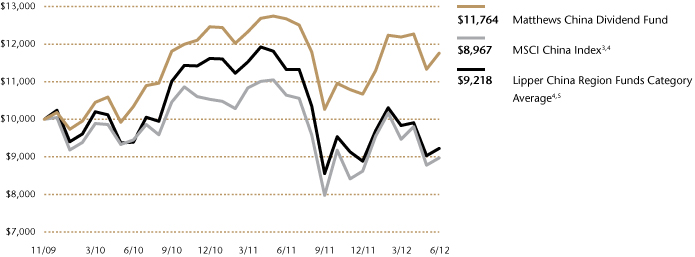

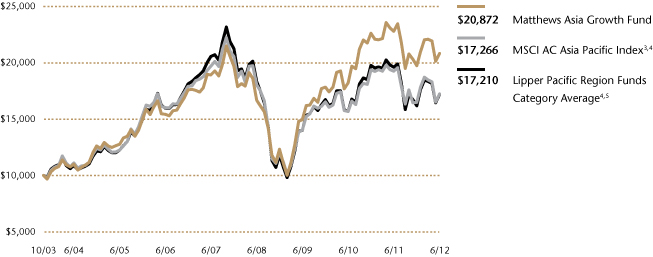

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-08510 |

|

Matthews International Funds |

(Exact name of registrant as specified in charter) |

|

Four Embarcadero Center, Suite 550 San Francisco, CA 94111 |

(Address of principal executive offices) (Zip code) |

|

William J. Hackett, President Four Embarcadero Center, Suite 550 San Francisco, CA 94111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 415-788-7553 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | June 30, 2012 | |

| | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Matthews Asia Funds | Semi-Annual Report

June 30, 2012 | matthewsasia.com

ASIA FIXED INCOME STRATEGY

Matthews Asia Strategic Income Fund

ASIA GROWTH AND INCOME STRATEGIES

Matthews Asian Growth and Income Fund

Matthews Asia Dividend Fund

Matthews China Dividend Fund

ASIA GROWTH STRATEGIES

Matthews Asia Growth Fund

Matthews Pacific Tiger Fund

Matthews China Fund

Matthews India Fund

Matthews Japan Fund

Matthews Korea Fund

ASIA SMALL COMPANY STRATEGIES

Matthews Asia Small Companies Fund

Matthews China Small Companies Fund

ASIA SPECIALTY STRATEGY

Matthews Asia Science and Technology Fund

'12

Performance and Expenses

| | | | | Average Annual Total Return | | | | 2011 Gross

Annual | |

| | | 1 year | | 5 years | | 10 years | | Since

Inception | | Inception

Date | | Operating

Expenses* | |

| Matthews Asia Strategic Income Fund | |

| Investor Class (MAINX) | | | n.a. | | | | n.a. | | | | n.a. | | | | 3.64 | %1 | | | 11/30/11 | | | | 1.93 | %2 | |

| After Fee Waiver and Reimbursement | | | | | | | | | | | | | | | | | | | | | | | 1.40 | %3 | |

| Institutional Class (MINCX) | | | n.a. | | | | n.a. | | | | n.a. | | | | 3.73 | %1 | | | 11/30/11 | | | | 1.78 | %2 | |

| After Fee Waiver and Reimbursement | | | | | | | | | | | | | | | | | | | | | | | 1.25 | %3 | |

| Matthews Asian Growth & Income Fund | |

| Investor Class (MACSX) | | | -3.68 | % | | | 4.08 | % | | | 12.33 | % | | | 10.49 | % | | | 9/12/94 | | | | 1.12 | % | |

| Institutional Class (MICSX) | | | -3.55 | % | | | n.a. | | | | n.a. | | | | 0.33 | % | | | 10/29/10 | | | | 0.99 | % | |

| Matthews Asia Dividend Fund | |

| Investor Class (MAPIX) | | | -3.30 | % | | | 6.95 | % | | | n.a. | | | | 9.51 | % | | | 10/31/06 | | | | 1.10 | % | |

| Institutional Class (MIPIX) | | | -3.21 | % | | | n.a. | | | | n.a. | | | | 0.51 | % | | | 10/29/10 | | | | 1.00 | % | |

| Matthews China Dividend Fund | |

| Investor Class (MCDFX) | | | -7.25 | % | | | n.a. | | | | n.a. | | | | 6.50 | % | | | 11/30/09 | | | | 1.52 | % | |

| After Fee Waiver and Reimbursement | | | | | | | | | | | | | | | | | | | | | | | 1.50 | %4 | |

| Institutional Class (MICDX) | | | -7.05 | % | | | n.a. | | | | n.a. | | | | -1.04 | % | | | 10/29/10 | | | | 1.31 | % | |

| Matthews Asia Growth Fund | |

| Investor Class (MPACX) | | | -8.58 | % | | | 1.94 | % | | | n.a. | | | | 8.86 | % | | | 10/31/03 | | | | 1.18 | % | |

| Institutional Class (MIAPX) | | | -8.46 | % | | | n.a. | | | | n.a. | | | | -3.12 | % | | | 10/29/10 | | | | 1.03 | % | |

| Matthews Pacific Tiger Fund | |

| Investor Class (MAPTX) | | | -8.34 | % | | | 4.73 | % | | | 14.57 | % | | | 8.68 | % | | | 9/12/94 | | | | 1.11 | % | |

| Institutional Class (MIPTX) | | | -8.20 | % | | | n.a. | | | | n.a. | | | | -2.80 | % | | | 10/29/10 | | | | 0.95 | % | |

| Matthews China Fund | |

| Investor Class (MCHFX) | | | -17.13 | % | | | 2.81 | % | | | 14.40 | % | | | 10.72 | % | | | 2/19/98 | | | | 1.13 | % | |

| Institutional Class (MICFX) | | | -16.94 | % | | | n.a. | | | | n.a. | | | | -11.45 | % | | | 10/29/10 | | | | 0.96 | % | |

| Matthews India Fund | |

| Investor Class (MINDX) | | | -23.88 | % | | | -0.16 | % | | | n.a. | | | | 9.33 | % | | | 10/31/05 | | | | 1.18 | % | |

| Institutional Class (MIDNX) | | | -23.72 | % | | | n.a. | | | | n.a. | | | | -18.35 | % | | | 10/29/10 | | | | 0.99 | % | |

| Matthews Japan Fund | |

| Investor Class (MJFOX) | | | -5.69 | % | | | -3.92 | % | | | 2.98 | % | | | 3.52 | % | | | 12/31/98 | | | | 1.21 | % | |

| Institutional Class (MIJFX) | | | -5.54 | % | | | n.a. | | | | n.a. | | | | 3.59 | % | | | 10/29/10 | | | | 1.07 | % | |

| Matthews Korea Fund | |

| Investor Class (MAKOX) | | | -10.28 | % | | | -0.76 | % | | | 10.84 | % | | | 5.13 | % | | | 1/3/95 | | | | 1.18 | % | |

| Institutional Class (MIKOX) | | | -10.08 | % | | | n.a. | | | | n.a. | | | | 3.51 | % | | | 10/29/10 | | | | 1.07 | % | |

| Matthews Asia Small Companies Fund | |

| Investor Class (MSMLX) | | | -17.24 | % | | | n.a. | | | | n.a. | | | | 17.56 | % | | | 9/15/08 | | | | 1.52 | % | |

| Matthews China Small Companies Fund | |

| Investor Class (MCSMX) | | | -26.16 | % | | | n.a. | | | | n.a. | | | | -27.23 | % | | | 5/31/11 | | | | 5.32 | %2 | |

| After Fee Waiver and Reimbursement | | | | | | | | | | | | | | | | | | | | | | | 2.00 | %5 | |

| Matthews Asia Science and Technology Fund | |

| Investor Class (MATFX) | | | -12.69 | % | | | -0.38 | % | | | 9.12 | % | | | -0.71 | % | | | 12/27/99 | | | | 1.21 | % | |

* These figures are from the Funds' current prospectus and may differ from the actual expense ratios for the preceding fiscal year, as shown in the Financial Highlights section of this report.

1 Actual return for fiscal period beginning 11/30/11 through 6/30/12, not annualized.

2 Gross annual operating expenses for 2011 are annualized.

3 Matthews has contractually agreed to waive fees and reimburse expenses until August 31, 2014 to the extent needed to limit Total Annual Fund Operating Expenses to 1.25% for the Institutional Class and agreed to reduce the expense ratio by an equal amount for the Investor Class. Because certain expenses of the Investor Class may be higher than the Institutional Class, the Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may exceed 1.25%. The amounts of the waivers and reimbursements are based on estimated Fund expenses. The fee waiver and expense reimbursement may be terminated at any time by the Fund on 60 days' written notice.

4 The Advisor has contractually agreed to waive the Fund's fees and reimburse expenses until at least August 31, 2013 to the extent needed to limit total annual operating expenses to 1.50%.

5 The Advisor has contractually agreed to waive the Fund's fees and reimburse expenses until at least August 31, 2014 to the extent needed to limit total annual operating expenses to 2.00%.

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds' fees and expenses had not been waived, returns would have been lower. For the Funds' most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds' prospectus and Statement of Additional Information for more risk disclosure.

Contents

| Message to Shareholders | | | 2 | | |

|

| Manager Commentaries, Fund Characteristics and Schedules of Investments: | |

|

| ASIA FIXED INCOME STRATEGY | |

|

| Matthews Asia Strategic Income Fund | | | 4 | | |

|

| ASIA GROWTH AND INCOME STRATEGIES | |

|

| Matthews Asian Growth and Income Fund | | | 9 | | |

|

| Matthews Asia Dividend Fund | | | 14 | | |

|

| Matthews China Dividend Fund | | | 19 | | |

|

| ASIA GROWTH STRATEGIES | |

|

| Matthews Asia Growth Fund | | | 24 | | |

|

| Matthews Pacific Tiger Fund | | | 29 | | |

|

| Matthews China Fund | | | 34 | | |

|

| Matthews India Fund | | | 39 | | |

|

| Matthews Japan Fund | | | 44 | | |

|

| Matthews Korea Fund | | | 49 | | |

|

| ASIA SMALL COMPANY STRATEGIES | |

|

| Matthews Asia Small Companies Fund | | | 54 | | |

|

| Matthews China Small Companies Fund | | | 59 | | |

|

| ASIA SPECIALTY STRATEGY | |

|

| Matthews Asia Science and Technology Fund | | | 64 | | |

|

| Disclosures | | | 68 | | |

|

| Index Definitions | | | 69 | | |

|

| Disclosure of Fund Expenses | | | 70 | | |

|

| Statements of Assets and Liabilities | | | 72 | | |

|

| Statements of Operations | | | 75 | | |

|

| Statements of Changes in Net Assets | | | 78 | | |

|

| Financial Highlights | | | 85 | | |

|

| Notes to Financial Statements | | | 98 | | |

|

Cover photo: Open umbrella under tree, Kyoto, Japan

This report has been prepared for Matthews Asia Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds' investment objectives, risks and expenses. Additional copies of the prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of June 30, 2012. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund's future investment intent. Current and future portfolio holdings are subject to risk.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

Matthews Asia Funds are distributed in the United States by Foreside Funds Distributors LLC, Berwyn, Pennsylvania

Matthews Asia Funds are distributed in Latin America by HMC Partners

"We focus on companies that we believe will be good stewards of capital; that allocate investments carefully and delight in creating value for shareholders..."

Message to Shareholders

from the Investment Advisor

July 2012

Dear Fellow Shareholders,

According to legend, King Midas gained the power to turn everything that he touched into gold. Delighted with this power, he touched the branch of a tree and it turned to gold. But he soon found himself unable to drink or eat as anything that touched his lips aurified instantly. His final tragedy came when, heedless of his despairing protests, his daughter embraced him and thus was transformed into a priceless, lifeless golden statue. Midas had managed to deprive his life of all value.

I see parallels in the current market environment. Cash, cash and cash—it is all that anyone seems to care about at the moment. European nations need it to pay down debt as do U.S. homeowners and China's local governments. Central banks, meanwhile, seem disinclined to increase the rate at which new cash is supplied. That is the case even in the U.S. and Europe, but it is particularly striking in Asia where central banks have been following quite a tight policy. This has all led to a scramble for cash and, as a consequence, machines idle and rust and labor languishes unemployed. At least in my view, these investors appear to be focusing on the value of cash to the extent that they lose sight of value elsewhere. Midas eventually starved for his love of gold and it is hard not to draw the conclusion that love of cash is starving the world of economic activity and starving labor of potential productivity.

Investors have also bid up prices of the "next best thing to cash"—U.S. treasuries, for example. And they have bid down prices of what are seen as riskier assets such as Asian equities. The notion of a "risk on, risk off" narrative has also added the fuel of a short-term mentality to this investment approach. It has brought valuations in Asia's markets down to levels that are below historic 20-year averages. At the end of the second quarter, a broad-based universe of Asia ex-Japan stocks was trading on about 10X forward 12-month earnings. This is about a 20% discount to that 20-year average, which has historically been an infrequent occurrence. The current Asia ex-Japan dividend yield of 2.7% is similarly infrequently seen. Given the slow drips of bad news out of the U.S. and Europe, the markets have had plenty of time to ruminate on risks to short-term and long-term growth. This is not a fast-moving crisis, and much analysis has been focused on the issues concerning investors. This means it is not something that the markets have had to try to digest quickly with no past knowledge, insight or experience. Consequently, the low valuations are based on relatively subdued forecasts for the near term. Margins are expected to decline year-over-year.

For us, it does mean that there is more value in the markets than there has been in a while. And as a portfolio manager, it is always enticing to see established, seasoned businesses offering good dividend or cash flow yields, particularly when convinced of the long-term demand for their services or products. The frustration of a portfolio manager is, of course, that at the very time when there are so many enticing options, you often don't have the cash to capture that value. At Matthews, portfolio managers witness the high value many investors place on cash—one of the things that we value least. Cash levels in the Funds reflect this. We generally remain fully invested.

2 MATTHEWS ASIA FUNDS

It is not that we don't care about cash—indeed we focus on companies that we believe will be good stewards of capital; that allocate investments carefully, and delight in creating value for shareholders or returning cash to them. As portfolio managers, we are interested in cash only to immediately put it to work, for we see a greater value in what we believe to be the underappreciated potential of Asia's 4 billion people. In the past, extreme demand for cash has often been transitory—which is not the assumption that markets seem to be making about today's world. The "new normal" and similar discussions of a loss of potential output in the global economy make sense to me only if they are a surrender to the idea that this love of cash will be much longer-lasting. Whether or not that assumption is right, it seems to be less appropriate for Asia, where the proximate cause of demand for cash may be the fact that policymakers and central banks have been following relatively tight policies. Compare this policy conservatism with the rest of the world in which one can blame the accumulation of excessive debt over years, even decades. For us, it remains a view that seems to be at odds with the broad sweep of Asia's development and also with our discussions in recent company meetings.

We are meeting companies at a faster pace this year than we did last year. This is partly because we are in the enviable position of having been able to increase our investment team's research resources over the past year and now have "more hands on the wheel." It is also because during these times, when everyone is focusing on cash, short-term trends and the macro picture, we think it is best to take a view which the market may view as contrarian.

As I mentioned in some of my previous communications, we spend a lot of time looking at India and China, particularly small-capitalization companies. But, in truth, the opportunities are quite broad-based across countries and industries. We have seen some effect of the slowdown in global growth. Nevertheless, many of the companies we visit are focused on domestic demand and are somewhat insulated from the weakness in Europe and the U.S.

The portfolios remain fully invested: biased toward businesses that we believe will grow profitably over the coming decades from the growth in spending of Asia's households, the development of new products, the enjoyment of new services and the enhanced expression of individual tastes and preferences. As such we hope to avoid King Midas's fate, to focus instead on what can be valued over the long term.

As always, it is a privilege to act as your investment advisor.

Robert Horrocks, PhD

Chief Investment Officer

Matthews International Capital Management, LLC

Shareholder Notification

Dear Valued Investor,

Beginning with the quarter ending September 30, 2012, Matthews will cease its production of the First Quarter and Third Quarter shareholder reports. The information previously contained in these reports has been and will continue to be available on matthewsasia.com.

As many of our communications are now accessed primarily online, we believe that eliminating these reports—and publishing the information online—is not only a more time-efficient means of communicating updates, but will also result in cost savings for shareholders. All elements previously contained in the First and Third Quarter reports can be found on matthewsasia.com, including:

• Message to Shareholders from the Investment Advisor

• Fund Manager Commentaries

• Performance and Expenses

• Top 10 and Portfolio Holdings

• Fund Characteristics

matthewsasia.com | 800.789.ASIA 3

ASIA FIXED INCOME STRATEGY

PORTFOLIO MANAGERS

Teresa Kong, CFA

Lead Manager

Gerald M. Hwang, CFA, Robert J. Horrocks, PhD

Co-Managers

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MAINX | | MINCX | |

| CUSIP | | 577125503 | | 577125602 | |

| Inception | | 11/30/11 | | 11/30/11 | |

| NAV | | $10.18 | | $10.18 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.93% | | 1.78% | |

After fee waiver,

Reimbursement and

Recoupment | | 1.40% | | 1.25% | |

Portfolio Statistics

| Total # of Positions | | 46 | |

| Net Assets | | $23.2 million | |

| Modified Duration | | 5.1 years2 | |

| Portfolio Turnover | | 3.66%3 | |

Benchmarks

HSBC Asian Local Bond Index

J.P. Morgan Asia Credit Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Total return over the long term with an emphasis on income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total assets, which include borrowings for investment purposes, in income-producing securities including, but not limited to, debt and debt-related instruments issued by governments, quasi-governmental entities, supra-national institutions, and companies in Asia. Investments may be denominated in any currency, and may represent any part of a company's capital structure from debt to equity or with features of both.

1 Gross annual operating expenses for the Fund for 2011 are annualized. The Advisor has contractually agreed to waive fees and reimburse expenses until August 31, 2014 to the extent needed to limit Total Annual Fund Operating Expenses to 1.25% for the Institutional Class and agreed to reduce the expense ratio by an equal amount for the Investor Class. Because certain expenses of the Investor Class may be higher than the Institutional Class, the Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may exceed 1.25%. The amounts of the waivers and reimbursements are based on estimated Fund expenses. The fee waiver and expense reimbursement may be terminated at any time by the Fund on 60 days' written notice. Matthews Asia Funds does not charge 12b-1 fees.

2 Modified duration measures the percent change in value of the fixed income portion of the portfolio in response to a 1% change in interest rates. In a multi-currency denominated portfolio with sensitivities to different interest rate regimes, modified duration will not accurately reflect the change in value of the overall portfolio from a change in any one interest rate regime.

3 Not annualized. The Fund commenced operations on November 30, 2011. The lesser of fiscal year 2011 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary

For the first half of 2012, the Matthews Asia Strategic Income Fund gained 4.18% (Investor Class) and 4.27% (Institutional Class) while its primary benchmark, the HSBC Asian Local Bond Index and its secondary benchmark, the J.P. Morgan Asia Credit Index, gained 2.35% and 6.68%, respectively. For the quarter ended June 30, the Fund returned 0.59% (Investor Class) and 0.64% (Institutional Class), while the indices returned –0.42% and 2.60%, respectively.

Overall, securities with consistent and sustainable cash flows did well during this period of uncertainty and low global yields. The top contributor to performance by issuer was the Republic of Philippines during the second quarter. Philippines bonds rallied on positive performance in credit, currency and interest rates. The credit spread on the U.S. dollar-denominated Republic of Philippines bonds tightened on expectations that this sovereign will be the next to be upgraded to investment grade status. The Philippine peso was the second best returning currency after the Japanese yen over the quarter with a spot return of 1.82%. The country's robust economy and continued foreign inflows sustained the strength of the peso. The policy rate remained stable at 4%, with inflation coming in lower than expected despite robust GDP growth. Local interest rates fell with greater demand for the Republic of Philippines bonds, driving up prices.

The biggest detractors to performance during the second quarter included positions denominated in Indonesian rupiah and Malaysian ringgit and the Japanese yen. The Fund's Indonesian rupiah-denominated, Indonesian Government bonds (due 2021) and Malaysian ringgit-denominated Malaysian Government bonds (due 2021) lagged due to the underperformance of these currencies relative to the U.S. dollar. Conversely, the Fund's short position in a Japanese yen currency forward underperformed due to the outperformance of the Japanese yen against the U.S. dollar.

Across global bond markets, government yields have hit historic lows. The U.S. 10-year Treasury yield reached 1.45% in June, the lowest yield since the founding of the New York Stock Exchange in 1792. At the same time, yields for Hong Kong and Singapore government bonds also hit multi-decade lows of 0.97% and 1.40%, respectively. This leads us to conclude that central banks are willing to keep interest rates low so capital remains cheap in order to re-start growth. It is at times like this when investors seem to have an insatiable appetite for assets considered "risk-free." We believe a contrarian approach is appropriate. Hence, we have adjusted the portfolio's credit, currency and interest rate positioning.

First on credit, we want to highlight the Fund's increased exposure to Chinese property. Chinese property is going through a perfect storm on three fronts: A slowdown in exports driven by the recession in Europe and slow recovery in the U.S.; the oversupply of residential property driven by China's stimulus in 2008—2009; and uncertainty stemming from China's once in a decade power transition. While the problems in Europe and the U.S. are persistent, we see China's housing oversupply and political issues as temporary in nature and may already be on the mend. While the property sector as a whole still faces challenges, we are finding value in solid companies whose bonds have priced in much of the downside. Specifically, we like developers with large shares in their local markets, strong balance sheets and access to capital. We believe these developers are likely going to gain market share at the detriment of

(continued)

4 MATTHEWS ASIA FUNDS

PERFORMANCE AS OF JUNE 30, 2012

| | | Actual Return,

Not Annualized | | | |

| | | 3 Months | | Since

Inception | | Inception

Date | |

| Investor Class (MAINX) | | | 0.59 | % | | | 3.64 | % | | 11/30/11 | |

| Institutional Class (MINCX) | | | 0.64 | % | | | 3.73 | % | | 11/30/11 | |

| HSBC Asian Local Bond Index4 | | | -0.42 | % | | | 3.13 | % | | | | | |

| J.P. Morgan Asia Credit Index4 | | | 2.60 | % | | | 7.63 | % | | | | | |

| Lipper Emerging Market Debt Category Average5 | | | -0.07 | % | | | 6.83 | % | | | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance visit matthewsasia.com.

The performance data does not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

4 It is not possible to invest directly in an index. Source: Index data from HSBC and J.P. Morgan; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 69 for index definition.

5 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

INCOME DISTRIBUTION HISTORY

| | | 2012 | | 2011 | |

| | | Q1 | | Q2 | | Q3 | | Q4 | | Total | | Q1 | | Q2 | | Q3 | | Q4 | | Total | |

| Investor Class (MAINX) | | $ | 0.09 | | | $ | 0.07 | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.02 | | | $ | 0.02 | | |

| Institutional Class (MINCX) | | $ | 0.10 | | | $ | 0.07 | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.02 | | | $ | 0.02 | | |

Note: This table does not include capital gains distributions. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

3.87% (Investor Class) 4.02% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/12, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc

YIELD TO WORST:

4.93%

Yield to worst is the lowest yield that can be received on a bond assuming that the issuer does not default. It is calculated by utilizing the worst case assumptions for a bond with respect to certain income-reducing factors, including prepayment, call or sinking fund provisions. It does not represent the yield that an investor should expect to receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems

TOP TEN POSITIONS6

| | | Sector | | Currency | | % Net Assets | |

| Malaysian Government Bond, 4.160%, 7/15/2021 | | Government Bonds | | Malaysian Ringgit | | | 7.1 | % | |

| Indonesia Government Bond, 8.250%, 7/15/2021 | | Government Bonds | | Indonesian Rupiah | | | 4.7 | % | |

| Korea Treasury Bond, 3.500%, 9/10/2016 | | Government Bonds | | Korean Won | | | 3.8 | % | |

| Longfor Properties Co., Ltd., 9.500%, 4/7/2016 | | Financials | | U.S. Dollar | | | 3.4 | % | |

| Melco Crown Entertainment, Ltd., 3.750%, 5/9/2013 | | Consumer Discretionary | | Chinese Renminbi | | | 3.3 | % | |

| Republic of Philippines, 6.250%, 1/14/2036 | | Government Bonds | | Philippine Peso | | | 3.3 | % | |

| KWG Property Holding, Ltd., 12.500%, 8/18/2017 | | Financials | | U.S. Dollar | | | 3.1 | % | |

| Galaxy Entertainment Group, Ltd., 4.625%, 12/16/2013 | | Consumer Discretionary | | Chinese Renminbi | | | 3.1 | % | |

| Axiata SPV1 Labuan, Ltd., 5.375%, 4/28/2020 | | Telecommunication Services | | U.S. Dollar | | | 3.0 | % | |

| Global Logistic Properties, Ltd., 3.375%, 5/11/2016 | | Financials | | Chinese Renminbi | | | 3.0 | % | |

| % OF ASSETS IN TOP TEN | | | | | | | 37.8 | % | |

6 Holdings may combine more than one security from same issuer and related depositary receipts.

CURRENCY ALLOCATION (%)7,8

| U.S. Dollar (USD) | | | 44.1 | | |

| Chinese Renminbi (CNY) | | | 11.4 | | |

| Korean Won (KRW) | | | 8.9 | | |

| Malaysian Ringgit (MYR) | | | 8.5 | | |

| Philippine Peso (PHP) | | | 6.1 | | |

| Singapore Dollar (SGD) | | | 5.3 | | |

| Indonesian Rupiah (IDR) | | | 4.7 | | |

| Thai Baht (THB) | | | 3.4 | | |

| Hong Kong Dollar (HKD) | | | 2.7 | | |

| Cash and Other Assets, Less Liabilities | | | 4.9 | | |

7 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

8 Cash and other assets may include forward currency exchange contracts and certain derivative instruments that have been marked-to-market.

COUNTRY ALLOCATION (%)8

(By issuer's country of risk)

| China/Hong Kong | | | 27.7 | | |

| Philippines | | | 14.7 | | |

| South Korea | | | 12.5 | | |

| Malaysia | | | 11.5 | | |

| Indonesia | | | 9.8 | | |

| Thailand | | | 7.1 | | |

| Singapore | | | 6.6 | | |

| Australia | | | 2.6 | | |

| Sri Lanka | | | 1.6 | | |

| Japan | | | 1.0 | | |

| Cash And Other Assets, Less Liabilities | | | 4.9 | | |

matthewsasia.com | 800.789.ASIA 5

SECTOR ALLOCATION (%)9

| Government Bonds | | | 34.9 | | |

| Financials | | | 28.7 | | |

| Consumer Discretionary | | | 8.6 | | |

| Industrials | | | 8.2 | | |

| Telecommunication Services | | | 5.0 | | |

| Energy | | | 4.9 | | |

| Utilities | | | 3.2 | | |

| Information Technology | | | 1.6 | | |

Cash and Other Assets,

Less Liabilities | | | 4.9 | | |

ASSET TYPE BREAKDOWN (%)9,10

| Corporate Bonds | | | 53.4 | | |

| Government Bonds | | | 34.9 | | |

| Common Equities and ADRs | | | 6.8 | | |

Cash and Other Assets,

Less Liabilities | | | 4.9 | | |

9 Cash and other assets may include forward currency exchange contracts and certain derivative instruments that have been marked-to-market.

10 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary (continued)

smaller players who are over-leveraged or do not have the balance sheets to ride out this downturn.

Second, in terms of our currency exposure, on the margin, we have found more interesting opportunities in U.S. dollar-denominated Asian corporate bonds. Our U.S. dollar exposure is approximately 5% higher than it was at the end of the first quarter and is about 10% higher than it was at the end of 2011. During the quarter, we reduced the portfolio's exposure to the Indonesian rupiah (by selling rupiah-denominated Indonesian Government bonds) given the country's overly loose monetary policy and increasingly protectionist policies that could depress foreign interest going forward. These policies include limiting participation of foreign banks in Indonesia's foreign exchange market, as well as potential limitations on foreign ownership of Indonesian banks.

Finally, in terms of interest rate exposure, we moderated our exposure to Indonesia given our view that interest rates were much more likely to rise than fall. We saw the long end of the yield curve as being especially vulnerable given the relative flatness of the curve. As such, we sold our long-dated Indonesian Government bonds. We believe shorter-term rates are relatively anchored since we don't anticipate Bank Indonesia lowering or raising rates in the medium term.

As always, we will continue to focus on valuations. We believe the market is overly focused on macro events and outcomes rather than security selection, leaving certain issues undervalued. Accordingly, we anticipate taking positions in securities where our own views may differ from implied market expectations of the securities' credit, currency and interest rates.

Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. Investing in emerging markets involves different and greater risks, as these countries are substantially smaller, less liquid and more volatile than securities markets in more developed markets.

6 MATTHEWS ASIA FUNDS

Matthews Asia Strategic Income Fund June 30, 2012

Schedule of Investmentsa (unaudited)

FOREIGN GOVERNMENT OBLIGATIONS: 34.9%

| | | Face Amount* | | Value | |

| SOUTH KOREA: 8.9% | |

Korea Treasury Bond

3.500%, 09/10/16 | | KRW | 1,000,000,000 | | | $ | 875,701 | | |

Korea Treasury Bond

5.750%, 09/10/18 | | KRW | 500,000,000 | | | | 489,742 | | |

Korea Treasury Bond

3.250%, 12/10/14 | | KRW | 500,000,000 | | | | 436,138 | | |

Korea Treasury Bond

4.000%, 09/10/15 | | KRW | 300,000,000 | | | | 266,846 | | |

| Total South Korea | | | | | 2,068,427 | | |

| MALAYSIA: 8.5% | |

Malaysian Government Bond

4.160%, 07/15/21 | | MYR | 5,000,000 | | | | 1,655,390 | | |

Malaysian Government Bond

3.580%, 09/28/18 | | MYR | 1,000,000 | | | | 318,904 | | |

| Total Malaysia | | | | | 1,974,294 | | |

| PHILIPPINES: 7.9% | |

Republic of Philippines

6.250%, 01/14/36 | | PHP | 30,000,000 | | | | 759,167 | | |

Republic of Philippines

6.375%, 01/15/32 | | | 500,000 | | | | 631,250 | | |

Republic of Philippines

4.950%, 01/15/21 | | PHP | 18,000,000 | | | | 445,087 | | |

| Total Philippines | | | | | 1,835,504 | | |

| INDONESIA: 6.0% | |

Indonesia Government Bond

8.250%, 07/15/21 | | IDR | 9,000,000,000 | | | | 1,094,037 | | |

Republic of Indonesia

5.875%, 03/13/20 | | | 250,000 | | | | 288,125 | | |

| Total Indonesia | | | | | 1,382,162 | | |

| THAILAND: 2.0% | |

Thailand Government Bond

4.250%, 03/13/13 | | THB | 15,000,000 | | | | 475,884 | | |

| Total Thailand | | | | | 475,884 | | |

| SRI LANKA: 1.6% | |

Republic of Sri Lanka

7.400%, 01/22/15 | | | 350,000 | | | | 374,500 | | |

| Total Sri Lanka | | | | | 374,500 | | |

| TOTAL FOREIGN GOVERNMENT OBLIGATIONS | | | | | 8,110,771 | | |

| (Cost $8,094,663) | | | | | | | |

CORPORATE BONDS: 53.4%

| | | Face Amount* | | Value | |

| CHINA/HONG KONG: 25.0% | |

Longfor Properties Co., Ltd.

9.500%, 04/07/16 | | | 750,000 | | | $ | 783,750 | | |

Melco Crown Entertainment, Ltd.

3.750%, 05/09/13 | | CNY | 5,000,000 | | | | 777,925 | | |

KWG Property Holding, Ltd.

12.500%, 08/18/17 | | | 750,000 | | | | 726,039 | | |

Galaxy Entertainment Group, Ltd.

4.625%, 12/16/13 | | CNY | 4,500,000 | | | | 708,895 | | |

FPT Finance, Ltd.

6.375%, 09/28/20 | | | 550,000 | | | | 573,312 | | |

Hutchison Whampoa International 11, Ltd.

4.625%, 01/13/22b | | | 500,000 | | | | 524,540 | | |

Standard Chartered Bank Hong Kong, Ltd.

4.150%c, 10/27/21 | | SGD | 500,000 | | | | 406,627 | | |

Wharf Finance No. 1, Ltd.

4.500%, 07/20/21 | | SGD | 500,000 | | | | 392,801 | | |

Tencent Holdings, Ltd.

4.625%, 12/12/16b | | | 350,000 | | | | 361,389 | | |

Fita International, Ltd.

7.000%, 02/10/20 | | | 300,000 | | | | 312,217 | | |

Beijing Enterprises Water Group, Ltd.

3.750%, 06/30/14 | | CNY | 1,500,000 | | | | 234,165 | | |

| Total China/Hong Kong | | | | | 5,801,660 | | |

| PHILIPPINES: 5.9% | |

Alliance Global Group, Inc.

6.500%, 08/18/17 | | | 550,000 | | | | 579,958 | | |

SM Investments Corp.

5.500%, 10/13/17 | | | 500,000 | | | | 507,002 | | |

International Container Terminal Services, Inc.

7.375%, 03/17/20 | | | 250,000 | | | | 276,929 | | |

| Total Philippines | | | | | 1,363,889 | | |

| SINGAPORE: 4.7% | |

Global Logistic Properties, Ltd.

3.375%, 05/11/16 | | CNY | 4,500,000 | | | | 687,924 | | |

Oversea-Chinese Banking Corp., Ltd.

3.750%c, 11/15/22 | | | 400,000 | | | | 401,941 | | |

| Total Singapore | | | | | 1,089,865 | | |

| THAILAND: 3.8% | |

Bangkok Bank Public Co., Ltd.

9.025%, 03/15/29 | | | 500,000 | | | | 612,500 | | |

PTTEP Canada International Finance, Ltd.

5.692%, 04/05/21b | | | 250,000 | | | | 266,680 | | |

| Total Thailand | | | | | 879,180 | | |

| INDONESIA: 3.8% | |

PT Berau Coal Energy

7.250%, 03/13/17b | | | 400,000 | | | | 389,000 | | |

PT Adaro Indonesia

7.625%, 10/22/19b | | | 250,000 | | | | 265,000 | | |

Berau Capital Resources Pte., Ltd.

12.500%, 07/08/15 | | | 200,000 | | | | 220,000 | | |

| Total Indonesia | | | | | 874,000 | | |

matthewsasia.com | 800.789.ASIA 7

Matthews Asia Strategic Income Fund June 30, 2012

Schedule of Investmentsa (unaudited) (continued)

CORPORATE BONDS (continued)

| | | Face Amount* | | Value | |

| SOUTH KOREA: 3.6% | |

Kia Motors Corp.

3.625%, 06/14/16 | | | 500,000 | | | $ | 513,385 | | |

Korea Hydro & Nuclear Power Co., Ltd.

4.750%, 07/13/21 | | | 300,000 | | | | 326,133 | | |

| Total South Korea | | | | | 839,518 | | |

| MALAYSIA: 3.0% | |

Axiata SPV1 Labuan, Ltd.

5.375%, 04/28/20 | | | 650,000 | | | | 705,871 | | |

| Total Malaysia | | | | | 705,871 | | |

| AUSTRALIA: 2.6% | |

Macquarie Bank, Ltd.

6.625%, 04/07/21 | | | 600,000 | | | | 602,001 | | |

| Total Australia | | | | | 602,001 | | |

| JAPAN: 1.0% | |

ORIX Corp.

4.000%, 11/29/14 | | CNY | 1,500,000 | | | | 234,839 | | |

| Total Japan | | | | | 234,839 | | |

| TOTAL CORPORATE BONDS | | | | | 12,390,823 | | |

| (Cost $12,242,828) | | | | | |

COMMON EQUITIES: 6.8%

| | | Shares | | | |

| CHINA/HONG KONG: 2.7% | |

| The Link REIT | | | 55,000 | | | | 225,437 | | |

| HSBC Holdings PLC | | | 24,000 | | | | 212,330 | | |

| Power Assets Holdings, Ltd. | | | 25,000 | | | | 187,605 | | |

| Total China/Hong Kong | | | | | 625,372 | | |

| SINGAPORE: 1.9% | |

| StarHub, Ltd. | | | 90,000 | | | | 243,939 | | |

| Ascendas REIT | | | 110,000 | | | | 187,654 | | |

| Total Singapore | | | | | 431,593 | | |

| THAILAND: 1.3% | |

| Kasikornbank Public Co., Ltd. | | | 60,000 | | | | 309,371 | | |

| Total Thailand | | | | | 309,371 | | |

| | | Shares | | Value | |

| PHILIPPINES: 0.9% | |

| Globe Telecom, Inc. | | | 8,000 | | | $ | 212,495 | | |

| Total Philippines | | | | | 212,495 | | |

| TOTAL COMMON EQUITIES | | | | | 1,578,831 | | |

| (Cost $1,423,659) | | | |

| TOTAL INVESTMENTS: 95.1% | | | | | 22,080,425 | | |

| (Cost $21,761,150d) | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 4.9% | | | | | 1,147,620 | | |

| NET ASSETS: 100.0% | | | | $ | 23,228,045 | | |

a Certain securities were fair valued under the discretion of the Board of Trustees (Note 2-A).

b Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. The security may be resold in transactions exempt from registration normally to qualified institutional buyers. The security has been determined to be liquid in accordance with procedures adopted by the Fund's Board of Directors.

c Variable rate security. The rate represents the rate in effect at June 30, 2012.

d Cost for federal income tax purposes is $21,761,150 and net unrealized appreciation consists of:

| Gross unrealized appreciation | | $ | 484,699 | | |

| Gross unrealized depreciation | | | (165,424 | ) | |

| Net unrealized appreciation | | $ | 319,275 | | |

* All values are in USD unless otherwise noted.

CNY Chinese Renminbi (Yuan)

IDR Indonesian Rupiah

JPY Japanese Yen

KRW Korean Won

MYR Malaysian Ringgit

PHP Philippine Peso

REIT Real Estate Investment Trust

SGD Singapore Dollar

THB Thai Baht

USD U.S. Dollar

FORWARD FOREIGN CURRENCY EXCHANGE CONTRACTS:

| | | Currency Purchased | | Currency Sold | | Counterparty | | Settlement Date | | Unrealized

Appreciation | |

| LONG | | SGD | 1,000,000 | | | USD | 776,072 | | | Brown Brothers Harriman | | 09/05/12 | | $ | 13,397 | | |

| SHORT | | USD | 776,072 | | | JPY | 60,927,861 | | | Brown Brothers Harriman | | 09/05/12 | | $ | 13,116 | | |

FINANCIAL FUTURES CONTRACTS SOLD AS OF JUNE 30, 2012 WERE AS FOLLOWS:

| Contracts | | Issue | | Exchange | | Expiration | | Notional Value | | Unrealized

Appreciation | |

| | 10 | | | U.S. Treasury Notes (10 Year) | | Chicago Board of Trade | | September, 2012 | | $ | 1,333,750 | | | $ | 7,525 | | |

See accompanying notes to financial statements.

8 MATTHEWS ASIA FUNDS

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Robert J. Horrocks, PhD

Lead Manager

Kenneth Lowe, CFA

Co-Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MACSX | | MICSX | |

| CUSIP | | 577130206 | | 577130842 | |

| Inception | | 9/12/94 | | 10/29/10 | |

| NAV | | $16.30 | | $16.30 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.12% | | 0.99% | |

Portfolio Statistics

| Total # of Positions | | 67 | |

| Net Assets | | $3.3 billion | |

| Weighted Average Market Cap | | $26.1 billion | |

| Portfolio Turnover | | 16.54%2 | |

Benchmark

MSCI AC Asia ex Japan Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Long-term capital appreciation. The Fund also seeks to provide some current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in dividend-paying common stock, preferred stock and other equity securities, and convertible securities as well as fixed-income securities, of any duration or quality, of companies located in Asia, including developed, emerging and frontier countries and markets in the Asian region.

1 Matthews Asia Funds does not charge 12b-1 fees.

2 The lesser of fiscal year 2011 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary

For the first half of 2012, the Matthews Asian Growth and Income Fund gained 9.51% (Investor Class) and 9.67% (Institutional Class), outperforming its benchmark, the MSCI All Country Asia ex Japan Index, which returned 6.10%. While Asia's stock markets declined in the second quarter, the Fund was able to outperform in this environment. For the quarter ended June 30, the Fund fell –1.35% (Investor Class) and –1.28% (Institutional Class), while its benchmark returned –6.74%.

Detractors to Fund performance over the quarter included, perhaps not surprisingly, the more cyclical industries such as energy, materials and industrials. Contributors to performance included telecommunications businesses, broadcast media, health care companies and some select consumer businesses. We believe the divergences in performance were mainly due to marginal investors taking a very short-term view of profits and trying to guess the course of major macroeconomic events for the remainder of the year.

We continue to evaluate new opportunities with the same philosophy as in the past. The strategy has sought downside protection with some participation on the upside—or what we sometimes refer to as "optionality" in the securities we own. This can be found through the type of security purchased, such as a convertible bond; by the kind of business purchased; or by taking advantage of valuations (particularly dividend yield) and what we see as perverse market sentiment. More recently, we have focused on identifying gaps between what we judge to be short-term market sentiment and our longer-term view of the world.

Starting with convertible bonds, we added to our position in the long-dated convertible bond of an Australian-based insurer, QBE Funding Trust. The bond offers a U.S. dollar yield to put of about 3%—the annualized yield should investors decide to sell back to the company at the next available call date. In addition, since the maturity date for the bond is May 2030, we stand to benefit from any improvement in the underlying business, which has been depressed now for five years. We exited smaller convertible bond positions that had less attractive risk-return profiles.

During the quarter, we also exited two relatively volatile equity positions—one was a Japanese manufacturer of photonics equipment and the other an Australian retailer. Shedding these positions allowed us to add a new position in BHP Billiton, an Australian-based natural resource giant. Typically, the energy and materials sectors have not held major weightings in the Fund. However, BHP is a large, dominant company in control of assets for which there should be long-term demand and its common stock was yielding close to 4% at the end of the second quarter, an attractive yield for this portfolio. BHP management has also postponed some capital expenditure and its CEO has announced: "We are not in the commodity business; we are in the shareholder return business." We wholeheartedly embrace the sentiments behind his comments.

We also added two holdings with long histories in Asia: AIA Group, a regional insurance company founded in 1919 and Jardine Matheson Holdings, a conglomerate that was founded in the 1800s. AIA has a leading position in developed markets such as Hong Kong and Singapore and a footprint in Asia's developing markets. Besides its long history in the region, AIA also exhibits an impressive professionalism and focus on

(continued)

matthewsasia.com | 800.789.ASIA 9

PERFORMANCE AS OF JUNE 30, 2012

| | | | | Average Annual Total Returns | | | |

| | | 3 Months | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Since

Inception | | Inception

Date | |

| Investor Class (MACSX) | | | -1.35 | % | | | -3.68 | % | | | 11.46 | % | | | 4.08 | % | | | 12.33 | % | | | 10.49 | % | | 9/12/94 | |

| Institutional Class (MICSX) | | | -1.28 | % | | | -3.55 | % | | | n.a. | | | | n.a. | | | | n.a. | | | | 0.33 | % | | 10/29/10 | |

| MSCI AC Asia ex Japan Index3 | | | -6.74 | % | | | -13.15 | % | | | 10.25 | % | | | 0.82 | % | | | 11.78 | % | | | 3.42 | %4 | | | |

| Lipper Pacific Region Funds Category Average5 | | | -5.56 | % | | | -9.80 | % | | | 7.39 | % | | | -3.10 | % | | | 7.37 | % | | | 3.12 | %4 | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance, visit matthewsasia.com.

INCOME DISTRIBUTION HISTORY

| | | 2012 | | 2011 | |

| | | June | | December | | Total | | June | | December | | Total | |

| Investor Class (MACSX) | | $ | 0.20 | | | n.a | | n.a | | $ | 0.27 | | | $ | 0.21 | | | $ | 0.48 | | |

| Institutional Class (MICSX) | | $ | 0.21 | | | n.a | | n.a | | $ | 0.28 | | | $ | 0.22 | | | $ | 0.50 | | |

Note: This table does not include capital gains distributions. Institutional Class Shares were first offered on October 29, 2010. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

2.91% (Investor Class) 3.07% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/12, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 3.43%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividend paid per share during the last 12 months divided by the current price. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems, Bloomberg, MICM

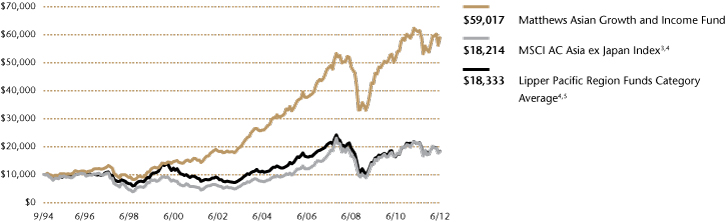

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

3 It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 69 for index definition.

4 Calculated from 8/31/94.

5 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN HOLDINGS6

| | | Sector | | Country | | % Net Assets | |

| Singapore Technologies Engineering, Ltd. | | Industrials | | Singapore | | | 3.9 | % | |

| Telstra Corp., Ltd. | | Telecommunication Services | | Australia | | | 3.6 | % | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | Information Technology | | Taiwan | | | 3.3 | % | |

| China Petroleum & Chemical Corp. (Sinopec), Cnv., 0.000%, 4/24/2014 | | Energy | | China/Hong Kong | | | 3.1 | % | |

| CLP Holdings, Ltd. | | Utilities | | China/Hong Kong | | | 3.1 | % | |

| HSBC Holdings PLC | | Financials | | China/Hong Kong | | | 3.0 | % | |

| Hisamitsu Pharmaceutical Co., Inc. | | Health Care | | Japan | | | 3.0 | % | |

| Ascendas REIT | | Financials | | Singapore | | | 2.8 | % | |

| PTT Public Co., Ltd. | | Energy | | Thailand | | | 2.7 | % | |

| AMMB Holdings BHD | | Financials | | Malaysia | | | 2.4 | % | |

| % OF ASSETS IN TOP TEN | | | | | | | 30.9 | % | |

6 Holdings may combine more than one security from same issuer and related depositary receipts.

10 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary (continued)

maintaining this competitive advantage over the long term. Whilst the absolute yield of the equity is not high—forecasts for the next 12 months suggest yield just short of 1.5%, that yield is growing due to careful management of the firm's capital and the breadth and quality of the franchise offers some protection from market volatility.

Focused traditionally on China, Jardine Matheson Holdings has more recently expanded into the fast-growing Indonesian economy and its businesses span across several industries including consumer staples, leisure, real estate, motor distribution and logistics. The common stock enjoys a dividend yield of about 2.4% and a free cash flow yield of about 7.4%. The company has been able to navigate Asia's political and financial upheavals throughout nearly two centuries. Its management has proven itself to be careful stewards of capital and we expect this to continue.

Undoubtedly, there are still risks in the markets—not least, the continued slowdown in China due to the determination of authorities to try to prevent a real estate bubble. Fumbles in Western economic policy still affect sentiment toward Asian markets. However, we approach the future with optimism, as we see opportunities to buy compelling business in various sectors at attractive valuations.

COUNTRY ALLOCATION (%)7

| China/Hong Kong | | | 26.8 | | |

| Singapore | | | 18.9 | | |

| Australia | | | 9.4 | | |

| Thailand | | | 7.8 | | |

| Japan | | | 6.3 | | |

| South Korea | | | 5.9 | | |

| India | | | 5.5 | | |

| Taiwan | | | 5.3 | | |

| Malaysia | | | 5.1 | | |

| Indonesia | | | 2.9 | | |

| United Kingdom | | | 1.9 | | |

| Philippines | | | 1.7 | | |

| Vietnam | | | 1.2 | | |

Cash and Other Assets,

Less Liabilities | | | 1.3 | | |

SECTOR ALLOCATION (%)

| Financials | | | 29.7 | | |

| Telecommunication Services | | | 14.7 | | |

| Industrials | | | 14.2 | | |

| Utilities | | | 7.7 | | |

| Energy | | | 6.9 | | |

| Health Care | | | 6.7 | | |

| Consumer Discretionary | | | 6.3 | | |

| Consumer Staples | | | 5.3 | | |

| Information Technology | | | 4.6 | | |

| Materials | | | 2.6 | | |

Cash and Other Assets,

Less Liabilities | | | 1.3 | | |

MARKET CAP EXPOSURE (%)8

| Large Cap (over $5B) | | | 68.6 | | |

| Mid Cap ($1B–$5B) | | | 23.9 | | |

| Small Cap (under $1B) | | | 6.2 | | |

Cash and Other Assets,

Less Liabilities | | | 1.3 | | |

ASSET TYPE BREAKDOWN (%)9

| Common Equities | | | 80.4 | | |

| Convertible Bonds | | | 15.0 | | |

| Preferred Equities | | | 3.1 | | |

| Corporate Bonds | | | 0.2 | | |

Cash and Other Assets,

Less Liabilities | | | 1.3 | | |

7 Australia, United Kingdom and Japan are not included in the MSCI All Country Asia ex Japan Index.

8 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

9 Bonds are not included in the MSCI All Country Asia ex Japan Index.

matthewsasia.com | 800.789.ASIA 11

Matthews Asian Growth and Income Fund June 30, 2012

Schedule of Investmentsa (unaudited)

COMMON EQUITIES: 80.4%

| | | Shares | | Value | |

| CHINA/HONG KONG: 22.0% | |

| CLP Holdings, Ltd. | | | 11,771,700 | | | $ | 100,045,971 | | |

| HSBC Holdings PLC ADR | | | 2,230,333 | | | | 98,424,595 | | |

| AIA Group, Ltd. | | | 19,459,600 | | | | 67,214,617 | | |

China Pacific Insurance Group Co., Ltd.

H Shares | | | 20,355,800 | | | | 66,428,693 | | |

| Hang Lung Properties, Ltd. | | | 19,139,920 | | | | 65,470,376 | | |

| Television Broadcasts, Ltd. | | | 8,897,000 | | | | 62,021,468 | | |

| China Mobile, Ltd. ADR | | | 905,500 | | | | 49,503,685 | | |

Shandong Weigao Group Medical

Polymer Co., Ltd. H Shares | | | 43,012,000 | | | | 48,013,455 | | |

| Vitasoy International Holdings, Ltd.† | | | 51,771,000 | | | | 43,506,325 | | |

| VTech Holdings, Ltd. | | | 3,405,300 | | | | 40,675,652 | | |

| Jardine Matheson Holdings, Ltd. | | | 736,000 | | | | 35,850,779 | | |

Citic Telecom International

Holdings, Ltd.† | | | 132,231,000 | | | | 24,130,131 | | |

| Cafe' de Coral Holdings, Ltd. | | | 6,726,000 | | | | 17,995,324 | | |

| I-CABLE Communications, Ltd.b | | | 2,870,000 | | | | 138,360 | | |

| Total China/Hong Kong | | | | | 719,419,431 | | |

| SINGAPORE: 14.6% | |

Singapore Technologies

Engineering, Ltd. | | | 52,104,125 | | | | 128,450,746 | | |

| Ascendas REIT | | | 53,925,000 | | | | 91,993,304 | | |

| Keppel Corp., Ltd. | | | 8,415,900 | | | | 68,947,418 | | |

| United Overseas Bank, Ltd. | | | 3,861,000 | | | | 57,334,053 | | |

| SIA Engineering Co., Ltd. | | | 10,768,000 | | | | 34,038,381 | | |

| Cerebos Pacific, Ltd. | | | 7,740,000 | | | | 32,342,880 | | |

| ARA Asset Management, Ltd. | | | 28,381,100 | | | | 32,133,029 | | |

| Singapore Post, Ltd. | | | 38,209,000 | | | | 31,880,558 | | |

| Total Singapore | | | | | 477,120,369 | | |

| THAILAND: 7.8% | |

| PTT Public Co., Ltd. | | | 8,719,200 | | | | 89,316,850 | | |

| BEC World Public Co., Ltd. | | | 30,807,800 | | | | 49,373,261 | | |

| Glow Energy Public Co., Ltd. | | | 21,887,400 | | | | 42,986,711 | | |

| Land & Houses Public Co., Ltd. NVDR | | | 145,090,300 | | | | 36,019,558 | | |

| Banpu Public Co., Ltd. | | | 2,480,250 | | | | 35,253,914 | | |

| Total Thailand | | | | | 252,950,294 | | |

| AUSTRALIA: 7.4% | |

| Telstra Corp., Ltd. | | | 31,377,088 | | | | 118,885,252 | | |

| CSL, Ltd. | | | 1,758,532 | | | | 71,329,094 | | |

| Macquarie Group, Ltd. | | | 1,879,326 | | | | 50,749,103 | | |

| Total Australia | | | | | 240,963,449 | | |

| JAPAN: 6.3% | |

| Hisamitsu Pharmaceutical Co., Inc. | | | 1,983,600 | | | | 97,622,058 | | |

| Japan Real Estate Investment Corp., REIT | | | 7,889 | | | | 72,332,312 | | |

| NTT DoCoMo, Inc. | | | 22,250 | | | | 37,024,057 | | |

| Total Japan | | | | | 206,978,427 | | |

| | | Shares | | Value | |

| TAIWAN: 5.3% | |

Taiwan Semiconductor

Manufacturing Co., Ltd.b | | | 20,673,187 | | | $ | 56,592,193 | | |

Taiwan Semiconductor

Manufacturing Co., Ltd. ADRb | | | 3,558,724 | | | | 49,679,787 | | |

| Chunghwa Telecom Co., Ltd. ADR | | | 1,277,525 | | | | 40,152,611 | | |

| Taiwan Hon Chuan Enterprise Co., Ltd. | | | 9,901,193 | | | | 22,303,528 | | |

| CyberLink Corp. | | | 1,146,770 | | | | 3,346,798 | | |

| Total Taiwan | | | | | 172,074,917 | | |

| MALAYSIA: 5.1% | |

| AMMB Holdings BHD | | | 40,175,100 | | | | 79,985,252 | | |

| Axiata Group BHD | | | 29,634,423 | | | | 51,298,507 | | |

| Telekom Malaysia BHD | | | 20,245,551 | | | | 36,189,871 | | |

| Total Malaysia | | | | | 167,473,630 | | |

| INDONESIA: 2.9% | |

| PT Perusahaan Gas Negara Persero | | | 141,686,000 | | | | 53,640,056 | | |

PT Telekomunikasi Indonesia

Persero ADR | | | 1,153,600 | | | | 40,179,888 | | |

| Total Indonesia | | | | | 93,819,944 | | |

| SOUTH KOREA: 2.8% | |

| S1 Corp. | | | 771,922 | | | | 38,873,383 | | |

| KT Corp. ADR | | | 2,089,505 | | | | 27,539,676 | | |

| GS Home Shopping, Inc. | | | 298,935 | | | | 25,255,502 | | |

| Total South Korea | | | | | 91,668,561 | | |

| UNITED KINGDOM: 1.9% | |

| BHP Billiton PLC | | | 2,153,817 | | | | 61,216,545 | | |

| Total United Kingdom | | | | | 61,216,545 | | |

| PHILIPPINES: 1.7% | |

| Globe Telecom, Inc. | | | 2,065,510 | | | | 54,863,987 | | |

| Total Philippines | | | | | 54,863,987 | | |

| INDIA: 1.4% | |

| Housing Development Finance Corp. | | | 3,875,750 | | | | 45,703,421 | | |

| Total India | | | | | 45,703,421 | | |

| VIETNAM: 1.2% | |

| Vietnam Dairy Products JSC | | | 5,842,535 | | | | 24,581,995 | | |

| Bao Viet Holdings | | | 7,539,961 | | | | 15,898,531 | | |

| Total Vietnam | | | | | 40,480,526 | | |

| TOTAL COMMON EQUITIES | | | | | 2,624,733,501 | | |

| (Cost $2,268,374,958) | | | | | |

12 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund June 30, 2012

Schedule of Investmentsa (unaudited) (continued)

PREFERRED EQUITIES: 3.1%

| | | Shares | | Value | |

| SOUTH KOREA: 3.1% | |

Samsung Fire & Marine Insurance

Co., Ltd., Pfd. | | | 515,311 | | | $ | 33,248,774 | | |

| Hyundai Motor Co., Ltd., Pfd. | | | 541,280 | | | | 31,670,606 | | |

| Hyundai Motor Co., Ltd., 2nd Pfd. | | | 305,760 | | | | 20,089,861 | | |

| LG Household & Health Care, Ltd., Pfd. | | | 121,855 | | | | 16,255,597 | | |

| Total South Korea | | | | | 101,264,838 | | |

| TOTAL PREFERRED EQUITIES | | | | | 101,264,838 | | |

| (Cost $48,826,622) | | | | | |

CORPORATE BONDS: 15.2%

| | | Face Amount* | | | |

| CHINA/HONG KONG: 4.8% | |

China Petroleum & Chemical Corp.

(Sinopec), Cnv.

0.000%, 04/24/14 | | HKD | 676,210,000 | | | | 100,978,904 | | |

Power Regal Group, Ltd., Cnv.

2.250%, 06/02/14 | | HKD | 234,020,000 | | | | 35,293,267 | | |

PB Issuer No. 2, Ltd., Cnv.

1.750%, 04/12/16 | | | 21,820,000 | | | | 19,583,450 | | |

| Total China/Hong Kong | | | | | 155,855,621 | | |

| SINGAPORE: 4.3% | |

CapitaLand, Ltd., Cnv.

3.125%, 03/05/18 | | SGD | 62,000,000 | | | | 51,256,759 | | |

CapitaLand, Ltd., Cnv.

2.875%, 09/03/16 | | SGD | 41,750,000 | | | | 32,362,372 | | |

Wilmar International, Ltd., Cnv.

0.000%, 12/18/12 | | | 26,500,000 | | | | 30,713,500 | | |

Olam International, Ltd., Cnv.

6.000%, 10/15/16 | | | 24,300,000 | | | | 25,223,400 | | |

| Total Singapore | | | | | 139,556,031 | | |

| INDIA: 4.1% | |

Tata Power Co., Ltd., Cnv.

1.750%, 11/21/14 | | | 56,200,000 | | | | 55,160,300 | | |

Larsen & Toubro, Ltd., Cnv.

3.500%, 10/22/14 | | | 41,200,000 | | | | 41,117,600 | | |

Sintex Industries, Ltd., Cnv.

0.000%, 03/13/13 | | | 26,900,000 | | | | 30,733,250 | | |

Housing Development

Finance Corp.

0.000%, 08/24/12 | | INR | 300,000,000 | | | | 6,648,518 | | |

| Total India | | | | | 133,659,668 | | |

| | | Face Amount* | | Value | |

| AUSTRALIA: 2.0% | |

QBE Funding Trust, Cnv.

0.000%, 05/12/30 | | | 104,571,000 | | | $ | 66,402,585 | | |

| Total Australia | | | | | 66,402,585 | | |

| TOTAL CORPORATE BONDS | | | | | 495,473,905 | | |

| (Cost $514,114,277) | | | | | |

| TOTAL INVESTMENTS: 98.7% | | | | | 3,221,472,244 | | |

| (Cost $2,831,315,857c) | | | | | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 1.3% | | | | | 43,357,468 | | |

| NET ASSETS: 100.0% | | | | $ | 3,264,829,712 | | |

a Certain securities were fair valued under the discretion of the Board of Trustees (Note 2-A).

b Non-income producing security.

c Cost for federal income tax purposes is $2,834,173,847 and net unrealized appreciation consists of:

| Gross unrealized appreciation | | $ | 538,220,758 | | |

| Gross unrealized depreciation | | | (150,922,361 | ) | |

| Net unrealized appreciation | | $ | 387,298,397 | | |

† Affiliated Issuer, as defined under the Investment Company Act of 1940 (ownership of 5% or more of the outstanding voting securities of this issuer)

* All values are in USD unless otherwise noted.

ADR American Depositary Receipt

BHD Berhad

Cnv. Convertible

HKD Hong Kong Dollar

INR Indian Rupee

JSC Joint Stock Co.

NVDR Non-voting Depositary Receipt

Pfd. Preferred

REIT Real Estate Investment Trust

SGD Singapore Dollar

USD U.S. Dollar

See accompanying notes to financial statements.

matthewsasia.com | 800.789.ASIA 13

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Jesper O. Madsen, CFA

Lead Manager

Yu Zhang, CFA

Co-Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

| Ticker | | MAPIX | | MIPIX | |

| CUSIP | | 577125107 | | 577130750 | |

| Inception | | 10/31/06 | | 10/29/10 | |

| NAV | | $13.37 | | $13.36 | |

| Initial Investment | | $2,500 | | $3 million | |

| Gross Expense Ratio1 | | 1.10% | | 1.00% | |

Portfolio Statistics

| Total # of Positions | | 61 | |

| Net Assets | | $2.8 billion | |

| Weighted Average Market Cap | | $24.4 billion | |

| Portfolio Turnover | | 16.48%2 | |

Benchmark

MSCI AC Asia Pacific Index

Redemption Fee

2% within first 90 calendar days of purchase

OBJECTIVE

Total return with an emphasis on providing current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in income-paying equity securities of companies located in Asia, including developed, emerging and frontier countries and markets in the Asian region. The Fund may also invest in convertible debt and equity securities.

1 Matthews Asia Funds does not charge 12b-1 fees.

2 The lesser of fiscal year 2011 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asia Dividend Fund

Portfolio Manager Commentary

For the first half of 2012, the Matthews Asia Dividend Fund gained 8.76% (Investor Class) and 8.75% (Institutional Class), outperforming its benchmark, the MSCI All Country Asia Pacific Index, which rose 4.58%. For the quarter ended June 30, the Fund declined –2.50% (Investor Class) and –2.47% (Institutional Class) while its benchmark fell –6.70%. In June, the Fund distributed 13.9 cents per share (Investor Class), bringing its total year-to-date income distribution to 19.9 cents per share (Investor Class).

Volatility in financial markets picked up during the second quarter as it became evident that a political consensus around a clear resolution to Europe's debt crisis was not forthcoming. Furthermore, economic data continued to reflect a slowdown in economic activity, not just in Europe and the U.S., but also China. Earlier this year, China's leaders revised down the country's target for 2012 annual GDP growth to 7.5% from 8%—a sign that a moderation in economic expansion should be expected. Since taking its first steps toward opening its economy in 1978, China has evolved from an agrarian economy of about US$220 billion into the world's second-largest economy at almost US$7.3 trillion. Given the sheer scale of the economy, it should come as no surprise that China is likely to face a structural moderation in growth.

Investors and policymakers tend to be overly reliant on headline GDP growth as an indicator of economic activity. However, economic growth is neither one dimensional nor of uniform "quality." In China's case, a moderation in growth could result in growth of higher quality and sustainability—less fueled by fixed asset investments and powered instead by domestic consumption and services-based companies. While a slowdown in China's headline GDP growth may create short-term volatility in equities, investors that are exposed to companies catering to the rising consumption within China should find that such a moderation in growth may not be for the worst.

While May was a tough month in terms of absolute performance, the Fund held up well relative to its benchmark during the second quarter, mainly due to its Japanese holdings. Among the top three performers were Pigeon, a manufacturer of baby care products and Lawson, a convenience store retailer—both Japanese consumer staples firms—and EPS Corporation, a Japanese health care company. Given Japan's dour macroeconomic outlook, we are often asked why we invest in the country. Quite simply, the Fund invests in companies that we believe can grow dividends and pay investors an attractive yield relative to that growth. Since our portfolio construction is not dictated by its benchmark, we invest in companies, including Japanese companies, precisely because we believe they offer the attractive combination of growth and dividend yield. The overall positive performance of the Fund's Japanese holdings during the quarter also illustrated that they can act as effective diversifiers in choppy markets.

Not surprisingly, the Fund's Chinese holdings were the main detractors to performance during the second quarter, given general worries regarding the severity of an economic slowdown. Our Chinese holdings within the energy and materials sectors, which are perceived to be proxies for economic growth, were among the worst performers.

(continued)

14 MATTHEWS ASIA FUNDS

PERFORMANCE AS OF JUNE 30, 2012

| | | | | Average Annual Total Returns | | | |

| | | 3 Months | | 1 Year | | 3 Years | | 5 Years | | Since

Inception | | Inception

Date | |

| Investor Class (MAPIX) | | | -2.50 | % | | | -3.30 | % | | | 14.62 | % | | | 6.95 | % | | | 9.51 | % | | 10/31/06 | |

| Institutional Class (MIPIX) | | | -2.47 | % | | | -3.21 | % | | | n.a. | | | | n.a. | | | | 0.51 | % | | 10/29/10 | |

| MSCI AC Asia Pacific Index3 | | | -6.70 | % | | | -10.48 | % | | | 7.17 | % | | | -2.62 | % | | | 0.43 | %4 | | | |

| Lipper Pacific Region Funds Category Average5 | | | -5.56 | % | | | -9.80 | % | | | 7.39 | % | | | -3.10 | % | | | 0.64 | %4 | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance, visit matthewsasia.com.

INCOME DISTRIBUTION HISTORY

| | | 2012 | | 2011 | |

| | | Q1 | | Q2 | | Q3 | | Q4 | | Total | | Q1 | | Q2 | | Q3 | | Q4 | | Total | |

| Investor Class (MAPIX) | | $ | 0.06 | | | $ | 0.14 | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.10 | | | $ | 0.11 | | | $ | 0.12 | | | $ | 0.03 | | | $ | 0.36 | | |

| Institutional Class (MIPIX) | | $ | 0.06 | | | $ | 0.14 | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.11 | | | $ | 0.12 | | | $ | 0.12 | | | $ | 0.03 | | | $ | 0.38 | | |

Note: This table does not include capital gains distributions. Institutional Class Shares were first offered on October 29, 2010. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

3.13% (Investor Class) 3.25% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/12, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 4.09%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividend paid per share during the last 12 months divided by the current price. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems, Bloomberg, MICM.

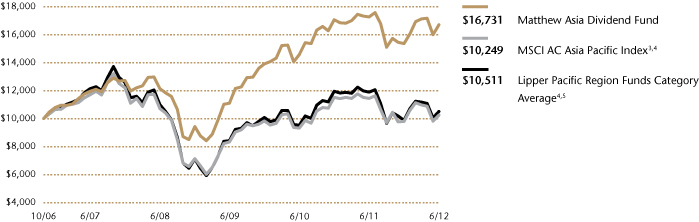

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

3 It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 69 for index definition.

4 Calculated from 10/31/06.

5 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN HOLDINGS6

| | | Sector | | Country | | % Net Assets | |

| Japan Tobacco, Inc. | | Consumer Staples | | Japan | | | 3.8 | % | |

| ITOCHU Corp. | | Industrials | | Japan | | | 3.6 | % | |

| ORIX Corp. | | Financials | | Japan | | | 3.3 | % | |

| HSBC Holdings PLC | | Financials | | China/Hong Kong | | | 3.1 | % | |

| Metcash, Ltd. | | Consumer Staples | | Australia | | | 3.1 | % | |

| KT&G Corp. | | Consumer Staples | | South Korea | | | 2.9 | % | |

| China Mobile, Ltd. | | Telecommunication Services | | China/Hong Kong | | | 2.8 | % | |

| Singapore Technologies Engineering, Ltd. | | Industrials | | Singapore | | | 2.7 | % | |

| Cheung Kong Infrastructure Holdings, Ltd. | | Utilities | | China/Hong Kong | | | 2.7 | % | |

| NTT DoCoMo, Inc. | | Telecommunication Services | | Japan | | | 2.6 | % | |

| % OF ASSETS IN TOP TEN | | | | | | | 30.6 | % | |

6 Holdings may combine more than one security from same issuer and related depositary receipts.

matthewsasia.com | 800.789.ASIA 15

COUNTRY ALLOCATION (%)7

| China/Hong Kong | | | 30.2 | | |

| Japan | | | 24.0 | | |

| Singapore | | | 11.8 | | |

| Australia | | | 8.2 | | |

| Taiwan | | | 7.9 | | |

| Thailand | | | 5.6 | | |

| South Korea | | | 4.1 | | |

| Indonesia | | | 3.1 | | |

| Philippines | | | 1.6 | | |

Cash and Other Assets,

Less Liabilities | | | 3.5 | | |

SECTOR ALLOCATION (%)

| Consumer Staples | | | 20.6 | | |

| Financials | | | 19.5 | | |

| Consumer Discretionary | | | 12.4 | | |

| Industrials | | | 10.8 | | |

| Telecommunication Services | | | 9.3 | | |

| Utilities | | | 6.3 | | |

| Health Care | | | 5.5 | | |

| Energy | | | 5.4 | | |

| Information Technology | | | 4.6 | | |

| Materials | | | 2.1 | | |

Cash and Other Assets,

Less Liabilities | | | 3.5 | | |

MARKET CAP EXPOSURE (%)8

| Large Cap (over $5B) | | | 49.7 | | |

| Mid Cap ($1B–$5B) | | | 25.2 | | |

| Small Cap (under $1B) | | | 21.6 | | |

Cash and Other Assets,

Less Liabilities | | | 3.5 | | |

7 The United Kingdom is not included in the MSCI All Country Asia Pacific Index.

8 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

Matthews Asia Dividend Fund

Portfolio Manager Commentary (continued)

Also in the second quarter, the Fund's holdings within the health care and telecommunications services sectors were main contributors to performance, while holdings in more cyclical sectors such as consumer discretionary and information technology hurt performance. Two of the Fund's consumer discretionary holdings, Esprit Holdings and Li Ning, continued to face ongoing challenges in turning around their businesses and both stocks suffered as a result. We continue to monitor these companies, which remain holdings as we believe their businesses are worth more than their current market capitalization reflects. More importantly, we believe both companies have the capacity to deliver dividend growth if and when they turn around their businesses.