As filed with the Securities and Exchange Commission on March 9, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-8352

LKCM Funds

(Exact name of registrant as specified in charter)

c/o Luther King Capital Management Corporation

301 Commerce Street, Suite 1600

Fort Worth, TX 76102

(Address of principal executive offices) (Zip code)

K&L Gates LLP

1601 K Street, NW

Washington, DC 20006

(Name and address of agent for service)

1-800-688-LKCM and 1-800-423-6369

Registrant’s telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2017

| Item 1. | Reports to Stockholders. |

LKCM

FUNDS

LKCM Small Cap Equity Fund

LKCM Small-Mid Cap Equity Fund

LKCM Equity Fund

LKCM Balanced Fund

LKCM Fixed Income Fund

Annual Report

December 31, 2017

Dear Fellow Shareholders:

We report the following performance information for the LKCM Funds for the indicated periods ended December 31, 2017:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Funds | | Inception

Dates | | | NAV @

12/31/17 | | | Net

Expense

Ratio*, ** | | | Gross

Expense

Ratio** | | | One Year

Total

Return

Ended

12/31/17 | | | Five Year

Average

Annualized

Return

Ended

12/31/17 | | | Ten Year

Average

Annualized

Return

Ended

12/31/17 | | | Avg.

Annual

Total

Return

Since

Incept. | |

LKCM Equity Fund - | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 1/3/96 | | | $ | 26.02 | | | | 0.80% | | | | 0.98% | | | | 21.69% | | | | 12.76% | | | | 8.31% | | | | 8.65% | |

S&P 500® Index(1) | | | | | | | | | | | | | | | | | | | 21.83% | | | | 15.79% | | | | 8.50% | | | | 8.90% | |

LKCM Small Cap Equity Fund - | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 7/14/94 | | | $ | 18.44 | | | | 1.00% | | | | 1.05% | | | | 17.04% | | | | 9.59% | | | | 6.88% | | | | 10.47% | |

Russell 2000® Index(2) | | | | | | | | | | | | | | | | | | | 14.65% | | | | 14.12% | | | | 8.71% | | | | 9.60% | |

LKCM Small Cap Equity Fund - | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Adviser Class | | | 6/5/03 | | | $ | 17.13 | | | | 1.25% | | | | 1.30% | | | | 16.70% | | | | 9.31% | | | | 6.61% | | | | 9.27% | |

Russell 2000® Index(2) | | | | | | | | | | | | | | | | | | | 14.65% | | | | 14.12% | | | | 8.71% | | | | 10.13% | |

LKCM Small-Mid Cap Equity Fund - | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 5/2/11 | | | $ | 10.60 | | | | 1.02% | | | | 1.25% | | | | 24.13% | | | | 9.67% | | | | N/A | | | | 6.64% | |

Russell 2500® Index(3) | | | | | | | | | | | | | | | | | | | 16.81% | | | | 14.33% | | | | N/A | | | | 11.00% | |

LKCM Balanced Fund | | | 12/30/97 | | | $ | 22.18 | | | | 0.81% | | | | 1.04% | | | | 12.88% | | | | 10.28% | | | | 7.47% | | | | 6.64% | |

S&P 500® Index(1) | | | | | | | | | | | | | | | | | | | 21.83% | | | | 15.79% | | | | 8.50% | | | | 7.19% | |

Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index(4) | | | | | | | | | | | | | | | | | | | 2.14% | | | | 1.50% | | | | 3.32% | | | | 4.54% | |

LKCM Fixed Income Fund | | | 12/30/97 | | | $ | 10.68 | | | | 0.51% | | | | 0.79% | | | | 2.15% | | | | 1.49% | | | | 3.63% | | | | 4.34% | |

Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index(4) | | | | | | | | | | | | | | | | | | | 2.14% | | | | 1.50% | | | | 3.32% | | | | 4.54% | |

Performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. The Funds impose a 1.00% redemption fee on shares held less than 30 days. If reflected, the fee would reduce performance shown.

| * | Luther King Capital Management Corporation, the Funds’ investment adviser, has contractually agreed to waive all or a portion of its management fee and/or reimburse expenses of each Fund to maintain the expense ratios designated in the Funds’ current prospectus through May 1, 2018. This expense limitation excludes interest, taxes, brokerage commissions, indirect fees and expenses related to investments in other investment companies, including money market funds, and extraordinary expenses. Investment performance reflects fee waivers, if any, in effect during the relevant period. In the absence of such waivers, total return would be reduced. Investment performance is based upon the net expense ratio. LKCM waived management fees and/or reimbursed expenses for each Fund during the fiscal year ended December 31, 2017. |

| ** | Expense ratios above are as of May 1, 2017, as reported in the Funds’ current prospectus. Expense ratios reported for other periods in the financial highlights of this report may differ. |

| (1) | The S&P 500® Index is an unmanaged capitalization-weighted index of 500 selected stocks that is generally considered representative of the performance of large capitalization companies in the U.S. stock market. |

| (2) | The Russell 2000® Index is an unmanaged index which measures the performance of the 2,000 smallest companies in the Russell 3000® Index. |

| (3) | The Russell 2500® Index is an unmanaged index which measures the performance of the 2,500 smallest companies in the Russell 3000® Index. |

| (4) | The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index is an unmanaged market value weighted index measuring both the principal price changes of, and income provided by, the underlying universe of securities that comprise the index. Securities included in the index must meet the following criteria: fixed as opposed to variable rate; remaining maturity of one to ten years; minimum outstanding par value of $250 million; rated investment grade or higher by Moody’s Investors Service or equivalent; must be dollar denominated and non-convertible; and must be publicly issued. |

Note: The indices defined above are not available for direct investment and the index performance therefore does not include fees, expenses or taxes.

2017 Review

A year ago investors were attempting to understand the implications of President-elect Donald Trump’s agenda of tax reform, lighter regulation, and infrastructure spending to spur economic growth and create jobs. Initial investor optimism eroded in March as the failure to repeal and replace Obamacare, a Republican-controlled Congress’ multi-year objective, cast doubt on the potential for the White House to accomplish other legislative agenda items, chiefly tax reform. Despite the legislative set back, three interest rate hikes by the Federal Reserve Board, and trade policy concerns, healthy corporate profit growth following two years of stagnation propelled the equity market to a record high in 2017. The S&P 500® Index rose 21.83% for the year ended December 31, 2017, driven by higher earnings growth and expanded earnings multiples. The market advance was broad-based and persistent. Nine of the eleven equity market sectors recorded a positive return for the year, led by the Information Technology sector. In addition, the S&P 500® Index rose during each month of the year—a first for the index. We believe the strong equity market performance reflected the continued improvement of economic data, particularly related to manufacturing, housing, and jobs.

2

Despite significant strength in broad equity market indices over the past year, we believe equity market internals were less impressive. First, the S&P 500® Index, which is market-capitalization weighted, outperformed the S&P 500® Equal Weight Index an equal-weighted version of the S&P 500® Index, by 2.9% during the year. We believe this market characteristic is often associated with undistinguished market performance. Second, the performance of small capitalization stocks, as measured by the Russell 2000® Index, trailed the S&P 500® Index, which is generally comprised of large capitalization stocks, by approximately 7.2% for the year. We believe the performance of the equity market in 2017 was also remarkable for its lack of daily volatility. There were only seven trading days in 2017 when the S&P 500® Index changed by greater than 1% but less than 2%. Moreover, the last year in which the equity markets, as measured by the S&P 500® Index, recorded no daily moves greater than 2% was 2005.

Turning to interest rates, after a roller-coaster year the yield on the 10-Year Treasury closed 2017 at 2.41%, a mere 0.04% less than where the yield began the year. The peak in yield on the 10-Year Treasury during 2017 of 2.63% occurred in March, two days prior to the third interest rate increase by the Federal Reserve Board for this tightening cycle. It appeared that jobs data was improving and investors began discounting the potential for rising inflation and further interest rate hikes by the Federal Reserve Board. The peak in the 10-Year Treasury yield coincided with investor concern regarding the White House agenda following the failure of Congress and the Administration to revamp health care regulation. In addition, geopolitical tension with regard to Syria and North Korea was rising and the U.S. dollar continued to weaken. On the heels of the 0.25% interest rate increase by the Federal Reserve Board in March, the Federal Reserve Board raised rates an additional 0.25% in June and December. The short end of the yield curve rose dramatically, partially in reaction to an increased pace of interest rate hikes. The yield on the 2-Year Treasury reached a nine-year high by late October and finished the year yielding 1.89%. The result was a dramatic flattening of the yield curve, or the difference in yields between the 2-Year Treasury and the 10-Year Treasury. In our view, a flattening of the yield curve has historically been viewed as a harbinger of slowing economic growth and rising recession risk. We believe that this traditional reading of a flattening yield curve is less applicable in today’s environment where long yields are weighed down by ultra-low global bond yields, particularly in the Eurozone. Finally, due to the sharp rise in the 2-Year Treasury yield during 2017 we believe it is competitive with the dividend yield on the S&P 500® Index for the first time since 2008.

In our view, the current expansion is likely to continue as fiscal stimulus in the form of lower tax rates and the probability of infrastructure spending should propel economic growth into the second half of 2019. We believe if the economy were to post two consecutive quarters of economic contraction, it would likely be the result of overly tight monetary policy or the ever possible exogenous shock to the economy caused by a geopolitical event. We believe such risks are unlikely to occur, but the possibility remains. We believe it is much more likely that the Federal Reserve Board accelerates its pace of interest rate hikes in 2018 in response to rising inflation.

2018 Outlook

The prior year ended with passage of the most sweeping tax reform legislation in over 30 years. We believe the permanent reduction in the corporate tax rate to 21% from the highest 35% bracket will have significant, though uneven, implications for corporations. We are mindful of a corporation’s effective tax rate, which represents the amount corporations actually pay in taxes as a share of their pre-tax income. Historically, the effective tax rate could be materially less than the highest statutory tax rate of 35%. This paradox was especially true of multinational companies owing to the peculiar nature of our nation’s approach to the taxation of foreign earnings of domestic companies.

We believe the reduction in the corporate tax rate is a clear near-term tailwind for corporate earnings and we have upgraded our outlook for the equity market in 2018. We also believe it would be unusual for the equity market to decline during a year in which we anticipate corporate profits to rise at a mid-teen growth rate. While optimistic about the prospects for economic growth and the equity market, we believe the timing of the tax cuts paradoxically increases the risk of shortening the current business cycle. In the past, Congress has used tax cuts to revive economic growth following recessions. The recent tax cut, in contrast, arrives in year nine of economic growth and amidst what we believe are clear signs of strengthening manufacturing, better housing data, tightening labor conditions, rising energy prices, and a falling U.S. dollar. We believe real economic growth should accelerate from the 2% level recorded in recent years to closer to 3% for 2018. Such a move could ignite inflationary pressures thereby prompting the Federal Reserve Board to quicken its pace of interest rate hikes and bring about the familiar close of a business cycle through an overtightening of monetary policy. We believe inflationary readings will be key data to monitor in 2018 for signs the Federal Reserve may accelerate monetary tightening.

We anticipate that Gross Domestic Product, or GDP, growth will accelerate in 2018 driven in part by higher personal consumption, which represents almost 70% of GDP. We believe most workers should see an increase in their payroll check this year because of the new tax legislation. This incremental consumer income is arriving at a time when the personal savings rate of 2.9% of personal disposable income is near a decade low level. Americans were saving an average of 6.0% of personal disposable income as recently as the fourth quarter of 2015. We believe real GDP growth could potentially rise to 3% for 2018 and corporate profits could grow between 15% and 18% year-over-year, which would indicate the economy is set to receive a near-term dose of fiscal stimulus. We believe it would be unusual for equity prices to perform poorly against this economic backdrop although we would not be surprised if the equity market retraced 5% to 10%, or greater, at some point within the next year as we believe the equity market is historically overdue for a correction.

LKCM Equity Fund

The LKCM Equity Fund posted a return of 21.69% for the year ended December 31, 2017 compared to a return of 21.83% for the S&P 500® Index, the Fund’s benchmark. The Fund generated solid performance results from stock selection in the Industrials, Healthcare and Financials sectors relative to the benchmark, although stock selection in the Information Technology and Energy sectors underperformed relative to the benchmark. The Fund benefited from an underweight position in the Telecommunications, Utilities and Real Estate sectors

3

relative to the benchmark, which was offset by the Fund’s overweight position in the Energy and Information Technology sectors. We remain committed to our investment strategy and stock selection process for the Fund, and we believe the Fund is well positioned for 2018 with a portfolio of companies that we believe are high quality, have solid balance sheets, are reasonably valued, and otherwise meet our stringent investment criteria.

LKCM Small Cap Equity Fund

The LKCM Small Cap Equity Fund—Institutional Class returned 17.04% for the year ended December 31, 2017 and outperformed its benchmark, the Russell 2000® Index, which returned 14.65% for the year. For 2017, stock selection was responsible for the vast majority of the Fund’s relative outperformance although sector allocation decisions for the Fund were also positive and contributed to the Fund’s relative performance. Stock selection in the Consumer Discretionary, Industrials and Materials sectors was strong and contributed significantly to the Fund’s outperformance relative to the benchmark. Stock selection in the Healthcare sector was the biggest detractor to the Fund’s relative performance. The Fund’s overweight position in the Energy sector was also a drag on the Fund’s relative performance, especially during the first part of the year. The Fund also benefited during the year from a tilt toward growth companies and underweight positions in those sectors more sensitive to interest rates. The Fund further benefited during the year from five portfolio companies being acquired and four portfolio companies graduating out of our small cap investment strategy due to market appreciation. We continue to remain confident in our strategy of investing in companies that we believe are high quality and competitively advantaged and otherwise meet our stringent investment criteria.

LKCM Balanced Fund

The LKCM Balanced Fund advanced 12.88% for the year ended December 31, 2017 versus the 21.83% return for the S&P 500® Index and the 2.14% return for the Bloomberg Barclays Intermediate Government/Credit Bond Index. While generating significant absolute returns, the Fund’s equity portfolio lagged the performance of the S&P 500® Index. The Fund benefited from strong stock selection in the Healthcare and Financials sectors relative to the benchmark, while stock selection in the Consumer Discretionary and Information Technology sectors detracted from the Fund’s relative performance. We believe the Fund’s equity portfolio is well-positioned for a gradual lift in interest rates, with relatively low exposure to interest rate sensitive sectors like Real Estate and Utilities. The Fund’s fixed income portfolio slightly outperformed the Bloomberg Barclays Intermediate Government/Credit Bond Index during the year. The Fund’s fixed income portfolio remains focused on high quality intermediate maturity bonds, which serves the dual objective of generating income and moderating the overall risk level of the Fund’s total portfolio.

LKCM Fixed Income Fund

The LKCM Fixed Income Fund advanced 2.15% for the year ended December 31, 2017 compared to 2.14% for the Fund’s benchmark, the Bloomberg Barclays Intermediate Government/Credit Bond Index. The Fund’s overweight position in corporate bonds relative to the benchmark, specifically BBB rated corporate bonds and those in the Healthcare, Capital Goods and Information Technology sectors, were additive to the Fund’s relative performance as credit spreads tightened. Floating rate and U.S. Government agency step-up fixed income securities were also additive to the Fund’s relative performance as short-term interest rates rose and the yield curve flattened as the Federal Reserve Board tightened monetary policy. The Fund’s underweight position in the U.S. Government sector also benefitted the Fund’s relative performance as U.S. Treasuries and U.S. Government agency fixed income securities underperformed their lower quality counterparts in the corporate bond sector. The Fund’s defensive duration posture of approximately 3.2 years, versus 4.0 years for the benchmark, detracted from the Fund’s relative performance as the yield curve flattened and longer duration issues outperformed their shorter duration counterparts. The Fund remains largely focused on short-to-intermediate investment grade corporate bonds with strong underlying credit fundamentals in an effort to mitigate interest rate and credit risk as expectations for inflation and growth increase.

LKCM Small-Mid Cap Equity Fund

The LKCM Small-Mid Cap Equity Fund returned 24.13% for the year ended December 31, 2017 and outperformed its benchmark, the Russell 2500® Index, which returned 16.81% for the year. For 2017, stock selection was responsible for the vast majority of the Fund’s relative outperformance although sector allocation decisions for the Fund were also positive and contributed to the Fund’s relative performance. Stock selection in the Financials, Consumer Discretionary, Healthcare, Information Technology and Materials sectors was strong and contributed significantly to the Fund’s outperformance relative to the benchmark. The Fund’s overweight position in the Energy sector was a drag on the Fund’s relative performance, especially during the first part of the year. The Fund also benefited during the year from a tilt toward growth companies and underweight positions in those sectors more sensitive to interest rates. The Fund further benefited during the year from three portfolio companies being acquired and three portfolio companies graduating out of our small-mid cap investment strategy due to market appreciation. We continue to remain confident in our strategy of investing in companies that we believe are high quality and competitively advantaged and otherwise meet our stringent investment criteria

J. Luther King, Jr., CFA, CIC

February 3, 2018

4

The information provided herein represents the opinion of J. Luther King, Jr., CFA, CIC and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice.

Please refer to the Schedule of Investments found on pages 16-28 of the report for more information on Fund holdings. Fund holdings and sector allocations are subject to change and are not recommendations to buy or sell any securities.

Mutual fund investing involves risk. Principal loss is possible. Past performance is not a guarantee of future results. Small and medium capitalization funds typically carry additional risks, since smaller companies generally have a higher risk of failure, and, historically, their stocks have experienced a greater degree of market volatility than stocks on average. Investments in debt securities typically decrease in value when interest rates rise. This risk is greater for longer-term debt securities. Investments in mortgage backed securities include additional risks that investors should be aware of such as credit risk, prepayment risk, possible illiquidity and default, as well as increased susceptibility to adverse economic developments. These risks are discussed in the Funds’ summary and statutory prospectuses.

Earnings growth is not a measure of future performance.

Duration is a commonly used measure of the potential volatility of the price of a debt security, or the aggregate market value of a portfolio of debt securities, prior to maturity. Securities with a longer duration generally have more volatile prices than securities of comparable quality with a shorter duration.

Spread is the percentage point difference between yields of various classes of bonds compared to treasury bonds.

BBB refers to bond ratings. Bond ratings are grades given to bonds that indicate their credit quality as determined by private independent rating services such as Standard & Poor’s, Moody’s and Fitch. These firms evaluate a bond issuer’s financial strength, or its ability to pay a bond’s principal and interest in a timely fashion. Ratings are expressed as letters ranging from ‘AAA’, which is the highest grade, to ‘D’, which is the lowest grade.

Dividend yield is a dividend expressed as a percentage of current share price.

The S&P 500® Equal Weight Index is the equal-weight version of the S&P 500® Index. It has the same constituents as the capitalization weighted S&P 500® Index, but each company is allocated a fixed weight of 0.2 percent quarterly.

Investment grade is a level of credit rating regarded as carrying a relatively low level of risk to investors.

Must be preceded or accompanied by a prospectus.

Quasar Distributors, LLC, distributor.

5

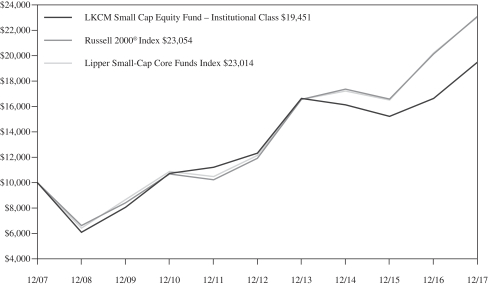

PERFORMANCE:

The following information illustrates the historical performance of the LKCM Small Cap Equity Fund as of December 31, 2017 compared to the Fund’s representative benchmark and peer group indices.

Performance data quoted represents past performance; past performance does not guarantee future results. The graph and table reflect the reinvestment of dividends and other distributions, if any, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. Returns would have been lower if LKCM had not waived a portion of its management fee and/or reimbursed certain expenses of the Fund. Please see Note B to the Notes to the Financial Statements for specific information regarding management fee waiver and/or expense reimbursement arrangements for the Fund.

An index is an unmanaged portfolio and does not trade or incur any expenses. The Lipper Small-Cap Core Funds Index, however, does reflect the fees and expenses borne by the Funds included in that index. One can not invest in an unmanaged index.

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Past

10 Years(1) | | | Since

Inception(1)(2) | |

LKCM Small Cap Equity Fund – Institutional Class | | | 17.04% | | | | 9.59% | | | | 6.88% | | | | 10.47% | |

Russell 2000® Index | | | 14.65% | | | | 14.12% | | | | 8.71% | | | | 9.60% | |

Lipper Small-Cap Core Funds Index | | | 13.95% | | | | 13.64% | | | | 8.69% | | | | 10.41% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM SMALL CAP EQUITY FUND – INSTITUTIONAL CLASS

(for the ten years ended December 31, 2017)

The Russell 2000® Index is an unmanaged index consisting of the 2,000 smallest companies in the Russell 3000® Index.

The Lipper Small-Cap Core Funds Index is an unmanaged index generally considered representative of small cap core mutual funds tracked by Lipper, Inc.

6

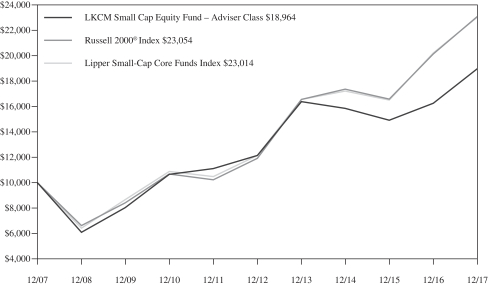

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Past

10 Years(1) | | | Since

Inception(1)(2) | |

LKCM Small Cap Equity Fund – Adviser Class | | | 16.70% | | | | 9.31% | | | | 6.61% | | | | 9.27% | |

Russell 2000® Index | | | 14.65% | | | | 14.12% | | | | 8.71% | | | | 10.13% | |

Lipper Small-Cap Core Funds Index | | | 13.95% | | | | 13.64% | | | | 8.69% | | | | 10.49% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM SMALL CAP EQUITY FUND – ADVISER CLASS

(for the ten years ended December 31, 2017)

The Russell 2000® Index is an unmanaged index consisting of the 2,000 smallest companies in the Russell 3000® Index.

The Lipper Small-Cap Core Funds Index is an unmanaged index generally considered representative of small cap core mutual funds tracked by Lipper, Inc.

7

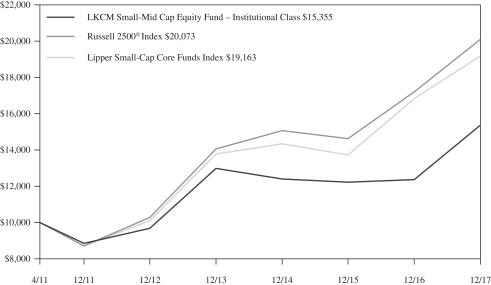

PERFORMANCE:

The following information illustrates the historical performance of the LKCM Small-Mid Cap Equity Fund as of December 31, 2017 compared to the Fund’s benchmark and peer group indices.

Performance data quoted represents past performance; past performance does not guarantee future results. The graph and table reflect the reinvestment of dividends and other distributions, if any, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. Returns would have been lower if LKCM had not waived a portion of its management fee and/or reimbursed certain expenses of the Fund. Please see Note B to the Notes to the Financial Statements for specific information regarding management fee waiver and/or expense reimbursement arrangements for the Fund.

An index is an unmanaged portfolio and does not trade or incur any expenses. The Lipper Small-Cap Core Funds Index, however, does reflect the fees and expenses borne by the Funds included in that index. One can not invest in an unmanaged index.

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Since

Inception(1)(2) | |

LKCM Small-Mid Cap Equity Fund – Institutional Class | | | 24.13% | | | | 9.67% | | | | 6.64% | |

Russell 2500® Index | | | 16.81% | | | | 14.33% | | | | 11.00% | |

Lipper Small-Cap Core Funds Index | | | 13.95% | | | | 13.64% | | | | 10.24% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM SMALL-MID CAP EQUITY FUND – INSTITUTIONAL CLASS

(for the period from May 2, 2011 to December 31, 2017)

The Russell 2500® Index is an unmanaged index consisting of the 2,500 smallest companies in the Russell 3000® Index.

The Lipper Small-Cap Core Funds Index is an unmanaged index generally considered representative of small cap core mutual funds tracked by Lipper, Inc.

8

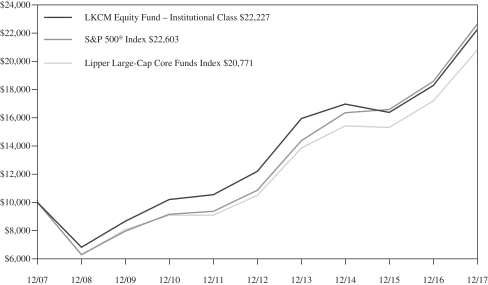

PERFORMANCE:

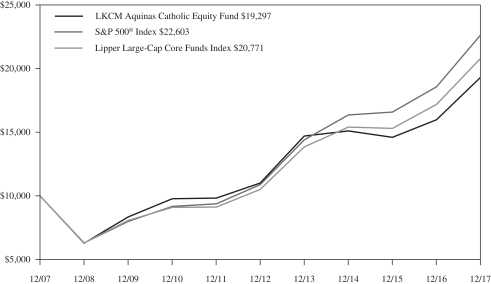

The following information illustrates the historical performance of the LKCM Equity Fund as of December 31, 2017 compared to the Fund’s benchmark and peer group indices.

Performance data quoted represents past performance; past performance does not guarantee future results. The graph and table reflect the reinvestment of dividends and other distributions, if any, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. Returns would have been lower if LKCM had not waived a portion of its management fee and/or reimbursed certain expenses of the Fund. Please see Note B to the Notes to the Financial Statements for specific information regarding management fee waiver and/or expense reimbursement arrangements for the Fund.

An index is an unmanaged portfolio and does not trade or incur any expenses. The Lipper Large-Cap Core Funds Index, however, does reflect the fees and expenses borne by the Funds included in that index. One can not invest in an unmanaged index.

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Past

10 Years(1) | | | Since

Inception(1)(2) | |

LKCM Equity Fund – Institutional Class | | | 21.69% | | | | 12.76% | | | | 8.31% | | | | 8.65% | |

S&P 500® Index | | | 21.83% | | | | 15.79% | | | | 8.50% | | | | 8.90% | |

Lipper Large-Cap Core Funds Index | | | 20.90% | | | | 14.63% | | | | 7.58% | | | | 7.93% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM EQUITY FUND – INSTITUTIONAL CLASS

(for the ten years ended December 31, 2017)

The S&P 500® Index is an unmanaged capitalization-weighted index of 500 selected stocks that is generally considered representative of the performance of large capitalization companies in the U.S. stock market.

The Lipper Large-Cap Core Funds Index is an unmanaged index generally considered representative of large cap core mutual funds tracked by Lipper, Inc.

9

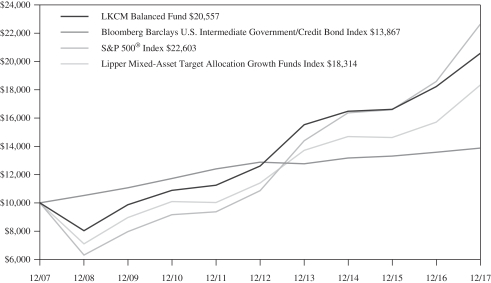

PERFORMANCE:

The following information illustrates the historical performance of the LKCM Balanced Fund as of December 31, 2017 compared to the Fund’s benchmark and peer group indices.

Performance data quoted represents past performance; past performance does not guarantee future results. The graph and table reflect the reinvestment of dividends and other distributions, if any, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. Returns would have been lower if LKCM had not waived a portion of its management fee and/or reimbursed certain expenses of the Fund. Please see Note B to the Notes to the Financial Statements for specific information regarding management fee waiver and/or expense reimbursement arrangements for the Fund.

An index is an unmanaged portfolio and does not trade or incur any expenses. The Lipper Mixed-Asset Target Allocation Growth Funds Index, however, does reflect the fees and expenses borne by the Funds included in that index. One can not invest in an unmanaged index.

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Past

10 Years(1) | | | Since

Inception(1)(2) | |

LKCM Balanced Fund | | | 12.88% | | | | 10.28% | | | | 7.47% | | | | 6.64% | |

Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index | | | 2.14% | | | | 1.50% | | | | 3.32% | | | | 4.54% | |

S&P 500® Index | | | 21.83% | | | | 15.79% | | | | 8.50% | | | | 7.19% | |

Lipper Mixed-Asset Target Allocation Growth Funds Index | | | 16.67% | | | | 9.96% | | | | 6.24% | | | | 6.44% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM BALANCED FUND

(for the ten years ended December 31, 2017)

The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index is an unmanaged market value weighted index measuring both the principal price changes of, and income provided by, the underlying universe of securities that comprise the index. Securities included in the index must meet the following criteria; fixed as opposed to variable rate; remaining maturity of one to ten years; minimum outstanding par value of $250 million; rated investment grade or higher by Moody’s Investors Service or equivalent; must be dollar denominated and non-convertible; and must be publicly issued.

10

The Lipper Mixed-Asset Target Allocation Growth Funds Index is an unmanaged index generally considered representative of mutual funds tracked by Lipper, Inc. that, by portfolio practice, maintain a mix of between 60%-80% equity securities, with the remainder invested in bonds, cash and cash equivalents.

The S&P 500® Index is an unmanaged capitalization-weighted index of 500 selected stocks that is generally considered representative of the performance of large capitalization companies in the U.S. stock market.

11

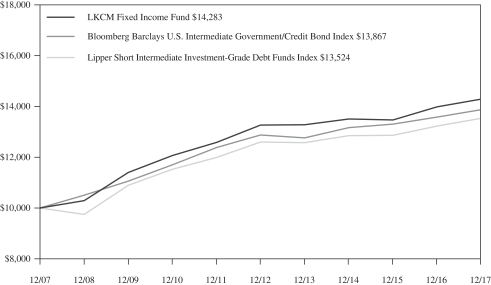

PERFORMANCE:

The following information illustrates the historical performance of the LKCM Fixed Income Fund as of December 31, 2017 compared to the Fund’s benchmark and peer group indices.

Performance data quoted represents past performance; past performance does not guarantee future results. The graph and table reflect the reinvestment of dividends and other distributions, if any, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-800-688-LKCM. Returns would have been lower if LKCM had not waived a portion of its management fee and/or reimbursed certain expenses of the Fund. Please see Note B to the Notes to the Financial Statements for specific information regarding management fee waiver and/or expense reimbursement arrangements for the Fund.

An index is an unmanaged portfolio and does not trade or incur any expenses. The Lipper Short Intermediate Investment-Grade Debt Funds Index, however, does reflect the fees and expenses borne by the Funds included in that index. One can not invest in an unmanaged index.

AVERAGE ANNUAL TOTAL RETURN (Periods Ended December 31, 2017)

| | | | | | | | | | | | | | | | |

| | | Past

1 Year | | | Past

5 Years(1) | | | Past

10 Years(1) | | | Since

Inception(1)(2) | |

LKCM Fixed Income Fund | | | 2.15% | | | | 1.49% | | | | 3.63% | | | | 4.34% | |

Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index | | | 2.14% | | | | 1.50% | | | | 3.32% | | | | 4.54% | |

Lipper Short Intermediate Investment-Grade Debt Funds Index | | | 2.25% | | | | 1.44% | | | | 3.06% | | | | 4.01% | |

A HYPOTHETICAL $10,000 INVESTMENT IN LKCM FIXED INCOME FUND

(for the ten years ended December 31, 2017)

The Bloomberg Barclays U.S. Intermediate Government/Credit Bond Index is an unmanaged market value weighted index measuring both the principal price changes of, and income provided by, the underlying universe of securities that comprise the index. Securities included in the index must meet the following criteria: fixed as opposed to variable rate; remaining maturity of one to ten years; minimum outstanding par value of $250 million; rated investment grade or higher by Moody’s Investors Service or equivalent; must be dollar denominated and non-convertible; and must be publicly issued.

The Lipper Short Intermediate Investment-Grade Debt Funds Index is an unmanaged index generally considered representative of short intermediate investment grade mutual funds tracked by Lipper, Inc.

12

LKCM Funds Expense Example — December 31, 2017

As a shareholder of the Funds, you incur two types of costs: (1) transaction costs, including redemption fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (7/1/17-12/31/17).

ACTUAL EXPENSES

The first line of the tables below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. Although the Funds charge no sales load, you will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. If you request that a redemption be made by wire transfer, currently a $15.00 fee is charged by the Funds’ transfer agent. You will be charged a redemption fee equal to 1.00% of the net amount of the redemption if you redeem your shares of the LKCM Small Cap Equity, Small-Mid Cap Equity, Equity, Balanced and Fixed Income Funds within 30 days of purchase, unless otherwise determined by the Funds in their discretion. To the extent the Funds invest in shares of other investment companies as part of their investment strategies, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Funds invest in addition to the expenses of the Funds. Actual expenses of the underlying funds are expected to vary among the various underlying funds. These expenses are not included in the example below. The example below includes management fees, registration fees and other expenses. However, the example below does not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under generally accepted accounting principles.

HYPOTHETICAL EXAMPLES FOR COMPARISON PURPOSES

The second line of the tables below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds’ actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactions costs were included, your costs would have been higher.

| | | | | | | | | | | | |

| | | LKCM Small Cap Equity Fund – Institutional Class | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,093.10 | | | $ | 5.28 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,020.16 | | | $ | 5.09 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 1.00%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| | | | | | | | | | | | |

| | | LKCM Small Cap Equity Fund – Adviser Class | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,090.80 | | | $ | 6.59 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,018.90 | | | $ | 6.36 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| | | | | | | | | | | | |

| | | LKCM Small-Mid Cap Equity Fund | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,151.00 | | | $ | 5.42 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,020.16 | | | $ | 5.09 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 1.00%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

13

| | | | | | | | | | | | |

| | | LKCM Equity Fund | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,103.20 | | | $ | 4.24 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,021.17 | | | $ | 4.08 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 0.80%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| | | | | | | | | | | | |

| | | LKCM Balanced Fund | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,063.90 | | | $ | 4.16 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,021.17 | | | $ | 4.08 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 0.80%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| | | | | | | | | | | | |

| | | LKCM Fixed Income Fund | |

| | | Beginning

Account Value

7/1/17 | | | Ending

Account Value

12/31/17 | | | Expenses Paid

During Period*

7/1/17–12/31/17 | |

Actual | | $ | 1,000.00 | | | $ | 1,005.40 | | | $ | 2.53 | |

Hypothetical (5% return before expense) | | $ | 1,000.00 | | | $ | 1,022.68 | | | $ | 2.55 | |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 0.50%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

14

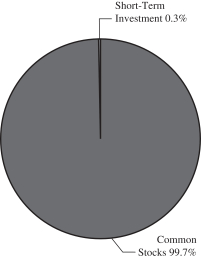

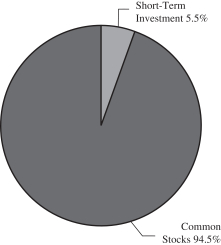

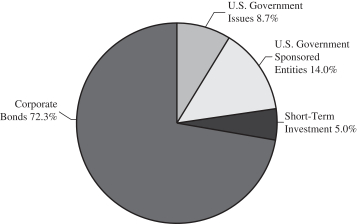

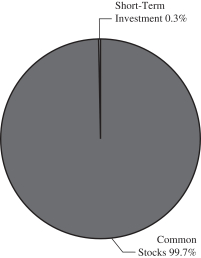

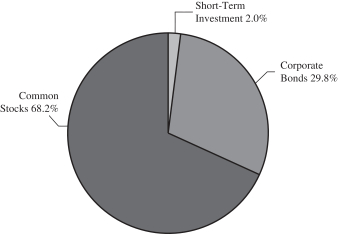

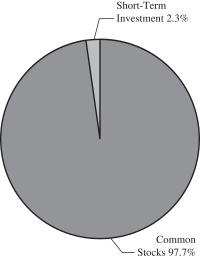

ALLOCATION OF PORTFOLIO HOLDINGS — LKCM Funds — December 31, 2017

Percentages represent market value as a percentage of total investments.

LKCM Small Cap Equity Fund

LKCM Equity Fund

LKCM Fixed Income Fund

LKCM Small-Mid Cap Equity Fund

LKCM Balanced Fund

15

|

| LKCM SMALL CAP EQUITY FUND |

| SCHEDULEOF INVESTMENTS |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS - 99.9% | | Shares | | | Value | |

Aerospace & Defense - 2.8% | |

Hexcel Corporation | | | 26,855 | | | $ | 1,660,982 | |

Mercury Systems, Inc. (a) | | | 76,950 | | | | 3,951,382 | |

| | | | | | | | |

| | | | | | | 5,612,364 | |

| | | | | | | | |

Banks - 10.8% | | | | | | | | |

BancorpSouth Bank | | | 104,014 | | | | 3,271,240 | |

Cadence BanCorporation (a) | | | 103,310 | | | | 2,801,767 | |

CBTX, Inc. | | | 51,540 | | | | 1,528,676 | |

Glacier Bancorp, Inc. | | | 56,265 | | | | 2,216,278 | |

Green Bancorp, Inc. (a) | | | 84,060 | | | | 1,706,418 | |

Hanmi Financial Corporation | | | 82,490 | | | | 2,503,572 | |

LegacyTexas Financial Group, Inc. | | | 50,575 | | | | 2,134,771 | |

Pinnacle Financial Partners, Inc. | | | 49,125 | | | | 3,256,988 | |

Seacoast Banking Corporation of Florida (a) | | | 91,935 | | | | 2,317,681 | |

| | | | | | | | |

| | | | | | | 21,737,391 | |

| | | | | | | | |

Biotechnology - 3.6% | | | | | | | | |

Charles River Laboratories International, Inc. (a) | | | 36,135 | | | | 3,954,976 | |

Neogen Corporation (a) | | | 39,353 | | | | 3,235,210 | |

| | | | | | | | |

| | | | | | | 7,190,186 | |

| | | | | | | | |

Building Products - 5.1% | | | | | | | | |

American Woodmark Corporation (a) | | | 17,140 | | | | 2,232,485 | |

Builders FirstSource, Inc. (a) | | | 165,195 | | | | 3,599,599 | |

CSW Industrials, Inc. (a) | | | 35,200 | | | | 1,617,440 | |

PGT, Inc. (a) | | | 165,056 | | | | 2,781,194 | |

| | | | | | | | |

| | | | | | | 10,230,718 | |

| | | | | | | | |

Capital Markets - 1.2% | | | | | | | | |

BGC Partners Inc - Class A | | | 155,585 | | | | 2,350,889 | |

| | | | | | | | |

Chemicals - 3.2% | | | | | | | | |

Ferro Corporation (a) | | | 103,545 | | | | 2,442,627 | |

Ferroglobe PLC (a) (b) | | | 214,125 | | | | 3,468,825 | |

GCP Applied Technologies Inc. (a) | | | 20,000 | | | | 638,000 | |

| | | | | | | | |

| | | | | | | 6,549,452 | |

| | | | | | | | |

Commercial Services & Supplies - 1.8% | | | | | | | | |

Healthcare Services Group, Inc. | | | 70,315 | | | | 3,707,007 | |

| | | | | | | | |

Communication Equipment - 1.7% | | | | | | | | |

Alarm.com Holdings, Inc. (a) | | | 50,175 | | | | 1,894,106 | |

Finisar Corporation (a) | | | 15,000 | | | | 305,250 | |

Infinera Corporation (a) | | | 221,830 | | | | 1,404,184 | |

| | | | | | | | |

| | | | | | | 3,603,540 | |

| | | | | | | | |

Construction & Engineering - 2.6% | | | | | | | | |

EMCOR Group, Inc. | | | 39,285 | | | | 3,211,548 | |

MasTec Inc. (a) | | | 41,485 | | | | 2,030,691 | |

| | | | | | | | |

| | | | | | | 5,242,239 | |

| | | | | | | | |

Construction Materials - 1.6% | | | | | | | | |

Summit Materials, Inc. - Class A (a) | | | 104,294 | | | | 3,279,003 | |

| | | | | | | | |

Consumer Finance - 2.6% | | | | | | | | |

First Cash Financial Services, Inc. | | | 76,425 | | | | 5,154,866 | |

| | | | | | | | |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Electronic Equipment & Instruments - 1.9% | |

Littelfuse, Inc. | | | 10,505 | | | $ | 2,078,099 | |

Mesa Laboratories, Inc. | | | 14,535 | | | | 1,806,701 | |

| | | | | | | | |

| | | | | | | 3,884,800 | |

| | | | | | | | |

Energy Equipment & Services - 0.3% | | | | | | | | |

Mammoth Energy Services, Inc. (a) | | | 30,000 | | | | 588,900 | |

| | | | | | | | |

Food & Drug Retailing - 0.6% | | | | | | | | |

Sprouts Farmers Market, Inc. (a) | | | 48,280 | | | | 1,175,618 | |

| | | | | | | | |

Food Products - 0.3% | | | | | | | | |

Hostess Brands, Inc. (a) | | | 47,695 | | | | 706,363 | |

| | | | | | | | |

Health Care Equipment & Supplies - 4.8% | |

Cantel Medical Corp. | | | 37,890 | | | | 3,897,744 | |

K2M Group Holdings Inc. (a) | | | 18,575 | | | | 334,350 | |

PRA Health Sciences, Inc. (a) | | | 58,662 | | | | 5,342,349 | |

STAAR Surgical Company (a) | | | 10,000 | | | | 155,000 | |

| | | | | | | | |

| | | | | | | 9,729,443 | |

| | | | | | | | |

Health Care Providers & Services - 3.7% | |

HealthEquity, Inc. (a) | | | 56,305 | | | | 2,627,191 | |

Omnicell, Inc. (a) | | | 54,275 | | | | 2,632,338 | |

U.S. Physical Therapy, Inc. | | | 30,140 | | | | 2,176,108 | |

| | | | | | | | |

| | | | | | | 7,435,637 | |

| | | | | | | | |

Hotel, Restaurants & Leisure - 1.1% | | | | | | | | |

Planet Fitness, Inc. - Class A (a) | | | 62,410 | | | | 2,161,258 | |

| | | | | | | | |

Insurance - 0.7% | | | | | | | | |

Trupanion, Inc. (a) | | | 47,955 | | | | 1,403,643 | |

| | | | | | | | |

Internet & Catalog Retail - 1.7% | | | | | | | | |

Nutrisystem, Inc. | | | 66,005 | | | | 3,471,863 | |

| | | | | | | | |

Internet Software & Services - 6.4% | | | | | | | | |

Carbonite Inc. (a) | | | 46,815 | | | | 1,175,056 | |

Coupa Software Incorporated (a) | | | 55,000 | | | | 1,717,100 | |

Euronet Worldwide, Inc. (a) | | | 36,470 | | | | 3,073,327 | |

New Relic, Inc. (a) | | | 77,070 | | | | 4,452,334 | |

The Trade Desk, Inc. - Class A (a) | | | 29,750 | | | | 1,360,468 | |

Twilio Inc. - Class A (a) | | | 45,540 | | | | 1,074,744 | |

| | | | | | | | |

| | | | | | | 12,853,029 | |

| | | | | | | | |

IT Consulting & Services - 1.6% | | | | | | | | |

Acxiom Corporation (a) | | | 65,871 | | | | 1,815,405 | |

FireEye, Inc. (a) | | | 106,820 | | | | 1,516,844 | |

| | | | | | | | |

| | | | | | | 3,332,249 | |

| | | | | | | | |

Leisure Equipment & Products - 1.2% | | | | | | | | |

Pool Corporation | | | 18,670 | | | | 2,420,566 | |

| | | | | | | | |

Machinery - 5.7% | | | | | | | | |

John Bean Technologies Corporation | | | 31,250 | | | | 3,462,500 | |

Kennametal Inc. | | | 85,760 | | | | 4,151,641 | |

Lindsay Corporation | | | 25,815 | | | | 2,276,883 | |

Watts Water Technologies, Inc. - Class A | | | 20,465 | | | | 1,554,317 | |

| | | | | | | | |

| | | | | | | 11,445,341 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

16

|

| LKCM SMALL CAP EQUITY FUND |

| SCHEDULEOF INVESTMENTS, CONTINUED |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Marine - 0.9% | | | | | | | | |

Kirby Corporation (a) | | | 26,500 | | | $ | 1,770,200 | |

| | | | | | | | |

Metals & Mining - 1.5% | | | | | | | | |

Carpenter Technology Corporation | | | 59,375 | | | | 3,027,531 | |

| | | | | | | | |

Multiline Retail - 3.3% | | | | | | | | |

Five Below, Inc. (a) | | | 23,170 | | | | 1,536,634 | |

Ollie’s Bargain Outlet Holdings,

Inc. (a) | | | 94,380 | | | | 5,025,735 | |

| | | | | | | | |

| | | | | | | 6,562,369 | |

| | | | | | | | |

Oil & Gas & Consumable Fuels - 3.6% | | | | | | | | |

Matador Resources Company (a) | | | 50,000 | | | | 1,556,500 | |

Oasis Petroleum Inc. (a) | | | 150,000 | | | | 1,261,500 | |

PDC Energy, Inc. (a) | | | 19,405 | | | | 1,000,134 | |

WPX Energy Inc. (a) | | | 244,055 | | | | 3,433,854 | |

| | | | | | | | |

| | | | | | | 7,251,988 | |

| | | | | | | | |

Pharmaceuticals - 0.9% | | | | | | | | |

Cambrex Corp. (a) | | | 38,535 | | | | 1,849,680 | |

| | | | | | | | |

Real Estate Investment Trusts - 3.5% | | | | | | | | |

First Industrial Realty Trust, Inc. | | | 90,400 | | | | 2,844,888 | |

Life Storage, Inc. | | | 25,000 | | | | 2,226,750 | |

Outfront Media Inc. | | | 2,850 | | | | 66,120 | |

Stag Industrial, Inc. | | | 72,840 | | | | 1,990,717 | |

| | | | | | | | |

| | | | | | | 7,128,475 | |

| | | | | | | | |

Road & Rail - 1.4% | | | | | | | | |

Genesee & Wyoming Inc. - Class A (a) | | | 36,400 | | | | 2,865,772 | |

| | | | | | | | |

Semiconductor Equipment & Products - 0.6% | |

Lattice Semiconductor Corporation (a) | | | 5,000 | | | | 28,900 | |

Rambus Inc. (a) | | | 76,690 | | | | 1,090,532 | |

| | | | | | | | |

| | | | | | | 1,119,432 | |

| | | | | | | | |

Software - 7.3% | | | | | | | | |

ACI Worldwide, Inc. (a) | | | 100,060 | | | | 2,268,360 | |

Callidus Software, Inc. (a) | | | 50,535 | | | | 1,447,828 | |

Envestnet, Inc. (a) | | | 71,081 | | | | 3,543,388 | |

Fair Isaac Corporation | | | 16,220 | | | | 2,484,904 | |

Manhattan Associates, Inc. (a) | | | 11,145 | | | | 552,123 | |

Proofpoint, Inc. (a) | | | 24,635 | | | | 2,187,834 | |

RealPage, Inc. (a) | | | 40,900 | | | | 1,811,870 | |

SecureWorks Corp. - Class A (a) | | | 47,196 | | | | 418,629 | |

| | | | | | | | |

| | | | | | | 14,714,936 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods - 2.7% | | | | | |

Columbia Sportswear Company | | | 40,996 | | | | 2,946,793 | |

Oxford Industries, Inc. | | | 34,485 | | | | 2,592,927 | |

| | | | | | | | |

| | | | | | | 5,539,720 | |

| | | | | | | | |

Thrifts & Mortgage Finance - 2.9% | | | | | |

Banc of California, Inc. | | | 124,125 | | | | 2,563,181 | |

Home BancShares Inc. | | | 142,881 | | | | 3,321,983 | |

| | | | | | | | |

| | | | | | | 5,885,164 | |

| | | | | | | | |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Trading Companies & Distributors - 4.3% | | | | | |

MSC Industrial Direct Co., Inc. - Class A | | | 18,040 | | | $ | 1,743,746 | |

Textainer Group Holdings Limited (a) (b) | | | 162,925 | | | | 3,502,888 | |

Triton International Limited of Bermuda (b) | | | 88,985 | | | | 3,332,488 | |

| | | | | | | | |

| | | | | | | 8,579,122 | |

| | | | | | | | |

TOTAL COMMON STOCKS | | | | | | | | |

(Cost $134,630,193) | | | | | | | 201,560,754 | |

| | | | | | | | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS - 0.3% | |

Money Market Funds - 0.3% | | | | | | | | |

Invesco Short-Term Investments Trust - Government & Agency Portfolio - Institutional Shares, 1.21% (c) | | | 579,421 | | | | 579,421 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS | | | | | |

(Cost $579,421) | | | | | | | 579,421 | |

| | | | | | | | |

Total Investments - 100.2% | | | | | | | | |

(Cost $135,209,614) | | | | | | | 202,140,175 | |

Liabilities in Excess of Other Assets - (0.2)% | | | | (477,695 | ) |

| | | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | | $ | 201,662,480 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (b) | Security issued by non-U.S. incorporated company. |

| (c) | The rate quoted is the annualized seven-day yield of the fund at period end. |

Investments are classified by industry pursuant to the Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of Morgan Stanley Capital International, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

17

|

| LKCM SMALL-MID CAP EQUITY FUND |

| SCHEDULEOF INVESTMENTS |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS - 100.0% | | Shares | | | Value | |

Aerospace & Defense - 3.6% | | | | | | | | |

HEICO Corporation | | | 3,878 | | | $ | 365,889 | |

Mercury Systems, Inc. (a) | | | 6,310 | | | | 324,019 | |

| | | | | | | | |

| | | | | | | 689,908 | |

| | | | | | | | |

Banks - 6.2% | | | | | | | | |

LegacyTexas Financial Group, Inc. | | | 8,370 | | | | 353,298 | |

Pinnacle Financial Partners, Inc. | | | 4,475 | | | | 296,692 | |

SVB Financial Group (a) | | | 2,340 | | | | 547,022 | |

| | | | | | | | |

| | | | | | | 1,197,012 | |

| | | | | | | | |

Biotechnology - 1.9% | | | | | | | | |

Charles River Laboratories International, Inc. (a) | | | 3,430 | | | | 375,413 | |

| | | | | | | | |

Building Products - 3.5% | | | | | | | | |

Builders FirstSource, Inc. (a) | | | 18,115 | | | | 394,726 | |

Fortune Brands Home & Security Inc. | | | 4,135 | | | | 282,999 | |

| | | | | | | | |

| | | | | | | 677,725 | |

| | | | | | | | |

Capital Markets - 3.9% | | | | | | | | |

Lazard Ltd - Class A (b) | | | 7,660 | | | | 402,150 | |

SEI Investments Company | | | 5,040 | | | | 362,174 | |

| | | | | | | | |

| | | | | | | 764,324 | |

| | | | | | | | |

Chemicals - 7.3% | | | | | | | | |

CF Industries Holdings, Inc. | | | 8,775 | | | | 373,288 | |

FMC Corporation | | | 7,380 | | | | 698,591 | |

Ferroglobe PLC (a) (b) | | | 21,295 | | | | 344,979 | |

| | | | | | | | |

| | | | | | | 1,416,858 | |

| | | | | | | | |

Commercial Services & Supplies - 1.7% | | | | | | | | |

Healthcare Services Group, Inc. | | | 6,074 | | | | 320,221 | |

| | | | | | | | |

Consumer Finance - 3.3% | | | | | | | | |

First Cash Financial Services, Inc. | | | 9,350 | | | | 630,658 | |

| | | | | | | | |

Diversified Financials - 2.4% | | | | | | | | |

MSCI Inc. | | | 3,620 | | | | 458,075 | |

| | | | | | | | |

Electronic Equipment & Instruments - 6.6% | |

FLIR Systems, Inc. | | | 7,500 | | | | 349,650 | |

Littelfuse, Inc. | | | 1,710 | | | | 338,272 | |

Trimble Navigation Limited (a) | | | 14,550 | | | | 591,312 | |

| | | | | | | | |

| | | | | | | 1,279,234 | |

| | | | | | | | |

Food Products - 1.5% | | | | | | | | |

Snyder’s-Lance, Inc. | | | 5,690 | | | | 284,955 | |

| | | | | | | | |

Health Care Equipment & Supplies - 5.6% | |

Cantel Medical Corp. | | | 4,070 | | | | 418,681 | |

PRA Health Sciences, Inc. (a) | | | 7,295 | | | | 664,356 | |

| | | | | | | | |

| | | | | | | 1,083,037 | |

| | | | | | | | |

Health Care Providers & Services - 1.4% | | | | | | | | |

HealthEquity, Inc. (a) | | | 5,725 | | | | 267,129 | |

| | | | | | | | |

Internet & Catalog Retail - 2.1% | | | | | | | | |

Nutrisystem, Inc. | | | 7,800 | | | | 410,280 | |

| | | | | | | | |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Internet Software & Services - 3.2% | | | | | | | | |

Akamai Technologies, Inc. (a) | | | 5,290 | | | $ | 344,062 | |

Euronet Worldwide, Inc. (a) | | | 3,320 | | | | 279,776 | |

| | | | | | | | |

| | | | | | | 623,838 | |

| | | | | | | | |

IT Consulting & Services - 1.1% | | | | | | | | |

Acxiom Corporation (a) | | | 7,500 | | | | 206,700 | |

| | | | | | | | |

Leisure Equipment & Products - 3.1% | | | | | | | | |

Polaris Industries Inc. | | | 2,885 | | | | 357,711 | |

Pool Corporation | | | 1,855 | | | | 240,501 | |

| | | | | | | | |

| | | | | | | 598,212 | |

| | | | | | | | |

Machinery - 3.7% | | | | | | | | |

John Bean Technologies Corporation | | | 3,325 | | | | 368,410 | |

Kennametal Inc. | | | 7,375 | | | | 357,024 | |

| | | | | | | | |

| | | | | | | 725,434 | |

| | | | | | | | |

Marine - 1.1% | | | | | | | | |

Kirby Corporation (a) | | | 3,310 | | | | 221,108 | |

| | | | | | | | |

Metals & Mining - 1.8% | | | | | | | | |

Reliance Steel & Aluminum Co. | | | 4,080 | | | | 350,023 | |

| | | | | | | | |

Multiline Retail - 2.0% | | | | | | | | |

Ollie’s Bargain Outlet Holdings, Inc. (a) | | | 7,445 | | | | 396,446 | |

| | | | | | | | |

Oil & Gas & Consumable Fuels - 6.7% | | | | | | | | |

Diamondback Energy Inc. (a) | | | 2,685 | | | | 338,981 | |

Matador Resources Company (a) | | | 8,640 | | | | 268,963 | |

Parsley Energy, Inc. - Class A (a) | | | 10,175 | | | | 299,552 | |

WPX Energy Inc. (a) | | | 28,125 | | | | 395,719 | |

| | | | | | | | |

| | | | | | | 1,303,215 | |

| | | | | | | | |

Real Estate Investment Trusts - 3.8% | | | | | | | | |

CyrusOne Inc. | | | 4,965 | | | | 295,567 | |

First Industrial Realty Trust, Inc. | | | 7,405 | | | | 233,035 | |

Life Storage, Inc. | | | 2,370 | | | | 211,096 | |

| | | | | | | | |

| | | | | | | 739,698 | |

| | | | | | | | |

Road & Rail - 1.9% | | | | | | | | |

Genesee & Wyoming Inc. - Class A (a) | | | 4,770 | | | | 375,542 | |

| | | | | | | | |

Software - 9.5% | | | | | | | | |

Envestnet, Inc. (a) | | | 6,070 | | | | 302,590 | |

Fair Isaac Corporation | | | 2,300 | | | | 352,360 | |

Fortinet Inc. (a) | | | 7,315 | | | | 319,592 | |

Guidewire Software Inc. (a) | | | 4,770 | | | | 354,220 | |

Take-Two Interactive Software, Inc. (a) | | | 4,655 | | | | 511,026 | |

| | | | | | | | |

| | | | | | | 1,839,788 | |

| | | | | | | | |

Specialty Retail - 1.6% | | | | | | | | |

Tiffany & Co. | | | 2,990 | | | | 310,811 | |

| | | | | | | | |

Textiles, Apparel & Luxury Goods - 3.5% | | | | | | | | |

Columbia Sportswear Company | | | 3,900 | | | | 280,332 | |

Michael Kors Holdings Limited (a) (b) | | | 6,455 | | | | 406,342 | |

| | | | | | | | |

| | | | | | | 686,674 | |

| | | | | | | | |

Thrifts & Mortgage Finance - 1.3% | | | | | | | | |

Home BancShares Inc. | | | 10,575 | | | | 245,869 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

18

|

| LKCM SMALL-MID CAP EQUITY FUND |

| SCHEDULEOF INVESTMENTS, CONTINUED |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Trading Companies & Distributors - 4.7% | | | | | | | | |

MSC Industrial Direct Co., Inc. - Class A | | | 2,465 | | | $ | 238,267 | |

Triton International Limited of

Bermuda (b) | | | 8,305 | | | | 311,022 | |

Watsco, Inc. | | | 2,065 | | | | 351,133 | |

| | | | | | | | |

| | | | | | | 900,422 | |

| | | | | | | | |

TOTAL COMMON STOCKS | | | | | | | | |

(Cost $13,859,024) | | | | | | | 19,378,609 | |

| | | | | | | | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS - 0.3% | | | | | | |

Money Market Funds - 0.3% | | | | | | | | |

Invesco Short-Term Investments Trust - Government & Agency Portfolio - Institutional Shares, 1.21% (c) | | | 56,384 | | | | 56,384 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS | |

(Cost $56,384) | | | | | | | 56,384 | |

| | | | | | | | |

Total Investments - 100.3% | | | | | | | | |

(Cost $13,915,408) | | | | | | | 19,434,993 | |

Liabilities in Excess of Other Assets - (0.3)% | | | | (56,877 | ) |

| | | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | | $ | 19,378,116 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (b) | Security issued by non-U.S. incorporated company. |

| (c) | The rate quoted is the annualized seven-day yield of the fund at period end. |

Investments are classified by industry pursuant to the Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of Morgan Stanley Capital International, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

19

|

| LKCM EQUITY FUND |

| SCHEDULEOF INVESTMENTS |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS - 94.3% | | Shares | | | Value | |

Aerospace & Defense - 2.7% | | | | | | | | |

Honeywell International Inc. | | | 60,000 | | | $ | 9,201,600 | |

| | | | | | | | |

Banks - 9.1% | | | | | | | | |

Bank of America Corporation | | | 385,000 | | | | 11,365,200 | |

Comerica Incorporated | | | 126,000 | | | | 10,938,060 | |

Cullen/Frost Bankers, Inc. | | | 65,000 | | | | 6,152,250 | |

Glacier Bancorp, Inc. | | | 60,000 | | | | 2,363,400 | |

| | | | | | | | |

| | | | | | | 30,818,910 | |

| | | | | | | | |

Beverages - 2.6% | | | | | | | | |

The Coca-Cola Company | | | 65,000 | | | | 2,982,200 | |

PepsiCo, Inc. | | | 49,000 | | | | 5,876,080 | |

| | | | | | | | |

| | | | | | | 8,858,280 | |

| | | | | | | | |

Biotechnology - 2.0% | | | | | | | | |

Amgen Inc. | | | 40,000 | | | | 6,956,000 | |

| | | | | | | | |

Chemicals - 7.0% | | | | | | | | |

DowDuPont Inc. | | | 83,330 | | | | 5,934,763 | |

Ecolab Inc. | | | 30,000 | | | | 4,025,400 | |

FMC Corporation | | | 80,000 | | | | 7,572,800 | |

Monsanto Company | | | 55,000 | | | | 6,422,900 | |

| | | | | | | | |

| | | | | | | 23,955,863 | |

| | | | | | | | |

Commercial Services & Supplies - 2.0% | | | | | | | | |

Waste Connections, Inc. (b) | | | 97,500 | | | | 6,916,650 | |

| | | | | | | | |

Communication Equipment - 0.7% | | | | | | | | |

Alarm.com Holdings, Inc. (a) | | | 62,000 | | | | 2,340,500 | |

| | | | | | | | |

Computers & Peripherals - 2.1% | | | | | | | | |

Apple Inc. | | | 42,500 | | | | 7,192,275 | |

| | | | | | | | |

Construction Materials - 1.3% | | | | | | | | |

Martin Marietta Materials, Inc. | | | 20,000 | | | | 4,420,800 | |

| | | | | | | | |

Containers & Packaging - 1.6% | | | | | | | | |

Ball Corporation | | | 140,000 | | | | 5,299,000 | |

| | | | | | | | |

Diversified Financials - 3.2% | | | | | | | | |

JPMorgan Chase & Co. | | | 102,000 | | | | 10,907,880 | |

| | | | | | | | |

Electrical Equipment & Instruments - 2.9% | |

Franklin Electric Co., Inc. | | | 85,000 | | | | 3,901,500 | |

Roper Technologies, Inc. | | | 23,000 | | | | 5,957,000 | |

| | | | | | | | |

| | | | | | | 9,858,500 | |

| | | | | | | | |

Electronic Equipment & Instruments - 2.9% | |

Littelfuse, Inc. | | | 18,000 | | | | 3,560,760 | |

National Instruments Corporation | | | 55,000 | | | | 2,289,650 | |

Trimble Navigation Limited (a) | | | 100,000 | | | | 4,064,000 | |

| | | | | | | | |

| | | | | | | 9,914,410 | |

| | | | | | | | |

Health Care Equipment & Supplies - 6.4% | |

Danaher Corporation | | | 75,000 | | | | 6,961,500 | |

PerkinElmer, Inc. | | | 100,000 | | | | 7,312,000 | |

Thermo Fisher Scientific Inc. | | | 40,000 | | | | 7,595,200 | |

| | | | | | | | |

| | | | | | | 21,868,700 | |

| | | | | | | | |

Household Durables - 1.0% | | | | | | | | |

Newell Brands, Inc. | | | 113,817 | | | | 3,516,945 | |

| | | | | | | | |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Household Products - 1.8% | | | | | | | | |

Kimberly-Clark Corporation | | | 50,000 | | | $ | 6,033,000 | |

| | | | | | | | |

Internet & Catalog Retail - 2.8% | | | | | | | | |

Amazon.com, Inc. (a) | | | 8,000 | | | | 9,355,760 | |

| | | | | | | | |

Internet Software & Services - 5.7% | | | | | | | | |

Akamai Technologies, Inc. (a) | | | 90,000 | | | | 5,853,600 | |

Alphabet, Inc. - Class A (a) | | | 7,000 | | | | 7,373,800 | |

Facebook, Inc. - Class A (a) | | | 35,000 | | | | 6,176,100 | |

| | | | | | | | |

| | | | | | | 19,403,500 | |

| | | | | | | | |

IT Consulting & Services - 1.6% | | | | | | | | |

PayPal Holdings, Inc. (a) | | | 75,000 | | | | 5,521,500 | |

| | | | | | | | |

Machinery - 5.2% | | | | | | | | |

Generac Holdings, Inc. (a) | | | 108,000 | | | | 5,348,160 | |

The Toro Company | | | 74,000 | | | | 4,827,020 | |

Valmont Industries, Inc. | | | 45,000 | | | | 7,463,250 | |

| | | | | | | | |

| | | | | | | 17,638,430 | |

| | | | | | | | |

Marine - 0.9% | | | | | | | | |

Kirby Corporation (a) | | | 45,000 | | | | 3,006,000 | |

| | | | | | | | |

Media - 1.9% | | | | | | | | |

Time Warner Inc. | | | 70,000 | | | | 6,402,900 | |

| | | | | | | | |

Oil & Gas & Consumable Fuels - 7.4% | | | | | | | | |

Cabot Oil & Gas Corporation | | | 170,000 | | | | 4,862,000 | |

ConocoPhillips | | | 62,000 | | | | 3,403,180 | |

EOG Resources, Inc. | | | 65,000 | | | | 7,014,150 | |

Occidental Petroleum Corporation | | | 100,000 | | | | 7,366,000 | |

Range Resources Corporation | | | 140,000 | | | | 2,388,400 | |

| | | | | | | | |

| | | | | | | 25,033,730 | |

| | | | | | | | |

Personal Products - 1.1% | | | | | | | | |

The Estee Lauder Companies Inc. - Class A | | | 30,000 | | | | 3,817,200 | |

| | | | | | | | |

Pharmaceuticals - 7.1% | | | | | | | | |

AbbVie Inc. | | | 65,000 | | | | 6,286,150 | |

Johnson & Johnson | | | 38,000 | | | | 5,309,360 | |

Merck & Co., Inc. | | | 80,000 | | | | 4,501,600 | |

Pfizer Inc. | | | 115,000 | | | | 4,165,300 | |

Zoetis Inc. | | | 53,500 | | | | 3,854,140 | |

| | | | | | | | |

| | | | | | | 24,116,550 | |

| | | | | | | | |

Road & Rail - 1.2% | | | | | | | | |

Kansas City Southern | | | 40,000 | | | | 4,208,800 | |

| | | | | | | | |

Software - 4.8% | | | | | | | | |

Adobe Systems Incorporated (a) | | | 45,000 | | | | 7,885,800 | |

Microsoft Corporation | | | 100,000 | | | | 8,554,000 | |

| | | | | | | | |

| | | | | | | 16,439,800 | |

| | | | | | | | |

Specialty Retail - 3.1% | | | | | | | | |

The Home Depot, Inc. | | | 40,000 | | | | 7,581,200 | |

Tiffany & Co. | | | 30,000 | | | | 3,118,500 | |

| | | | | | | | |

| | | | | | | 10,699,700 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

20

|

| LKCM EQUITY FUND |

| SCHEDULEOF INVESTMENTS, CONTINUED |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Textiles, Apparel & Luxury Goods - 2.2% | |

V.F. Corporation | | | 100,000 | | | $ | 7,400,000 | |

| | | | | | | | |

TOTAL COMMON STOCKS | | | | | | | | |

(Cost $179,643,028) | | | | | | | 321,103,183 | |

| | | | | | | | |

| | | | | | | | |

| SHORT-TERM INVESTMENTS - 5.5% | |

Money Market Funds - 5.5% | | | | | | | | |

Invesco Short-Term Investments Trust - Government & Agency Portfolio - Institutional Shares, 1.21% (c) | | | 18,734,415 | | | | 18,734,415 | |

| | | | | | | | |

TOTAL SHORT-TERM INVESTMENTS | |

(Cost $18,734,415) | | | | | | | 18,734,415 | |

| | | | | | | | |

Total Investments - 99.8% | | | | | | | | |

(Cost $198,377,443) | | | | | | | 339,837,598 | |

Other Assets in Excess of Liabilities - 0.2% | | | | 763,756 | |

| | | | | | | | |

TOTAL NET ASSETS - 100.0% | | | | | | $ | 340,601,354 | |

| | | | | | | | |

| (a) | Non-income producing security. |

| (b) | Security issued by non-U.S. incorporated company. |

| (c) | The rate quoted is the annualized seven-day yield of the fund at period end. |

Investments are classified by industry pursuant to the Global Industry Classification Standard (GICS®), which was developed by and/or is the exclusive property of Morgan Stanley Capital International, Inc. (“MSCI”) and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements.

21

|

| LKCM BALANCED FUND |

| SCHEDULEOF INVESTMENTS |

| December 31, 2017 |

| | | | | | | | |

| COMMON STOCKS - 66.9% | | Shares | | | Value | |

Aerospace & Defense - 1.6% | | | | | | | | |

Honeywell International Inc. | | | 5,100 | | | $ | 782,136 | |

Rockwell Collins, Inc. | | | 4,300 | | | | 583,166 | |

| | | | | | | | |

| | | | | | | 1,365,302 | |

| | | | | | | | |

Banks - 5.9% | | | | | | | | |

Bank of America Corporation | | | 38,500 | | | | 1,136,520 | |

Comerica Incorporated | | | 10,100 | | | | 876,781 | |

Cullen/Frost Bankers, Inc. | | | 5,900 | | | | 558,435 | |

SunTrust Banks, Inc. | | | 11,500 | | | | 742,785 | |

Wells Fargo & Company | | | 12,471 | | | | 756,616 | |

Zions Bancorporation | | | 17,500 | | | | 889,525 | |

| | | | | | | | |

| | | | | | | 4,960,662 | |

| | | | | | | | |

Beverages - 1.8% | | | | | | | | |

The Coca-Cola Company | | | 17,600 | | | | 807,488 | |

PepsiCo, Inc. | | | 5,800 | | | | 695,536 | |

| | | | | | | | |

| | | | | | | 1,503,024 | |

| | | | | | | | |

Biotechnology - 1.7% | | | | | | | | |

Celgene Corporation (a) | | | 6,700 | | | | 699,212 | |

Charles River Laboratories International, Inc. (a) | | | 6,800 | | | | 744,260 | |

| | | | | | | | |

| | | | | | | 1,443,472 | |

| | | | | | | | |

Capital Markets - 1.3% | | | | | | | | |

SEI Investments Company | | | 14,500 | | | | 1,041,970 | |

| | | | | | | | |

Chemicals - 6.8% | | | | | | | | |

Air Products and Chemicals, Inc. | | | 5,100 | | | | 836,808 | |

DowDuPont Inc. | | | 16,076 | | | | 1,144,933 | |

Ecolab Inc. | | | 4,800 | | | | 644,064 | |

FMC Corporation | | | 11,200 | | | | 1,060,192 | |

GCP Applied Technologies Inc. (a) | | | 16,000 | | | | 510,400 | |

Monsanto Company | | | 5,600 | | | | 653,968 | |

Praxair, Inc. | | | 5,500 | | | | 850,740 | |

| | | | | | | | |

| | | | | | | 5,701,105 | |

| | | | | | | | |

Commercial Services & Supplies - 0.8% | | | | | | | | |

Waste Management, Inc. | | | 7,900 | | | | 681,770 | |

| | | | | | | | |

Computers & Peripherals - 1.5% | | | | | | | | |

Apple Inc. | | | 7,150 | | | | 1,209,994 | |

| | | | | | | | |

Construction Materials - 1.0% | | | | | | | | |

Martin Marietta Materials, Inc. | | | 3,900 | | | | 862,056 | |

| | | | | | | | |

Containers & Packaging - 0.4% | | | | | | | | |

Ball Corporation | | | 8,800 | | | | 333,080 | |

| | | | | | | | |

Diversified Financials - 2.1% | |

JPMorgan Chase & Co. | | | 8,400 | | | | 898,296 | |

Moody’s Corporation | | | 6,000 | | | | 885,660 | |

| | | | | | | | |

| | | | | | | 1,783,956 | |

| | | | | | | | |

Diversified Telecommunication Services - 0.9% | |

AT&T Inc. | | | 8,232 | | | | 320,060 | |

Verizon Communications Inc. | | | 8,641 | | | | 457,368 | |

| | | | | | | | |

| | | | | | | 777,428 | |

| | | | | | | | |

| | | | | | | | |

| COMMON STOCKS | | Shares | | | Value | |

Electronic Equipment & Instruments - 1.3% | | | | | |

National Instruments Corporation | | | 7,500 | | | $ | 312,225 | |

Trimble Navigation Limited (a) | | | 18,200 | | | | 739,648 | |

| | | | | | | | |

| | | | | | | 1,051,873 | |

| | | | | | | | |

Food & Drug Retailing - 1.5% | | | | | | | | |

Walgreens Boots Alliance, Inc. | | | 11,400 | | | | 827,868 | |

Wal-Mart Stores, Inc. | | | 4,100 | | | | 404,875 | |

| | | | | | | | |

| | | | | | | 1,232,743 | |

| | | | | | | | |

Food Products - 1.6% | | | | | | | | |

Hormel Foods Corporation | | | 13,900 | | | | 505,821 | |

Mondelez International Inc. - Class A | | | 19,800 | | | | 847,440 | |

| | | | | | | | |

| | | | | | | 1,353,261 | |

| | | | | | | | |

Health Care Equipment & Supplies - 3.7% | | | | | | | | |

Danaher Corporation | | | 9,600 | | | | 891,072 | |

Medtronic, PLC (b) | | | 7,600 | | | | 613,700 | |

PerkinElmer, Inc. | | | 11,600 | | | | 848,192 | |

Thermo Fisher Scientific, Inc. | | | 3,700 | | | | 702,556 | |

| | | | | | | | |

| | | | | | | 3,055,520 | |

| | | | | | | | |

Household Durables - 1.4% | | | | | | | | |

Newell Brands, Inc. | | | 15,509 | | | | 479,228 | |

Whirlpool Corporation | | | 3,900 | | | | 657,696 | |

| | | | | | | | |