Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8194

FINANCIAL INVESTORS TRUST

(exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

David T. Buhler, Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: May 1, 2012 - October 31, 2012

Table of Contents

| Item 1. | Reports to Stockholders. |

Table of Contents

Table of Contents

| 1 | ||||

| 5 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| 13 | ||||

| 17 | ||||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 22 | ||||

| 26 | ||||

| 29 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 38 | ||||

| 42 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 48 | ||||

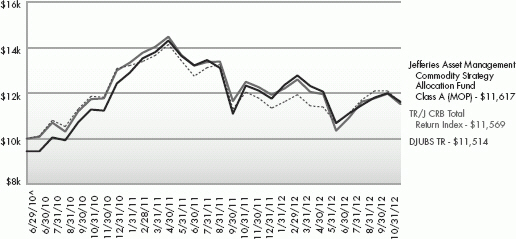

Jefferies Asset Management Commodity Strategy Allocation Fund | ||||

| 54 | ||||

| 57 | ||||

| 61 | ||||

| 62 | ||||

| 63 | ||||

| 64 | ||||

| 67 | ||||

| 79 | ||||

| 91 | ||||

| 93 | ||||

| 94 | ||||

| 99 | ||||

| 116 | ||||

| 138 | ||||

| 142 | ||||

Table of Contents

| October 31, 2012 (Unaudited) |

Performance

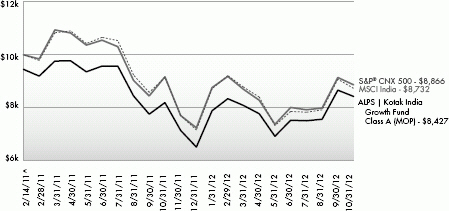

The ALPS | Kotak India Growth Fund’s (the “Fund”) Class A Shares, INDAX, during the 6-month period ended 10/31/2012, delivered a net return of 8.39% at Net Asset Value (Class A delivered a net return of 2.41% at MOP, Class C, INFCX, was 6.98% with CDSC, Class I, INDIX, was 8.61%). The Fund’s performance was above that of the S&P® CNX 500 Index (“CNX 500”) -5.53%, over the same period, without taking into account sales charges for Class A and C Shares.

During the period, the Indian equity markets rallied along with the global markets with broader Indian indices like CNX 500 returning 5.53%, S&P® CNX Nifty Index (“Nifty”)7 returning 4.75% and S&P® CNX Midcap Index (“CNX MIDCAP”)8 returning 1.65% (all in United States Dollar (“USD”) terms). The investment environment during this period was impacted by the factors described below, with May and September marking the worst and best monthly change respectively (CNX 500 returned -12.49% in May, 8.23% in June, -1.38% in July, 0.61% in August, 14.35% in September, and -3.07% in October).

| « | Global equity markets rallied in the period with tension in Euro-area countries subsiding as the European Central Bank unveiled the European Stability Mechanism. In the U.S., the Fed’s announcement of the third and open ended Quantitative Easing (QE) focusing on Mortgage Backed Securities and extension of operation twist1 until December 2012 also added to market optimism. In India, the announcement of several key reforms activities and strong FII (Foreign Institutional Investor) flows of around USD 9.4 billion during the period helped the performance of the Indian equity market and counter the weakness seen at the beginning of the period due to uncertainty on the GAAR2 (General Anti-Avoidance Rule) issue. |

| « | During the period, the Reserve Bank of India (RBI) cut the Cash Reserve Ratio (CRR), refraining from cutting interest rates (Repo3 and Reverse repo rate4 is maintained at 8% and 7% respectively). Thus, in the period, RBI cuts CRR by 25 basis points5 (bps), bringing CRR to 4.50% on its 09/17/2012 policy meeting. The CRR cut will inject Indian Rupee (INR) 170 billion to the banking system. RBI clearly has been worried on the inflation front and has refrained from cutting rates on that account. The policy document states a few times that the rate cuts in April were front loaded in nature and were a result of the anticipated changes with respect to containment of the fiscal deficit. We continue to expect the RBI to cut interest rate to the cumulative of 50bps for Financial Year (FY) 2013, with rate cut likely to happen from January onwards. |

| « | For the quarter ending June 2012 (Q1FY13), real GDP growth came in at 5.5%, higher than previous quarter number of 5.3% and Bloomberg consensus expectation of 5.2%. Agriculture (2.9% year-on-year) and Construction (10.9% YoY) growth within the Industry category (3.6% YoY) came in as a positive surprise while Services (6.9% YoY v/s 7.9% in previous quarter) growth fell to the lowest since March 2009. Currently Services sector contribute nearly 60% to India GDP followed by Industry (27%) and Agriculture (13%). Post these numbers, we expect the full year FY13 GDP growth to be at best 5.7% and see a potential downward revision in future to the central bank’s estimate of 6.5%. |

| « | The period also saw the INR appreciating in the month of September with strong FII flow, announcement of major reforms activities, and announcement of open-ended QE3 in U.S. Nevertheless, the INR fell back in the month of October due to worsening global risk sentiment and RBI’s macroeconomic assessment where RBI lowered its GDP estimate for FY13 to 5.8% (v/s 6.5% earlier) while increased its inflation estimate for FY13 to 7.5% (v/s 7% earlier). |

| « | India inflation number (Wholesale price Index - WPI) averaged to 7.6% during the period with the October inflation number standing at 7.45% (v/s September’s 7.8%), better than the Bloomberg consensus expectation of 7.9%. All three broad components - primary articles, fuel and power, and manufactured product inflation - rose at slower pace than September’s. Core inflation also slowed down to a 4-month low at 5.2% (v/s September’s 5.6%) while food inflation also fell substantially. |

| « | The Government also announced several key reforms activities during the period. In May, the Government finally hiked petrol prices by INR 7.5/liter or around 10% (highest ever) with a follow up on diesel price (INR 5 hike or around 12%) in September. Besides that, in September, the Government also announced series of major reforms activities, surprising the market on the upside. The Government announced the opening of Foreign Direct Investment (FDI) in Multi Brand Retailing (up to 51%), Aviation (up to 49%), Broadcasting (49% to 74%), and Power-Trading Exchanges (up to 49%). In addition, the Government also announced divestment plan which will see the Government divest its holding in MMTC, Oil India, Nalco, and Hindustan Copper. The divestments are expected to cover around half of the divestment plan announced in the union budget last March (INR 300 billion). In October, reforms activities continue with the announcement of FDI in insurance companies (up to 49%) and pension funds (up to 26%). |

| « | The period also saw changes in Finance Ministry of the Government of India. Mr. P. Chidambaram came back as Finance Minister after replacing Mr. Pranab Mukherjee who left the post to become the 13th President of India in July. This has raised expectations of the economic reforms process getting stepped up with some of them eventually materialized in September. |

| « | The Indian Corporate earnings during the period were mixed, with Q2FY13 (quarter ending September 2012) result showing some improvement as compared to previous quarter. The results showed that the Profit after tax growth was led by Cement, Technology, Health Care, and Private Sector Banks. In addition, Technology, Capital Goods & Engineering, and Auto results were mixed. Public sector banks continued to surprise negatively on the asset quality side while Oil & Gas and Telecom sector reported a decline in profits. |

Fund Composition

The Fund is constructed to potentially benefit from the strong macro-economic growth in the Indian economy across four broad themes in India – Consumption led by favorable demographics, Financial Services, Infrastructure and Outsourcing. The Fund has

1 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

Management Commentary | October 31, 2012 (Unaudited) |

the flexibility to invest across market capitalizations – depending on market conditions, valuation differential, earnings growth, liquidity, etc.

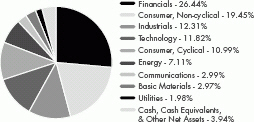

For the 6-month period ending October 31, 2012, sectorally the key changes to the portfolio have been in Capital Goods & Engineering (added 170bps), Auto & Auto Ancillary (added 120bps), Fast Moving Consumer Goods (added 90bps), Banking & Finance (reduced 180bps), Utilities (reduced 140bps), and Infrastructure (reduced 160bps). Thematically, Consumption (at about 34%) and Financials (at about 24%) are the largest themes in the Fund while infrastructure exposure is less than 9% due to poor policy initiatives by the Government. Over the last 6 months, exposure to midcap and small-cap companies in the Fund has moved marginally from 26.25% in April 2012 to 25.69% in October 2012.

Sectorally, the Fund is overweight Pharmaceutical, Information Technology, and Durables while underweight Oil & Gas, Banking & Finance, and Fast Moving Consumer Goods as of 10/31/2012.

Outlook

Post the result season, attention will once again be on further reforms initiatives by the Government. Thus, the winter session in parliament beginning 11/22/2012 will have important implications on the ability of the Government to pass through key reforms. Failure to do so may increase the speculation of an early election in India. The progress of the 2G telecom auctions would also be keenly watched by the market. While the recent credit policy indicated a status quo on policy rates, we continue to expect the RBI to cut interest rate by another 50bps in stages for FY13 starting January 2013.

The U.S. presidential election outcome and the subsequent discussion on fiscal cliff6 may also have a bearing on global markets and may determine the global risk-on/risk-off mode in the near future which would have an implication on emerging market inflows. All these factors would contribute to some volatility in the interim.

We believe we are positioned to capture any positive momentum in the market and also the Fund construction with exposures to Defensive sectors will ensure limited downside in case of any global risk-off affecting Indian markets. As of 10/31/2012, the S&P® CNX 500 Index is trading at 13.91x FY13 and 11.93x FY14 Earnings Per Share (EPS) respectively. S&P® CNX Nifty Index is trading at 14.5x FY13 and 12.82x FY14 EPS respectively. S&P® CNX Midcap Index is trading at 12.01x FY13 and 9.76x FY14 EPS, respectively. With valuations still near long term average and with the confidence building measures through pro reforms policy initiated by the Government, we believe India would continue to remain one of the attractive markets for long term investment.

| 1 | Operation Twist is a program conducted by the U.S. Federal Reserve in late 2011 and 2012 to help stimulate the economy. Operation Twist is the nickname for the Fed’s initiative of buying longer-term Treasuries and simultaneously selling some of the shorter-dated issues it already held in order to bring down long-term interest rates. No additional money printing occurred for this. |

| 2 | Tax Avoidance is an area of concern across the world. The rules are framed in different countries to minimize such avoidance of tax. Such rules in simple terms are known as “General Anti Avoidance Rules” or GAAR. Thus GAAR is a set of general rules enacted so as to check the tax avoidance. |

| 3 | The rate at which the RBI lends money to commercial banks is called repo rate. |

| 4 | The rate at which the RBI borrows money from commercial banks.is called the Reverse Repo rate. |

| 5 | Basis Points or bps is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. |

| 6 | Fiscal Cliff is a term used to describe the situation that the U.S. government will face at the end of 2012, when the terms of the Budget Control Act of 2011 are scheduled to go into effect. Fiscal cliff is an USD600bn automatic tax increase and spending cuts to reduce U.S. fiscal deficit that will take effect on 1st Jan 2013 should Congress not act. The U.S. Congressional Budget Office estimated that if no changes are made, there is a high probability that U.S. will fall into recession in 2013. |

| 7 | The S&P CNX 500 is India’s first broad based benchmark of the Indian capital market. The S&P CNX 500 companies are disaggregated into 72 industry indices. Industry weightages in the index reflect the industry weightages in the market. An investor may not invest directly in an index. |

| 8 | The CNX Midcap Index is a free float capitalization-weighted index designed to represent the midcap segment of the market in India. The index was developed with a base value of 1000 as of January 1, 2003. This index replaces the old CNX Midcap 200 Index which was discontinued effective July 18, 2005. |

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Kotak Mahindra (UK) Limited does not accept any liability for losses either direct or consequential caused by the use of this information.

| 2 | October 31, 2012 |

Table of Contents

ALPS | Kotak India Growth Fund | ||

Management Commentary | October 31, 2012 (Unaudited) |

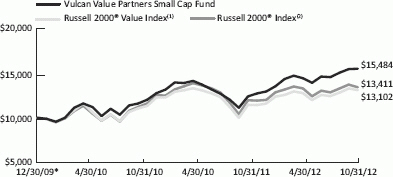

Performance of $10,000 Initial Investment (for the period ended October 31, 2012)

Comparison of change in value of a $10,000 investment (includes applicable sales loads of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

3 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

Management Commentary | October 31, 2012 (Unaudited) |

Average Annual Total Returns (as of October 31, 2012)

| 1 Year | Since Inception ^ | Total Expense Ratio | What you Pay * | |||||

Class A (NAV)1 | 2.84% | -6.49% | 12.50% | 2.00% | ||||

Class A (MOP)2 | -2.76% | -9.52% | ||||||

Class C (NAV)1 | 2.16% | -7.16% | 13.10% | 2.60% | ||||

Class C (CDSC)2 | 1.16% | -7.16% | ||||||

Class I | 3.18% | -6.18% | 12.10% | 1.60% | ||||

S&P® CNX 500 Index3 | -3.06% | -9.03% | ||||||

MSCI India Index Total Return4 | -4.74% | -7.62% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% to shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance shown does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data please call 1-866-759-5679.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested. Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the funds original investment.

| 1 | Net Asset Value (NAV) is the share price without sales charges. |

| 2 | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%; Class C returns include the 1.00% CDSC. |

| 3 | S&P® CNX 500 - India’s first broad based benchmark of the Indian capital market. The S&P® CNX 500 companies are disaggregated into 72 industry indices. Industry weightages in the market. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| 4 | MSCI India Index - a free float weighted equity index. It was developed with a base value of 100 as-of December 31,1992. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of February 14, 2011. |

| * | What You Pay reflects the Advisor’s and Sub-Advisor’s decision to contractually limit expenses through August 31, 2013. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

This Fund is not suitable for all investors and is subject to investment risks, including possible loss of the principal amount invested.

Mutual funds are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

Investing in India involves risk and considerations not present when investing in more established securities markets. The Fund may be more susceptible to economic, market, political and local risks of the region than a fund that is more geographically diversified.

Top Ten Long Holdings (as a % of Net Assets)†

|

| |||

ICICI Bank, Ltd. | 5.49 | % | ||

HDFC Bank, Ltd. | 5.24 | % | ||

ITC, Ltd. | 4.71 | % | ||

Infosys, Ltd. | 4.14 | % | ||

Reliance Industries, Ltd. | 3.93 | % | ||

Larsen & Toubro, Ltd. | 3.12 | % | ||

Housing Development Finance Corp. | 2.54 | % | ||

Tata Consultancy Services, Ltd. | 2.33 | % | ||

State Bank of India | 2.30 | % | ||

Tata Motors, Ltd. | 2.03 | % | ||

Top Ten Holdings | 35.83 | % | ||

| † | Holdings are subject to change. Table presents indicative values only. |

Industry Sector Allocation

(as a % of Net Assets)

4 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

| Consolidated Statement of Investments | October 31, 2012 (Unaudited) |

| Shares | Value (Note 2) | |||||||

COMMON STOCKS (96.06%) |

| |||||||

Basic Materials (2.97%) |

| |||||||

Mining (2.97%) | ||||||||

Hindalco Industries, Ltd. | 27,497 | $59,204 | ||||||

Hindustan Zinc, Ltd. | 22,610 | 56,075 | ||||||

Sterlite Industries India, Ltd. | 30,357 | 55,925 | ||||||

|

| |||||||

| 171,204 | ||||||||

|

| |||||||

TOTAL BASIC MATERIALS |

| 171,204 | ||||||

|

| |||||||

Communications (2.99%) |

| |||||||

Media (1.64%) | ||||||||

Dish TV India, Ltd.(a) | 40,495 | 56,628 | ||||||

Sun TV Network, Ltd. | 6,200 | 37,854 | ||||||

|

| |||||||

| 94,482 | ||||||||

|

| |||||||

Telecommunications (1.35%) |

| |||||||

Bharti Airtel, Ltd. | 15,647 | 78,215 | ||||||

|

| |||||||

TOTAL COMMUNICATIONS |

| 172,697 | ||||||

|

| |||||||

Consumer, Cyclical (10.99%) |

| |||||||

Apparel (1.18%) | ||||||||

Bata India, Ltd. | 4,315 | 68,360 | ||||||

|

| |||||||

Auto Manufacturers (4.70%) |

| |||||||

Bajaj Auto, Ltd. | 1,780 | 59,971 | ||||||

Mahindra & Mahindra, Ltd. | 5,762 | 94,318 | ||||||

Tata Motors, Ltd. | 24,611 | 117,054 | ||||||

|

| |||||||

| 271,343 | ||||||||

|

| |||||||

Auto Parts & Equipment (1.67%) |

| |||||||

Motherson Sumi Systems, Ltd. | 33,310 | 96,181 | ||||||

|

| |||||||

Home Builders (1.12%) |

| |||||||

Sobha Developers, Ltd. | 9,762 | 64,929 | ||||||

|

| |||||||

Home Furnishings (1.24%) |

| |||||||

TTK Prestige, Ltd. | 1,205 | 71,587 | ||||||

|

| |||||||

Textiles (1.08%) |

| |||||||

Raymond, Ltd. | 8,803 | 62,348 | ||||||

|

| |||||||

TOTAL CONSUMER, CYCLICAL |

| 634,748 | ||||||

|

| |||||||

Consumer, Non-cyclical (19.45%) |

| |||||||

Agriculture (4.71%) |

| |||||||

ITC, Ltd. | 51,865 | 271,866 | ||||||

|

| |||||||

Commercial Services (1.03%) |

| |||||||

Info Edge India, Ltd. | 9,185 | 59,681 | ||||||

|

| |||||||

| Shares | Value (Note 2) | |||||||

Food (2.74%) | ||||||||

Britannia Industries, Ltd. | 7,150 | $64,283 | ||||||

GlaxoSmithKline Consumer Healthcare, Ltd. | 1,663 | 93,724 | ||||||

|

| |||||||

| 158,007 | ||||||||

|

| |||||||

Household Products & Wares (2.64%) |

| |||||||

Hindustan Unilever, Ltd. | 9,246 | 93,753 | ||||||

Marico, Ltd. | 15,044 | 58,450 | ||||||

|

| |||||||

| 152,203 | ||||||||

|

| |||||||

Pharmaceuticals (8.33%) |

| |||||||

Cadila Healthcare, Ltd. | 3,790 | 61,299 | ||||||

Cipla, Ltd. | 9,318 | 62,872 | ||||||

Divi’s Laboratories, Ltd. | 2,807 | 62,627 | ||||||

Dr. Reddy’s Laboratories, Ltd. | 2,748 | 89,514 | ||||||

Glenmark Pharmaceuticals, Ltd. | 8,832 | 70,309 | ||||||

Lupin, Ltd. | 7,378 | 77,564 | ||||||

Sun Pharmaceutical Industries, Ltd. | 4,415 | 56,868 | ||||||

|

| |||||||

| 481,053 | ||||||||

|

| |||||||

TOTAL CONSUMER, NON-CYCLICAL |

| 1,122,810 | ||||||

|

| |||||||

Energy (7.11%) | ||||||||

Oil & Gas (7.11%) | ||||||||

Cairn India, Ltd.(a) | 11,693 | 72,956 | ||||||

Oil & Natural Gas Corp., Ltd. | 22,229 | 110,708 | ||||||

Reliance Industries, Ltd. | 15,199 | 226,787 | ||||||

|

| |||||||

| 410,451 | ||||||||

|

| |||||||

TOTAL ENERGY |

| 410,451 | ||||||

|

| |||||||

Financials (26.44%) |

| |||||||

Banks (19.13%) | ||||||||

Axis Bank, Ltd. | 4,439 | 97,022 | ||||||

HDFC Bank, Ltd. | 25,777 | 302,729 | ||||||

ICICI Bank, Ltd. | 16,289 | 317,004 | ||||||

IndusInd Bank, Ltd. | 15,852 | 106,956 | ||||||

State Bank of India | 3,399 | 132,703 | ||||||

Union Bank of India | 23,672 | 85,760 | ||||||

Yes Bank, Ltd. | 8,201 | 62,608 | ||||||

|

| |||||||

| 1,104,782 | ||||||||

|

| |||||||

Diversified Financial Services (5.15%) |

| |||||||

Bajaj Finance, Ltd. | 3,474 | 83,045 | ||||||

Housing Development Finance Corp. | 10,389 | 146,661 | ||||||

Shriram Transport Finance Co., Ltd. | 5,825 | 67,463 | ||||||

|

| |||||||

| 297,169 | ||||||||

|

| |||||||

Investment Companies (1.17%) |

| |||||||

Bajaj Holdings and Investment, Ltd. | 4,202 | 67,757 | ||||||

|

| |||||||

5 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

Consolidated Statement of Investments | October 31, 2012 (Unaudited) |

| Shares | Value (Note 2) | |||||||

Real Estate (0.99%) |

| |||||||

DLF, Ltd. | 15,245 | $57,150 | ||||||

|

| |||||||

TOTAL FINANCIALS | 1,526,858 | |||||||

|

| |||||||

Industrials (12.31%) |

| |||||||

Building Materials (4.29%) |

| |||||||

Century Textiles & Industries, Ltd. | 9,806 | 70,278 | ||||||

India Cements, Ltd. | 40,300 | 71,309 | ||||||

Shree Cement, Ltd. | 1,350 | 105,980 | ||||||

|

| |||||||

| 247,567 | ||||||||

|

| |||||||

Engineering & Construction (5.28%) |

| |||||||

Engineers India, Ltd. | 16,243 | 70,489 | ||||||

GMR Infrastructure, Ltd.(a) | 146,340 | 54,317 | ||||||

Larsen & Toubro, Ltd. | 5,978 | 180,022 | ||||||

|

| |||||||

| 304,828 | ||||||||

|

| |||||||

Machinery Diversified (1.55%) |

| |||||||

Thermax, Ltd. | 8,241 | 89,417 | ||||||

|

| |||||||

Metal Fabricate/Hardware (1.19%) |

| |||||||

SKF India, Ltd. | 5,737 | 68,905 | ||||||

|

| |||||||

TOTAL INDUSTRIALS | 710,717 | |||||||

|

| |||||||

Technology (11.82%) | ||||||||

Computers (8.02%) | ||||||||

Infosys, Ltd. | 5,461 | 239,082 | ||||||

Redington India, Ltd. | 59,533 | 89,476 | ||||||

Tata Consultancy Services, Ltd. | 5,507 | 134,431 | ||||||

|

| |||||||

| 462,989 | ||||||||

|

| |||||||

Software (3.80%) | ||||||||

HCL Technologies, Ltd. | 5,325 | 60,011 | ||||||

Oracle Financial Services Software, Ltd.(a) | 1,308 | 70,465 | ||||||

Persistent Systems, Ltd. | 10,013 | 89,034 | ||||||

|

| |||||||

| 219,510 | ||||||||

|

| |||||||

TOTAL TECHNOLOGY | 682,499 | |||||||

|

| |||||||

Utilities (1.98%) | ||||||||

Electric (1.98%) | ||||||||

Power Grid Corp. of India, Ltd. | 26,457 | 55,937 | ||||||

PTC India, Ltd. | 49,600 | 58,606 | ||||||

|

| |||||||

| 114,543 | ||||||||

|

| |||||||

TOTAL UTILITIES | 114,543 | |||||||

|

| |||||||

TOTAL COMMON STOCKS (Cost $5,199,602) | 5,546,527 | |||||||

|

| |||||||

| 7-Day Yield | Shares | Value (Note 2) | ||||||||||

SHORT TERM INVESTMENTS (0.14%) |

| |||||||||||

Money Market Fund (0.14%) |

| |||||||||||

Dreyfus Cash Advantage Fund, Institutional Class | 0.088 | % | 8,207 | $8,207 | ||||||||

|

| |||||||||||

TOTAL SHORT TERM INVESTMENTS (Cost $8,207) |

| 8,207 | ||||||||||

|

| |||||||||||

TOTAL INVESTMENTS (96.20%) (Cost $5,207,809) |

| $5,554,734 | ||||||||||

Other Assets In Excess Of Liabilities (3.80%) |

| 219,572 | ||||||||||

|

| |||||||||||

NET ASSETS (100.00%) |

| $5,774,306 | ||||||||||

|

| |||||||||||

| (a) | Non-Income Producing Security. |

Common Abbreviations:

Ltd. - Limited.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

6 | October 31, 2012 |

Table of Contents

ALPS | Kotak India Growth Fund | ||

| October 31, 2012 (Unaudited) |

ASSETS | ||||

Investments, at value | $ | 5,554,734 | ||

Cash | 1,173 | |||

Foreign currency, at value (Cost $181,212) | 181,207 | |||

Foreign currency held at broker for futures contracts (Cost $58,056) | 55,211 | |||

Receivable for investments sold | 43,322 | |||

Receivable for shares sold | 23,621 | |||

Dividends receivable | 2,195 | |||

Receivable due from advisor | 27,806 | |||

Prepaid expenses and other assets | 14,352 | |||

Total Assets | 5,903,621 | |||

LIABILITIES | ||||

Payable for investments purchased | 52,250 | |||

Administration and transfer agency fees payable | 25,832 | |||

Distribution and services fees payable | 4,883 | |||

Legal fees payable | 87 | |||

Audit fees payable | 43,640 | |||

Trustees’ fees and expenses payable | 170 | |||

Accrued expenses and other liabilities | 2,453 | |||

Total Liabilities | 129,315 | |||

NET ASSETS | $ | 5,774,306 | ||

NET ASSETS CONSIST OF | ||||

Paid-in capital | $ | 6,081,313 | ||

Accumulated net investment loss | (28,736) | |||

Accumulated net realized loss on investments, future contracts and foreign currency transactions | (622,298) | |||

Net unrealized appreciation on investments and translation of assets and liabilities denominated in foreign currencies | 344,027 | |||

NET ASSETS | $ | 5,774,306 | ||

INVESTMENTS, AT COST | $ | 5,207,809 | ||

PRICING OF SHARES | ||||

Class A: | ||||

Net Asset Value, offering and redemption price per share(a) | $ | 8.91 | ||

Net Assets | $ | 2,915,577 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 327,144 | |||

Maximum offering price per share ((NAV/0.9450), based on maximum sales charge of 5.50% of the offering price) | $ | 9.43 | ||

Class C: Net Asset Value, offering and redemption price per share(a) | $ | 8.80 | ||

Net Assets | $ | 650,918 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 73,942 | |||

Class I: Net Asset Value, offering and redemption price per share | $ | 8.96 | ||

Net Assets | $ | 2,207,811 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 246,324 | |||

| (a) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. For a description of a possible sales charge, please see the Fund’s Prospectus. |

See Notes to Financial Statements.

7 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

| For the Six Months Ended October 31, 2012 (Unaudited) |

INVESTMENT INCOME | ||||

Dividends | $ | 50,937 | ||

Total Investment Income | 50,937 | |||

EXPENSES | ||||

Investment advisory fees | 29,567 | |||

Administrative and transfer agency fees | 75,817 | |||

Distribution and service fees | ||||

Class A | 4,913 | |||

Class C | 2,380 | |||

Legal fees | 3,309 | |||

Audit fees | 25,987 | |||

Reports to shareholders and printing fees | 505 | |||

State registration fees | 19,975 | |||

Insurance fees | 105 | |||

Custody fees | 36,149 | |||

Trustees’ fees and expenses | 1,026 | |||

Miscellaneous expenses | 11,603 | |||

Total Expense | 211,336 | |||

Less fees waived/reimbursed by investment advisor | ||||

Class A | (86,553) | |||

Class C | (16,556) | |||

Class I | (63,088) | |||

Net Expenses | 45,139 | |||

Net Investment Income | 5,798 | |||

Net realized loss on investments | (328,863) | |||

Net realized gain on futures contracts | 671 | |||

Net realized gain on foreign currency transactions | 249,468 | |||

Net change in unrealized appreciation on investments | 472,183 | |||

Net change in unrealized appreciation on translation of assets and liabilities denominated in foreign currencies | 167 | |||

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 393,626 | |||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 399,424 | ||

See Notes to Financial Statements.

8 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund | ||

For the Six Months Ended October 31, 2012 (Unaudited) | For the Year Ended April 30, 2012 | |||||||

OPERATIONS | ||||||||

Net investment income/(loss) | $ | 5,798 | $ | (28,880) | ||||

Net realized loss on investments, futures contracts and foreign currency transactions | (78,724) | (581,197) | ||||||

Net change in unrealized appreciation/(depreciation) on investments, futures contracts and translation of assets and liabilities denominated in foreign currencies | 472,350 | (159,023) | ||||||

Net Increase/(Decrease) in Net Assets Resulting from Operations | 399,424 | (769,100) | ||||||

DISTRIBUTIONS | ||||||||

Dividends to shareholders from net realized gains | ||||||||

Class A | 0 | (1,040) | ||||||

Class C | 0 | (511) | ||||||

Class I | 0 | (1,048) | ||||||

Net Decrease in Net Assets from Distributions | 0 | (2,599) | ||||||

BENEFICIAL INTEREST TRANSACTIONS (NOTE 6) | ||||||||

Shares sold | ||||||||

Class A | 879,021 | 2,225,793 | ||||||

Class C | 202,000 | 604,159 | ||||||

Class I | 470,835 | 1,530,305 | ||||||

Dividends reinvested | ||||||||

Class A | 0 | 923 | ||||||

Class C | 0 | 505 | ||||||

Class I | 0 | 964 | ||||||

Shares redeemed | ||||||||

Class A | (558,078) | (455,302) | ||||||

Class C | (20,247) | (439,459) | ||||||

Class I | (46,990) | (216,102) | ||||||

Net Increase in Net Assets Derived from Beneficial Interest Transactions | 926,541 | 3,251,786 | ||||||

Net increase in net assets | 1,325,965 | 2,480,087 | ||||||

NET ASSETS | ||||||||

Beginning of year | 4,448,341 | 1,968,254 | ||||||

End of period * | $ | 5,774,306 | $ | 4,448,341 | ||||

*Including accumulated net investment loss of: | $ | (28,736) | $ | (34,534) | ||||

See Notes to Financial Statements.

9 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund – Class A | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated: | ||

For the Six Months Ended October 31, 2012 (Unaudited)(a) | For the Year Ended April 30, 2012(a) | For the Period February 14, 2011 (Inception) to April 30, 2011(a) | ||||

Net asset value, beginning of period | $8.22 | $10.35 | $10.00 | |||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||

Net investment income/(loss)(b) | 0.01 | (0.08) | (0.04) | |||

Net realized and unrealized gain/(loss) | 0.68 | (2.04) | 0.39 | |||

Total from investment operations | 0.69 | (2.12) | 0.35 | |||

DISTRIBUTIONS: | ||||||

From net realized gains | – | (0.01) | – | |||

Total distributions | – | (0.01) | – | |||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | 0.00(c) | 0.00(c) | 0.00(c) | |||

Net increase/(decrease) in net asset value | 0.69 | (2.13) | 0.35 | |||

Net asset value, end of period | $8.91 | $8.22 | $10.35 | |||

TOTAL RETURN(d) | 8.39% | (20.44)% | 3.40% | |||

RATIOS/SUPPLEMENTAL DATA: | ||||||

Net assets, end of period (000s) | $2,916 | $2,404 | $935 | |||

Ratio of expenses to average net assets excluding fee waivers and reimbursements | 9.05%(e) | 12.42% | 69.96%(e) | |||

Ratio of expenses to average net assets including fee waivers and reimbursements | 2.00%(e) | 2.00% | 2.00%(e) | |||

Ratio of net investment income/(loss) to average net assets | 0.15%(e) | (0.89)% | (1.82)%(e) | |||

Portfolio turnover rate(f) | 57% | 114% | 9% | |||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Kotak Mauritius Portfolio |

(wholly-owned subsidiary).

| (b) | Calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (e) | Annualized. |

| (f) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

10 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund – Class C | ||

Consolidated Financial Highlights | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated: | ||

For the Six Months Ended October 31, 2012 (Unaudited)(a) | For the Year Ended April 30, 2012(a) | For the Period February 14, 2011 (Inception) to April 30, 2011(a) | ||||

Net asset value, beginning of period | $8.15 | $10.32 | $10.00 | |||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||

Net investment loss(b) | (0.02) | (0.13) | (0.05) | |||

Net realized and unrealized gain/(loss) | 0.67 | (2.03) | 0.37 | |||

Total from investment operations | 0.65 | (2.16) | 0.32 | |||

DISTRIBUTIONS: | ||||||

From net realized gains | – | (0.01) | – | |||

Total distributions | – | (0.01) | – | |||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | – | 0.00(c) | – | |||

Net increase/(decrease) in net asset value | 0.65 | (2.17) | 0.32 | |||

Net asset value, end of period | $8.80 | $8.15 | $10.32 | |||

TOTAL RETURN(d) | 7.98% | (20.97)% | 3.20% | |||

RATIOS/SUPPLEMENTAL DATA: | ||||||

Net assets, end of period (000s) | $651 | $435 | $466 | |||

Ratio of expenses to average net assets excluding fee waivers and reimbursements | 9.56%(e) | 13.39% | 69.64%(e) | |||

Ratio of expenses to average net assets including fee waivers and reimbursements | 2.60%(e) | 2.60% | 2.60%(e) | |||

Ratio of net investment loss to average net assets | (0.45)%(e) | (1.49)% | (2.42)%(e) | |||

Portfolio turnover rate(f) | 57% | 114% | 9% | |||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Kotak Mauritius Portfolio |

(wholly-owned subsidiary).

| (b) | Calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (e) | Annualized. |

| (f) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

11 | October 31, 2012

Table of Contents

ALPS | Kotak India Growth Fund – Class I | ||

Consolidated Financial Highlights | ||

Selected data for a share of beneficial interest outstanding throughout the periods indicated: | ||

For the Six Months Ended October 31, 2012 (Unaudited)(a) | For the Year Ended April 30, 2012(a) | For the Period February 14, 2011 (Inception) to April 30, 2011(a) | ||||

Net asset value, beginning of period | $8.25 | $10.34 | $10.00 | |||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||

Net investment income/(loss)(b) | 0.02 | (0.04) | (0.03) | |||

Net realized and unrealized gain/(loss) | 0.69 | (2.04) | 0.37 | |||

Total from investment operations | 0.71 | (2.08) | 0.34 | |||

DISTRIBUTIONS: | ||||||

From net realized gains | – | (0.01) | – | |||

Total distributions | – | (0.01) | – | |||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | – | 0.00(c) | – | |||

Net increase/(decrease) in net asset value | 0.71 | (2.09) | 0.34 | |||

Net asset value, end of period | $8.96 | $8.25 | $10.34 | |||

TOTAL RETURN(d) | 8.61% | (20.23)% | 3.50% | |||

RATIOS/SUPPLEMENTAL DATA: | ||||||

Net assets, end of period (000s) | $2,208 | $1,609 | $568 | |||

Ratio of expenses to average net assets excluding fee waivers and reimbursements | 8.62%(e) | 12.05% | 96.67%(e) | |||

Ratio of expenses to average net assets including fee waivers and reimbursements | 1.60%(e) | 1.60% | 1.60%(e) | |||

Ratio of net investment income/(loss) to average net assets | 0.55%(e) | (0.49)% | (1.36)%(e) | |||

Portfolio turnover rate(f) | 57% | 114% | 9% | |||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Kotak Mauritius Portfolio |

(wholly-owned subsidiary).

| (b) | Calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (e) | Annualized. |

| (f) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

12 | October 31, 2012

Table of Contents

| October 31, 2012 (Unaudited) |

Overview

With only two months to go in 2012, it’s easy to see why equity values, and Listed Private Equity, have done well overall; there has been a noticeable absence of major drama. No drama these days has appeared to equate to rising values, especially in Listed Private Equity. Sure, there were the all too familiar “issues”: 1) Europe; ongoing political and economic upheaval in Spain, Greece and Italy, Germany’s ongoing support of the Euro/EU, the role of the European Central Bank (ECB), flat to declining GDP and unemployment; 2) the U.S.; the recent Presidential election, continued dysfunction in Washington, D.C., the year-end budget drama, known as the fiscal cliff, growing deficits, a third round of quantitative easing and a lack of business confidence; and 3) the Middle East; Iran, Syria, Israel, Libya, et al. However, investors seem to have taken some degree of comfort that the “issues” are contained, or least not spinning out of control, for the time being. As I’ve said in the past, stay tuned, there’s more to follow.

Macro issues aside, the world of private equity continues to move forward. While the pace of new investments continues to be muted, sales of existing investments, also known as exits or realizations, continue to be robust. Per one of the largest global Private Equity Fund of Fund Managers, Pantheon, trade sales (when a private equity firm sells one of its portfolio companies to a corporate buyer) within their portfolio for the past year represented approximately 62% of exits, compared with Initial Public Offerings (IPOs) representing approximately 1%. That gives one a sense of just how closed the public equity markets are. If a Company wants to issue debt: no problem. On the other hand, if a Company wants to issue equity: not so easy. And therein lies the problem: investors continue to be exceedingly cautious. Growth is elusive. Survival, and hence maintaining what you have, is still the common refrain. Risk assets (equity as a whole) continue to be out of favor. Return of principal, even with puny to negative real returns, is the focus. Until this dynamic changes, we expect private equity to muddle along with pockets of success, but with a cautious approach as well.

Taking it one layer deeper, certain behaviors of Listed Private Equity have been similar to those of illiquid partnership-based private equity: new investments, exits/realizations, and the general mood towards the future is almost exactly the same. The one notable exception, Listed Private Equity discounts continue to be an issue on investors’ minds, although not to the degree that we’ve seen in previous quarters. Progress is being made. Investors are beginning to see more capital coming back to them in the form of dividends/special dividends. Realizations in private equity portfolios continue to be done at uplifts to last valuations, and consolidation within the listed space continues; the $1.3 billion acquisition of Conversus Capital LP by HarbourVest in July 2012 being the most recent example.

While it didn’t necessarily feel this way during the summer, it was a good several months. Sometimes no drama is a good thing.

Portfolio Review

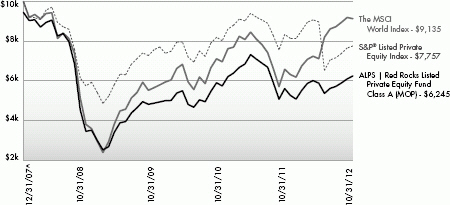

The Fund’s Class A Shares, LPEFX, returned 6.21% net of fees, (Class A delivered a net return of 0.40% at MOP), compared with 2.12% and 8.97% for the MSCI World Index and the S&P® Listed Private Equity Index, respectively for the Semi-Annual period ending October 31, 2012.

During the period we exited three holdings, Brookfield Infrastructure Partners LP, Fosun International and Leucadia National Corporation. In addition, we added three holdings, Carlyle Group, Hosken Consolidated Investments LTD and Investor AB, a previous holding of the Fund.

As any investor that has held or followed the Fund over the past few years knows, diversification continues to be the cornerstone of how we manage exposure and risk. The recent period was no different: with approximately 40 holdings in some of the top performing private equity firms/funds around the globe, the Fund offers investors fully diversified private equity exposure.

Net contributors to performance for the period included:

| • | AP Alternative Assets LP |

| • | Wendel Investissement |

| • | Apollo Global Management LLC, Class A |

Net detractors to performance for the period were:

| • | SVG Capital PLC |

| • | Fosun International |

| • | Ratos AB, B Shares |

Outlook

I’d like to suggest that the outlook for private equity in the coming period and into early 2013 is quite positive. While it certainly could be positive, I’m less than comfortable predicting that. A number of developments point to better times ahead within private equity portfolio holdings; improving individual company level cash flow, solid balance sheets, continued rationalization and consolidation in some cases and strong trade sale valuations and activity. However, the global macro and political backdrop is uncertain at best. Until there is clarity here, investor confidence may be muted.

Despite the uncertainty, we continue to believe that the private equity model is fundamentally alive and well. We continue to believe that the patient investor will be rewarded when we consider the value of portfolio assets and the cash flow that they may generate.

As always, we appreciate your continued support and interest in Red Rocks and the Listed Private Equity strategy.

Adam Goldman

Co-Portfolio Manager

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned herein. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Red Rocks Capital LLC does not accept any liability for losses either direct or consequential caused by the use of this information.

| 13 | October 31, 2012 |

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

Management Commentary | October 31, 2012 (Unaudited) |

Performance of $10,000 Initial Investment (for the period ended October 31, 2012)

Comparison of change in value of a $10,000 investment (includes applicable sales loads of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

14 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

Management Commentary | October 31, 2012 (Unaudited) | |

Average Annual Total Returns (as of October 31, 2012)

| 1 Year | 3 Year | Since Inception ^ | Total Expense Ratio | What you Pay * | ||||||

Class A (NAV)1 | 11.44% | 9.08% | -8.20% | 3.34% | 3.28% | |||||

Class A (MOP)2 | 5.25% | 7.07% | -9.27% | |||||||

Class C (NAV)1 | 10.51% | 8.05% | -9.00% | 4.00% | 3.88% | |||||

Class C (CDSC)2 | 9.51% | 8.05% | -9.00% | |||||||

Class I | 11.47% | 9.33% | -7.98% | 3.04% | 2.88% | |||||

Class R | 11.19% | 8.69% | -8.62% | 3.52% | 3.38% | |||||

S&P® LPE Total Return Index3 | 17.84% | 12.00% | -5.12% | |||||||

MSCI World Index4 | 9.45% | 7.88% | -1.86% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. The Fund imposes a 2.00% redemption fee on shares held for less than 90 days. The Fund imposes a maximum Contingent Deferred Sales Charge (“CDSC”) of 1.00% on Class C shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 12 months after a purchase in excess of $1 million. Performance data does not reflect the redemption fee or the CDSC, which if reflected would reduce the performance quoted. For the most current month-end performance data, please call 1-866-759-5679.

Performance shown for Class C shares prior to June 30, 2010 reflects the historical performance of the Fund’s Class A shares, calculated using the fees and expenses of Class C shares.

| 1 | Net Asset Value (NAV) is the share price without sales charges. The performance data shown does not reflect the decution of the sales load or the redemption fee or CDSC, and that, if reflected, the load or fee would reduce the performance quoted. |

| 2 | Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. CDSC performance for Class C shares includes a 1% contingent deferred sales charge (CDSC) on C shares redeemed within 12 months of purchase. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. |

| 3 | S&P® Listed Private Equity Index: The S&P® Listed Private Equity Index is comprised of 30 leading listed private equity companies that meet size, liquidity, exposure, and activity requirements. The index is designed to provide tradable exposure to the leading publicly listed companies in the private equity space. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| 4 | MSCI World Index: Morgan Stanley Capital International’s market capitalization weighted index is composed of companies representative of the market structure of 22 developed market countries in North America, Europe and the Asia/Pacific Region. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund inception date of December 31, 2007. |

| * | What You Pay reflects the Advisor’s and Sub-Advisor’s decision to contractually limit expenses through August 31, 2013. Please see the prospectus for additional information. |

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Listed Private Equity Companies are subject to various risks depending on their underlying investments, which could include, but are not limited to, additional liquidity risk, industry risk, non-U.S. security risk, currency risk, credit risk, managed portfolio risk and derivatives risk (derivatives risk is the risk that the value of the Listed Private Equity Companies’ derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment).

There are inherent risks in investing in private equity companies, which encompass financial institutions or vehicles whose principal business is to invest in and lend capital to privately held companies. Generally, little public information exists for private and thinly traded companies, and there is a risk that investors may not be able to make a fully informed investment decision.

Listed Private Equity Companies may have relatively concentrated investment portfolios, consisting of a relatively small number of holdings. A consequence of this limited number of investments is that the aggregate returns realized may be adversely impacted by the poor performance of a small number of investments, or even a single investment, particularly if a company experiences the need to write down the value of an investment.

Certain of the Fund’s investments may be exposed to liquidity risk due to low trading volume, lack of a market maker or legal restrictions limiting the ability of the Fund to sell particular securities at an advantageous price and/or time. As a result, these securities may be more difficult to value. Foreign investing involves special risks, such as currency fluctuations and political uncertainty. The Fund invests in derivatives and is subject to the risk that the value of those derivative investments will fall because of pricing difficulties or lack of correlation with the underlying investment.

Mutual funds are not insured or guaranteed by the FDIC or by any other government agency or government sponsored agency of the federal government or any state, not deposits, obligations or guaranteed by any bank or its affiliates and are subject to investment risks, including possible loss of the principal amount invested.

15 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

Management Commentary | October 31, 2012 (Unaudited) |

Top Ten Holdings (as a % of Net Assets) † | ||||

| ||||

Conversus Capital LP | 5.12 | % | ||

Electra Private Equity PLC | 4.72 | % | ||

SVG Capital PLC | 4.56 | % | ||

Blackstone Group LP | 4.50 | % | ||

Wendel Investissement | 4.46 | % | ||

AP Alternative Assets LP | 4.38 | % | ||

KKR & Co. LP | 4.32 | % | ||

Onex Corp. | 4.31 | % | ||

Eurazeo | 3.75 | % | ||

| Apollo Global Management LLC, Class A | 3.65 | % | ||

Top Ten Holdings | 43.77 | % | ||

† Holdings are subject to change. Table presents indicative values only. |

| |||

Industry Sector Allocation (as a % of Net Assets)

16 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

| October 31, 2012 (Unaudited) |

| Shares | Value (Note 2) | |||

COMMON STOCKS (99.03%) | ||||

Communications (3.79%) | ||||

Internet (3.79%) | ||||

ICG Group, Inc.(a) | 340,000 | $3,563,200 | ||

Safeguard Scientifics, Inc.(a) | 192,041 | 3,043,850 | ||

| ||||

| 6,607,050 | ||||

| ||||

TOTAL COMMUNICATIONS | 6,607,050 | |||

| ||||

Diversified (11.87%) | ||||

Holding Companies-Diversified Operations (11.87%) | ||||

Ackermans & van Haaren N.V. | 72,586 | 5,902,693 | ||

Remgro, Ltd. | 140,000 | 2,397,744 | ||

Schouw & Co. | 202,472 | 4,626,142 | ||

Wendel Investissement | 88,300 | 7,781,415 | ||

| ||||

| 20,707,994 | ||||

| ||||

TOTAL DIVERSIFIED | 20,707,994 | |||

| ||||

Financials (83.37%) | ||||

Closed-End Funds (40.06%) | ||||

AP Alternative Assets LP(a) | 518,724 | 7,645,992 | ||

Candover Investments PLC(a) | 192,000 | 1,113,883 | ||

Castle Private Equity, Ltd.(a) | 238,876 | 3,257,517 | ||

Conversus Capital LP | 438,548 | 8,924,460 | ||

Electra Private Equity PLC(a) | 279,501 | 8,231,628 | ||

Graphite Enterprise Trust PLC | 903,000 | 6,098,496 | ||

HarbourVest Global Private Equity, Ltd.(a) | 602,200 | 4,353,906 | ||

HBM Healthcare Investments AG Class A(a) | 72,400 | 3,863,717 | ||

HgCapital Trust PLC | 256,542 | 4,144,118 | ||

Pantheon International Participations PLC, Ordinary Shares(a) | 267,016 | 3,623,872 | ||

Pantheon International Participations PLC, Redeemable Shares(a) | 135,200 | 1,805,445 | ||

Princess Private Equity Holding, Ltd. | 741,225 | 6,350,447 | ||

Standard Life European Private Equity Trust PLC, Ordinary Shares | 980,573 | 2,519,990 | ||

SVG Capital PLC(a) | 1,913,000 | 7,961,701 | ||

| ||||

| 69,895,172 | ||||

| ||||

Diversified Financial Services (16.33%) | ||||

Blackstone Group LP | 511,000 | 7,848,960 | ||

Intermediate Capital Group PLC | 1,130,000 | 5,565,478 | ||

KKR & Co. LP | 501,300 | 7,544,565 | ||

Onex Corp. | 186,900 | 7,522,784 | ||

| ||||

| 28,481,787 | ||||

| ||||

| Shares | Value (Note 2) | |||||

Investment Companies (4.86%) | ||||||

Hosken Consolidated | 239,500 | $2,695,899 | ||||

Investor AB, B Shares | 116,000 | 2,558,579 | ||||

Ratos AB, B Shares | 375,700 | 3,225,756 | ||||

| ||||||

| 8,480,234 | ||||||

| ||||||

Private Equity (19.58%) | ||||||

3i Group PLC | 891,000 | 3,097,155 | ||||

Altamir Amboise | 373,650 | 3,351,382 | ||||

Apollo Global Management | 419,000 | 6,364,610 | ||||

Aurelius AG | 74,818 | 3,818,868 | ||||

Bure Equity AB | 464,881 | 1,604,996 | ||||

The Carlyle Group LP | 51,200 | 1,330,688 | ||||

Deutsche Beteiligungs AG | 108,572 | 2,742,726 | ||||

Eurazeo | 143,000 | 6,545,579 | ||||

GIMV N.V. | 89,351 | 4,318,616 | ||||

IP Group PLC(a) | 513,000 | 978,530 | ||||

| ||||||

| 34,153,150 | ||||||

| ||||||

Real Estate (2.54%) | ||||||

Brookfield Asset | 128,900 | 4,439,316 | ||||

| ||||||

TOTAL FINANCIALS | 145,449,659 | |||||

| ||||||

TOTAL COMMON STOCKS (Cost $152,635,884) | 172,764,703 | |||||

| ||||||

7-Day Yield | Shares | Value (Note 2) | ||||

SHORT TERM INVESTMENTS (1.05%) | ||||||

Money Market Fund (1.05%) | ||||||

Dreyfus Treasury Prime | 0.00003% | 1,829,091 | 1,829,091 | |||

| ||||||

TOTAL SHORT TERM INVESTMENTS (Cost $1,829,091) | 1,829,091 | |||||

| ||||||

TOTAL INVESTMENTS (100.08%) (Cost $154,464,975) | $174,593,794 | |||||

Liabilities In Excess Of Other Assets | (133,842) | |||||

| ||||||

NET ASSETS (100.00%) | $174,459,952 | |||||

| ||||||

17 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

Statement of Investments | October 31, 2012 (Unaudited) |

| (a) | Non-Income Producing Security. |

Common Abbreviations:

AB - Aktiebolag is the Swedish equivalent of the term corporation.

AG - Aktiengesellschaft is a German term that refers to a corporation that is limited by shares, i.e., owned by shareholders.

LLC - Limited Liability Company.

LP - Limited Partnership.

Ltd. - Limited.

N.V. - Naamloze Vennootschap is the Dutch term for a public limited liability corporation.

PLC - Public Limited Company.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry subclassifications for reporting ease. Industries are shown as a percent of net assets. These industry classifications are based on third party definitions and are unaudited. The definitions are industry terms and do not reflect the legal status of any of the investments or the companies in which the Fund has invested.

See Notes to Financial Statements.

18 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

| October 31, 2012 (Unaudited) |

ASSETS | ||||

Investments, at value | $ | 174,593,794 | ||

Cash | 44 | |||

Foreign currency, at value (Cost $87,140) | 87,581 | |||

Receivable for investments sold | 516,560 | |||

Dividends and interest receivable | 159,596 | |||

Prepaid expenses and other assets | 21,538 | |||

Total Assets | 175,379,113 | |||

LIABILITIES | ||||

Payable for investments purchased | 205,885 | |||

Payable for shares redeemed | 305,513 | |||

Investment advisory fees payable | 126,994 | |||

Administration and transfer agency fees payable | 21,329 | |||

Distribution and services fees payable | 112,978 | |||

Legal fees payable | 2,652 | |||

Audit fees payable | 28,718 | |||

Custody fees payable | 72,052 | |||

Trustees’ fees and expenses payable | 5,885 | |||

Accrued expenses and other liabilities | 37,155 | |||

Total Liabilities | 919,161 | |||

NET ASSETS | $ | 174,459,952 | ||

NET ASSETS CONSIST OF | ||||

Paid-in capital | $ | 189,593,089 | ||

Accumulated net investment loss | (9,081,714 | ) | ||

Accumulated net realized loss on investments and foreign currency transactions | (26,176,504 | ) | ||

Net unrealized appreciation on investments and translation of assets and liabilities denominated in foreign currencies | 20,125,081 | |||

NET ASSETS | $ | 174,459,952 | ||

INVESTMENTS, AT COST | $ | 154,464,975 | ||

PRICING OF SHARES | ||||

Class A: Net Asset Value, offering and redemption price per share(a) | $ | 4.96 | ||

Net Assets | $ | 80,246,827 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 16,185,066 | |||

Maximum offering price per share ((NAV/0.9450), based on maximum sales charge of 5.50% of the offering price) | $ | 5.25 | ||

Class C: | ||||

Net Asset Value, offering and redemption price per share(a) | $ | 4.85 | ||

Net Assets | $ | 2,953,891 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 608,785 | |||

Class I: | ||||

Net Asset Value, offering and redemption price per share | $ | 4.98 | ||

Net Assets | $ | 91,208,979 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 18,298,341 | |||

Class R: | ||||

Net Asset Value, offering and redemption price per share | $ | 4.42 | ||

Net Assets | $ | 50,255 | ||

Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 11,377 | |||

| (a) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. For a description of a possible sales charge, please see the Fund’s Prospectus. |

See Notes to Financial Statements.

19 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

| For the Six Months Ended October 31, 2012 (Unaudited) | ||

INVESTMENT INCOME | ||||

Dividends | $ | 2,815,556 | ||

Foreign taxes withheld on dividends | (201,887) | |||

Interest and other income | 6,407 | |||

Total Investment Income | 2,620,076 | |||

EXPENSES | ||||

Investment advisory fees | 696,148 | |||

Administrative and transfer agency fees | 137,815 | |||

Distribution and service fees | ||||

Class A | 163,295 | |||

Class C | 14,104 | |||

Class R | 127 | |||

Legal fees | 6,276 | |||

Audit fees | 16,248 | |||

Networking fees | ||||

Class A | 14,178 | |||

Class C | 889 | |||

Class I | 38,142 | |||

Class R | 48 | |||

Reports to shareholders and printing fees | 25,819 | |||

State registration fees | 32,591 | |||

Insurance fees | 4,090 | |||

Custody fees | 59,055 | |||

Trustees’ fees and expenses | 9,758 | |||

Miscellaneous expenses | 7,385 | |||

Total Expense | 1,225,968 | |||

Less fees waived/reimbursed by investment advisor | ||||

Class A | (41,771) | |||

Class C | (398) | |||

Class I | (24,174) | |||

Class R | (39) | |||

Net Expenses | 1,159,586 | |||

Net Investment Income | 1,460,490 | |||

Net realized loss on investments | (1,325,946) | |||

Net realized loss on foreign currency transactions | (40,367) | |||

Net change in unrealized appreciation on investments | 9,966,848 | |||

Net change in unrealized appreciation on translation of assets and liabilities denominated in foreign currencies | 994 | |||

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 8,601,529 | |||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 10,062,019 | ||

See Notes to Financial Statements.

20 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund | ||

For the Six Months Ended October 31, 2012 | For the Year Ended April 30, 2012 | |||||||

OPERATIONS | ||||||||

Net investment income | $ | 1,460,490 | $ | 2,252,886 | ||||

Net realized loss on investments and foreign currency transactions | (1,366,313) | (1,997,056) | ||||||

Net change in unrealized appreciation/(depreciation) on investments and translation of assets and liabilities denominated in foreign currencies | 9,967,842 | (40,079,612) | ||||||

Net Increase/(Decrease) in Net Assets Resulting from Operations | 10,062,019 | (39,823,782) | ||||||

DISTRIBUTIONS | ||||||||

Dividends to shareholders from net investment income | ||||||||

Class A | 0 | (7,773,831) | ||||||

Class C | 0 | (232,203) | ||||||

Class I | 0 | (5,228,944) | ||||||

Class R | 0 | (9,179) | ||||||

Net Decrease in Net Assets from Distributions | 0 | (13,244,157) | ||||||

BENEFICIAL INTEREST TRANSACTIONS (NOTE 6) | ||||||||

Shares sold | ||||||||

Class A | 11,213,935 | 55,043,701 | ||||||

Class C | 297,182 | 1,787,116 | ||||||

Class I | 20,978,524 | 50,688,416 | ||||||

Class R | 5,823 | 41,342 | ||||||

Dividends reinvested | ||||||||

Class A | 0 | 6,987,024 | ||||||

Class C | 0 | 172,533 | ||||||

Class I | 0 | 1,952,666 | ||||||

Class R | 0 | 8,650 | ||||||

Shares redeemed | ||||||||

Class A | (21,431,278) | (67,995,564) | ||||||

Class C | (338,130) | (718,469) | ||||||

Class I | (12,764,304) | (22,792,481) | ||||||

Class R | (5,253) | (85,079) | ||||||

Net Increase/(Decrease) in Net Assets Derived from Beneficial Interest Transactions | (2,043,501) | 25,089,855 | ||||||

Net increase/(decrease) in net assets | 8,018,518 | (27,978,084) | ||||||

NET ASSETS | ||||||||

Beginning of year | 166,441,434 | 194,419,518 | ||||||

End of period * | $ | 174,459,952 | $ | 166,441,434 | ||||

*Including accumulated net investment loss of: | $ | (9,081,714) | $ | (10,542,204) | ||||

See Notes to Financial Statements.

21 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund – Class A | ||

| Selected data for a share of beneficial interest outstanding throughout the periods indicated: | ||

For the Ended | For the Year Ended 2012 | For the Year Ended 2011 | For the Year Ended 2010 | For the Year Ended 2009 | For the Period 2007 2008 | |||||||

Net asset value, beginning of period | $4.67 | $6.44 | $5.17 | $3.56 | $9.47 | $10.00 | ||||||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||

Net investment income | 0.04(a) | 0.07(a) | 0.04(a) | 0.14 | 0.08(a) | 0.11 | ||||||

Net realized and unrealized gain/(loss) | 0.25 | (1.41) | 1.61 | 1.99 | (5.97) | (0.64) | ||||||

Total from investment operations | 0.29 | (1.34) | 1.65 | 2.13 | (5.89) | (0.53) | ||||||

DISTRIBUTIONS: | ||||||||||||

From net investment income | – | (0.43) | (0.38) | (0.52) | (0.03) | – | ||||||

From net realized gains | – | – | – | – | (0.00)(b) | – | ||||||

Total distributions | – | (0.43) | (0.38) | (0.52) | (0.03) | – | ||||||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | 0.00(b) | 0.00(b) | 0.00(b) | 0.00(b) | 0.01 | – | ||||||

Net increase/(decrease) in net asset value | 0.29 | (1.77) | 1.27 | 1.61 | (5.91) | (0.53) | ||||||

Net asset value, end of period | $4.96 | $4.67 | $6.44 | $5.17 | $3.56 | $9.47 | ||||||

TOTAL RETURN(c) | 6.21% | (19.68)% | 33.22% | 61.68% | (62.01)% | (5.30)% | ||||||

RATIOS/SUPPLEMENTAL DATA: | ||||||||||||

Net assets, end of period (000s) | $80,247 | $85,807 | $124,874 | $67,192 | $27,860 | $832 | ||||||

Ratio of expenses to average net assets excluding fee waiver sand reimbursements(g) | 1.65%(d) | 1.71% | 1.70% | 1.71% | 2.08% | 39.07%(d) | ||||||

Ratio of expenses to average net assets including fee waivers and reimbursements(g) | 1.55%(d) | 1.50% | 1.50% | 1.44%(e) | 1.25% | 1.25%(d) | ||||||

Ratio of net investment income to average net assets(g) | 1.72%(d) | 1.34% | 0.67% | 0.42% | 2.16% | 4.68%(d) | ||||||

Portfolio turnover rate(f) | 18% | 72% | 43% | 54% | 59% | 15% | ||||||

| (a) | Calculated using the average shares method. |

| (b) | Less than $0.005 and ($0.005) per share. |

| (c) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (d) | Annualized. |

| (e) | Effective September 1, 2009, the net expense ratio limitation changed from 1.25% to 1.50% (exclusive of distribution and service (12b-1) fees, acquired fund fees and expenses, brokerage expenses, interest expense, short sale dividend expense, taxes and extraordinary expenses). |

| (f) | Portfolio turnover rate for periods less than one full year have not been annualized. |

| (g) | The ratios exclude the impact of expenses of the underlying funds in which the Fund invests as represented in the Statement of lnvestments. |

See Notes to Financial Statements.

22 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund – Class C | ||

Financial Highlights | Selected data for a share of beneficial interest outstanding throughout the periods indicated: | |

| For the Six Months Ended October 31, 2012 (Unaudited) | For the Year Ended April 30, 2012 | For the Period July 2, 2010 (Inception) to April 30, 2011 | ||||

Net asset value, beginning of period | $4.59 | $6.37 | $4.39 | |||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||

Net investment income/(loss)(a) | 0.02 | 0.03 | (0.01) | |||

Net realized and unrealized gain/(loss) | 0.24 | (1.39) | 2.36 | |||

Total from investment operations | 0.26 | (1.36) | 2.35 | |||

DISTRIBUTIONS: | ||||||

From net investment income | – | (0.42) | (0.37) | |||

Total distributions | – | (0.42) | (0.37) | |||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | 0.00(b) | 0.00(b) | 0.00(b) | |||

Net increase/(decrease) in net asset value | 0.26 | (1.78) | 1.98 | |||

Net asset value, end of period | $4.85 | $4.59 | $6.37 | |||

TOTAL RETURN(c) | 5.66% | (20.33)% | 55.32% | |||

RATIOS/SUPPLEMENTAL DATA: | ||||||

Net assets, end of period (000s) | $2,954 | $2,838 | $2,566 | |||

Ratio of expenses to average net assets excluding fee waivers and reimbursements(g) | 2.28%(d) | 2.37% | 2.31%(d) | |||

Ratio of expenses to average net assets including fee waivers and reimbursements(g) | 2.25%(d) | 2.25% | 2.25%(d) | |||

Ratio of net investment income/(loss) to average net assets(g) | 0.96%(d) | 0.59% | (0.19)%(d) | |||

Portfolio turnover rate(e) | 18% | 72% | 43%(f) | |||

| (a) | Calculated using the average shares method. |

| (b) | Less than $0.005 per share. |

| (c) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

| (d) | Annualized. |

| (e) | Portfolio turnover rate for periods less than one full year have not been annualized. |

| (f) | Portfolio turnover rate is calculated at the Fund Level and represents the year ended April 30, 2011. |

| (g) | The ratios exclude the impact of expenses of the underlying funds in which the Fund invests as represented in the Statement of lnvestments. |

See Notes to Financial Statements.

23 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund – Class I | ||

Financial Highlights | Selected data for a share of beneficial interest outstanding throughout the periods indicated: | |

For the Six Months | For the Year Ended April 30, 2012 | For the Year Ended April 30, 2011 | For the Year Ended April 30, 2010 | For the Year Ended April 30, 2009 | For the Period Ended April 30, 2008(a) | |||||||

Net asset value, beginning of period | $4.69 | $6.47 | $5.19 | $3.57 | $9.47 | $10.00 | ||||||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||

Net investment income | 0.04(b) | 0.08(b) | 0.05(b) | 0.28 | 0.10(b) | 0.13 | ||||||

Net realized and unrealized gain/(loss) | 0.25 | (1.42) | 1.62 | 1.87 | (5.97) | (0.66) | ||||||

Total from investment operations | 0.29 | (1.34) | 1.67 | 2.15 | (5.87) | (0.53) | ||||||

DISTRIBUTIONS: | ||||||||||||

From net investment income | – | (0.44) | (0.39) | (0.53) | (0.05) | – | ||||||

From net realized gains | – | – | – | – | (0.00)(c) | – | ||||||

Total distributions | – | (0.44) | (0.39) | (0.53) | (0.05) | – | ||||||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | 0.00(c) | 0.00(c) | 0.00(c) | 0.00(c) | 0.02 | – | ||||||

Net increase/(decrease) in net asset value | 0.29 | (1.78) | 1.28 | 1.62 | (5.90) | (0.53) | ||||||

Net asset value, end of period | $4.98 | $4.69 | $6.47 | $5.19 | $3.57 | $9.47 | ||||||

TOTAL RETURN(d) | 6.18% | (19.52)% | 33.47% | 62.09% | (61.79)% | (5.30)% | ||||||

RATIOS/SUPPLEMENTAL DATA: | ||||||||||||

Net assets, end of period (000s) | $91,209 | $77,750 | $66,854 | $45,144 | $12,938 | $21 | ||||||

Ratio of expenses to average net assets excluding fee waivers and reimbursements(h) | 1.31%(e) | 1.41% | 1.36% | 1.47% | 2.05% | 35.33%(e) | ||||||

Ratio of expenses to average net assets including fee waivers and reimbursements(h) | 1.25%(e) | 1.25% | 1.25% | 1.19%(f) | 1.00% | 1.00%(e) | ||||||

Ratio of net investment income to average net assets(h) | 1.88%(e) | 1.60% | 0.91% | 0.78% | 2.56% | 6.11%(e) | ||||||

Portfolio turnover rate(g) | 18% | 72% | 43% | 54% | 59% | 15% | ||||||

| (a) | The Fund commenced operations on December 31, 2007. |

| (b) | Calculated using the average shares method. |

| (c) | Less than $0.005 and ($0.005) per share. |

| (d) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (e) | Annualized. |

| (f) | Effective September 1, 2009, the net expense ratio limitation changed from 1.00% to 1.25% (exclusive of distribution and service (12b-1) fees, acquired fund fees and expenses, brokerage expenses, interest expense, short sale dividend expense, taxes and extraordinary expenses). |

| (g) | Portfolio turnover rate for periods less than one full year have not been annualized. |

| (h) | The ratios exclude the impact of expenses of the underlying funds in which the Fund invests as represented in the Statement of lnvestments. |

See Notes to Financial Statements.

24 | October 31, 2012

Table of Contents

ALPS | Red Rocks Listed Private Equity Fund – Class R | ||

Financial Highlights | Selected data for a share of beneficial interest outstanding throughout the periods indicated: | |

For the Six Months | For the Year Ended April 30, 2012 | For the Year Ended April 30, 2011 | For the Year Ended April 30, 2010 | For the Year Ended April 30, 2009 | For the Period Ended April 30, 2008(a) | |||||||

Net asset value, beginning of period | $4.17 | $5.82 | $4.73 | $3.31 | $9.46 | $10.00 | ||||||

INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||

Net investment income/(loss) | 0.03(b) | 0.05(b) | 0.03(b) | (0.09) | 0.15(b) | 0.12 | ||||||

Net realized and unrealized gain/(loss) | 0.22 | (1.27) | 1.43 | 2.02 | (6.05) | (0.66) | ||||||

Total from investment operations | 0.25 | (1.22) | 1.46 | 1.93 | (5.90) | (0.54) | ||||||

DISTRIBUTIONS: | ||||||||||||

From net investment income | – | (0.43) | (0.37) | (0.51) | (0.26) | – | ||||||

From net realized gains | – | – | – | – | (0.00)(c) | – | ||||||

Total distributions | – | (0.43) | (0.37) | (0.51) | (0.26) | – | ||||||

REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | – | – | – | – | 0.01 | – | ||||||

Net increase/(decrease) in net asset value | 0.25 | (1.65) | 1.09 | 1.42 | (6.15) | (0.54) | ||||||