UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08194

FINANCIAL INVESTORS TRUST

(Exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Karen Gilomen, Esq., Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: May 1, 2016 – October 31, 2016

Item 1. Reports to Stockholders.

TABLE OF CONTENTS

| PAGE | |

| Manager Commentary | 1 |

| Performance Update | 3 |

| Consolidated Disclosure of Fund Expenses | 5 |

| Consolidated Schedule of Investments | 6 |

| Consolidated Statement of Assets & Liabilities | 8 |

| Consolidated Statement of Operations | 9 |

| Consolidated Statements of Changes in Net Assets | 10 |

| Consolidated Financial Highlights | 11 |

| Notes to Consolidated Financial Statements | 13 |

| Additional Information | 20 |

| Aspen Managed Futures Strategy Fund | Manager Commentary |

| October 31, 2016 (Unaudited) |

October 31, 2016

Performance Results

For the six‐month period ending October 31, 2016, the Class I shares of the Aspen Managed Futures Strategy Fund (the “Fund”) posted a return of ‐3.45%. Per its mandate, the Fund maintained tight correlation(1) to the Aspen Managed Futures Beta Index (“Aspen MFBI” or the “Index”)(2). The Index uses a combination of trend and counter‐trend algorithms to determine exposures to 23 futures markets. In following the Index, the Fund can take long or short positions in each of the eligible markets. A long position in a futures market will profit if the price of the futures contract rises, whereas a short position will profit if the price of the futures contract falls.

The BTOP50 Index(3), a managed futures benchmark, returned ‐4.01% over the same period. It is important to note that there are substantive differences between the Fund and the Index in terms of construction. There were no significant changes to the Fund strategy during this period.

Explanation of Fund Performance

The Fund returned ‐2.45% in May. A surprise rate cut by the Reserve Bank of Australia was a factor in the monthly loss. The cut drove down the Australian dollar, causing losses in long AUD positions in the Index’s Trend and Counter‐Trend models.

The month of June provided a gain of +3.18% for the Fund. The majority of that return occurred on a single day, June 24, the first day of market reaction to the surprise results of the UK’s “Brexit”(4) vote to leave European Union. The Aspen MFBI’s futures positioning around Brexit arose from the crosswinds of pre‐Brexit market moves. Because the vote was a rare, point‐in‐time volatility‐inducing event that everyone could see coming in advance, volatility naturally spiked in advance in the weeks preceding the vote—which led to a Broad Risk Indicator‐driven increase in the Trend/Counter‐Trend ratio in the Index. Risk assets, particularly European issues, declined—which led to net short risk exposures in the Trend model. However, concerns notwithstanding, at no point prior to the actual vote tally did markets predict a greater than 50% probability of a UK “Leave” vote. In particular, over the course of the week of the actual vote, the market’s movements reflected increasing confidence that the “Remain” side would win. This resulted in Index positioning that, while risk‐off overall, was not positioned strongly short risk assets, but was decidedly long fixed income. In aggregate, that positioning enabled the Fund to capture a gain of about +2% on June 24. Remarkably, it took only about a week for global equity markets, including those in the UK itself, to recover their Brexit losses. Typically a “V‐bottom” bounce of that nature is problematic for a trend‐following model such as the one tracked by the Fund, but in this case, the Fund was actually able to profit during the market rebound as well as the initial market drop. The primary reason for this was the fact that the Fund’s long fixed income positions continued to post profits, as the post‐Brexit rebound was apparently driven in part by speculation of further easing, which in turn benefitted sovereign bonds as well as equity markets.

After the craziness of Brexit, the markets settled into a quieter mode for the remainder of the reporting period. A trendless, low‐volatility backdrop created difficult conditions for the Index’s trend model, but it benefitted the Index’s risk‐on counter‐trend model. Trend attribution was negative and counter‐trend attribution was positive in each of the remaining four months of the period—a pattern that previously had not occurred for more than two consecutive months. Because the Index is always primarily trend‐following, this pattern led to losses for the Fund in all four months (July: ‐0.50%, August: ‐0.78%, September: ‐1.01%, October: ‐1.93%). However, the boost provided by the counter‐trend sub‐model kept losses over the entire period relatively modest—i.e., the losses over the entire four‐month period were only about 100 basis points(5) greater than the gains in June alone.

At the end of October, heading toward the U.S. presidential election, the most notable development in the Fund was the adoption of net short fixed income futures positioning for the first time all year, in response to rising global interest rates over the last couple months of the reporting period.

Outlook

On September 9th, the bears appeared to be running the table. Investors were concerned that a month of central bank announcements would lead to a market pullback. In addition, concerns about the end of easy money, sky‐high equity valuations and lack of economic growth in Europe seemed to confirm traders’ worst suspicions, as the S&P 500® Total Return Index(6) fell over 2.5% that day. However, in the weeks that followed, the markets were able to shake off the gloom. So what gives?

Apparently, those arguments just weren’t enough to end the 7 ½ ‐ year bull market. News of the improving domestic economy was certainly a plus, along with less hawkish news from the European Central Bank and the Federal Reserve (“Fed”). And with interest rates so low, the current high valuation of stocks seem not to be enough of a catalyst to push the markets lower.

A deeper dive into the third quarter’s market performance gives some indication of the larger concerns among investors. The weakness during the period of the so‐called bond proxy sectors (utilities, real estate, and consumer staples) was mainly due to worries about rising rates. Likewise, weakness in U.S. exporters and multinationals signals skepticism around a global economic upswing.

| Semi-Annual Report | October 31, 2016 | 1 |

| Aspen Managed Futures Strategy Fund | Manager Commentary |

| October 31, 2016 (Unaudited) |

These concerns are not new, of course. But it should be noted that even if the Fed does raise rates in December, it is in our view likely to be only 25 basis points. That would still leave rates extremely low. As has been the case for the last several years, we believe the market will continue to fall in anticipation of bad news, only to recover when the worst‐case scenario doesn’t come to fruition.

Donald Trump’s surprise victory in the U.S. presidential race ranks with Brexit as one of the most stunning events of the year. Besides showing clients the value of discipline for staying in the market even after nine consecutive down sessions, Wednesday’s market action after the election also contains some interesting clues about the potential direction of markets as we approach year‐end.

The most important observation is stock prices rising in the face of higher rates. The 10‐year note yield has climbed from 1.89% before the election to 2.30%, and equity markets have also risen during that period. Have we finally reached a point where rallies are not entirely dependent on dovish Fed action? That may be the case. Last month’s release of third quarter Gross Domestic Product numbers showing 2.90% growth was certainly encouraging.

We feel that it is also positive to see the yield curve finally steepening (i.e., long‐term rates rising more than short‐term rates). A move such as this should be a boon for bank stocks, making it easier for banks to profit from lending activity.

Sincerely,

Bryan R. Fisher

William Ware Bush

Bryan R. Fisher

William Ware Bush

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data please call 1-855-845-9444.

The views of Aspen Partners, Ltd. and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writers’ current views. The views expressed are those of the Fund’s adviser only, and represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither Aspen Partners Ltd. nor the Fund accepts any liability for losses either direct or consequential caused by the use of this information.

The Aspen Managed Futures Strategy Fund is distributed by ALPS Distributors, Inc.

The Fund is subject to investment risks, including possible loss of the principal amount invested and therefore is not suitable for all investors. The Fund may not achieve its objectives.

Diversification does not eliminate the risk of experiencing investment losses.

| (1) | Correlation - a statistical measure of how two securities or portfolios move in relation to each other. |

| (2) | Aspen Managed Futures Beta Index (Aspen MFBI) is constructed using a quantitative, rules-based model designed to replicate the trend-following and counter-trend exposure of futures markets by allocating assets to liquid futures contracts of certain financial and commodities futures markets. The Index therefore seeks to reflect the performance of strategies and exposures common to a broad universe of futures markets, i.e., managed futures beta. |

| (3) | Barclay BTOP50 Index is an index of the largest investable CTA programs as measured by assets under management. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly into the Index. |

| (4) | Brexit is an abbreviation for "British exit," which refers to the June 23, 2016, referendum whereby British citizens voted to exit the European Union. The referendum roiled global markets, including currencies, causing the British pound to fall to its lowest level in decades. |

| (5) | Basis point is a common unit of measure fir interest rates and other percentages in finance. One basis point is equal to 1/100th of 1% or 0.01%(.0001). |

| (6) | The S&P 500® Total Return Index is an unmanaged index of 500 common stocks chosen for market size, liquidity and industry group representation. It is a market-value weighted index. The Index is not actively managed and does not reflect any deductions for fees, expenses or taxes. An investor may not invest directly in the Index. |

| 2 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Performance Update |

| October 31, 2016 (Unaudited) |

Cumulative Total Return Performance as of October 31, 2016

| Aspen Managed Futures Strategy Fund | 6 Months | Calendar Year-to-Date | 1 Year | 3 Year | 5 Year | Since Inception* | Expense Ratios | |

| Total | Net(1) | |||||||

Aspen Managed Futures Strategy Fund ‐ Class A (NAV)(2) | ‐3.28% | ‐4.47% | ‐3.49% | 1.23% | 0.19% | ‐0.97% | 1.61% | 1.61% |

Aspen Managed Futures Strategy Fund ‐ Class A (MOP)(3) | ‐8.57% | ‐9.73% | ‐8.77% | ‐0.65% | ‐0.94% | ‐2.03% | 1.61% | 1.61% |

| Aspen Managed Futures Strategy Fund ‐ Class I | ‐3.45% | ‐4.73% | ‐3.51% | 1.52% | 0.50% | ‐0.66% | 1.23% | 1.23% |

SG CTA Index(4) | ‐3.33% | ‐1.65% | ‐0.40% | 5.18% | 2.13% | 1.14% | ||

Aspen Managed Futures Beta Index(5) | ‐2.76% | ‐3.35% | ‐1.95% | 3.30% | 2.35% | 1.27% | ||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please call 1-855-845-9444.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Subject to investment risks, including possible loss of the principal amount invested.

Returns for periods greater than 1 year are annualized.

| * | Fund Inception date of August 2, 2011. |

| (1) | Aspen Partners, Ltd. (the “Adviser”) has agreed to waive and/or reimburse fees or expenses in order to limit total annual Fund operating expenses after fee waiver/expense reimbursements (excluding distribution and service (12b-1) fees, shareholder services fees, acquired fund fees and expenses, brokerage expenses, interest expenses, taxes and extraordinary expenses) to 1.55% of the Fund’s average daily net assets. This agreement (the “Expense Agreement”) is in effect through August 31, 2017. The Adviser will be permitted to recover, on a class-by-class basis, expenses it has borne through the Expense Agreement to the extent that the Fund’s expenses in later periods fall below the expense cap in effect at the time of waiver or reimbursement. Notwithstanding the foregoing, the Fund will not be obligated to pay any such deferred fees and expenses more than three years after the end of the fiscal year in which the fees and expenses were deferred. The Expense Agreement may not be terminated or modified prior to August 31, 2017 except with the approval of the Fund’s Board of Trustees |

| (2) | Net Asset Value (NAV) is the share price without sales charges. |

| (3) | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Fund’s maximum sales charge of 5.50%. |

| (4) | The SG CTA Index (formerly, the Newedge CTA Index) provides the market with a reliable daily performance benchmark of major commodity trading advisors (CTAs). The SG CTA Index calculates the daily rate of return for a pool of CTAs selected from the larger managers that are open to new investment. Selection of the pool of qualified CTAs used in construction of the Index will be conducted annually, with re-balancing on January 1st of each year. A committee of industry professionals has been established to monitor the methodology of the index on a regular basis. The Index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor cannot invest directly in the Index. |

| (5) | Aspen Managed Futures Beta Index – The Managed Futures Beta Index is constructed using a quantitative, rules-based model designed to replicate the trend-following and counter-trend exposure of futures markets by allocating assets to liquid futures contracts of certain financial and commodities futures markets. The Index therefore seeks to reflect the performance of strategies and exposures common to a broad universe of futures markets, i.e., managed futures beta. The index is not actively managed and does not reflect any deductions for fees, expense or taxes. An investor may not invest directly in an index. |

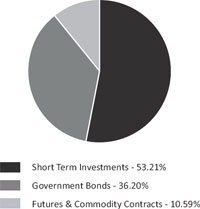

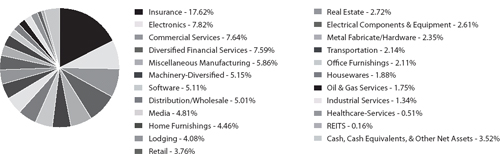

Portfolio Composition as of October 31, 2016

As a percentage of Net Assets^

^ | Holdings subject to change, and may not reflect the current or future position of the portfolio. |

| Semi-Annual Report | October 31, 2016 | 3 |

| Aspen Managed Futures Strategy Fund | Performance Update |

| October 31, 2016 (Unaudited) |

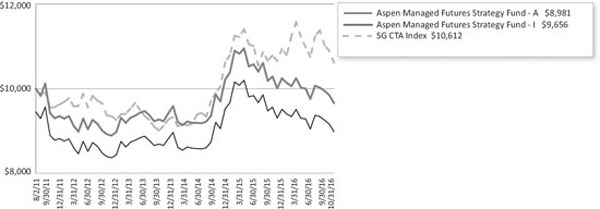

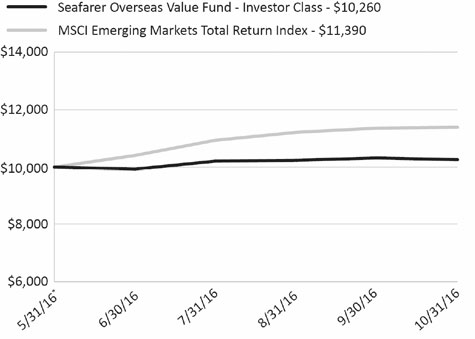

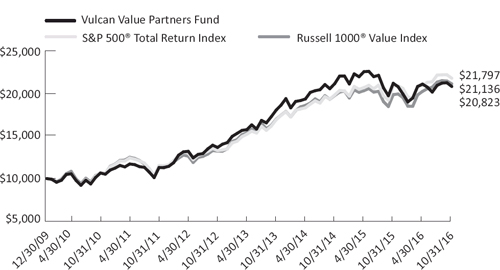

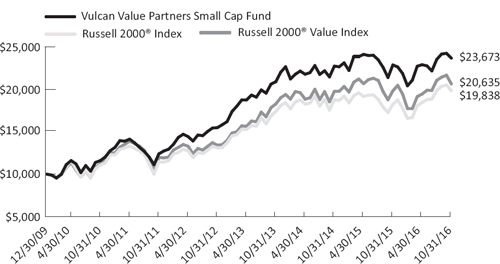

Performance of $10,000 Initial Investment (as of October 31, 2016)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested.

| 4 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Consolidated Disclosure of Fund Expenses |

| October 31, 2016 (Unaudited) |

As a shareholder of the Fund, you incur two types of costs: transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b‐1) fees; shareholder servicing fees; and other fund operating expenses. This example is intended to help you understand your ongoing costs (in dollars), of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six‐month period of May 1, 2016 through October 31, 2016.

Actual Expenses The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as applicable sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value 5/1/16 | Ending Account Value 10/31/16 | Expense Ratio(a) | Expenses Paid During period 5/1/16 - 10/31/16(b) | |

| Class A | ||||

| Actual | $1,000.00 | $967.20 | 1.03% | $5.11 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,020.01 | 1.03% | $5.24 |

| Class I | ||||

| Actual | $1,000.00 | $965.50 | 1.24% | $6.14 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,018.95 | 1.24% | $6.31 |

| (a) | The Fund's expense ratios have been based on the Fund's most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184)/365 (to reflect the half-year period). |

| Semi-Annual Report | October 31, 2016 | 5 |

| Aspen Managed Futures Strategy Fund | Consolidated Schedule of Investments |

October 31, 2016 (Unaudited)

| Principal Amount/Shares | Value (Note 2) | |||||||

| GOVERNMENT BONDS (36.20%) | ||||||||

| U.S. TREASURY NOTES (36.20%) | ||||||||

| 0.500%, 11/30/2016 | $ | 9,047,000 | $ | 9,049,325 | ||||

| 0.500%, 01/31/2017 | 8,010,000 | 8,014,446 | ||||||

| 0.500%, 03/31/2017 | 15,014,000 | 15,019,855 | ||||||

| 0.625%, 05/31/2017 | 10,065,000 | 10,070,304 | ||||||

| 0.625%, 07/31/2017 | 19,823,000 | 19,822,604 | ||||||

| 0.625%, 08/31/2017 | 5,045,000 | 5,043,522 | ||||||

| 1.000%, 09/15/2017 | 5,000,000 | 5,014,160 | ||||||

| 0.625%, 09/30/2017 | 6,050,000 | 6,046,812 | ||||||

| 0.750%, 10/31/2017 | 7,134,000 | 7,137,481 | ||||||

| 0.625%, 11/30/2017 | 5,135,000 | 5,129,783 | ||||||

| TOTAL GOVERNMENT BONDS (Cost $90,305,637) | 90,348,292 | |||||||

| SHORT TERM INVESTMENTS (53.21%) | ||||||||

| MONEY MARKET FUND (3.89%) | ||||||||

| Dreyfus Treasury & Agency Cash Management Fund ‐ Institutional Shares, 7‐day yield, 0.207% | 9,713,818 | 9,713,818 | ||||||

| U.S. TREASURY BILLS (49.32%) | ||||||||

0.496%, 11/10/2016(a) | 10,000,000 | 9,998,747 | ||||||

0.563%, 12/08/2016(a) | 13,350,000 | 13,344,080 | ||||||

0.565%, 01/05/2017(a) | 10,500,000 | 10,495,096 | ||||||

0.397%, 02/02/2017(a) | 10,400,000 | 10,390,806 | ||||||

0.510%, 03/30/2017(a) | 8,500,000 | 8,486,630 | ||||||

0.570%, 04/27/2017(a) | 5,600,000 | 5,586,510 | ||||||

0.492%, 05/25/2017(a) | 10,500,000 | 10,471,818 | ||||||

0.429%, 06/22/2017(a) | 13,350,000 | 13,307,227 | ||||||

0.402%, 07/20/2017(a) | 10,000,000 | 9,961,480 | ||||||

0.557%, 08/17/2017(a) | 14,000,000 | 13,938,190 | ||||||

0.528%, 09/14/2017(a) | 7,800,000 | 7,759,822 | ||||||

0.631%, 10/12/2017(a) | 9,400,000 | 9,342,989 | ||||||

| 123,083,395 | ||||||||

| TOTAL SHORT TERM INVESTMENTS (Cost $132,796,920) | 132,797,213 | |||||||

TOTAL INVESTMENTS (89.41%) (Cost $223,102,557) | $ | 223,145,505 | ||||||

| Other Assets In Excess Of Liabilities (10.59%) | 26,424,761 | (b) | ||||||

| NET ASSETS (100.00%) | $ | 249,570,266 | ||||||

| (a) | Rate shown represents the bond equivalent yield to maturity at date of purchase. |

| (b) | Includes cash which is being held as collateral for futures contracts. |

See Notes to Consolidated Financial Statements.

| 6 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Consolidated Schedule of Investments |

October 31, 2016 (Unaudited)

FUTURES CONTRACTS

At October 31, 2016, the Fund had outstanding futures contracts:

| Description | Position | Contracts | Expiration Date | Underlying Face Amount at Value | Unrealized Appreciation | ||||||||

| Equity Contracts | |||||||||||||

Euro STOXX 50® Index Future | Long | 311 | 12/16/2016 | $ | 10,422,952 | $ | 13,715 | ||||||

FTSE® 100 Index Future | Long | 182 | 12/16/2016 | 15,435,603 | 291,652 | ||||||||

| Nikkei 225 Index Future | Long | 121 | 12/08/2016 | 10,539,100 | 248,471 | ||||||||

| Foreign Currency Contracts | |||||||||||||

| Canadian Dollar Currency Future | Short | 519 | 12/20/2016 | (38,678,475 | ) | 336,881 | |||||||

| Euro FX Currency Future | Short | 401 | 12/19/2016 | (55,072,338 | ) | 258,953 | |||||||

| Japanese Yen Currency Future | Short | 110 | 12/19/2016 | (13,125,063 | ) | 48,443 | |||||||

| New Zealand Dollar Currency Future | Long | 227 | 12/19/2016 | 16,194,180 | 182,217 | ||||||||

| Swiss Franc Currency Future | Short | 129 | 12/19/2016 | (16,321,725 | ) | 4,516 | |||||||

| Interest Rate Contracts | |||||||||||||

| Canadian 10 Year Bond Future | Short | 129 | 12/19/2016 | (13,908,879 | ) | 71,375 | |||||||

| Euro‐Bund Future | Short | 80 | 12/08/2016 | (14,241,773 | ) | 77,981 | |||||||

| Long Gilt Future | Short | 91 | 12/28/2016 | (13,960,878 | ) | 83,035 | |||||||

| U.S. 10 Year Note Future | Short | 110 | 12/20/2016 | (14,258,750 | ) | 19,099 | |||||||

| $ | (126,976,046 | ) | $ | 1,636,338 | |||||||||

| Description | Position | Contracts | Expiration Date | Underlying Face Amount at Value | Unrealized Depreciation | ||||||||

| Commodity Contracts | |||||||||||||

Copper Future(a) | Short | 57 | 12/28/2016 | $ | (3,142,125 | ) | $ | (145,058 | ) | ||||

Corn Future(a) | Short | 170 | 12/14/2016 | (3,015,375 | ) | (187,618 | ) | ||||||

Gold 100 Oz. Future(a) | Short | 23 | 12/28/2016 | (2,928,130 | ) | (42,654 | ) | ||||||

New York Harbor ULSD Future(a) | Long | 136 | 11/30/2016 | 8,590,277 | (363,149 | ) | |||||||

Silver Future(a) | Long | 34 | 12/28/2016 | 3,025,320 | (161,094 | ) | |||||||

Soybean Future(a) | Long | 61 | 01/13/2017 | 3,085,838 | (28,439 | ) | |||||||

Sugar No. 11 (World) Future(a) | Long | 352 | 02/28/2017 | 8,503,757 | (819,696 | ) | |||||||

WTI Crude Future(a) | Long | 182 | 11/21/2016 | 8,528,520 | (689,304 | ) | |||||||

| Equity Contracts | |||||||||||||

S&P 500® E‐Mini Future | Long | 49 | 12/16/2016 | 5,194,245 | (44,116 | ) | |||||||

| Foreign Currency Contracts | |||||||||||||

| Australian Dollar Currency Future | Long | 723 | 12/19/2016 | 54,890,160 | (174,409 | ) | |||||||

| $ | 82,732,487 | $ | (2,655,537 | ) | |||||||||

Common Abbreviations:

FTSE - Financial Times and the London Stock Exchange

S&P - Standard and Poor's

ULSD - Ultra Low Sulfur Diesel

(a) | Owned by an entity that is owned by the Fund and is consolidated as described in Note 1 of the Notes to the Consolidated Financial Statements. |

For Fund compliance purposes, the Fund's industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percentage of net assets.

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2016 | 7 |

| Aspen Managed Futures Strategy Fund | Consolidated Statement of Assets & Liabilities |

October 31, 2016 (Unaudited)

| ASSETS: | ||||

| Investments, at value | $ | 223,145,505 | ||

| Cash | 3,351,619 | |||

| Deposit with broker for futures contracts (Note 3) | 28,948,750 | |||

| Receivable for shares sold | 18,951 | |||

| Variation margin receivable | 44,556 | |||

| Interest receivable | 126,841 | |||

| Prepaid and other assets | 36,108 | |||

| Total assets | 255,672,330 | |||

| LIABILITIES: | ||||

| Foreign cash due to broker for futures contracts (Note 3)(Cost $4,931,226) | 4,842,728 | |||

| Payable to advisor | 161,054 | |||

| Variation margin payable | 878,756 | |||

| Payable for shares redeemed | 31,300 | |||

| Payable for administration fees | 19,522 | |||

| Payable for distribution and service fees | ||||

| Class A | 22,993 | |||

| Payable for transfer agency fees | 9,434 | |||

| Delegated transfer agent equivalent services fees | ||||

| Class A | 2,100 | |||

| Class I | 40,633 | |||

| Payable for trustee fees and expenses | 7,503 | |||

| Payable for professional fees | 18,877 | |||

| Payable for chief compliance officer fees | 3,083 | |||

| Payable for principal financial officer fees | 854 | |||

| Payable for licensing fees | 53,684 | |||

| Accrued expenses and other liabilities | 9,543 | |||

| Total liabilities | 6,102,064 | |||

| NET ASSETS | $ | 249,570,266 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid‐in capital (Note 5) | $ | 272,349,786 | ||

| Accumulated net investment income | 1,192,248 | |||

| Accumulated net realized loss | (23,084,015 | ) | ||

| Net unrealized depreciation | (887,753 | ) | ||

| NET ASSETS | $ | 249,570,266 | ||

| INVESTMENTS, AT COST | $ | 223,102,557 | ||

| PRICING OF SHARES: | ||||

| Class A: | ||||

| Net Asset Value, offering and redemption price per share | $ | 8.54 | ||

| Net Assets | $ | 7,242,638 | ||

| Shares of beneficial interest outstanding | 848,419 | |||

| Maximum offering price per share (NAV/0.9450), based on maximum sales charge of 5.50% of the offering price | $ | 9.04 | ||

| Class I: | ||||

| Net Asset Value, offering and redemption price per share | $ | 8.67 | ||

| Net Assets | $ | 242,327,628 | ||

| Shares of beneficial interest outstanding | 27,960,915 | |||

See Notes to Consolidated Financial Statements.

| 8 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Consolidated Statement of Operations |

For the Six Months Ended October 31, 2016 (Unaudited)

| INVESTMENT INCOME: | ||||

| Interest | $ | 608,303 | ||

| Dividends | 9,768 | |||

| Total investment income | 618,071 | |||

| EXPENSES: | ||||

| Investment advisory fees (Note 6) | 1,000,139 | |||

| Investment advisory fees ‐ subsidiary (Note 6) | 92,487 | |||

| Administrative fees | 109,756 | |||

| Transfer agency fees | 35,834 | |||

| Delegated transfer agent equivalent services fees | ||||

| Class A | 2,795 | |||

| Class I | 77,595 | |||

| Professional fees | 22,140 | |||

| Custodian fees | 6,273 | |||

| Trustee fees and expenses | 9,684 | |||

| Principal financial officer fees | 2,520 | |||

| Chief compliance officer fees | 17,554 | |||

| Licensing fees | 333,380 | |||

| Other | 26,107 | |||

| Total expenses before waiver/reimbursement | 1,736,264 | |||

| Waiver of investment advisory fees ‐ subsidiary (Note 6) | (92,487 | ) | ||

| Total net expenses | 1,643,777 | |||

| NET INVESTMENT LOSS | (1,025,706 | ) | ||

| Net realized gain on investments | 1,601 | |||

| Net realized loss on futures contracts | (2,559,565 | ) | ||

| Net realized gain on foreign currency transactions | 163,180 | |||

| Total net realized loss | (2,394,784 | ) | ||

| Net change in unrealized depreciation of investments | (51,839 | ) | ||

| Net change in unrealized depreciation on futures contracts | (6,139,116 | ) | ||

| Net change in unrealized appreciation on translation of assets and liabilities denominated in foreign currency transactions | 129,199 | |||

| Net change in unrealized depreciation | (6,061,756 | ) | ||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (8,456,540 | ) | ||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (9,482,246 | ) | |

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2016 | 9 |

| Aspen Managed Futures Strategy Fund | Consolidated Statements of Changes in Net Assets |

For the Six Months Ended October 31, 2016 (Unaudited) | For the Year Ended April 30, 2016 | |||||||

| OPERATIONS: | ||||||||

| Net investment loss | $ | (1,025,706 | ) | $ | (2,786,624 | ) | ||

| Net realized loss | (2,394,784 | ) | (22,047,854 | ) | ||||

| Net change in unrealized appreciation/(depreciation) | (6,061,756 | ) | 9,897,802 | |||||

| Net decrease in net assets resulting from operations | (9,482,246 | ) | (14,936,676 | ) | ||||

| DISTRIBUTIONS TO SHAREHOLDERS (Note 4): | ||||||||

| From net investment income | ||||||||

| Class A | – | (290,384 | ) | |||||

| Class I | – | (4,854,577 | ) | |||||

| From net realized gains on investments | ||||||||

| Class A | – | (1,080,184 | ) | |||||

| Class I | – | (15,329,525 | ) | |||||

| Net decrease in net assets from distributions | – | (21,554,670 | ) | |||||

| SHARE TRANSACTIONS (Note 5): | ||||||||

| Class A | ||||||||

| Proceeds from sales of shares | 4,207,015 | 17,757,620 | ||||||

| Distributions reinvested | – | 1,314,015 | ||||||

| Cost of shares redeemed | (16,345,074 | ) | (20,727,211 | ) | ||||

| Redemption fees | 2,269 | 5,100 | ||||||

| Class I | ||||||||

| Proceeds from sales of shares | 26,346,180 | 83,806,547 | ||||||

| Distributions reinvested | – | 16,756,950 | ||||||

| Cost of shares redeemed | (39,438,757 | ) | (44,568,213 | ) | ||||

| Redemption fees | 477 | 2,041 | ||||||

| Net increase/(decrease) from share transactions | (25,227,890 | ) | 54,346,849 | |||||

| Net increase/(decrease) in net assets | (34,710,136 | ) | 17,855,503 | |||||

| NET ASSETS: | ||||||||

| Beginning of period | 284,280,402 | 266,424,899 | ||||||

| End of period* | $ | 249,570,266 | $ | 284,280,402 | ||||

| *Includes accumulated net investment income of: | $ | 1,192,248 | $ | 2,217,954 | ||||

| Other Information: | ||||||||

| SHARE TRANSACTIONS: | ||||||||

| Class A | ||||||||

| Sold | 481,951 | 1,836,531 | ||||||

| Distributions reinvested | – | 146,490 | ||||||

| Redeemed | (1,863,492 | ) | (2,134,823 | ) | ||||

| Net decrease in shares outstanding | (1,381,541 | ) | (151,802 | ) | ||||

| Class I | ||||||||

| Sold | 2,947,888 | 8,468,843 | ||||||

| Distributions reinvested | – | 1,837,385 | ||||||

| Redeemed | (4,438,176 | ) | (4,699,475 | ) | ||||

| Net increase/(decrease) in shares outstanding | (1,490,288 | ) | 5,606,753 | |||||

See Notes to Consolidated Financial Statements.

| 10 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund – Class A | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

For the Six Months Ended October 31, 2016 (Unaudited)(a) | For the Year Ended April 30, 2016 (a) | For the Year Ended April 30, 2015 (a) | For the Year Ended April 30, 2014 (a) | For the Year Ended April 30, 2013 (a) | For the Period August 2, 2011 (Inception) to April 30, 2012 (a) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 8.83 | $ | 10.01 | $ | 8.97 | $ | 9.29 | $ | 8.95 | $ | 10.00 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

Net investment loss(b) | (0.02 | ) | (0.12 | ) | (0.14 | ) | (0.16 | ) | (0.16 | ) | (0.13 | ) | ||||||||||||

| Net realized and unrealized gain/(loss) on investments | (0.27 | ) | (0.39 | ) | 1.39 | (0.05 | ) | 0.50 | (0.92 | ) | ||||||||||||||

| Total from investment operations | (0.29 | ) | (0.51 | ) | 1.25 | (0.21 | ) | 0.34 | (1.05 | ) | ||||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | – | (0.14 | ) | – | – | – | – | |||||||||||||||||

| Distributions from net realized gain on investments | – | (0.53 | ) | (0.21 | ) | (0.12 | ) | – | – | |||||||||||||||

| Total distributions | – | (0.67 | ) | (0.21 | ) | (0.12 | ) | – | – | |||||||||||||||

| REDEMPTION FEES ADDED TO PAID IN CAPITAL | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.01 | 0.00 | (c) | – | ||||||||||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.29 | ) | (1.18 | ) | 1.04 | (0.32 | ) | 0.34 | (1.05 | ) | ||||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 8.54 | $ | 8.83 | $ | 10.01 | $ | 8.97 | $ | 9.29 | $ | 8.95 | ||||||||||||

TOTAL RETURN(d) | (3.28 | %)(e) | (5.20 | %) | 14.00 | % | (2.15 | %) | 3.80 | % | (10.50 | %)(e) | ||||||||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (000's) | $ | 7,243 | $ | 19,682 | $ | 23,850 | $ | 12,914 | $ | 3,350 | $ | 1,254 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.03 | %(f)(g) | 1.56 | %(g) | 1.64 | % | 1.83 | % | 1.80 | % | 2.53 | %(f) | ||||||||||||

| Operating expenses including fee waivers/reimbursements | 1.03 | %(f) | 1.56 | % | 1.64 | % | 1.83 | % | 1.80 | % | 1.80 | %(f) | ||||||||||||

| Net investment loss including fee waivers/reimbursements | (0.56 | %)(f) | (1.24 | %) | (1.50 | %) | (1.72 | %) | (1.75 | %) | (1.79 | %)(f) | ||||||||||||

| PORTFOLIO TURNOVER RATE | 12 | %(e) | 58 | % | 38 | % | 90 | % | 0 | % | 0 | %(e) | ||||||||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Futures Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | Per share numbers have been calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Total return does not reflect the effect of sales charges. |

| (e) | Not annualized. |

| (f) | Annualized. |

| (g) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.10% and 1.64% for the six months ended October 31, 2016 and the year ended April 30, 2016, respectively. |

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2016 | 11 |

| Aspen Managed Futures Strategy Fund – Class I | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

For the Six Months Ended October 31, 2016 (Unaudited)(a) | For the Year Ended April 30, 2016 (a) | For the Year Ended April 30, 2015 (a) | For the Year Ended April 30, 2014 (a) | For the Year Ended April 30, 2013 (a) | For the Period August 2, 2011 (Inception) to April 30, 2012 (a) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 8.98 | $ | 10.17 | $ | 9.07 | $ | 9.36 | $ | 8.98 | $ | 10.00 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

Net investment loss(b) | (0.03 | ) | (0.09 | ) | (0.11 | ) | (0.11 | ) | (0.11 | ) | (0.11 | ) | ||||||||||||

| Net realized and unrealized gain/(loss) on investments | (0.28 | ) | (0.40 | ) | 1.42 | (0.06 | ) | 0.49 | (0.91 | ) | ||||||||||||||

| Total from investment operations | (0.31 | ) | (0.49 | ) | 1.31 | (0.17 | ) | 0.38 | (1.02 | ) | ||||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | – | (0.17 | ) | – | – | – | – | |||||||||||||||||

| Distributions from net realized gain on investments | – | (0.53 | ) | (0.21 | ) | (0.12 | ) | – | – | |||||||||||||||

| Total distributions | – | (0.70 | ) | (0.21 | ) | (0.12 | ) | – | – | |||||||||||||||

| REDEMPTION FEES ADDED TO PAID IN CAPITAL | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | ||||||||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.31 | ) | (1.19 | ) | 1.10 | (0.29 | ) | 0.38 | (1.02 | ) | ||||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 8.67 | $ | 8.98 | $ | 10.17 | $ | 9.07 | $ | 9.36 | $ | 8.98 | ||||||||||||

| TOTAL RETURN | (3.45 | %)(d) | (4.97 | %) | 14.51 | % | (1.81 | %) | 4.23 | % | (10.20 | %)(d) | ||||||||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (000's) | $ | 242,328 | $ | 264,598 | $ | 242,575 | $ | 167,258 | $ | 120,769 | $ | 90,450 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.24 | %(e)(f) | 1.22 | %(f) | 1.25 | % | 1.30 | % | 1.25 | % | 1.75 | %(e) | ||||||||||||

| Operating expenses including fee | ||||||||||||||||||||||||

| waivers/reimbursements | 1.24 | %(e) | 1.22 | % | 1.25 | % | 1.30 | % | 1.25 | % | 1.55 | %(e) | ||||||||||||

| Net investment loss including fee | ||||||||||||||||||||||||

| waivers/reimbursements | (0.78 | %)(e) | (0.94 | %) | (1.11 | %) | (1.20 | %) | (1.20 | %) | (1.54 | %)(e) | ||||||||||||

| PORTFOLIO TURNOVER RATE | 12 | %(d) | 58 | % | 38 | % | 90 | % | 0 | % | 0 | %(d) | ||||||||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Futures Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | Per share numbers have been calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Not annualized. |

| (e) | Annualized. |

| (f) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.31% and 1.30% for the six months ended October 31, 2016 and the year ended April 30, 2016, respectively. |

See Notes to Consolidated Financial Statements.

| 12 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

1. ORGANIZATION

Financial Investors Trust (the “Trust”), a Delaware statutory trust, is an open‐end management investment company registered under the Investment Company Act of 1940, as amended (“1940 Act”). The Trust consists of multiple separate portfolios or series. . This semi‐annual report describes the Aspen Managed Futures Strategy Fund (the “Fund”). The Fund seeks investment results that replicate as closely as possible, before fees and expenses, the price and yield performance of the Aspen Managed Futures Beta Index (the “MFBI” or “Index”). The Aspen Managed Futures Strategy Fund offers Class A and Class I shares.

Basis of Consolidation for the Aspen Futures Fund, Ltd.

Aspen Futures Fund, Ltd. (the “Subsidiary”), a Cayman Islands exempted company, is a wholly owned subsidiary of the Fund. The Subsidiary’s investment objective is designed to enhance the ability of the Fund to obtain exposure to equities, financial, currency and commodities markets consistent with the limits of the U.S. federal tax law requirements applicable to registered investment companies. The Subsidiary is subject to substantially the same investment policies and investment restrictions as the Fund. The Subsidiary acts as an investment vehicle for the Fund in order to effect certain commodity‐related investments on behalf of the Fund. Investments in the Subsidiary are expected to provide the Fund with exposure to the commodity markets within the limitations of Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”), and recent IRS revenue rulings, as discussed below under “Federal Income Taxes”. The Fund is the sole shareholder of the Subsidiary pursuant to a subscription agreement dated as of August 2, 2011, and it is intended that the Fund will remain the sole shareholder and will continue to control the Subsidiary. Under the Articles of Association of the Subsidiary, shares issued by the Subsidiary confer upon a shareholder the right to wholly own and vote at general meetings of the Subsidiary and certain rights in connection with any winding‐up or repayment of capital, as well as the right to participate in the profits or assets of the Subsidiary. The Fund may invest up to 25% of its total assets in shares of the Subsidiary. As a wholly owned subsidiary of the Fund, all assets and liabilities, income and expenses of the Subsidiary are consolidated in the financial statements and financial highlights of the Fund. All investments held by the Subsidiary are disclosed in the accounts of the Fund. As of October 31, 2016, net assets of the Fund were $249,570,266, of which $20,524,355 or 8.22%, represented the Fund’s ownership of all issued shares and voting rights of the Subsidiary.

2. SIGNIFICANT ACCOUNTING POLICIES

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates. The Fund is considered an investment company for financial reporting purposes under U.S. GAAP. The following is a summary of significant accounting policies consistently followed by the Fund and Subsidiary in preparation of the financial statements.

Investment Valuation: The Fund generally values its securities based on market prices determined at the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern Time, on each day the NYSE is open for trading.

For equity securities and mutual funds that are traded on an exchange, the market price is usually the closing sale or official closing price on that exchange. In the case of equity securities not traded on an exchange, or if such closing prices are not otherwise available, the securities are valued at the mean of the most recent bid and ask prices on such day. Redeemable securities issued by open‐end registered investment companies are valued at the investment company’s applicable net asset value, with the exception of exchange‐traded open‐end investment companies, which are priced as equity securities.

The market price for debt obligations is generally the price supplied by an independent third‐party pricing service approved by the Board of Trustees (the “Board”), which may use a matrix, formula or other objective method that takes into consideration quotations from dealers, market transactions in comparable investments, market indices and yield curves. If vendors are unable to supply a price, or if the price supplied is deemed to be unreliable, the market price may be determined using quotations received from one or more brokers–dealers that make a market in the security.

Futures contracts that are listed or traded on a national securities exchange, commodities exchange, contract market or comparable over‐the‐counter market, and that are freely transferable, are valued at their closing settlement price on the exchange on which they are primarily traded or based upon the current settlement price for a like instrument acquired on the day on which the instrument is being valued. A settlement price may not be used if the market makes a limit move with respect to a particular commodity.

Forward currency exchange contracts have a fair value determined by the prevailing foreign currency exchange daily rates and current foreign currency exchange forward rates. The foreign currency exchange forward rates are calculated using an automated system that estimates rates on the basis of the current day foreign currency exchange rates and forward foreign currency exchange rates supplied by a pricing service.

| Semi-Annual Report | October 31, 2016 | 13 |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

Investment securities that are primarily traded on foreign securities exchanges are valued at the preceding closing values of such securities on their respective exchanges, except when an occurrence subsequent to the time a value was so established is likely to have changed such value. In such an event, the fair value of those securities are determined in good faith through consideration of other factors in accordance with procedures established by and under the general supervision of the Board.

When such prices or quotations are not available, or when Aspen Partners, Ltd. (the “Adviser”) believes that they are unreliable, securities may be priced using fair value procedures approved by the Board.

Fair Value Measurements: The Fund discloses the classification of its fair value measurements following a three‐tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

| Level 1 – | Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| Level 2 – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

| Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

The following is a summary of each input used to value the Fund as of October 31, 2016:

| Investments in Securities at Value | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Government Bonds | $ | – | $ | 90,348,292 | $ | – | $ | 90,348,292 | ||||||||

| Short Term Investments | ||||||||||||||||

| Money Market Fund | 9,713,818 | – | – | 9,713,818 | ||||||||||||

| U.S. Treasury Bills | – | 123,083,395 | – | 123,083,395 | ||||||||||||

| TOTAL | $ | 9,713,818 | $ | 213,431,687 | $ | – | $ | 223,145,505 | ||||||||

| Other Financial Instruments | ||||||||||||||||

| Assets: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Equity Contracts | $ | 553,838 | $ | – | $ | – | $ | 553,838 | ||||||||

| Foreign Currency Contracts | 831,010 | – | – | 831,010 | ||||||||||||

| Interest Rate Contracts | 251,490 | – | – | 251,490 | ||||||||||||

| Liabilities: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Commodity Contracts | (2,437,012 | ) | – | – | (2,437,012 | ) | ||||||||||

| Equity Contracts | (44,116 | ) | – | – | (44,116 | ) | ||||||||||

| Foreign Currency Contracts | (174,409 | ) | – | – | (174,409 | ) | ||||||||||

| TOTAL | $ | (1,019,199 | ) | $ | – | $ | – | $ | (1,019,199 | ) | ||||||

The Fund recognizes transfers between levels as of the end of the period. For the six months ended October 31, 2016, the Fund did not have any transfers between Level 1 and Level 2 securities. For the six months ended October 31, 2016, the Fund did not have any securities that used significant unobservable inputs (Level 3) in determining fair value.

| 14 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

Investment Transactions and Investment Income: Investment transactions are accounted for on the date the investments are purchased or sold (trade date). Realized gains and losses from investment transactions are reported on an identified cost basis, which is the same basis the Fund uses for federal income tax purposes. Interest income, which includes accretion of discounts, is accrued and recorded as earned. Dividend income is recognized on the ex‐dividend date or for certain foreign securities, as soon as information is available to the Fund. All of the realized and unrealized gains and losses and net investment income, are allocated daily to each class in proportion to its average daily net assets.

Foreign Securities: The Fund may directly purchase securities of foreign issuers. Investing in securities of foreign issuers involves special risks not typically associated with investing in securities of U.S. issuers. The risks include possible reevaluation of currencies, the inability to repatriate foreign currency, less complete financial information about companies and possible future adverse political and economic developments. Moreover, securities of many foreign issuers and their markets may be less liquid and their prices more volatile than those of securities of comparable U.S. issuers.

Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Investment valuations and other assets and liabilities initially expressed in foreign currencies are converted each business day into U.S. dollars based upon current exchange rates. Prevailing foreign exchange rates may generally be obtained at the close of the NYSE (normally, 4:00 p.m. Eastern Time). The portion of realized and unrealized gains or losses on investments due to fluctuations in foreign currency exchange rates is not separately disclosed and is included in realized and unrealized gains or losses on investments, when applicable.

Foreign Currency Spot Contracts: The Fund may enter into foreign currency spot contracts to facilitate transactions in foreign securities or to convert foreign currency receipts into U.S. dollars. A foreign currency spot contract is an agreement between two parties to buy and sell currencies at the current market rate, for settlement generally within two business days. The U.S. dollar value of the contracts is determined using current currency exchange rates supplied by a pricing service. The contract is marked‐to‐market daily for settlements beyond one day and any change in market value is recorded as an unrealized gain or loss. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value on the open and close date. Losses may arise from changes in the value of the foreign currency, or if the counterparties do not perform under the contract’s terms. The maximum potential loss from such contracts is the aggregate face value in U.S. dollars at the time the contract was opened.

Trust Expenses: Some expenses of the Trust can be directly attributed to the Fund. Expenses which cannot be directly attributed to the Fund are apportioned among all funds in the Trust based on average net assets of each fund.

Fund and Class Expenses: Expenses that are specific to a class of shares of the Fund, including distribution fees (Rule 12b‐1 fees) and shareholder servicing fees, are charged directly to that share class. All expenses of the Fund, other than class specific expenses, are allocated daily to each class in proportion to its average daily net assets.

Federal Income Taxes: The Fund complies with the requirements under Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies and intends to distribute substantially all of their net taxable income and net capital gains, if any, each year so that it will not be subject to excise tax on distributed income and gains. The Fund is not subject to income taxes to the extent such distributions are made.

As of and during the six months ended October 31, 2016, the Fund did not have a liability for any unrecognized tax benefits. The Fund files U.S. federal, state, and local tax returns as required. The Fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return for federal purposes and four years for most state returns. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

Distributions to Shareholders: The Fund normally pays dividends and distributes capital gains, if any, on an annual basis. Income dividend distributions are derived from interest and other income the Fund receives from its investments, including short term capital gains. Long term capital gains distributions are derived from gains realized when the Fund sells a security it has owned for more than a year. The Fund may make additional distributions and dividends at other times if the portfolio manager believes doing so may be necessary for the Fund to avoid or reduce taxes.

3. DERIVATIVE INSTRUMENTS

The Fund uses derivatives (including futures) to pursue its investment objective. The Fund’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments. These risks may include (i) the risk that the counterparty to a derivative transaction may not fulfill its contractual obligations, (ii) risk of mispricing or improper valuation, and (iii) the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset, rate or index. These risks could cause

| Semi-Annual Report | October 31, 2016 | 15 |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

the Fund to lose more than the principal amount invested. In addition, investments in derivatives involve leverage, which means a small percentage of assets invested in derivatives can have a disproportionately large impact on the Fund.

The Fund’s use of derivatives can result in losses due to unanticipated changes in the market risk factors and the overall market. In instances where the Fund is using derivatives to decrease, or hedge, exposures to market risk factors for securities held by the Fund, there are also risks that those derivatives may not perform as expected resulting in losses for the combined or hedged positions. Derivatives may have little or no initial cash investment relative to their market value exposure and therefore can produce significant gains or losses in excess of their cost. This use of embedded leverage allows the Fund to increase its market value exposure relative to its net assets and can substantially increase the volatility of the Fund’s performance.

In addition, use of derivatives may increase or decrease exposure to the following risk factors:

| • | Equity Risk: Equity risk relates to the change in value of equity securities as they relate to increases or decreases in the general market. |

| • | Interest Rate Risk: When the Fund invests in fixed‐income securities or derivatives, the value of an investment in the Fund will fluctuate with changes in interest rates. Typically, a rise in interest rates causes a decline in the value of fixed‐income securities or derivatives owned by the Fund. In general, the market price of debt securities with longer maturities will increase or decrease more in response to changes in interest rates than shorter‐term securities. Other risk factors include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments). |

| • | Foreign Currency Risk: Currency trading involves significant risks, including market risk, interest rate risk, country risk, counterparty credit risk and short sale risk. Market risk results from the price movement of foreign currency values in response to shifting market supply and demand. Interest rate risk arises whenever a country changes its stated interest rate target associated with its currency. Country risk arises because virtually every country may interfer with international transactions in its currency. Counterparty credit risk arises when the counterparty will not fulfill its obligations to the Fund. Short sale risk arises from the sale of a security that is not owned, or any sale that is completed by the delivery of a security borrowed. |

| • | Commodity Risk: Exposure to the commodities markets may subject the Fund to greater volatility than investments in traditional securities. Commodity prices are influenced by unfavorable weather, animal and plant disease, geologic and environmental factors, as well as changes in government regulation such as tariffs, embargoes or burdensome production rules and restrictions. |

Futures: The Fund and the Subsidiary may enter into futures contracts. Futures contracts are agreements between two parties to buy and sell a particular commodity, instrument or index for a specified price on a specified future date. When the Fund or the Subsidiary enters into a futures contract, it is required to deposit with (or for the benefit of) its broker an amount of cash or short‐term high‐quality securities as “initial margin”. The margin requirements are set by the exchange on which the contract is traded and may be modified during the term of the contract. The initial margin is in the nature of a performance bond or good faith deposit on the futures contract that is returned to the Fund upon termination of the contract, assuming all contractual obligations have been satisfied. As the value of the contract changes, the value of the futures contract position increases or declines. Subsequent payments, known as “variation margin”, are made or received by the Fund or the Subsidiary each day, depending on the price fluctuations in the fair value of the contract and the value of cash or securities on deposit with the broker. Such payments or receipts are recorded for financial statement purposes as unrealized gains or losses by the Fund. Variation margin does not represent a borrowing or loan by the Fund but is instead a settlement between the Fund and the broker of the amount one would owe the other if the futures contract expired. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. When the Fund or the Subsidiary enters into a futures contract certain risks may arise, such as illiquidity in the futures market, which may limit the Fund’s or the Subsidiary’s ability to close out a futures contract prior to settlement date, and unanticipated movements in the value of securities, commodities or interest rates. Futures contracts are exchange‐traded. Exchange‐traded futures are standardized contracts and are settled through a clearing house with fulfillment supported by the credit of the exchange. Therefore, counterparty credit risk to the Fund and the Subsidiary is reduced. With exchange traded futures, there is minimal counterparty credit risk to the Funds since futures are exchange traded and the exchange’s clearinghouse, as a counterparty to all exchange traded futures, guarantees the futures against default.

| 16 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

Consolidated Balance Sheet – Fair Value of Derivative Instruments as of October 31, 2016

| Risk Exposure | Asset Derivatives Balance Sheet Location | Fair Value | Liabilities Derivatives Balance Sheet Location | Fair Value | ||||||

| Futures Contracts | Unrealized appreciation on futures contracts(a) | $ | 1,636,338 | Unrealized depreciation on futures contracts (a) | $ | 2,655,537 | ||||

| $ | 1,636,338 | $ | 2,655,537 | |||||||

| Risk Exposure to Fund | ||||||||||

| Commodity Contracts | $ | – | $ | 2,437,012 | ||||||

| Equity Contracts | 553,838 | 44,116 | ||||||||

| Foreign Currency Contracts | 831,010 | 174,409 | ||||||||

| Interest Rate Contracts | 251,490 | – | ||||||||

| $ | 1,636,338 | $ | 2,655,537 | |||||||

| (a) | Represents cumulative appreciation/(depreciation) of futures contracts as reported in the Consolidated Statement of Investments. Only the current day’s net variation margin is reported within the Consolidated Statement of Assets and Liabilities. |

Consolidated Statement of Operations – The effect of Derivative Instruments for the six months ended October 31, 2016:

| Derivatives Instruments | Location of Gain/(Loss) on Derivatives Recognized in Income | Realized Gain/ (Loss) on Derivatives Recognized in Income | Change in Unrealized Appreciation/(Depreciation) on Derivatives Recognized in Income | ||||||

| Futures Contracts | Net realized loss on futures contracts/Net change in unrealized depreciation on futures contracts | $ | (2,559,565 | ) | $ | (6,139,116 | ) | ||

| $ | (2,559,565 | ) | $ | (6,139,116 | ) | ||||

| Risk Exposure to Fund | |||||||||

| Commodity Contracts | $ | 824,954 | $ | (3,948,875 | ) | ||||

| Equity Contracts | (6,923,613 | ) | 1,123,509 | ||||||

| Foreign Currency Contracts | 1,523,088 | (4,122,371 | ) | ||||||

| Interest Rate Contracts | 2,016,006 | 808,621 | |||||||

| $ | (2,559,565 | ) | $ | (6,139,116 | ) | ||||

The average number of net futures contracts held by the fund during the period was 1,962.

4. TAX BASIS INFORMATION

Tax Basis of Investments: As of October 31, 2016, the aggregate cost of investments, gross unrealized appreciation/(depreciation) and net unrealized appreciation for Federal tax purposes was as follows:

| Cost of Investments | Gross Appreciation (excess of value over tax cost) | Gross Depreciation (excess of tax cost over value) | Net Appreciation on Investments | |||||||||||||

| Aspen Managed Futures Strategy Fund | $ | 223,102,557 | $ | 60,337 | $ | (17,389 | ) | $ | 42,948 | |||||||

Tax Basis of Distributions to Shareholders: Distributions are determined in accordance with federal income tax regulations, which differ from GAAP, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

The tax character of distributions paid during the year ending April 30, 2016 were as follows:

| Ordinary Income | Long-Term Capital Gain | |||||||

| Aspen Managed Futures Strategy Fund | $ | 13,114,807 | $ | 8,439,863 | ||||

| Semi-Annual Report | October 31, 2016 | 17 |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

The amounts and characteristics of tax basis distributions and composition of distributable earnings/(accumulated losses) are finalized at fiscal year-end. Accordingly, tax basis balances have not been determined as of October 31, 2016.

5. SHARES OF BENEFICIAL INTEREST

The capitalization of the Trust consists of an unlimited number of shares of beneficial interest with no par value per share. Holders of the shares of the Fund of the Trust have one vote for each share held and a proportionate fraction of a vote for each fractional share. All shares issued and outstanding are fully paid and are transferable and redeemable at the option of the shareholder. Purchasers of the shares do not have any obligation to make payments to the Trust or its creditors solely by reason of the purchasers’ ownership of the shares. Shares have no pre-emptive rights.

Fund shares redeemed within 30 days of purchase may incur a 2% short-term redemption fee deducted from the redemption amount. The amount of redemption fees received during the period are presented in the Consolidated Statement of Changes in Net Assets.

6. MANAGEMENT AND RELATED-PARTY TRANSACTIONS

The Adviser, subject to the authority of the Board, is responsible for the overall management and administration of the Fund’s business affairs. The Adviser manages the investments of the Fund in accordance with the Fund’s investment objective, policies and limitations and investment guidelines established jointly by the Adviser and the Board. Pursuant to the Investment Advisory Agreement, (the “Advisory Agreement”), the Fund will pay the Adviser an annual management fee of 0.75%, based on the Fund’s average daily net assets. The management fee is paid on a monthly basis.

The Subsidiary has entered into a separate advisory agreement (the “Subsidiary Advisory Agreement”) with the Adviser for the management of the Subsidiary’s portfolio pursuant to which the Subsidiary is obligated to pay the Adviser a management fee at the same rate that the Fund pays the Adviser for investment advisory services provided to the Fund. The Adviser has agreed to waive the advisory fee it receives from the Fund in an amount equal to the management fee paid by the Subsidiary. This waiver may not be terminated or modified without the consent of the Board. This agreement may not be terminated or modified prior to this date except with the approval of the Board. For the period ended October 31, 2016, this amount equaled $92,487 and is disclosed in the Consolidated Statement of Operations. These waivers are not subject to reimbursement/recoupment.

The Adviser has contractually agreed to limit the Fund’s total annual fund operating expenses (exclusive of distribution and service (12b-1) fees, shareholder services fees, acquired fund fees and expenses, brokerage expenses, interest expense, taxes and extraordinary expenses) to 1.55% of the Fund’s average daily net assets for each of Class A and Class I Shares. This agreement (the “Expense Agreement”) is in effect from September 1, 2016 through August 31, 2017. The prior Expense Agreement was in effect from April 1, 2013 through August 31, 2016. The Adviser will be permitted to recover, on a class-by-class basis, expenses it has borne through the Expense Agreement to the extent that the Fund’s expenses in later periods fall below the expense cap in effect at the time of waiver or reimbursement. Notwithstanding the foregoing, the Fund will not be obligated to pay any such fees and expenses more than three years after the end of the fiscal year in which the fees or expenses were foregone or reimbursed. The Adviser may not discontinue or modify this waiver prior to August 31, 2017 without the approval by the Fund’s Board of Trustees.

Fund Administrator Fees and Expenses

ALPS Fund Services, Inc. (“ALPS”) serves as administrator to the Fund and the Fund has agreed to pay expenses incurred in connection with its administrative activities. Pursuant to an Administration Agreement, ALPS provides operational services to the Fund including, but not limited to, fund accounting and fund administration and generally assist in the Fund’s operations. Officers of the Trust are employees of ALPS. The Fund’s administration fee is accrued on a daily basis and paid monthly. Administration fees paid by the Fund for the six months ended October 31, 2016 are disclosed in the Consolidated Statement of Operations.

ALPS is reimbursed by the Fund for certain out-of-pocket expenses.

Transfer Agent

ALPS serves as transfer, dividend paying and shareholder servicing agent for the Fund. ALPS receives an annual minimum fee, a fee based upon the number of shareholder accounts, and is also reimbursed by the Fund for certain out-of-pocket expenses. Transfer agent fees paid by the Fund for the six months ended October 31, 2016 are disclosed in the Consolidated Statement of Operations.

Compliance Services

ALPS provides services that assist the Trust’s chief compliance officer in monitoring and testing the policies and procedures of the Trust in conjunction with requirements under Rule 38a-1 under the 1940 Act and receives an annual base fee. ALPS is reimbursed for certain out-of-pocket expenses by the Fund. Compliance service fees paid by the Fund for the six months ended October 31, 2016 are disclosed in the Consolidated Statement of Operations.

| 18 | www.aspenfuturesfund.com |

| Aspen Managed Futures Strategy Fund | Notes to Consolidated Financial Statements |

October 31, 2016 (Unaudited)

Principal Financial Officer

ALPS receives an annual fee for providing principal financial officer services to the Fund. Principal financial officer fees paid by the Fund for the six months ended October 31, 2016 are disclosed in the Consolidated Statement of Operations.

Distributor

ALPS Distributors, Inc. (“ADI” or the “Distributor”) (an affiliate of ALPS) acts as the distributor of the Fund’s shares pursuant to a Distribution Agreement with the Trust. Shares are sold on a continuous basis by ADI as agent for the Fund, and ADI has agreed to use its best efforts to solicit orders for the sale of the Fund’s shares, although it is not obliged to sell any particular amount of shares. ADI is not entitled to any compensation for its services as Distributor. ADI is registered as a broker-dealer with the U.S. Securities and Exchange Commission.

The Fund has adopted a plan of distribution for Class A shares pursuant to Rule 12b-1 under the 1940 Act (the “Plan”). The Plan allows the Fund to use Class A assets to pay fees in connection with the distribution and marketing of Class A shares and/or the provision of shareholder services to Class A shareholders. The Plan permits payment for services in connection with the administration of plans or programs that use Class A shares as their funding medium and for related expenses. The recipients of such payments may include the Distributor, other affiliates of the Adviser, broker-dealers, financial institutions, plan sponsors and administrators and other financial intermediaries through which investors may purchase shares of the Fund. The Plan permits the Fund to use its Class A assets to make total payments at an annual rate of up to 0.25% of the Fund’s average daily net assets attributable to its Class A shares. The expenses of the plan are reflected as distribution and service fees in the Consolidated Statement of Operations.

The Fund has adopted a shareholder service plan (a “Shareholder Services Plan”) for Class A shares. Under the Shareholder Services Plan the Fund is authorized to compensate certain financial intermediaries, including broker-dealers and Fund affiliates, which may include the Distributor, Adviser and/or the transfer agent (“Participating Organizations”), an aggregate fee in an amount not to exceed on an annual basis 0.15% for Class A shares of the average daily net asset value of the Class A shares attributable to or held in the name of a Participating Organizations for its clients as compensation for providing shareholder service activities, which do not include distribution services, pursuant to an agreement with a Participating Organizations. Any amount of such payment not paid to the Participating Organizations during the Fund’s fiscal year for such service activities shall be reimbursed to the Fund. Shareholder Services Plan fees are included with distribution and service fees on the Consolidated Statement of Operations.

Certain intermediaries may charge networking, omnibus account or other administrative fees with respect to transactions in shares of the Fund. Transactions may be processed through the National Securities Clearing Corporation (“NSCC”) or similar systems or processed on a manual basis. These fees are paid by the Fund to the Distributor, which uses such fees to reimburse intermediaries. In the event an intermediary receiving payments from the Distributor on behalf of the Fund converts from a networking structure to an omnibus account structure or otherwise experiences increased costs, fees borne by the Fund may increase. Fees paid by the Fund for the six months ended October 31, 2016 are disclosed in the Consolidated Statement of Operations as Delegated Transfer Agent Equivalent Services.

Index Licensing Services

The Fund has adopted an Index Licensing Agreement with Quantitative Equity Strategies, LLC (“QES”) and the Adviser, joint owners of the Index, pursuant to which the Fund pays QES a monthly annualized licensing fee of 0.25%, based on the Fund’s average daily net assets for the right to use the Index in connection with the Fund.

7. SECURITIES TRANSACTIONS

The cost of purchases and proceeds from sales of U.S. Government securities (excluding short-term securities) during the six months ended October 31, 2016 were as follows:

| Aspen Managed Futures Strategy Fund | ||||

| Cost of Investments Purchased | $ | 17,279,475 | ||

| Proceeds from Investments Sold | $ | 84,383,518 | ||

8. INDEMNIFICATIONS

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liability arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that may contain general indemnification clauses, which may permit indemnification to the extent permissible under applicable law. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred.

| Semi-Annual Report | October 31, 2016 | 19 |

| Aspen Managed Futures Strategy Fund | Additional Information |

October 31, 2016 (Unaudited)

1. FUND HOLDINGS