daily net assets. This agreement is in effect through August 31, 2011 and is reevaluated on an annual basis. Without this agreement, expenses could be higher.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The Fund enters into a short sale by selling a security it has borrowed. If the market price of a security increases after the Fund borrows the security, the Fund will suffer a potentially unlimited loss when it replaces the borrowed security at the higher price. Short sales also involve transaction and other costs that will reduce potential Fund gains and increase potential Fund losses. Please refer to the prospectus for complete information regarding all risks associated with the fund.

The Fund is less than a year old and has limited operating history. This fund is not suitable for all investors. Subject to investment risks, including possible loss of the principal amount invested.

Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund’s original investment. |

4 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads); and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010.

| Beginning Account Value 5/1/10 | Ending Account Value 10/31/10 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/10-10/31/10 | |||||||||||||

Class A | ||||||||||||||||

Actual | $1,000.00 | $998.70 | 3.12% | $15.72 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,009.48 | 3.12% | $15.80 | ||||||||||||

Class I | ||||||||||||||||

Actual | $1,000.00 | $1,001.20 | 2.98% | $15.03 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,010.18 | 2.98% | $15.10 | ||||||||||||

| (a) | The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 365. |

5 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

| Shares | Value (Note 1) | |||||||

COMMON STOCKS (75.11%) |

| |||||||

Basic Materials (16.99%) |

| |||||||

Mining (16.99%) |

| |||||||

Cia de Minas Buenaventura SA, ADR | 11,500 | $ | 609,960 | |||||

Newmont Mining | 13,000 | 791,310 | ||||||

| 1,401,270 | ||||||||

TOTAL BASIC MATERIALS |

| 1,401,270 | ||||||

Communications (5.33%) |

| |||||||

Internet (5.33%) |

| |||||||

Baidu, Inc., Sponsored ADR(a) | 4,000 | 440,040 | ||||||

TOTAL COMMUNICATIONS |

| 440,040 | ||||||

Consumer, Non-Cyclical (42.27%) |

| |||||||

Agriculture (18.97%) |

| |||||||

Archer-Daniels-Midland Co. | 18,000 | 599,760 | ||||||

Philip Morris International, | 16,500 | 965,250 | ||||||

| 1,565,010 | ||||||||

Beverages (5.95%) |

| |||||||

The Coca-Cola Co. | 8,000 | 490,560 | ||||||

Biotechnology (4.87%) |

| |||||||

Dendreon Corp.(a) | 11,000 | 401,500 | ||||||

Food (7.43%) |

| |||||||

Kraft Foods, Inc., Class A | 19,000 | 613,130 | ||||||

Pharmaceuticals (5.05%) |

| |||||||

Medicis Pharmaceutical Corp., Class A | 14,000 | 416,500 | ||||||

TOTAL CONSUMER, NON-CYCLICAL |

| 3,486,700 | ||||||

Financial (5.35%) |

| |||||||

Insurance (5.35%) |

| |||||||

American International Group, Inc.(a) | 10,500 | 441,105 | ||||||

TOTAL FINANCIAL |

| 441,105 | ||||||

Technology (5.17%) |

| |||||||

Software (5.17%) |

| |||||||

Microsoft Corp.(b) | 16,000 | 426,240 | ||||||

TOTAL TECHNOLOGY |

| 426,240 | ||||||

| Shares | Value (Note 1) | |||||||

TOTAL COMMON STOCKS |

| |||||||

(Cost $5,643,758) | 6,195,355 | |||||||

| Shares | Value (Note 1) | |||||||||||

EXCHANGE TRADED FUNDS (5.22%) |

| |||||||||||

SPDR Gold Shares(a) |

| 3,250 | $ | 431,080 | ||||||||

TOTAL EXCHANGE TRADED FUNDS |

| |||||||||||

(Cost $366,262) |

| 431,080 | ||||||||||

| Expiration Date | Exercise Price | Number of Contracts | Value (Note 1) | |||||||||

PURCHASED PUT OPTIONS (5.03%) |

| |||||||||||

F5 Networks, Inc |

| |||||||||||

January, 2011 | $100.00 | 100 | 35,500 | |||||||||

iShares Russell 2000 Index Fund |

| |||||||||||

January, 2011 | 69.00 | 400 | 130,400 | |||||||||

Moody’s Corp. |

| |||||||||||

January, 2011 | 25.00 | 200 | 21,400 | |||||||||

SPDR S&P 500 |

| |||||||||||

January, 2011 | 116.00 | 600 | 227,400 | |||||||||

TOTAL PURCHASED PUT OPTIONS |

| |||||||||||

(Cost $536,500) |

| 414,700 | ||||||||||

| 7-Day Yield | Shares/ Principal Amount | Value (Note 1) | ||||||||||

SHORT TERM INVESTMENTS (30.78%) |

| |||||||||||

Money Market Fund (6.53%) |

| |||||||||||

Dreyfus Treasury Prime Cash Management Fund, Investor Shares |

| |||||||||||

| 0.00004 | % | 538,720 | 538,720 | |||||||||

U.S. Government & Agency Obligations (24.25%) |

| |||||||||||

U.S. Treasury Bill DN(b) |

| |||||||||||

11/26/10 | 0.13 | % | $2,000,000 | 1,999,862 | ||||||||

TOTAL SHORT TERM INVESTMENTS |

| |||||||||||

(Cost $2,538,582) |

| 2,538,582 | ||||||||||

TOTAL INVESTMENTS - (116.14%) |

| |||||||||||

(Cost $9,085,102) |

| $ | 9,579,717 | |||||||||

Liabilities in Excess of Other Assets (-16.14%) |

| (1,330,969 | ) | |||||||||

NET ASSETS (100.00%) |

| $ | 8,248,748 | |||||||||

6 | October 31, 2010

Table of Contents

| ALPS | GNI Long-Short Fund | ||||||

Statement of Investments |

October 31, 2010 (Unaudited) | |||||

| Expiration Date | Exercise Price | Number of Contracts | Value (Note 1) | |||||||||||||

PUT OPTIONS WRITTEN(a) |

| |||||||||||||||

iShares Russell 2000 Index Fund |

| |||||||||||||||

| January, 2011 | $64.00 | 200 | $ | (34,600 | ) | |||||||||||

Moody’s Corp. |

| |||||||||||||||

| January, 2011 | $20.00 | 200 | (4,400 | ) | ||||||||||||

SPDR S&P 500 |

| |||||||||||||||

| January, 2011 | 110.00 | 300 | (63,600 | ) | ||||||||||||

TOTAL PUT OPTIONS WRITTEN (Premiums received $123,398) |

|

| (102,600 | ) | ||||||||||||

TOTAL OPTIONS WRITTEN (Premiums received $123,398) |

|

| $ (102,600) |

| ||||||||||||

| SCHEDULE OF SECURITIES SOLD SHORT | Shares | Value (Note 1) | ||||||

COMMON STOCKS |

| |||||||

AutoZone, Inc.(a) | (800 | ) | $ | (190,104 | ) | |||

Boston Beer Co., Inc., Class A(a) | (3,500 | ) | (250,565 | ) | ||||

Brown-Forman Corp., Class B | (2,500 | ) | (152,025 | ) | ||||

Career Education Corp.(a) | (3,000 | ) | (52,620 | ) | ||||

First Solar, Inc.(a) | (700 | ) | (96,376 | ) | ||||

Foot Locker, Inc. | (6,000 | ) | (95,580 | ) | ||||

Garmin, Ltd. | (3,500 | ) | (114,940 | ) | ||||

Intuitive Surgical, Inc.(a) | (465 | ) | (122,272 | ) | ||||

NetFlix, Inc.(a) | (1,000 | ) | (173,500 | ) | ||||

OfficeMax, Inc.(a) | (6,000 | ) | (106,200 | ) | ||||

ProShares Ultra S&P500 | (12,000 | ) | (508,200 | ) | ||||

Regions Financial Corp. | (17,500 | ) | (110,250 | ) | ||||

| Shares | Value (Note 1) | |||||||

COMMON STOCKS (continued) |

| |||||||

RPC, Inc. | (5,500 | ) | $ | (121,055 | ) | |||

Salesforce.com, Inc(a) | (1,000 | ) | (116,070 | ) | ||||

Terex Corp.(a) | (2,500 | ) | (56,125 | ) | ||||

Williams-Sonoma, Inc. | (3,000 | ) | (97,110 | ) | ||||

TOTAL SECURITIES SOLD SHORT (Proceeds $2,250,009) |

| $ (2,362,992 | ) | |||||

Common Abbreviations:

ADR - American Depositary Receipt

DN - Discount Note

SA - Generally designates corporations in various countries, mostly employing the civil law.

S&P - Standard & Poor’s

SPDR - Standard & Poor’s Depositary Receipt

| (a) | Non-Income Producing Security. |

| (b) | All or a portion of the security is pledged as collateral on written options and/or short sales as of October 31, 2010. Aggregate collateral segregation to cover margin or segregration requirements on options contracts and short sales as of October 31, 2010 was $3,166,832. |

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

Top Ten Long Holdings (as a % of Net Assets) †

Philip Morris International, Inc. | 11.70 | % | ||

Newmont Mining Corp. | 9.59 | % | ||

Kraft Foods, Inc., Class A | 7.43 | % | ||

Cia de Minas Buenaventura SA, ADR | 7.39 | % | ||

Archer-Daniels-Midland Co. | 7.27 | % | ||

The Coca-Cola Co. | 5.95 | % | ||

American International Group, Inc. | 5.35 | % | ||

Baidu, Inc. ADR | 5.33 | % | ||

Microsoft Corp. | 5.17 | % | ||

Medicis Pharmaceutical Corp., Class A | 5.05 | % | ||

Top Ten Long Holdings | 70.23 | % | ||

† Holdings are subject to change. | ||||

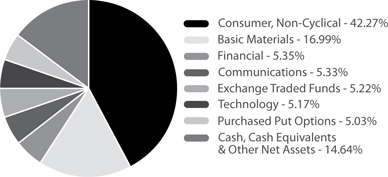

Industry Sector Allocation (Long Positions as a % of Net Assets)

7 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

Overview

The first half of this fiscal year may go down as one of the strangest in our history of managing the ALPS | Red Rocks Listed Private Equity Fund (the “Fund”). Strange because the see-saw nature of world economic news, and the ensuing manic behavior of the equity markets was, at times, out of sync with the overall positive fundamental news coming from our portfolio companies. That development coupled with the quiet and orderly flow of activity in the listed private equity markets made for an almost surreal six months. There were no disruptions (major or minor) in the private equity world on which we focus. The debt markets continued to be accommodating to the underlying businesses of our listed private equity portfolio. In addition, the mergers and acquisitions environment was very robust with a number of transactions being both announced and consummated during the period ended October 31, 2010. In almost all examples such transactions had a positive impact on the most recent carrying valuations of our portfolio companies. In summary, the healing process of the previous year has continued.

That’s not to say that everything is back to normal and times are good. They’re far from it. Our portfolio companies, and their existing underlying businesses, continue to be challenged to find top line organic growth in a less than robust world. Consumers and corporations alike are extremely picky as to where they spend their sacred cash. The new strategy appears to be one of deferral: defer purchases until absolutely needed, or until something actually breaks or wears out. Doing more with less appears to be the new mantra. And de-levering is all the rage, whether by choice or not.

All of these issues have conspired to make for extremely challenging times for the private equity world. The management teams of our listed private equity portfolio are working harder than ever. Harder in squeezing out value through operational excellence in the businesses they own - and not through financial engineering. Harder in finding new businesses to invest in - the competition for high quality acquisition targets has rarely been higher. Harder in searching for investment alternatives in an ever-changing and different environment.

We seriously doubt that anyone had a relaxing and easy summer in the private equity world in which we invest.

Portfolio Review

For the six months ended October 31, 2010, the Class A shares returned 1.46% net of fees and sales loads, compared with 4.11% and 3.05% for the S&P Listed Private Equity Index and the MSCI World Index, respectively. As has become typical, we made few changes to the portfolio during the previous six months. The historically low turnover of the portfolio builds on our theme of being long-term investors in listed private equity companies, especially when management is steadfast in its execution.

Overall, we were quite pleased with how the portfolio performed during the previous six months, meeting, or in certain cases, exceeding our expectations.

Net contributors to performance for the six-month period included:

| » | 3i Group: 3i Group continued to be quite active, achieving liquidity within the portfolio (MHM Holding GmbH is being sold for to Caterpillar for approximately $810M), making several new investments, and forming a separate business line through the purchase of Mizuho Investment Management UK, a debt asset manager. In addition, 3i has reduced its net debt by $1.5B+ in the past year. |

| » | Intermediate Capital Group: The purchase of Royal Bank of Scotland’s €1.4 billion corporate loan portfolio by Intermediate Capital was seen as a major positive by the investor public. |

Net detractors to performance for the six-month period included:

| » | Jafco: The Japanese economy continues to be challenged from a growth perspective, muting any positive liquidity events for Jafco. |

| » | Candover Investments: After doubling in price from the beginning of 2010 to the end of April, Candover gave back a good portion of its stock price gains. The primary culprit, of the run up and the give back, was the rumored takeover of Candover by a Canadian pension plan which failed to materialize. Notwithstanding, Candover achieved several liquidity events (including Ontex and Equity Trust), and looks to be on firmer footing in 2010. |

The portfolio has seen very little movement from a diversification standpoint. Broad indirect geographic, industry, vintage and stage of investment diversification is the cornerstone of the Red Rocks listed private equity strategy. Investors in our product continue to receive institutional exposure to the private equity asset class without the inherent risk that can be associated with a non-diversified portfolio approach.

8 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

Looking Ahead

Uncertainty surrounding the future is THE topic that we continue to hear about. Are we entering a period of prolonged deflation? When will the consumer come back? What about government spending and taxes? What’s going to happen with China, especially with respect to trade and its currency, the yuan? Are Portugal, Italy, Ireland, Greece and Spain real problems that can significantly disrupt the European Union (and the rest of the world), or is that concern overblown? How is the developed world going to pay for the ever increasing amounts of government debt and unfunded liabilities? Is the banking system truly fixed and on sustainable ground?

The answer to these questions and many more is: no one knows, at least not yet.

A potentially more relevant question is how will the outcomes of these issues affect the listed private equity portfolio that we’re managing for you, our shareholders? We continue to ask ourselves that question on a daily basis. While we may not have THE answer(s), we have positioned the portfolio to both weather the continuing storm of uncertainty and to benefit as conditions improve and hopefully move forward.

As always, we appreciate your continued support and interest in Red Rocks and in the ALPS | Red Rocks Listed Private Equity Fund.

Adam Goldman | Co-Portfolio Manager

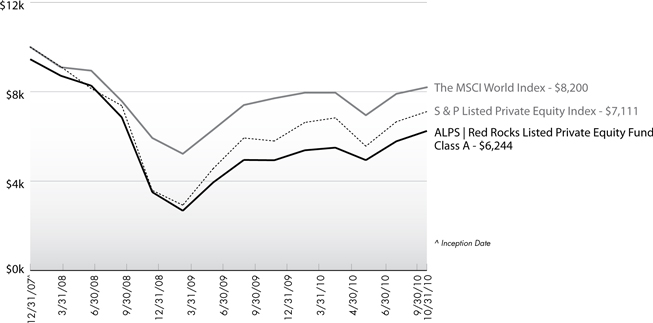

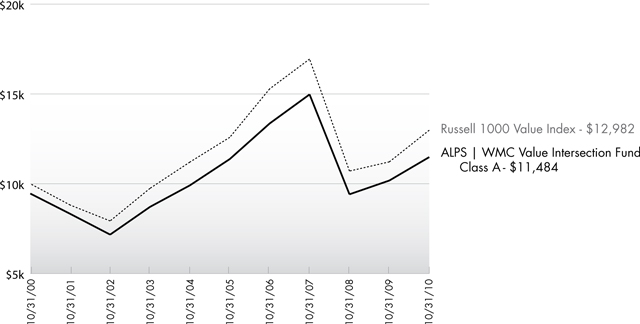

Performance of $10,000 Initial Investment (as of October 31, 2010)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

Source: Morningstar

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

9 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

| Average Annual Total Returns (as of October 31, 2010) | ||||||||||

| 6 Month Cummulative Returns | 1 Year | Since Inception^ | Gross Expense Ratio | Net Expense Ratio* | ||||||

Class A (NAV)1 | 7.35% | 22.60% | -15.30% | 1.86% | 1.65% | |||||

Class A (MOP)2 | 1.46% | 15.93% | -16.97% | |||||||

Class C (NAV)1 | 6.44% | 21.11% | -16.08% | 2.46% | 2.40% | |||||

Class C (CDSC)2 | 5.44% | 20.11% | -16.08% | |||||||

Class I | 7.32% | 22.97% | -15.06% | 1.62% | 1.40% | |||||

Class R | 6.77% | 21.93% | -15.80% | 2.42% | 1.90% | |||||

MSCI World Index3 | 3.05% | 12.74% | -6.76% | |||||||

S&P LPE Index4 | 4.11% | 28.81% | -11.34% | |||||||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 90 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call (866) 759-5679.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. CDSC performance for Class C shares includes a 1% contingent deferred sales charge (CDSC) on C shares redeemed within 12 months of purchase. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account.

Performance shown for Class C shares prior to June 30, 2010 reflects the historical performance of the Fund’s Class A shares, calculated using the fees and expenses of Class C shares.

1 Net Asset Value (NAV) is the share price without sales charges. The performance data shown does not reflect the decution of the sales load or the redemption fee or CDSC, and that, if reflected, the load or fee would reduce the performance quoted. 2 Maximum Offering Price (MOP) includes sales charges. Returns include effects of the Fund’s maximum sales charge of 5.50% for ALPS/Red Rocks Listed Private Equity Fund - A Shares. 3 MSCI World Index: Morgan Stanley Capital International’s market capitalization weighted index is composed of companies representative of the market structure of 22 developed market countries in North America, Europe and the Asia/Pacific Region. You cannot invest directly in the index. 4 S&P Listed Private Equity Index: The S&P Listed Private Equity Index is comprised of 30 leading listed private equity companies that meet size, liquidity, exposure, and activity requirements. The index is designed to provide tradable exposure to the leading publicly listed companies in the private equity space. ^ Fund inception date of 12/31/2007. The Fund began trading on 1/2/2008. * Effective through August 31, 2011, the Adviser and the Red Rocks Capital LLC (the “Sub-Adviser”) have given a contractual agreement to the Fund to limit the amount of the Fund’s total annual expenses, exclusive of distribution and service (12b-1) fees, shareholder service fees (C shares only), acquired fund fees and expenses, brokerage expenses, interest expenses, taxes and extraordinary expenses, to 1.25% of the Fund’s average daily net assets. This agreement is reevaluated on an annual basis. Without this agreement expenses could be higher.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Listed Private Equity Companies are subject to various risks depending on their underlying investments, which could include, but are not limited to, additional liquidity risk, industry risk, non-U.S. security risk, currency risk, credit risk, managed portfolio risk and derivatives risk (derivatives risk is the risk that the value of the Listed Private Equity Companies’ derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment).

There are inherent risks in investing in private equity companies, which encompass financial institutions or vehicles whose principal business is to invest in and lend capital to privately held companies. Generally, little public information exists for private and thinly traded companies, and there is a risk that investors may not be able to make a fully informed investment decision.

Listed Private Equity Companies may have relatively concentrated investment portfolios, consisting of a relatively small number of holdings. A consequence of this limited number of investments is that the aggregate returns realized may be adversely impacted by the poor performance of a small number of investments, or even a single investment, particularly if a company experiences the need to write down the value of an investment.

Certain of the Fund’s investments may be exposed to liquidity risk due to low trading volume, lack of a market maker or legal restrictions limiting the ability of the Fund to sell particular securities at an advantageous price and/or time. As a result, these securities may be more difficult to value. Foreign investing involves special risks, such as currency fluctuations and political uncertainty. The Fund invests in derivatives and is subject to the risk that the value of those derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment. | ||||||||||

10 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges, redemption fees, or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010. |

| Beginning Account Value 5/1/10 | Ending Account Value 10/31/10 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/10- 10/31/10 | |||||||||||||

Class A | ||||||||||||||||

Actual | $1,000.00 | $1,073.50 | 1.50% | $7.84 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,017.64 | 1.50% | $7.63 | ||||||||||||

Class C(c) | ||||||||||||||||

Actual | $1,000.00 | $1,064.40 | 2.25% | $7.76 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,017.68 | 2.25% | $11.42 | ||||||||||||

Class I | ||||||||||||||||

Actual | $1,000.00 | $1,073.20 | 1.25% | $6.53 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,018.90 | 1.25% | $6.36 | ||||||||||||

Class R | ||||||||||||||||

Actual | $1,000.00 | $1,067.70 | 1.75% | $9.12 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,016.38 | 1.75% | $8.89 | ||||||||||||

| (a) | The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 365. |

| (c) | Class C shares commenced operations on July 2, 2010. |

11 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

| Shares | Value (Note 1) | |||||||

COMMON STOCKS (99.29%) |

| |||||||

Communications (1.56%) |

| |||||||

Internet (1.56%) |

| |||||||

Internet Capital Group, Inc.(a) | 171,000 | $ | 2,135,790 | |||||

TOTAL COMMUNICATIONS | 2,135,790 | |||||||

Consumer, Non-Cyclical (1.40%) |

| |||||||

Food (1.40%) |

| |||||||

Orkla ASA | 198,000 | 1,916,914 | ||||||

TOTAL CONSUMER, NON-CYCLICAL |

| 1,916,914 | ||||||

Diversified (12.21%) |

| |||||||

Holding Companies-Diversified Operations (12.21%) |

| |||||||

Ackermans & van Haaren N.V. | 34,300 | 2,956,000 | ||||||

HAL Trust | 34,400 | 4,194,129 | ||||||

Leucadia National Corp.(a) | 225,300 | 5,727,126 | ||||||

Wendel Investissement | 49,000 | 3,797,297 | ||||||

| 16,674,552 | ||||||||

TOTAL DIVERSIFIED |

| 16,674,552 | ||||||

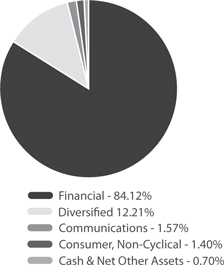

Financial (84.12%) | ||||||||

Closed-End Funds (25.97%) |

| |||||||

AP Alternative Assets LP | 481,600 | 3,621,632 | ||||||

ARC Capital Holdings, Ltd.(a) | 2,488,000 | 2,948,280 | ||||||

Candover Investments PLC(a) | 171,000 | 1,986,524 | ||||||

Castle Private Equity, Ltd.(a) | 85,000 | 669,427 | ||||||

Conversus Capital LP(a) | 347,000 | 6,003,100 | ||||||

Electra Private Equity PLC(a) | 166,000 | 4,154,788 | ||||||

Graphite Enterprise Trust PLC | 572,357 | 2,751,364 | ||||||

HBM BioVentures AG, Class A(a) | 75,927 | 3,136,459 | ||||||

HgCapital Trust PLC(a) | 47,670 | 66,073 | ||||||

HgCapital Trust PLC | 190,000 | 2,864,857 | ||||||

Princess Private Equity | ||||||||

Holding, Ltd.(a) | 346,472 | 2,623,290 | ||||||

Standard Life European Private | ||||||||

Equity Trust PLC | 40,178 | 80,153 | ||||||

SVG Capital PLC(a) | 1,407,666 | 4,556,283 | ||||||

| 35,462,230 | ||||||||

Diversified Financial Services (23.11%) |

| |||||||

Blackstone Group LP | 401,500 | 5,412,220 | ||||||

GP Investments, Ltd.(a) | 517,000 | 2,189,261 | ||||||

Intermediate Capital Group PLC | 1,133,900 | 5,865,000 | ||||||

KKR & Co. LP | 833,600 | 10,570,048 | ||||||

Onex Corp. | 256,600 | 7,515,091 | ||||||

| 31,551,620 | ||||||||

| Shares | Value (Note 1) | |||||||||||

Investment Companies (18.93%) |

| |||||||||||

American Capital Strategies, Ltd.(a) | 217,000 | $ | 1,514,660 | |||||||||

Apollo Investment Corp. | 127,500 | 1,401,225 | ||||||||||

China Merchants China | ||||||||||||

Direct Investments, Ltd. | 1,066,000 | 2,461,719 | ||||||||||

DeA Capital SpA(a) | 761,000 | 1,388,566 | ||||||||||

Eurazeo | 83,300 | 6,330,193 | ||||||||||

Investor AB, Class B | 188,000 | 3,858,705 | ||||||||||

MVC Capital, Inc. | 119,300 | 1,592,655 | ||||||||||

Ratos AB, B Shares | 152,200 | 5,427,536 | ||||||||||

RHJ International(a) | 240,450 | 1,874,097 | ||||||||||

| 25,849,356 | ||||||||||||

Private Equity (15.14%) |

| |||||||||||

3i Group PLC | 1,553,000 | 7,455,435 | ||||||||||

Altamir Amboise(a) | 388,000 | 3,040,321 | ||||||||||

Deutsche Beteiligungs AG | 81,610 | 2,363,713 | ||||||||||

Dinamia Capital Privado | ||||||||||||

S.C.R., SA | 110,770 | 1,347,451 | ||||||||||

GIMV N.V. | 70,400 | 3,892,875 | ||||||||||

IP Group PLC(a) | 1,145,315 | 532,209 | ||||||||||

JAFCO Co., Ltd. | 98,050 | 2,049,461 | ||||||||||

| 20,681,465 | ||||||||||||

Real Estate (0.97%) |

| |||||||||||

Brookfield Asset Management, | ||||||||||||

Inc., Class A | 44,500 | 1,322,540 | ||||||||||

TOTAL FINANCIAL |

| 114,867,211 | ||||||||||

TOTAL COMMON STOCKS |

| |||||||||||

(Cost $108,466,055) |

| 135,594,467 | ||||||||||

| 7-Day Yield | Shares | Value (Note 1) | ||||||||||

SHORT TERM INVESTMENTS (0.71%) |

| |||||||||||

Money Market Fund (0.71%) |

| |||||||||||

Dreyfus Treasury Prime Cash Management, Investor Shares | 0.00004 | % | 961,958 | 961,958 | ||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $961,958) |

| 961,958 | ||||||||||

TOTAL INVESTMENTS (100.00%) |

| |||||||||||

(Cost $109,408,013) |

| $ | 136,556,425 | |||||||||

Other Assets in Excess |

| 3,291 | ||||||||||

NET ASSETS (100.00%) |

| $ | 136,559,716 | |||||||||

12 | October 31, 2010

Table of Contents

| ALPS | Red Rocks Listed Private Equity Fund | ||||||

Statement of Investments |

October 31, 2010 (Unaudited) | |||||

Common Abbreviations:

AB - Aktiebolag is the Swedish equivalent of the term corporation.

AG - Aktiengesellschaft is a German term that refers to a corporation that is limited by shares, i.e., owned by shareholders.

ASA - Allmennaksjeselskap is the Norweigian term for a public company.

LP - Limited Partnership

Ltd. - Limited

N.V. - Naamloze Vennootschap is the Dutch term for a public limited liability corporation.

PLC - Public Limited Company

SA - Generally designates corporations in various countries, mostly those employing the civil law. This translates literally in all languages mentioned as anonymous company.

SpA - Societa Per azioni is an Italian shared company.

| (a) | Non-Income Producing Security. |

| (b) | Less than 0.005% of Net Assets. |

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

Top Ten Holdings (as a % of Net Assets) †

KKR & Co. LP | 7.74% | |||

Onex Corp. | 5.50% | |||

3i Group PLC | 5.46% | |||

Eurazeo | 4.64% | |||

Conversus Capital LP | 4.40% | |||

Intermediate Capital Group PLC | 4.29% | |||

Leucadia National Corp. | 4.19% | |||

Ratos AB, B Shares | 3.97% | |||

Blackstone Group LP | 3.96% | |||

SVG Capital PLC | 3.34% | |||

Top Ten Holdings | 47.49% |

| † | Holdings are subject to change. |

Industry Sector Allocation (as a % of Net Assets)

13 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

Market Comment

US equities rebounded in the latter part of the period as investors shrugged off concerns about the pace of economic growth. Strong corporate earnings, and robust merger and acquisition activity boosted investors’ enthusiasm for stocks. Favorable economic data helped to ease fears of a double-dip global recession and increase investors’ appetite for risk. The September and October rally erased much of the losses experienced early on in the period and pushed the broad market back into positive ground for the six months ending October 31, 2010.

Within the Russell 1000 Value Index, seven of the ten sectors recorded positive absolute returns during the period. Telecommunications Services, Utilities, and Consumer Staples led the Index higher posting the most positive returns while Financials, Industrials, and Consumer Discretionary lagged.

Fund Review

The Portfolio outperformed the Index, net of fees, for the period posting positive relative results in six of the ten broad market sectors. Strong stock selection in the Consumer Staples, Health Care, and Financials sectors more than offset negative returns within the Consumer Discretionary and Telecommunications Services sectors.

Among the top relative contributors to performance were TRW Automotive Holdings (Consumer Discretionary), Freeport-McMoRan (Materials) and Ameriprise Financial (Financials). Auto supplier TRW Automotive’s results exceeded expectations and management raised guidance citing a reduced cost structure, new business wins, and higher levels of vehicle production. Freeport-McMoRan, a global mining company with attractive copper and gold assets, is benefiting from solid demand trends and favorable pricing for copper. Ameriprise Financial is a provider of financial planning and asset management products and services. Higher average balances and good expense control at its Wealth Management and Asset Management businesses contributed to higher margins and profits. We believe the company should benefit from continued margin improvements in these divisions. Additionally, the acquisition of Columbia Management offers additional upside for the stock.

Among the top relative detractors to performance were Gap (Consumer Discretionary), Wells Fargo & Company (Financials) and Office Depot (Consumer Discretionary). Gap is a US-based global specialty retailer offering clothing, accessories, and personal care products. The company reported better-than expected second quarter earnings; however, sales disappointed and increasing inventory levels raised concerns about potential markdown risk. We trimmed our position due to softer sales trends. Wells Fargo, a diversified financial services company, shares declined modestly during the period due to ongoing concerns about regulatory pressures and the risk of mortgage “put backs”. We continue to hold our position as the shares trade at a low multiple of normalized earnings (average earnings over a cycle), as we believe the impact of put backs, if it occurs, should be very small, and overall we feel the company should benefit from an improving economy. Office Depot is a provider of office products, services, and supplies globally. Our holdings in Office Depot detracted from relative performance during the period as investors started to discount the potential for economic slowing in the second half of 2010. Given the company’s broad enterprise exposure and earnings sensitivity to incremental sales, we believe that the stock remains attractive in a scenario where we see a continued economic recovery.

Outlook

Throughout much of the recent downturn, developed market fiscal and monetary stimulus provided much-needed support to the global economy. While this was beneficial in the short term, over the longer run we believe it has the potential to open the door to imbalances in the economy as the government squeezes out private sector growth. As the recovery progresses and stimulus spending winds down, we believe that growth in the more efficient, productivity-enhancing private sector will provide sluggish Gross Domestic Product expansion for 2011. Global deflation is unlikely due to an unprecedented amount of government fiscal and monetary stimulus. The US Government recently announced that it intends to further support the economy through additional quantitative easing, if necessary. Given the high level of developed market economic slack created by the recession, we believe policy bias is likely to remain loose for some time.

14 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

The Fund focuses on stock selection as the key driver of returns and uses proprietary fundamental and quantitative research in a disciplined framework to build a portfolio of the most attractive stocks. We are confident this unique investment process can provide shareholders with more consistent and style pure investment results. Sector exposures are residuals from this bottom-up stock selection process and are not explicit management decisions. Based on individual stock decisions, the Fund ended the period most overweight the Industrials, Consumer Discretionary, and Energy sectors and most underweight Consumer Staples, Telecommunication Services, and Information Technology sectors relative to the Russell 1000 Value Index, the Fund’s benchmark.

Performance of $10,000 Initial Investment (as of October 31, 2010)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

Source: Morningstar

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

15 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

| Average Annual Total Returns (as of October 31, 2010) |

| 6 Month Cummulative Returns | 1 Year | 5 Year | 10 Year | Gross Expense Ratio | Net Expense Ratio^ | |||||||

Class A (NAV)1 | -1.21% | 12.80% | 0.19% | 1.96% | 1.71% | 1.41% | ||||||

Class A (MOP)2 | -6.62% | 6.64% | -0.93% | 1.39% | ||||||||

Class C (NAV)1 | -1.47% | 12.08% | -0.54% | 1.22% | 2.46% | 2.16% | ||||||

Class C (CDSC)2 | -2.46% | 11.08% | -0.54% | 1.22% | ||||||||

Class I | -1.07% | 13.13% | 0.38% | 2.11% | 1.50% | 1.16% | ||||||

Russell 1000 Value Index3 | -1.75% | 15.71% | 0.62% | 2.64% | ||||||||

S&P 500 Index4 | 0.74% | 16.52% | 1.73% | -0.02% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call (866) 759-5679.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. CDSC performance for Class C shares includes a 1% CDSC on C shares redeemed within 12 months of purchase. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account.

Performance shown for Class C shares prior to June 30, 2010 reflects the historical performance of the Fund’s Class A shares, calculated using the fees and expenses of Class C shares.

The performance shown for the ALPS | WMC Value Intersection Fund (the “Fund”) for periods prior to August 29, 2009, reflects the performance of the Activa Mutual Funds Trust – Activa Value Fund (as result of a prior reorganization of Activa Mutual Funds Trust – Activa Value Fund into the Fund).

1 Net Asset Value (NAV) is the share price without sales charges. 2 Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%. 3 The Russell 1000 Value Index measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. You cannot invest directly in the index. 4 The S&P 500 Index is the Standard & Poor’s composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices. You cannot invest directly in the index. ^ The Adviser has given a contractual agreement to the Fund to limit the amount of the Fund’s total annual expenses, exclusive of distribution and service (12b-1) fees, shareholder service fees, brokerage expenses, interest expenses, taxes and extraordinary expenses, to 1.15% of the Fund’s average daily net assets. This agreement is in effect through August 31, 2011.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Mutual funds, annuities and other investments are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested. Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund’s original investment. |

16 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads); and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

The examples are based on an investment of $1,000 invested on May 1, 2010 and held until October 31, 2010. |

| Beginning Account Value 5/1/10 | Ending Account Value 10/31/10 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/10-10/31/10 | |||||||||||||

Class A | ||||||||||||||||

Actual | $1,000.00 | $987.90 | 1.40% | $7.01 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,018.15 | 1.40% | $7.12 | ||||||||||||

Class C(c) | ||||||||||||||||

Actual | $1,000.00 | $1,145.30 | 2.15% | $7.71 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,009.52 | 2.15% | $10.89 | ||||||||||||

Class I | ||||||||||||||||

Actual | $1,000.00 | $989.30 | 1.15% | $5.77 | ||||||||||||

Hypothetical (5% return before expenses) | $1,000.00 | $1,019.41 | 1.15% | $5.85 | ||||||||||||

(a) The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. (b) Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 365. (c) Class C shares commenced operations on July 2, 2010. |

17 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

| Shares | Value (Note 1) | |||||||

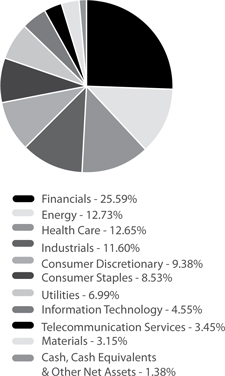

COMMON STOCKS (98.62%) |

| |||||||

Consumer Discretionary (9.38%) |

| |||||||

Automobiles & Components (2.74%) |

| |||||||

Ford Motor Co.(a) | 65,900 | $ | 931,167 | |||||

TRW Automotive Holdings | 14,100 | 644,229 | ||||||

| 1,575,396 | ||||||||

Consumer Durables & Apparel (1.02%) |

| |||||||

Mattel, Inc. | 13,600 | 317,288 | ||||||

Whirlpool Corp. | 3,600 | 272,988 | ||||||

| 590,276 | ||||||||

Consumer Services (0.22%) |

| |||||||

Carnival Corp. | 2,900 | 125,193 | ||||||

Media (2.71%) |

| |||||||

CBS Corp., Class B | 27,700 | 468,961 | ||||||

Gannett Co., Inc. | 24,000 | 284,400 | ||||||

Time Warner Cable, Inc. | 13,939 | 806,650 | ||||||

| 1,560,011 | ||||||||

Retailing (2.69%) |

| |||||||

Abercrombie & Fitch Co. - Class A | 10,800 | 462,888 | ||||||

The Gap, Inc. | 18,300 | 347,883 | ||||||

Kohl’s Corp.(a) | 4,800 | 245,760 | ||||||

Lowe’s Cos., Inc. | 11,100 | 236,763 | ||||||

Office Depot, Inc.(a) | 56,300 | 252,787 | ||||||

| 1,546,081 | ||||||||

TOTAL CONSUMER DISCRETIONARY |

| 5,396,957 | ||||||

Consumer Staples (8.53%) |

| |||||||

Food & Staples Retailing (1.34%) |

| |||||||

Wal-Mart Stores, Inc. | 14,200 | 769,214 | ||||||

Food Beverage & Tobacco (5.42%) |

| |||||||

Altria Group, Inc. | 30,200 | 767,684 | ||||||

Archer-Daniels-Midland Co. | 17,500 | 583,100 | ||||||

Dr Pepper Snapple Group, Inc. | 12,900 | 471,495 | ||||||

Lorillard, Inc. | 6,700 | 571,778 | ||||||

Philip Morris International, Inc. | 12,425 | 726,862 | ||||||

| 3,120,919 | ||||||||

Household & Personal Products (1.77%) |

| |||||||

Herbalife, Ltd. | 7,100 | 453,406 | ||||||

Kimberly-Clark Corp. | 8,900 | 563,726 | ||||||

| 1,017,132 | ||||||||

TOTAL CONSUMER STAPLES |

| 4,907,265 | ||||||

| Shares | Value (Note 1) | |||||||

Energy (12.73%) | ||||||||

Energy (12.73%) |

| |||||||

Anadarko Petroleum Corp. | 11,500 | $ | 708,055 | |||||

Apache Corp. | 1,400 | 141,428 | ||||||

Baker Hughes, Inc. | 10,500 | 486,465 | ||||||

Chevron Corp. | 20,419 | 1,686,814 | ||||||

ConocoPhillips | 6,100 | 362,340 | ||||||

Exxon Mobil Corp. | 7,564 | 502,779 | ||||||

Hess Corp. | 9,700 | 611,391 | ||||||

Marathon Oil Corp. | 29,000 | 1,031,530 | ||||||

National Oilwell Varco, Inc. | 15,700 | 844,032 | ||||||

Occidental Petroleum Corp. | 12,100 | 951,423 | ||||||

TOTAL ENERGY | 7,326,257 | |||||||

Financials (25.59%) | ||||||||

Banks (6.13%) |

| |||||||

Comerica, Inc. | 12,360 | 442,241 | ||||||

PNC Financial Services | 11,700 | 630,630 | ||||||

US Bancorp | 27,900 | 674,622 | ||||||

Wells Fargo & Co. | 68,200 | 1,778,656 | ||||||

| 3,526,149 | ||||||||

Diversified Financials (9.90%) |

| |||||||

Ameriprise Financial, Inc. | 17,800 | 920,082 | ||||||

Bank of America Corp. | 110,912 | 1,268,833 | ||||||

Citigroup, Inc.(a) | 67,300 | 280,641 | ||||||

The Goldman Sachs Group, Inc. | 6,700 | 1,078,365 | ||||||

JPMorgan Chase & Co. | 48,700 | 1,832,581 | ||||||

SLM Corp.(a) | 26,600 | 316,540 | ||||||

| 5,697,042 | ||||||||

Insurance (7.64%) | ||||||||

ACE, Ltd. | 13,300 | 790,286 | ||||||

Allied World Assurance Co. Holdings, Ltd. | 7,800 | 446,238 | ||||||

Axis Capital Holdings, Ltd. | 15,000 | 510,150 | ||||||

Everest Re Group, Ltd. | 4,300 | 362,404 | ||||||

Genworth Financial, Inc. - Class A(a) | 37,500 | 425,250 | ||||||

Hartford Financial Services | 23,400 | 561,132 | ||||||

MetLife, Inc. | 12,200 | 492,026 | ||||||

The Travelers Cos., Inc. | 8,500 | 469,200 | ||||||

Unum Group | 15,200 | 340,784 | ||||||

| 4,397,470 | ||||||||

18 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

Statement of Investments |

October 31, 2010 (Unaudited) | |||||

| Shares | Value (Note 1) | |||||||

Real Estate (1.92%) |

| |||||||

Annaly Capital Management, Inc. | 27,200 | $ | 481,712 | |||||

Forest City Enterprises, Inc. - | ||||||||

Class A(a) | 42,800 | 624,452 | ||||||

| 1,106,164 | ||||||||

TOTAL FINANCIALS |

| 14,726,825 | ||||||

Health Care (12.65%) |

| |||||||

Health Care Equipment & Services (3.78%) |

| |||||||

Aetna, Inc. | 11,500 | 343,390 | ||||||

McKesson Corp. | 7,600 | 501,448 | ||||||

UnitedHealth Group, Inc. | 20,500 | 739,025 | ||||||

WellPoint, Inc.(a) | 10,900 | 592,306 | ||||||

| 2,176,169 | ||||||||

Pharmaceuticals, Biotechnology & Life Sciences (8.87%) |

| |||||||

Amgen, Inc.(a) | 13,900 | 794,941 | ||||||

Eli Lilly & Co. | 13,700 | 482,240 | ||||||

Forest Laboratories, Inc.(a) | 9,828 | 324,816 | ||||||

Gilead Sciences, | 7,600 | 301,492 | ||||||

Merck & Co., Inc. | 17,400 | 631,272 | ||||||

Pfizer, Inc. | 96,123 | 1,672,540 | ||||||

Thermo Fisher Scientific, Inc.(a) | 8,400 | 431,928 | ||||||

Watson Pharmaceuticals, Inc.(a) | 10,000 | 466,500 | ||||||

| 5,105,729 | ||||||||

TOTAL HEALTH CARE |

| 7,281,898 | ||||||

Industrials (11.60%) |

| |||||||

Capital Goods (10.56%) |

| |||||||

3M Co. | 3,800 | 320,036 | ||||||

Caterpillar, Inc. | 8,400 | 660,240 | ||||||

Dover Corp. | 13,100 | 695,610 | ||||||

General Dynamics Corp. | 9,100 | 619,892 | ||||||

General Electric Co. | 59,800 | 957,996 | ||||||

Joy Global, Inc. | 5,300 | 376,035 | ||||||

Northrop Grumman Corp. | 9,100 | 575,211 | ||||||

Oshkosh Corp.(a) | 7,000 | 206,570 | ||||||

Parker Hannifin Corp. | 8,500 | 650,675 | ||||||

The Boeing Co. | 4,300 | 303,752 | ||||||

United Technologies Corp. | 9,500 | 710,315 | ||||||

| 6,076,332 | ||||||||

Commercial & Professional Services (0.45%) |

| |||||||

RR Donnelley & Sons Co. | 14,100 | 260,145 | ||||||

| Shares | Value (Note 1) | |||||||

Transportation (0.59%) |

| |||||||

Delta Air Lines, Inc.(a) | 24,500 | $ | 340,305 | |||||

TOTAL INDUSTRIALS |

| 6,676,782 | ||||||

Information Technology (4.55%) |

| |||||||

Semiconductors & Semiconductor Equipment (1.14%) |

| |||||||

Intel Corp. | 14,000 | 280,980 | ||||||

Xilinx, Inc. | 14,000 | 375,340 | ||||||

| 656,320 | ||||||||

Software & Services (3.41%) |

| |||||||

Accenture PLC - Class A | 16,400 | 733,244 | ||||||

eBay, Inc.(a) | 25,100 | 748,231 | ||||||

Microsoft Corp. | 18,100 | 482,184 | ||||||

| 1,963,659 | ||||||||

TOTAL INFORMATION TECHNOLOGY |

| 2,619,979 | ||||||

Materials (3.15%) |

| |||||||

Materials (3.15%) |

| |||||||

CF Industries Holdings, Inc. | 2,760 | 338,183 | ||||||

Freeport-McMoRan Copper & Gold, Inc. | 6,700 | 634,356 | ||||||

Newmont Mining Corp. | 4,400 | 267,828 | ||||||

Owens-Illinois, Inc.(a) | 8,700 | 243,861 | ||||||

Valspar Corp. | 10,200 | 327,420 | ||||||

TOTAL MATERIALS |

| 1,811,648 | ||||||

Telecommunication Services (3.45%) |

| |||||||

Telecommunication Services (3.45%) |

| |||||||

AT&T, Inc. | 69,645 | 1,984,882 | ||||||

TOTAL TELECOMMUNICATION SERVICES |

| 1,984,882 | ||||||

Utilities (6.99%) |

| |||||||

Utilities (6.99%) |

| |||||||

CenterPoint Energy, Inc. | 22,800 | 377,568 | ||||||

DPL, Inc. | 8,500 | 221,850 | ||||||

Entergy Corp. | 3,500 | 260,855 | ||||||

NextEra Energy, Inc. | 11,200 | 616,448 | ||||||

Northeast Utilities | 15,100 | 472,328 | ||||||

PG&E Corp. | 13,600 | 650,352 | ||||||

UGI Corp. | 31,600 | 950,844 | ||||||

Xcel Energy, Inc. | 19,700 | 470,042 | ||||||

TOTAL UTILITIES |

| 4,020,287 | ||||||

TOTAL COMMON STOCKS (Cost $49,366,767) |

| 56,752,780 | ||||||

19 | October 31, 2010

Table of Contents

| ALPS | WMC Value Intersection Fund | ||||||

Statement of Investments |

October 31, 2010 (Unaudited) | |||||

| 7-Day Yield | Shares | Value (Note 1) | ||||||||

SHORT TERM INVESTMENTS (0.51%) |

| |||||||||

Money Market Fund (0.51%) |

| |||||||||

Fidelity Institutional Money Market - Money Market Portfolio - Class I | 0.23% | 292,498 | $ | 292,498 | ||||||

TOTAL SHORT TERM INVESTMENTS (Cost $292,498) |

| 292,498 | ||||||||

TOTAL INVESTMENTS (99.13%) (Cost $49,659,265) |

| $ | 57,045,278 | |||||||

Other Assets in Excess of |

| 498,182 | ||||||||

NET ASSETS (100.00%) |

| $ | 57,543,460 | |||||||

| (a) | Non-Income Producing Security. |

Common Abbreviations:

Ltd. - Limited

PLC - Public Limited Company

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

Top Ten Holdings (as a % of Net Assets) †

| ||||

AT&T, Inc. | 3.45 | % | ||

JPMorgan Chase & Co. | 3.18 | % | ||

Wells Fargo & Co. | 3.09 | % | ||

Chevron Corp. | 2.93 | % | ||

Pfizer, Inc. | 2.91 | % | ||

Bank of America Corp. | 2.20 | % | ||

The Goldman Sachs Group, Inc. | 1.87 | % | ||

Marathon Oil Corp. | 1.79 | % | ||

General Electric Co. | 1.66 | % | ||

Occidental Petroleum Corp. | 1.65 | % | ||

Top Ten Holdings | 24.73 | % |

| † | Holdings are subject to change. |

Industry Sector Allocation (as a % of Net Assets)

20 | October 31, 2010

Table of Contents

| Clough China Fund | ||||||

|

October 31, 2010 (Unaudited) | |||||

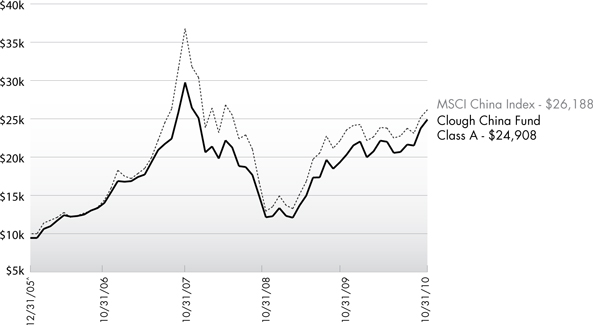

The Clough China Fund - A Shares (excluding applicable sales loads) rose 13.13% for the six-month period ended October 31, 2010 and stood 15.67% higher for the one-year period ended at October 31, 2010. The Fund has outperformed its benchmark, the MSCI China Index, which returned 10.07% and 11.11% over the same periods. The investment environment during the six-month period ended October 31, 2010 was generally positive, yet volatile, especially in the month of September when major international markets began to anticipate new monetary stimulus from the US Federal Reserve. The Fund consistently outperformed the MSCI China Index every month during the quarter, including during August when the benchmark index retreated.

Investment Environment

It appears to us that investors are becoming more comfortable with the outlook for economic growth in China. Despite a noticeable deceleration in the large US and European economies, evidence is pointing towards a “soft landing” in China. GDP grew 10.3% in the second quarter in China, a modest slowdown from the prior quarter, yet still high. Further, while recent data revealed a desirable slowdown in fixed asset investment, exports were resilient as evidenced by the $66.5 billion trade surplus for the third quarter.1 Several economists revised their forecasts for growth marginally down for the full year 2010 (Morgan Stanley to 10%, Deutsche Bank to 9.6%), but took the view the risk of a hard landing was very limited.

Property transaction volumes remained strong in Mainland China and housing prices weakened only slightly despite concerted efforts of government policy to rein in prices and curb speculation. This prompted the Central government to shift its focus towards increasing supply by accelerating the building of affordable housing. The social housing policy will become an important driver of economic growth in China over the coming years.

International pressure on China became louder and stronger for Beijing to speed up the appreciation of the Chinese Yuan (CNY) after the “de-pegging” from the US dollar in June. The reluctance of China’s leaders to bend to this pressure raised new concerns of potential trade conflict. Therefore, investors preferred to remain cautious on Chinese exporters. Meanwhile, domestic consumption remained steady and healthy. Retail sales increased 18.2% year-over-year in the first half2 and accelerated to 18.4% in August.2 Though inflation rose to 3.5% in August from 2.9% in June, it still looks under control. Regardless, purchasing power is rising much faster than prices; household income growth is supported by generous wage increases as

labor markets tighten. According to Morgan Stanley, 27 of the 31 Chinese Provinces have raised minimum wages this year by an average of 20%, some regions have even granted rises above 30%.

Portfolio Composition

To capitalize on the strong growth in consumer purchasing power, the Fund has been massively overweight consumer discretionary and consumer staples relative to the MSCI China index. The consumer discretionary and industrials sectors were the main contributors to the Fund’s outperformance during the quarter. Information technology, health care and energy were the main detractors.

In terms of individual stocks, three major contributors to performance were: 1) China State Construction International (CSCI): the largest construction firm in Hong Kong with expansion opportunities in Mainland China related to the social housing policies. While the Hong Kong infrastructure business remains strong, CSCI is one of the first listed companies with an affordable-housing project in China. CSCI also benefits from the strong support of their parent company, a state-owned enterprise based in Beijing. 2) Air China: the nation’s largest international carrier returned to profit in 2009 and is enjoying strong passenger and cargo traffic growth this year. Air China also benefits from currency appreciation as approximately 80% of its financial debts are US dollar denominated. 3) Vinda International: a leading household tissue paper producer has been building domestic brand and benefits from rising household incomes and consumer’s desires for healthier lifestyles.

Three of the major detractors to performance were: 1) China Life Insurance: the country’s largest life insurance company with over 40% market share, whose premium growth has slowed this year. 2) China Resources Power (CRP): the most profitable and efficient power producer in China, CRP is vertically integrated in coal mining to reduce raw material costs and improve margins. CRP’s underperformance had more to do with its belonging to the utilities’ sector rather than specific company issues. 3) Ruinian International: China’s largest amino acid-based nutritional supplement manufacturer. Ruinian shares declined after some of their products failed official quality tests. We eliminated this position during the quarter.

Investment Outlook

Clough Capital remains optimistic on China’s economic growth and equity markets over the next 12 – 18 months. China’s

21 | October 31, 2010

Table of Contents

| Clough China Fund | ||||||

Management Commentary |

October 31, 2010 (Unaudited) | |||||

growth model is evolving as fixed asset investment is moving from the coastal provinces, which already have well developed infrastructure like highways, rail transport, airports and power generation. We believe the new beneficiaries of investment capital will be the interior provinces in Central and Western China which have significantly lagged in infrastructure quality. This rebalancing is also helping to tighten labor markets as migrant workers have improved access to higher paying jobs at home and find it less attractive to migrate to the export factory hubs, particularly in Southern China. The income prospects for the Chinese worker have never been better in our opinion and this is very positive for the equity markets. Importantly, government policy is firmly behind this economic rebalancing which should be evident when the draft of the government’s 12th Five Year plan is released in the coming months.

While the Fund has performed well this year, Chinese equity markets have been sluggish, especially compared to the rest of Asia. Hong Kong’s Hang Seng index only recently went positive and the Shanghai Composite index remains 7.54% lower calendar year-to-date, as we write. The major reason for China underperforming the region has been weak returns from the banking sector, which has been held back over concerns