UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08194

FINANCIAL INVESTORS TRUST

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1000, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

Brendan Hamill, Esq., Secretary

Financial Investors Trust

1290 Broadway, Suite 1000

Denver, Colorado 80203

(Name and address of agent for service)

Registrant’s telephone number, including area code: 303-623-2577

Date of fiscal year end: October 31

Date of reporting period: November 1, 2020 - October 31, 2021

Item 1. Reports to Stockholders.

| (a) | Report to Stockholders |

Table of Contents

| Disclosure of Fund Expenses | 1 |

| ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund | |

| Management Commentary | 7 |

| Performance Update | 9 |

| Consolidated Statement of Investments | 11 |

| Consolidated Statement of Assets and Liabilities | 17 |

| Consolidated Statement of Operations | 18 |

| Consolidated Statements of Changes in Net Assets | 19 |

| Consolidated Financial Highlights | 20 |

| ALPS | Kotak India Growth Fund | |

| Management Commentary | 24 |

| Performance Update | 27 |

| Statement of Investments | 29 |

| Statement of Assets and Liabilities | 32 |

| Statement of Operations | 33 |

| Statements of Changes in Net Assets | 34 |

| Financial Highlights | 35 |

| ALPS | Smith Funds | |

| Management Commentary | 40 |

| Performance Update | 45 |

| Statements of Investments | 53 |

| Statements of Assets and Liabilities | 103 |

| Statements of Operations | 105 |

| Statement of Changes in Net Assets | 106 |

| Financial Highlights | 110 |

| ALPS | Red Rocks Global Opportunity Fund | |

| Management Commentary | 126 |

| Performance Update | 128 |

| Statement of Investments | 131 |

| Statement of Assets and Liabilities | 133 |

| Statement of Operations | 134 |

| Statements of Changes in Net Assets | 135 |

| Financial Highlights | 136 |

| Clough China Fund | |

| Management Commentary | 141 |

| Performance Update | 143 |

| Statement of Investments | 145 |

| Statement of Assets and Liabilities | 148 |

| Statement of Operations | 149 |

| Statements of Changes in Net Assets | 150 |

| Financial Highlights | 151 |

| RiverFront Global Allocation Series | |

| Management Commentary | 155 |

| Performance Update | 157 |

| Statements of Investments | 163 |

| Statements of Assets and Liabilities | 166 |

| Statements of Operations | 168 |

| Statements of Changes in Net Assets | 169 |

| Financial Highlights | 172 |

| Notes to Financial Statements | 186 |

| Report of Independent Registered Public Accounting Firm | 217 |

| Additional Information | 219 |

| Trustees and Officers | 232 |

| Privacy Policy | 236 |

As permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds' annual and semiannual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on the Funds' website (www.alpsfunds.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary.

alpsfunds.com

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

Board Examples. As a shareholder of the Funds, you incur two types of costs: (1) transaction costs, including applicable sales charges (loads) and redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees, shareholder service fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on May 1, 2021 and held until October 31, 2021.

Actual Expenses. The first line under each class in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period May 1, 2021 – October 31, 2021” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line under each class in the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other mutual funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges or redemption fees. Therefore, the second line under each class in the table below is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

| | Beginning Account Value

May 1, 2021 | Ending Account Value

October 31, 2021 | Expense

Ratio(a) | Expenses Paid

During Period

May 1, 2021 -

October 31, 2021(b) |

| ALPS | CoreCommodity Management CompleteCommodities® Strategy Fund(c) | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,137.70 | 1.35% | $ 7.27 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.40 | 1.35% | $ 6.87 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,140.10 | 1.29% | $ 6.96 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.70 | 1.29% | $ 6.56 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,136.00 | 2.00% | $ 10.77 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.12 | 2.00% | $ 10.16 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,139.80 | 1.09% | $ 5.88 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.71 | 1.09% | $ 5.55 |

| ALPS | Kotak India Growth Fund | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,183.50 | -1.22% | $ -6.71 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,031.36 | -1.22% | $ -6.25 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,185.20 | -1.02% | $ -5.62 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,030.35 | -1.02% | $ -5.22 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,179.90 | -1.88% | $ -10.33 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,034.68 | -1.88% | $ -9.64 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,185.70 | -1.67% | $ -9.20 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,033.62 | -1.67% | $ -8.56 |

| Class II | | | | |

| Actual | $ 1,000.00 | $ 1,187.40 | -0.48% | $ -2.65 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,027.63 | -0.48% | $ -2.45 |

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

| | Beginning Account Value

May 1, 2021 | Ending Account Value

October 31, 2021 | Expense

Ratio(a) | Expenses Paid

During Period

May 1, 2021 -

October 31, 2021(b) |

| ALPS | Smith Short Duration Bond Fund | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 999.70 | 0.75% | $ 3.78 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,021.42 | 0.75% | $ 3.82 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 999.70 | 0.75% | $ 3.78 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,021.42 | 0.75% | $ 3.82 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 995.40 | 1.49% | $ 7.49 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.69 | 1.49% | $ 7.58 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,001.00 | 0.49% | $ 2.47 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.74 | 0.49% | $ 2.50 |

| ALPS | Smith Total Return Bond Fund | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,010.20 | 0.94% | $ 4.76 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.47 | 0.94% | $ 4.79 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,010.30 | 0.93% | $ 4.71 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.52 | 0.93% | $ 4.74 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,006.60 | 1.65% | $ 8.35 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,016.89 | 1.65% | $ 8.39 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,010.70 | 0.65% | $ 3.29 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,021.93 | 0.65% | $ 3.31 |

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

| | Beginning Account Value

May 1, 2021 | Ending Account Value

October 31, 2021 | Expense

Ratio(a) | Expenses Paid

During Period

September 16, 2020 - October 31, 2021(b) |

| ALPS | Smith Credit Opportunities Fund | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,018.20 | 1.18% | $ 6.00 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.26 | 1.18% | $ 6.01 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,018.40 | 1.15% | $ 5.85 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.41 | 1.15% | $ 5.85 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,014.70 | 1.90% | $ 9.65 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.63 | 1.90% | $ 9.65 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,018.70 | 0.90% | $ 4.58 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.67 | 0.90% | $ 4.58 |

| ALPS | Smith Balanced Opportunity Fund | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,038.20 | 1.11% | $ 5.70 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.61 | 1.11% | $ 5.65 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,038.30 | 1.10% | $ 5.65 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.66 | 1.10% | $ 5.60 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,034.50 | 1.85% | $ 9.49 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,015.88 | 1.85% | $ 9.40 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,039.50 | 0.85% | $ 4.37 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,020.92 | 0.85% | $ 4.33 |

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

| | Beginning Account Value

May 1, 2021 | Ending Account Value

October 31, 2021 | Expense

Ratio(a) | Expenses Paid

During Period

May 1, 2021 -

October 31, 2021(b) |

| ALPS | Red Rocks Global Opportunity Fund | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,116.50 | 1.43% | $ 7.63 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.00 | 1.43% | $ 7.27 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,117.10 | 1.41% | $ 7.52 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.10 | 1.41% | $ 7.17 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,112.70 | 2.16% | $ 11.50 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,014.32 | 2.16% | $ 10.97 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,117.40 | 1.16% | $ 6.19 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,019.36 | 1.16% | $ 5.90 |

| Class R | | | | |

| Actual | $ 1,000.00 | $ 1,114.40 | 1.62% | $ 8.63 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.04 | 1.62% | $ 8.24 |

| Clough China Fund | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 864.00 | 1.60% | $ 7.52 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.14 | 1.60% | $ 8.13 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 864.30 | 1.60% | $ 7.52 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,017.14 | 1.60% | $ 8.13 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 860.80 | 2.35% | $ 11.02 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,013.36 | 2.35% | $ 11.93 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 865.20 | 1.35% | $ 6.35 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.40 | 1.35% | $ 6.87 |

| Disclosure of Fund Expenses | |

| | October 31, 2021 (Unaudited) |

| | Beginning Account Value

May 1, 2021 | Ending Account Value

October 31, 2021 | Expense

Ratio(a) | Expenses Paid

During Period

May 1, 2021 -

October 31, 2021(b) |

| RiverFront Asset Allocation Moderate | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,046.70 | 0.50% | $ 2.58 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,046.70 | 0.50% | $ 2.58 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,042.40 | 1.25% | $ 6.43 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,047.90 | 0.25% | $ 1.29 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,023.95 | 0.25% | $ 1.28 |

| RiverFront Asset Allocation Aggressive | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,059.40 | 0.50% | $ 2.60 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,059.20 | 0.50% | $ 2.60 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,055.30 | 1.25% | $ 6.48 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,060.90 | 0.25% | $ 1.30 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,023.95 | 0.25% | $ 1.28 |

| Investor Class II | | | | |

| Actual | $ 1,000.00 | $ 1,059.20 | 0.50% | $ 2.60 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class L | | | | |

| Actual | $ 1,000.00 | $ 1,061.00 | 0.25% | $ 1.30 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,023.95 | 0.25% | $ 1.28 |

| RiverFront Asset Allocation Growth & Income | | | | |

| Investor Class | | | | |

| Actual | $ 1,000.00 | $ 1,047.70 | 0.50% | $ 2.58 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class A | | | | |

| Actual | $ 1,000.00 | $ 1,047.80 | 0.50% | $ 2.58 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,022.68 | 0.50% | $ 2.55 |

| Class C | | | | |

| Actual | $ 1,000.00 | $ 1,043.50 | 1.25% | $ 6.44 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,018.90 | 1.25% | $ 6.36 |

| Class I | | | | |

| Actual | $ 1,000.00 | $ 1,049.20 | 0.25% | $ 1.29 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $ 1,023.95 | 0.25% | $ 1.28 |

| (a) | Annualized, based on the Fund's most recent fiscal half year expenses. |

| (b) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (184), divided by 365. |

| (c) | Includes expenses of the CoreCommodity Management Cayman Commodity Fund Ltd. (wholly-owned subsidiary), exclusive of the subsidiary's management fee. |

| ALPS | CoreCommodity Management | |

| CompleteCommodities® Strategy Fund | |

| Management Commentary | October 31, 2021 (Unaudited) |

The twelve month period ending on October 31, 2021 produced positive returns for commodities as measured by the diversified Bloomberg Commodity Index Total Return (“BCOM”), up +43.94%. The ALPS CoreCommodity Complete Commodities Strategy Fund (“I” Shares – “JCRIX” or the “Fund”) delivered a net positive return of +57.74% (JCRAX was up +57.25%, JCCSX was up +48.75% at MOP and JCRCX was up +55.37% with CDSC).

The Fund outperformed its benchmark, BCOM, by 13.80% during the period. The Fund employs a strategy that combines an actively managed portfolio of commodity futures (collateralized by nominal and inflation-adjusted Treasuries), commodity equities, and physical commodity ETFs. On average, for the past twelve months, the Fund allocated approximately 68% of its assets toward commodity futures-related investments and approximately 32% of its assets toward commodity equities. The Fund was more than 99% invested at the end of the period.

The past one year period ending in October 2021 marked a tremendous rise in commodity prices across the board. The rapid introduction of multiple COVID-19 vaccines beginning in December 2020 became a launching point for economic re-engagement on a global scale. In addition to improvements from a vaccination standpoint, trillions of dollars in stimulus proved successful in promoting greater consumption and mobility. Despite a second wave of the Delta variant, most major economies re-opened to some semblance of normalcy. The asset class benefitted from a “v-shaped” recovery in demand and a seemingly benign recovery in supply. The imbalance has led to massive inventory drawdowns, worsening supply chain bottlenecks, and price spikes throughout the commodity spectrum.

During the timeframe under review, the Fund's largest sector underweight relative to the BCOM was in agriculture at -2.8%. The Fund’s agriculture sector outperformed that of the BCOM by +10%, +47.8% to +37.8%. A higher concentration of certain “luxury” commodities such as coffee (+95.4%), cotton (+66.6%), and sugar (+34.2%) added to the outperformance. Coffee in particular was bolstered by severe weather in top-producer Brazil, in addition to rising freight costs. An underweight to soybean oil (+82.3%) resulted in a slight drag on performance considering the recent supply issues faced by the vegetable oil market and heightened focus on biodiesel. Accounting for the underweight and positive performance among the agriculture producers (+52.5%), the sector contributed +1.8% to total alpha on a gross basis.

As the sector leader, energy prices advanced by a sizeable +83.5% as measured by the BCOM energy sub-index. In fact, the top five performing commodities over the prior year were in the energy sector – gasoil (+135.6%), gasoline (+134.6%), WTI crude oil (+133.5%), heating oil (+130.9%), and Brent crude oil (+125.3%). Fuels of all types benefited from disciplined supply and a rapid return to pre-COVID demand levels. The market was heavily supported by scheduled OPEC+ production cuts and a beleaguered US shale industry. Despite past tendencies to ramp up drilling at all costs, shale producers remained focused on returning capital to

shareholders and shoring up debt-laden balance sheets. The commodity futures in the Fund were further supported by strong performance by the energy equity holdings (+106.1%). Given the Fund’s mix of futures and equities, and a modest overweight to the sector, the Fund’s energy holdings added +6.1% to outperformance on a gross basis for the period.

Industrial metals represented the largest sector overweight within the Fund, boasting a position of 18.9% compared to 15.9% in the BCOM. The tactical overweight proved favorable as industrial metal prices rose nearly +40% over the year as measured by the BCOM industrial metals sub-index. The industry was supported by strong housing numbers, large year-over-year increases to GDP, the transition to low-carbon technologies, and historically low inventory levels. Similar to the oil markets, base metals faced a dramatic decrease in long-cycle capital expenditures following the Global Financial Crisis of 2021. As a consequence, the world is now reeling for materials that are deteriorating in ore quality and are massively underfunded. Fortunately, the industrial metals miners held within the Fund (+77.2% during the reported period) were able to capitalize on the underlying futures performance and helped provide nearly +6.9% in gross alpha to the annual tally.

Precious metals was the only sector to post negative performance over the twelve month period ending October 31, 2021, a return of -4.6% as measured by the BCOM precious metals sub-index total return. As the global economy roared back to life, the desire to hold safe-haven assets diminished. Additionally, while the US dollar continued its downward trend into year-end 2020, it managed to reverse course and rise thereafter through October month-end, up nearly +5% calendar year-to-date. Despite the poor beta move, the Fund’s inclusion of platinum (+20.3%) and tactical overweight to silver (+1.3%) added to outperformance. Accounting for the underweight the sector contributed nearly +0.9% in positive gross alpha on a gross basis. Both platinum and silver remain key ingredients to the world’s decarbonization efforts which we believe will only intensify following the recent United Nations gathering in Glasgow for COP26.

The Fund’s top equity holdings at the end of October 2021 included Tyson Foods Inc (TSN US) +43.23% YTD, CF Industries Holdings Inc (CF US) +111.72% YTD, Sanderson Farms Inc (SAFM US) +49.62% YTD, EOG Resources Inc (EOG US) +179.45% YTD, Inpex Corp (1605 JP) +102.29% YTD, Nutrien Ltd (NTR CN) +65.01% YTD, Evoqua Water Technologies Corp (AQUA US) +82.42% YTD, Boliden AB (BOL SS) +29.94% YTD, Lundin Energy AB (LUNE SS) +109.58% YTD, Fortuna Silver Mines Inc (FSM US) -26.59% YTD.

US Treasury Inflation Protected Securities (“TIPS”) and nominal US Treasuries are held by the Fund to invest excess cash and are used as collateral for commodity futures-related investments held in the Fund’s Cayman Island subsidiary. Over the previous calendar year, rates rose significantly due to inflationary pressure and the expectation for tapering by leading central banks. The yield on US 10-year notes rose from roughly 0.87% to 1.60% in twelve months’

| ALPS | CoreCommodity Management | |

| CompleteCommodities® Strategy Fund | |

| Management Commentary | October 31, 2021 (Unaudited) |

time. At the end of the period, the average maturity of the Fund’s collateral was approximately 0.3 years.

The previous fiscal year witnessed substantial appreciation in commodity prices; yet, despite the rally, we maintain a strong conviction that we are just now entering early innings of a larger structural bull market. In our view, many of the fundamental drivers that have pushed prices higher were in development well before the global pandemic, and many will likely take years more to find equilibrium. Most of the underlying markets accounted for within the Fund are now in deficit due to years of underinvestment in long-cycle projects. The supply-chain norm from years past of “just-in-time” inventories is now under tremendous strain and is prompting many to consider re-stocking campaigns. On the political front, the past decade was dedicated to achieving financial stability – the next decade will likely be dedicated to achieving social stability. With social reform come redistribution efforts, supply chain redundancies, de-globalization, and climate change initiatives – all of which would require massive spending and offset the low-cost efficiency gains of the 2000s. Together, we anticipate the levers pushing and pulling commodity markets into a new period of scarcity are due to persist until prices rise high enough to balance the market once again. With inflation for most leading economies now well above target and traditional asset valuations near all-time highs, we believe the commodity asset class is well-positioned for much greater participation among the investment community.

Bob Hyman

Portfolio Manager

CoreCommodity Management, LLC

Past performance if not indicative of future results. “Bloomberg®” and “Bloomberg Commodity IndexSM” are service marks of Bloomberg L.P. (“Bloomberg”) as the case may be. Source for all Index data: Bloomberg L.P. Global. Commodity Sectors and individual commodities are represented by the respective Bloomberg Commodity Sub-Index. This document does not constitute an offer of any commodities, securities or investment advisory services. Any such offer may be made only by means of a disclosure document or similar materials which contain a description of material terms and risks. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. The economic statistics presented herein are subject to revision by the agencies that issue them. CoreCommodity Management assumes no obligation to provide this information in the future or to advise of changes in this information. Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. All investments are subject to risk.

The views of the authors and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer's current views. The views expressed are those of the authors only, and represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither ALPS, Advisors, Inc., CoreCommodity Management, LLC, nor the Fund accepts any liability for losses either direct or consequential caused by the use of this information.

Indices do not reflect deductions for fees, expenses, or taxes.

An investor may not invest directly in an index.

Diversification cannot guarantee gain or prevent losses.

Bob Hyman is a registered representative of ALPS Distributors, Inc.

ALPS Portfolio Solutions Distributor, Inc., ALPS Distributors, Inc. and ALPS Advisors Inc. are affiliated.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Performance Update | October 31, 2021 (Unaudited) |

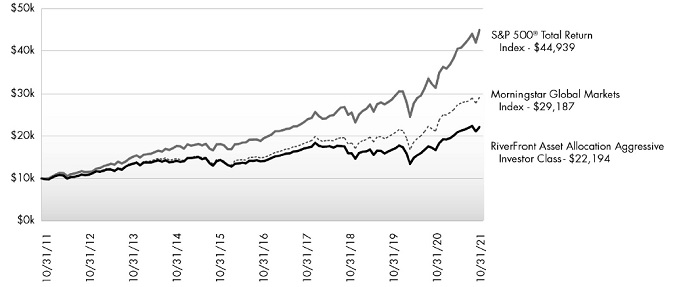

Performance of $10,000 Initial Investment (as of October 31, 2021)

Comparison of change in value of a $10,000 investment

The chart above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance does not guarantee future results. This chart does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Average Annual Total Returns (as of October 31, 2021)

| | 1 Year | 3 Year | 5 Year | 10 Year | Since

Inception^ | Total Expense Ratio | What You

Pay* |

| Investor# (NAV) | 57.25% | 9.54% | 6.89% | -1.11% | 1.37% | 1.45% | 1.45% |

| Class A (NAV) | 57.33% | 9.62% | 6.93% | -1.09% | 1.39% | 1.45% | 1.45% |

| Class A (LOAD) | 48.75% | 7.57% | 5.74% | -1.65% | 0.89% |

| Class C (NAV) | 56.37% | 8.87% | 6.21% | -1.74% | 0.75% | 2.05% | 2.05% |

| Class C (LOAD) | 55.37% | 8.87% | 6.21% | -1.74% | 0.75% |

| Class I | 57.74% | 9.85% | 7.14% | -0.84% | 1.65% | 1.15% | 1.15% |

| Refinitiv/CoreCommodity CRB Commodity Total Return Index1 | 64.31% | 8.63% | 6.17% | -2.34% | -0.12% | | |

| Bloomberg Commodity TR Index1 | 43.94% | 8.56% | 5.17% | -3.04% | -1.07% | | |

Performance data quoted represents past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than the original cost. Current performance data may be higher or lower than actual data quoted. For the most current month-end performance data, please call 1-866-759-5679.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. Performance shown at NAV does not include these sales charges and would have been lower had it been taken into account. If you invest $1 million or more, either as a lump sum or through the Fund’s accumulation or letter of intent programs, you can purchase Class A shares without an initial sales charge (load). A Contingent Deferred Sales Charge (“CDSC”) of 1.00% may apply to Class C shares redeemed within the first 12 months after a purchase, and on Class A shares redeemed within the first 18 months after a purchase in excess of $1 million. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days.

Performance less than 1 year is cumulative.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Performance Update | October 31, 2021 (Unaudited) |

Performance shown for Class A shares prior to June 12, 2018 reflects the historical performance of the Fund’s Investor shares, calculated using the fees and expenses of Class A shares.

| 1 | The Bloomberg Commodity TR Index (formerly the Dow Jones-UBS Commodity Index) and the Refinitiv/Core Commodity CRB Index are unmanaged indices used as a measurement of change in commodity market conditions based on the performance of a basket of different commodities. Each index is composed of a different basket of commodities, a different weighting of the commodities in the basket, and a different re-balancing schedule. The indices are not actively managed and do not reflect any deduction for fees, expenses or taxes. An investor may not invest directly in an index. |

| ^ | Fund Inception date of June 29, 2010 for Investor Class and Classes C and I; Fund Inception date of June 12, 2018 for Class A. |

| * | What You Pay reflects the Advisor’s decision to contractually limit expenses through February 28, 2022. Please see the prospectus dated February 28, 2021 for additional information. |

| # | Prior to December 1, 2017, Investor Class was known as Class A. |

Investments in securities of Master Limited Partnerships (MLPs) involve risks that differ from an investment in common stock. MLPs are controlled by their general partners, which generally have conflicts of interest and limited fiduciary duties to the MLP, which may permit the general partner to favor its own interests over the MLPs. The benefit you are expected to derive from the Fund’s investment in MLPs depends largely on the MLPs being treated as partnerships for federal income tax purposes. As a partnership, an MLP has no federal income tax liability at the entity level. Therefore, treatment of one or more MLPs as a corporation for federal income tax purposes could affect the Fund’s ability to meet its investment objective and would reduce the amount of cash available to pay or distribute to you. Legislative, judicial, or administrative changes and differing interpretations, possibly on a retroactive basis, could negatively impact the value of an investment in MLPs and therefore the value of your investment in the Fund.

Investing in commodity-related securities involves risk and considerations not present when investing in more conventional securities. The Fund may be more susceptible to high volatility of commodity markets.

Derivatives generally are more sensitive to changes in economic or market conditions than other types of investments; this could result in losses that significantly exceed the Fund's original investment.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

This Fund is not suitable for all investors, and is subject to investment risks, including possible loss of the principal amount invested.

There is no guarantee that the Fund will continue to hold any one particular security or stay invested in any one particular company. The composition of the Fund's top holdings is subject to change. Performance figures are historical and reflect the change in share price, reinvested distributions, changes in net asset value, sales charges and capital gains distributions, if any.

Not FDIC Insured – No Bank Guarantee – May Lose Value

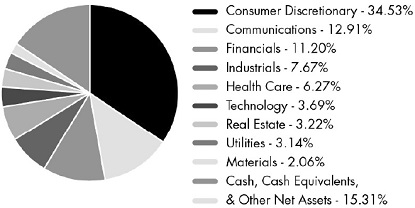

Asset Type Allocation (as a % of Net Assets)†

| Government Bonds | 60.12% |

| Common Stocks | 29.81% |

| Master Limited Partnerships | 0.04% |

| Cash, Cash Equivalents, & Other Net Assets | 10.03% |

| Total | 100.00% |

| † | Holdings are subject to change, and may not reflect the current or future position of the portfolio. Table presents approximate values only. |

Industry Sector Allocation (as a % of Net Assets) ^

| ^ | Notional Value of Derivative Exposure included |

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

| | | Shares | | | Value

(Note 2) | |

| COMMON STOCKS (29.81%) | | | | | | | | |

| Argentina (0.02%) | | | | | | | | |

| YPF SA, Sponsored ADR(a) | | | 73,592 | | | $ | 309,086 | |

| | | | | | | | | |

| Australia (1.75%) | | | | | | | | |

| Beach Energy, Ltd. | | | 1,202,200 | | | | 1,261,571 | |

| BHP Group, Ltd. | | | 57,246 | | | | 1,575,250 | |

| BlueScope Steel, Ltd. | | | 10,426 | | | | 161,721 | |

| Costa Group Holdings, Ltd. | | | 104,343 | | | | 229,196 | |

| Fortescue Metals Group, Ltd. | | | 303,039 | | | | 3,175,487 | |

| GrainCorp, Ltd., Class A | | | 85,256 | | | | 402,759 | |

| IGO, Ltd. | | | 132,309 | | | | 959,460 | |

| Iluka Resources, Ltd. | | | 195,693 | | | | 1,383,770 | |

| Incitec Pivot, Ltd. | | | 575,835 | | | | 1,295,179 | |

| Mineral Resources, Ltd. | | | 12,584 | | | | 365,304 | |

| Newcrest Mining, Ltd. | | | 63,097 | | | | 1,181,393 | |

| Northern Star Resources, Ltd. | | | 295,840 | | | | 2,056,314 | |

| Nufarm, Ltd.(a) | | | 147,504 | | | | 482,674 | |

| Oil Search, Ltd. | | | 73,894 | | | | 238,466 | |

| Orocobre, Ltd.(a) | | | 239,467 | | | | 1,603,232 | |

| Perseus Mining, Ltd.(a) | | | 532,660 | | | | 633,093 | |

| Sandfire Resources NL | | | 78,872 | | | | 329,882 | |

| Santos, Ltd. | | | 400,731 | | | | 2,104,113 | |

| South32, Ltd. | | | 823,504 | | | | 2,211,539 | |

| St Barbara, Ltd. | | | 162,515 | | | | 179,098 | |

| Woodside Petroleum, Ltd. | | | 18,740 | | | | 327,899 | |

| | | | | | | | 22,157,400 | |

| | | | | | | | | |

| Austria (0.09%) | | | | | | | | |

| OMV AG | | | 6,908 | | | | 418,449 | |

| voestalpine AG | | | 18,655 | | | | 708,202 | |

| | | | | | | | 1,126,651 | |

| | | | | | | | | |

| Brazil (0.71%) | | | | | | | | |

| BRF SA, ADR(a) | | | 193,584 | | | | 799,502 | |

| Cia de Saneamento Basico do Estado de Sao Paulo, ADR | | | 126,298 | | | | 793,151 | |

| Cia Siderurgica Nacional SA, Sponsored ADR | | | 267,613 | | | | 1,091,861 | |

| Gerdau SA, Sponsored ADR | | | 334,480 | | | | 1,582,090 | |

| Petroleo Brasileiro SA, Sponsored ADR | | | 270,198 | | | | 2,653,345 | |

| Vale SA, Sponsored ADR | | | 163,817 | | | | 2,085,391 | |

| | | | | | | | 9,005,340 | |

| | | | | | | | | |

| Canada (5.67%) | | | | | | | | |

| Agnico Eagle Mines, Ltd. | | | 19,374 | | | | 1,027,791 | |

| Alamos Gold, Inc., Class A | | | 218,074 | | | | 1,622,471 | |

| ARC Resources, Ltd. | | | 398,100 | | | | 3,818,234 | |

| B2Gold Corp. | | | 655,682 | | | | 2,714,523 | |

| Ballard Power Systems, Inc.(a) | | | 118,198 | | | | 2,141,748 | |

| Barrick Gold Corp. | | | 49,181 | | | | 903,455 | |

| Cameco Corp. | | | 63,522 | | | | 1,543,585 | |

| Canadian Solar, Inc.(a) | | | 71,489 | | | | 2,970,368 | |

| Canfor Corp.(a) | | | 28,900 | | | | 598,736 | |

| Centerra Gold, Inc. | | | 133,600 | | | | 1,001,784 | |

| Crescent Point Energy Corp. | | | 795,000 | | | | 3,995,556 | |

| | | Shares | | | Value

(Note 2) | |

| Canada (continued) | | | | | | | | |

| Dundee Precious Metals, Inc. | | | 137,800 | | | $ | 906,345 | |

| Eldorado Gold Corp.(a) | | | 135,739 | | | | 1,216,221 | |

| Endeavour Silver Corp.(a) | | | 231,350 | | | | 1,168,318 | |

| Enerplus Corp. | | | 44,048 | | | | 417,135 | |

| First Majestic Silver Corp. | | | 125,311 | | | | 1,587,690 | |

| First Quantum Minerals, Ltd. | | | 56,000 | | | | 1,325,792 | |

| Fortuna Silver Mines, Inc.(a) | | | 950,860 | | | | 4,621,180 | |

| Hudbay Minerals, Inc. | | | 180,500 | | | | 1,258,658 | |

| IAMGOLD Corp.(a) | | | 346,775 | | | | 960,567 | |

| Interfor Corp. | | | 59,000 | | | | 1,351,050 | |

| Ivanhoe Mines, Ltd., Class A(a) | | | 125,500 | | | | 984,652 | |

| Kinross Gold Corp. | | | 420,610 | | | | 2,527,866 | |

| Kirkland Lake Gold, Ltd. | | | 3,800 | | | | 160,186 | |

| Lundin Mining Corp. | | | 184,000 | | | | 1,601,228 | |

| Maple Leaf Foods, Inc. | | | 22,700 | | | | 494,866 | |

| MEG Energy Corp.(a) | | | 135,900 | | | | 1,217,785 | |

| Northland Power, Inc. | | | 40,900 | | | | 1,314,973 | |

| Nutrien, Ltd. | | | 77,400 | | | | 5,409,744 | |

| Pan American Silver Corp. | | | 151,713 | | | | 3,885,370 | |

| Parex Resources, Inc. | | | 85,000 | | | | 1,650,412 | |

| PrairieSky Royalty, Ltd. | | | 31,600 | | | | 388,872 | |

| Pretium Resources, Inc.(a) | | | 49,531 | | | | 598,334 | |

| Silvercorp Metals, Inc. | | | 168,876 | | | | 712,657 | |

| SSR Mining, Inc. | | | 144,286 | | | | 2,276,712 | |

| Suncor Energy, Inc. | | | 145,800 | | | | 3,834,672 | |

| Torex Gold Resources, Inc.(a) | | | 109,600 | | | | 1,274,357 | |

| Tourmaline Oil Corp. | | | 93,300 | | | | 3,372,098 | |

| Turquoise Hill Resources, Ltd.(a) | | | 10,049 | | | | 127,321 | |

| Vermilion Energy, Inc.(a) | | | 150,000 | | | | 1,626,535 | |

| Village Farms International, Inc.(a) | | | 148,148 | | | | 1,121,480 | |

| | | | | | | | 71,731,327 | |

| | | | | | | | | |

| Chile (0.29%) | | | | | | | | |

| Antofagasta PLC | | | 53,247 | | | | 1,038,779 | |

| Sociedad Quimica y Minera de Chile SA, Sponsored ADR | | | 47,357 | | | | 2,599,426 | |

| | | | | | | | 3,638,205 | |

| | | | | | | | | |

| China (0.23%) | | | | | | | | |

| China Petroleum & Chemical Corp., ADR | | | 5,780 | | | | 281,370 | |

| Daqo New Energy Corp., ADR(a) | | | 7,613 | | | | 592,215 | |

| JinkoSolar Holding Co., Ltd., ADR(a) | | | 27,133 | | | | 1,623,097 | |

| PetroChina Co., Ltd., ADR | | | 8,809 | | | | 425,122 | |

| | | | | | | | 2,921,804 | |

| | | | | | | | | |

| Colombia (0.07%) | | | | | | | | |

| Ecopetrol SA, Sponsored ADR | | | 56,879 | | | | 861,717 | |

| | | | | | | | | |

| Denmark (0.11%) | | | | | | | | |

| FLSmidth & Co. A/S | | | 14,347 | | | | 545,342 | |

| Orsted AS(b)(c) | | | 6,179 | | | | 871,878 | |

| | | | | | | | 1,417,220 | |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

| | | Shares | | | Value

(Note 2) | |

| Faroe Islands (0.05%) | | | | | | | | |

| Bakkafrost P/F | | | 6,869 | | | $ | 634,382 | |

| | | | | | | | | |

| Finland (0.18%) | | | | | | | | |

| Metso Outotec Oyj | | | 121,017 | | | | 1,214,297 | |

| Outokumpu Oyj(a) | | | 166,365 | | | | 1,038,519 | |

| | | | | | | | 2,252,816 | |

| | | | | | | | | |

| France (0.12%) | | | | | | | | |

| Constellium SE(a) | | | 34,942 | | | | 643,282 | |

| TotalEnergies SE, ADR | | | 16,315 | | | | 817,545 | |

| | | | | | | | 1,460,827 | |

| | | | | | | | | |

| Germany (0.18%) | | | | | | | | |

| K+S AG(a) | | | 70,154 | | | | 1,207,958 | |

| Nordex SE(a) | | | 10,156 | | | | 186,672 | |

| Salzgitter AG(a) | | | 10,429 | | | | 383,620 | |

| SMA Solar Technology AG | | | 3,703 | | | | 195,456 | |

| thyssenkrupp AG(a) | | | 17,747 | | | | 184,476 | |

| VERBIO Vereinigte BioEnergie AG | | | 2,122 | | | | 168,278 | |

| | | | | | | | 2,326,460 | |

| | | | | | | | | |

| Great Britain (1.45%) | | | | | | | | |

| Anglo American PLC | | | 24,783 | | | | 943,735 | |

| Atlantica Sustainable Infrastructure PLC | | | 49,229 | | | | 1,937,161 | |

| BP PLC, Sponsored ADR | | | 124,106 | | | | 3,573,012 | |

| CNH Industrial N.V. | | | 81,081 | | | | 1,387,296 | |

| Evraz PLC | | | 91,946 | | | | 782,176 | |

| Pennon Group PLC | | | 41,248 | | | | 658,207 | |

| Pentair PLC | | | 27,500 | | | | 2,034,175 | |

| Rio Tinto PLC, Sponsored ADR | | | 48,371 | | | | 3,060,433 | |

| Severn Trent PLC | | | 36,254 | | | | 1,358,471 | |

| Subsea 7 SA | | | 50,511 | | | | 452,978 | |

| TechnipFMC PLC | | | 74,155 | | | | 546,522 | |

| United Utilities Group PLC | | | 99,030 | | | | 1,407,454 | |

| Weir Group PLC | | | 6,090 | | | | 144,603 | |

| | | | | | | | 18,286,223 | |

| | | | | | | | | |

| Israel (0.19%) | | | | | | | | |

| SolarEdge Technologies, Inc.(a) | | | 6,820 | | | | 2,418,918 | |

| | | | | | | | | |

| Italy (0.07%) | | | | | | | | |

| Eni SpA, Sponsored ADR | | | 18,989 | | | | 546,694 | |

| ERG SpA | | | 10,237 | | | | 369,457 | |

| | | | | | | | 916,151 | |

| | | | | | | | | |

| Japan (1.63%) | | | | | | | | |

| AGC, Inc. | | | 69,700 | | | | 3,467,417 | |

| Daido Steel Co., Ltd. | | | 6,200 | | | | 237,447 | |

| Ezaki Glico Co., Ltd. | | | 4,600 | | | | 166,686 | |

| GS Yuasa Corp. | | | 21,600 | | | | 468,861 | |

| Hitachi Metals, Ltd.(a) | | | 34,000 | | | | 643,457 | |

| Inpex Corp. | | | 661,133 | | | | 5,522,251 | |

| JFE Holdings, Inc. | | | 35,900 | | | | 549,013 | |

| Kobe Steel, Ltd. | | | 77,200 | | | | 453,819 | |

| Kubota Corp. | | | 24,700 | | | | 524,990 | |

| | | Shares | | | Value

(Note 2) | |

| Japan (continued) | | | | | | | | |

| Kurita Water Industries, Ltd. | | | 25,716 | | | $ | 1,263,519 | |

| Morinaga Milk Industry Co., Ltd. | | | 6,500 | | | | 380,961 | |

| NGK Insulators, Ltd. | | | 34,800 | | | | 577,685 | |

| Nippon Light Metal Holdings Co., Ltd. | | | 23,800 | | | | 394,039 | |

| Nippon Steel Corp. | | | 102,590 | | | | 1,799,319 | |

| RENOVA, Inc.(a) | | | 24,800 | | | | 1,087,958 | |

| Sumitomo Forestry Co., Ltd. | | | 28,759 | | | | 547,550 | |

| Sumitomo Metal Mining Co., Ltd. | | | 51,300 | | | | 1,990,787 | |

| Tokyo Steel Manufacturing Co., Ltd. | | | 50,500 | | | | 560,939 | |

| | | | | | | | 20,636,698 | |

| | | | | | | | | |

| Luxembourg (0.27%) | | | | | | | | |

| APERAM SA | | | 14,100 | | | | 840,735 | |

| ArcelorMittal | | | 24,464 | | | | 835,935 | |

| ArcelorMittal SA | | | 5,056 | | | | 171,397 | |

| Tenaris SA, ADR | | | 27,417 | | | | 610,851 | |

| Ternium SA, Sponsored ADR | | | 19,564 | | | | 906,400 | |

| | | | | | | | 3,365,318 | |

| | | | | | | | | |

| Malaysia (0.07%) | | | | | | | | |

| Lynas Rare Earths, Ltd.(a) | | | 150,983 | | | | 832,516 | |

| | | | | | | | | |

| Mexico (0.15%) | | | | | | | | |

| Grupo Mexico SAB de CV, Series B | | 445,700 | | | | 1,953,131 | |

| | | | | | | | | |

| Netherlands (0.23%) | | | | | | | | |

| AMG Advanced Metallurgical Group NV | | | 9,059 | | | | 267,461 | |

| Core Laboratories N.V. | | | 48,394 | | | | 1,258,727 | |

| OCI N.V.(a) | | | 15,679 | | | | 444,062 | |

| Royal Dutch Shell PLC, Class A, Sponsored ADR | | | 8,932 | | | | 410,158 | |

| Royal Dutch Shell PLC, Class B | | | 2,551 | | | | 58,826 | |

| SBM Offshore N.V. | | | 27,872 | | | | 440,127 | |

| | | | | | | | 2,879,361 | |

| | | | | | | | | |

| Norway (1.34%) | | | | | | | | |

| Aker BP ASA | | | 75,504 | | | | 2,894,891 | |

| Aker Solutions ASA(a) | | | 61,939 | | | | 175,452 | |

| DNO ASA(a) | | | 516,958 | | | | 752,682 | |

| Equinor ASA | | | 130,031 | | | | 3,290,063 | |

| Leroy Seafood Group ASA | | | 70,514 | | | | 641,044 | |

| Mowi ASA | | | 80,496 | | | | 2,330,676 | |

| NEL ASA(a) | | | 476,921 | | | | 1,006,582 | |

| Salmar ASA | | | 12,666 | | | | 964,055 | |

| Scatec ASA(b)(c) | | | 52,789 | | | | 1,037,921 | |

| TGS ASA | | | 50,202 | | | | 461,854 | |

| Yara International ASA | | | 64,676 | | | | 3,374,706 | |

| | | | | | | | 16,929,926 | |

| | | | | | | | | |

| Peru (0.12%) | | | | | | | | |

| Cia de Minas Buenaventura SAA, ADR | | | 24,873 | | | | 195,999 | |

| Southern Copper Corp. | | | 22,386 | | | | 1,342,936 | |

| | | | | | | | 1,538,935 | |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

| | | Shares | | | Value

(Note 2) | |

| South Africa (0.61%) | | | | | | | | |

| African Rainbow Minerals, Ltd. | | | 36,752 | | | $ | 489,698 | |

| Anglo Platinum, Ltd. | | | 4,780 | | | | 482,976 | |

| AngloGold Ashanti, Ltd., Sponsored ADR | | | 68,785 | | | | 1,271,147 | |

| Gold Fields, Ltd., Sponsored ADR | | | 294,242 | | | | 2,730,565 | |

| Impala Platinum Holdings, Ltd. | | | 54,000 | | | | 699,932 | |

| Kumba Iron Ore, Ltd. | | | 15,133 | | | | 459,885 | |

| Sasol, Ltd.(a) | | | 77,701 | | | | 1,305,325 | |

| Sibanye Stillwater, Ltd., ADR | | | 23,619 | | | | 335,390 | |

| | | | | | | | 7,774,918 | |

| | | | | | | | | |

| Spain (0.34%) | | | | | | | | |

| Acerinox SA | | | 44,206 | | | | 615,016 | |

| Fluidra SA | | | 22,858 | | | | 873,310 | |

| Iberdrola SA | | | 122,968 | | | | 1,452,075 | |

| Repsol SA | | | 21,441 | | | | 274,032 | |

| Siemens Gamesa Renewable Energy SA(a) | | | 24,558 | | | | 665,157 | |

| Solaria Energia y Medio Ambiente SA | | | 18,123 | | | | 361,811 | |

| | | | | | | | 4,241,401 | |

| | | | | | | | | |

| Sweden (1.33%) | | | | | | | | |

| AAK AB | | | 17,147 | | | | 374,766 | |

| Boliden AB | | | 147,867 | | | | 5,215,291 | |

| Epiroc AB, Class A | | | 59,249 | | | | 1,474,326 | |

| Holmen AB, B Shares | | | 8,330 | | | | 369,360 | |

| Lundin Energy AB | | | 124,444 | | | | 4,915,161 | |

| SSAB AB, A Shares(a) | | | 190,388 | | | | 1,084,068 | |

| Svenska Cellulosa AB SCA, Class B | | 218,017 | | | | 3,399,217 | |

| | | | | | | | 16,832,189 | |

| | | | | | | | | |

| Switzerland (0.06%) | | | | | | | | |

| Bucher Industries AG | | | 799 | | | | 402,816 | |

| Ferrexpo PLC | | | 75,872 | | | | 323,964 | |

| | | | | | | | 726,780 | |

| | | | | | | | | |

| United States (12.48%) | | | | | | | | |

| Allegheny Technologies, Inc.(a) | | | 34,615 | | | | 557,302 | |

| American Water Works Co., Inc. | | | 10,923 | | | | 1,902,568 | |

| APA Corp. | | | 46,650 | | | | 1,222,697 | |

| Archer-Daniels-Midland Co. | | | 24,736 | | | | 1,589,041 | |

| Archrock, Inc. | | | 40,183 | | | | 329,099 | |

| Arconic, Inc.(a) | | | 11,241 | | | | 330,710 | |

| Array Technologies, Inc.(a) | | | 28,924 | | | | 617,527 | |

| Baker Hughes Co. | | | 54,605 | | | | 1,369,493 | |

| Beyond Meat, Inc.(a) | | | 36,822 | | | | 3,644,642 | |

| Bunge, Ltd. | | | 35,629 | | | | 3,300,671 | |

| Callon Petroleum Co.(a) | | | 35,045 | | | | 1,812,878 | |

| Cal-Maine Foods, Inc. | | | 14,471 | | | | 521,824 | |

| Centennial Resource Development, Inc., Class A(a) | | | 253,214 | | | | 1,823,141 | |

| Century Aluminum Co.(a) | | | 19,099 | | | | 252,298 | |

| CF Industries Holdings, Inc. | | | 128,383 | | | | 7,292,153 | |

| ChampionX Corp.(a) | | | 42,298 | | | | 1,109,477 | |

| Chemours Co. | | | 33,674 | | | | 943,545 | |

| Chevron Corp. | | | 16,947 | | | | 1,940,262 | |

| | | Shares | | | Value

(Note 2) | |

| United States (continued) | | | | | | | | |

| Cleveland-Cliffs, Inc.(a) | | | 35,956 | | | $ | 866,899 | |

| CNX Resources Corp.(a) | | | 64,935 | | | | 948,700 | |

| Commercial Metals Co. | | | 23,930 | | | | 770,067 | |

| Compass Minerals International, Inc. | | | 7,430 | | | | 487,408 | |

| Comstock Resources, Inc.(a) | | | 179,790 | | | | 1,774,527 | |

| ConocoPhillips | | | 55,244 | | | | 4,115,126 | |

| Continental Resources, Inc. | | | 17,307 | | | | 844,755 | |

| Corteva, Inc. | | | 62,955 | | | | 2,716,508 | |

| Coterra Energy, Inc. | | | 61,433 | | | | 1,309,752 | |

| Deere & Co. | | | 4,669 | | | | 1,598,245 | |

| Devon Energy Corp. | | | 43,208 | | | | 1,731,777 | |

| Diamondback Energy, Inc. | | | 36,615 | | | | 3,924,762 | |

| Enphase Energy, Inc.(a) | | | 10,981 | | | | 2,543,529 | |

| EOG Resources, Inc. | | | 63,868 | | | | 5,905,234 | |

| Essential Utilities, Inc. | | | 25,937 | | | | 1,220,855 | |

| Evoqua Water Technologies Corp.(a) | | | 126,349 | | | | 5,285,179 | |

| Exxon Mobil Corp. | | | 22,980 | | | | 1,481,521 | |

| First Solar, Inc.(a) | | | 10,918 | | | | 1,305,684 | |

| FMC Corp. | | | 3,036 | | | | 276,306 | |

| Freeport-McMoRan, Inc. | | | 29,192 | | | | 1,101,122 | |

| FuelCell Energy, Inc.(a) | | | 194,280 | | | | 1,552,297 | |

| Green Plains, Inc.(a) | | | 33,207 | | | | 1,260,206 | |

| Halliburton Co. | | | 82,737 | | | | 2,067,598 | |

| Hecla Mining Co. | | | 211,701 | | | | 1,223,632 | |

| Helix Energy Solutions Group, Inc.(a) | | | 302,387 | | | | 1,143,023 | |

| Helmerich & Payne, Inc. | | | 52,323 | | | | 1,624,106 | |

| Hess Corp. | | | 15,736 | | | | 1,299,322 | |

| HollyFrontier Corp. | | | 22,080 | | | | 746,304 | |

| Ingredion, Inc. | | | 24,933 | | | | 2,374,370 | |

| Kinder Morgan, Inc. | | | 5,763 | | | | 96,530 | |

| Kosmos Energy, Ltd.(a) | | | 351,823 | | | | 1,266,563 | |

| Laredo Petroleum, Inc.(a) | | | 3,530 | | | | 266,162 | |

| Liberty Oilfield Services, Inc., Class A(a) | | | 27,088 | | | | 349,977 | |

| Livent Corp.(a) | | | 39,051 | | | | 1,102,019 | |

| Magnolia Oil & Gas Corp., Class A | | | 91,528 | | | | 1,911,105 | |

| Marathon Oil Corp. | | | 157,414 | | | | 2,568,996 | |

| Marathon Petroleum Corp. | | | 24,420 | | | | 1,610,011 | |

| Matador Resources Co. | | | 9,992 | | | | 418,165 | |

| Mosaic Co. | | | 80,002 | | | | 3,325,683 | |

| Murphy Oil Corp. | | | 65,937 | | | | 1,835,027 | |

| National Oilwell Varco, Inc.(a) | | | 84,671 | | | | 1,187,087 | |

| New WEI, Inc.(a) | | | 68,768 | | | | 103 | |

| Newmont Corp. | | | 28,525 | | | | 1,540,350 | |

| Northern Oil and Gas, Inc.(a) | | | 13,153 | | | | 304,623 | |

| Occidental Petroleum Corp. | | | 69,074 | | | | 2,316,053 | |

| Oceaneering International, Inc.(a) | | | 69,252 | | | | 941,827 | |

| Ormat Technologies, Inc. | | | 50,064 | | | | 3,621,129 | |

| Ovintiv, Inc. | | | 57,283 | | | | 2,149,258 | |

| Patterson-UTI Energy, Inc. | | | 187,413 | | | | 1,604,255 | |

| PDC Energy, Inc. | | | 67,573 | | | | 3,534,744 | |

| Phillips 66 | | | 8,398 | | | | 628,002 | |

| Pilgrim's Pride Corp.(a) | | | 45,023 | | | | 1,267,848 | |

| Pioneer Natural Resources Co. | | | 12,603 | | | | 2,356,509 | |

| Plug Power, Inc.(a) | | | 21,677 | | | | 829,579 | |

| PotlatchDeltic Corp., REIT | | | 68,244 | | | | 3,567,114 | |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

| | | Shares | | | Value

(Note 2) | |

| United States (continued) | | | | | | | | |

| ProPetro Holding Corp.(a) | | | 114,066 | | | $ | 1,093,893 | |

| Rayonier, Inc., REIT | | | 22,544 | | | | 841,568 | |

| Reliance Steel & Aluminum Co. | | | 4,037 | | | | 590,048 | |

| Renewable Energy Group, Inc.(a) | | | 49,914 | | | | 3,194,496 | |

| Royal Gold, Inc. | | | 8,866 | | | | 877,911 | |

| RPC, Inc.(a) | | | 140,085 | | | | 755,058 | |

| Sanderson Farms, Inc. | | | 38,329 | | | | 7,261,428 | |

| Schlumberger NV | | | 29,651 | | | | 956,541 | |

| SM Energy Co. | | | 28,819 | | | | 989,068 | |

| SunPower Corp.(a) | | | 64,160 | | | | 2,159,626 | |

| Talos Energy, Inc.(a) | | | 84,365 | | | | 1,094,214 | |

| Tellurian, Inc.(a) | | | 84,139 | | | | 329,825 | |

| Transocean, Ltd.(a) | | | 327,020 | | | | 1,154,381 | |

| Tyson Foods, Inc., Class A | | | 113,035 | | | | 9,039,408 | |

| US Silica Holdings, Inc.(a) | | | 105,682 | | | | 1,023,002 | |

| Valero Energy Corp. | | | 15,840 | | | | 1,224,907 | |

| Warrior Met Coal, Inc. | | | 18,618 | | | | 446,273 | |

| Williams Cos., Inc. | | | 1,855 | | | | 52,107 | |

| | | | | | | | 157,740,615 | |

| | | | | | | | | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $317,380,513) | | | | | | | 376,916,315 | |

| | | | | | | | | |

| MASTER LIMITED PARTNERSHIPS (0.04%) | | | | | | | | |

| United States (0.04%) | | | | | | | | |

| Energy Transfer LP | | | 4,974 | | | | 47,303 | |

| Enterprise Products Partners LP | | | 10,676 | | | | 242,131 | |

| Magellan Midstream Partners LP | | | 2,054 | | | | 100,646 | |

| MPLX LP | | | 1,555 | | | | 46,837 | |

| Plains All American Pipeline LP | | | 3,090 | | | | 31,271 | |

| | | | | | | | 468,188 | |

| | | | | | | | | |

| TOTAL MASTER LIMITED PARTNERSHIPS | | | | | | | | |

| (Cost $900,221) | | | | | | | 468,188 | |

| | | | | | | | | |

| | | Principal

Amount | | | Value

(Note 2) | |

| GOVERNMENT BONDS (60.12%) | | | | | | | | |

| U.S. Treasury Bonds (60.12%) | | | | | | | | |

| United States Treasury Bill | | | | | | | | |

| 0.002%, 11/4/21(d) | | $ | 345,400,000 | | | $ | 345,399,137 | |

| 0.049%, 1/27/22 | | | 27,000,000 | | | | 26,996,574 | |

| United States Treasury Inflation Indexed Bonds | | | | | | | | |

| 0.125%, 1/15/22(d) | | | 220,992,510 | | | | 222,973,942 | |

| 0.625%, 4/15/23 | | | 112,330,560 | | | | 118,137,777 | |

| United States Treasury Notes | | | | | | | | |

| 1.750%, 2/28/22(d) | | | 19,500,000 | | | | 19,607,912 | |

| 1.875%, 5/31/22 | | | 27,000,000 | | | | 27,279,227 | |

| | | | | | | | 760,394,569 | |

| TOTAL GOVERNMENT BONDS | | | | | | | | |

| (Cost $758,455,493) | | | | | | | 760,394,569 | |

| | | Value

(Note 2) | |

| TOTAL INVESTMENTS (89.97%) | | | | |

| (Cost $1,076,736,227) | | $ | 1,137,779,072 | |

| | | | | |

| Other Assets In Excess Of Liabilities (10.03%) | | | 126,781,355 | |

| NET ASSETS - 100.00% | | $ | 1,264,560,427 | |

| (a) | Non-Income Producing Security. |

| (b) | Security exempt from registration under rule 144A of the securities act of 1933. This Security may be resold in transactions exempt from registration, normally to qualified institutional buyers. As of October 31, 2021, the market value of those securities was $1,909,799 representing 0.15% of the Fund's net assets. |

| (c) | Securities were purchased pursuant to Regulation S under the Securities Act of 1933, which exempts securities offered and sold outside of the United States from registration. Such securities cannot be sold in the United States without either an effective registration statement filed pursuant to the Securities Act of 1933, or pursuant to an exemption from registration. These securities have been deemed liquid under guidelines approved by the Fund's Board of Trustees. As of October 31, 2021 the aggregate market value of those securities was $1,909,799 representing 0.15% of net assets. |

| (d) | Security, or portion of security, is being held as collateral for total return swap contracts and futures contracts aggregating a total market value of $80,130,017. |

For Fund compliance purposes, the Fund's industry and geographical classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine sub-classifications for reporting ease. Industries and regions are shown as a percent of net assets.

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

FUTURES CONTRACTS

| Description | | Counterparty | | Position | | Contracts | | Expiration Date | | Notional Amount/

Fair Value (Note 2) | | | Unrealized Appreciation | |

| Corn Future | | Morgan Stanley | | Long | | 297 | | 12/14/21 | | $ | 8,438,513 | | | $ | 89,228 | |

| Frzn Concentrated OJ | | Morgan Stanley | | Short | | (12) | | 01/10/22 | | | (221,490 | ) | | | 2,275 | |

| Gasoline RBOB Future | | Morgan Stanley | | Short | | (44) | | 11/30/21 | | | (4,379,206 | ) | | | 93,128 | |

| Gold Future | | Morgan Stanley | | Long | | 206 | | 12/29/21 | | | 36,748,340 | | | | 67,612 | |

| Hard Red Winter Wheat Future | | Morgan Stanley | | Long | | 64 | | 12/14/21 | | | 2,514,400 | | | | 224,642 | |

| Heating Oil Future | | Morgan Stanley | | Short | | (102) | | 11/30/21 | | | (10,618,751 | ) | | | 273,088 | |

| Lean Hogs Future | | Morgan Stanley | | Long | | 82 | | 12/14/21 | | | 2,495,260 | | | | 57,353 | |

| Live Cattle Future | | Morgan Stanley | | Short | | (202) | | 12/31/21 | | | (10,445,420 | ) | | | 337,410 | |

| LME Copper Future | | Morgan Stanley | | Long | | 300 | | 11/15/21 | | | 72,963,750 | | | | 2,734,677 | |

| LME Nickel Future | | Morgan Stanley | | Long | | 126 | | 11/15/21 | | | 14,761,656 | | | | 229,048 | |

| LME Zinc Future | | Morgan Stanley | | Long | | 267 | | 11/15/21 | | | 22,977,019 | | | | 1,926,563 | |

| Low Su Gasoil G Nov21 | | Morgan Stanley | | Long | | 332 | | 11/11/21 | | | 23,854,200 | | | | 512,505 | |

| Platinum Future | | Morgan Stanley | | Long | | 265 | | 01/27/22 | | | 13,524,275 | | | | 1,272,266 | |

| Silver Future | | Morgan Stanley | | Long | | 194 | | 12/29/21 | | | 23,230,530 | | | | 760,235 | |

| Sugar #11 (World) | | Morgan Stanley | | Short | | (229) | | 02/28/22 | | | (4,942,370 | ) | | | 335,510 | |

| Wheat Future | | Morgan Stanley | | Long | | 45 | | 12/14/21 | | | 1,738,688 | | | | 99,452 | |

| | | | | | | | | | | $ | 192,639,394 | | | $ | 9,014,992 | |

| Description | | Counterparty | | Position | | Contracts | | Expiration Date | | Notional Amount/

Fair Value (Note 2) | | | Unrealized Depreciation | |

| Brent Crude Future | | Morgan Stanley | | Long | | 908 | | 11/30/21 | | $ | 76,017,760 | | | $ | (364,470 | ) |

| Coffee 'C' Future | | Morgan Stanley | | Short | | (39) | | 12/20/21 | | | (2,982,769 | ) | | | (715,996 | ) |

| Copper Future | | Morgan Stanley | | Short | | (474) | | 03/29/22 | | | (51,429,000 | ) | | | (201,983 | ) |

| Cotton No.2 Future | | Morgan Stanley | | Short | | (166) | | 12/08/21 | | | (9,532,550 | ) | | | (2,484,128 | ) |

| LME Aluminum Future | | Morgan Stanley | | Long | | 164 | | 11/15/21 | | | 11,120,225 | | | | (88,223 | ) |

| LME Copper Future | | Morgan Stanley | | Short | | (36) | | 11/15/21 | | | (8,755,650 | ) | | | (93,489 | ) |

| Natural Gas Future | | Morgan Stanley | | Long | | 834 | | 11/26/21 | | | 45,252,840 | | | | (834,898 | ) |

| Soybean Future | | Morgan Stanley | | Long | | 93 | | 03/14/22 | | | 5,854,350 | | | | (23,480 | ) |

| Soybean Meal Future | | Morgan Stanley | | Long | | 349 | | 12/14/21 | | | 11,607,740 | | | | (883,952 | ) |

| WTI Crude Future | | Morgan Stanley | | Short | | (230) | | 01/20/22 | | | (18,395,400 | ) | | | (2,536,074 | ) |

| WTI Crude Future | | Morgan Stanley | | Short | | (1,008) | | 02/22/22 | | | (79,087,680 | ) | | | (2,710,583 | ) |

| | | | | | | | | | | $ | (20,330,134 | ) | | $ | (10,937,276 | ) |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Investments | October 31, 2021 |

TOTAL RETURN SWAP CONTRACTS(a)

| Swap Counterparty | | Reference Obligation | | Notional Amount | | | Floating Rate/Fixed Amount Paid by Fund* | | Termination Date | | Value | | | Unrealized Appreciation | |

| Citibank | | CRB 3m Fwd TR Index** | | $ | 206,078,650 | | | USB3MTA + 24 bps | | 9/30/2022 | | $ | 206,078,655 | | | $ | 5 | |

| Goldman Sachs | | CRB 3m Fwd TR Index** | | | 15,852,885 | | | USB3MTA + 25 bps | | 9/30/2022 | | $ | 15,852,886 | | | | 1 | |

| Societe Generale | | CRB 3m Fwd TR Index** | | | 62,825,070 | | | USB3MTA + 28 bps | | 11/30/2021 | | $ | 62,825,073 | | | | 3 | |

| UBS Group AG | | CRB 3m Fwd TR Index** | | | 216,901,376 | | | USB3MTA + 25 bps | | 11/30/2021 | | $ | 216,901,377 | | | | 1 | |

| | | | | $ | 501,657,981 | | | | | | | $ | 501,657,991 | | | $ | 10 | |

| Swap Counterparty | | Reference Obligation | | Notional Amount | | | Floating Rate/Fixed Amount Paid by Fund* | | Termination Date | | Value | | | Unrealized Depreciation | |

| Merrill Lynch | | CRB 3m Fwd TR Index** | | $ | 203,368,817 | | | USB3MTA + 25 bps | | 6/29/2022 | | $ | 203,368,542 | | | $ | (275 | ) |

| | | | | $ | 203,368,817 | | | | | | | $ | 203,368,542 | | | $ | (275 | ) |

| (a) | For long positions in the total return swap, the Fund receives payments based on any positive return of the Reference Obligation less the rate paid by the Fund. The Fund makes payments on any negative return of such Reference Obligations plus the rate paid by the fund. For short positions in the total return swap, the Fund makes payments based on any positive return of the Reference Obligation less the rate paid by the Fund. The Fund receives payments on any negative return of such Reference Obligations plus the rate paid by the Fund. |

| * | United States Auction Results 3 Month Treasury Bill High Discount. Total return swap resets monthly. |

| ** | CRB - Commodity Research Bureau |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Assets and Liabilities | October 31, 2021 |

| ASSETS | | | |

| Investments, at value | | $ | 1,137,779,072 | |

| Cash | | | 98,259,720 | |

| Foreign currency, at value (Cost $1,641,701) | | | 1,644,885 | |

| Unrealized appreciation on total return swap contracts | | | 10 | |

| Receivable for shares sold | | | 10,916,331 | |

| Receivable due from broker for total return swap contracts | | | 18,265,832 | |

| Receivable due from broker for futures contracts | | | 4,708,576 | |

| Dividends and interest receivable | | | 699,441 | |

| Prepaid expenses and other assets | | | 91,309 | |

| Total Assets | | | 1,272,365,176 | |

| LIABILITIES | | | | |

| Payable for investments purchased | | | 3,053,878 | |

| Payable for variation margin on futures contracts | | | 2,128,906 | |

| Payable for shares redeemed | | | 762,862 | |

| Unrealized depreciation on total return swap contracts | | | 275 | |

| Investment advisory fees payable | | | 891,156 | |

| Administration and transfer agency fees payable | | | 415,377 | |

| Distribution and services fees payable | | | 61,218 | |

| Trustees' fees and expenses payable | | | 12,936 | |

| Professional fees payable | | | 38,284 | |

| Accrued expenses and other liabilities | | | 439,857 | |

| Total Liabilities | | | 7,804,749 | |

| NET ASSETS | | $ | 1,264,560,427 | |

| NET ASSETS CONSIST OF | | | | |

| Paid-in capital | | $ | 1,046,287,514 | |

| Total distributable earnings | | | 218,272,913 | |

| NET ASSETS | | $ | 1,264,560,427 | |

| INVESTMENTS, AT COST | | $ | 1,076,736,227 | |

| | | | | |

| PRICING OF SHARES | | | | |

| Investor Class: | | | | |

| Net Asset Value, offering and redemption price per share | | $ | 9.50 | |

| Net Assets | | $ | 89,299,731 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 9,395,938 | |

| Class A: | | | | |

| Net Asset Value, offering and redemption price per share | | $ | 9.52 | |

| Net Assets | | $ | 7,348,589 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 772,219 | |

| Maximum offering price per share ((NAV/0.9450), based on maximum sales charge of 5.50% of the offering price) | | $ | 10.07 | |

| Class C: | | | | |

| Net Asset Value, offering and redemption price per share(a) | | $ | 8.94 | |

| Net Assets | | $ | 13,789,112 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 1,542,693 | |

| Class I: | | | | |

| Net Asset Value, offering and redemption price per share | | $ | 9.62 | |

| Net Assets | | $ | 1,154,122,995 | |

| Shares of beneficial interest outstanding (unlimited number of shares, no par value common stock authorized) | | | 119,981,495 | |

| (a) | Redemption price per share may be reduced for any applicable contingent deferred sales charge. For a description of a possible sales charge, please see the Fund's Prospectus. |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

| Consolidated Statement of Operations | For the Year Ended October 31, 2021 |

| | | | |

| INVESTMENT INCOME | | | |

| Dividends | | $ | 7,892,861 | |

| Foreign taxes withheld on dividends | | | (649,719 | ) |

| Interest and other income, net of premium amortization and accretion of discount | | | 16,433,815 | |

| Total Investment Income | | | 23,676,957 | |

| | | | | |

| EXPENSES | | | | |

| Investment advisory fees | | | 7,289,229 | |

| Investment advisory fees - subsidiary (Note 8) | | | 1,543,180 | |

| Administrative fees | | | 951,243 | |

| Transfer agency fees | | | 778,440 | |

| Distribution and service fees | | | | |

| Investor Class | | | 272,133 | |

| Class A | | | 12,877 | |

| Class C | | | 62,103 | |

| Professional fees | | | 43,546 | |

| Reports to shareholders and printing fees | | | 49,690 | |

| State registration fees | | | 80,922 | |

| Insurance fees | | | 6,683 | |

| Custody fees | | | 51,635 | |

| Trustees' fees and expenses | | | 44,159 | |

| Repayment of previously waived fees | | | | |

| Class C | | | 105 | |

| Miscellaneous expenses | | | 28,473 | |

| Total Expenses | | | 11,214,418 | |

| Less fees waived/reimbursed by investment advisor (Note 8) | | | | |

| Waiver of investment advisory fees - subsidiary | | | (1,543,180 | ) |

| Net Expenses | | | 9,671,238 | |

| Net Investment Income | | | 14,005,719 | |

| Net realized gain on investments | | | 38,200,917 | |

| Net realized gain on futures contracts | | | 18,559,386 | |

| Net realized gain on total return swap contracts | | | 190,103,040 | |

| Net realized gain on foreign currency transactions | | | 16,108 | |

| Net Realized Gain | | | 246,879,451 | |

| Net change in unrealized appreciation on investments | | | 72,253,407 | |

| Net change in unrealized appreciation on futures contracts | | | 3,713,079 | |

| Net change in unrealized appreciation on total return swap contracts | | | 65 | |

| Net change in unrealized depreciation on translation of assets and liabilities denominated in foreign currencies | | | (2,035 | ) |

| Net Change in Unrealized Appreciation | | | 75,964,516 | |

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | | 322,843,967 | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 336,849,686 | |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund

Consolidated Statements of Changes in Net Assets

| | | For the Year Ended October 31, 2021 | | | For the Year Ended October 31, 2020 | |

| OPERATIONS | | | | | | |

| Net investment income | | $ | 14,005,719 | | | $ | 2,937,921 | |

| Net realized gain/(loss) | | | 246,879,451 | | | | (53,797,734 | ) |

| Net change in unrealized appreciation | | | 75,964,516 | | | | 8,098,709 | |

| Net Increase/(Decrease) in Net Assets Resulting from Operations | | | 336,849,686 | | | | (42,761,104 | ) |

| | | | | | | | | |

| TOTAL DISTRIBUTIONS | | | | | | | | |

| From distributable earnings | | | | | | | | |

| Investor Class | | | (174,393 | ) | | | (375,275 | ) |

| Class A | | | (5,446 | ) | | | (7,077 | ) |

| Class C | | | (5,670 | ) | | | (53,444 | ) |

| Class I | | | (1,745,843 | ) | | | (4,950,473 | ) |

| Net Decrease in Net Assets from Distributions | | | (1,931,352 | ) | | | (5,386,269 | ) |

| | | | | | | | | |

| BENEFICIAL INTEREST TRANSACTIONS (NOTE 6) | | | | | | | | |

| Shares sold | | | | | | | | |

| Investor Class | | | 36,968,075 | | | | 21,811,745 | |

| Class A | | | 5,771,217 | | | | 856,402 | |

| Class C | | | 10,727,794 | | | | 336,823 | |

| Class I | | | 583,450,695 | | | | 187,684,821 | |

| Dividends reinvested | | | | | | | | |

| Investor Class | | | 167,790 | | | | 358,287 | |

| Class A | | | 2,437 | | | | 5,821 | |

| Class C | | | 4,530 | | | | 28,534 | |

| Class I | | | 1,555,689 | | | | 3,950,674 | |

| Shares redeemed, net of redemption fees | | | | | | | | |

| Investor Class | | | (27,008,696 | ) | | | (9,300,933 | ) |

| Class A | | | (1,052,463 | ) | | | (304,997 | ) |

| Class C | | | (1,304,792 | ) | | | (3,677,008 | ) |

| Class I | | | (171,560,901 | ) | | | (208,665,894 | ) |

| Net Increase/(Decrease) in Net Assets Derived from Beneficial Interest Transactions | | | 437,721,375 | | | | (6,915,725 | ) |

| | | | | | | | | |

| Net increase/(decrease) in net assets | | | 772,639,709 | | | | (55,063,098 | ) |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of year | | | 491,920,718 | | | | 546,983,816 | |

| End of year | | $ | 1,264,560,427 | | | $ | 491,920,718 | |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund – Investor Class

Consolidated Financial Highlights

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| | | For the

Year Ended

October 31,

2021 | | | For the

Year Ended

October 31,

2020 | | | For the

Year Ended

October 31,

2019 | | | For the

Year Ended

October 31,

2018(a) | | | For the

Year Ended

October 31,

2017 | |

| Net asset value, beginning of period(b) | | $ | 6.06 | | | $ | 6.68 | | | $ | 7.54 | | | $ | 7.64 | | | $ | 7.29 | |

| INCOME/(LOSS) FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | |

| Net investment income/(loss)(c) | | | 0.11 | | | | 0.02 | | | | 0.06 | | | | 0.05 | | | | (0.01 | )(d) |

| Net realized and unrealized gain/(loss) | | | 3.35 | | | | (0.58 | ) | | | (0.71 | ) | | | 0.04 | | | | 0.36 | |

| Total from investment operations | | | 3.46 | | | | (0.56 | ) | | | (0.65 | ) | | | 0.09 | | | | 0.35 | |

| DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.02 | ) | | | (0.06 | ) | | | (0.21 | ) | | | (0.19 | ) | | | (0.00 | )(e) |

| Total distributions | | | (0.02 | ) | | | (0.06 | ) | | | (0.21 | ) | | | (0.19 | ) | | | (0.00 | )(e) |

| REDEMPTION FEES ADDED TO PAID-IN CAPITAL (NOTE 6) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) | | | 0.00 | (e) |

| Net increase/(decrease) in net asset value | | | 3.44 | | | | (0.62 | ) | | | (0.86 | ) | | | (0.10 | ) | | | 0.35 | |

| Net asset value, end of year | | $ | 9.50 | | | $ | 6.06 | | | $ | 6.68 | | | $ | 7.54 | | | $ | 7.64 | |

| TOTAL RETURN(f) | | | 57.25 | % | | | (8.44 | )% | | | (8.71 | )% | | | 1.23 | % | | | 4.85 | % |

| RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 89,300 | | | $ | 49,060 | | | $ | 39,226 | | | $ | 48,728 | | | $ | 47,845 | |

| Ratio of expenses to average net assets excluding fee waivers and reimbursements | | | 1.37 | %(g) | | | 1.40 | %(g) | | | 1.39 | %(g) | | | 1.40 | %(g) | | | 1.38 | % |

| Ratio of expenses to average net assets including fee waivers and reimbursements | | | 1.37 | % | | | 1.40 | % | | | 1.39 | % | | | 1.40 | % | | | 1.38 | % |

| Ratio of net investment income/(loss) to average net assets | | | 1.36 | % | | | 0.40 | % | | | 0.82 | % | | | 0.66 | % | | | (0.10 | )% |

| Portfolio turnover rate(h) | | | 54 | % | | | 98 | % | | | 81 | % | | | 42 | % | | | 66 | % |

| (a) | Prior to December 1, 2017, Investor Class was known as Class A. |

| (b) | Per share amounts and ratios to average net assets include income and expenses of the CoreCommodity Management Cayman Commodity Fund Ltd. (wholly-owned subsidiary). |

| (c) | Calculated using the average shares method. |

| (d) | The per share amount does not correspond to activity reflected in the Statement of Operations due to class specific expenses during the period. |

| (e) | Less than $0.005 or ($0.005) per share. |

| (f) | Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (g) | The ratio of operating expenses excluding fee waiver/reimbursements to average net assets is calculated excluding the waived Subsidiary management fee (see Note 8 for additional detail). The ratio inclusive of that fee would be for the years ended October 31, 2021, October 31, 2020, October 31, 2019 and October 31, 2018, respectively, 1.55%, 1.58%, 1.54% and 1.56%. |

| (h) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

ALPS | CoreCommodity Management

CompleteCommodities® Strategy Fund – Class A

Consolidated Financial Highlights

Selected data for a share of beneficial interest outstanding throughout the periods indicated:

| | | For the

Year Ended

October 31,

2021 | | | For the Year Ended October 31, 2020 | | | For the Year Ended October 31, 2019 | | | For the Period June 12, 2018 (Commencement of Operations) to October 31, 2018 | |

| Net asset value, beginning of period(a) | | $ | 6.07 | | | $ | 6.68 | | | $ | 7.54 | | | $ | 8.16 | |

| | | | | | | | | | | | | | | | | |

| INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | |