UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08194

FINANCIAL INVESTORS TRUST

(Exact name of Registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Karen Gilomen, Esq., Secretary

Financial Investors Trust

1290 Broadway, Suite 1100

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: April 30

Date of reporting period: October 31, 2018

| Item 1. | Reports to Stockholders. |

TABLE OF CONTENTS

| PAGE | |

| Manager Commentary | |

| Aspen Managed Futures Strategy Fund | 1 |

| Aspen Portfolio Strategy Fund | 3 |

| Performance Update | |

| Aspen Managed Futures Strategy Fund | 5 |

| Aspen Portfolio Strategy Fund | 7 |

| Consolidated Disclosure of Fund Expenses | 9 |

| Consolidated Schedule of Investments | |

| Aspen Managed Futures Strategy Fund | 10 |

| Aspen Portfolio Strategy Fund | 12 |

| Consolidated Statements of Assets & Liabilities | 14 |

| Consolidated Statements of Operations | 15 |

| Consolidated Statements of Changes in Net Assets | |

| Aspen Managed Futures Strategy Fund | 16 |

| Aspen Portfolio Strategy Fund | 17 |

| Consolidated Financial Highlights | |

| Aspen Managed Futures Strategy Fund | 18 |

| Aspen Portfolio Strategy Fund | 20 |

| Notes to Consolidated Financial Statements | 22 |

| Additional Information | 33 |

| Privacy Policy | 34 |

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website at www.aspenfuturesfund.com and you will be notified by mail each time a report is posted and provided with a website link to access the report.

Beginning on January 1, 2019, you may, notwithstanding the availability of shareholder reports online, elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1.855.845.9444 to let the Funds know you wish to continue receiving paper copies of your shareholder reports.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by enrolling at www.aspenfuturesfund.com.

| Aspen Managed Futures Strategy Fund | Manager Commentary |

October 31, 2018 (Unaudited)

November 5, 2018

Performance Results

For the six-month period ending October 31, 2018, the Class I shares of the Aspen Managed Futures Strategy Fund (the “Fund”) posted a return of -1.25%. Per its mandate, the Fund maintained tight correlation to the Aspen Managed Futures Beta Index (“Aspen MFBI” or the “Index”). The Index uses a combination of trend and counter-trend algorithms to determine exposures to 23 futures markets. In following the Index, the Fund can take long or short positions in each of the eligible markets. A long position in a futures market may profit if the price of the futures contract rises, whereas a short position may profit if the price of the futures contract falls.

The BTOP50 Index, a managed futures benchmark, returned -2.77% over the same period. It is important to note that there are substantive differences between the Fund and this index in terms of construction. There were no significant changes to the Fund strategy during this period.

Explanation of Fund Performance

Over most of this six-month period, backdrop market volatility was very low, and that was reflected in low monthly volatility for the Fund itself. Every monthly return for the Fund in the six-month period was less than 1% in magnitude, and June, July, and August produced a remarkable three-month stretch of 0.00% Fund returns each month.

While low-volatility market environments are not typically auspicious for trend-following models like the Aspen MFBI, they do not generally produce significant losses either. The low-vol backdrop that prevailed from May through September fit this mold, as the Fund’s minor losses aggregated to just -0.44%, via a -0.89% return in May, a +0.45% return in September, and the 0.00% returns in each of the three months in between. Losses from trend following were mitigated by gains in the counter-trend model.

In October, the market backdrop changed dramatically, in a manner reminiscent of the activity in February, 2018. As in February, U.S. equity markets in October reversed from all-time highs into a rapidly developing correction (i.e., a drop of greater than 10% in major indices). Global equity markets participated in the decline. Short positions in European equity futures markets mitigated the resulting losses, but could not overcome them entirely. By mid-month, the trend model was net short equities.

Initially the drop was accompanied by rising global interest rates, which enabled gains from the trend model’s short fixed income positioning (bond prices generally fall as interest rates rise), but as the correction deepened, markets assumed more traditional “risk-off” behavior, such that model losses from rising bond prices offset gains from the recently established net short equity positioning. An equity rally at the end of the month pulled U.S. equities out of their correction; on those days the short fixed income trends mitigated losses from the short equity trends. In the end, the Fund returned -0.88% for the month of October.

Another notable similarity to February is that both months exemplified the common tendency for Aspen’s model to outperform the managed futures universe in particularly difficult backdrops for equities. The industry benchmark BTOP50 Index’s return for the month of October was -2.44%, so October returns produced the entire differential between the Fund and the benchmark over the reporting period.

Outlook

Despite the low volatility that has prevailed for much of the year, 2018 has provided a couple of glimpses indicating markets may be more likely to demonstrate increased volatility given an inducement to do so. Historically, persistently elevated volatility has tended to provide a relatively favorable backdrop for trend following. However, given the strength of the domestic and global economies, a full-blown equity bear market would come as a surprise at present (though of course not an impossible surprise), and for the past several years, the only circumstances under which even historically “normal” levels of volatility have prevailed is during brief periods of equity stress. As October demonstrates, short-lived volatility spikes are typically not helpful to a trend system, since they are usually sparked by a change of direction for risk assets, and they often end just as rapidly with another change of direction (and both such changes are essentially anti-trend by nature). To catalyze improved fortunes for trend following models, we continue to look for more sustained market volatility. With less accommodative monetary policy and an economy where a decade of recovery may be approaching its peak, a return to more normalized volatility appears increasingly likely, though of course timing is always difficult to gauge.

Sincerely,

Bryan R. Fisher

William Ware Bush

Aspen Partners, Ltd.

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data please call 1-855-845-9444.

| Semi-Annual Report | October 31, 2018 | 1 |

| Aspen Managed Futures Strategy Fund | Manager Commentary |

October 31, 2018 (Unaudited)

The views of Aspen Partners, Ltd. and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writers’ current views. The views expressed are those of the Fund’s adviser only, and represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither Aspen Partners Ltd. nor the Fund accepts any liability for losses either direct or consequential caused by the use of this information.

The Aspen Managed Futures Strategy Fund is distributed by ALPS Distributors, Inc.

The Fund is subject to investment risks, including possible loss of the principal amount invested and therefore is not suitable for all investors. The Fund may not achieve its objectives.

Diversification does not eliminate the risk of experiencing investment losses.

Correlation - a statistical measure of how two securities or portfolios move in relation to each other.

Aspen Managed Futures Beta Index (Aspen MFBI) is constructed using a quantitative, rules-based model designed to replicate the trend following and counter-trend exposure of futures markets by allocating assets to liquid futures contracts of certain financial and commodities futures markets. The Index therefore seeks to reflect the performance of strategies and exposures common to a broad universe of futures markets, i.e., managed futures beta. The Index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor cannot invest directly in the Index.

Barclay BTOP50 Index is an index of the largest investable CTA programs as measured by assets under management. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor may not invest directly into the Index.

2

| Aspen Portfolio Strategy Fund | Manager Commentary |

October 31, 2018 (Unaudited)

November 5, 2018

Performance Results

For the six-month period ending October 31, 2018, the Class I shares of the Aspen Portfolio Strategy Fund (the “Fund”) posted a return of -1.36%. Per its mandate, the Fund traded the Aspen Portfolio Strategy, which combines full exposure to US large-cap equities (the “Equity Strategy”) with full exposure to Aspen’s proprietary diversified trend following program (the “Futures Strategy”). To capture the Equity Strategy, the Fund can employ a variety of vehicles, including exchange-traded funds and futures contracts. To capture the Futures Strategy, the Fund can take long or short positions in each eligible futures market. A long position in a futures market may profit if the price of the futures contract rises, whereas a short position may profit if the price of the futures contract falls.

The S&P 500® Index, a US large-cap equity benchmark, returned +3.40%. See the following section for a description of the sources of the sub-period and full-period return differential between the Fund and the S&P 500.

Explanation of Fund Performance

Over the first five months of this six-month period, backdrop market volatility was very low, and that was reflected in single-digit annualized volatility for the Fund. May (+0.53%), June (+0.45%), and September (+0.45%) returns were each only about half a percent in magnitude, while July (+3.04%) and August (+3.28%) returns were larger. All five months were profitable, via positive returns for the S&P 500, which were captured by the Equity Strategy.

While low-volatility market environments are not typically auspicious for trend-following models like the Aspen MFBI, they do not generally produce significant losses either. The low-vol backdrop that prevailed from May through September fit this mold, as the Fund’s trend-following Futures Strategy produced modest losses over the five-month period, but never large enough to overcome the monthly gains from equities.

In October, the market backdrop changed dramatically, in a manner reminiscent of the activity in February, 2018. As in February, U.S. equity markets in October reversed from all-time highs into a rapidly developing correction (i.e., a drop of greater than 10% in major indices). Global equity markets participated in the decline. Short positions in the Futures Strategy’s European equity futures trend positions mitigated the resulting losses in the Strategy, but could not overcome them entirely. By mid-month, the trend model was net short equities.

Initially the equity drop was accompanied by rising global interest rates, which enabled gains from the Futures Strategy’s short fixed income positioning (bond prices generally fall as interest rates rise), but as the correction deepened, markets assumed more traditional “risk-off” behavior, such that model losses from rising bond prices offset gains from the recently established net short equity positioning. An equity rally at the end of the month pulled U.S. equities out of their correction; the S&P 500 produced a -6.84% return for October (total return). In the end-of-month rally, the short fixed income trends mitigated losses from the short equity trends within the Futures Strategy. In the end, the Fund returned -8.73% for the month of October.

Outlook

Despite the low volatility that has prevailed for much of the year, 2018 has provided a couple of glimpses indicating markets may be more likely to demonstrate increased vol given an inducement to do so. Historically, persistently elevated volatility has tended to provide a relatively favorable backdrop for trend following strategies, such as the Fund’s Futures Strategy. However, given the strength of the domestic and global economies, a full-blown equity bear market would come as a surprise at present (though of course not an impossible surprise), and for the past several years, the only circumstances under which even historically “normal” levels of volatility have prevailed is during brief periods of equity stress. As October demonstrates, short-lived volatility spikes are typically not helpful to a trend system, since they are usually sparked by a change of direction for risk assets, and they often end just as rapidly with another change of direction (and both such changes are essentially anti-trend by nature). To catalyze improved fortunes for trend following models, we continue to look for more sustained market volatility, with an ideal environment for the Fund most likely being one of equity gains against more a volatile backdrop. With less accommodative monetary policy and an economy where a decade of recovery may be approaching its peak, a return to more normalized volatility appears increasingly likely, though of course timing is always difficult to gauge.

Sincerely,

Bryan R. Fisher

William Ware Bush

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data please call 1-855-845-9444.

| Semi-Annual Report | October 31, 2018 | 3 |

| Aspen Portfolio Strategy Fund | Manager Commentary |

October 31, 2018 (Unaudited)

The views of Aspen Partners, Ltd. and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writers’ current views. The views expressed are those of the Fund’s adviser only, and represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the portfolios or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither Aspen Partners Ltd. nor the Fund accepts any liability for losses either direct or consequential caused by the use of this information.

The Aspen Portfolio Strategy Funds are distributed by ALPS Distributors, Inc.

The Fund is subject to investment risks, including possible loss of the principal amount invested and therefore is not suitable for all investors. The Fund may not achieve its objectives.

Diversification does not eliminate the risk of experiencing investment losses.

The S&P 500® Index is an unmanaged index of 500 common stocks chosen for market size, liquidity and industry group representation. It is a market-value weighted index. The Index is not actively managed and does not reflect any deductions for fees, expenses or taxes. An investor may not invest directly in the Index.

4

| Aspen Managed Futures Strategy Fund | Performance Update |

October 31, 2018 (Unaudited)

Annualized Total Return Performance as of October 31, 2018

| Since | Expense Ratios | |||||

| Aspen Managed Futures Strategy Fund | 1 Year | 3 Year | 5 Year | Inception* | Total | Net(1) |

| Aspen Managed Futures Strategy Fund - Class A (NAV)(2) | -3.37% | -3.95% | -0.97% | -1.87% | 1.82% | 1.82% |

| Aspen Managed Futures Strategy Fund - Class A (MOP)(3) | -8.72% | -5.74% | -2.08% | -2.63% | 1.82% | 1.82% |

| Aspen Managed Futures Strategy Fund - Class I | -3.31% | -3.96% | -0.81% | -1.65% | 1.48% | 1.48% |

| SG CTA Index(4) | -5.22% | -1.84% | 2.02% | 0.11% | ||

| Aspen Managed Futures Beta Index(5) | -2.60% | -3.47% | -0.38% | -1.16% | ||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please call 1-855-845-9444.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Subject to investment risks, including possible loss of the principal amount invested.

Returns for periods less than 1 year are cumulative.

| * | Fund Inception date of August 2, 2011. |

| (1) | Aspen Partners, Ltd. (the “Adviser”) has agreed to waive and/or reimburse fees or expenses in order to limit total annual Fund operating expenses after fee waiver/expense reimbursements (excluding distribution and service (12b-1) fees, shareholder services fees, acquired fund fees and expenses, brokerage expenses, interest expenses, taxes and extraordinary expenses) to 1.55% of the Funds’ average daily net assets. This agreement (the “Expense Agreement”) is in effect through August 31, 2019. The Adviser will be permitted to recover, on a class-by-class basis, expenses it has borne through the Expense Agreement to the extent that the Funds’ expenses in later periods fall below the expense cap in effect at the time of waiver or reimbursement. Notwithstanding the foregoing, the Fund will not be obligated to pay any such deferred fees and expenses more than three years after the date of the waiver or reimbursement. The Expense Agreement may not be terminated or modified prior to August 31, 2019 except with the approval of the Funds’ Board of Trustees |

| (2) | Net Asset Value (NAV) is the share price without sales charges. |

| (3) | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Funds’ maximum sales charge of 5.50%. |

| (4) | The SG CTA Index (formerly, the Newedge CTA Index) provides the market with a reliable daily performance benchmark of major commodity trading advisors (CTAs). The SG CTA Index calculates the daily rate of return for a pool of CTAs selected from the larger managers that are open to new investment. Selection of the pool of qualified CTAs used in construction of the Index will be conducted annually, with re-balancing on January 1st of each year. A committee of industry professionals has been established to monitor the methodology of the index on a regular basis. The Index is not actively managed and does not reflect any deduction for fees, expenses or taxes. An investor cannot invest directly in the Index. |

| (5) | Aspen Managed Futures Beta Index – The Managed Futures Beta Index is constructed using a quantitative, rules-based model designed to replicate the trend-following and counter-trend exposure of futures markets by allocating assets to liquid futures contracts of certain financial and commodities futures markets. The Index therefore seeks to reflect the performance of strategies and exposures common to a broad universe of futures markets, i.e., managed futures beta. The index is not actively managed and does not reflect any deductions for fees, expense or taxes. An investor may not invest directly in an index. |

Portfolio Composition as of October 31, 2018

As a percentage of Net Assets^

| ^ | Holdings subject to change, and may not reflect the current or future position of the portfolio. |

| Semi-Annual Report | October 31, 2018 | 5 |

| Aspen Managed Futures Strategy Fund | Performance Update |

October 31, 2018 (Unaudited)

Performance of $10,000 Initial Investment (as of October 31, 2018)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested.

6

| Aspen Portfolio Strategy Fund | Performance Update |

October 31, 2018 (Unaudited)

Annualized Total Return Performance as of October 31, 2018

| Since | Expense Ratios | |||

| Aspen Portfolio Strategy Fund | 1 Year | Inception* | Gross | Net(1) |

| Aspen Portfolio Strategy Fund - Class A (NAV)(2) | -2.14% | 1.90% | 2.03% | 1.97% |

| Aspen Portfolio Strategy Fund - Class A (MOP)(3) | -7.53% | -1.19% | 2.03% | 1.97% |

Aspen Portfolio Strategy Fund - Class I | -1.95% | 2.20% | 1.70% | 1.57% |

| S&P 500® Index(4) | 7.35% | 12.83% | ||

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please call 1-855-845-9444.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Subject to investment risks, including possible loss of the principal amount invested.

Returns for periods less than 1 year are cumulative.

| * | Fund Inception date of December 28, 2016. |

| (1) | Aspen Partners, Ltd. (the “Adviser”) has agreed to waive and/or reimburse fees or expenses in order to limit total annual Fund operating expenses after fee waiver/expense reimbursements (excluding distribution and service (12b-1) fees, shareholder services fees, acquired fund fees and expenses, brokerage expenses, interest expenses, taxes and extraordinary expenses) to 1.55% of the Funds’ average daily net assets. This agreement (the “Expense Agreement”) is in effect through August 31, 2019. The Adviser will be permitted to recover, on a class-by-class basis, expenses it has borne through the Expense Agreement to the extent that the Funds’ expenses in later periods fall below the expense cap in effect at the time of waiver or reimbursement. Notwithstanding the foregoing, the Fund will not be obligated to pay any such deferred fees and expenses more than three years after the date of the waiver or reimbursement. The Expense Agreement may not be terminated or modified prior to August 31, 2019 except with the approval of the Funds’ Board of Trustees |

| (2) | Net Asset Value (NAV) is the share price without sales charges. |

| (3) | Maximum Offering Price (MOP) includes sales charges. Class A returns include effects of the Funds’ maximum sales charge of 5.50%. |

| (4) | The S&P 500® Index is an unmanaged index of 500 common stocks chosen for market size, liquidity and industry group representation. It is a market-value weighted index. The Index is not actively managed and does not reflect any deductions for fees, expenses or taxes. An investor may not invest directly in the Index. |

Portfolio Composition as of October 31, 2018

As a percentage of Net Assets^

| ^ | Holdings subject to change, and may not reflect the current or future position of the portfolio. |

| Semi-Annual Report | October 31, 2018 | 7 |

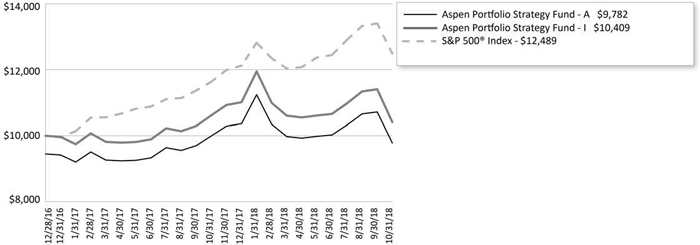

| Aspen Portfolio Strategy Fund | Performance Update |

October 31, 2018 (Unaudited)

Performance of $10, 000 Initial Investment (as of October 31, 2018)

Comparison of change in value of a $10,000 investment (includes applicable sales loads)

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Investing in the Fund is subject to investment risks, including possible loss of the principal amount invested.

8

| Aspen Funds | Consolidated Disclosure of Fund Expenses |

October 31, 2018 (Unaudited)

As a shareholder of the Fund, you incur two types of costs: transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; shareholder servicing fees; and other fund operating expenses. This example is intended to help you understand your ongoing costs (in dollars), of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period of May 1, 2018 through October 31, 2018.

Actual Expenses The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as applicable sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value 5/1/18 | Ending Account Value 10/31/18 | Expense Ratio(a) | Expenses Paid During period 5/1/18 - 10/31/18(b) | |

| Aspen Managed Futures Strategy Fund | ||||

| Class A | ||||

| Actual | $1,000.00 | $987.30 | 1.76% | $8.82 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,016.33 | 1.76% | $8.94 |

| Class I | ||||

| Actual | $1,000.00 | $987.50 | 1.55% | $7.76 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,017.39 | 1.55% | $7.88 |

| Aspen Portfolio Strategy Fund | ||||

| Class A | ||||

| Actual | $1,000.00 | $985.30 | 1.81% | $9.06 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,016.08 | 1.81% | $9.20 |

| Class I | ||||

| Actual | $1,000.00 | $986.50 | 1.55% | $7.76 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,017.39 | 1.55% | $7.88 |

| (a) | The Fund's expense ratios have been based on the Fund's most recent fiscal half-year expenses. |

| (b) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184)/365 (to reflect the half-year period). |

| Semi-Annual Report | October 31, 2018 | 9 |

| Aspen Managed Futures Strategy Fund | Consolidated Schedule of Investments |

October 31, 2018 (Unaudited)

Principal Amount/Shares | Value (Note 2) | |||||||

| SHORT TERM INVESTMENTS (86.70%) | ||||||||

| MONEY MARKET FUND (2.90%) | ||||||||

| Dreyfus Treasury & Agency Cash Management Fund - Institutional Shares, 7-day yield, 2.071% | 1,643,374 | $ | 1,643,374 | |||||

| U.S. TREASURY BILLS (83.80%) | ||||||||

| 1.752%, 11/08/2018(a) | $ | 6,550,000 | 6,547,330 | |||||

| 1.819%, 12/06/2018(a) | 9,150,000 | 9,131,019 | ||||||

| 2.074%, 01/31/2019(a) | 5,500,000 | 5,468,232 | ||||||

| 2.087%, 02/28/2019(a) | 5,000,000 | 4,961,986 | ||||||

| 2.118%, 03/28/2019(a) | 8,200,000 | 8,121,147 | ||||||

| 2.259%, 04/25/2019(a) | 10,000,000 | 9,882,969 | ||||||

| 2.325%, 06/20/2019(a) | 3,400,000 | 3,346,167 | ||||||

| 47,458,850 | ||||||||

| TOTAL SHORT TERM INVESTMENTS | ||||||||

| (Cost $49,128,628) | 49,102,224 | |||||||

| TOTAL INVESTMENTS (86.70%) | ||||||||

| (Cost $49,128,628) | $ | 49,102,224 | ||||||

| Other Assets In Excess Of Liabilities (13.30%) | 7,529,803 | (b) | ||||||

| NET ASSETS (100.00%) | $ | 56,632,027 | ||||||

| (a) | Rate shown represents the bond equivalent yield to maturity at date of purchase. |

| (b) | Includes cash which is being held as collateral for futures contracts. |

10

| Aspen Managed Futures Strategy Fund | Consolidated Schedule of Investments |

October 31, 2018 (Unaudited)

FUTURES CONTRACTS

At October 31, 2018, the Fund had the following outstanding futures contracts:

| Description | Counterparty | Position | Contracts | Expiration Date | Notional Value | Value and Unrealized Appreciation | |||||||||

| Commodity Contracts | |||||||||||||||

| Copper Future(a) | R.J. O'Brien & Associates LLC | Short | 30 | 12/27/2018 | $ | (1,994,250 | ) | $ | 87,940 | ||||||

| Silver Future(a) | R.J. O'Brien & Associates LLC | Short | 42 | 12/27/2018 | (2,999,220 | ) | 25,039 | ||||||||

| Soybean Future(a) | R.J. O'Brien & Associates LLC | Short | 72 | 01/14/2019 | (3,066,300 | ) | 28,521 | ||||||||

| WTI Crude Future(a) | R.J. O'Brien & Associates LLC | Short | 15 | 11/19/2018 | (979,650 | ) | 22,601 | ||||||||

| Equity Contracts | |||||||||||||||

| Euro Stoxx 50 Index Future | R.J. O'Brien & Associates LLC | Short | 150 | 12/21/2018 | (5,426,528 | ) | 120,358 | ||||||||

| Foreign Currency Contracts | |||||||||||||||

| Australian Dollar Currency Future | R.J. O'Brien & Associates LLC | Short | 173 | 12/17/2018 | (12,243,210 | ) | 58,690 | ||||||||

| Canadian Dollar Currency Future | R.J. O'Brien & Associates LLC | Short | 100 | 12/18/2018 | (7,599,500 | ) | 88,665 | ||||||||

| Euro FX Currency Future | R.J. O'Brien & Associates LLC | Short | 90 | 12/17/2018 | (12,774,938 | ) | 203,662 | ||||||||

| Japanese Yen Currency Future | R.J. O'Brien & Associates LLC | Short | 37 | 12/17/2018 | (4,104,919 | ) | 23,926 | ||||||||

| Swiss Franc Currency Future | R.J. O'Brien & Associates LLC | Short | 5 | 12/17/2018 | (622,375 | ) | 7,958 | ||||||||

| Interest Rate Contracts | |||||||||||||||

| 10 Year U.S. Treasury Note Future | R.J. O'Brien & Associates LLC | Short | 110 | 12/19/2018 | (13,028,125 | ) | 13,881 | ||||||||

| Canadian 10 Year Bond Future | R.J. O'Brien & Associates LLC | Short | 86 | 12/18/2018 | (8,632,990 | ) | 3,417 | ||||||||

| Euro-Bond Future | R.J. O'Brien & Associates LLC | Long | 24 | 12/10/2008 | 4,356,445 | 217 | |||||||||

| $ | (69,115,560 | ) | $ | 684,875 | |||||||||||

| Description | Counter party | Position | Contracts | Expiration Date | Notional Value | Value and Unrealized Depreciation | |||||||||

| Commodity Contracts | |||||||||||||||

| Corn Future(a) | R.J. O'Brien & Associates LLC | Long | 110 | 12/14/2018 | $ | 1,997,875 | $ | (59,107 | ) | ||||||

| FTSE 100 Index Future | R.J. O'Brien & Associates LLC | Short | 40 | 12/21/2018 | (3,635,715 | ) | (43,077 | ) | |||||||

| Gold 100 Oz Future(a) | R.J. O'Brien & Associates LLC | Short | 9 | 12/26/2018 | (1,093,500 | ) | (17,309 | ) | |||||||

| Long Gilt Future | R.J. O'Brien & Associates LLC | Short | 28 | 12/27/2008 | (4,381,009 | ) | (48,029 | ) | |||||||

| NY Harbor ULSD Future(a) | R.J. O'Brien & Associates LLC | Long | 21 | 11/30/2018 | 1,985,735 | (1,391 | ) | ||||||||

| Sugar No. 11 (World) Future(a) | R.J. O'Brien & Associates LLC | Long | 135 | 02/28/2019 | 1,994,328 | (103,806 | ) | ||||||||

| Equity Contracts | |||||||||||||||

| Nikkei 225 Index Future | R.J. O'Brien & Associates LLC | Short | 33 | 12/13/2018 | (3,596,175 | ) | (32,579 | ) | |||||||

| S&P 500 E-Mini Future | R.J. O'Brien & Associates LLC | Short | 14 | 12/21/2018 | (1,897,770 | ) | (3,124 | ) | |||||||

| $ | (8,626,231 | ) | $ | (308,422 | ) | ||||||||||

Common Abbreviations:

FTSE - Financial Times and the London Stock Exchange

S&P - Standard and Poor's

ULSD - Ultra Low Sulfur Diesel

| (a) | Owned by an entity that is owned by the Fund and is consolidated as described in Note 1 of the Notes to the Consolidated Financial Statements. |

For Fund compliance purposes, the Fund's industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percentage of net assets.

| Semi-Annual Report | October 31, 2018 | 11 |

| Aspen Portfolio Strategy Fund | Consolidated Schedule of Investments |

October 31, 2018 (Unaudited)

| Shares | Value (Note 2) | |||||||

| EXCHANGE TRADED FUNDS (75.88%) | ||||||||

| SPDR® S&P 500® ETF Trust | 138,319 | $ | 37,433,303 | |||||

| iShares® Core S&P 500® ETF | 37,179 | 10,140,944 | ||||||

| TOTAL EXCHANGE TRADED FUNDS | ||||||||

| (Cost $42,836,476) | 47,574,247 | |||||||

| SHORT TERM INVESTMENTS (15.99%) | ||||||||

| MONEY MARKET FUND (15.99%) | ||||||||

| Dreyfus Treasury & Agency Cash Management Fund - Institutional Shares, 7-day yield, 2.071% | 10,026,338 | 10,026,338 | ||||||

| TOTAL SHORT TERM INVESTMENTS | ||||||||

| (Cost $10,026,338) | 10,026,338 | |||||||

| TOTAL INVESTMENTS (91.87%) | ||||||||

| (Cost $52,862,814) | $ | 57,600,585 | ||||||

| Other Assets In Excess Of Liabilities (8.13%) | 5,099,219 | (a) | ||||||

| NET ASSETS (100.00%) | $ | 62,699,804 | ||||||

| (a) | Includes cash which is being held as collateral for futures contracts. |

12

| Aspen Portfolio Strategy Fund | Consolidated Schedule of Investments |

October 31, 2018 (Unaudited)

FUTURES CONTRACTS

At October 31, 2018, the Fund had the following outstanding futures contracts:

| Description | Counterparty | Position | Contracts | Expiration Date | Notional Value | Value and Unrealized Appreciation | |||||||||

| Commodity Contracts | |||||||||||||||

| Copper Future(a) | R.J. O'Brien & Associates LLC | Short | 35 | 12/27/2018 | $ | (2,326,625 | ) | $ | 114,536 | ||||||

| Silver Future(a) | R.J. O'Brien & Associates LLC | Short | 48 | 12/27/2018 | (3,427,680 | ) | 34,689 | ||||||||

| Soybean Future(a) | R.J. O'Brien & Associates LLC | Short | 81 | 01/14/2019 | (3,449,587 | ) | 35,513 | ||||||||

| WTI Crude Future(a) | R.J. O'Brien & Associates LLC | Short | 18 | 11/19/2018 | (1,175,580 | ) | 31,901 | ||||||||

| Equity Contracts | |||||||||||||||

| Euro Stoxx 50 Index Future | R.J. O'Brien & Associates LLC | Short | 172 | 12/21/2018 | (6,222,419 | ) | 187,890 | ||||||||

| Nikkei 225 Index Future | R.J. O'Brien & Associates LLC | Short | 38 | 12/13/2018 | (4,141,050 | ) | 31,102 | ||||||||

| Foreign Currency Contracts | |||||||||||||||

| Australian Dollar Currency Future | R.J. O'Brien & Associates LLC | Short | 197 | 12/17/2018 | (13,941,690 | ) | 68,780 | ||||||||

| Canadian Dollar Currency Future | R.J. O'Brien & Associates LLC | Short | 122 | 12/18/2018 | (9,271,390 | ) | 56,426 | ||||||||

| Euro FX Currency Future | R.J. O'Brien & Associates LLC | Short | 98 | 12/17/2018 | (13,910,488 | ) | 224,534 | ||||||||

| Japanese Yen Currency Future | R.J. O'Brien & Associates LLC | Short | 42 | 12/17/2018 | (4,659,638 | ) | 20,609 | ||||||||

| Interest Rate Contracts | |||||||||||||||

| 10 Year U.S. Treasury Note Future | R.J. O'Brien & Associates LLC | Short | 125 | 12/19/2018 | (14,804,688 | ) | 76,266 | ||||||||

| Canadian 10 Year Bond Future | R.J. O'Brien & Associates LLC | Short | 98 | 12/18/2018 | (9,837,593 | ) | 32,391 | ||||||||

| $ | (87,168,428 | ) | $ | 914,637 | |||||||||||

| Description | Counter party | Position | Contracts | Expiration Date | Notional Value | Value and Unrealized Depreciation | |||||||||

| Commodity Contracts | |||||||||||||||

| Corn Future(a) | R.J. O'Brien & Associates LLC | Long | 126 | 12/14/2018 | $ | 2,288,475 | $ | (73,741 | ) | ||||||

| FTSE 100 Index Future | R.J. O'Brien & Associates LLC | Short | 45 | 12/21/2018 | (4,090,180 | ) | (16,113 | ) | |||||||

| Gold 100 Oz Future(a) | R.J. O'Brien & Associates LLC | Short | 9 | 12/26/2018 | (1,093,500 | ) | (16,899 | ) | |||||||

| Long Gilt Future | R.J. O'Brien & Associates LLC | Short | 32 | 12/27/2008 | (5,006,867 | ) | (62,777 | ) | |||||||

| NY Harbor ULSD Future(a) | R.J. O'Brien & Associates LLC | Long | 24 | 11/30/2018 | 2,269,411 | (6,533 | ) | ||||||||

| Sugar No. 11 (World) Future(a) | R.J. O'Brien & Associates LLC | Long | 154 | 02/28/2019 | 2,275,011 | (113,254 | ) | ||||||||

| Equity Contracts | |||||||||||||||

| S&P 500 E-Mini Future | R.J. O'Brien & Associates LLC | Long | 94 | 12/21/2018 | 12,742,170 | (751,475 | ) | ||||||||

| Interest Rate Contracts | |||||||||||||||

| Euro-Bond Future | R.J. O'Brien & Associates LLC | Long | 27 | 12/10/2008 | 4,901,001 | (220 | ) | ||||||||

| $ | 14,285,521 | $ | (1,041,012 | ) | |||||||||||

Common Abbreviations:

FTSE - Financial Times and the London Stock Exchange

S&P - Standard and Poor's

ULSD - Ultra Low Sulfur Diesel

| (a) | Owned by an entity that is owned by the Fund and is consolidated as described in Note 1 of the Notes to the Consolidated Financial Statements. |

For Fund compliance purposes, the Fund's industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications for reporting ease. Industries are shown as a percentage of net assets.

| Semi-Annual Report | October 31, 2018 | 13 |

| Aspen Funds | Consolidated Statements of Assets & Liabilities |

October 31, 2018 (Unaudited)

Aspen Managed Futures Strategy Fund | Aspen Portfolio Strategy Fund | |||||||

| ASSETS: | ||||||||

| Investments, at value | $ | 49,102,224 | $ | 57,600,585 | ||||

| Foreign cash due from broker for futures contracts(Cost $167,149 and $123,804) (Note 3) | 167,149 | 123,597 | ||||||

| Deposit with broker for futures contracts (Note 3) | 7,354,839 | 4,329,133 | ||||||

| Receivable for investments sold | 383,808 | 190,956 | ||||||

| Receivable for shares sold | 11,726 | 1,105 | ||||||

| Variation margin receivable | 271,913 | 643,217 | ||||||

| Interest receivable | 10,024 | 14,928 | ||||||

| Prepaid and other assets | 23,439 | 5,207 | ||||||

| Total assets | 57,325,122 | 62,908,728 | ||||||

| LIABILITIES: | ||||||||

| Foreign cash due to broker for futures contracts (Note 3) | 165,563 | 24,872 | ||||||

| Payable to advisor | 39,035 | 52,708 | ||||||

| Payable for investments purchased | 312 | 66 | ||||||

| Variation margin payable | 19,173 | 41,253 | ||||||

| Payable for shares redeemed | 383,467 | 37,115 | ||||||

| Payable for administration fees | 16,955 | 19,140 | ||||||

| Payable for distribution and service fees | ||||||||

| Class A | 2,099 | 2,192 | ||||||

| Payable for transfer agency fees | 8,683 | 6,829 | ||||||

| Delegated transfer agent equivalent services fees | ||||||||

| Class A | 56 | – | ||||||

| Class I | 12,863 | 2,976 | ||||||

| Payable for trustee fees and expenses | 6,886 | 6,476 | ||||||

| Payable for professional fees | 14,893 | 9,702 | ||||||

| Payable for chief compliance officer fees | 5,258 | 2,611 | ||||||

| Payable for principal financial officer fees | 569 | 283 | ||||||

| Payable for licensing fees | 13,012 | – | ||||||

| Accrued expenses and other liabilities | 4,271 | 2,701 | ||||||

| Total liabilities | 693,095 | 208,924 | ||||||

| NET ASSETS | $ | 56,632,027 | $ | 62,699,804 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid-in capital (Note 5) | $ | 85,560,287 | $ | 61,074,376 | ||||

| Total distributable earnings | $ | (28,928,260 | ) | $ | 1,625,428 | |||

| NET ASSETS | $ | 56,632,027 | $ | 62,699,804 | ||||

| INVESTMENTS, AT COST | $ | 49,128,628 | $ | 52,862,814 | ||||

| PRICING OF SHARES: | ||||||||

| Class A: | ||||||||

| Net Asset Value, offering and redemption price per share | $ | 7.75 | $ | 25.43 | ||||

| Net Assets | $ | 1,718,057 | $ | 2,844,777 | ||||

| Shares of beneficial interest outstanding | 221,728 | 111,863 | ||||||

| Maximum offering price per share (NAV/0.9450), based on maximum sales charge of 5.50% of the offering price | $ | 8.20 | $ | 26.91 | ||||

| Class I: | ||||||||

| Net Asset Value, offering and redemption price per share | $ | 7.89 | $ | 25.52 | ||||

| Net Assets | $ | 54,913,970 | $ | 59,855,027 | ||||

| Shares of beneficial interest outstanding | 6,956,942 | 2,345,659 | ||||||

See Notes to Consolidated Financial Statements.

| 14 |

| Aspen Funds | Consolidated Statements of Operations |

For the Six Months Ended October 31, 2018 (Unaudited)

Aspen Managed Futures Strategy Fund | Aspen Portfolio Strategy Fund | |||||||

| INVESTMENT INCOME: | ||||||||

| Interest | $ | 575,195 | $ | – | ||||

| Dividends | 61,232 | 516,906 | ||||||

| Total investment income | 636,427 | 516,906 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees (Note 6) | 282,932 | 292,590 | ||||||

| Investment advisory fees - subsidiary (Note 6) | 58,772 | 7,320 | ||||||

| Administrative fees | 103,180 | 85,579 | ||||||

| Distribution and service fees | ||||||||

| Class A | 6,173 | 6,083 | ||||||

| Transfer agency fees | 26,095 | 26,078 | ||||||

| Delegated transfer agent equivalent services fees | ||||||||

| Class A | 73 | – | ||||||

| Class I | 32,528 | 14,266 | ||||||

| Professional fees | 14,543 | 16,702 | ||||||

| Custodian fees | 5,612 | 5,037 | ||||||

| Trustee fees and expenses | 7,397 | 6,918 | ||||||

| Principal financial officer fees | 1,543 | 975 | ||||||

| Chief compliance officer fees | 14,272 | 9,014 | ||||||

| Licensing fees | 94,311 | – | ||||||

| Other | 22,791 | 23,637 | ||||||

| Total expenses before waiver/reimbursement | 670,222 | 494,199 | ||||||

| Waiver of investment advisory fees (Note 6) | (23,658 | ) | (29,308 | ) | ||||

| Waiver of investment advisory fees - subsidiary (Note 6) | (58,772 | ) | (7,320 | ) | ||||

| Total net expenses | 587,792 | 457,571 | ||||||

| NET INVESTMENT INCOME | 48,635 | 59,335 | ||||||

| Net realized gain/(loss) on investments | (4,560 | ) | 166,160 | |||||

| Net realized loss on futures contracts | (1,806,276 | ) | (2,321,720 | ) | ||||

| Net realized gain/(loss) on foreign currency transactions | 25,588 | (21,290 | ) | |||||

| Total net realized loss | (1,785,248 | ) | (2,176,850 | ) | ||||

| Net change in unrealized appreciation of investments | 57,115 | 435,236 | ||||||

| Net change in unrealized appreciation on futures contracts | 655,677 | 506,147 | ||||||

| Net change in unrealized appreciation/(depreciation) on translation of assets and liabilities denominated in foreign currency transactions | (11,369 | ) | 1,628 | |||||

| Net change in unrealized appreciation | 701,423 | 943,011 | ||||||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (1,083,825 | ) | (1,233,839 | ) | ||||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (1,035,190 | ) | $ | (1,174,504 | ) | ||

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2018 | 15 |

| Aspen Managed Futures Strategy Fund | Consolidated Statement of Changes in Net Assets |

For the Six Months Ended October 31, 2018 (Unaudited) | For the Year Ended April 30, 2018 | |||||||

| OPERATIONS: | ||||||||

| Net investment income/(loss) | $ | 48,635 | $ | (659,959 | ) | |||

| Net realized loss | (1,785,248 | ) | (5,221,890 | ) | ||||

| Net change in unrealized appreciation | 701,423 | 2,248,600 | ||||||

| Net decrease in net assets resulting from operations | (1,035,190 | ) | (3,633,249 | ) | ||||

| SHARE TRANSACTIONS (Note 5): | ||||||||

| Class A | ||||||||

| Proceeds from sales of shares | 214,997 | 1,957,143 | ||||||

| Cost of shares redeemed | (1,907,107 | ) | (4,685,659 | ) | ||||

| Redemption fees | 2,248 | 40 | ||||||

| Class I | ||||||||

| Proceeds from sales of shares | 3,079,264 | 36,658,111 | ||||||

| Cost of shares redeemed | (32,509,667 | ) | (142,925,441 | ) | ||||

| Redemption fees | 522 | 7,858 | ||||||

| Net decrease from share transactions | (31,119,743 | ) | (108,987,948 | ) | ||||

| Net decrease in net assets | (32,154,933 | ) | (112,621,197 | ) | ||||

| NET ASSETS: | ||||||||

| Beginning of period | 88,786,960 | 201,408,157 | ||||||

| End of period | $ | 56,632,027 | $ | 88,786,960 | (a) | |||

| Other Information: | ||||||||

| SHARE TRANSACTIONS: | ||||||||

| Class A | ||||||||

| Sold | 27,677 | 244,494 | ||||||

| Redeemed | (245,576 | ) | (584,494 | ) | ||||

| Net decrease in shares outstanding | (217,899 | ) | (340,000 | ) | ||||

| Class I | ||||||||

| Sold | 386,423 | 4,482,058 | ||||||

| Redeemed | (4,105,867 | ) | (17,442,220 | ) | ||||

| Net decrease in shares outstanding | (3,719,444 | ) | (12,960,162 | ) | ||||

| (a) | For the year ended April 30, 2018, included Accumulated Net Investment loss of $367,562. |

See Notes to Consolidated Financial Statements.

| 16 |

| Aspen Portfolio Strategy Fund | Consolidated Statement of Changes in Net Assets |

For the Six Months Ended October 31, 2018 (Unaudited) | For the Year Ended April 30, 2018 | |||||||

| OPERATIONS: | ||||||||

| Net investment income | $ | 59,335 | $ | 60,396 | ||||

| Net realized gain/(loss) | (2,176,850 | ) | 10,886 | |||||

| Net change in unrealized appreciation | 943,011 | 3,022,499 | ||||||

| Net increase/(decrease) in net assets resulting from operations | (1,174,504 | ) | 3,093,781 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS (Note 4): | ||||||||

| From distributable earnings | ||||||||

| Class I | – | (44,849 | ) | |||||

| Class A | – | (881,756 | ) | |||||

| Net decrease in net assets from distributions | – | (926,605 | )(a) | |||||

| SHARE TRANSACTIONS (Note 5): | ||||||||

| Class A | ||||||||

| Proceeds from sales of shares | 514,312 | 717,112 | ||||||

| Distributions reinvested | – | 44,794 | ||||||

| Cost of shares redeemed | (352,971 | ) | (345,910 | ) | ||||

| Class I | ||||||||

| Proceeds from sales of shares | 16,398,904 | 9,638,520 | ||||||

| Distributions reinvested | – | 767,869 | ||||||

| Cost of shares redeemed | (2,948,138 | ) | (6,046,036 | ) | ||||

| Redemption fees | 69 | 284 | ||||||

| Net increase from share transactions | 13,612,176 | 4,776,633 | ||||||

| Net increase in net assets | 12,437,672 | 6,943,809 | ||||||

| NET ASSETS: | ||||||||

| Beginning of period | 50,262,132 | 43,318,323 | ||||||

| End of period | $ | 62,699,804 | $ | 50,262,132 | (b) | |||

| Other Information: | ||||||||

| SHARE TRANSACTIONS: | ||||||||

| Class A | ||||||||

| Sold | 19,267 | 27,302 | ||||||

| Distributions reinvested | – | 1,679 | ||||||

| Redeemed | (13,151 | ) | (13,079 | ) | ||||

| Net increase in shares outstanding | 6,116 | 15,902 | ||||||

| Class I | ||||||||

| Sold | 617,525 | 361,712 | ||||||

| Distributions reinvested | – | 28,731 | ||||||

| Redeemed | (109,457 | ) | (232,745 | ) | ||||

| Net increase in shares outstanding | 508,068 | 157,698 | ||||||

| (a) | For the year ended April 30, 2018, Total Distributions consisted of Net Investment Income of $10,269 for Class A and $268,936 for Class I, and Net Realized Gains of $34,580 for Class A and $612,820 for Class I. |

| (b) | For the year ended April 30, 2018, included Accumulated Net Investment loss of $24,568. |

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2018 | 17 |

| Aspen Managed Futures Strategy Fund – Class A | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

For the Six Months Ended October 31, 2018 (Unaudited) (a) | For the Year Ended April 30, 2018 (a) | For the Year Ended April 30, 2017 (a) | For the Year Ended April 30, 2016 (a) | For the Year Ended April 30, 2015 (a) | For the Year Ended April 30, 2014 (a) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 7.85 | $ | 8.12 | $ | 8.83 | $ | 10.01 | $ | 8.97 | $ | 9.29 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

| Net investment loss(b) | (0.00 | ) | (0.06 | ) | (0.04 | ) | (0.12 | ) | (0.14 | ) | (0.16 | ) | ||||||||||||

| Net realized and unrealized gain/(loss) on investments | (0.11 | ) | (0.21 | ) | (0.57 | ) | (0.39 | ) | 1.39 | (0.05 | ) | |||||||||||||

| Total from investment operations | (0.11 | ) | (0.27 | ) | (0.61 | ) | (0.51 | ) | 1.25 | (0.21 | ) | |||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | – | – | (0.10 | ) | (0.14 | ) | – | – | ||||||||||||||||

| Distributions from net realized gain on investments | – | – | – | (0.53 | ) | (0.21 | ) | (0.12 | ) | |||||||||||||||

| Total distributions | – | – | (0.10 | ) | (0.67 | ) | (0.21 | ) | (0.12 | ) | ||||||||||||||

| REDEMPTION FEES ADDED TO PAID IN CAPITAL | 0.01 | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.01 | ||||||||||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.10 | ) | (0.27 | ) | (0.71 | ) | (1.18 | ) | 1.04 | (0.32 | ) | |||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 7.75 | $ | 7.85 | $ | 8.12 | $ | 8.83 | $ | 10.01 | $ | 8.97 | ||||||||||||

| TOTAL RETURN(d) | (1.27 | %)(e) | (3.33 | %) | (6.97 | %) | (5.20 | %) | 14.00 | % | (2.15 | %) | ||||||||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (000's) | $ | 1,718 | $ | 3,452 | $ | 6,331 | $ | 19,682 | $ | 23,850 | $ | 12,914 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.76% | (f)(g) | 1.66 | %(g) | 1.00 | %(g) | 1.56 | %(g) | 1.64 | % | 1.83 | % | ||||||||||||

| Operating expenses including fee waivers/reimbursements | 1.76 | %(f) | 1.66 | % | 1.00 | % | 1.56 | % | 1.64 | % | 1.83 | % | ||||||||||||

| Net investment loss including fee waivers/reimbursements | (0.06 | %)(f) | (0.72 | %) | (0.52 | %) | (1.24 | %) | (1.50 | %) | (1.72 | %) | ||||||||||||

| PORTFOLIO TURNOVER RATE | 0 | %(e) | 0 | % | 31 | % | 58 | % | 38 | % | 90 | % | ||||||||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Futures Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | Per share numbers have been calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Total return does not reflect the effect of sales charges. |

| (e) | Not annualized. |

| (f) | Annualized. |

| (g) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.92%, 1.76%, 1.07% and 1.64% for the period/years ended October 31, 2018, April 30, 2018, April 30, 2017 and April 30, 2016, respectively. |

See Notes to Consolidated Financial Statements.

| 18 |

| Aspen Managed Futures Strategy Fund – Class I | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

| For the Six Months Ended October 31, 2018 (Unaudited) (a) | For the Year Ended April 30, 2018 (a) | For the Year Ended April 30, 2017 (a) | For the Year Ended April 30, 2016 (a) | For the Year Ended April 30, 2015 (a) | For the Year Ended April 30, 2014 (a) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 7.99 | $ | 8.25 | $ | 8.98 | $ | 10.17 | $ | 9.07 | $ | 9.36 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

| Net investment income/(loss)(b) | 0.01 | (0.04 | ) | (0.07 | ) | (0.09 | ) | (0.11 | ) | (0.11 | ) | |||||||||||||

| Net realized and unrealized gain/(loss) on investments | (0.11 | ) | (0.22 | ) | (0.58 | ) | (0.40 | ) | 1.42 | (0.06 | ) | |||||||||||||

| Total from investment operations | (0.10 | ) | (0.26 | ) | (0.65 | ) | (0.49 | ) | 1.31 | (0.17 | ) | |||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | – | – | (0.08 | ) | (0.17 | ) | – | – | ||||||||||||||||

| Distributions from net realized gain on investments | – | – | – | (0.53 | ) | (0.21 | ) | (0.12 | ) | |||||||||||||||

| Total distributions | – | – | (0.08 | ) | (0.70 | ) | (0.21 | ) | (0.12 | ) | ||||||||||||||

| REDEMPTION FEES ADDED TO PAID IN CAPITAL | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | 0.00 | (c) | ||||||||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.10 | ) | (0.26 | ) | (0.73 | ) | (1.19 | ) | 1.10 | (0.29 | ) | |||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 7.89 | $ | 7.99 | $ | 8.25 | $ | 8.98 | $ | 10.17 | $ | 9.07 | ||||||||||||

| TOTAL RETURN | (1.25 | %)(d) | (3.15 | %) | (7.33 | %) | (4.97 | %) | 14.51 | % | (1.81 | %) | ||||||||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (000's) | $ | 54,914 | $ | 85,335 | $ | 195,077 | $ | 264,598 | $ | 242,575 | $ | 167,258 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.62% | (e)(f) | 1.46 | %(f) | 1.28 | %(f) | 1.22 | %(f) | 1.25 | % | 1.30 | % | ||||||||||||

| Operating expenses including fee waivers/reimbursements | 1.55 | %(e) | 1.46 | % | 1.28 | % | 1.22 | % | 1.25 | % | 1.30 | % | ||||||||||||

| Net investment income/(loss) including fee waivers/reimbursements | 0.14 | %(e) | (0.53 | %) | (0.78 | %) | (0.94 | %) | (1.11 | %) | (1.20 | %) | ||||||||||||

| PORTFOLIO TURNOVER RATE | 0 | %(d) | 0 | % | 31 | % | 58 | % | 38 | % | 90 | % | ||||||||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Futures Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | Per share numbers have been calculated using the average shares method. |

| (c) | Less than $0.005 per share. |

| (d) | Not annualized. |

| (e) | Annualized. |

| (f) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.78%, 1.56%, 1.35% and 1.30% for the period/years ended October 31, 2018, April 30, 2018, April 30, 2017 and April 30, 2016, respectively. |

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2018 | 19 |

| Aspen Portfolio Strategy Fund – Class A | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

For the Six Months Ended October 31, 2018 (Unaudited) | For the Year Ended April 30, 2018(a) | For the Period Ended April 30, 2017(a)(b) | ||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 25.81 | $ | 24.45 | $ | 25.00 | ||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||

| Net investment loss(c) | (0.01 | )(d) | (0.02 | )(d) | (0.03 | ) | ||||||

| Net realized and unrealized gain/(loss) on investments | (0.37 | ) | 1.86 | (0.52 | ) | |||||||

| Total from investment operations | (0.38 | ) | 1.84 | (0.55 | ) | |||||||

| LESS DISTRIBUTIONS: | ||||||||||||

| From net investment income | – | (0.11 | ) | – | ||||||||

| Distributions from net realized gain on investments | – | (0.37 | ) | – | ||||||||

| Total distributions | – | (0.47 | ) | – | ||||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.38 | ) | 1.36 | (0.55 | ) | |||||||

| NET ASSET VALUE, END OF PERIOD | $ | 25.43 | $ | 25.81 | $ | 24.45 | ||||||

| TOTAL RETURN(e) | (1.47 | %)(f) | 7.44 | % | (2.20 | %)(f) | ||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||

| Net assets, end of period (000's) | $ | 2,845 | $ | 2,730 | $ | 2,196 | ||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.87 | %(g)(h) | 1.93 | %(h) | 2.79 | %(g)(h) | ||||||

| Operating expenses including fee waivers/reimbursements | 1.81 | %(g) | 1.79 | % | 1.95 | %(g) | ||||||

| Net investment loss including fee waivers/reimbursements | (0.05 | %)(g) | (0.09 | %) | (0.40 | %)(g) | ||||||

| PORTFOLIO TURNOVER RATE | 8 | %(f) | 0 | % | 0 | %(f)(i) | ||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Portfolio Strategy Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | The Aspen Portfolio Strategy Fund is for the period from December 29, 2016 (commencement of operations) to April 30, 2017. |

| (c) | Per share numbers have been calculated using the average shares method. |

| (d) | The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and redemptions of Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund. |

| (e) | Total return does not reflect the effect of sales charges. |

| (f) | Not annualized. |

| (g) | Annualized. |

| (h) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.89%, 1.96% and 2.82% for the periods/year ended October 31, 2018, April 30, 2018 and for the period ended April 30, 2017, respectively. |

| (i) | Less than 0.05%. |

See Notes to Consolidated Financial Statements.

| 20 |

| Aspen Portfolio Strategy Fund – Class I | Consolidated Financial Highlights |

For a share outstanding throughout the periods presented.

For the Six Months Ended October 31, 2018 (Unaudited) | For the Year Ended April 30, 2018(a) | For the Period Ended April 30, 2017(a)(b) | ||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 25.87 | $ | 24.48 | $ | 25.00 | ||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||

| Net investment income(c) | 0.03 | 0.04 | 0.00 | (d)(e) | ||||||||

| Net realized and unrealized gain/(loss) on investments | (0.38 | ) | 1.88 | (0.52 | ) | |||||||

| Total from investment operations | (0.35 | ) | 1.92 | (0.52 | ) | |||||||

| LESS DISTRIBUTIONS: | ||||||||||||

| From net investment income | – | (0.16 | ) | – | ||||||||

| Distributions from net realized gain on investments | – | (0.37 | ) | – | ||||||||

| Total distributions | – | (0.52 | ) | – | ||||||||

| REDEMPTION FEES ADDED TO PAID IN CAPITAL | 0.00 | (d) | 0.00 | (d) | 0.00 | (d) | ||||||

| INCREASE/(DECREASE) IN NET ASSET VALUE | (0.35 | ) | 1.39 | (0.52 | ) | |||||||

| NET ASSET VALUE, END OF PERIOD | $ | 25.52 | $ | 25.87 | $ | 24.48 | ||||||

| TOTAL RETURN | (1.35 | %)(f) | 7.76 | % | (2.08 | %)(f) | ||||||

| RATIOS AND SUPPLEMENTAL DATA: | ||||||||||||

| Net assets, end of period (000's) | $ | 59,855 | $ | 47,532 | $ | 41,122 | ||||||

| RATIOS TO AVERAGE NET ASSETS: | ||||||||||||

| Operating expenses excluding fee waivers/reimbursements | 1.65 | %(g)(h) | 1.75 | %(h) | 2.22 | %(g)(h) | ||||||

| Operating expenses including fee waivers/reimbursements | 1.55 | %(g) | 1.55 | % | 1.55 | %(g) | ||||||

| Net investment income including fee waivers/reimbursements | 0.22 | %(g) | 0.14 | % | 0.01 | %(g) | ||||||

| PORTFOLIO TURNOVER RATE | 8 | %(f) | 0 | % | 0 | %(f)(i) | ||||||

| (a) | Per share amounts and ratios to average net assets include income and expenses of the Aspen Portfolio Strategy Fund Ltd. (subsidiary), exclusive of the subsidiary's management fee. |

| (b) | The Aspen Portfolio Strategy Fund is for the period from December 29, 2016 (commencement of operations) to April 30, 2017. |

| (c) | Per share numbers have been calculated using the average shares method. |

| (d) | Less than $0.005 per share. |

| (e) | The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations for the period due to the timing of sales and redemptions of Fund shares in relation to income earned and/or fluctuating market value of the investments of the Fund. |

| (f) | Not annualized. |

| (g) | Annualized. |

| (h) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 6 for additional detail). The ratio inclusive of that fee would be 1.67%, 1.78% and 2.25% for the periods/year ended October 31, 2018, April 30, 2018 and for the period ended April 30, 2017, respectively. |

| (i) | Less than 0.05%. |

See Notes to Consolidated Financial Statements.

| Semi-Annual Report | October 31, 2018 | 21 |

| Aspen Funds | Notes to Consolidated Financial Statements |

October 31, 2018 (Unaudited)

1. ORGANIZATION

Financial Investors Trust (the “Trust”), a Delaware statutory trust, is an open-end management investment company registered under the Investment Company Act of 1940, as amended (“1940 Act”). As of October 31, 2017, the Trust consists of multiple separate portfolios or series. This semi-annual report describes the Aspen Managed Futures Strategy Fund and the Aspen Portfolio Strategy Fund (individually a “Fund” and collectively, the “Funds”). The Aspen Managed Futures Strategy Fund seeks investment results that replicate as closely as possible, before fees and expenses, the price and yield performance of the Aspen Managed Futures Beta Index (the “MFBI” or “Index”). The Aspen Portfolio Strategy Fund seeks long-term capital appreciation. The Funds offer Class A and Class I shares.

Basis of Consolidation

Aspen Futures Fund, Ltd. (the “Aspen Fund Subsidiary”), a Cayman Islands exempted company, is a wholly owned subsidiary of the Aspen Managed Futures Strategy Fund and Aspen Portfolio Strategy Fund, Ltd. (the “Aspen Portfolio Subsidiary”), a Cayman Islands exempted company, is a wholly owned subsidiary of the Aspen Portfolio Strategy Fund. The investment objective of both the Aspen Fund Subsidiary and the Aspen Portfolio Subsidiary (collectively the “Subsidiaries”) is designed to enhance the ability of the Funds to obtain exposure to equities, financial, currency and commodities markets consistent with the limits of the U.S. federal tax law requirements applicable to registered investment companies. The Subsidiaries are subject to substantially the same investment policies and investment restrictions as the Funds. The Subsidiaries act as an investment vehicle for the Funds in order to effect certain commodity-related investments on behalf of the Funds. Investments in the Subsidiaries are expected to provide the Funds with exposure to the commodity markets within the limitations of Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”), and recent IRS revenue rulings, as discussed below under “Federal Income Taxes”. The Funds are the sole shareholder of the Subsidiaries pursuant to a subscription agreement dated as of August 2, 2011 for the Aspen Fund Subsidiary and December 16, 2016 for the Aspen Portfolio Subsidiary and it is intended that each Fund will remain the sole shareholder and will continue to control the Subsidiaries. Under the Articles of Association of the Subsidiaries, shares issued by the Subsidiaries confers upon a shareholder the right to wholly own and vote at general meetings of the Subsidiaries and certain rights in connection with any winding-up or repayment of capital, as well as the right to participate in the profits or assets of the Subsidiaries. Each Fund may invest up to 25% of their total assets in shares of the Subsidiaries. All investments held by the Subsidiaries are disclosed in the accounts of each Fund. As a wholly owned subsidiary of the Funds, all assets and liabilities, income and expenses of the Subsidiaries are consolidated in the financial statements and financial highlights of the Funds. All investments held by the Subsidiaries are disclosed in the accounts of the Funds. As of October 31, 2018, net assets of the Aspen Managed Futures Strategy Fund were $56,632,027, of which net assets of $15,319,807 or 27.05%, represented the Fund’s ownership of all issued shares and voting rights of the Aspen Fund Subsidiary. As of October 31, 2018, net assets of the Aspen Portfolio Strategy Fund were $62,699,804, of which $944,973 or 2.18%, represented the Fund’s ownership of all issued shares and voting rights of the Aspen Portfolio Subsidiary.

2. SIGNIFICANT ACCOUNTING POLICIES

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates. The Funds are considered an investment company for financial reporting purposes under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board Accounting Standards Codification Topic 946. The following is a summary of significant accounting policies consistently followed by the Funds and Subsidiaries in preparation of the financial statements.

Investment Valuation: The Funds generally value their securities based on market prices determined at the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern Time, on each day the NYSE is open for trading.

For equity securities and mutual funds that are traded on an exchange, the market price is usually the closing sale or official closing price on that exchange. In the case of equity securities not traded on an exchange, or if such closing prices are not otherwise available, the securities are valued at the mean of the most recent bid and ask prices on such day. Redeemable securities issued by open-end registered investment companies are valued at the investment company’s applicable net asset value, with the exception of exchange-traded open-end investment companies, which are priced as equity securities.

The market price for debt obligations is generally the price supplied by an independent third-party pricing service approved by the Board of Trustees (the “Board”), which may use a matrix, formula or other objective method that takes into consideration quotations from dealers, market transactions in comparable investments, market indices and yield curves. If vendors are unable to supply a price, or if the price supplied is deemed to be unreliable, the market price may be determined using quotations received from one or more brokers–dealers that make a market in the security.

22

| Aspen Funds | Notes to Consolidated Financial Statements |

October 31, 2018 (Unaudited)

Futures contracts that are listed or traded on a national securities exchange, commodities exchange, contract market or comparable over-the-counter market, and that are freely transferable, are valued at their closing settlement price on the exchange on which they are primarily traded or based upon the current settlement price for a like instrument acquired on the day on which the instrument is being valued. A settlement price may not be used if the market makes a limit move with respect to a particular commodity.

Forward currency exchange contracts have a fair value determined by the prevailing foreign currency exchange daily rates and current foreign currency exchange forward rates. The foreign currency exchange forward rates are calculated using an automated system that estimates rates on the basis of the current day foreign currency exchange rates and forward foreign currency exchange rates supplied by a pricing service.

Investment securities that are primarily traded on foreign securities exchanges are valued at the preceding closing values of such securities on their respective exchanges, except when an occurrence subsequent to the time a value was so established is likely to have changed such value. In such an event, the fair value of those securities are determined in good faith through consideration of other factors in accordance with procedures established by and under the general supervision of the Board.

When such prices or quotations are not available, or when Aspen Partners, Ltd. (the “Adviser”) believes that they are unreliable, securities may be priced using fair value procedures approved by the Board.

Fair Value Measurements: The Funds disclose the classification of their fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of each of the Funds’ investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in their entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

| Level 1 – | Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Funds have the ability to access at the measurement date; |

| Level 2– | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

| Level 3 – | Significant unobservable prices or inputs (including the Funds’ own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

| Semi-Annual Report | October 31, 2018 | 23 |

| Aspen Funds | Notes to Consolidated Financial Statements |

October 31, 2018 (Unaudited)

The following is a summary of each input used to value the Funds as of October 31, 2018:

Aspen Managed Futures Strategy Fund

| Investments in Securities at Value | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Short Term Investments Money Market Fund | $ | 1,643,374 | $ | – | $ | – | $ | 1,643,374 | ||||||||

| U.S. Treasury Bills | – | 47,458,850 | – | 47,458,850 | ||||||||||||

| TOTAL | $ | 1,643,374 | $ | 47,458,850 | $ | – | $ | 49,102,224 | ||||||||

| Other Financial Instruments Assets: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Commodity Contracts | $ | 164,101 | $ | – | $ | – | $ | 164,101 | ||||||||

| Equity Contracts | 120,358 | – | – | 120,358 | ||||||||||||

| Foreign Currency Contracts | 382,901 | – | – | 382,901 | ||||||||||||

| Interest Rate Contracts | 17,515 | – | – | 17,515 | ||||||||||||

| Liabilities: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Commodity Contracts | (272,719 | ) | – | – | (272,719 | ) | ||||||||||

| Equity Contracts | (35,703 | ) | – | – | (35,703 | ) | ||||||||||

| TOTAL | $ | 376,453 | $ | – | $ | – | $ | 376,453 | ||||||||

Aspen Portfolio Strategy Fund

| Investments in Securities at Value | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Exchange Traded Funds | $ | 47,574,247 | $ | – | $ | – | $ | 47,574,247 | ||||||||

| Short Term Investments | 10,026,338 | – | – | 10,026,338 | ||||||||||||

| TOTAL | $ | 57,600,585 | $ | – | $ | – | $ | 57,600,585 | ||||||||

| Other Financial Instruments | �� | |||||||||||||||

| Assets: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Commodity Contracts | $ | 216,639 | $ | – | $ | – | $ | 216,639 | ||||||||

| Equity Contracts | 218,992 | – | – | 218,992 | ||||||||||||

| Foreign Currency Contracts | 370,349 | – | – | 370,349 | ||||||||||||

| Interest Rate Contracts | 108,657 | – | – | 108,657 | ||||||||||||

| Liabilities: | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Commodity Contracts | (289,317 | ) | – | – | (289,317 | ) | ||||||||||