UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-8194

FINANCIAL INVESTORS TRUST

(exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

David T. Buhler, Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: October 31

Date of reporting period: November 1, 2014 – April 30, 2015

| Item 1. | Reports to Stockholders. |

table of

CONTENTS

CONTENTS

| Disclosure of Fund Expenses | 1 | |

| ALPS | Alerian MLP Infrastructure Index Fund | ||

| Management Commentary | 5 | |

| Performance Update | 6 | |

| Statement of Investments | 8 | |

| Statement of Assets and Liabilities | 9 | |

| Statement of Operations | 10 | |

| Statements of Changes in Net Assets | 11 | |

| Financial Highlights | 12 | |

| ALPS | CoreCommodity Management | ||

CompleteCommodities® Strategy Fund | ||

| Management Commentary | 16 | |

| Performance Update | 18 | |

| Consolidated Statement of Investments | 20 | |

| Consolidated Statement of Assets and Liabilities | 27 | |

| Consolidated Statement of Operations | 29 | |

| Consolidated Statements of Changes in Net Assets | 30 | |

| Consolidated Financial Highlights | 31 | |

| ALPS | Kotak India Growth Fund | ||

| Management Commentary | 34 | |

| Performance Update | 36 | |

| Consolidated Statement of Investments | 38 | |

| Consolidated Statement of Assets and Liabilities | 40 | |

| Consolidated Statement of Operations | 41 | |

| Consolidated Statements of Changes in Net Assets | 42 | |

| Consolidated Financial Highlights | 43 | |

| ALPS | Red Rocks Listed Private Equity Fund | ||

| Management Commentary | 46 | |

| Performance Update | 48 | |

| Statement of Investments | 51 | |

| Statement of Assets and Liabilities | 53 | |

| Statement of Operations | 54 | |

| Statements of Changes in Net Assets | 55 | |

| Financial Highlights | 56 | |

| ALPS | Sterling ETF Tactical Rotation Fund | ||

| Management Commentary | 60 | |

| Performance Update | 61 | |

| Statement of Investments | 63 | |

| Statement of Assets and Liabilities | 64 | |

| Statement of Operations | 65 | |

| Statements of Changes in Net Assets | 66 | |

| Financial Highlights | 67 | |

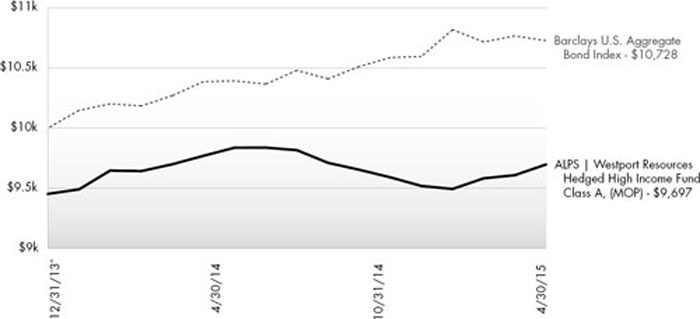

| ALPS | Westport Resources Hedged High Income Fund | ||

| Management Commentary | 70 | |

| Performance Update | 71 | |

| Statement of Investments | 73 | |

| Statement of Assets and Liabilities | 81 | |

| Statement of Operations | 82 | |

| Statements of Changes in Net Assets | 83 | |

| Financial Highlights | 84 | |

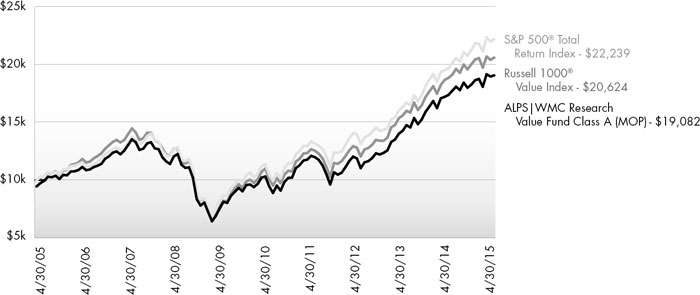

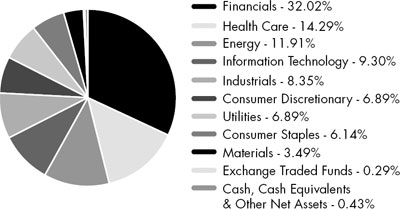

| ALPS | WMC Research Value Fund | ||

| Management Commentary | 87 | |

| Performance Update | 89 | |

| Statement of Investments | 91 | |

| Statement of Assets and Liabilities | 95 | |

| Statement of Operations | 96 | |

| Statements of Changes in Net Assets | 97 | |

| Financial Highlights | 98 | |

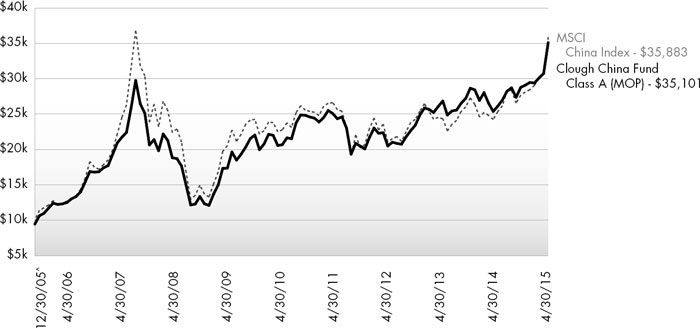

| Clough China Fund | ||

| Management Commentary | 101 | |

| Performance Update | 104 | |

| Statement of Investments | 106 | |

| Statement of Assets and Liabilities | 110 | |

| Statement of Operations | 111 | |

| Statements of Changes in Net Assets | 112 | |

| Financial Highlights | 113 | |

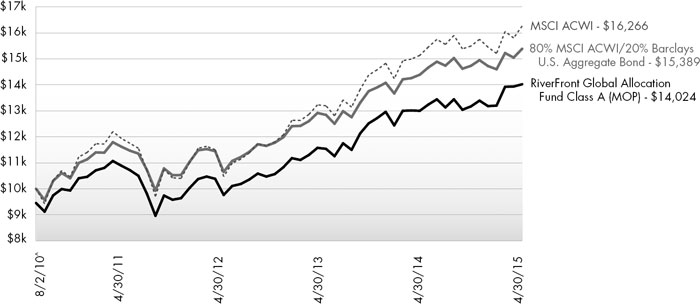

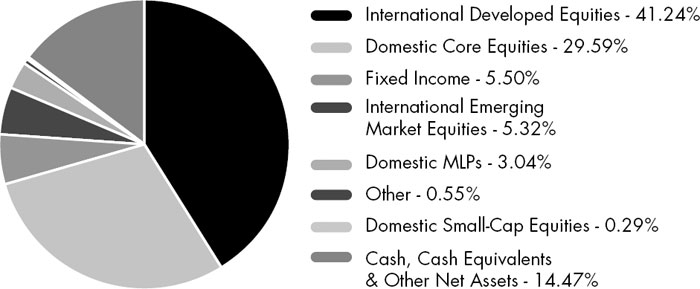

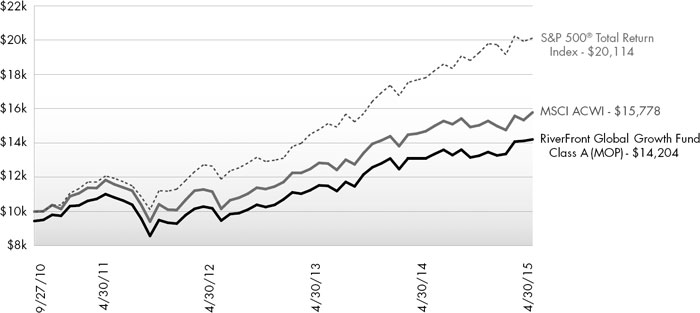

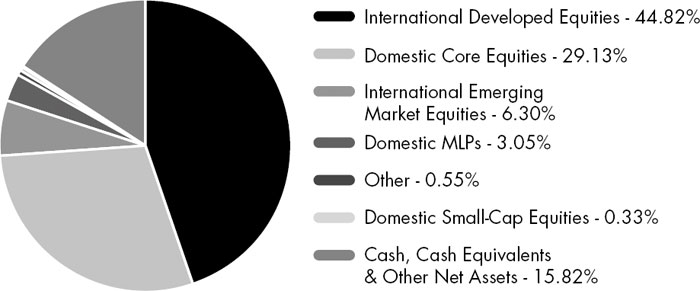

| RiverFront Global Allocation Series | ||

| Management Commentary | 116 | |

| Performance Update | 118 | |

| Statements of Investments | 128 | |

| Statements of Assets and Liabilities | 138 | |

| Statements of Operations | 140 | |

| Statements of Changes in Net Assets | 141 | |

| Financial Highlights | 146 | |

| Notes to Financial Statements | 163 | |

| Additional Information | 194 |

www.alpsfunds.com

| Disclosure of Fund Expenses | |

| April 30, 2015 (Unaudited) |

Examples. As a shareholder of the Funds, you will incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on November 1, 2014 and held until April 30, 2015.

Actual Expenses. The first line under each class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period November 1, 2014 – April 30, 2015” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line under each class in the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other mutual funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges or redemption fees. Therefore, the second line under each class in the following table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

1 | April 30, 2015

| Disclosure of Fund Expenses | |

| April 30, 2015 (Unaudited) |

Beginning Account Value November 1, 2014 | Ending Account Value April 30, 2015 | Expense Ratio(a) | Expenses Paid During Period November 1, 2014 - April 30, 2015(b) | ||||||||||

| ALPS | Alerian MLP Infrastructure Index Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 956.10 | 1.24 | % | $ | 6.01 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,018.65 | 1.24 | % | $ | 6.21 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 954.00 | 1.85 | % | $ | 8.96 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.62 | 1.85 | % | $ | 9.25 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 957.20 | 0.85 | % | $ | 4.12 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.58 | 0.85 | % | $ | 4.26 | |||||

ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund(c) | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 889.10 | 1.45 | % | $ | 6.79 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.60 | 1.45 | % | $ | 7.25 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 887.10 | 2.05 | % | $ | 9.59 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.63 | 2.05 | % | $ | 10.24 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 890.90 | 1.15 | % | $ | 5.39 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

ALPS | Kotak India Growth Fund(d) | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,003.70 | 1.92 | % | $ | 9.54 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.27 | 1.92 | % | $ | 9.59 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,000.30 | 2.60 | % | $ | 12.90 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,011.90 | 2.60 | % | $ | 12.97 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,007.10 | 1.60 | % | $ | 7.96 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,016.86 | 1.60 | % | $ | 8.00 | |||||

| ALPS | Red Rocks Listed Private Equity Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,105.40 | 1.53 | % | $ | 7.99 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.21 | 1.53 | % | $ | 7.65 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,101.10 | 2.12 | % | $ | 11.04 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.28 | 2.12 | % | $ | 10.59 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,108.00 | 1.16 | % | $ | 6.06 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.04 | 1.16 | % | $ | 5.81 | |||||

| Class R | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,104.70 | 1.58 | % | $ | 8.25 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,016.96 | 1.58 | % | $ | 7.90 | |||||

| ALPS | Sterling ETF Tactical Rotation Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,008.70 | 1.54 | % | $ | 7.67 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.16 | 1.54 | % | $ | 7.70 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,005.80 | 2.15 | % | $ | 10.69 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.13 | 2.15 | % | $ | 10.74 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,012.40 | 1.15 | % | $ | 5.74 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

2 | April 30, 2015

| Disclosure of Fund Expenses | |

| April 30, 2015 (Unaudited) |

Beginning Account Value November 1, 2014 | Ending Account Value April 30, 2015 | Expense Ratio(a) | Expenses Paid During Period November 1, 2014 - April 30, 2015(b) | ||||||||||

| ALPS | Westport Resources Hedged High Income Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,004.50 | 2.39 | % | $ | 11.88 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,012.94 | 2.39 | % | $ | 11.93 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,002.60 | 2.99 | % | $ | 14.85 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,009.97 | 2.99 | % | $ | 14.90 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,007.50 | 1.99 | % | $ | 9.91 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.93 | 1.99 | % | $ | 9.94 | |||||

ALPS | WMC Research Value Fund(e) | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,043.50 | 1.40 | % | $ | 7.09 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,017.85 | 1.40 | % | $ | 7.00 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,040.30 | 2.15 | % | $ | 10.88 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,014.13 | 2.15 | % | $ | 10.74 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,045.20 | 1.15 | % | $ | 5.83 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Clough China Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,219.90 | 1.95 | % | $ | 10.73 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.12 | 1.95 | % | $ | 9.74 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,215.00 | 2.70 | % | $ | 14.83 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,011.41 | 2.70 | % | $ | 13.47 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,221.40 | 1.70 | % | $ | 9.36 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,016.36 | 1.70 | % | $ | 8.50 | |||||

| RiverFront Conservative Income Builder Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,020.90 | 1.15 | % | $ | 5.76 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,016.10 | 1.90 | % | $ | 9.50 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.37 | 1.90 | % | $ | 9.49 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,021.10 | 0.90 | % | $ | 4.51 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

| RiverFront Dynamic Equity Income Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,059.00 | 1.15 | % | $ | 5.87 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,055.10 | 1.90 | % | $ | 9.68 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.37 | 1.90 | % | $ | 9.49 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,059.80 | 0.90 | % | $ | 4.60 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

3 | April 30, 2015

| Disclosure of Fund Expenses | |

| April 30, 2015 (Unaudited) |

| Beginning Account Value November 1, 2014 | Ending Account Value April 30, 2015 | Expense Ratio(a) | Expenses Paid During Period November 1, 2014 - April 30, 2015(b) | ||||||||||

| RiverFront Global Allocation Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,064.60 | 1.15 | % | $ | 5.89 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,060.80 | 1.90 | % | $ | 9.71 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.37 | 1.90 | % | $ | 9.49 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,065.70 | 0.90 | % | $ | 4.61 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

| RiverFront Global Growth Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,071.50 | 1.15 | % | $ | 5.91 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,067.70 | 1.90 | % | $ | 9.74 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.37 | 1.90 | % | $ | 9.49 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,072.30 | 0.90 | % | $ | 4.62 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

| Class L | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,073.20 | 0.90 | % | $ | 4.63 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

| Investor Class | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,071.20 | 1.15 | % | $ | 5.91 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| RiverFront Moderate Growth & Income Fund | |||||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,036.90 | 1.15 | % | $ | 5.81 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,019.09 | 1.15 | % | $ | 5.76 | |||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,033.40 | 1.90 | % | $ | 9.58 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,015.37 | 1.90 | % | $ | 9.49 | |||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,038.90 | 0.90 | % | $ | 4.55 | |||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.33 | 0.90 | % | $ | 4.51 | |||||

(a) | Annualized, based on the Fund's most recent fiscal half year expenses. |

(b) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (181), divided by 365. |

(c) | Includes expenses of the CoreCommodity Management Cayman Commodity Fund Ltd. (wholly-owned subsidiary), exclusive of the subsidiary's management fee. |

(d) | Includes expenses of the Kotak Mauritius Portfolio (wholly-owned subsidiary). |

(e) | Prior to February 28, 2015, the ALPS | WMC Research Value Fund was known as the ALPS | WMC Disciplined Value Fund. |

4 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Management Commentary | April 30, 2015 (Unaudited) |

During the six-month period of November 1, 2014 to April 30, 2015 the Alerian MLP Infrastructure Index Fund’s (“Fund”) Class A shares delivered a net return of -4.39% at Net Asset Value. Class A delivered a net return of -9.65% at MOP, Class C was -5.54% with CDSC, and Class I was -4.28%. This compares to the Fund’s index, the Alerian MLP Infrastructure Index (“AMZI”), which returned -8.36% on a price-return and -5.99% on a total-return basis. The difference in performance between the AMZI and the Fund is primarily attributable to the Fund’s operating expenses and the impact of the Fund’s C Corporation tax election.

During the period, the Fund paid a distribution of $0.182 on February 19, representing a 1.1% increase compared to the previous quarter and a 4.6% increase compared to the previous year.

Top contributors to the AMZI during the period include NuStar Energy (NS), TC Pipelines (TCP), Buckeye Partners (BPL), and Western Gas Partners (WES). The majority of the master limited partnerships (MLPs) in the AMZI generated negative returns during the period, including Targa Resource Partners (NGLS), DCP Midstream (DPM), and Williams Partners (WPZ). During the period, Williams Partners (WPZ)* was removed from the AMZI due to its merger with Access Midstream Partners (ACMP), Atlas Pipeline Partners (APL) was removed from the AMZI due to its merger with Targa Resource Partners (NGLS), and Regency Energy Partners (RGP) was removed from the AMZI due to its merger with Energy Transfer Partners (ETP).

The energy markets continued to experience a downward slide during the six-month period ending April 30. West Texas Intermediate (WTI) oil prices fell 46% from $80.53/barrel at the end of October to a low of $43.39/barrel on March 17. Since March however, oil prices have somewhat recovered and found support around the $50-55/barrel range during April, representing a net 30% decline for the six-month period. Directionally, the AMZI performed similarly to oil prices during the period, falling 15.6% from the end of October until mid-March, followed by a seven-week streak of positive returns for a total decline of 8.4% for the six-month period. Despite weak long-term historical correlations to commodity prices, MLPs exhibited a strong correlation to crude prices during the period.

While equity price volatility may persist until crude oil prices stabilize, long-term fundamentals for the energy infrastructure industry still remain intact. Throughout the period, MLPs continued to announce organic projects backed with successful long-term binding commitments. These projects include a new crude oil pipeline from the Permian Basin to the Gulf Coast, a new pipeline moving natural gas liquids (NGLs) from Northwest Louisiana to Mont Belvieu, Texas, and additional pipeline infrastructure in the Northeast to meet increased demand for natural gas and relieve congestion in the current infrastructure grid. In addition, 15 of the 22 MLPs in the AMZI increased their distribution during the first calendar quarter of 2015 and the remaining 7 MLPs maintained their distribution.

Recent comments from the White House in April outlining the need to modernize the current US energy infrastructure grid in order to better support the increasing domestic supply of energy re sources should bode well for energy infrastructure MLPs in the AMZI. With billions of dollars of infrastructure opportunities over the next few decades, we believe that MLPs continue to represent a compelling potential investment opportunity for investors seeking after-tax yield and access to real assets.

| * | After the merger completion, Access Midstream Partners changed its name to Williams Partners and ticker from “ACMP” to “WPZ”. |

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither ALPS Advisors, Inc., Alerian, nor the Fund accept any liability for losses either direct or consequential caused by the use of this information.

5 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Performance Update | April 30, 2015 (Unaudited) |

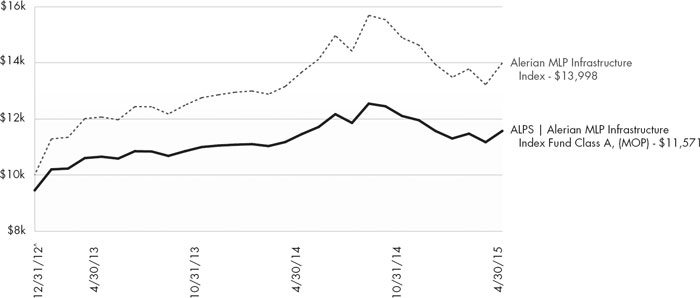

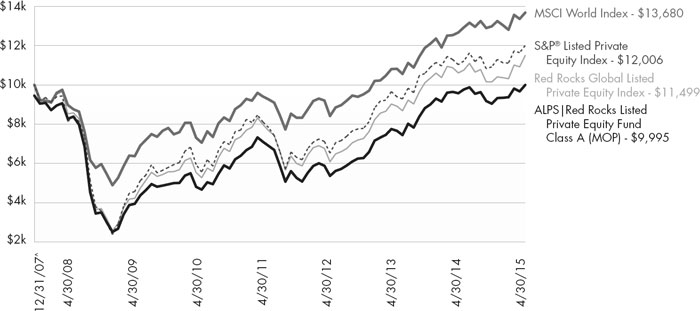

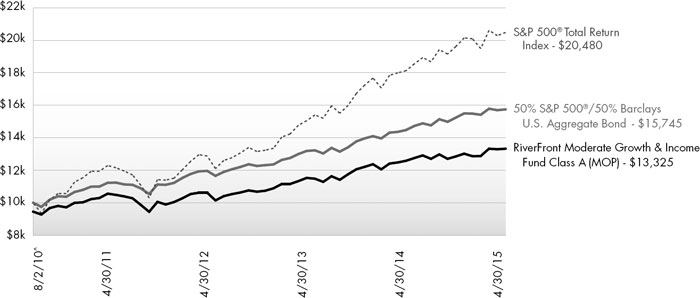

Performance of $10,000 Initial Investment (as of April 30, 2015)

Comparison of change in value of a $10,000 investment (includes maximum sales charges of 5.50%)

Comparison of change in value of a $10,000 investment (includes maximum sales charges of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Average Annual Total Returns (as of April 30, 2015)

| 6 Month | 1 Year | Since Inception^ | Total Expense Ratio* | What You Pay*,** | |||||||||

| Class A (NAV) | -4.39% | 0.98 | % | 9.07 | % | 2.22% | 1.25% | ||||||

| Class A (MOP) | -9.65% | -4.55 | % | 6.47 | % | ||||||||

| Class C (NAV) | -4.60% | 0.52 | % | 8.62 | % | 2.82% | 1.85% | ||||||

| Class C (CDSC) | -5.54% | -0.43 | % | 8.62 | % | ||||||||

| Class I | -4.28% | 1.25 | % | 9.28 | % | 1.81% | 0.85% | ||||||

Alerian MLP Infrastructure Index1 | -5.99% | 2.39 | % | 15.54 | % | ||||||||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data please call 1-866-759-5679.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. If you invest $1 million or more, either as a lump sum or through the Fund’s accumulation or letter of intent programs, you can purchase Class A shares without an initial sales charge (load). A Contingent Deferred Sales Charge (“CDSC”) of 1.00% may apply to Class C shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 18 months after a purchase in excess of $1 million.

Performance less than 1 year is cumulative.

6 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Performance Update | April 30, 2015 (Unaudited) |

1 | Alerian MLP Infrastructure Index is comprised of 25 midstream energy Master Limited Partnerships. The index is not actively managed and does not reflect any deductions for fees, expenses or taxes. An investor may not invest directly in an index. |

^ | Fund inception date of December 31, 2012. |

| * | Excludes deferred income tax expense of 4.49% for Class A, 4.27% for Class C, and 4.63% for Class I. |

| ** | What You Pay reflects the Advisor’s and Sub-Advisor’s decision to contractually limit expenses through February 29, 2016. Please see the prospectus for additional information. |

Investments in securities of MLPs involve risks that differ from an investment in common stock. MLPs are controlled by their general partners, which generally have conflicts of interest and limited fiduciary duties to the MLP, which may permit the general partner to favor its own interests over the MLPs. The benefit you are expected to derive from the Fund’s investment in MLPs depends largely on the MLPs being treated as partnerships for federal income tax purposes. As a partnership, an MLP has no federal income tax liability at the entity level. Therefore, treatment of one or more MLPs as a corporation for federal income tax purposes could affect the Fund’s ability to meet its investment objective and would reduce the amount of cash available to pay or distribute to you. Legislative, judicial, or administrative changes and differing interpretations, possibly on a retroactive basis, could negatively impact the value of an investment in MLPs and therefore the value of your investment in the Fund.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

This Fund is not suitable for all investors and is subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Not FDIC Insured – No Bank Guarantee – May Lose Value

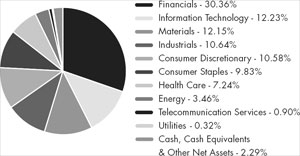

Top Ten Holdings (as a % of Net Assets) †

| Enterprise Products Partners LP | 10.07 | % | ||

| Energy Transfer Partners LP | 7.75 | % | ||

| Magellan Midstream Partners LP | 7.57 | % | ||

| Williams Partners LP | 7.33 | % | ||

| Plains All American Pipeline LP | 7.31 | % | ||

| MarkWest Energy Partners LP | 7.27 | % | ||

| Sunoco Logistics Partners LP | 4.87 | % | ||

| Buckeye Partners LP | 4.83 | % | ||

| Targa Resources Partners LP | 4.78 | % | ||

| ONEOK Partners LP | 4.71 | % | ||

| Top Ten Holdings | 66.49 | % | ||

† | Holdings are subject to change. Table presents approximate values only. |

Industry Sector Allocation (as a % of Total Investments)

7 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Statement of Investments | April 30, 2015 (Unaudited) |

| Shares | Value (Note 2) | |||||||

| MASTER LIMITED PARTNERSHIPS (100.04%) | ||||||||

| Gathering & Processing (30.60%) | ||||||||

| Pipelines (30.60%) | ||||||||

| Crestwood Midstream Partners LP | 40,953 | $ | 649,924 | |||||

| DCP Midstream Partners LP | 24,399 | 995,479 | ||||||

| EnLink Midstream Partners LP | 28,505 | 733,434 | ||||||

| MarkWest Energy Partners LP | 37,221 | 2,510,929 | ||||||

| Targa Resources Partners LP | 36,333 | 1,650,972 | ||||||

| Western Gas Partners LP | 20,521 | 1,495,776 | ||||||

| Williams Partners LP | 51,221 | 2,530,317 | ||||||

| 10,566,831 | ||||||||

| TOTAL GATHERING & PROCESSING | 10,566,831 | |||||||

| Natural Gas Transportation (29.87%) | ||||||||

| Pipelines (29.87%) | ||||||||

| Energy Transfer Partners LP | 46,312 | 2,675,928 | ||||||

| Enterprise Products Partners LP | 101,514 | 3,476,854 | ||||||

| EQT Midstream Partners LP | 10,479 | 924,248 | ||||||

| ONEOK Partners LP | 38,804 | 1,627,828 | ||||||

| Spectra Energy Partners LP | 14,170 | 767,730 | ||||||

| TC PipeLines LP | 12,386 | 843,239 | ||||||

| 10,315,827 | ||||||||

| TOTAL NATURAL GAS TRANSPORTATION | 10,315,827 | |||||||

| Petroleum Transportation (39.57%) | ||||||||

| Pipelines (39.57%) | ||||||||

| Buckeye Partners LP | 20,460 | 1,669,127 | ||||||

| Enbridge Energy Partners LP | 43,133 | 1,601,959 | ||||||

| Genesis Energy LP | 21,297 | 1,058,674 | ||||||

| Magellan Midstream Partners LP | 31,302 | 2,613,717 | ||||||

| NGL Energy Partners LP | 19,649 | 574,930 | ||||||

| NuStar Energy LP | 17,269 | 1,160,131 | ||||||

| Plains All American Pipeline LP | 50,409 | 2,525,995 | ||||||

| Sunoco Logistics Partners LP | 37,947 | 1,683,329 | ||||||

| Tesoro Logistics LP | 13,827 | 774,727 | ||||||

| 13,662,589 | ||||||||

| TOTAL PETROLEUM TRANSPORTATION | 13,662,589 | |||||||

| TOTAL MASTER LIMITED PARTNERSHIPS (Cost $32,607,698) | 34,545,247 | |||||||

7-Day Yield | Shares | Value (Note 2) | ||||||||||

| SHORT TERM INVESTMENTS (3.07%) | ||||||||||||

| Money Market Fund (3.07%) | ||||||||||||

| Morgan Stanley Institutional Liquidity Fund - Prime Portfolio | 0.077 | % | 1,060,633 | $ | 1,060,633 | |||||||

| TOTAL SHORT TERM INVESTMENTS (Cost $1,060,633) | 1,060,633 | |||||||||||

| TOTAL INVESTMENTS (103.11%) (Cost $33,668,331) | $ | 35,605,880 | ||||||||||

| Liabilities In Excess Of Other Assets (-3.11%) | (1,074,060 | ) | ||||||||||

| NET ASSETS (100.00%) | $ | 34,531,820 | ||||||||||

Common Abbreviations:

LP - Limited Partnerships.

For Fund compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percent of net assets.

See Notes to Financial Statements.

8 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Statement of Assets and Liabilities | April 30, 2015 (Unaudited) |

| ASSETS | ||||

| Investments, at value | $ | 35,605,880 | ||

| Receivable for investments sold | 1,654,948 | |||

| Receivable for shares sold | 455,103 | |||

| Dividends receivable | 192,904 | |||

| Income tax receivable | 3,139 | |||

| Prepaid expenses and other assets | 25,366 | |||

| Total Assets | 37,937,340 | |||

| LIABILITIES | ||||

| Payable for investments purchased | 2,689,874 | |||

| Deferred tax liability | 451,821 | |||

| Franchise tax payable | 2,660 | |||

| Payable for shares redeemed | 201,553 | |||

| Investment advisory fees payable | 4,803 | |||

| Administration and transfer agency fees payable | 3,568 | |||

| Distribution and services fees payable | 16,095 | |||

| Trustees’ fees and expenses payable | 95 | |||

| Professional fee payable | 18,080 | |||

| Accrued expenses and other liabilities | 16,971 | |||

| Total Liabilities | 3,405,520 | |||

| NET ASSETS | $ | 34,531,820 | ||

| NET ASSETS CONSIST OF | ||||

| Paid-in capital | $ | 34,072,835 | ||

| Accumulated net investment loss, net of deferred income taxes | (285,799 | ) | ||

| Accumulated net realized loss on investments, net of deferred income taxes | (503,354 | ) | ||

| Net unrealized appreciation on investments, net of deferred income taxes | 1,248,138 | |||

| NET ASSETS | $ | 34,531,820 | ||

| INVESTMENTS, AT COST | $ | 33,668,331 | ||

| PRICING OF SHARES | ||||

| Class A: | ||||

| Net Asset Value, offering and redemption price per share | $ | 10.64 | ||

| Net Assets | $ | 17,093,294 | ||

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 1,607,267 | |||

| Maximum offering price per share ((NAV/0.9450), based on maximum sales charge of 5.50% of the offering price) | $ | 11.26 | ||

| Class C: | ||||

Net Asset Value, offering and redemption price per share(a) | $ | 10.53 | ||

| Net Assets | $ | 10,321,364 | ||

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 979,815 | |||

| Class I: | ||||

| Net Asset Value, offering and redemption price per share | $ | 10.69 | ||

| Net Assets | $ | 7,117,162 | ||

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | 665,822 | |||

(a) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. For a description of a possible sales charge, please see the Fund’s Prospectus. |

See Notes to Financial Statements.

9 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund | |

| Statement of Operations | For the Six Months Ended April 30, 2015 (Unaudited) |

| INVESTMENT INCOME | ||||

| Dividends | $ | 101 | ||

| Distributions from master limited partnerships | 689,641 | |||

| Less return of capital distributions | (689,641 | ) | ||

| Total Investment Income | 101 | |||

| EXPENSES | ||||

| Investment advisory fees | 99,288 | |||

| Administrative fees | 14,868 | |||

| Transfer agency fees | 488 | |||

| Distribution and service fees | ||||

| Class A | 24,479 | |||

| Class C | 45,170 | |||

| Professional fees | 44,640 | |||

| Reports to shareholders and printing fees | 1,619 | |||

| State registration fees | 21,444 | |||

| SEC registration fees | 521 | |||

| Insurance fees | 143 | |||

| Custody fees | 7,943 | |||

| Trustees’ fees and expenses | 327 | |||

| Miscellaneous expenses | 8,892 | |||

| Total Expenses | 269,822 | |||

| Less fees waived/reimbursed by investment advisor (Note 8) | ||||

| Class A | (35,672 | ) | ||

| Class C | (25,325 | ) | ||

| Class I | (18,612 | ) | ||

| Net Expenses | 190,213 | |||

| Net Investment Loss, Before Income Taxes | (190,112 | ) | ||

| Deferred income tax benefit | 41,621 | |||

| Deferred income tax benefit - Class A | 9,136 | |||

| Deferred income tax benefit - Class C | 16,261 | |||

| Net Investment Loss, Net of Income Taxes | (123,094 | ) | ||

| REALIZED AND UNREALIZED GAIN/(LOSS) | ||||

| Net realized loss on investments, before income taxes | (137,362 | ) | ||

| Deferred income tax benefit | 48,730 | |||

| Net Realized Loss on investments, Net of Income Taxes | (88,632 | ) | ||

| Net change in unrealized appreciation on investment, before deferred income taxes | (1,528,380 | ) | ||

| Deferred income tax expense | 552,396 | |||

| Net Change in Unrealized Appreciation on Investments | (975,984 | ) | ||

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS, NET OF INCOME TAXES | (1,064,616 | ) | ||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (1,187,710 | ) | |

See Notes to Financial Statements.

10 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund |

| Statements of Changes in Net Assets |

For the Six Months Ended April 30, 2015 (Unaudited) | For the Fiscal Period Ended October 31, 2014(a) | |||||||

| OPERATIONS | ||||||||

| Net investment loss, net of income taxes | $ | (123,094 | ) | $ | (84,514 | ) | ||

| Net realized gain/(loss) on investments, net of income taxes | (88,632 | ) | 3,372 | |||||

| Net change in unrealized appreciation/(depreciation) on investments, net of deferred income taxes | (975,984 | ) | 902,714 | |||||

| Net Increase/(Decrease) in Net AssetsResulting from Operations | (1,187,710 | ) | 821,572 | |||||

| DISTRIBUTIONS | ||||||||

| Dividends to shareholders from net investment income | ||||||||

| Class A | (24,107 | ) | (26,390 | ) | ||||

| Class C | (18,360 | ) | (32,401 | ) | ||||

| Class I | (11,722 | ) | (36,117 | ) | ||||

| Dividends to shareholders from tax return of capital | ||||||||

| Class A | (187,466 | ) | (422,657 | ) | ||||

| Class C | (142,772 | ) | (205,706 | ) | ||||

| Class I | (91,157 | ) | (200,052 | ) | ||||

| Net Decrease in Net Assets from Distributions | (475,584 | ) | (923,323 | ) | ||||

| BENEFICIAL INTEREST TRANSACTIONS (NOTE 6) | ||||||||

| Shares sold | ||||||||

| Class A | 8,318,067 | 3,317,091 | ||||||

| Class C | 5,402,989 | 3,457,848 | ||||||

| Class I | 4,163,046 | 5,196,869 | ||||||

| Dividends reinvested | ||||||||

| Class A | 199,739 | 427,003 | ||||||

| Class C | 160,017 | 178,058 | ||||||

| Class I | 102,150 | 219,273 | ||||||

| Shares redeemed | ||||||||

| Class A | (1,318,423 | ) | (1,375,093 | ) | ||||

| Class C | (1,484,998 | ) | (245,100 | ) | ||||

| Class I | (3,396,938 | ) | (184,339 | ) | ||||

| Net Increase in Net Assets Derived from Beneficial Interest Transactions | 12,145,649 | 10,991,610 | ||||||

| Net increase in net assets | 10,482,355 | 10,889,859 | ||||||

| NET ASSETS | ||||||||

| Beginning of period | 24,049,465 | 13,159,606 | ||||||

| End of period * | $ | 34,531,820 | $ | 24,049,465 | ||||

| *Including accumulated net investment loss, net of deferred income taxes, of: | $ | (285,799 | ) | $ | (162,705 | ) | ||

(a) | Effective May 1, 2014, the Board approved changing the fiscal year-end of the Funds from April 30 to October 31. |

See Notes to Financial Statements.

11 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund – Class A |

| Financial Highlights |

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| For the Period | ||||||||||||||||

| For the Six | For the Fiscal | January 2, 2013 | ||||||||||||||

| Months Ended | Period Ended | For the Year | (Commencement) | |||||||||||||

| April 30, 2015 | October 31, | Ended | to | |||||||||||||

| (Unaudited) | 2014(a) | April 30, 2014 | April 30, 2013 | |||||||||||||

| Net asset value, beginning of period | $ | 11.32 | $ | 11.23 | $ | 11.10 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||||||

Net investment loss(b) | (0.04 | ) | (0.05 | ) | (0.09 | ) | (0.03 | ) | ||||||||

| Net realized and unrealized gain/(loss) | (0.46 | ) | 0.67 | 0.90 | 1.29 | |||||||||||

| Total from investment operations | (0.50 | ) | 0.62 | 0.81 | 1.26 | |||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| From net investment income | (0.02 | ) | (0.03 | ) | (0.36 | ) | – | |||||||||

| From tax return of capital | (0.16 | ) | (0.50 | ) | (0.32 | ) | (0.16 | ) | ||||||||

| Total distributions | (0.18 | ) | (0.53 | ) | (0.68 | ) | (0.16 | ) | ||||||||

| Net increase/(decrease) in net asset value | (0.68 | ) | 0.09 | 0.13 | 1.10 | |||||||||||

| Net asset value, end of period | $ | 10.64 | $ | 11.32 | $ | 11.23 | $ | 11.10 | ||||||||

TOTAL RETURN(c) | (4.39 | )% | 5.61 | % | 7.59 | % | 12.68 | % | ||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||

| Net assets, end of period (000s) | $ | 17,093 | $ | 10,619 | $ | 8,223 | $ | 928 | ||||||||

| Ratio of expenses to average net assets before waivers, franchise tax expense and income tax expense/benefit | 1.80 | %(d) | 2.20 | %(d) | 3.09 | % | 5.51 | %(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.97 | %)(d) | (1.84 | %) | (4.26 | %)(d)(e) | ||||||||

| Ratio of expenses to average net assets net of waivers before franchise tax expense and income tax expense/benefit | 1.24 | %(d)(f) | 1.23 | %(d)(f) | 1.25 | % | 1.25 | %(d)(e) | ||||||||

Ratio of franchise tax expense and deferred income tax expense to average net assets(g) | 4.68 | %(d) | 4.49 | %(d) | 5.38 | % | 20.55 | %(d) | ||||||||

| Ratio of total expenses to average net assets | 5.92 | %(d) | 5.72 | %(d) | 6.63 | % | 21.80 | %(d) | ||||||||

| Ratio of investment loss to average net assets before waivers, franchise tax expense and income tax expense/benefit | (1.80 | %)(d) | (2.20% | )(d) | (3.09 | %) | (5.51 | %)(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.97 | %)(d) | (1.84 | %) | (4.26 | %)(d)(e) | ||||||||

| Ratio of investment loss to average net assets net of waivers before franchise tax expense and income tax expense/benefit | (1.24 | %)(d)(f) | (1.23 | %)(d)(f) | (1.25 | %) | (1.25% | )(d)(e) | ||||||||

Ratio of franchise tax expense and deferred income tax benefit to average net assets(h) | 0.44 | %(d) | 0.43 | %(d) | 0.43 | % | 0.40 | %(d) | ||||||||

| Ratio of net investment loss to average net assets | (0.80 | %)(d) | (0.80 | %)(d) | (0.82 | %) | (0.85 | %)(d) | ||||||||

Portfolio turnover rate(i) | 35 | % | 7 | % | 63 | % | 3 | % | ||||||||

See Notes to Financial Statements.

12 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund – Class A |

| Financial Highlights |

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

(a) | Effective May 1, 2014, the Board approved changing the fiscal year-end of the Funds from April 30 to October 31. |

(b) | Calculated using the average shares method. |

(c) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

(d) | Annualized. |

(e) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

(f) | According to the Fund’s shareholder services plan with respect to the Fund’s Class A shares, any amount of such payment not paid during the Fund’s fiscal year for such service activities shall be reimbursed to the Fund as soon as practical after the end of the fiscal year. Fees were reimbursed to the Fund during the period ended April 30, 2015 and October 31, 2014, for the prior fiscal year in the amount of 0.01% and 0.02% of average net assets of Class A shares respectively. |

(g) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

(h) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

(i) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

13 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund – Class C |

| Financial Highlights |

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| For the Period | ||||||||||||||||

| For the Six | For the Fiscal | January 2, 2013 | ||||||||||||||

| Months Ended | Period Ended | For the Year | (Commencement) | |||||||||||||

| April 30, 2015 | October 31, | Ended | to | |||||||||||||

| (Unaudited) | 2014(a) | April 30, 2014 | April 30, 2013 | |||||||||||||

| Net asset value, beginning of period | $ | 11.23 | $ | 11.17 | $ | 11.09 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||||||

Net investment loss(b) | (0.06 | ) | (0.07 | ) | (0.13 | ) | (0.05 | ) | ||||||||

| Net realized and unrealized gain/(loss) | (0.46 | ) | 0.66 | 0.89 | 1.30 | |||||||||||

| Total from investment operations | (0.52 | ) | 0.59 | 0.76 | 1.25 | |||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| From net investment income | (0.02 | ) | (0.08 | ) | (0.35 | ) | – | |||||||||

| From tax return of capital | (0.16 | ) | (0.45 | ) | (0.33 | ) | (0.16 | ) | ||||||||

| Total distributions | (0.18 | ) | (0.53 | ) | (0.68 | ) | (0.16 | ) | ||||||||

| Net increase/(decrease) in net asset value | (0.70 | ) | 0.06 | 0.08 | 1.09 | |||||||||||

| Net asset value, end of period | $ | 10.53 | $ | 11.23 | $ | 11.17 | $ | 11.09 | ||||||||

TOTAL RETURN(c) | (4.60 | )% | 5.37 | % | 7.13 | % | 12.58 | % | ||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||

| Net assets, end of period (000s) | $ | 10,321 | $ | 6,773 | $ | 3,429 | $ | 563 | ||||||||

| Ratio of expenses to average net assets before waivers, franchise tax expense and income tax expense/benefit | 2.41 | %(d) | 2.82 | %(d) | 3.71 | % | 7.01 | %(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.97 | %)(d) | (1.86 | %) | (5.16 | %)(d)(e) | ||||||||

| Ratio of expenses to average net assets net of waivers before franchise tax expense and income tax expense/benefit | 1.85 | %(d) | 1.85 | %(d) | 1.85 | % | 1.85 | %(d)(e) | ||||||||

Ratio of franchise tax expense and deferred income tax expense to average net assets(f) | 4.89 | %(d) | 4.27 | %(d) | 5.16 | % | 20.55 | %(d) | ||||||||

| Ratio of total expenses to average net assets | 6.74 | %(d) | 6.12 | %(d) | 7.01 | % | 22.40 | %(d) | ||||||||

| Ratio of investment loss to average net assets before waivers,franchise tax expense and income tax expense/benefit | (2.41 | %)(d) | (2.82 | %)(d) | (3.71 | %) | (7.01 | %)(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.97 | %)(d) | (1.86 | %) | (5.16 | %)(d)(e) | ||||||||

| Ratio of investment loss to average net assets net of waivers before franchise tax expense and income tax expense/benefit | (1.85 | %)(d) | (1.85 | %)(d) | (1.85 | %) | (1.85 | %)(d)(e) | ||||||||

Ratio of franchise tax expense and deferred income tax benefit to average net assets(g) | 0.65 | %(d) | 0.65 | %(d) | 0.65 | % | 0.40 | %(d) | ||||||||

| Ratio of net investment loss to average net assets | (1.20 | %)(d) | (1.20 | %)(d) | (1.20 | %) | (1.45 | %)(d) | ||||||||

Portfolio turnover rate(h) | 35 | % | 7 | % | 63 | % | 3 | % | ||||||||

(a) | Effective May 1, 2014, the Board approved changing the fiscal year-end of the Funds from April 30 to October 31. |

(b) | Calculated using the average shares method. |

(c) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns shown exclude any applicable sales charges. |

(d) | Annualized. |

(e) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

(f) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

(g) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

(h) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

14 | April 30, 2015

| ALPS | Alerian MLP Infrastructure Index Fund – Class I |

| Financial Highlights |

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| For the Period | ||||||||||||||||

| For the Six | For the Fiscal | January 2, 2013 | ||||||||||||||

| Months Ended | Period Ended | For the Year | (Commencement) | |||||||||||||

| April 30, 2015 | October 31, | Ended | to | |||||||||||||

| (Unaudited) | 2014(a) | April 30, 2014 | April 30, 2013 | |||||||||||||

| Net asset value, beginning of period | $ | 11.36 | $ | 11.25 | $ | 11.11 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | ||||||||||||||||

Net investment loss(b) | (0.03 | ) | (0.03 | ) | (0.06 | ) | (0.02 | ) | ||||||||

| Net realized and unrealized gain/(loss) | (0.46 | ) | 0.67 | 0.88 | 1.29 | |||||||||||

| Total from investment operations | (0.49 | ) | 0.64 | 0.82 | 1.27 | |||||||||||

| DISTRIBUTIONS: | ||||||||||||||||

| From net investment income | (0.02 | ) | (0.04 | ) | (0.27 | ) | – | |||||||||

| From tax return of capital | (0.16 | ) | (0.49 | ) | (0.41 | ) | (0.16 | ) | ||||||||

| Total distributions | (0.18 | ) | (0.53 | ) | (0.68 | ) | (0.16 | ) | ||||||||

| Net increase/(decrease) in net asset value | (0.67 | ) | 0.11 | 0.14 | 1.11 | |||||||||||

| Net asset value, end of period | $ | 10.69 | $ | 11.36 | $ | 11.25 | $ | 11.11 | ||||||||

TOTAL RETURN(c) | (4.28 | )% | 5.78 | % | 7.68 | % | 12.78 | % | ||||||||

| RATIOS/SUPPLEMENTAL DATA: | ||||||||||||||||

| Net assets, end of period (000s) | $ | 7,117 | $ | 6,658 | $ | 1,507 | $ | 2,256 | ||||||||

| Ratio of expenses to average net assets before waivers, franchise tax expense and income tax expense/benefit | 1.41 | %(d) | 1.81 | %(d) | 3.03 | % | 6.01 | %(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.96 | %)(d) | (2.18 | %) | (5.16 | )%(d)(e) | ||||||||

| Ratio of expenses to average net assets net of waivers before franchise tax expense and income tax expense/benefit | 0.85 | %(d) | 0.85 | %(d) | 0.85 | % | 0.85 | %(d)(e) | ||||||||

Ratio of franchise tax expense and deferred income tax expense to average net assets(f) | 4.53 | %(d) | 4.63 | %(d) | 5.53 | % | 20.55 | %(d) | ||||||||

| Ratio of total expenses to average net assets | 5.38 | %(d) | 5.48 | %(d) | 6.38 | % | 21.40 | %(d) | ||||||||

| Ratio of investment loss to average net assets before waivers,franchise tax expense and income tax expense/benefit | (1.41 | %)(d) | (1.81 | %)(d) | (3.03 | %) | (6.01 | %)(d)(e) | ||||||||

| Ratio of expense waivers to average net assets | (0.56 | %)(d) | (0.96 | %)(d) | (2.18 | %) | (5.16 | %)(d)(e) | ||||||||

| Ratio of investment loss to average net assets net of waivers before franchise tax expense and income tax expense/benefit | (0.85 | %)(d) | (0.85 | %)(d) | (0.85 | %) | (0.85 | %)(d)(e) | ||||||||

| Ratio of franchise tax expense and deferred income tax benefit to | ||||||||||||||||

average net assets(g) | 0.29 | %(d) | 0.28 | %(d) | 0.29 | % | 0.40 | %(d) | ||||||||

| Ratio of net investment loss to average net assets | (0.56 | %)(d) | (0.57% | )(d) | (0.56 | %) | (0.45 | %)(d) | ||||||||

Portfolio turnover rate(h) | 35 | % | 7 | % | 63 | % | 3 | % | ||||||||

(a) | Effective May 1, 2014, the Board approved changing the fiscal year-end of the Funds from April 30 to October 31. |

(b) | Calculated using the average shares method. |

(c) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(d) | Annualized. |

(e) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

(f) | Deferred income tax expense estimate for the ratio calculation is derived from the net investment loss, and realized and unrealized gains/losses. |

(g) | Deferred income tax benefit for the ratio calculation is derived from net investment loss only. |

(h) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

15 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Management Commentary | April 30, 2015 (Unaudited) |

Commodity prices for the six month period ending April 30, 2015 were lower: Spot commodity prices, as measured by the diversified Bloomberg Commodity Spot Index (BCOMSP), were down, -8.69% during this period. Commodity equities, evaluated against the Standard & Poor’s Global Natural Resources Total Return Index (SPGNRUN), were modestly lower, -1.39% for the period. The ALPS CoreCommodity Management CompleteCommodities® Strategy Fund (JCRIX) delivered a net negative total return of -10.91% for the period (JCRAX was -11.09% and JCRCX was down -11.29%). The Bloomberg Commodity Total Return Index (BCOMTR) declined-11.87% during the same period.

The ALPS CoreCommodity CompleteCommodities® Strategy Fund aspires to deliver returns close to spot commodity results. Spot commodity prices are essentially uninvestable. For the six months ending April 30, 2015, the ALPS CoreCommodity CompleteCommodities® Strategy Fund (“I” Shares—JCRIX) underperformed spot commodity returns Bloomberg Commodity Spot Index (BCOMSP) by 222 basis points after fees. The Fund employs a strategy that combines an actively managed portfolio of commodity futures related exposure (collateralized by Treasury Inflation Protected Securities – TIPS), commodity equities, and physical commodity Exchange-Traded Funds. The Fund maintains a well-diversified exposure to all sectors of the commodity markets without leverage. While the exact composition of the Fund changes from time to time in response to structural and value opportunities identified by the Fund Policy Committee, the Fund allocated approximately 66% of its assets toward commodity futures related investments and approximately 34% of its assets in commodity equities on average throughout the year. The Fund was about 99% invested by the end of April.

With a few exceptions, commodity prices were under price pressure for the six month period ending in April 30, 2015. Disappointing global growth rates may have contributed to the underperformance of commodity prices generally. The strength of the US Dollar likely created additional headwinds for commodity prices. Since most commodities are traded in US currency, commodity prices tend to move inversely to USD fluctuations. For the six month period we are examining, the USD climbed by approximately +8%, accounting for substantially all of the losses suffered by the BCOMSP Spot Index.

Energy prices were particularly weak during the 6-month period ending April 30, 2015. West Texas Intermediate (WTI) crude oil, the US marker crude, fell by -24.62%. Natural gas dropped even more, down -28.97%. Technological advances in drilling and gathering techniques increased supplies primarily in North America. Underwhelming global growth kept energy demand at a slower pace. A significant oversupply situation ensued and prices declined substantially to reflect the balance shift.

Additionally, many agricultural prices were also pressured lower. Political and economic stress in South America, specifically in Brazil and Argentina, pushed local currencies lower. Farmers were encouraged to sell their crops to monetize their assets and to receive foreign currency. Coffee, sugar, and orange juice prices were down -26.89%, -17.83%, and -16.96% respectively. Favorable early weather patterns supported early planting and optimistic outlooks for wheat and soybean supplies. Wheat prices fell by -10.99% while soybeans declined by -6.98%.

Base metals prices were also influenced by the move in the US Dollar, but generally did not lose as much as the Dollar appreciated. Copper prices edged down by -5.27%. Aluminum was off by -6.93% and Nickel dropped by -11.56%.

Precious metals benefited from the announcement by the ECB (European Central Bank) to pursue an aggressive low interest rate campaign through quantitative easing. The measures were perceived as a highly stimulative attempt to lower the value of the Euro and to manage the level of European interest rates to the downside. Gold managed a modest gain of +0.92% and silver added +0.11%. Considering the magnitude of the US Dollar’s advance, the performance of precious metals was positive.

{The Fund’s top equity holdings at the end of April 2015 included Sanderson Farms (SAFM) -10.60 YTD, Monsanto (MON) -4.61% YTD, CF Industries (CF) +5.48% YTD, Mosaic (MOS) -3.61% YTD, Pilgrim’s Pride (PPC) -24.67% YTD, FMC Corp (FMC) +4.00% YTD, AGCO Corporation (AGCO) +13.96% YTD, CNOOC Ltd-ADR +26.44% YTD, Hormel Foods Corp (HRL) +4.32% YTD, and K+S Ag (SDF GR)+27.58% YTD}

US Treasuries and/or U.S. Treasury Inflation Protected Bonds or TIPS are held by the Fund to invest excess cash and as collateral for commodity futures related investments held in our Cayman Island subsidiary. Nominal yield on the US Treasury benchmark 10-year note stood at 2.25% in the beginning of November 2014. It had declined to 2.03%, at the end of April. 10 year rates dipped to 1.64% in mid-March as the effects of European Central Bank policies to purchase European Union debt through quantitative easing spread globally to other bond rates. Despite the efforts by the Federal Reserve and other central banks to maintain historically low interest rates, we believe we may be nearing the end of what has been a significant multi-year rally in US treasury prices. As a result, we continue to invest in TIPS with limited duration exposure along with short-dated US Treasury Bills. At the end of April, our weighted average maturity was approximately 1.15 years in our TIPS portion of the collateral.

We strongly believe that the long term fundamental drivers of commodity demand and ultimately higher prices are still in place. The recent underperformance of commodity prices relative to the Standard and Poor’s 500 Index (S&P) may be a temporary phenomenon. Population growth is likely to remain unabated regardless of the economic environment in the US and Europe. A billion more people will probably be added to the world population over the next decade. The trend of wealth distribution to the developing world as those economies grow at rapid rates relative to the slow or negative growth occurring in the developed countries is likely contributing to ever increasing demand for raw materials and food. Incremental gains in disposable income in the developing nations have led to competition for the commodities needed for more complex and costly lifestyles. In a world with limited supplies of food, fuel, building materials, and other necessities of life, price may become the ultimate allocator. Additionally, the aggressively accommodative central bank monetary policies recently announced coupled with measures already in place globally are likely to make commodities and other real assets more attractive over time as currencies, including the US Dollar, may decline in value.

Satch Chada

Co-Portfolio Manager

Robert Hyman

Co-Portfolio Manager

16 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Management Commentary | April 30, 2015 (Unaudited) |

Standard & Poor’s 500 Index is a composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices. An investor may not invest directly in an index.

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither the Fund nor CoreCommodity Management, LLC accepts any liability for losses either direct or consequential caused by the use of this information.

Diversification cannot guarantee gain or prevent losses.

17 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Performance Update | April 30, 2015 (Unaudited) |

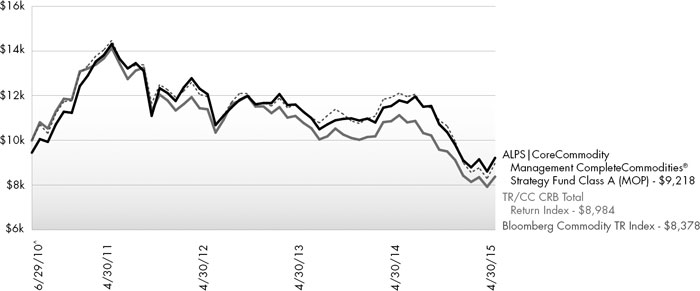

Performance of $10,000 Initial Investment (as of April 30, 2015)

Comparison of change in value of a $10,000 investment (includes maximum sales charges of 5.50%)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Average Annual Total Returns (as of April 30, 2015)

| 6 Month | 1 Year | 3 Year | Since Inception^ | Total Expense Ratio | What You Pay* | |

| Class A (NAV) | -11.09% | -21.80% | -8.58% | -0.52% | 1.46% | 1.45% |

| Class A (MOP) | -16.01% | -26.09% | -10.29% | -1.67% | ||

| Class C (NAV) | -11.29% | -22.22% | -9.12% | -1.07% | 2.07% | 2.05% |

| Class C (CDSC) | -12.18% | -23.00% | -9.12% | -1.07% | ||

| Class I | -10.91% | -21.49% | -8.31% | -0.22% | 1.16% | 1.15% |

TR/CC CRB Total Return Index1 | -15.61% | -25.84% | -9.09% | -2.19% | ||

Bloomberg Commodity TR Index1 | -11.87% | -24.69% | -9.73% | -3.59% |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please call 1-866-759-5679.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. If you invest $1 million or more, either as a lump sum or through the Fund’s accumulation or letter of intent programs, you can purchase Class A shares without an initial sales charge (load). A Contingent Deferred Sales Charge (“CDSC”) of 1.00% may apply to Class C shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 18 months after a purchase in excess of $1 million. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days.

Performance less than 1 year is cumulative.

18 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Performance Update | April 30, 2015 (Unaudited) |

| 1 | Thomson Reuters/CC CRB Total Return Index and the Bloomberg Commodity TR Index (formerly the Dow Jones-UBS Commodity Index) are unmanaged indices used as a measurement of change in commodity market conditions based on the performance of a basket of different commodities. Each index is composed of a different basket of commodities, a different weighting of the commodities in the basket, and a different re-balancing schedule. The indices are not actively managed and do not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund Inception date of June 29, 2010. |

| * | What You Pay reflects the Advisor’s decision to contractually limit expenses through February 29, 2016. Please see the prospectus for additional information. |

Investments in securities of MLPs involve risks that differ from an investment in common stock. MLPs are controlled by their general partners, which generally have conflicts of interest and limited fiduciary duties to the MLP, which may permit the general partner to favor its own interests over the MLPs. The benefit you are expected to derive from the Fund’s investment in MLPs depends largely on the MLPs being treated as partnerships for federal income tax purposes. As a partnership, an MLP has no federal income tax liability at the entity level. Therefore, treatment of one or more MLPs as a corporation for federal income tax purposes could affect the Fund’s ability to meet its investment objective and would reduce the amount of cash available to pay or distribute to you. Legislative, judicial, or administrative changes and differing interpretations, possibly on a retroactive basis, could negatively impact the value of an investment in MLPs and therefore the value of your investment in the Fund.

Investing in commodity-related securities involves risk and considerations not present when investing in more conventional securities. The Fund may be more susceptible to high volatility of commodity markets.

Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund’s original investment.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

This Fund is not suitable for all investors, and is subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund’s top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Not FDIC Insured – No Bank Guarantee – May Lose Value

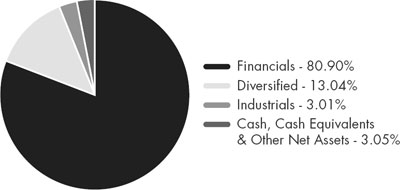

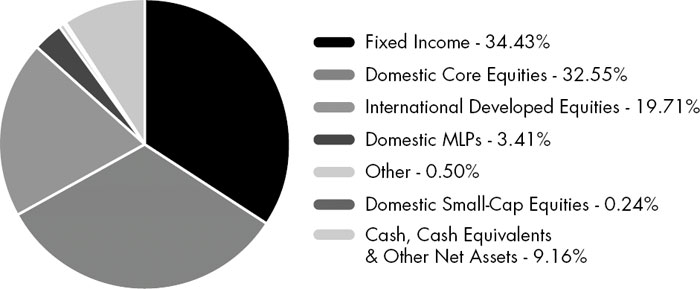

Asset Type Allocation (as a % of Net Assets) †

| Government Bonds | 50.55% |

| Common Stocks | 33.56% |

| Commodity-Linked Notes | 0.91% |

| Master Limited Partnerships | 0.43% |

| Purchased Options | 0.12% |

| Short Term Investments and Other Assets | 14.43% |

| Total | 100.00% |

| † | Holdings are subject to change. Table presents approximate values only. |

19 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Consolidated Statement of Investments | April 30, 2015 (Unaudited) |

| Value | ||||||||

| Shares | (Note 2) | |||||||

| COMMON STOCKS (33.56%) | ||||||||

| Argentina (0.19%) | ||||||||

| YPF SA, Sponsored ADR | 27,285 | $ | 833,284 | |||||

| Australia (1.17%) | ||||||||

| BHP Billiton, Ltd. | 68,819 | 1,741,084 | ||||||

| Caltex Australia, Ltd. | 14,292 | 400,712 | ||||||

| Fortescue Metals Group, Ltd. | 31,313 | 53,772 | ||||||

| GrainCorp, Ltd., Class A | 41,007 | 321,588 | ||||||

| Iluka Resources, Ltd. | 60,429 | 390,215 | ||||||

| Incitec Pivot, Ltd. | 188,051 | 593,769 | ||||||

Newcrest Mining, Ltd.(a) | 28,587 | 326,893 | ||||||

| Nufarm, Ltd. | 36,328 | 209,574 | ||||||

| Orica, Ltd. | 38,628 | 617,479 | ||||||

Regis Resources, Ltd. (a) | 206,540 | 205,124 | ||||||

| Sandfire Resources NL | 41,755 | 162,571 | ||||||

| Woodside Petroleum, Ltd. | 9,366 | 259,783 | ||||||

| 5,282,564 | ||||||||

| Austria (0.19%) | ||||||||

| OMV AG | 10,960 | 366,116 | ||||||

| Voestalpine AG | 11,421 | 479,877 | ||||||

| 845,993 | ||||||||

| Bermuda (0.17%) | ||||||||

Kosmos Energy, Ltd.(a) | 50,884 | 497,646 | ||||||

| Nabors Industries, Ltd. | 11,916 | 198,997 | ||||||

| Seadrill, Ltd. | 4,179 | 54,703 | ||||||

| 751,346 | ||||||||

| Brazil (0.55%) | ||||||||

| Cia de Saneamento Basico do Estado de Sao Paulo, ADR | 77,481 | 456,363 | ||||||

| Cia Siderurgica Nacional SA, Sponsored ADR | 1,580 | 4,250 | ||||||

| Gerdau SA, Sponsored ADR | 190,337 | 639,533 | ||||||

Petroleo Brasileiro SA, Sponsored ADR(a) | 35,152 | 333,944 | ||||||

| Vale SA, Sponsored ADR | 136,571 | 1,048,865 | ||||||

| 2,482,955 | ||||||||

| Canada (4.59%) | ||||||||

| Agnico‐Eagle Mines, Ltd. | 15,403 | 466,652 | ||||||

| Alamos Gold, Inc. | 61,800 | 427,196 | ||||||

| ARC Resources, Ltd. | 6,787 | 138,890 | ||||||

Argonaut Gold, Inc.(a) | 14,775 | 24,860 | ||||||

| AuRico Gold, Inc. | 67,852 | 236,803 | ||||||

B2Gold Corp.(a) | 168,500 | 263,958 | ||||||

| Barrick Gold Corp. | 59,330 | 772,477 | ||||||

| Cameco Corp. | 12,079 | 212,349 | ||||||

| Canadian Natural Resources, Ltd. | 5,741 | 190,888 | ||||||

| Canadian Oil Sands, Ltd. | 169,108 | 1,837,552 | ||||||

| Cenovus Energy, Inc. | 74,429 | 1,402,214 | ||||||

| Centerra Gold, Inc. | 78,900 | 408,070 | ||||||

| Crescent Point Energy Corp. | 10,981 | 286,789 | ||||||

Detour Gold Corp.(a) | 16,587 | 175,287 | ||||||

| Value | ||||||||

| Shares | (Note 2) | |||||||

| Canada (continued) | ||||||||

| Eldorado Gold Corp. | 65,346 | $ | 324,116 | |||||

| Encana Corp. | 81,800 | 1,162,378 | ||||||

Endeavour Silver Corp.(a) | 18,980 | 38,340 | ||||||

| First Quantum Minerals, Ltd. | 44,647 | 683,860 | ||||||

| Franco‐Nevada Corp. | 9,227 | 478,235 | ||||||

| Goldcorp, Inc. | 31,061 | 584,879 | ||||||

| HudBay Minerals, Inc. | 23,000 | 227,426 | ||||||

| Husky Energy, Inc. | 10,586 | 236,726 | ||||||

IAMGOLD Corp.(a) | 456 | 1,021 | ||||||

| Imperial Oil, Ltd. | 25,209 | 1,111,160 | ||||||

Kinross Gold Corp.(a) | 140,786 | 342,110 | ||||||

Lundin Mining Corp.(a) | 37,100 | 184,501 | ||||||

| Maple Leaf Foods, Inc. | 10,500 | 201,471 | ||||||

MEG Energy Corp.(a) | 5,900 | 113,794 | ||||||

New Gold, Inc.(a) | 69,617 | 235,305 | ||||||

| Osisko Gold Royalties, Ltd. | 2,569 | 34,431 | ||||||

| Pacific Rubiales Energy Corp. | 228,700 | 773,391 | ||||||

| Pan American Silver Corp. | 49,160 | 468,003 | ||||||

| Peyto Exploration & Development Corp. | 13,600 | 395,319 | ||||||

| Potash Corp. of Saskatchewan, Inc. | 20,852 | 680,609 | ||||||

Primero Mining Corp.(a) | 37,900 | 139,789 | ||||||

Sandstorm Gold, Ltd.(a) | 39,467 | 141,292 | ||||||

SEMAFO, Inc.(a) | 110,100 | 338,559 | ||||||

Silver Standard Resources, Inc.(a) | 44,960 | 244,807 | ||||||

| Silver Wheaton Corp. | 29,773 | 587,719 | ||||||

| SunCoke Energy, Inc. | 16,171 | 283,478 | ||||||

| Suncor Energy, Inc. | 52,160 | 1,699,026 | ||||||

| Tahoe Resources, Inc. | 6,600 | 93,270 | ||||||

| Teck Resources, Ltd., Class B | 64,472 | 977,556 | ||||||

| TransCanada Corp. | 7,142 | 331,498 | ||||||

Turquoise Hill Resources, Ltd.(a) | 81,758 | 340,113 | ||||||

| Yamana Gold, Inc. | 92,948 | 355,068 | ||||||

| 20,653,235 | ||||||||

| Chile (0.12%) | ||||||||

| Sociedad Quimica y Minera de Chile SA, Sponsored ADR | 25,642 | 560,021 | ||||||

| China (1.24%) | ||||||||

| China Petroleum & Chemical Corp., ADR | 464 | 43,834 | ||||||

| China Petroleum & Chemical Corp., Class H | 400,358 | 375,018 | ||||||

| China Shenhua Energy Co., Ltd., Class H | 95,369 | 247,942 | ||||||

| CNOOC, Ltd. | 250,001 | 423,842 | ||||||

| CNOOC, Ltd., Sponsored ADR | 18,859 | 3,229,604 | ||||||

| Jiangxi Copper Co., Ltd., Class H | 50,082 | 103,905 | ||||||

| PetroChina Co., Ltd., ADR | 4,087 | 526,896 | ||||||

| PetroChina Co., Ltd., Class H | 330,045 | 424,131 | ||||||

| Zijin Mining Group Co., Ltd., Class H | 560,331 | 216,164 | ||||||

| 5,591,336 | ||||||||

20 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Consolidated Statement of Investments | April 30, 2015 (Unaudited) |

| Value | ||||||||

| Shares | (Note 2) | |||||||

| Colombia (0.19%) | ||||||||

| Ecopetrol SA, Sponsored ADR | 50,903 | $ | 871,459 | |||||

| Denmark (0.06%) | ||||||||

| FLSmidth & Co. A/S | 6,011 | 257,549 | ||||||

| Finland (0.30%) | ||||||||

| Kemira OYJ | 10,739 | 126,250 | ||||||

| Neste Oil OYJ | 19,790 | 539,086 | ||||||

Outokumpu OYJ (a) | 61,518 | 373,699 | ||||||

| Outotec OYJ | 43,438 | 304,840 | ||||||

| 1,343,875 | ||||||||

| France (0.17%) | ||||||||

| TOTAL SA | 4,886 | 266,000 | ||||||

| TOTAL SA, Sponsored ADR | 9,057 | 489,984 | ||||||

| 755,984 | ||||||||

| Germany (0.66%) | ||||||||

| Aurubis AG | 639 | 40,704 | ||||||

| K+S AG | 78,161 | 2,573,213 | ||||||

| Salzgitter AG | 10,429 | 358,918 | ||||||

| 2,972,835 | ||||||||

| India (0.08%) | ||||||||

Reliance Industries, Ltd., Sponsored GDR(b) | 8,852 | 238,119 | ||||||

| Sesa Sterlite, Ltd., ADR | 9,014 | 118,444 | ||||||

| 356,563 | ||||||||

| Israel (0.06%) | ||||||||

| The Israel Corp., Ltd. | 785 | 289,476 | ||||||

| Italy (0.14%) | ||||||||

| Eni SpA, Sponsored ADR | �� | 16,393 | 629,983 | |||||

| Japan (1.60%) | ||||||||

| Hitachi Metals, Ltd. | 50,000 | 787,688 | ||||||

| Idemitsu Kosan Co., Ltd. | 25,931 | 504,721 | ||||||

| Inpex Corp. | 106,133 | 1,342,218 | ||||||

| Iseki & Co., Ltd. | 20,907 | 43,600 | ||||||

| JFE Holdings, Inc. | 12,600 | 285,980 | ||||||

| Kubota Corp. | 18,000 | 282,890 | ||||||

| Kurita Water Industries, Ltd. | 10,616 | 277,403 | ||||||

| Maruichi Steel Tube, Ltd. | 20,000 | 510,050 | ||||||

| Nihon Nohyaku Co., Ltd. | 16,100 | 170,169 | ||||||

| Nihon Trim Co., Ltd. | 4,101 | 127,426 | ||||||

| Nippon Steel & Sumitomo Metal Corp. | 208,342 | 546,156 | ||||||

| Nisshin Steel Co., Ltd. | 29,000 | 390,067 | ||||||

| Osaka Titanium Technologies Co., Ltd. | 8,500 | 184,167 | ||||||

| Showa Shell Sekiyu KK | 44,500 | 431,583 | ||||||

| Sumitomo Forestry Co., Ltd. | 15,159 | 176,982 | ||||||

| Sumitomo Metal Mining Co., Ltd. | 26,000 | 384,883 | ||||||

| Tokyo Steel Manufacturing Co., Ltd. | 37,000 | 258,442 | ||||||

| Value | ||||||||

| Shares | (Note 2) | |||||||

| Japan (continued) | ||||||||

| TonenGeneral Sekiyu KK | 36,000 | $ | 346,432 | |||||

| Yamato Kogyo Co., Ltd. | 6,700 | 158,859 | ||||||

| 7,209,716 | ||||||||

| Jersey (0.11%) | ||||||||

| Randgold Resources, Ltd., ADR | 6,784 | 516,737 | ||||||

| Luxembourg (0.35%) | ||||||||

APERAM SA (a) | 13,273 | 508,511 | ||||||

| ArcelorMittal | 13,316 | 142,297 | ||||||

| ArcelorMittal SA | 13,635 | 145,758 | ||||||

| Subsea 7 SA | 63,173 | 701,810 | ||||||

| Tenaris SA, ADR | 2,743 | 84,347 | ||||||

| 1,582,723 | ||||||||

| Mexico (0.34%) | ||||||||

| Grupo Mexico SAB de CV, Series B | 424,283 | 1,311,123 | ||||||

| Industrias Penoles SAB de CV | 13,107 | 222,124 | ||||||

| 1,533,247 | ||||||||

| Netherlands (0.06%) | ||||||||

| Royal Dutch Shell PLC, Class A, | ||||||||

| Sponsored ADR | 4,503 | 285,625 | ||||||

| Norway (0.63%) | ||||||||

| Marine Harvest ASA | 75,761 | 926,173 | ||||||

| Norsk Hydro ASA | 104,109 | 492,083 | ||||||

| Statoil ASA | 48,474 | 1,023,595 | ||||||

| Yara International ASA | 7,649 | 392,522 | ||||||

| 2,834,373 | ||||||||

| Peru (0.18%) | ||||||||

| Cia de Minas Buenaventura SAA, ADR | 71,096 | 794,853 | ||||||

| Singapore (0.25%) | ||||||||

| Golden Agri‐Resources, Ltd. | 893,758 | 283,690 | ||||||

Kenon Holdings, Ltd.(a) | 5,495 | 118,990 | ||||||

| Olam International, Ltd. | 46,254 | 70,612 | ||||||

| Wilmar International, Ltd. | 257,061 | 633,327 | ||||||

| 1,106,619 | ||||||||

| South Africa (0.58%) | ||||||||

Anglo Platinum, Ltd. (a) | 5,831 | 160,354 | ||||||

| AngloGold Ashanti, Ltd., ADR | 77,918 | 882,811 | ||||||

| Gold Fields, Ltd., Sponsored ADR | 60,039 | 274,378 | ||||||

Harmony Gold Mining Co., Ltd., Sponsored ADR(a) | 38,989 | 75,639 | ||||||

Impala Platinum Holdings, Ltd. (a) | 39,295 | 218,007 | ||||||

| Kumba Iron Ore, Ltd. | 1,186 | 15,967 | ||||||

| Sasol, Ltd. | 24,099 | 973,643 | ||||||

| Sibanye Gold, Ltd., Sponsored ADR | 2,515 | 23,767 | ||||||

| 2,624,566 | ||||||||

21 | April 30, 2015

| ALPS | CoreCommodity Management | |

CompleteCommodities® Strategy Fund | |

| Consolidated Statement of Investments | April 30, 2015 (Unaudited) |

| Value | ||||||||

| Shares | (Note 2) | |||||||

| South Korea (0.04%) | ||||||||

| POSCO, Sponsored ADR | 2,859 | $ | 168,910 | |||||

| Spain (0.03%) | ||||||||

| Acerinox SA | 10,270 | 150,604 | ||||||

| Sweden (0.33%) | ||||||||

| Boliden AB | 7,842 | 171,175 | ||||||