UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8194

FINANCIAL INVESTORS TRUST

(exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

David T. Buhler, Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: May 1, 2013 - October 31, 2013

Item 1. Reports to Stockholders.

| ||

| ||

| ||

Table of Contents October 31, 2013 |

| Disclosure of Fund Expenses | 1 | |||||||

| ALPS | Alerian MLP Infrastructure Index Fund | ||||||||

| 5 | ||||||||

| 6 | ||||||||

| 8 | ||||||||

| 9 | ||||||||

| 10 | ||||||||

| 11 | ||||||||

| 12 | ||||||||

| ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||||||||

| 15 | ||||||||

| 17 | ||||||||

| 19 | ||||||||

| 25 | ||||||||

| 26 | ||||||||

| 27 | ||||||||

| 28 | ||||||||

| ALPS | Kotak India Growth Fund | ||||||||

| 31 | ||||||||

| 34 | ||||||||

| 36 | ||||||||

| 38 | ||||||||

| 39 | ||||||||

| 40 | ||||||||

| 41 | ||||||||

| ALPS | Red Rocks Listed Private Equity Fund | ||||||||

| 44 | ||||||||

| 45 | ||||||||

| 47 | ||||||||

| 49 | ||||||||

| 50 | ||||||||

| 51 | ||||||||

| 52 | ||||||||

| ALPS | WMC Disciplined Value Fund | ||||||||

| 56 | ||||||||

| 57 | ||||||||

| 59 | ||||||||

| 62 | ||||||||

| 63 | ||||||||

| 64 | ||||||||

| 65 | ||||||||

| Clough China Fund | ||||||||

| 68 | ||||||||

| 70 | ||||||||

| 72 | ||||||||

| 75 | ||||||||

| 76 | ||||||||

| 77 | ||||||||

| 78 | ||||||||

| RiverFront Global Allocation Series | ||||||||

| 81 | ||||||||

| 83 | ||||||||

| 93 | ||||||||

| 103 | ||||||||

| 105 | ||||||||

| 106 | ||||||||

| 111 | ||||||||

| Notes to Financial Statements | 128 | |||||||

| Additional Information | 153 | |||||||

| October 31, 2013 (Unaudited) | ||

As a shareholder of the Funds, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2013 and held until October 31, 2013.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges, redemption fees, or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| 1 | October 31, 2013 |

Disclosure of Fund Expenses | ||

| October 31, 2013 (Unaudited) | ||

| Beginning Account Value May 1, 2013 | Ending Account Value October 31, 2013 | Expense Ratio(a) | Expense Paid During Period May 1, 2013 - October 31, 2013(b) | |||||

| ALPS | Alerian MLP Infrastructure Index Fund | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 1,032.40 | 1.25% | $ 6.40 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 1,029.70 | 1.85% | $ 9.46 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.88 | 1.85% | $ 9.40 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 1,033.30 | 0.85% | $ 4.36 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.92 | 0.85% | $ 4.33 | ||||

| ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund(c) | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 974.00 | 1.45% | $ 7.21 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.90 | 1.45% | $ 7.38 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 970.90 | 2.05% | $ 10.18 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,014.87 | 2.05% | $ 10.41 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 974.90 | 1.15% | $ 5.72 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

| ALPS | Kotak India Growth Fund(d) | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 932.40 | 2.00% | $ 9.74 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.12 | 2.00% | $ 10.16 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 929.30 | 2.60% | $ 12.64 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,012.10 | 2.60% | $ 13.19 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 933.00 | 1.60% | $ 7.80 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.14 | 1.60% | $ 8.13 | ||||

| ALPS | Red Rocks Listed Private Equity Fund | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 1,137.20 | 1.65% | $ 8.89 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,016.89 | 1.65% | $ 8.39 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 1,133.40 | 2.25% | $ 12.10 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,013.86 | 2.25% | $ 11.42 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 1,139.80 | 1.25% | $ 6.74 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 | ||||

| Class R | ||||||||

Actual | $ 1,000.00 | $ 1,136.80 | 1.75% | $ 9.43 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,016.38 | 1.75% | $ 8.89 | ||||

| 2 | October 31, 2013 |

Disclosure of Fund Expenses | ||

| October 31, 2013 (Unaudited) | ||

| Beginning Account Value May 1, 2013 | Ending Account Value October 31, 2013 | Expense Ratio(a) | Expense Paid During Period May 1, 2013 - October 31, 2013(b) | |||||

ALPS | WMC Disciplined Value Fund | ||||||||

Class A | ||||||||

Actual | $ 1,000.00 | $ 1,114.90 | 1.40% | $ 7.46 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.15 | 1.40% | $ 7.12 | ||||

Class C | ||||||||

Actual | $ 1,000.00 | $ 1,111.80 | 2.15% | $ 11.44 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,014.37 | 2.15% | $ 10.92 | ||||

Class I | ||||||||

Actual | $ 1,000.00 | $ 1,116.80 | 1.15% | $ 6.14 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

| Clough China Fund | ||||||||

Class A | ||||||||

Actual | $ 1,000.00 | $ 1,043.80 | 1.95% | $ 10.05 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.38 | 1.95% | $ 9.91 | ||||

Class C | ||||||||

Actual | $ 1,000.00 | $ 1,040.10 | 2.70% | $ 13.88 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,011.59 | 2.70% | $ 13.69 | ||||

Class I | ||||||||

Actual | $ 1,000.00 | $ 1,045.80 | 1.70% | $ 8.77 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,016.64 | 1.70% | $ 8.64 | ||||

| RiverFront Conservative Income Builder Fund | ||||||||

Class A | ||||||||

Actual | $ 1,000.00 | $ 1,031.60 | 1.15% | $ 5.89 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

Class C | ||||||||

Actual | $ 1,000.00 | $ 1,027.00 | 1.90% | $ 9.71 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 | ||||

Class I | ||||||||

Actual | $ 1,000.00 | $ 1,031.90 | 0.90% | $ 4.61 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| RiverFront Dynamic Equity Income Fund | ||||||||

Class A | ||||||||

Actual | $ 1,000.00 | $ 1,063.30 | 1.15% | $ 5.98 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

Class C | ||||||||

Actual | $ 1,000.00 | $ 1,060.50 | 1.90% | $ 9.87 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 | ||||

Class I | ||||||||

Actual | $ 1,000.00 | $ 1,066.00 | 0.90% | $ 4.69 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| RiverFront Global Allocation Fund | ||||||||

Class A | ||||||||

Actual | $ 1,000.00 | $ 1,081.30 | 1.15% | $ 6.03 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

Class C | ||||||||

Actual | $ 1,000.00 | $ 1,077.70 | 1.90% | $ 9.95 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 | ||||

Class I | ||||||||

Actual | $ 1,000.00 | $ 1,082.80 | 0.90% | $ 4.72 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| 3 | October 31, 2013 |

Disclosure of Fund Expenses | ||

| October 31, 2013 (Unaudited) | ||

Beginning Account Value May 1, 2013 | Ending Account Value October 31, 2013 | Expense Ratio(a) | Expense Paid During Period May 1, 2013 - October 31, 2013(b) | |||||

| RiverFront Global Growth Fund | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 1,091.30 | 1.15% | $ 6.06 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 1,088.10 | 1.90% | $ 10.00 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 1,093.20 | 0.90% | $ 4.75 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| Class L | ||||||||

Actual | $ 1,000.00 | $ 1,093.30 | 0.90% | $ 4.75 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| Investor Class | ||||||||

Actual | $ 1,000.00 | $ 1,091.80 | 1.15% | $ 6.06 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

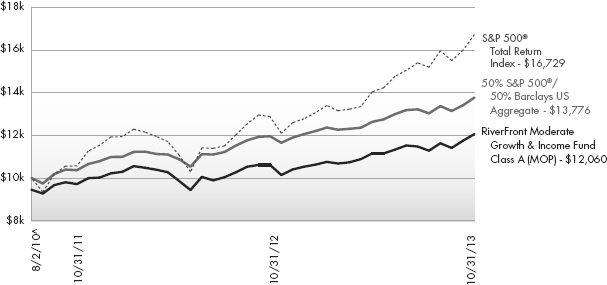

| RiverFront Moderate Growth & Income Fund | ||||||||

| Class A | ||||||||

Actual | $ 1,000.00 | $ 1,046.20 | 1.15% | $ 5.93 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 | ||||

| Class C | ||||||||

Actual | $ 1,000.00 | $ 1,042.30 | 1.90% | $ 9.78 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 | ||||

| Class I | ||||||||

Actual | $ 1,000.00 | $ 1,047.20 | 0.90% | $ 4.64 | ||||

Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 | ||||

| (a) | Annualized, based on the Fund’s most recent fiscal half year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), divided by 365. |

| (c) | Includes expenses of the CoreCommodity Management Cayman Commodity Fund Ltd. (wholly-owned subsidiary), exclusive of the subsidiary’s management fee. |

| (d) | Includes expenses of the Kotak Mauritius Portfolio (wholly-owned subsidiary), exclusive of subsidiary’s management fee. |

| 4 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund

| ||

| October 31, 2013 (Unaudited) | ||

Performance

During the six month period of May 1, 2013 to October 31, 2013, the Alerian MLP Infrastructure Index Fund’s Class A Shares delivered a net return of 3.24% at Net Asset Value (Class A delivered a net return of -2.47% at MOP1 , Class C was 1.97% with CDSC, and Class I was 3.33%).

Performance of the Fund’s MLP holdings during this period was impacted both by the Federal Reserve’s May announcement to taper its bond buying program as well as uncertainty in the months following as to when tapering would actually begin. Expectations for rising rates disproportionately impacted income-oriented equities such as MLPs, REITs and utilities during this period. However, the distribution growth element of the Fund’s MLP holdings as well as investors becoming more comfortable with valuations mitigated most of the impact. To that point, the Fund’s two distributions during this period—payable May 14, 2013 and August 14, 2013—represented a 1.4% and 1.8% increase from the previous quarter.

In 2013, MLPs announced and put into service several infrastructure assets addressing takeaway needs from various areas experiencing dramatic production growth. In the Marcellus Shale in the Northeast, natural gas pipelines were expanded, connecting lines were built to larger trunklines, and a handful of pipelines transporting natural gas liquids are either under construction or being proposed. In the Bakken Shale in North Dakota, MLPs are at the forefront of the crude-by-rail trend, constructing loading and unloading terminals along major rail lines. Moving crude via rail has allowed producers the flexibility to ship Bakken crude to favorably priced markets across the US including California, the Midwest, and the Gulf Coast.

Further down south in Mont Belvieu, Texas, many MLPs continue to build out fractionation plants and expand pipelines that carry natural gas liquids to petrochemical plants along the Gulf Coast. In addition, MLPs have emerged as the leading operators of liquefied petroleum gas (LPG) export facilities along the Gulf Coast. The oversupply of natural gas liquids domestically plus an increased demand for propane and butane in emerging countries overseas has created favorable opportunities for MLPs to expand and built out additional export docks and ancillary facilities.

We believe an energy revolution is taking place in the United States through directional drilling and hydraulic fracturing, and recoverable oil and gas reserves are at levels not seen in decades. Industry executives and analysts estimate that the US will be net energy independent sometime in the next 10 years. The MLP-owned energy infrastructure assets, including pipelines, storage tanks, and processing plants, are the means by which the reserves and production in supply basins make their way to demand centers.

With toll-road business models anchored by inflation-indexed tariff increases and billions of dollars of infrastructure opportunities over the next few decades, MLPs continue, in our view, to represent a compelling investment opportunity for investors seeking after-tax yield.

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Alerian does not accept any liability for losses either direct or consequential caused by the use of this information.

| 1 | Maximum Offering Price (MOP) includes sales charge. |

| 5 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund

| ||

| October 31, 2013 (Unaudited) | ||

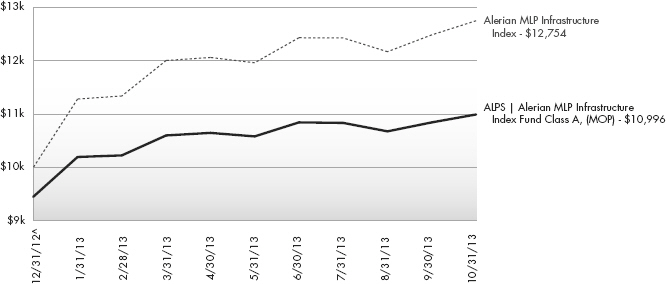

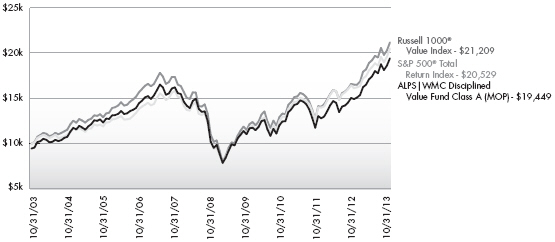

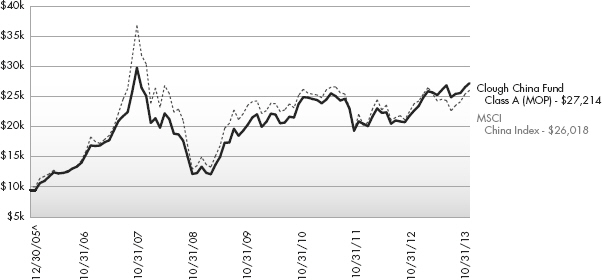

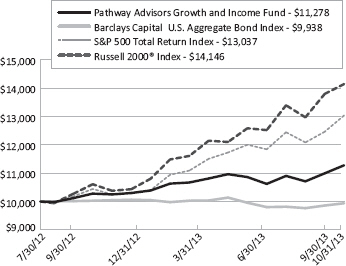

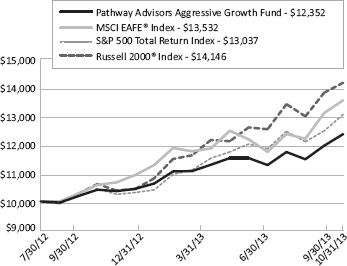

Performance of $10,000 Initial Investment (as of October 31, 2013)

Comparison of change in value of a $10,000 investment (includes maximum sales charges of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Average Annual Total Returns (as of October 31, 2013)

| Since Inception ^ | Total Expense Ratio * | What You Pay ** | ||||

Class A (NAV)1 | 16.33% | 1.49% | 1.25% | |||

Class A (MOP)2 | 9.96% | |||||

Class C (NAV)1 | 15.92% | 2.09% | 1.85% | |||

Class C (CDSC)2 | 14.92% | |||||

Class I | 16.54% | 1.09% | 0.85% | |||

Alerian MLP Infrastructure Index3 | 27.54% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 18 months after a purchase in excess of $1 million. Performance shown does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data please call 1-866-759-5679.

Investments in securities of MLPs involve risks that differ from an investment in common stock. MLPs are controlled by their general partners, which generally have conflicts of interest and limited fiduciary duties to the MLP, which may permit the general partner to favor its own interests over the MLPs. The benefit you are expected to derive from the Fund’s investment in MLPs depends largely on the MLPs being treated as partnerships for federal income tax purposes. As a partnership, an MLP has no federal income tax liability at the entity level. Therefore, treatment of one or more MLPs as a corporation for federal income tax purposes could affect the Fund’s ability to meet its investment objective and would reduce the amount of cash available to pay or distribute to you. Legislative, judicial, or administrative changes and differing interpretations, possibly on a retroactive basis, could negatively impact the value of an investment in MLPs and therefore the value of your investment in the Fund.

| 6 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund

| ||

Performance Update | October 31, 2013 (Unaudited) | |

| 1 | Net Asset Value (NAV) is the share price without sales charges. |

| 2 | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%; Class C returns include the 1.00% CDSC. |

| 3 | Alerian MLP Infrastructure Index is comprised of 25 midstream energy Master Limited Partnerships. The index is not actively managed and does not reflect any deductions for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of December 31, 2012. The Fund commenced operations on January 2, 2013. |

| * | Excludes current and deferred income tax expense. |

| ** | What You Pay reflects the Advisor’s and Sub-Advisor’s decision to contractually limit expenses through August 31, 2014. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

This Fund is not suitable for all investors and is subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Mutual funds are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

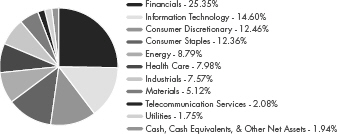

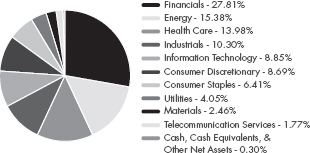

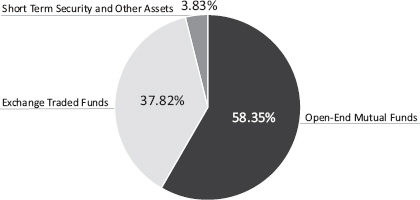

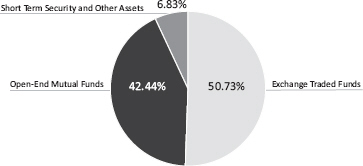

Top Ten Long Holdings (as a % of Net Assets) †

|

| Industry Sector Allocation (as a % of Net Assets)

| ||||||

Enterprise Products Partners LP | 9.98 | % |

| |||||

Kinder Morgan Energy Partners LP | 9.31 | % | ||||||

Magellan Midstream Partners LP | 7.70 | % | ||||||

MarkWest Energy Partners LP | 7.24 | % | ||||||

Energy Transfer Partners LP | 7.11 | % | ||||||

Plains All American Pipeline LP | 6.92 | % | ||||||

ONEOK Partners LP | 4.87 | % | ||||||

Williams Partners LP | 4.82 | % | ||||||

Buckeye Partners LP | 4.60 | % | ||||||

Enbridge Energy Partners LP | 4.33 | % | ||||||

Top Ten Holdings | 66.88 | % | ||||||

† Holdings are subject to change. Table presents indicative values only. |

| |||||||

| 7 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund

| ||

| October 31, 2013 (Unaudited) | ||

| Shares | Value (Note 2) | |||||||

| ||||||||

MASTER LIMITED PARTNERSHIPS (102.19%) |

| |||||||

Gathering & Processing (27.86%) |

| |||||||

Pipelines (27.86%) | ||||||||

Access Midstream Partners LP | 6,328 | $ | 338,801 | |||||

Atlas Pipeline Partners LP | 5,575 | 214,972 | ||||||

DCP Midstream Partners LP | 5,283 | 256,648 | ||||||

MarkWest Energy Partners LP | 10,933 | 812,103 | ||||||

Regency Energy Partners LP | 11,794 | 300,629 | ||||||

Targa Resources Partners LP | 7,160 | 373,108 | ||||||

Western Gas Partners LP | 4,750 | 285,522 | ||||||

Williams Partners LP | 10,518 | 540,836 | ||||||

|

| |||||||

| 3,122,619 | ||||||||

|

| |||||||

TOTAL GATHERING & PROCESSING |

| 3,122,619 | ||||||

|

| |||||||

Natural Gas Pipelines (32.65%) | ||||||||

Pipelines (32.65%) | ||||||||

Boardwalk Pipeline Partners LP | 9,069 | 271,616 | ||||||

El Paso Pipeline Partners LP | 9,826 | 398,543 | ||||||

Energy Transfer Partners LP | 15,041 | 796,722 | ||||||

Enterprise Products Partners LP | 17,684 | 1,119,043 | ||||||

ONEOK Partners LP | 10,153 | 545,927 | ||||||

PVR Partners LP | 7,459 | 195,351 | ||||||

Spectra Energy Partners LP | 3,547 | 155,075 | ||||||

TC Pipelines LP | 3,491 | 178,076 | ||||||

|

| |||||||

| 3,660,353 | ||||||||

|

| |||||||

TOTAL NATURAL GAS PIPELINES |

| 3,660,353 | ||||||

|

| |||||||

Petroleum Transportation (41.68%) |

| |||||||

Pipelines (41.68%) | ||||||||

Buckeye Partners LP | 7,666 | 515,692 | ||||||

Enbridge Energy Partners LP | 16,029 | 485,198 | ||||||

Genesis Energy LP | 5,340 | 272,126 | ||||||

Kinder Morgan Energy Partners LP | 12,934 | 1,043,774 | ||||||

Magellan Midstream Partners LP | 14,373 | 862,955 | ||||||

NuStar Energy LP | 5,029 | 216,850 | ||||||

Plains All American Pipeline LP | 15,136 | 775,266 | ||||||

Sunoco Logistics Partners LP | 5,415 | 380,025 | ||||||

Tesoro Logistics LP | 2,235 | 120,020 | ||||||

|

| |||||||

| 4,671,906 | ||||||||

|

| |||||||

TOTAL PETROLEUM TRANSPORTATION |

| 4,671,906 | ||||||

|

| |||||||

TOTAL MASTER LIMITED PARTNERSHIPS (Cost $10,340,554) |

| 11,454,878 | ||||||

|

| |||||||

| 7-Day Yield | Shares | Value (Note 2) | ||||||||||

| ||||||||||||

SHORT TERM INVESTMENTS (4.07%) |

| |||||||||||

Money Market Fund (4.07%) |

| |||||||||||

Dreyfus Treasury Prime Cash Management Fund, Institutional Shares | 0.00004 | % | 456,597 | $ | 456,597 | |||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $ 456,597) |

| 456,597 | ||||||||||

|

| |||||||||||

TOTAL INVESTMENTS (106.26%) (Cost $ 10,797,151) |

| $ | 11,911,475 | |||||||||

Liabilities In Excess Of Other Assets (-6.26%) |

| (702,083) | ||||||||||

|

| |||||||||||

NET ASSETS (100.00%) |

| $ | 11,209,392 | |||||||||

|

| |||||||||||

Common Abbreviations:

LP - Limited Partnerships.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets.

See Notes to Financial Statements.

| 8 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund | ||

| October 31, 2013 (Unaudited) | ||

ASSETS | ||||

Investments, at value | $ | 11,911,475 | ||

Dividends receivable | 82,133 | |||

Receivable due from advisor | 15,803 | |||

Prepaid offering costs | 11,397 | |||

Prepaid expenses and other assets | 32,004 | |||

| ||||

Total Assets | 12,052,812 | |||

| ||||

LIABILITIES | ||||

Payable for investments purchased | 445,941 | |||

Deferred tax liability | 373,238 | |||

Current tax payable | 10,182 | |||

Administration and transfer agency fees payable | 1,206 | |||

Distribution and services fees payable | 4,250 | |||

Trustees’ fees and expenses payable | 85 | |||

Legal fees payable | 63 | |||

Audit and tax fees payable | 954 | |||

Accrued expenses and other liabilities | 7,501 | |||

| ||||

Total Liabilities | 843,420 | |||

| ||||

NET ASSETS | $ | 11,209,392 | ||

| ||||

NET ASSETS CONSIST OF | ||||

Paid-in capital | $ | 10,558,970 | ||

Accumulated net investment loss, net of deferred income taxes | (31,390) | |||

Accumulated net realized loss on investments, net of deferred income taxes | (26,713) | |||

Net unrealized appreciation on investments, net of deferred income taxes | 708,525 | |||

| ||||

NET ASSETS | $ | 11,209,392 | ||

| ||||

INVESTMENTS, AT COST | $ | 10,797,151 | ||

| ||||

PRICING OF SHARES | ||||

Class A: | ||||

Net Asset Value, offering and redemption price per share(a) | $ | 11.12 | ||

Net Assets | $ | 6,994,470 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 629,049 | |||

Maximum offering price per share ((NAV/0.9450), based on maximum sales charge of 5.50% of the offering price) | $ | 11.77 | ||

Class C: | ||||

Net Asset Value, offering and redemption price per share(a) | $ | 11.08 | ||

Net Assets | $ | 1,650,844 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 149,001 | |||

Class I: | ||||

Net Asset Value, offering and redemption price per share | $ | 11.14 | ||

Net Assets | $ | 2,564,078 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 230,206 | |||

| (a) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. For a description of a possible sales charge, please see the Fund’s Prospectus. |

See Notes to Financial Statements. |

| 9 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund | ||

| For the Six Months Ended October 31, 2013 (Unaudited) | ||

INVESTMENT INCOME | ||||

Distributions from master limited partnerships | 181,312 | |||

Less return of capital distributions | (181,312) | |||

| ||||

Total Investment Income | – | |||

| ||||

EXPENSES | ||||

Investment advisory fees | 22,245 | |||

Administrative and transfer agency fees | 4,129 | |||

Distribution and service fees | ||||

Class A | 6,417 | |||

Class C | 3,950 | |||

Legal fees | 16 | |||

Audit and tax fees | 23,462 | |||

Reports to shareholders and printing fees | 706 | |||

State registration fees | 4,294 | |||

SEC registration fees | 690 | |||

Custody fees | 6,270 | |||

Trustees’ fees and expenses | 122 | |||

Offering costs | 34,620 | |||

Miscellaneous expenses | 4,612 | |||

| ||||

Total Expenses | 111,533 | |||

Less fees waived/reimbursed by investment advisor (Note 7) | ||||

Class A | (34,955) | |||

Class C | (9,835) | |||

Class I | (29,365) | |||

| ||||

Net Expenses | 37,378 | |||

| ||||

Net Investment Loss, Before Deferred Income Taxes | (37,378) | |||

Deferred income tax benefit | 13,614 | |||

| ||||

Net Investment Loss, Net of Deferred Income Taxes | (23,764) | |||

| ||||

REALIZED AND UNREALIZED GAIN/(LOSS) | ||||

Net realized loss on investments, before deferred income taxes | (10,884) | |||

Current income tax expense | (10,182) | |||

Deferred income tax benefit | 14,146 | |||

| ||||

Net Realized Loss on investments, Net of Deferred Income Taxes | (6,920) | |||

| ||||

Net change in unrealized appreciation on investment, before deferred income taxes | 480,401 | |||

Deferred income tax expense | (175,051) | |||

| ||||

Net Change in Unrealized Appreciation on Investments | 305,350 | |||

| ||||

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS, NET OF DEFERRED INCOME TAXES | 298,430 | |||

| ||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 274,666 | ||

| ||||

See Notes to Financial Statements. |

| 10 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund | ||

| For the Six MonthsEnded October 31, 2013 (Unaudited) | For the Period January 2, 2013 (Commencement) to April 30, 2013 | |||||||

| ||||||||

OPERATIONS | ||||||||

Net investment loss, net of deferred income taxes | (23,764) | (7,626) | ||||||

Net realized loss on investments, net of deferred income taxes | (6,920) | (764) | ||||||

Net change in unrealized appreciation on investments, net of deferred income taxes | 305,350 | 403,175 | ||||||

| ||||||||

Net Increase in Net Assets Resulting from Operations | 274,666 | 394,785 | ||||||

| ||||||||

DISTRIBUTIONS | ||||||||

Dividends to shareholders from net realized gains | ||||||||

Class A | (5,165) | – | ||||||

Class C | (2,812) | – | ||||||

Class I | (11,052) | – | ||||||

Dividends to shareholders from tax return of capital | ||||||||

Class A | (26,670) | (8,653) | ||||||

Class C | (14,520) | (8,137) | ||||||

Class I | (57,063) | (32,548) | ||||||

| ||||||||

Net Decrease in Net Assets from Distributions | (117,282) | (49,338) | ||||||

| ||||||||

BENEFICIAL INTEREST TRANSACTIONS (NOTE 6) | ||||||||

Shares sold | ||||||||

Class A | 6,409,506 | 851,295 | ||||||

Class C | 1,050,687 | 500,010 | ||||||

Class I | 230,232 | 2,000,010 | ||||||

Dividends reinvested | ||||||||

Class A | 27,042 | 8,653 | ||||||

Class C | 17,181 | 8,137 | ||||||

Class I | 68,115 | 32,548 | ||||||

Shares redeemed | ||||||||

Class A | (496,825) | (10) | ||||||

Class C | – | (10) | ||||||

Class I | – | (10) | ||||||

| ||||||||

Net Increase in Net Assets Derived from Beneficial Interest Transactions | 7,305,938 | 3,400,623 | ||||||

| ||||||||

Net increase in net assets | 7,463,322 | 3,746,070 | ||||||

NET ASSETS | ||||||||

Beginning of period | 3,746,070 | – | ||||||

| ||||||||

End of period * | $ | 11,209,392 | $ | 3,746,070 | ||||

| ||||||||

*Including accumulated net investment loss, net of Deferred Income Taxes, of: | $ | (31,390) | $ | (7,626) | ||||

See Notes to Financial Statements. |

| 11 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund – Class A | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

For the Six Months Ended October 31, 2013 | For the Period January 2, 2013 April 30, 2013 | |||

| ||||

Net asset value, beginning of period | $11.10 | $10.00 | ||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||

Net investment loss(a) | (0.05) | (0.03) | ||

Net realized and unrealized gain | 0.40 | 1.29 | ||

| ||||

Total from investment operations | 0.35 | 1.26 | ||

| ||||

DISTRIBUTIONS: | ||||

From net realized gains | (0.05) | – | ||

From tax return of capital | (0.28) | (0.16) | ||

| ||||

Total distributions | (0.33) | (0.16) | ||

| ||||

Net increase in net asset value | 0.02 | 1.10 | ||

| ||||

Net asset value, end of period | $11.12 | $11.10 | ||

| ||||

TOTAL RETURN(b) | 3.24% | 12.68% | ||

RATIOS/SUPPLEMENTAL DATA: | ||||

Net assets, end of period (000s) | $6,994 | $928 | ||

Ratio of expenses to average net assets before waivers and income tax expense | 3.43%(c)(d) | 5.51%(c)(d) | ||

Ratio of expense waivers to average net assets | (2.18%)(c)(d) | (4.26%)(c)(d) | ||

| ||||

Ratio of expenses to average net assets net of waivers and before income tax expense | 1.25%(c)(d) | 1.25%(c)(d) | ||

Ratio of deferred income tax expense to average net assets(e) | 4.96%(c) | 20.55%(c) | ||

| ||||

Ratio of total expenses to average net assets | 6.21%(c) | 21.80%(c) | ||

| ||||

Ratio of investment loss to average net assets before waivers and income tax expense | (3.43%)(c)(d) | (5.51%)(c)(d) | ||

Ratio of expense waivers to average net assets | (2.18%)(c)(d) | (4.26%)(c)(d) | ||

| ||||

Ratio of investment loss to average net assets net of waivers and before income tax expense | (1.25%)(c)(d) | (1.25%)(c)(d) | ||

Ratio of deferred income tax benefit to average net assets(f) | 0.42%(c) | 0.40%(c) | ||

| ||||

Ratio of net investment loss to average net assets | (0.83%)(c) | (0.85%)(c) | ||

| ||||

Portfolio turnover rate(g) | 7% | 3% | ||

| (a) | Calculated using the average shares method. |

| (b) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (c) | Annualized. |

| (d) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (e) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

| (f) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

| (g) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements. |

| 12 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund – Class C | ||

Financial Highlights | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

For the Six Months Ended | For the Period January 2, 2013 (Commencement) to April 30, 2013 | |||

| ||||

Net asset value, beginning of period | $11.09 | $10.00 | ||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||

Net investment loss(a) | (0.08) | (0.05) | ||

Net realized and unrealized gain | 0.40 | 1.30 | ||

| ||||

Total from investment operations | 0.32 | 1.25 | ||

| ||||

DISTRIBUTIONS: | ||||

From net realized gains | (0.05) | – | ||

From tax return of capital | (0.28) | (0.16) | ||

| ||||

Total distributions | (0.33) | (0.16) | ||

| ||||

Net increase/(decrease) in net asset value | (0.01) | 1.09 | ||

| ||||

Net asset value, end of period | $11.08 | $11.09 | ||

| ||||

TOTAL RETURN(b) | 2.97% | 12.58% | ||

RATIOS/SUPPLEMENTAL DATA: | ||||

Net assets, end of period (000s) | $1,651 | $563 | ||

Ratio of expenses to average net assets before waivers and income tax expense | 4.34%(c)(d) | 7.01%(c)(d) | ||

Ratio of expense waivers to average net assets | (2.49%)(c)(d) | (5.16%)(c)(d) | ||

| ||||

Ratio of expenses to average net assets net of waivers and before income tax expense | 1.85%(c)(d) | 1.85%(c)(d) | ||

Ratio of deferred income tax expense to average net assets(e) | 4.96%(c) | 20.55%(c) | ||

| ||||

Ratio of total expenses to average net assets | 6.81%(c) | 22.40%(c) | ||

| ||||

Ratio of investment loss to average net assets before waivers and income tax expense | (4.34%)(c)(d) | (7.01%)(c)(d) | ||

Ratio of expense waivers to average net assets | (2.49%)(c)(d) | (5.16%)(c)(d) | ||

| ||||

Ratio of investment loss to average net assets net of waivers and before income tax expense | (1.85%)(c)(d) | (1.85%)(c)(d) | ||

Ratio of deferred income tax benefit to average net assets(f) | 0.42%(c) | 0.40%(c) | ||

| ||||

Ratio of net investment loss to average net assets | (1.43%)(c) | (1.45%)(c) | ||

| ||||

Portfolio turnover rate(g) | 7% | 3% | ||

| (a) | Calculated using the average shares method. |

| (b) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (c) | Annualized. |

| (d) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (e) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

| (f) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

| (g) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements. |

| 13 | October 31, 2013 |

ALPS | Alerian MLP Infrastructure Index Fund – Class I | ||

Financial Highlights | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| For the Six Months Ended October 31, 2013 (Unaudited) | For the Period January 2, 2013 (Commencement) to April 30, 2013 | |||

| ||||

Net asset value, beginning of period | $11.11 | $10.00 | ||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||

Net investment loss(a) | (0.02) | (0.02) | ||

Net realized and unrealized gain | 0.38 | 1.29 | ||

| ||||

Total from investment operations | 0.36 | 1.27 | ||

| ||||

DISTRIBUTIONS: | ||||

From net realized gains | (0.05) | – | ||

From tax return of capital | (0.28) | (0.16) | ||

| ||||

Total distributions | (0.33) | (0.16) | ||

| ||||

Net increase in net asset value | 0.03 | 1.11 | ||

| ||||

Net asset value, end of period | $11.14 | $11.11 | ||

| ||||

TOTAL RETURN(b) | 3.33% | 12.78% | ||

RATIOS/SUPPLEMENTAL DATA: | ||||

Net assets, end of period (000s) | $2,564 | $2,256 | ||

Ratio of expenses to average net assets before waivers and income tax expense | 3.34%(c)(d) | 6.01%(c)(d) | ||

Ratio of expense waivers to average net assets | (2.49%)(c)(d) | (5.16%)(c)(d) | ||

| ||||

Ratio of expenses to average net assets net of waivers and before income tax expense | 0.85%(c)(d) | 0.85%(c)(d) | ||

Ratio of deferred income tax expense to average net assets(e) | 4.96%(c) | 20.55%(c) | ||

| ||||

Ratio of total expenses to average net assets | 5.81%(c) | 21.40%(c) | ||

| ||||

Ratio of investment loss to average net assets before waivers and income tax expense | (3.34%)(c)(d) | (6.01%)(c)(d) | ||

Ratio of expense waivers to average net assets | (2.49%)(c)(d) | (5.16%)(c)(d) | ||

| ||||

Ratio of investment loss to average net assets net of waivers and before income tax expense | (0.85%)(c)(d) | (0.85%)(c)(d) | ||

Ratio of deferred income tax benefit to average net assets(f) | 0.42%(c) | 0.40%(c) | ||

| ||||

Ratio of net investment loss to average net assets | (0.43%)(c) | (0.45%)(c) | ||

| ||||

Portfolio turnover rate(g) | 7% | 3% | ||

| (a) | Calculated using the average shares method. |

| (b) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (c) | Annualized. |

| (d) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (e) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

| (f) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

| (g) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements. |

| 14 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

| October 31, 2013 (Unaudited) | ||

The six month period ending on October 31, 2013 produced mixed returns for commodities. Commodity futures prices, as measured by the Thomson Reuters/CoreCommodity CRB Total Return Index, were down 3.54%. On the other hand, commodity equities appreciated during the quarter, up 3.27% as measured by the Standard and Poor’s Global Natural Resources Net Total Return Index. Commodity equities may have benefitted from the performance of the broader Standard & Poor’s 500 Total Return Index for the period which posted +11.14% gains. The ALPS CoreCommodity Strategy Allocation Fund (JCRIX) delivered a net negative return of -2.51% (JCRAX was -2.60% and JCRCX was down 2.91%).

The Fund outperformed its benchmark, the Thomson Reuters/CoreCommodity CRB Index, by approximately 103 basis points1 during this period (measured against the performance of the “I” shares). The Fund employs a strategy that combines an actively managed portfolio of commodity futures related exposure (collateralized by Treasury Inflation Protected Securities – TIPS), commodity equities, and physical commodity ETFs. Throughout most of the quarter, the Fund allocated approximately 65% of its assets toward commodity futures related investments and approximately 35% of its assets in commodity equities. The Fund was almost 98% invested by the end of October.

Commodity prices were generally under pressure during the six month period ending in October 2013. With certain exceptions, commodity prices declined at the hint of tapering of quantitative easing (QE- US Treasury bonds and mortgage backed securities purchased by the Federal Reserve with newly created currency). Many market participants equated the possibility of a reduction in the stimulus provided by QE as de facto tightening, despite the Fed’s insistence that it would maintain extremely low short term rates for an extended period of time. The Federal Reserve’s attitude toward the possibility of tapering was predicated on improving economic metrics including higher employment, increasing economic activity, and higher levels of inflation. While some of the numbers improved modestly, inflation remained stubbornly low, according to the Fed’s objectives.

Lean hogs were the best performing commodity within the Thomson Reuters/CoreCommodity CRB Index from the end of April 2013 to the end of October 2013, up 13.02%. Lingering effects of last summer’s extreme drought and heat in the mid-west contributed to smaller numbers or hogs and cattle. Live cattle prices added 4.35% in the time frame. Cocoa prices (up 12.80% for the 6 month period) were supported by dry conditions and political tension in key growing regions in Africa. Crude oil prices rose for both domestic and international markers. Modestly higher economic growth and ongoing problems in Libya, Syria, and Iran combined to gently push demand while international crude supply was constrained. West Texas Intermediate (WTI) crude rose 5.46% and Brent North Sea crude added 8.45%. The Fund has exposure to both crude oil contracts.

Coffee prices declined by the greatest percentage during the six-month period ending in October 2013, down 24.77%. Ideal weather and high yields have depressed prices for Arabica coffee globally.

Arabica beans are preferred by most premium coffee drinkers. Natural gas prices were challenged with increasing US supplies and a very quiet hurricane season in the Gulf region. Natural gas prices fell 22.56% from April through October. Corn and wheat prices retreated by 22.53% and 11.38% respectively. Farmers planted additional quantities of both grains as a response to the high prices from last year. Favorable conditions prevailed for growing and harvesting seasons. The Environmental Protection Agency (EPA) relaxed the scheduled mandate to increase ethanol to 15% from the current 10% level in reformulated gasoline. The move withdrew a certain amount of anticipated demand for corn in particular. Ethanol production diverts about 40% of the entire US corn crop from human and animal consumption. Precious metal prices continued under pressure. Gold prices went down 10.34% while silver fell 9.99%.

The Fund’s top equity holdings at the end of October 2013 included Monsanto (MON) +11.28% YTD, Exxon/Mobil (XOM) +3.28% YTD, Syngenta AG (SYNN) +2.64% YTD, Chevron Corporation (CVX) +11.80% YTD , Deere & Company (DE) -5.05% YTD, Potash (POT) -21.57% YTD, Archer Daniels Midland +46.21% YTD, British Petroleum (BP US) +11.62% YTD, CF Industries Holdings (CF) +5.16% YTD , Royal Dutch Shell (RDS/A) +.58% YTD.

TIPS are held by the Fund to invest excess cash and as collateral for commodity futures related investments held in our Cayman Island subsidiary. Nominal yields on the benchmark 10 year note began the quarter at 1.926% and ended the six month period significantly higher, 2.55%. At one point in early September, ten year note yields briefly exceeded 3%. Despite the efforts by the Federal Reserve and other central banks to maintain historically low interest rates, we believe we may be nearing the end of what has been a significant multi-year rally in US treasury prices. As a result, we continue to invest in TIPS with limited duration exposure. At the end of October, our weighted average maturity was approximately 1.75 years in our TIPS portfolio.

We strongly believe that the long term fundamental drivers of commodity demand and ultimately higher prices are still in place. Population growth is likely to remain unabated regardless of the economic environment in the US and Europe. A billion more people will be added to the world population over the next decade. The trend of wealth distribution to the developing world as those economies grow at rapid rates relative to the slow or negative growth occurring in the developed countries is contributing to ever increasing demand for raw materials and food. Incremental gains in disposable income in the developing nations have led to competition for the commodities needed for more complex and costly lifestyles. In a world with limited supplies of food, fuel, building materials, and other necessities of life, price may become the ultimate allocator. Additionally, the aggressively accommodative central bank monetary policies recently announced coupled with measures already in place globally are likely to make commodities and other real assets more attractive over time as currencies, including the US Dollar, may decline in value.

| 15 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Management Commentary | October 31, 2013 (Unaudited) | |

| 1 | Basis Points or bps is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. |

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. CoreCommodity Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

| 16 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

| October 31, 2013 (Unaudited) | ||

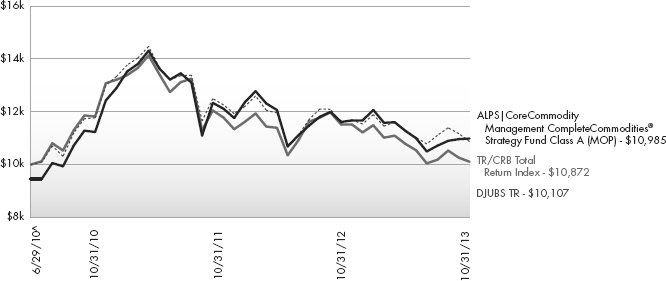

Performance of $10,000 Initial Investment (as of October 31, 2013)

Comparison of change in value of a $10,000 investment (includes maximum sales charges of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Average Annual Total Returns (as of October 31, 2013)

| 1 Year | 3 Years | Since Inception ^ | Total Expense Ratio | What You Pay * | ||||||

Class A (NAV)1 | -5.42% | -0.89% | 4.61% | 1.55% | 1.46% | |||||

Class A (MOP)2 | -10.66% | -2.72% | 2.85% | |||||||

Class C (NAV)1 | -6.02% | -1.54% | 4.02% | 2.15% | 2.06% | |||||

Class C (CDSC)2 | -6.95% | -1.54% | 4.02% | |||||||

Class I | -5.17% | -0.65% | 4.91% | 1.17% | 1.16% | |||||

TR/CRB Total Return Index3 | -6.02% | -2.52% | 2.53% | |||||||

DJUBS Commodity TR3 | -12.22% | -5.19% | 0.32% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 18 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call 1-866-759-5679.

| 17 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Performance Update | October 31, 2013 (Unaudited) | |

| 1 | Net Asset Value (NAV) is the share price without sales charges. |

| 2 | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%; Class C returns include the 1.00% CDSC. |

| 3 | Thomson Reuters / CRB Index and the Dow Jones-UBS Commodity Index are unmanaged indices used as a measurement of change in commodity market conditions based on the performance of a basket of different commodities. The indices are not actively managed and do not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of June 29, 2010. |

| * | What You Pay reflects the Sub-Advisor’s decision to contractually limit expenses through August 31, 2014. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Mutual funds are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

This Fund is not suitable for all investors, and is subject to investment risks, including possible loss of the principal amount invested.

Investing in commodity-related securities involves risk and considerations not present when investing in more conventional securities. The Fund may be more susceptible to high volatility of commodity markets.

Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund’s original investment.

| 18 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

| October 31, 2013 (Unaudited) | ||

| Shares | Value (Note 2) | |||||||

| ||||||||

COMMON STOCKS (38.22%) |

| |||||||

Australia (0.46%) | ||||||||

Fortescue Metals Group, Ltd. | 31,313 | $ | 154,193 | |||||

Iluka Resources, Ltd. | 7,779 | 75,729 | ||||||

Incitec Pivot, Ltd. | 265,758 | 668,144 | ||||||

Newcrest Mining, Ltd. | 11,624 | 113,161 | ||||||

Regis Resources, Ltd. | 104,820 | 345,757 | ||||||

Woodside Petroleum, Ltd. | 9,366 | 343,646 | ||||||

|

| |||||||

| 1,700,630 | ||||||||

|

| |||||||

Brazil (0.38%) | ||||||||

Cia Siderurgica Nacional SA, ADR | 1,580 | 8,753 | ||||||

Gerdau SA, ADR | 10,527 | 83,479 | ||||||

Petroleo Brasileiro SA, ADR | 25,208 | 439,375 | ||||||

Vale SA, ADR | 52,655 | 843,007 | ||||||

|

| |||||||

| 1,374,614 | ||||||||

|

| |||||||

Canada (4.83%) | ||||||||

Agnico-Eagle Mines, Ltd. | 9,541 | 281,746 | ||||||

Agrium, Inc. | 24,201 | 2,064,829 | ||||||

AuRico Gold, Inc. | 120,230 | 494,145 | ||||||

Barrick Gold Corp. | 38,755 | 751,459 | ||||||

Cameco Corp. | 5,892 | 111,948 | ||||||

Canadian Natural Resources, Ltd. | 5,741 | 182,277 | ||||||

Eldorado Gold Corp. | 28,088 | 189,594 | ||||||

Encana Corp. | 19,565 | 350,605 | ||||||

First Quantum Minerals, Ltd. | 16,847 | 319,603 | ||||||

Goldcorp, Inc. | 24,289 | 617,669 | ||||||

IAMGOLD Corp. | 228,430 | 1,164,993 | ||||||

Kinross Gold Corp. | 93,747 | 475,297 | ||||||

New Gold, Inc.(a) | 81,391 | 476,137 | ||||||

Osisko Mining Corp.(a) | 85,692 | 418,331 | ||||||

Pan American Silver Corp. | 72,423 | 768,408 | ||||||

Potash Corp. of Saskatchewan, Inc. | 155,079 | 4,822,957 | ||||||

Silver Standard Resources, | 68,096 | 382,700 | ||||||

Silver Wheaton Corp. | 26,173 | 593,342 | ||||||

Suncor Energy, Inc. | 36,444 | 1,324,739 | ||||||

Teck Resources, Ltd., Class B | 14,026 | 375,055 | ||||||

TransCanada Corp. | 12,731 | 573,759 | ||||||

Turquoise Hill Resources, Ltd.(a) | 109,666 | 528,590 | ||||||

Yamana Gold, Inc. | 45,719 | 453,990 | ||||||

|

| |||||||

| 17,722,173 | ||||||||

|

| |||||||

Chile (0.09%) | ||||||||

Sociedad Quimica y Minera de Chile SA, ADR | 11,464 | 316,521 | ||||||

|

| |||||||

China (0.54%) | ||||||||

China Petroleum & Chemical Corp., Class H | 718,358 | 586,509 | ||||||

China Shenhua Energy Co., Ltd., Class H | 95,369 | 290,302 | ||||||

CNOOC, Ltd. | 250,001 | 513,352 | ||||||

Jiangxi Copper Co., Ltd., Class H | 50,082 | 96,250 | ||||||

PetroChina Co., Ltd., Class H | 330,045 | 378,021 | ||||||

| Shares | Value (Note 2) | |||||||

| ||||||||

China (continued) | ||||||||

Zijin Mining Group Co., Ltd.,Class H | 560,331 | $ | 129,368 | |||||

|

| |||||||

| 1,993,802 | ||||||||

|

| |||||||

Colombia (0.16%) | ||||||||

Ecopetrol SA | 12,334 | 584,138 | ||||||

|

| |||||||

France (0.60%) | ||||||||

Total SA | 35,634 | 2,190,022 | ||||||

|

| |||||||

Germany (0.32%) | ||||||||

K+S AG | 34,170 | 871,752 | ||||||

ThyssenKrupp AG(a) | 11,855 | 303,011 | ||||||

|

| |||||||

| 1,174,763 | ||||||||

|

| |||||||

India (0.25%) | ||||||||

Reliance Industries, Ltd., GDR(b) | 23,796 | 710,787 | ||||||

Sesa Goa, Ltd.(a) | 16,933 | 218,438 | ||||||

|

| |||||||

| 929,225 | ||||||||

|

| |||||||

Israel (0.28%) | ||||||||

Israel Chemicals, Ltd. | 55,718 | 461,071 | ||||||

The Israel Corp., Ltd.(a) | 1,110 | 559,997 | ||||||

|

| |||||||

| 1,021,068 | ||||||||

|

| |||||||

Italy (0.54%) | ||||||||

Eni SpA, ADR | 39,236 | 1,993,189 | ||||||

|

| |||||||

Japan (0.25%) | ||||||||

Inpex Corp. | 73,900 | 852,259 | ||||||

Nippon Steel & Sumitomo Metal Corp. | 20,342 | 66,820 | ||||||

|

| |||||||

| 919,079 | ||||||||

|

| |||||||

Jersey (0.06%) | ||||||||

Randgold Resources, Ltd., ADR | 2,744 | 202,782 | ||||||

|

| |||||||

Luxembourg (0.14%) | ||||||||

ArcelorMittal | 20,626 | 325,066 | ||||||

Tenaris SA, ADR | 4,150 | 194,261 | ||||||

|

| |||||||

| 519,327 | ||||||||

|

| |||||||

Mexico (0.17%) | ||||||||

Grupo Mexico SAB de CV, Series B | 54,387 | 172,366 | ||||||

Industrias Penoles SAB de CV | 14,794 | 429,547 | ||||||

|

| |||||||

| 601,913 | ||||||||

|

| |||||||

Netherlands (1.15%) | ||||||||

CNH Industrial N.V.(a) | 51,797 | 607,575 | ||||||

Nutreco N.V. | 12,688 | 622,160 | ||||||

Royal Dutch Shell PLC, ADR | 44,624 | 2,974,636 | ||||||

|

| |||||||

| 4,204,371 | ||||||||

|

| |||||||

Norway (0.46%) | ||||||||

Norsk Hydro ASA | 26,688 | 119,250 | ||||||

| 19 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Consolidated Statement of Investments | October 31, 2013 (Unaudited) | |

| Shares | Value (Note 2) | |||||||

| ||||||||

Norway (continued) | ||||||||

Yara International ASA | 36,159 | $ | 1,561,026 | |||||

|

| |||||||

| 1,680,276 | ||||||||

|

| |||||||

Peru (0.07%) | ||||||||

Cia de Minas Buenaventura SA, ADR | 18,729 | 271,571 | ||||||

|

| |||||||

Russia (1.86%) | ||||||||

Gazprom OAO, ADR | 159,410 | 1,492,078 | ||||||

LUKOIL OAO, ADR | 18,380 | 1,205,728 | ||||||

Mechel Steel Group, ADR(a) | 16,800 | 53,088 | ||||||

MMC Norilsk Nickel OJSC, ADR | 90,197 | 1,365,583 | ||||||

NovaTek OAO, GDR(c) | 1,817 | 255,288 | ||||||

Rosneft Oil OAO, GDR(c) | 53,474 | 422,177 | ||||||

Severstal OAO, GDR(c) | 78,269 | 683,288 | ||||||

Uralkali OJSC, GDR(c) | 50,441 | 1,347,279 | ||||||

|

| |||||||

| 6,824,509 | ||||||||

|

| |||||||

Singapore (0.53%) | ||||||||

Golden Agri-Resources, Ltd. | 1,263,360 | 610,221 | ||||||

Olam International, Ltd. | 331,254 | 410,668 | ||||||

Wilmar International, Ltd. | 330,439 | 920,398 | ||||||

|

| |||||||

| 1,941,287 | ||||||||

|

| |||||||

South Africa (0.76%) | ||||||||

Anglo Platinum, Ltd. | 2,554 | 103,325 | ||||||

AngloGold Ashanti, Ltd., ADR | 39,786 | 600,769 | ||||||

Gold Fields, Ltd., ADR | 187,690 | 863,374 | ||||||

Harmony Gold Mining Co., Ltd., ADR | 36,130 | 122,842 | ||||||

Impala Platinum Holdings, Ltd. | 39,295 | 477,548 | ||||||

Kumba Iron Ore, Ltd. | 1,186 | 49,647 | ||||||

Sasol, Ltd. | 10,287 | 525,583 | ||||||

Sibanye Gold, Ltd., ADR | 8,280 | 46,534 | ||||||

|

| |||||||

| 2,789,622 | ||||||||

|

| |||||||

South Korea (0.14%) | ||||||||

POSCO, ADR | 6,977 | 519,507 | ||||||

|

| |||||||

Sweden (0.10%) | ||||||||

Holmen AB, B Shares | 11,000 | 365,476 | ||||||

|

| |||||||

Switzerland (2.21%) | ||||||||

Glencore Xstrata PLC | 164,660 | 897,661 | ||||||

Syngenta AG | 15,982 | 6,455,506 | ||||||

Transocean, Ltd. | 8,890 | 418,452 | ||||||

Weatherford International, Ltd.(a) | 20,498 | 336,987 | ||||||

|

| |||||||

| 8,108,606 | ||||||||

|

| |||||||

United Kingdom (2.28%) | ||||||||

Anglo American PLC(a) | 27,213 | 647,960 | ||||||

Antofagasta PLC | 13,306 | 182,414 | ||||||

BG Group PLC | 55,192 | 1,126,990 | ||||||

BHP Billiton PLC, ADR | 20,756 | 1,279,400 | ||||||

BP PLC, ADR | 74,317 | 3,455,740 | ||||||

Kazakhmys PLC | 11,431 | 48,003 | ||||||

Lonmin PLC(a) | 32,588 | 168,565 | ||||||

| Shares | Value (Note 2) | |||||||

| ||||||||

United Kingdom (continued) |

| |||||||

Petropavlovsk PLC | 10,690 | $ | 13,712 | |||||

Rio Tinto PLC, ADR | 28,325 | 1,436,078 | ||||||

|

| |||||||

| 8,358,862 | ||||||||

|

| |||||||

United States (19.59%) | ||||||||

AGCO Corp. | 21,956 | 1,281,791 | ||||||

Alcoa, Inc. | 15,849 | 146,920 | ||||||

Allegheny Technologies, Inc. | 19,804 | 655,512 | ||||||

Allied Nevada Gold Corp.(a) | 95,099 | 388,004 | ||||||

American Vanguard Corp. | 4,915 | 128,281 | ||||||

Anadarko Petroleum Corp. | 8,727 | 831,596 | ||||||

Apache Corp. | 7,118 | 632,078 | ||||||

Archer-Daniels-Midland Co. | 105,307 | 4,307,056 | ||||||

Baker Hughes, Inc. | 10,613 | 616,509 | ||||||

Boardwalk Pipeline Partners LP | 3,100 | 92,845 | ||||||

Buckeye Partners LP | 1,400 | 94,178 | ||||||

Bunge, Ltd. | 15,262 | 1,253,468 | ||||||

Cameron International Corp.(a) | 11,146 | 611,470 | ||||||

CF Industries Holdings, Inc. | 14,847 | 3,201,013 | ||||||

Chevron Corp. | 43,292 | 5,193,308 | ||||||

Cliffs Natural Resources, Inc. | 7,741 | 198,789 | ||||||

Coeur Mining, Inc.(a) | 9,712 | 118,583 | ||||||

ConocoPhillips | 21,492 | 1,575,364 | ||||||

CST Brands, Inc. | 2,472 | 79,697 | ||||||

Deere & Co. | 60,913 | 4,985,120 | ||||||

Detour Gold Corp.(a) | 2,430 | 19,857 | ||||||

Devon Energy Corp. | 8,015 | 506,708 | ||||||

El Paso Pipeline Partners LP | 2,300 | 93,288 | ||||||

Enbridge Energy Partners LP, Class A | 3,000 | 90,810 | ||||||

Energy Transfer Partners LP | 2,000 | 105,940 | ||||||

Ensco PLC, Class A | 4,284 | 246,973 | ||||||

Enterprise Products Partners LP | 1,500 | 94,920 | ||||||

EOG Resources, Inc. | 3,478 | 620,475 | ||||||

Exxon Mobil Corp. | 107,497 | 9,633,881 | ||||||

First Majestic Silver Corp.(a) | 40,390 | 456,811 | ||||||

FMC Technologies, Inc.(a) | 6,853 | 346,419 | ||||||

Freeport-McMoRan Copper & Gold,Inc. | 13,813 | 507,766 | ||||||

Halliburton Co. | 18,836 | 998,873 | ||||||

Hecla Mining Co. | 32,888 | 102,611 | ||||||

Helmerich & Payne, Inc. | 5,481 | 425,052 | ||||||

Hess Corp. | 4,033 | 327,480 | ||||||

HollyFrontier Corp. | 9,280 | 427,437 | ||||||

Ingredion, Inc. | 17,747 | 1,167,043 | ||||||

Intrepid Potash, Inc. | 35,134 | 521,740 | ||||||

Kinder Morgan Energy Partners LP | 1,200 | 96,840 | ||||||

Kinder Morgan, Inc. | 15,180 | 536,006 | ||||||

Magellan Midstream Partners LP | 1,780 | 106,871 | ||||||

Marathon Oil Corp. | 34,740 | 1,224,932 | ||||||

Marathon Petroleum Corp. | 14,714 | 1,054,405 | ||||||

Monsanto Co. | 94,514 | 9,912,628 | ||||||

The Mosaic Co. | 54,139 | 2,482,273 | ||||||

Murphy Oil Corp. | 9,398 | 566,887 | ||||||

National Oilwell Varco, Inc. | 8,251 | 669,816 | ||||||

Newmont Mining Corp. | 22,497 | 613,268 | ||||||

| 20 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Consolidated Statement of Investments | October 31, 2013 (Unaudited) | |

| Shares | Value (Note 2) | |||||||

| ||||||||

United States (continued) |

| |||||||

Noble Energy, Inc. | 9,360 | $ | 701,345 | |||||

Nucor Corp. | 4,675 | 242,025 | ||||||

Occidental Petroleum Corp. | 19,094 | 1,834,552 | ||||||

Peabody Energy Corp. | 7,370 | 143,568 | ||||||

Phillips 66 | 17,658 | 1,137,705 | ||||||

Pioneer Natural Resources Co. | 2,762 | 565,602 | ||||||

Plains All American Pipeline LP | 1,800 | 92,196 | ||||||

Plum Creek Timber Co., Inc | 6,200 | 281,480 | ||||||

Potlatch Corp. | 7,200 | 293,976 | ||||||

Rayonier, Inc. | 5,350 | 251,557 | ||||||

Regency Energy Partners LP | 3,500 | 89,215 | ||||||

Royal Gold, Inc. | 9,863 | 473,819 | ||||||

Schlumberger, Ltd. | 26,128 | 2,448,716 | ||||||

Southern Copper Corp. | 6,156 | 172,060 | ||||||

Southwestern Energy Co.(a) | 7,599 | 282,835 | ||||||

Spectra Energy Corp. | 5,869 | 208,760 | ||||||

Tesoro Corp. | 8,749 | 427,739 | ||||||

Valero Energy Corp. | 23,762 | 978,282 | ||||||

Weyerhaeuser Co. | 10,200 | 310,080 | ||||||

The Williams Co., Inc. | 15,553 | 555,398 | ||||||

|

| |||||||

| 71,840,502 | ||||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $141,029,672) |

| 140,147,835 | ||||||

|

| |||||||

EXCHANGE TRADED FUNDS (1.38%) |

| |||||||

iShares® Gold Trust(a) | 218,898 | 2,812,839 | ||||||

SPDR® Gold Trust(a) | 17,688 | 2,259,465 | ||||||

|

| |||||||

TOTAL EXCHANGE TRADED FUNDS (Cost $6,391,017) |

| 5,072,304 | ||||||

|

| |||||||

WARRANTS (0.00%)(d) | ||||||||

Canada (0.00%)(d) | ||||||||

Kinross Gold Corp., Strike Price $21.30, Expires 9/17/14(a) | 19 | 1 | ||||||

|

| |||||||

TOTAL WARRANTS (Cost $69) |

| 1 | ||||||

|

| |||||||

Principal Amount | Value (Note 2) | |||||||

| ||||||||

GOVERNMENT BONDS (44.23%) |

| |||||||

U.S. Treasury Bonds (44.23%) |

| |||||||

United States Treasury Inflation Indexed Bonds | ||||||||

2.000%, 1/15/14(e) | $ | 6,296,858 | 6,308,173 | |||||

1.250%, 4/15/14 | 8,785,227 | 8,838,764 | ||||||

2.000%, 7/15/14 | 11,476,475 | 11,742,764 | ||||||

1.625%, 1/15/15(e)(f) | 13,748,268 | 14,180,046 | ||||||

0.500%, 4/15/15(e) | 11,789,823 | 12,037,598 | ||||||

1.875%, 7/15/15 | 8,717,038 | 9,185,578 | ||||||

2.000%, 1/15/16 | 9,131,903 | 9,760,789 | ||||||

0.125%, 4/15/16 | 21,720,160 | 22,321,700 | ||||||

2.500%, 7/15/16 | 11,290,890 | 12,461,439 | ||||||

2.375%, 1/15/17(e)(f) | 10,147,288 | 11,266,655 | ||||||

0.125%, 4/15/17(e)(f) | 14,930,070 | 15,445,620 | ||||||

| Principal Amount | Value (Note 2) | |||||||

| ||||||||

U.S. Treasury Bonds (continued) |

| |||||||

2.625%, 7/15/17(e) | $ | 14,387,100 | $ | 16,359,701 | ||||

1.625%, 1/15/18 | 11,163,300 | 12,311,468 | ||||||

|

| |||||||

| 162,220,295 | ||||||||

|

| |||||||

TOTAL GOVERNMENT BONDS |

| 162,220,295 | ||||||

|

| |||||||

| Expiration Date | Exercise Price | Number of Contracts | Value | |||||||||||

| ||||||||||||||

PURCHASED CALL OPTIONS (0.73%) |

| |||||||||||||

| Market Vectors® Gold Miners ETF: | ||||||||||||||

| 1/18/14 | $30.00 | 245 | $ | 10,167 | ||||||||||

| 1/18/14 | 36.00 | 200 | 1,400 | |||||||||||

| 1/18/14 | 38.00 | 100 | 400 | |||||||||||

| 1/18/14 | 39.00 | 550 | 2,200 | |||||||||||

|

| |||||||||||||

| 14,167 | ||||||||||||||

|

| |||||||||||||

| S&P 500® Index Future: | ||||||||||||||

| 6/20/14 | 1750.00 | 120 | 2,253,000 | |||||||||||

| E-mini S&P 500® Future: | ||||||||||||||

| 11/16/13 | 1640.00 | 75 | 421,125 | |||||||||||

TOTAL PURCHASED CALL OPTIONS |

| 2,688,292 | ||||||||||||

| ||||||||||||||

PURCHASED PUT OPTIONS (0.13%) |

| |||||||||||||

SPDR® S&P 500® ETF Trust | 9/30/14 | 170.00 | 500 | 460,500 | ||||||||||

TOTAL PURCHASED PUT OPTIONS |

| 460,500 | ||||||||||||

| ||||||||||||||

| 7-Day Yield | Shares | Value (Note 2) | ||||||||||

| ||||||||||||

SHORT TERM INVESTMENTS (14.48%) |

| |||||||||||

Money Market Fund (14.48%) |

| |||||||||||

Dreyfus Treasury Prime Cash Management Fund, Institutional Shares | 0.00004 | % | 53,092,263 | $ | 53,092,263 | |||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS |

| 53,092,263 | ||||||||||

|

| |||||||||||

TOTAL INVESTMENTS (99.17%) |

| $ | 363,681,490 | |||||||||

Other Assets In Excess Of Liabilities (0.83%) |

| 3,053,472(g) | ||||||||||

| ||||||||||||

NET ASSETS - 100.00% |

| $ | 366,734,962 | |||||||||

| ||||||||||||

| 21 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Consolidated Statement of Investments | October 31, 2013 (Unaudited) | |

| (a) | Non-Income Producing Security. |

| (b) | Security exempt from registration under rule 144A of the securities act of 1933. This security may be resold in transactions exempt from registration, normally to qualified institutional buyers. At period end, the market value of those securities was $710,787, representing 0.19% of the Fund’s net assets. |

| (c) | These securities initially sold to other parties pursuant to Regulation S under the 1933 Act and subsequently resold to the Fund. At period end, the aggregate market value of those securities was $2,708,032, representing 0.74% of the Fund’s net assets. |

| (d) | Less than 0.005%. |

| (e) | Security, or portion of security, is being held as collateral for total return swap contracts. |

| (f) | Security, or portion of security, is being held as collateral for futures contracts. |

| (g) | Includes cash which is being held as collateral for written options. |

Common Abbreviations:

| AB | - Aktiebolag is the Swedish equivalent of the term corporation. |

| ADR | - American Depositary Receipt. |

| AG | - Aktiengesellschaft is a German term that refers to a corporation that is limited by shares, i.e., owned by shareholders. |

| ASA | - Allmennaksjeselskap is the Norwegian term for public limited company. |

| ETF | - Exchange Traded Fund. |

| GDR | - Global Depositary Receipt. |

| Ltd. | - Limited. |

| LP | - Limited Partnership. |

| N.V. | - Naamloze vennootschap is the Dutch term for a public limited liability corporation. |

| OAO | - Russian open joint stock company. |

| OJSC | - Open joint stock company. |

| PLC | - Public Limited Co. |

| SA | - Generally designated corporations in various countries, mostly those employing the civil law. |

| SAB | de CV - A variable capital company. |

| SpA | - Societa per Azione. |

| SPDR | - Standard & Poor’s Depository Receipt. |

For Fund compliance purposes, the Fund’s industry and geographical classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease. Industries and regions are shown as a percent of net assets.

See Notes to Financial Statements.

| 22 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Consolidated Statement of Investments | October 31, 2013 (Unaudited) | |

SCHEDULE OF WRITTEN OPTIONS | Expiration Date | Exercise Price | Contracts | Value | ||||||

Written Call Options | ||||||||||

Gold 100 Oz. Future: | ||||||||||

| 12/28/13 | $ 1,285.00 | (20) | $ (100,800) | |||||||

| 12/28/13 | 1,290.00 | (5) | (23,350) | |||||||

Market Vectors® Gold Miners ETF | 11/16/13 | 27.00 | (300) | (6,600) | ||||||

| ||||||||||

TOTAL WRITTEN CALL OPTIONS | ||||||||||

(Premiums received $ 147,071) | (130,750) | |||||||||

| ||||||||||

Written Put Options | ||||||||||

Market Vectors® Gold Miners ETF | 1/18/14 | 25.00 | (100) | (19,000) | ||||||

Monsanto Co. | 1/18/14 | 110.00 | (50) | (36,750) | ||||||

Phillips 66 | 1/18/14 | 65.00 | (100) | (36,500) | ||||||

| ||||||||||

TOTAL WRITTEN PUT OPTIONS | ||||||||||

(Premiums received $ 81,002) | (92,250) | |||||||||

| ||||||||||

TOTAL WRITTEN OPTIONS | ||||||||||

(Premiums received $ 228,073) | $ (223,000) | |||||||||

| ||||||||||

FUTURES CONTRACTS | ||||||||||||||||||

| Description | Position | Contracts | Expiration Date | Value (Note 2) | Unrealized Appreciation | |||||||||||||

Brent Crude Future | Long | 150 | 11/15/13 | $ 16,326,000 | $ 235,890 | |||||||||||||

WTI Crude Future | Short | (170) | 11/20/13 | (16,384,600) | 1,141,890 | |||||||||||||

|

|

|

| |||||||||||||||

| $ (58,600) | $ 1,377,780 | |||||||||||||||||

|

|

|

| |||||||||||||||

Description | Position | Contracts | | Expiration Date | |

| Value (Note 2) |

| | Unrealized Depreciation | | |||||||

E-mini S&P 500® Future | Short | (215) | 12/23/13 | $ (18,823,250) | $ (504,072) | |||||||||||||

Gold 100 Oz. Future | Long | 35 | 12/30/13 | 4,632,950 | (15,034) | |||||||||||||

S&P 500® Index Future | Short | (54) | 12/20/13 | (23,638,500) | (472,598) | |||||||||||||

|

|

|

| |||||||||||||||

| $ (37,828,800) | $ (991,704) | |||||||||||||||||

|

|

|

| |||||||||||||||

See Notes to Financial Statements. |

| 23 | October 31, 2013 |

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | ||

Consolidated Statement of Investments | October 31, 2013 (Unaudited) | |

| TOTAL RETURN SWAP CONTRACTS(a) | ||||||||||||||||

| Swap Counterparty | Reference Obligation | Notional Dollars | Rate Paid by the Fund | Termination Date | Unrealized Appreciation | |||||||||||

Bank of America - Merrill Lynch | ML eXtra Silver GA6 | $ | 706,507 | 0.10% | 6/30/14 | $ | 5,483 | |||||||||

Bank of America - Merrill Lynch | ML Index Robusta | (5,434,669) | 0.00% | 6/30/14 | 476,736 | |||||||||||

Bank of America - Merrill Lynch | MLCS Coffee J-F3 | (3,012,014) | 0.10% | 6/30/14 | 213,834 | |||||||||||

Bank of America - Merrill Lynch | MLCS Copper J-F3 | (5,548,322) | 0.10% | 6/30/14 | 39,721 | |||||||||||