Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8194

FINANCIAL INVESTORS TRUST

(exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

JoEllen L. Legg, Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: May 1, 2011 - October 31, 2011

Table of Contents

Item 1. Reports to Stockholders.

Table of Contents

Table of Contents

| October 31, 2011 (Unaudited) |

Table of Contents

| October 31, 2011 (Unaudited)

| |||

Performance

During the six-month period ended 10/31/2011, the Indian equity markets fell along with the global markets with broader Indian indices like CNX 5001 returning -17.06% in the period, large cap index (Nifty) returning -15.88% and midcap index (CNX Midcap) returning -19.54% (all in USD terms). The investment environment during this period was impacted by the following, with August marking the worst monthly decline (CNX 500 returned -4.73% in May, 1.79% in June, -1.38% in July, -12.47% in August, -6.20% in September, and 5.33% in October).

| » | The worsening debt situation in Europe, S&P downgrade of long term US sovereign rating, and deteriorating global economic growth have impacted investor sentiment, resulting in a sell-off in equity markets worldwide. On the domestic side, increasing interest rates, persistent high levels of inflation, weakening GDP growth, and lack of significant reform activities also resulted in increased pessimism in the Indian market. |

| » | Currency has been a big spoiler for international investors investing in India. The Indian Rupee depreciated 10.12% during the 6-month period against the USD. India’s twin deficits, current account & fiscal account, are negatively affecting the Indian currency harder than any previous cycle. The issue is getting compounded by still elevated commodity prices and the global deleveraging by European banks which is affecting the capital flows. Historically, the current account deficit has been funded by the capital flows but in the current environment, it seems challenging to expect capital flows to compensate for trade deficit. |

| » | During the period, the market witnessed corporate India announcing their earning results. Revenue and earnings growth have been subdued as a result of the weakening environment, high interest costs, and inflation. |

| » | For the quarter ending September 2012, real GDP growth number came in at 6.9%, lower than previous quarter’s number of 7.7% and last year’s 8.4%, with Manufacturing and Mining sector leading the decline. In our view, it is clear that growth for 2012 as a whole is unlikely to exceed 7%. Also the likelihood of further revisions to growth estimates for 2013 is high. Investment growth continues to show signs of weakness as the lag impact of the high interest rates are felt and the likelihood of a significant slowdown in export growth appears large. The trends in GDP growth by aggregate demand also clearly reflect the impact of higher interest rates on demand with the declining growth trajectory in the case of private consumption expenditure and the fact that Gross Fixed Capital Formation has recorded negative growth in the quarter. Going forward, |

we believe that proactive government policies are needed to restore private corporate sentiment and to boost investments leading to capital formation. |

| » | During the period, the inflation number has been persistently above 9% with the highest inflation number recorded in the month of August (9.78%). The inflation number also marked the tenth consecutive month of inflation above 9%. Fuel & Power inflation rose significantly during the period reflecting the rising oil price and significant rupee depreciation (as India is a major importer of Oil) |

| » | The Central bank in its October credit policy increased the interest rate by another 25 basis points (bps), in line with expectation, bringing the repo2 and reverse repo rate to 8.50% and 7.50% respectively. In the policy note, RBI (Reserve Bank of India) also hinted that this may be the last interest rate hike for the year. RBI also lowered its 2012 GDP growth forecast to 7.6% (v/s 8.0% previously), acknowledging the fact that its anti-inflationary monetary policy measures of increasing interest rate has dented growth. Nevertheless, RBI maintained its inflation target of 7% for March 2012 citing that inflation will start declining significantly December onwards. |

| » | Post the state elections in 2011, government announced several reforms activities such as increase in diesel price, introduction of Land Acquisition, Rehabilitation, and Resettlement bill (LARR), and deregulation of saving bank deposit rates. While these initiatives signal some policy activity by the government, big reform activities have not yet been initiated. Policy inaction remains the single largest concern for the Indian economy in a deteriorating global environment, as the current policy blocks do not infuse much confidence for significant capital formation. |

Portfolio Composition

The portfolio is constructed to potentially benefit from the strong macro-economic growth in the Indian economy across four broad themes in India – Consumption lead by favourable demographics, Financial services, Infrastructure and Outsourcing. The Fund has the flexibility to invest across market capitalizations – depending on market conditions, valuation differential, earnings growth, liquidity, etc.

For the 6-month period ending 10/31/2011, sectorally the key changes have been in Consumer staples (added 350 bps), Oil & Gas (added 350 bps), Information Technology (added 180 bps), Metals (reduced 110 bps), Aviation (reduced 100 bps), and Capital goods (reduced 75 bps). Thematically, Consumption (at about 25%), Financials (at about 22%) are the largest themes in the portfolio while Infrastructure exposure is less than 10% due to poor policy initiatives by the government. Over the last

| 2 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

6 month, exposure to mid-cap and small-cap companies in the fund has moved up from 17.21% in April 2011 to 26.79% in July 2011, then down to 20.76% in October 2011.

Sectorally, the portfolio is overweight Oil & Gas, Media, Infrastructure while underweight Financials, Auto, Capital goods, Consumer staples, and Utilities as of 10/31/2011.

Market Outlook

For international investors, Indian equities have been one of the worst performing markets, with depressed equity returns exacerbated by weak currency. We feel that the major reasons of this under-performance can be attributed to:

| » | Persistence of high inflation and subsequent tightening of interest rates |

| » | High oil prices impacting Indian fiscal deficit |

| » | Policy paralysis by the government |

| » | Global concerns on sovereign debt |

While inflation has begun to ease off and the RBI has signaled its intent on focusing on growth rather than inflation, the government continues to be bound by political compulsions with hardly any policy decision to improve investment climate in India. While monetary policy will increasingly become more accommodative towards growth, participants will be watchful of government policy initiatives (especially as it presents its annual budget in Feb 2012).

If inflation was the biggest concern at the start of 2011, we enter 2012 with concerns on growth. As of October 2011, S&P CNX Nifty is trading at consensus Bloomberg estimates of 14.9x 2012 earnings per share and CNX Midcap index is trading at 11.9x 2012 earnings per share, which in our opinion factors a slowing economic growth. However, we believe despite attractive valuations, market participants will wait to see government policy in action before a significant re-rating of the Indian equities.

| 1 | CNX 500- The S & P’s CNX 500 is India’s first broad based stock market index |

| 2 | REPO- A form of short term barrowing for dealers in government securities. The dealers sells the securities to the investor usually on an overnight basis, and buys them back the following day Reverse REPO- The purchase of a securities with the agreement to sell them at a high price at a specific future date. (investopedia) |

Past performance does not guarantee future results.

| 3 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

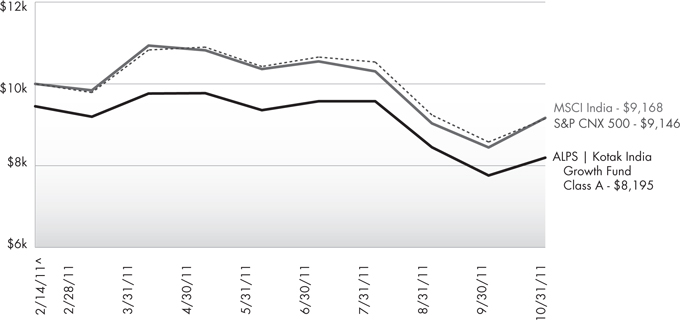

Performance of $10,000 Initial Investment (as of October 31, 2011)

Comparison of change in value of a $10,000 investment (includes applicable sales loads of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 4 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Cumulative Return (as of October 31, 2011)

| Since Inception^ | Total Expense Ratio | What You Pay* | ||||

Class A (NAV)1 | -13.30% | 69.97% | 2.01% | |||

Class A (MOP)2 | -18.05% | |||||

Class C (NAV)1 | -13.80% | 69.65% | 2.61% | |||

Class C (CDSC)2 | -14.66% | |||||

Class I | -13.10% | 96.68% | 1.61% | |||

S&P CNX 500 Index3 | -8.54% | |||||

MSCI India Index4 | -8.32% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data please call (866) 759-5679.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested. Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the funds original investment.

| 1 | Net Asset Value (NAV) is the share price without sales charges. |

| 2 | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%; Class C returns include the 1.00% CDSC. |

| 3 | S&P CNX 500 - India’s first broad based benchmark of the Indian capital market. The S&P CNX 500 companies are disaggregated into 72 industry indices. Industry weightages in the market. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| 4 | MSCI India Index - a free float weighted equity index. It was developed with a base value of 100 as-of December 31, 1992. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of 2/14/2011. |

| * | What You Pay reflects the Adviser’s and Sub-Adviser’s decision to contractually limit expenses through August 31, 2012. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The Fund is less than a year old and has limited operating history. This Fund is not suitable for all investors. Subject to investment risks, including possible loss of the principal amount invested.

Investing in India involves risk and considerations not present when investing in more established securities markets. The Fund may be more susceptible to economic, market, political and local risks of the region than a fund that is more geographically diversified.

Top Ten Long Holdings (as a % of Net Assets) †

Reliance Industries, Ltd. | 7.59% | |

Infosys, Ltd. | 6.22% | |

ICICI Bank, Ltd. | 4.22% | |

Tata Consultancy Services, Ltd. | 3.91% | |

ITC, Ltd. | 3.80% | |

HDFC Bank, Ltd. | 3.72% | |

Housing Development Finance Corp. | 3.03% | |

Larsen & Toubro, Ltd. | 2.75% | |

Dr Reddy’s Laboratories, Ltd. | 2.27% | |

Mahindra & Mahindra, Ltd. | 2.25% | |

Top Ten Long Holdings | 39.76% |

| † | Holdings are subject to change. |

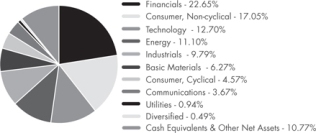

Industry Sector Allocation (Long Positions as a % of Net Assets)

| 5 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

| October 31, 2011 (Unaudited)

| |||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2011 and held until October 31, 2011.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 5/1/11 | Ending Account Value 10/31/11 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/11 - 10/31/11 | |||||||||||||||||

Class A | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 838.50 | 2.00 | % | $ | 9.24 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.08 | 2.00 | % | $ | 10.13 | ||||||||||||

Class C | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 835.30 | 2.60 | % | $ | 11.99 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,012.07 | 2.60 | % | $ | 13.15 | ||||||||||||

Class I | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 839.60 | 1.60 | % | $ | 7.40 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.09 | 1.60 | % | $ | 8.11 | ||||||||||||

| (a) | The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 366. |

| 6 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

| October 31, 2011 (Unaudited)

| |||

| Shares | Value (Note 1) | |||||||

COMMON STOCKS (89.23%) |

| |||||||

Basic Materials (6.27%) | ||||||||

Chemicals (2.01%) | ||||||||

Asian Paints, Ltd. | 650 | $42,109 | ||||||

Gujarat State Fertilisers & Chemicals, Ltd. | 3,850 | 37,372 | ||||||

|

| |||||||

| 79,481 | ||||||||

|

| |||||||

Iron & Steel (1.41%) | ||||||||

Jindal Steel & Power, Ltd. | 4,846 | 55,524 | ||||||

|

| |||||||

Mining (2.85%) | ||||||||

Hindustan Zinc, Ltd. | 29,290 | 74,986 | ||||||

Sterlite Industries India, Ltd. | 14,450 | 37,791 | ||||||

|

| |||||||

| 112,777 | ||||||||

|

| |||||||

TOTAL BASIC MATERIALS | 247,782 | |||||||

|

| |||||||

Communications (3.67%) | ||||||||

Media (1.86%) | ||||||||

Dish TV India, Ltd.(a) | 17,000 | 26,318 | ||||||

Jagran Prakashan, Ltd. | 21,295 | 47,442 | ||||||

|

| |||||||

| 73,760 | ||||||||

|

| |||||||

Telecommunications (1.81%) |

| |||||||

Bharti Airtel, Ltd. | 8,921 | 71,424 | ||||||

|

| |||||||

TOTAL COMMUNICATIONS | 145,184 | |||||||

|

| |||||||

Consumer, Cyclical (4.57%) | ||||||||

Auto Manufacturers (2.25%) |

| |||||||

Mahindra & Mahindra, Ltd. | 5,050 | 89,117 | ||||||

|

| |||||||

Leisure Time (1.41%) | ||||||||

Bajaj Auto, Ltd. | 1,579 | 55,831 | ||||||

|

| |||||||

Textiles (0.91%) | ||||||||

Raymond, Ltd. | 4,500 | 35,779 | ||||||

|

| |||||||

TOTAL CONSUMER, CYCLICAL |

| 180,727 | ||||||

|

| |||||||

Consumer, Non-cyclical (17.05%) |

| |||||||

Agriculture (3.80%) | ||||||||

ITC, Ltd. | 34,500 | 150,431 | ||||||

|

| |||||||

Beverages (0.53%) | ||||||||

United Spirits, Ltd. | 1,175 | 21,059 | ||||||

|

| |||||||

Commercial Services (1.98%) |

| |||||||

Gujarat Pipavav Port, Ltd.(a) | 12,000 | 17,556 | ||||||

Mundra Port and Special | ||||||||

Economic Zone, Ltd. | 18,150 | 60,827 | ||||||

|

| |||||||

| 78,383 | ||||||||

|

| |||||||

| Shares | Value (Note 1) | |||||||

Food (2.03%) | ||||||||

GlaxoSmithKline Consumer Healthcare, Ltd. | 764 | $36,974 | ||||||

Shree Renuka Sugars, Ltd. | 36,880 | 43,079 | ||||||

|

| |||||||

| 80,053 | ||||||||

|

| |||||||

Household Products & Wares (3.39%) |

| |||||||

Godrej Consumer Products, Ltd. | 4,222 | 37,770 | ||||||

Hindustan Unilever, Ltd. | 7,643 | 58,857 | ||||||

Marico, Ltd. | 11,800 | 37,363 | ||||||

|

| |||||||

| 133,990 | ||||||||

|

| |||||||

Pharmaceuticals (5.32%) |

| |||||||

Divi’s Laboratories, Ltd. | 4,045 | 63,837 | ||||||

Dr Reddy’s Laboratories, Ltd. | 2,648 | 89,696 | ||||||

Lupin, Ltd. | 5,900 | 56,751 | ||||||

|

| |||||||

| 210,284 | ||||||||

|

| |||||||

TOTAL CONSUMER, NON-CYCLICAL |

| 674,200 | ||||||

|

| |||||||

Diversified (0.49%) | ||||||||

Holding Companies-Diversified Operations (0.49%) |

| |||||||

Sintex Industries, Ltd. | 8,000 | 19,230 | ||||||

|

| |||||||

TOTAL DIVERSIFIED |

| 19,230 | ||||||

|

| |||||||

Energy (11.10%) | ||||||||

Oil & Gas (11.10%) |

| |||||||

Hindustan Petroleum Corp., Ltd. | 10,410 | 71,221 | ||||||

Oil & Natural Gas Corp., Ltd. | 11,885 | 67,520 | ||||||

Reliance Industries, Ltd. | 16,765 | 300,147 | ||||||

|

| |||||||

TOTAL ENERGY | 438,888 | |||||||

|

| |||||||

Financials (22.65%) | ||||||||

Banks (16.02%) | ||||||||

Allahabad Bank | 11,485 | 35,137 | ||||||

Axis Bank, Ltd. | 1,760 | 41,584 | ||||||

Bank of Baroda | 3,425 | 53,916 | ||||||

HDFC Bank, Ltd. | 14,740 | 146,956 | ||||||

ICICI Bank, Ltd. | 8,849 | 166,831 | ||||||

IndusInd Bank, Ltd. | 8,380 | 49,066 | ||||||

State Bank of India | 1,239 | 48,177 | ||||||

Union Bank of India | 7,182 | 33,179 | ||||||

Yes Bank, Ltd. | 9,183 | 58,829 | ||||||

|

| |||||||

| 633,675 | ||||||||

|

| |||||||

Diversified Financial Services (5.83%) |

| |||||||

Bajaj Finance, Ltd. | 3,754 | 52,493 | ||||||

Housing Development Finance Corp. | 8,510 | 119,723 | ||||||

Power Finance Corp., Ltd. | 19,050 | 58,339 | ||||||

|

| |||||||

| 230,555 | ||||||||

|

| |||||||

| 7 | October 31, 2011 |

Table of Contents

ALPS | Kotak India Growth Fund | ||||

Statement of Investments

| October 31, 2011 (Unaudited)

| |||

| Shares | Value (Note 1) | |||||||

Real Estate (0.80%) |

| |||||||

Phoenix Mills, Ltd. | 7,704 | $31,612 | ||||||

|

| |||||||

TOTAL FINANCIALS | 895,842 | |||||||

|

| |||||||

Industrials (9.79%) | ||||||||

Building Materials (1.93%) |

| |||||||

Shree Cement, Ltd. | 1,965 | 76,454 | ||||||

|

| |||||||

Electrical Components & Equipment (2.21%) |

| |||||||

Bharat Heavy Electricals, Ltd. | 7,620 | 49,472 | ||||||

V-Guard Industries, Ltd. | 9,188 | 38,000 | ||||||

|

| |||||||

| 87,472 | ||||||||

|

| |||||||

Engineering & Construction (4.31%) |

| |||||||

IRB Infrastructure Developers, Ltd. | 18,400 | 61,675 | ||||||

Larsen & Toubro, Ltd. | 3,771 | 108,746 | ||||||

|

| |||||||

| 170,421 | ||||||||

|

| |||||||

Machinery Diversified (0.92%) |

| |||||||

Thermax, Ltd. | 3,841 | 36,394 | ||||||

|

| |||||||

Packaging & Containers (0.42%) |

| |||||||

Ess Dee Aluminium, Ltd. | 4,293 | 16,399 | ||||||

|

| |||||||

TOTAL INDUSTRIALS | 387,140 | |||||||

|

| |||||||

Technology (12.70%) | ||||||||

Computers (11.71%) |

| |||||||

Infosys, Ltd. | 4,206 | 246,052 | ||||||

Redington India, Ltd. | 31,968 | 62,155 | ||||||

Tata Consultancy Services, Ltd. | 6,802 | 154,683 | ||||||

|

| |||||||

| 462,890 | ||||||||

|

| |||||||

Software (0.99%) |

| |||||||

HCL Technologies, Ltd. | 4,342 | 39,225 | ||||||

|

| |||||||

TOTAL TECHNOLOGY | 502,115 | |||||||

|

| |||||||

Utilities (0.94%) | ||||||||

Electric (0.94%) |

| |||||||

NTPC, Ltd. | 10,150 | 37,184 | ||||||

|

| |||||||

TOTAL UTILITIES | 37,184 | |||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $3,823,181) |

| 3,528,292 | ||||||

|

| |||||||

| 7-Day Yield | Shares | Value (Note 1) | ||||||||||

SHORT TERM INVESTMENTS (0.24%) |

| |||||||||||

Money Market Fund (0.24%) |

| |||||||||||

Dreyfus Cash Advantage Fund, Institutional Class | 0.067 | % | 9,491 | $9,491 | ||||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $9,491) |

| 9,491 | ||||||||||

|

| |||||||||||

TOTAL INVESTMENTS (89.47%) (Cost $3,832,672) |

| $ | 3,537,783 | |||||||||

Other Assets In Excess Of |

| 416,280 | ||||||||||

|

| |||||||||||

NET ASSETS (100.00%) |

| $ | 3,954,063 | |||||||||

|

| |||||||||||

| (a) | Non-Income Producing Security. |

Common Abbreviations:

Ltd. - Limited.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry subclassifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

FUTURES CONTRACTS

At October 31, 2011, the Fund had outstanding futures contracts:

| Description | Position | Contracts | Expiration Date | Value (Note 1) | Unrealized Appreciation | |||||||||

Induslnd Bank Future | Long | 3 | 11/25/11 | $ | 858,000 | $ | 678 | |||||||

S&P CNX NIFTY Future | Long | 33 | 11/25/11 | 8,822,715 | 2,134 | |||||||||

|

|

|

| |||||||||||

| $ | 9,680,715 | $ | 2,812 | |||||||||||

|

|

|

| |||||||||||

See Notes to Financial Statements.

| 8 | October 31, 2011 |

Table of Contents

| October 31, 2011 (Unaudited)

| |||

Overview

What happens when you mix fear with uncertainty? You get a very anxious, volatile environment. In the case of the world equity markets, you get volatile equity values. Exactly what we experienced in the semi-annual period ending October 31, 2011…and private equity was not immune.

The period started off on a fairly stable, if not upbeat, tone. Yes, there were unresolved problems: ballooning US federal deficits, concern surrounding Greece and the unity of the Euro, gridlock on the political/policy front, stagnating employment, lackluster consumer spending and pockets of input inflation. On the other hand, corporations as a whole were doing well: most were seeing modest revenue growth, some were getting squeezed with higher input costs, but overall margins were stable and bottom line profitability looked good. It was the calm before the storm. What ensued next was overwhelming. The combination of political gridlock in the US over the federal debt level and the lack of a unified approach to resolving the sovereign debt crisis in Europe spelled fear and uncertainty with investors. The new focus: fault lines in the credit markets, widening credit spreads and the soundness of the banking community. The equity, debt, and commodity markets around the globe acted accordingly; a swift and volatile sell-off. The “R” word (as in Recession) was now part of the conversation.

And the private equity markets? How did the asset class fare? Not so well. What had started out as another robust year for growth within their portfolio of private businesses, increases in valuations, good M&A activity and strong realizations, quickly came to an end for most private equity firms. The music had stopped. Not because their portfolio of businesses had seen a reversal in fortune. No, it was the declining equity markets that dragged everything down with it. Like it or not, we live in a very correlated world and private equity, at least in the short term, is not immune to this correlation.

Listed private equity companies, with few exceptions, saw their share price decline significantly. Discounts to stated net asset value widened out to levels not seen since 2009. The performance of the Red Rocks Listed Private Equity Fund (LPEIX) went from +11.13% for the six month period ended June 30, 2011 to -23.34% for the six month period ended October 31, 2011.

What’s perplexing to us is that when we look at listed private equity today vs. 2-3 years ago, we’re seeing the following in the private businesses/investments:

| » | Lower debt levels (leverage) to Earnings Before Taxes, Depreciation and Amortization (EBITDA); |

| » | Debt maturities have been extended with flexible terms; and |

| » | Stable to growing revenue and EBITDA. |

In addition, the listed private equity companies themselves (the holding company level) look equally as healthy:

| » | Commitment levels are much lower and very manageable; |

| » | Credit facilities have been re-negotiated with flexible terms; |

| » | Cash levels are high; |

| » | Valuations are conservative, with uplifts being the norm; and |

| » | Realizations have been quite strong. |

In summary, we believe that things look pretty good. Yet the public markets don’t seem to care or are signaling tough times (very tough times?) ahead for private equity.

Portfolio Review

For the six month period ended October 31, 2011, the Fund’s Class A Shares, LPEFX, returned -23.45% at Net Asset Value, (Class A delivered a net return of -27.61% at MOP), compared with -11.32% and -22.18% for the MSCI World Index and the S&P Listed Private Equity Index, respectively.

During the period we exited seven holdings: Aker ASA, China Merchants, Dinamia, HAL Trust, Investor AB, JAFCO and Marfin. We added six holdings as well: Aurelius, Brookfield Infrastructure Partners, Fosun, Harbourvest, RHJ International and Softbank Corp.

While the share price of most every holding in Fund was negatively impacted during the period, the underlying fundamentals continue to appear quite good. The private businesses are performing well with strong uplifts in values and ongoing liquidity events. Hence, we continue to be pleased with the portfolio.

Net contributors to performance for the period included:

| » | IP Group PLC |

| » | Aurelius AG |

| » | Graphite Enterprise Trust |

Net detractors to performance for the period included:

| » | Euarzeo |

| » | KKR & Co. |

| » | Ratos AB |

| 9 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Looking Ahead

It’s our view that until the issues in the US and Europe are resolved (mainly government policy in nature), we will continue to experience a very nervous equity market; private equity included. Our hope is that more rational minds prevail and our elected officials can fix the self-induced problems and restore confidence.

As always, we appreciate your continued support and interest in Red Rocks and the Listed Private Equity strategy.

Adam Goldman, Co-Portfolio Manager

Past Performance does not guarantee future results.

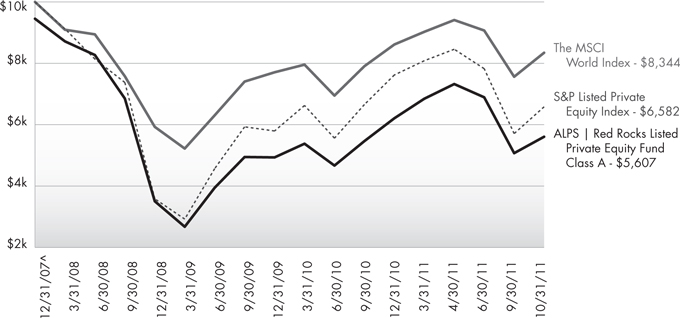

Performance of $10,000 Initial Investment (as of October 31, 2011)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

Source: Morningstar

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| ^ | Fund inception date of 12/31/2007. |

| 10 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

| Average Annual Total Returns (as of October 31, 2011) | ||||||||

| 1 Year | Since Inception^ | Total Expense Ratio | What You Pay* | |||||

Class A (NAV)1 | -5.00% | -12.73% | 1.71% | 1.51% | ||||

Class A (MOP)2 | -10.18% | -14.00% | ||||||

Class C (NAV)1 | -5.73% | -13.50% | 2.32% | 2.26% | ||||

Class C (CDSC)2 | -6.62% | -13.50% | ||||||

Class I | -4.66% | -12.46% | 1.37% | 1.26% | ||||

Class R | -5.29% | -13.17% | 1.88% | 1.76% | ||||

MSCI World Index3 | -7.45% | -10.33% | ||||||

S&P LPE Index4 | 1.76% | -4.61% | ||||||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 90 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call (866) 759-5679.

Performance shown for Class C shares prior to June 30, 2010 reflects the historical performance of the Fund’s Class A shares, calculated using the fees and expenses of Class C shares.

| 1 | Net Asset Value (NAV) is the share price without sales charges. The performance data shown does not reflect the decution of the sales load or the redemption fee or CDSC, and that, if reflected, the load or fee would reduce the performance quoted. |

| 2 | Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. CDSC performance for Class C shares includes a 1% contingent deferred sales charge (CDSC) on C shares redeemed within 12 months of purchase. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. |

| 3 | MSCI World Index: Morgan Stanley Capital International’s market capitalization weighted index is composed of companies representative of the market structure of 22 developed market countries in North America, Europe and the Asia/Pacific Region. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| 4 | S&P Listed Private Equity Index: The S&P Listed Private Equity Index is comprised of 30 leading listed private equity companies that meet size, liquidity, exposure, and activity requirements. The index is designed to provide tradable exposure to the leading publicly listed companies in the private equity space. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of 12/31/2007. |

| * | What You Pay reflects the Adviser’s and Sub-Adviser’s decision to contractually limit expenses through August 31, 2012. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Listed Private Equity Companies are subject to various risks depending on their underlying investments, which could include, but are not limited to, additional liquidity risk, industry risk, non-U.S. security risk, currency risk, credit risk, managed portfolio risk and derivatives risk (derivatives risk is the risk that the value of the Listed Private Equity Companies’ derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment).

There are inherent risks in investing in private equity companies, which encompass financial institutions or vehicles whose principal business is to invest in and lend capital to privately held companies. Generally, little public information exists for private and thinly traded companies, and there is a risk that investors may not be able to make a fully informed investment decision.

Listed Private Equity Companies may have relatively concentrated investment portfolios, consisting of a relatively small number of holdings. A consequence of this limited number of investments is that the aggregate returns realized may be adversely impacted by the poor performance of a small number of investments, or even a single investment, particularly if a company experiences the need to write down the value of an investment.

Certain of the Fund’s investments may be exposed to liquidity risk due to low trading volume, lack of a market maker or legal restrictions limiting the ability of the Fund to sell particular securities at an advantageous price and/or time. As a result, these securities may be more difficult to value. Foreign investing involves special risks, such as currency fluctuations and political uncertainty. The Fund invests in derivatives and is subject to the risk that the value of those derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment.

| 11 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Top Ten Holdings (as a % of Net Assets) † | ||||||

3i Group PLC | 4.71 | % | ||||

KKR & Co. LP | 4.56 | % | ||||

Conversus Capital LP | 4.43 | % | ||||

Eurazeo | 4.42 | % | ||||

Wendel Investissement | 4.38 | % | ||||

Blackstone Group LP | 4.30 | % | ||||

SVG Capital PLC | 3.78 | % | ||||

AP Alternative Assets LP | 3.74 | % | ||||

Onex Corp. | 3.73 | % | ||||

Electra Private Equity PLC | 3.58 | % | ||||

Top Ten Holdings | 41.63 | % | ||||

| † | Holdings are subject to change. |

Industry Sector Allocation (as a % of Net Assets)

| 12 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

| October 31, 2011 (Unaudited)

| |||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2011 and held until October 31, 2011.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges, redemption fees, or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 5/1/11 | Ending Account Value 10/31/11 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/11 - 10/31/11 | |||||||||||||

Class A | ||||||||||||||||

Actual | $ | 1,000.00 | $ | 765.50 | 1.50 | % | $ | 6.66 | ||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.60 | 1.50 | % | $ | 7.61 | ||||||||

Class C | ||||||||||||||||

Actual | $ | 1,000.00 | $ | 761.80 | 2.25 | % | $ | 9.96 | ||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,013.83 | 2.25 | % | $ | 11.39 | ||||||||

Class I | ||||||||||||||||

Actual | $ | 1,000.00 | $ | 766.60 | 1.25 | % | $ | 5.55 | ||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.85 | 1.25 | % | $ | 6.34 | ||||||||

Class R | ||||||||||||||||

Actual | $ | 1,000.00 | $ | 763.30 | 1.75 | % | $ | 7.76 | ||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,016.34 | 1.75 | % | $ | 8.87 | ||||||||

| (a) | The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 366. |

| 13 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

| October 31, 2011 (Unaudited)

| |||

| Shares | Value (Note 1) | |||||||

COMMON STOCKS (99.65%) |

| |||||||

Communications (5.31%) |

| |||||||

Internet (4.13%) |

| |||||||

Internet Capital Group, Inc.(a) | 207,000 | $2,233,530 | ||||||

Safeguard Scientifics, Inc.(a) | 199,000 | 3,365,090 | ||||||

|

| |||||||

| 5,598,620 | ||||||||

|

| |||||||

Telecommunications (1.18%) |

| |||||||

Softbank Corp. | 48,200 | 1,595,569 | ||||||

|

| |||||||

TOTAL COMMUNICATIONS | 7,194,189 | |||||||

|

| |||||||

Consumer, Non-cyclical (1.01%) |

| |||||||

Food (1.01%) |

| |||||||

Orkla ASA | 157,000 | 1,367,277 | ||||||

|

| |||||||

TOTAL CONSUMER, NON-CYCLICAL | 1,367,277 | |||||||

|

| |||||||

Diversified (11.04%) | ||||||||

Holding Companies-Diversified Operations (11.04%) |

| |||||||

Ackermans & van Haaren N.V. | 28,200 | 2,285,031 | ||||||

Leucadia National Corp. | 94,500 | 2,535,435 | ||||||

Remgro, Ltd. | 128,000 | 1,943,671 | ||||||

Schouw & Co. | 103,332 | 2,257,793 | ||||||

Wendel Investissement | 79,500 | 5,935,824 | ||||||

|

| |||||||

TOTAL DIVERSIFIED | 14,957,754 | |||||||

|

| |||||||

Financials (77.72%) |

| |||||||

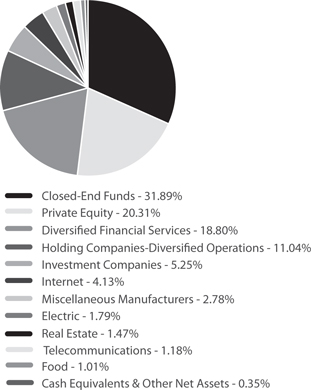

Closed-End Funds (31.89%) |

| |||||||

AP Alternative Assets LP | 524,835 | 5,064,658 | ||||||

ARC Capital Holdings, Ltd.(a) | 2,469,000 | 1,754,718 | ||||||

Candover Investments PLC(a) | 148,000 | 1,166,048 | ||||||

Castle Private Equity, Ltd.(a) | 212,000 | 2,089,086 | ||||||

Conversus Capital LP | 294,000 | 5,997,600 | ||||||

Electra Private Equity PLC(a) | 199,267 | 4,850,871 | ||||||

Graphite Enterprise Trust PLC | 574,797 | 3,484,290 | ||||||

HarbourVest Global Private Equity, Ltd.(a) | 94,000 | 629,800 | ||||||

HBM BioVentures AG, Class A(a) | 41,784 | 1,999,234 | ||||||

HgCapital Trust PLC | 154,648 | 2,541,287 | ||||||

HgCapital Trust PLC(a) | 57,520 | 106,239 | ||||||

Pantheon International Participations PLC(a) | 203,389 | 2,125,687 | ||||||

Pantheon International Participations PLC(a) | 129,000 | 1,306,739 | ||||||

Princess Private Equity Holding, Ltd. | 469,388 | 4,007,367 | ||||||

Standard Life European Private Equity Trust PLC | 482,308 | 946,113 | ||||||

SVG Capital PLC(a) | 1,515,000 | 5,125,271 | ||||||

|

| |||||||

| 43,195,008 | ||||||||

|

| |||||||

| Shares | Value (Note 1) | |||||||

Diversified Financial Services (18.80%) |

| |||||||

Blackstone Group LP | 395,700 | $5,820,747 | ||||||

GP Investments, Ltd.(a) | 748,000 | 2,021,563 | ||||||

Intermediate Capital Group PLC | 1,090,000 | 4,286,881 | ||||||

KKR & Co. LP | 458,000 | 6,173,840 | ||||||

Onex Corp. | 152,500 | 5,056,559 | ||||||

Partners Group Holding AG | 11,200 | 2,098,883 | ||||||

|

| |||||||

| 25,458,473 | ||||||||

|

| |||||||

Investment Companies (5.25%) |

| |||||||

LMS Capital PLC(a) | 1,322,446 | 1,254,551 | ||||||

Ratos AB, B Shares | 345,000 | 4,615,916 | ||||||

RHJ International SA(a) | 232,776 | 1,124,102 | ||||||

THL Credit, Inc. | 10,378 | 119,866 | ||||||

|

| |||||||

| 7,114,435 | ||||||||

|

| |||||||

Private Equity (20.31%) |

| |||||||

3i Group PLC | 1,930,000 | 6,380,268 | ||||||

Altamir Amboise(a) | 316,000 | 2,925,197 | ||||||

Apollo Global Management LLC, Class A | 219,000 | 2,901,750 | ||||||

Aurelius AG | 40,259 | 1,638,325 | ||||||

Bure Equity AB(a) | 359,000 | 1,063,100 | ||||||

Deutsche Beteiligungs AG | 81,900 | 1,756,538 | ||||||

Eurazeo | 124,800 | 5,989,606 | ||||||

GIMV N.V. | 75,200 | 3,844,804 | ||||||

IP Group PLC(a) | 902,376 | 1,015,650 | ||||||

|

| |||||||

| 27,515,238 | ||||||||

|

| |||||||

Real Estate (1.47%) |

| |||||||

Brookfield Asset Management, Inc., Class A | 68,800 | 1,995,200 | ||||||

|

| |||||||

TOTAL FINANCIALS | 105,278,354 | |||||||

|

| |||||||

Industrials (2.78%) |

| |||||||

Miscellaneous Manufacturers (2.78%) |

| |||||||

Fosun International, Ltd. | 6,563,000 | 3,767,761 | ||||||

|

| |||||||

TOTAL INDUSTRIALS | 3,767,761 | |||||||

|

| |||||||

Utilities (1.79%) |

| |||||||

Electric (1.79%) |

| |||||||

Brookfield Infrastructure Partners LP | 96,800 | 2,428,712 | ||||||

|

| |||||||

TOTAL UTILITIES | 2,428,712 | |||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $135,864,659) |

| 134,994,047 | ||||||

|

| |||||||

| 14 | October 31, 2011 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||||

Statement of Investments

| October 31, 2011 (Unaudited)

| |||

| 7-Day Yield | Shares | Value (Note 1) | |||||||||

SHORT TERM INVESTMENTS (0.24%) |

| |||||||||||

Money Market Fund (0.24%) |

| |||||||||||

Dreyfus Treasury Prime Cash Management, Investor Shares | 0.00004 | % | 322,282 | $322,282 | ||||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $322,282) |

| 322,282 | ||||||||||

|

| |||||||||||

TOTAL INVESTMENTS (99.89%) (Cost $136,186,941) |

| $ | 135,316,329 | |||||||||

Other Assets In Excess Of Liabilities (0.11%) |

| 148,485 | ||||||||||

|

| |||||||||||

NET ASSETS (100.00%) |

| $ | 135,464,814 | |||||||||

|

| |||||||||||

| (a) | Non-Income Producing Security. |

Common Abbreviations:

| AB | - Aktiebolag is the Swedish equivalent of the term corporation. |

| AG | - Aktiengesellschaft is a German term that refers to a corporation that is |

| limited | by shares, i.e., owned by shareholders. |

| ASA | - Allmennaksjeselskap is the Norwegian term for a public company. |

| LLC | - Limited Liability Company. |

| LP | - Limited Partnership. |

| Ltd. | - Limited. |

| N.V. | - Naamloze Vennootschap is the Dutch term for a public limited liability |

| corporation. |

| PLC | - Public Limited Company. |

| SA | - Generally designates corporations in various countries, mostly those |

| employing | the civil law. This translates literally in all languages |

| mentioned | as anonymous company. |

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/ or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

| 15 | October 31, 2011 |

Table of Contents

| October 31, 2011 (Unaudited)

| |||

Market Comment

Upheaval shook global asset markets during the period as prices for most risk assets fell sharply starting in late July. Investors transitioned from excitement over economic strength and the recovery in corporate earnings to apprehension over the risks to global growth. The primary catalysts behind this shift were the European sovereign debt crisis, US political gridlock, falling consumer confidence, and concerns over sustained growth in emerging markets. Markets rallied in the final month of the period as improving US economic data and optimism related to a resolution of the ongoing European debt crisis lifted investor sentiment, but this was not enough to offset negative returns earlier in the period.

Within the Russell 1000 Value Index, eight of ten sectors posted negative returns, with the traditionally defensive Utilities and Consumer Staples sectors managing gains. Materials -17.7%, Financials -17.1%, and Industrials -13.5% were the worst performing sectors for the period.

Fund Review

The Portfolio underperformed its benchmark for the period, posting positive relative results in two out of ten broad market sectors. Overall, stock selection was negative relative to the Russell 1000 Value Index, as decisions in Financials, Utilities, and Materials more than offset positive relative performance in Information Technology and Consumer Staples.

Detractors to performance for the period included Intel (Information Technology), Bank of America (Financials), and Hartford Financial Services (Financials). Intel, a leading manufacturer of semiconductors for computing and communications, rose over the period as solid global PC sales and the company’s manufacturing advantages were perceived positively by investors. Not owning the stock detracted from relative results. Bank of America, a large US-based multinational financial services firm, declined amid negative headlines regarding litigation uncertainty related to its ownership of Countrywide Financial. Hartford Financial Services, a provider of insurance and financial services products, declined over the period as the firm’s results disappointed due to higher-than-normal catastrophe losses and a large reserve charge.

Top contributors to relative performance included Citigroup (Financials), Apple (Information Technology), and Kimberly-Clark (Consumer Staples). Citigroup, a global financial services company, reduced estimates on higher expenses and saw continued growth weakness in securities/banking and domestic consumer banking. Not holding the stock during the period contributed to performance. Apple is a designer, manufacturer, and retailer of a range of personal electronics products. The company remains a dominant leader in personal communication devices, and we believe longer-term opportunities such as expanded distribution in China, an expanding tablet market, and the potential to enter the Smart TV market should continue to support outperformance in the stock. Kimberly-Clark, a global manufacturer of consumer products, benefited from the company’s relatively stable revenue and earnings profile in a weak market environment, as well as a modest pullback in pulp prices. Our overweight position contributed to performance during the period.

Outlook

Equity markets struggled for the period, and the overhangs that caused much of the market turmoil still exist. The European sovereign debt crisis and US budget deficit issues have raised concerns about the economy falling into a double dip recession. These fears are exacerbated by concerns surrounding the overall health of the banking system.

We believe that both the European sovereign debt crisis and the US budget deficit will eventually have positive outcomes. However, the combination of these two overhangs will likely mean that developed economies are going to grow at a slower pace than they have in the past. We believe emerging economies are in reasonably good health and should continue to grow. From a global perspective, considering both developed and emerging economies, economic growth could be similar to what it was in the past; the difference being that the growth is now coming from emerging markets and not from developed markets.

| 16 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Performance of $10,000 Initial Investment (as of October 31, 2011)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

Source: Morningstar

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| 17 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Average Annual Total Returns (as of October 31, 2011)

| 1 Year | 5 Year | 10 Year | Total Expense Ratio | What You Pay* | ||||||

Class A (NAV)1 | 4.76% | -2.07% | 3.75% | 1.71% | 1.40% | |||||

Class A (MOP)2 | -1.04% | -3.17% | 3.16% | |||||||

Class C (NAV)1 | 3.85% | -2.80% | 2.98% | 2.49% | 2.15% | |||||

Class C (CDSC)2 | 2.85% | -2.80% | 2.98% | |||||||

Class I | 5.01% | -1.86% | 3.91% | 1.46% | 1.15% | |||||

Russell 1000 Value Index3 | 6.16% | -2.05% | 4.57% | |||||||

S&P 500 Index4 | 8.09% | 0.25% | 3.69% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call (866) 759-5679.

Performance shown for Class C shares prior to June 30, 2010 reflects the historical performance of the Fund’s Class A shares, calculated using the fees and expenses of Class C shares.

The performance shown for the ALPS | WMC Value Intersection Fund (the “Fund”) for periods prior to August 29, 2009, reflects the performance of the Activa Mutual Funds Trust – Activa Value Fund (as result of a prior reorganization of Activa Mutual Funds Trust – Activa Value Fund into the Fund).

| 1 | Net Asset Value (NAV) is the share price without sales charges. |

| 2 | Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. CDSC performance for Class C shares includes a 1% CDSC on C shares redeemed within 12 months of purchase. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. |

| 3 | The Russell 1000 Value Index measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| 4 | The S&P 500 Index is the Standard & Poor’s composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| * | What You Pay reflects the Adviser’s decision to contractually limit expenses through August 31, 2012. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Mutual funds, annuities and other investments are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested. Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund’s original investment.

| 18 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

Management Commentary

| October 31, 2011 (Unaudited)

| |||

Top Ten Holdings (as a % of Net Assets) †

Chevron Corp. | 3.25 | % | ||||

Wells Fargo & Co. | 2.97 | % | ||||

JPMorgan Chase & Co. | 2.85 | % | ||||

Pfizer, Inc. | 2.75 | % | ||||

Merck & Co., Inc. | 2.67 | % | ||||

Cisco Systems, Inc. | 2.12 | % | ||||

AT&T, Inc. | 2.09 | % | ||||

Occidental Petroleum Corp. | 1.89 | % | ||||

Kimberly-Clark Corp. | 1.78 | % | ||||

Bank of America Corp. | 1.63 | % | ||||

Top Ten Holdings | 24.00 | % |

| † | Holdings are subject to change. |

Industry Sector Allocation (as a % of Net Assets)

| 19 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

| October 31, 2011 (Unaudited)

| |||

As a shareholder of the Fund, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads); and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2011 and held until October 31, 2011.

Actual Expenses. The first line of the table on the next page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expense Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table on the next page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing Fund costs only and do not reflect transaction fees, such as sales charges or exchange fees. Therefore, the second line of the table on the next page is useful in comparing ongoing costs only, and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 5/1/11 | Ending Account Value 10/31/11 | Expense Ratio(a) | Expense Paid During Period(b) 5/1/11 - 10/31/11 | |||||||||||||||||

Class A | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 881.90 | 1.40 | % | $ | 6.62 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.10 | 1.40 | % | $ | 7.10 | ||||||||||||

Class C | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 878.20 | 2.15 | % | $ | 10.15 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.33 | 2.15 | % | $ | 10.89 | ||||||||||||

Class I | ||||||||||||||||||||

Actual | $ | 1,000.00 | $ | 882.90 | 1.15 | % | $ | 5.44 | ||||||||||||

Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.36 | 1.15 | % | $ | 5.84 | ||||||||||||

| (a) | The Fund’s expense ratios have been based on the Fund’s most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), then divided by 366. |

| 20 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

| October 31, 2011 (Unaudited)

| |||

| Shares | Value (Note 1) | ||||||

COMMON STOCKS (97.97%) |

| |||||||

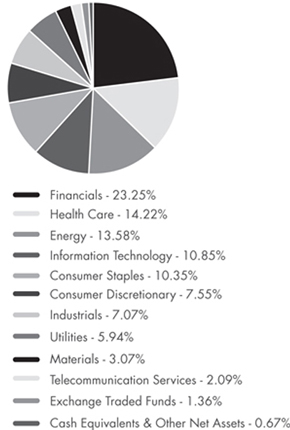

Consumer Discretionary (7.55%) |

| |||||||

Automobiles & Components (1.73%) |

| |||||||

Ford Motor Co.(a) | 55,200 | $644,736 | ||||||

TRW Automotive Holdings | 12,820 | 539,722 | ||||||

|

| |||||||

| 1,184,458 | ||||||||

|

| |||||||

Consumer Durables & Apparel (1.06%) |

| |||||||

PVH Corp. | 9,680 | 720,289 | ||||||

|

| |||||||

Consumer Services (0.82%) |

| |||||||

Carnival Corp. | 15,990 | 563,008 | ||||||

|

| |||||||

Media (1.07%) |

| |||||||

News Corp., Class A | 41,500 | 727,080 | ||||||

|

| |||||||

Retailing (2.87%) |

| |||||||

Abercrombie & Fitch Co., Class A | 8,660 | 644,304 | ||||||

Lowe’s Cos., Inc. | 28,270 | 594,235 | ||||||

TJX Cos., Inc. | 12,260 | 722,482 | ||||||

|

| |||||||

| 1,961,021 | ||||||||

|

| |||||||

TOTAL CONSUMER DISCRETIONARY |

| 5,155,856 | ||||||

|

| |||||||

Consumer Staples (10.35%) |

| |||||||

Food & Staples Retailing (1.27%) |

| |||||||

CVS Caremark Corp. | 23,930 | 868,659 | ||||||

|

| |||||||

Food Beverage & Tobacco (6.12%) |

| |||||||

Altria Group, Inc. | 32,140 | 885,457 | ||||||

Dr Pepper Snapple Group, Inc. | 15,630 | 585,343 | ||||||

The JM Smucker Co. | 10,060 | 774,821 | ||||||

Lorillard, Inc. | 9,400 | 1,040,204 | ||||||

Philip Morris International, Inc. | 12,785 | 893,288 | ||||||

|

| |||||||

| 4,179,113 | ||||||||

|

| |||||||

Household & Personal Products (2.96%) |

| |||||||

Energizer Holdings, Inc.(a) | 10,850 | 800,622 | ||||||

Kimberly-Clark Corp. | 17,440 | 1,215,742 | ||||||

|

| |||||||

| 2,016,364 | ||||||||

|

| |||||||

TOTAL CONSUMER STAPLES |

| 7,064,136 | ||||||

|

| |||||||

| Shares | Value (Note 1) | ||||||

Energy (13.58%) |

| |||||||

Energy (13.58%) |

| |||||||

Anadarko Petroleum Corp. | 13,200 | $1,036,200 | ||||||

Baker Hughes, Inc. | 12,000 | 695,880 | ||||||

Chesapeake Energy Corp. | 21,500 | 604,580 | ||||||

Chevron Corp. | 21,119 | 2,218,551 | ||||||

Exxon Mobil Corp. | 12,564 | 981,123 | ||||||

Hess Corp. | 11,100 | 694,416 | ||||||

Marathon Oil Corp. | 24,700 | 642,941 | ||||||

Marathon Petroleum Corp. | 12,350 | 443,365 | ||||||

National Oilwell Varco, Inc. | 9,275 | 661,585 | ||||||

Occidental Petroleum Corp. | 13,900 | 1,291,866 | ||||||

|

| |||||||

TOTAL ENERGY | 9,270,507 | |||||||

|

| |||||||

Financials (23.25%) |

| |||||||

Banks (6.59%) |

| |||||||

BB&T Corp. | 27,610 | 644,418 | ||||||

PNC Financial Services Group, Inc. | 13,400 | 719,714 | ||||||

US Bancorp | 43,270 | 1,107,279 | ||||||

Wells Fargo & Co. | 78,200 | 2,026,162 | ||||||

|

| |||||||

| 4,497,573 | ||||||||

|

| |||||||

Diversified Financials (10.18%) |

| |||||||

Ameriprise Financial, Inc. | 20,400 | 952,272 | ||||||

Bank of America Corp. | 162,862 | 1,112,347 | ||||||

BlackRock, Inc. | 1,900 | 299,801 | ||||||

The Goldman Sachs Group, Inc. | 9,880 | 1,082,354 | ||||||

Invesco, Ltd. | 28,200 | 565,974 | ||||||

JPMorgan Chase & Co. | 55,900 | 1,943,084 | ||||||

The NASDAQ OMX Group, Inc.(a) | 23,020 | 576,651 | ||||||

SLM Corp. | 30,500 | 416,935 | ||||||

|

| |||||||

| 6,949,418 | ||||||||

|

| |||||||

Insurance (5.50%) |

| |||||||

ACE, Ltd. | 15,300 | 1,103,895 | ||||||

Allied World Assurance Co. Holdings, Ltd. | 8,900 | 517,090 | ||||||

Hartford Financial Services Group, Inc. | 34,860 | 671,055 | ||||||

MetLife, Inc. | 14,000 | 492,240 | ||||||

Prudential Financial, Inc. | 11,400 | 617,880 | ||||||

Unum Group | 14,800 | 352,832 | ||||||

|

| |||||||

| 3,754,992 | ||||||||

|

| |||||||

Real Estate (0.98%) |

| |||||||

Forest City Enterprises, Inc., Class A(a) | 49,100 | 671,688 | ||||||

|

| |||||||

TOTAL FINANCIALS | 15,873,671 | |||||||

|

| |||||||

| 21 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

Statement of Investments

| October 31, 2011 (Unaudited)

| |||

| Shares | Value (Note 1) | ||||||

Health Care (14.22%) |

| |||||||

Health Care Equipment & Services (4.06%) |

| |||||||

Aetna, Inc. | 15,700 | $624,232 | ||||||

Covidien PLC | 12,030 | 565,891 | ||||||

McKesson Corp. | 5,970 | 486,853 | ||||||

UnitedHealth Group, Inc. | 22,830 | 1,095,612 | ||||||

|

| |||||||

| 2,772,588 | ||||||||

|

| |||||||

Pharmaceuticals, Biotechnology & Life Sciences (10.16%) |

| |||||||

Amgen, Inc. | 16,190 | 927,201 | ||||||

Forest Laboratories, Inc.(a) | 12,228 | 382,737 | ||||||

Gilead Sciences, Inc.(a) | 9,510 | 396,187 | ||||||

Merck & Co., Inc. | 52,870 | 1,824,015 | ||||||

Pfizer, Inc. | 97,623 | 1,880,219 | ||||||

Thermo Fisher Scientific, | 13,760 | 691,715 | ||||||

Watson Pharmaceuticals, Inc.(a) | 12,450 | 836,142 | ||||||

|

| |||||||

| 6,938,216 | ||||||||

|

| |||||||

TOTAL HEALTH CARE |

| 9,710,804 | ||||||

|

| |||||||

Industrials (7.07%) |

| |||||||

Capital Goods (6.03%) |

| |||||||

3M Co. | 5,980 | 472,540 | ||||||

The Boeing Co. | 8,070 | 530,925 | ||||||

Caterpillar, Inc. | 6,080 | 574,317 | ||||||

Dover Corp. | 10,150 | 563,629 | ||||||

Northrop Grumman Corp. | 10,400 | 600,600 | ||||||

Parker Hannifin Corp. | 6,270 | 511,319 | ||||||

United Technologies Corp. | 11,050 | 861,679 | ||||||

|

| |||||||

| 4,115,009 | ||||||||

|

| |||||||

Commercial & Professional Services (1.04%) |

| |||||||

Towers Watson & Co., Class A | 10,830 | 711,531 | ||||||

|

| |||||||

TOTAL INDUSTRIALS | 4,826,540 | |||||||

|

| |||||||

Information Technology (10.85%) |

| |||||||

Semiconductors & Semiconductor Equipment (0.51%) |

| |||||||

Xilinx, Inc. | 10,420 | 348,653 | ||||||

|

| |||||||

Software & Services (6.98%) |

| |||||||

Accenture PLC, Class A | 12,310 | 741,801 | ||||||

Activision Blizzard, Inc. | 46,150 | 617,948 | ||||||

eBay, Inc.(a) | 25,550 | 813,256 | ||||||

Oracle Corp. | 18,780 | 615,421 | ||||||

Solera Holdings, Inc. | 9,430 | 515,161 | ||||||

Teradata Corp.(a) | 8,080 | 482,053 | ||||||

Visa, Inc., Class A | 6,440 | 600,594 | ||||||

The Western Union Co. | 21,680 | 378,750 | ||||||

|

| |||||||

| 4,764,984 | ||||||||

|

| |||||||

| Shares | Value (Note 1) | ||||||

Technology Hardware & Equipment (3.36%) |

| |||||||

Apple, Inc.(a) | 2,090 | $845,990 | ||||||

Cisco Systems, Inc. | 78,280 | 1,450,529 | ||||||

|

| |||||||

| 2,296,519 | ||||||||

|

| |||||||

TOTAL INFORMATION TECHNOLOGY |

| 7,410,156 | ||||||

|

| |||||||

Materials (3.07%) |

| |||||||

Materials (3.07%) |

| |||||||

The Dow Chemical Co. | 37,788 | 1,053,530 | ||||||

The Mosaic Co. | 6,520 | 381,811 | ||||||

Newmont Mining Corp. | 9,871 | 659,679 | ||||||

|

| |||||||

TOTAL MATERIALS |

| 2,095,020 | ||||||

|

| |||||||

Telecommunication Services (2.09%) |

| |||||||

Telecommunication Services (2.09%) |

| |||||||

AT&T, Inc. | 48,675 | 1,426,664 | ||||||

|

| |||||||

TOTAL TELECOMMUNICATION SERVICES |

| 1,426,664 | ||||||

|

| |||||||

Utilities (5.94%) |

| |||||||

Utilities (5.94%) |

| |||||||

American Electric Power Co., Inc | 21,600 | 848,448 | ||||||

NextEra Energy, Inc. | 19,030 | 1,073,292 | ||||||

PG&E Corp. | 25,240 | 1,082,796 | ||||||

Xcel Energy, Inc. | 40,680 | 1,051,578 | ||||||

|

| |||||||

TOTAL UTILITIES | 4,056,114 | |||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $61,391,960) |

| 66,889,468 | ||||||

|

| |||||||

EXCHANGE TRADED FUNDS (1.36%) |

| |||||||

Equity Fund (1.36%) |

| |||||||

iShares® Russell 1000® Value Index Fund | 14,710 | 927,759 | ||||||

|

| |||||||

TOTAL EXCHANGE TRADED FUNDS (Cost $878,021) |

| 927,759 | ||||||

|

| |||||||

7-Day Yield | Shares | Value (Note 1) | ||||||

SHORT TERM INVESTMENTS (0.25%) |

| |||||||

Money Market Fund (0.25%) |

| |||||||

Fidelity Institutional Money Market Portfolio - Class I 0.149% | 169,609 | 169,609 | ||||||

|

| |||||||

TOTAL SHORT TERM INVESTMENTS (Cost $169,609) |

| 169,609 | ||||||

|

| |||||||

| 22 | October 31, 2011 |

Table of Contents

ALPS | WMC Value Intersection Fund | ||||

Statement of Investments

| October 31, 2011 (Unaudited)

| |||

| Value (Note 1) | |||

TOTAL INVESTMENTS (99.58%) (Cost $62,439,590) | $ | 67,986,836 | ||

Other Assets In Excess Of Liabilities (0.42%) | 286,409 | |||

|

| |||

NET ASSETS (100.00%) | $ | 68,273,245 | ||

|

| |||

| (a) | Non-Income Producing Security. |

Common Abbreviations:

Ltd. - Limited.

PLC - Public Limited Company.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry subclassifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

| 23 | October 31, 2011 |

Table of Contents

| October 31, 2011 (Unaudited)

| |||

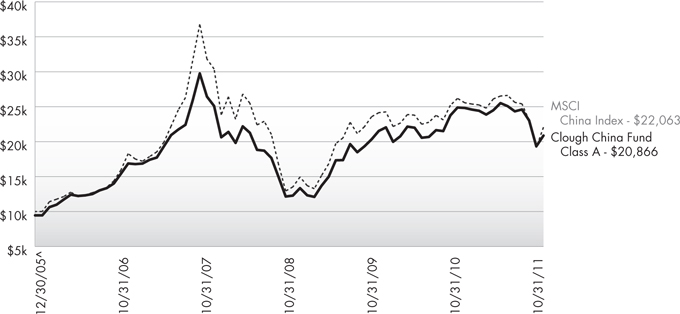

During the six month period under review ending October 31, the Clough Capital China Fund fell 18.11% or roughly in line with the MSCI China index which declined 18.50% over the same period.

Investment Environment

With investors becoming more and more concerned about the financial turmoil in Europe and the US economic recovery being hampered by high unemployment, fears of global contagion and risk aversion severely pressured stock markets all around the world. China was no exception particularly as specific concerns over Chinese economic growth and the health of its financial system emerged. The fact that some of these concerns were sometimes contradictory added to market’s volatility. For instance, doubts on the government’s ability to rein in inflation and property price increases were quickly replaced by fears that Beijing’s policy tightening was too harsh, and that a sharp slowdown in economic growth due to lower external demand depressing exports and delayed capital spending on infrastructure projects such as new nuclear power plants, after the Fukushima disaster in Japan, and high speed railway expansion, post the train accident last July would trigger an economic “hard landing”. Reports of investment trust financing of real estate projects also grabbed market attention and spread concerns over “shadow” banking and the opacity of real debts in the system. The challenges faced by many small and midsize enterprises (SMEs) to secure access to bank lending – not a new problem, but one that became more acute recently – further undermined sentiment for equities.

In fact, we see this as the primary issue hampering Chinese equity markets. Investor sentiment is extremely poor at present, dominated by macro fears while corporate fundamentals are seemingly disregarded. Trading volumes have been weak and mainly made up of derivatives and warrants while institutional interest remains low and “real” investors either defensively withdraw funds or remain on the side lines.

In terms of sectors, all cyclical industries such as steel, cement, but also financials and property were the major victims of the market downturn. Lately, some consumer related equities also declined after some reports by retailers that consumers had become a bit more cautious in their daily spending, in particular on luxury goods.

The Clough China Fund was consistently underweight banks, cyclical and property stocks during the period under review, whereas we continued to focus on our consumption themes by overweighting the consumer sector.

Looking at individual stocks, the three major positive contributors to the Fund’s performance were China Telecom, Lenovo and China Shenhua. China Telecom is China’s largest

wireline telephone company gradually penetrating mobile telecom and data system areas. It is recording strong 2G and 3G wireless subscriber additions. The rapidly growing wireless business is driving revenue acceleration. Earnings growth is well supported by cost control and a strong management team. The telecom sector also benefited from being considered as defensive. Lenovo, the world’s third largest personal computer vendor behind HP and Dell, is the fastest growing PC company in the world. We believe a dominant position in fast growing China and the Emerging Markets should vault Lenovo to second place in terms of global market share by year end. Rapid revenue growth and improving margins have driven earnings above market expectations and should serve to support a higher valuation for this company, which also supports a strong balance sheet with net cash equivalent to more than 50% of its market capitalization. China Shenhua, the largest thermal coal producer in China, benefits from a fully integrated business model, including mining, coal trading, railway network, power generation and port facilities. The company generates strong cash flow and high profit margins. Attractive coal industry fundamentals and a high quality management team support good visibility for Shenhua’s profit outlook.