UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-08510 | |

| | |

| Matthews International Funds | |

| (Exact name of registrant as specified in charter) | |

| | |

| Four Embarcadero Center, Suite 550 | |

| | San Francisco, CA 94111 | | |

| (Address of principal executive offices) (Zip code) | |

| | |

| William J. Hackett, President | |

| Four Embarcadero Center, Suite 550 | |

| | San Francisco, CA 94111 | | |

| (Name and address of agent for service) | |

| | |

| Registrant’s telephone number, including area code: 415-788-7553 | |

| | |

| Date of fiscal year end: December 31 | |

| | |

| Date of reporting period: June 30, 2015 | |

| | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Matthews Asia Funds | Semi-Annual Report

June 30, 2015 | matthewsasia.com

ASIA FIXED INCOME STRATEGY

Matthews Asia Strategic Income Fund

ASIA GROWTH AND INCOME STRATEGIES

Matthews Asian Growth and Income Fund

Matthews Asia Dividend Fund

Matthews China Dividend Fund

ASIA GROWTH STRATEGIES

Matthews Asia Focus Fund

Matthews Asia Growth Fund

Matthews Pacific Tiger Fund

Matthews Asia ESG Fund

Matthews Emerging Asia Fund

Matthews China Fund

Matthews India Fund

Matthews Japan Fund

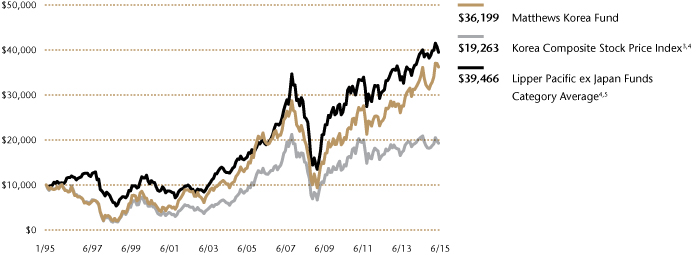

Matthews Korea Fund

ASIA SMALL COMPANY STRATEGIES

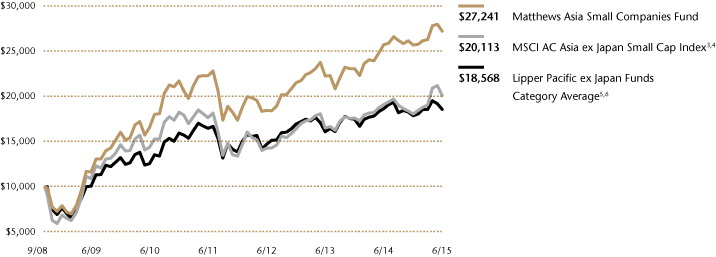

Matthews Asia Small Companies Fund

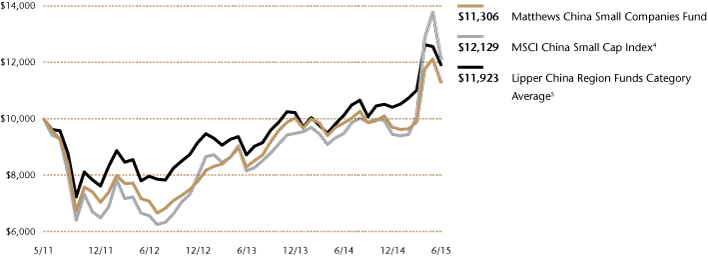

Matthews China Small Companies Fund

ASIA SPECIALTY STRATEGY

Matthews Asia Science and Technology Fund

Message to Shareholders | | | 4 | | |

Manager Commentaries, Fund Characteristics and Schedules of Investments: | |

ASIA FIXED INCOME STRATEGY | |

Matthews Asia Strategic Income Fund | | | 6 | | |

ASIA GROWTH AND INCOME STRATEGIES | |

Matthews Asian Growth and Income Fund | | | 11 | | |

Matthews Asia Dividend Fund | | | 16 | | |

Matthews China Dividend Fund | | | 21 | | |

ASIA GROWTH STRATEGIES | |

Matthews Asia Focus Fund | | | 26 | | |

Matthews Asia Growth Fund | | | 30 | | |

Matthews Pacific Tiger Fund | | | 35 | | |

Matthews Asia ESG Fund | | | 40 | | |

Matthews Emerging Asia Fund | | | 45 | | |

Matthews China Fund | | | 50 | | |

Matthews India Fund | | | 55 | | |

Matthews Japan Fund | | | 60 | | |

Matthews Korea Fund | | | 65 | | |

ASIA SMALL COMPANY STRATEGIES | |

Matthews Asia Small Companies Fund | | | 70 | | |

Matthews China Small Companies Fund | | | 75 | | |

ASIA SPECIALTY STRATEGY | |

Matthews Asia Science and Technology Fund | | | 80 | | |

Disclosures | | | 85 | | |

Index Definitions | | | 85 | | |

Disclosure of Fund Expenses | | | 86 | | |

Statements of Assets and Liabilities | | | 88 | | |

Statements of Operations | | | 96 | | |

Statements of Changes in Net Assets | | | 100 | | |

Financial Highlights | | | 108 | | |

Notes to Financial Statements | | | 124 | | |

Approval of Investment Advisory Agreement | | | 141 | | |

Results of Special Meeting of Shareholders | | | 143 | | |

Cover photo: Ancient Architecture, China

This report has been prepared for Matthews Asia Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Matthews Asia Funds prospectus, which contains more complete information about the Funds' investment objectives, risks and expenses. Additional copies of the prospectus or summary prospectus may be obtained at matthewsasia.com. Please read the prospectus carefully before you invest or send money.

The views and opinions in this report were current as of June 30, 2015. They are not guarantees of performance or investment results and should not be taken as investment advice. Investment decisions reflect a variety of factors, and the managers reserve the right to change their views about individual stocks, sectors and the markets at any time. As a result, the views expressed should not be relied upon as a forecast of a Fund's future investment intent. Current and future portfolio holdings are subject to risk.

Statements of fact are from sources considered reliable, but neither the Funds nor the Investment Advisor makes any representation or guarantee as to their completeness or accuracy.

Investment Risk: Mutual fund shares are not deposits or obligations of, or guaranteed by, any depositary institution. Shares are not insured by the FDIC, Federal Reserve Board or any government agency and are subject to investment risks, including possible loss of principal amount invested. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. In addition, single-country and sector funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector or geographic location. Investing in small and mid-size companies is more risky than investing in large companies as they may be more volatile and less liquid than larger companies. Please see the Funds' prospectus and Statement of Additional Information for more risk disclosure.

Investor Class Performance and Expenses (June 30, 2015)

| | | | | Average Annual Total Return | | | | Prospectus | | Prospectus

Expense Ratios

after Fee Waiver | |

Investor Class | | 1 year | | 5 years | | 10 years | | Since

Inception | | Inception

Date | | Expense

Ratios* | | and Expense

Reimbursement* | |

ASIA FIXED INCOME STRATEGY | |

Asia Strategic Income Fund (MAINX) | | | -1.54 | % | | | n.a. | | | | n.a. | | | | 4.17 | % | | 11/30/11 | | | 1.27 | % | | | 1.10 | %1 | |

ASIA GROWTH AND INCOME STRATEGIES | |

Asian Growth and Income Fund (MACSX) | | | -2.03 | % | | | 7.49 | % | | | 8.76 | % | | | 10.08 | % | | 9/12/94 | | | 1.08 | % | | | n.a. | | |

Asia Dividend Fund (MAPIX) | | | 6.64 | % | | | 9.89 | % | | | n.a. | | | | 10.30 | % | | 10/31/06 | | | 1.06 | % | | | 1.05 | %2 | |

China Dividend Fund (MCDFX) | | | 25.14 | % | | | 13.12 | % | | | n.a. | | | | 12.35 | % | | 11/30/09 | | | 1.19 | % | | | n.a. | | |

ASIA GROWTH STRATEGIES | |

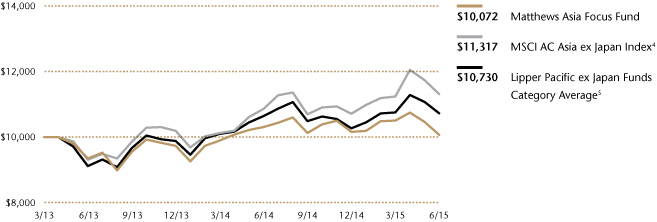

Asia Focus Fund (MAFSX) | | | -2.32 | % | | | n.a. | | | | n.a. | | | | 0.33 | % | | 4/30/13 | | | 2.16 | % | | | 1.50 | %3 | |

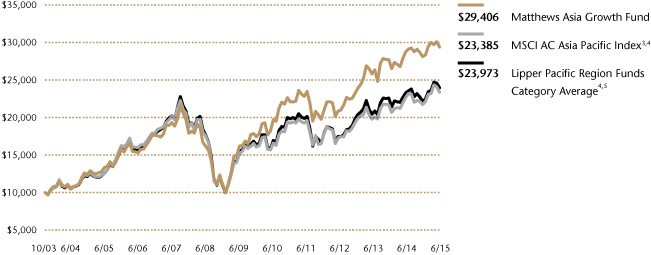

Asia Growth Fund (MPACX) | | | 2.15 | % | | | 10.03 | % | | | 8.70 | % | | | 9.69 | % | | 10/31/03 | | | 1.11 | % | | | n.a. | | |

Pacific Tiger Fund (MAPTX) | | | 9.41 | % | | | 10.49 | % | | | 12.10 | % | | | 9.21 | % | | 9/12/94 | | | 1.09 | % | | | 1.08 | %2 | |

Asia ESG Fund (MASGX) | | | n.a. | | | | n.a. | | | | n.a. | | | | -1.60 | % | | 4/30/15 | | | 2.11 | % | | | 1.45 | %3 | |

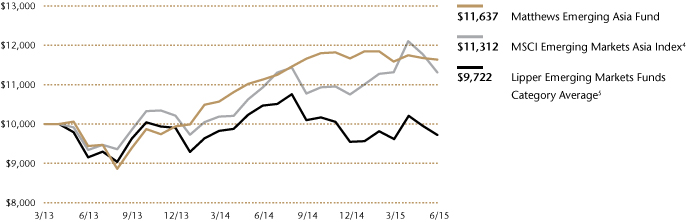

Emerging Asia Fund (MEASX) | | | 4.56 | % | | | n.a. | | | | n.a. | | | | 7.25 | % | | 4/30/13 | | | 1.78 | % | | | 1.48 | %3 | |

China Fund (MCHFX) | | | 19.20 | % | | | 5.42 | % | | | 13.14 | % | | | 10.57 | % | | 2/19/98 | | | 1.13 | % | | | n.a. | | |

India Fund (MINDX) | | | 28.22 | % | | | 10.27 | % | | | n.a. | | | | 13.58 | % | | 10/31/05 | | | 1.12 | % | | | n.a. | | |

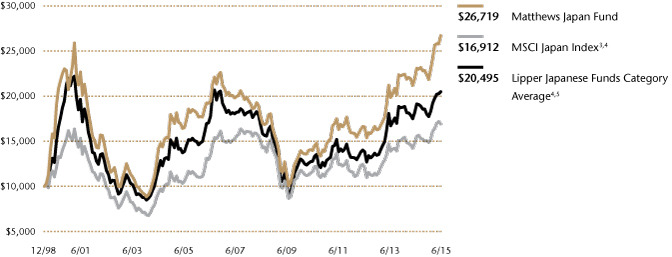

Japan Fund (MJFOX) | | | 15.69 | % | | | 14.87 | % | | | 4.18 | % | | | 6.14 | % | | 12/31/98 | | | 1.03 | % | | | n.a. | | |

Korea Fund (MAKOX) | | | 9.04 | % | | | 13.30 | % | | | 10.19 | % | | | 6.48 | % | | 1/3/95 | | | 1.11 | % | | | n.a. | | |

ASIA SMALL COMPANY STRATEGIES | |

Asia Small Companies Fund (MSMLX) | | | 5.83 | % | | | 10.47 | % | | | n.a. | | | | 15.91 | % | | 9/15/08 | | | 1.47 | % | | | n.a. | | |

China Small Companies Fund (MCSMX) | | | 14.72 | % | | | n.a. | | | | n.a. | | | | 3.05 | % | | 5/31/11 | | | 1.90 | % | | | 1.50 | %4 | |

ASIA SPECIALTY STRATEGY | |

Asia Science and Technology Fund (MATFX) | | | 10.13 | % | | | 14.05 | % | | | 10.67 | % | | | 3.04 | % | | 12/27/99 | | | 1.16 | % | | | n.a. | | |

* These figures are from the fund's prospectus dated as of April 30, 2015, and may differ from the actual expense ratios for fiscal year 2015, as shown in the financial highlights section of this report.

1 Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

2. Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund's average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time (i) by the Trust on behalf of the Fund or by the Board of Trustees upon 60 days' prior written notice to Matthews; or (ii) by Matthews upon 60 days' prior written notice to the Trust, in each case without payment of any penalty.

3. Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.25%, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.25% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.25%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016 for the Asia Focus Fund and Emerging Asia Fund, and until April 30, 2017 for the Asia ESG Fund, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

4. Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) to 1.50%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

2 MATTHEWS ASIA FUNDS

Institutional Class Performance and Expenses (June 30, 2015)

| | | | | Average Annual Total Return | | | | Prospectus | | Prospectus

Expense Ratios

after Fee Waiver | |

Institutional Class | | 1 year | | 5 years | | 10 years | | Since

Inception | | Inception

Date | | Expense

Ratios* | | and Expense

Reimbursement* | |

ASIA FIXED INCOME STRATEGY | |

Asia Strategic Income Fund (MINCX) | | | -1.34 | % | | | n.a. | | | | n.a. | | | | 4.35 | % | | 11/30/11 | | | 1.07 | % | | | 0.90 | %1 | |

ASIA GROWTH AND INCOME STRATEGIES | |

Asian Growth and Income Fund (MICSX) | | | -1.86 | % | | | n.a. | | | | n.a. | | | | 5.10 | % | | 10/29/10 | | | 0.92 | % | | | n.a. | | |

Asia Dividend Fund (MIPIX) | | | 6.80 | % | | | n.a. | | | | n.a. | | | | 7.72 | % | | 10/29/10 | | | 0.93 | % | | | n.a. | | |

China Dividend Fund (MICDX) | | | 25.28 | % | | | n.a. | | | | n.a. | | | | 10.73 | % | | 10/29/10 | | | 1.01 | % | | | n.a. | | |

ASIA GROWTH STRATEGIES | |

Asia Focus Fund (MIFSX) | | | -2.05 | % | | | n.a. | | | | n.a. | | | | 0.58 | % | | 4/30/13 | | | 1.94 | % | | | 1.25 | %3 | |

Asia Growth Fund (MIAPX) | | | 2.33 | % | | | n.a. | | | | n.a. | | | | 6.54 | % | | 10/29/10 | | | 0.91 | % | | | n.a. | | |

Pacific Tiger Fund (MIPTX) | | | 9.56 | % | | | n.a. | | | | n.a. | | | | 6.84 | % | | 10/29/10 | | | 0.92 | % | | | 0.91 | %2 | |

Asia ESG Fund (MISFX) | | | n.a. | | | | n.a. | | | | n.a. | | | | -1.60 | % | | 4/30/15 | | | 1.95 | % | | | 1.25 | %3 | |

Emerging Asia Fund (MIASX) | | | 4.80 | % | | | n.a. | | | | n.a. | | | | 7.49 | % | | 4/30/13 | | | 1.59 | % | | | 1.25 | %3 | |

China Fund (MICFX) | | | 19.35 | % | | | n.a. | | | | n.a. | | | | 1.80 | % | | 10/29/10 | | | 0.97 | % | | | n.a. | | |

India Fund (MIDNX) | | | 28.48 | % | | | n.a. | | | | n.a. | | | | 6.69 | % | | 10/29/10 | | | 0.94 | % | | | n.a. | | |

Japan Fund (MIJFX) | | | 15.82 | % | | | n.a. | | | | n.a. | | | | 13.19 | % | | 10/29/10 | | | 0.90 | % | | | n.a. | | |

Korea Fund (MIKOX) | | | 9.35 | % | | | n.a. | | | | n.a. | | | | 10.66 | % | | 10/29/10 | | | 0.93 | % | | | n.a. | | |

ASIA SMALL COMPANY STRATEGY | |

Asia Small Companies Fund (MISMX) | | | 6.07 | % | | | n.a. | | | | n.a. | | | | 8.17 | % | | 4/30/13 | | | 1.25 | % | | | n.a. | | |

ASIA SPECIALTY STRATEGY | |

Asia Science and Technology Fund (MITEX) | | | 10.34 | % | | | n.a. | | | | n.a. | | | | 20.20 | % | | 4/30/13 | | | 0.95 | % | | | n.a. | | |

* These figures are from the fund's prospectus dated as of April 30, 2015, and may differ from the actual expense ratios for fiscal year 2015, as shown in the financial highlights section of this report.

1 Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

2. Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund's average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time (i) by the Trust on behalf of the Fund or by the Board of Trustees upon 60 days' prior written notice to Matthews; or (ii) by Matthews upon 60 days' prior written notice to the Trust, in each case without payment of any penalty.

3. Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.25%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016 for the Asia Focus Fund and the Emerging Asia Fund, and until April 30, 2017 for the Asia ESG Fund, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

Past Performance: All performance quoted in this report is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the returns quoted. If certain of the Funds' fees and expenses had not been waived, returns would have been lower. For the Funds' most recent month-end performance, please call 800.789.ASIA (2742) or visit matthewsasia.com.

matthewsasia.com | 800.789.ASIA 3

Message to Shareholders from the Investment Advisor

Dear Valued Investors,

Valuations remain at the forefront of my thoughts when I look at Asia's stock markets. We are swimming against the tide a bit now, as the markets have risen at a faster pace than the underlying growth of Asia's companies. A price-to-earnings ratio* of 15.6X for Asia ex Japan is significantly above long-run averages. Now, I know that there is some justification for higher valuations in a world in which bond yields are extremely low. And there is some good news for investors in Asia's equity markets—they remain at a similar valuation to troubled Europe and at a discount of about 15% to the U.S.1 There are clearly some signs of excess as I'll get into in discussing China and India. And there is always the danger of dismissing everything as a bubble when there is still value to be had in the markets. Nevertheless, I do think it is wise to tread a little more cautiously in light of the re-rating of Asian equities in recent months.

Let us start with China. There has been plenty of talk about bubbles recently. Isn't it peculiar how China has just switched from one form of pessimism (a fear of imminent economic collapse) to another (a fear of an overheated stock market) without the usual step of optimism in between? Such is the lot of the world's second-largest economy and pretender to the U.S.'s crown. Undoubtedly, there are some strange goings-on in China's market. High retail participation increases the casino-like actions in the markets. Taking a passive approach to the markets right now risks buying into some companies that have very limited history and business models that are built on hopes rather than reality—and yet they can be multibillion dollar companies thanks to the valuations put on them by local speculators. And certainly, China stocks as a whole have seen the biggest short-term rise in their average valuations in the region. Yet, it remains true that the market of Hong Kong, through which most China investing is done, remains much more reasonably priced, at 14.4X forward earnings. Indeed, one can find businesses that have stood the test of time still trading at reasonable, sometimes cheap valuations. But it is definitely an environment in which one needs to tread carefully, and not get carried away.

In India, the problem remains partly cyclical and partly structural. Macroeconomic policy has been fairly tight over the past couple of years. This has impacted earnings growth, which has been disappointing. And although the new Modi government appears to be making changes to some of India's structural bottlenecks—and particularly improving the efficiency of government—it has to contend with pushback from India's formidable bureaucracy and the need to maintain foreign investor confidence. Reforms will likely have to be funded by fickle foreign portfolio flows, unless India can do better at attracting foreign direct investment. All of this should be seen as more of an opportunity than a threat—if it were not for the valuations of the markets, which at 16.4X forward earnings, is still among the more expensive in the region. We have been fairly cautious on India for a while. The good news is that the market has faltered this year and so the sentiment is no longer perhaps as ebullient as it has been. But the market hasn't really become any cheaper either. Stock prices have just reacted to weak underlying corporate results.

In Japan, we have noted some success from attempts to reflate the economy, much to the surprise of those who suggested it would merely debase the currency and precipitate a debt crisis. The stock market has performed strongly.

4 MATTHEWS ASIA FUNDS

And this performance has only been enhanced with recent moves to improve corporate governance, particularly when highly rated companies embrace the government's push for greater transparency. It gives other companies nowhere to hide. No longer can they say: "Well, the most respected companies don't do it, why should we?" But at the same time, we have yet to see a lot of evidence for change in the operating metrics of corporate Japan. That may come. Until now, there remains more hope than reality, too. We have certainly seen, however, some signs of better use of cash. In a deflationary world, it was easy to let cash build up on the balance sheet, because it was earning a return. Now, with positive inflation rates, we have seen companies more inclined to raise dividend payments. Japan is by no means, however, a cheap market. And to justify the current valuations, companies have to follow through with better operating results.

In contrast to the big three economies, it is the Association of Southeast Asian Nations (ASEAN) that has struggled a bit recently, and now appears the more reasonably priced part of the region. It also remains among the more vulnerable to tighter money and a series of U.S. Federal Reserve rate hikes. My view remains that we ought not to see a series of Fed rate hikes in the current environment. Inflation is still in abeyance. The most likely scenario that would justify a sustained series of rate hikes would be a return of faster nominal growth in the world—real growth plus inflation. In such an environment, even higher interest rates are unlikely to be too much of a headwind, as Asia, and particularly ASEAN economies should benefit from easier business conditions.

I have been fairly upbeat in the recent past about the economic conditions in Asia. And I remain upbeat. Governments in the region seem to be determined to tackle long-term structural issues. The reason for my more cautious message is simply valuation. I admit that there is a risk in being too sensitive to valuations, but there does seem to be a relationship between current valuation levels and future returns on average. It often pays, unsurprisingly, to be buying when markets are cheap; it is just hard to do. As always, it pays to be patient—to buy quality, sustainable growth, but to do so at reasonable prices.

Robert Horrocks, PhD

Chief Investment Officer

Matthews Asia

1 In terms of Factset aggregates.

* Price-to-Earnings Ratio (P/E Ratio) is a valuation ratio of a company's current share price compared to its per-share earnings and is calculated as the market value per share divided by the Earnings per Share (EPS).

matthewsasia.com | 800.789.ASIA 5

ASIA FIXED INCOME STRATEGY

PORTFOLIO MANAGERS

Teresa Kong, CFA | | | |

Lead Manager | | | |

Gerald M. Hwang, CFA | | Satya Patel | |

Co-Manager | | Co-Manager | |

FUND FACTS

| | | Investor Class | | Institutional Class | |

Ticker | | MAINX | | MINCX | |

CUSIP | | 577125503 | | 577125602 | |

Inception | | 11/30/11 | | 11/30/11 | |

NAV | | $10.25 | | $10.24 | |

Initial Investment | | $2,500 | | $3 million | |

Gross Expense Ratio1 | | 1.27% | | 1.07% | |

After Fee Waiver and

Reimbursement2 | | 1.10% | | 0.90% | |

Portfolio Statistics

Total # of Positions | | 51 | |

Net Assets | | $69.9 million | |

Modified Duration | | 3.83 | |

Portfolio Turnover | | 34.28%4 | |

Benchmark

HSBC Asian Local Bond Index | |

OBJECTIVE

Total return over the long term with an emphasis on income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total assets, which include borrowings for investment purposes, in income-producing securities including, but not limited to, debt and debt-related instruments issued by governments, quasi-governmental entities, supra-national institutions, and companies in Asia. Asia consists of all countries and markets in Asia and includes developed, emerging, and frontier countries and markets in the Asian region. Investments may be denominated in any currency, and may represent any part of a company's capital structure from debt to equity or with features of both.

1 Prospectus expense ratios.

2 Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, front-end or contingent deferred loads, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation in a year within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or to exceed any other agreed upon expense limitation for that year. This agreement will remain in place until April 30, 2016, may be renewed for additional periods not exceeding one year and may be terminated at any time by the Board of Trustees or the Trust on behalf of the Fund on 60 days' written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.

3 Modified duration measures the percent change in value of the fixed income portion of the portfolio in response to a 1% change in interest rates. In a multi-currency denominated portfolio with sensitivities to different interest rate regimes, modified duration will not accurately reflect the change in value of the overall portfolio from a change in any one interest rate regime.

4 The lesser of fiscal year 2014 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary

Period ended June 30, 2015

For the first half of 2015, the Matthews Asia Strategic Income Fund returned 0.38% (Investor Class) and 0.48% (Institutional Class), while its benchmark, the HSBC Asian Local Bond Index (ALBI) returned –0.44%. For the quarter ending June 30, the Fund returned –0.31% (Investor Class) and –0.26% (Institutional Class), while its benchmark returned –0.76%.

Market Environment:

As we look back at the first half of 2015, we recall the headline events of the Greek default, the meteoric rise and fall of Chinese onshore equity markets, and the debt restructuring of Puerto Rico. While all these events caused short-term volatility, the real drivers of return in Asia bonds were the steady depreciation of Asian currencies and the steepening of yield curves.

Most Asian currencies continued to mildly depreciate, relative to the U.S. dollar, as the U.S. Federal Reserve is expected to raise interest rates while most Asian governments have been operating more in terms of monetary easing instead of tightening. The general steepening of yield curves should be framed more as normalizing from unusually flat curves at the end of 2014, resulting from global disinflation. The dovish bias of Asian central banks pushed short-dated yields (less than two years) lower while the normalization described caused medium and long-end yields to rise. Finally, credit spreads diverged. Investment-grade spreads widened by about 10 basis points (0.10%), in line with the mild rise one would expect from steepening yield curves. Conversely, non-investment grade spreads tightened by about 27 basis points (0.27%), driven largely by Chinese property bonds. In the first quarter, Chinese property developer Kaisa defaulted on its bonds. The market recovered as the market came to the conclusion that the Kaisa default was not contagious and home prices recovered from further central bank easing and loosening of home ownership regulations.

Performance Contributors and Detractors:

The biggest positive contributors to performance for the first half of the year were our holdings in convertible and corporate bonds issued by Chinese companies. We made a deliberate reallocation away from local currency bonds into the convertible bonds. We found value in several convertibles of Chinese companies as Chinese equity markets rallied. This upside skew, combined with protected downside risk (as we targeted convertibles of solid companies with little leverage that were valued at or below their bond floor), provided attractive return vs. risk. Examples include our holdings of Ctrip.com and Biostime convertible bonds. The other category of outperformers included Chinese real estate holdings as our holdings recovered from the containment of the Kaisa default as well as the rise in property prices described previously.

The biggest detractors to performance were bonds of longest duration as the yield curves steepened. These hit our holdings of Yum! Brands, a solid investment grade name. Since these are the longest bonds in our portfolio, with a maturity of 2043, these bonds sold off the most. Our holdings

6 MATTHEWS ASIA FUNDS

PERFORMANCE AS OF JUNE 30, 2015

| | | | | | | | | Average Annual

Total Returns | | | |

| | | 3 Months | | YTD | | 1 Year | | 3 Years | | Since

Inception | |

Inception Date | |

Investor Class (MAINX) | | | -0.31 | % | | | 0.38 | % | | | -1.54 | % | | | 3.76 | % | | | 4.17 | % | | 11/30/11 | |

Institutional Class (MINCX) | | | -0.26 | % | | | 0.48 | % | | | -1.34 | % | | | 3.94 | % | | | 4.35 | % | | 11/30/11 | |

HSBC Asian Local Bond Index5 | | | -0.76 | % | | | -0.44 | % | | | -1.04 | % | | | 1.40 | % | | | 2.04 | % | | | | | |

Lipper International Income Funds Category Average6 | | | -1.60 | % | | | -3.10 | % | | | -6.81 | % | | | -0.08 | % | | | 0.83 | % | | | | | |

| Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. For the Fund's most recent month-end performance visit matthewsasia.com. | |

INCOME DISTRIBUTION HISTORY

| | 2015 | | 2014 | |

| | Q1 | | Q2 | | Q3 | | Q4 | | Total | | Q1 | | Q2 | | Q3 | | Q4 | | Total | |

Investor (MAINX) | | $ | 0.00 | | | $ | 0.10 | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.10 | | | $ | 0.09 | | | $ | 0.07 | | | $ | 0.10 | | | $ | 0.38 | | |

Inst'l (MINCX) | | $ | 0.01 | | | $ | 0.10 | | | | n.a. | | | | n.a. | | | | n.a. | | | $ | 0.11 | | | $ | 0.10 | | | $ | 0.08 | | | $ | 0.11 | | | $ | 0.40 | | |

Note: This table does not include capital gains distributions. Totals may differ by $0.02 due to rounding. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

Investor Class: 4.58% (4.36% excluding expense waiver)

Inst'l Class: 4.83% (4.59% excluding expense waiver)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/15, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

YIELD TO WORST:

6.33%

Yield to worst is the lowest yield that can be received on a bond assuming that the issuer does not default. It is calculated by utilizing the worst case assumptions for a bond with respect to certain income-reducing factors, including prepayment, call or sinking fund provisions. It does not represent the yield that an investor should expect to receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems

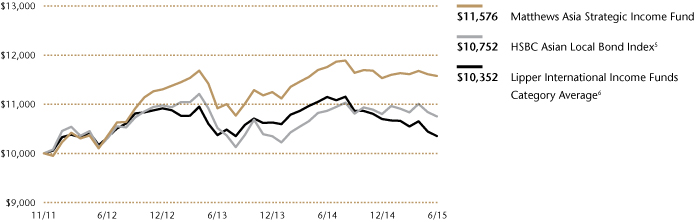

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

5 It is not possible to invest directly in an index. Source: Index data from HSBC, and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 85 for index definitions.

6 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN POSITIONS

| | | Sector | | Currency | | % of Net Assets | |

DFCC Bank PLC, 9.625%, 10/31/2018 | | Financials | | U.S. Dollar | | | 4.0 | % | |

Homeinns Hotel Group, Cnv., 2.000%, 12/15/2015 | | Consumer Discretionary | | U.S. Dollar | | | 3.9 | % | |

PT Perusahaan Listrik Negara, 5.250%, 10/24/2042 | | Utilities | | U.S. Dollar | | | 3.1 | % | |

Longfor Properties Co., Ltd., 6.875%, 10/18/2019 | | Financials | | U.S. Dollar | | | 3.0 | % | |

TML Holdings Pte, Ltd., 5.750%, 05/07/2021 | | Consumer Discretionary | | U.S. Dollar | | | 3.0 | % | |

Bank of Baroda, 6.625%, 05/25/2022 | | Financials | | U.S. Dollar | | | 3.0 | % | |

ICICI Bank, Ltd., 6.375%, 04/30/2022 | | Financials | | U.S. Dollar | | | 2.9 | % | |

Shimao Property Holdings, Ltd., 6.625%, 01/14/2020 | | Financials | | U.S. Dollar | | | 2.9 | % | |

Global Logistic Properties, Ltd., 3.375%, 05/11/2016 | | Financials | | Chinese Renminbi | | | 2.9 | % | |

Value Success International, Ltd., 4.750%, 11/04/2018 | | Financials | | Chinese Renminbi | | | 2.8 | % | |

% OF ASSETS IN TOP TEN | | | | | | | 31.5 | % | |

matthewsasia.com | 800.789.ASIA 7

CURRENCY ALLOCATION (%)7,8

U.S. Dollar (USD) | | | 60.4 | | |

Indian Rupee (INR) | | | 11.6 | | |

Singapore Dollar (SGD) | | | 0.8 | | |

Indonesian Rupiah (IDR) | | | 5.4 | | |

Sri Lanka Rupee (LKR) | | | 5.5 | | |

Chinese Renminbi (CNY) | | | 7.7 | | |

South Korean Won (KRW) | | | 2.3 | | |

Hong Kong Dollar (HKD) | | | 2.4 | | |

Philippine Peso (PHP) | | | 0.5 | | |

Cash and Other Assets, Less Liabilities | | | 3.4 | | |

COUNTRY ALLOCATION (%)8,9

China/Hong Kong | | | 32.9 | | |

India | | | 22.8 | | |

Indonesia | | | 16.9 | | |

Sri Lanka | | | 13.0 | | |

Singapore | | | 3.7 | | |

South Korea | | | 2.3 | | |

Philippines | | | 2.1 | | |

Australia | | | 1.8 | | |

Supranational10 | | | 1.1 | | |

Cash and Other Assets, Less Liabilities | | | 3.4 | | |

SECTOR ALLOCATION (%)8

Financials | | | 44.9 | | |

Consumer Discretionary | | | 16.5 | | |

Foreign Government Bonds | | | 13.8 | | |

Industrials | | | 8.5 | | |

Utilities | | | 6.6 | | |

Consumer Staples | | | 2.5 | | |

Information Technology | | | 2.4 | | |

Telecommunication Services | | | 1.4 | | |

Cash and Other Assets, Less Liabilities | | | 3.4 | | |

Please note: Foreign Government Bonds category includes Supranationals.

ASSET TYPE BREAKDOWN (%)7,8

Non-Convertible Corporate Bonds | | | 65.2 | | |

Convertible Corporate Bonds | | | 16.3 | | |

Government Bonds | | | 13.8 | | |

Common Equities and ADRs | | | 1.3 | | |

Cash and Other Assets, Less Liabilities | | | 3.4 | | |

7 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

8 Cash and other assets may include forward currency exchange contracts and certain derivative instruments that have been marked-to-market.

9 Not all countries where the Fund may invest are included in the benchmark index.

10 Supranational is an international organization in which member states transcend national boundaries (ex. IMF).

Matthews Asia Strategic Income Fund

Portfolio Manager Commentary (continued)

in Indonesian government bonds were also hurt from yield curve steepening as well as the 7% depreciation of the Indonesian rupiah over this period.

Notable Portfolio Changes:

The most important change in our portfolio was our increased allocation into convertible bonds from local currency bonds. As mentioned above, we believed that convertibles represented the positive return potential given their upside optionality; protected downside when priced at or below the bond floor; and their low sensitivity to interest rates. We allocated away from local currency bonds as we expected Asian currencies to continue their gradual depreciation against the U.S. dollar.

Outlook:

At the time of writing, the market is digesting two major uncertainties from two ancient civilizations: Greece and China. The Greek referendum has resulted in a "No" vote. This signals a fundamental structural shift in the Euro zone, throwing into question the sanctity of a monetary union and higher volatility for all risky assets. Because of the bi-modal nature of the vote, the market has not priced in the uncertainties and the potential secondary effects. Instead of this news dissipating in weeks, the volatility could endure for several quarters as a chain reaction unfolds. One thing we learned from the default of Lehman Brothers is that it took more than two quarters for markets to bottom. Potential chain reactions might lead to the actual withdrawal of Greece from the Euro zone, which throws into question the potential for other countries to follow the same path.

While the fall of Chinese equities has certainly been sharp, the surprise has not been the fall but the policy response. Most investors understand that any market that rises so fast typically has the potential to fall twice as fast. More unexpected has been the rapid response of the Chinese government, which seems to signal that it is worried about the potential contagion resulting from an unwinding of assets, as providers of leverage may seize and sell collateral. This signals the vulnerability of a market in which the average participant is trading more on speculation than on fundamentals.

Given this highly uncertain context, we expect short-term returns to be driven by their historical and perceived riskiness. This means that the highest-carry currencies will underperform relative to safe-haven currencies; for sub-investment grade to underperform investment grade; for interest rates in safe-haven currencies to fall; and for interest rates in most Asian countries to rise. In summary, we expect Asia bonds to be volatile. Contributors to performance might even flip-flop in the short run as our convertible bonds may sell-off from falling Chinese equities, and our long duration, investment grade U.S. dollar assets may rally on their safe-haven characteristics. By the end of the year, we expect this volatility to subside and Asian assets to trade more on the relatively good fundamentals rather than the systematic risks we've highlighted.

Fixed income investments are subject to additional risks, including, but not limited to, interest rate, credit and inflation risks. Investing in emerging markets involves different and greater risks, as these countries are substantially smaller, less liquid and more volatile than securities markets in more developed markets.

8 MATTHEWS ASIA FUNDS

Matthews Asia Strategic Income Fund June 30, 2015

Schedule of Investmentsa (unaudited)

NON-CONVERTIBLE CORPORATE BONDS: 65.2%

| | Face Amount* | | Value | |

INDIA: 22.8% | |

TML Holdings Pte, Ltd.

5.750%, 05/07/21 | | | 2,000,000 | | | $ | 2,068,660 | | |

Bank of Baroda

6.625%b, 05/25/22 | | | 2,000,000 | | | | 2,067,068 | | |

ICICI Bank, Ltd.

6.375%b, 04/30/22 | | | 2,000,000 | | | | 2,055,820 | | |

Housing Development Finance Corp., Ltd.

9.240%, 06/24/24 | | INR | 100,000,000 | | | | 1,619,786 | | |

Housing Development Finance Corp., Ltd.

8.950%, 03/21/23 | | INR | 100,000,000 | | | | 1,589,777 | | |

Power Grid Corp. of India, Ltd.

9.250%, 12/26/15 | | INR | 100,000,000 | | | | 1,573,665 | | |

Delhi International Airport, Ltd.

6.125%, 02/03/22 | | | 1,400,000 | | | | 1,413,304 | | |

Axis Bank, Ltd.

7.250%b, 08/12/21 | | | 1,000,000 | | | | 1,024,220 | | |

Rural Electrification Corp., Ltd.

9.340%, 08/25/24 | | INR | 52,000,000 | | | | 856,747 | | |

Power Grid Corp. of India, Ltd., Series B

9.300%, 09/04/24 | | INR | 52,000,000 | | | | 854,668 | | |

Rural Electrification Corp., Ltd.

9.020%, 06/18/19 | | INR | 50,000,000 | | | | 799,770 | | |

Total India | | | | | 15,923,485 | | |

CHINA/HONG KONG: 16.6% | |

Longfor Properties Co., Ltd.

6.875%, 10/18/19 | | | 2,000,000 | | | | 2,084,500 | | |

Shimao Property Holdings, Ltd.

6.625%, 01/14/20 | | | 2,000,000 | | | | 2,017,600 | | |

Value Success International, Ltd.

4.750%, 11/04/18 | | CNY | 12,000,000 | | | | 1,980,664 | | |

Yum! Brands, Inc.

5.350%, 11/01/43 | | | 2,000,000 | | | | 1,913,690 | | |

MCE Finance, Ltd.

5.000%, 02/15/21 | | | 2,000,000 | | | | 1,900,000 | | |

Wynn Macau, Ltd.

5.250%, 10/15/21 | | | 1,480,000 | | | | 1,398,600 | | |

Alibaba Group Holding, Ltd.

3.600%, 11/28/24c | | | 300,000 | | | | 288,838 | | |

Total China/Hong Kong | | | | | 11,583,892 | | |

INDONESIA: 12.0% | |

PT Perusahaan Listrik Negara

5.250%, 10/24/42 | | | 2,500,000 | | | | 2,175,000 | | |

Theta Capital Pte, Ltd.

7.000%, 05/16/19 | | | 1,500,000 | | | | 1,544,154 | | |

Alam Synergy Pte, Ltd.

6.950%, 03/27/20c | | | 1,500,000 | | | | 1,447,500 | | |

Jababeka International BV

7.500%, 09/24/19 | | | 1,400,000 | | | | 1,378,213 | | |

TBG Global Pte, Ltd.

4.625%, 04/03/18c | | | 1,000,000 | | | | 995,000 | | |

Alam Synergy Pte, Ltd.

6.950%, 03/27/20 | | | 500,000 | | | | 482,500 | | |

PT Astra Sedaya Finance

8.600%, 02/21/17 | | IDR | 5,000,000,000 | | | | 369,173 | | |

Total Indonesia | | | | | 8,391,540 | | |

| | Face Amount* | | Value | |

SRI LANKA: 7.5% | |

DFCC Bank PLC

9.625%, 10/31/18 | | | 2,650,000 | | | $ | 2,784,275 | | |

National Savings Bank

5.150%, 09/10/19 | | | 2,000,000 | | | | 1,935,000 | | |

National Savings Bank

8.875%, 09/18/18 | | | 500,000 | | | | 541,900 | | |

Total Sri Lanka | | | | | 5,261,175 | | |

SINGAPORE: 2.9% | |

Global Logistic Properties, Ltd.

3.375%, 05/11/16 | | CNY | 12,500,000 | | | | 2,002,392 | | |

Total Singapore | | | | | 2,002,392 | | |

AUSTRALIA: 1.8% | |

Macquarie Bank, Ltd.

6.625%, 04/07/21 | | | 1,100,000 | | | | 1,258,761 | | |

Total Australia | | | | | 1,258,761 | | |

PHILIPPINES: 1.6% | |

Alliance Global Group, Inc.

6.500%, 08/18/17 | | | 1,050,000 | | | | 1,113,000 | | |

Total Philippines | | | | | 1,113,000 | | |

TOTAL NON-CONVERTIBLE CORPORATE BONDS | | | | | 45,534,245 | | |

(Cost $46,766,409) | | | | | | | |

CONVERTIBLE CORPORATE BONDS: 16.3%

CHINA/HONG KONG: 16.3% | |

Homeinns Hotel Group, Cnv.

2.000%, 12/15/15 | | | 2,800,000 | | | | 2,751,000 | | |

E-House China Holdings, Ltd., Cnv.

2.750%, 12/15/18c | | | 2,010,000 | | | | 1,924,575 | | |

Biostime International Holdings, Ltd., Cnv.

0.000%, 02/20/19 | | HKD | 14,000,000 | | | | 1,709,013 | | |

China Singyes Solar Technologies Holdings, Ltd., Cnv.

5.000%, 08/08/19 | | CNY | 9,000,000 | | | | 1,429,688 | | |

Qihoo 360 Technology Co., Ltd., Cnv.

1.750%, 08/15/21c | | | 1,500,000 | | | | 1,383,750 | | |

Ctrip.com International, Ltd., Cnv.

1.250%, 10/15/18 | | | 1,000,000 | | | | 1,141,250 | | |

Johnson Electric Holdings, Ltd., Cnv.

1.000%, 04/02/21 | | | 1,000,000 | | | | 1,050,000 | | |

Total China/Hong Kong | | | | | 11,389,276 | | |

TOTAL CONVERTIBLE CORPORATE BONDS | | | | | 11,389,276 | | |

(Cost $11,217,305) | | | | | |

matthewsasia.com | 800.789.ASIA 9

Matthews Asia Strategic Income Fund June 30, 2015

Schedule of Investmentsa (unaudited) (continued)

FOREIGN GOVERNMENT OBLIGATIONS: 13.8%

| | Face Amount* | | Value | |

SRI LANKA: 5.5% | |

Sri Lanka Government Bond

8.500%, 06/01/18 | | LKR | 200,000,000 | | | $ | 1,525,788 | | |

Sri Lanka Government Bond

8.500%, 04/01/18 | | LKR | 110,000,000 | | | | 840,194 | | |

Sri Lanka Government Bond

8.500%, 07/15/18 | | LKR | 100,000,000 | | | | 761,641 | | |

Sri Lanka Government Bond

8.000%, 11/15/18 | | LKR | 100,000,000 | | | | 750,970 | | |

Total Sri Lanka | | | | | 3,878,593 | | |

INDONESIA: 4.9% | |

Indonesia Treasury Bond

7.875%, 04/15/19 | | IDR | 20,000,000,000 | | | | 1,486,983 | | |

Indonesia Treasury Bond

6.125%, 05/15/28 | | IDR | 16,000,000,000 | | | | 985,142 | | |

Indonesia Treasury Bond

9.000%, 03/15/29 | | IDR | 12,000,000,000 | | | | 948,659 | | |

Total Indonesia | | | | | 3,420,784 | | |

SOUTH KOREA: 2.3% | |

Korea Treasury Bond

3.500%, 09/10/16 | | KRW | 1,000,000,000 | | | | 915,911 | | |

Korea Treasury Bond

3.500%, 03/10/24 | | KRW | 400,000,000 | | | | 388,990 | | |

Korea Treasury Bond

4.000%, 09/10/15 | | KRW | 300,000,000 | | | | 270,217 | | |

Total South Korea | | | | | 1,575,118 | | |

SUPRANATIONAL: 1.1% | |

International Finance Corp.

7.750%, 12/03/16 | | INR | 50,000,000 | | | | 788,713 | | |

Total Supranational | | | | | 788,713 | | |

TOTAL FOREIGN GOVERNMENT OBLIGATIONS | | | | | 9,663,208 | | |

(Cost $9,923,901) | | | |

COMMON EQUITIES: 1.3%

| | Shares | | | |

SINGAPORE: 0.8% | |

Vicom, Ltd. | | | 118,000 | | | | 544,946 | | |

Total Singapore | | | | | 544,946 | | |

PHILIPPINES: 0.5% | |

Alliance Global Group, Inc. | | | 780,000 | | | | 375,486 | | |

Total Philippines | | | | | 375,486 | | |

TOTAL COMMON EQUITIES | | | | | 920,432 | | |

(Cost $1,039,054) | | | |

TOTAL INVESTMENTS: 96.6% | | | | | 67,507,161 | | |

(Cost $68,946,669d) | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 3.4% | | | | | 2,411,314 | | |

NET ASSETS: 100.0% | | | | $ | 69,918,475 | | |

a Certain securities were fair valued under the valuation polices approved by the Board of Trustees (Note 2-A).

b Variable rate security. The rate represents the rate in effect at June 30, 2015.

c Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. The security may be resold in transactions exempt from registration normally to qualified institutional buyers. The security has been determined to be liquid in accordance with procedures adopted by the Fund's Board of Directors.

d Cost for federal income tax purposes is $68,946,669 and net unrealized depreciation consists of:

Gross unrealized appreciation | | $ | 724,327 | | |

Gross unrealized depreciation | | | (2,163,835 | ) | |

Net unrealized depreciation | | ($ | 1,439,508 | ) | |

* All values are in USD unless otherwise noted.

Cnv. Convertible

CNY Chinese Renminbi (Yuan)

IDR Indonesian Rupiah

INR Indian Rupee

HKD Hong Kong Dollar

KRW Korean Won

LKR Sri Lankan Rupee

USD U.S. Dollar

See accompanying notes to financial statements.

10 MATTHEWS ASIA FUNDS

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Robert J. Horrocks, PhD

Lead Manager

Kenneth Lowe, CFA

Lead Manager

FUND FACTS

| | | Investor Class | | Institutional Class | |

Ticker | | MACSX | | MICSX | |

CUSIP | | 577130206 | | 577130842 | |

Inception | | 9/12/94 | | 10/29/10 | |

NAV | | $18.42 | | $18.41 | |

Initial Investment | | $2,500 | | $3 million | |

Gross Expense Ratio1 | | 1.08% | | 0.92% | |

Portfolio Statistics

Total # of Positions | | 60 | |

Net Assets | | $4.0 billion | |

Weighted Average Market Cap | | $34.2 billion | |

Portfolio Turnover | | 16.79%2 | |

Benchmark

MSCI AC Asia ex Japan Index

OBJECTIVE

Long-term capital appreciation. The Fund also seeks to provide some current income.

STRATEGY

Under normal market conditions, the Fund seeks to achieve its investment objective by investing at least 80% of its total net assets, which include borrowings for investment purposes, in dividend-paying common stock, preferred stock and other equity securities, and convertible securities as well as fixed-income securities, of any duration or quality, of companies located in Asia, which consists of all countries and markets in Asia, including developed, emerging and frontier countries and markets in the Asian region.

1 Prospectus expense ratios.

2 The lesser of fiscal year 2014 long-term purchase costs or sales proceeds divided by the average monthly market value of long-term securities.

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary

For the first half of 2015, the Matthews Asian Growth and Income Fund gained 3.46% (Investor Class) and 3.55% (Institutional Class), underperforming its benchmark, the MSCI All Country Asia ex Japan Index, which rose 5.59%. For the quarter ending June 30, the Fund gained 1.43% (Investor Class) and 1.51% (Institutional Class) while its benchmark rose 0.65%.

Market Environment:

Monetary policy and politics took center stage during the second quarter of the year, sparking yet further volatility across global markets. In the U.S., following the dropping of the word "patient" from the previous U.S. Federal Reserve policy statement, Fed Chairwoman Janet Yellen further commented that rate rises will be gradual in nature as they wait for more decisive evidence of economic growth. In Europe, Greece once again dominated headlines as the heavily indebted nation defaulted on a repayment to the International Monetary Fund. Despite this, at the time of writing, the Greek government continues to refuse European officials' request for structural reform in order to ensure additional bailout funds. Turning to Asia, China underwent further liquidity injections into the financial system through reserve ratio requirement cuts, interest rate reductions and capital injections into state-owned policy banks. Additionally, the Chinese finance ministry, central bank and banking regulator announced plans to allow commercial banks to use local government bonds that they purchase as collateral for low-cost loans from the central bank in order to increase overall liquidity. All of these measures, alongside yet more retail investor participation and margin lending, led the domestic Chinese and Hong Kong markets to outperform those across the rest of the region. Markets in Southeast Asia were the poorest performers on slowing growth and political woes.

Portfolio Contributors and Detractors:

The largest contributors to Fund performance during the quarter came from our holdings in Hong Kong and China, with our convertible bond in Hong Kong Exchanges & Clearing the strongest of these. The underlying stock was up strongly on increasing average daily turnover as markets rallied and Exchange Traded Funds participation increased. We used this as an opportunity to exit our position as valuations had become stretched at 40X price-to-earnings.* Yum! Brands, the quick service restaurant chain that owns Taco Bell, KFC and Pizza Hut, also performed well as it appears that the reputational damage they suffered from supply chain issues in China is subsiding, and customers are returning to their stores. The stock was also helped after a well-known activist investor took a stake in the company, highlighting potential value realization from a break up of its businesses.

Although the Fund has little exposure to the Philippines, our holding in Globe Telecom, the number two wireless carrier in the market, also helped returns. Increasing smartphone penetration and decreasing competitive intensity on data pricing helped the firm deliver good earnings growth.

The Fund's holdings within Malaysia were the largest detractors to returns, partially due to a challenging political backdrop in the wake of a corruption scandal involving Prime Minister Najib Razak and the state-owned investment fund 1Malaysia Development Bhd (1MDB). Alongside this, the country's exposure to energy prices also created challenges. Additionally, we witnessed stock weakness in holdings, such as commercial bank AMMB, as concerns arise around potential asset quality issues within the financial system.

matthewsasia.com | 800.789.ASIA 11

PERFORMANCE AS OF JUNE 30, 2015

| | | | | | | | | Average Annual Total Returns | | | |

| | | 3 Months | | YTD | | 1 Year | | 3 Years | | 5 Years | | 10 Years | | Since

Inception | | Inception

Date | |

Investor Class (MACSX) | | | 1.43 | % | | | 3.46 | % | | | -2.03 | % | | | 7.68 | % | | | 7.49 | % | | | 8.76 | % | | | 10.08 | % | | 9/12/94 | |

Institutional Class (MICSX) | | | 1.51 | % | | | 3.55 | % | | | -1.86 | % | | | 7.84 | % | | | n.a. | | | | n.a. | | | | 5.10 | % | | 10/29/10 | |

MSCI AC Asia ex Japan Index3 | | | 0.65 | % | | | 5.59 | % | | | 4.14 | % | | | 9.87 | % | | | 7.74 | % | | | 9.68 | % | | | 4.33 | %4 | | | | | |

Lipper Pacific Region Funds Category Average5 | | | 1.24 | % | | | 6.66 | % | | | 2.78 | % | | | 10.13 | % | | | 8.61 | % | | | 6.79 | % | | | 4.18 | %4 | | | | | |

Performance assumes reinvestment of all dividends and/or distributions before taxes. All performance quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate with market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. For the Fund's most recent month-end performance, visit matthewsasia.com.

INCOME DISTRIBUTION HISTORY

| | 2015 | | 2014 | |

| | June | | December | | Total | | June | | December | | Total | |

Investor (MACSX) | | $ | 0.21 | | | | n.a. | | | | n.a. | | | $ | 0.15 | | | $ | 0.20 | | | $ | 0.35 | | |

Inst'l (MICSX) | | $ | 0.23 | | | | n.a. | | | | n.a. | | | $ | 0.16 | | | $ | 0.21 | | | $ | 0.38 | | |

Note: This table does not include capital gains distributions. Totals may differ by $0.01 due to rounding. For income distribution history, visit matthewsasia.com.

30-DAY YIELD:

2.13% (Investor Class) 2.30% (Institutional Class)

The 30-Day Yield represents net investment income earned by the Fund over the 30-day period ended 6/30/15, expressed as an annual percentage rate based on the Fund's share price at the end of the 30-day period. The 30-Day Yield should be regarded as an estimate of the Fund's rate of investment income, and it may not equal the Fund's actual income distribution rate.

Source: BNY Mellon Investment Servicing (US) Inc.

DIVIDEND YIELD: 3.46%

The dividend yield (trailing) for the portfolio is the weighted average sum of the dividends paid by each equity security held by the Fund over the 12 months ended 6/30/15 divided by the current price of each equity as of 6/30/15. The annualized dividend yield for the Fund is for the equity-only portion of the portfolio. Please note that this is based on gross equity portfolio holdings and does not reflect the actual yield an investor in the Fund would receive. Past yields are no guarantee of future yields.

Source: FactSet Research Systems, Bloomberg, MICM

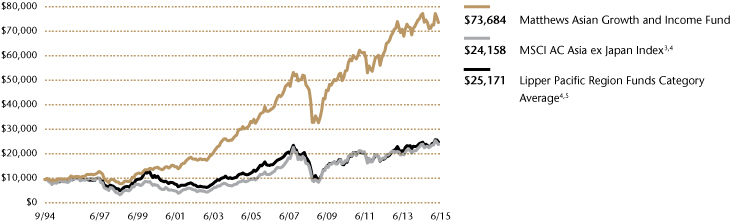

GROWTH OF A $10,000 INVESTMENT SINCE INCEPTION—INVESTOR CLASS

Plotted monthly. The performance data and graph do not reflect the deduction of taxes that a shareholder would pay on dividends, capital gains distributions or redemption of Fund shares. Values are in US$.

3 It is not possible to invest directly in an index. Source: Index data from Morgan Stanley Capital International and Bloomberg; total return calculations performed by BNY Mellon Investment Servicing (US) Inc. Please see page 85 for index definition.

4 Calculated from 8/31/94.

5 The Lipper Category Average does not reflect sales charges and is based on total return, including reinvestment of dividends and capital gains for the stated periods.

TOP TEN HOLDINGS6

| | | Sector | | Country | | % of Net Assets | |

Jardine Matheson Holdings, Ltd. | | Industrials | | China/Hong Kong | | | 3.4 | % | |

Yum! Brands, Inc. | | Consumer Discretionary | | China/Hong Kong | | | 2.9 | % | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | Information Technology | | Taiwan | | | 2.9 | % | |

AIA Group, Ltd. | | Financials | | China/Hong Kong | | | 2.8 | % | |

Globe Telecom, Inc. | | Telecommunication Services | | Philippines | | | 2.6 | % | |

Singapore Technologies Engineering, Ltd. | | Industrials | | Singapore | | | 2.5 | % | |

United Overseas Bank, Ltd. | | Financials | | Singapore | | | 2.5 | % | |

Ascendas REIT | | Financials | | Singapore | | | 2.4 | % | |

Hang Lung Properties, Ltd. | | Financials | | China/Hong Kong | | | 2.2 | % | |

HSBC Holdings PLC | | Financials | | China/Hong Kong | | | 2.2 | % | |

% OF ASSETS IN TOP TEN | | | | | | | 26.4 | % | |

6 Holdings may combine more than one security from same issuer and related depositary receipts.

12 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund

Portfolio Manager Commentary (continued)

Notable Portfolio Changes:

The Fund initiated four new positions during the quarter. The first of these was Techtronic Industries, a market-leading power tool and floor care appliance brand owner and manufacturer. We believe the company has fairly strong growth prospects as it continues to win market share from its rivals in both the DIY and professional power tool markets due to its impressive cordless technology and price points. Earnings should also benefit from lower commodity prices and greater efficiencies. The stock is trading at what we believe to be an attractive 17x P/E in light of these growth prospects and a strong balance sheet.

We also initiated positions in Singapore Telecom ("Singtel"), a regional wireless company, Guangdong Investment, and Insurance Australia Group. For Singtel, we believe that the company has an attractive set of quality assets across Asia Pacific that still has room for growth as smartphone and 4G penetration increase, whilst the company continues to better tier pricing. The stock currently provides a healthy combination of both growth potential and income given its yield of about 4% year to date. Guangdong Investment is somewhat similar in nature as the regulated water utility provides a defensive and visible stream of earnings and dividends that are both still growing healthily on continued volume increases and new projects. Insurance Australia Group is the country's largest personal lines insurance company, and as of the end of June offered an attractive 5% yield given an interesting combination of stable cash flow at home and growth options in Asia.

These positions were funded through the sale of our holdings in Hong Kong Exchanges & Clearing, and China Oilfield Services Limited.

Outlook:

The overall demand backdrop across the globe continues to be moderately weak, with Europe particularly challenged by the threat of deflation, leading to little support for Asian exports. Additionally, fairly aggressive credit growth across much of Asia since the Global Financial Crisis of 2008 means that further increases in indebtedness is unlikely to fuel economic growth. In prior commentaries we have noted that many governments throughout the region now have pro-reform regimes in place, and progress within these is vital in order to ensure that the region sees sustainable growth coming from productivity improvements. Although moderately early on in the reigns of many, change has been somewhat slow to materialize, at the very least in relation to what were quite lofty expectations for leaders such as India's Narendra Modi and Indonesia's Joko Widodo. In the latter case, for example, we have seen an array of mixed signals and nationalistic tendencies in what appears to be a man in a weak leadership position.

With these issues in mind, we believe that it is likely that the corporate earnings cycle in Asia will continue to disappoint and suffer further downgrades. A combination of volatile macroeconomic headlines, weak earnings and valuations that are not overly compelling—at about 18.7x P/E on average for the MSCI All Country Asia ex Japan Index on an equal weighted-basis year to date—provide us with reason for caution. More positively, despite this, the Fund looks relatively well-placed given our ethos of buying into what we believe are quality companies at attractive valuations that have the ability to protect our fund holder's capital in more challenging environments.

* Price-to-Earnings Ratio (P/E Ratio) is a valuation ratio of a company's current share price compared to its per-share earnings and is calculated as the market value per share divided by the Earnings per Share (EPS).

COUNTRY ALLOCATION (%)7

China/Hong Kong | | | 33.1 | | |

Singapore | | | 16.5 | | |

South Korea | | | 9.2 | | |

Malaysia | | | 7.8 | | |

Japan | | | 5.6 | | |

Australia | | | 4.5 | | |

Taiwan | | | 4.2 | | |

Thailand | | | 4.2 | | |

New Zealand | | | 3.0 | | |

Indonesia | | | 3.0 | | |

Philippines | | | 2.6 | | |

Vietnam | | | 1.7 | | |

United Kingdom | | | 1.4 | | |

Cash and Other Assets, Less Liabilities | | | 3.2 | | |

SECTOR ALLOCATION (%)

Financials | | | 19.2 | | |

Consumer Discretionary | | | 17.1 | | |

Industrials | | | 16.0 | | |

Telecommunication Services | | | 15.2 | | |

Consumer Staples | | | 14.2 | | |

Information Technology | | | 6.3 | | |

Utilities | | | 5.7 | | |

Health Care | | | 1.7 | | |

Materials | | | 1.4 | | |

Cash and Other Assets, Less Liabilities | | | 3.2 | | |

MARKET CAP EXPOSURE (%)8

Mega Cap (over $25B) | | | 33.9 | | |

Large Cap ($10B–$25B) | | | 21.8 | | |

Mid Cap ($3B–$10B) | | | 29.0 | | |

Small Cap (under $3B) | | | 12.1 | | |

Cash and Other Assets, Less Liabilities | | | 3.2 | | |

ASSET TYPE BREAKDOWN (%)9

Common Equities and ADRs | | | 87.9 | | |

Convertible Corporate Bonds | | | 6.5 | | |

Preferred Equities | | | 2.4 | | |

Cash and Other Assets, Less Liabilities | | | 3.2 | | |

7 Not all countries where the Fund may invest are included in the benchmark index.

8 Source: FactSet Research Systems. Percentage values in data are rounded to the nearest tenth of one percent; the values may not sum to 100% due to rounding.

9 Bonds are not included in the MSCI All Country Asia ex Japan Index.

matthewsasia.com | 800.789.ASIA 13

Matthews Asian Growth and Income Fund June 30, 2015

Schedule of Investmentsa (unaudited)

COMMON EQUITIES: 87.9%

| | Shares | | Value | |

CHINA/HONG KONG: 28.7% | |

Jardine Matheson Holdings, Ltd. | | | 2,402,000 | | | $ | 136,175,020 | | |

Yum! Brands, Inc. | | | 1,317,300 | | | | 118,662,384 | | |

AIA Group, Ltd. | | | 17,078,600 | | | | 111,671,128 | | |

Hang Lung Properties, Ltd. | | | 30,498,920 | | | | 90,640,467 | | |

HSBC Holdings PLC ADR | | | 1,987,433 | | | | 89,056,873 | | |

Vitasoy International Holdings, Ltd. | | | 49,593,000 | | | | 84,451,187 | | |

CLP Holdings, Ltd. | | | 9,338,700 | | | | 79,370,101 | | |

China Mobile, Ltd. ADR | | | 1,233,400 | | | | 79,048,606 | | |

VTech Holdings, Ltd. | | | 5,885,200 | | | | 78,052,355 | | |

Techtronic Industries Co., Ltd. | | | 21,378,000 | | | | 69,898,083 | | |

Café de Coral Holdings, Ltd. | | | 18,352,000 | | | | 66,290,742 | | |

CK Hutchison Holdings, Ltd. | | | 4,400,172 | | | | 64,691,242 | | |

Guangdong Investment, Ltd. | | | 31,217,000 | | | | 43,683,322 | | |

Cheung Kong Property Holdings, Ltd.b | | | 4,400,172 | | | | 36,499,934 | | |

Television Broadcasts, Ltd. | | | 2,213,000 | | | | 13,132,599 | | |

Total China/Hong Kong | | | | | 1,161,324,043 | | |

SINGAPORE: 14.4% | |

Singapore Technologies Engineering, Ltd. | | | 41,921,425 | | | | 102,640,929 | | |

United Overseas Bank, Ltd. | | | 5,797,000 | | | | 99,180,737 | | |

Ascendas REIT | | | 53,925,000 | | | | 98,452,352 | | |

Singapore Telecommunications, Ltd. | | | 21,686,400 | | | | 67,677,170 | | |

Keppel Corp., Ltd. | | | 9,879,000 | | | | 60,213,746 | | |

SIA Engineering Co., Ltd. | | | 20,761,800 | | | | 59,190,283 | | |

Singapore Post, Ltd. | | | 38,209,000 | | | | 53,735,043 | | |

ARA Asset Management, Ltd. | | | 31,219,210 | | | | 40,441,777 | | |

Total Singapore | | | | | 581,532,037 | | |

MALAYSIA: 7.8% | |

Genting Malaysia BHD | | | 75,188,700 | | | | 83,639,567 | | |

British American Tobacco Malaysia BHD | | | 4,164,600 | | | | 68,370,561 | | |

AMMB Holdings BHD | | | 40,974,400 | | | | 65,417,633 | | |

Axiata Group BHD | | | 37,993,923 | | | | 64,422,296 | | |

Telekom Malaysia BHD | | | 20,245,551 | | | | 35,026,107 | | |

Total Malaysia | | | | | 316,876,164 | | |

SOUTH KOREA: 6.8% | |

Kangwon Land, Inc. | | | 2,051,776 | | | | 67,988,681 | | |

KT&G Corp. | | | 743,294 | | | | 62,997,051 | | |

Samsung Electronics Co., Ltd. | | | 54,642 | | | | 61,996,060 | | |

GS Home Shopping, Inc. | | | 227,544 | | | | 42,801,951 | | |

KEPCO Plant Service & Engineering

Co., Ltd. | | | 386,300 | | | | 40,865,480 | | |

Total South Korea | | | | | 276,649,223 | | |

JAPAN: 5.6% | |

Japan Tobacco, Inc. | | | 2,299,400 | | | | 81,742,011 | | |

Lawson, Inc. | | | 1,086,500 | | | | 74,350,517 | | |

KDDI Corp. | | | 3,000,100 | | | | 72,398,273 | | |

Total Japan | | | | | 228,490,801 | | |

| | Shares | | Value | |

AUSTRALIA: 4.5% | |

CSL, Ltd. | | | 1,044,381 | | | $ | 69,625,190 | | |

Insurance Australia Group, Ltd. | | | 14,241,305 | | | | 61,228,782 | | |

Woolworths, Ltd. | | | 2,394,197 | | | | 49,749,694 | | |

Total Australia | | | | | 180,603,666 | | |

TAIWAN: 4.2% | |

Taiwan Semiconductor Manufacturing

Co., Ltd. | | | 13,915,187 | | | | 63,294,891 | | |

Chunghwa Telecom Co., Ltd. ADR | | | 1,747,125 | | | | 55,768,230 | | |

Taiwan Semiconductor Manufacturing

Co., Ltd. ADR | | | 2,296,124 | | | | 52,144,976 | | |

Total Taiwan | | | | | 171,208,097 | | |

THAILAND: 4.2% | |

Advanced Info Service Public Co., Ltd. | | | 9,595,700 | | | | 67,998,121 | | |

Glow Energy Public Co., Ltd. | | | 21,887,400 | | | | 55,085,771 | | |

BEC World Public Co., Ltd. | | | 40,566,000 | | | | 44,915,793 | | |

Total Thailand | | | | | 167,999,685 | | |

NEW ZEALAND: 3.0% | |

SKYCITY Entertainment Group, Ltd. | | | 21,703,820 | | | | 61,751,609 | | |

SKY Network Television, Ltd. | | | 15,123,711 | | | | 61,569,049 | | |

Total New Zealand | | | | | 123,320,658 | | |

INDONESIA: 3.0% | |

PT Telekomunikasi Indonesia Persero ADR | | | 1,621,002 | | | | 70,335,277 | | |

PT Perusahaan Gas Negara Persero | | | 159,343,000 | | | | 51,469,002 | | |

Total Indonesia | | | | | 121,804,279 | | |

PHILIPPINES: 2.6% | |

Globe Telecom, Inc. | | | 1,862,720 | | | | 103,621,475 | | |

Total Philippines | | | | | 103,621,475 | | |

VIETNAM: 1.7% | |

Vietnam Dairy Products JSC | | | 13,033,926 | | | | 67,442,070 | | |

Total Vietnam | | | | | 67,442,070 | | |

UNITED KINGDOM: 1.4% | |

BHP Billiton PLC | | | 2,888,196 | | | | 56,786,446 | | |

Total United Kingdom | | | | | 56,786,446 | | |

TOTAL COMMON EQUITIES | | | | | 3,557,658,644 | | |

(Cost $3,056,798,480) | | | | | |

PREFERRED EQUITIES: 2.4%

SOUTH KOREA: 2.4% | |

LG Household & Health Care, Ltd., Pfd. | | | 121,855 | | | | 36,996,804 | | |

Hyundai Motor Co., Ltd., Pfd. | | | 355,983 | | | | 32,534,786 | | |

Hyundai Motor Co., Ltd., 2nd Pfd. | | | 318,246 | | | | 29,927,645 | | |

Total South Korea | | | | | 99,459,235 | | |

TOTAL PREFERRED EQUITIES | | | | | 99,459,235 | | |

(Cost $38,549,481) | | | | | |

14 MATTHEWS ASIA FUNDS

Matthews Asian Growth and Income Fund June 30, 2015

Schedule of Investmentsa (unaudited) (continued)

CONVERTIBLE CORPORATE BONDS: 6.5%

| | Face Amount* | | Value | |

CHINA/HONG KONG: 4.4% | |

Shine Power International, Ltd., Cnv.

0.000%, 07/28/19 | | HKD | 446,000,000 | | | $ | 56,170,379 | | |

Johnson Electric Holdings, Ltd., Cnv.

1.000%, 04/02/21 | | | 49,750,000 | | | | 52,237,500 | | |

Hengan International Group Co., Ltd., Cnv.

0.000%, 06/27/18 | | HKD | 339,000,000 | | | | 46,575,846 | | |

PB Issuer No. 2, Ltd., Cnv.

1.750%, 04/12/16 | | | 21,820,000 | | | | 21,383,600 | | |

Total China/Hong Kong | | | | | 176,367,325 | | |

SINGAPORE: 2.1% | |

CapitaLand, Ltd., Cnv.

1.950%, 10/17/23 | | SGD | 110,250,000 | | | | 85,111,510 | | |

Total Singapore | | | | | 85,111,510 | | |

TOTAL CONVERTIBLE CORPORATE BONDS | | | | | 261,478,835 | | |

(Cost $265,389,724) | | | | | |

TOTAL INVESTMENTS: 96.8% | | | | | 3,918,596,714 | | |

(Cost $3,360,737,685c) | | | | | |

CASH AND OTHER ASSETS,

LESS LIABILITIES: 3.2% | | | | | 129,922,019 | | |

NET ASSETS: 100.0% | | | | $ | 4,048,518,733 | | |

a Certain securities were fair valued under the valuation polices approved by the Board of Trustees (Note 2-A).

b Non-income producing security.

c Cost for federal income tax purposes is $3,361,040,470 and net unrealized appreciation consists of:

Gross unrealized appreciation | | $ | 745,986,047 | | |

Gross unrealized depreciation | | | (188,429,803 | ) | |

Net unrealized appreciation | | $ | 557,556,244 | | |

* All values are in USD unless otherwise noted.

ADR American Depositary Receipt

BHD Berhad

Cnv. Convertible

HKD Hong Kong Dollar

JSC Joint Stock Co.

Pfd. Preferred

REIT Real Estate Investment Trust

SGD Singapore Dollar

USD U.S. Dollar

See accompanying notes to financial statements.

matthewsasia.com | 800.789.ASIA 15

ASIA GROWTH AND INCOME STRATEGIES

PORTFOLIO MANAGERS

Yu Zhang, CFA | | Robert Horrocks, PhD | |

Lead Manager | | Lead Manager | |

Vivek Tanneeru | | | |

Co-Manager | | | |

FUND FACTS

| | | Investor Class | | Institutional Class | |

Ticker | | MAPIX | | MIPIX | |

CUSIP | | 577125107 | | 577130750 | |

Inception | | 10/31/06 | | 10/29/10 | |

NAV | | $16.99 | | $16.99 | |

Initial Investment | | $2,500 | | $3 million | |

Gross Expense Ratio1 | | 1.06% | | 0.93% | |

After Fee Waiver and

Reimbursement | | 1.05%2 | | n.a. | |

Portfolio Statistics

Total # of Positions | | 72 | |

Net Assets | | $5.9 billion | |

Weighted Average Market Cap | | $35.8 billion | |

Portfolio Turnover | | 20.06%3 | |

Benchmark

MSCI AC Asia Pacific Index

OBJECTIVE

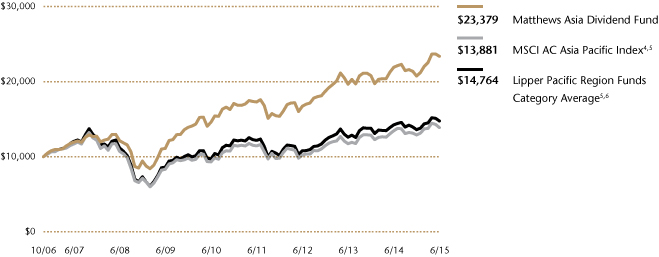

Total return with an emphasis on providing current income.

STRATEGY