As filed with the U.S. Securities and Exchange Commission on July 10, 2019

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-08348

LORD ASSET MANAGEMENT TRUST

(Exact name of registrant as specified in charter)

425 South Financial Place

Chicago, Illinois 60605-1028

(Address of principal executive offices) (Zip code)

Thomas S. White, Jr.

Thomas White International, Ltd.

425 South Financial Place

Chicago, Illinois 60605-1028

(Name and address of agent for service)

(312)663-8300

Registrant’s telephone number, including area code

Date of fiscal year end: 10/31

Date of reporting period: 11/1/2018 – 4/30/2019

Item 1. Reports to Stockholders.

SEMI-ANNUAL REPORT

APRIL 30, 2019

THE INTERNATIONAL FUND

THE EMERGING MARKETS FUND

THE AMERICAN OPPORTUNITIES FUND

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank if you hold your shares through such an institution. Instead, the reports will be made available on the Funds’ website (www.thomaswhitefunds.com/fundreports-and-literature), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting your financial intermediary or, if you hold your shares directly with the Funds, by calling 1-800-811-0535.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call 1-800-811-0535 to let the Funds know you wish to continue receiving paper copies of your shareholder reports. Your election to receive shareholder reports in paper may apply to all funds that you hold through the financial intermediary and will apply to all Funds held directly.

CONTENTS

Message to Shareholders

Dear Shareholders and Friends:

We want to thank you for your ongoing confidence and support you have shown through your continued investments in the Thomas White Funds. As we proceed into a new era for the Thomas White Funds family, we believe our commitment to a disciplined investment process honed over the past 20+ years will allow us to navigate the global equity markets. Our firm remains focused on helping you achieve your long term investment goals.

Our industry continues to adapt to competitive pressures in the market. The Active vs. Passive debate rages on and asset flows continue to be dominated by an influx into Exchange Traded Funds (ETF) and passive index strategies. Statistics from the Investment Company Institute (ICI) show that actively managed domestic equity mutual funds have seen outflows every year since 2005 and that the passively-managed market share has doubled over the past decade from 18% to 36%. Theseon-going flows have led to further consolidation amongst both money managers and pension consultants.

Another trend that continues to be extensively debated is the integration of Environmental, Social and Governance (ESG) factors into the investment process. Our firm has researched this issue in depth and continues to analyze how to further

incorporate these factors into our security analysis which ultimately lead to the holdings selected for the portfolios of the three Thomas White Funds. Across each of our funds, these issues can have a varying impact on the companies we research. Analyzing corporate governance policies innon-U.S. developed and emerging market companies has always been part of our analysis. This includes understanding the corporate board structure, voting control, founding family relationships, cross-holdings, as well as state ownership, if any. Each of these governance issues can impact corporate decision making which typically impacts total shareholder return. Social issues can vary to how a company integrates into its local markets from hiring policies to pay practices. A company’s policies and attitudes to the environment is also relevant to our expectations of how a company should perform in the future. Integration of ESG factors across the industry and within our firm will continue to grow as our industry moves to accept these policies as the norm.

2019 Equity Markets Got Off to a Strong Start but Uncertainty Increasing

The unexpected shift by the U.S. Federal Reserve to a more accommodative monetary policy stance has lifted investor sentiment and drove strong market gains through April 30th. The pace of U.S. economic growth moderated from last year’s high base as the boost from tax cuts has started wearing off.

| | | | |

| www.thomaswhitefunds.com | | | 1 | |

While aggregate macroeconomic data in the U.S. remains healthy, other major economies continue to show the effects of political turmoil resulting from Brexit and the tariff battles. Manufacturing output declined in the Eurozone, Japan, the U.K. and Canada at the beginning of 2019. Growing uncertainties related to global trade remain a significant headwind, and relatively weaker economic expansion overseas could dampen revenue growth in U.S. businesses that operate globally. However, as core inflation remains benign and weaker than expected, it is possible that the Fed may cut its benchmark rate early in the third quarter of this year.

The European Central Bank (ECB) also pushed back its rate hike timeline and is providing additional funding support to European banks. These pronounced moves, combined with U.S. Federal Reserve actions, reduced global recessionary risks in the near term and also helped propel global equity gains seen so far in 2019. The ECB’s actions, in the continuing absence of meaningful fiscal spending in Europe, are also necessary measures to prevent further economic deceleration in the region. Similarly, the Bank of Japan is expected to continue its quantitative easing, or even expand the program if domestic consumer demand weakens ahead of the proposed consumption tax increase. In addition, easier global liquidity conditions should continue to drive capital flows into most equity markets.

Our Portfolio Strategies

Equity markets continue to be volatile, reacting to tariff wars and other macroeconomic and political events over the quarter. We believe an active investment

approach is the best way to navigate these market environments. Each of our three funds outperformed over thesix-month review period but were impacted differently by recent events as detailed in their respective fund reviews. Trade negotiations between the U.S. and China continue to drag on as both sides are negotiating final details on technology transfers and the mechanics of compliance and enforcement of a potential deal. Ultimately a U.S.-China trade deal, with the elimination of tariff threats, will likely be needed to prevent further slowing to their respective economies as well as the global economy. We believe each of the Funds are well-positioned to benefit from a successfully negotiated agreement between the U.S. and China.

Our investment analysts continue to focus on understanding the impact of these macro events on the future growth and profitability of the companies in the Funds’ portfolios. We remain broadly diversified across sectors, as well as across countries and regions for the International Fund and the Emerging Markets Fund. It is in these types of environment that we believe we can identify attractive opportunities that will benefit the portfolios over the long run.

Thank you for your continued confidence in the Thomas White Funds.

Douglas M. Jackman, CFA

President and Portfolio Manager

Thomas White International and

Thomas White Funds

| | |

| 2 | | www.thomaswhitefunds.com |

Past performance is not a guarantee of future results.

Opinions expressed are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

Must be preceded or accompanied by a prospectus.

Mutual fund investing involves risk. Principal loss is possible. Investing in international markets may involve additional risks such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. These risks are greater for emerging markets. Investing in small and mid-cap companies can involve more risk than investing in larger companies.

Diversification does not assure a profit nor protect against loss in a declining market.

Earnings growth for a Fund holding does not guarantee a corresponding increase in the market value of the holding of the Fund.

The Thomas White Funds are distributed by Quasar Distributors, LLC.

It is not possible to invest directly in an index.

Cash Flow: Measures the cash generating capability of a company by adding non-cash charges (i.e. depreciation) and interest expense to pretax income.

Dividend Yield: Dividend yield is the ratio of a company’s annual dividend compared to its share price.

G-20: The G-20 (or Group of Twenty) is an international forum for the governments and central bank governors from 19 countries and the European Union. Although membership is generally based on the size of each member’ economy in terms of Gross Domestic Product, this is not an absolute criteria. The organization has stated that “In a forum such as the G-20, it is particularly important for the number of countries involved to be restricted and fixed to ensure the effectiveness and continuity of its activity. There are no formal criteria for G-20 membership and the composition of the group has remained unchanged since it was established. In view of the objectives of the G-20, it was considered important that countries and regions of systemic significance for the international financial system be included. Aspects such as geographical balance and population representation also played a major part.”

Active investing has higher management fees because of the manager’s increased level of involvement while passive investing has lower management and operating fees. Investing in both actively and passively managed mutual funds involves risk and principal loss is possible. Both actively and passively managed mutual funds generally have daily liquidity. There are no guarantees regarding the performance of actively and passively managed mutual funds. Actively managed mutual funds may have higher portfolio turnover than passively managed funds. Excessive turnover can limit returns and can incur capital gains.

While there are no sales charges, management fees and other expenses still apply. Please refer to the prospectus for further details.

| | | | |

| www.thomaswhitefunds.com | | | 3 | |

THOMAS WHITE INTERNATIONAL FUND

| | | | | | | | | | | | | | |

| | | | | | | | |

| | | Unaudited

Sales

Charge | | Deferred

Sales

Charge | | Administrative

Services

Fee | | 12b-1 Fees | | Operating

Expenses1,3 | | Prospectus

Gross

Annual

Operating

Expense2 | | Prospectus

Net

Annual

Operating

Expense2,3 |

| Investor Class | | None | | None | | Up to 0.25% | | None | | 1.24% | | 1.34% | | 1.24% |

| Class I | | None | | None | | None | | None | | 0.99% | | 1.18% | | 0.99% |

1 In the absence of the fee deferral/expense reimbursement arrangement for the International Fund, the ratio of expenses to average net assets would have been 1.60% for Investor Class shares and 1.43% for Class I shares.

2 Gross Annual Operating Expense and Net Annual Operating Expense are based on the most recent prospectus and may differ from other expense ratios appearing in this report.

3 Thomas White International, Ltd. (“Advisor”) has agreed to defer its fees and/or reimburse the Fund to the extent that the operating expenses for Investor Class and Class I shares exceed (as a percentage of average daily net assets) 1.24% and 0.99%, respectively. The fee deferral/expense reimbursement agreement expires February 29, 2020. The Fund has agreed to repay the Advisor for amounts deferred or reimbursed by the Advisor pursuant to the agreement provided that such repayment does not cause the Fund to exceed the above limits and the repayment is made within three years after the year in which the Advisor incurred the expense. The fee deferral/expense reimbursement agreement may only be amended or terminated by the Fund’s Board of Trustees.The net expense ratio is applicable to investors.

| | | | | | | | |

| | | | | |

| | | NAV | | Net Assets | | Redemption Fee | | Portfolio Turnover |

| Investor Class | | $15.34 | | $29.3 million | | 2.00% on shares held less than 60 days | | 18% |

| Class I | | $15.31 | | $100.5 million |

| | |

| 4 | | www.thomaswhitefunds.com |

APRIL 30, 2019

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Average Annual Returns as of April 30, 2019 (Unaudited) | |

| Class | | Sales Charge | | 6 month | | | Calendar

YTD | | | 1 Yr | | | 3 Yrs | | | 5 Yrs | | | 10 Yrs | | | Since

Inception

(6/28/1994)* | |

| | | | | | | | | |

| Investor Class shares (TWWDX) | | None | | | 10.68% | | | | 14.73% | | | | -4.96% | | | | 6.50% | | | | 0.78% | | | | 6.86% | | | | 6.54% | |

| | | | | | | | | |

| Class I shares1 (TWWIX) | | None | | | 10.86% | | | | 14.77% | | | | -4.74% | | | | 6.71% | | | | 1.01% | | | | 7.03% | | | | 6.61% | |

| | | | | | | | | |

| MSCI All Country World ex US Index2 | | N/A | | | 9.12% | | | | 13.22% | | | | -3.23% | | | | 8.09% | | | | 2.83% | | | | 7.75% | | | | 5.19% | |

* The inception date of the Investor Class shares.

1 Performance figures for Class I shares, first offered on August 31, 2012, include the historical performance of Investor Class shares through August 30, 2012.

2 The MSCI All Country World ex US Index is a free float-adjusted market capitalization-weighted index of both developed and emerging markets. The index is unmanaged and returns assume the reinvestment of dividends. It is not possible to invest directly in an index.

Returns of each share class reflect differences in expenses applicable to each class which are primarily differences in service fees.

The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns reflect the actual performance for each period and do not include the impacts of trades executed on the last business day of the period that were recorded on the first business day of the next period.

Performance data is based upon past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please call 1-800-811-0535 to obtain performance data as of the most recent month-end. The Fund imposes a 2% redemption fee on shares held less than 60 days. Performance data does not reflect the redemption fee. If reflected, total returns would be lower. Investment performance reflects any fee waivers that were in effect. In the absence of such waivers, total return would have been reduced. The Gross Expense Ratios, based on the most recent prospectus, are 1.34% (Investor Class) and 1.18% (Class I).

| | | | |

| www.thomaswhitefunds.com | | | 5 | |

THOMAS WHITE INTERNATIONAL FUND

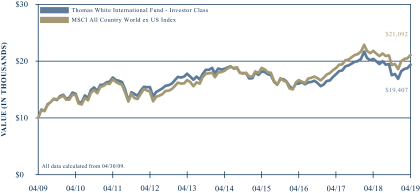

GROWTH OF A $10,000 INVESTMENT WITH DIVIDENDS REINVESTED (Unaudited)

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund’s Investor Class shares and its benchmark, the MSCI All Country World ex US Index, for the past 10 years through April 30, 2019. It assumes reinvestment of dividends and capital gains, but does not reflect the effect of any applicable redemption fees. This chart does not imply future performance. Past performance does not guarantee future results. The cumulative ten year return was 94.07% for the Fund’s Investor Class shares and 110.92% for the benchmark. The Fund’s Investor Class shares average annual total return since inception on June 28, 1994 was 6.54%. The MSCI All Country World ex US Index is a free float-adjusted market capitalization-weighted index of both developed and emerging markets. The index is unmanaged and returns assume the reinvestment of dividends. It is not possible to invest directly in an index. During the periods shown, the Fund’s manager reimbursed certain Fund expenses. Absent this reimbursement, performance would have been lower. Performance will vary from class to class based on differences in class-specific expenses.

| | |

| 6 | | www.thomaswhitefunds.com |

APRIL 30, 2019

The Thomas White International Fund primarily invests in equity securities of companies located in the world’s developed countries outside of the U.S. There may also be a portion of the Fund’s assets invested in companies located in emerging market countries.

Portfolio Managers

Jinwen Zhang, Ph.D., CFA

Douglas M. Jackman, CFA

Wei Li, Ph.D., CFA

John Wu, Ph.D., CFA

Rex Mathew, CFA, CMA

Ramkumar Venkatramani, CFA

Performance Review

The Thomas White International Fund Class I shares returned +10.86% for thesix-month period ended April 30, 2019, compared to +9.12% for the benchmark MSCI All Country World ex US Index. Since the Fund’s inception on June 28, 1994, the Fund’s Class I shares have returned +6.61%* annualized while the benchmark index returned +5.19% for the same period.

International Equities Weather Growth and Trade War Noise

International equity prices rebounded strongly during the first four months of 2019 after the sharp decline at the end of the previous year. Fears about a rapid slowdown in global growth and the worrisome headlines about the ongoing U.S.-China trade dispute had eroded investor confidence during the last quarter of 2018. However, economic growth data from the large

countries at the beginning of this year turned out to be better than expected. Further, the U.S. Federal Reserve reversed its monetary policy stance and indicated that future interest rate decisions will take into consideration possible economic weakness and benign inflation. Similarly, the European Central Bank reiterated its readiness to roll out more accommodative policy steps if the need arises, and the Bank of Japan is continuing its bond purchases.

Economic growth across most large developed economies remained healthy during the first quarter of 2019. The pace of U.S. expansion exceeded expectations and remains the main driver of global growth. Eurozone growth was also above forecasts and helped allay fears of another downturn in the region. Growth in Japan also accelerated at the beginning of this year, compared to the last quarter of 2018. Among the large emerging countries, growth in China was resilient to the decline in trade while the pace slowed in India and Brazil. Global manufacturing and services output growth has decelerated in recent months, largely due to the softness in external trade. Order inflows have also slowed, especially in the manufacturing sector, which suggests softer output data in the coming months.

Portfolio Review

During thesix-month review period, positive stock selection across all sectors, with the exception of communication services, helped the International Fund outperform its benchmark. Stock selection was notably effective in the consumer staples, industrials, financials and healthcare sectors. At the

| * | Performance for Class I shares includes the historical performance of Investor Class shares through August 30, 2012. |

| | | | |

| www.thomaswhitefunds.com | | | 7 | |

THOMAS WHITE INTERNATIONAL FUND

country and region level, stock selection was positive in Japan as well as the developed markets in Europe and Asia Pacific. On the negative side, stock selection was less effective in emerging markets in Asia and Latin America. The higher allocation to emerging markets helped the relative performance of the Fund during the review period.

Kweichow Moutai, a manufacturer of premium Chinese liquor, wasthe largest contributor to Fund returns during the review period as strong earnings growth erased investor fears about slowing consumer demand in China. Kweichow is also revamping its distribution to make its products more accessible.Techtronic Industries, a manufacturer of power tools, gained on strong demand in the U.S. and elsewhere. Japanese technology and telecom holding companySoftBanksurged after announcing a large share buyback program and also on optimism about the merger of its U.S. telecom business Sprint with rivalT-Mobile.Naspers Limitedbenefited from strong earnings growth at a number of its holdings, including Tencent, a Chinese online gaming company. European luxury goods retailerKering outperformed as the company continues to report healthy earnings growth.

Japanese parking lot operatorPark24 detracted the most from Fund returns during the period on skepticism about demand for parking spaces in large cities as ride hailing services like Uber becomes more popular. Japanese retailerRyohin Keikaku was hurt by weaker than expected revenues at its stores.Exide Industries, a manufacturer of automotive and industrial batteries based in

India, was negatively affected by doubts about automobile demand in the near term. Nevertheless, we expect the company to benefit from strong replacement demand. European banking groupSociete Generale lagged after reporting weaker than expected revenues from its trading operations, though we believe the current valuation is low and the dividend yield attractive. European banks have also been hurt by the yield compression that has dragged their margins even lower. Argentinean bankBanco Macro underperformed during the period on concerns about increased political uncertainties. Banco Macro recovered after the end of the review period as investor fears have eased.

Compelling Valuations Likely Outweigh Trade and Geopolitical Risks

Prospects for the settlement of U.S.-China trade disputes continue to be uncertain as the positions on both sides appear to have hardened. The Trump administration’s willingness to use trade tariffs to achieve other goals, such as stopping illegal migration, have worsened investor sentiment even further. A comprehensive U.S.-China deal at theG-20 summit scheduled for the end of June appears unlikely at this point, given the large differences concerning the enforcement of trade agreements and structural reforms. However, it is hoped that the dispute will not escalate further and both sides will continue to negotiate for a better trade deal. Meanwhile, China is likely to buffer its economy from trade tensions with additional fiscal stimulus and liquidity boosts.

| | |

| 8 | | www.thomaswhitefunds.com |

APRIL 30, 2019

After the leadership change in the U.K., the country’s exit from the European Union (EU) appears more likely by October of this year. The exit agreement negotiated earlier in the year failed to get approved by the U.K. parliament, and it seems unlikely that the EU will be willing to make major concessions. If a new exit agreement is not reached in time, a hard Brexit is the more likely scenario. That will likely be disruptive to trade flows in the region and could hurt business sentiment. However, the expected central bank actions in such a scenario and currency weakness could offset part of the expected negative effects.

While the alarming headlines about trade wars and other geopolitical risks have unnerved investors, international equity valuations remain compelling. Although revenue growth has moderated in several sectors, well run businesses have managed to defend their margins to a large extent. They have also deliberately tried to reduce balance sheet risks, given the macro uncertainties. The continuing drop in borrowing costs is helping the more leveraged companies as the abundant market liquidity is allowing them to refinance expensive debt. Lower fixed income yields also typically make equities more attractive to investors, especially in Europe where several large companies now offer near-double digit dividend yields.

We sincerely appreciate the trust you have kept in the Thomas White International Fund.

| | | | |

| www.thomaswhitefunds.com | | | 9 | |

THOMAS WHITE INTERNATIONAL FUND

Portfolio Country and Industry Allocation as of April 30, 2019 (Unaudited)

| | | | |

| | |

Country Allocation | | % of TNA | |

Argentina | | | 0.3% | |

| | |

Australia | | | 5.6% | |

| | |

Belgium | | | 0.9% | |

| | |

Brazil | | | 1.9% | |

| | |

Canada | | | 5.1% | |

| | |

China | | | 9.1% | |

| | |

Finland | | | 2.0% | |

| | |

France | | | 6.4% | |

| | |

Germany | | | 3.4% | |

| | |

Hong Kong | | | 2.8% | |

| | |

India | | | 4.2% | |

| | |

Indonesia | | | 2.3% | |

| | |

Ireland | | | 1.1% | |

| | |

Italy | | | 1.3% | |

| | |

Japan | | | 13.8% | |

| | |

Mexico | | | 1.7% | |

| | |

Netherlands | | | 2.0% | |

| | |

Poland | | | 0.6% | |

| | |

Russia | | | 2.5% | |

| | |

Singapore | | | 1.3% | |

| | |

South Africa | | | 2.4% | |

| | |

South Korea | | | 4.5% | |

| | |

Spain | | | 1.6% | |

| | |

Sweden | | | 2.7% | |

| | |

Switzerland | | | 2.4% | |

| | |

Taiwan | | | 2.3% | |

| | |

Thailand | | | 2.0% | |

| | |

Turkey | | | 0.4% | |

| | |

United Kingdom | | | 11.5% | |

| | |

| Cash & Other | | | 1.9% | |

| | | | |

| | |

Industry Allocation | | % of TNA | |

Automobiles & Components | | | 2.5% | |

| | |

Banks | | | 18.4% | |

| | |

Capital Goods | | | 9.0% | |

| | |

Commercial & Professional Services | | | 1.6% | |

| | |

Consumer Durables & Apparel | | | 4.3% | |

| | |

Consumer Services | | | 2.4% | |

| | |

Diversified Financials | | | 3.5% | |

| | |

Energy | | | 5.9% | |

| | |

Food, Beverage & Tobacco | | | 5.4% | |

| | |

Health Care Equipment & Services | | | 3.5% | |

| | |

Household & Personal Products | | | 3.2% | |

| | |

Insurance | | | 3.4% | |

| | |

Materials | | | 10.4% | |

| | |

Media & Entertainment | | | 5.6% | |

| | |

Pharmaceuticals, Biotechnology & Life Sciences | | | 2.8% | |

| | |

Retailing | | | 1.9% | |

| | |

Semiconductors & Semiconductor Equipment | | | 2.3% | |

| | |

Software & Services | | | 2.0% | |

| | |

Technology Hardware & Equipment | | | 2.7% | |

| | |

Telecommunication Services | | | 3.4% | |

| | |

Transportation | | | 3.9% | |

| | |

Cash & Other | | | 1.9% | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | |

TNA - Total Net Assets

Fund holdings and industry allocations are subject to change and should not be considered a recommendation to buy or sell any securities. For a complete list of Fund holdings, please refer to the Investment Portfolio section of this report.

| | |

| 10 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

COMMON

STOCKS (96.9%) | | | | | | | | | | |

|

| |

| ARGENTINA (0.3%) | | | | | | | | |

| | Banco Macro SA - ADR | | Banks | | | 10,900 | | | | $442,322 | |

|

| |

| AUSTRALIA (5.6%) | | | | | | | | |

| | Aristocrat Leisure Limited + | | Consumer Services | | | 68,600 | | | | 1,261,286 | |

| | BHP Billiton Ltd + | | Materials | | | 88,900 | | | | 2,347,941 | |

| | CSL Limited + | | Pharmaceuticals, Biotechnology & Life Sciences | | | 15,350 | | | | 2,148,802 | |

| | Treasury Wine Estates Limited + | | Food, Beverage & Tobacco | | | 120,100 | | | | 1,457,590 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 7,215,619 | |

|

| |

| BELGIUM (0.9%) | | | | | | | | | | |

| | KBC Group NV + | | Banks | | | 15,400 | | | | 1,142,019 | |

|

| |

| BRAZIL (0.7%) | | | | | | | | | | |

| | Ambev SA | | Food, Beverage & Tobacco | | | 190,900 | | | | 899,218 | |

|

| |

| CANADA (5.1%) | | | | | | | | |

| | Canadian National Railway Company | | Transportation | | | 17,700 | | | | 1,644,090 | |

| | Nutrien Ltd. | | Materials | | | 23,800 | | | | 1,290,817 | |

| | Open Text Corporation | | Software & Services | | | 40,100 | | | | 1,541,502 | |

| | Suncor Energy, Inc. | | Energy | | | 34,200 | | | | 1,127,832 | |

| | The Toronto-Dominion Bank | | Banks | | | 18,300 | | | | 1,043,880 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,648,121 | |

|

| |

| CHINA (9.1%) | | | | | | | | |

| | Alibaba Group Holding Ltd. - ADR * | | Retailing | | | 10,550 | | | | 1,957,763 | |

| | Anhui Conch Cement Company Limited - H Shares + | | Materials | | | 222,500 | | | | 1,354,413 | |

| | Baidu, Inc. - ADR * | | Media & Entertainment | | | 8,200 | | | | 1,363,086 | |

| | China Molybdenum Co., Ltd. - H Shares + | | Materials | | | 2,682,000 | | | | 1,005,427 | |

| | Kweichow Moutai Co., Ltd. - A Shares + | | Food, Beverage & Tobacco | | | 15,300 | | | | 2,211,940 | |

| | Midea Group Co., Ltd. - A Shares + | | Consumer Durables & Apparel | | | 203,800 | | | | 1,584,805 | |

| | Ping An Insurance (Group) Company of China Limited - H Shares + | | Insurance | | | 192,000 | | | | 2,313,440 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 11,790,874 | |

|

| |

| FINLAND (2.0%) | | | | | | | | |

| | Konecranes OYJ + | | Capital Goods | | | 31,000 | | | | 1,293,665 | |

| | Sampo Oyj - A Shares + | | Insurance | | | 27,700 | | | | 1,268,605 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,562,270 | |

|

| |

| FRANCE (6.4%) | | | | | | | | |

| | Danone + | | Food, Beverage & Tobacco | | | 18,500 | | | | 1,496,140 | |

| | Dassault Systemes + | | Software & Services | | | 6,900 | | | | 1,095,200 | |

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 11 | |

| | |

| Thomas White International Fund | | |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

| FRANCE (CONT.) | | | | | | | | |

| | Eiffage + | | Capital Goods | | | 12,400 | | | | $1,297,848 | |

| | Kering + | | Consumer Durables & Apparel | | | 3,700 | | | | 2,189,341 | |

| | Safran SA + | | Capital Goods | | | 8,425 | | | | 1,227,734 | |

| | Societe Generale SA + | | Banks | | | 32,300 | | | | 1,023,334 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,329,597 | |

|

| |

| GERMANY (3.4%) | | | | | | | | |

| | Bayer AG + | | Pharmaceuticals, Biotechnology & Life Sciences | | | 10,600 | | | | 704,507 | |

| | Bayerische Motoren Werke Aktiengesellschaft + | | Automobiles & Components | | | 18,450 | | | | 1,574,104 | |

| | Fresenius SE & Co KGaA + | | Health Care Equipment & Services | | | 15,200 | | | | 862,200 | |

| | Scout24 AG + | | Media & Entertainment | | | 25,900 | | | | 1,333,846 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 4,474,657 | |

|

| |

| HONG KONG (2.8%) | | | | | | | | |

| | Hong Kong Exchanges & Clearing Limited + | | Diversified Financials | | | 34,100 | | | | 1,183,959 | |

| | Techtronic Industries Company Limited + | | Consumer Durables & Apparel | | | 245,600 | | | | 1,777,563 | |

| | United Company RUSAL Plc * + | | Materials | | | 1,450,000 | | | | 621,590 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,583,112 | |

|

| |

| INDIA (4.2%) | | | | | | | | |

| | Exide Industries Ltd. + | | Automobiles & Components | | | 377,500 | | | | 1,162,202 | |

| | HDFC Bank Ltd. - ADR | | Banks | | | 18,300 | | | | 2,098,095 | |

| | Larsen & Toubro Ltd + | | Capital Goods | | | 64,900 | | | | 1,258,406 | |

| | Vedanta Limited + | | Materials | | | 394,200 | | | | 945,510 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,464,213 | |

|

| |

| INDONESIA (2.3%) | | | | | | | | | | |

| | PT Bank Central Asia Tbk + | | Banks | | | 740,900 | | | | 1,494,761 | |

| | PT Telekomunikasi Indonesia Persero Tbk + | | Telecommunication Services | | | 5,625,000 | | | | 1,501,087 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,995,848 | |

|

| |

| IRELAND (1.1%) | | | | | | | | | | |

| | CRH PLC + | | Materials | | | 42,190 | | | | 1,418,461 | |

|

| |

| ITALY (1.3%) | | | | | | | | | | |

| | Intesa Sanpaolo S.p.A. + | | Banks | | | 621,500 | | | | 1,628,761 | |

|

| |

| JAPAN (13.8%) | | | | | | | | | | |

| | East Japan Railway Company + | | Transportation | | | 9,100 | | | | 856,657 | |

| | H.I.S. Co., Ltd. + | | Consumer Services | | | 30,900 | | | | 985,271 | |

| | Kansai Paint Co., Ltd. + | | Materials | | | 65,900 | | | | 1,255,480 | |

| | KOSE Corporation + | | Household & Personal Products | | | 5,460 | | | | 1,017,663 | |

| | M3, Inc. + | | Health Care Equipment & Services | | | 76,300 | | | | 1,357,411 | |

The accompanying notes are an integral part of these financial statements

| | |

| 12 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

| JAPAN (CONT.) | | | | | | | | | | |

| | Mizuho Financial Group, Inc. + | | Banks | | | 564,400 | | | | $882,420 | |

| | Nidec Corporation + | | Capital Goods | | | 7,400 | | | | 1,056,176 | |

| | Nintendo Co., Ltd. + | | Media & Entertainment | | | 3,400 | | | | 1,165,916 | |

| | ORIX Corporation + | | Diversified Financials | | | 66,300 | | | | 932,833 | |

| | Park24 Co., Ltd. + | | Commercial & Professional Services | | | 54,200 | | | | 1,140,711 | |

| | RYOHIN KEIKAKU CO., LTD. + | | Retailing | | | 2,700 | | | | 510,516 | |

| | SMC CORPORATION + | | Capital Goods | | | 3,600 | | | | 1,496,283 | |

| | SoftBank Corp. + | | Telecommunication Services | | | 27,500 | | | | 2,870,833 | |

| | Sompo Holdings, Inc. + | | Insurance | | | 23,600 | | | | 878,910 | |

| | Sumitomo Corporation + | | Capital Goods | | | 56,700 | | | | 806,233 | |

| | Takeda Pharmaceutical Company Limited + | | Pharmaceuticals, Biotechnology & Life Sciences | | | 19,633 | | | | 727,854 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 17,941,167 | |

|

| |

| MEXICO (1.7%) | | | | | | | | | | |

| | Cemex SAB de CV * | | Materials | | | 1,761,024 | | | | 815,592 | |

| | Grupo Aeroportuario del Sureste SAB de CV - Class B | | Transportation | | | 87,800 | | | | 1,441,832 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,257,424 | |

|

| |

| NETHERLANDS (2.0%) | | | | | | | | |

| | ING Groep N.V. + | | Banks | | | 125,400 | | | | 1,597,763 | |

| | Koninklijke Philips NV + | | Health Care Equipment & Services | | | 22,600 | | | | 965,766 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,563,529 | |

|

| |

| POLAND (0.6%) | | | | | | | | | | |

| | Bank Polska Kasa Opieki SA + | | Banks | | | 26,800 | | | | 797,754 | |

|

| |

| RUSSIA (2.5%) | | | | | | | | | | |

| | LUKOIL PJSC - ADR + | | Energy | | | 21,200 | | | | 1,803,812 | |

| | Sberbank of Russia PJSC - ADR + | | Banks | | | 101,500 | | | | 1,459,145 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,262,957 | |

|

| |

| SINGAPORE (1.3%) | | | | | | | | | | |

| | DBS Group Holdings Limited + | | Banks | | | 81,300 | | | | 1,689,733 | |

|

| |

| SOUTH AFRICA (2.4%) | | | | | | | | |

| | FirstRand Limited + | | Diversified Financials | | | 270,600 | | | | 1,284,498 | |

| | Naspers Limited - N Shares + | | Media & Entertainment | | | 7,300 | | | | 1,864,652 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,149,150 | |

|

| |

| SOUTH KOREA (4.5%) | | | | | | | | |

| | KB Financial Group Inc. + | | Banks | | | 44,250 | | | | 1,750,318 | |

| | LG Household & Health Care Ltd. + | | Household & Personal Products | | | 1,145 | | | | 1,394,228 | |

| | POSCO + | | Materials | | | 4,050 | | | | 884,459 | |

| | Samsung Electronics Co., Ltd. + | | Technology Hardware & Equipment | | | 46,950 | | | | 1,839,641 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 5,868,646 | |

|

| |

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 13 | |

| | |

| Thomas White International Fund | | |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

| SPAIN (1.6%) | | | | | | | | | | |

| | Banco Bilbao Vizcaya Argentaria, S.A. + | | Banks | | | 331,500 | | | | $2,020,500 | |

|

| |

| SWEDEN (2.7%) | | | | | | | | | | |

| | Hexagon AB - B Shares + | | Technology Hardware & Equipment | | | 30,300 | | | | 1,652,189 | |

| | SKF AB - B Shares + | | Capital Goods | | | 97,700 | | | | 1,807,287 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,459,476 | |

|

| |

| SWITZERLAND (2.4%) | | | | | | | | |

| | Adecco Group AG + | | Commercial & Professional Services | | | 16,200 | | | | 930,733 | |

| | Credit Suisse Group AG + | | Diversified Financials | | | 87,700 | | | | 1,173,211 | |

| | Ems-Chemie Holding AG + | | Materials | | | 1,600 | | | | 970,502 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,074,446 | |

|

| |

| TAIWAN (2.3%) | | | | | | | | |

| | Taiwan Semiconductor Manufacturing Company, Ltd. + | | Semiconductors & Semiconductor Equipment | | | 62,000 | | | | 523,719 | |

| | Taiwan Semiconductor Manufacturing Company, Ltd. - ADR | | Semiconductors & Semiconductor Equipment | | | 55,400 | | | | 2,427,628 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,951,347 | |

|

| |

| THAILAND (2.0%) | | | | | | | | |

| | Airports of Thailand Public Company Ltd. + | | Transportation | | | 508,200 | | | | 1,091,242 | |

| | Kasikornbank Public Company Limited + | | Banks | | | 258,500 | | | | 1,543,146 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,634,388 | |

|

| |

| TURKEY (0.4%) | | | | | | | | |

| | Tofas Turk Otomobil Fabrikasi A.S. + | | Automobiles & Components | | | 167,700 | | | | 503,879 | |

|

| |

| UNITED KINGDOM (11.5%) | | | | | | | | |

| | Ashtead Group Plc + | | Capital Goods | | | 50,000 | | | | 1,386,249 | |

| | BP p.l.c. + | | Energy | | | 306,900 | | | | 2,231,506 | |

| | British American Tobacco P.L.C. + | | Food, Beverage & Tobacco | | | 25,500 | | | | 1,000,215 | |

| | Carnival plc + | | Consumer Services | | | 16,600 | | | | 879,292 | |

| | Glencore plc + | | Materials | | | 158,100 | | | | 631,082 | |

| | Lloyds Banking Group plc + | | Banks | | | 2,085,600 | | | | 1,702,092 | |

| | Reckitt Benckiser Group PLC + | | Household & Personal Products | | | 20,800 | | | | 1,685,218 | |

| | Royal Dutch Shell PLC - B Shares + | | Energy | | | 79,600 | | | | 2,551,963 | |

| | Smith & Nephew plc + | | Health Care Equipment & Services | | | 69,900 | | | | 1,349,603 | |

| | WPP plc + | | Media & Entertainment | | | 123,100 | | | | 1,537,204 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 14,954,424 | |

|

| |

Total Common

Stocks | | | | (Cost $112,657,321) | | | | | | | 125,723,912 | |

| | | | | | | | | | | | |

|

| |

The accompanying notes are an integral part of these financial statements

| | |

| 14 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

PREFERRED

STOCK (1.2%) | | | | | | | | | | | | |

|

| |

| BRAZIL (1.2%) | | | | | | | | | | |

| | Itau Unibanco Holding S.A. (7/29/19, 0.51%) ^ | | Banks | | | 184,740 | | | | $1,599,060 | |

|

| |

Total Preferred

Stock | | | | (Cost $1,325,082) | | | | | | | 1,599,060 | |

| | | | | | | | | | | | |

|

| |

| Total Investments | | 98.1% | | (Cost $113,982,403) | | | | | | | $127,322,972 | |

Other Assets,

Less Liabilities | | 1.9% | | | | | | | | | 2,469,144 | |

| Total Net Assets: | | 100.0% | | | | | | | | | $129,792,116 | |

|

| |

| * | Non-Income Producing Securities |

| ^ | Maturity Date and Preferred Dividend Rate of Preferred Stock |

| PLC | - Public Limited Company |

| ADR | - American Depositary Receipt |

Industry classifications shown in the Investment Portfolio are based off of the Global Industry Classification Standard (GICS®). GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 15 | |

| | |

| Thomas White International Fund | | |

The following table summarizes the inputs used, as of April 30, 2019, in valuating the Fund’s assets:

| | | | | | | | | | | | | | | | |

| | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | | | | | | | | | | | | | | | |

| | | | | |

| Argentina | | | $442,322 | | | | $------- | | | | $------- | | | | $442,322 | |

| | | | | |

| Australia | | | ------- | | | | 7,215,619 | | | | ------- | | | | 7,215,619 | |

| | | | | |

| Belgium | | | ------- | | | | 1,142,019 | | | | ------- | | | | 1,142,019 | |

| | | | | |

| Brazil | | | 899,218 | | | | ------- | | | | ------- | | | | 899,218 | |

| | | | | |

| Canada | | | 6,648,121 | | | | ------- | | | | ------- | | | | 6,648,121 | |

| | | | | |

| China | | | 3,320,849 | | | | 8,470,025 | | | | ------- | | | | 11,790,874 | |

| | | | | |

| Finland | | | ------- | | | | 2,562,270 | | | | ------- | | | | 2,562,270 | |

| | | | | |

| France | | | ------- | | | | 8,329,597 | | | | ------- | | | | 8,329,597 | |

| | | | | |

| Germany | | | ------- | | | | 4,474,657 | | | | ------- | | | | 4,474,657 | |

| | | | | |

| Hong Kong | | | ------- | | | | 3,583,112 | | | | ------- | | | | 3,583,112 | |

| | | | | |

| India | | | 2,098,095 | | | | 3,366,118 | | | | ------- | | | | 5,464,213 | |

| | | | | |

| Indonesia | | | ------- | | | | 2,995,848 | | | | ------- | | | | 2,995,848 | |

| | | | | |

| Ireland | | | ------- | | | | 1,418,461 | | | | ------- | | | | 1,418,461 | |

| | | | | |

| Italy | | | ------- | | | | 1,628,761 | | | | ------- | | | | 1,628,761 | |

| | | | | |

| Japan | | | ------- | | | | 17,941,167 | | | | ------- | | | | 17,941,167 | |

| | | | | |

| Mexico | | | 2,257,424 | | | | ------- | | | | ------- | | | | 2,257,424 | |

| | | | | |

| Netherlands | | | ------- | | | | 2,563,529 | | | | ------- | | | | 2,563,529 | |

| | | | | |

| Poland | | | ------- | | | | 797,754 | | | | ------- | | | | 797,754 | |

| | | | | |

| Russia | | | ------- | | | | 3,262,957 | | | | ------- | | | | 3,262,957 | |

| | | | | |

| Singapore | | | ------- | | | | 1,689,733 | | | | ------- | | | | 1,689,733 | |

| | | | | |

| South Africa | | | ------- | | | | 3,149,150 | | | | ------- | | | | 3,149,150 | |

| | | | | |

| South Korea | | | ------- | | | | 5,868,646 | | | | ------- | | | | 5,868,646 | |

| | | | | |

| Spain | | | ------- | | | | 2,020,500 | | | | ------- | | | | 2,020,500 | |

| | | | | |

| Sweden | | | ------- | | | | 3,459,476 | | | | ------- | | | | 3,459,476 | |

| | | | | |

| Switzerland | | | ------- | | | | 3,074,446 | | | | ------- | | | | 3,074,446 | |

| | | | | |

| Taiwan | | | 2,427,628 | | | | 523,719 | | | | ------- | | | | 2,951,347 | |

| | | | | |

| Thailand | | | ------- | | | | 2,634,388 | | | | ------- | | | | 2,634,388 | |

| | | | | |

| Turkey | | | ------- | | | | 503,879 | | | | ------- | | | | 503,879 | |

| | | | | |

| United Kingdom | | | ------- | | | | 14,954,424 | | | | ------- | | | | 14,954,424 | |

| Total Common Stocks | | | $18,093,657 | | | | $107,630,255 | | | | $------- | | | | $125,723,912 | |

| Preferred Stock | | | | | | | | | | | | | | | | |

| | | | | |

| Brazil | | | $1,599,060 | | | | $------- | | | | $------- | | | | $1,599,060 | |

| Total Preferred Stock | | | $1,599,060 | | | | $------- | | | | $------- | | | | $1,599,060 | |

| Total Investments | | | $19,692,717 | | | | $107,630,255 | | | | $------- | | | | $127,322,972 | |

For more information on valuation inputs, please refer to Note 1(A) of the accompanying Notes to Financial Statements.

The accompanying notes are an integral part of these financial statements

| | |

| 16 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

The Fund’s assets assigned to Level 2 include certain foreign securities for which a third party statistical pricing service may be employed for purposes of fair market valuation. There were no transfers into or out of Level 3 during the reporting period, as compared to their classification from the prior annual report.

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 17 | |

THOMAS WHITE EMERGING MARKETS FUND

| | | | | | | | | | | | | | |

| | | | | | | | |

| | | Unaudited

Sales

Charge | | Deferred

Sales

Charge | | Administrative

Services

Fee | | 12b-1 Fees | | Operating

Expenses1,3 | | Prospectus

Gross

Annual

Operating

Expense2 | | Prospectus

Net Annual

Operating

Expense2,3 |

| Investor Class | | None | | None | | Up to 0.25% | | None | | 1.34% | | 1.55% | | 1.35% |

| Class I | | None | | None | | None | | None | | 1.09% | | 1.52% | | 1.10% |

1 In the absence of the fee deferral/expense reimbursement arrangement for the Emerging Markets Fund, the ratio of expenses to average net assets would have been 1.58% for Investor Class shares and 1.55% for Class I shares.

2 Gross Annual Operating Expense and Net Annual Operating Expense are based on the most recent prospectus and may differ from other expense ratios appearing in this report.

3 Thomas White International, Ltd. (“Advisor”) has agreed to defer its fees and/or reimburse the Fund to the extent that the operating expenses for Investor Class and Class I shares exceed (as a percentage of average daily net assets) 1.34% and 1.09%, respectively. The fee deferral/expense reimbursement agreement expires February 29, 2020. The Fund has agreed to repay the Advisor for amounts deferred or reimbursed by the Advisor pursuant to the agreement provided that such repayment does not cause the Fund to exceed the above limits and the repayment is made within three years after the year in which the Advisor incurred the expense. The fee deferral/expense reimbursement agreement may only be amended or terminated by the Fund’s Board of Trustees. The net expense ratio is applicable to investors.

| | | | | | | | |

| | | | | |

| | | NAV | | Net Assets | | Redemption Fee | | Portfolio Turnover |

| Investor Class | | $11.25 | | $1.8 million | | 2.00% on shares held less than 60 days | | 12% |

| Class I | | $11.38 | | $37.9 million |

| | |

| 18 | | www.thomaswhitefunds.com |

APRIL 30, 2019

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| |

| Average Annual Returns as of April 30, 2019 (Unaudited) | |

| Class | | Sales Charge | | 6 month | | | Calendar

YTD | | | 1 Yr | | | 3 Yrs | | | 5 Yrs | | | Since

Inception

(6/28/2010)* | |

| | | | | | | | |

| Investor Class shares (TWEMX) | | None | | | 13.98% | | | | 15.15% | | | | -3.91% | | | | 7.97% | | | | 1.28% | | | | 2.48% | |

| | | | | | | | |

| Class I shares1 (TWIIX) | | None | | | 14.14% | | | | 15.18% | | | | -3.62% | | | | 8.24% | | | | 1.54% | | | | 2.66% | |

| | | | | | | | |

| MSCI Emerging Markets Index2 | | N/A | | | 13.76% | | | | 12.23% | | | | -5.04% | | | | 11.25% | | | | 4.04% | | | | 3.87% | |

* The inception date of the Investor Class shares.

1 Performance figures for Class I shares, first offered on August 31, 2012, include the historical performance of Investor Class shares through August 30, 2012.

2 The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The index is unmanaged and returns assume the reinvestment of dividends. It is not possible to invest directly in an index.

Returns of each share class reflect differences in expenses applicable to each class which are primarily differences in service fees.

The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns reflect the actual performance for each period and do not include the impacts of trades executed on the last business day of the period that were recorded on the first business day of the next period.

Performance data is based upon past performance, which is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please call 1-800-811-0535 to obtain performance data as of the most recent month-end. The Fund imposes a 2% redemption fee on shares held less than 60 days. Performance data does not reflect the redemption fee. If reflected, total returns would be lower. Investment performance reflects any fee waivers that were in effect. In the absence of such waivers, total return would have been reduced. The Gross Expense Ratios, based on the most recent prospectus, are 1.55% (Investor Class) and 1.52% (Class I).

| | | | |

| www.thomaswhitefunds.com | | | 19 | |

THOMAS WHITE EMERGING MARKETS FUND

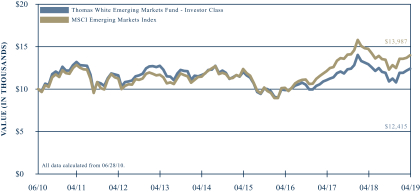

GROWTH OF A $10,000 INVESTMENT WITH DIVIDENDS REINVESTED (Unaudited)

This chart illustrates the performance of a hypothetical $10,000 investment made in the Fund’s Investor Class shares and its benchmark, the MSCI Emerging Markets Index, since inception on June 28, 2010 through April 30, 2019. It assumes reinvestment of dividends and capital gains, but does not reflect the effect of any applicable redemption fees. This chart does not imply future performance. Past performance does not guarantee future results. The cumulative return since inception was 24.15% for the Fund’s Investor Class shares and 39.87% for the benchmark. The Fund’s Investor Class shares average annual total return since inception on June 28, 2010 was 2.48%. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The index is unmanaged and returns assume the reinvestment of dividends. It is not possible to invest directly in an index. During the periods shown, the Fund’s manager reimbursed certain Fund expenses. Absent this reimbursement, performance would have been lower. Performance will vary from class to class based on differences in class-specific expenses.

| | |

| 20 | | www.thomaswhitefunds.com |

APRIL 30, 2019

The Thomas White Emerging Markets Fund invests primarily in securities of companies located in or whose businesses are closely associated with the world’s emerging markets countries.

Portfolio Managers

Jinwen Zhang, Ph.D., CFA

Douglas M. Jackman, CFA

Wei Li, Ph.D., CFA

John Wu, Ph.D., CFA

Rex Mathew, CFA, CMA

Ramkumar Venkatramani, CFA

Performance Review

During the trailingsix-month period ended April 30, 2019, the Thomas White Emerging Markets Fund Class I shares returned +14.14%, compared to +13.76% for its benchmark MSCI Emerging Markets Index. Since its inception on June 28, 2010, the Fund’s Class I shares have returned +2.66%* annualized, against +3.87% for the benchmark index.

Despite Trade War Noise, Emerging Markets Outperform

Emerging market equity prices outperformed the developed markets during the review period, despite recurring concerns about the U.S.-China trade war and slower global growth. Aggregate economic growth in major countries such as China, India and Indonesia remained healthy, though lower trade volumes restricted the pace of expansion in select countries. Central banks in some emerging countries also lowered

interest rates or took steps to infuse liquidity to ensure credit availability. The targeted fiscal stimulus measures in China have helped support consumer demand in that country in recent months.

There-election of market-friendly governments in India and Indonesia attracted much investor attention and drove capital inflows into those markets. The Brazilian government’s efforts to move forward with crucial structural changes such as the pension system reforms have been received well by investors, though weaker than expected economic growth did dampen some of the optimism. Global commodity prices were volatile during the review period, but average prices remained remunerative enough for the resource exporting countries. Manufacturing activity softened across most emerging markets, reflecting the weaker global trade volumes.

Portfolio Review

Consumer staples, communication services and consumer discretionary were the best performing sectors during the review period as doubts about consumer spending in major markets such as China faded. Materials and energy sectors underperformed as the price volatility dissuaded investors from increasing their allocations to these areas. Effective stock selection in the consumer staples, industrials, communication services and financials sectors contributed to the Fund’s relative returns against the benchmark during the period. Stock selection was not as effective in the technology, consumer discretionary and materials sectors.

| | | | |

| www.thomaswhitefunds.com | | | 21 | |

THOMAS WHITE EMERGING MARKETS FUND

Higher exposure to the consumer discretionary sector and lower allocation to the healthcare sector helped the Fund. Being overweight energy and materials as well as being underweight communication services hurt the Fund’s relative performance. At the country level, stock selection was most effective in China, Russia, South Africa and Korea. Stock selection effect was negative in India, Indonesia and Brazil. Higher allocation to Latin America and lower exposure to Asia detracted from relative performance during the period.

Chinese online gaming and communications groupTencent Holdings contributed the most to returns, helped by strong earnings growth as well the Chinese government’s decision to withdraw the temporary restrictions on new online game approvals. South African investment holding companyNaspers, which is the major shareholder in Tencent, also benefited from the resurgent technology valuations. Chinese ecommerce groupAlibaba advanced as its topline growth continued to exceed expectations and the company remains confident about sustaining high growth rates.Reliance Industries, an Indian conglomerate with businesses in refining, retail and telecom, advanced as it continued to gain market share in the domestic telecom market.PingAn Insurance, one of the largest insurers in Asia, outperformed as demand for its higher margin products remained robust.

Catcher Technologies, the leading Taiwanese manufacturer of camera lenses used in smartphones, detracted the most from returns during the review period on concerns that additional tariffs could negatively impact volumes. Catcher was also hurt by the U.S.

government’s actions against Chinese equipment manufacturer Huawei, though sales to Huawei only represent about 5% of Catcher’s revenues. Brazilian steelmakerGerdau was hurt by weaker than expected economic growth in the country that could dampen steel demand. Brazilian oil producerPetrobras was negatively affected by relatively lower oil prices, as well as uncertainties about fuel subsidies in the country. Chinese internet search services providerBaidu declined on concerns that growth in advertising sales is slowing, while revenue generation from the company’s investments in autonomous driving and artificial intelligence could be delayed.PT United Tractors, and Indonesian coal miner and distributor of heavy equipment, underperformed on weaker Chinese coal demand.

Depressed Valuations Make Emerging Markets Appear Attractive

Given the unexpected deterioration in the U.S.-China trade talks, as well as the hardened rhetoric from both sides, it appears less likely that a trade deal will be reached anytime soon. Disagreements have resurfaced over several important areas such as intellectual property protections and enforcement of commitments made in agreements. At the same time, given the high stakes involved and the potential damage to economic growth on both sides, the risk of the current standoff escalating to a full blown trade war is also relatively low. We believe it is more likely that the U.S. and China will agree to a truce, possibly at theG-20 meeting scheduled for end of June and then continue negotiations to settle the contentious issues. If this occurs, it should be largely positive for

| | |

| 22 | | www.thomaswhitefunds.com |

APRIL 30, 2019

investor sentiment as it will avoid the risk of further economic growth deceleration while at the same time reduce the possibility of future conflicts by addressing the deeper structural disputes.

While external trade flows have weakened for most emerging economies this year, domestic demand trends remain fairly healthy. Governments in select countries, including China and India, have offset the slower household income growth with targeted fiscal stimulus and other income support measures. This is sustainable in our view as the fiscal deficits of emerging market countries, except a few, are not excessive. In addition, central banks in several emerging markets continue to ease liquidity, as in the case of China, or lower interest rates. As inflation risks remain benign, we believe monetary policy in emerging economies can remain accommodative for an extended period. This favorable fiscal and monetary support should continue to attract investor interest to emerging market equities, where current valuations remain depressed in our opinion.

We thank you for confidence in the Thomas White Emerging Markets Fund.

| | | | |

| www.thomaswhitefunds.com | | | 23 | |

THOMAS WHITE EMERGING MARKETS FUND

Portfolio Country and Industry Allocation as of April 30, 2019 (Unaudited)

| | | | |

| | |

| Country Allocation | | % of TNA | |

| Argentina | | | 0.6% | |

| | |

| Brazil | | | 7.7% | |

| | |

| Chile | | | 1.0% | |

| | |

| China | | | 33.6% | |

| | |

| Hong Kong | | | 0.8% | |

| | |

| India | | | 8.8% | |

| | |

| Indonesia | | | 3.4% | |

| | |

| Malaysia | | | 1.0% | |

| | |

| Mexico | | | 5.1% | |

| | |

| Panama | | | 0.9% | |

| | |

| Philippines | | | 1.7% | |

| | |

| Poland | | | 1.1% | |

| | |

| Russia | | | 5.2% | |

| | |

| South Africa | | | 4.4% | |

| | |

| South Korea | | | 11.3% | |

| | |

| Taiwan | | | 6.9% | |

| | |

| Thailand | | | 2.7% | |

| | |

| Turkey | | | 0.5% | |

| | |

| United States | | | 1.0% | |

| | |

| Cash & Other | | | 2.3% | |

| | |

| | | | | |

| | |

| | | | | |

| | |

| | | | | |

| | | | |

| | |

| Industry Allocation | | % of TNA | |

| Automobiles & Components | | | 2.3% | |

| | |

| Banks | | | 18.0% | |

| | |

| Capital Goods | | | 0.9% | |

| | |

| Consumer Durables & Apparel | | | 3.0% | |

| | |

| Diversified Financials | | | 2.8% | |

| | |

| Energy | | | 10.0% | |

| | |

| Food & Staples Retailing | | | 0.7% | |

| | |

| Food, Beverage & Tobacco | | | 3.4% | |

| | |

| Health Care Equipment & Services | | | 0.8% | |

| | |

| Household & Personal Products | | | 1.5% | |

| | |

| Insurance | | | 2.4% | |

| | |

| Materials | | | 7.9% | |

| | |

| Media & Entertainment | | | 7.3% | |

| | |

| Pharmaceuticals, Biotechnology & Life Sciences | | | 1.3% | |

| | |

| Real Estate | | | 2.2% | |

| | |

| Retailing | | | 6.8% | |

| | |

| Semiconductors & Semiconductor Equipment | | | 6.1% | |

| | |

| Software & Services | | | 8.1% | |

| | |

| Technology Hardware & Equipment | | | 5.7% | |

| | |

| Telecommunication Services | | | 1.2% | |

| | |

| Transportation | | | 4.3% | |

| | |

| Utilities | | | 1.0% | |

| | |

| Cash & Other | | | 2.3% | |

TNA - Total Net Assets

Fund holdings and industry allocations are subject to change and should not be considered a recommendation to buy or sell any securities. For a complete list of Fund holdings, please refer to the Investment Portfolio section of this report.

| | |

| 24 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

COMMON

STOCKS (91.4%) | | | | | | | | | | |

|

| |

| ARGENTINA (0.6%) | | | | | | | | | | |

| | Banco Macro SA - ADR | | Banks | | | 5,900 | | | | $239,422 | |

|

| |

| BRAZIL (3.2%) | | | | | | | | |

| | Ambev SA | | Food, Beverage & Tobacco | | | 60,200 | | | | 283,567 | |

| | B3 SA - Brasil Bolsa Balcao | | Diversified Financials | | | 45,400 | | | | 400,033 | |

| | Fleury SA | | Health Care Equipment & Services | | | 60,100 | | | | 318,195 | |

| | Hypera SA | | Pharmaceuticals, Biotechnology & Life Sciences | | | 36,900 | | | | 265,756 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,267,551 | |

|

| |

| CHILE (1.0%) | | | | | | | | |

| | Enel Americas SA | | Utilities | | | 2,347,000 | | | | 411,843 | |

|

| |

| CHINA (33.6%) | | | | | | | | |

| | Alibaba Group Holding Ltd. - ADR * | | Retailing | | | 11,125 | | | | 2,064,466 | |

| | Anhui Conch Cement Company Limited - H Shares + | | Materials | | | 138,900 | | | | 845,519 | |

| | Baidu, Inc. - ADR * | | Media & Entertainment | | | 2,475 | | | | 411,419 | |

| | Brilliance China Automotive Holdings Ltd. + | | Automobiles & Components | | | 188,000 | | | | 206,251 | |

| | China Construction Bank Corp. - H Shares + | | Banks | | | 1,053,000 | | | | 928,731 | |

| | China Overseas Land & Investment Limited + | | Real Estate | | | 146,000 | | | | 546,631 | |

| | China Petroleum and Chemical Corporation (Sinopec) - H Shares + | | Energy | | | 656,000 | | | | 502,922 | |

| | CSPC Pharmaceutical Group Limited + | | Pharmaceuticals, Biotechnology & Life Sciences | | | 128,000 | | | | 245,995 | |

| | Ctrip.com International, Ltd. - ADR * | | Retailing | | | 9,800 | | | | 431,690 | |

| | Haier Electronics Group Co., Ltd. + | | Consumer Durables & Apparel | | | 119,000 | | | | 340,719 | |

| | Kweichow Moutai Co., Ltd. - A Shares + | | Food, Beverage & Tobacco | | | 2,800 | | | | 404,799 | |

| | Midea Group Co., Ltd. - A Shares + | | Consumer Durables & Apparel | | | 33,000 | | | | 256,617 | |

| | Momo Inc. - ADR # | | Media & Entertainment | | | 12,600 | | | | 441,882 | |

| | NetEase, Inc. - ADR | | Media & Entertainment | | | 2,315 | | | | 658,687 | |

| | Ping An Insurance (Group) Company of China Limited - H Shares + | | Insurance | | | 80,200 | | | | 966,343 | |

| | Shanghai International Airport Co., Ltd. - A Shares + | | Transportation | | | 37,000 | | | | 387,903 | |

| | Shenzhou International Group Holdings Ltd. + | | Consumer Durables & Apparel | | | 44,000 | | | | 589,332 | |

| | SINA Corporation * | | Media & Entertainment | | | 4,300 | | | | 270,642 | |

| | Tencent Holdings Limited + | | Software & Services | | | 45,400 | | | | 2,249,241 | |

| | ZTO Express (Cayman) Inc. - ADR # | | Transportation | | | 30,600 | | | | 609,858 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 13,359,647 | |

|

| |

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 25 | |

| | |

| Thomas White Emerging Markets Fund | | |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

| HONG KONG (0.8%) | | | | | | | | |

| | Thai Beverage Public Company Limited + | | Food, Beverage & Tobacco | | | 511,600 | | | | $316,317 | |

|

| |

| INDIA (8.8%) | | | | | | | | |

| | Coal India Limited + | | Energy | | | 115,700 | | | | 419,894 | |

| | Exide Industries Ltd. + | | Automobiles & Components | | | 94,300 | | | | 290,319 | |

| | HDFC Bank Ltd. - ADR | | Banks | | | 4,800 | | | | 550,320 | |

| | ITC Limited + | | Food, Beverage & Tobacco | | | 84,500 | | | | 366,139 | |

| | Larsen & Toubro Ltd + | | Capital Goods | | | 18,200 | | | | 352,896 | |

| | Mahindra & Mahindra Ltd. - GDR + | | Automobiles & Components | | | 47,198 | | | | 432,392 | |

| | Vedanta Limited + | | Materials | | | 134,500 | | | | 322,606 | |

| | WNS (Holdings) Ltd. - ADR * | | Software & Services | | | 9,900 | | | | 565,785 | |

| | YES BANK Limited + | | Banks | | | 78,400 | | | | 189,986 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 3,490,337 | |

|

| |

| INDONESIA (3.4%) | | | | | | | | |

| | PT Bank Negara Indonesia (Persero) Tbk * + | | Banks | | | 772,800 | | | | 520,603 | |

| | PT Matahari Department Store Tbk + | | Retailing | | | 713,600 | | | | 203,933 | |

| | PT Telekomunikasi Indonesia Persero Tbk + | | Telecommunication Services | | | 1,006,000 | | | | 268,461 | |

| | PT United Tractors Tbk + | | Energy | | | 189,400 | | | | 361,176 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,354,173 | |

|

| |

| MALAYSIA (1.0%) | | | | | | | | |

| | CIMB Group Holdings Berhad + | | Banks | | | 312,800 | | | | 398,699 | |

|

| |

| MEXICO (4.3%) | | | | | | | | | | |

| | Cemex SAB de CV * # | | Materials | | | 534,720 | | | | 247,648 | |

| | Grupo Aeroportuario del Sureste SAB de CV - Class B | | Transportation | | | 21,300 | | | | 349,784 | |

| | Grupo Financiero Banorte, S.A.B. de C.V. - Class O | | Banks | | | 129,100 | | | | 818,003 | |

| | Wal-Mart de Mexico S.A.B. de C.V. | | Food & Staples Retailing | | | 95,100 | | | | 279,414 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,694,849 | |

|

| |

| PANAMA (0.9%) | | | | | | | | | | |

| | Banco Latinoamericano de Comercio Exterior, S.A. - E Shares # | | Diversified Financials | | | 17,100 | | | | 369,873 | |

|

| |

| PHILIPPINES (1.7%) | | | | | | | | |

| | Metropolitan Bank & Trust Company + | | Banks | | | 253,972 | | | | 361,829 | |

| | Semirara Mining and Power Corporation + | | Energy | | | 695,700 | | | | 318,470 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 680,299 | |

|

| |

| POLAND (1.1%) | | | | | | | | | | |

| | Bank Polska Kasa Opieki SA + | | Banks | | | 5,700 | | | | 169,671 | |

| | KGHM Polska Miedz S.A. * + | | Materials | | | 10,600 | | | | 285,998 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 455,669 | |

|

| |

The accompanying notes are an integral part of these financial statements

| | |

| 26 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

| RUSSIA (5.2%) | | | | | | | | | | |

| | LUKOIL PJSC - ADR + | | Energy | | | 14,700 | | | | $1,250,756 | |

| | Sberbank of Russia PJSC - ADR + | | Banks | | | 56,075 | | | | 806,124 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,056,880 | |

|

| |

| SOUTH AFRICA (4.4%) | | | | | | | | |

| | Absa Group Limited + | | Banks | | | 24,500 | | | | 281,308 | |

| | FirstRand Limited + | | Diversified Financials | | | 71,000 | | | | 337,026 | |

| | Naspers Limited - N Shares + | | Media & Entertainment | | | 4,350 | | | | 1,111,129 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,729,463 | |

|

| |

| SOUTH KOREA (10.3%) | | | | | | | | |

| | KB Financial Group Inc. + | | Banks | | | 10,550 | | | | 417,307 | |

| | Korea Zinc Co Ltd + | | Materials | | | 1,075 | | | | 416,461 | |

| | LG Chem Ltd. + | | Materials | | | 875 | | | | 271,082 | |

| | LG Household & Health Care Ltd. + | | Household & Personal Products | | | 490 | | | | 596,656 | |

| | POSCO + | | Materials | | | 1,425 | | | | 311,199 | |

| | Samsung Electronics Co., Ltd. + | | Technology Hardware & Equipment | | | 39,950 | | | | 1,565,360 | |

| | Shinhan Financial Group Co., Ltd. + | | Banks | | | 14,025 | | | | 529,569 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 4,107,634 | |

|

| |

| TAIWAN (6.9%) | | | | | | | | |

| | Catcher Technology Co., Ltd + | | Technology Hardware & Equipment | | | 33,000 | | | | 261,140 | |

| | Largan Precision Company Limited + | | Technology Hardware & Equipment | | | 3,000 | | | | 451,477 | |

| | Taiwan Semiconductor Manufacturing Company, Ltd. + | | Semiconductors & Semiconductor Equipment | | | 240,700 | | | | 2,033,211 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,745,828 | |

|

| |

| THAILAND (2.7%) | | | | | | | | |

| | Airports of Thailand Public Company Ltd. + | | Transportation | | | 162,400 | | | | 348,717 | |

| | Kasikornbank Public Company Limited + | | Banks | | | 48,400 | | | | 288,929 | |

| | PTT Exploration and Production Public Company Limited + | | Energy | | | 108,100 | | | | 452,390 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,090,036 | |

|

| |

| TURKEY (0.5%) | | | | | | | | |

| | Turkcell Iletisim Hizmetleri AS + | | Telecommunication Services | | | 91,600 | | | | 191,879 | |

|

| |

| UNITED STATES (1.0%) | | | | | | | | |

| | Cognizant Technology SolutionsCorporation - A Shares | | Software & Services | | | 5,400 | | | | 393,984 | |

|

| |

Total Common

Stocks | | | | (Cost $28,838,501) | | | | | | | 36,354,383 | |

| | | | | | | | | | | | |

|

| |

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 27 | |

| | |

| Thomas White Emerging Markets Fund | | |

| | | | | | | | | | | | |

| Country | | Issue | | Industry | | Shares | | | Value (US$) | |

| | | | | | | | | | | |

PREFERRED

STOCKS (5.5%) | | | | | | | | | | |

|

| |

| BRAZIL (4.5%) | | | | | | | | | | |

| | Banco Bradesco S.A. (7/25/19, N/A) ^ | | Banks | | | 39,600 | | | | $359,531 | |

| | Gerdau S.A. (8/7/19, 1.01%) ^ | | Materials | | | 119,300 | | | | 432,037 | |

| | Itau Unibanco Holding S.A. (7/29/19, 0.51%) ^ | | Banks | | | 35,423 | | | | 306,612 | |

| | Petroleo Brasileiro SA Petrobras (7/25/19, 0.07%) ^ | | Energy | | | 100,200 | | | | 693,026 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,791,206 | |

|

| |

| SOUTH KOREA (1.0%) | | | | | | | | |

| | Samsung Electronics Co., Ltd. (7/8/19, 3.95%) ^ + | | Semiconductors & Semiconductor Equipment | | | 12,500 | | | | 397,447 | |

|

| |

Total Preferred

Stocks | | | | (Cost $1,930,722) | | | | | | | 2,188,653 | |

| | | | | | | | | | | | |

|

| |

| REAL ESTATE INVESTMENT TRUST (REIT) (0.8%) | | | | | | | | | | |

|

| |

| MEXICO (0.8%) | | | | | | | | |

| | Fibra Uno Administracion SA de CV | | Real Estate | | | 212,600 | | | | 315,125 | |

|

| |

| Total REIT | | | | (Cost $268,290) | | | | | | | 315,125 | |

| | | | | | | | | | | | |

|

| |

SHORT TERM

INVESTMENT (2.1%) | | | | | | | | | | |

|

| |

| MONEY MARKET FUND (2.1%) | | | | | | | | |

| | Northern Institutional Treasury Portfolio, 2.34%(a) | | | | | 844,564 | | | | 844,564 | |

|

| |

Total Short Term

Investment | | (Cost $844,564) | | | | | | | 844,564 | |

| | | | | | | | | | | | |

|

| |

| | | | |

HELD AS COLLATERAL

FOR SECURITIES LENDING (0.7%) | | | | | | | | | | | | |

|

| |

SHORT TERM

INVESTMENT (0.7%) | | | | | | | | | | |

|

| |

| MONEY MARKET FUND (0.7%) | | | | | | | | |

| | Northern Institutional Liquid Assets Portfolio, 2.46%(a) | | | | | 267,360 | | | | 267,360 | |

|

| |

Total held as

collateral for

securities lending | | (Cost $267,360) | | | | | | | 267,360 | |

| | | | | | | | | | | | |

|

| |

| Total Investments | | 100.5% | | (Cost $32,149,437) | | | | | | | $39,970,085 | |

Liabilities in

excess of other

assets | | (0.5)% | | | | | | | | | (198,394 | ) |

| Total Net Assets: | | 100.0% | | | | | | | | | $39,771,691 | |

|

| |

The accompanying notes are an integral part of these financial statements

| | |

| 28 | | www.thomaswhitefunds.com |

| | |

| Investment Portfolio (Unaudited) | | April 30, 2019 |

| * | Non-Income Producing Securities |

| # | All or a portion of securities on loan at April 30, 2019. The market value of the securities loaned was $1,611,893. The loaned securities were secured with cash collateral of $267,360 andnon-cash collateral with a value of $1,392,086. Thenon-cash collateral received consists of short term investments and long term bonds, and is held for the benefit of the Fund at the Fund’s custodian. The Fund cannot repledge or resell this collateral. Collateral is calculated based on prior day’s prices. - See Note 1(I) to Financial Statements |

| ^ | Maturity Date and Preferred Dividend Rate of Preferred Stock |

| ADR | - American Depositary Receipt |

| GDR | - Global Depositary Receipt |

Industry classifications shown in the Investment Portfolio are based off of the Global Industry Classification Standard (GICS®). GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The accompanying notes are an integral part of these financial statements

| | | | |

| www.thomaswhitefunds.com | | | 29 | |

| | |

| Thomas White Emerging Markets Fund | | |

The following table summarizes the inputs used, as of April 30, 2019, in valuating the Fund’s assets:

| | | | | | | | | | | | | | | | |

| | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | | | | | | | | | | | | | | | |

| | | | | |

| Argentina | | | $239,422 | | | | $------- | | | | $------- | | | | $239,422 | |

| | | | | |